| (a)securities; (b)units in a collective investment scheme;

(c)exchange-traded derivatives contracts;

(d)over-the-counter derivatives contracts; or

(e)spot foreign exchange contracts for the purposes of leveraged foreign exchange trading.

| (b) | units in a collective investment scheme; |

| (c) | exchange-traded derivatives contracts; |

| (d) | over-the-counter derivatives contracts; or |

| (e) | spot foreign exchange contracts for the purposes of leveraged foreign exchange trading. |

| 16. | Moomoo Financial Singapore must notify the MAS of any addition to the list of capital markets products indicated against its appointed representative’s name in the public register of representatives, by lodging a notice in the prescribed form.form and in the manner specified at http://www.mas.gov.sg. |

| 17. | FutuMoomoo Financial Singapore shall, no later than the next business day after the day on which any of its appointed representatives, provisional representatives or temporary representatives has ceased to carry on business in dealing in capital markets products in respect of any or all types of capital markets products indicated against his name in the public register of representatives, notify the MAS by lodging a notice in the prescribed form.form and in the manner specified at http://www.mas.gov.sg.

|

| 18. | FutuWhere Moomoo Financial Singapore must carry on business in dealing in capital markets products only in respect of capital markets products that are securities, units in a collective investment scheme and exchange-traded derivatives contracts. Where Futu Singapore intends to carry on business in dealing in capital markets products other than the aforesaid, it must seek MAS’ approval by lodging a notice in the prescribed form. The MAS may require Futu Singapore to furnish it with such information or documents as the MAS considers necessary.

|

19.

| Where Futu Singapore ceases to carry on business in dealing in capital markets products in respect of any particularadditional type of capital markets products other than securities, units in a collective investment scheme, exchange-traded derivatives contracts, over-the-counter derivatives contracts, and spot foreign exchange contracts for the purposes of leveraged foreign exchange trading, Moomoo Financial Singapore must seek MAS’ approval to deal in those additional types of capital markets products by lodging a notice in the prescribed form and in the manner specified at http://www.mas.gov.sg. The MAS may require Moomoo Financial Singapore to furnish it with such information or documents as the MAS considers necessary in relation to its request.

|

| 19. | Where Moomoo Financial Singapore ceases carrying on business in dealing in capital markets products in respect of any type of capital markets products, but has not ceased to carry on business in dealing in capital markets products in the remaining types of capital markets products, FutuMoomoo Financial Singapore must notify MAS of such cessation by lodging a notice in the prescribed form and in the manner specified at http://www.mas.gov.sg, by not later than 14 days from the date of cessation. |

| 20. | Where FutuMoomoo Financial Singapore has commenced carrying on business in dealing in capital markets products in respect of some types of capital markets products but not others for which it is allowed to deal in under its license by the end of the period of 6 months from the date on which its license was granted (or such longer period as the MAS may allow in any particular case), FutuMoomoo Financial Singapore must immediately lodge with the MAS a notice in the prescribed form. |

| 21. | Where the MAS varies the types of capital markets products in respect of which FutuMoomoo Financial Singapore carries on business in dealing after receiving the request from Futu Singapore,in condition 18 above, or the notifications in conditions 19 or 20 above, the MAS may issue a new license to FutuMoomoo Financial Singapore which reflects the types of capital markets products in respect of which it carries on business in dealing. |

| 22. | FutuMoomoo Financial Singapore must carry on business in dealing in capital markets products only in respect of capital markets products that are securities, units in a collective investment scheme, exchange-traded derivatives contracts, over-the-counter derivatives contracts, and spot foreign exchange contracts for the purposes of leveraged foreign exchange trading.

|

| 23. | Moomoo Financial Singapore shall satisfy itself of compliance with all relevant laws and requirements in the relevant foreign jurisdictions, before it starts offering products and services to investors residing in that foreign jurisdiction. |

Representatives, Directors, and CEO Requirements Under Section 99B(1) of the SFA, individuals who are employed by or who are acting for a CMSL holder in Singapore to carry out the regulated activities are required to be registered with MAS as appointed, provisional or temporary representatives under the SFA, unless otherwise exempted. In addition, pursuant to the MAS Guidelines SFA 04-G01 on Criteria for the Grant of a Capital Markets Services License Other than for Fund Management and Real Estate Investment Trust ManagementLicence (last revised on October 8, 2018)August 2, 2022), FutuMoomoo Financial Singapore is required amongst other things, to employ at least two full-time individuals as appointed representatives in respect of each of the regulated activities which it is being licensed to conduct. FutuMoomoo Financial Singapore isshould also required to ensure that its board of directors comprise a minimum of two directors on its board, at least one of whom is resident in Singapore. The chief executive officer of FutuMoomoo Financial Singapore mustshould also be resident in Singapore. The approval of the MAS is also required forshould be obtained prior to the appointment or change of theits chief executive officer, all resident directors, and all directorsany director who is directly responsible for Futu Singapore’sits business in Singapore. “Fit and Proper” Requirement Persons applying to the MAS for a CMSL under the SFA, as well as its directors, representatives, and shareholders, must satisfy, the MAS Fit and Proper Criteria, and continue to satisfy the said criteria after the grant of the CMSL by the MAS.MAS, that they are fit and proper persons. Generally, a fit and proper person refers to a personmeans one who is financially sound, competent, honest, and has not been in breach of relevant laws and regulations. MAS administers this regime through a set of Fit and Proper Guidelines which apply to variousall classes of regulated entities (including CMSL holders). are ordinarily expected to follow. Base Capital Requirements A corporation granted a CMSL in respect of regulated activities shall at all times meet the base capital requirement thresholds under the Securities and Futures (Financial and Margin Requirements for Holders of Capital Markets Services Licenses) Regulations (“SF(FMR)R”), in respect of the regulated activities for which it is licensed to conduct. In view of this obligation, it would be prudent for the CMSL holder to maintain an additional capital buffer over and above the requisite base amount. The base capital requirement thresholds applicable to the regulated activities carried on by FutuMoomoo Financial Singapore are set out under the First Schedule to the SF(FMR)R as follows: | | | | | Base capital | Regulated activity | | requirement (SG$) | Dealing in capital markets products that are securities, units in a collective investment scheme or exchange-traded derivatives contracts and the applicant is not a member of an approved exchange.(5) | S$ | 1,000,0001 million

| Carrying out product financing. | S$ | 1,000,0001 million

| Providing custodial services. | S$ | 1,000,0001 million

|

Notes: (5) Under the SFA, an “approved exchange” means a corporation that is approved by the MAS under the SFA as an approved exchange. An example of such an approved exchange is the Singapore Exchange Securities Trading Limited, or SGX. Generally, where more than one base capital requirement is applicable to a CMSL holder, the highest of such base capital requirements will apply. Hence, the base capital requirement of FutuMoomoo Financial Singapore is S$1 million. By Regulation 4 of the SF(FMR)R, a CMSL holder shall not cause or permit its base capital to fall below the base capital requirement applicable to it. Where the base capital falls below the base capital requirement or where the CMSL holder becomes aware that the base capital will fall below the base capital requirement, the MAS must be notified immediately. Failure to comply with base capital requirements entail serious consequences and may jeopardise the CMSL itself. Hence, in view Risk Capital Requirements Furthermore, a CMSL holder shall at all times meet the risk-based capital requirement in the SF(FMR)R upon obtaining its license. The particular capital requirements are generally based on various risk factors faced by the CMSL holder, and the risk measurements are proxied from various items of information within the CMSL holder’s financial statements. In this regard, under Regulations 6 and 7 of the SF(FMR)R, a CMSL holderlicensed corporation shall: | (a) | not cause or permit its financial resources (as defined in the SF(FMR)R and by notices issued by MAS) to fall below the total risk requirement (as defined in the SF(FMR)R and by notices issued by MAS); and |

| (b) | immediately notify the MAS if its financial resources fall below 120% of its total risk requirements. |

Continuing Obligations A holder of a CMSLAn entity licensed under Part IV4 of the SFA must comply withwould typically expect that various ongoing operational obligations set outwould apply, in the SFA, in subsidiary legislation made under the SFA, in other regulatory instruments issued by MAS as well as theaddition to any specific conditions set out inwhich the CMSL itself. TheMAS may impose when granting its licence. There are different ongoing business conduct compliance obligations would differ depending on the type of regulated activity carried on by the holder of the CMSL.relevant licensing category. In respect of FutuMoomoo Financial Singapore, these include, but are not limited to, the following key requirements under the Securities and Futures (Licensing and Conduct of Business) Regulations, or the SF(LCB)R:

| (a) | maintenance of a minimum security deposit in the sum of S$100,000 with the MAS (Regulation 7 of the SF(LCB)R); |

| (b) | implementing,implement, and ensuringensure compliance with, effective written policies on all operational areas, including financial policies, accounting and internal controls, and internal auditing (Regulation 13(b)(i) of the SF(LCB)R); |

| (c) | identifying, addressingidentify, address and monitoringmonitor the risks associated with the trading or business activities (Regulation 13(b)(iii) of the SF(LCB)R); |

| (d) | ensuringensure that its business activities are subject to adequate internal audit (Regulation 13(b)(iv) of the SF(LCB)R); |

| (e) | observing detailed book-keeping and record-keeping obligations (Regulation 39 of the SF(LCB)R); |

| (f) | providingprovision of statements to customers (Regulation 40 of the SF(LCB)R); and |

| (g) | observing regulations on product advertisements (Regulation 46 of the SF(LCB)R). |

Licensing Regime under the Financial Advisers Act For completeness, the provision of financial advisory services is regulated in Singapore under the Financial Advisers Act 2001 (2020 Revised Edition) (“FAA”), and its related subsidiary legislation. Under Section 6(1) of the FAA, a person is not to act as a financial adviser in Singapore in respect of any financial advisory services unless he is authorised to do so in respect of that financial advisory service by a financial adviser’s license (“FAL”), or is an exempt financial adviser. Further, under Section 6(4) of the FAA, a person who contravenes Section 6(1) will be liable on conviction to a maximum fine of S$75,000 or imprisonment for a term of up to 3 years or both. The term “financial adviser” generally refers to a person who carries on a business of providing any financial advisory service under the FAA. There are currently 3 types of financial advisory services under the FAA: | a. | advising others, either directly or through publications or writings, and whether in electronic, print or other form, concerning any investment product;(6) |

| b. | advising others by issuing or promulgating research analyses or research reports, whether in electronic, print or other form, concerning any investment product; and |

| c. | arranging of any contract of insurance in respect of life policies (other than a contract of reinsurance). |

As at the date of this annual report, FutuMoomoo Financial Singapore does not hold a FAL and is not an exempt financial adviser under the FAA. Accordingly, it is importantFAA, but has not commenced to note that Futu Singapore is not authorisedconduct the above regulated activities in Singapore to engage in the activities licensable under the FAA.yet. Notes: | (6) | Under the FAA, “investment product” includes any capital markets products, spot foreign exchange contracts other than for the purposes of leveraged foreign exchange trading, and any life policy. |

Anti-Money Laundering And Counter-Terrorist Financing (“AML/CTF”) Sector-specific requirements applicable to capital markets intermediaries In Singapore, financial institutionscorporations which are licensed by the MAS are generally required to comply with the applicable anti-money laundering and counter-terrorist financing laws and regulations in Singapore as well as various notices and guidelines. In particular, FutuMoomoo Financial Singapore as a CMSL holder will be required to comply with the Notice on Prevention of Money Laundering and Countering the Financing of Terrorism – Capital Markets Intermediaries (last revised on April 20, 2022) (“SFA 04-N02”) issued by the MAS, which should be read together with the Guidelines to MAS Notice SFA 04-N02 (collectively, the “AML/CTF Notices and Guidelines”). The AML/CTF Notices and Guidelines establish a framework within which CMSL holders are to design and develop their own AML/CTF policies, procedures and controls to help prevent money laundering and terrorism financing in Singapore. A CMSL holder should, among other things: | (a) | take appropriate steps to identify, assess and update its money laundering and terrorism financing risks in relation to the launch or use of new products, new business practices, new delivery mechanisms, or new or developing technologies, and to ensure that appropriate measures and controls are implemented to mitigate and manage such risks; |

| (b) | conduct anti-money laundering and customer due diligence (“CDD”) checks on all new customers (which checks must extend(extending to the beneficial owners, connected parties of the customer and persons appointed to act on the customer’s behalf), and update its CDD checks on existing customers from time to time; |

| (c) | perform such CDD checks where the licensed corporation first establishes business relations with any customer, where the licensed corporation undertakes any transaction of a value exceeding S$20,000 for any customer who has not otherwise established business relations with it, where there is a suspicion of money laundering or terrorism financing, or where the licensed corporation has doubts about the veracity or adequacy of any information previously obtained; |

| (d) | reserve the right to request for such information as deemed necessary to verify the identity, tax status and/or source of payment of a customer in order to comply with any applicable law or regulation of any jurisdiction; |

| (e) | implement internal risk management systems, policies, procedures and controls to determine if particular business relations with or transactions for any customer presents a higher risk for money laundering or terrorism financing; |

| (f) | conduct on-going monitoring of activities of its customers to ensure that they are consistent with the nature of business, the risk profile and source of funds, as well as identify transactions that are complex, large or unusual, or patterns of transactions that have no apparent economic or lawful purpose; |

| (g) | conduct comprehensive on-going screening against the United Nations watch lists, other relevant money laundering and terrorism financing sources and lists and information provided by the MAS or other relevant authorities in Singapore; and |

| (h) | report transactions suspected to contain the proceeds of criminal conduct or that is connected in any way with money laundering, tax evasion or terrorist financing to the Suspicious Transactions Reporting Office and the MAS, and document the basis for its assessment and the decision to report the transaction. |

Aside from the AML/CTF Notices and Guidelines, Singapore’s AML/CTF legal framework is governed by a patchwork of legal instruments. We set out below the key legislations in Singapore applicable to FutuMoomoo Financial Singapore which concern money laundering and terrorist financing. Corruption, Drug Trafficking and Other Serious Crimes (Confiscation of Benefits) Act The Corruption, Drug Trafficking and Other Serious Crimes (Confiscation of Benefits) Act 1992 of Singapore (2020 Revised Edition) (“CDSA”) criminalisescriminalizes money laundering and organisesorganizes money laundering offences into two main groups: drug-related offences and other criminal offences. In particular, Part 6 of the CDSA criminalisescriminalizes the laundering of proceeds generated by drug trafficking and criminal conduct via the following principal offences: | (a) | the assistance of another person in retaining, controlling or using the benefitbenefits of drug dealing or criminal conduct under an arrangement (whether by concealment, removal from jurisdiction, transfer to nominees or otherwise) (Sections 50(1) and 51(1) of the CDSA); |

| (b) | the concealment, conversion, transfer or removal from the jurisdiction, or the acquisition, possession or use of benefits of drug dealing or criminal conduct (Sections 5053(1) and 5154(1) of the CDSA) |

| (c) | the concealment, conversion, transfer or removal from the jurisdiction of another person’s benefits of drug dealing or criminal conduct (Sections 53(2) and 54(2) of the CDSA); |

| (b)(d) | the acquisition, possession or use concealment or transfer of theanother person’s benefits of drug dealing or criminal conduct(Sections 53conduct (Sections 53(3) and 5454(3) of the CDSA); and |

| (c)(e) | the possession or use of any property that may be reasonably suspected to beof being benefits of drug dealing or criminal conduct, without a satisfactory account as to how the property had been occasioned (Section 5555(1) of the CDSA). |

Upon conviction of an offence under Sections 50, 51, 53, or 54 and 55 of the CDSA, individuals will be liable to a maximum fine of S$500,000 or imprisonment for a term of up to 10 years or both, while non-individuals will be liable to a maximum fine of S$1 million or twice the value of the benefits of drug dealing or criminal conduct in respect of which the money laundering offence was committed, whichever is higher. If convicted under Section 55 of the CDSA, individuals will be liable to a maximum fine of S$150,000 or imprisonment for a term of up to 3 years, or both, while non-individuals will be liable to a maximum fine of S$300,000. In addition to any criminal liability, Section 6 of the CDSA also allows for the confiscation of proceeds of crime. In particular, a confiscation, restraint or charging order may be made by the court in respect of realisablerealizable property. A confiscation order under Section 664 of the CDSA is an order for the defendant to pay an amount of money assessed to correspond to the value of the benefit he or she derived from drug dealing or criminal conduct, a restraint order under Section 19 serves to prohibit any person from dealing with realisablerealizable property, and a charging order under Section 20 (applicable to immovable property and to capital markets products) serves to secure payment of any amount payable under a confiscation order. In terms of reporting requirements, Section 45(1) of the CDSA provides for the mandatory reporting of suspicious transactions when a person, in the course of his or her trade, profession, business or employment, knows or has reasonable grounds to suspect money laundering. Suspicious transaction reports are to be made to the Commercial Affairs Department of the Singapore Police Force. A failure to report a suspicious transaction would constitute an offence under Section 45(3) of the CDSA. Individuals will be liable on conviction to a fine not exceeding S$250,000 or to imprisonment for a term not exceeding 3 years or to both, while non-individuals would be liable on conviction to a fine not exceeding S$500,000. The CDSA also provides for the offence of tipping-off. Section 57 of the CDSA provides that it is an offence if: (i) a person, who knows or reasonably suspects that an authorisedauthorized officer is acting or proposing to act in a money laundering investigation, discloses, to a second person, any information that is likely to prejudice that investigation or proposed investigation; or (ii) a person, who knows or reasonably suspects that a suspicious transaction report has been filed, discloses to a second person, any information that is likely to prejudice any investigation that might be conducted following the suspicious transaction report. A contravention of Section 57 will lead to an offence, and a fine not exceeding S$250,000 or to imprisonment for a term not exceeding 3 years or to both. Terrorism (Suppression of Financing) Act The Terrorism (Suppression of Financing) Act 2002 of Singapore (2020 Revised Edition) (“TSOFA”) implements within Singapore the provisions of the International Convention for the Suppression of Financing of Terrorism, as well as resolutions of the United Nations (“UN”) Security Council concerning terrorism-related sanctions. It broadly operates in parallel with the CDSA, and like the CDSA, it also provides for mandatory reporting of suspicious transactions. Transactions reported under the TSOFA are also made to the Commercial Affairs Department of the Singapore Police Force. The TSOFA sets out various actions which are deemed terrorist financing acts and constitute offence under the TSOFA. Broadly speaking, the TSOFA criminalisescriminalizes the handling of terrorist property and the provision of services (including financial support) for terrorist activity. This effectively prohibits any and all dealings with terrorists and terrorist property, including the provision of services supporting terrorism. As such, financial institutions must ensure that they do not, inadvertently or otherwise, have dealings with persons or entities which have been designated as terrorists under the TSOFA. The TSOFA also has a designation regime, whereby certain individuals and entities may be designated as terrorists by the Singapore government or by the UN Security Council. Sanctions Within the financial sector, the UNUnited Nations sanctions are given effect to via regulations issued by the MAS pursuant to Section 27A of the Monetary Authority of Singapore Act 1970 (“of Singapore (2020 Revised Edition) (the “MAS Act”). As at the date of this annual report, the MAS sanctions regulations which have been issued pursuant to Section 27A of the MAS Act are as follows: | (a) | MAS (Freezing of Assets of Persons – Democratic Republic of the Congo) Regulations 2006 (S155/2006);2006; |

| (b) | (b)MAS (Freezing of Assets of Persons – Sudan) Regulations 2006; |

| (c) | MAS (Sanctions and Freezing of Assets of Persons – Somalia) Regulations 2010; |

| (d) | MAS (Sanctions and Freezing of Assets of Persons – Libya) Regulations 2011; |

| (e) | MAS (Freezing of Assets of Persons – South Sudan) Regulations 2015 (S776/2015);2015; |

| (c) | MAS (Freezing of Assets of Persons – Sudan) Regulations 2006 (S553/2006); |

| (d)(f) | MAS (Freezing of Assets of Persons – Yemen) Regulations 2015 (S109/2015);2015; |

| (e)(g) | MAS (Sanctions and Freezing of Assets of Persons – Democratic People’s Republic of Korea) Regulations 2016 (S275/2016);2016; and |

| (f)(h) | MAS (Sanctions and Freezing of Assets of Persons – Iran) Regulations 2016 (S276/2016); and |

| (g) | MAS (Sanctions and Freezing of Assets of Persons – Somalia) Regulations 2010 (S706/2010).2016. |

While specific provisions may differ, broadly speaking, these above regulations generally: (i)prohibit financial institutions from entering into transactions with or relating to a sanctioned person;

| (i) | prohibit financial institutions from entering into transactions with or relating to a sanctioned person; |

| (ii) | prohibit financial institutions from entering into transactions that have a specific purpose which is being targeted by the sanctions rule; or |

| (iii) | require financial institutions to freeze assets that may be in their possession or control, where the assets belong to or are controlled by a sanctioned person or where the assets are for the specific purpose that the sanctions rule is targeting, and to notify the authorities accordingly. |

(ii)prohibit financial institutions from entering into transactions that have a specific purpose which is being targeted by the sanctions rule; or

(iii)require financial institutions to freeze assets that may be in their possession or control, where the assets belong to or are controlled by a sanctioned person or where the assets are for the specific purpose that the sanctions rule is targeting, and to notify the authorities accordingly.

The failure to comply with any MAS sanctions regulation is an offence under Section 27A(5) of the MAS Act, for which the financial institution will be liable on conviction to a fine of up to S$1 million. Employees The Employment Act 1968 of Singapore (2020 Revised Edition) (the “EA”) is regulated by the Ministry of Manpower (the “MOM”) and sets out the basic terms and conditions of employment and the rights and responsibilities of employers as well as employees who are covered under the EA. In particular, Section 35 of the Employment Act provides that Part 4 of the EA, which sets out requirements for rest days, hours of work and other conditions of service, apply in respect of workmen who receive monthly basic salaries not exceeding S$4,500 and employees (other than workmen) who receive monthly basic salaries not exceeding S$2,600. Section 38(8) of the EA provides that an employee is not allowed to work for more than 12 hours in any one day except in specified circumstances, such as where the work is essential to the life of the community, defence or security. In addition, Section 38(5) of the EA limits the extent of overtime work that an employee can perform to 72 hours a month. An employer who breaches the above provisions shall be guilty of an offence and shall be liable on conviction to a fine not exceeding S$5,000, and for a second or subsequent offence to a fine not exceeding S$10,000 or to imprisonment for a term not exceeding 12 months or to both, pursuant to Section 53 of the EA. Employment of Foreign Manpower Act The employment of foreign workers in Singapore is governed by the Employment of Foreign Manpower Act 1990 (2020 Revised Edition) (the “EFMA”) and is regulated by the MOM. In Singapore, under Section 5(1) of the EFMA, no person shall employ a foreign employee unless he has obtained a valid work pass which allows the foreign worker to work for him. Section 5(6) of the EFMA provides that any person who fails to comply with or contravenes Section 5(1) of the EFMA shall be guilty of an offence and shall (a) be liable on conviction to a fine not less than S$5,000 and not more than S$30,000 or to imprisonment for a term not exceeding 12 months or to both; and (b) on a second or subsequent conviction, (i) in the case of an individual, be punished with a fine of not less than S$10,000 and not more than S$30,000 and with imprisonment for a term of not less than one month and not more than 12 months; or (ii) in any other case, be punished with a fine not less than S$20,000 and not more than S$60,000. An employer of foreign workers is also subject to, amongst others, the provisions set out in the EA, the EFMA, the Immigration Act 1959 of Singapore (2020 Revised Edition) (the “Immigration Act”) and the regulations issued pursuant to the Immigration Act. Central Provident Fund Act The Central Provident Fund (the “CPF”) system is a mandatory social security savings scheme funded by contributions from employers and employees. Pursuant to the Central Provident Fund Act 1953 of Singapore (2020 Revised Edition) (the “CPFA”), an employer is obliged to make CPF contributions for all employees who are citizens or permanent residents of Singapore who are employed in Singapore under a contract of service and employed under a permanent, part-time or casual basis (with the exception of a contract of service or other agreement entered into in Singapore as a master, a seaman or an apprentice in any vessel where the owners have been exempted from the provisions of the CPFA). CPF contributions are required for both ordinary wages and additional wages (subject to the respective CPF contribution ceilings) of employees at the applicable prescribed rates which are dependent on, inter alia, the amount of monthly wages and the age of the employee. Ordinary wages are wages due wholly or exclusively for an employee’s employment in a month and are payable before the due date of CPF contributions for that month, whereas additional wages are wages which are not granted wholly and exclusively for the employment in a month, such as annual bonus and leave pay. Under Section 7 of the CPFA, an employer shall pay both the employer’s and employee’s shares of the monthly CPF contribution. However, pursuant to Section 7(2) of the CPFA, an employer is entitled to recover its employee’s share of the CPF contribution by deducting such a share from the wages of the employee. An employer who fails to pay the CPF contributions in accordance with the CPFA shall be guilty of an offence and may be liable on conviction to a fine not exceeding S$10,000 or to imprisonment for a term not exceeding 7 years or to both, pursuant to Section 7(3) of the CPFA. Personal Data Protection Act The Personal Data Protection Act 2012 (2020 Revised Edition) (“PDPA”) is the main legislation governing the protection and handling (collection, storage, use or onward disclosure) of personal data in Singapore. The PDPA also established the Personal Data Protection Commission (“PDPC”) to administer and enforce the PDPA. Under Section 2 of the PDPA, “personal data” means any data, whether true or not, about an individual who can be identified from that data, or from that data and some other information to which an organization has or is likely to have access. Under the PDPA, an organisationorganization will have to comply with the following general obligations when dealing with personal data: | (a) | obtain the consent of the individual before collecting, using or disclosing his personal data for a purpose. Consent is not considered given unless the purpose of the collection, use or disclosure is notified to the individual and his consent is obtained in relation to such notified purpose; |

| (b) | collect, use or disclose personal data about an individual only for purposes that a reasonable person would consider appropriate and, if applicable, have been notified to the individual concerned; |

| (c) | notify the individual of the purposes for which an individual’s personal data is intended to be collected, used or disclosed on or before such collection, use or disclosure; |

| (d) | give an individual reasonable access to his or her own personal data which the organization has in its possession or control (including informing the individual of the ways in which his personal data has been used or disclosed over the past year); |

| (e) | correct errors and omissions in the personal data of an individual if the individual so requests; |

| (f) | make reasonable effort to ensure that personal data collected by it is accurate and complete; |

| (g) | take reasonable security measures to protect the personal data from unauthorised access, collection, use, disclosure, tampering or disposal, and the loss of any storage medium or device on which the personal data is stored; |

| (h) | not retain personal data or to remove the means by which personal data can be associated with particular individuals, as soon as it is reasonable to assume that the original purpose of the collection is no longer served by retention and that retention is also no longer needed for legal or business purposes; |

| (i) | ensure that when personal data is transferred out of Singapore to another country, a standard of protection comparable to that under Singapore law is given to the transferred personal data; |

| (j) | notify the PDPC of a data breach that results in or is likely to result in significant harm to an affected individual or that is or is likely to be of a significant scale; and |

| (k) | implement policies and procedures to comply with the PDPA and to make information about such policies and procedures publicly available. |

In addition to the obligations above, the PDPA has also established a Do-Not-Call Registry (“DNC Registry”) under Part 9 of the PDPA, which allows individuals to register their Singapore telephone numbers to opt out of receiving marketing phone calls, mobile text messages and faxes from organisations. Under Section 43 of the PDPA, no person shall send a “specified message” addressed to a Singapore telephone number unless it has been confirmed that the number is not listed on the relevant DNC Registry. A “specified message” is defined as one that, among others, relates to offering, supplying, advertising or promoting any goods, service, land, interest in land, business opportunity or investment opportunity.

If the PDPC finds that an organisation hasorganization intentionally or negligently failedfails to comply with its obligations under the PDPA, it may require, by written notice,will be liable under Sections 48J(1)(a) and 48J(3) of the organisationPDPA to pay a financial penalty. In the casepenalty of organisations, the amount of financial penalty will be up to S$1 million (or in due course, up to S$1 million or 10% of the organisation’sthat organization’s annual turnover in Singapore whichever is higher). (where the organization’s annual turnover in Singapore exceeds S$10 million), or S$1 million in any other case. In any case, whenever there isall instances of non-compliance, the PDPC has the power under Section 48I(2) of the PDPA to issue binding directions to organisationsdirect organizations to stop collecting, using or disclosing personal data in contravention of the PDPA, to destroy personal data collected in contravention of the PDPA, or to comply with any direction of the PDPC to provide access to or to correct personal data. Failure to comply with the requirements of the PDPA may also separately attract civil liability. A person who suffers loss or damage directly as a result of a breach by an organization of various provisions of the PDPA is able under Section 48O to bring an action against the organisationorganization in a civil court for compensation. In addition to the obligations above, the PDPA also established a Do-Not-Call Registry (“DNC Registry”) under Part 9 of the PDPA, which allows individuals to register their Singapore telephone numbers to opt out of receiving marketing phone calls, mobile text messages and faxes from organizations. Under Section 43 of the PDPA, no person shall send a “specified message” addressed to a Singapore telephone number unless it has been confirmed that the number is not listed on the relevant DNC Registry. A “specified message” is one that, among others, purports to offer to supply or advertise or promote goods and services. Any person who fails to confirm that a Singapore telephone number is not listed in the DNC Registry, prior to sending a specified message to that number, will be liable to a fine of up to S$10,000 or imprisonment for a term of up to 3 years or to both. Laws and Regulations Relating to Companies in Singapore Our Singapore subsidiary, FutuMoomoo Financial Singapore, is incorporated and governed under the provisions of the Companies Act 1967 of Singapore (2020 Revised Edition) (the “Companies Act”). The Companies Act generally governs, amongst others, matters relating to the status, power and capacity of a company, shares and share capital of a company (which includes issue of new shares (including preference shares), treasury shares, share buybacks, redemption, share capital reduction), declaration of dividends, financial assistance, directors and officers and shareholders of a company (including meetings and proceedings of directors and shareholders, dealings between such persons and the company), protection of minority shareholders’ rights, accounts, arrangements, reconstructions and amalgamations, winding up and dissolution. Members of a company are also subject to, and are bound by the provisions in its constitution. In addition, members of a company are subject to, and bound by, the provisions of the constitution of the company. The constitution of a company contains, inter alia, provisions relating to some of the matters in the foregoing paragraph, transfers of shares as well as sets out the rights and privileges attached to the different classes of shares of the company (if applicable). Dividend Distributions Our operations in Singapore are conducted via our Singapore subsidiary, Futu Singapore.Moomoo Financial Singapore, which has limited revenue contribution during the past three years. Pursuant to Section 403 of the Companies Act, dividends are only payable out of profits. Typically, the directors will recommend a particular rate of dividend and the company in general meeting will declare the dividend subject to the maximum recommended by the directors. Singapore adopts a one-tier corporate tax system under which the tax collected from corporate profits is a final tax and the after-tax profits of a company resident in Singapore can be distributed to its shareholders as tax-exempt dividends. Such dividends are tax-exempt in the hands of the shareholders, irrespective of whether the shareholder is a company or an individual and whether or not the shareholder is a Singapore tax resident. Singapore does not currently impose withholding tax on dividends paid to resident or non-resident shareholders. Singapore Taxation The following summary of the laws and regulations relating to taxation in Singapore is based on laws, regulations and interpretations presently in effect. The laws, regulations and interpretations, however, may change at any time, and any change could be retroactive. These laws and regulations are also subject to various interpretations and the relevant tax authorities or the courts of Singapore may later disagree with the explanations or conclusions set out below. This summary is not intended to constitute a complete or exhaustive description of all of the Singapore tax considerations and do not purport to deal with the tax consequences applicable to all categories of investors of the notes. It is not intended to be and does not constitute legal or tax advice. Corporate Income Tax The prevailing corporate tax rate in Singapore is 17% with effect from Year of Assessment 2010. In addition, the partial tax exemption scheme for Year of Assessment 2019 and before applies on the first S$300,000 of normal chargeable income; specifically 75% of up to the first S$10,000 of a company’s normal chargeable income, and 50% of up to the next S$290,000 is exempt from corporate tax. Starting from Year of Assessment 2020, the partial tax exemption scheme applies on the first S$200,000 of a company’s normal chargeable income; specifically 75% of up to the first S$10,000 of a company’s normal chargeable income, and 50% of up to the next S$190,000 is exempt from corporate tax. The remaining chargeable income (after the partial tax exemption) will be taxed at 17%. For the Years of Assessment 2019 and 2020, companies will be granted a corporate income tax rebate of 20% and 25% respectively of the tax payable for the year of assessment, subject to a cap of S$10,000 and S$15,000 respectively per year of assessment. Singapore has a tax exemption scheme for new start-up companies to support entrepreneurship and help the growth of local enterprises. Where any of the first three (3) years of assessment falls in or after Year of Assessment 2020, there will be 75% exemption on the first S$100,000 of normal chargeable income, and a further 50% exemption on the next S$100,000 of normal chargeable income. FutuAccordingly, Moomoo Financial Singapore is subject to Singapore corporate income tax at a rate of 17%.

Goods and Services Tax (“GST”GST”) GST in Singapore is a consumption tax that is levied on import of goods into Singapore, as well as nearly all supplies of goods and services in Singapore at a prevailing rate of 7%.9% since January 1, 2024. Overview of the Laws and Regulations Relating to Our Business and Operations in Australia AFSL Obligations Under section 911A(1) of the Corporations Act 2001 in Australia, or the Corporations Act, a person who carries on a financial services business in Australia must generally hold an Australian financial services license, or AFSL, unless a relevant exception applies. Relevant AFSL Holder Futu Securities (Australia) Ltd, a fully-owned subsidiary of Futu Holding Limited, holds an AFSL, under which it is authorised to provide various financial services to both retail and wholesale clients in Australia, including but not limited to: provide general financial advice and dealing service on securities, derivatives, foreign exchange contracts, government bonds, deposit products and managed investment schemes (such as mutual funds), and provide custodial or depository services. Substantive Obligations As an AFSL holder, Futu Securities (Australia) Ltd is subject to the following obligations (among others): | ● | To adhere to various financial, capital, and audit requirements; |

| ● | To ensure that its representatives who provide financial services are adequately trained and competent to do so; |

| ● | To comply with the "client money" rules outlined in Chapter 7.8 of the Corporations Act; |

| ● | To maintain accurate financial and order records as required by Chapter 7.8 of the Corporations Act; |

| ● | To implement adequate compliance arrangements for the financial services provided; |

| ● | To have sufficient financial, technological, and human resources to provide the licensed financial services; |

| ● | To comply with Australian financial services laws and take reasonable measures to ensure that its representatives do so; |

| ● | To ensure that regulated activities in Australia are provided efficiently, honestly, and fairly; |

| ● | To implement adequate conflict of interest management arrangements; |

| ● | To have appropriate risk management systems in place; and |

| ● | To report significant breaches of Australian financial services laws and AFSL conditions to the Australian Securities and Investments Commission. |

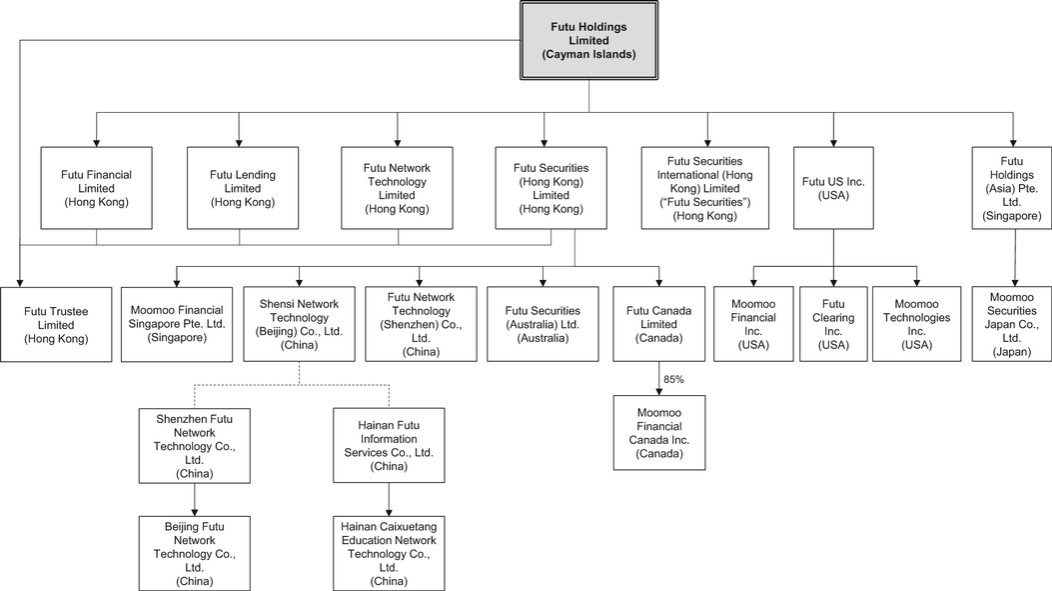

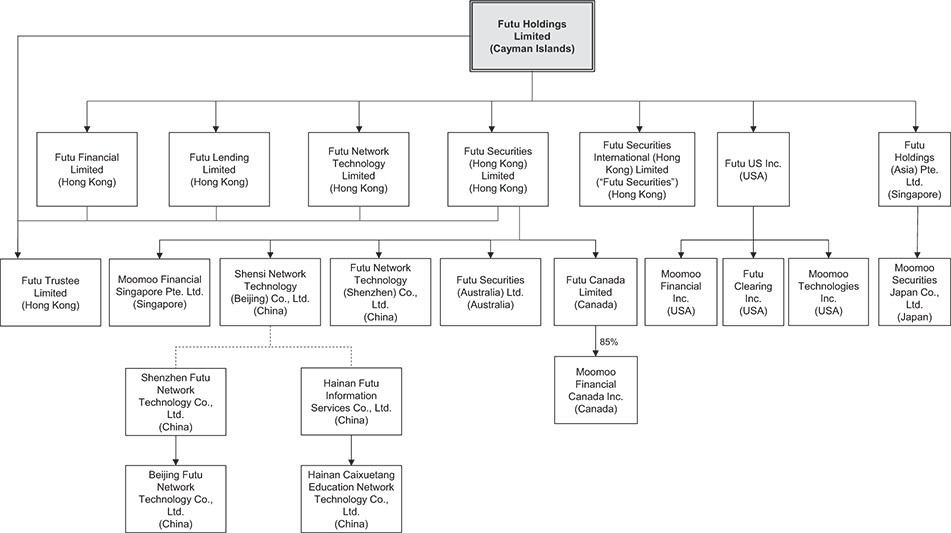

C. Organizational Structure The following diagram illustrates our corporate structure, including our significant subsidiaries and the VIE,Consolidated Affiliated Entities, as of the date of this annual report:

Note:Notes:

(1) | “➝” denotes direct legal and beneficial ownership in equity interest (100% ownership unless otherwise indicated). |

(2) | “┈” denotes the contractual arrangements that provide the WFOE with the ability to direct the activities of the Consolidated Affiliated Entities through (i) the powers of attorney to exercise all shareholders’ rights of the registered shareholders in the VIEs; (ii) exclusive options to acquire all or part of the equity interest in the VIEs; and (iii) equity pledges by the registered shareholders in favor of the WFOE over the equity interests in the VIEs. |

(3) | As of December 31, 2023, Shenzhen Futu Network Technology Co., Ltd. held a Valued-added Telecommunication Business Operation License, or an ICP License, a Radio and Television Program Production and Operation License and an Internet Culture Operation License; and Hainan Caixuetang Education Network Technology Co., Ltd. held an Internet Culture Operation License, a Radio and Television Program Production and Operation License, an ICP License and a Publication Operation License. |

(4) | Mr. Leaf Hua Li and Ms. Lei Li hold 85% and 15% equity interests, respectively, in each of Shenzhen Futu respectively.Network Technology Co., Ltd. and Hainan Futu Information Services Co., Ltd. Mr. Li is theour founder, chairman of board of directors and chief executive officer of our company andofficer. Ms. Lei Li is Mr. Li’s spouse. |

(2)(5)

| Each of Futu Holdings Limited, Futu Financial Limited, Futu Lending Limited, Futu Network Technology Limited and Futu Securities (Hong Kong) Limited owns 20% of the share capital in Futu Trustee Limited. |

(6) | Moomoo Financial Singapore Pte. Ltd. was formerly known as Futu Singapore Pte. Ltd.; Moomoo Financial Inc. was formerly known as Futu Inc.; and Moomoo Technologies Inc. was formerly known as Moomoo Inc. |

Contractual Arrangements with the VIEs and Their Shareholders A description of each of the specific agreements that comprise the Contractual Arrangements entered into by WFOE and each of the VIEs and their registered shareholders is set out below: Exclusive Business Cooperation Agreement. Under the exclusive business cooperation agreements dated September 30, 2021 between the VIEs and the WFOE (the “Exclusive Business Cooperation Agreements”), in exchange for a service fee, payable monthly, the VIEs agreed to engage the WFOE as its exclusive provider of certain technical and consulting services, including but not limited to (i) licensing of the relevant software, trademarks and technologies for use by the VIEs, (ii) providing development, maintenance and update of relevant application software required by the VIEs’ business, (iii) providing design, installation, daily management and maintenance, and update of VIEs’ computers, network software, hardware equipment and databases, (iv) providing technical support and training to personnel of the VIEs, (v) providing technical consultation and research for the VIEs, and (vi) other relevant services required by the VIEs’ business needs and in consideration of WFOE’s capacity as agreed between the parties. Under the Exclusive Business Cooperation Agreements, the service fee shall consist of 100% of the total consolidated profit of the VIEs, after the deduction of any accumulated deficit of the VIEs in respect of the preceding financial year(s), operating costs, expenses, taxes and other statutory contributions. Notwithstanding the foregoing, the WFOE may adjust the amount of the services fee in accordance with PRC tax law principles and tax practices and with reference to the operational needs of the VIEs, and the VIEs will accept such adjustment. The WFOE shall calculate the service fee on a monthly basis and issue a corresponding invoice to the VIEs. The VIEs must make the payment to the WFOE within ten business days of receiving such invoice. In addition, without the prior written consent of the WFOE, during the term of the Exclusive Business Cooperation Agreements, with respect to the services subject to the Exclusive Business Cooperation Agreements and other matters, the VIEs shall not accept the same or any similar services provided by any third party. In addition, without the prior consent of the WFOE, the VIEs shall not enter into any business cooperation with any third party, and the WFOE shall have the exclusive right of first refusal in respect of such business cooperation with the VIEs under the same terms. The Exclusive Business Cooperation Agreements also provide that the WFOE has the exclusive proprietary rights to and interests in any and all intellectual property rights developed or created by the VIEs during the performance of the Exclusive Business Cooperation Agreements. The Exclusive Business Cooperation Agreements shall remain effective unless otherwise terminated by the WFOE in writing or in accordance with the provisions of the Exclusive Business Cooperation Agreements. If, during the term of the Exclusive Business Cooperation Agreement, the operation period under the business license of either the WFOE or the VIEs expires and the renewal of which is declined or rejected by the relevant government authorities, the Exclusive Business Cooperation Agreements shall be terminated at the expiry of such operation period. Exclusive Option Agreement. As part of the Contractual Arrangements, with the VIE and Its Shareholders On September 30, 2021, a termination agreement was entered into among the WFOE, the VIE and its shareholders, pursuant to which the parties agreed to terminate the prior contractual arrangements and replaced it with a new set of agreements containing substantially the same terms. The following is a summaryeach of the currently effective contractual arrangements by and among the WFOE, the VIE and its shareholders. These contractual arrangements enable us to (i) exercise effective control over the VIE; (ii) receive substantially allregistered shareholders of the economic benefits of the VIE; and (iii) haveVIEs respectively entered into an exclusive option to purchase all or part of the equity interests in and/or assets of the VIE when and to the extent permitted by PRC laws.

Exclusive Business Cooperation Agreement. Pursuant to the exclusive business cooperation agreement entered into September 30, 2021 by and among the WFOE, the VIE and its shareholders, the VIE engages the WFOE as the exclusive service provider of technical support, consulting services and other services to the VIE. The VIE and its shareholders undertake that without the WFOE’s prior written consent, the VIE shall not directly or indirectly obtain from any third party any services identical to or similar to those provided by the WFOE under the agreement, and shall not enter into any similar partnership with any third party with respect to the matters described in the agreement. The VIE agrees to pay a service fee at an amount equivalent to 100% of the consolidated gross profits of the VIE for any fiscal year after offsetting the accumulated losses of the VIE and its subsidiaries in the previous fiscal years (if any) and after deducting working capital, expenditure, taxes and other statutory contributions required in any fiscal year . Unless otherwise terminated in accordance with the terms of this agreement or otherwise agreed by the WFOE, this agreement will remain effective. During the term of the agreement, each of the VIE and the WFOE shall renew its operation term prior to the expiration thereof so as to enable this agreement to remain effective. This agreement shall be terminated upon the expiration of the operation term of a party if the application for the renewal of its operation term is not approved by the relevant government departments.

Equity Interest Pledge Agreement. Pursuant to the equity interest pledge agreement entered into(the “Exclusive Option Agreements”) on September 30, 2021 bywith the VIEs and among the WFOE, the VIEeach of which contains similar terms and its shareholders, each shareholder of the VIE agrees that, during the term of this agreement, he or she will not dispose of the pledged equity interests or create or allow any encumbrance on the pledged equity interests without the prior written consent of the WFOE. The equity interest pledge agreement will remain effective until the latter of the full payment of all secured debt under the agreement and the VIE and its shareholders discharge all their obligations under the contractual arrangements. As of the date of this annual report, each shareholder of the VIE has completed registration of the pledge of his or her equity interest in the VIE to the WFOE.

Power of Attorney.conditions. Pursuant to the power of attorney entered into by and amongExclusive Option Agreements, the WFOE the VIE and its shareholders on September 30, 2021, each shareholder of the VIE irrevocably authorized the WFOE to exercise such shareholder’s rights in the VIE, including without limitation, the power to participate in and vote at the VIE’s shareholder’s meetings, the power to nominate and appoint the directors, senior management, and other shareholders’ voting rights permitted by the VIE’s articles of association.

Exclusive Option Agreement. Pursuant tohas the exclusive option agreement entered into on September 30, 2021, by and amongirrevocable right to require the WFOE, the VIE and itsregistered shareholders each shareholder of the VIE has irrevocably granted the WFOE an exclusive option, to the extent permitted by PRC laws and exercisable at the WFOE’s discretion attransfer any time, to purchase or designate another person to purchase all or part of such shareholder’stheir equity interests in the VIE. Unless PRC lawsVIEs to the WFOE and/or regulations require valuationany third party/parties designated by it, in whole or in part at any time and from time to time, at the lower of the VIE’s equity interests, the purchase price shall be the greater of (i) the actual amount of the registered shareholders’ respective paid-in capital paid byin the VIE’s shareholders in respect of the equity to be purchased or (ii)VIEs and the lowest price permitted by theunder applicable PRC laws.laws at the time. Each shareholder of the VIE undertakesregistered shareholders of the VIEs has covenanted that, without the prior written consent of the WFOE, he or she will not, among other things, (i) create any pledge or encumbrance on his or her equity interests in the VIE,VIEs, (ii) transfer or otherwise dispose of his or her equity interests in the VIE,VIEs, (iii) change the VIE’sVIEs’ registered capital, (iv) amend the VIE’sVIEs’ articles of association, (v) liquidate or dissolve the VIE,VIEs, or (vi) distribute dividends to the shareholders of the VIE.VIEs. In addition, each of the VIE undertakesVIEs and the respective registered shareholders of the VIEs has covenanted that, without the prior written consent of the WFOE, it will not, among other things, dispose of its material assets, provide any loans to any third parties, enter into any material contract (except for the contract concluded in the normal course of business), or create any pledge or encumbrance on any of its assets, or transfer or otherwise dispose of its material assets. This agreementThe Exclusive Option Agreements shall beremain effective unless otherwise terminated upon and only uponin the occurrence of any ofevent that the following circumstances: (i)entire equity interest in the WFOE unilaterally terminates this agreement in accordance with this agreement; (ii) all equity interestsVIEs held by the registered shareholders of the VIE or their respective successors or permitted transferees have been transferred to the WFOE and/or any other person designated by the WFOE in accordance with this agreement; and (iii)its appointee(s) or in accordance with the requirementsprovisions of the Exclusive Option Agreements.

Equity Pledge Agreement. As part of the Contractual Arrangements, each of the registered shareholders of the VIEs respectively entered into the equity pledge agreements (the “Equity Pledge Agreements”) on September 30, 2021 with the VIEs and the WFOE, each of which contains similar terms and conditions. Pursuant to the Equity Pledge Agreements, the registered shareholders have agreed to pledge all their respective equity interests in the VIEs that they own, including any dividend or distribution derived from the shares, to WFOE as a security interest to guarantee the performance of contractual obligations and the payment of outstanding debts. The pledges under the Equity Pledge Agreements have been effective upon completion of registration with the relevant administration for market regulation and shall remain valid until after all the contractual obligations of the registered shareholders of the VIEs and the VIEs under the relevant Contractual Arrangements have been fully performed and all the outstanding debts of the registered shareholders of the VIEs and the VIEs under the relevant Contractual Arrangements have been paid. Upon the occurrence and during the continuance of an event of default (as defined in the Equity Pledge Agreements), the WFOE shall have the right to exercise all such rights as a secured party under the Equity Pledge Agreements and any applicable PRC laws.law, including without limitations, being paid in priority with the equity interests based on the monetary valuation that such equity interests are converted into or from the proceeds from auction or sale of the equity interest upon written notice to the registered shareholders of the VIEs. The registrations of the Equity Pledge Agreements in relation to the VIEs had been completed. Power of Attorney.The registered shareholders have executed the powers of attorney dated September 30, 2021 (the “Powers of Attorney”). Under the Powers of Attorney, the registered shareholders irrevocably appointed the WFOE and its designated person(s) (including but not limited to the directors of our company and their successors and the liquidators replacing such directors or successors, but excluding those non-independent or who may give rise to conflict of interests) as their exclusive attorneys-in-fact to exercise on their behalf, any and all rights that they have in respect of their equity interests in the VIEs, including without limitation: (i) to convene and attend shareholders’ meetings of the VIEs and execute the relevant resolutions and meeting minutes; (ii) to file documents with the relevant companies registry; (iii) to exercise the voting rights and any power they are entitled to as shareholders of the VIEs under the applicable laws and the articles of association of the VIEs, including but not limited to the sale, transfer, pledge or disposal of all or part of his/her equity interest; and (iv) to nominate and appoint the legal representatives, directors, supervisors, general manager and other members of senior management of the VIEs. Further, the Powers of Attorney are irrevocable and shall remain effective for so long as each registered shareholder holds equity interests in the VIEs. Spousal Consent LettersUndertakings. The spousesspouse of each of the relevant registered shareholders, ofwhere applicable, has signed undertakings to the VIE have each signed a spousal consent letter. Under the spousal consent letter, the signing spouse unconditionally and irrevocably approved the execution by his or her spouse of the above-mentioned equity interest pledge agreement, exclusive option agreement and power of attorney, as applicable, andeffect that, his or her spouse may perform, amend or terminate such agreements without his or her consent. Moreover, the spouse confirmed he or among other things, (i) he/she has no rights, and will not assert in the future any right to or control over the equity interests in the VIEVIEs (together with any other interests therein) presently or in the future held by histhe respective registered shareholder and will not have any claim on such interests; (ii) the registered shareholder’s equity interests in the VIEs (together with any other interests therein) do not fall within the scope of communal properties; (iii) he/she has not participated, and does to plan to participate in, the day-to-day management and voting matters of the respective VIEs; (iv) he/she confirms that the respective registered shareholder may further amend or her spouse. terminate the Contractual Arrangements without the need for authorization or consent by him/her; and (v) if he/she is being transferred any shares held by their spouse for any reason, he/she will be bound by the Contractual Arrangements and will observe obligations as a shareholder of the VIEs, and will sign all necessary documents and to take all necessary actions to ensure the Contractual Arrangements are properly preformed. Dispute Resolution.Each of the agreements under the Contractual Arrangements contains a dispute resolution provision. Pursuant to such provision, in the event of any dispute arising from the performance of or relating to the Contractual Arrangements, any party has the right to submit the relevant dispute to the China International Economic and Trade Arbitration Commission (“CIETAC”) for arbitration, in accordance with the then effective arbitration rules. The arbitral tribunal shall consist of three arbitrators appointed in accordance with the arbitration rules, with the claimant and respondent each appointing one arbitrator and the third arbitrator being agreed and appointed by the first two arbitrators or by CIETAC. The seat of arbitration shall be in Beijing, and the arbitration award shall be final and binding on all parties. The dispute resolution provisions also provide that to the extent permitted by PRC law, the arbitral tribunal may award remedies over the shares or assets of the VIEs and its subsidiaries or injunctive relief (for example, limiting the conduct of business, limiting or restricting transfer or sale of shares or assets) or order the winding up of the VIEs. The WFOE may apply to the courts of the PRC, Hong Kong, the Cayman Islands (being the place of incorporation of our Company) and the places where the principal assets of the WFOE or the VIEs are located for interim remedies or injunctive relief in support of arbitration proceedings. During the arbitration, except for the disputed areas which are subject to arbitration, the parties shall continue to perform their other obligations under the Contractual Arrangements. In connection with the dispute resolution method as set out in the Contractual Arrangements and the practical consequences, we are advised by our PRC legal counsel, Han Kun Law Offices, that: (a) under PRC laws, an arbitral body does not have the power to grant any injunctive relief or provisional or final liquidation order for the purpose of protecting assets of or equity interest in the Consolidated Affiliated Entities in case of disputes. As such, these remedies may not be available to our Group under PRC laws; (b) further, under the PRC laws, courts or judicial authorities in the PRC generally would not award remedies over the shares and/or assets of the Consolidated Affiliated Entities, injunctive relief or winding-up of each of the Consolidated Affiliated Entities as interim remedies, before there is any final outcome of arbitration; (c) however, the PRC laws do not disallow the arbitral body to give award of transfer of assets of or an equity interest in each of the VIEs at the request of arbitration applicant. In the event of non-compliance with such award, enforcement measures may be sought from the court. However, the court may or may not support such award of the arbitral body when deciding whether to take enforcement measures; (d) in addition, interim remedies or enforcement orders granted by overseas courts such as Hong Kong and the Cayman Islands may not be recognizable or enforceable in the PRC; therefore, in the event we are unable to enforce the Contractual Arrangements, we may not be able to direct the activities that most significantly impact the economic performance of each of the Consolidated Affiliated Entities, and our ability to conduct our business may be negatively affected; and (e) even if the aforementioned provisions may not be enforceable under PRC laws, the remaining provisions of the dispute resolution clauses are legal, valid and binding on the parties to the agreement under the Contractual Arrangements. As a result of the above, in the event that the spouse obtainsVIEs or their respective registered shareholders breach any equity interestof the Contractual Arrangements, we may not be able to obtain sufficient remedies in a timely manner, and our ability to direct the activities of the Consolidated Affiliated Entities and conduct our business could be materially and adversely affected. See “Item 3. Key Information—D. Risk Factors—Risks Related to our Corporate Structure” for further details. Loss Sharing.Under the relevant PRC laws and regulations, none of our company and the WFOE is legally required to share the losses of, or provide financial support to, the Consolidated Affiliated Entities. Further, the Consolidated Affiliated Entities are limited liability companies and shall be solely liable for their own debts and losses with assets and properties owned by them. The WFOE intends to continuously provide to or assist the Consolidated Affiliated Entities in obtaining financial support when deemed necessary. In addition, given that our Group conducts a substantial portion of its operations in the VIE heldPRC through the Consolidated Affiliated Entities, which hold the requisite the PRC operational licenses and approvals, and that their financial position and results of operations are consolidated into our Group’s financial statements under the applicable accounting principles, our Company’s business, financial position and results of operations would be adversely affected if the Consolidated Affiliated Entities suffer losses. However, as provided in the Exclusive Option Agreements, without the prior written consent of WFOE, the VIEs shall not, among others, (i) sell, transfer, pledge or dispose of in any manner any material asset, business or revenue of the VIEs and their subsidiaries or the legal or beneficial interest therein, or allow the encumbrance thereon of any security interest; (ii) incur, inherit, guarantee or assume any debt, except for (a) debts incurred in the ordinary course of business other than payables incurred by hisway of a loan, and (b) intra-group debts between the VIEs and their respective subsidiaries; (iii) execute any material contracts, except the contracts executed in the ordinary course of business; (iv) provide any person with any loan or her spousecredit, except for the provision of loan or credit by the VIEs to their respective wholly-owned subsidiaries; and (v) enter into any reason, heconsolidation or she agrees to be boundmerger with any third party, or being acquired by and signor invest in any legal documents substantially similarthird party. Therefore, due to the contractual arrangements entered intorelevant restrictive provisions in the agreements, the potential adverse effect on the WFOE and our company in the event of any loss suffered from the VIEs can be limited to a certain extent. Conflict of Interests. Each of the registered shareholders of the VIEs has given their irrevocable undertakings in the Powers of Attorney which address potential conflicts of interests that may arise in connection with the Contractual Arrangements. For further details, see the sub-paragraph headed “—Powers of Attorney” above. Liquidation. Pursuant to the Equity Pledge Agreements, in the event of a mandatory liquidation required by histhe PRC laws upon the request of the WFOE, the registered shareholders of the VIEs shall transfer the proceeds they received from liquidation to the account designated by the WFOE under the management of the WFOE, or her spouse,give such proceeds as may be amended from timea gift to time.the WFOE or the party/parties designated by the WFOE to the extent permitted by the PRC laws. As a result of these contractual agreements,the Contractual Arrangements, we controldirect the activities and receive the economic benefits of the business operations of the VIE and its subsidiaries,Consolidated Affiliated Entities, which is not equivalent to equity ownership in the VIE and its subsidiaries. Under U.S. GAAP,Consolidated Affiliated Entities. We depend on these contractual arrangements to provide our subsidiary with a company is deemed“controlling financial interest” in the VIEs, as defined in FASB ASC 810, making it the primary beneficiary of and can consolidate the resultsVIEs, Terms contained in each set of a VIE when the company, or its subsidiary, through contractual arrangements haswith the powerVIEs and their respective shareholders are substantially similar, which enable our company to (1) direct the activities that most significantly impact the VIE’s economic performance, bearsand (2) receive the risks of and enjoyseconomic benefits from the rewards normally associated with ownership ofVIEs that could be significant to the VIE.VIEs. Accordingly, we areour company is considered the primary beneficiary of the VIEVIEs for accounting purposes and consolidate the financial results of the VIE and its subsidiariesConsolidated Affiliated Entities in our consolidated financial statements in accordance with U.S. GAAP. Neither we nor our investors own any equity ownership in, direct foreign investment in, or control of the VIEVIEs as a result of the WFOE’s contractual agreements with the VIE and its shareholdersContractual Arrangements and these agreementsarrangements have not been tested in a court of law in the PRC. These contractual arrangementsThe Contractual Arrangements may not be as effective as direct ownership in providing us with control over the VIE.power to direct the activities of the Consolidated Affiliated Entities. If the VIEVIEs or itsthe registered shareholders fail to perform their respective obligations under these contractual arrangements,the Contractual Arrangements, our recourse to the assets held by the VIEVIEs is indirect and we may have to incur substantial costs and expend significant resources to enforce such arrangements in reliance on legal remedies under PRC law. These remedies may not always be effective, particularly in light of uncertainties in the PRC legal system. Furthermore, in connection with litigation, arbitration or other judicial or dispute resolution proceedings, assets under the name of any of record holder of equity interest in the VIE,VIEs, including such equity interest, may be put under court custody. As a consequence, we cannot be certain that the equity interest will be disposed pursuant to the contractual arrangement or ownership by the record holder of the equity interest.

Based on the opinion ofabove, our PRC legal counsel, Han Kun Law Offices, ouris of the opinion that the Contractual Arrangements are narrowly tailored to minimize the potential conflict with relevant PRC legal counsel:laws and regulations to the maximum extent and that: | (i) | ● | each of the ownership structures of Shensi BeijingWFOE and the VIE will not result in any violation of applicableVIEs is a duly incorporated and validly existing company and their respective establishment is valid, effective and complies with the relevant PRC laws or regulations currently in effect; andlaws; |

| (ii) | ● | as confirmed by the contractual arrangements as a whole andparties to each of the agreements comprisingunder the contractual arrangements are legal, validContractual Arrangements, each of them has obtained all necessary approvals and authorizations to execute the agreements and perform their respective obligations thereunder. Each of such agreements is binding on the parties thereto and none of them is void or may become invalid pursuant to the Civil Code of the PRC; |

| (iii) | none of the agreement under the Contractual Arrangements violates any provisions of the respective articles of association of the VIEs or the WFOE; |

| (iv) | no approvals or authorizations from the PRC governmental authorities are required for the execution and performance of the Contractual Arrangements, except that: |

| a. | the exercise of the option by the WFOE or its designee of its rights under the Exclusive Option Agreements to acquire all or part of the equity interests in the VIEs is subject to the approvals of, consent of, filing with and/or registrations with the PRC governmental authorities; |

| b. | the equity pledges contemplated under the Equity Pledge Agreements are subject to the registration with the relevant state or local administration bureau for market regulation; |

| c. | the arbitration awards/interim remedies provided under the dispute resolution provision of the Contractual Arrangements shall be recognized by the PRC courts before compulsory enforcement; and |

| (v) | each of the agreements under the Contractual Arrangements is valid, legal and binding under the PRC laws, except that the Contractual Arrangements provide that the arbitral body may award interim remedies over the shares and/or assets of the VIEs, injunctive relief (such as for the conduct of business or to compel the transfer of assets) and/or order the winding up of the VIEs, and regulations currentlythat courts of Hong Kong, the Cayman Islands (being the place of incorporation of our company) and the PRC (being the place of incorporation of the VIEs) also have jurisdiction for the grant and/or enforcement of arbitral award and interim remedies against the shares and/or assets of the VIEs, while under PRC laws, an arbitral body has no power to grant injunctive relief and may not directly issue a provisional or final liquidation order for the purpose of protecting assets of or equity interests in effect.the VIEs in case of disputes. In addition, interim remedies or enforcement orders granted by overseas courts such as Hong Kong and the Cayman Islands may not be recognizable or enforceable in China. |

However, we have been further advised by our PRC legal counsel, Han Kun Law Offices, also advised us that there are substantial uncertainties regarding the interpretation and application of current and future PRC laws and regulations and rules.over the validity of the Contractual Arrangements. Accordingly, there can be no assurance that the PRC regulatory authorities maywill not in the future take a view that is contrary to or otherwise different from the above opinion of our PRC legal counsel, and there can be no assurance that the PRC government will ultimately take a view that is consistent with the opinion of our PRC legal counsel. It is also uncertain whether any new PRC laws, regulations or rules relating to the “variable interest entity” structure will be adopted and if adopted, what would be their impact on our contractual arrangements with the VIE.opinion. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Business and Industry—We depend on contractual arrangements with the VIE and its shareholders to operate a limited part of our operations in China, which may not be as effective as direct ownership in providing operational control” and “Item 3. Key Information—D. Risk Factors—Risks Related to Our Operations in China—If the PRC government deems that the contractual arrangements in relation to the VIE do not comply with PRC regulatory restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations.Corporate Structure.” D. Property, Plant and Equipment Our principal executivecorporate headquarters are located in Hong Kong. As of December 31, 2023, we leased 32 properties in China, Hong Kong, the United States, Singapore, Australia, Japan, Malaysia and Canada, with an aggregate gross floor area of over 44,000 square meters. Our leased properties are primarily used for corporate offices, are leased from independent third parties,data centers and other facilities. The relevant lease agreements have a term of two to seven and a half years. As of the date of this annual report, we plan to renew our lease from time to time as needed.owned one property in California, USA for corporate office purpose. A summary of our leased office premises as of December 31, 20212023 is included in the table below: | | | Location | | Size (in square meters) | Hong Kong |

| 1,7324,065

| Mainland China |

| 32,54935,823

| United States |

| 7671,533

| Singapore |

| 488811

| Australia | | 180374

| Japan | | 588 | Malaysia | | 914 | Canada |

| 296 |