0001114700ggal:ElectricityAndCommunicationsMember2022-01-012022-12-310001114700ggal:TransferFromStageOneToStageThreeMemberggal:WholesalePortfolioMemberifrs-full:AdvertisingAndMarketingMember2022-01-012022-12-310001114700ggal:StageOneMemberggal:MovementsWithProfitAndLossImpactMemberggal:TransferFromStageThreeToStageTwoMemberifrs-full:TwelvemonthExpectedCreditLossesMemberggal:RetailPortfolioMember2023-01-012023-12-310001114700ggal:RetailLikePortfolioMemberifrs-full:LifetimeExpectedCreditLossesMemberggal:StageThreeMember2022-01-012022-12-31StageThreeMemberggal:TransferFromStageThreeToStageOneMember2022-01-012022-12-31

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON APRIL 24, 202326, 2024

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________

FORM 20-F

__________________________

(Mark One)

| | | | | |

| o | Registration Statement pursuant to Section 12(b) or (g) of the Securities Exchange Act of 1934 |

or

| | | | | |

| x | Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

for the fiscal year ended December 31, 20222023

or

| | | | | |

| o | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

or

| | | | | |

| o | Shell Company Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

Commission File Number 000-30852

__________________________

GRUPO FINANCIERO GALICIA SA

(Exact name of Registrant as specified in its charter)

__________________________

GALICIA FINANCIAL GROUP

(Translation of Registrant’s name into English)

REPUBLIC OF ARGENTINA

(Jurisdiction of incorporation or organization)

Grupo Financiero Galicia SA

Tte. Gral. Juan D. Perón 430, 25th floor

C1038 AAJ - Buenos Aires, Argentina

(Address of principal executive offices)

Diego Rivas, Chief Financial Officer & Compliance

Tel: 54 11 4343 7528, / Fax: 54 11 4 331 9183, drivas@gfgsa.com

Perón 430, 25° Piso C1038AAJ Buenos Aires ARGENTINA

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

__________________________

Securities registered or to be registered pursuant to Section 12(b) of the Act:

American Depositary Shares, each representing ten Class B ordinary Shares

Name of each exchange on which registered

Nasdaq Capital Market

Title of each class

Class B Ordinary Shares, Ps.1.00 par value, (not for trading but only in connection with the listing of the American Depositary Shares on the Nasdaq Capital Market)

__________________________

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| American Depositary Shares, each representing the right to receive ten ordinary shares, par value Ps.1.00 per share New York Stock Exchange | | GGAL | | NASDAQ |

| Ordinary shares, par value Ps.1.00 per share* | | GGAL | | NASDAQ |

*Not for trading, but only in connection with the registration of the American Depositary Shares representing such ordinary shares on the NASDAQ.

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

__________________________

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

| | | | | | | | | | | |

| Class A Ordinary Shares, Ps.1.00 par value | 281,221,650 | |

| Class B Ordinary Shares, Ps.1.00 par value | 1,193,470,441 | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | | | | | | | | | | | | |

| Large Accelerated Filer | x | Accelerated Filer | o | Non-accelerated Filer | o |

| | | | | |

| | | | Emerging Growth Company | o |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards † provided pursuant to Section 13(a) of the Exchange Act. o

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive- based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| | | | | | | | | | | | | | | | | |

| U.S. GAAP | o | International Financial Reporting Standards | | Other | o |

| | | As issued by the International Accounting Standards Board | x | | |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

TABLE OF CONTENTS

PRESENTATION OF FINANCIAL INFORMATION

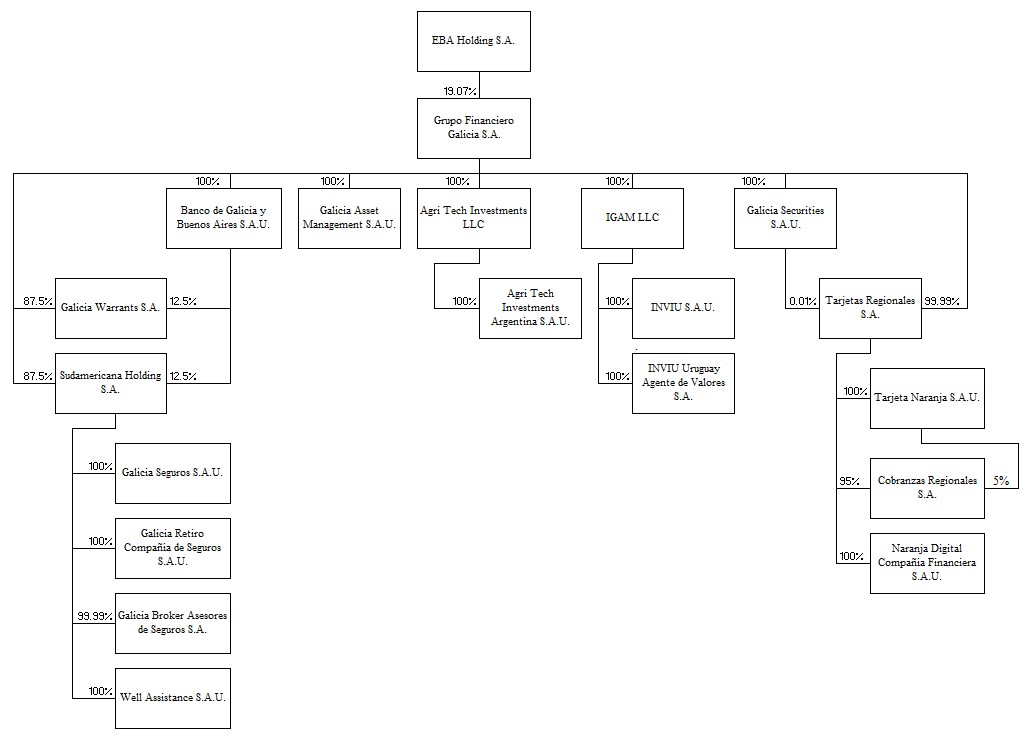

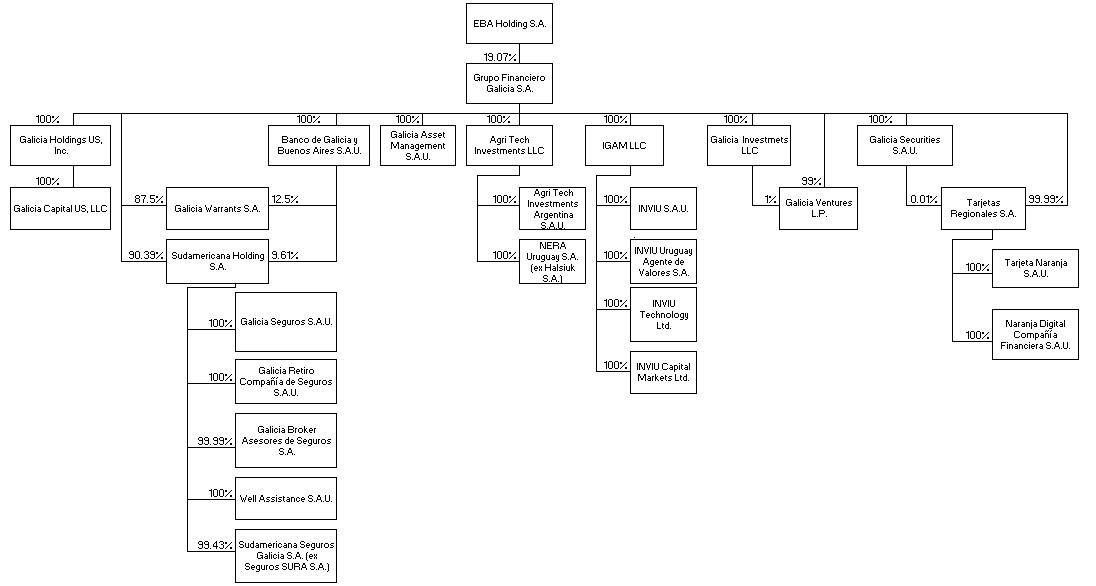

Grupo Financiero Galicia S.A. (“Grupo Financiero Galicia”, “Grupo Galicia”, “GFG” or the “Company”) is a financial services holding company incorporated in Argentina and is one of Argentina’s largest financial services groups. In this annual report, references to “we”, “our”, and “us” are to Grupo Financiero Galicia and its consolidated subsidiaries, except where otherwise noted. Our consolidated financial statements consolidate the accounts of the following companies:

•Grupo Financiero Galicia;

•Banco de Galicia y Buenos Aires S.A.U. (“Banco Galicia” or the “Bank”), our largest subsidiary;

•Tarjetas Regionales S.A. (“Tarjetas Regionales” or "Naranja X") and its subsidiaries;

•Sudamericana Holding S.A. (“Sudamericana”("Sudamericana Holding" or “Sudamericana”) and its subsidiaries;

•Galicia Warrants S.A. (“Galicia Warrants”);

•Galicia Asset Management S.A.U. (“Galicia Asset Management” or “Fima”);

•IGAM LLC (“IGAM" or "Inviu”) and its subsidiaries;

•Galicia Securities S.A.U. (“Galicia Securities”); and

•Agri Tech Investments LLC ("Agri Tech" or "Nera") and its subsidiaries.subsidiaries;

•Galicia Ventures LP ("Galicia Ventures");

•Galicia Investments LLC ("Galicia Investments"); and

•Galicia Holdings US, Inc. ("Galicia Holdings").

These consolidated financial statements have been prepared in accordance and in compliance with the International Financial ReportingIFRS Accounting Standards (“IFRS”) issued by the International Financial Reporting Standards Board (“IASB”) and the interpretations of the International Financial Reporting Interpretations Committee (“IFRIC”). IFRS in force as of the date of preparation of these consolidated financial statements for the fiscal years ended December 31, 2023, 2022 2021 and 20202021 have been applied. We maintain our financial books and records in Argentine Pesos and prepare our financial statements in conformity with IFRS, as issued by the IASB, effective as of the fiscal year beginning on January 1, 2018.

As of July 1, 2018, Argentina qualified as a hyperinflationary economy for accounting purposes. Grupo Galicia’s functional currency is the Argentine peso and its financial statements have been prepared in accordance with IAS 29 Financial Reporting in Hyperinflationary Economies as if the Argentine economy had always been hyperinflationary. The financial position and results of operations as of December 31, 20222023 and 20212022 and for the years ended December 31, 2023, 2022 2021 and 20202021 are reflected in terms of current purchasing power using the Consumer Price Index (“CPI”) as of December 31, 2022.2023.

In this annual report, references to “US$” and “Dollars” are to United States Dollars and references to “Ps.” or “Pesos” are to Argentine Pesos. The exchange rate used in translating Pesos into Dollars and used in calculating the convenience translations included in the following tables is the “Reference Exchange Rate” that is published by the Argentine Central Bank (commonly referred to as “BCRA” for its Spanish acronym) and that was Ps.808.4833, Ps.177.1283 Ps.102.7500 and Ps.84.1450Ps.102.7500 per US$1.00 as of December 31, 2022,2023, December 31, 20212022 and December 31, 2020,2021, respectively. The exchange rate translations contained in this annual report should not be construed as representations that the stated Peso amounts actually represent or have been or could be converted into Dollars at the rates indicated or at any other rate.

Our fiscal year ends on December 31, and references in this annual report to any specific fiscal year are to the twelve-month period ended December 31 of such year.

Unless otherwise indicated, all information regarding deposit and loan market shares and other financial industry information has been derived from information published by the BCRA, which is not adjusted according to the IAS 29.

We have expressed all amounts in millions of Pesos, except percentages, ratios, multiples and per-share data.

Certain figures included in this annual report have been rounded for purposes of presentation. Percentage figures included in this annual report have been calculated on the basis of such rounded figures. Certain numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them due to rounding.

FORWARD LOOKING STATEMENTS

This annual report contains forward-looking statements that involve substantial risks and uncertainties, including, in particular, statements about our plans, strategies and prospects under the captions Item 4. “Information on the Company”-A. “History and Development of the Company”-“Capital Investments and Divestitures,” Item 5. “Operating and Financial Review and Prospects”-A. “Operating Results-Principal Trends” and B. “Liquidity and Capital Resources.” All statements other than statements of historical facts contained in this annual report (including statements regarding our future financial position, business strategy, budgets, projected costs and management’s plans and objectives for future operations) are forward-looking statements. In addition, forward-looking statements generally can be identified by the use of such words as “may”, “will”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “continue” or other similar terminology. Although we believe that the expectations reflected in these forward-looking statements are reasonable, no assurance can be provided with respect to these statements. Because these statements are subject to risks and uncertainties, actual results may differ materially and adversely from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially and adversely from those contemplated in such forward-looking statements include, but are not limited to:

•changes in general political, legal, social or other conditions in Argentina, Latin America or other countries or regions;

•changes in the macroeconomic situation at the regional, national or international levels, and the influence of these changes on the microeconomic conditions of the financial markets in Argentina;

•changes in capital markets in general that may affect policies or attitudes toward lending to Argentina or Argentine companies, including expected or unexpected turbulence or volatility in domestic or international financial markets;

•financial difficulties of the Argentine government (“Government”) and its ability (or inability) to restructure or rollover its outstanding debt that is held by international credit entities;

•changes in Government regulations applicable to financial institutions, including tax regulations and changes in or failures to comply with banking or other regulations;

•volatility of the Peso and the exchange rates between the Peso and foreign currencies;

•fluctuations in the Argentine rate of inflation, including hyperinflation;

•increased competition in the banking, financial services, credit card services, insurance, asset management, mutual funds and related industries;

•Grupo Financiero Galicia’s subsidiaries’ inability to sustain or improve their performance;

•a loss of market share by any of Grupo Financiero Galicia’s main businesses;

•a change in the credit cycle, increased borrower defaults and/or a decrease in the fees charged to clients;

•changes in the saving and consumption habits of its customers and other structural changes in the general demand for financial products, such as those offered by Banco Galicia;

•changes in interest rates which may, among other things, adversely affect margins;

•Banco Galicia’s inability to obtain additional debt or equity financing on attractive conditions or at all, which may limit its ability to fund existing operations and to finance new activities;

•technological changes and changes in Banco Galicia’s ability to implement new technologies;

•impact of epidemics or pandemics (such as COVID-19 (oror other future outbreaks, epidemics or pandemics)outbreaks) on the global, regional and national economy, on financial activity, on global trade -both in terms of volumesvolume and prices-, and on the Company’s ability to recover from the negative effects of the pandemic (or other future outbreak);

•other factors discussed under Item 3. “Key Information” - D.“Risk Factors” in this annual report.

You should not place undue reliance on forward-looking statements, which speak only as of the date that they were made. Moreover, you should consider these cautionary statements in connection with any written or oral forward-looking statements that we may issue in the future. We do not undertake any obligation to release publicly any revisions to forward-looking statements after completion of this annual report to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

In light of the risks and uncertainties described above, the forward-looking events and circumstances discussed in this annual report might not occur and are not guarantees of future performance.

PART I

Item 1.Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3.Key Information

A. [Reserved]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

You should carefully consider the risks described below in addition to the other information contained in this annual report. In addition, most, if not all, of the risks described below must be evaluated bearing in mind that our most important asset is our equity interest in Banco Galicia. Thus, a material change in Banco Galicia’s shareholders’ equity or income statement would also adversely affect our businesses and results of operations. We may also face risks and uncertainties that are not presently known to us or that we currently deem immaterial, which may impair our business. Our operations, property and customers are located in Argentina. Accordingly, the quality of our customer portfolio, loan portfolio, financial condition and results of operations depend, to a significant extent, on the macroeconomic and political conditions prevailing in Argentina. In general, the risk assumed when investing in the securities of issuers from countries such as Argentina is higher than when investing in the securities of issuers from developed countries.

Risk Factors Relating to Argentina

The current state of the Argentine economy, together with uncertainty regarding the government, may adversely affect our business and prospects.

Grupo Financiero Galicia’s results of operations may be affected by inflation, fluctuations in the exchange rate, modifications in interest rates, changes in the Argentine government’s policies and other political or economic developments either internationally or in Argentina.

During the course of the last decades, Argentina’s economy has been marked by a high degree of instability and volatility, periods of low or negative economic growth and high, fluctuating levels of inflation and currency devaluation. Grupo Financiero Galicia’s results of operations, the rights of holders of securities issued by Grupo Financiero Galicia and the value of such securities could be materially and adversely affected by a number of possible factors. Some of these factors include Argentina’s inability to achieve a sustainable economic growth path, high inflation rates, Argentina’s ability to obtain financing, a decline in the international prices for Argentina’s main commodity exports, fluctuations in the exchange rates of other countries (which affects local commercial competitiveness) and the vulnerability of the economy to external shocks.

During the past decade Argentina experienced economic stagnation as a result of unstable monetary, fiscal and economic regulatory policies. This, combined with a lack of institutional transparency, led to increasing inflation rates, lack of economic growth, currency instability and low investment levels, among others. As there will be Argentine Presidential and Congressional elections in 2023, additional risks may arise if new policies are implemented by the newly elected Government that further exacerbate the existing macroeconomic imbalances (as described herein). In addition to such possible new

possible new policies, no assurance can be provided regarding other events, such as the enactment of other governmental policies, that may occur in the future and their impact on the Argentina economy and on the results of Grupo Financiero Galicia’s operations.

As a result of the current state of the Argentine economy as described above and herein and the uncertainty regarding the Government and policies it may enact, the financial position and results of operations of private sector companies in Argentina, including Grupo Financiero Galicia, the rights of the holders of securities issued by such institutions and the value thereof may be negatively and adversely impacted.

Economic conditions in Argentina may deteriorate, which may adversely impact Grupo Galicia’s business and financial condition.

Economic conditions in Argentina may deteriorate. In particular, a less favorable international economic environment, a decrease in the competitiveness of the Peso as compared to foreign currencies, low consumer confidence and low confidence from both local and foreign investors together with high inflation rates, among other factors, may affect the development and growth of the Argentine economy and cause volatility in the local capital markets. Such events may adversely impact Grupo Financiero Galicia’s business and financial condition.

In particular, the Argentine economy has proven to be and continues to be vulnerable to several factors, including:

•economic growth rate volatility;

•high inflation rates;

•regulatory uncertainty for certain economic activities and sectors;

•volatility in Argentina's main export commodities’ prices. The economic recovery has depended in the past, in part, on the high prices of commodities produced by Argentina, which are volatile and beyond the control of the Government;

•The stability and competitiveness of the Peso with respect to other currencies;

•external financial conditions;

•fluctuations in the BCRA’s international reserves; and

•uncertainty with respect to exchange and capital controls

No

We cannot provide assurance can be provided that a decline in economic growth or certain economic instability will not occur. Any stagnation, slowdown or economic and political instability could have a significant adverse effect on Grupo Financiero Galicia’s business, financial position and results of operations, and the trading price for its ADSs.

The ability of the current administration to implement economic policy reforms, and the impact that these measures and any future measures taken by a new administration will have on the Argentine economy, remains uncertain.

As of the date of this annual report, the impact that the reforms adopted by the Government will have on the Argentine economy as a whole, and the financial sector in particular, cannot be predicted. In addition, it is currently unclear what additional measures the current administration may implement in the future and what the effects of the same may be on the Argentine economy.

For example, foreign exchange market (the “FX market”) restrictions, in combination with a relatively loose monetary and fiscal policy and additional restrictions on foreign trade could result in lower economic growth rates in Argentina for the coming years.

It is impossiblenot possible to predict the impact of these measures, as well as any present or future measures that may be adopted will have on the Argentine economy overall and the financial sector in particular.

In particular, interventionist measures

Measures adopted by the Government or future measures implemented may be disruptive to the economy and may fail to benefit, or may harm, our business. In particular, Grupo Financiero Galicia has no control over the implementation of reforms to the regulatory framework that governs its operations and cannot guarantee that these reforms will be beneficial, will be implemented or that they will be implemented in a manner that will benefit its business. The failure of these measures to achieve their intended goals could adversely affect the Argentine economy and Grupo Financiero Galicia’s business, financial position and results of operations and the trading price for its ADSs.

If high levels of inflation continue, the Argentine economy and Grupo Galicia’s financial position and business could be adversely affected.

Since 2007, Argentina has experienced increasing inflation rates. Moreover, between 2007 and 2015 official figures became unreliable and private estimates of inflation were more frequently used.

Specifically, the national statistics agency INDEC (Instituto Nacional de Estadística y Censos; “INDEC” for its acronym in Spanish), is the only institution in Argentina with legal power to produce official national statistics.

Despite the fact that, due to the reforms implemented in recent years,since 2016, current inflation rates calculated by INDEC are generally accepted, the possibility that they may be manipulated in the future cannot be ruled out. Any such future manipulation could affect the Argentine economy in general and the financial sector in particular.

In addition to concerns related to the trustworthiness of inflation figures, in the past, inflation has materially undermined the Argentine economy and the Government’s ability to generate conditions that fostered economic growth. In particular, high inflation rates or a high level of volatility with respect to the same, may materially and adversely affect the business volume of the financial system and prevent the growth of financial intermediation activity. This, in turn, could adversely affect economic activity and employment levels in Argentina.

Combined with high inflation rates, Argentina has also displayed high volatility in its currency valuation, as a consequence of local imbalances and external shocks. Both high inflation rates and high levels of volatility in the inflation rate affectimpact Argentina’s competitiveness abroad, as well as real salaries, employment rates, consumption rates and interest rates. A high level of uncertainty with regard to these economic variables, and lack of stability in terms of inflation, could lead to shortened contractual terms and affect the ability to plan and make decisions. This may have a negative impact on economic activity and the income of consumers and their purchasing power. All of the above could materially and adversely affect Grupo Financiero Galicia’s financial position, results of operations and business, and the trading price for its ADSs.

Argentina’s and Argentine companies’ ability to obtain financing and to attract direct foreign investment is limited and may adversely affect Grupo Galicia’s financial position, results of operations and business.

In the past, Argentina has had and Argentine companiescontinues to have had limited access to foreignexternal financing, in recent years, primarily as a result of a default in December 2001 by Argentina on itsand has had different debt torestructuring processes with foreign bondholders, multilateral financial institutions and other financial institutions. In September 2020, Argentina settled all of its outstandingrenegotiated debt terms with foreign bondholders. In March 25, 2022, Argentina and the IMF in 2006, carried outInternational Monetary Fund signed an arrangement under the Extended Fund Facility, whereby a variety of debt swaps with certain bondholders between 2004 and 2010, and reached an agreement with the Paris Club in 2014. After several years of litigation, on March 1, 2016, an agreementcredit line was reached between the Argentine government and certain creditors to which the Argentine government was previously in default.

On April 18, 2016,granted in order to make a payment owedmeet payments under the Stand-By Arrangement signed in 2018 with the international organization.

Argentina has recently gained access to similarly situated bondholders, Argentina issued bonds in an amountadditional sources of US$16.5 billion, with interest rates between 6.25% and 8% and maturitiesfinancing, such as loans from the Development Bank of three, five, ten and thirty years. The payment of approximately US$9.3 billion to the bondholders was made on April 22, 2016, thus resolving the Argentine debt in default.

During the remainder of 2016, 2017Latin America and the first four monthsCaribbean and a currency swap with the People's Bank of 2018,China. In addition, the Argentine government continuedExtended Fund Facility Agreement with the International Monetary Fund is estimated to seekcontinue until December 31, 2024.

Notwithstanding the above mentioned recent but limited increased access to sources of financing, fromnew or more onerous regulations and restrictions that limit access to international markets. Followingfinancing for the exchange rate crisis beginningprivate sector could arise again in April 2018, however,the future. Such an event could have a negative impact on the Company's business, financial condition and results of operations. In addition, Argentina was not ablemay be unable to service its debt, may again be unable to access the international capital markets resulting in the Argentine government requesting a loan from the IMF (which was provided pursuant to a Stand-By Agreement in an amount equal to US$57 billion).

In 2019, the value of Argentina’s bonds plummeted and the country risk soared after the Primary Presidential Elections that took place on August 11, in which the Fernandez-Fernandez platform won by a landslide, resulting in the country being unable to refinance its existing debt with the private sector. As a result, the Macri administration that was then in office decided to unilaterally restructure the maturity dates on short-term debt issued by the Argentine Government, including debt denominated in Pesos and in Dollars. When President Fernandez took office, his administration commenced debt-restructuring negotiations for debt held by the Government that was held by foreign creditors. In March 2022, the Government entered into a new Extended Fund Facility with the IMF. Pursuant to said new agreement with the IMF the Government is able to request disbursements to be used to honor payments due under the 2018 Stand-By Agreement. The ability of the Government to receive such disbursements is conditioned on the Government meeting certain performance criteria. Failure by the Government to meet such criteria could result in the IMF no longer making disbursements under the

Extended Fund Facility, which would likely result in a failure by the Government to make payments due under the Stand-By-Agreement. Any such default on the IMF debt or other current outstandingsources of financing or may need to go through a debt of the Government would likely inhibit or prevent access by the Government and Argentine companies to the international financial markets and may also compromise the abilityrestructuring process again. All of such entities to obtain bilateral financing. This wouldscenarios could have an adverse effect on the Argentine economy includingand, consequently, on Grupo Financiero Galicia, and would likely cause a negative impact on the ability of companies, including Grupo Financiero Galicia, to obtain foreign financing.Galicia's operations.

A decline in the international prices of Argentina’s main commodity exports and a real appreciation of the Peso against the Dollar could affect the Argentine economy and create new pressures on the foreign exchange market, which, in turn, could have a material adverse effect on Grupo Galicia’s financial condition, prospects and operating results.

The Argentine economy’s reliance on the export of certain commodities, particularly soybeans and its by products, corn and wheat, has made the country more vulnerable to fluctuations in their prices. A decrease in commodity prices may adversely affect the Government’s fiscal revenues and the Argentine economy as a whole. Given its reliance on such agricultural commodities, the country is also vulnerable to weather events that may negatively affect production, reducing fiscal revenues and the inflow of Dollars derived from such exports.

In order to counterbalance and diversify its reliance on the above noted agricultural commodities as well as to add another source of revenue, Argentina has focused on increasing its oil and gas exports. A long-term decrease in the international price of oil would negatively impact such prospects and result in a decrease in foreign investment in such sectors.

Additionally, a significant increase in the real appreciation of the Peso could affect Argentina’s competitiveness. Such an increase could substantially affect the price (and thus attractiveness) of its exports, prompt new recessionary

pressures on Argentina’s economy, create a new imbalance in the foreign exchange market and exacerbate exchange rate volatility. A significant appreciation of the real exchange rate could adversely affect the Argentine public sector’s tax revenues in real terms. The occurrence of the foregoing could intensify the existing inflationary environment and potentially materially and adversely affect the Argentine economy, as well as Grupo Financiero Galicia’s financial condition and operating results and, thus, the trading prices for its ADSs.

Volatility in the regulatory framework could have a material and adverse effect on Argentina’s economy in general, and on Grupo Galicia’s financial position, specifically.

From time to time the Argentine government has enacted several laws amending the regulatory framework governing a number of different activities as a measure to stimulate the economy, some of which have had adverse effects on Grupo Financiero Galicia’s business. Although a formerthe new administration eliminated some of these regulations, political and social pressures could inhibit the Argentine government’s implementation of policies designed to generate growth and enhance consumer and investor confidence.

No assurance can be provided that future regulations, especially those related to the financial system, will not materially and adversely affect the assets, revenues and operating income of Argentine private sector companies, including Grupo Financiero Galicia, the rights of holders of securities issued by those entities, or the value of those securities. The lack of regulatory foresight could impose significant limitations on activities of the financial system and Grupo Financiero Galicia’s business, and thus generate uncertainty regarding its future financial position and result of operations and trading price for its ADSs.

The Argentine economy and its goods, financial services and securities markets remain vulnerable to external factors, which could affect Argentina’s economic growth and Grupo Galicia’s prospects.

The financial and securities markets in Argentina are influenced, to varying degrees, by economic and market conditions in other countries. Although such conditions may vary from country to country, investor reactions to events occurring in one country may affect capital flows to issuers in other countries, and consequently affect the trading prices of their securities. Decreased capital inflows and lower prices in the stock market of a country may have a material adverse effect on the real economy of those countries in the form of higher interest rates and foreign exchange volatility.

During periods of uncertainty in international markets, investors generally choose to invest in high-quality assets (“flight to quality”) over emerging market assets. This has caused and could continue to cause an adverse impact on the Argentine economy and could continue to adversely affect the country’s economy in the near future.

The monetary and fiscal policies implemented by the world’s leading economies, such as the US, China and the European Union have an affect on the Argentine economy through impacts on its interest rates, commodity prices and economic growth rates. Current higher interest rates in leading economies negatively affect emerging markets such as Argentina.

The economic activity of Brazil, one of Argentina’s main trade partners, also has an impact on Argentina’s economy. A depreciation of the Brazilian Real against the Dollar has in the past and would again in the future put additional pressure on the exchange rate for the Argentine Peso against the Dollar. Likewise, a weak economic performance from Brazil would affect Argentine exports, particularly in the case of industrial goods, many of which Argentina exports to Brazil.

Adverse climate conditions and events may also affect Argentina’s economy, either by negatively impacting the local harvest and thus reducing export volumes or by impacting other competing countries and affecting international commodities’ prices, which determine Argentine agricultural exports’ value.

The international financial environment may also result in a devaluation of regional currencies and exchange rates, including the Peso, which would also cause economic volatility in Argentina. A new global economic or financial crisis or the effects of deterioration in the current international context, could negatively affect the Argentine economy and, consequently, Grupo Financiero Galicia’s results of operations, financial conditions and the trading price for its ADSs.

A potential additional devaluation of the Peso may hinder or potentially prevent Grupo Galicia from being able to honor its foreign currency denominated obligations.

The Argentine Peso depreciated 90.1%98.2 % as compared to the Dollar between December 31, 2016 and December 2022,April 3, 2024, according to the official quotation of the BCRA. If the Peso further depreciates against the Dollar, as has recently occurred

and which could occur again in the future, this could have an adverse effect on the ability of Argentine companies to make timely payments on their debts denominated in or indexed or otherwise connected to a foreign currency, generate very high inflation rates, reduce real salaries significantly, and have an adverse effect on companies focused on the domestic market, such as public utilities and the financial industry. Such a potential devaluation could also adversely affect the Argentine government’s capacity to honor its foreign debt, with adverse consequences for Grupo Financiero Galicia’s and Banco Galicia’s businesses, which could, in turn, affect Grupo Financiero Galicia’s capacity to meet obligations denominated in a foreign currency. All of the foregoing could have a material adverse effect on the trading prices for Grupo Financiero Galicia’s ADSs.

Additionally, the BCRA may intervene in the foreign exchange market to influence exchange rates. Purchases of Pesos by the BCRA could result in a decrease of its international reserves. A significant decrease in the BCRA’s international reserves may have an adverse impact on Argentina’s ability to withstand external shocks to the economy, and any adverse effects to the Argentine economy could, in turn, adversely affect the financial position and business of Grupo Financiero Galicia and its subsidiaries.

In order to control the depreciation of the Peso, on September 1, 2019 the Executive Branch introduced capital controls, which allows the BCRA to exercise control over the Peso and therefore to prevent the Argentine currency from depreciating. Throughout 2020, 2021, 2022 and 2022,2023, the capital controls initially imposed in 2019 were bolstered while additional restrictions limited personal and corporate access to foreign currencies in the official market. A further depreciation of the Peso could adversely affect the Argentine economy and Grupo Financiero Galicia’s financial condition, its business, and its ability to service its existing debt obligations. Moreover, an acceleration of inflation caused by an exchange rate crisis would raise the costs associated with Grupo Financiero Galicia’s subsidiaries servicing their foreign currency-denominated debt. All or any of the above which could increase Grupo Financiero Galicia’s costs and therefore have a material adverse effect on Grupo Financiero Galicia’s financial condition and results of operations and, thus, the trading value of its ADSs.

Changes or new regulations in the Argentine foreign exchange market may adversely affect the ability and the manner in which Grupo Galicia repays its obligations denominated in, indexed to or otherwise connected to a foreign currency.

In the last two decades, different Argentine government administrations have established and implemented various restrictions on foreign currency transfers (both in respect of transfers into and out of Argentina).

The impact that these measures or potential future measures will have on the Argentine economy and Grupo Financiero Galicia is uncertain. No assurance can be provided that the current regulations will not be amended, or that no new regulations will be enacted in the future imposing greater limitations on funds flowing into and out of the Argentine foreign exchange market. Any such new measures, as well as any additional controls and/or restrictions, could materially adversely affect Grupo Financiero Galicia’s ability to access the international capital markets and may undermine its ability to make payments of principal and/or interest on its obligations denominated in a foreign currency or transfer funds abroad (in total or in part) to make payments on its obligations (which could negatively affect Grupo Financiero Galicia’s financial condition and results of operations). Therefore, Argentine resident or non-resident investors should take special notice of these regulations (and their amendments) that limit access to the foreign exchange market. In the future Grupo Financiero Galicia may be prevented from making payments in Dollars and/or making payments outside of Argentina due to the restrictions in place at that time in the foreign exchange market and/or due to the restrictions on the ability of Argentine companies to transfer funds abroad.

It may be difficult to effect service of process against Grupo Galicia’s executive officers and directors, and foreign judgments may be difficult to enforce or may be unenforceable.

Service of process upon individuals or entities which are not resident in the United States may be difficult to obtain in the United States. Grupo Financiero Galicia and its subsidiaries are companies incorporated under the laws of Argentina. Most of their shareholders, directors, members of the Supervisory Syndics’ Committee, officers, and some specialists named herein are domiciled in Argentina and the most significant part of their assets is located in Argentina. Although Grupo Financiero Galicia has an agent to receive service of process in any action against it in the United States with respect to its ADSs, none of its executive officers or directors has consented to service of process in the United States or to the jurisdiction of any United States court. As a result, it may be difficult to effect service of process against Grupo Financiero Galicia’s executive officers and directors. Additionally, under Argentine law, the enforcement of foreign judgments will only be allowed if the requirements in sections 517 to 519 of the National Code of Civil and Commercial Procedures or the applicable local code of procedures are met, and provided that the foreign judgment does not infringe on concepts of public policy in Argentine law, as determined by the competent courts of Argentina. As such, an Argentine court may find that the enforcement in Argentina of a foreign judgment (including a U.S. court) that requires payment be made by an Argentine individual to holders of its foreign currency-denominated securities outside of Argentina is contrary to the public policy if,

for instance, there are legal restrictions in place prohibiting Argentine debtors from transferring foreign currency abroad to pay off debts.

The intervention of the Argentine government in the electric power sector could have a material adverse impact on the Argentine economy, which may have a material adverse impact on Grupo Galicia’s results of operations.

Historically, the Argentine government has played an active role in the electric power sector through the holding and management of state-owned companies engaged in the generation, transmission and distribution of electric power. To address the Argentine economic crisis of 2001 and 2002, the Government adopted regulations which made several material changes to the regulatory framework applicable to the electric power sector and distorted supply and demand in the sector. These changes included the freezing of distribution margins, the reversal of adjustment and inflation indexation mechanisms for tariffs, a limitation on the ability of electric power distribution companies to pass on to the consumer increases in costs and the introduction of a new price-setting mechanism in the wholesale electricity market, all of which had a significant impact on electric power generators and caused substantial price differences within the market.

The Macri administration began significant reforms in the electric power sector. As part of such reforms, the administration took actions designed to guarantee the supply of electric power in Argentina, instructing the Ministry of Energy and Mining to develop and implement a coordinated program to guarantee the quality of the electric power system and ration individuals’ and public entities’ consumption of energy by increasing tariffs.

However, between 2019 and 2022,2023, the tariffs that electrical power companies can charge were kept virtually unchanged. As such, the increasing costs incurred by these electrical power companies that are not covered by the current tariffs have been paid for using governmental subsidies. This use of governmental subsidies instead of increases in tariffs has led to an increase in the level of public spending by the Government. In recent months, tariffs began a gradual recovery process in order to reduce subsidies, and are expected to continue rising until the subsidy reaches zero for the majority of the population, which could have a material adverse effect on inflation and, thus, on Argentine consumers’ disposable income and the financial and operating performance of Argentine companies. A similar situation has occurred or has been in effect with public transportation, which up until the current government, had been continuously subsidized. As of the date hereof, gradual adjustments are expected until the ride fare paid by the user reflects the true value of the ticket. The reduction of subsidies on the ride fares could have a material adverse effect on inflation and, thus, on Argentine users real income and the financial and operating performance of Argentine companies. As a result, itsuch aforementioned changes could, in turn, affect Grupo Financiero Galicia’s financial condition and results of operations and the trading price of our ADSs as well.

The measures adopted by the Argentine government and the claims filed by workers on an individual basis or as part of a labor union action may lead to pressures to increase salaries or additional benefits, which would increase companies’, including Grupo Galicia’s, operating costs. Additionally, labor union activity could lead to strikes or work stoppages, which may materially and adversely affect Grupo Galicia’s results of operations.

In the past, the Argentine government has passed laws and regulations requiring private sector companies to maintain certain salary levels and provide their employees with additional work-related benefits. Furthermore, employers, both in the public sector and in the private sector, have been experiencing intense pressure from their personnel, or from the labor unions representing such personnel, demanding salary increases and certain benefits for the workers, given the prevailing high inflation rates.

For example, duringin the early monthsrecent history of 2019Argentina there have been strikes promoted by the union representing Argentine union that represents banking sector employees declared general strikes. Thesebank employees. Some of these strikes did not have a direct effect on banks (including our principal subsidiary, Banco Galicia) but did impact banks’ clients who were not able to access branches. Strikes such as the one that took place in 2019Such strikes can also lower the perception the public has of banks, which could have a reputational cost for Banco Galicia (the main subsidiary of Grupo Galicia) and, consequently, for Grupo Galicia. Labor movements are active in Argentina and can potentially lead to further strikes or work stoppages if demands are not satisfied, which could have a material and adverse effect on Grupo Financiero Galicia’s operations and operating costs.

There can be no assurance that the Argentine government will not adopt measures in the future mandating salary increases or the provision of additional employee benefits, or that employees or their unions will not exert pressure on companies, such as Grupo Financiero Galicia or its subsidiaries, in demanding the implementation of such measures. The implementation of any such measures could have a material and adverse effect on Grupo Financiero Galicia’s expenses and business, results of operations and financial condition and, thus, on the trading prices for its ADSs.

High levels of public expenditures in Argentina could generate long lasting adverse consequences for the Argentine economy.

Since 2007, Argentina increased its spending to Gross Domestic Product (“GDP”) ratio to reach a maximum of 24% in 2015, quite above the ratio of the rest of the countries in the region. Between 2016 and 2019, a decreasing trend in expenditures was observed. However, in 2020 the spending-to-GDP ratio increased again, as the fiscal stimulus package implemented to deal with COVID-19 and the mobility restrictions resulting from COVID-19 put pressure on the fiscal balance and resulted in increased expenditures. In 2020, the primary deficit amounted to 6.5% of GDP and it was mainly financed by assistance from the BCRA. The primary deficit was reduced to 3.0% of GDP in 2021 and to approximately 2.5% of GDP in 2022. However, such reduction is insufficientthe primary deficit in 2023 increased to ensure debt sustainability.2.9% of GDP.

If the fiscal deficit is not reduced and debt financing is insufficient, the Government may be forced to continue its reliance on BCRA financing.

The lack of reduction in Argentina’s deficit could have a negative effect on the Government’s ability to access and incur the long-term debt in the financial markets, and in turn, could limit the access to such markets for Argentine companies, such as Grupo Financiero Galicia and its subsidiaries. The same may have a material and adverse effect on Grupo Financiero Galicia’s financial condition, results of operations and the trading price for its ADSs.

Exposure to multiple provincial and municipal tax legislation and regulations could adversely affect Grupo Financiero Galicia’s business or results of operations.

Argentina has a federal system of government with 23 provinces and the Autonomous City of Buenos Aires. Each of these, under the Argentine National Constitution, has full power to enact legislation concerning taxes. Likewise, within each province, municipal governments have broad powers to regulate said matters. Given that the bank branches of our primary subsidiary, Banco Galicia, are located in multiple provinces, we are subject to various provincial and municipal legislation and regulations that may vary from time to time. Future developments in provincial and municipal legislation concerning taxes, provincial regulations or other matters could have a material and adverse effect on Grupo Financiero Galicia’s expenses and business, results of operations and financial condition and thus the trading price for its ADSs could decrease.

Epidemics and pandemics, such as the COVID-19 pandemic, could have an adverse effect on our business operations.

In March 2020, the World Health Organization declared COVID-19 a pandemic. As a result, most countries adopted several measures to control the coronavirus, including the use of quarantine, lockdown and severe restrictions on the movement of their respective populations by certain air carriers and foreign governments. Variants of COVID-19 or anAn outbreak of another pandemic, or epidemics disease or similar public health threat could have material adverse effects on global economic, financial and business conditions, which could materially and adversely affect our business, financial condition and results of operations.

The long-term effects to the global economy and to Grupo Financiero Galicia of epidemics, pandemics and other public health crises, such as COVID-19, are difficult to assess or predict, and may include risks to employee’s health and safety, and reduce our business operations. Also, such long-term effects depend on several other factors which are uncertain (such circumstances may include further waves of infection, further variants of the Covid-19 virus, the lasting effects of vaccines, the global roll out of vaccination programs, the percentage of vaccinated population, possible lockdowns or other restrictions, and the speed and stability of the economic recovery, among others).

Epidemics, pandemics and other health crises, such as COVID-19, may negatively impact the business and operations of third-party service providers who perform services critical for our business. Furthermore, in such cases, the Government may impose certain measures such as travel restrictions, border closures and lock-downs, which may force us to set in place work from home arrangements for our employees and may also have a material impact on our ability to operate and achieve our business goals.

If the global and Argentine economies are unable to sustain the post-pandemic recovery, we may also experience higher default rates on our customer financing, liquidity shortfalls, and difficulties in our ability to service our debt and other financial obligations. We may also encounter difficulties in accessing the debt and capital markets and be forced to refinance pre-existing financing arrangements. Although the actual impact is impossible to assess, the occurrence of any of these events could have a material adverse effect on our operations.

Finally, it is unclear whether these challenges and uncertainties will increase or diminish, and what effects they may have on long-term global political and economic conditions. Moreover, we also cannot predict whether the recovery of the Argentine economy exhibited during 2022 can also be sustained during 2023. The impact of COVID-19 and other health crises could have a material and

adverse effect on Grupo Financiero Galicia’s business, results of operations, and financial condition and, therefore, on the trading prices of its ADSs.

Failure to adequately address actual and perceived risks arising from institutional deterioration and corruption could adversely affect Argentina’s economy and financial position and the ability of Argentine companies to attract foreign investment.

The lack of a solid institutional framework governing contracts entered into by the Government and its agencies and allegations of corruption have affected and continue to affect Argentina. The International Corruption Perceptions and Transparency Index, which measures corruption in 180 countries, has ranked Argentina No. 9498 in 2022, 2 places higher than in 2021, but maintaining the same2023, with a score of 3837 points out of a possible 100. In addition, as of the date of this report, Argentina has been invited to join the Organization for Economic Cooperation and Development (OECD). However, if the country is not able to carry out the reforms and assume the commitments required by this organization, its membership could be rejected. Failure to to address these issues could increase the risk of political instability and distort the decision-making process, adversely affecting Argentina’s international reputation and the ability of its companies to attract foreign investment.

A deterioration in the Argentine reputation could have a material and adverse effect on Grupo Financiero Galicia’s financial condition and results of operations and, thus, on the trading price for its ADSs.

The Argentine economy could be negatively affected by external factors, thatsuch us epidemics and pandemics, which have an impact in the whole world, such as the one COVID-19’s spread had, and the consequent implementation of measures destined to deal with the mentioned external factors, and their economic impact both on a local and an international level.

The Argentine economy is vulnerable to external factors. In this sense, most economies infactors the world (including Argentina and its main trade partners) were affected byArgentine government may adopt measures to protect the spread of COVID-19 during 2020 and 2021. The virus’

progression, which was declared a pandemic by the World Health Organization, led to the application of measures throughout 2020 and 2021 that had a severe economic impact.

In Argentina, these measures included the implementation of a generalized quarantine with the intention of hindering the virus’ spread and avoiding the collapsehealth of the local health system. This entailed a halt in most economic activities (excluding essential ones, such as healthcare services, manufacturing of food products, medical equipment or pharmaceuticals, supermarkets and pharmacies, and the provision of security forces) and the suspension of road and air travel, among others.population.

These measures, and any others the Argentine government mightmay implement in the future, could have had a negative and direct impact on the country’s economy, by reducing both aggregate supply and demand.

Additionally, the progression of the virus and the resulting measures destined to fight the virus affected economic growth in Argentina’s trade partners (such as Brazil, the European Union, China, and the United States). In 2020, the contraction of the economies of trade partners had a sizeable and adverse impact on Argentina’s trade balance and economy resulting in a decrease of 15.7% in the demand for Argentine exports as compared to the previous year.

Higher uncertainty levels associated with an unexpected external shock, such as a global pandemic, could exacerbate the volatility of financial conditions, particularly in emerging markets, which could pose a threat to Argentina’s currency and financing availability.

Any of these potential risks to the Argentine economy could have a material and adverse effect on Grupo Financiero Galicia’s business, results of operations and financial condition and, thus, on the trading prices for its ADSs.

Risk Factors Relating to the Argentine Financial System

The stability of the Argentine financial system is dependent upon the ability of financial institutions, including Banco Galicia, the main subsidiary of Grupo Galicia, to maintain and increase the confidence of depositors.

The measures implemented by the Argentine government in late 2001 and early 2002, in particular the restrictions imposed on depositors to withdraw money freely from banks and the “pesification” and restructuring of their deposits, were strongly opposed by depositors due to the losses on their savings and undermined their confidence in the Argentine financial system and in all financial institutions operating in Argentina.

If depositors once again withdraw their money from banks in the future, there may be a substantial negative impact on the manner in which financial institutions, including Banco Galicia (our main subsidiary), conduct their business, and on their ability to operate as financial intermediaries. Loss of confidence in the international financial markets may also adversely affect the confidence of Argentine depositors in local banks.

An adverse economic situation, even if it is not related to the financial system, could trigger a massive withdrawal of capital from local banks by depositors, as an alternative to protect their assets from potential crises. Any massive withdrawal of deposits could cause liquidity issues in the financial sector and, consequently, a contraction in credit supply.

The occurrence of any of the above could have a material and adverse effect on Grupo Financiero Galicia’s expenses and business, results of operations and financial condition and, thus, on the trading prices for its ADSs.

If financial intermediation activity volumes relative to GDP are not restored to significant levels, the capacity of financial institutions, including Banco Galicia, the main subsidiary of Grupo Galicia, to generate profits may be negatively affected.

As a result of the 1999-2002 financial crisis (in which the Argentine economy fell 18.4%), the volume ofvarious economic crises, financial intermediation activity dropped dramatically:has declined in Argentina; private sector credit plummeted from 24% of GDPloans and deposits have fallen both in December 2000 to 7.7% in June 2004volume and total deposits as a percentage of GDP fell from 31% to 23.2% during the same period.GDP. The depth of the crisis and the effect it had on depositors’ confidence in the financial system created uncertainty regarding its ability to act as an intermediary between savings and credit.

Furthermore, the ratio of the total financial system’s private-sector deposits and loans to GDP remains low when compared to international levels. Private-sector deposits and loans in pesos amounted to 18.1%17.2% and 8.0%8.1% of GDP, respectively, as of December, 31, 2022.2023.

There is no assurance that financial intermediation activities will continue in a manner sufficient to reach the necessary volumes to provide financial institutions, including Banco Galicia, with sufficient capacity to generate income, or that those actions will be sufficient to prevent Argentine financial institutions, such as Banco Galicia, from having to assume excessive risks in terms of maturity mismatches.

Under these circumstances and for an undetermined period of time, the (i) scale of the operations of Argentine-based financial institutions operating in Argentina, including Banco Galicia, (ii) volume of their business, volume, the(iii) size of their assets and liabilities or (iv) their income-generation capacityability to generate results, could be much lower than before the 1999-2002 crisis whichlimited and/or restricted, would may, in turn, impact the results of operations of Banco Galicia and potentially the trading price for Grupo Financiero Galicia’sGalicia's ADSs.

The Argentine financial system’s growth and income, including that of Banco Galicia, the main subsidiary of Grupo Galicia, depend in part on the development of medium- and long-term funding sources.

In spite of the fact that the financial system’s and Banco Galicia’s deposits continue to grow, they are mostly demand or short-term time deposits and the sources of medium- and long-term funding for financial institutions are currently limited. If Argentine financial institutions, such as Banco Galicia, are unable to access adequate sources of medium and long-term funding or if they are required to pay high costs in order to obtain the same and/or if they cannot generate profits and/or maintain their current volume and/or scale of their business, this may adversely affect Grupo Financiero Galicia’s ability to honor its debts. Additionally, this could negatively affect the trading prices for its ADSs.

Argentine financial institutions (including Banco Galicia) continue to have exposure to public sector debt (including securities issued by the BCRA) and its repayment capacity, which in periods of economic recession, may negatively affect their results of operations.

Argentine financial institutions continue to be exposed, to some extent, to public sector debt and the public sector’s repayment capacity. The Argentine government’s ability to honor its financial obligations is dependent on, among other things, its ability to establish economic policies that succeed in fostering sustainable growth and development in the long term, generating tax revenues and controlling public expenditures, which could, either partially or totally, fail to take place.

Banco Galicia’s (our main subsidiary) exposure to the public sector as of December 31, 20222023 was Ps.1,284,662Ps3,583,823 million, representing approximately 44%41% of its total assets and 256%217% of its shareholders’ equity. Of this total, Ps.754,870Ps.386,299 million were BCRA debt instruments, Ps.434,677Ps.2,132,387 million corresponded to Argentine governmentdebt securities issued by the public sector, and Ps.93,793Ps1,064,534 million corresponded to repurchase agreement transactions issued by the BCRA, swaps, while the remaining corresponded to other receivables resulting from financial brokerage. As a result, Grupo Financiero Galicia’s income-generating capacity may be materially impacted or may be particularly affected by the Argentine public sector’s repayment capacity and the performance of public sector bonds, which, in turn, is dependent on the factors referred to above.

The Consumer Protection Law may limit some of the rights afforded to Grupo Galicia and its subsidiaries.

Argentine Law No.24,240 (as amended by Law No. 26,361, Law No. 27,250, Law No. 27,265 and Law No. 27,266, the “Consumer Protection Law”) sets forth a series of rules and principles designed to protect consumers, which include Banco Galicia’s customers. Additionally, Law No.25,065 (as amended by Law No.26,010, and Law No.26,361, and the Decree of Necessity and Urgency No. 70/2023 the “Credit Card Law”) also sets forth public policy regulations designed to protect credit card holders. Additionally, the Civil and Commercial Code captured the principles of Consumer Protection Law and established their application to banking agreements.

Furthermore, Law No.26,993 created the “System to Solve Disputes in Consumer Relationships”, an administrative and legal procedure within the framework of the Consumer Protection Law; namely, an administrative and a

judicial regime for such matters. Additionally, the BCRA issued Communication “A” 6072, as supplemented and amended, granting broad protection to financial services customers, limiting fees and charges that financial institutions may validly collect from their clients.

The application of both the Consumer Protection Law and the Credit Card Law by administrative authorities and courts at the federal, provincial and municipal levels has increased. This trend has led to an increase in general consumer

protection levels. In the event that Grupo Financiero Galicia and/or its subsidiaries are found to be liable for violations of any of the provisions of the Consumer Protection Law or the Credit Card Law, the potential penalties could limit some of Grupo Financiero Galicia and its subsidiaries’ rights, for example, with respect to their ability to collect payments due from services and financing provided by Grupo Financiero Galicia or its subsidiaries, and adversely affect their financial results of operations. There can be no assurance that court and administrative rulings based on the regulation or measures adopted by the enforcement authorities will not increase the degree of protection given to its debtors and other customers in the future, or that they will not favor the claims brought by consumer groups or associations.

The implementation of the Consumer Protection Law, the Credit Card Law and other applicable regulations by administrative authorities and courts may prevent or hinder the collection of payments resulting from services rendered and financing granted by Grupo Financiero Galicia’s subsidiaries, which may have an adverse effect on their results and operations and, in turn, on the trading price for the ADSs.

The maintenance or implementation of measures regarding the charging of fees and regulated rates could materially and adversely affect Grupo Financiero Galicia’s consolidated financial condition and results of operations

The BCRA has various regulations regarding the fees and interest rates that entities can charge in the banking business. One of Grupo Financiero Galicia’s primary subsidiaries, Banco Galicia, is required to comply with the applicable regulations. Interest rates and regulated fees (e.g. setting caps on the rates and fees that an entity can charge its customers) could affect the interest rates and fees earned by Banco Galicia, which could result in a reduction in Grupo Financiero Galicia’s consolidated income or a decrease in customer demand for Banco Galicia’s loan or deposit products. In addition, if Banco Galicia were permitted to (and actually did) increase the interest rates and fees it charged (or if the same were otherwise raised by the BCRA or otherwise), such increases could result in higher debt service obligations for Banco Galicia’s customers; which could, in turn, result in higher levels of delinquent loans or discourage customers from borrowing. Interest rates and regulated fees are highly sensitive to many factors beyond Banco Galicia’s control, such as regulation of the financial sector in Argentina, domestic and international economic and political conditions, among other factors. Changes in the demand for our subsidiaries services and/or increases in the levels of delinquency of their customers could have a material and adverse effect on their businesses and, in turn, on Grupo Financiero Galicia’s business, results of operations and financial condition and on the trading price for it ADSs.

Class actions against financial institutions for an indeterminate amount may adversely affect the profitability of the financial system and of Banco Galicia, specifically.

Certain public and private organizations have initiated class actions against financial institutions in Argentina, including Banco Galicia. Class actions are contemplated in the Argentine National Constitution and the Consumer Protection Law, but their guidance with respect to procedural rules for instituting and trying class action cases is limited. The courts, however, have admitted class actions in spite of lacking specific regulations, providing some guidanceguidelines with respect to the procedures for the same. These courts have admitted several complaints filed against financial institutions to defend collective interests, based on arguments that object to charges applied to certain products, applicable interest rates and the advisory services rendered in the sale of government securities, among others.

Final judgments entered against financial institutions under these class actions may affect the profitability of financial institutions in general and of Banco Galicia specifically in relation to class actions filed against Banco Galicia. For further information regarding class actions brought against Banco Galicia, please refer to the Item 8. “Financial Information”─A. “Consolidated Statements and Other Financial Information”—“Legal Proceedings”— “Banco Galicia”. To the extent that the profitability of Banco Galicia is impacted by the foregoing, the same could have a material and adverse effect on Grupo Financiero Galicia’s business, results of operations and financial condition and on the trading price for it ADSs.

Administrative procedures filed by the tax authorities of certain provinces against financial institutions, such as Banco Galicia (the primary subsidiary of Grupo Financiero Galicia) and amendments to tax laws applicable to Grupo Galicia could generate losses for Grupo Galicia.

In the last years, the City of Buenos Aires tax authorities, as well as certain provincial tax authorities, have initiated administrative proceedings against financial institutions in order to collect higher gross income taxes from such financial institutions.

Although Banco Galicia (the primary subsidiary of Grupo Financiero Galicia) believes it has met its tax obligations regarding current regulations and has properly recorded provisions for those risks based on the opinions and advice of its external legal advisors and pursuant to the applicable accounting standards, certain risks may render those provisions inadequate. Tax authorities may not agree with Banco Galicia’s tax treatment, possibly leading to an increase in its tax liabilities.

Moreover, amendments to existing regulations may increase Grupo Financiero Galicia’s tax rate and a material increase in the tax burden could adversely affect its financial results, results of operations and the trading price for its ADSs.

Restriction on the distribution of results by financial institutions.

In the context of the COVID-19 pandemic, on 19 March 2020,Financial institutions must obtain prior authorization from the BCRA issued Communication "A" 6939, through which it suspended, until June 30, 2020, anybefore they can pay distributions. The distribution of earnings byresults from financial institutions in order to maintain the lending capacity of financial institutions. This suspension was extended: (i) until December 31, 2020, by means of Communication "A" 7035; (ii) until June 2021, by means of Communication "A" 7181; and (iii) finally, until December 31, 2021, by means of Communication "A" 7312.

On December 16, 2021, by means of Communication "A" 7421, the BCRA established that, from January 1, 2022 and until December 31, 2022, financial institutions (i) may distribute profits up to 20% of the applicable amount in accordance with the provisions established under the "Distribution of profits" rules (ii) such distribution should be performed in 12 equal, monthly and consecutive installments.

By means of Communication “A” 7659 dated December 15, 2022, the BCRA restricted once again any distribution of earnings of financial institutionssuspended from January 1, 2023 to Decemberuntil March 31, 2023.

Nevertheless, by means of Communication “A” 7719 dated March 9, 2023, the BCRA established that as and until December 31, 2023, financial institutions that had the BCRA's authorization – in accordance with the provisions of Section 6 of the regulations on "Distribution of Results" – may distribute earnings: (i) forresults in 6 equal, monthly, and consecutive installments, representing up to 40% of the amount that would have correspondedbeen applicable under the current regulations. Likewise, pursuant to Communication "A" 7984, the BCRA has determined that, from March 21, 2024, to December 31, 2024, financial institutions with prior authorization from the BCRA - in accordance with Section 6 of the applicable regulations above-mentioned; and (ii)on "Distribution of Results" - may distribute results in 6 equal, monthly, and consecutive installments.

.installments for up to 60% of the amount that would have corresponded if said regulations had been applied.

Current or future restrictions on the distribution of dividends by Argentine financial institutions could affect the distribution of dividends of Banco Galicia, our main subsidiary, which would, in turn, adversely impact the dividends received by Grupo Financiero Galicia and, thus, distributions on its ADSs.

Risk Factors Relating to Us

Grupo Galicia may be unable to repay its financial obligations due to a lack of liquidity it may suffer because of being a holding company.

Grupo Financiero Galicia, as a holding company, conducts its operations through its subsidiaries. Consequently, it does not operate or hold substantial assets, except for equity investments in its subsidiaries. Except for such assets, Grupo Financiero Galicia’s ability to invest in its business development and/or to repay obligations is subject to the funds generated by its subsidiaries and their ability to pay cash dividends. In the absence of such funds, Grupo Financiero Galicia may be forced to resort to financing options at unappealing prices, rates and conditions. Additionally, such financing could be unavailable when Grupo Financiero Galicia may need it.

Grupo Financiero Galicia’s subsidiaries are under no obligation to pay any amount to enable Grupo Financiero Galicia to carry out investment activities and/or to pay its liabilities or to give Grupo Financiero Galicia funds for such purposes. Each of the subsidiaries is a legal entity separate from Grupo Financiero Galicia, and due to certain circumstances, legal or contractual restrictions, as well as to the subsidiaries’ financial condition and operating requirements, Grupo Financiero Galicia’s ability to receive dividends and its ability to develop its business and/or to comply with payment obligations could be limited. Under certain regulations, Banco Galicia has restrictions relating to dividend distributions.

Investors should take notice of the above, prior to deciding on their investment in equity in Grupo Financiero Galicia as a failure to receive the noted dividends may materially and adversely impact the ability of Grupo Financiero Galicia to pay any amounts in respect of the ADSs. For further information on dividend distribution restrictions, see Item 5. “Operating and Financial Review and Prospects”─B. “Liquidity and Capital Resources”.

Corporate governance standards and disclosure policies that govern companies listing their shares pursuant to the public offering system in Argentina may differ from those regulating highly developed capital markets, such as the U.S. As a foreign private issuer, Grupo Galicia applies disclosure policies and requirements that differ from those governing U.S. domestic registrants.

As a foreign private issuer, Grupo Financiero Galicia is subject to different disclosure policies and other requirements than a domestic U.S. registrant. For example, as a foreign private issuer in the U.S., Grupo Financiero Galicia is not subject to the same requirements and disclosure policies as a domestic U.S. registrant under the Exchange Act, including the requirements to prepare and issue financial statements, report on significant events and the standards applicable to domestic U.S. registrants under Section 14 of the Exchange Act or the insider reporting and short-swing profit rules applicable to domestic U.S. registrants.