The number of outstanding shares as of December 31, 20182021, was 22,602,73729,450,551 Class A common shares and 27,658,29027,400,848 Class B common shares.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes☐ No☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes☐ No☒

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes☒ No☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Yes☐ No☐(not required)

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,filer”, "accelerated filer,” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

| | | | ||||

| | | | ||||

Large Accelerated Filer | ☒ | Accelerated Filer | ◻ | Non-accelerated Filer | ◻ | Emerging growth company | ☐ |

Large Accelerated Filer☐ Accelerated Filer☐ Non-accelerated Filer☒ Emerging growth company☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report: ☒

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this annual report:

filing:

☐ | U.S. GAAP |

☒ |

International Financial Reporting Standards as issued by the International Accounting Standards Board |

☐ |

Other |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes☐ No☒☐

Arco platform limitedARCO PLATFORM LIMITED

TABLE OF CONTENTS

Page

i

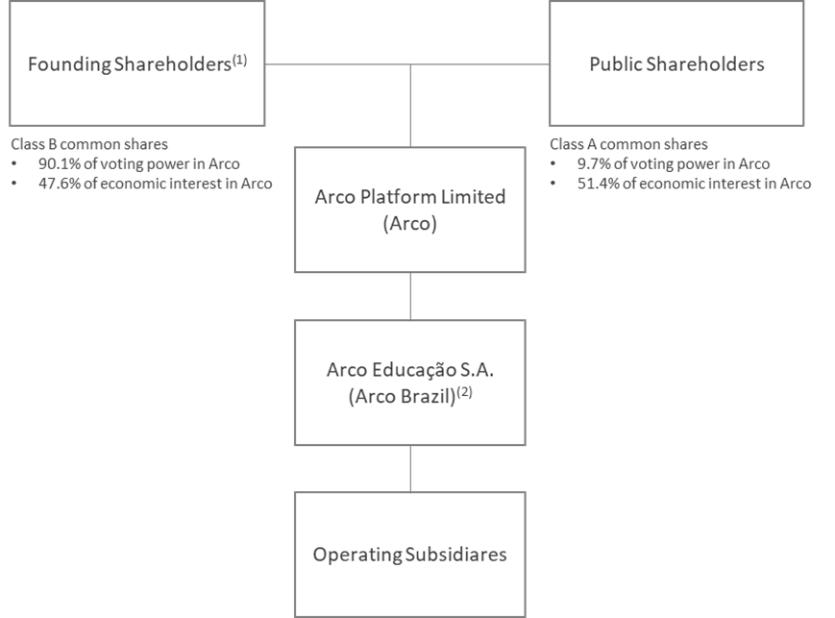

The full consequences of a credit rating downgrade are inherently uncertain, as they depend upon numerous dynamic, complex, and inter-related factors and assumptions, including market conditions at the time of any downgrade. A prolongation or worsening of the current Brazilian recession and continued political uncertainty, among other factors, could lead to further ratings downgrades. We cannot assure you that the rating agencies will maintain their current ratings or outlooks, and such changes could increase our funding costs and adversely affect our results of operations. Any further downgrade of Brazil’s sovereign credit ratings could heighten investors’ perception of risk and, as a result, cause the trading price of our Class A common shares to decline. 31 Certain Factors Relating to Our Class A Common Shares The Founding Shareholders, our largest group of shareholders, own 100% of our outstanding Class B common shares, which represents As of December 31,

Our Articles of Association contain anti-takeover provisions that may discourage a third-party from acquiring us and adversely affect the rights of holders of our Class A common shares. Our Articles of Association contain certain provisions that could limit the ability of others to acquire our control, including a provision that grants authority to our board of directors to establish and issue from time to time one or more series of preferred shares without action by our shareholders and to determine, with respect to any series of preferred shares, the terms and rights of that series. These provisions could have the effect of depriving our shareholders of the opportunity to sell their shares at a premium over the prevailing market price by discouraging third parties from seeking to obtain our control in a tender offer or similar transactions.

If securities or industry analysts do not publish research, or publish inaccurate or unfavorable research, about our business, the price of our Class A common shares and our trading volume could decline. The trading market for our Class A common shares 32 inaccurate or unfavorable research about our business, the price of our Class A common shares would likely decline. If one or more of these analysts cease coverage of our company or fail to publish reports on us regularly, demand for our Class A common shares could decrease, which might cause the price of our Class A common shares and trading volume to decline. We do not anticipate paying any cash dividends in the foreseeable future. We currently intend to retain our future earnings, if any, for the foreseeable future, to fund the operation of our business and future growth. We do not intend to pay any dividends to holders of our Class A common shares. As a result, capital appreciation in the price of our Class A common shares, if any, will be your only source of gain on an investment in our Class A common shares. Our dual class capital structure means our shares In 2017, FTSE Russell, S&P Dow Jones and MSCI announced changes to their eligibility criteria for inclusion of shares of public companies on certain indices to exclude companies with multiple classes of shares of common stock, such as ours, from being added to such indices. FTSE Russell announced plans to require new constituents of its indices to have at least five percent of their voting rights in the hands of public stockholders, whereas S&P Dow Jones announced that companies with multiple share classes, such as ours, will not be eligible for inclusion in the S&P 500, S&P MidCap 400 and S&P SmallCap 600, which together make up the S&P Composite 1500. MSCI also opened public consultations on their treatment of no-vote and multi-class structures and The dual class structure of our common stock has the effect of concentrating voting control with the Founding Shareholders; this will limit or preclude your ability to influence corporate matters. Each Class A common share entitles its holder to one vote per share, and each Class B common share will entitle its holder to ten votes per share, so long as the total number of the issued and outstanding Class B common shares is at least 10% of the total number of shares outstanding. Due to the ten-to-one voting ratio between our Class B and Class A common shares, the beneficial owners of our Class B common shares In addition, our Articles of Association provide that at any time when there are Class A common shares in issue, additional Class B common shares may only be issued pursuant to (1) a share split, subdivision of shares or similar transaction or where a dividend or other distribution is paid by the issue of shares or rights to acquire shares or following capitalization of profits, (2) a merger, consolidation, or other business combination involving the issuance of Class B common shares as full or partial consideration, or (3) an issuance of Class A common shares, whereby holders of the Class B common shares are entitled to purchase a number of Class B common shares that would allow them to maintain their proportional ownership interests in Arco (following an offer by us to each holder of Class B common shares to issue to such holder, upon the same economic terms and at the same price, such number of Class B common shares as would ensure that such holder may maintain a proportional ownership interest in Arco pursuant to our Articles of Association).

33 Future transfers by holders of Class B common shares will generally result in those shares converting to Class A common shares, subject to limited exceptions, such as certain transfers effected to permitted transferees or for estate planning or charitable purposes. The conversion of Class B common shares to Class A common shares will have the effect, over time, of increasing the relative voting power of those holders of Class B common shares who retain their shares in the long term. In light of the above provisions relating to the issuance of additional Class B common shares, the fact that future transfers by holders of Class B common shares will generally result in those shares converting to Class A common shares, subject to limited exceptions as provided in the Articles of Association; as well as the ten-to-one voting ratio of our Class B common shares and Class A common shares, holders of our Class B common shares will in many situations continue to maintain control of all matters requiring shareholder approval. This concentrated control will limit or preclude your ability to influence corporate matters for the foreseeable future. For a description of our dual class structure, see “Item 10. Additional Information—B. Memorandum and articles of association—Voting Rights.” We are a Cayman Islands exempted company with limited liability. The rights of our shareholders, including with respect to fiduciary duties and corporate opportunities, may be different from the rights of shareholders governed by the laws of U.S. jurisdictions. We are a Cayman Islands exempted company with limited liability. Our corporate affairs are governed by our Articles of Association and by the laws of the Cayman Islands. The rights of shareholders and the responsibilities of members of our board of directors may be different from the rights of shareholders and responsibilities of directors in companies governed by the laws of U.S. jurisdictions. As a foreign private issuer, registrants. As a foreign private issuer, We will follow Cayman Islands laws and regulations that are applicable to Cayman Islands companies. However, Cayman Islands laws and regulations applicable to Cayman Islands companies do not contain any provisions comparable to the U.S. proxy rules, the U.S. rules relating to the filing of reports on Form 10-Q or 8-K or the U.S. rules relating to liability for insiders who profit from trades made in a short period of time, as referred to above.

34 Furthermore, foreign private issuers are required to file their annual report on Form 20-F within 120 days after the end of each fiscal year, while U.S. domestic issuers that are accelerated filers are required to file their annual report on Form 10-K within 75 days after the end of each fiscal year. Foreign private issuers are also exempt from Regulation Fair Disclosure, aimed at preventing issuers from making selective disclosures of material information, although we will be subject to Cayman Islands laws and regulations having substantially the same effect as Regulation Fair Disclosure. As a result of the above, even though we are required to file reports on Form 6-K disclosing the limited information which we have made or are required to make public pursuant to Cayman Islands law, or are required to distribute to shareholders generally, and that is material to us, you may not receive information of the same type or amount that is required to be disclosed to shareholders of a U.S. company.

As a foreign private issuer, we are permitted to, and we will, rely on exemptions from certain Nasdaq corporate governance standards applicable to U.S. issuers, including the requirement that a majority of an issuer’s directors consist of independent directors. This may afford less protection to holders of our Class A common shares. Section 5605 of the Nasdaq equity rules requires listed companies to have, among other things, a majority of their board members be independent, and to have independent director oversight of executive compensation, nomination of directors and corporate governance matters. As a foreign private issuer, however, we are permitted to, and we will, follow home country practice in lieu of the above requirements. See “Item 16G Corporate Governance—Principal Differences between Cayman Islands and U.S. Corporate Law.” We may lose our foreign private issuer status which would then require us to comply with the Exchange Act’s domestic reporting regime and cause us to incur significant legal, accounting and other expenses.

Our shareholders may face difficulties in protecting their interests because we are a Cayman Islands exempted company. Our corporate affairs are governed by our Articles of Association, by the Companies While Cayman Islands law allows a dissenting shareholder to express the shareholder’s view that a court sanctioned reorganization of a Cayman Islands company would not provide fair value for the shareholder’s shares, Cayman Islands statutory law does not specifically provide for shareholder appraisal rights in connection with a Shareholders of Cayman Islands exempted companies (such as us) have no general rights under Cayman Islands law to inspect corporate records and accounts or to obtain copies of lists of shareholders. Our directors have discretion under our Articles of Association to determine whether, 35 obliged to make them available to our shareholders. This may make it more difficult for you to obtain information needed to establish any facts necessary for a shareholder motion or to solicit proxies from other shareholders in connection with a proxy contest.

United States civil liabilities and certain judgments obtained against us by our shareholders may not be enforceable. We are a Cayman Islands exempted company and substantially all Further, it is unclear if original actions predicated on civil liabilities based solely upon U.S. federal securities laws are enforceable in courts outside the United States, including in the Cayman Islands and Brazil. Courts of the Cayman Islands may not, in an original action in the Cayman Islands, recognize or enforce judgments of U.S. courts predicated upon the civil liability provisions of the securities laws of the United States or any state of the United States on the grounds that such provisions are penal in nature. Although there is no statutory enforcement in the Cayman Islands of judgments obtained in the United States, courts of the Cayman Islands will recognize and enforce a foreign judgment of a court of competent jurisdiction if such judgment is final, for a liquidated sum, provided it is not in respect of taxes or a fine or penalty, is not inconsistent with a Cayman Islands’ judgment in respect of the same matters, and was not obtained in a manner which is contrary to the public policy of the Cayman Islands. In addition, a Cayman Islands court may stay proceedings if concurrent proceedings are being brought elsewhere.

Judgments of Brazilian courts to enforce our obligations with respect to our Class A common shares may be payable only in reais. Most of our assets are The Economic Substance Act of the Cayman Islands may affect our operations. The Cayman Islands has recently enacted the International Tax Co-operation (Economic Substance) Act (As Revised), or the Cayman Economic Substance Act. We are required to comply with the Cayman Economic Substance Act. As we are a Cayman Islands company, compliance obligations include filing annual notifications for the Company, which need to state whether we are carrying out any relevant activities and if so, whether we have satisfied economic substance tests to the extent required under the Cayman Economic Substance Act. As it is a new regime, it is anticipated that the Cayman Economic Substance Act will evolve and be subject to further clarification and amendments. We may need to allocate additional resources to keep updated with these developments and may have to make changes to our operations in order to comply with all requirements under the Cayman Economic Substance Act. Failure to satisfy these requirements may subject us to penalties under the Cayman Economic Substance Act. Our Class A common shares may not be a suitable investment for all investors, as investment in our Class A common shares presents risks and the possibility of financial losses. The investment in our Class A common shares is subject to risks. Investors who wish to invest in our Class A common shares are thus subject to asset losses, including loss of the entire value of their investment, as well as other risks, including those related to our Class A common shares, us, the sector in which we operate, our shareholders and the general macroeconomic environment in Brazil, among other risks. 36 Each potential investor in our Class A common shares must therefore determine the suitability of that investment

ITEM 4. INFORMATION ON THE COMPANY A. History and Development of the Company We were founded in 2004. However, our history goes back to 1941, when the grandfather of our CEO and founder, Ari de Sá Cavalcante Neto, acquired a small school in downtown Fortaleza. Over decades, the school grew into a large educational group with several branches providing K-12 education to

Colégio Ari de Sá developed a proprietary educational methodology aimed at improving student academic performance. The methodology is based on instilling discipline and a culture of hard work, stimulating students to develop a study routine and to demonstrate a proactive and considerate attitude toward their learning habits. In 2004, our CEO and founder, Ari de Sá Cavalcante Neto, decided to start an independent company exclusively focused on content and technology for K-12 schools, SAS. The SAS method was created with the aim of offering it as a solution to private schools across Brazil. Our system uses technology as a powerful tool to promote improvements in student performance. This is achieved, in part, by allowing students to prepare for class in advance by using our platform’s video lessons, homework tools and daily class reviews, as well as our practical workbooks with class-specific content, homework and performance reports. The SAS method is based

on the concept of personalized and adaptive learning, aimed at providing tailored education to each student according to his or her individual needs, with concentration on the main areas in need of improvement, which manifests in higher levels of academic achievement. Since 2015, we have been investing in technology and our printed methodology has evolved into an educational platform capable of delivering its curriculum content in both printed and digital format. It has also evolved into a robust omni-channel platform, capable of delivering the entire K-12 curriculum in both printed and digital format, withlecturettes featuring expert, on-screen teachers and tailored assignments and assessments to engage students and ensure subject-area mastery across all grades. 37 With this integrated approach, students can track their progress and performance, teachers have access to real-time data to evaluate students and personalize their teaching, and school administrators have access to their school’s performance both on absolute and comparative terms.

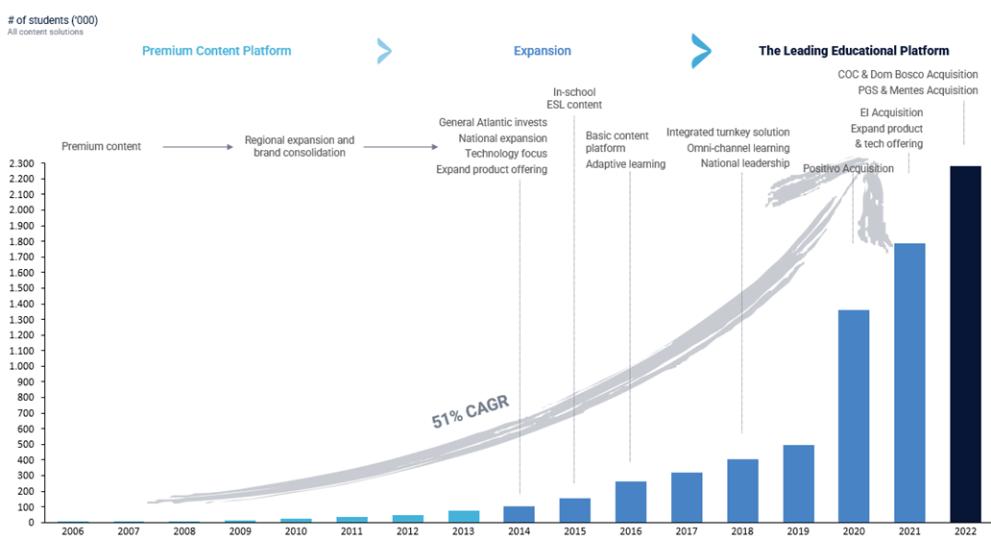

With an asset-light and highly scalable business model that emphasizes operating efficiency and profitability, we were able to grow the number of students served at a On September 25, 2018, the registration On October 29, 2019, we completed a follow-on public offering, consisting of 3,450,656 Class A common shares issued and sold by us, and 4,268,847 Class A common shares sold by certain selling shareholders. The public offering price was US$43.00 per Class A common share. We received net proceeds of US$143.9 million, after deducting US$3.7 million in underwriting discounts and commissions. On November 26, 2019, an additional 661,112 Class A common shares were sold by General Atlantic Arco (Bermuda), L.P. following the exercise by the underwriters of their option to purchase additional shares. On June 4, 2020, we completed a follow-on public offering, by which General Atlantic Arco (Bermuda), L.P. and Alfaco Holding Inc. sold an aggregate amount of 5,563,203 Class A common shares issued by us, at a public offering price of US$47.70 per Class A common share. We did not receive any proceeds from the sale of Class A common shares by the selling shareholders in connection with this offering. 38 On September 8, 2020, we completed a follow-on public offering, consisting of 2,500,000 Class A common shares issued and sold by us. The public offering price was US$44.80 per Class A common share. We received net proceeds of US$109.8 million, after deducting USS$2.2 million in underwriting discounts and commissions. On January 6, 2021, our Board of Directors approved the Repurchase Program to comply with management long-term incentive plan obligations. Pursuant to the Repurchase Program, we may repurchase up to 500,000 of our outstanding Class A common shares in the open market, based on prevailing market prices, or in privately negotiated transactions, over a period beginning on January 6, 2021, continuing until the earlier of the completion of the repurchase or January 6, 2023, depending upon market conditions. On March 31, 2021, our Board of Directors approved the increase of the share repurchase limit of our Repurchase Program to up to 2.5 million of our outstanding Class A common shares in the open market, based on prevailing market prices, or in privately negotiated transactions, continuing until the earlier of the completion of the repurchase or January 6, 2023, depending upon market conditions. As of the date of this annual report, we had purchased an aggregate of 1,818,779 Class A common shares for a total of approximately US$43.2 million under the Repurchase Program. On November 1, 2021, we cancelled 750,000 treasury shares with the approval of our Board of Directors. On December 1, 2021, we issued US$150 million in senior notes convertible into our Class A common shares (US$100 million to Dragoneer, and US$50 million to General Atlantic), bearing interest at 8% per annum in fixed Brazilian reais and maturing on November 15, 2028. Each note will be convertible at the option of the holder into our Class A common shares at the agreed conversion rate, which is equivalent to an initial conversion price of US$29 per share. The conversion price represents an approximately 65% premium to the trailing 30-day volume-weighted share price at the time of signing the investment agreements for the convertible notes. Dragoneer and General Atlantic will beneficially own approximately 5.6% and 2.8%, respectively, of our total shares (on an as converted basis for the convertible senior notes). Following over a decade of growth, and our initial public offering in 2018, we are excited about the future and how technological advances can impact education. We believe that students are increasingly looking for modern, dynamic and client oriented educational platforms and that our tech-enabled approach is positioned to deliver a variety of content and provide a new learning experience that is more effective, personal, engaging, and enjoyable. Acquisitions and Investments Acquisition of Edupass

Acquisition of Eduqo On April 22, 2021, we entered into a purchase agreement for the acquisition of 100% of the equity interest of Eduqo. The transaction closed on July 1, 2021, following CADE’s approval. Eduqo is a learning management system (LMS) platform that connects students and professors, and offers question banks, exams and diagnostics to its clients. The purchase price for the acquisition is structured as follows: (i) R$15,097 million was paid on July 1, 2021, (ii) R$ 6.969 million will be paid on July 1, 2022, and (iii) R$6.504 million will be paid on July 1, 2023. Additionally, on November 16, 2021, Eduqo shareholders and Arco entered into an agreement to amend the earnout structure previously agreed, to a fixed value of R$2.603 million to be paid on July 1, 2023. Investment in Tera On April 9, 2021, we acquired a 23.43% equity interest of Tera for a total amount of R$15 million. The transaction was divided in a capital injection and an acquisition of shares from Tera’s founders and early-stage investors. The company offers tech-related courses such as UX design, full stack development and data analytics, among others, for the B2B and B2C markets. 39 Acquisition of Me Salva!

According to the transaction agreements, 60% of the company’s interest was transferred on the signing date for a total amount of R$27.6 million, and the remaining 40% will be transferred in 2025, in an amount equal to the multiple of the net revenues of Me Salva! Acquisition of COC and Dom Bosco learning systems and PGS and Coleção Mentes do Amanhã supplemental solutions On March 6, 2021, we entered into a definitive agreement with Pearson Education do Brasil Ltda. (“Pearson”) to acquire 100 % interest in P2D, owner of COC and Dom Bosco learning systems, for the total amount of R$920 million, of which (i) 80% was paid on closing, and (ii) the remaining 20% of the purchase price will be paid on the first anniversary of the closing date, as adjusted. The transaction also includes an agreement with Pearson to distribute some supplemental educational solutions for K-12 schools in Brazil. On October 1, 2021, following final approval from CADE for this acquisition, we closed the transaction. The payment terms set forth in the purchase agreement were updated upon closing of the transaction to a total purchase price of R$800.4 million, adjusted for COC’s and Dom Bosco’s cash and working capital positions as of September 30, 2021, paid in a single installment on the transaction closing date. The incorporation of COC and Dom Bosco into Companhia Brasileira de Educação e Sistema de Ensino S.A., our subsidiary incorporating the acquired businesses, is expected to be concluded in the first quarter of 2022. In addition to the acquisition of P2D, CBE entered into a Commercial Cooperation and Distribution Agreement with Pearson pursuant to which CBE would be the sole distributor in Brazil of the PGS bilingual courseware and teaching methodology and the supplemental solution focused on 21st century skills Mentes do Amanhã, with the option to acquire these business lines in the long term. On February 1, 2022, Pearson and CBE entered into an Asset Purchase Agreement and an Intellectual Property License Agreement, pursuant to which CBE acquired the right of such solutions in Brazil for a total amount to be calculated considering 1.5x Net Revenue for 2022, with a base price of R$15.0 million. CBE is licensed to use the PGS trademark until 2026, when a new brand is expected to be launched. Investment in Isaac On January 25, 2021, we entered into a Series B Ordinary Shares Purchase Agreement, among other ancillary and transactional documents, with INCO Limited, or INCO, the controlling entity of OISA Tecnología e Serviços Ltda., or OISA (a company indirectly controlled by David Peixoto dos Santos, Arco’s former CFO), pursuant to which we acquired 8,571,427 series B ordinary shares, equivalent to 30% of the total stock capital of INCO, for R$25 million. INCO Limited provides financial assistance to private schools. In addition, on April 22, 2021, we and other investors entered into a Series A and Series A-1 Preferred Shares Purchase Agreement, pursuant to which we acquired 3,653,788 Series A Preferred Shares of INCO Limited, for R$33.2 million, with the option to acquire an additional 2,935,010 Series A-1 Preferred Shares, which was exercised on September 17, 2021 for an amount of R$52.0 million. As of March 31, 2022, INCO Limited had additional investments rounds in which we did not participate. As of the date of this annual report, we hold 47,375,702 shares of INCO Limited, equivalent to 25.06% of its total capital stock (22.43% on fully diluted basis) representing a total investment of R$110.3 million. 40 Acquisition of Escola da Inteligência On December 2, 2020, we closed the acquisition of Escola da Inteligência, the leading solution in social-emotional learning (SEL) in Brazil, which was approved by CADE, with no restrictions, on the same date. This transaction broadens our supplemental market presence by adding a strong brand to its portfolio. We believe there is a favorable market trend for SEL, pushed forward by the COVID-19 pandemic, and that Escola da Inteligência is well positioned to capture this demand outside and within our school base. The acquisition involves only the private sector business of Escola da Inteligência and under the terms of transaction, we acquired 100% of Escola da Inteligência’s shares, which will be officially transferred in two phases, of which 60% was acquired for R$288 million, with R$200 million paid at closing and the remaining R$88 million in the second quarter of 2021. The amount due for the remaining 40% of Escola da Inteligência’s shares will be calculated considering 6 times the 2023 ACV booking value and will be paid in the second quarter of 2023. The remaining shares will be transferred to us on the day of such payment. For further information, see note 4h to our audited consolidated financial statements. Acquisition of Studos On September 21, 2020, we acquired 100.0% of the outstanding shares and voting rights of Studos, a leading provider of adaptive solutions. For further information, see note 4f to our audited consolidated financial statements. This acquisition is part of our strategy to acquire technology companies that increase the value of our learning systems to partner schools and parents, improve student’s academic performance and enable teachers to thrive. Investment in Bewater Ventures I GA On July 24, 2020, we acquired a 14.48% interest in Bewater Ventures I GA, a fund legally managed by Paraty Capital, through the purchase of 9,670 Class B quotas for R$9.7 million. As a result of the fund's capital call, we currently own 9,713 Class B Shares, equivalent to a 11% interest, representing a total investment of R$9.8 million The fund’s main goal is the minority investment in Grupo A, a company that provides educational solutions for higher education, which happened subsequently to our investment. For further information, see note 11 to our audited consolidated financial statements. Acquisition of Positivo Soluções Didáticas On November 1, 2019, we closed the acquisition of Positivo, one of the largest K-12 content providers to private schools in Brazil, and other companies of the Positivo Group (as defined below), or Positivo Acquisition. Positivo is part of a group founded in 1972 in Curitiba by a group of teachers as a preparatory course focused on admission exams to universities in the state of Paraná, or Positivo Group. The preparatory course reached 2,300 enrolled students in the first year of operation and its success led the group to quickly open new schools for all K-12 grades under the brand Colégio Positivo. In a short period of time, the proprietary content and methodology developed and used by Colégio Positivo schools achieved significant recognition among teachers, parents and students. The high-quality content and its dynamic approach led to the foundation of Positivo in 1979, allowing the Positivo brand to expand far beyond the reach of Colégio Positivo, being adopted by third-party schools in several cities of the state of Paraná and other Brazilian states. With over 40 years of brand legacy, Positivo evolved to become a leading content providing platform that transforms the lives of many students of private schools across all Brazilian states. This is a vibrant ecosystem with several opportunities to effectively address the needs of parents, students, teachers and school owners. Positivo is focused on building long-term relationships with partner schools and this approach is an important factor to its success, proven by the fact that more than 50% of its client base has over ten years of relationship. This carve-out acquisition encompassed only the private school learning systems and did not include the other assets of the Positivo Group, such as the public-school learning system, the printing company, the Universidade Positivo post-secondary education business, and the Colégio Positivo proprietary schools. 41 The agreed purchase price was R$1,684.8 million (equity value), of which (i) 50% was paid in cash on the transaction closing date, and (ii) the remaining 50% will be paid in four installments as follows: (1) 10% per year to be paid in cash in each of 2021 and 2022, and (2) 15% per year to be paid in cash in each of 2023 and 2024, all as adjusted by the CDI rate (Brazilian interest rates). The Positivo Acquisition allowed us to increase our student base twofold, reaching over 1.2 million students in 2019. In addition, it allowed us to accelerate our growth with the same B2B2C business model, with predictable subscription-based revenue, high operating leverage and cash flow conversion while remaining asset-light. By adding complementary assets, Positivo also enables us to broaden our product offerings and expand our footprint. Positivo comprises two different brands with reciprocal business profiles: (i) Sistema de Ensino Positivo, or SPE, an educational solution consisting of content, technology and services provided to private schools serving upper-middle-income students; and (ii) Conquista Solução Educacional, or Conquista, which is focused on private schools serving lower-middle income students. Together, SPE and Conquista enhance our Core Curriculum offering, allowing us to reach a larger base of schools at different price points. In addition, Positivo also owns Positivo English Solution, or PES, an affordably priced second language-offering that enhances our Supplemental Solutions. Positivo has a strong presence in the South and Southeast regions of Brazil, with relatively low geographic overlap with our student base. The acquisition will also allow us to add opportunities through our scale and technology, strengthening our capacity to invest in high quality content and technology and enabling us to enhance our student base experience and academic outcomes through technology improvements and our cross-selling capabilities. Acquisition of EEM On June 4, 2019, we closed the acquisition of EEM, or the EEM Acquisition, an app developer that enhances communication between schools and parents by providing chat-based interactions, location-based identifications, Net Promoter Scores, or NPS, tool to assess parent’s satisfaction and pilot project related to payments. The EEM Acquisition provided us with new capabilities that further increases our value proposition to partner schools, parents and students, and also allowed us to access EEM’s network of schools. The purchase consideration transferred was R$18.3 million. The amount of R$16.1 million was paid on the closing date, the amount of R$0.3 million was paid on June 29, 2019, and the deferred payment in the amount of R$1.9 million, which has been retained for a period of two years as guarantee for the payment of any contingent liabilities, will be released in accordance with the provisions of the agreement. Any remaining balance will be transferred to the former owners of the acquired entity. For further information, see note 17c to our audited consolidated financial statements. Acquisition of NAV In May 2019, we acquired a 13.2% interest in the share capital of NAV, a developer of competence-based learning content present in more than 50 schools and reaching 16,000 students, according to NAV’s website, for the total subscription price of R$4.2 million, hereinafter referred to as the NAV Acquisition. Pursuant to the investment and share purchase agreement, we have agreed to acquire the remaining 86.8% of the outstanding share capital of NAV in three tranches. We acquired: (i) Tranche 1, corresponding to 37.8% of the outstanding share capital of NAV, on October 29, 2019, for the amount of R$21.1 million, and (ii) Tranche 2 and Tranche 3, corresponding to 24% and 25% of the outstanding share capital of NAV, respectively, on February 15, 2021, for the total amount of R$22.6 million. By anticipating the payment of Tranche 3, NAV became our wholly owned subsidiary on February 25, 2021. NAV enhances our Supplemental Solutions offering and the cross-selling capacity of our Core Curriculum offering through a competence-based curriculum to address 21st century skills. The EEM Acquisition and NAV Acquisition provide us with new capabilities that further increases our value proposition to partner schools, parents and students, and also allows us to access each acquisition’s network of schools. Through projects, problem solving and technology, NAV helps students develop transferable skills, such as critical and creative thinking, and communication skills. Acquisition of Geekie In December 2016, we acquired a 6.54% interest in Geekie, an entity that provides technology for adaptive assessment and learning products and engages in the production, development and licensing of software tailored to the specific requirements of 42 education sector customers. On September 20, 2019, we acquired an additional 0.96% interest in the share capital of Geekie through a capital increase of R$1.2 million. On October 14, 2019, we acquired an additional 1.92% interest in the share capital of Geekie through a capital increase of R$2.5 million, increasing our total interest to 10.92%. In addition, on October 25, 2019, we acquired an additional 18.44% interest in the share capital of Geekie from a minority shareholder for the amount of R$21.9 million, increasing our total interest to 29.36%. On November 15, 2019, we acquired an additional 1.17% interest in the share capital of Geekie through a capital increase of R$2.0 million, increasing our total interest to 30.53%. In December 2019, we acquired an additional 7.00% interest in the share capital of Geekie through a capital increase of R$4.3 million and the purchase of minority shareholders for R$5.8 million increasing our total interest to 37.53% as of December 31, 2019. On March 4, 2020, we acquired an additional 10.51% interest in Geekie’s share capital from minority shareholders for R$12.7 increasing our total interest to 48.04%. On July 6, 2020, we acquired an additional 4.62% interest in Geekie’s share capital from minority shareholders for R$5.8 million, increasing our total interest to 52.67%. On September 21, 2020, we acquired an additional 1.76% interest in the share capital of Geekie through a capital increase of R$4,500 increasing its total interest to 54.43%. On November 11, 2020, we acquired an additional 1.64% interest in Geekie’s share capital through a capital increase of R$4,500 increasing our total interest to 56.06%. On January 20, 2021, we acquired an additional 1.36% interest in Geekie’s share capital through a capital increase of R$4,000, increasing our total interest to 57.42%. On November 27, 2020, we entered into a new shareholders’ agreement with the other Geekie’s shareholders, by which we acquired control of Geekie and started to consolidate Geekie in our financial statements as our subsidiary. We expect to acquire the remaining 42.58% interest in Geekie’s share capital in June 2022, for the amount to be calculated considering the ACV of Geekie or Arco for 2022 and the company’s debts, whichever results on the highest amount to be received by the sellers, and the net revenue of Geekie products as of January 2023, which will be payable in June 2022 and January 2023. For further information, see note Acquisition of SAE In June 2016, we acquired a 70% interest in the share capital of SAE. In October 2017, we acquired the remaining 30% in the share capital of SAE. Acquisition of International School In December 2015 The Investment Agreement contains certain contractual arrangements for the 43 Pursuant to the Acquisition of Content Providers In April 2015, we acquired a 99.99% interest in Editora e Livraria Alegre POA Ltda., a content provider to Acquisition of WPensar In April 2015, we acquired a 25% interest in WPensar, a company that develops and licenses school management systems software. Corporate Information Our principal executive offices are located at Rua Augusta 2840, 9th floor, suite 91, Consolação, São The SEC maintains an internet website that contains reports and other information about issuers, like us, that file electronically with the SEC. The address of that website is www.sec.gov. Investors should contact us for any inquiries through the address and telephone number of our principal executive office. Our principal website is www.arcoeducacao.com.br. The information contained in, or accessible through, our website is not incorporated into this annual report.

Our mission is to transform the way students learn by delivering high-quality education at scale through technology to schools and students. We provide a complete pedagogical system with technology-enabled features to deliver educational content to private schools and students in Brazil. Our turnkey curriculum solutions provide educational content in both printed and digital formats delivered through our platform to improve the learning process.

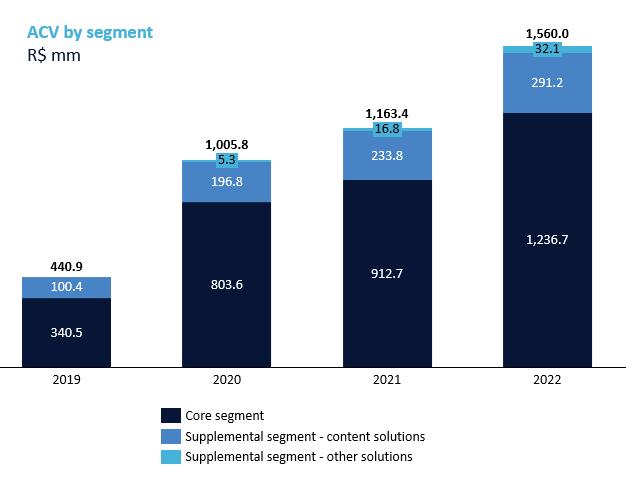

We have an asset-light, 44 Our network in our B2B2C Core Curriculum and Supplemental Content Solutions as of March 31, 2022, consisted of 8,056 partner schools compared to 6,119 schools as of March 31, 2021, 5,414 schools as of March 31, 2020, and 1,464 schools as of March 31, 2019, representing annual growth rates of 31.7%, 13.0% and 269.8%, respectively. We had 2,279,025 expected number of enrolled students, or Number of Enrolled Students, across all Brazilian states as of March 31, 2022, compared to 1,489,707 final number of enrolled students, or Final Number of Enrolled Students of as of September 30, 2021 (or 1,785,576 Number of Enrolled Students as of March 31, 2021), 1,362,141 as of March 31, 2020, and 498,553 as of March 31, 2019, representing annual growth rates of 27.6%, 31.1% and 173.2%, respectively. In years prior to the COVID-19 pandemic, the difference between our Number of Enrolled Students and our Final Number of Enrolled Students was not material. However, during 2020 and 2021 and as result of the impacts of the COVID-19 pandemic, our partner schools experienced atypical dropout rates from March 31 to September 30 ”. Our B2B2C Core Curriculum and Supplemental Content Solutions business model has allowed us to grow and achieve profitability since our founding. Our net revenue totaled R$ ACV Bookings for the Supplemental Solutions (both B2B2C Supplemental Content Solutions and other supplemental solutions) totaled R$323.3 million for the 2022 school year, resulting in a 2% ACV market share of the total addressable market of such segment in Brazil, which includes after-school education, based on Educa Insights’ 2021 assessment of the private K-12 market. In addressing the core solutions market, Arco’s ACV Bookings for the 2022 school year of R$1,236.7 million results in a 24% core solutions market share, which considers the potential market for private K-12 learning systems and textbooks in Brazil, based on Educa Insights’ 2021 assessment of the private K-12 learning systems market. We believe that the quality of our platform, together with the credibility of our client base and the strong reputation of our brand, has driven our significant growth, allowing us to expand our footprint quickly and efficiently In March 2021, Arco started serving students directly through the acquisition of Me Salva!, a B2C test prep player. The online solution offers recorded and live video classes, comprehensive exercises, essay writing tools, assessment tests, 1-on-1 tutoring and personalized study plans. Despite currently representing only a small and immaterial part of our business, this vertical allows Arco to tap a large and underserved market of students from public schools, that lack quality education at affordable prices. We also plan to reinforce our Supplemental portfolio by offering schools a solution on the test prep and tutoring vertical, developed on top of Me Salva!’s know-how and digital offering, allowing them to better prepare their students for the ENEM. Context The 21st century has been characterized by rapid and accelerating technological innovation, with students at the forefront of the adoption of new technologies. We believe that we can deliver a more effective, personal, engaging, and enjoyable learning experience for students by combining We founded our company with the aim of creating 45 training, and commercializing and managing K-12 education. Simultaneously, students acquired educational content through textbooks from various publishers across retail channels. Our platform aims to replace this multitude of third-party educational providers with a streamlined, one-stop solution that delivers high quality education at scale. Our Core Curriculum and Supplemental Solutions enable students, teachers, and school administrators to have access to engaging and easy-to-use resources that propel academic success and meet students’ diverse learning needs. Pairing our printed and digital curriculum with real-time data and teacher-led learning allows us to personalize learning at the individual level, improving both individual student and aggregate school performance. We develop our educational content using a model based on extensive research and performance-based standards. We combine printed and digital content with onlinelecturettes featuring expert, on-screen teachers and tailored assignments and assessments to engage students and help them master their subject areas. With this integrated approach, students can track their progress and performance, teachers can access real-time data to evaluate students and personalize their teaching and school administrators can better manage their school’s performance both on absolute and comparative terms. The increase in internet penetration and the rapid increase in the use of mobile devices and cloud-based services is broadening access to educational content and services and expanding the potential reach of educational institutions. Our platform does not require our partner schools to make any significant capital expenditures or setup investments and is compatible with most mainstream computing platforms (including tablets and mobile phones). Our solutions are designed to be highly interactive and enjoyable, which we believe results in enhanced educational outcomes when compared to traditional models.

Underlying Trends We believe that the strength of our business and Demand for quality education is driving a shift from public to private K-12 education A wide gap in the quality of education 2011. Technological innovation is driving enhancements in private K-12 education

Technology has created opportunities to make learning more affordable, accessible, flexible, personal and effective. Classroom instruction and delivery models are changing and are likely to have a substantial impact on the industry.

46 As a result of the COVID-19 outbreak, which was declared a pandemic by the World Health Organization in March 2020, state and local authorities in Brazil suspended school operations. On-site school activities were postponed, forcing schools to teach classes remotely. Although schools have historically been late adopters of technology and resistant to change, the impacts of the COVID-19 pandemic led them to turn to technology to continue offering their students educational content and pedagogical support. As part of our sales strategy during the COVID-19 outbreak, we have unbundled part of our solutions throughout 2020, allowing approximately 400 schools to use the trial versions of our products and therefore creating a large pipeline of leads for the following commercial cycles. We believe that as we have rapidly evolved our solutions to meet schools needs during the COVID-19 pandemic, we are now uniquely positioned to benefit from the higher willingness from schools to adopt learning systems that offer quality content combined with technological features that will improve the learning experience. Importance of K-12 performance in university admissions processes The best higher education institutions in Brazil are public, with a highly competitive admissions process based largely on challenging standardized admissions exams. According to Expansion of school hours and after-school programs including, but not limited to, English as a Second Language, or ESL, bilingual programs and 21st century skills programs The increased focus on education has led to an increase in the length of the average school day. After-school education,

For many parents, after-school education is considered a lifeline that helps them work without worry and balance their schedules, given (i) that Brazil has one of the highest average working hours per week in the world, and (ii) the increased participation of women in the workforce. In addition, an increase in disposable income has increased demand for private education and after-school programs, and parent expectations for their children’s education are high considering the strong competition to gain admission into top public universities. Accordingly, Obsolescence of traditional content distribution models We believe that traditional content distribution models are becoming obsolete. Traditional educational publishers are almost exclusively focused on physical textbooks, which they sell through retailers rather than directly to schools. These traditional suppliers have limited capability to develop and offer integrated digital solutions to schools, teachers, and students, and typically rely on 47 party authors, illustrators and graphic designers to develop new content. In contrast, because of our robust technology backbone, use of data and strong relationships with teachers and administrators, we can offer a comprehensive solution and content that is continuously updated and improved. Limited and unintegrated product offering Due to the lack of turnkey education solutions, school administrators often rely on a multitude of third-party vendors for K-12 educational content, teacher training, student testing, management, and communication tools. Traditional education providers have struggled to develop mission critical education platforms for several reasons, including the significant costs associated with the development of content and technologies, as well as the lack of extensive in-house technological expertise. In addition, developing a comprehensive and effective methodology is difficult to achieve since it requires many years of proven educational experience and a successful track record. We

Our Market Opportunity According to

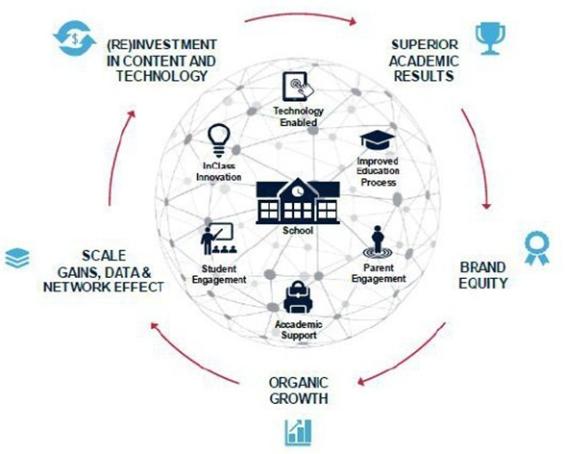

We believe that the challenges inherent in the traditional content distribution model, coupled with increasing demand for modern content and integrated value-added services, present a unique market opportunity for our business. By providing an affordable, modern, and efficient platform, we believe that we can continue to disrupt the Brazilian education market and increase our penetration into current and new markets. As for our B2C model, we benefit from the intense competition for higher education admission driving demand for test prep, as the best universities in Brazil are public (and costs are subsidized by the government) and offer a leap in earnings potential for students. As a result, parents and students demonstrate unmet needs and willingness to pay for access to top quality content, individualized learning, and convenience. The K-12 tutoring, and test prep markets are very fragmented and currently mostly offline, while we observe an increasingly preferred for online due to cost, quality and convenience. Additionally, COVID-19 pandemic to further accelerates the habit-change and conversion from offline to online. The Arco Way Quality, a key component for the success in the K-12 market, is always at the center of our decisions and it has been the gear of our virtuous cycle over the years.

48 According to the 2022 university admission data published through the Unified Selection System, 1,513students within our partner school base have been accepted in the first place of their respective majors (an 15% increase when compared to 1,318 students in 2021, considering the same solutions). Considering the number students within our partner school base that were accepted in top 10 positions, the number increases to 7,242 students (a 4% increase when compared to the 6,981 students in 2021, considering the same solutions). The strong results achieved by our partner schools improve our brand equity, help build our reputation and As we grow and add new partner schools, our network becomes a powerful source of leads generation and data. In addition, the increased scale allows us to reinvest in content, quality, and service, contributing to the positive loop.

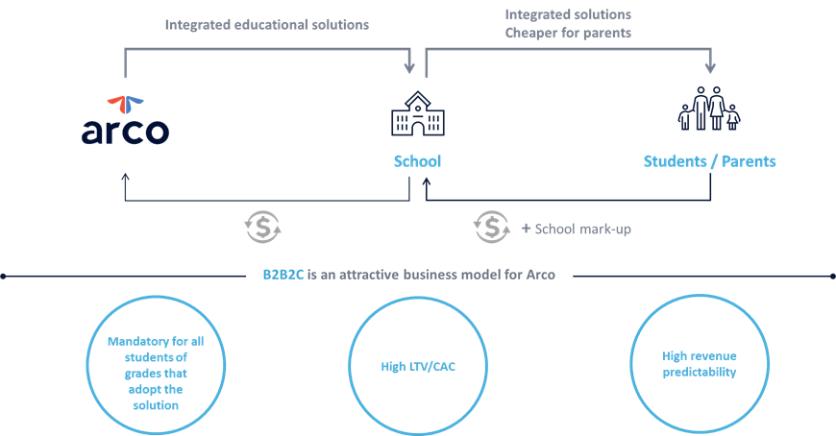

Our Business Model Our B2B2C model is financially aligned with our partner schools. Our revenues consist of wholesale content fees paid by our partner schools annually on a per-student, per-year basis. On average, partner schools charge students’ parents an incremental markup on top of our wholesale fees, ensuring that their incentives are aligned with ours. Accordingly, we provide a supplemental revenue stream to our partner schools through our B2B2C model, which is a feature that the traditional education model does not employ. Once schools adopt our platform for a particular class year, access to, and payment for, our platform becomes mandatory for all enrolled students in each class year, and such payments are charged as a supplement to tuition. Typically, we revise our contract fees annually, in line with our price-setting policies, which are usually above published inflation indices, to account for improvements in our platform and for changes in our cost and expenses

49 The following chart illustrates our business-to-business-to-consumer (B2B2C) model:

A portion of our historical average 6.0% annual attrition rate is attributable to the early termination or suspension of performance by us, at our option, of contracts with certain partner schools as a result of their failure to timely pay our contract fees.

Our platform on the B2B2C model is difficult to replicate. We have continuously developed our platform since our founding, with the benefit of over 50 years of an evolving educational methodology and a dedicated team of education specialists focused on developing and improving our Core Curriculum and Supplemental Solutions materials. Accordingly, we believe that the depth of our educational content and the technological experience necessary to develop our products makes our platform difficult to replicate. Our B2C model is 100% subscription-based and has attractive unit economics. Our revenues consist of retail content fees paid by students upon subscribing for one of our plans. Despite shorter-term when compared to our B2B2C model, customer acquisition cost is also reduced, leading to profitable unit economics. Our Solutions In the education sector, we believe that quality is fundamental. Our platform on the B2B2C model was developed with the benefit of over 50 years of an evolving educational methodology and robust track record of academic results. Our track record of high-performing educational outcomes motivated us to create a digital, technology-driven product that could deliver high quality education at scale. 50 Additionally, Positivo is the pioneer in the learning system segment in Brazil and has served the K-12 private school market for more than 40 years. The pedagogical methodology developed inside the Colégio Positivo schools was transformed into a comprehensive educational solution that quickly expanded to other schools in Brazil. Over time, Positivo expanded its product offering to address different profiles of schools and increase its addressable market. We provide a complete suite of turnkey curriculum solutions and technology-enabled features to help our students, teachers, partner schools and parents, targeting our students’ educational success.

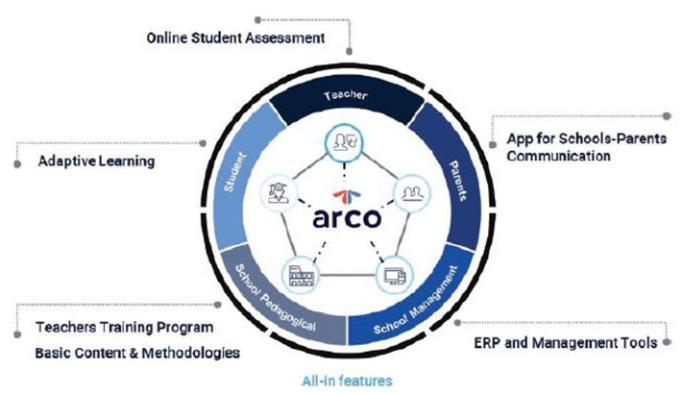

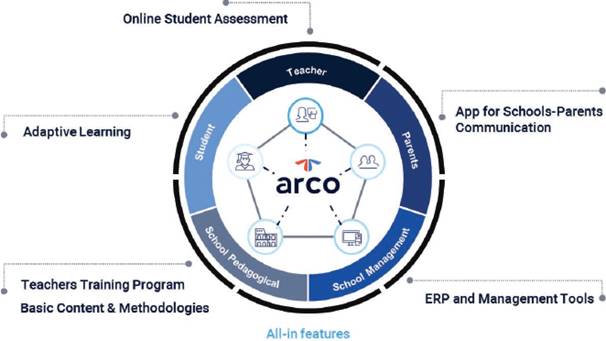

Our turnkey educational platform solutions comprise core K-12 curricula, as well as supplemental language and 21st century skills programs (such as social and emotional learning - SEL). Benefits Across Our Educational Platform We deliver the following benefits to all the stakeholders engaged in the learning process:

51 Our Products We believe that innovation is an important part of our success. As a technology company in the education sector, we believe that our dynamic and adaptive nature is essential to our continued growth. Our product offerings

Our Core Curriculum comprises

As part of our Core Curriculum, we offer complementary support

52

Our Supplemental Solutions We have a Supplemental Content solutions market share of 2%, calculated by dividing Arco’s Supplementary Solutions ACV Bookings for the 2022 school year by the total addressable market for Supplemental Solutions, which consists of English as a Second Language (ESL) bilingual programs (International School, PES and PGS) and 21st century skills programs (Pleno, Escola da Inteligência, NAV and Mentes), based on Educa Insights’ assessment of the private K-12 market. We started offering Upon the acquisition of Positivo in 2019, our Supplemental Solution also offers the PES, a bilingual program with an approach that promotes integrated learning of content and language, in partnership with Cambridge University Press. The program consists of 2-5 weekly hours of English classes with several tools to develop the skills needed to communicate well. PES also provides teachers’ training and pedagogical support to its partner schools. PES was launched in 2015 and has a strong cross-sell potential within our Core Solution partner schools’ network and to expand to schools that have not yet adopted our solution. In 2019, we started investing in the development of a social-emotional supplemental solution called Pleno, developed to meet schools’ demand for a product that goes beyond the student’s cognitive development. Through the same B2B2C business model and integrated with the K-12 curriculum, Pleno helps students to develop competencies and skills, such as self and social-awareness, design thinking and entrepreneurship.

In December 2020, we concluded the acquisition of Escola da Inteligência, the leading solution in social-emotional learning (SEL) in Brazil, based on a proprietary methodology and great reputation in the K-12 market. In February 2022, we acquired PGS, a K-12 bilingual courseware and teaching methodology, formerly known as Pearson Global School, complementing our ESL offering with a high-quality solution with a differentiated pricing point; and Mentes do Amanhã (“Mentes”), a K-12 supplemental solution focused on 21st century skills (social-emotional learning, financial literacy, and technology). 53 We intend to continue adding supplemental educational modules to our Supplemental Content Solutions portfolio over time, broadening Arco’s supplemental market presence by adding high-quality solutions with pricing complementarity to our current offering. Arco believes in the large potential for English as a Second Language and in the favorable market trend for 21st century skills. An even stronger portfolio better positions Arco to capture this demand outside and within Arco’s school base. The key attributes of our Supplemental Solutions are:

Our Supplemental offering also includes other solutions such as technological and managerial features to partner schools, B2C test prep and education as a benefit. Our tech and managerial features include (i) WPensar (acquired in 2015), a company that develops and licenses school management systems software, (ii) Escola Em Movimento, or EEM (acquired in 2019), an app developer that enhances communication between schools and parents by providing chat-based interactions, location-based identifications, Net Promoter Scores, or NPS, tool to assess parent’s satisfaction and pilot project related to payments, (iii) Studos (acquired in 2020) a leading provider of adaptive solutions, and (iv) Eduqo (acquired in 2011), a learning management system (LMS) platform that connects students and professors, and also offers question banks, exams and diagnostics to its clients. In March 2021, we acquired Me Salva!, a B2C digital test prep solution, allowing Arco to start delivering high quality education to public sector students at affordable prices. Finally, in February 2022, we acquired Pearson Global School, a K-12 bilingual courseware and teaching methodology, and Coleção Mentes, a K-12 supplemental solution focused on 21st century skills (social-emotional learning, financial literacy and technology). In September 2021, we acquired EduPass, a company that offers education as a benefit to corporate clients and aims to prepare the Brazilian workforce to the future of work through education and upskilling. Our Team and Culture We have a strong corporate culture, and we encourage our employees to actively adopt it. We believe in: 54 Technology We believe that the use of technology is fundamental to achieving our goal of placing each student at the center of the educational experience. In our view, technology is a To implement our vision, we’ve redesigned our structure, creating ArcoTech, a centralized tech unit responsible for integrating our user experience¸ maximizing the value of our products and reducing the time spent with repeated demands. The revamp of our technological backbone will allow for an easy plug-and-play structure for specifics products to all Arco brands - respecting their individuality and value proposition. Our application programming interfaces, or APIs, provide a standardized way to provision, manage, engage, and deliver content to students, faculty and administrators. The APIs manage authentication and access for our entire technology stack and is designed to manage and interface with new technologies as they are introduced. All Our products help (i) schools to create and manage their classes more efficiently; (ii) teachers to easily transpose their content into the platform, access thousands of questions, schedule classes and keep up with their student’s development; and (iii) families to be closer to their children’s performance through the usage of easy-to-use communication tools.

Following the best frameworks in digital product development, we offer a buy-and-build solution from the customer The main drivers of our technology strategy are:

What Sets Us Apart We believe that we have the following business strengths that allow us to disrupt the private K-12 education market: 55 Disruptive approach to traditional school model Instead of simply delivering content as a product through textbooks, we provide an education solution through a technology-based platform. We believe that our platform is cutting-edge, modern, dynamic and According to internal studies, we believe that the parents of As of December 31, Strong combination of content development team and technology to develop a best-in-class learning experience As of December 31, Widespread positive customer satisfaction and strong academic outcomes Our customer satisfaction is driven by our ability to meaningfully improve the performance of our partner schools’ enrolled students SISU system (Sistema de Seleção Unificada, or Unified Selection System): Strong brand equity and aligned incentives resulting in high retention rates We prioritize quality by employing a “white glove” service model across our business, with clear financial incentives (in the form of bonuses) to our sales force that drive long-term relationships with our partner schools. Educational performance is one of the main drivers of school growth, and the success of our partner schools is a critical part of our value proposition. Due to the quality of our academic outcomes, we rarely lose clients. In addition, we have historically been highly effective in increasing contract

93% in 2021, 93% in 2020 and 93% in 2019. Attractive financial model with a high level of visibility and predictability We have cash flow visibility given our long-term contracts with partner schools. Initial contract terms generally average three years, with high switching costs resulting in a customer churn of approximately 56 Founder-led and experienced management, innovation-driven culture Our culture flows from our founder and CEO’s family, who have specialized in education for over 50 years. Our founder and CEO, Mr. Ari de Sá Cavalcante Neto, has brought his family’s successful school formula to scale by creating a leading educational platform. We strive to innovate and instill in our professionals a passion for serving all As of December 31, Our Growth Strategies We aim to continue driving rapid, profitable growth and to generate greater shareholder value by implementing the following strategic initiatives: Deepen relationships with our existing customer base We intend to increase student enrollments within our existing partner schools at a minimum marginal cost as we see major opportunities for increased penetration through:

Expand our partner school base

known, our sales efforts will benefit from the referrals generated by current school base. Add new Supplemental Solutions We consistently review potential opportunities to provide additional Continue to innovate and extend our technological leadership Innovation is a cornerstone of our culture. As such, we employ significant efforts and resources to ensure the constant development and improvement of our portfolio of solutions. We have also invested in a select group of education technology startups 57 We intend to increase the functionality of our platform and continue our investment in the development and acquisition of new applications that extend our technological leadership. We also intend to continue to improve and update our print and digital content based on the real-time feedback we receive from our partner schools.

Continue to pursue M&A opportunities We plan to continue We believe that we have developed a strong capability and track record of identifying, negotiating, and integrating acquisitions. Moreover, we have developed a systematic model that enables us to integrate our acquired businesses in a timely and efficient manner. Since 2011, we have successfully acquired or invested in We have already executed several strategic transactions since our Investments.” Marketing and Sales Our platform has evolved into a complex solution. The adoption of our platform by partner schools requires us to first build trust and confidence in our solutions, which can only be achieved by engaging them with our solutions and demonstrating a proven track record of success and quality, while constantly monitoring client satisfaction and feedback. We have a non-traditional sales approach, which is structured around a practice we refer to as “Educational Consulting,” which reflects both our core value of ensuring that education is our first priority, as well as the unique sales dynamics associated with our industry. We have a lead time (which we define as the period from the moment of first contact to the execution of a contract) for the acquisition of new partner schools, and we typically enter The success of our sales process requires uniquely qualified professionals, who must not only have an academic background, but are also

58 data, is continuously undertaking industry research and analysis and receives regular feedback from, and is in regular contact with, our consultants deployed in the field. Additionally, we promote specialized events that are aimed to retain current partner schools. The most relevant event is Positivo’s Course Program that provides teacher’s training, workshops of recent trends in education and lectures from highly specialized and trained pedagogical professionals. In 2021, the Course Program reached 3,975 teachers. In addition, we work in conjunction with a branding agency, which assists us in developing and strengthening our brands, increasing their national awareness, and building our institutional image. Our brand portfolio is structured to reflect our value proposition and leverage our marketing and sales strategy. A study conducted by Expertise as of July 2021 showed that the Positivo brand is the most recognizable among parents, teachers, and school events.

the contract. The loyalty program allows SPE to offer more personalized consulting services from our pedagogical experts, literature materials to complement the school’s curriculum, cooperative media, and other products or services, to increase a contract’s profitability. Our Customer Service and Support We believe that the best way to ensure the loyalty of our customers is to maintain a healthy, long-term relationship with our partner schools. We aim to achieve this through our customer engagement and support service, which supports partner schools in the implementation and integration of our educational solutions into their systems, as well as help them identify and achieve their pedagogical, business and Pedagogical Consulting Our pedagogical consulting department is responsible for the pedagogical supervision and educational development of our partner schools. It aims to ensure that our educational platform is being used efficiently, and to actively assist our partner schools in improving the learning experience of their students and helping them develop the necessary skills inside and outside the classroom. It also leverages a dedicated management team to train and support our partner schools in maximizing their supplemental revenue streams. Our pedagogical consulting team activities with partner schools include:

59 Customer Support Our customer support department provides day-to-day customer and administrative support to our partner schools in connection with our educational platform by e-mail and/or by telephone. Our customer support department interacts with our pedagogical consulting department when necessary to minimize the risk of miscommunication and ensure a unified approach to customer satisfaction. Our Geographic Presence We believe our platform can be adopted by virtually any private ACV Bookings. Our Clients We Our Competition We compete with traditional publishers and textbook providers, other providers of core curriculum solutions, as well as with online education platforms. Factors influencing competition in this industry may include price, overall education experience and track record, industry experience and reputation, content quality, availability of technology, faculty, facilities, location and program offerings, among others.

Most traditional publishers and textbook providers are typically focused exclusively on physical textbooks. They do not produce their own content, do not update their content frequently, and do not have developed digital platforms. Furthermore, we believe that traditional publishers and textbook providers whose strategy it is to develop education solutions similar to ours do not possess the content development expertise, brand awareness, or the track record to sell such solutions directly to schools. Other core curriculum solutions providers offer primarily printed content and a limited amount of digital content. Other online platforms that offer education solutions through digital channels face difficulties to efficiently integrate solutions for schools, parents, students, and teachers. We believe our proprietary content is engaging to students, teachers, and parents, as illustrated by our ability to persuade schools to switch from other products to our products. We seek to differentiate ourselves from our competitors primarily on the basis of our simple, integrated and personalized educational platform. We believe the following factors are critical to success in the private K-12 education in Brazil:

60

Table of

Seasonality Our revenues and operating results normally fluctuate ESG, at Arco Arco was born with the mission to transform the way students learn by delivering high quality education at scale. We believe that our mission and the social impact we aim to achieve will only be delivered if we are able to engage our stakeholders and manage properly our Environmental, Social and Governance risks. During 2021, we conducted a ESG’s materiality process in consultation with a specialized ESG firm, which identified the material topics for our company and prioritized them through interviews and a survey with over 200 stakeholders, including employees, investors, sell-side analyst, suppliers and Non-Governmental Organizations supported by the Arco Institute. We also established an ESG Advisory Group constituted by Arco’s CHRO, COO, CFO and legal department, which supported the establishment of material topics, the prioritization according to the business impact, the engagement of the whole team and communication with different areas of the Company. As a result, we have established three ESG pillars: Promote the Impact on Education To guarantee Arco’s continuous evolution, we need to keep delivering and improving the quality of our content and technology, be able to grow in scale and increase the accessibility of our products and services. Our progress in those topics is quantified by our ability to:

In our latest ESG report, we have quantified those aspects through different metrics, such as NPS, retention rates and number of National Exam approvals, among others. Focus on our people Arco is a company built upon the belief that our people is our strength. We are constantly looking for highly talented and diverse people, aligned with our values and engaged on delivering our purpose. We work to maintain a sense of ownership and engagement by investing in the development and continuous evolution of our people, creating a diverse environment in which people belong and can prosper. 61 To measure the success of our people-centric culture, our teams’ perception regarding Arco and its career opportunities, we track:

Strong and sustainable structure This pillar can be divided in two main parts. The first part, relating to our corporate governance and stakeholders’ alignment, is ensured by:

For further information on Corporate Governance, please see Item 16.G of this annual report, as well as the main indicators on our ESG Report. With respect to the second part, regarding the sustainability of our supply chain, we work constantly to reduce our impact in the environment by:

We have also established goals to constantly evolve our ESG practices. For further information, please see our 2021 ESG Report published on our IR website (https://investor.arcoplatform.com/esg/). Legal Proceedings See “Item 8. Financial Information—A. Consolidated statements and other financial information—Legal Proceedings.” Regulatory Overview The Brazilian constitution establishes education as a right of all citizens, the provision of which is a duty of the state and the family. Accordingly, the government is required to provide all Brazilian citizens with access to free primary education that requires 62 compulsory attendance. Private investment in education is permitted so long as entities providing education services comply with the applicable rules and regulations. The Brazilian education system is organized as a cooperation regime among federal, state, and municipal governments. The federal government is required to organize and coordinate the federal education system in order to guarantee equal opportunity and quality of education throughout Law No. 9,394/1996, or