The Group is exposed to inherent risks in relation to changing technology and systems

The Group is reliant upon certain technologies, systems and systems (including IT systems)platforms for the running of its business, particularly those which are highly integrated with business operational processes. DisruptionSome of these are dependent upon the products and services of third-party technology providers. The failure of any such third-party provider to those technologies provide products and/or systemsperform services could materially adversely affectimpact the efficiency of the business, notwithstanding business continuity or disaster recovery processes. Group’s business.

The Group may also have to make substantial additional investments in new technologies or systems to remain competitive. Failing to keep pace with developments in technologies or systems may put the Group at a competitive disadvantage. The technologies or systems that the Group chooses may not be commercially successful or the technology or system strategy employed may not be sufficiently aligned with the needs of the business or responsive to changes in business strategy. As a result, the Group could adversely affect guest experiences, lose customers, fail to attract new customers, or incur substantial costs or face other losses.

The Group is reliant on the reputation of its brands and the protection of its intellectual property rights

Any event that materially damages the reputation of one or more of the Group’s existing or new brands and/or fails to sustain the appeal of the Group’s existing or new brands to its customers may have an adverse impact on the value of that brand and subsequent revenues from that brand or business.

In particular, where the Group is unable to enforce adherence to its safety or operating and quality standards, or the significant regulations applicable to hotel operations, pursuant to its franchise and management contracts, there may be further adverse impact upon brand reputation or customer perception and therefore the value of the Group’s brands.

In addition, the value of the Group’s brands is influenced by a number of other factors, some of which may be outside the Group’s control, including commoditization (whereby price and/or quality becomes relatively more important than brand identifications due, in part, to the increased prevalence of travel comparison websites and online travel agents), consumer preference and perception, or other factors affecting consumers’ willingness to purchase goods and services provided by the Group.

Given the importance of brand recognition to the Group’s business, the protection of its intellectual property poses a risk due to the variability and change of controls, laws and effectiveness of enforcement globally. Any widespread infringement, misappropriation or weakening of the control environment could materially harm the value of the Group’s brands and its ability to develop the business.

The Group is reliant upon its proprietary reservations system and is exposed to the risk of failures in the system and increased competition in reservations infrastructure

The value of the Group’s brands is partly derived from the ability to drive reservations through its proprietary HolidexPlus reservations system, a central repository of the Group’s hotel room inventories linked electronically to multiple sales channels including the Group’s own websites, call centers and hotels, third party intermediaries and travel agents.

Lack of resilience and operational availability and/or the failure of a third-party technology provider could lead to prolonged service disruption and may result in significant business interruption, impact the guest booking experience and subsequently impact on revenues. Lack of investment in these systems may also result in reduced capability, stability and ability to compete. Additionally, failure to maintain an appropriate technology strategy and select the right technology partners could erode the Group’s long-term competitiveness.

The Group is exposed to the risks related to information security and data privacy

The Group is increasingly dependent upon the availability, integrity and confidentiality of information including but not limited to, guest and employee credit card, financial and personal data, business performance, financial reporting and commercial development. This information is sometimes held in different formats such as digital, paper, voice and video and could be stored in many places including facilities managed by third-party service providers.

The threats towards the Group’s information are dynamic including cyber attacks, fraudulent use, loss or misuse by employees and breaches of the Group’s vendors’ security arrangements amongst others. The legal and regulatory environment and requirements set out by the payment card industry surrounding information security and data privacy across the many jurisdictions in which the Group operates are constantly evolving. If the Group fails to appropriately protect information and ensure relevant controls are in place to enable the release of information through the appropriate channels in a timely and accurate manner, system performance, guest experiences and the reputation of the Group may be adversely affected. This can lead to revenue losses, fines, penalties and other additional costs, including legal fees.

The Group is exposed to a variety of risks associated with safety, security and crisis management

There is a constant need to protect the safety and security of our guests, employees and assets against natural and man-made threats. These include but are not limited to exceptional events such as extreme weather, civil or political unrest, violence and terrorism, serious and organized crime, fraud, employee dishonesty, cyber crime, fire and day-to-day accidents, incidents and petty crime which impact the guest or employee experience, could cause loss of life, sickness or injury and result in compensation claims, fines from regulatory bodies, litigation and impact reputation. Serious incidents or a combination of events could escalate into a crisis which if managed poorly could further expose the Group and its brands to significant adverse reputational damage.

The Group requires the right people, skills and capability to manage growth and change

In order to remain competitive, the Group must employ the right people. This includes hiring and retaining highly skilled employees with particular expertise or leadership capability. The implementation of the Group’s strategic business plans could be undermined by failure to build resilient corporate culture, failure to recruit or retain key personnel, unexpected loss of key senior employees, failures in the Group’s succession planning and incentive plans, or a failure to invest in the development of key skills.

Some of the markets in which the Group operates are experiencing economic growth and the Group must compete against other companies inside and outside the hospitality industry for suitably qualified or experienced employees. Some emerging markets may not have the required local expertise to operate a hotel industry supply and demand cycle

may not be able to attract the right talent. Failure to attract and retain employees may threaten the success of the Group’s operations in these markets. Additionally, unless skills are supported by a sufficient infrastructure to enable knowledge and skills to be passed on, the Group risks losing accumulated knowledge if key employees leave the Group.The Group is required to comply with existing and changing regulations across numerous countries, territories and jurisdictions

Governmental regulations affect countless aspects of the Group’s business ranging from corporate governance, health and safety, environmental, bribery and corruption, employment law and diversity, disability access, relationships, data privacy and information protection, financial, accounting and tax.

Regulatory changes may require significant changes in the way the business operates and may inhibit the strategy including the markets the Group operates in, brand protection, and use or transmittal of customer data. If the Group fails to comply with existing or changing regulations, the Group may be subject to fines, prosecution, loss of license to operate or reputation damage.

The Group is exposed to the risk of litigation

Certain companies in the Group are the subject of various claims and proceedings. The ultimate outcome of these matters is subject to many uncertainties, including future operating results ofevents and uncertainties inherent in litigation.

In addition, the Group could be adversely affected by industry overcapacity (by numberat risk of rooms) and weak demand due,litigation from many parties, including but not limited to, guests, customers, joint venture partners, suppliers, employees, regulatory authorities, franchisees and/or the owners of hotels it manages. Claims filed in part, to the cyclical natureUS may include requests for punitive damages as well as compensatory damages. Unfavorable outcomes of claims or proceedings could have a material impact on the hotel industry, or other differences between planning assumptions and actual operating conditions. Reductions in room rates and occupancy levels would adversely impact theGroup’s results of Group operations.

The Groupoperations, cash flow and/or financial position. Exposure to significant litigation or fines may experience a lackalso affect the reputation of selected development opportunities

While the Group is operating in 100 countries and territories, if the availability of suitable development sites becomes limited for the Group and its prospective hotel owners, for example, due to saturation or changing geo-political circumstances, this could adversely affect the Group’s future growth pipeline.

brands.The Group is exposed to risks related to corporate responsibility

The reputation of the Group and the value of its brands are influenced by a wide variety of factors, including the perception of key stakeholders andstakeholder groups such as the communities in which the Group operates. The social and environmental impacts of business are under increasing scrutiny, and the Group is exposed to the risk of damage to its reputation if it fails to demonstrate sufficiently responsible practices, ethical behavior, or fails to comply with relevant regulatory requirements in a number of areas such as fraud, bribery and corruption, safety and security, sustainability and responsible tourism, environmental management, equality, diversity and human rights, and support for local communities.

requirements.The Group is exposed to a variety of risks associated with its financial stability and ability to borrow and satisfy debt covenants

While the riskstrategy of litigation

the Group is to extend the hotel network through activities that do not involve significant amounts of its own capital, the Group does require capital to fund some development opportunities and to maintain and improve owned hotels. The Group

could be at riskis reliant upon having financial strength and access to borrowing facilities to meet these expected capital requirements. The majority of

litigation from many parties, including guests, customers, joint venture partners, suppliers, employees, regulatory authorities, franchiseesand/orthe

owners of hotels managed by it. Claims filedGroup’s borrowing facilities are only available if the financial covenants in the

USfacilities are complied with. Non-compliance with covenants could result in the lenders demanding repayment of the funds advanced. If the Group’s financial performance does not meet market expectations, it may

include requestsnot be able to refinance existing facilities on terms considered favorable.The Group is exposed to funding risks in relation to the defined benefits under its pension plans

The Group is required by law to maintain a minimum funding level in relation to its ongoing obligation to provide current and future pensions for punitive damages as well as compensatory damages. Exposuremembers of its UK pension plans who are entitled to litigation or fines imposeddefined benefits. The contributions payable by regulatory authorities may also affect the reputationGroup must be set with a view to making prudent provision for the benefits accruing under the plans of the Group.

In particular, the trustees of the Group’s UK defined benefit plan may demand increases to the contribution rates relating to the funding of this plan, which would oblige relevant employers of the Group to contribute extra amounts. The trustees must consult the plan’s actuary and principal employer before exercising this power.

In practice, contribution rates are agreed between the Group and the trustees on actuarial advice, and are set for three-year terms. The funding implications of the last actuarial review are disclosed in the Notes to the Consolidated Financial Statements on pages F-30 to F-35.

The Group may face difficulties insuring its business

Historically, the Group has maintained insurance at levels determined to be appropriate in light of the cost of cover and the risk profiles of the business in which it operates. However, forces beyond the Group’s control, including market forces, may limit the scope of coverage the Group can obtain and the Group’s ability to obtain coverage at reasonable rates. Other forces beyond the Group’s control, such as terrorist attacks or natural disasters may be uninsurable or simply too expensive to insure. Inadequate or insufficient insurance could expose the Group to large claims or could result in the loss of capital invested in properties, as well as the anticipated future revenue from properties, and could leave the Group responsible for guarantees, debt or other financial obligations related to such properties.

12

The Group’s pipeline ensures sustainable development in new and emerging markets that best suit the Company’s strengths and anticipate the future needs of customers. The Group has committed development teams ensuring a sizeable pipeline in developing markets: during 2010 the Group opened 7,253 rooms in Greater China, representing 20% of all new rooms opened by it across the globe during 2010.

The Group’s pipeline is the largest branded hotel pipeline in the world, representing 18% of all hotels under development, including those that are independent or unaffiliated.

Winning with our scale and expertise

The major benefit the Group brings to guests who stay in the Group’s portfolio of hotels, and owners who invest with us, is our system to help guests book and stay with us, and then maintain the relationship with them after they leave. This includes having hotels in key locations, great brands with consumer appeal, efficient reservations systems, global web presence, our loyalty rewards schemes, along with other elements. Together, these form the largest such ‘system’ in the industry and are the engine of our business, delivering, on average, 68% of total rooms revenue in 2010.

With continued focus on the success of this global system, we have developed“best-in-class” marketing and technology to support our hotels and drive incremental revenues.

Our focus on key geographical markets where we operate a large number of hotels, such as the US, UK, China, Middle East and Germany, means we can run hotels and our operating system with greater efficiencies, delivering more to the consumer at a lower cost.

The size of the global hotel market is estimated by the Group to be close to 20include 21.5 million rooms. Competitors in the market include other branded hotel companies, both large and small, international and domestic, and independently owned hotels.

IHG remains the largest branded hotel company, with our share currently at approximately 10% of the branded rooms (SmithSmith Travel Research), and a presence in 100 countries and territories. Leading research (Smith Travel Research)Research calculates that there are 6.67.3 million branded hotel rooms, with the remainder a combination of independent hotels, guesthouses and other types of lodging.

Although The Group believes that it holds the largest share of branded rooms, currently

less than halfapproximately 9% of

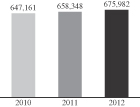

allbranded supply, distributed across nearly 100 countries and territories around the world. In 2012 the Group opened 33,922 new rooms worldwide (226 new hotels), resulting in an increase in the number of open Group hotel rooms

are branded,to 675,982 (4,602 hotels) at December 31, 2012, up 2.7% from 2011, taking into account the

benefitsremoval of

being parthotels which left the Group’s system.The benefits of a brand, such as the greater security and performance of a global reservation system, loyalty programs and international networks, are recognized byclear to many owners and the growthGroup is well-positioned to win the business of branded rooms has exceededowners seeking to grow with a hotel brand. Additionally, the growth of unbranded rooms over the past 10 years. Raising finance is still an issue globally,Group and branded hotels are perceived as offering greater security through global reservations systems, loyalty schemes, and international networks. Brandedother large hotel companies such ashave the Group, are attractive to independent hotel owners and are therefore gaining market share at the expensecompetitive advantage of the unbranded portion of the industry. The Group is well positioned to benefit from this trend.

Hotel owners are increasingly recognising the benefits of franchising or managing with the Group, which can offer a

global portfolio of brands

tothat suit the different real estate

or market opportunities an owner may

have.To ensure the Group’s strategy continues to be sustainable in the changing business environment and suitable for the Group’s capabilities, the Group closely monitors markets across the globe and follows key industry and business metrics such as RevPAR, average daily rate, demand, GDP and guest satisfaction.

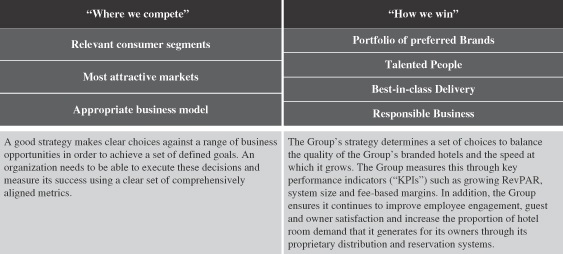

The Group’s strategy

With a portfolio of preferred Brands in the most attractive markets, the Group’s talented People are focused on delivering Great Hotels Guests Love and executing a clear set of priorities to achieve its Vision of becoming one of the great companies in the world.

Delivering the elements of the Group’s strategy

“Where we compete”

Competing in relevant consumer segments

The hotel industry is usually segmented according to price point and IHG is focused on the three segments that generate over 90% of branded hotels revenue, namely midscale (broadly three star), upscale (mostly four star) and luxury (five star). However, to build preferred Brands, the Group believes it needs to advance its understanding of its guests and their needs to ensure its brands remain contemporary and relevant.

The Group has therefore completed a fundamental occasion-based needs segmentation analysis to understand why guests book hotels — looking at who they are, the occasion they are traveling for and their needs when traveling. Many guests no longer have togethera single purpose for their hotel stay — for example, business trips turn into family holidays, and the Group needs to meet these demands, focusing more on the needs of its guests, to deliver loyalty and brand preference. The Group used this analysis to develop the brand proposition for its two new brands, HUALUXE Hotels & Resorts and EVEN Hotels, and it continues to work on this needs-based segmentation to help inform its view of the hotel market and its brand strategies going forward.

Competing in the most attractive markets

The Group’s strategy is to build preferred Brands with effective revenue delivery through global reservations channels. Furthermore, hotel ownership is increasingly being separatedscale positions in the most attractive markets globally. Concentrating growth in the largest markets means the Group and owners can operate more efficiently and benefit from hotel operations, encouraging hotel owners to use third parties,enhanced revenues and reduced costs. The Group’s key markets include large developed markets such as the US, UK and Germany, as well as emerging markets like China and India.

The US is the largest market for branded hotels, with 3.38 million rooms, accounting for 69% of all US rooms available. The segment in the US with the greatest share is midscale, with 1.38 million branded hotel rooms, and the Group’s Holiday Inn brand family, comprising Holiday Inn, Holiday Inn Express, Holiday Inn Club Vacations and Holiday Inn Resort, is the largest brand in this segment.

In China, the Group sees the greatest opportunity for growth of any single country and its strategy has been to enter the market early, to develop its relationships with key local third-party owners and grow its presence rapidly. In a country with 659,000 branded hotel rooms, the Group is the largest international hotel company with

over 61,000 rooms across its brands and more than 50,000 in the planning phase or under construction. This rapid pace of openings for the Group has been in anticipation of increasing demand for hotels, driven by a large, emerging middle class and growing domestic and international travel.

The Group is also focused on developing in other high priority markets. It seeks to develop its portfolio of brands in those markets which will be sources of strong hotel demand in the future. The Group has continued to build its position in these markets in the last year. For example, the Group increased the distribution of its core brands in India, building on its leadership position of Holiday Inn. In Russia and the Commonwealth of Independent States (“CIS”), there are opportunities for new construction and conversions as well as strong demand for branded hotels. The Group continues to adapt its business model by market, choosing partnerships and joint ventures where appropriate.

Outside the largest markets, the Group focuses on building presence in key gateway cities where its brands can generate revenue premiums from high business and leisure demand.

During 2012, the Group opened 33,922 rooms in 26 countries and territories, and signed a further 53,812 rooms into its development pipeline (hotels in planning and under construction but not yet opened) across 33 countries and territories. As part of its ongoing commitment to maintaining the quality of its brands, the Group removed 16,288 rooms during the year. As at December 31, 2012, the Group had the second largest pipeline in the industry, with 169,030 rooms in 1,053 hotels across 60 countries and territories. This represents a market share of 12% of all hotels under development, including those that are independent or unaffiliated with a brand.

Competing with an appropriate business model

As can be seen in the diagrams above and below, the Group’s business model is focused on franchising and managing hotels, rather than owning them, enabling it to grow at an accelerated pace with limited capital investment. This allows the Group to manage their hotels.

focus on building strong, preferred Brands based on relevant consumer needs, leaving asset management and real estate to its local third-party owners with the necessary expertise. With this “asset-light” approach, the Group also benefits from the reduced volatility of fee-based income streams, as compared with the ownership of assets. It allows the Group to focus on building strong delivery systems such as its branded hotel websites and call centers, creating greater returns for owners.A key characteristic of the franchised and managed business model is that it is highly cash generative, with a high return on capital employed. This business model enables the Group to focus on growing its fee revenues (Group revenue excluding owned and leased hotels, managed leases (being properties structured for legal reasons

as operating leases but with the same characteristics as management contracts) and significant liquidated damages) and fee-based margins (operating profit as a percentage of revenue, excluding revenue and operating profit from owned and leased hotels, managed leases and significant liquidated damages).

As at December 31, 2012, 86% of the Group’s operating profit (before regional and central overheads and exceptional items) wasderived from franchised and managed operations. In some situations, the Group supports its brands by using its capital to build or support the funding of flagship assets in high-demand locations in order to drive growth. The Group plans to recycle capital by selling these assets when the time is right and to reinvest elsewhere in the business and across its portfolio.

On November 6, 2012, the Group announced that the InterContinental London Park Lane would be the next hotel considered for sale and that discussions regarding the disposal of the InterContinental New York Barclay were progressing and would be opened to a wider group of prospective buyers. On February 19, 2013, the Company announced that the disposal process for InterContinental London Park Lane had commenced, and was continuing for InterContinental New York Barclay.

The Group continues to invest for growth, strengthening both its existing brands and launching new ones.

“How we win”

Winning with oura portfolio of preferred Brands

The Group aims to build a portfolio of brands that are bigger, better, and stronger:

Bigger means the Group has prioritized its growth strategy to build brand scale and leverage this scale through greater operational efficiency.

Better means a focus on continuous improvement in how the Group develops and delivers its brands to ensure guest needs are met with a consistent, high-quality experience.

Stronger means a focus on driving brand preference among guests, owners, investors and employees.

As part of the Group’s commitment to deliver against its brand strategy, in 2012, the Group launched two unique new brands to the market, which complement its overall portfolio of brands.

Further information on the Group’s portfolio can be found on page 27.

Winning with talented People

The Group believes that its preferred Brands are brought to life by its talented and passionate People. Therefore to deliver on its brand promise, the Group must attract, retain and develop the very best talent in the industry to service its guests and bring its Brands to life.

The Group directly employed an average of 7,981 people worldwide in the year ended December 31, 2012, whose costs were borne by the Group. When the whole of the Group’s estate is taken into account (including staff working in the franchised and values

managed hotels) over 350,000 people worked globally across all the Group’s brands as at December 31, 2012.The four pillars of the Group’s People strategy are:

Our Vision can only be realized if we have collaborativeDeveloping a BrandHearted culture: The Group’s brands are brought to life by its talented and engaged employees, deliveringpassionate People and it has focused on developing and improving its tools, to make it easy for its People to deliver the right experiencebrand promise. In 2012, the Group launched a new brand framework focused on transforming its brand standards and looked at how it manages projects - all part of developing a BrandHearted culture.

Making IHG a great place to our guests through shared valueswork: The Group believes in treating people as individuals and living our brands. We have extensive on-boarding, communication, development and recognition programs, aligned under our employment brand,celebrating achievements. The Group calls this “Room to be yourself”, providing the right environment for our people and this commitment is brought to life by four key promises. The Group continues to be successful.recognized around the globe as an employer of choice.

20

Delivering world-class People Tools to our owners: By partnering with the hotel human resources community, the Group has developed a set of award-winning “People Tools” that not only help increase employee retention and guest satisfaction but also drive efficiencies and increase revenue for the Group’s owners.

Building a strong leadership team: To grow its business sustainably and responsibly, the Group needs a strong BrandHearted leadership team. Therefore, it has created a “Leadership Framework”, which clearly defines what great leadership looks like to help develop the Group’s leaders of tomorrow.

Being the hotel company for the London 2012 Olympic and Paralympic Villages was a groundbreaking opportunity for the Group, giving its People in London 2012 the opportunity to benefit from new skills and experiences.

Winning with best-in-class DeliveryDuring 2012, the Group remained focused on attracting guests (room nights) to its hotels and its portfolio of brands. The Group leverages its size and scale to drive demand to its hotels, executing a multi-channel strategy that enables guests to search and book in the most appropriate mode for them, either over the phone, by computer or via an application on a mobile device. The Group maximizes the demand it delivers through these channels through advanced techniques that manage revenue per booking, drive customer loyalty and maximize owner returns. The Group’s channels and loyalty program, Priority Club Rewards, are the engine of the Group’s business.

Our people dictate our culture,The Group’s channelsAs part of its multi-channel strategy, the Group aims to increase revenue and bookings using its direct channels. During 2012, revenue generated through the Group’s websites increased to $3.4 billion whilst its global call centers answered more than 23 million inbound contacts and drove more than $1.9 billion in revenue for its hotels.

Mobile communications are also having profound effects on the hotel industry and the Group is aligned around great values which are consistently broughthas been quick to life through a set of five behaviors, the “Winning Ways”:

| | |

| • | Do the right thing; |

|

| • | Show we care; |

|

| • | Aim Higher; |

|

| • | Celebrate difference; and |

|

| • | Work better together. |

Business relationshipsadapt to these new channels with others

significant growth in revenue generated thorough its branded mobile applications, across all major platforms, rising from $2.4 million in 2009 to more than $330 million in 2012.The Group maintains effective relationships across all aspectsis also a founding member of roomkey.com, which was launched in 2012 as the first industry-owned hotel search engine, providing another innovative channel to increase guest nights to its brands.

Social media has also changed the way in which the Group communicates with guests and with its stakeholders in general. The Group’s new “Guest Ratings and Review” tool, which launched on its websites in 2012 enables guests to share their thoughts about their hotel experiences so that future guests can take this into account during the booking process.

Priority Club Rewards

Priority Club Rewards was the hotel industry’s first loyalty program and is the largest of its operations. kind in the world with 71.4 million members at the end of 2012, an increase of 13% during the year. In 2012, it won Premier Traveler magazine’s inaugural award for Best Hotel Loyalty Program and Global Traveler magazine’s award for Best Hotel Rewards Program for the eighth consecutive year.

The Group’s operations are not dependent upon any single customer, supplier or hotel owner dueGroup also leverages sales and marketing expertise in order to support its multi-channel strategy. The System Fund (the “Fund”) is a $1.2 billion fund of cash assessments and contributions, collected by the extent of its brands, market segments and geographical coverage. For example,Group from hotels within the Group’s largest third-party hotel owner controls just 3%system, and proceeds from the sale of the Group’s total room count.

Priority Club Rewards points. The Group continued to enhance and streamline its procurement processes during 2010, and with the implementation of initiatives to combat waste and enhance relationships with suppliers,System Fund is managed by the Group is striving to ensure best-practice is employed throughout the Group. With a focus on ensuring high-quality goods and services are sourced at competitive prices, the Group strives to ensure enhanced value for the Group, our hotel owners and shareholders.

IHG is proud of its strong and important relationship with the IAHI, the Owners’ Association for ownersbenefit of hotels in the Group’s

sevensystem with the objective of driving revenues for the hotels. It is therefore used to pay for marketing, the Priority Club Rewards loyalty program and the global reservation system.As a result of the power of its revenue delivery systems the Group has built strong relationships with its owners. These relationships are founded on the ability to deliver high returns to owners using premium revenue generating products. The Group meets with the IHG Owners Association (the organization that represents owners of hotels operating under the Group’s brands across the world. IHG meets with the IAHI, in large and small groups,world) on a regular basis and works together to support and facilitate the continued development of the Group’s brands and systems. During 2010,

Winning with Responsible Business practices

With over 4,600 hotels in nearly 100 countries and territories around the combined workworld, the Group’s commitment to being a Responsible Business is central to its Vision of being one of the great companies of the world. The Group understands how important it is to champion and protect the trusted reputation of the Group and IAHI implemented several enhancementsits brands and this is embedded in its culture. The Group believes that being a responsible business is necessary to the Group’s system.

Examples of such enhancements include:

Holiday Inn relaunch — the near completionenable it to stay ahead of the $1 billion global relaunchcompetition and grow, creating value for all of its shareholders and stakeholders in the Holiday Inn brand family;

InnSupply — improving purchasing efficiencieslong term. Amongst other things, it offers the Group a huge opportunity to innovate, create employment, empower people to perform at their best and streamlining the procurement processes across both organizations;

Way of Sales — developing“best-in-class” practicesfeel good about what they do, and drive value for the sales operations of both organizations, having identified critical roles for generating revenues;

Celebrate Service week — giving recognition and thanks to the many thousands of front-line employees, and emphasizing engagement through the Group’s brands; and

People Tools — enhancing the recruitment, hiring, training and retention practices across both organizations, with specific focus on reflecting the individual qualities ofbusiness. That’s why Responsible Business underpins each brand. These tools are supplied to all hotels: managed, franchised and owned and leased.

Many jurisdictions and countries regulate the offering of franchise agreements and recent trends indicate an increase in the number of countries adopting franchise legislation. As a significant percentage of the Group’s

revenue is derived from franchise fees,three strategic corporate priorities of preferred Brands, talented People and best-in-class Delivery, which work together to determine “How We Win” to create Great Hotels Guests Love.Governance and leadership

The Group’s Chairman, the Board and its committees (Audit Committee, Corporate Responsibility Committee, Nomination Committee and Remuneration Committee) provide strong leadership and promote a responsible business culture by maintaining high standards in corporate governance, corporate responsibility and internal control and risk management.

Brands

Trusted brands deliver a superior and consistent brand experience and to achieve this, the Group requiresaclear brand framework. Brand standards are the foundations of a clear brand framework for all the Group’s continuedhotels and its compliance teams ensure that its hotels deliver in accordance with franchise legislationthese. The Group’s brand safety standards assist hotels in providing a safe and secure environment for its guests and employees. The Group’s corporate responsibility programs have also been designed so that they can be implemented throughout the Group’s hotel brands and corporate offices in any region.

People

At the core of being a Responsible Business is important toensuring that the successful deploymentactions of all of the Group’s strategy.

21

DeliveryHaving in place an effective system of internal controls and risk management is essential to being a Responsible Business. The Group’s tools, processes and procedures ensure a business based on a solid foundation with a commitment to doing the right thing for the benefit of all its stakeholders.

“Measuring our successsuccess”

We measure our success in terms of shareholder value, as well as throughThe Group has a holistic set of strategic priorities. These form ourcarefully selected key performance indicators (KPIs)(“KPIs”) to ensure a consistent approach to runningmonitor its success in achieving its strategy. These are organized around the business. These KPIs consistelements of “Wherethe Group’s strategy:

“Where we compete”, includingfocusing on relevant consumer segments, the most attractive markets and the appropriate business model, key target marketsmodel; and consumer segments; and “How

“How we win”, including financial returns, our people,focusing on corporate priorities of preferred Brands, talented People, best-in-class Delivery and Responsible Business.

In particular, the guest experienceGroup uses the following measures to monitor performance:

fee revenues and responsible business.fee-based margins;

system contribution — the proportion of business delivered to Group hotels by its dedicated IHG booking channels;

Responsible Business practices.

These KPIs are used to measure the progress of the Group to deliver Great Hotels Guests Love and achieve its Vision of becoming one of the great companies of the world.

The Group’s performance against these KPIs over the 2010-2012 period is summarized below:

“Where we competecompete”

| | | | | | |

| Strategic priorities | | KPIs | | Current status and 2012 development | | 2013 priorities |

| | Key performance

| | Current statusMost attractive markets and

| | |

Strategic priorities

| | indicators (KPIs)

| | 2010 developments

| | 2011 priorities

|

|

| appropriate business model To accelerate profitable growth of ourits core business in the largestits most attractive markets where presence and scale really count using the right business model to drive its fee revenue and also in key global gateway cities. Seek opportunities to leverage our scale in new business areas.income streams. | | • Sustained system size growth; and

• deal signings focused

Net rooms supply

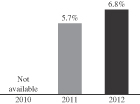

Growth in scale markets and key gateway cities.fee revenue1

Fee-based margins | | • System size maintained at 647,161grown to 675,982 rooms;

• over 90% of deals signed in4,602 hotels opened globally; • built scale markets and key gateway cities;

• re-entry into Hawaii with a Holiday Inn Resort;

• opening our second Hotel Indigo in London, and our first in Asia Pacific, on the Bund in Shanghai;

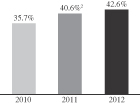

• 17 signings of Hotel Indigo brand to 50 hotels globally; and Staybridge Suites outside • fee-based margins of North America; and

• 259 hotels opened globally.42.6%, up two percentage points on 2011, a particularly strong result. | | • Continue international roll-out of Staybridge Suites and Hotel Indigo;

• accelerateAccelerate growth strategies in quality locations in agreed scale markets; and

• continue to leverage scale and build upon improved strategic position during the economic downturn.scale. |

22

| 2 | One percentage point growth on an underlying basis. |

“How we winwin” — Delivering Great Hotels Guests Love

| | | | | | |

| Strategic priorities | | KPIs | | Current status and 2012 development | | 2013 priorities |

Strategic priorities

Financial returns

To generate higher returns forPreferred Brands Operate a portfolio of preferred, locally-relevant brands attractive to both owners and guests that have clear market positions and differentiation in the Groupeyes of the guest. | |

Global RevPAR growth/(decline) Comparable hotels, constant $ | | •Clarified the brand propositions for Holiday Inn and Holiday Inn Express and celebrated the Holiday Inn 60th anniversary; •continued the repositioning of Crowne Plaza; •achieved two new brand launches in two geographies; and •achieved strong brand successes in Greater China, particularly through the growth of HUALUXE Hotels & Resorts with 15 signings for the brand and improved the strength of Crowne Plaza through brand preference and awareness. | | •Invest to build long-term brand preference for the Holiday Inn brand family; •continue the repositioning of the Crowne Plaza brand; •support growth of its new brands: EVEN Hotels in the US and HUALUXE Hotels & Resorts in Greater China; and •continue to deliver a consistent brand experience and increased revenue share, improved operating efficiency and growing margins.

Our people

Creatingguest satisfaction through its needs-based segmentation analysis. |

Talented People Create hotels that are well run, with brands brought to life by people who are proud of the work they do.

Guest experience

To operate | |

Employee engagement scores Average of two Employee Engagement surveys per year | | •New brand management training launched for General Managers; •all of its corporate offices and more than 4,000 Group hotels participated in Celebrate Service week, its global employee recognition event; •created a portfolionew Mandarin recruitment site and launched career pages on social networking platforms in China to continue its aim to be employer of brands attractivechoice; and •industry-leading suite of People Tools now embedded in its franchised and managed hotel estate. | | •Empower its frontline teams with the tools and training to bothconsistently deliver great guest experiences that build brand preference, advocacy and repeat business; •continue to strengthen its talent pipeline and succession planning to meet its growth ambitions; •instill a winning culture through strong leadership and performance management; and •build on its strong employer brand to make the Group a magnet for talent. |

| | | | | | |

| Strategic priorities | | KPIs | | Current status and 2012 development | | 2013 priorities |

Best-in-class Delivery Generate higher returns for owners and guests that have clear market positionsthe Group through increased revenue share, improved operating efficiency and differentiationgrowing margins. | |

Total gross revenue Actual $billion | | •Launched strategic industry partnership in roomkey.com; •71.4 million Priority Club Rewards members — 8.4 million new members enrolled in 2012, up 13% on 2011; and •global Group sales force with 17,600 sales professionals. | | •Continue to strengthen the eyesGroup’s system of delivering profitable demand to hotels; •put in place the guest.

required technology infrastructure to enable growth; and •continue to increase business from its loyalty program, Priority Club Rewards. |

Responsible business

To takeBusiness Take a proactive stance and seek creative solutions through innovationon environmental sustainability and collaboration on environment and community issues, and to drive increasedsustainable communities in a way that drives shared value for the Group, owners, guests and the communities where we operate.in which IHG operates. | |

Hotels signed-up to Green Engage Hotels, cumulative

Participants benefiting from the IHG Academy | | Current status and 2010 developments

• Further procurement efficiencies made;

• enhanced Customer Relationship Management with new technology and campaign management tools to involve non-Priority Club Rewards (PCR) members; and

• enhanced communications with PCR loyalty program members with refreshed loyalty systems.

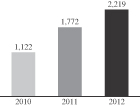

• Launched and cascaded our Vision to become one2,219 of the world’s great companies;

• developed management tools to deliver a branded guest experience;

• further emphasis on our cultureGroup’s hotels enrolled in Green Engage by end of learning and development with industry recognition;

2012; • “Celebrate Service” week — a global event to recognize our people,11.7% energy savings in partnership with the IAHI ownership community; and

• managing employee engagement.

• Global pilots to identify opportunities to create branded hallmarks with guest appeal;

• near completion of the Holiday Inn relaunch; and

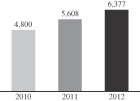

• grew our industry-leading loyalty program PCR, to 56 million members, contributing $6.5 billion of global system rooms revenue.

• “Green Engage” developed (patent pending); rolled out to over 1,000 hotels by December 31, 2010;

• collaborated with the University of Oxford’s Department of Plant Sciences to understand better how hotel design and development impacts the environment; and

• Corporate Responsibility approach defined and agreed. | | 2011 priorities

• Capitalize on recovery of group and meetings business;

• strengthen global sales force effectiveness;

• optimize revenues from third party and Group websites;

• ensure the Group’s industry leading system of delivering demand and revenue to hotels retains competitive advantage; and

• strengthen loyalty program, with enhanced member offer.

• Cascade of branded management tools to whole hotel estate, including our franchised hotels;

• ongoing partnership with IAHI ownership community for people events;

• continued focus on developing skills to deliver our Vision and branding capability; and

• opportunities for employees and communities to be involved with Olympics partnership.

• Leverage strong position of Holiday Inn relaunch with roll-out of global marketing initiatives;

• ensure growth plans of each brand aligns fully with corporate Vision;

• focus on strength of Priority Club Rewards and visibly enhance offering to its members in hotels and across global reservations channels; and

• increase the Group’s business from Priority Club Rewards members.

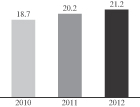

• Continue to roll out “Green Engage” to our owned and managed hotels,estate by end of 2012 (on a per available room night basis);•industry standard for measuring carbon was launched in 2012 and expand into the franchised estateincluded in all regions;

• work with stakeholders, such as Harvard University, to educate decision-makers onGreen Engage via the Group’s economic impacts;new carbon calculator; •over 150 IHG Academy programs by the end of 2012; and

•fan base of the “IHG Planet CR” Facebook page expanded to over 20,000 by the end of 2012. | | •Work to ensure all Group hotels that are enrolled in Green Engage effectively use the tool for the greatest impact; •continue to embed our community strategy, including establishingdrive awareness and engagement around the “IHG Academy”IHG Shelter in a Storm Programme; •continue to expand the IHG Academy program throughout the world; and •focus on driving awareness of the Group’s approach to corporate responsibility across internal and activating our strategic partner in providing disaster recovery.external stakeholder groups using a variety of channels, to maximize employee pride, and reinforce the Group’s reputation as a Responsible Business. |

23

Segmental Resultsresults by Activityactivity

The following table shows the Group’s continuing revenue and operating profit before exceptional operating items by activity and the percentage contribution of each activity, for the years ended December 31, 2010, 20092012, 2011 and 2008.

| | | | | | | | | | | | | |

| | | Year ended December 31, |

| | | 2010 | | 2009 | | 2008 |

| | | ($ million) |

| |

Revenue(1) | | | | | | | | | | | | |

| Americas | | | | | | | | | | | | |

| Franchised | | | 465 | | | | 437 | | | | 495 | |

| Managed | | | 119 | | | | 110 | | | | 168 | |

| Owned and leased | | | 223 | | | | 225 | | | | 300 | |

| | | | | | | | | | | | | |

| | | | 807 | | | | 772 | | | | 963 | |

| | | | | | | | | | | | | |

| EMEA | | | | | | | | | | | | |

| Franchised | | | 81 | | | | 83 | | | | 110 | |

| Managed | | | 130 | | | | 119 | | | | 168 | |

| Owned and leased | | | 203 | | | | 195 | | | | 240 | |

| | | | | | | | | | | | | |

| | | | 414 | | | | 397 | | | | 518 | |

| | | | | | | | | | | | | |

| Asia Pacific | | | | | | | | | | | | |

| Franchised | | | 12 | | | | 11 | | | | 18 | |

| Managed | | | 155 | | | | 105 | | | | 113 | |

| Owned and leased | | | 136 | | | | 129 | | | | 159 | |

| | | | | | | | | | | | | |

| | | | 303 | | | | 245 | | | | 290 | |

| | | | | | | | | | | | | |

Central(2) | | | 104 | | | | 124 | | | | 126 | |

| | | | | | | | | | | | | |

| Total | | | 1,628 | | | | 1,538 | | | | 1,897 | |

| | | | | | | | | | | | | |

Operating profit before exceptional operating items(1)(3) | | | | | | | | | | | | |

| Americas | | | | | | | | | | | | |

| Franchised | | | 392 | | | | 364 | | | | 426 | |

| Managed | | | 21 | | | | (40 | ) | | | 51 | |

| Owned and leased | | | 13 | | | | 11 | | | | 55 | |

| Regional overheads | | | (57 | ) | | | (47 | ) | | | (67 | ) |

| | | | | | | | | | | | | |

| | | | 369 | | | | 288 | | | | 465 | |

| | | | | | | | | | | | | |

| EMEA | | | | | | | | | | | | |

| Franchised | | | 59 | | | | 60 | | | | 75 | |

| Managed | | | 62 | | | | 65 | | | | 95 | |

| Owned and leased | | | 40 | | | | 33 | | | | 45 | |

| Regional overheads | | | (36 | ) | | | (31 | ) | | | (44 | ) |

| | | | | | | | | | | | | |

| | | | 125 | | | | 127 | | | | 171 | |

| | | | | | | | | | | | | |

| Asia Pacific | | | | | | | | | | | | |

| Franchised | | | 7 | | | | 5 | | | | 8 | |

| Managed | | | 73 | | | | 44 | | | | 55 | |

| Owned and leased | | | 35 | | | | 30 | | | | 43 | |

| Regional overheads | | | (26 | ) | | | (27 | ) | | | (38 | ) |

| | | | | | | | | | | | | |

| | | | 89 | | | | 52 | | | | 68 | |

| | | | | | | | | | | | | |

Central(2) | | | (139 | ) | | | (104 | ) | | | (155 | ) |

| | | | | | | | | | | | | |

| Total | | | 444 | | | | 363 | | | | 549 | |

| | | | | | | | | | | | | |

Footnotes on page 25.

24

| | | | | | | | | | | | |

| | | Year ended December 31, | |

| | | 2012 | | | 2011 | | | 2010 | |

| | | ($ million) | |

Revenue(1) | | | | | | | | | | | | |

Americas | | | | | | | | | | | | |

Franchised | | | 541 | | | | 502 | | | | 465 | |

Managed | | | 97 | | | | 124 | | | | 119 | |

Owned and leased | | | 199 | | | | 204 | | | | 223 | |

| | | | | | | | | | | | |

| | | 837 | | | | 830 | | | | 807 | |

| | | | | | | | | | | | |

Europe | | | | | | | | | | | | |

Franchised | | | 91 | | | | 86 | | | | 76 | |

Managed | | | 147 | | | | 118 | | | | 70 | |

Owned and leased | | | 198 | | | | 201 | | | | 180 | |

| | | | | | | | | | | | |

| | | 436 | | | | 405 | | | | 326 | |

| | | | | | | | | | | | |

AMEA | | | | | | | | | | | | |

Franchised | | | 18 | | | | 19 | | | | 15 | |

Managed | | | 152 | | | | 151 | | | | 155 | |

Owned and leased | | | 48 | | | | 46 | | | | 43 | |

| | | | | | | | | | | | |

| | | 218 | | | | 216 | | | | 213 | |

| | | | | | | | | | | | |

Greater China | | | | | | | | | | | | |

Franchised | | | 3 | | | | 2 | | | | 2 | |

Managed | | | 89 | | | | 77 | | | | 60 | |

Owned and leased | | | 138 | | | | 126 | | | | 116 | |

| | | | | | | | | | | | |

| | | 230 | | | | 205 | | | | 178 | |

| | | | | | | | | | | | |

Central(2) | | | 114 | | | | 112 | | | | 104 | |

| | | | | | | | | | | | |

Total | | | 1,835 | | | | 1,768 | | | | 1,628 | |

| | | | | | | | | | | | |

Operating profit before exceptional operating items(1)(3) | | | | | | | | | | | | |

Americas | | | | | | | | | | | | |

Franchised | | | 466 | | | | 431 | | | | 392 | |

Managed | | | 48 | | | | 52 | | | | 21 | |

Owned and leased | | | 24 | | | | 17 | | | | 13 | |

Regional overheads | | | (52 | ) | | | (49 | ) | | | (57 | ) |

| | | | | | | | | | | | |

| | | 486 | | | | 451 | | | | 369 | |

| | | | | | | | | | | | |

Europe | | | | | | | | | | | | |

Franchised | | | 65 | | | | 65 | | | | 55 | |

Managed | | | 32 | | | | 26 | | | | 17 | |

Owned and leased | | | 50 | | | | 49 | | | | 38 | |

Regional overheads | | | (32 | ) | | | (36 | ) | | | (32 | ) |

| | | | | | | | | | | | |

| | | 115 | | | | 104 | | | | 78 | |

| | | | | | | | | | | | |

AMEA | | | | | | | | | | | | |

Franchised | | | 12 | | | | 12 | | | | 8 | |

Managed | | | 90 | | | | 87 | | | | 88 | |

Owned and leased | | | 6 | | | | 5 | | | | 4 | |

Regional overheads | | | (20 | ) | | | (20 | ) | | | (18 | ) |

| | | | | | | | | | | | |

| | | 88 | | | | 84 | | | | 82 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | Year ended December 31, |

| | | 2010 | | 2009 | | 2008 |

| | | (%) |

| |

| Revenue | | | | | | | | | | | | |

| Americas | | | | | | | | | | | | |

| Franchised | | | 28.6 | | | | 28.4 | | | | 26.1 | |

| Managed | | | 7.3 | | | | 7.2 | | | | 8.9 | |

| Owned and leased | | | 13.7 | | | | 14.6 | | | | 15.8 | |

| | | | | | | | | | | | | |

| | | | 49.6 | | | | 50.2 | | | | 50.8 | |

| | | | | | | | | | | | | |

| EMEA | | | | | | | | | | | | |

| Franchised | | | 5.0 | | | | 5.4 | | | | 5.8 | |

| Managed | | | 8.0 | | | | 7.7 | | | | 8.9 | |

| Owned and leased | | | 12.4 | | | | 12.7 | | | | 12.6 | |

| | | | | | | | | | | | | |

| | | | 25.4 | | | | 25.8 | | | | 27.3 | |

| | | | | | | | | | | | | |

| Asia Pacific | | | | | | | | | | | | |

| Franchised | | | 0.7 | | | | 0.7 | | | | 0.9 | |

| Managed | | | 9.5 | | | | 6.8 | | | | 6.0 | |

| Owned and leased | | | 8.4 | | | | 8.4 | | | | 8.4 | |

| | | | | | | | | | | | | |

| | | | 18.6 | | | | 15.9 | | | | 15.3 | |

| | | | | | | | | | | | | |

| Central | | | 6.4 | | | | 8.1 | | | | 6.6 | |

| | | | | | | | | | | | | |

| Total | | | 100.0 | | | | 100.0 | | | | 100.0 | |

| | | | | | | | | | | | | |

| Operating profit before exceptional operating items | | | | | | | | | | | | |

| Americas | | | | | | | | | | | | |

| Franchised | | | 88.3 | | | | 100.2 | | | | 77.6 | |

| Managed | | | 4.7 | | | | (11.0 | ) | | | 9.3 | |

| Owned and leased | | | 2.9 | | | | 3.0 | | | | 10.0 | |

| Regional overheads | | | (12.8 | ) | | | (12.9 | ) | | | (12.2 | ) |

| | | | | | | | | | | | | |

| | | | 83.1 | | | | 79.3 | | | | 84.7 | |

| | | | | | | | | | | | | |

| EMEA | | | | | | | | | | | | |

| Franchised | | | 13.3 | | | | 16.5 | | | | 13.6 | |

| Managed | | | 14.0 | | | | 17.9 | | | | 17.3 | |

| Owned and leased | | | 9.0 | | | | 9.1 | | | | 8.2 | |

| Regional overheads | | | (8.1 | ) | | | (8.5 | ) | | | (8.0 | ) |

| | | | | | | | | | | | | |

| | | | 28.2 | | | | 35.0 | | | | 31.1 | |

| | | | | | | | | | | | | |

| Asia Pacific | | | | | | | | | | | | |

| Franchised | | | 1.6 | | | | 1.4 | | | | 1.5 | |

| Managed | | | 16.4 | | | | 12.1 | | | | 10.0 | |

| Owned and leased | | | 7.9 | | | | 8.2 | | | | 7.8 | |

| Regional overheads | | | (5.9 | ) | | | (7.4 | ) | | | (6.9 | ) |

| | | | | | | | | | | | | |

| | | | 20.0 | | | | 14.3 | | | | 12.4 | |

| | | | | | | | | | | | | |

| Central | | | (31.3 | ) | | | (28.6 | ) | | | (28.2 | ) |

| | | | | | | | | | | | | |

| Total | | | 100.0 | | | | 100.0 | | | | 100.0 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | Year ended December 31, | |

| | | 2012 | | | 2011 | | | 2010 | |

| | | ($ million) | |

Greater China | | | | | | | | | | | | |

Franchised | | | 4 | | | | 3 | | | | 3 | |

Managed | | | 51 | | | | 43 | | | | 30 | |

Owned and leased | | | 45 | | | | 37 | | | | 33 | |

Regional overheads | | | (19 | ) | | | (16 | ) | | | (12 | ) |

| | | | | | | | | | | | |

| | | 81 | | | | 67 | | | | 54 | |

| | | | | | | | | | | | |

Central(2) | | | (156 | ) | | | (147 | ) | | | (139 | ) |

| | | | | | | | | | | | |

Total | | | 614 | | | | 559 | | | | 444 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | Year ended December 31, | |

| | | 2012 | | | 2011 | | | 2010 | |

| | | (%) | |

Revenue | | | | |

Americas | | | | | | | | | | | | |

Franchised | | �� | 29.5 | | | | 28.4 | | | | 28.6 | |

Managed | | | 5.3 | | | | 7.0 | | | | 7.3 | |

Owned and leased | | | 10.8 | | | | 11.6 | | | | 13.7 | |

| | | | | | | | | | | | |

| | | 45.6 | | | | 47.0 | | | | 49.6 | |

| | | | | | | | | | | | |

Europe | | | | | | | | | | | | |

Franchised | | | 5.0 | | | | 4.9 | | | | 4.7 | |

Managed | | | 8.0 | | | | 6.7 | | | | 4.3 | |

Owned and leased | | | 10.8 | | | | 11.3 | | | | 11.0 | |

| | | | | | | | | | | | |

| | | 23.8 | | | | 22.9 | | | | 20.0 | |

| | | | | | | | | | | | |

AMEA | | | | | | | | | | | | |

Franchised | | | 1.0 | | | | 1.1 | | | | 0.9 | |

Managed | | | 8.3 | | | | 8.5 | | | | 9.5 | |

Owned and leased | | | 2.6 | | | | 2.6 | | | | 2.7 | |

| | | | | | | | | | | | |

| | | 11.9 | | | | 12.2 | | | | 13.1 | |

| | | | | | | | | | | | |

Greater China | | | | | | | | | | | | |

Franchised | | | 0.2 | | | | 0.1 | | | | 0.1 | |

Managed | | | 4.8 | | | | 4.4 | | | | 3.7 | |

Owned and leased | | | 7.5 | | | | 7.1 | | | | 7.1 | |

| | | | | | | | | | | | |

| | | 12.5 | | | | 11.6 | | | | 10.9 | |

| | | | | | | | | | | | |

Central | | | 6.2 | | | | 6.3 | | | | 6.4 | |

| | | | | | | | | | | | |

Total | | | 100.0 | | | | 100.0 | | | | 100.0 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | Year ended December 31, | |

| | | 2012 | | | 2011 | | | 2010 | |

| | | (%) | |

Operating profit before exceptional operating items | | | | | | | | | | | | |

Americas | | | | | | | | | | | | |

Franchised | | | 75.9 | | | | 77.1 | | | | 88.3 | |

Managed | | | 7.8 | | | | 9.3 | | | | 4.7 | |

Owned and leased | | | 3.9 | | | | 3.0 | | | | 2.9 | |

Regional overheads | | | (8.4 | ) | | | (8.7 | ) | | | (12.8 | ) |

| | | | | | | | | | | | |

| | | 79.2 | | | | 80.7 | | | | 83.1 | |

| | | | | | | | | | | | |

Europe | | | | | | | | | | | | |

Franchised | | | 10.6 | | | | 11.6 | | | | 12.4 | |

Managed | | | 5.2 | | | | 4.6 | | | | 3.8 | |

Owned and leased | | | 8.1 | | | | 8.8 | | | | 8.6 | |

Regional overheads | | | (5.2 | ) | | | (6.4 | ) | | | (7.2 | ) |

| | | | | | | | | | | | |

| | | 18.7 | | | | 18.6 | | | | 17.6 | |

| | | | | | | | | | | | |

AMEA | | | | | | | | | | | | |

Franchised | | | 2.0 | | | | 2.1 | | | | 1.8 | |

Managed | | | 14.6 | | | | 15.6 | | | | 19.8 | |

Owned and leased | | | 1.0 | | | | 0.9 | | | | 0.9 | |

Regional overheads | | | (3.3 | ) | | | (3.6 | ) | | | (4.0 | ) |

| | | | | | | | | | | | |

| | | 14.3 | | | | 15.0 | | | | 18.5 | |

| | | | | | | | | | | | |

Greater China | | | | | | | | | | | | |

Franchised | | | 0.7 | | | | 0.5 | | | | 0.7 | |

Managed | | | 8.3 | | | | 7.7 | | | | 6.7 | |

Owned and leased | | | 7.3 | | | | 6.6 | | | | 7.4 | |

Regional overheads | | | (3.1 | ) | | | (2.8 | ) | | | (2.7 | ) |

| | | | | | | | | | | | |

| | | 13.2 | | | | 12.0 | | | | 12.1 | |

| | | | | | | | | | | | |

Central | | | (25.4 | ) | | | (26.3 | ) | | | (31.3 | ) |

| | | | | | | | | | | | |

Total | | | 100.0 | | | | 100.0 | | | | 100.0 | |

| | | | | | | | | | | | |

| (1) | | The results of operations have been translated into US dollars at the average rates of exchange for the year. In the case of sterling, the translation rate $1 = £0.65 (2009£0.63 (2011 $1 = £0.64, 2008£0.62, 2010 $1 = £0.55)£0.65). In the case of the euro, the translation rate is $1 = €0.76 (2009€0.78 (2011 $1 = €0.72, 20082010 $1 = €0.68)€0.76). |

|

| (2) | | Central revenue primarily relates to Holidex (the Group’s proprietary reservation system)technology fee income. Central operating profit includes central revenue less costs related to global functions. |

|

| (3) | | Operating profit before exceptional operating items does not include exceptional operating items for all periods presented. Exceptional operating items (charge unless otherwise noted) by region were theThe Americas $8 million (2009 $301 million, 2008 $99 million); EMEA credit of $3$23 million (2009 $22(2011 credit of $35 million, 2008 $212010 $8 million); Asia Pacific $2Europe $4 million (2009 $7(2011 $39 million, 2008 $22010 $5 million); AMEA $5 million (2011 credit of $26 million, 2010 credit of $6 million); Greater China $nil (2011 $nil, 2010 $nil); and Central $nil (2009 $43$18 million 2008 $10 million)(2011 credit of $35 million, 2010 $nil). |

25

Global System

In addition to management or franchise fees, hotels within the Group’s system pay cash assessments and contributions which are collected by the Group for specific use within the System Fund (the “Fund”).Fund. The Fund also receives proceeds from the sale of Priority Club Rewards points. The Fund is managed for the benefit of hotels in the system with the objective of driving revenues for the hotels. The Fund is used to pay for marketing, the Priority Club Rewards loyalty program and the global reservations system.

Priority Club Rewards:The Group’s worldwide loyalty scheme, Priority Club Rewards, is the largest of its kind in the hotel industry. Members enjoy a variety of privileges and rewards as they stay at the Group’s hotels around the world. The global system room revenue generated from Priority Club Rewards members during 20102012 was $6.6$7.2 billion. Priority Club Rewards membership reached 5671 million customers as at December 31, 2010,2012, compared to 4863 million as at December 31, 2009.

2011.Central Reservations System Technology:The Group operatesowns the HolidexPlus reservations system. The HolidexPlus system receives reservations requests entered on terminals located at most of the Group’s reservations centers, as well as from global distribution systems operated by a number of major corporations and travel agents. Where local hotel systems allow, the HolidexPlus system immediately confirms reservations or indicates alternative accommodation available within the Group’s network. Confirmations are transmitted electronically to the hotel for which the reservation is made.

During 2012, the Group entered into a five-year technology outsourcing agreement with International Business Machines Corporation (“IBM”), pursuant to which IBM operates and maintains the infrastructure of the HolidexPlus system.Reservations Call Centers:The Group operates 10 reservations call centers around the world which enable it to sell in local languages in many countries and offer a high qualityhigh-quality service to customers.

Internet:The Group introduced electronic hotel reservations in 1995. The Internetinternet is an important communications, branding and distribution channel for hotel sales. The Group is a founding member of roomkey.com, which was launched in 2012 as the first industry-owned online hotel search engine.

During 2010, 24% (24%2012 the Group’s leading mobile booking platforms realized $330 million in 2009) of global system room revenue booked via the Internet through various branded websites, such as www.intercontinental.com and www.holidayinn.com, as well as certified third parties.

revenues, up from $2.4 million in 2009.The Group has established standards for working with third-party intermediaries — online travel distributors — who sell or re-sell the Group’s branded hotel rooms via their Internetinternet sites. Under the standards, certified distributors are required to respect the Group’s trademarks, ensure reservations are guaranteed through an automated and common confirmation process, and clearly present fees to customers.

During 2010, global system room revenue booked through the Group’s global systems (which includes Priority Club Rewards members, central reservations and call centers, global distribution systems and the Internet) was 68% (68% in 2009).

Sales and Marketingmarketing

The Group targets its sales and marketing expenditure in each region on driving revenue and brand awareness or, in the case of sales investments, targeting segments such as corporate accounts, travel agencies and meeting organizers. The majority of the Group’s sales and marketing expenditure is funded by contractual fees paid by most hotels in the system.

26

Global Brands

The Group offers hotel brands that appeal to guests with different needs and tastes. This requires a portfolio of large global brands, growing alongside innovative new brands to meet the unique experiences our guests desire.

The hotel industry is usually split into segments based upon price point and consumer expectations. The Group is focused on the three segments that together generate over 90% of branded hotel revenues: midscale (broadly 3 star hotels), upscale (mostly 4 star), and luxury (5 star).

| | | | | | | | | |

| | | At December 31, 2010 |

Brands | | Room numbers | | Hotels |

| |

| InterContinental Hotels & Resorts | | | 58,429 | | | | 171 | |

| Crowne Plaza Hotels & Resorts | | | 106,155 | | | | 388 | |

Holiday Inn Hotels & Resorts(1) | | | 230,117 | | | | 1,247 | |

| Holiday Inn Express | | | 191,228 | | | | 2,075 | |

| Staybridge Suites | | | 20,762 | | | | 188 | |

| Candlewood Suites | | | 28,253 | | | | 288 | |

| Hotel Indigo | | | 4,548 | | | | 38 | |

| Other | | | 7,669 | | | | 42 | |

| | | | | | | | | |

| Total | | | 647,161 | | | | 4,437 | |

| | | | | | | | | |

The Group operates the following brands:

| | | | | | | | |

| | | At December 31, 2012 | |

| | | Room numbers | | | Hotels | |

InterContinental Hotels & Resorts | | | 57,314 | | | | 170 | |

Crowne Plaza Hotels & Resorts | | | 108,307 | | | | 392 | |

Holiday Inn Hotels & Resorts(1) | | | 231,488 | | | | 1,247 | |

Holiday Inn Express | | | 205,631 | | | | 2,192 | |

Staybridge Suites | | | 20,696 | | | | 189 | |

Candlewood Suites | | | 28,675 | | | | 299 | |

Hotel Indigo | | | 5,661 | | | | 50 | |

Other | | | 18,210 | | | | 63 | |

| | | | | | | | |

Total | | | 675,982 | | | | 4,602 | |

| | | | | | | | |

| | |

| (1) | | IncludesIncluded Holiday Inn Club Vacations (2,892(3,701 rooms, 610 hotels) and Holiday Inn Resort properties (8,806 rooms, 37 hotels). |

InterContinental Hotels & Resorts

| | | | | | | | | | | | | |

| | | Americas | | EMEA | | Asia Pacific |

| |

Average room rate $(1) | | | 158.54 | | | | 232.90 | | | | 174.76 | |

Room numbers(2) | | | 19,120 | | | | 20,111 | | | | 19,198 | |

| | | | | | | | | | | | | | | | |

| | | Americas | | | Europe | | | AMEA | | | Greater China | |

Average room rate $(1) | | | 181.58 | | | | 251.80 | | | | 214.01 | | | | 171.37 | |

Room numbers(2) | | | 17,756 | | | | 9,394 | | | | 20,791 | | | | 9,373 | |

| | |

| (1) | | For the year ended December 31, 2010;2012; quoted at constant US$US dollar exchange rate. Average room rate is for comparable InterContinental hotels. |

|

| (2) | | At December 31, 2010.2012. |

InterContinental Hotels & Resorts (“InterContinental”) is the Group’s 5-starluxury brand located in majorkey cities in overand resort destinations across more than 60 countries worldwide. With over 60 years’years of experience, the brand’s understanding of high quality, understated service andtalented people supported by outstanding facilities coupled with a genuine interest in our guestshelp the Group to differentiate it in a competitive segment.segment by understanding that well-traveled and affluent people want to be connected to what is special about a hotel and its destination. The philosophy of the brandbrand’s ethos is to enable every guestempower guests to maximize the enjoyment ofshare their stay — specializing in engaging guests with the destination by sharing local knowledge to create authenticenjoy great experiences that enrich our guests’ lives and help them broaden their outlook.

lives.InterContinental hotels are principally managed by the Group. At December 31, 2010,2012, there were 171170 InterContinental hotels which represented 9%8% of the Group’s total hotel rooms. During 2010, nine2012, six InterContinental hotels were added to the portfolio, while fourfive hotels were removed.

27

Crowne Plaza Hotels & Resorts

| | | | | | | | | | | | | |

| | | Americas | | EMEA | | Asia Pacific |

| |

Average room rate $(1) | | | 101.94 | | | | 140.39 | | | | 105.16 | |

Room numbers(2) | | | 57,073 | | | | 22,941 | | | | 26,141 | |

| | | | | | | | | | | | | | | | |

| | | Americas | | | Europe | | | AMEA | | | Greater China | |

Average room rate $(1) | | | 110.3 | | | | 134.26 | | | | 142.22 | | | | 100.55 | |

Room numbers(2) | | | 48,730 | | | | 19,566 | | | | 18,559 | | | | 21,452 | |

| | |

| (1) | | For the year ended December 31, 2010;2012; quoted at constant US$US dollar exchange rate. Average room rate is for comparable Crowne Plaza hotels. |

|

| (2) | | At December 31, 2010.2012. |

Crowne Plaza Hotels & Resorts (“Crowne Plaza”), is the Group’s upscale brand and is currently the world’s fourth largest full-service hotel brand in the upscale, 4 star segment, specializesupper segments. The brand continues to appeal to business travelers, providing facilities and services that cater to these types of travelers. The Group continues to progress the multi-year Crowne Plaza repositioning program. As part of the Group’s commitment to strengthen the brand, quality audits have been carried out at almost all Crowne Plaza hotels in offeringstate-of-the-art businessThe Americas and meeting facilities that provide productive, successfulEurope and energizing experiencesthe Group has been actively managing the estate in order to guests who believe travel is fun and rewarding.

drive brand consistency.The majority of Crowne Plaza hotels are operated under franchise agreements in the US and Europe, and managed in other markets by the Group. In China, Crowne Plaza is the largest international upscale brand. At December 31, 2010,2012, there were 388392 Crowne Plaza hotels which represented 16% of the Group’s total hotel rooms. During 2010, 292012, 21 Crowne Plaza hotels were added to the portfolio, while seven16 hotels were removed.

The Holiday Inn Family of Brands

The Holiday Inn brand family, of brandswhich comprises Holiday Inn, Holiday Inn Club Vacations, Holiday Inn Resort and Holiday Inn Express, is the world’s largest midscale hotel brand family by number of rooms andat December 31, 2012. It is the largest brand in the Group’s most significant operation. Focused aroundportfolio predominantly operating under franchise agreements in The Americas and Europe and management agreements elsewhere.

Holiday Inn is for the contemporary traveler looking for innovative comfort in a relaxed atmosphere,relaxing hotel environment. Holiday Inn aims to provide guests familiarity, convenience and reliability while supporting and meeting all guest needs. As official hotel provider to the brands are designed to support both business travellersLondon 2012 Olympic and families. During 2010,Paralympic Games, the Group opened the Holiday Inn London, Stratford City. In 2012, the brand family neared completioncelebrated its 60th birthday and opened the largest Holiday Inn to date — the stunning Holiday Inn Macao Cotai Central, China with 1,224 rooms.

Holiday Inn Club Vacations, the Group’s timeshare business in North America, provides guests with all the benefits of a $1 billion refresh, updating their image by upgrading facilities, service and amenities, ensuringvacation home with none of the brands continue to remain competitive within their midscale markets. The hassle.

Holiday Inn family wasResort is our Holiday Inn brand family’s resort proposition, with 37 properties currently in the first internationalportfolio, for guests who work hard but also want to lead a balanced life.

Holiday Inn Express is a brand for the traveler looking for efficiency. The brand offers a straightforward, uncomplicated guest experience providing the things a guest needs, and is delivered in a way that is stimulating and engaging. One of the world’s fastest growing hotel chainbrands, it is geared to open in China in 1984the smart business or private traveler who appreciates value without compromising on comfort and the first hotel chain to launch a direct bookings website in 1995.

style.Holiday Inn Hotels & Resorts

| | | | | | | | | | | | | |

| | | Americas | | EMEA | | Asia Pacific |

| |

Average room rate $(1) | | | 95.12 | | | | 115.51 | | | | 88.57 | |

Room numbers(2)(3) | | | 147,575 | | | | 52,945 | | | | 29,597 | |

| | | | | | | | | | | | | | | | |

| | | Americas | | | Europe | | | AMEA | | | Greater China | |

Average room rate $(1) | | | 102.02 | | | | 112.36 | | | | 121.68 | | | | 82.21 | |

Room numbers(2)(4) | | | 146,661 | (3) | | | 46,610 | | | | 17,440 | | | | 20,777 | |

| | |

| (1) | | For the year ended December 31, 2010;2012; quoted at constant US$US dollar exchange rate. Average room rate is for comparable Holiday Inn hotels. |

|

| (2) | | At December 31, 2010.2012. |

|

| (3) | | The Americas total includes Holiday Inn Club Vacations (2,892(3,701 rooms). |

| (4) | Includes Holiday Inn Resorts properties — Americas 4,240 rooms, Europe 362 rooms, AMEA 3,311 rooms and Greater China 893 rooms. |

Holiday Inn Hotels & Resorts (including Holiday Inn Club Vacations)Vacations and Holiday Inn Resort) (“Holiday Inn”) are predominantly operated under franchise agreements. At December 31, 2010,2012, there were 1,247 Holiday Inn hotels which represented 36%34% of the Group’s total hotel rooms, of which 64%63% were located in theThe Americas. During 2010, 532012, 48 Holiday Inn hotels were added to the portfolio, while 13141 hotels were removed.

| | | | | | | | | | | | | |

| | | Americas | | EMEA | | Asia Pacific |

| |

Average room rate $(1) | | | 95.55 | | | | 95.18 | | | | 45.70 | |

Room numbers(2) | | | 159,867 | | | | 23,706 | | | | 7,655 | |

| | | | | | | | | | | | | | | | |

| | | Americas | | | Europe | | | AMEA | | | Greater China | |

Average room rate $(1) | | | 102.12 | | | | 93.04 | | | | 76.15 | | | | 49.88 | |

Room numbers(2) | | | 168,398 | | | | 24,903 | | | | 2,877 | | | | 9,453 | |

| | |

| (1) | | For the year ended December 31, 2010;2012; quoted at constant US$US dollar exchange rate. Average room rate is for comparable Holiday Inn Express hotels. |

|

| (2) | | At December 31, 2010.2012. |

Holiday Inn Express hotels are almost entirely operated under franchise agreements. At December 31, 2010,2012, there were 2,0752,192 Holiday Inn Express hotels worldwide which represented 30% of the Group’s total hotel rooms, of which 84%82% were located in theThe Americas. During 2010, 1222012, 114 new Holiday Inn Express hotels were added to the portfolio, while 11636 hotels were removed.

28

Staybridge Suites

| | | | | | | | | |

| | | Americas | | EMEA |

| |

Average room rate $(1) | | | 94.16 | | | | 112.18 | |

Room numbers(2) | | | 20,014 | | | | 748 | |

| | | | | | | | | | | | |

| | | Americas | | | Europe | | | AMEA | |

Average room rate $(1) | | | 104.11 | | | | 110.30 | | | | 140.02 | |

Room numbers(2) | | | 19,787 | | | | 605 | | | | 304 | |

| | |

| (1) | | For the year ended December 31, 2010;2012; quoted at constant US$US dollar exchange rate. Average room rate is for comparable Staybridge Suites hotels. |

|

| (2) | | At December 31, 2010.2012. |

Staybridge Suites is the Group’s upscale extended stay brand for guests on longer trips, offering studios and suites complete with full kitchens and separate sleeping and work areas in a sociable, family-like atmosphere. It was the fastest upper-tier extended stay brand to reach the 50-hotel and 100-hotel milestones, and was ranked highest in the prestigious J.D. Power and Associates’ 2009 North America Hotel Guest Satisfaction Index Study for extended stay hotels. In 2008 Staybridge Suites opened its first EMEA hotelplayed a significant role in LiverpoolIHG’s partnership with the London 2012 Olympic and has since opened properties in Cairo, Abu Dhabi and Newcastle.