UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

[ ]

| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) |

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year endedDecember 31 2017, 2021

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to ______________________

OR

[ ] SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report _________________________

Commission file number:001-35722

CHINA INFORMATION TECHNOLOGY,

TAOPING INC.

(Exact Name of Registrant as Specified in Its Charter)

Not Applicable

(Translation of Registrant’s Name Into English)

British Virgin Islands

(Jurisdiction of Incorporation or Organization)

21st Floor, Everbright Bank Building

Zhuzilin, Futian District

Unit 3102, 31/F, Citicorp Centre

Shenzhen, Guangdong 518040

18 Whitefield Road, Hong KongPeople’s Republic of China

(Address of Principal Executive Offices)

Mr. Jianghuai Lin, Chief Executive Officer21st Floor, Everbright Bank Building

Zhuzilin, Futian District

Unit 3102, 31/F, Citicorp Centre

Shenzhen, Guangdong 518040

18 Whitefield Road, Hong Kong

People’s Republic of China

Tel: +86-755-88319888

+852-36117837

Fax: + 86-755-83709333

852-36166449

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange On Which Registered | ||

| Ordinary Shares, no par value | TAOP | NASDAQ Capital Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report (December 31, 2017)2021): 40,231,159 ordinary shares, no par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] ☐ No [X] ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes [ ] ☐ No [X] ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] ☒ No [ ]☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [X] ☒ No [ ]☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer.filer, or an emerging growth company. See definition of “large accelerated filer, “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer ☐ | Accelerated Filer | Non-Accelerated Filer | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards†standards provided pursuant to Section 13(a) of the Exchange Act. [ ]☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP | International Financial Reporting | Other | ||

| Standards as issued by the International | ||||

| Accounting Standards Board |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.[ ] ☐ Item 17 [ ]☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] ☐ No [X] ☒

Annual Report on Form 20-F

Year Ended December 31, 2021

TABLE OF CONTENTS

i

ii

| ii |

INTRODUCTORY NOTES

Use of Certain Defined Terms

Except as otherwise indicated by the context and for the purposes of this report only, references in this report to:

“ | ||

| ● | “We,” “us,” “our” and | |

| “ | ||

| “ | ||

| “TopCloud” are to TopCloud Software Co., Ltd., a PRC company; | ||

| “IST” are to Information Security | ||

| “ISIOT” are to Information Security IoT | ||

| “iASPEC” are to iASPEC | ||

| “Geo” are to Wuda Geoinformatics Co., Ltd., a PRC company; | ||

| “Biznest” are to Biznest Internet Technology Co., Ltd., a PRC company; | ||

| “Bocom” are to iASPEC Bocom IoT Technology Co. Ltd., a PRC company; | ||

| “BVI” are to the British Virgin Islands; | ||

| “Hong Kong” are to the Hong Kong Special Administrative Region of the People’s Republic of China; | ||

| “PRC” and “China” are to the People’s Republic of China; | ||

| “SEC” are to the Securities and Exchange Commission; | ||

| “Exchange Act” are to the Securities Exchange Act of 1934, as amended; | ||

| “Securities Act” are to the Securities Act of 1933, as amended; | ||

| “Renminbi” and “RMB” are to the legal currency of China; and | ||

| “U.S. dollars,” “dollars” and “$” are to the legal currency of the United States. |

On July 30, 2020, we completed a share combination of the Company’s ordinary shares at a ratio of one-for-six, which decreased the Company’s outstanding ordinary shares to approximately 7,332,434 shares. This share combination did not change the Company’s authorized amount of shares or the par value of the Company’s ordinary shares. Accordingly, except as otherwise indicated, all share and per share information contained in this annual report has been restated to retroactively show the effect of the share combination.

Forward-Looking Information

In addition to historical information, this annual report contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. We use words such as “believe,” “expect,” “anticipate,” “project,” “target,” “plan,” “optimistic,” “intend,” “aim,” “will” or similar expressions which are intended to identify forward-looking statements. Such statements include, among others, those concerning market and industry segment growth and demand and acceptance of new and existing products; any projections of sales, earnings, revenue, margins or other financial items; any statements of the plans, strategies and objectives of management for future operations; and any statements regarding future economic conditions or performance, as well as all assumptions, expectations, predictions, intentions or beliefs about future events. You are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, as well as assumptions, which, if they were to ever materialize or prove incorrect, could cause the results of the Company to differ materially from those expressed or implied by such forward-looking statements. Potential risks and uncertainties include, among other things, the possibility that third parties hold proprietary rights that preclude us from marketing our products, the emergence of additional competing technologies, changes in domestic and foreign laws, regulations and taxes, changes in economic conditions, uncertainties related to legal system and economic, political and social events in China, a general economic downturn, a downturn in the securities markets, and other risks and uncertainties which are generally set forth under Item 3 “Key information—D. Risk Factors” and elsewhere in this annual report.

Readers are urged to carefully review and consider the various disclosures made by us in this report and our other filings with the SEC. These reports attempt to advise interested parties of the risks and factors that may affect our business, financial condition and results of operations and prospects. The forward-looking statements made in this report speak only as of the date hereof and we disclaim any obligation, except as required by law, to provide updates, revisions or amendments to any forward-looking statements to reflect changes in our expectations or future events.

1

| 1 |

PART I

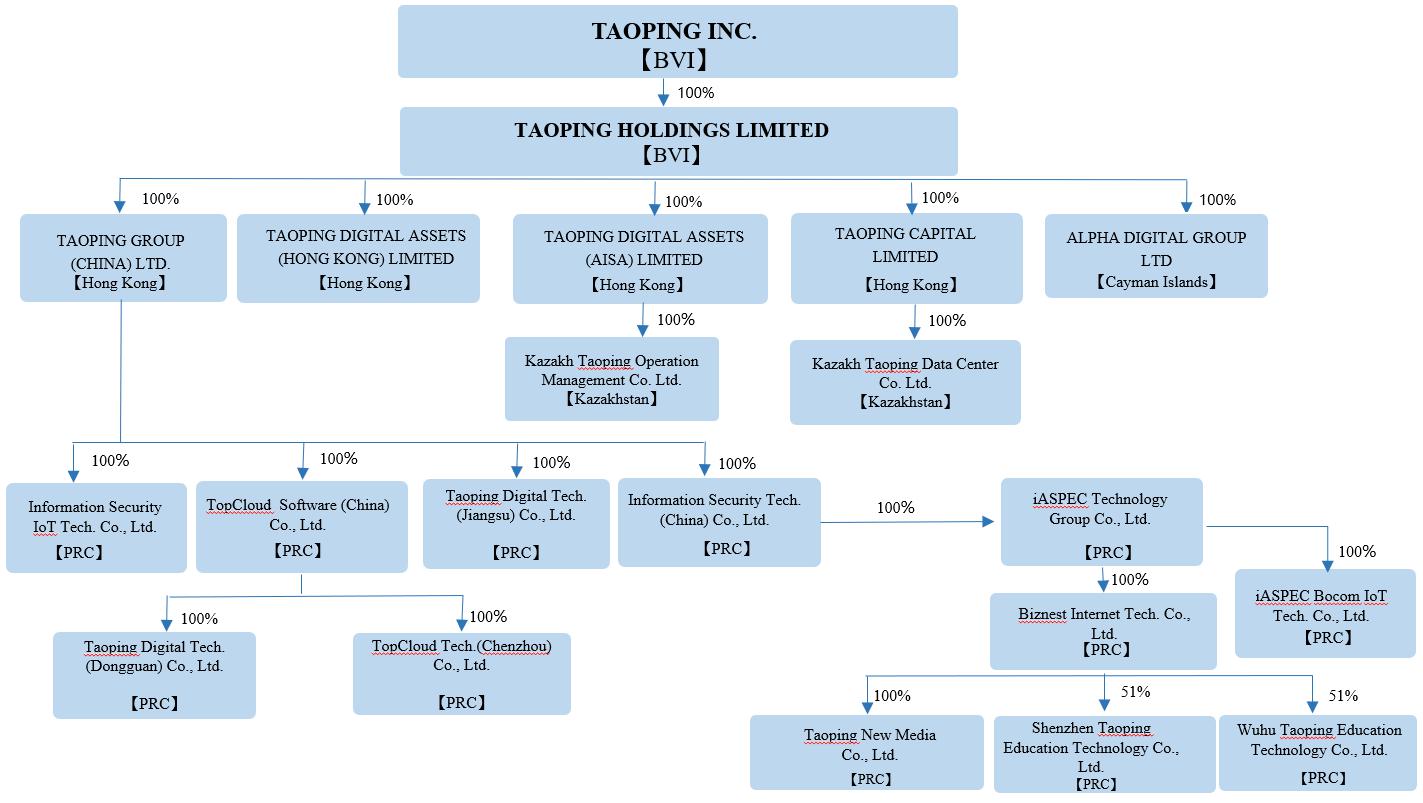

Taoping is not an operating company but rather a holding company incorporated in the British Virgin Islands. Because Taoping has no business operations of its own, we conduct our business through Taoping’s operating subsidiaries, primarily in Hong Kong, mainland China and Kazakhstan. This structure involves unique risks to investors and you may never directly hold equity interests in Taoping’s operating entities. You are specifically cautioned that there are significant legal and operational risks associated with being based in or having the majority of operations in China, including that changes in the legal, political and economic policies of the Chinese government, the relations between China and the United States, or Chinese or United States regulations may materially and adversely affect our business, financial condition, results of operations and the market price of the Company’s securities. Moreover, the Chinese government may exercise significant oversight and discretion over the conduct of our business and may intervene in or influence our operations at any time, which could result in a material change in our operations and/or the value of the securities we are registering for sale or could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. For a detailed description of risks related to the holding corporate structure, • see Item 3 “Key Information—D. Risk Factors—Risks Related to Doing Business in China”.

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

A. Directors and Senior Management

Not applicable.

B. Advisors

Not applicable.

C. Auditors

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

A. Offer Statistics

Not applicable.

B. Method and Expected Timetable

Not applicable.

ITEM 3. KEY INFORMATION

Taoping was incorporated in the British Virgin Islands under the BVI Act on June 18, 2012. Taoping is not an operating company but rather a holding company conducting its operations through Taoping’s operating subsidiaries, primarily in Hong Kong, mainland China and Kazakhstan. This structure involves unique risks to investors and you may never directly hold equity interests in Taoping’s operating entities. You are specifically cautioned that there are significant legal and operational risks associated with being based in or having the majority of operations in China. Specifically, the PRC government recently initiated a series of regulatory actions and made a number of public statements on the regulation of business operations in China, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using a variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding efforts in anti-monopoly enforcement. We do not believe that our subsidiaries in Hong Kong or mainland China are directly subject to these regulatory actions or statements, as we have not carried out any monopolistic behavior and our business does not involve the collection of personal information or implicate national security. We also have dissolved the variable interest entity structure in 2021 as our business does not involve any type of restricted industry. However, since these statements and regulatory actions by the PRC government are newly published and detailed official guidance and related implementation rules have not been issued or taken effect, uncertainties exist as to how soon the regulatory bodies in China will finalize implementation measures, and the impacts the modified or new laws and regulations will have on our daily business operation, the ability to accept foreign investments and list the Company’s securities on an U.S. or other foreign exchange. For a detailed description of various risks related to doing business in China, see Item 3 “Key Information—D. Risk Factors—Risks Related to Doing Business in China”.

| 2 |

In addition, pursuant to the Holding Foreign Companies Accountable Act (the “HFCA Act”) enacted in 2020, if the auditor of a U.S. listed company’s financial statements is not subject to Public Company Accounting Oversight Board (the “PCAOB”) inspections for three consecutive “non-inspection” years, the Securities and Exchange Commission (the “SEC”) is required to prohibit the securities of such issuer from being traded on a U.S. national securities exchange, such as NYSE and Nasdaq, or in U.S. over-the-counter markets. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which if enacted into law would amend the HFCA Act and require the SEC to prohibit an issuer’s securities from trading on U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive “non-inspection” years instead of three. The PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong because of a position taken by one or more authorities in such jurisdictions. In addition, the PCAOB’s report identified specific registered public accounting firms which are subject to these determinations. Our current registered public accounting firm, PKF Littlejohn LLP (“PKF”), or our former registered public accounting firm, UHY LLP, is not headquartered in mainland China or Hong Kong and was not identified in this report as a firm subject to the PCAOB’s determination. They both are subject to full inspection by the PCAOB and the PCAOB is able to inspect the audit workpapers of our China subsidiaries, as such workpapers are electronic files possessed by our registered public accounting firms. However, if the PCAOB determines in the future that it cannot inspect or fully investigate our auditor at such future time, trading in the Company’s securities would be prohibited under the HFCA Act. See “Risk Factor—Risks Related to Doing Business in China— The increased regulatory scrutiny focusing on U.S.-listed companies with significant operations in China in the U.S. could add uncertainties to our business operations, share price and reputation. Although our former auditor, UHY LLP, and current auditor, PKF, are both subject to inspection by the PCAOB, trading in the Company’s securities may be prohibited under the Holding Foreign Companies Accountable Act if the PCAOB subsequently determines our audit work is performed by auditors that the PCAOB is unable to inspect or investigate completely, and as a result, U.S. national securities exchanges, such as the Nasdaq, may determine to delist the Company’s securities. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which, if enacted, would amend the HFCA Act and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to the PCAOB inspections for two consecutive years instead of three.”

Cash is transferred through our organization in the following manner:

| Our equity structure is a direct holding structure, that is, Taoping, the British Virgin Islands entity listed in the U.S., controls its operating subsidiaries in Hong Kong, mainland China and Kazakhstan, through Taoping Holdings, a British Virgin Islands subsidiary of Taoping. See Item 4. “Information of the Company – A. History and Development of the Company – Corporate Structure” for more details. | ||

| ● | As of the date of this report, neither Taoping nor any of its subsidiaries have paid dividends or made distributions to U.S. investors. |

A. Selected Financial Data

The following table presents selected financial data

| ● | Within our direct holding structure, the cross-border transfer of funds from Taoping to its Chinese subsidiaries is legal and compliant with the laws and regulations of China. Taoping is permitted to provide funding to its subsidiaries in mainland China in the form of shareholder loans or capital contributions, subject to satisfaction of applicable government registration, approval and filing requirements of the respective jurisdiction. There are no quantity limits on Taoping’s ability to make capital contributions to its subsidiaries in mainland China under the PRC regulations. Historically, cash proceeds raised from overseas financing activities by Taoping have been first transferred to its BVI subsidiary, Taoping Holdings. Whenever we need to make capital contributions to either of our PRC subsidiaries by contributing any of such net proceeds, and convert the contributed proceeds into RMB, we will need to increase the PRC subsidiary’s registered capital by registering and/or filing the increase with the Ministry of Commerce or one of its local branches, the State Administration of Foreign Exchange (“SAFE”) or one of its local branches, or an authorized bank. If we transfer any of the proceeds to one of our PRC subsidiaries through loans, under current PRC law we will also need to register such loans with the SAFE or one of its local branches, and the amount that we may convert into RMB and loan to one of these entities will be limited by applicable SAFE regulations, in the case of a loan to one of our PRC subsidiaries, to the greater of (i) the difference between the subsidiary’s approved total investment and the subsidiary’s total registered capital and (ii) two times the PRC subsidiary’s net assets. |

| 3 |

| ● | As a holding company, Taoping relies on dividends and other distributions on equity paid by its operating subsidiaries in Hong Kong, mainland China and Kazakhstan for cash requirements, including the funds necessary to pay dividends and other cash distributions to its shareholders or to any service expenses it may incur. For operating subsidiaries in mainland China, they will first transfer funds to Taoping Group in accordance with applicable laws and regulations of Hong Kong and mainland China, and then to Taoping through Taoping Holdings. Taoping will then distribute dividends to its shareholders in proportion to their respective shareholding, regardless of whether the shareholders are U.S. investors or investors in other countries or regions. As of the date of this report, none of our subsidiaries has made any transfers, dividends or other distributions to Taoping, the holding company. We intend to retain most, if not all, of our available funds and any future earnings to the development and growth of our business in China and do not expect to pay dividends in the foreseeable future. | |

| ● | The ability of our subsidiaries in mainland China to distribute dividends is based upon their distributable earnings. Current PRC regulations permit these subsidiaries to pay dividends to their respective shareholders only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, each of our subsidiaries in mainland China is required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. These reserves are not distributable as cash dividends. In addition, if any of our operating subsidiaries incurs debt on its own behalf in the future, the instruments governing such debt may restrict its ability to pay dividends to Taoping. We believe, other than above, current PRC regulations do not prohibit or limit using cash generated from one subsidiary to fund another subsidiary’s operations. We currently do not have our own cash management policy and procedures that dictate how funds are transferred. |

Summary of Risk Factors

There are a number of risks that you should consider and understand before making an investment decision regarding our business. Itthe Company’s securities. You should be read in conjunction with our consolidated financial statements and related notes contained elsewherecarefully consider all of the information set forth in this annual report and, in particular, the information under Item 5 “Operating and Financial Review and Prospects.” The selected consolidated statement of income (loss) data for the fiscal years ended December 31, 2017, 2016, and 2015, and the selected consolidated balance sheet data as of December 31, 2017 and 2016 have been derived from our audited consolidated financial statements that are included in this annual report beginning on page F-1. The selected consolidated statement of income (loss) data for the fiscal years ended December 31, 2014 and 2013, and the selected consolidated balance sheet data as of December 31, 2015, 2014 and 2013 have been derived from our audited consolidated financial statements that are not included in this annual report.

Our consolidated financial statements are prepared and presented in accordance with generally accepted accounting principles in the United States, or U.S. GAAP. The selected financial data information is only a summary and should be read in conjunction with the historical consolidated financial statements and related notes contained elsewhere herein. The financial statements contained elsewhere fully represent our financial condition and operations; however, they are not indicative of our future performance.

| Years Ended December 31, | ||||||||||||||

| 2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||

Statement of Income Data | |||||||||||||||

Total revenue | $ | 18,189,274 | $ | 10,193,590 | $ | 10,284,868 | $ | 38,634,747 | $ | 55,419,831 | |||||

Total cost of revenue | $ | 9,867,508 | $ | 7,607,190 | $ | 6,381,205 | $ | 28,146,390 | $ | 45,867,163 | |||||

Gross profit | $ | 8,321,766 | $ | 2,586,400 | $ | 3,903,663 | $ | 10,488,357 | $ | 9,552,668 | |||||

(Loss) income from operations | $ | (450,703 | ) | $ | (14,577,928 | ) | $ | (26,963,357 | ) | $ | (23,909,213 | ) | $ | (118,215,368 | ) |

Net income (loss) attributable to CNIT- continuing operations | $ | 858,605 | $ | (18,170,601 | ) | $ | (7,504,262 | ) | $ | (24,087,098 | ) | $ | (118,511,760 | ) | |

Net income (loss) per share-continuing operations - basic | $ | 0.02 | $ | (0.45 | ) | $ | (0.26 | ) | $ | (0.79 | ) | $ | (4.33 | ) | |

Net income (loss) per share-continuing operations - diluted | $ | 0.02 | $ | (0.45 | ) | $ | (0.26 | ) | $ | (0.79 | ) | $ | (4.33 | ) | |

Balance Sheet Data | |||||||||||||||

Cash and cash equivalents | $ | 3,260,808 | $ | 3,752,375 | $ | 3,786,846 | $ | 6,689,848 | $ | 6,044,692 | |||||

Working (deficiency) capital | $ | (1,494,326 | ) | $ | (5,739,129 | ) | $ | (1,649,728 | ) | $ | (56,043,116 | ) | $ | (46,779,407 | ) |

Total assets | $ | 37,639,430 | $ | 34,286,999 | $ | 66,091,704 | $ | 179,405,809 | $ | 189,238,990 | |||||

Total liabilities | $ | 23,121,938 | $ | 21,484,751 | $ | 35,637,467 | $ | 140,827,000 | $ | 129,059,540 | |||||

Temporary equity | $ | - | $ | - | $ | 360,000 | $ | 1,425,000 | $ | 2,175,000 | |||||

Total equity | $ | 14,517,492 | $ | 12,802,248 | $ | 30,094,237 | $ | 37,153,809 | $ | 58,004,450 | |||||

2

Exchange Rate Information

Our business is primarily conducted in China and almost all of our revenues are denominated in RMB. This annual report contains translations of RMB amounts into U.S. dollars at specific rates solely for the convenience of the reader. Unless otherwise noted, all translations from RMB to U.S. dollars and from U.S. dollars to RMB in this annual report were made at a rate of RMB6.5063 to US$1.00, the exchange ratefactors set forth in the H.10 statistical release of the Board of Governors of the Federal Reserve System on December 30, 2017. We make no representation that any RMB or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or RMB, as the case may be, at any particular rate, the rates stated below, or at all. The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of RMB into foreign exchange and through restrictions on foreign trade. On March 23, 2018, the certified exchange rate was RMB6.3110 to US$1.00.

The following table sets forth information concerning exchange rates between the RMB and the U.S. dollar for the periods indicated.section titled “Risk Factors” below. These rates are provided solely for your convenience andrisks include, but are not necessarily the exchange rates that we used in this annual report or will use in the preparation of any other periodic reports or any other information to be provided to you. The source of these rates is the Federal Reserve Statistical Release.limited to:

| Exchange rate | ||||||||||||

Period | Period End | Average(1) | Low | High | |||||||||

| (RMB Per US$1.00) | ||||||||||||

2013 | 6.0537 | 6.1478 | 6.0537 | 6.2438 | |||||||||

2014 | 6.2046 | 6.1620 | 6.0402 | 6.2591 | |||||||||

2015 | 6.4778 | 6.2827 | 6.1870 | 6.4896 | |||||||||

2016 | 6.9430 | 6.6549 | 6.4480 | 6.9580 | |||||||||

2017 | 6.5063 | 6.7350 | 6.4773 | 6.9575 | |||||||||

September | 6.6533 | 6.5690 | 6.4773 | 6.6591 | |||||||||

October | 6.6328 | 6.6254 | 6.5712 | 6.6533 | |||||||||

November | 6.6090 | 6.6200 | 6.5967 | 6.6385 | |||||||||

December | 6.5063 | 6.5932 | 6.5063 | 6.6210 | |||||||||

2018 | |||||||||||||

January | 6.2841 | 6.4233 | 6.2841 | 6.5263 | |||||||||

February | 6.3280 | 6.3183 | 6.2649 | 6.3471 | |||||||||

March (through March 23, 2018) | 6.3110 | 6.3283 | 6.3093 | 6.3491 | |||||||||

_________________________Source: Federal Reserve Statistical Release

| As of the |

| 4 |

| ● | There are significant legal and operational risks associated with having significant business operations in China, including that changes in the legal, political and economic policies of the Chinese government, the relations between China and the United States, or Chinese or United States regulations may materially and adversely affect our business, financial condition, results of operations and the value of the Company’s securities. Any such changes may take place quickly and with very little notice and as a result, could significantly limit or completely hinder our ability to offer or continue to offer Taoping’s securities to investors, and could cause the value of Taoping’s securities to significantly decline or become worthless. Recent statements made and regulatory actions undertaken by China’s government, such as those related to data security or anti-monopoly concerns and any other future laws and regulations may require us to incur significant expenses and could materially affect our ability to conduct our business or accept foreign investments. | |

| ● | The increased regulatory scrutiny focusing on U.S.-listed companies with significant operations in China in the U.S. could add uncertainties to our business operations, share price and reputation. In recent years, as part of increased regulatory focus in the United States on access to audit information, the United States enacted the HFCA Act in December 2020. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which, if enacted, would amend the HFCA Act and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to the PCAOB inspections for two consecutive years instead of three. Pursuant to the HFCA Act, the PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong, a Special Administrative Region and dependency of the PRC, because of a position taken by one or more authorities in such jurisdictions. In addition, the PCAOB’s report identified specific registered public accounting firms which are subject to these determinations. Our current registered public accounting firm, PKF, or our former registered public accounting firm, UHY LLP, is not headquartered in mainland China or Hong Kong and was not identified in this report as a firm subject to the PCAOB’s determination. They both are subject to full inspection by the PCAOB and the PCAOB is able to inspect the audit workpapers of our China subsidiaries, as such workpapers are electronic files possessed by our registered public accounting firms. However, if the PCAOB determines in the future that it cannot inspect or fully investigate our auditor at such future time, trading in the Company’s securities would be prohibited under the HFCA Act. | |

| ● | The Chinese government may intervene or influence our operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in our operations and in the value of the Company’s securities. Any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. | |

| ● | There are uncertainties regarding the interpretation and enforcement of PRC laws, rules and regulations. | |

| ● | The cryptocurrency mining market is highly competitive and fragmented with low barriers to entry. We face uncertainties and challenges as we enter into the new blockchain technology business. | |

| ● | If the market for cryptocurrency ceases to exist or diminishes significantly, our business, results of operations and financial condition would be materially harmed. | |

| ● | Any failure to obtain or renew any required approvals, licenses, permits or certifications for our cryptocurrency mining business could materially and adversely affect our business and results of operations. | |

| ● | We have a limited operating history of selling cloud-based products and services and may be unable to achieve or sustain profitability or reasonably predict our future results. | |

| ● | Our independent registered auditors have expressed substantial doubt about our ability to continue as a going concern. | |

| ● | If we fail to comply with the continued listing requirements of NASDAQ, we would face possible delisting, which would result in a limited public market for our shares and make obtaining future debt or equity financing more difficult for us. | |

| ● | The trading price of Taoping’s ordinary shares has been and likely continue to be highly volatile, which could result in significant losses to holders of the ordinary shares. | |

| ● | Because we do not expect to pay dividends in the foreseeable future, you must rely on price appreciation of your shares for return on your investment. |

| 5 |

| ● | You may face difficulties in protecting your interests, and your ability to protect your rights through U.S. courts may be limited, because we are incorporated under British Virgin Islands law and a significant majority of our current business operations are conducted in the PRC. | |

| ● | Taoping is a foreign private issuer within the meaning of the rules under the Exchange Act, and as such we are exempt from certain provisions applicable to U.S. domestic public companies. | |

| ● | As a foreign private issuer, Taoping is permitted to rely on exemptions from certain Nasdaq corporate governance standards applicable to domestic U.S. issuers. This may afford less protection to holders of Taoping’s securities. |

A. [Reserved]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

3

D. Risk Factors

An investment in our capital stockthe Company’s securities involves a high degree of risk. INVESTORS PURCHASING OUR SECURITIES ARE PURCHASING SECURITIES OF TAOPING INC., THE BRITISH VIRGIN ISLANDS HOLDING COMPANY RATHER THAN SECURITIES OF TAOPING INC.’S SUBSIDIARIES THAT HAVE SUBSTANTIVE BUSINESS OPERATIONS IN CHINA AND OTHER COUNTRIES. You should carefully consider the risks described below, together with all of the other information included in this annual report, before making an investment decision. If any of the following risks actually occurs, our business, financialcondition or results of operations could suffer. In that case, the trading pricevalue of our ordinary sharesthe Company’s securities could significantly decline or be worthless and you may lose all or part of your investment.

Risks Relating to our Business

If the COVID-19 pandemic is not effectively controlled in a short period of time, our business operation and financial condition in the long-term may be materially and adversely affected as a result of any slowdown in economic growth, operation disruptions or other factors that we cannot predict.

With operations in China and other countries worldwide, we are subject to numerous risks outside of our control, including risks arising from natural disasters, such as fires, earthquakes, hurricanes, floods, tornadoes, unusual weather conditions, pandemic outbreaks and other global health emergencies, terrorist acts or disruptive global political events, or similar disruptions that could materially adversely affect business and financial performance. The spread of the novel coronavirus (“COVID-19”), which was declared a pandemic by the World Health Organization in March 2020, has spread across many countries and is impacting worldwide economic activity. While we have seen gradual recovery of our overall business as well as the supply chain, project execution and cash collection resulting from improving health statistics in China since March 2020, the spread of COVID-19 may be prolonged and worsened, and we may be forced to scale back or even suspend our operations. As this outbreak persists, commercial activities throughout the world have been curtailed with decreased consumer spending, business operation disruptions, interrupted supply chain, difficulties in travel and reduced workforces. The duration and intensity of disruptions resulting from the COVID-19 outbreak is uncertain. It is unclear as to when the outbreak will be eventually contained, and we also cannot predict if the impact will be short-lived or long-lasting. The extent to which outbreak impacts our long-term financial results will depend on many factors beyond our control. Major factors include the extent of resurgences of the disease and its variants, vaccine distribution and other actions taken to contain the impact of COVID-19. The measures taken by the governments of countries affected could disrupt the demand from our customers, our sales efforts, the delivery of our products and services, reduce our customers’ ability to pay and adversely impact our business, financial condition and results, or results of operations. If the COVID-19 pandemic is not effectively controlled in a short period of time, our long-term business operation and financial condition may be materially and adversely affected as a result of any slowdown in economic growth, operation disruptions or other factors that we cannot predict.

| 6 |

The cryptocurrency mining market is highly competitive and fragmented with low barriers to entry. We face uncertainties and challenges as we enter into the new blockchain technology business.

As part of our strategic business transformation, we established a blockchain technology business segment in 2021, which is dedicated to the research and application of blockchain technology and digital assets. We launched cryptocurrency mining operations, a blockchain related new business, as the first initiative of this new business segment in the first quarter of 2021. With multiple cloud data centers deployed outside of China mainland, the Company continues to improve computing power and create value for the encrypted digital currency industry. Due to our limited experience with cryptocurrency and the mining activities, we face challenges and uncertainties relating to the possibility of success of our new business. We cannot assure you that the introduction and development of this new line of business would not encounter significant difficulties or would achieve the profitability as we expect. Failure to successfully manage those risks in the development and implementation of any new lines of business or new products or services could have a material adverse effect on our business, results of operations and prospects. For example, with respect to our plan to develop our cryptocurrency mining business, we may not be able to acquire cryptocurrency mining machines at a reasonable cost, or at all. In addition, although the market for the cryptocurrency mining operations is new and evolving, the barriers to entry are quite low. Therefore, if cryptocurrency mining remains profitable, we expect additional competitors to enter the market, some of whom may have greater resources than we do. If we fail to establish our strengths or maintain our competitiveness in this industry, our business prospects, results of operations and financial condition may be materially and adversely affected.

The price of cryptocurrency has historically been volatile. Sharp declines in the price of cryptocurrencies could adversely impact our results of operations and subject us to impairment charges.

Our cryptocurrency mining revenue is determined by the fair value of the cryptocurrency awards we receive, as is based upon the quoted price of the related cryptocurrency at the time of receipt. The demand for, and pricing of, the cryptocurrencies that we receive from our mining activities are subject to various factors and significant fluctuations. For example, the prevalence of such assets is a relatively recent trend, and their long-term adoption by investors, consumers and businesses is unpredictable. Moreover, their lack of a physical form, their reliance on technology for their creation, existence and transactional validation and their decentralization may subject their integrity to the threat of malicious attacks and technological obsolescence. Finally, the extent to which securities laws or other regulations apply or may apply in the future to such assets is unclear and may change in the future. We expect our results of operations to be affected by the prices of the cryptocurrencies as we generate an increasing amount of revenue from our mining activities. Our results of operations could be harmed if the prices of cryptocurrencies decrease significantly.

In addition, as we may hold part of the cryptocurrencies we receive from our mining activities, we may be subject to impairment charges that may be caused by reductions in the price of those cryptocurrencies. Digital assets are currently considered indefinite-lived intangible assets under applicable accounting rules, meaning that any decrease in their fair values below our carrying values for such assets at any time subsequent to their acquisition will require us to recognize impairment charges, whereas we may make no upward revisions for any market price increases until a sale, which may adversely affect our operating results in any period in which such impairment occurs. Moreover, there is no guarantee that future changes in U.S. generally accepted accounting principles, or GAAP, would not require us to change the way we account for digital assets held by us. Various factors, mostly beyond our control, could impact the price of cryptocurrencies. If the price of cryptocurrencies drops, the expected economic return of cryptocurrency mining activities will diminish.

If the market for cryptocurrency ceases to exist or diminishes significantly, our business, results of operations and financial condition would be materially harmed.

If the market for cryptocurrencies ceases to exist or diminishes significantly, our efforts and investment in establishing and developing our cryptocurrency mining business may become futile. Several adverse factors may affect the market for cryptocurrencies. As there is no wide consensus with respect to the value and application of cryptocurrency, any future development may continue to affect the demand and the market for cryptocurrency.

| 7 |

Decentralization, or the lack of control by a central authority, is a key reason that cryptocurrencies like bitcoin have attracted many committed users. However, the decentralized nature of cryptocurrencies is subject to growing discussion and skepticism. Some claim that most of the actual services and businesses built within the cryptocurrency ecosystem are in fact centralized since they are run by specific people, in specific locations, with specific computer systems, and that they are susceptible to specific regulations. Individuals, companies or groups, as well as cryptocurrency exchanges that own vast amounts of cryptocurrencies, can affect their market price. Furthermore, mining equipment production and mining pool locations are becoming centralized. Some argue that the decentralized nature of cryptocurrencies is a fundamental flaw rather than a strength. The skepticism about the decentralized nature of cryptocurrency may cause loss of confidence in the prospect of the cryptocurrency industry, which in turn could adversely affect the market demand for cryptocurrencies and our business.

Substantial increases in the supply of mining machines connected to the cryptocurrency network would lead to an increase in network capacity, which in turn would increase mining difficulty and negatively affect the economic returns of cryptocurrency mining activities.

The difficulty of cryptocurrency mining, or the amount of computational resources required for a set amount of reward for recording a new block, directly affects the expected economic returns for cryptocurrency miners. Cryptocurrency mining difficulty is a measure of how much computing power is required to record a new block and it is affected by the total amount of computing power in the cryptocurrency network. The cryptocurrency algorithm is designed so that one block is generated, on average, every ten minutes, no matter how much computing power is in the network. Thus, as more computing power joins the network, and assuming the rate of block creation does not change (remaining at one block generated every ten minutes), the amount of computing power required to generate each block and hence the mining difficulty increases. In other words, based on the current design of the cryptocurrency network, cryptocurrency mining difficulty would increase with the total computing power available in the cryptocurrency network, which is in turn affected by the number of cryptocurrency mining machines in operation. As a result, a strong growth in the cryptocurrency mining industry can lead to growth in the total computing power in the network, thereby driving up the difficulty of cryptocurrency mining and resulting in downward pressure on the expected economic return of cryptocurrency mining.

Cryptocurrency mining computers and other necessary hardware are subject to malfunctions and normal wear and tear. In addition, we may face difficulty and increased cost in obtaining new hardware due to supply chain strains.

Our cryptocurrency miners are subject to malfunctions and normal wear and tear, and, at any point in time, a certain number of our cryptocurrency miners may be off-line for maintenance or repair. The physical degradation of our miners will require us to replace miners that are no longer functional. Any major cryptocurrency miner malfunction out of the typical range of downtime for normal maintenance and repair could cause significant economic damage to us.

Additionally, as technology evolves, we may need to acquire newer models of miners to remain competitive in the market. New miners can be costly and may be in short supply. Given the relatively long production period to manufacture and assemble cryptocurrency miners and the current global semiconductor chip shortage, there can be no assurance that we can acquire enough cryptocurrency mining computers or replacement parts on a cost-effective basis, if at all, for the maintenance and expansion of our cryptocurrency mining operations. We rely on our subsidiaries to purchase and assemble cryptocurrency miners and shortages of cryptocurrency miners or their component parts, material increases in cryptocurrency miner costs, or delays in delivery of the cryptocurrency miners to our overseas mining data centers, including due to trade restrictions and COVID-19 supply chain disruptions, could significantly interrupt our plans for expanding our cryptocurrency mining capacity in the near term and future.

This upgrading and replacement process requires capital investment and we may face challenges in doing so on a timely and cost-effective basis. Shortages of cryptocurrency mining computers could result in reduced cryptocurrency mining capacity and increased operating costs, which could materially delay the completion of our planned cryptocurrency mining capacity expansion and put us at a competitive disadvantage.

| 8 |

Cryptocurrency exchanges and wallets, and to a lesser extent, the cryptocurrency network itself, are subject to substantial hacking and fraud risks, which may adversely affect the economic return of our cryptocurrency mining business.

Cryptocurrency transactions are entirely digital and, as with any virtual system, are at risk from hackers, malware and operational glitches. Hackers can target cryptocurrency exchanges and cryptocurrency transactions, to gain access to thousands of accounts and digital wallets where cryptocurrency are stored. Cryptocurrency transactions and accounts are not insured by any type of government program and all cryptocurrency transactions are permanent because there is no third party or payment processor. Cryptocurrency like bitcoin has suffered from hacking and cyber-theft as such incidents have been reported by several cryptocurrency exchanges and miners, highlighting concerns about the security of bitcoin and other cryptocurrencies and affecting their demand and price. Also, the price and exchange of cryptocurrency may be affected due to fraud risk. While cryptocurrency uses private key encryption to verify owners and register transactions, fraudsters and scammers may attempt to sell false cryptocurrencies. All of the above may adversely affect our operation and the economic return of our cryptocurrency mining business.

Currently, our cryptocurrencies received from the mining pools are stored in electronic wallets, which can only be exclusively transferred to the Company’s FTX trading account. It requires approval from signatories to transfer any cryptocurrency out of our FTX trading account. Four of our management level employees have been designated as the signatories of such transfer-out transactions, including the sales of cryptocurrency and the payment of related service fee in the form of cryptocurrency. Two cashiers have been assigned to simultaneously execute the sale/payment process. Each cashier holds a part of the electronic private key password. Any transfer out of the trading account would immediately trigger an email notice to each of the above-mentioned management employees. However, despite our efforts and measures to ensure the safety of our cryptocurrencies and the transactions, there can be no assurance that such efforts or measures will protect us from hacking or fraud incidents. We may suffer from cryptocurrency hacking and fraud and the economic return of our cryptocurrency mining business may be materially and adversely harmed if such risk occurs.

We may not be able to realize the benefits of forks, and forks in a digital asset network may occur in the future which may affect the value of cryptocurrency held by us.

To the extent that a significant majority of users and miners on a cryptocurrency network install software that changes the cryptocurrency network or properties of a cryptocurrency, including the irreversibility of transactions and limitations on the mining of new cryptocurrency, the cryptocurrency network would be subject to new protocols and software. However, if less than a significant majority of users and miners on the cryptocurrency network consent to the proposed modification, and the modification is not compatible with the software prior to its modification, a “fork” of the network would occur, with one prong of the network running the pre-modified software and the other running the modified software. The effect of such a fork would be the existence of two versions of the cryptocurrency running in parallel, yet lacking interchangeability and necessitating exchange-type transaction to convert currencies between the two forks. After a fork, it may be unclear which fork represents the original asset and which is the new asset.

If we hold cryptocurrency at the time of a hard fork into two cryptocurrencies, industry standards would dictate that we would be expected to hold an equivalent amount of the old and new assets following the fork. However, we may not be able to secure or realize the economic benefit of the new asset. Our business may be adversely impacted by forks in the cryptocurrency network.

Banks and other financial institutions may decline to provide bank accounts, banking or other financial services to cryptocurrency investors or businesses that engage in cryptocurrency-related activities or that accept cryptocurrency as payment.

A number of companies that engage in cryptocurrency-related activities have been unable to find banks or financial institutions that are willing to provide them with bank accounts and other services. Changing governmental regulations about the legality of transferring or holding cryptocurrency may prompt other banks and financial institutions to close existing bank accounts or discontinue banking or other financial services to such companies in the cryptocurrency industry, or even investors with accounts for transferring, receiving or holding their cryptocurrency. Specifically, China already restricts financial institutions from holding, trading or facilitating transactions in bitcoin, Ethereum, and among other cryptocurrencies. Similarly, other countries have proposed cryptocurrency legislation that could have a significant impact on the ability to utilize banking services in such countries for cryptocurrency.

| 9 |

Should such rules and restrictions continue or proliferate, we may not be able to obtain or maintain these services for our business. The difficulty that many businesses that engage in cryptocurrency-related activities have and may continue to have in finding banks and financial institutions willing to provide them services may diminish the usefulness of cryptocurrency as a payment system and harm public perception of cryptocurrency. If we are unable to obtain or maintain banking services for our business as a result of our cryptocurrency-related activities, our results of operations and financial condition could be materially adversely affected.

We do not maintain insurance for our digital assets, which may expose us to the risk of loss of our digital assets, and legal recourse available to us to recover our losses may be limited.

We do not maintain insurance for the digital assets held by us. Banking institutions do not accept our digital assets. We may suffer loss with respect to our digital assets which are not covered by insurance, and we may not be able to recover any of our carried value in these digital assets if they are lost or stolen or suffer significant and sustained reduction in conversion spot price. If we are not otherwise able to recover damages from a malicious actor in connection with these losses, our business, results of operations and share price may be adversely affected.

There has been limited precedent set for financial accounting of digital assets, and thus, it is unclear how we will be required to account for digital asset transactions.

While we record digital assets as indefinite-lived intangible assets in accordance with Accounting Standards Codification, or ASC, 350, there is currently no authoritative guidance under GAAP which specifically addresses the accounting for digital assets, including digital currencies.

We recognize cryptocurrency related revenue when cryptocurrency is earned. The receipt of cryptocurrency is generally recorded as revenue, using the spot price of a prominent exchange at the time of daily reward and cryptocurrencies are recorded on the balance sheet at their cost basis and are reviewed for impairment frequently.

A change in financial accounting standards or their interpretation could result in changes in accounting treatment applicable to our cryptocurrency business, which may have an adverse effect on our results of operations.

As cryptocurrencies grow in both popularity and market size, governments around the world have reacted differently to them. Ongoing and future regulation and regulatory actions could significantly restrict or eliminate the market for or uses of cryptocurrencies and/or materially and adversely impact our results of operation and financial condition.

As cryptocurrencies generally have grown in both popularity and market size, governments around the world have reacted differently to them. Certain governments have deemed them illegal, while others have allowed their use and trade without restriction. Based on stated efforts to curtail energy usage on mining and to protect investors or to prevent criminal activity, regulations have proliferated recently. In March 2021, a new law was proposed in India to criminalize the mining, transfer or holding of cryptocurrencies, and current rules require extensive disclosure to the government of cryptocurrency holdings. Similarly, China has also limited certain mining and trading, although not possession, of cryptocurrency, to reduce energy usage. On April 16, 2021, Turkey imposed bans on the use of cryptocurrency as payment and now requires transactions of a certain size to be reported to a government agency in the wake of alleged fraud at one of Turkey’s largest exchanges. In addition, in May 2021, Iran announced a temporary ban on cryptocurrency mining as a way to reduce energy consumption amid power blackouts. Many jurisdictions, such as the United States, subject cryptocurrencies to extensive, and in some cases overlapping, unclear and evolving regulatory requirements. Further, in January 2021, Russia adopted legislation to identify cryptocurrency as a digital asset and legitimize its trading, but also prohibit its use as a payment method. Mining operations have also grown significantly in Russia since then. Such varying government regulations and pronouncements are likely to continue for the near future. In the U.S., the Federal Reserve Board, U.S. Congress and certain U.S. agencies (e.g., the Commodity Futures Trading Commission, the SEC, the Financial Crimes Enforcement Network of the U.S. Treasury Department (“FinCEN”) and the Federal Bureau of Investigation) have begun to examine the operations of the cryptocurrency network, cryptocurrency users and the cryptocurrency exchange market.

| 10 |

Compliance with increasing regulation and regulatory scrutiny may entail significant expenses, divert our management’s time and attention, and change aspects of our business. Moreover, ongoing and future regulations that ban the mining, use, transfer or possession of cryptocurrencies could significantly restrict or eliminate the market for cryptocurrencies and/or materially and adversely impact our results of operation and financial condition.

Acquisition, possession, ownership, sale or use of cryptocurrencies, participation in the blockchain, or transfer or use of digital assets may be or become illegal in China or the international markets where we plan to operate, which could materially negatively impact our operations.

Our blockchain and cryptocurrency mining business could be significantly affected by the regulatory and policy developments in mainland China, Hong Kong and international markets where we operate, such as Kazakhstan. Governmental authorities are likely to continue to issue new laws, rules and regulations governing the blockchain and cryptocurrency industry and enhance enforcement of existing laws, rules and regulations. For example, the People’s Bank of China (the “PBOC”), Ministry of Industry and Information Technology, State Administration for Industry and Commerce, China Banking Regulatory Commission, CSRC and China Insurance Regulatory Commission issued the Announcement on Preventing Token Fundraising Risks on September 4, 2017, prohibiting all organizations and individuals from engaging in initial coin offering transactions. On May 21, 2021, the Financial Stability and Development Committee of the PRC State Council called for the need to resolutely control financial risks and crack down on bitcoin mining and trading activities. Furthermore, on June 21, 2021, the PBOC was reported to have held interviews with certain financial institutions in China, and stressed that banks and other financial institutions in China shall strictly implement the Guarding Against Bitcoin Risks and the Announcement on Preventing Token Fundraising Risks and other regulatory requirements, diligently fulfill their customer identification obligations, and shall not provide account opening, registration, trading, clearing, settlement and other services related to blockchain and cryptocurrency business.

Also, China restricts various uses of cryptocurrencies, including the use of cryptocurrencies as a medium of exchange and the conversion between cryptocurrencies and fiat currencies or between cryptocurrencies. In light of the regulatory restrictions in mainland China, we currently carry out substantially all of our cryptocurrency mining operations outside of mainland China. At present, we focus on the international markets for our cryptocurrency mining operations. In addition to Hong Kong, we plan to construct additional mining data centers in Kazakhstan to carry out operation and maintenance of cryptocurrency mining machines, and rent out excess operating capacity to third parties. We cannot assure you that the government authorities in the international markets will not adopt new laws and regulations in the future to restrict blockchain and cryptocurrency business.

In addition, cryptocurrencies may be used by market participants for black market transactions to conduct fraud, money laundering and terrorism-funding, tax evasion, economic sanction evasion or other illegal activities. As a result, governments may seek to regulate, restrict, control or ban the mining, use, holding and transferring of cryptocurrencies. We may not be able to eliminate all instances where other parties use cryptocurrencies mined by us to engage in money laundering or other illegal or improper activities. There is no assurance that we will successfully detect and prevent all money laundering or other illegal or improper activities which may adversely affect our reputation, business, financial condition and results of operations. In addition, due to the environmental concerns related to the potential high demand for electricity to support cryptocurrency mining activity, political and other concerns, we may be required to cease mining operations in our locations without much or any prior notice by a national or local government’s formal or informal requirement or because of the anticipation of an impending requirement. Any such government action or anticipated action could have a negative impact not only on the value of existing miners owned by us, but on our ability to purchase new miners and their prices. Such government action or anticipated action could also have a deleterious impact on the price of cryptocurrencies. Such events could result in an increase in the volatility of the price of the cryptocurrencies and value of miners owned by us. Moreover, if we discontinue mining operations in one location in response to such government action or anticipated action, we likely would transfer miners to another location. However, this process would result in costs associated with the transfer to be incurred by us, as well as the transferred miners being off-line and not able to mine cryptocurrencies for some time. Our business, financial condition and results of operations may be materially and adversely affected by these adverse changes in the regulations and policies in the markets where we operate our blockchain and cryptocurrency mining operations.

| 11 |

Any failure to obtain or renew any required approvals, licenses, permits or certifications for our cryptocurrency mining business could materially and adversely affect our business and results of operations.

We may be required to maintain various approvals, licenses, permits and certifications in order to operate our cryptocurrency mining business. Complying with such laws and regulations may require substantial expense, and any non-compliance may expose us to liability. Presently, substantially all of our cryptocurrency mining operations are carried outside of mainland China, and our operations in mainland China primarily involve the provision of administrative supports to our cryptocurrency mining business out of mainland China, as well as the provision of information technology services to our operating entities and mining pools outside mainland China. However, due to the complex and evolving nature of our industry and the regulatory regimes, we cannot assure you that we have obtained all the permits or licenses required for conducting our blockchain business in China or internationally or will be able to maintain our existing licenses or obtain any new licenses required under any new laws or regulations.

As we plan to establish cryptocurrency mining data centers in Kazakhstan, we will become subject to regulations applicable to operators of cryptocurrency mining business and data processing business in such jurisdiction. We will apply for relevant governmental approval and license required for our proposed data center operations in Kazakhstan. However, we cannot assure you that we will be able to obtain the required government approval, permit, licenses for our proposed operations on commercially reasonable terms and in a timely manner, or at all. Failure to obtain these government approvals, permits or licenses for our international operations will delay the establishment of our data centers and may subject us to regulatory investigations or legal proceedings and fines in such jurisdiction, which could disrupt our international operations and materially and adversely affect our business, financial condition and results of operations.

More broadly, we cannot assure you that we will be able to fulfill all the conditions necessary to obtain the required government approvals in the jurisdictions where we operate, or that the governmental authorities in these jurisdictions will always, if ever, exercise their discretion in our favor, or that we will be able to adapt to any new laws, regulations or policies. There may also be delays on the part of governmental authorities in reviewing our applications and granting approvals, whether due to the lack of administrative resources or the imposition of new rules, regulations, government policies, or for no discernible reason at all. If we are unable to obtain, or experience material delays in obtaining, necessary government approvals, our operations may be substantially disrupted, which could materially and adversely affect our business, financial condition and results of operations.

If cryptocurrencies are determined to be investment securities and we hold a significant portion of our assets in such cryptocurrency, investment securities or non-controlling equity interests of other entities, we may inadvertently violate the Investment Company Act of 1940, as amended, and we could incur substantial expenses to adjust our operations to avoid being registered as an investment company or to register as an investment company or could terminate operations altogether.

We believe that we are not engaged in the business of investing, reinvesting, or trading in securities, and we do not hold ourselves out as being engaged in those activities. However, under the Investment Company Act of 1940, as amended (the “Investment Company Act”), a company may be deemed an investment company under section 3(a)(1)(C) thereof if the value of its investment securities is more than 40% of its total assets (exclusive of government securities and cash items) on an unconsolidated basis. The cryptocurrency we own, acquire or mine may be deemed an investment security by the SEC, although we do not believe any of the cryptocurrencies we own, acquire or mine are securities. However, SEC rules and applicable law are subject to change, especially in the evolving world of cryptocurrency, and further, the Investment Company Act analysis may not be uniform across all forms of cryptocurrency that we might mine or hold.

An inadvertent investment company can avoid being classified as an investment company if it can rely on one of the exclusions under the Investment Company Act. One such exclusion, Rule 3a-2 under the Investment Company Act, allows an inadvertent investment company a grace period of one year from the earlier of (a) the date on which an issuer owns securities and/or cash having a value exceeding 50% of the issuer’s total assets on either a consolidated or unconsolidated basis and (b) the date on which an issuer owns or proposes to acquire investment securities having a value exceeding 40% of the value of such issuer’s total assets (exclusive of government securities and cash items) on an unconsolidated basis. In that year, the company would be required to take actions to cause the investment securities held by it to be less than 40% of its total assets, which could include acquiring assets with its cash and/or cryptocurrency on hand, liquidating its investment securities or seeking a no-action letter from the SEC if it is unable to acquire sufficient assets or liquidate sufficient investment securities in a timely manner. Such actions could require significant cost, disruption to operations or growth plans and diversion of management time and attention. Further, the Rule 3a-2 exception is available to a company no more than once every three years.

| 12 |

Current and future legislation and the SEC rulemaking and other regulatory developments, including interpretations released by a regulatory authority, may impact the manner in which cryptocurrencies are treated for classification and clearing purposes. The SEC’s July 25, 2017 Report expressed its view that digital assets may be securities depending on the facts and circumstances. As of the date hereof, we are not aware of any rules that have been proposed to regulate cryptocurrencies as securities. We cannot be certain as to how future regulatory developments will impact the treatment of cryptocurrency under the applicable U.S. laws. Such additional registrations may result in extraordinary, non-recurring expenses, thereby materially and adversely impacting our operations.

Classification as an investment company under the Investment Company Act requires registration with the SEC. If an investment company fails to register, it would have to stop doing almost all business, and its contracts would become voidable. Registration is time consuming and restrictive and would require a restructuring of operations, and it would be very constrained in the kind of business it could do as a registered investment company. Furthermore, such company would become subject to substantial regulation concerning management, operations, transactions with affiliated persons and portfolio composition, and would need to file reports under the Investment Company Act regime.

We need to access a large quantity of power at a reasonable cost in order to support our cryptocurrency mining operations, which may be adversely affected by legislative or regulatory changes relating to climate change and other energy consumption requirements.

We need to access a large quantity of power at a reasonable cost in order to support our cryptocurrency mining operations, but we do not have any long-term contract for the provision of power at specified prices. As competition in the area we operate increases, we may not be able to access power at reasonable costs or at all. Any shortage of electricity supply or increase in electricity cost in a jurisdiction may negatively impact the viability and the expected economic return for cryptocurrency mining activities in that jurisdiction.

In addition, a number of governments or governmental bodies have introduced or are contemplating legislative and regulatory changes in response to various climate change interest groups and the potential impact of climate change. Given the very significant amount of electrical power required to operate cryptocurrency miners, as well as the environmental impact of mining for the rare earth metals used in the production of mining servers, the cryptocurrency mining industry may become a target for future environmental and energy regulation. Legislation and increased regulation regarding climate change could impose significant costs on us and our suppliers, including costs related to increased energy requirements, capital equipment, environmental monitoring and reporting, and other costs to comply with such regulations. Any future climate change regulations could also negatively impact our ability to compete with companies situated in areas not subject to such limitations. Given the political significance and uncertainty around the impact of climate change and how it should be addressed, we cannot predict how legislation and regulation will affect our financial condition, operating performance and ability to compete. Furthermore, even without such regulation, increased awareness and any adverse publicity in the global marketplace about potential impacts on climate change by us or other companies in our industry could harm our reputation. Any of the foregoing could result in a material adverse effect on our business and financial condition.

We are subject to risks and disruptions related to the COVID-19 pandemic, including supply chain issues in semiconductors and other necessary mining components, which could significantly impact our operating performance and financial condition.

The COVID-19 pandemic outbreak has and may continue to adversely affect the economies of many countries, resulting in an economic downturn that may have an adverse effect on financial markets, cryptocurrency prices, the demand for cryptocurrency and other factors that could impact the financial results of our digital assets segment.

Our suppliers and our subsidiaries have experienced disruption to operations caused by quarantines, restrictions on employees’ ability to work, office and factory temporary closures, disruptions to ports and other shipping infrastructure, border closures, or other travel or health-related restrictions. Depending on the magnitude of such effects on our supply chain, procurement of parts for our existing miners, as well as any new miners we purchase, may be delayed. As our miners require repair or become obsolete and require replacement, our ability to obtain adequate replacements or repair parts from miner manufacturers may therefore be hampered. Supply chain disruptions could therefore negatively impact our operations.

| 13 |

In addition, multiple factors including some related to the COVID-19 pandemic have created a global semiconductor shortage. Since the inception of the pandemic, factory shutdowns and limitations due to employee illness or public health requirements have significantly slowed output, while global demand for products requiring chips increased. These 2020-2021 challenges worsened a pre-existing semiconductor and other supply shortage. Semiconductor supply has not yet rebounded, and manufacturers across all industries are waiting and driving up demand and costs. While we believe we will have sufficient cryptocurrency miners for our 2022 plans, any delay or disruption in deploying such miners, or future miners necessary for our success and growth, may have a material and negative impact on our results of operations.

We have a limited operating history of selling our cloud-based products and services and may be unable to achieve or sustain profitability or reasonably predict our future results.

In early 2013, we made a strategic decision to transform our business from servicing the public sector to focusing on the private sector. Leveraging our experience and expertise in handling large-scale IT projects for the public sector, we started investing in research and development to develop software products for the private sector. In 2014, continuing our business transition from the public sector to the private sector, we identified and provided cloud-based ecosystem solutions to four core markets including new media, healthcare, education, and residential community management. Underpinning our ecosystems are our industry-specific integrated technology platform, resource exchange, and big data services. In 2014, we predominately sold our cloud-based solutions to the Chinese new media industry. Starting from 2015, we further expanded the customer base of cloud-based solutions to education, government, and residential community management. In 2016, we grewexpanded our business from the industry-specific integrated technology platform, resource exchange, and big data services tointo the elevator IoT sectors. From May 2017, we have focused our business to provide products and services inon Cloud-App-Terminal (CAT) and IoT technology based digital advertising distribution networknetworks and new media resource sharing platformplatforms in the Out-of-Homeout-of-home adverting market in China. As such, we have a limited operating history of selling our cloud-based products and professional services to the private sector, which makes it difficult to evaluate our current business and future prospects and may increase the risk of your investment. In 2017,2021 and 2020, we generated approximately $17.0$18.8 million ofand $10.7 million in revenue inrespectively, from our cloud-based technology (CBT) segment for customers in the education, new media, and Out-of-Homeout-of-home advertising market sectors. We expect to have significant operating expenses in the future to further support and grow our business, including expanding the scope of our customer base, expanding our direct and indirect selling capabilities, pursuing acquisitions of complementary businesses, investing in our data storage and analysis infrastructure, and research and development, and increasing our international presence. As a result of our new initiatives, although we had net income of $0.9 million in 2017, we cannot assure you that we will sustain profitability in the future.

Our independent registered auditors have expressed substantial doubt about our ability to continue as a going concern.

Our independent auditors have added an explanatory paragraph to their audit opinion issued in connection with our financial statements included in this report which states that the financial statements were prepared assuming that we would continue as a going concern.