UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended June 30, 20122014

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition periodfrom ___________ to ___________.___________.

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report _________________________

Commission file number:001-33602

HOLLYSYS AUTOMATION TECHNOLOGIES LTD.

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

British Virgin Islands

(Jurisdiction of incorporation or organization)

No. 2 Disheng Middle Road,

Beijing Economic-Technological Development Area,

Beijing, P. R. China 100176

(Address of principal executive offices)

Jennifer Zhang, Tel: (86 10) 5898 1386, Email:zhangqiuju@hollysys.com

Address: No. 2 Disheng Middle Road, Beijing Economic-Technological Development Area, Beijing, P.R. China 100176

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Name of each exchange on which registered | |

| Ordinary Shares, $0.001 par value per share | The NASDAQ Global Select Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or ordinary shares as of the close of the period covered by the annual report (June 30, 2012)2014): 55,998,917[57,554,824] ordinary shares.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. xYes ¨YesxNo

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨Yesx No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.xYes¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer.

Large accelerated filer¨x Accelerated filerx¨ Non-accelerated filer¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAPx | International Financial Reporting Standards as issued by the International Accounting Standards Board¨ | Other¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).¨Yes x No

HOLLYSYS AUTOMATION TECHNOLOGIES LTD.

ANNUAL REPORT ON FORM 20-F

FOR THE FISCAL YEAR ENDED JUNE 30, 20122014

TABLE OF CONTENTS

| ITEM 16F. | CHANGE IN REGISTRANT’S CERTIFYING ACCOUNTANT | 91 |

| ITEM | ||

| ITEM | ||

| PART III | ||

| FINANCIAL STATEMENTS | 92 | |

| ITEM | FINANCIAL STATEMENTS | |

| ITEM 19. | EXHIBITS | |

USE OF CERTAIN DEFINED TERMS

Except as otherwise indicated by the context, references in this annual report to:

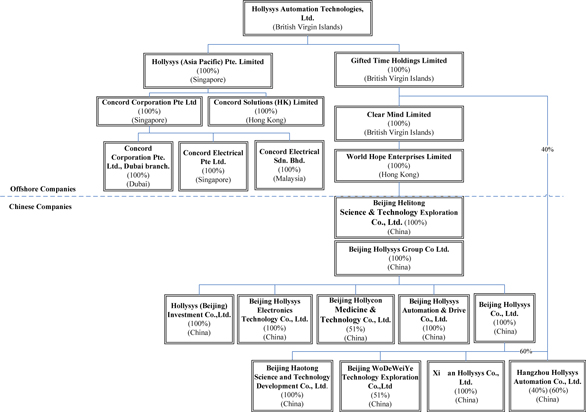

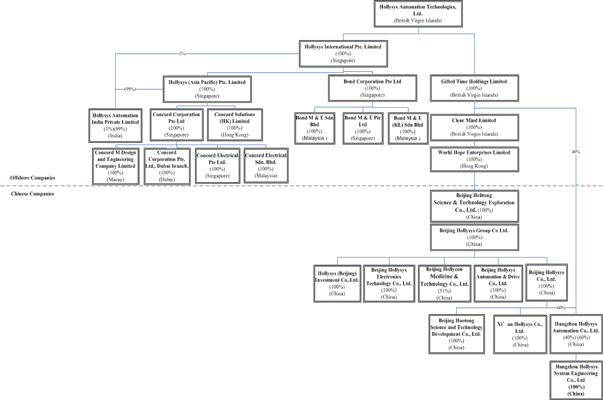

| · | “Hollysys” “we,” “us,” or “our,” and the “Company,” are references to the combined business of Hollysys Automation Technologies Ltd., a BVI company, and its consolidated subsidiaries, HI, HAP, HAIP, Bond, Concord, CSHK, CDME, GTH, Clear Mind, World Hope, Helitong, |

| · | “HI” are references to Hollysys International Pte. Limited, a Singapore company; |

| · | “HAP” are references to Hollysys (Asia Pacific) Pte. Limited, a Singapore company; |

| · | “HAIP” are references to Hollysys Automation India Private Limited, an India Company; |

| · | “Concord” are references to a group of our Singapore |

| · | “CSHK” are references to |

| · | “CMDE” are references to Concord M Design and Engineering Company Limited, a Macau company; |

| · | “Bond” are references to a group of our Southeastern Asia subsidiaries, including Bond Corporation Pte. Ltd., a Singapore company (“BCPL”), Bond M&E Pte. Ltd., a Singapore Company (“BMSG”), Bond M&E Sdn. Bhd., a Malaysia company (“BMJB”), and Bond M&E (K.L.) Sdn. Bhd.,a Malaysia company (“BMKL”); |

| · | “GTH” are references to Gifted Time Holdings Limited, a BVI company; |

| · | “Clear Mind” are references to Clear Mind Limited, a BVI company; |

| · | “World Hope” are references to World Hope Enterprises Limited, a Hong Kong company; |

| · | “Helitong” are references Beijing Helitong Science & Technology Exploration Co., Ltd.; |

| · | “ |

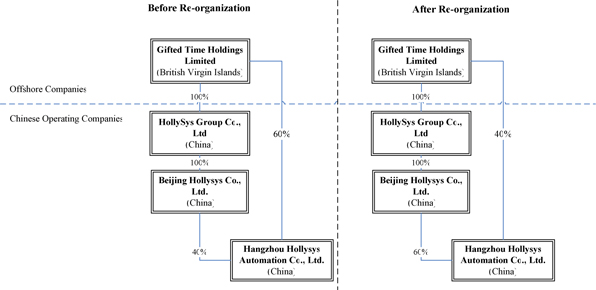

| · | “Hangzhou Hollysys” are references to Hangzhou Hollysys Automation Co., Ltd. |

| · | “Hangzhou System” are references to Hangzhou Hollysys System Engineering Co., Ltd., a PRC company; |

| · | “Hollysys A&D” are references to Beijing Hollysys Automation & Drive Co., Ltd. |

| · | “Beijing Hollysys” are references to Beijing Hollysys Co., Ltd. |

| · | “Hollysys Electronics” are references to Beijing Hollysys Electronics Technology Co., Ltd. |

| · | “Hollycon” are references to Beijing Hollycon Medicine & Technology. Co., Ltd. |

| · | “Haotong” are references to Beijing Haotong Science and Technology Development Co., Ltd. |

| · | “Xi’an Hollysys” are references to Xi’an Hollysys Co., |

| · | “Hollysys Investment” are references to Hollysys (Beijing) Investment Co., Ltd. |

| · | “ |

| · | “BVI” are references to the British Virgin Islands; |

| · | “China” and “PRC” are references to the People’s Republic of |

| · | “Hong Kong” are references to the Hong Kong Special Administrative Region of China; |

| · | “Macau” are references to the Macau Special Administrative Region of China; |

| · | “Exchange Act” are references to the Securities Exchange Act of 1934, as amended; and |

| · | “Securities Act,” are references to the Securities Act of 1933, as amended. |

FORWARD-LOOKING INFORMATION

This annual report contains forward-looking statements and information relating to us that are based on the current beliefs, expectations, assumptions, estimates and projections of our management regarding our company and industry. When used in this annual report, the words “may”, “will”, “anticipate”, “believe”, “estimate”, “expect”, “intend”, “plan” and similar expressions, as they relate to us or our management, are intended to identify forward-looking statements. These statements reflect management's current view of us concerning future events and are subject to certain risks, uncertainties and assumptions, including among many others: our potential inability to achieve similar growth in future periods as we did historically, a decrease in the availability of our raw materials, the emergence of additional competing technologies, changes in domestic and foreign laws, regulations and taxes, changes in economic conditions, uncertainties related to China’s legal system and economic, political and social events in China, the volatility of the securities markets, and other risks and uncertainties which are generally set forth under the heading, “Key information — Risk Factors” and elsewhere in this annual report. Should any of these risks or uncertainties materialize, or should the underlying assumptions about our business and the commercial markets in which we operate prove incorrect, actual results may vary materially from those described as anticipated, estimated or expected in this annual report.

All forward-looking statements included herein attributable to us or other parties or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Except to the extent required by applicable laws and regulations, we undertake no obligations to update these forward-looking statements to reflect events or circumstances after the date of this annual report or to reflect the occurrence of unanticipated events.

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| ITEM 3. | KEY INFORMATION |

A. Selected Consolidated Financial Data

The following table presents selected financial data regarding our business. It should be read in conjunction with our consolidated financial statements and related notes contained elsewhere in this annual report and the information under Item 5, “Operating and Financial Review and Prospects.” The selected consolidated statement of comprehensive income data for the fiscal years ended June 30, 2010, 20112012, 2013 and 20122014 and the consolidated balance sheet data as of June 30, 20112013 and 20122014 have been derived from the audited consolidated financial statements of Hollysys that are included in this annual report beginning on page F-1. The selected statement of comprehensive income data for the fiscal years ended June 30, 20082010 and 2009,2011, and balance sheet data as of June 30, 2008, 20092010, 2011 and 20102012 have been derived from our audited financial statements that are not included in this annual report.

The audited consolidated financial statements for the years ended June 30, 2010, 20112012, 2013 and 20122014 are prepared and presented in accordance with generally accepted accounting principles in the United States, or US GAAP. The selected financial data information is only a summary and should be read in conjunction with the historical consolidated financial statements and related notes of Hollysys contained elsewhere herein. The financial statements contained elsewhere fully represent our financial condition and operations; however, they are not indicative of our future performance.

Financial information in this report is reported in United States dollars, the reporting currency of the Company.

| Years Ended June 30, | ||||||||||||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | ||||||||||||||||

| Statement of Income Data | ||||||||||||||||||||

| Revenue | 121,498,752 | 157,502,067 | 174,089,196 | 262,841,886 | 321,703,932 | |||||||||||||||

| Operating income (loss) | 5,844,538 | (5,550,479 | ) | 32,547,400 | 44,690,766 | 65,438,184 | ||||||||||||||

| Income (loss) before income taxes | 2,248,419 | (5,603,121 | ) | 35,219,424 | 47,909,081 | 66,926,065 | ||||||||||||||

| Net loss (income) attributable to Hollysys | (1,677,178 | ) | (13,851,064 | ) | 25,704,538 | 41,469,998 | 56,221,847 | |||||||||||||

| Add: Amortization of discount and interest on notes payable related to bridge loan | 3,244,434 | - | - | - | - | |||||||||||||||

| Share based compensation costs | 17,084,473 | 39,559,026 | 524,076 | 551,966 | 1,139,368 | |||||||||||||||

| Non-GAAP net income attributable to Hollysys | 18,651,729 | 25,707,962 | 26,228,614 | 42,021,964 | 57,361,215 | |||||||||||||||

| Weighted average ordinary shares | 37,658,437 | 44,950,883 | 51,243,667 | 54,564,842 | 55,659,765 | |||||||||||||||

| Weighted average number of diluted ordinary shares | 37,658,437 | 44,950,883 | 51,838,294 | 54,949,280 | 55,828,361 | |||||||||||||||

| Basic earnings (loss) per share | (0.04 | ) | (0.31 | ) | 0.50 | 0.76 | 1.01 | |||||||||||||

| Diluted earnings (loss) per share | (0.04 | ) | (0.31 | ) | 0.50 | 0.75 | 1.01 | |||||||||||||

| Non-GAAP basic earnings per share | 0.50 | 0.57 | 0.51 | 0.77 | 1.03 | |||||||||||||||

| Non-GAAP diluted earnings per share | 0.48 | 0.51 | 0.51 | 0.76 | 1.03 | |||||||||||||||

| Balance Sheet Data | ||||||||||||||||||||

| Total current assets | 214,320,514 | 283,971,473 | 301,359,086 | 362,411,956 | 437,672,433 | |||||||||||||||

| Total assets | 252,734,095 | 345,443,522 | 384,730,251 | 458,583,944 | 552,754,975 | |||||||||||||||

| Total current liabilities | 71,028,772 | 101,121,574 | 135,917,248 | 161,038,804 | 188,828,622 | |||||||||||||||

| Total liabilities | 87,794,820 | 149,424,388 | 171,258,661 | 192,715,669 | 213,469,996 | |||||||||||||||

| Noncontrolling interests | 17,645,377 | 22,479,241 | 774,865 | 810,618 | 1,183,864 | |||||||||||||||

| Stockholders’ equity | 147,293,898 | 173,539,893 | 212,696,725 | 265,057,657 | 338,101,115 | |||||||||||||||

| Years Ended June 30, | ||||||||||||||||||||

| 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||||||

| Statement of Comprehensive Income Data | ||||||||||||||||||||

| Revenue | 174,089,196 | 262,841,886 | 321,703,932 | 349,055,002 | 521,331,846 | |||||||||||||||

| Operating income | 32,547,400 | 44,690,766 | 65,438,184 | 57,702,105 | 98,407,029 | |||||||||||||||

| Income before income taxes | 35,219,424 | 47,909,081 | 66,926,065 | 60,617,681 | 91,311,475 | |||||||||||||||

| Net income attributable to Hollysys | 25,704,538 | 41,469,998 | 56,221,847 | 51,994,402 | 69,619,583 | |||||||||||||||

| Add: Share-based compensation costs | 524,076 | 551,966 | 1,139,368 | 1,599,496 | 2,986,192 | |||||||||||||||

| Amortization of acquired intangible assets | - | - | - | 2,847,773 | 5,412,766 | |||||||||||||||

| Acquisition-related consideration fair value adjustments | - | - | - | 1,163,179 | 8,919,629 | |||||||||||||||

| Non-GAAP net income attributable to Hollysys | 26,228,614 | 42,021,964 | 57,361,215 | 57,604,850 | 86,938,170 | |||||||||||||||

| Weighted average ordinary shares: | ||||||||||||||||||||

| Basic | 51,243,667 | 54,564,842 | 55,659,765 | 56,167,592 | 57,926,333 | |||||||||||||||

| Diluted | 51,838,294 | 54,949,280 | 55,828,361 | 56,412,469 | 58,426,642 | |||||||||||||||

| Earnings per share: | ||||||||||||||||||||

| Basic | 0.50 | 0.76 | 1.01 | 0.93 | 1.20 | |||||||||||||||

| Diluted | 0.50 | 0.75 | 1.01 | 0.92 | 1.19 | |||||||||||||||

| Non-GAAP earnings per share: | ||||||||||||||||||||

| Basic | 0.51 | 0.77 | 1.03 | 1.03 | 1.50 | |||||||||||||||

| Diluted | 0.51 | 0.76 | 1.03 | 1.02 | 1.49 | |||||||||||||||

| Balance Sheet Data | ||||||||||||||||||||

| Total current assets | 301,359,086 | 362,411,956 | 437,672,433 | 546,448,188 | 729,892,656 | |||||||||||||||

| Total assets | 384,730,251 | 458,583,944 | 552,754,975 | 744,632,926 | 926,694,505 | |||||||||||||||

| Total current liabilities | 135,917,248 | 161,038,804 | 188,828,622 | 268,452,183 | 398,891,030 | |||||||||||||||

| Total liabilities | 171,258,661 | 192,715,669 | 213,469,996 | 329,157,931 | 434,636,627 | |||||||||||||||

| Net assets | 213,471,590 | 265,868,275 | 339,284,979 | 415,474,995 | 492,057,878 | |||||||||||||||

| Noncontrolling interest | 774,865 | 810,618 | 1,183,864 | 1,746,707 | 3,583,331 | |||||||||||||||

| Stockholders’ equity | 212,696,725 | 265,057,657 | 338,101,115 | 413,728,288 | 488,474,547 | |||||||||||||||

In evaluating our results, the non-GAAP measures of “Non-GAAP Generalgeneral and Administrative Expenses (hereafter “Gadministrative expenses (“Non-GAAP G&A Expenses”expenses”)”,“Non-GAAP cost of integrated contracts”, “Non-GAAP Income (loss) from Operations”other income (expenses), net”, “Non-GAAP interest expenses”, “Non-GAAP net income attributable to Hollysys” and “Non-GAAP Net income (loss) and Earnings (loss)earnings per share” serve as additional indicators of our operating performance and not as a replacement for other measures in accordance with US GAAP. We believe these non-GAAP measures are useful to investors as they excludeexclude: 1) share-based compensation expenses, 2) amortization of discountacquired intangible assets and interest on notes payable related to the bridge loan and share based compensation costs. The amortization3) acquisition-related consideration adjustments. All of discount and interest on notes payable related to bridge loan is non-recurring and non-operation-related in nature. The share based compensation is calculated based on, among others, the number of shares/options granted and the stock price as of the grant date. Itabove will not result in any operating cash inflows or outflows. We believe that using non-GAAP measures help our shareholders to have a better understanding of our operating results and growth prospects. In addition, given the business nature of Hollysys, it has been a common practice for investors and analysts to use such non-GAAP measures to evaluate the Company.Company.Specifically, the non-GAAP measuresexcluded the following items:

1) Share-based compensation expenses,which is calculated based on the number of shares or options granted and the fair value as of grant date.

2) Amortization of acquired intangible assets, which is a non-cash expense relating primarily to acquisitions. At the time of an acquisition, the identifiable definite-lived intangible assets of the acquired company, such as customer relationships and order backlog, are valued and amortized over their estimated lives. Value is also assigned to acquired indefinite-lived intangible assets, which comprise goodwill that are not subject to amortization.

3) Acquisition-related consideration adjustmentsare accounting adjustments to report contingent share consideration liabilities at fair value and cash consideration at present value.These adjustments can be highly variable and are excluded from our assessment of performance because they are considered non-operational in nature and, therefore, are not indicative of current or future performance or ongoing costs of doing business.

The following table provides a reconciliation of U.S. GAAP measures to the non-GAAP measures for the periods indicated:

| Years ended June 30, | ||||||||||||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | ||||||||||||||||

| G&A Expenses | 26,588,771 | 48,981,078 | 13,914,091 | 16,671,448 | 26,025,459 | |||||||||||||||

| Minus: Share based compensation costs | 17,084,473 | 39,559,026 | 524,076 | 551,966 | 1,139,368 | |||||||||||||||

| Non-GAAP G&A Expenses | 9,504,298 | 9,422,052 | 13,390,015 | 16,119,482 | 24,886,091 | |||||||||||||||

| Net income (loss) attributable to Hollysys | (1,677,178 | ) | (13,851,064 | ) | 25,704,538 | 41,469,998 | 56,221,847 | |||||||||||||

| Add: Amortization of discount and interest on notes payable related to bridge loan | 3,244,434 | - | - | - | - | |||||||||||||||

| Add: Share based compensation costs | 17,084,473 | 39,559,026 | 524,076 | 551,966 | 1,139,368 | |||||||||||||||

| Non-GAAP net income attributable to Hollysys | 18,651,729 | 25,707,962 | 26,228,614 | 42,021,964 | 57,361,215 | |||||||||||||||

| Weighted average ordinary shares | 37,658,437 | 44,950,883 | 51,243,667 | 54,564,842 | 55,659,765 | |||||||||||||||

| Weighted average number of diluted ordinary shares | 38,664,032 | 50,015,536 | 51,838,294 | 54,949,280 | 55,828,361 | |||||||||||||||

| Non-GAAP basic earnings per share | 0.50 | 0.57 | 0.51 | 0.77 | 1.03 | |||||||||||||||

| Non-GAAP diluted earnings per share | 0.48 | 0.51 | 0.51 | 0.76 | 1.03 | |||||||||||||||

| Years ended June 30, | ||||||||||||||||||||

| 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||||||

| Cost of integrated contracts | 110,268,475 | 165,354,157 | 189,152,826 | 218,586,778 | 330,038,563 | |||||||||||||||

| Less: amortization of acquired intangibles | - | - | - | 2,847,773 | 5,412,766 | |||||||||||||||

| Non-GAAP cost of integrated contracts | 110,268,475 | 165,354,157 | 189,152,826 | 215,739,005 | 324,625,797 | |||||||||||||||

| G&A expenses | 13,914,091 | 16,671,448 | 26,025,459 | 29,647,665 | 39,716,156 | |||||||||||||||

| Less: share-based compensation costs | 524,076 | 551,966 | 1,139,368 | 1,599,496 | 2,986,192 | |||||||||||||||

| Non-GAAP G&A expenses | 13,390,015 | 16,119,482 | 24,886,091 | 28,048,169 | 36,729,964 | |||||||||||||||

| Other (expenses) income, net | (215,277 | ) | (208,093 | ) | 792,817 | 879,427 | (5,658,524 | ) | ||||||||||||

| Add: acquisition-related incentive share contingent consideration fair value adjustments | - | - | - | 854,549 | 7,988,640 | |||||||||||||||

| Non-GAAP other (expenses) income, net | (215,277 | ) | (208,093 | ) | 792,817 | 1,733,976 | 2,330,116 | |||||||||||||

| Interest expenses | (2,220,467 | ) | (2,680,141 | ) | (3,097,754 | ) | (2,169,667 | ) | (1,998,311 | ) | ||||||||||

| Add: acquisition-related cash consideration adjustments | - | - | - | 308,630 | 930,988 | |||||||||||||||

| Non-GAAP interest expenses | (2,220,467 | ) | (2,680,141 | ) | (3,097,754 | ) | (1,861,037 | ) | (1,067,323 | ) | ||||||||||

| Net income attributable to Hollysys | 25,704,538 | 41,469,998 | 56,221,847 | 51,994,402 | 69,619,583 | |||||||||||||||

| Add: share-based compensation costs | 524,076 | 551,966 | 1,139,368 | 1,599,496 | 2,986,192 | |||||||||||||||

| Amortization of acquired intangible assets | - | - | - | 2,847,773 | 5,412,766 | |||||||||||||||

| Acquisition-related consideration adjustments | - | - | - | 1,163,179 | 8,919,629 | |||||||||||||||

| Non-GAAP net income attributable to Hollysys | 26,228,614 | 42,021,964 | 57,361,215 | 57,604,850 | 86,938,170 | |||||||||||||||

| Weighted average number of ordinary shares outstanding used in computation: | ||||||||||||||||||||

| Basic | 51,243,667 | 54,564,842 | 55,659,765 | 56,167,592 | 57,926,333 | |||||||||||||||

| Diluted | 51,838,294 | 54,949,280 | 55,828,361 | 56,412,469 | 58,426,642 | |||||||||||||||

| Non-GAAP earnings per share: | ||||||||||||||||||||

| Basic | 0.51 | 0.77 | 1.03 | 1.03 | 1.50 | |||||||||||||||

| Diluted | 0.51 | 0.76 | 1.03 | 1.02 | 1.49 | |||||||||||||||

Exchange Rate Information

A majority of our business is conducted in China. We also operate in Singapore and Malaysia through HAP, and Concord, Bond, and several other jurisdictions in Asia and the Middle East. We use US dollars as our reporting currency in our financial statements and in this annual report. For entities whose functional currencies are not US dollars, balance sheet items are translated into US dollars at the rates of exchange as of the balance sheet date; equity accounts are translated at historical exchange rates and revenues, expenses, gains and losses are translated using the average rate for the year as published by the Federal Reserve Bank of New York and the Federal Reserve Board. Translation adjustments are reported as cumulative translation adjustments and are shown as a separate component of other comprehensive income in the consolidated statement of comprehensive income and changes in equity. Transactions and amounts in other parts of this annual report in foreign currencies recorded at the rates of exchange prevailing when the transactions occurred. With respect to amounts not recorded in our consolidated financial statements but included elsewhere in this annual report, all transactions fromconversion between Renminbi intoand US dollars and from US dollars to Renminbi in this annual report on Form 20-F were made at a rate of RMB6.3249RMB 6.1468 to $1.00, and all transactions fromconversion between Singapore dollars intoand US dollars and from US dollars to Singapore dollars in this annual report on Form 20-F were made at a rate of SGD 1.27371.2602 to $1.00, as set forth by the Federal Reserve Bank of New York. We make no representation of any kind that any Renminbi, Singapore dollar, US dollar or any other currency amountsreferenced in this report could have been, or could be, converted into the other stated currencies at any particular rate, the rates stated below, any particular rate, or at all. The Chinese government imposes control over its foreign-currency reserves in part through both direct regulation of theconcerns conversion of Renminbi into foreign exchange and through restrictions on foreign trade. On August 31, 2012,September 19, 2014, the closing buying rate wasfor using RMB 6.3542 to $1.00, and SGD 1.2491 to $1.00,buy 1.00 USD was 6.1403 and 1.2662 respectively, as set forth by the Federal Reserve Board.

The following table sets forth information concerning exchange rates between the Renminbi, Singapore dollars and the US dollar for the periods indicated. These rates are provided solely for your convenience and are not necessarily the exchange rates that we used in this annual report on Form 20-F or will use in the preparation of our periodic reports or any other information to be provided to you.

| Exchange Rate between RMB and US$ | Exchange Rate between SGD and US$ | |||||||||||||||||||||||||||||||

| Period | Period End | Average | Low | High | Period End | Average | Low | High | ||||||||||||||||||||||||

| Calendar year 2007 | 7.2946 | 7.5806 | 7.8127 | 7.2946 | 1.436 | 1.5065 | 1.5439 | 1.436 | ||||||||||||||||||||||||

| Calendar year 2008 | 6.8225 | 6.9193 | 7.2946 | 6.78 | 1.4377 | 1.414 | 1.531 | 1.3472 | ||||||||||||||||||||||||

| Calendar year 2009 | 6.8259 | 6.8295 | 6.847 | 6.8176 | 1.4035 | 1.4543 | 1.5565 | 1.3795 | ||||||||||||||||||||||||

| Calendar year 2010 | 6.6 | 6.4356 | 6.7861 | 6.7503 | 1.2885 | 1.3629 | 1.4228 | 1.2824 | ||||||||||||||||||||||||

| Calendar year 2011 | 6.2939 | 6.463 | 6.6364 | 6.2939 | 1.2948 | 1.2565 | 1.3135 | 1.2007 | ||||||||||||||||||||||||

| January 31, 2012 | 6.308 | 6.3119 | 6.333 | 6.294 | 1.2576 | 1.2777 | 1.2973 | 1.2526 | ||||||||||||||||||||||||

| February 29, 2012 | 6.2935 | 6.2997 | 6.312 | 6.2935 | 1.2474 | 1.2535 | 1.2646 | 1.2424 | ||||||||||||||||||||||||

| March 30, 2012 | 6.2975 | 6.3125 | 6.3315 | 6.2975 | 1.2573 | 1.259 | 1.2686 | 1.2474 | ||||||||||||||||||||||||

| April 30, 2012 | 6.279 | 6.3043 | 6.315 | 6.279 | 1.2368 | 1.251 | 1.2627 | 1.2368 | ||||||||||||||||||||||||

| May 31, 2012 | 6.3684 | 6.3242 | 6.3684 | 6.3052 | 1.2888 | 1.262 | 1.2888 | 1.2355 | ||||||||||||||||||||||||

| June 29, 2012 | 6.353 | 6.3632 | 6.3703 | 6.353 | 1.2673 | 1.2784 | 1.2918 | 1.2654 | ||||||||||||||||||||||||

| July 31, 2012 | 6.361 | 6.3714 | 6.3879 | 6.3487 | 1.2437 | 1.2603 | 1.2729 | 1.2437 | ||||||||||||||||||||||||

| August 31, 2012 | 6.3484 | 6.3593 | 6.3738 | 6.3484 | 1.2477 | 1.248 | 1.2537 | 1.2403 | ||||||||||||||||||||||||

| Exchange Rate between RMB and US$ | Exchange Rate between SGD and US$ | |||||||||||||||||||||||||||||||

| Period | Period End | Average | Low | High | Period End | Average | Low | High | ||||||||||||||||||||||||

| Calendar year 2009 | 6.8259 | 6.8295 | 6.8470 | 6.8176 | 1.4035 | 1.4543 | 1.5565 | 1.3795 | ||||||||||||||||||||||||

| Calendar year 2010 | 6.6000 | 6.4356 | 6.7861 | 6.7503 | 1.2885 | 1.3629 | 1.4228 | 1.2824 | ||||||||||||||||||||||||

| Calendar year 2011 | 6.2939 | 6.4630 | 6.6364 | 6.2939 | 1.2948 | 1.2565 | 1.3135 | 1.2007 | ||||||||||||||||||||||||

| Calendar year 2012 | 6.2301 | 6.2990 | 6.3879 | 6.2221 | 1.2214 | 1.2492 | 1.2973 | 1.2159 | ||||||||||||||||||||||||

| Calendar year 2013 | 6.0537 | 6.1478 | 6.0537 | 6.2438 | 1.2622 | 1.2511 | 1.2203 | 1.2831 | ||||||||||||||||||||||||

| January 31, 2014 | 6.0590 | 6.0509 | 6.0402 | 6.0600 | 1.2772 | 1.2726 | 1.2647 | 1.2792 | ||||||||||||||||||||||||

| February 28, 2014 | 6.1448 | 6.0816 | 6.0591 | 6.1448 | 1.2669 | 1.2659 | 1.2602 | 1.2755 | ||||||||||||||||||||||||

| March 31, 2014 | 6.2164 | 6.1729 | 6.1183 | 6.2273 | 1.2583 | 1.2672 | 1.2583 | 1.2774 | ||||||||||||||||||||||||

| April 30, 2014 | 6.2591 | 6.2246 | 6.1966 | 6.2591 | 1.2553 | 1.2548 | 1.2473 | 1.2633 | ||||||||||||||||||||||||

| May 30, 2014 | 6.2471 | 6.2380 | 6.2255 | 6.2591 | 1.2543 | 1.2514 | 1.2460 | 1.2564 | ||||||||||||||||||||||||

| June 28, 2014 | 6.2036 | 6.2306 | 6.2036 | 6.2548 | 1.2465 | 1.2512 | 1.2465 | 1.2572 | ||||||||||||||||||||||||

| July 31, 2014 | 6.1737 | 6.1984 | 6.1712 | 6.2115 | 1.2466 | 1.2427 | 1.2376 | 1.2472 | ||||||||||||||||||||||||

| August 29, 2014 | 6.1430 | 6.1541 | 6.1395 | 6.1793 | 1.2485 | 1.2484 | 1.2444 | 1.2514 | ||||||||||||||||||||||||

| September 19, 2014 | 6.1403 | 6.1387 | 6.1284 | 6.1480 | 1.2662 | 1.2603 | 1.2522 | 1.2678 | ||||||||||||||||||||||||

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

An investment in our capital stock involves a high degree of risk. You should carefully consider the risks described below, together with all of the other information included in this annual report, before making an investment decision. If any of the following risks actually occurs, our business, prospects, financial condition or results of operations could suffer. In that case, the trading price of our capital stock could decline, and you may lose all or part of your investment.

RISKS RELATED TO OUR BUSINESS

We will need to commit greatersubstantial resources to new product and service development and acquisition opportunities in order to stay competitive and grow our business, and we may fail to offset the increased cost of such developmentinvestment with a sufficient increase in net sales or margins.

The success of our business depends in great measure on our ability to keep pace with, or even lead, changes that occur in our industry and expand our product and service offerings. Traditionally, the automation and control systems business was relatively stable and slow moving. Successive generations of products offered only marginal improvements in terms of functionality and reliability. However, the emergence of computers, computer networks and electronic components as key elements of the systems that we design and build has accelerated the pace of change in our industry. Where there was formerly as much as a decade or more between successive generations of automation systems, the time between generations is now as little as two to three years. Technological advances and the introduction of new products, new designs and new manufacturing techniques by our competitors could adversely affect our business unless we are able to respond with similar advances. To remain competitive, we must continue to incur significant costs in product development, equipment and facilities and to make capital investments.investments and seek complementary acquisitions. These costs may increase, resulting in greater fixed costs and operating expenses than we have incurred to date. As a result, we could be required to expend substantial funds for and commit significant resources to the following:

| · | Research and development activities on existing and potential product solutions; |

| · | Additional engineering and other technical personnel; |

| · | Advanced design, production and test equipment; |

| · | Manufacturing services that meet changing customer needs; |

| · | Technological changes in manufacturing processes; |

| · | Expansion of manufacturing capacity; and |

| · | Acquiring technology through licensing and acquisitions. |

Our future operating results will depend to a significant extent on our ability to continue providing new product and service solutions that compare favorably on the basis of time to market, cost and performance, with competing third-party suppliers and technologies. Our failure to increase net sales sufficiently to offset the increased costs needed to achieve those advances would adversely affect our operating results.

We may experience trade barriers in expanding to our targeted emerging markets and may be subject to tariffs and taxes that will result in significant additional costs for our business and products.

We may experience barriers to conducting business and trade in our planned expansion to emerging markets. These barriers may be in the form of delayed customs clearances, customs duties or tariffs. In addition, we may be subject to repatriation taxes levied upon the exchange of income from local currency into foreign currency, substantial taxes of profits, revenues, assets and payroll, as well as value-added tax. The markets into which we may expand may impose onerous and unpredictable duties, tariffs and taxes on our business and products. These barriers or expenses could have an adverse effect on our operations and financial results.

To the extent we acquire businesses and technologies from others, we will need to integrate these into our business, which if not successful will adversely impact our business and increase our financial expenses.

As we develop our business, oneOne important aspect of our expansion has been and will be the use of acquisitions, which may include acquiring an operating business or specific assets. One such example wasExamples of this strategy have been the acquisitionacquisitions of Concord.Concordin 2011 and Bond in 2013. As with any acquisition, we will have to integrate the business with our operations so as to achieve the value of our investment. Accommodating different business cultures, operating systems and product lines, as well as understanding and implementing different regulatory issues, often takes time and can result in unexpected expenses. Acquisitions are not always successful, resulting in unintended expenses and write-downs.

As we expand our business outside of China, we will encounter the increasing need for international certifications and compliance with the regulation of different governments, which if not obtained and complied with may adversely impact our business.

We are expanding our business outside of China, including seeking business opportunities in Hong Kong SAR, Singapore, Malaysia and the Middle East. For our marketing both withinin China and in other jurisdictions, we seek international certifications and have obtained certificates such as the European Safety Standard Certification Level 4. As we operate in jurisdictions other than China, we will have to comply with local law, some of which relate to various safety and quality requirements for the kinds of products we provide. The failure to have any necessary or beneficial certifications and the failure to comply with local law will have an adverse impact on our marketing and business, and may result in additional costs and expenses.

During our expansion into overseas market, a lack of qualified local engineers and the inability to relocate enough China’s experienced engineers to overseas could delay our international projects’ execution and lose potential business opportunities.

In our international business expansion to Southeast Asia and the Middle East, we may not be able to find adequate and qualified local engineers to bid and complete sizable rail transportation orders and industrial automation projects, and because of the visa problems, we may have difficulties to relocate adequate engineers from China to various foreign countries and have them stay there long enough to finish the projects, which could cause adverse impact on our international business expansion.

We do not have long-term purchase commitments from our customers, so our customers are free to choose products from our competitors, which increases our marketing expenses to continually find new clients and win new contracts.

We are engaged in the design, production and installation of automation and process control systems. As a result, our revenues result from numerous individual contracts that are nonrecurring in nature. Furthermore, customers may change or delay or terminate orders for products and services without notice for any number of reasons unrelated to us, including lack of market acceptance for the products to be produced by the process that our system was designed to control. As a result, in order to maintain and expand our business, we must expend increasing amounts on marketing to identify clients and win contracts so as to be able to replenish the orders in our pipeline on a continuous basis. Increased marketing expenses and the inability to continue with current contracts or win new sources of revenue will result in a decline in revenues and profitability.

The success of our business depends, in part, on securing a steady stream of new customers.

Other than our contracts to supply products, systems and services to our rail, power plant and building retrofit customers, our average integrated solutions contract is worth approximately $150,000. While some of those contracts are for upgrades and additions to existing control systems, most of them are for new installations. In order for our business to continue to succeed and grow, we need to secure contracts with new customers on a regular basis. We may not be successful in securing new contracts, which would impact our revenues and profitability.

Although we do not have a concentration of business with any customer at this time, recently our business has become more dependent on a few significant customers.

We have developed significant customer relationships with the several local subway providers and the Ministry of Railways and local railway bureausauthorities in respect of the high speed train system in China. We currently also have significant contracts with the MTR Corporation Ltd. of Hong Kong.Kong, and SMRT Corporation Ltd. and Thales Solutions Asia Pte. Ltd. of Singapore. We expect that these relationships will continue to grow, and we will win more contracts with them over time. We also are expanding into the businessestablished a joint venture with China General Nuclear Power Corporation which has about 60% of control systemsChina’s nuclear market share, to secure us for conventional and nuclear plants and building retrofitting which may develop into a significant customer basemarket share for the automation and control products providing for the nuclear power plants in the future.China. To the extent that these customer groups or specific customers with a group represent an increasing proportion of our business, we will become more dependent on them for our revenues and business growth. In that case, our cash flowflows also will become more dependent on those customers’ payment practices and overall public funding policies, including the lengthening of collection times under contracts that have been performed. Therefore, the loss of one or more of these customers or market groups as customers would have a material adverse impact on our revenues and our business operations and development.

We have a substantial backlog of contracts.contracts, the execution of the unfinished contracts in the backlog may be lengthened due to various external reasons, and the increase of backlog may not necessarily reflect our business expansion.

To date, our backlog has been a reflection of our ability to sell our products and services and increase our business. This represents an amount of unrealized revenue to be earned from contracts secured by the Company. Backlog, however, can also reflect upon our abilityinability to perform our contracts on a timely basis. Therefore, when evaluating our backlog, analysis should be made ofas to whether or not it is a reflection of an expanding business, successful marketing and increasing acceptance of our products and services in the marketplacemarket place or problems in our contract performance and acceptance.

A lack of adequate engineering resources could cause our business to have diminished profitability and lose potential business prospects.

Among the competitive advantages and key business advantages that we enjoy are the plentiful supply of engineering talent in China and the comparatively lower cost of our engineering staff compared to those of our Western and Japan-based competitors. Recently, however, our costs for these persons has been subject to increased wage pressures due to the economic growth of China and certain inflationary pressures and additional employment related taxation. If the available supply of engineers were to be absorbed by competing demands, or otherwise not as plentiful as we have experienced to date, then the costs of hiring, training and retaining capable engineers would likely increase. ThisIf we are unable to pass any additional costs through to our customers, this could result in a reduction in our profitability, and the inability to have qualified and trained persons could adversely affect our business prospects or could even cause a change in our business strategy.

Our products may contain design or manufacturing defects, which could result in reduced demand for our products or services, customer claims and uninsured liabilities.

Our products are very complex, integrated systems, often with elements designed specifically for the particular situation of a customer, which may have undetected design or manufacturing issues or defects until put into actual use. Also, we manufacture spare parts for maintenance and replacement purposes after completion of integrated solution contracts. While there have been no significant issues or defects identified so far, any issues or defects in the design, manufacture and spare parts we provide may result in returns, claims, delayed shipments to customers or reduced or cancelled customer orders and other forms of damages asserted against the company. If these issues or defects occur, we will incur additional costs, and if they occur in large quantity or frequency, we may sustain a permanent increase in costs, a loss of business reputation and legal liability. Moreover, we are increasingly active in the conventional and nuclear power generation and railway control systems sectors. Each of these sectors poses a substantially higher risk of liability in the event of a system failure, than was present in the industrial process controls markets in which we traditionally compete.

We generally do not havecarry large amounts of insurance, now, and in the future we may not be able to obtain adequate insurance coverage, to protect us against the risks associated with our business.coverage. The typical practice of the industries with which we are involved is for the customers to obtain insurance to protect their own operational risks. As a practice, we do not carry insurance coverage to protect against the risks related to product failure. It is possible that customers could assert claims against us for any damages caused by a failure in one of our systems, and as a result, the failure of any of our designs, manufacture and installation of our products could result in a liability that would seriously impair our financial condition or even force us out of business.

Our failure to adequately protect our intellectual property rights may undermine our competitive position, and litigation to protect our intellectual property rights may be costly.

Our business is based on a number of proprietary products and systems, some of which are patented and others of which we protect as trade secrets. We strive to strengthen and differentiate our product portfolio by developing new and innovative products and product improvements. As a result, we believe that the protection of our intellectual property will become increasingly important to our business as the functionality of automation systems increases to meet customer demand and as we try to open new markets for our products.

Currently, we hold 80 PRC utility patents that relate to various product configurations and product components and 95 software copyrights and have 45 pending PRC patent applications. We will continue to rely on a combination of patents, trade secrets, trademarks and copyrights to provide protection in this regard, but this protection may be inadequate.

Our pending or future patent applications may not be approved or, if allowed, they may not be of sufficient strength or scope. As a result, third parties may use the technologies and proprietary processes that we have developed and compete with us, which could negatively affect any competitive advantage we enjoy, dilute our brand and harm our operating results.

In addition, policing the unauthorized use of our proprietary technology can be difficult and expensive. Litigation may be necessary to enforce our intellectual property rights. Protection of intellectual property and proprietary rights in China may not be as effective as in other countries. Given the fact that the majority of our intellectual property rights are in China and under Chinese law, the relative unpredictability of China’s legal system and potential difficulties of enforcing a court judgment in China may result in an outcome that is unfavorable to us when we assert intellectual property ownership in a particular situation. Furthermore, any litigation may be costly and may divert management attention away from our business operations. An adverse determination in any lawsuit involving our intellectual property is likely to jeopardize our business prospects and reputation and result in additional expense for penalties, licensing and redesign. We have no insurance coverage against litigation costs so we would be forced to bear all litigation costs if we cannot recover them from other parties. All of the foregoing factors could harm our business and financial condition.

As we are going to sell more of our proprietarily developed products and systems to foreign countries, we may not continue to have the protection of our patents and software copyright in foreign countries for some of our proprietary products, which could negatively impact our competitive position and our business expansion in overseas.

We may develop new products that do not gain market acceptance, which would result in the failure to recover the significant costs for design and manufacturing services for new product solutions, thus adversely affecting operating results.

We operate in an industry characterized by increasingly frequent and rapid technological advances, product introductions and new design and manufacturing improvements. As a result, we must expend funds and commit resources to research and development activities, possibly requiring additional engineering and other technical personnel; purchasing new design, production, and test equipment; and enhancing our design and manufacturing processes and techniques. We may invest in equipment employing new production techniques for existing products and new equipment in support of new technologies that fail to generate adequate returns on the investment due to insufficient productivity, functionality or market acceptance of the products for which the equipment may be used. We could, therefore, incur significant costs for design and manufacturing services for new product solutions that do not generate a sufficient return on that investment, which would adversely affect our future operating results. Our future operating results will depend significantly on our ability to provide timely design and manufacturing services for new products that compete favorably with design and manufacturing capabilities of third party suppliers.

Although the Company’s goodwill outstanding as at June 30, 2014 was assessed not impaired, it may be impaired in the future depending on the future market development and the outcome of the tendering of local mechanical and electrical engineering contracts in Singapore, Malaysia and Middle East.

The goodwill outstanding as at June 30, 2014 was related to the acquisition of Concord in 2012 and Bond in 2013. Based on our quantitative assessment the goodwill was not impaired as at June 30, 2014. However, the fair value of Concord calculated using discounted cash flow method was only 9.1% higher than its carrying value as at June 30, 2014. The fair value of Concord is highly dependent on the future market development and the outcome of its tendering of local mechanical and electrical engineering contracts in Singapore, Malaysia and Middle East. Slow down in mechanical and electrical engineering sector, or fewer than expected contract awards to Concord may result in goodwill impairment in the future.

RISKS RELATING TO THE INDUSTRY IN WHICH WE OPERATE

The plans for growth rely oncompany mainly operates in the industrial and manufacturing automation sectors, and the high-speed rail, subway and nuclear power automation sectors; in some industry verticals within the industrial automation sector, we may experience slowerthe inconstant growth or decrease in growthrate from time to time, which may present fewervariation of business opportunities; the contracts for high-speed rail, subway and nuclear power are substantially larger which may result in a greater dependence on a particular customer or business sector, and could cause significant fluctuations in our revenues.

The principal focus of our business until recently has been to provide Distributed Control Systems, Programmable Logic Controller and related industrial automation and control software and hardware devices to industrial and manufacturing companies. Even though there are enormous opportunities in the industrial automation arena, some industry verticals may experience slower growth or decreased growth that will provide us with fewer opportunities and contract awards from the industry and manufacturing sectors. Both high-speed rail and nuclear power sectors have one or few customers and are closely related to the national development policies, and the contract size for these two sectors is usually much larger, and as a result, there could be severe fluctuation of these sectors’ growth, which may affect our business and revenues. The competition of SCADA (Surveillance Control and Data Acquisition) in the subway sector is substantial; therefore we may not be able to sustain our position in the market and achieve new contract wins, resulting in a decrease of our revenue within this sector.

To the extent that we devote more of our marketing and business capacities to the larger customer, our revenues and business development will be more dependent on our being able to service their needs. To the extent that the nuclear industry and high speed railway in China may experience slower growth, we would expect that there would be a slowing of our expansion into these business areas.

Although China is committed to expanding its energy production with nuclear power and building a high speed railway network, both these industries have experienced various setbacks due to higher than expected accidents for various reasons. To the extent that the government slows their development and expansion withinreasons years ago. The future growth rate of these two industriessectors may not be as fast as the market previously expected but on which we are becominga more reliant, we may experience a slowing of our business growth due the inability to win contracts or our ability to win contracts for smaller amounts than previously experiencedsustainable and anticipated. If we are unable to generate the revenues that we seek and we are unable to replace the revenues in our traditional markets or other new markets, thensafer basis, thus we will, likely experience slower annual growth or possibly even a reduction in these sectors’ revenues.

To the extent that our business is more dependent on large contracts and contracts from a few customers, our revenues, cash flow and profits will be influenced by this type of contracting and the timely payment for our products and services.

As we develop our business with the entities responsible for building municipal subway systems and railroads, power plants and larger system contract customers, such as building retrofits, we will be entering into contracts for larger sized projects than in the past, which will be for significantly greater contract value. These contracts will require us to commit greater operating resources to a more limited number of customers and contract fulfillment. Therefore, our revenues, cash flow and profit will become increasingly dependent on our ability to perform these contracts and collect the payments due on a timely basis. As manySome of the entities that are ultimately responsible for the funding of these types ofinfrastructure projects are governmental authorities or ministries, our contract requirements and collections will become subject to these entities being able to adequately budget and have the revenues to timely pay for our products and services. We expect a long collection period in some of our business. To some extent, we may become subject to delays and reductions in scope of project due to changes in the policies, objectives and budgeting of any of the public entities which control the projects on which we are contracting. We will also become increasingly subject to government contract requirements in the performance of contracts that are ultimately the responsibility of public bodies.

At this time, contracting with the entities that provide the subway and rail systems and power plants for which we provide control systems is similar to contracting with the customers we have sold to in the past. Therefore, our contracts are written on a similar basis as before, and we expect that we will be operating under these contracts and accounting for their revenues in a similar manner as before.

Many of our competitors have substantially greater resources than we do, allowing them to be able to reduce their prices, which would force us to reduce our prices.compete on an advantageous basis.

We operate in a very competitive environment with many major international and domestic companies, such as Honeywell, General Electric, ABB, Siemens, Emerson, Yokogawa and Hitachi. Many of our competitors are much better established and more experienced than we are, have substantially greater financial resources, operate in many international markets and are much more diversified than we are. As a result, they are in a strong position to compete effectively with us by, for example, reducing their prices, which could force us to reduce our prices.us. These large competitors are also in a better position than we are to weather any extended weaknesses in the market for automation and control systems. Other emerging companies or companies in related industries may also increase their participation in our market, which would add to the competitive pressures that we face.

A decrease in the rate of growth in Chinese industryChina’s industrial activity and the Chinese economy in general may lead to a slower growth or decrease in our revenues because industrial companies in China are the principal current sourcesignificant sources of revenues for us.

Industrial companies operating in China are the principal current sourcesignificant sources of revenues for us. Our business benefited in the past from the rapid expansion of China’s industrial activity, which has created additional demand from existing companies and led to the formation of numerous additional companies that have need for our products and services. We have also benefited from the infrastructure projects of the different governmental authorities of China, such as power production and transportation systems. China’s industrial and infrastructure expansion has been fueled in large measure by international demand for the low-cost goods that China is able to produce due to labor advantages and other comparative advantages, such as governmental subsidies to offset research and development expenses and taxes and reduced land use/facilities costs for targeted industries. The Chinese economy may not be able to sustain this rate of growth in the future and any reduction in the rate of China’s industrial growth or a shrinking of China’s industrial base could adversely affect our revenues. We may also be impacted as major infrastructure projects are completed. The resulting increase in competition for customers might also cause erosion of profit margins that we have been able to achieve historically.

Our efforts to operate in the international automation market may not prove successful, and we may expend capital resources without achieving value and needlessly divert management’s time and attention from our principal market.

We are penetrating international markets, emphasizing Southeast Asia and the Middle East.East with the objective of diversifying our products, clients and places of operations and growing our overall business. Our expansion is likely to use substantial resources, including substantial amounts of capital and equity and deploy meaningful amounts of management time and attention. Our products and our overall approach to the automation and controls system business may not be accepted in other markets to the extent needed to make that effort profitable. In addition, the additional demands on our management from these activities may detract from our efforts in the domestic Chinese market and market of surrounding countries, causing the operating results in our principal markets to be adversely affected.

We depend heavily on key personnel, and loss of key employees and senior management could harm our business.

Our future business and results of operations depend in significant part upon the continued contributions of our key technical and senior management personnel, including Dr. Changli Wang, our Chairman and Chief Executive Officer. Wepersonnel. The company also will depend in significant part upon its ability to attract and retain additional qualified senior executives and management, technical, marketing and sales and support personnel for our operations. If we lose a key employee, if a key employee fails to perform in his or her current position or if we are not able to attract and retain skilled employees as needed, our business could suffer. Turnover in our senior management could significantly deplete institutional knowledge held by our existing senior management team and impair our operations.

In addition, if any of these key personnel joins a competitor or forms a competing company, we may lose some of our customers. We have entered into confidentiality and non-competition agreements with key personnel. However, if any disputes arise between these key personnel and us, it is not clear, in light of uncertainties associated with the PRC legal system, what the court decisions will be and the extent to which these court decisions could be enforced in China, where all of these key personnel reside and hold some of their assets.

Our control systems are used in infrastructure projects such as subway systems, surface railways and nuclear plants; to the extent that our systems do not perform as designed, we could be found responsible for the damage resulting from that failure.

We face potential responsibility for the failure of our control systems in performing the various functions for which they are designed and the damages resulting from any such problem. To the extent that we contract to provide control systems in larger scale projects, the level of damages for which we may be held responsible is likely to increase. To the extent that any of our installed control systems do not perform as designed for their intended purposes, and we are held responsible for the consequences of those performance failures and resulting damages, there may be an adverse impact on our business, business reputation, revenues and profits. To date, we do believe our control systems have performed as designed, and there are no claims asserted against us based on any significant, non-performance event. Notwithstanding our record, no assurance can be given that no claims will be sought in the future based on the design and performance of our control systems.

We may be exposed to potential risks relating to our internal controls over financial reporting and our ability to have those controls positively attested to by our independent auditors.

As directed by Section 404 of the Sarbanes-Oxley Act of 2002, the SEC adopted rules requiring public companies to include a report of management on the Company’s internal controls over financial reporting in their annual reports and the independent registered public accounting firm auditing a company’s financial statements to attest to and report on the operating effectiveness of such company’s internal controls. Although our independent auditorNo material weakness has provided a positive attestationbeen identified as of June 30, 2012, we can provide no assurance that we will comply with all of the requirements imposed thereby and we will receive a positive attestation from our independent auditors in the future.2014. In the event we identify material weaknesses in our internal controls that we cannot remediate in a timely manner or we are unable to receive a positive attestation from our independent auditors with respect to our internal controls, investors and others may lose confidence in the reliability of our financial statements.

| 15 |

Our auditor, like other independent registered public accounting firms operating in China, is not permitted to be subject to inspection by the Public Company Accounting Oversight Board, and as such, investors may be deprived of the benefits of such inspection.

TheOur independent registered public accounting firm that issues the audit reports included in our annual report filed with the SEC, as an auditor of companies that are traded publicly in the United States and a firm registered with the Public Company Accounting Oversight Board (United States), or the PCAOB, is required by the laws of the United States to undergo regular inspections by the PCAOB to assess its compliance with the laws of the United States and professional standards. Because our auditor is located in China, a jurisdiction where the PCAOB is currently unable to conduct inspections without the approval of the PRC authorities like other independent registered public accounting firms operating in China, our auditor is currently not inspected by the PCAOB.

Inspections of other firms that the PCAOB has conducted have identified deficiencies in those firms’ audit procedures and quality control procedures, which may be addressed as part of the inspection process to improve future audit quality. The inability of the PCAOB to conduct inspections of independent registered public accounting firms operating in China makes it more difficult to evaluate the effectiveness of our auditor’s audit procedures or quality control procedures. As a result, investors may be deprived of the benefits of the PCAOB inspections.

Proceedings instituted by the SEC against five PRC-based accounting firms, including our independent registered public accounting firm, could result in financial statements being determined to be not in compliance with the requirements of the Securities Exchange Act of 1934.

In December 2012, the SEC instituted proceedings under Rule 102(e)(1)(iii) of the SEC’s Rules of Practice against five PRC-based accounting firms, including our independent registered public accounting firm, alleging that these firms had violated U.S. securities laws and the SEC’s rules and regulations thereunder by failing to provide to the SEC the firms’ work papers related to their audits of certain PRC-based companies that are publicly traded in the United States. Rule 102(e)(1)(iii) grants to the SEC the authority to deny to any person, temporarily or permanently, the ability to practice before the SEC who is found by the SEC, after notice and opportunity for a hearing, to have willfully violated, or willfully aided and abetted the violation of, any such laws or rules and regulations. On January 22, 2014, an initial administrative law discuss was issued, sanctioning four of these accounting firms and suspending them from practicing before the SEC for a period of six months. The sanction will not take effect until there is an order of effectiveness issued by the SEC. The accounting firms involved have appealed and the sanction will not become effective until after a full appeal process is concluded and a final decision is issued by the SEC. While we cannot predict the outcome of the SEC’s proceedings, if our independent registered public accounting firm is denied, temporarily or permanently, the ability to practice before the SEC, and we are unable to find in a timely manner another registered public accounting firm which can audit and issue a report on our financial statements, our financial statements could be determined to not be in compliance with the requirements for financial statements of public companies with a class of securities registered under the Securities Exchange Act of 1934, as amended, or the Exchange Act. Such a determination could ultimately lead to the SEC’s revocation of the registration of our ordinary shares under the Exchange Act, which would cause the immediate delisting of our ordinary shares from the NASDAQ Global Select Market, and the effective termination of the trading market for our ordinary shares in the United States, which would likely have a significant adverse effect on the value of our ordinary shares. In addition, because the issues raised in the SEC proceedings would likely extend to all independent public accounting firms in the PRC that currently are authorized to practice before the SEC, it may not be possible for us to attempt to address this issue by changing our independent registered public accounting firm.

RISKS RELATED TO DOING BUSINESS IN CHINA

The majority

A significant portion of our operating assets are located in China and the majoritya substantial portion of our revenue will be derived from our operations in China so our business, results of operations and prospects are subject to the economic, political and legal policies, developments and conditions in China.

Because the majoritya substantial portion of our business is conducted in China, despite the significant operations in Singapore and other SouthSoutheast Asian and Middle Eastern jurisdictions, the PRC’s economic, political and social conditions, as well as government policies, will have a tremendous influence on our business currently and in the nearer future.business. The PRC economy differs from the economies of most developed countries in many respects. China’s GDP has grown consistently since 1978 (National Bureau of Statistics of China). However, we cannot assure you that such growth will be sustained in the future. If, in the future, China’s economy experiences a downturn or grows at a slower rate than expected, there may be less demand for spending in certain industries. A decrease in demand for spending in certain industries could impair our ability to remain profitable. The PRC’s economic growth has been uneven, both geographically and among various sectors of the economy. The PRC government has implemented various measures to encourage economic growth and guide the allocation of resources. Some of these measures benefit the overall PRC economy, but may have a negative effect on us. For example, our financial condition and results of operations may be hindered by PRC government control over capital investments or changes in tax regulations.

The PRC economy has been transitioning from a planned economy to a more market-oriented economy. Although in recent years the PRC government has implemented measures emphasizing the use of market forces for economic reform, the reduction of state ownership of productive assets and the establishment of sound corporate governance in business enterprises, a substantial portion of productive assets in China is still owned by the PRC government. In addition, the PRC government continues to play a significant role in regulating industry development by imposing industrial policies. It also exercises significant control over PRC economic growth through the allocation of resources, controlling payment of foreign currency-denominated obligations, setting monetary policy and providing preferential treatment to particular industries or companies.

If the China Securities Regulatory Commission, or CSRC, or another PRC regulatory agency, determines that CSRC approval of our initial merger was required or if other regulatory obligations are imposed upon us, we may incur sanctions, penalties or additional costs which would damage our business.

On August 8, 2006, six PRC regulatory agencies, including the CSRC, promulgated the Regulations on Mergers and Acquisitions of Domestic Companies by Foreign Investors, or the M&A Regulations, which became effective on September 8, 2006. Under these regulations, the prior approval of the CSRC is required for the overseas listing of offshore special purpose vehicles that are directly or indirectly controlled by PRC companies or individuals and used for the purpose of listing PRC onshore interests on an overseas stock exchange.

On September 20, 2007, we completed a merger transaction with Chardan North China Acquisition Corporation, or Chardan, which resulted in our current ownership and corporate structure. We believe that CSRC approval was not required for our merger transaction or for the listing and trading of our securities on a trading market because we are not an offshore special purpose vehicle that is directly or indirectly controlled by PRC companies or individuals. Although the M&A Regulations provide specific requirements and procedures, there are still many ambiguities in the meaning of many provisions. Further regulations are anticipated in the future, but until there has been clarification either by pronouncements, regulation or practice, there is some uncertainty in the scope of the regulations and the regulators have wide latitude in the enforcement of the regulations and approval of transactions. If the CSRC or another PRC regulatory agency subsequently determines that the CSRC’s approval was required, we may face sanctions by the CSRC or another PRC regulatory agency. If this happens, these regulatory agencies may impose fines and penalties on our operations in China, limit our operating privileges in China, restrict or prohibit payment or remittance of dividends paid by Hollysys, or take other actions that could damage our business, financial condition, results of operations, reputation and prospects, as well as the trading price of our securities.

We anticipate that the PRC will experience inflation in the near term, which may have an adverse effect on our cost of operations and profitability.

The PRC economy is experiencing general inflationary pressures due to a number of factors which overall will effect Hollysys. If we are unable to increase the value of our contracts commensurate with increases in our operating expenses, we will experience a reduction in our profit margins. If we raise our contract prices, we may not win the kind and amount of contracts that will permit us to operate profitably and grow our business.

If the PRC imposes restrictions designed to reduce inflation, future economic growth in the PRC could be severely curtailed which could hurt our business and profitability.

While the economy of the PRC has experienced rapid growth, this growth has been uneven among various sectors of the economy and in different geographical areas of the country. Rapid economic growth often can lead to growth in the supply of money and rising inflation. In order to control inflation in the past, the PRC has imposed controls on bank credits, limits on loans for fixed assets and restrictions on state bank lending. Imposition of similar restrictions may lead to a slowing of economic growth, a decrease in demand for our products and generally damage our business and profitability.

Fluctuations in exchange rates could harm our business and the value of our securities.

The value of our securities will be indirectly affected by the foreign exchange rate between US dollars and RMB and between those currencies and other currencies in which our sales may be denominated. Because substantially mosta large portion of our earnings and cash assets are denominated in RMB, Singapore Dollar and Malaysian Ringgit, and our financial results are reported in US dollars, fluctuations in the exchange rate between the US dollar and the RMB will affect our balance sheet and our earnings per share as stated in US dollars. In addition, appreciation or depreciation in the value of the RMB relative to the US dollar would affect our financial results reported in US dollar terms without giving effect to any underlying change in our business or results of operations. Fluctuations in the exchange rate will also affect the relative value of any dividend we issue that will be exchanged into US dollars as well as earnings from, and the value of, any US dollar-denominated investments we make in the future. Since July 2005, the RMB has no longer been pegged to the US dollar. Although the People’s Bank of China regularly intervenes in the foreign exchange market to prevent significant short-term fluctuations in the exchange rate, the RMB may appreciate or depreciate significantly in value against the US dollar in the medium to long term. Moreover, it is possible that in the future PRC authorities may lift restrictions on fluctuations in the RMB exchange rate and lessen intervention in the foreign exchange market.

Very limited hedging transactions are available in China to reduce our exposure to exchange rate fluctuations. To date, we have not entered into any hedging transactions. While we may enter into hedging transactions in the future, the availability and effectiveness of these transactions may be limited, and we may not be able to successfully hedge our exposure at all. In addition, our foreign currency exchange losses may be magnified by PRC exchange control regulations that restrict our ability to convert RMB into foreign currencies.

Exchange controls that exist in the PRC may limit our ability to utilize our cash flow effectively.

We are subject to the PRC’s rules and regulations on currency conversion. In the PRC, the State Administration for Foreign Exchange, or SAFE, regulates the conversion of the RMB into foreign currencies. Currently, foreign investment enterprises, or FIEs, are required to apply to the SAFE for “Foreign Exchange Registration Certificates for FIEs.” We believe Beijing Helitong is an FIE. With such registration certificates, which need to be renewed annually, FIEs are allowed to open foreign currency accounts including a “basic account” and “capital account.” Currency conversion within the scope of the “basic account,” such as remittance of foreign currencies for payment of dividends, can be effected without requiring the approval of the SAFE. However, conversion of currency in the “capital account,” including capital items such as direct investment, loans and securities, still require approval of the SAFE. We cannot assure you that the PRC regulatory authorities will not impose further restrictions on the convertibility of the RMB. Any future restrictions on currency exchanges may limit our ability to use our cash flow for the distribution of dividends to our shareholders or to fund operations it may have outside of the PRC.

APRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident beneficial owners or our company to liabilities or penalties, limit our ability to contribute capital to our PRC subsidiaries, limit the ability of our PRC subsidiaries to increase their registered capital or distribute profits to us, or otherwise materially and adversely affect us.

On July 14, 2014, the SAFE issued the Circular Relating to Foreign Exchange Administration of Offshore Investment, Financing and Roundtrip Investment by Domestic Residents Through Special Purpose Vehicles, or Circular 37. Circular 37 repeals and replaces the Notice Concerning Foreign Exchange Controls on Domestic Residents’ Financing and Roundtrip Investment Through Offshore Special Purpose Vehicles, or Circular 75. Under Circular 37, PRC residents are required to register with the SAFE or its local branches prior to establishing, or acquiring control of, an offshore company for the purpose of investment or financing that offshore company with equity interests in, or assets of, a PRC enterprise or with offshore equity interest or assets legally held by such PRC resident. In addition, PRC residents are required to amend their registrations with the SAFE and its local branches to reflect any material changes with respect to such PRC resident’s investment in such offshore company, including changes to basic information of such PRC resident, increase or decrease in capital, share transfer or share swap, merger or division. In the event that a PRC shareholder fails to make the required registration or update the previously filed registration, the PRC subsidiaries of that offshore special purpose vehicle may be prohibited from distributing their profits and the proceeds from any reduction in capital, share transfer or liquidation to their offshore parent company, and the offshore parent company may also be prohibited from contributing additional capital into its PRC subsidiaries. Furthermore, failure byto comply with the various foreign exchange registration requirements described above could result in liability under the PRC laws for evasion of applicable foreign exchange restrictions.