2

| Table of Contents | |||

| 5 | |||

| 5 | |||

| 7 | |||

| 7 | |||

| 7 | |||

| 7 | |||

| 7 | |||

7 | |||

| 15 | |||

| 16 | |||

| 20 | |||

| 21 | |||

| 21 | |||

| 30 | |||

| 52 | |||

| 57 | |||

| 58 | |||

| 59 | |||

| 59 | |||

| 59 | |||

| 59 | |||

| 59 | |||

| 60 | |||

| 60 | |||

| 60 | |||

| 62 | |||

| 62 | |||

| 63 | |||

| 63 | |||

| 63 | |||

| 63 | |||

3

| 63 | |||

| 63 | |||

| 63 | |||

| 64 | |||

| 64 | |||

| 64 | |||

| 64 | |||

| 64 | |||

| 65 | |||

| 68 | |||

| 68 | |||

| 68 | |||

| 69 | |||

| 69 | |||

| 74 | |||

| 74 | |||

| 74 | |||

| 74 | |||

| 74 | |||

| 75 | |||

| 75 | |||

| 75 | |||

| 76 | |||

| 76 | |||

| 76 | |||

| 77 | |||

| 79 | |||

| 80 | |||

| 80 | |||

| 80 | |||

| 80 | |||

| 81 | |||

| 81 | |||

| 81 | |||

| 81 | |||

| 83 | |||

| 83 | |||

| 84 | |||

| 84 | |||

| 84 | |||

Introduction

Audited financial information presented in this Annual Report on Form 20-F is for the 12-month periodyear ended October 31, 20192021 and the comparative 18-month periodyears ended October 31, 20182020 and the 12-month period ended April 30, 2017.2019.

The Securities and Exchange Commission, or the SEC, encourages companies to disclose forward-looking information so that investors can better understand a company’s future prospects and make informed investment decisions. Except for the historical information contained in this Annual Report on Form 20-F, the statements contained in this annual reportAnnual Report on Form 20-F are “forward-looking statements”, which reflect our current view with respect to future events and financial results.

These risks include, but are not limited to, risks and uncertainties regarding:

our ability to develop products and services that satisfy the needs of our customers;

the effectiveness of our sales force and distribution channels;

competition or changes in growth rates in the markets in which we operate;

our ability to attract and retain sufficiently qualified management and key employees;

the ongoing integration of HPE Software business into the Company, which may impede the ability of the Enlarged Group to obtain the same types and levels of benefits, services and resources that have historically been provided to HPE Software business by HPE, which could lead to a failure to realize the anticipated benefits of the merger;

our ability to identify, manage, complete and integrate acquisitions, divestitures and other significant transactions successfully;

the availability, integrity and security of our IT systems;

our ability to comply with national and regional laws and regulations, including those that relate to ESG matters (such as the Task Force on Climate-related Financial Disclosure (“TCFD”) requirements) across the various jurisdictions in which the Group operates;

our dependence on intellectual property, our ability to protect intellectual property and third-party claims of infringement on intellectual property;

our ability to comply with the covenants under our Credit Facilities (see note 18 “Borrowings” of the Consolidated financial statements in Item 18);

restrictions on our ability to secure additional financing or refinance our existing financing;

our exposure to fluctuations in currency exchange rates and interest rates, which could affect our variable rate indebtedness;

the possibility of being required, in certain circumstances, to make tax indemnification payments to the former owner of the HPE Software business;

the impact of future changes to, or interpretations of, US and non-US tax laws;

Our exposure to prevailing macro-economic trends, including inflation;

Our exposure to prevailing macro economic trends;

our ability to protect the personal information of our customers;

our ability to discover and address any material weaknesses or deficiencies in the Group’s internal controls over financial reporting;

a cybersecurity attack or breach, or cybersecurity vulnerabilities in our products, infrastructure, or services, or economic espionage could result in significant legal and

our ability to manage the risks involved in the foregoing.

In light of these assumptions, risks and uncertainties, the results and events discussed in the forward-looking statements contained in this annual reportAnnual Report on Form 20-F might not occur. Investors are cautioned not to place undue reliance on the forward-looking statements, which speak only as of the date of this annual report.Annual Report on Form 20-F. We are not under any obligation, and we expressly disclaim any obligation, to update or alter any forward- looking statements, whether as a result of new information, future events or otherwise. All subsequent forward-looking statements attributable to us or to any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this document.

6

PART I

| Not applicable. |

Not applicable.

12 months ended October 31, 2019 | 18 months ended October 31, 20181 | 12 months ended April 30, 2017 | 12 months ended April 30, 2016 | 12 months ended April 30, 2015 | ||||||||||||||||

| $m | $m | $m | $m | $m | ||||||||||||||||

| Revenue | 3,348.4 | 4,754.4 | 1,077.3 | 991.2 | 733.4 | |||||||||||||||

| Cost of sales | (789.9 | ) | (1,302.7 | ) | (216.4 | ) | (202.5 | ) | (83.3 | ) | ||||||||||

| Gross Profit | 2,558.5 | 3,451.7 | 860.9 | 788.7 | 650.1 | |||||||||||||||

| Selling and distribution costs | (1,224.8 | ) | (1,764.2 | ) | (363.1 | ) | (312.6 | ) | (252.4 | ) | ||||||||||

| Research and development expenses | (491.2 | ) | (680.8 | ) | (122.8 | ) | (117.4 | ) | (141.9 | ) | ||||||||||

| Administrative expenses | (620.8 | ) | (629.9 | ) | (147.6 | ) | (111.5 | ) | (119.2 | ) | ||||||||||

| Operating profit | 221.7 | 376.8 | 227.4 | 247.2 | 136.6 | |||||||||||||||

| Finance costs | (282.4 | ) | (350.4 | ) | (96.8 | ) | (98.4 | ) | (56.2 | ) | ||||||||||

| Finance income | (26.6 | ) | 7.7 | 1.0 | 1.0 | 1.2 | ||||||||||||||

| (Loss)/profit before tax | (34.1 | ) | 34.1 | 131.6 | 149.8 | 81.6 | ||||||||||||||

| Taxation | 16.0 | 673.1 | (7.5 | ) | (13.9 | ) | 14.3 | |||||||||||||

| (Loss)/profit from continuing operations | (18.1 | ) | 707.2 | 124.1 | 135.9 | 95.9 | ||||||||||||||

| Profit from discontinued operation (attributable to equity shareholders of the Company) | 1,487.2 | 76.9 | 33.7 | 27.0 | 5.5 | |||||||||||||||

| Profit after tax | 1,469.1 | 784.1 | 157.8 | 162.9 | 101.4 | |||||||||||||||

| Other comprehensive (expense)/income | (306.0 | ) | 29.3 | (5.7 | ) | 0.6 | (11.3 | ) | ||||||||||||

| Total comprehensive income for the period | 1,163.1 | 813.4 | 152.1 | 163.5 | 90.1 | |||||||||||||||

| Attributable to: | ||||||||||||||||||||

| Equity shareholders of the Company | 1,162.8 | 813.3 | 152.2 | 163.4 | 90.4 | |||||||||||||||

| Non-controlling interest | 0.3 | 0.1 | (0.1 | ) | 0.1 | (0.3 | ) | |||||||||||||

| Total comprehensive income for the period | 1,163.1 | 813.4 | 152.1 | 163.5 | 90.1 | |||||||||||||||

| Continuing and Discontinued Operations | ||||||||||||||||||||

| Earnings per share | ||||||||||||||||||||

| Basic (cents) | 388.50 | 201.70 | 68.88 | 74.50 | 58.54 | |||||||||||||||

| Diluted (cents) | 384.35 | 196.17 | 66.51 | 71.61 | 56.71 | |||||||||||||||

| Continuing Operations | ||||||||||||||||||||

| Earnings per share | ||||||||||||||||||||

| Basic (cents) | (4.87 | ) | 181.91 | 54.17 | 62.40 | 55.36 | ||||||||||||||

| Diluted (cents) | (4.87 | ) | 176.92 | 52.31 | 59.97 | 53.64 | ||||||||||||||

October 31, 2019 | October 31, 2018 | April 30, 2017 | April 30, 2016 | April 30, 2015 | ||||||||||||||||

$m | $m | $m | $m | $m | ||||||||||||||||

Non-current assets | 12,846.7 | 13,720.5 | 3,995.5 | 3,482.6 | 3,629.7 | |||||||||||||||

Current assets | 1,448.1 | 1,917.6 | 442.2 | 954.4 | 460.9 | |||||||||||||||

Current assets classified as held for sale | - | 1,142.5 | - | - | - | |||||||||||||||

| Total assets | 14,294.8 | 16,780.6 | 4,437.7 | 4,437.0 | 4,090.6 | |||||||||||||||

Current liabilities | 1,802.0 | 2,010.4 | 944.7 | 1,061.8 | 988.0 | |||||||||||||||

Current liabilities classified as held for sale | - | 437.7 | - | - | - | |||||||||||||||

Non-current liabilities | 6,216.5 | 6,540.5 | 1,879.5 | 1,781.4 | 1,824.6 | |||||||||||||||

| Total liabilities | 8,018.5 | 8,988.6 | 2,824.2 | 2,843.2 | 2,812.6 | |||||||||||||||

| Net Assets/(Liabilities) | 6,276.3 | 7,792.0 | 1,613.5 | 1,593.8 | 1,278.0 | |||||||||||||||

Share Capital | 47.2 | 65.8 | 39.7 | 39.6 | 39.6 | |||||||||||||||

Number of shares | 363,583,328 | 436,800,513 | 229,674,479 | 228,706,210 | 228,587,397 | |||||||||||||||

12 months ended October 31, 2019 | 18 months ended October 31, 2019 | 12 months ended April 30, 2017 | 12 months ended April 30, 2016 | 12 months ended April 30, 2015 | ||||||||||||||||

Interim dividend 1 | 58.33 | 34.60 | 29.73 | 16.94 | 15.40 | |||||||||||||||

Interim dividend 2 | - | 58.33 | - | - | - | |||||||||||||||

Final dividend | 58.33 | 58.33 | 58.33 | 49.74 | 33.00 | |||||||||||||||

Dividend declared per share (cents) | 116.66 | 151.26 | 88.06 | 66.68 | 48.40 | |||||||||||||||

Not applicable.

Not applicable.

There are risks associated with owning Micro Focus ADSs. In addition to the other information included elsewhere in this Annual Report on Form 20-F, including in the section entitled ‘‘Cautionary Statement on Forward-Looking Statements,’’ you should carefully consider the following discussion of what we believe to be the most important risk factors.factors applicable to the Group. The risks and uncertainties described below are not the only risks and uncertainties that the Enlarged Group and holders of Micro Focus ADSs may face. AdditionalIn addition, it is not possible to predict or identify all such factors and additional risks and uncertainties not presently known to the Company, or that the Company currently considers immaterial, which could also negativelymaterially adversely affect the business, results of operation, financial condition and prospects of the Enlarged Group, as well as the value of Micro Focus ADSs.

The order in which the following risk factors are presented does not necessarily reflect the likelihood of their occurrence or the relative magnitude of their potential material adverse effect on the business, financial condition, results of operation or prospects of the Enlarged Group or the market price of the Micro Focus Shares or Micro Focus ADSs.

The information given is as of the date of this information statement/prospectus,Annual Report on Form 20-F, and any forward-looking statements are made subject to the reservations specified under the section entitled ‘‘Cautionary Statement on Forward-Looking Statements”.

Principal risks and uncertainties

In common with all businesses, the Group could be affected by risks and uncertainties that may have a material adverse effect on its business operations and achieving its strategic objectives including its business model, future performance, solvency, liquidity and/or reputation. This includes any new, emerging or continuing direct or indirect risks posed by COVID-19. These risks could cause actual results to differ materially from forecasts or historic results. Accepting that risk is an inherent part of doing business, the Boardboard is mindful of the interdependencies of some risks. Where possible, the Group seeks to mitigate risks through its RMF, (“Risk Management Framework”), internal controls and insurance, but this can only provide reasonable assurance and not absolute assurance against material losses. In particular, insurance policies may not fully cover all of the consequences of any event, including damage to persons or property, business interruptions, failure of counterparties to conform to the terms of an agreement or other liabilities. The following are the principal risks and uncertainties, and potential impacts and mitigations that are relevant to the Group as a provider of software products and associated services at this time. They do not comprise all of the risks associated with the Group and are not set out in priority order. Additional risks not presently known to management, or currently deemed to be less material, may also have an adverse effect on the Group.

Products | ||

Principal To remain successful, the Group must ensure that its products continue to meet the requirements of customers and investment must be effectively balanced between growth and mature products. Investment in research and innovation in product development is essential to meet customer and partner requirements in order to maximize customer value, revenues and corporate performance. The Group has a large number of products, at differing stages of their | ||

Potential If products do not meet the requirements of customers, they will seek alternative solutions, resulting in the loss of existing maintenance and new revenue opportunities and the cancellation of existing contracts. Insufficient focus on key research and development projects may damage the |

Sales / Go-To-Market (“GTM”) | ||

Principal risk description For the Group to succeed in meeting sales revenue and growth targets, it requires successful GTM models across the full | ||

Potential impact Poor design and/or execution of GTM plans may limit the success of the Group by targeting the wrong customers through the wrong channels and positioning the wrong product or solution offerings, reducing the value that customers receive from Micro Focus. |

Competition | ||

Principal risk description Comprehensive information about the markets in which Micro Focus operates is required for the Group to assess competitive risks effectively and to perform successfully. The Group operates in a number of competitive markets and success in those markets depends on a variety of factors. | ||

Potential impact Failure to understand the competitive landscape adequately and thereby identify where competitive threats exist may damage the successful sales of the Group’s products. If the Group is not able to compete effectively against its competitors, it is likely to lose customers and suffer a decrease in sales, which may result in lost market share and weaker financial performance. |

Employees and culture | ||

Principal risk description The | ||

Potential impact Failure to |

IT | ||

Principal risk description The Group’s operations, as with most businesses, are dependent on maintaining and protecting the integrity and security of the IT systems and management of information. | ||

Potential impact Disruption to the IT systems could adversely affect business and Group operations in a variety of ways, which may result in an adverse impact on business operations, revenues, customer relations, supplier relations, and reputational damage. Dependency on IT providers could have an adverse impact on revenue and compliance in the event that they cannot resume business operations. |

Business strategy and change management | |

Principal risk description The Group is engaged in a number of major change projects, including acquisitions and divestments, to shape and grow the business by strengthening the portfolio of products and capabilities and IT projects to standardize systems and processes. The Group is also executing a series of operational transformation initiatives. These projects expose the Group to significant transformation risks. The Group’s strategy may involve the making of further acquisitions or divestments to protect or enhance its competitive position and failure to identify, manage, complete and integrate acquisitions, divestments and other significant transactions successfully could have a material adverse effect on the Group’s business. | |

Potential impact Failure to successfully analyze, execute and coordinate the implementation and delivery of the core systems and associated business processes with the various integration, divestment and transformation programs may result in the disruption of the on-going business without delivering the anticipated strategic and operational benefits of such transactions and/or initiatives. In addition, this may affect the ability to execute strategic plans for growth. |

Legal and | ||

Principal risk description The Group operates across a number of jurisdictions and two regulated exchanges. Compliance with national and regional laws and regulations, including those that relate to ESG matters, such as Task Force on Climate-related Disclosure (“TCFD”) requirements, is essential to successful business operations. The Group may be involved in legal and other proceedings from time to time, and as a result may face damage to its reputation or legal liability. The Group has entered into various acquisitions and | ||

Potential impact Failure to comply could result in civil or criminal sanctions |

Intellectual | ||

Principal risk description The Group is dependent upon its | ||

Potential |

Treasury | ||

Principal risk description The The Group targets a Net The 1 Net Debt is defined as cash and cash equivalents less borrowings and 2 Adjusted EBITDA is defined as net earnings before finance costs, finance income, taxation, share of results of associates, depreciation of property, plant and equipment, depreciation of right-of-use assets, amortization of intangible assets, exceptional items including the gain on disposal of discontinued operation, share-based compensation, product development intangible costs capitalized and foreign exchange (gains)/losses. | ||

Potential | The relative values of currencies can fluctuate and may have a significant impact on business results. |

Tax | ||

Principal risk description The tax treatment of the Group’s operations is subject to the risk of challenge by tax authorities in all territories in which it operates. Cross-border transactions may be challenged under tax rules and initiatives targeting multinationals’ tax International tax rules continue to develop at each of the As a result of the HPE Software business | ||

Potential impact Tax liabilities in |

Principal risk description The Group’s businesses may be subject to inherent risks arising from the general and sector specific economic, public health, pandemics and political conditions, including as a result of any pandemics or natural disasters, in one or more of the markets in which the Group | ||

Potential Impact Adverse economic conditions could affect sales, and other external economic or political matters, such as price controls, could affect the business and revenues. |

COVID-19 | |

Principal risk description The Group, like all businesses continues to navigate through a period of disruption, as it has responded to the practical and macro-economic impacts of COVID-19. COVID-19 still presents fast moving, and in some areas unpredictable, direct and indirect risks to the Group’s businesses. The Group may be subject to inherent risks arising from the continuation of the on-going COVID-19 pandemic, including the emergence of virus variants. | |

Potential impact Adverse economic conditions arising as a result of the continuation of the COVID-19 pandemic could affect sales performance and business operations. |

| Cyber | security | |

Principal risk description There could be a data security breach (Micro Focus data or customer data) involving personal, commercial or product data, either directly from Micro Focus or a third party. This could occur as a result of a malicious or criminal act, or an inadvertent system error. | ||

Potential impact Data loss, which could harm client and customer relationships, compliance and/or perception of the effectiveness of the Group’s products. |

Internal | ||

Principal risk description Internal controls over financial reporting may not prevent or detect an error, fraud, financial misstatement or other financial loss, leading to a material misstatement in the Group’s financial statements. | ||

Potential impact Failure to discover and address any material weaknesses or deficiencies in the Group’s internal controls over financial reporting could result in material misstatement in the Group’s financial statements and impair the Group’s ability to comply with applicable financial reporting requirements and related regulatory filings on a timely basis. Based on the assessment as at October 31, |

Overview

Micro Focus International plc (“Micro Focus”) is a global enterprise software business delivering value to approximately 40,000tens of thousands of customers. Micro Focus helps organizations run and transform their business. Driven by customer-centric innovation, Micro Focus software provides the critical tools customers need to build, operate, secure and analyze the enterprise. Micro Focus delivered revenues of $3,348.4m and profit for the period of $1,469.1m for the 12 months ended October 31, 2019.

The Company is subject to the information requirements of the US Securities Exchange Act of 1934 applicable to foreign private issuers. In accordance with these requirements, the company files its Annual Report on Form 20-F and other documents with the SEC. The Company’s SEC filings are available to the public at the SEC’s website, www.sec.gov.

Access comprehensive information about the Company and download shareholder publications at the corporate website; visit the Investor Relations section for the latest company news, dividend and share price data.

Our website – www.microfocus.com

The Micro Focus Group, headquartered in Newbury, U.K., is a global enterprise software company supporting the technology needs and challenges of the Global 2000.company. The registered office of the Company is The Lawn, 22-30 Old Bath Road, Newbury, Berkshire, RG14 1QN, United Kingdom (Tel: +44 (0) 1635 565200). Its solutions help organizations leverage existing IT investments, enterprise applications and emerging technologies to address complex, rapidly evolving business requirements while protecting corporate information at all times.

Micro Focus was founded in 1976 and in 1981 it became the first company to win the Queen’s Award for Industry purely for developing a software product. The product was CIS COBOL, a standard-compliant COBOL implementation for microcomputers. Micro Focus’ COBOL products remain important components of theThe Micro Focus Product Portfolio which now extends to more thanalmost 300 products.

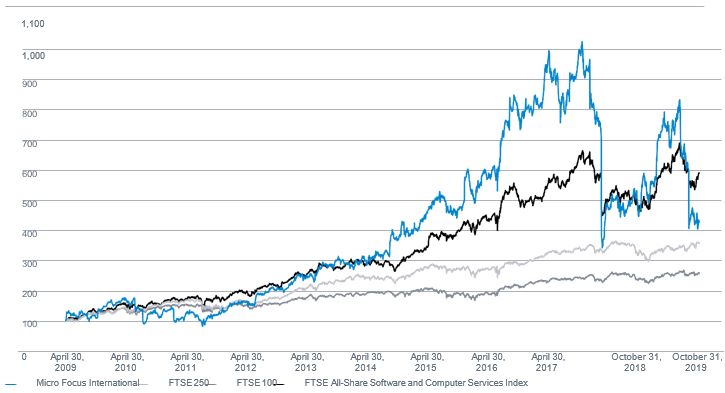

Micro Focus International plc is listed on the London Stock Exchange and is a member of the FTSE 250 index. The Company’s American Depositary Shares (the “ADSs”) are listed on the New York Stock Exchange.

As of February 19, 202024, 2022 (the latest practicable date prior to the date of this Annual Report on Form 20-F), Micro Focus had a market capitalization of £2.67£1.3 billion ($3.451.7 billion).

Micro Focus has more than 40 years of experience in delivering proven, scalable and robust solutions.

Acquisitions and Investments

This annual reportAnnual Report covers the 12-monthsyear ended October 31, 20192021 with the comparative periods being the 18-monthsyears ended October 31, 2018,2020 and 12-months ended April 30, 2017.2019.

Who we are

We supply sector-agnostic products across multiple markets that are focused on digital transformation. We have tens of thousands of customers, including many of the largest companies in the world.

Our broad set of technology needsfor security, IT operations, application delivery, governance, modernization, and analytics provides the innovative solutions that the world’s largest organizations need to run and transform concurrently.

Helping customers run and transform

To deliver on the promise of digital transformation customers need to balance the often conflicting challenges of 40,000running and transforming their businesses simultaneously.

This requires finding the right balance between cost, risk, and agility. We help them do that by focusing on four key outcomes which customers are striving to achieve: accelerate application delivery, simplify IT transformation, strengthen Cyber reslilence and analyze data in time to act.

Combining decades of technical expertise with a unique approach to innovation we create new and better solutions to help our customers thrive with ever-evolving technologies.

Our portfolio and product groups

Micro Focus has a broad and diverse portfolio of products which are organized into five product groups with each group containing multiple products that operate at the varying stages of the continuum from small and medium size enterprisesstable/declining (0% or less growth) to many in the Forbes Global 2000. The Group’shigh growth (11 to 20% growth).

Application Modernization & Connectivity (“AMC”)

AMC solutions help organizations leverage existingcustomers unlock the value from core business applications through the provision of innovative solution for modernization which enable a transformational journey to deliver ongoing value and greater flexibility from longstanding IT investments, enterpriseon or off the mainframe.

Application Delivery Management (“ADM”)

ADM solutions help customers increase velocity, remove bottlenecks and deliver high-performing applications to better support their digital business. Combined, these solutions increase stakeholder alignment and the delivery of value, while liberating resources to release faster without compromising quality.

IT Operations Management (“ITOM”)

ITOM Solutions simplify the complexity of IT operations. Powered by built-in analytics, they help business users easily engage with IT through Enterprise Service Management, deliver Full-Stack AIOps for service assurance, automate the service fulfilment life cycle, and strengthen IT service governance.

CyberRes (previously Security)

Comprehensive security solutions help enterprises create cyber resilience through detecting threats, securing data and applications, and emerging technologiesprotecting identities – enabling customers to address complex, rapidly evolving business requirements, includingadapt and evolve for the protection of corporate information at all times.future. Artificial Intelligence, machine learning and behavioral analytics capabilities enable this to be done and enterprise scale.

IM&G solutions help customers analyze, understand, and control data – to derive value and manage enterprise risk. Efficient compliance, governance, customer behavior, and IOT analytics are representative use cases.

During the 12-monthsyear ended October 31, 2019. The prior period was 18-month ended October 31, 2018 as a result of moving our year-end from the end of April to the end of October.

Micro Focus Product Portfolio, – The Micro Focus and does not include SUSE.

Product Portfolio segment contains both mature softwaredevelopments

In the year ended October 31, 2021 we have delivered significant new innovation through Licence, SaaS and subscription offerings to enable customers to consume it more effectively and quickly.

Key examples of progress include: the removal of dependencies on third-party products embedded in the core of some of our key solutions, the delivery of comprehensive artificial intelligence, machine learning and high growthanalytics capabilities in every portfolio, and the work to rearchitect many of our products to support new cloud and hybrid deployment options. Within each portfolio we have introduced new SaaS offerings, that are managed on aimproved the existing SaaS offerings and invested significantly in our SaaS delivery infrastructure.

Overall, we exited the year with improved competitive positioning, with highlights by portfolio basis akin to a “fund of funds” investment portfolio. This portfolio is managed within a single Group – with five sub-portfolios based on industrial logic and management of the Micro Focus sub-portfolios: Application Modernization & Connectivity, Application Delivery Management, IT Operations Management, Security and Information Management & Governance. The software is sold and supported through a geographic Go-to-Market organization.including:

| - | IMG: new unified SaaS offering, Vertica Accelerator, delivers high performance and scalable analytics as well as end-to-end, in-database machine learning. |

| - | ITOM: released OPTIC (Operations Platform for Transformation, Intelligence and Cloud), empowering IT operations with built-in, unlimited-use intelligence at the core and the ability to optimize the cloud. Additionally, revitalized roadmaps to focus on the delivery of artificial intelligence and SaaS capabilities. |

| - | ADM: delivered material improvements to our SaaS offerings, launching a number of native cloud solutions; |

| - | AMC: made continued progress with our AWS relationship and are a strategic partner enabling their new AWS Mainframe Modernization service. |

| - | CyberRes: in data security integration with Amazon Macie provides a new and unique solution to allow AWS customers to automate data-centric protection onto data discovery, classification, and remediation processes. New SaaS capabilities in Identity Management enable customers to exploit new use cases and advanced analytics enable threat detection and remediation at scale with ArcSight. |

Item 4.B.2 Principal markets

Details of the principal markets in which the Group operates including a breakdown of revenue by activity and geographic market is disclosed in note 2 “Supplementary Information” of the Consolidated financial statements in Item 18.

Our markets

Today’s technology landscape

Digital transformation has been at the top of virtually every organization’s list of objectives for several years. Often, it represents a foundational program of technology change to underpin a significant business change.

Leveraging enterprise technology to embrace organizational change is not a new phenomenon. However, few will argue that the recent past has been a uniquely difficult period. Significant changes to customer behavior, staff locations, supply chains, technology strategies, and market trends have introduced tremendously diverse, time-critical requirements on the IT organization. Many consider the last two years to be the most dramatic chapter yet in the digital transformation era.

Change often necessitates investment. Rather than tapering off after enterprises reacted to the challenges presented by the pandemic, spending on solutions in the digital transformation space is expected to continue to increase at a solid pace. “From 2021 through 2024, IDC forecasts $7.8 trillion of direct digital transformation (DX) investments across services, hardware, and software; growing at a 16.4% compound annual growth rate (“CAGR”) vs (0.1%) CAGR reduction for non-DX investments over the same timeframe,” according to Shawn Fitzgerald, Research Director, Worldwide Digital Transformation Strategies.

Major investment in change also carries significant business risk. It is difficult to switch from what’s tried-and-true to new technology when it could significantly disrupt the flow of everyday business. Still, organizations need a way to enhance the customer experience, accelerate new business models, and foster rapid growth. They just want certainty before they press the “go” button.

In the end, IT leaders must find a strategy that allows them to continue to invest in digital transformation, while still protect existing operations that are already under significant strain. Enterprises need to be in it for now and for the future. A successful transformation strategy is more imperative than ever before.

This is our customers’ digital dilemma – how to run and transform their business at the same time so they can achieve the critical elements of a successful digital transformation program. Micro Focus helps organizations simultaneously manage both the existing operational landscape, and emerging technology and innovation requirements of the future.

Digital transformation

Digital transformation touches virtually every corner of the organization, and technology priorities often vary among numerous stakeholders. We find there are four key outcomes that our customers demand.

Accelerate Application Delivery

Customers can employ Agile and DevOps practices supported by value stream management capabilities to sustain delivery velocity requirements as operations run.

At the same time, they can create digital value – from strategy through release – as they transform using AI and machine learning to deliver high-quality applications at scale.

Simplify IT Transformation

Customers can simplify the complexity of running a mix of traditional and cloud services by taking a Digital Factory approach to running today.

With a unified platform for IT operations, they can integrate or replace incompatible tools collected over decades – freeing up resources and accelerating transformation.

Strengthen Cyber Resilience

Customers can protect what matters most by detecting threat actors, responding to advanced threats, and recovering from an attack, as their operations run today.

Then they can evolve at the speed of change using security analytics for hybrid environments to help their organization transform.

Analyze Data in Time to Act

Customers can unify their analytics today, without moving their data to one place so they can run their analytics practice more efficiently.

As they transform their organization to grow, they can ensure they’re able to support more users and greater data volumes with the highest performance at scale for accurate and actionable predictive insights.

| Item 4.B.3 | Seasonality |

Micro Focus’ quarterly revenues have historically been affected by a variety of seasonal factors typical of the seasonality of an enterprise software business with a licenselicence fee model and the industry in which it operates.

The operating margins of its businessesthe Group are generally affected by seasonal factors in a similar manner because its base ofthe Group has largely fixed costs remainswhich remain consistent throughout the year. Micro Focus believes that this trend will continue in the future and that its total revenue will continue to peak in the fourth fiscal quarter of each year. In aligning the financial year end of the Enlarged Group to October 31 following Closing in the prior year, Micro Focus the fourth quarter license fee peak moved from April 30, 2018 to October 31, 2018. Maintenance and subscription fee renewals are spread throughout the financial year, however, there is a seasonal peak in the quarter ending January 31 as a result of the calendar year end, which coincides with the financial year-end of a large number of other companies.

Item 4.B.4 |

Not applicable

Item 4.B.5

Go-To-Market

We have restructured our Go-to-Market teams, moving from three distinct geographic organizations to enable better clarity and provide the necessary context, a summary of the key issues, the progress made within this reporting period and the outcome of the review is set out below.

Whilst further improvements are anticipatedrequired to drive operational improvementsachieve the levels of productivity and efficiencies.effectiveness we believe possible, the foundations are now in place to support delivery of this goal.

Our global network of more than 7,500 authorized partners is to ensure customers fully understand our product strategy and are able to deploy our latest technology releases successfully.

When you consider all of the key SaaS offerings were not engineered correctly to create a profitablepeople, processes, and sustainable source of incremental revenue.

Most of all, our partners inspire confidence and trust in Micro Focus products and services. Our partners have the expertise our customers need to solve their digital dilemmas – running their businesses while also protecting the investments they have already madetoday and transforming them for tomorrow’s opportunities.

Product groups

Our product groups operate in our offerings. In addition, the Group delivers solutions that are openhighly competitive markets with often specific challenges and integrated,opportunities. By moving to this product group operating model (see Item 5.D) we aim to enable more agility and help bridge existingeffective execution within each product group in responding to these challenges and emerging technologies. This combination allows customers to build an eco-system that serves their long-term needs and ultimately achieve lasting success in an ever-evolving marketplace.opportunities.

During the year ended October 31, 2021 we made good progress in repositioning our product portfolio and changing our Go-to-Market approach (see above); the next phase is to evolve our business model to be much more product portfolio-centric end-to-end.

The aim over the next two years is to align the Group evaluates its options within eachby product portfolio, against a set of characteristics mapped to each stage of the adoption cycle, as represented in the table below.

Item 4.B.6 |

With nearly 40% of our employee base dedicated to R&D, we were able to integrate the latest technology into more than 1,000 product releases in the year ended October 31, 2021. Details of the Groups key financial contracts are included in Items 5.B and 10.C.

Item 4.B.7

Not applicable

Item 4.B.8

Not applicable

A full list of the Group’s subsidiaries can be found in Exhibit 8.1note 34 “Related undertakings” of the Consolidated financial statements in Item 19.18.

The Group owns or leases various offices under non-cancellable operating lease agreements. Thea large number of properties, owned or leased and operated by the Group’s subsidiaries are maintained in good condition and are believed to be suitable and adequate for the Group’s present needs.over 40 countries worldwide. The Group’s headquarters are located at premises in Newbury, England.England and are owned by the Group. The Group owns or leases properties amounting to over 2.4 million square feet of space, in over 40 countries worldwide. Twohas two individual leased properties which are material to the Group. One is located in Provo, Utah, where the Group currently leases approximately 405,700 square feet of office space. The lease onGroup has recently concluded negotiations with the landlord for this facility for which the lease was set to end in 2024 to extend the lease term with a reduction in floor space in stages. In February 2022 an initial reduction to approximately 239,100 square feet, then from June 2024 to approximately 219,900 square feet with a further reduction in floor space from December 2024 to approximately 142,300 square feet. This new lease agreement expires in 2024,2034, with an option to extend for a further three, 5-yearfive-year periods. The Group’s current annual rent under this lease is $8.2 million.$8.7 million (2020: $8.4 million) and this will reduce as the floor space reduces to $5.3 million per annum in February 2022 and $3.6 million per annum from December 2024. Since March 1, 2019, part of the property has been sublet. Current annual sub-lease income is $1.0 million.$1.1 million (2020: $1.1 million). The othersecond property is located in Santa Clara, California, where the Group currently leases approximately 635,000 square feet of office space. The lease on this facility expires in 2029, with an option to extend for one further 5-yearfive-year period. The Group’s current annual rent under this lease is $4.6 million.$4.9 million (2020: $4.7 million). The Group is currently not utilizing one and a half floors of this facility and the related right-of-use assets has been tested for impairment with a partial impairment recorded.

“Property, plant and equipment” in note 12 of the “Notes to the consolidatedConsolidated financial statements”statements in Item 18;

“Operating lease commitments – minimum lease payments”Leases” in note 3419 of the “Notes to the consolidatedConsolidated financial statements”statements in Item 18.

As a result of the disposal of the Digital Safe business which completed on January 31, 2022 leases with right-of-use assets of $27 million will be sub leased to Smarsh Inc. from January 31, 2022.

There are no unresolved written comments from the SEC staff regarding its periodic reports under the Exchange Act received more than 180 days before October 31, 2019.2021.

The following discussion and analysis is intended to provide investors with an understanding of the historical performance of the Company and its financial condition. This discussion and analysis presents the factors that had a material effect on the results of operations of Micro Focusthe Group for:

the 12 month periodyear ended October 31, 2019,2021, as compared to the 18 month periodyear ended October 31, 2018;2020, and

the 18 month periodyear ended October 31, 2018,2020, as compared to the 12 month periodyear ended April 30, 2017.

The following discussion and analysis contains forward-looking statements. See “Risk Factors” in Item 3D on page 7 and “Cautionary Statement on Forward-Looking Statements”Statements’’ on page 5 in this Annual Report on Form 20-F for a discussion of the uncertainties, risks and assumptions associated with these statements. The following should be read in conjunction with the Group’s consolidatedConsolidated financial statements and the notes thereto included in Item 18.

Business Overview

This Annual Report covers the year ended October 31, 2021 with the comparative periods being the years ended October 31, 2020 and 2019.

The following discussion and analysis contains forward-looking statements. See “Cautionary Statement on Forward-Looking Statements’’ on page 5 and “Risk Factors”discussions for the year ended October 31, 2020 as compared to the year ended October 31, 2019 can be found in Item 3D on pages 10 to 15 in thisItems 5.A of the Group’s Annual Report on Form 20-F for a discussion of the uncertainties, risks and assumptions associated with these statements.

As disclosed in item 4 subsequent to October 31, 2021 on November 3, 2021 the 18 monthsGroup announced the agreement of definitive terms to sell its Archiving and Risk Management portfolio (the “Digital Safe business”) to Smarsh Inc., for a total cash consideration of $375m. During the year ended October 31, 20182021 the Digital Safe business generated revenue of $108m which are reported in the IM&G product group and 12 months ended April 30, 2017.

Results of Operations

The results of operations should be read in conjunction with the consolidatedConsolidated financial statements included under Item 18 in this Annual Report on Form 20-F. The consolidatedConsolidated financial statements have been prepared in accordance with IFRS as issued by the IASB.

All narrative within this report focuses on the continuing operations unless otherwise stated. All narrative is presented based on results using actual exchange rates unless stated. The impact of foreign currency fluctuations is shown on page 29 where revenue is presented at actual and constant currency.

The results of the discontinued operationsoperation relate to the disposal of SUSE, which was disposed in the year ended October 31, 2019, are shown as a single amount on the face of the Consolidated statement of comprehensive income in Item 18 comprising the post-tax profit or loss of the discontinued operations and the post-tax gain or loss recognized either on measurement to fair value less costs to sell or on the disposal of the discontinued operation. The Consolidated statement of cash flows has been presented in Item 18 including the discontinued operations.operation. Results and cash flows of the discontinued operation for the threetwo reported periods are shown in note 3730 “Discontinued operation and assets held for sale” of the Consolidated financial statements in Item 18.

Year ended October 31, 2021 | Year ended October 31, 2020 | Period- on- period change | Year ended October 31, 2019 | Period-on- period change | ||||||||||||||||

| Continuing operations | $m | $m | % | $m | % | |||||||||||||||

| Revenue | 2,899.9 | 3,001.0 | (3.4 | )% | 3,348.4 | (10.4 | )% | |||||||||||||

| Costs of sales | (776.3 | ) | (702.7 | ) | 10.5 | % | (789.9 | ) | (11.0 | )% | ||||||||||

| Gross profit | 2,123.6 | 2,298.3 | (7.6 | )% | 2,558.5 | (10.2 | )% | |||||||||||||

| Selling and distribution expenses | (1,344.6 | ) | (1,112.1 | ) | 20.9 | % | (1,224.8 | ) | (9.2 | )% | ||||||||||

| Research and development expenses | (521.8 | ) | (513.6 | ) | 1.6 | % | (491.2 | ) | (4.6 | )% | ||||||||||

| Administrative expenses | (522.8 | ) | (3,334.0 | ) | (84.3 | )% | (620.8 | ) | 437.0 | % | ||||||||||

| Operating (loss)/profit* | (265.6 | ) | (2,661.4 | ) | 90.0 | % | 221.7 | (1,300.5 | )% | |||||||||||

| Net finance costs | (252.2 | ) | (279.0 | ) | 9.6 | % | (255.8 | ) | (9.1 | )% | ||||||||||

| (Loss) before tax | (517.8 | ) | (2,940.4 | ) | 82.4 | % | (34.1 | ) | (8,522.9 | )% | ||||||||||

| Taxation | 82.7 | (34.2 | ) | 341.8 | % | 16.0 | (313.8 | )% | ||||||||||||

| (Loss) from continuing operations | (435.1 | ) | (2,974.6 | ) | 85.4 | % | (18.1 | ) | (16,334.3 | )% | ||||||||||

| Profit from discontinued operation | 10.7 | 5.1 | 109.8 | % | 1,487.2 | (99.7 | )% | |||||||||||||

| (Loss)/profit for the period | (424.4 | ) | (2,969.5 | ) | 85.7 | % | 1,469.1 | (302.1 | )% | |||||||||||

* Exceptional items of $247.1 million have been recorded with operating (loss)/profit in the reporting periods presented below.

12 months ended October 31, 2019 | 18 months ended October 31, 2018 | |||||||

| Continuing operations | $m | $m | ||||||

| Revenue | 3,348.4 | 4,754.4 | ||||||

Operating profit (before exceptional items) | 515.9 | 915.0 | ||||||

Exceptional items | (294.2 | ) | (538.2 | ) | ||||

| Operating profit | 221.7 | 376.8 | ||||||

Net finance costs (excluding exceptional items) | (255.8 | ) | (336.9 | ) | ||||

Exceptional finance costs | - | (5.8 | ) | |||||

| (Loss)/profit before tax | (34.1 | ) | 34.1 | |||||

Taxation | 16.0 | 673.1 | ||||||

| (Loss)/profit from continuing operations | (18.1 | ) | 707.2 | |||||

Profit from discontinued operation | 1,487.2 | 76.9 | ||||||

| Profit for the period | 1,469.1 | 784.1 | ||||||

Revenue

In the 12 monthsyear ended October 31, 2019,2021, the Group generated revenue of $3,348.4$2,899.9 million, which represents a decrease of $1,406.0$101.1 million (29.6%(3.4%) on the $4,754.4$3,001.0 million in 18 monthsyear ended October 31, 2018.2020.

12 months ended October 31, 2019 | 18 months ended October 31, 2018 | Period-on – period change | Year ended October 31, 2021 | Year ended October 31, 2020 | Period-on- period change | Year ended October 31, 2019 | Period- on – period change | |||||||||||||||||||||||||

| Continuing operations | $m | $m | % | $m | $m | % | $m | % | ||||||||||||||||||||||||

Licence | 800.0 | 1,213.7 | (34.1 | )% | 688.6 | 646.5 | 6.5 | % | 800.0 | (19.2 | )% | |||||||||||||||||||||

Maintenance | 2,057.6 | 2,861.6 | (28.1 | )% | 1,791.7 | 1,921.2 | (6.7 | )% | 2,057.6 | (6.6 | )% | |||||||||||||||||||||

SaaS & other recurring | 279.7 | 373.9 | (25.2 | )% | 239.8 | 245.5 | (2.3 | )% | 279.7 | (12.2 | )% | |||||||||||||||||||||

Consulting | 217.9 | 366.3 | (40.5 | )% | 179.8 | 188.4 | (4.6 | )% | 217.9 | (13.5 | )% | |||||||||||||||||||||

| Revenue before haircut | 3,355.2 | 4,814.5 | (30.3 | )% | 2,899.9 | 3,001.6 | (3.4 | )% | 3,355.2 | (10.5 | )% | |||||||||||||||||||||

Deferred revenue haircut | (6.8 | ) | (61.1 | ) | (88.9 | )% | - | (0.6 | ) | 100.0 | % | (6.8 | ) | 91.2 | % | |||||||||||||||||

| Total Revenue | 3,348.4 | 4,754.4 | (29.6 | )% | 2,899.9 | 3,001.0 | (3.4 | )% | 3,348.4 | (10.4 | )% | |||||||||||||||||||||

Revenue in the table above and the subsequent trends in this section are presented before the impact of the deferred revenue haircut, which represents the unwinding of a fair value adjustment to acquired deferred revenue.

Revenue by stream performance

Licence revenue decreased grew by $413.7$42.1 million (34.1%(6.5%) to $800.0$688.6 million in the 12 monthsyear ended October 31, 20192021 compared with $1,213.7$646.5 million in the 18 monthsyear ended October 31, 2018.2020.

Licence revenue, with growth of 6.5%, is underpinned by improvements in sales execution and the benefit of investments made in our portfolios as outlined in Item 4.B.

In particular (page 24):

Licence revenue in AMC increased by 12.0% in the year ended October 31, 2021. Growth in Licence revenue was underpinned by strong performance in mainframe modernization. No revenue has been recognized from the AWS contract in the year ended October 31, 2021.

Licence revenue in ADM increased by 4.0% in the year ended October 31, 2021. The licence revenue decrease primarily relatedGroup has made good progress in the repositioning of our ADM portfolio, after performance in the year ended October 31, 2021 was below expectations. This has led to the shorter period of account. In addition, underlying performance if considered on a like for like basis, would show a declinesmall increase in licence revenue in the year, continued to be impactedperiod.

Licence revenue in ITOM declined by operational issues impacting sales execution and, as such, performance volatility. In particular1.4% in the third quarteryear ended October 31, 2021. This performance reflects a moderation in the rate of revenue decline compared to the year ended October 31, 2020 but remains below our medium-term expectations for the product group.

Licence revenue in CyberRes increased by 7.3% in the year ended October 31, 2021. Investments made in this product portfolio have resulted in new offerings and significant enhancements to existing offerings yielding growth in Licence for the portfolio and growth in total revenue for two of the financialfour sub-portfolios.

Licence revenue in IM&G increased by 17.3% in the year ended 31 October 31, 2021.This increase is primarily driven by growth in Vertica, the challenging macro environment resulted in a slowdown in customer purchases. This environment improved marginally inGroup’s Big Data offering. In the fourth quarter, but short-term volatility remainsthe Group launched Vertica Accelerator which is delivered in a continued risksubscription form as a managed service. The Group has made encouraging progress with this transition to subscriptions, with both bookings and new business in future trading periods.customers up substantially year-on-year.

Maintenance revenue decreased by $804.0$129.5 million (28.1%(6.7%) to $2,057.6$1,791.7 million in the 12 monthsyear ended October 31, 20192021 compared with $2,861.6$1,921.2 million in the 18 monthsyear ended October 31, 2018.2020.

The maintenance revenue decrease primarily relateddecline in the current year is impacted by a reduction in Licence volume over multiple previous financial periods combined with elevated attrition rates in four sub-portfolios. This is a major area of management focus for, and over the past 18 months the Group has implemented material changes across these product portfolios driven by direct customer feedback and focused on improving the overall user experience. There have also been significant new capabilities introduced to the shorter period of account.expand cloud, artificial intelligence and analytics capabilities. In addition, underlying performance if considered on a like for like basis, would show a declinemultiple leadership changes have been made within underperforming portfolios and the compensation of sales leadership is now linked to customer retention. These actions were embedded in revenue infirst half of the year was impacted by one-off events such as the disposal of Atalla and moving to selling to the US Government through a strategic partner rather than direct.

The main movements at a portfolio level were (page 24):

Maintenance revenue in AMC declined by 1.8% in the year October 31, 2021. The year-on-year decline was impacted by licence performance in the year ended October 31, 2020;

Maintenance revenue in ADM declined by 7.0% in the year ended October 31, 2021. The maintenance performance in the period was driven by a weak licence performance in the year ended October 31, 2020 combined with an element of transitioning some customers to SaaS based solutions within our performance testing portfolio;

Maintenance revenue in ITOM declined by 9.2% in the year ended October 31, 2021. This performance reflects a moderation in the rate of revenue decline compared to the year ended October 31, 2020 but remains below our medium-term expectations for the product group. The improvements made to the product roadmaps and in refocusing resources are key to improving attrition in sub-portfolios which will impact overall performance if successful.

Maintenance revenue in CyberRes declined by 7.9% in the year ended 31 October 2021. This performance is driven by one single product portfolio where we witnessed elevated attrition rates. This product has had significant investment over the last 24 months resulting in material improvements to the underlying architecture and overall capabilities. It is now much better positioned competitively and we expect to drive a significant moderation in the overall rate of maintenance decline in future periods.the medium-term.

The change in product mix combined with corrective actions explained in item 4.B.5 are intended to see renewal rates consistent with historical rates.drive a moderation in the rate of maintenance decline as part of the overall revenue stabilization plans.

SaaS and other recurring revenue decreased by $94.2$5.7 million (25.2%(2.3%) to $279.7$239.8 million in the 12 monthsyear ended October 31, 20192021 compared with $373.9$245.5 million in the 18 monthsyear ended October 31, 2018.2020.

Consulting revenue decreased by $8.6 million (4.6 %) to the shorter period of account. In addition, underlying performance during the year if considered on a like for like basis, would show a decline in revenue$179.8 million in the year reflected deliberate actions taken by the Group to rationalize unprofitable operations and practices and refocus resources and investments to deliver the product enhancements required for long-term success. The resulting underlying recurring revenue decline if considered on a like for like basis was in lineended October 31, 2021 compared with the Group’s expectations during the current financial year, which will allow the Group to deliver a more sustainable expected growth in SaaS revenue at a higher profit margin in the medium-term.

The Group has more thanapproximately 300 products reported under five product groups. These productsInvestment decisions are managedmade at a granular level using applicationby product depending on their growth trajectories and the profile of markets they participate in and are intended to deliver the Micro Focus four-box model.greatest return on investment. The cyclical nature of the software order cycle means that when considering underlying revenue trends, year-on-year growth rates by portfolioproduct group are not always indicative of an underlying trend and will be impacted by the timing of customer projects. As such, revenue trends at the sub-portfolio level should be viewed over the longer term and revenue trends overall viewed in a similar fashion to that of a portfolio of funds.

The table below presents the revenue performance by product group and revenue stream. The main movements in licence and maintenance revenue by product group are discussed in the Licence and Maintenance commentary above.

| Licence | Maintenance | SaaS & other recurring | Consulting | Total | ||||||||||||||||

| Continuing operations | $m | $m | $m | $m | $m | |||||||||||||||

| AMC | 155.3 | 315.9 | - | 10.3 | 481.5 | |||||||||||||||

| ADM | 106.1 | 408.5 | 78.9 | 18.6 | 612.1 | |||||||||||||||

| ITOM | 172.7 | 507.8 | 4.3 | 106.3 | 791.1 | |||||||||||||||

| CyberRes | 174.5 | 383.9 | 36.3 | 29.1 | 623.8 | |||||||||||||||

| IM&G | 80.0 | 175.6 | 120.3 | 15.5 | 391.4 | |||||||||||||||

| Subtotal | 688.6 | 1,791.7 | 239.8 | 179.8 | 2,899.9 | |||||||||||||||

| Deferred revenue haircut | - | - | - | - | - | |||||||||||||||

| Total Revenue | 688.6 | 1,791.7 | 239.8 | 179.8 | 2,899.9 | |||||||||||||||

Licence | Maintenance | SaaS & other recurring | Consulting | Total | ||||||||||||||||

| Continuing operations | $m | $m | $m | $m | $m | |||||||||||||||

Application Modernization & Connectivity (AMC) | 170.9 | 326.1 | - | 11.7 | 508.7 | |||||||||||||||

Application Delivery Management (ADM) | 130.3 | 485.4 | 87.8 | 18.2 | 721.7 | |||||||||||||||

IT Operations Management (ITOM) | 237.5 | 645.8 | 11.0 | 127.5 | 1,021.8 | |||||||||||||||

Security | 185.7 | 416.7 | 35.0 | 43.9 | 681.3 | |||||||||||||||

Information Management & Governance (IM&G) | 75.6 | 183.6 | 145.9 | 16.6 | 421.7 | |||||||||||||||

| Subtotal | 800.0 | 2,057.6 | 279.7 | 217.9 | 3,355.2 | |||||||||||||||

Deferred revenue haircut | - | (6.0 | ) | (0.8 | ) | - | (6.8 | ) | ||||||||||||

| Total Revenue | 800.0 | 2,051.6 | 278.9 | 217.9 | 3,348.4 | |||||||||||||||

| Licence | Maintenance | SaaS & other recurring | Consulting | Total | ||||||||||||||||

| Continuing operations | $m | $m | $m | $m | $m | |||||||||||||||

| AMC | 138.6 | 321.6 | - | 10.1 | 470.3 | |||||||||||||||

| ADM | 102.0 | 439.2 | 73.9 | 15.9 | 631.0 | |||||||||||||||

| ITOM | 175.1 | 559.4 | 4.6 | 113.9 | 853.0 | |||||||||||||||

| CyberRes | 162.6 | 416.8 | 33.6 | 33.1 | 646.1 | |||||||||||||||

| IM&G | 68.2 | 184.2 | 133.4 | 15.4 | 401.2 | |||||||||||||||

| Subtotal | 646.5 | 1,921.2 | 245.5 | 188.4 | 3,001.6 | |||||||||||||||

| Deferred revenue haircut | - | (0.4 | ) | (0.2 | ) | - | (0.6 | ) | ||||||||||||

| Total Revenue | 646.5 | 1,920.8 | 245.3 | 188.4 | 3,001.0 | |||||||||||||||

Percentage change from October 31, 2020 to October 31, 2021:

| Licence | Maintenance | SaaS & other recurring | Consulting | Total | ||||||||||||||||

| Continuing operations | % | % | % | % | % | |||||||||||||||

| AMC | 12.0 | % | (1.8 | )% | - | 2.0 | % | 2.4 | % | |||||||||||

| ADM | 4.0 | % | (7.0 | )% | 6.8 | % | 17.0 | % | (3.0 | )% | ||||||||||

| ITOM | (1.4 | )% | (9.2 | )% | (6.5 | )% | (6.7 | )% | (7.3 | )% | ||||||||||

| CyberRes | 7.3 | % | (7.9 | )% | 8.0 | % | (12.1 | )% | (3.5 | )% | ||||||||||

| IM&G | 17.3 | % | (4.7 | )% | (9.8 | )% | 0.6 | % | (2.4 | )% | ||||||||||

| Subtotal | 6.5 | % | (6.7 | )% | (2.3 | )% | (4.6 | )% | (3.4 | )% | ||||||||||

| Deferred revenue haircut | - | 100 | % | 100 | % | - | 100 | % | ||||||||||||

| Total Revenue | 6.5 | % | (6.7 | )% | (2.2 | )% | (4.6 | )% | (3.4 | )% | ||||||||||

Revenue by geography

The Group is domiciled in the UK. The Group’s total segmental revenue from external customers by geographical location is detailed below:

Year ended October 31, 2021 | Year ended October 31, 2020 | Period-on- period change | Year ended October 31, 2019 | Period- on – period change | ||||||||||||||||

| $m | $m | % | $m | % | ||||||||||||||||

| UK | 160.0 | 173.0 | (7.5 | )% | 206.9 | (16.4 | )% | |||||||||||||

| USA | 1,263.0 | 1,289.8 | (2.1 | )% | 1,523.0 | (15.3 | )% | |||||||||||||

| Germany | 223.0 | 218.7 | 2.0 | % | 220.7 | (0.9 | )% | |||||||||||||

| Canada | 110.3 | 108.0 | 2.1 | % | 115.9 | (6.8 | )% | |||||||||||||

| France | 100.7 | 101.4 | (0.7 | )% | 123.3 | (17.8 | )% | |||||||||||||

| Japan | 95.6 | 96.9 | (1.3 | )% | 108.6 | (10.8 | )% | |||||||||||||

| Other | 947.3 | 1,013.2 | (6.5 | )% | 1,050.0 | (3.5 | )% | |||||||||||||

| Total Revenue | 2,899.9 | 3,001.0 | (3.4 | )% | 3,348.4 | (10.4 | )% | |||||||||||||

Operating costs

12 months ended October 31, 2019 | 18 months ended October 31, 2018 | Period-on- period change % | Year ended October 31, 2021 | Year ended October 31, 2020 | Period- on- period change | Year ended October 31, 2019 | Period- on- period change | |||||||||||||||||||||||||

| Continuing operations | $m | $m | $m | $m | % | $m | % | |||||||||||||||||||||||||

Cost of sales | 789.9 | 1,302.7 | (39.4 | )% | 776.3 | 702.7 | 10.5 | % | 789.9 | (11.0 | )% | |||||||||||||||||||||

Selling and distribution costs | 1,224.8 | 1,764.2 | (30.6 | )% | 1,344.6 | 1,112.1 | 20.9 | % | 1,224.8 | (9.2 | )% | |||||||||||||||||||||

Research and development expenses | 491.2 | 680.8 | (27.8 | )% | 521.8 | 513.6 | 1.6 | % | 491.2 | 4.6 | % | |||||||||||||||||||||

Administrative expenses | 620.8 | 629.9 | (1.4 | )% | 522.8 | 3,334.0 | (84.3 | )% | 620.8 | 437.0 | % | |||||||||||||||||||||

| Total operating costs | 3,126.7 | 4,377.6 | (28.6 | )% | 3,165.5 | 5,662.4 | (44.1 | )% | 3,126.7 | 81.1 | % | |||||||||||||||||||||

Total operating costs.

Total operating costs for the period decreased by $1,250.9$2,496.9 million, or 28.6%44.1% to $3,126.7$3,165.5 million in the 12 monthsyear ended October 31, 20192021 as compared to $4,377.6$5,662.4 million in the 18 monthsyear ended October 31, 2018.2020.

The single largest component of the operating costs relates to employee costs therefore the shorter period of accountdecrease in the current year only 12 months versus 18 monthsended October 31, 2021 compared to the results of the year ended October 31, 2020 is that the year ended October 31, 2020 included a goodwill impairment charge of $2,799.2 million compared to a charge of $nil in the prior period, means that most cost categories are significantly reduced. The narrative below explains the other key movements excluding employee costs. The exception toyear ended October 31, 2021. Excluding this is administrativecharge operating expenses increased by $302.3 million period-on-period which is discussedprimarily driven by an increase in the amortization expense in relation to the Group’s intangibles assets acquired in business combination of $282.3m resulting from a change in the assessed remaining useful economic lives in the year ended October 31, 2021. For further below.details see note 11 “Intangible assets” of the Consolidated financial statements in Item 18.

Impairment of sales. Costgoodwill is tested annually, or more frequently where there is an indication of sales decreased by $512.8 million, or 39.4%impairment. The Group has not recognized an impairment charge in the period compared to $789.9an impairment charge of $2,799.2 million in the 12 monthsyear ended October 31, 2021.

IFRS 16 “Leases”

The Group adopted IFRS 16 “Leases” on November 1, 2019 on a modified retrospective basis. As a result, the year ended October 31, 2019 continue to be reported under the previous accounting standard IAS 17 “Leases”. Under IAS 17 the cost of leasing assets depended on whether a lease was classified as an operating lease or a finance lease. For operating leases, the cost was recorded as a rental expense in operating costs and for finance leases the cost was recognized as depreciation and interest in operating costs. Under IFRS 16 all leases are treated in the manner of IAS 17 finance leases. As a result, the depreciation and interest expense for leases is significantly higher in the year ended October 31, 2021 and 2020 than in the comparative period ended October 31, 2019, with a similar reduction in rental expenses.

Cost of sales

Cost of sales increased by $73.6 million, or 10.5% to $776.3 million in the year ended October 31, 2021 as compared to $1,302.7$702.7 million in the 18 monthsyear ended October 31, 2018.2020.

The costs in this category predominantly relate to our consulting and helpline support operations amortization of product development costs and the amortization of acquired technology intangibles allintangibles.

25

The amortization of intangible purchased technology costs decreasedincreased by $80.4$67.0 million from $280.5$190.2 million in the 18 monthsyear ended October 31, 20182020 to $200.1$257.2 million in the 12 monthsyear ended October 31, 2019,2021 primarily due to the change in periodreassessment of account and the halting of amortization on SUSE related intangibles after the disposal was announced last year.useful economic lives described above.

Selling and distribution costs.

Selling and distribution costs decreased $539.4increased $232.5 million, or 30.6%20.9% to $1,224.8$1,344.6 million in the 12 monthsyear ended October 31, 20192021 as compared to $1,764.2$1,112.1 million in the 18 monthsyear ended October 31, 2018.2020.

The costs in this category predominantly relate to our salesGo-To-Market organization and the amortization of acquired trade names and amortization of acquired customer relationships all of which are directly reduced by the shorter period of account in the current period.relationships.

The amortization of intangible trade names and customer relationships costs decreasedincreased by $127.0$228.3 million from $572.7$413.9 million in the 18 monthsyear ended October 31, 20182020 to $445.7$642.2 million in the 12 monthsyear ended October 31, 2019,2021 primarily due to the change in periodreassessment of account.useful economic lives described above.

Research and development expenses.

Research and development expenses decreasedincreased by $189.6$8.2 million, or 27.8%1.6% to $491.2$521.8 million in the 12 monthsyear ended October 31, 20192021 as compared to $680.8$513.6 million in the 18 monthsyear ended October 31, 2018.2020.

Administrative expenses.

Administrative expenses decreased by $9.1$2,811.2 million, or 1.4%84.3% to $620.8$522.8 million in the 12 monthsyear ended October 31, 20192021 as compared to $629.9$3,334.0 million in the 18 monthsyear ended October 31, 2018.2020.

The amortizationprimary driver of purchased software intangibles increased by $3.4this increase is the goodwill impairment of $2,799.2 million from $30.7 millionrecorded in the 18 monthsyear ended October 31, 2018 to $34.12020 and discussed above. Excluding this, administrative expenses decreased by $12.0 million inyear on year.

Operating (loss)/profit

In the 12 monthsyear ended October 31, 2019 as the useful life of certain purchase software was revised resulting in an increased amortization charge. Share-based compensation costs increased by $4.5 million from $64.3 million in the 18 months ended October 31, 2018 to $68.8 million in the 12 months ended October 31, 2019 as a result of timing of the issue of share options under the Long-term Incentive Plan in the prior year which meant only 1 month charge was included in the prior period versus a full years charge in the current period.

In addition, the amortization of intangible assets decreasedincreased from $903.1$674.1 million in the 18 monthsyear ended October 31, 2018,2020, to $716.5$956.4 million in the 12 monthsyear ended October 31, 2019, related2021. As discussed above this relates primarily to the additional amortization in the period of technology, trade names, customer relationships established on the acquisition of Interset Software Inc and the impacta reassessment of the 18-month period of account. The reductionremaining useful economic lives for intangibles assets acquired in amortization is not just a result of the reduction in the accounting period as the majority of the amortization is on the intangibles resulting from the HPE acquisition which were only included for 14 months of the 18 month period of account compared to 12 months in the period ended October 31, 2019. The main components of this reduction are included in the discussion on cost by category above.business combinations.

Exceptional items (included within operating (loss)/profit)

Year ended October 31, 2021 | Year ended October 31, 2020 | Year ended October 31, 2019 | ||||||||||

| Exceptional items | $m | $m | $m | |||||||||

| MF/ HPE Software business integration related: | ||||||||||||

| System and IT infrastructure costs | 98.0 | 100.6 | 126.3 | |||||||||

| Integration, severance and property costs | 38.4 | 83.9 | 168.0 | |||||||||

| MF/ HPE Software business integration-related costs | 136.4 | 184.5 | 294.3 | |||||||||

| Other restructuring property costs, severance and legal, acquisition and divestiture costs | 35.3 | 27.9 | (0.1 | ) | ||||||||

| Legal settlement and associated costs | 75.4 | - | - | |||||||||

| 247.1 | 212.4 | 294.2 | ||||||||||

| Goodwill impairment | - | 2,799.2 | - | |||||||||

| Total exceptional costs (reported in Operating (loss)/profit) | 247.1 | 3,011.6 | 294.2 | |||||||||

12 months ended October 31, 2019 | 18 months ended October 31, 2018 | |||||||

| Exceptional items | $m | $m | ||||||

MF/ HPE Software business integration related: | ||||||||

System and IT infrastructure costs | 126.3 | 114.4 | ||||||

Integration costs | 119.6 | 147.6 | ||||||

Severance | 32.1 | 129.1 | ||||||

Property costs | 16.3 | 29.9 | ||||||

| MF/ HPE Software business integration related costs | 294.3 | 421.0 | ||||||

HPE Software business acquisition / pre-acquisition costs | (3.9 | ) | 70.1 | |||||

Integration in respect of previous acquisitions | - | 17.0 | ||||||

Other acquisition costs | 5.4 | - | ||||||

Property costs relating to previous acquisitions | - | 8.2 | ||||||

Divestiture gain on Atalla | (3.7 | ) | - | |||||

Severance costs relating to previous acquisitions | - | 0.6 | ||||||

Pre-disposal costs in relation to SUSE | - | 21.3 | ||||||

Other costs | 2.1 | - | ||||||

| Total exceptional costs (reported in Operating profit) | 294.2 | 538.2 | ||||||

In the 12 monthsyear ended October 31, 2019,2021, exceptional costs totaled $247.1 million and can be split into two categories. Firstly, the Group incurred $136.4m (2020: $184.5m) on integration-related costs in respect of the HPE Software business. This figure primarily relates to $294.2 million. Exceptionalthe migration of Micro Focus to one enterprise-wide platform. In total exceptional costs predominantly relateincurred in relation to the integration of the HPE Software business andsince the costsacquisition are $1,036.2m at October 31, 2021 (total cumulative cost at October 31, 2020: $899.8m). In the period, the Group incurred incremental HPE-related exceptional spend in order to accelerate the 12-month period include:

Secondly, other exceptional spend totaled $110.7m of which $715.2m has been incurred to date. The Group initially expected to incur exceptional costs in relation$75.4m relates to the HPE Software business integrationcost of $420.0m insettling the 12 months ended October 31, 2019, which compares to an actual charge of $294.3m in the financial year. This variance is driven by the phasing of integration programs.

On November 30, 2021, the Group announced the objective to remove a further c.$400 million to c.$500 million of gross annualized operating costs which is anticipated to be undertaken during the years ended October 31, 2022 and 2023. As a result of this program, exceptional spend in relation to delivering these plans are expected to total approximately $200 million over the next two financial years.

Net finance costs

Net finance costs (excluding exceptional items) were $255.8$252.2 million in the 12 monthsyear period ended October 31, 2019. The finance costs predominantly relate2021, compared to $279.0 million in the associated interest on the term loans put in place as part of the transaction to acquire the HPE Software business.year period ended October 31, 2020. Included within the $255.8 millionnet finance costs is $46.7$34.0 million in relation to the amortization of facility costs and original issue discounts, which were paid on initiation of the term loans.loan.

The declinedecrease on the prior year related to an acceleration of fees and discounts of $24.0 million resulting from refinancing completed in net finance costs (excluding exceptional items) between the periods of $81.1m, 24.1% from $336.9 million for the 18 months ended October 31, 2018 to $225.7 million for the 12 months ended October 31, 2019 reflects a $61.6 reduction in finance costs and a $19.5m increase in finance income. The reduction in finance costs primarily reflects a decrease in interest on bank borrowings of $51.1 million from $276.5 in the 18 months ended October 31, 2018 to $225.4 million in the 12 months ended October 31, 2019 as a result of the shorter accounting period. The increase in finance income primarily reflects an increase in bank interest earned of $12.7 million as a result of interest income earned on cash deposits held following the completion of the SUSE divestment until the Group returned $1.8 billion of proceeds to shareholders.that period

The Group holdholds interest rate swaps to hedge against the cash flow risk in the LIBOR rate charged on $2,250.0 million of the debt issued by Seattle Spinco, Inc. (the investment company used to acquire the software business of HPE)HPE Software business) from October 19, 2017 to September 30, 2022. Under the terms of the interest rate swaps, the Group pays a fixed rate of 1.94%1.95% and receives 1-month USDone-month US dollar LIBOR.

Taxation

The Group’sGroup reported a tax credit for the 12 monthsyear ended October 31, 2019 was a credit2021 of $16.0$82.7 million (18 months(year ended October 31, 2018:2020: charge of $34.2 million). There is no significant difference between the tax credit of $673.1 million, primarily due toin the one-off impact of USyear and the expected tax reforms).credit at the statutory rate.

(Loss)/profit after tax from continuing operations

The loss after tax from continuing operations was $18.1$435.1 million in the 12 monthsyear ended October 31, 2019,2021, compared to a profitloss after tax from continuing operations of $707.2$2,974.6 million in the 18 monthsyear ended October 31, 2018.2020.

Profit from discontinued operation

Earnings per share

The table below sets out the Earnings per Share (“EPS”). The Group is also required to present EPS for both the continuing and discontinued operations.

12 months ended October 31, 2019 | 18 months ended October 31, 2018 | Year ended October 31, 2021 | Year ended October 31, 2020 | Year ended October 31, 2019 | ||||||||||||||||||||||||||||||||||||

Basic Cents | Diluted 1 Cents | Basic Cents | Diluted Cents | Basic Cents | Diluted1 Cents | Basic Cents | Diluted 1 Cents | Basic Cents | Diluted1 Cents | |||||||||||||||||||||||||||||||

Continuing operations | (4.87 | ) | (4.87 | ) | 181.91 | 176.92 | (129.30 | ) | (129.30 | ) | (886.15 | ) | (886.15 | ) | (4.87 | ) | (4.87 | ) | ||||||||||||||||||||||

Discontinued operation | 393.37 | 389.16 | 19.79 | 19.25 | 3.18 | 3.18 | 1.52 | 1.52 | 393.37 | 389.16 | ||||||||||||||||||||||||||||||

| Total EPS | 388.50 | 384.35 | 201.70 | 196.17 | (126.12 | ) | (126.12 | ) | (884.63 | ) | (884.63 | ) | 388.50 | 384.35 | ||||||||||||||||||||||||||

1 As there is a loss from continuing operations attributable to the ordinary equity shareholders of the Company for the 12 monthsyear ended October 31, 20192021 ($18.4435.1 million) and 2020 ($2,974.6 million), the Diluted EPS is reported as equal to Basic EPS, as no account can be taken of the effect of dilutive securities under IAS 33. There was total earnings attributable to ordinary equity shareholders of

In the Company for the 12 monthsyear ended October 31, 2019 of $1,468.8 million and therefore the effect of dilutive securities can be reflected in the total Diluted EPS above.

18 months ended October 31, 2018 | 12 months ended April 30, 2017 | |||||||

| Continuing operations | $m | $m | ||||||

| Revenue | 4,754.4 | 1,077.3 | ||||||

Operating profit (before exceptional items) | 915.0 | 324.7 | ||||||

Exceptional items | (538.2 | ) | (97.3 | ) | ||||

| Operating profit | 376.8 | 227.4 | ||||||

Net finance costs (excluding exceptional items) | (336.9 | ) | (95.8 | ) | ||||

Exceptional finance costs | (5.8 | ) | - | |||||

| (Loss)/profit before tax | 34.1 | 131.6 | ||||||

Taxation | 673.1 | (7.5 | ) | |||||

| (Loss)/profit from continuing operations | 707.2 | 124.1 | ||||||

Profit from discontinued operation | 76.9 | 33.7 | ||||||

| Profit for the period | 784.1 | 157.8 | ||||||

18 months ended October 31, 2018 | 12 months ended April 30, 2017 | Period-on – period change | ||||||||||

| Continuing operations | $m | $m | % | |||||||||

Licence | 1,213.7 | 308.4 | 293.5 | % | ||||||||

Maintenance | 2,861.6 | 727.6 | 293.3 | % | ||||||||

SaaS & other recurring | 373.9 | - | n/a | |||||||||

Consulting | 366.3 | 48.2 | 660.0 | % | ||||||||

| Revenue before haircut | 4,815.5 | 1,082.2 | 344.2 | % | ||||||||

Deferred revenue haircut | (61.1 | ) | (6.9 | ) | 785.5 | % | ||||||

| Total Revenue | 4,754.4 | 1,077.3 | 341.3 | % | ||||||||

Licence | Maintenance | Consulting | SaaS & other recurring | Total | ||||||||||||||||

| Continuing operations | $m | $m | $m | $m | $m | |||||||||||||||

Application Modernization & Connectivity (AMC) | 256.3 | 497.6 | 17.9 | - | 771.8 | |||||||||||||||

Application Delivery Management (ADM) | 185.4 | 646.7 | 41.6 | 114.1 | 987.8 | |||||||||||||||

IT Operations Management (ITOM) | 363.2 | 869.9 | 192.8 | 15.1 | 1,441.0 | |||||||||||||||

Security | 291.6 | 580.2 | 81.4 | 41.6 | 994.8 | |||||||||||||||

Information Management & Governance (IM&G) | 117.2 | 267.2 | 32.6 | 203.1 | 620.1 | |||||||||||||||

| Subtotal | 1,213.7 | 2,861.6 | 366.3 | 373.9 | 4,815.5 | |||||||||||||||