SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| Registration statement pursuant to Section 12(b) or (g) of the Securities Exchange Act of 1934 | |

| Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |

| For the fiscal year ended January | |

| Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |

For the transition period from ________ to ________.

Commission file number 0-16945

SIGNET GROUP plc

(Exact name of Registrant as specified in its charter)

ENGLAND

(Jurisdiction of incorporation or organization)

Zenith House

The Hyde

London NW9 6EWEnglandEngland

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act:None

| Title of each class | Name of each exchange on which registered |

| Ordinary Shares, nominal value £0.005 each | New York Stock Exchange* |

| American Depositary Shares, | New York Stock Exchange |

| each representing 10 ordinary shares |

| * | Not for trading, but only in connection with the registration of the ADSs pursuant to the requirements of the Securities and Exchange Commission. |

Securities registered or to be registered pursuant to Section 12(g) of the Act:American Depositary SharesOrdinary Shares of 0.5 pence each

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

| Ordinary Shares of 0.5 pence each | |||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

![]() Yes

Yes ![]()

![]() No

No ![]()

Indicate by check mark which financial statement item the registrant has elected to follow.

![]() Item 17

Item 17 ![]()

![]() Item 18

Item 18 ![]()

Explanatory Note

This document comprises the annual report on Form 20-F and the annual report to shareholders for the year ended 3129 January 20042005 of Signet Group plc (the “2003/04“2004/05 Form 20-F”). Reference is made to the Cross referenceReference to Form 20-F table beginning on page 124137 hereof (the “Cross referenceReference to Form 20-F table”Table”). Only (i) the information in this document that is referenced in the Cross referenceReference to Form 20-F table,Table, (ii) the cautionary statement concerning forward-looking statements on page 1 and (iii) the Exhibits, shall be deemed to be filed with the Securities and Exchange Commission for any purpose, including incorporation by reference into the Registration Statements on Form S-8 (No. 333-8764, 333-9634 and 333-12304) of Signet Group plc (No. 333-12304, 333-9634, 333-8764 and 033-42119), and any other documents, including documents filed by Signet Group plc pursuant to the Securities Act of 1933, as amended, which purport to incorporate by reference the 2003/042004/05 Form 20-F. Any information herein which is not referenced in the Cross referenceReference to Form 20-F table,Table, or the Exhibits themselves, shall not be deemed to be so incorporated by reference.

![]()

| 2004/05 | |||

Group highlights |

| Reported | At constant | |||||

| basis | ||||||

| exchange rates(1)(2) | ||||||

| up | ||||||

| Sales: | £1,614.4m | up 0.6%(2) | up 7.8% | |||

| Operating profit: | £218.9m | up 4.1%(2) | up 11.3% | |||

| Profit before tax: | £210.3m | up 5.3%(2) | up 12.1% | |||

| Earnings per share(3): | 8.2p | up 9.3%(2) | up 15.5% | |||

| Dividend per share: | 3.0p | up 20.0% | ||||

| 26.5% | up from 25.9%(2) | |||||

| 11.3% | down from11.8%(2) | |||||

|  | |||||||

|  |

| ||||||

| (1) | See page | ||

| (2) | |||

| (3) | Earnings per share, return on capital employed and gearing are defined on page | ||

| (4) | 53 week year. | ||

| Annual Report & Accounts

Chairman’s statement Group results

The UK division also had a particularly strong first quarter but faced a softening trend in the trading environment during the rest of the

The Group continued to utilise its cash flow and strong balance sheet to invest in the growth of the business. £159.1 million was invested

Principles (“GAAP”) being replaced by International Financial Reporting Standards (“IFRS”), and both converging with US GAAP. The process this year has resulted in a restatement relating to the revenue recognition of extended service agreements in the US (see note 17, page 85) and the replacement in 2005/06 of UK GAAP by IFRS as explained in more detail in the Financial review (page 33). Dividend

People

Rob Anderson, Chief Executive of Signet’s UK division, joined the Board as an executive director in

Current trading

James McAdam

Group Chief Executive’s review Introduction

US division

New store space rose by 8% during 2004/05 further Growth in new store space and further development of the division’s competitive strengths in the critical areas of merchandising, store operations and marketing have contributed significantly to the out-performance of the business and remain key elements of future strategy. Given the continuing consolidation in the speciality jewellery sector, there should be opportunities to gain further market share both organically and, if appropriate, by acquisition. The US division is now targeting organic space growth of 7% - 9% in future years (previously 6% - 8%). UK

The Central to selling diamonds is the interaction between the customer and the salesperson. The roll-out of the new store format, which facilitates such interaction, was implemented as part of the store refurbishment cycle in 2004/05. The focus on customer service was also evident in the priority given to staff training. The significant changes taking place in the UK US

The operating margin

Group Chief Executive’s review (continued)

In the jewellery sector superior customer service and product knowledge are important competitive advantages readily identified by the consumer, and the division now has at least one certified diamontologist in every store. Also during 2004/05 all sales staff were coached using the “Ultimate Diamond Presentation” training course. Procedures for recruitment were strengthened and staff retention was also improved. The multi-year In mall stores the Strong marketing programmes again contributed to the

Kay, with a turnover of $1,155.5 million, became the number one speciality jewellery brand by sales during 2004/05 having consistently out-performed its major competitors. Over the last five years the number of Kay stores has increased by almost 200 to a total of 742 and average sales per store have grown to $1.584 million from $1.355 million. Brand name recognition has risen very significantly since the introduction of the “Every kiss begins with Kay” advertising campaign in 2000/01. It is planned to increase Kay’s representation in malls by between 20 and 30 new stores in 2005/06. In addition to mall locations, stores under the Kay brand are currently being opened in lifestyle and power strip centres. Ten such stores were opened in 2004/05 and a similar number are planned in 2005/06. In the current year it is anticipated that up to four stores will be trialled in metropolitan areas. Currently 321 mall stores trade under strong regional brand names. Sales in the year were over $450 million, reflecting average sales per store of $1.533 million. The regional stores could provide the potential to develop a second mall brand of sufficient size to justify the cost of national television advertising. This would require about 550 stores which could be achieved in the medium term by a mixture of store openings and acquisitions. In 2005/06 it is planned that 20-30 new stores will be opened under the regional brand names. Jared now has sales of just over

The change in store numbers by chain is shown in the following table:

In 2004/05 Recent investment in the store portfolio is

UK (32% of Group sales)

The division’s gross margin benefited from the effect of the lower dollar exchange rate on dollar denominated commodity costs. The operating margin at 15.2% was little changed after absorbing a restructuring charge of £1.7 million. Like for like sales were up by 1.9% in H.Samuel, while total sales were similar to last year due to nine net store closures and a significant increase in the number of temporary closures for refurbishment. H.Samuel’s sales per store increased to £0.723 million (2003/04: £0.707 million). Ernest Jones had another strong performance with like for like sales up by 4.5%, total sales increasing by 6.7% and sales per store reaching £1.150 million (2003/04: £1.101 million). Diamond jewellery assortments were enhanced during the year and continued to perform strongly, accounting for 20% of sales in H.Samuel and The outcomes. Particular benefit from improved staff training was gained in Catalogues remain the

In Recent investment in the store portfolio is set out below:

A similar pattern of store

Terry Burman

Five year financial summary

The financial data included in the Five year financial summary above has been derived, in part, from the consolidated accounts for such periods included elsewhere in this Annual Report. The financial data should be read in conjunction with the accounts, including the notes thereto, and the Financial review included on pages Further selected financial data is shown on pages

US operating review

Overview

Competitive advantages • Store operations and personnel

systems. The division now has at least one certified diamontologist in each of its stores. • Real estate • Merchandising

It is anticipated that Jared Initiatives in

US operating review (continued)

Signet’s total US dollar sales rose (excluding the acquisition of Marks & Morgan)

Management believes that the longer term outlook for jewellery sales is encouraging given the growth in disposable The US division competes on the basis of the quality of its personalised customer service, merchandise selection, availability, quality and value. Brand recognition, trust and store locations are also competitive advantages as is the ability to offer private label credit card programmes to customers. The US division holds no material patents, licenses, franchises or concessions but has a range of trading agreements with suppliers, the most important being in regard of the Leo Diamond. The established trademarks and trade names of the division are essential to maintaining its competitive position in the retail jewellery industry. The US retail jewellery industry is very competitive and highly fragmented.

retailer is believed to be Wal-Mart Stores, Inc., which includes a wide assortment of costume jewellery. Management believes that the business also competes with non-jewellery retailers for consumers’ discretionary spending. The US division’s largest speciality jewellery competitor is Zale Corporation, which has a speciality market share of about

sector. Management believes that the

Providing knowledgeable and responsive customer service is a

differentiation. It is believed that highly trained store sales staff with the necessary product knowledge to communicate the competitive value of the merchandise are critical to the success of the business. The US division’s substantial training and incentive programmes for all levels of store staff are designed to play an important role in recruiting, educating and retaining qualified store staff. The preferred practice is to promote managers of all levels from within the organisation in order to maintain continuity and familiarity with Retail sales personnel are encouraged to become America. All store personnel are required to meet daily performance standards and commit to goals. After completion of basic training, sales staff are paid a commission based on their individual sales performance and on meeting monthly store sales targets. Sales contests and incentive programmes also reward the achievement of specific goals with travel or additional cash awards. In addition to sales based incentives, bonuses are paid to store managers and district managers based on the achievement of key performance objectives. In Each store is led by a store manager who is responsible for various store level operations including overall store sales and branch level variable costs; certain personnel matters such as recruitment and training; and customer service. Administrative matters, including purchasing, merchandising, payroll, preparation of training materials, credit operations and divisional operating procedures are consolidated at divisional level. This allows the store manager to focus on those tasks that can be best executed at the store level while enabling the business to benefit from economies of scale in administrative matters and to help ensure consistency of execution across all the stores. Staff recruitment is primarily the responsibility of store and district managers. In 2004/05 the division began to develop a central recruitment facility that supplies field recruiters from the home office, and uses methods such as internet recruitment to provide stores with a larger number of better qualified candidates from which to select new staff. Management believes that the retention and recruitment of highly qualified and well-trained staff in the US head office in Akron, Ohio

US operating review (continued) US head office bonuses are mainly based on the performance of the division against predetermined annual profit targets. Promotion decisions for all non-management head office personnel are based on performance against service level and production goals; for managers they are based on annual objectives and performance against individual job requirements. Real estate Jared locations are typically free-standing sites in shopping complexes with high visibility and traffic flow, and positioned close to major roads. The retail centres in which Jared stores operate normally contain strong retail co-tenants, including other category killer destination stores such as Borders Books, Best Buy, Home Depot and Bed, Bath & Beyond. Details of recent investment in the store portfolio are set out below:

Management believes that the US division’s prime real estate portfolio, together with its regular investment in mall store refurbishments and relocations, are competitive advantages that help build store traffic. Superior like for like sales growth is normally achieved for a number of years following such investment. The typical benefits from mall store refurbishments, which normally occur on a ten year cycle, include an increase in linear footage of display cases positioned on the store frontage, improved lighting and better access to the store. When relocating a store to a better location in a mall, such as a centre court corner site from an in-line location, an increase in like for like sales is expected due to improved visibility to the customers, improved lighting and more display cases being positioned on the lease line between the store and the mall common areas. Criteria for investment in mall real estate remain stringent. Signet seeks sites in superior malls, in particular units located on busy centre court locations. In 2004/05 there was a net increase in the US division’s new store selling space of approximately 8%, at the top end of the target range. In 2005/06 it is planned to open approximately 15-20 Jared stores. 40-50 mall stores, up to ten additional off-mall Kay and up to four metropolitan stores will also be opened. Around 20 mall stores are planned for closure. The programme should result in a net increase in new store space of about 8% by the end of 2005/06. Signet may consider selective purchases of mall stores that meet its acquisition criteria regarding location, quality of real estate, customer base and return on investment for both the Kay and regional brands. Kay The development of Kay stores in suburban off-mall shopping centres, such as “lifestyle” and “power strip” centres, commenced in 2003/04 with the opening of ten stores. A further ten were opened in 2004/05, and it is intended that ten will be opened in 2005/06. A lifestyle centre is an open air shopping centre where the retail mix is biased toward fashion and leisure stores and is also likely to have a large number of restaurants. A power strip centre is also an open air shopping centre but the retail mix is predominantly category killer superstores with some smaller speciality units. Kay stores in these suburban centres are expected to have a lower capital expenditure, lower rents and lower sales per store at maturity than that of the Kay chain average. In 2005/06 up to four Kay stores are planned to be opened in traditional metropolitan locations in cities such as Boston, Chicago, San Francisco and New York. Kay stores in large metropolitan locations are anticipated to have higher capital expenditure, higher rents and higher sales per store at maturity than those of the Kay chain average. Management believes that the expansion of Kay in these new locations

The following table sets out information concerning the US stores operated by Signet during the period indicated:

presents a potential opportunity to reach new customers currently not served, and gain further leverage from its marketing expenditure and the US division’s central overhead. Regional chains In recent years, new regional chain stores have been opened if real estate satisfying the investment criteria becomes available in their respective trading areas or in adjacent areas where marketing support can be cost effective. Areas in which the scale to support cost-effective marketing can be built over a reasonable time span are now also considered for store openings. This is part of a strategy to potentially develop a second mall-based brand of sufficient size to take advantage of national television advertising. This strategy may also include the acquisition of small or large regional chains of speciality jewellery stores that meet the Group’s strict operational and financial criteria. Jared

US operating review

The following map shows the number and locations of Kay, Regional and Jared stores at 29 January 2005.

Jared targets an under-served sector at the upper end of the middle market. The customer profile is of a more mature, higher income customer than that of Signet’s US mall stores. An important advantage of a destination store is that the potential customer visits the store with the intention of making a jewellery purchase, whereas in a mall there is a greater possibility of the intended spend being diverted to non-jewellery purchases. The typical Jared store has about 4,700 square feet of selling space and 5,900 square feet of total space. Its size permits significantly expanded product ranges and enhanced customer services, including in-store repair and custom design facilities. A private viewing room is available for customers when required. There are also complimentary refreshments and a children’s play area. There were 93 Jared stores at 29 January 2005 (31 January 2004: 79 stores). The average retail price of merchandise sold in Jared stores during 2004/05 was $644 (2003/04: $586), which was more than double that of a Signet US mall store. In the first five years of trading a Jared store is projected to have a faster rate of like for like sales growth than that of a mall store

during the same period. At the end of this period the projected operating margin is expected to have risen to around that of the mall store at maturity, with a greater return on capital employed. Excluding the three prototype stores the average sales of the 25 Jared stores that have reached maturity is $5.6 million in their fifth full year. At 29 January 2005 some 70% of the Jared stores had been open for less than five years. The average sales per Jared store opened for the whole of the 2004/05 financial year were $4,975,000 (2003/04: $4,573,000) and reflects the immaturity of Jared. Since the first Jared store opened in 1993, the concept has been continually evaluated, developed and refined. Management believes that in addition to the competitive advantages possessed by the division as a whole, Jared also benefits from leveraging the division’s established infrastructure, access to a pool of experienced store management, and availability of capital required to develop and grow the brand. Management believes that the Jared concept has considerable growth potential and over 100 suitable markets have been identified, with many of these markets able to support multiple locations. Accordingly, in the longer term, the chain has the potential to expand nationwide to over 225 stores, generating annual sales of over $1 billion based on the current performance of existing Jared stores. Some Jared stores are being opened to test new real estate selection criteria that may increase the potential number of sites suitable for a Jared store. These include opening Jared stores nearer to each other in established markets with above-average population density (such as Atlanta, Georgia); entering smaller markets where national television advertising would make marketing support cost-effective (such as Tulsa, Oklahoma); and locating stores attached to the exterior of covered malls (such as Des Moines, Iowa). Merchandising and purchasing Sophisticated inventory management systems for merchandise testing, assortment planning, allocation and replenishment have been developed and implemented. Approximately two-thirds of the merchandise is common to all US division mall stores, with the remainder allocated to reflect demand in particular markets. It is believed that the merchandising and inventory management systems, as well as improvements in the productivity of the centralised distribution centre, have allowed the division to achieve inventory turns comparable to those of most of its quoted competitors although it has a less mature store base and undertakes more Programmes have been developed in conjunction with certain vendors for the provision of branded jewellery merchandise. For example, the Leo Diamond range is sold exclusively by Signet in the US and the UK. Management believes that the US division’s merchandising process, market share and relationship with suppliers position the business as an ideal partner to launch Other merchandising initiatives offer a distinctive product selection. For example, In The table below sets out Signet’s US merchandise sales mix as a percentage of sales:

US operating review (continued) It is believed that the US division has a competitive cost and quality advantage as approximately 55% of Merchandise is purchased complete as a finished product where the manufacturer’s price is more competitive than using direct sourcing, or the complexity of the product is great or the merchandise is considered likely to have a less predictable sales Merchandise held on consignment is used to enhance product selection and test new designs. This minimises exposure to changes in fashion trends and obsolescence and provides the flexibility to return non-performing merchandise. At In Marketing and advertising through percentage of sales was Advertising activities are concentrated on periods when customers are expected to be most receptive to the marketing message. During the

Jared advertising on local radio takes place for most of the

Statistical and technology based systems are employed to support a direct marketing programme that uses a proprietary database of over

key trading periods. In addition, invitations to special promotional in-store events are extended throughout the year. Special catalogues featuring ranges such as luxury watches are produced for Jared.

Credit operations The table below presents data related to the in-house credit business for the past three financial years. Since The credit portfolio turns approximately every seven months and the monthly collection rate

The bad debt charge for the year, at end of the range over the last eight years. In-house credit sales represented Authorisation and collections are all performed centrally at the US headquarters on an automated basis, rather than by store staff. The majority of credit applications can be processed and approved in less than two minutes; they can be made via in-store terminals, through a toll-free phone number or on-line through the marketing web sites. All applications are evaluated by the scoring of credit data and data obtained through third party credit bureaux. Investment in staff, training and systems to maintain or improve the quality of the credit portfolio continued throughout The new system will provide management with increased flexibility to implement and/or modify collection strategies, and a more user-friendly platform. Collection strategies and efforts continued to include increased emphasis on

US operating review (continued) Management tools and communications All stores are supported by the internally developed Store Information System, which includes electronic point of sale (“EPOS”) processing, in-house credit authorisation and support, a district manager information system and a satellite-based communications system that supports data transmissions and company-wide e-mail. The EPOS system updates sales, in-house credit and perpetual inventory replenishment systems from data captured throughout the day for each store. In order to allow staff more time for selling and customer service, further steps in the “World Class Store Systems” initiatives were taken. These have resulted in improvements in special orders and repair services procedures. Regulation

UK operating review

Overview At The UK strategy is to increase the average transaction value by focusing on fast growing product categories, particularly diamond jewellery, thereby improving store productivity and achieving operational leverage. To achieve this the division has a series of initiatives in the key areas of retail execution that are designed to grow the sales of diamonds. Competitive advantages •Store operations and personnel •Real estate •Merchandising •Marketing •Access to US expertise Initiatives in

UK operating review (continued)

The UK retail jewellery In the middle market H.Samuel competes with a large number of independent jewellers, the only competitor of significant size being F Hinds (108 stores). Competition at the lower end of the H.Samuel product range also comes from catalogue showroom outlets such as Argos and discount jewellery retailers such as Warren

In the upper middle market Ernest Jones’ competition is from independent speciality retailers and a limited number of other upper middle market jewellery groups such as Goldsmiths Group (169 stores); Beaverbrooks Based on

Store operations and personnel The new recruitment procedures continue to improve the suitability of new store personnel helping to ensure that they meet key basic requirements and are motivated to work within the jewellery store environment. Field and human resources management are responsible for the recruitment, performance review, training and development of sales staff, thereby ensuring consistency in operating standards and procedures throughout the business. All new store personnel must complete a “selling skills” learning programme during their probationary period and thereafter undertake additional training in selling, product knowledge and customer care. All store personnel have daily performance targets. They are given training and weekly feedback on their performance from store and field management to help them achieve these targets. In conjunction with the Signet Jewellery Academy, training for all tiers of store operations management was developed further last year to support the initiative to improve customer service. In 2004/05 the number of training courses completed nearly doubled. The preferred policy is to promote store managers from within the business; approximately 70% of store management appointed in 2004/05 were promoted from within the organisation. At any given time each chain has a number of sales staff who are qualified to advance to store management level, thus assuring the availability of newly trained managers familiar with operating standards and procedures.

In order to increase staff selling time and to improve efficiency, operating procedures are routinely reviewed to identify opportunities to enhance customer service and reduce in-store administrative tasks. The Signet intranet, introduced in all stores in 2003, provides a computer-based platform for improved communication between stores and head office, with sales floor and back office administrative functions being simplified and standardised through this medium. Various incentive schemes are operated to motivate and reward performance in the stores including bonuses based on key performance targets. In 2004/05 a commission-based remuneration test was carried out designed to increase the proportion of performance-related payments over time. The level of commission paid is dependent on the sales achieved by the individual and the overall sales of the store. During 2005/06 this commission system will be introduced more widely across the division. Management also believes that successful recruitment, training and retention of head office staff is essential. Comprehensive recruitment, training and incentive programmes for head office staff are in place in the Colindale and Birmingham offices. Programmes to provide employees with structured development plans, training and career paths have been implemented. Internal career advancement is encouraged and is supported by a succession planning process. Teamwork and service to the stores are encouraged through a performance bonus plan for head office staff, which is based on the division’s results. Opportunities for improving employment practices were identified through a “Staff Opinion Survey”. It is believed that the results provide a basis for further improvement in the motivation and retention of staff.

The performance of the new format has continued to be encouraging. The increase in sales from the additional investment meets the well established Group investment criteria. The reformatted stores achieved a rise in both diamond sales and average retail price. An additional 90 stores, primarily H.Samuel, were trading in the new format at 29 January 2005, bringing the total to 142, accounting for about 30% of the UK division’s sales. A multi-year rollout plan for the new format is being implemented as part of the normal refurbishment cycle; it is planned to refurbish or relocate 80 to 90 stores in 2005/06, the majority again being H.Samuel. The new format features open frontages which are intended to make the store more accessible and inviting to the customer, as well as improved presentation of the merchandise. The design draws on the Group’s mall store experience in the US, and for mall locations Much of the merchandise is

Details of recent investment in the store portfolio are set out below:

H.Samuel

The average retail price of items sold

UK operating review (continued) Ernest Jones (including Leslie Davis) The principal product categories are diamonds, branded watches and gold jewellery, which are all merchandised and marketed to appeal to the more affluent upper middle market customer (see At

Merchandising and purchasing The merchandise mix of Signet UK diamond sales was

Merchandise is purchased from a range of suppliers and manufacturers. In

Economies of scale Signet UK also employs contract Merchandising teams work in conjunction with the buyers and focus on assortment planning, branch grading, repeat orders, inventory levels and margin management. Product category reviews are regularly carried out with a focus on increasing potential gross margin return on investment. Rigorous test marketing procedures are used to trial products, and their

subsequent distribution is made strictly against rates of sale.

The size and quality of diamond jewellery available to customers was enhanced during the year, with a greater proportion of precious white metals. Branded diamonds exclusive to Signet have been Each store is assigned a range of merchandise that reflects local buying patterns. Display equipment and layouts are constantly reviewed and updated, and new display formats that draw upon the US division’s experience Marketing and advertising The primary marketing and advertising medium employed in

Public relations up to Valentine’s Day and Christmas. During 2004/05 customer relationship marketing was successfully trialled for Ernest Jones and During Insurance loss replacement business Credit operations Management tools and communications EPOS equipment, retail management systems, purchase order management systems and merchandise planning processes are in place to support financial management, inventory planning and control, purchasing, merchandising, replenishment and distribution and can

UK operating review (continued) and debit card fraud. The first phase of an electronic “Business To Business” communications project, developed to improve the efficiency and effectiveness of dealing with suppliers, was implemented. A perpetual inventory process allows store managers to check stock by product category. New systems have been introduced to enhance control over cash banking to support financial management. Major computer hardware upgrades have taken place to improve resilience and capacity, particularly during the peak Christmas season. The administration centre at Colindale in North London is the head office for UK store operations and houses the division’s senior management, financial planning, marketing, and buying and merchandising functions. The facilities for payroll, human resources, information technology, certain finance functions, distribution and customer services, as well as the insurance replacement business and call centre, are located in Birmingham. During 2004/05 various central administrative functions were relocated from Colindale and consolidated in Birmingham to enhance efficiency and should result in future cost savings. Regulation

Description of property & Group employees Signet attributes great importance to the location and appearance of its stores. Accordingly, in both Signet’s US and UK operations, investment decisions on selecting sites and refurbishing stores are made centrally, and strict real estate criteria are applied. The US The US division leases 17% of its store locations from Simon Property Group and 15% from General Growth Management, Inc. Otherwise, the division has no relationship with any lessor relating to 10% or more of its store locations. During the past five financial years the US business has been generally successful in renewing its store leases as they expire and has not experienced difficulty in securing suitable locations for its stores. It is not believed that any of the store leases are individually material to the Group’s US operations. A UK terms of up to 25 years, generally under full repairing and insuring leases (equivalent to triple net leases in the US). Wherever possible Signet is shortening the length of new leases that it enters into in order to improve the flexibility of its lease commitments. Rents are usually subject to upward review every five years if market conditions so warrant. An increasing proportion of rents are related to sales of the store, subject to a minimum annual value. At the end of the lease period, subject to certain limited exceptions, leaseholders generally have statutory rights to enter into a new lease of the premises on negotiated terms. At Signet owns a 255,000 square foot warehouse and distribution centre in Birmingham. Following the relocation and consolidation of certain of the UK division’s central administration functions to Birmingham Trademarks and trade names Group employees

None of Signet’s employees in the UK and less than 1% of Signet’s employees in the US are covered by collective bargaining agreements. Signet considers its relationship with its employees to be excellent.

Financial review

Introduction

In general, gross on the proportion of the merchandise cost accounted for by the value of the diamonds, and the greater the proportion, the lower the gross margin. In addition, the gross margin in a Jared store is slightly below that of a mall store, although at maturity the

division and Group. To maintain the operating profit margin the Group needs to achieve like for like sales growth sufficient to offset any adverse movement in gross margin, the increase in operating costs and the impact of immature selling space. There are not any known trends or uncertainties in future rent or amortisation expenses that could materially affect operating results or cash flows. Like for like sales growth above Signet’s longer term strategy of The impact on operating profits of sales variances (either adverse or favourable) is less in the US division than the UK, as certain expense items are more related to sales volumes in the US. A key factor in driving operating margin is the level of average sales per store, with higher productivity allowing leverage of expenses both in store and in central

Movements in the US dollar to pound sterling exchange rate impact the reported results of the Group as the US division’s results are translated into pounds sterling. The Board believes it is inappropriate to hedge this exposure as the US division’s sales and costs are dollar denominated and the cash flow from the US division is largely reinvested in the US space expansion or used to pay down US dollar denominated borrowings. The Group therefore would be putting in place a cash exposure to hedge a translation risk.

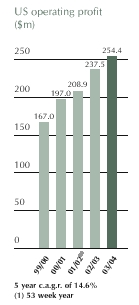

52 weeks ended Group operating margin increased to Net interest payable and similar charges decreased to Group profit before tax increased to

US to 2004/05 with an excellent performance during the UK Operating profit

US UK Group costs

Financial review (continued) Prior year adjustment As a result of this change the Group has restated prior years. Therefore the previously reported 2003/04 results now reflect a decrease in sales of £12.3 million and a reduction in profit before tax of £12.1 million. The difference of £0.2 million represents the movement in the incremental cost provision applied under the previous accounting policy. Consequently, restated profit before tax for the 52 weeks ended 31 January 2004 is £199.8 million. The effect on brought forward reserves at 31 January 2004 is a reduction of £52.7 million net of deferred tax, with shareholders’ funds at 31 January 2004 therefore restated to £674.9 million. The adjustment does not affect cash flows from operations. Return on capital employed Depreciation and capital expenditure Dividends share for Liquidity and capital resources The cash flow performance of the Group depends on a number of factors such as the:

Investment in new space requires significant investment in working capital, as well as fixed capital investment, due to the slow inventory turn, and the In years when the rate of new store space expansion in the US is towards the lower end of the planned The Group’s working capital requirements fluctuate during the year as a result of the seasonal nature of its business. As inventory is purchased for the Christmas season there is a working capital outflow which reaches its highest levels in the late autumn. This position then reverses over the key selling period of November and December. The working capital needs of the business are then relatively stable from January to August. The timing of the payment of the final dividend, normally in July, is also material.

The Board considers that the capital resources currently available are sufficient for both its present and near term requirements. The primary borrowing facilities are a $251 million securitisation against the US customer receivables which amortises between December 2005 and October 2006 and a

Group capital expenditure was £70.5 million (2003/04: £50.9 million,

Net debt The Company funds part of its private label credit card receivables programme through a privately placed receivables securitisation. Under this securitisation, interests in the US receivables portfolio, held by a trust were sold principally to institutional investors in the form of fixed-rate Class A, Class B and Class C investor certificates. The aggregate outstanding principal amount of the certificates totalled $251.0 million at In On 28 September 2004

The continued availability of the Facility Agreement is conditional upon the Group achieving certain financial performance criteria (see note 16 on page In July 1998 the Group entered into a $60 million unsecured seven year senior note issue (“Loan Note”), bearing a 7.25% fixed coupon. The Loan Note is also guaranteed by the Group’s principal holding and operating subsidiaries. The continued availability of the Loan Note is conditional upon the Group achieving certain financial performance criteria (see note 16 on page The principal financial covenants on each of these facilities are set out in note 16 on page It is the policy of the Group to enter into interest rate protection agreements in respect of at least 75% of its forecast US dollar borrowings. At

Financial review (continued) Pensions Contingent property liabilities additional properties were sub-let at that date. Should the assignees or sub-tenants fail to fulfil any obligations in respect of those leases or any other leases which have at any other time been assigned or sub-let, the Group or one of its UK subsidiaries may be liable for those defaults. The number of such claims arising to date has been small, and the liability, which is charged to the profit and loss account as it arises, has not been material. Contractual obligations

Impact of constant exchange rates analysing and explaining changes and trends in the Group’s

Financial review (continued) Prior year review of the 52 weeks ended 31 January 2004 Group operating margin increased to 13.1% (2002/03: 12.5%), with leverage from like for like sales growth more than offsetting the impact of immature space growth with gross margin little changed. The growth in total sales and the increased operating margin resulted in Group operating profit advancing to £210.2 million (2002/03: £199.9 million), up 5.2% on a reported basis and 12.2% at constant exchange rates. Net interest payable decreased to £10.4 million (2002/03: £14.0 million). £1.5 million of the reduction was due to exchange translation, the balance attributable to lower levels of net debt which more than offset the decrease in net interest credit on the UK defined benefit pension scheme. Group profit before tax increased to £199.8 million (2002/03: £185.9 million), up 7.5% on a reported basis and 14.3% at constant exchange rates. After a tax charge of 35.1% (2002/03: 35.3%) profit for the financial period rose to £129.6 million (2002/03: £120.2 million). Earnings per share was 7.5p (2002/03: 7.0p), up 7.1% on a reported basis and 13.6% at constant exchange rates.

Sales US UK like sales rose by 6.7%. For the year as a whole like for like sales increased by 5.5% and total sales by 5.8%. Operating profit US UK

Group costs Prior year adjustment Return on capital employed

Depreciation and capital expenditure Dividends Impact of constant exchange rates

Critical accounting policies

Revenue recognition

Financial review (continued) sale in proportion to anticipated claims arising. This period is based on the historical claims experience of the US business, which has been consistent since these products were launched. The Group reviews the pattern of claims at the end of each year to determine any significant trends that may require changes to revenue recognition rates. The treatment of US extended service Stock valuation Where necessary provision is made for obsolete, slow-moving and damaged stock. This provision represents the difference between the cost of the stock and its estimated market value, based upon stock turn rates, market conditions and trends in consumer demand. For further detail on the provisions for inventory and the amount of reserves recorded each year, refer to note 12 on page 83 in the notes to the accounts. In the US stock losses are recognised at the mid-year and fiscal year end based on complete physical inventories. In the UK stock losses are Foreign currency translation based on US sales, during the period and their balance sheets and attributable goodwill at the rates at the balance sheet date. Exchange differences arising from the translation of the net assets and attributable goodwill of overseas subsidiary undertakings Depreciation and impairment In the UK, there are circumstances where scheduled refurbishments are carried out close to the end of the lease term, such that the expected life of the newly installed leasehold improvements will exceed the lease term. Where the renewal of the lease is reasonably assured, such shopfronts, fixtures and fittings are depreciated over a period equal to the lesser of their economic useful life, or the remaining lease term plus the period of reasonably assured renewal. Reasonable assurance is gained through evaluation of the right to enter into a new lease, the peformance of the store and potential availability of alternative sites. Where appropriate, provision is made on assets that have a lower economic value than net book value. Additionally, Lease costs and incentives In accordance with FRS 12, where the Group has onerous lease obligations, provision is made for the discounted cash outflow that is expected to arise under the lease. The Group policy is to recognise a provision for onerous leases when the leased property ceases to be used by the Group. Receivables

Advertising and promotional costs International

The most significant elements contributing to the change in financial information are:

These changes have no impact on the Group’s historical or future net cash flow, the timing of cash received or the timing of payments. Transitional arrangements

Financial review (continued)

IAS 12 Income tax

These result in an additional charge to the profit and loss account of £3.5 million and a decrease in net assets of £17.9 million before deferred tax. There is no impact on cash flows.

IAS 18 Revenue recognition There are a number of other presentational changes that do not have an impact on the profit or net assets of the Group. Insurance income and

Risk and other factors

Forward-looking statements

• | financial market risks, including fluctuations in exchange rates between the pound sterling and the US dollar which may affect reported revenues, costs, the value of the Group’s consolidated borrowings, and the cost of capital. | | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Actual results may differ materially from those anticipated in exchange rates between the pound sterling and the US dollar whichsuch forward-looking statements even if experience or future changes make it clear that any projected results expressed or implied therein may affect reported revenues, costs, the value of the Group’s consolidated borrowings, and the cost of capital.not be realised. The Group undertakes no obligation to update or revise any forward-looking statements to reflect subsequent events or circumstances.

Impact of general economic conditions

Jewellery purchases are discretionary and may be particularly affected by adverse trends in the general economy.

The success of the Group’s operations depends to a significant extent upon a number of factors relating to discretionary consumer spending. These include economic conditions and perceptions of such conditions by consumers, employment, the rate of change in employment, the level of consumers’ disposable income, business conditions, interest rates, consumer debt levels, availability of credit and levels of taxation for the economy as a whole and in regional and local markets where the Group operates. There can be no assurance that consumer spending on jewellery will not be adversely affected by changes in general economic conditions. However, due to the limited seasonality in the product mix, the risk of having to discount inventory in order to be correctly stocked for the next selling season is more limited than for some other retail sectors. While the level of consumer expenditure may vary, the occasions when jewellery is purchased – engagements, weddings and events such as Christmas, wedding anniversaries, birthdays, Valentine’s Day and Mothers’ Day – occur on a regular basis.

As a substantial proportion of the Group’s US sales are made on credit, any significant deterioration in general economic conditions or consumer debt levels may inhibit consumers’ use of credit and cause a material adverse effect on the Group’s revenues and profitability. Furthermore, any downturn in general or local economic conditions in the markets in which the Group operates may adversely affect its collection of outstanding credit accounts receivable and hence the net bad debt charge. Currently there are all-time high levels of consumer debt in the US, however, the level of net bad debt charge as a percentage of credit sales in the Group’s US division in 2003/042004/05 was towards the lowest forbottom end of the last eight years.range.

| Signet Group plc Annual Report & Accounts year ended 29 January 2005 | 35 |

Risk and other factors (continued)

Merchandise selection, pricing, inventory and purchasing

The Group depends on consumer fashions, preferences for jewellery in general and the demand for particular products. Design trends in jewellery normally only change over relatively long periods and there is little seasonality in the merchandise mix. The ability to predict accurately future changes in taste, respond to changes in consumer preferences, carry the inventory demanded by customers, deliver the appropriate quality, price products correctly and implement effective purchasing procedures, all have an important influence on determining sales performance and achieved gross margin (see pages 1213 and 1820 for more details of the Group’s merchandising and purchasing procedures).

Risk and other factors (continued)

The Group’s operating experience suggests that while the price of jewellery is a consideration for consumers, it is not among the top three factors in determining where they buy jewellery. The Group believes these factors to be the level of service provided to the customer, the quality, together with the selection, of merchandise offered and the reputation of the retailer. Therefore while discounting price may increase sales, it may not increase profit.

Reputation and marketing

Primary factors in determining customer buying decisions in the jewellery sector include customer confidence in the retailer and the merchandise sold, together with the level and quality of customer service. The Group carries out quality control and staff training procedures and provides customer service facilities to help protect its reputation (see page 104116 for details of the processes by which the Group obtains an understanding of customer attitudes).

The ability to differentiate the Group’s stores from competitors by its branding, marketing and advertising programmes is a factor in attracting consumers. Therefore these programmes are carefully tested and their success monitored by methods such as market research (see pages 1214 and 1821 for more details).

The Diamond Trading Company (“DTC”), a subsidiary of De Beers Consolidated Mines Limited (“De Beers”), promotes diamonds and diamond jewellery in the US and the UK. The level of support provided by the DTC and the success of the promotions influence the size of the total jewellery market in those countries.

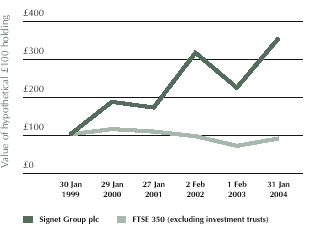

The Group’s reputation in the financial markets can influence the availability of capital, the cost of capital and the share price.

Staff

In speciality jewellery retailing, the level and quality of customer service is largely determined by the effectiveness of recruitment, training and retention of suitably qualified sales staff and this will help determine sales and profitability. The support provided to the Group’s store employees by staff at the divisional head offices and in the corporate functions will also influence the performance of the Group. Consequently the Group has in place comprehensive recruitment, training and incentive programmes, and employee attitude surveys (see pages 119 and 1718 for more details).

Store portfolio

The future growth of sales is partly dependent on the extent and results of the Group’s net space expansion and refurbishment strategy. The Group has followed a steady programme of space expansion and refurbishment and has established capital expenditure procedures with investment criteria set by the Board.

The projections used for investment decisions are reviewed and adjusted based on experience and economic conditions.

In particular, the success of the Jared off-mall destination store concept, which accounts for the majority of the Group’s net increase in new store space, will influence the future performance of the Group. This concept has been tested and developed over a number of years and its performance against the investment model is regularly reviewed. The rate of new store development is dependent on a number of factors including obtaining suitable real estate, the capital resources of the Group and the availability of appropriate staff and management.

The Group’s results are dependent on a number of factors relating to its stores. These include the availability of property, the location of the mall or shopping centre, the availability of attractive locations within a mall or high street,High Street, the terms of leases, agreedthe Group’s relationship with major landlords and the design and maintenance of the stores. In addition, the Group’s operations, particularly in the US, are dependent upon the continued popularity of malls as a shopping destination and the ability of malls, their tenants and other mall features to attract customers.

Competition

Competitive factors in the jewellery sector are discussed in the US and UK operating reviews (see pages 7 to 19)22).

If the Group falls behind competitors with respect to one or more of these factors, the Group’s operating results or financial condition could be adversely affected. In the US the Group has an estimated 7%7.2% market share of the speciality jewellery sector

| 36 | Signet Group plc Annual Report & Accounts year ended 29 January 2005 |

and has only one major national competitor. While another major national brand could develop, the sector is highly fragmented. In the UK the Group has an estimated 17% share of the total jewellery sector and has only limited scope to increase sales by opening new stores.

The channels through which consumers buy jewellery continually evolve and a major non-speciality retailer could enter the wider jewellery market. In the US, for example, sales by discount retailers have increased, while those of the department stores have been in relative decline and catalogue retailers have withdrawn from the market. In the UK a number of fashion and general retailers including a major supermarket chain, have introduced jewellery into their ranges whilst others have reduced their selection. In both the US and the UK, Internetinternet retailers sell jewellery and watches. The Group monitors the competitive environment and the development of possible new channels of distribution such as the Internet.internet. As part of this process there are marketing web sites for each of the Group’s major brands, and regular exercises to “shop the competition” take place.

Supply chain

During 2003/042004/05 the Group had one supplier that accounted for 8% of its merchandise. No other supplier accounted for more than 5%4% of its merchandise. Although the Group believes that alternative sources of supply are available, the abrupt loss of any significant supplier during the three month period (August to October) leading up to the Christmas season could result in a material adverse effect on the Group’s business. The Group is therefore in regular dialogue with suppliers and uses its merchandising systems to test and predict its future inventory needs.

Raw materials

The jewellery industry generally is affected by fluctuations in the price and supply of diamonds, gold and, to a lesser extent, other precious and semi-precious metals and stones. The Group undertakes some hedging of its requirement for gold through the use of options, forward contracts and outright commodity purchasing. It does not hedge against fluctuations in the cost of diamonds. The Group does hedge the exposure of the UK division to the US dollar with regard to diamond and other costs of goods sold. The cost of raw materials is only part of the costs involved in the retail selling price of jewellery with labour costs also being a significant factor.

Diamonds are the largest product category sold by the Group. The supply and price of diamonds in the principal world markets are significantly influenced by a single entity. The DTC (and its predecessor, the Central Selling Organisation) has for many years controlled the marketing of a substantial majority of the world’s

supply of rough diamonds and sells diamonds to diamond cutters in quantities and at prices determined at its sole discretion. In 2000 De Beers announced a change in corporate strategy designed to improve the efficiency of the supply chain and increase the level of marketing support for diamonds.

The availability of diamonds to the DTC and the Group’s suppliers is to some extent dependent on the political situation in diamond producing countries. Until alternative sources can be developed, any sustained interruption in the supply of diamonds from the significant producing countries could adversely affect the Group and the retail jewellery industry as a whole.

Consumer confidence in diamonds, gold and other metals and gemstones also influences the level of Group sales. Confidence could be affected by a variety of issues including the availability and consumer awareness of substitute products such as cubic zirconium,zirconia, moisanite and the development of syntheticlaboratory created diamonds; labour conditions in the supply chain; and concern over the source of raw materials. The Group, therefore, has a Supplier Code of Conduct which sets out the Group’s expectations of its suppliers.

An example of an issue that could affect confidence in this way is that of conflict diamonds, which is the term used for diamonds sold by rebel movements to raise funds for military campaigns. There have been a number of United Nations resolutions regarding conflict diamonds and an international agreement, known as the Kimberley Process, was signed in November 2002. This was designed to exclude conflict diamonds from the legitimate diamond trade. During 2003 legislation was passed, in the European Union and the US, implementing the Kimberley Process. The impact of the Kimberley Process and its associated legislation has not resulted in any disruption to the supply of rough diamonds to date and has helped to improve the integrity of the supply chain.

The Group reviewedreviews its procedures and documentation for compliance with the Kimberley Process and mademakes appropriate amendments. In addition, staff wereare briefed and suppliers have been contactedreminded about the changes.procedures. During the year the Group’s internal audit function checkedand mystery shopper programmes check for compliance with the new procedures.compliance. See page 104116 for further information on the Supplier Code of Conduct, the Kimberley Process and the Group’s policy on conflict diamonds.

Seasonality

The Group’s business is highly seasonal, with a very significant proportion of its sales and operating profit generated during its fourth quarter, which includes the Christmas season. The Group expects to continue to experience a seasonal fluctuation in its sales and profit. Therefore the Group has limited ability to compensate for shortfalls in fourth quarter sales or earnings by

| Signet Group plc Annual Report & Accounts year ended 29 January 2005 | 37 |

Risk and other factors (continued)

changes in its operations and strategies in other quarters, or to recover from any extensive disruption, for example due to inclement weather conditions. A significant shortfall in results for the fourth quarter of any financial year would thus be expected to have a material adverse effect on the Group’s annual results of operations. However, due to the limited seasonality in the product mix, the risk of having to discount inventory in order to be correctly stocked for the next selling season is more limited than for some other retail sectors. Disruption at more minor peaks in sales at Valentine’s Day and Mothers’ Day would impact the results of the Group to a lesser extent.

Social, ethical and environmental risks

Social, ethical and environmental (“SEE”) matters influence the Group’s reputation, demand for merchandise by consumers, the ability to recruit staff, relations with suppliers and standing in the financial markets. Signet, therefore, is committed to managing the SEE risks and responsibilities facing the Group. This commitment stems from the understanding that Signet’s success is dependent on the strength and effectiveness of its relationships with its various stakeholders: shareholders, customers, employees and suppliers.

Risk and other factors (continued)

In recent years stakeholder expectations of public companies have increased. Managing and responding as a business to these changing expectations, including with regard to SEE issues, is part of the normal responsibilities of corporate management.

The Group regularly carries out SEE risk reviews and benchmarking exercises with the assistance of an external adviser. Such reviews include an assessment of Group policies, procedures and controls in respect of SEE matters. Reports are regularly made to the Group’s Risk Committee and to the Board. The greatest SEE risks are judged to relate to the integrity of the merchandise and to the SEE standards in the Group’s supply chain.

On 21 October 2001 the Association of British Insurers published guidelines on Socially Responsible Investment. In line with that guidance the Board confirms that they haveit has identified and assessed the Group’s SEE risks and that these are being managed.

SEE matters are dealt with in more detail on pages 103115 to 106119 and in the corporate social responsibility section on www.signetgroupplc.comwww.signetgroupplc.com..

Systems

The Group is dependent on the suitability and reliability of its systems and procedures, including its information technology, warehousing and distribution systems. The Group has emergency procedures and carries out rehearsals to test them.which are regularly tested. The Group carries out evaluation, planning and implementation analysis before

updating or introducing new systems that have an impact on a function critical to the Group.

Regulatory requirements

Regulations govern various areas of business activity and changes in regulations can therefore influence the Group’s performance. For example in the US approximately 50% of sales utilise the Group’s in-house credit programmes therefore any change in the regulations or application of regulations relating to the provision of credit and associated services could affect the Group’s results.

The presentation of the Group’s accounts can also be affected by changes to generally accepted accounting policies, such as the adoption of International Accounting Standards for 2005/06 (see pages 33 to 34 for details). Such changes may influence the valuation of the Group’s shares.

Acquisitions

The Group may in the future make acquisitions and any difficulty integrating an acquisition may result in expected returns and other projected benefits from the acquisition not being realised. A significant acquisition could also disrupt the operation of the Group’s current activities. The Group’s growth strategy does not depend on acquisitions and an acquisition would be intended to accelerate the implementation of that strategy.

Pensions

In the UK the Group operates a defined benefit pension scheme. This Group Scheme was closed to new employees in 2004/05. The valuation of the Group Scheme’s assets and liabilities partly depends on assumptions based on the financial markets as well as longevity rates and staff retention rates. Funding requirements and the profit and loss items relating to this Group Scheme are also influenced by financial market factors. At 29 January 2005 there was a net pension liability of £1.3 million compared with a net asset of £1.2 million at the prior year end (see pages 87 to 89 for more details). In the UK the Group introduced a defined contribution plan which replaced the Group Scheme for new employees. The US also operate a defined contribution plan.

Equity and debt financing

The Group is dependent upon the availability of equity and debt financing to fund its operations and growth. Therefore it prepares annual budgets, medium term plans and headroom models which help to identify the future capital requirements so that appropriate facilities can be put in place on a timely basis. If these models are inaccurate adequate facilities may not be available.

| 38 | Signet Group plc Annual Report & Accounts year ended 29 January 2005 |

Financial market risks

The Group publishes its consolidated annual accounts in pounds sterling. The Group held approximately 64%65% of its total assets in US dollars at 3129 January 20042005 and generated approximately 69%68% of its sales and 68% of its operating profit in US dollars for the financial year then ended. Thus, although the Group’s US operations make substantially all of their sales and incur substantially all of their expenses in US dollars, in translating the results of its US operations, the Group’s results are subject to fluctuations in the exchange rate between the pound sterling and the US dollar. Accordingly, depreciation in the weighted average value of the US dollar against the pound sterling could

decrease reported revenues and operating profit (as was the case in 2002/03, 2003/04 and 2003/04)2004/05), and appreciation in the weighted average value of the US dollar against the pound sterling could increase reported revenues and operating profit (as was the case in 1999/00, 2000/01 and 2001/02). The Board has chosen not to hedge the translation effect of exchange rate movements on the results of the Group given that there is little movement of cash between the Group’s two divisions.

As part of its long-term strategy, the Group seeks to finance its US net assets with borrowings denominated in US dollars as a hedge against the impact of exchange rate fluctuations on its US operating profit. Currently nearly all of the Group’s borrowings are denominated in US dollars. Therefore fluctuations in the exchange rate between the pound sterling and the US dollar affect the amount of the Group’s consolidated borrowings.

In addition, the prices of materials and certain products bought on the international markets by the UK division are denominated in US dollars, and therefore the Group has an exposure to exchange rates on the cost of goods sold which will have an opposite effect to its exposure on US operating profit. The Group does use hedging operations in respect of purchases of US dollars by its UK operating division, within the treasury guidelines approved by the Group’s Board.

Cash dividends paid by the Group in respect of the shares will be in pounds sterling and fluctuations in the exchange rate between the pound sterling and the US dollar will affect the dollar amount received by holders of ADSs upon conversion of such dividends. Moreover, fluctuations in the exchange rate between the pound sterling and the US dollar will affect the US dollar equivalents of the pound sterling price of the shares on the London Stock Exchange and, as a result, are likely to affect the market price of the ADSs in the US.

The table on page 33overleaf sets out, for the calendar years indicated, the average, high, low and period end exchange rates for the pound sterling expressed in US dollars per £1.

The Group’s policy is to manage financial risk resulting from exposure to currency and interest rate fluctuations. Translation exposure relating to non-pound sterling denominated assets in the US is partially hedged by borrowing in US dollars. Interest rate exposure is managed through the use of swaps, caps and floors.

A committee of the Board is responsible for the implementation of treasury policies and guidelines which are considered to be

Exchange rates between pound sterling and the US dollar(1)

| At period | ||||||||

| Average | High | Low | end | |||||

| Calendar year | ||||||||

| 1999 | 1.62 | 1.68 | 1.55 | 1.62 | ||||

| 2000 | 1.51 | 1.65 | 1.40 | 1.50 | ||||

| 2001 | 1.44 | 1.50 | 1.38 | 1.45 | ||||

| 2002 | 1.51 | 1.61 | 1.41 | 1.61 | ||||

| 2003 | 1.62 | 1.79 | 1.55 | 1.77 | ||||

| 2004 (cumulative to 24 March) | 1.81 | 1.91 | 1.78 | 1.84 | ||||

| Month | ||||||||

| September 2003 | 1.60 | 1.66 | 1.56 | 1.66 | ||||

| October 2003 | 1.67 | 1.71 | 1.65 | 1.70 | ||||

| November 2003 | 1.69 | 1.72 | 1.65 | 1.72 | ||||

| December 2003 | 1.74 | 1.79 | 1.72 | 1.77 | ||||

| January 2004 | 1.81 | 1.86 | 1.78 | 1.82 | ||||

| February 2004 | 1.85 | 1.91 | 1.81 | 1.87 | ||||

appropriate by the Board for the management of financial risk. The Group’s funding, liquidity and exposure to interest rate and exchange rate risks are managed by the Group’s treasury department. The Group uses derivative instruments for risk management purposes only, and these are transacted by specialist treasury personnel.

For financial instruments held, the Group has used a sensitivity analysis technique that measures the change in the fair value of the Group’s financial instruments from hypothetical changes in market rates and this is shown in the table below.overleaf.

The amounts generated from the sensitivity analysis are forward-looking estimates of market risk assuming certain adverse market conditions occur. Actual results in the future may differ materially from those projected due to changes in the portfolio of financial instruments held and actual developments in the global financial markets. These may cause fluctuations in interest and exchange rates to exceed the hypothetical amounts disclosed in the table below.overleaf.

| Signet Group plc Annual Report & Accounts year ended 29 January 2005 | 39 |

The analysis below should not be considered a projection of likely future events.Back to Contents

Risk and other factors (continued)

Exchange rates between the pound sterling and the US dollar(1)

| Average | High | Low | At period end | |||||

| Calendar year | ||||||||

| 2000 | 1.51 | 1.65 | 1.40 | 1.50 | ||||

| 2001 | 1.44 | 1.50 | 1.38 | 1.45 | ||||

| 2002 | 1.51 | 1.61 | 1.41 | 1.61 | ||||

| 2003 | 1.62 | 1.79 | 1.55 | 1.77 | ||||

| 2004 | 1.79 | 1.96 | 1.75 | 1.92 | ||||

| 2005 (cumulative to 6 April) | 1.90 | 1.93 | 1.85 | 1.88 | ||||

| Month | ||||||||

| September 2004 | 1.80 | 1.82 | 1.77 | 1.81 | ||||

| October 2004 | 1.81 | 1.84 | 1.77 | 1.84 | ||||

| November 2004 | 1.85 | 1.90 | 1.84 | 1.91 | ||||

| December 2004 | 1.92 | 1.96 | 1.90 | 1.92 | ||||

| January 2005 | 1.89 | 1.89 | 1.85 | 1.88 | ||||

| February 2005 | 1.88 | 1.93 | 1.85 | 1.92 | ||||

| March 2005 | 1.90 | 1.93 | 1.85 | 1.89 | ||||

| (1) | Based on unweighted data points sourced from Reuters. |

The example shown for changes in the fair values of borrowings and associated derivative financial instruments at 3129 January 20042005 is set out in the table below. The fair values of borrowings and derivative financial instruments are estimated by discounting the future cash flows to net present values using appropriate market rates prevailing at the period end.

The estimated changes in fair values for interest rate movements

Fair value changes arising from:

are based on an instantaneous decrease of 1% (100 basis points) in the specific rate of interest applicable to each class of financial instruments from the levels effective at 3129 January 20042005 with all other variables remaining constant. The estimated changes in the fair value for foreign exchange rates are based on an instantaneous 10% weakening of the pound sterling against the US dollar from the levels applicable at 3129 January 20042005 with all other variables remaining constant.

| Estimated fair | 10% weakening | Estimated fair | ||||||

| value at | 1% decrease in | in £ against $ | value at | |||||

| 29 January | interest rates | favourable/ | 31 January | |||||

| 2005 | (unfavourable) | (unfavourable) | 2004 | |||||

| £m | £m | £m | £m | |||||

| Borrowings | (180.3 | ) | (2.4 | ) | (20.1 | ) | (207.9 | ) |

| Foreign currency receivable | 319.0 | – | (35.4 | ) | 292.6 | |||

| Foreign exchange contracts | (0.8 | ) | – | 1.3 | (2.9 | ) | ||

| Commodity hedging contracts | – | – | – | (2.1 | ) | |||

| Fair value changes arising from: | 10% | |||||||

| Estimated | 1% | weakening in | Estimated | |||||

| fair value at | decrease in | £ against $ | fair value at | |||||

| 31 January | interest rates | favourable/ | 1 February | |||||

| 2004 | (unfavourable) | (unfavourable) | 2003 | |||||

| £m | £m | £m | £m | |||||

| Borrowings | (207.9 | ) | (6.8 | ) | (17.2 | ) | (229.4 | ) |

| Foreign currency receivable | 292.9 | – | 32.5 | 299.2 | ||||

| Foreign exchange contracts | (2.9 | ) | – | 4.1 | (1.4 | ) | ||

| Commodity hedging contracts | (2.1 | ) | – | (2.1 | ) | – | ||

The analysis above should not be considered a projection of likely future events.

| 40 | Signet Group plc Annual Report & Accounts year ended |

Directors, officers and advisers

Directors

James McAdam CBE, 73,74, Chairman, appointed in 1992. He was also Group Chief Executive from 1992 until March 2000. From 31 March 2001, while continuing as Chairman, he ceased to be a full-time executive. Mr. McAdam is the non-executive Chairman of Bisley Office Equipment Company Limited, Chairman of the British Clothing Industry Association Limited and Chairman of the British Apparel & Textile Confederation; he devotes approximately 25% of his time to these roles collectively.latter roles. Mr. McAdam has indicated his intention to retire from the Board no later than at the conclusion of the annual general meeting in 2006.

Robert Anderson, 46, appointed in April 2005 (after completion of the period under review). He was appointed Chief Executive of the Group’s UK division in January 2003 having joined the Group as Chief Operating Officer of the UK division in August 2000. Prior to joining the Group Mr. Anderson had worked at Marks & Spencer Plc for 19 years, latterly as Business Unit Director.

Robert Blanchard*, 59,60, appointed in 2000. He was a Group Vice President of Procter & Gamble and President of its Global Skin Care and Cosmetics business until his retirement in 1999. He is a non-executive director of Bandag Inc. and is a non-executive director of Best Buy Co. Inc. and Bandag Inc. Mr. Blanchard also serves as President of Strategic and Marketing Services, a consulting companyalthough he founded uponhas indicated his retirementintention to retire from Procter & Gamble.that board in June 2005.

Walker Boyd, 51,52, appointed Group Finance Director in 1995. He is a member of the Institute of Chartered Accountants of Scotland. From 1992 he was Finance Director of the Group’s UK division. Mr. Boyd was appointed a non-executive director of WH Smith PLC in March 2004.2004 but resigned in January 2005 in order to meet good corporate governance requirements on the appointment of Robert Walker as Chairman of WH Smith PLC.

Terry Burman, 58,59, appointed Group Chief Executive in March 2000. He is also Chief Executive Officer of the Group’s US division. Mr. Burman was appointed to the Board in 1996. Prior to joining the Group in 1995 he was Chief Executive Officer of Barry’s Jewelers, Inc.

Dale Hilpert*, 62, appointed in 2003. He was Chief Executive of Williams-Sonoma, Inc. from April 2001 until his retirement in January 2003. Prior to this he was Chairman and Chief Executive of Foot Locker, Inc. (formerly the Venator Group, Inc.) which he joined as President and Chief Operating Officer in 1995.

| * | Non-executive directors, all of whom satisfied the definitions of independence in the revised Combined Code (“the Combined Code”) and are viewed as independent by the Board. |