As filed with the Securities and Exchange Commission on April 28, 2015May 30, 2017

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

ANNUAL REPORT PURSUANT TO

SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 20142016

Commission file number: 001-34175

ECOPETROL S.A.

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

REPUBLIC OF COLOMBIA

(Jurisdiction of incorporation or organization)

Carrera 13 No. 36 – 24

BOGOTA – COLOMBIA

(Address of principal executive offices)

Tel. (571) 234 4000

Claudia Trujillo

Andrés Felipe Sánchez

Investor Relations Officer

investors@ecopetrol.com.co

Tel. (571) 234 5190

Carrera 13 N.36-24 Piso 75

Bogota, Colombia

(Name, Telephone, E-Mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Name of each exchange on which registered: | |

| American Depository Shares (as evidenced by American Depository Receipts), each representing 20 common shares par value | New York Stock Exchange | |

| Ecopetrol common shares par value | New York Stock Exchange (for listing purposes only) | |

| 7.625% Notes due 2019 | New York Stock Exchange | |

| 4.250% Notes due 2018 | New York Stock Exchange | |

| 5.875% Notes due 2023 | New York Stock Exchange |

| Title of each class | Name of each exchange on which registered: | |

| 4.125% Notes due 2025 | New York Stock Exchange | |

| 5.375% Notes due 2026 | New York Stock Exchange | |

| 7.375% Notes due 2043 | New York Stock Exchange | |

| 5.875% Notes due 2045 | New York Stock Exchange | |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

41,116,698,45641,116,694,690 Ecopetrol common shares, par value Ps$250COP$609 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

x Yes¨ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

¨ Yesx No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

N/A

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filerx | Accelerated filer¨ | Non-accelerated filer¨ | Emerging growth company¨ |

��

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ¨ U.S. GAAP | xInternational Financial Reporting Standards as issued by the International Accounting Standards Board |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

¨ Item 17x¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as

(as defined in Rule 12b-2 of the Exchange Act).

¨ Yesx No

Annual Report on Form 20-F 20142016

| 6.5.1 | Colombian Tax Considerations | 131 | ||

| 6.5.2 | U.S. Federal Income Tax Consequences | 134 | ||

| 6.6. | Exchange Controls and Limitations | 137 | ||

| 6.7. | Exchange Rates | 138 | ||

| 6.8. | Major Shareholders | 139 | ||

| 6.9. | Enforcement of Civil Liabilities | 139 | ||

| 7. | Corporate Governance | 140 | ||

| 7.1. | Bylaws | 141 | ||

| 7.2. | Code of Ethics | 145 | ||

| 7.3. | Board of Directors | 145 | ||

| 7.3.1 | Board Practices | 147 | ||

| 7.3.2 | Board Committees | 148 | ||

| 7.4. | Compliance with NYSE Listing Rules | 150 | ||

| 7.5. | Management | 152 | ||

| 7.6. | Compensation of Directors and Management | 155 | ||

| 7.7. | Share Ownership of Directors and Executive Officers | 155 | ||

| 7.8. | Controls and Procedures | 155 | ||

| 8. | Financial Statements | 159 | ||

| 9. | Signature Page | 160 | ||

| 10. | Exhibits | 161 | ||

| 11. | Cross-reference to Form 20-F | 162 | ||

| 1. | Introduction | 1 | ||||

| 1.1 | About This Report | 1 | ||||

| 1.2 | Forward-looking Statements | 1 | ||||

| 1.3 | Selected Financial and Operating Data | 2 | ||||

| 2. | Strategy and Market Overview | 4 | ||||

| 2.1 | Our Corporate Strategy | 5 | ||||

| 3. | Business Overview | 6 | ||||

| 3.1 | Our History | 6 | ||||

| 3.2 | Our Corporate Structure | 7 | ||||

| 3.3 | Our Business | 9 | ||||

| 3.4 | Exploration and Production | 9 | ||||

| 3.4.1 | Exploration Activities | 9 | ||||

| 3.4.1.1 | Exploration Activities in Colombia | 9 | ||||

| 3.4.1.2 | Exploration Activities Outside of Colombia | 12 | ||||

| 3.4.2 | Production Activities | 13 | ||||

| 3.4.2.1 | Production Activities in Colombia | 14 | ||||

| 3.4.2.1.1. | Ecopetrol S.A.’s Production Activities in Colombia | 14 | ||||

| 3.4.2.1.2. | Ecopetrol S.A.’s Affiliates and Subsidiaries’ Production Activities in Colombia | 19 | ||||

| 3.4.2.2 | Production Activities Outside Colombia | 22 | ||||

| 3.4.2.3 | Marketing of Crude Oil, Natural Gas and Refined Products | 23 | ||||

| 3.4.3 | Reserves | 25 | ||||

| 3.4.4 | Joint Venture and Other Contractual Arrangements | 30 | ||||

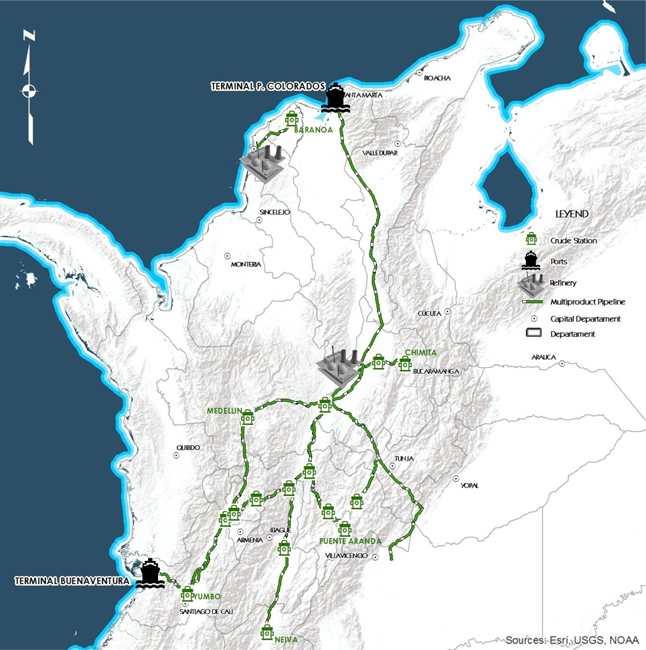

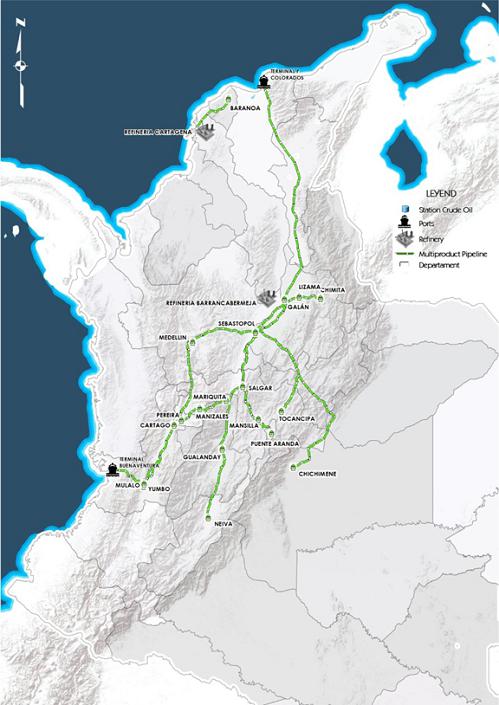

| 3.5 | Transportation and Logistics | 34 | ||||

| 3.5.1.1 | Transportation Activities | 34 | ||||

| 3.5.1.2 | Pipelines | 37 | ||||

| 3.5.1.3 | Export and Import Facilities | 39 | ||||

| 3.5.2 | Other Transportation Facilities | 39 | ||||

iii

iv

v

vi

| 6.6 | Exchange Controls and Limitations | 130 | ||

| 6.7 | Exchange Rates | 131 | ||

| 6.8 | Major Shareholders | 132 | ||

| 6.9 | Enforcement of Civil Liabilities | 132 | ||

| 7. | Corporate Governance | 134 | ||

| 7.1 | Bylaws | 134 | ||

| 7.2 | Code of Ethics | 137 | ||

| 7.3 | Board of Directors | 138 | ||

| 7.3.1 | Board Practices | 140 | ||

| 7.3.2 | Board Committees | 141 | ||

| 7.4 | Compliance with NYSE Listing Rules | 142 | ||

| 7.5 | Management | 143 | ||

| 7.6 | Compensation of Directors and Management | 147 | ||

| 7.7 | Share Ownership of Directors and Executive Officers | 147 | ||

| 7.8 | Controls and Procedures | 147 | ||

| 8. | Financial Statements | 151 | ||

| 9. | Signature Page | 152 | ||

| 10. | Exhibits | 153 | ||

| 11. | Cross-reference to Form 20-F | 154 | ||

vii

| 1. | Introduction |

| About This Report |

We file our Annual Report on Form 20-F and other information with the U.S. Securities and Exchange Commission.

We file reports, including annual reports on Form 20-F, and other information with the SEC pursuant to the rules and regulations of the SEC that apply to foreign private issuers. You may read and copy any materials filed with the SEC in the SEC’s public reference room at 100 F Street, NE, Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the operation of the public reference room. Any filings we make are also available to the public over the Internet at the SEC’s website at www.sec.gov and at our website at www.ecopetrol.com.co. (This URL is intended to be an inactive textual reference only. It is not intended to be an active hyperlink to our website. The information on our website, which might be accessible through a hyperlink resulting from this URL, is not and shall not be deemed to be incorporated into this annual report.)

Unless the context otherwise requires, the terms “Ecopetrol,” “we,” “us,”“Ecopetrol”, “we”, “us”, “our” or the “Company” are used in this annual report to refer to Ecopetrol S.A. and its subsidiaries on a consolidated basis.

References to the Nation in this annual report relate to the Republic of Colombia (“Colombia”), our controlling shareholder. References made to the Government of ColombiaColombian government or the Government correspond to the executive branch including the President of Colombia, the ministries and other governmental agencies responsible for regulating our business.

| Forward-looking Statements |

This annual report on Form 20-F contains forward-looking statements within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. These statements are not based on historical facts and reflect our expectations for future events and results. Most facts are uncertain because of their nature. Words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “should,” “plan,” “potential,” “predicts,” “prognosticate,” “project,” “target,”“anticipate”, “believe”, “could”, “estimate”, “expect”, “should”, “plan”, “potential”, “predicts”, “prognosticate”, “project”, “target”, “achieve” and “intend,”“intend”, among other similar expressions, are understood as forward-looking statements. We have made forward-looking statements that address, among other things:

| · | our exploration and production activities, including drilling; |

| · | import and export activities; |

| · | our liquidity, cash flow, and sources of funding; |

| · | our projected and targeted capital expenditures and other cost commitments and revenues; and |

| · | dates by which certain areas will be developed or will come on-stream. |

Our forward-looking statements are not guarantees of future performance and are subject to assumptions that may prove incorrect and to risks and uncertainties that are difficult to predict. Actual results could differ materially from those expressed or forecast in any forward-looking statements as a result of a variety of factors. These factors may include, but are not limited to, the following:

| · | general economic and business conditions, including crude oil and other commodity prices, refining margins and prevailing exchange rates; |

| · | competition; |

| · | our ability to obtain financing; |

| · | our ability to find, acquire or gain access to additional reserves and our ability to develop existing reserves; |

| 1 |

| · | uncertainties inherent in making estimates of our reserves; |

| · | significant political, economic and social developments in Colombia and other countries where we do business; |

| · | natural disasters, military operations, terrorist acts, wars or embargoes; |

| · | regulatory developments, including regulations related to climate change; |

| · | receipt of government approvals and licenses; |

| · | technical difficulties; and |

| · | other factors discussed in Section 5.1 of this document as “Risk Factors.” |

All forward-looking statements attributed to us are qualified in their entirety by this cautionary statement. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information or for any other reason. Accordingly, readers should not place undue reliance on the forward-looking statements contained in this annual report.

| Selected Financial and Operating Data |

The following table sets forth, for the periods and at the dates indicated, our selected historical financial and certain key operating data. The selected financial data has been derived from and should be read in conjunction with, and is qualified in its entirety by reference to, our consolidated audited financial statements, presented in Colombian Pesos. PricewaterhouseCoopers Ltda. audited our consolidated financial statements for the years ended December 31, 2014 and 2013. KPMG Ltda. audited our consolidated financial statements for the years ended December 31, 2012 and 2011. PricewaterhouseCoopers Ltda. also audited our consolidated financial statements for the year ended December 31, 2010.

Table 1 – Selected Operating Data

| 2014 | 2013 | 2012 | 2011 | 2010 | ||||||||||||||||

| Operating Information | ||||||||||||||||||||

| Oil and gas production (mboed) | 755.4 | 788.2 | 754.0 | 724.1 | 615.8 | |||||||||||||||

| Proved oil and gas reserves (Mmboe) (1) | 2,084 | 1,972 | 1,877 | 1,857 | 1,714 | |||||||||||||||

| Exploratory Wells(2) | 28 | 22 | 23 | 39 | 28 | |||||||||||||||

| Refinery Through-put (bpd)(3) | 240,484 | 283,362 | 296,340 | 305,631 | 296,044 | |||||||||||||||

| 1P Reserves replacement ratio | 146 | % | 139 | % | 108 | % | 164 | % | 193 | % | ||||||||||

| Financial Information | ||||||||||||||||||||

| COLOMBIAN GAAP | ||||||||||||||||||||

| (Expressed in millions of Colombian pesos, except for the net income per share and net operating income per share, which is expressed in Colombian pesos) | ||||||||||||||||||||

| Total revenue | 68,925,338 | 70,428,715 | 68,852,002 | 65,967,514 | 42,089,745 | |||||||||||||||

| Operating profit | 16,601,989 | 21,834,729 | 23,342,904 | 25,044,016 | 12,747,448 | |||||||||||||||

| Net income | 7,510,270 | 13,106,503 | 14,778,947 | 15,452,334 | 8,146,471 | |||||||||||||||

| Net operating income per share | 404 | 531 | 568 | 616 | 315 | |||||||||||||||

| Weighted average number of shares outstanding(4) | 41,116,698,456 | 41,116,698,456 | 41,116,698,456 | 40,634,882,725 | 40,472,512,588 | |||||||||||||||

| Net income per share(5) | 183 | 319 | 359 | 380 | 201 | |||||||||||||||

| Total assets | 142,181,291 | 132,427,994 | 113,879,578 | 92,277,386 | 68,769,356 | |||||||||||||||

| Shareholders’ Equity | 68,545,972 | 71,119,203 | 64,740,881 | 54,688,855 | 41,328,181 | |||||||||||||||

| Subscribed capital | 10,279,175 | 10,279,175 | 10,279,175 | 10,279,175 | 10,118,128 | |||||||||||||||

| Number of common shares(6) | 41,116,698,456 | 41,116,698,456 | 41,116,698,456 | 41,116,698,456 | 40,472,512,588 | |||||||||||||||

| Dividends declared per share | 133 | 260 | 300 | 145 | 91 | |||||||||||||||

| Total Liabilities | 69,439,384 | 56,735,043 | 46,536,530 | 35,335,900 | 26,955,224 | |||||||||||||||

| U.S. GAAP | ||||||||||||||||||||

| (Expressed in millions of Colombian pesos, except net income per share and net operating income per share, which is expressed in Colombian pesos) | ||||||||||||||||||||

| Total revenue | 66,117,500 | 68,432,645 | 66,867,137 | 62,715,815 | 40,879,324 | |||||||||||||||

| Operating profit | 16,461,798 | 23,319,936 | 23,556,963 | 23,673,787 | 13,878,515 | |||||||||||||||

| Net income attributable to Ecopetrol | 6,819,550 | 13,946,855 | 14,695,649 | 14,817,207 | 8,211,035 | |||||||||||||||

| Net operating income per share | 400 | 567 | 573 | 583 | 343 | |||||||||||||||

| Weighted average number of shares outstanding(4) | 41,116,698,456 | 41,116,698,456 | 41,116,698,456 | 40,634,882,725 | 40,472,512,588 | |||||||||||||||

| Net income per share | 166 | 339 | 357 | 365 | 203 | |||||||||||||||

| Total Assets | 102,310,815 | 91,687,916 | 81,519,332 | 70,909,079 | 52,332,148 | |||||||||||||||

| Shareholders’ Equity | 42,072,910 | 41,875,226 | 37,648,352 | 36,055,173 | 27,175,285 | |||||||||||||||

| Number of common shares(6) | 41,116,698,456 | 41,116,698,456 | 41,116,698,456 | 41,116,698,456 | 40,472,512,588 | |||||||||||||||

| Dividends declared per share | 133 | 260 | 300 | 145 | �� | 91 | ||||||||||||||

| Total Liabilities | 57,589,537 | 46,997,359 | 41,436,532 | 32,565,787 | 24,847,512 | |||||||||||||||

| Operating Information | 2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||||||

| Oil and gas production (mboed) | 717.9 | 760.7 | 755.4 | 788.2 | 754.0 | |||||||||||||||

| Proved oil and gas reserves (Mmboe)(1) | 1,598 | 1,849 | 2,084 | 1,972 | 1,877 | |||||||||||||||

| Exploratory Wells(2) | 6 | 5 | 28 | 22 | 23 | |||||||||||||||

| Refinery Through-put (bpd)(3) | 332,751 | 234,861 | 240,484 | 283,362 | 296,340 | |||||||||||||||

| 1P Reserves replacement ratio | (7 | %) | 6 | % | 146 | % | 139 | % | 108 | % | ||||||||||

| (1) | For 2016, 2015 and 2014, proved reserves |

| (2) | Gross exploratory wells. |

| (3) | Refinery through-put includes Barrancabermeja, Reficar, Apiay and Orito. |

Financial Information

International Financial Reporting Standards (“IFRS”)

(Expressed in millions of Colombian Pesos, except for the net income per share and net operating income per share, which are expressed in Colombian Pesos)

Table 2 – Selected Financial Data

| Financial Information | 2016 | 2015 | ||||||

| Revenue | 48,485,561 | 52,347,271 | ||||||

| Operating income | 8,904,548 | 2,131,165 | ||||||

| Net income (loss) attributable to Ecopetrol’s shareholders | 2,447,881 | (7,193,859 | ) | |||||

| Net operating income per share | 217 | 52 | ||||||

| Weighted average number of shares outstanding | 41,116,694,690 | 41,116,694,690 | ||||||

| Earnings(loss) per share (basic and diluted) | 59.5 | (175.0 | ) | |||||

| Total assets | 120,437,924 | 123,588,190 | ||||||

| Financial Information | 2016 | 2015 | ||||||

| Total equity | 43,560,501 | 43,100,963 | ||||||

| Subscribed and paid-in capital | 25,040,067 | 25,040,068 | ||||||

| Number of common shares | 41,116,694,690 | 41,116,694,690 | ||||||

| Dividends declared per share | 23 | - | ||||||

| Total liabilities | 76,877,423 | 80,487,227 | ||||||

Our consolidated financial statements have beenfor the years ended December 31, 2014, 2015 and 2016 were prepared under the Public Accounting Regime (Régimen de Contabilidad Pública), or RCP,in accordance with IFRS as adoptedissued by IASB. References in this annual report to IFRS mean IFRS as issued by the Colombian National Accounting Office (Contaduría General de la Nación), or CGN in September, 2007 and applicableIASB. Our date of transition to Ecopetrol beginning withIFRS was January 1, 2014. Our consolidated financial statements for the fiscal year ended December 31, 2008. See Note 1—Economic Entity2015 were our first set of consolidated financial statements prepared in accordance with IFRS.

IFRS differs in certain significant aspects from the current reporting standards as in effect in Colombia (“Colombian IFRS”)), which is the accounting standard we use for local reporting purposes. As a result, our financial information presented under IFRS is not directly comparable to our financial information presented under Colombian IFRS. For a description of the differences between Colombian IFRS and Principal AccountingIFRS see sectionFinancial Review—Summary of Differences between Internal Reporting Policies and PracticesIFRS,.

Our consolidated financial statements were consolidated line by line and all transactions and balances between subsidiaries have been eliminated. These financial statements include the financial results of all subsidiary companies controlled, directly or indirectly, by Ecopetrol S.A. See Exhibit 1 – Consolidated companies, associates and joint ventures, to theour consolidated financial statements included in this Annual Report.annual report.

As indicated in paragraphs 9 and 18 of the International Accounting Standard 27 “Consolidated and Separated Financial Statements” we must present our financial information on a consolidated basis as if we were a single entity, combining the financial statements of Ecopetrol S.A. and its subsidiaries line by line, adding assets, liabilities, shareholder’s equity, revenues and expenses of similar nature, removing the reciprocal items among members of the Ecopetrol Group and recognizing non-controlling interest. We referpresent our operating information on a consolidated basis.

The regulations of the SEC do not require foreign private issuers that prepare their financial statements on the basis of IFRS to RCP as Colombian Government Entityreconcile such financial statements to U.S. GAAP. Accordingly, while we have in the past reconciled our consolidated financial statements prepared in accordance with Colombian Government Entity GAAP differsto U.S. GAAP, those reconciliations are no longer presented in certain significant respects from generally accepted accounting principles inour filings before the United States, orSEC. We do continue to provide the disclosure required under the U.S. GAAP. Note 33Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 932 “Extractive Activities—Oil and Gas” (which we refer to the consolidated financial statements included inas ASC Topic 932), as this Annual Report provides a descriptionis required regardless of the principal differences betweenbasis of accounting on which we prepare our financial statements. Other than as required under ASC Topic 932, any references to accounting treatments under Colombian Government Entity GAAP andor U.S. GAAP as they relate solely to the application of Colombian Government Entity GAAP or U.S. GAAP to our auditedhistorical consolidated financial statements and provides a reconciliation of net income and shareholders’ equity for the years and as of the dates indicated therein. As a state-owned company, our consolidated financial statements are periodically reviewed by the CGN. However, the review of our accounts by the CGN does not constitute an audit.statements.

In this annual report, references to “US$” or “U.S. dollars” are to United States dollars and references to “Ps$“COP$,” “Peso”“Colombian Peso” or “Pesos”“Colombian Pesos” are to Colombian Pesos, the Ecopetrol Group’s functional and presentation currency under which we prepare our consolidated financial statements. This annual report translates certain Colombian Peso amounts into U.S. dollars at specified rates solely for the convenience of the reader. Unless otherwise indicated, such Colombian Peso amounts have been translated at the rate of Ps$2,392.46COP$3,053.42 per US$1.00, which corresponds to theTasa Representativa Promedio del Mercado(TRM), or Average Representative Market Exchange Rate, for December 31, 2014.2016. Such conversion should not be construed as a representation that the Colombian Peso amounts correspond to, or have been or could be converted into, U.S. dollars at that rate or any other rate. On April 28, 2015,May 26, 2017, the Representative Market Exchange Rate was Ps$2,419.81COP$2,911.66 per US$1.00.

Certain figures shown in this annual report have been subject to rounding adjustments and, accordingly, certain totals may therefore not precisely equal the sum of the numbers presented. In this annual report a billion is equal to one with nine zeros.

| 3 |

| 2. | Strategy and Market Overview |

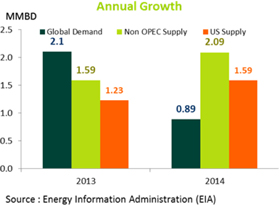

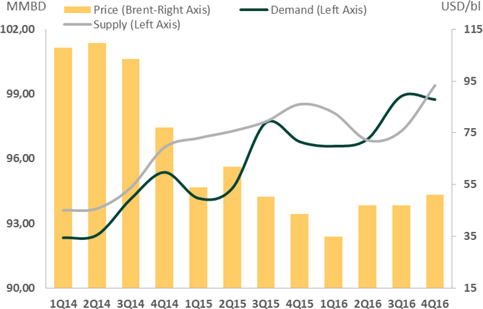

In the second half of 2014, internationalDue to market imbalances, there was a sharp contraction in crude oil benchmarkprice, particularly in the first quarter of 2016. As demand proved to sustain itself while producers implemented previously announced capital expenditure reduction decisions that encompassed the adjustments necessary under the new price environment, the market began its path towards tighter balances (see Graph 1 – Supply/Demand vs ICE Brent price evolution). Although oil prices declined dramatically. From its peak in June 2014,have recovered from the Brent monthly contract price fell by more than 50% by year-end, directly impactinglowest prices during the revenueoil crisis, high levels of oil producing companies. It is believed that the main reason behind the drop in prices is an imbalance between global supply and demand. According to some estimates, 2014 global oil demand growth was 1,500 mboepduncertainty persist indicating a less than supply growth. Non-OPEC supply grew 2,090 mboepdsmooth recovery. Nonetheless, the change in 2014 with mostOPEC’s stance, announced at the end of September 2016 and later ratified in early December 2016, towards coordinated production cuts provided a lift that allowed the growth coming fromICE Brent price to end the United States (+1,590 mboepd). Thanks to the shale revolution, for the past three years, the United States has been the world’s fastest-growing hydrocarbon producer. U.S. crude oil production rose by 40% over that period, while natural gas production has grown by 29% since 2008, transforming this country into the main supplier of natural gas and the third largest supplier of crude oil worldwide. On the other hand, global demand grew 0.890 mboepd, mainly due to weak global economic growth of the Euro zone and Japan, along with lower expectations for China´s growth.year above US$55 per barrel.

| |

Graph 1 – Supply/Demand Balance vs ICE Brent Price Evolution

Source: Energy Information Administration (EIA), “Annual Energy Outlook”.

PIRA Energy Group, “WorldWorld Oil Market Forecast”

Forecast (February 28, 2017)

Those imbalances caused a significant rise in global oil inventories during the first half of 2014, from 739 to 776 million barrels. As of December 31, 2014 global inventories were an estimated 770 million barrels, and since then they have increased further to 858 million barrels as of March 31, 2015. Historically such an excess of supply would have been offset through a cut in production from OPEC states. Nevertheless, OPEC members at their November 27, 2014 meeting decided to maintain their production levels. Given the fact that both the supply and demand of oil are relatively inelastic, particularly in the short term, Ecopetrol believes it will take some time for end consumers to see a reduction in gasoline prices significant enough to stimulate demand and for higher-cost production to decrease in reaction to lower crude prices. Thus, overall business sentiment points to an environment of short term weakness in crude oil prices.

Although international oil prices and global demand and supply dynamics are significant factors affecting our business and financial condition, Colombia’s local economic dynamics in Colombiafactors have also influenced and could continue to influence our performance given that we conduct substantially allmost of our business in Colombia. In 2014

The performance of Colombia’s gross domestic product (GDP) is one of the main drivers of fuel consumption in Colombia. According to the National Administrative Department of Statistics (DANE for its acronym in Spanish), during 2016 Colombia’s GDP grew by 4.6%,2% in real terms, as compared to 4.9%2015. The industries with the greatest growth rates were financial institutions, insurance, real estate and business services, construction and manufacturing. On the other hand, the industry with the largest drop in 2013, driven mainly by the performancegrowth was mining. Local sales of the construction, services and financial sectors. This economic performance resulted in higher local demand for liquid fuels which(diesel, gasoline, jet fuel and LPG) increased by 3.5%.2% mainly due to the increase in sales of gasoline. Gasoline domestic sales were more competitive than its substitutes due to its price decrease and fewer than expected conversions to natural gas for vehicles (NGV) in Colombia.

Recently,In 2016, there were no major changes in natural gas regulation. With respect to natural gas supply, in November 2016, a new regasification plant located in Cartagena became available, meaning that Colombia is now connected to the Colombian Government reduced its forecasted economic growthinternational LNG market and LNG prices will be a reference for 2015 from 4%-4.5% to 3.5%-4%, reflecting the impact of lower commodity prices, especially crude oilnational gas prices. Growth in 2015 is expected to be driven by the building construction and infrastructure sectors, mainly as a result of two ongoing programs: 4G (Cuarta Generacion) highway concessions, an ambitious program to build and operate under concession contracts more than 8,000 km of roads and 159 tunnels, and Mi Casa, a housing subsidy program aimed at Colombia’s low-income population that seeks to deliver 100,000 new houses at no cost plus other initiatives based on a reduction of the mortgage interest rate and direct subsidies.

| 4 |

Despite these positive events, Colombia’s economy faces significant challenges as a result of the lower crude oil lower prices, given that the country is a net oil exporter, and the slow recovery of its main business and trading partners. These factors have resulted in an increased current account deficit in Colombia and placed pressure on the exchange rate of the Colombian Peso against the U.S. dollar.

| Our Corporate Strategy |

The low oil price environment present at the end of 2015 and the beginning of 2016 led to a revision of our business plan 2015-2020, originally launched in May 2015, with a price scenario of US$80 per barrel. Our new 2017-2020 business plan is focused on value generation, profitability and financial sustainability under a price scenario of US$50 per barrel, and allows for considerable upsides in case of potential price increases. For example, if prices were to increase to an average price of US$70 per barrel, production by 2020 could reach 830 thousand barrels equivalent per day, or 16% over the current production.

The three pillars of the plan are: (i) cash flow focus and cost efficiency, (ii) strict capital discipline and (iii) profitable reserves and production growth.

Cash flow focus and cost efficiency: In 2015, we launched the 2015-2020 Transformation Program (the “Transformation Program”) with a goal of increasing our efficiency and decreasing cost. The Transformation Program has allowed us to decrease structural costs by US$1.5 billion compared to 2014. Such reduction has been accomplished due to the implementation of initiatives through our different business segments and corporate areas. The new business plan entails a second phase of the Transformation Program, with activities aimed to achieve excellence in project planning and execution as well as in our production, transportation, refining and marketing operations.

Capital discipline: We have preserved a rigorous level of capital discipline through the adjustment of investments and the adoption of strict controls to ensure that projects are delivered efficiently and within the expected time frame and budget. The plan calls for investments of approximately US$13 billion between 2017 and 2020. By 2020, approximately 90% of this investment will be allocated to the development of exploration and production projects, while investments in transportation and refining will seek to improve operational integrity and reliability.

As part of capital discipline, Ecopetrol is currently engaged in the approval phasedivestment of its strategy fornon-strategic assets and the period 2015-2030. This new strategy aims at generating sustainable value for Ecopetrol, reaffirming the Group’s strength aftersale of minor fields, and has also defined a decade of consistent growth that led Ecopetrol to consolidate its positiondividend policy as the largest Colombian company and one of the 35 largest oil companiesdescribed in the world.Section 6.2 Dividend Policy.

Ecopetrol has launchedProfitable growth in production and exploration: One of the pillars of the revised business plan is the view that a strong production portfolio and a greater exploratory success will bring about profitable growth. Under a price scenario of US$50 per barrel, production should average 760 thousand barrels of oil equivalent per day by 2020, an ambitious corporate transformation program in response to recent business dynamics and changesapproximately 6% growth from 2016. Approximately 94% of this production will come from the current producing assets.

In exploration, the plan estimates the incorporation of approximately 1,000 million barrels of contingent resources. In respect of adding reserves, we highlight the results of the exploratory campaigns in the global energy market, with two main objectives: (i) streamline processesColombian Caribbean offshore and improve the efficiencyGulf of the company to protect its financial and operational strength, and (ii) strengthen the capacities of Ecopetrol, to ensure a path for creating sustainable valueMexico in the medium and long term. In January 2015,United States. During the corporate transformation program was structured around eight key topics: Efficiency, Exploration, Recovery Factor, Culture and Leadership, Community Relationship, Projects, Technology and Capital Discipline.

Efficiency is the first axisperiod 2017 – 2020, Ecopetrol expects to add 600 million barrels of the transformation program. Ecopetrol is determined to achieve cumulative structural savings through the implementation of best practices in processes and focus on high-value activities. In addition, the program includes a thorough review of the project execution area and a more dynamic investment portfolio management, with the aim of optimizing capital allocation and ensuring that projects meet their budgets in terms of costs, time and profitability.

Strengthening the capacities of the company is also a key objective of the transformation program. For this reason, Ecopetrol is already structuring a comprehensive program for the improvement of its oil recovery factor, which will maximize cash generationproven reserves from current productive fields. In addition, Ecopetrol will reinforce its technical capabilities in explorationfields and will launch a capacity-building technology program, fundamental to the creation of sustainable value in the oil and gas industry. Finally, the transformation program aims at designing a new model for successfully relating Ecopetrol with its environment, and includes actions intended to reinforce the corporate culture of Ecopetrol and enhance its human talent and leadership.

This transformation program is the first piece of a new strategy for Ecopetrol for the period 2015-2030, which will be presented in detail once approved definitively by the Boardexploration.

Consistent with the new corporate strategybusiness plan update, in November 2016, the long term, and after a thorough reviewboard of the project portfolio to prioritize investments that maximize shareholder value, the directors of Ecopetrol (“Board of Directors of EcopetrolDirectors”) approved a $7.860US$3.5 billion investment plan for the year 2015.2017. The plan aims at achievingEcopetrol Group will continue to produce an annual average production of 760about 715 thousand barrels of oil and gas equivalent per day during 2017. This production level lays the foundation for the corporate group, of which 710 thousand correspond to Ecopetrol S.A.Ecopetrol’s expected increase in production by 2020.

OutMost of the total $7.86 billioninvestment will be in exploration and production. In refining, petrochemicals and biofuels, and transportation and logistics, investments will be made to comply with integrity and operational requirements as well as project completion. The table below sets forth the details of the investment plan approved for the Corporate group, $4.11 billion will be invested directly by Ecopetrol S.A. and $3.75 billion by subsidiaries, including $1.93 billion to be contributed by Ecopetrol S.A to its subsidiaries. Out of these investments, 92% will be held in Colombia and the remaining 8% abroad through subsidiaries. The highest percentage of resources will be directed toward production, the culmination of the modernization of the Cartagena refinery and the strengthening of the transportation capacity. The detail of the investments approved per segment is as follows:business segment.

Table 3 – 2017 Investment Plan

| Business Segment | Millions of US$(1) | % Percentage | ||||||

| Exploration | 650 | 18.6 | % | |||||

| Production | 2,200 | 62.9 | % | |||||

| Transportation and Logistics | 265 | 7.6 | % | |||||

| Refining, Petrochemicals, and Biofuels | 360 | 10.3 | % | |||||

| Others | 25 | 0.6 | % | |||||

| TOTAL | 3,500 | 100 | % | |||||

| (1) | Rounded figures. |

The resources requiredExploration

In the exploration segment, US$650 million will be allocated mainly to the evaluation and appraisal of discoveries and ongoing exploration efforts of Ecopetrol S.A. (approximately US$460 million), Hocol S.A. (“Hocol”) (approximately US$114 million), Ecopetrol America Inc. (approximately US$11 million), Ecopetrol Costa Afuera (approximately US$44 million) and Ecopetrol Brazil (approximately US$21 million).

Production

In the production segment, US$1,977 million will be allocated mainly to the execution of development and incremental production projects in the Castilla, Rubiales, Yarigui-Cantagallo, La Cira - Infantas, Tibú, Piedemonte, Chichimene, Quifa, Provincia and Cusiana-Cupiagua fields (approximately US$1,147 million). We have also allocated funds for our affiliates and subsidiaries as follows: US$64 million for the investmentoperation and maintenance of fields of Ecopetrol America Inc. in the U.S. Gulf of Mexico, US$88 million to Hocol, US$63 million to Equion and US$8 million to Savia.

Transportation and logistics

In the transportation and logistics segment, US$138 million will be allocated to investments focused on the completion of projects such as San Fernando-Monterrey and transportation of heavy crude oils as well as crude oil dilution projects. The segment is seeking a higher efficiency in operations and maintenance practices.

Refining, petrochemicals, and biofuels

In the refining, petrochemicals, and biofuels segment, US$105 million will be allocated to Reficar, US$150 million to programs to improve operations at the Barrancabermeja Refinery through initiatives aimed to increase revenues, improve efficiency and reduce operational costs and US$82 million to Bioenergy. The segment is seeking a higher efficiency in operations and maintenance practices. It is important to highlight that the Barrancabermeja Refinery modernization plan will come from internal cash generation, divestmentscontinue to be delayed until the oil price environment allows investments to be made in non-strategic assetssuch a major project. The mode of execution will be defined in this context, after analyzing alternatives which include a modular option in time and financing, consistent with preserving business and financial metrics that will ensure maintenance of Ecopetrol’s investment grade credit rating.investment.

| 3. | Business Overview |

| Our History |

We were formed in 1951 by the Colombian government as Empresa Colombiana de Petróleos and began operating the crude oil fields at La Cira-Infantas, the oldest Colombian oil field whose production started in 1918, and the pipeline that connected that field with the Barrancabermeja refineryRefinery and the port of Cartagena. In 1961, we assumed the direct operation of the Barrancabermeja refineryRefinery and continued its transformation into an industrial complex. In 1974, we acquired the Cartagena refinery,Refinery, which had been in operation since 1957.

In Pursuant to Decree 0062 of 1970, we adopted our first bylaws thatwere transformed us into a governmental industrial and commercial company administered by the Ministry of Mines and Energy. In 2003, we were transformed from an industrial and commercial company into a state-owned corporation, and renamed Ecopetrol S.A.company.

PursuantIn 2003 pursuant to Decree Law 1760, the Agencia Nacional de Hidrocarburos - National Hydrocarbons Agency (the “ANH”) was created and Ecopetrol´s public role as administrator and regulator of 2003, we were granted greaterthe national hydrocarbons resources was transferred to the ANH. Ecopetrol modified its organic structure and became Ecopetrol S.A., a public stock-holding corporation, one hundred percent state-owned, and continued the development of exploration and production activities in a competitive basis with autonomy over our business decisions and we accelerated our exploration activities.decisions. Since 2003,2006, according to Law 1118, we have been evolving from a wholly state-owned entity to a mixed-economy company with private capital. This process has resulted in a substantial change in the legal framework to which we are subject and in the nature of our relationship with the Nation. We carried out our initial public offering in November 2007 when our common shares became listed on the Colombian SecuritiesStock Exchange. Our American Depository Shares (“ADSs”) were listed on the New York Stock Exchange in 2008.

The following table sets forth a list of Starting in August 2010, our material acquisitions since January 1, 2009 andADSs began trading on the effective date as of which each acquisition has been reflected inToronto Stock Exchange (“TSX”) under the symbol “ECP.” On February 17, 2016, we announced our operating results.application for voluntary delisting from the TSX. On March 2, 2016, our ADR´s were officially delisted from the TSX.

We are in the process of selling some of our non-core shareholdings:

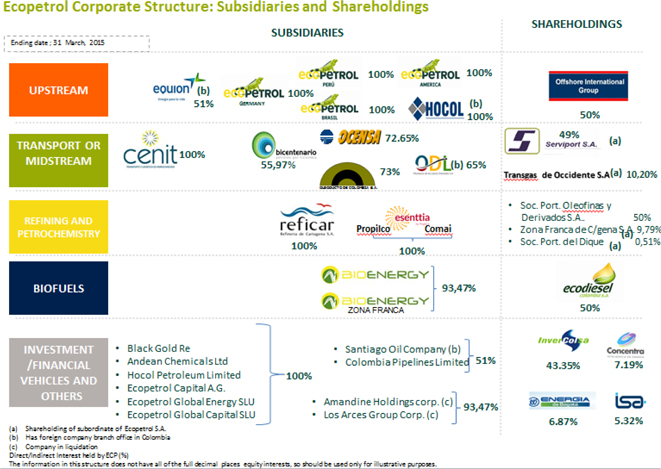

| Our Corporate Structure |

We operate in the following business segments: 1)i) Exploration and Production; 2)ii) Transportation and Logistics; 3)iii) Refining, Petrochemicals, and Biofuels.

Our subsidiaries Refinería de Cartagena (Reficar), Cenit and Ocensa are significant subsidiaries as such term is defined under SEC Regulation S-X.

We have a number of directly and indirectly held subsidiaries both in Colombia and abroad. Our subsidiaries are either directly owned by us or indirectly owned by us through one or more of our other subsidiaries. As of March 31, 2015,2017, we have eight directly owned and 1620 indirectly owned subsidiaries.

In June 2014 we organized a new wholly owned German subsidiary,During 2016, the following changes were made to the Ecopetrol Germany GmbH, to manage the 10% exploration and productions rights acquired from Statoil in Blocks 38 and 39 in Angola.Group’s structure:

| · | In January 2016, we organized a new wholly-owned subsidiary, Ecopetrol Costa Afuera Colombia S.A.S., which will be responsible for offshore exploration and production activities in Colombia. The new subsidiary seeks to develop offshore activities in Colombia, which the Company currently carries out as operator and non-operator, and take advantage of the benefits of Decree 2682/14, pursuant to which the conditions and requirements are established for declaring the existence of permanent offshore free trade zones. |

Our subsidiaries Refinería de Cartagena (Reficar), Cenit Transporte y Logística de Hidrocarburos S.A.S. (Cenit) and Oleoducto Central S.A. (Ocensa) are significant subsidiaries as such term is defined under SEC Regulation S-X.

| · | Polipropileno del Caribe S.A. (Propilco), a wholly owned subsidiary, incorporated Esenttia Resinas del Peru S.A.C in Peru. This new company is wholly indirectly owned by Ecopetrol S.A. For Propilco, the creation of this new company represents an opportunity to strengthen the company’s commercial strategy in Peru. |

| · | The process of reorganizing Ecopetrol S.A.’s indirect participation in Oleoducto de Colombia S.A. (“ODC”) (held through Equion Energia Limited) was successfully completed. As a result of this reorganization, Equion transferred 100% of the shares issued by Sento S.A.S. (“Sento”) to Cenit S.A.S.(“Cenit”), and consequently Sento S.A.S. became the holder of 7.43% of the outstanding capital stock in ODC. However, this restructuring had no impact on our consolidated financial statements. |

| · | In January 2017, the merger by absorption between Sento and Cenit was completed, with the latter being the absorbing company as of January 6, 2017. As a result, Cenit is now the direct holder of a 51.28% equity interest in the outstanding capital stock of ODC.However, this restructuring had no impact on our consolidated financial statements. |

The following tableExhibit 8.1 to this annual report identifies our principal operating subsidiaries, their respective countries of incorporation, and our percentage ownership in each (both directly and indirectly through other subsidiaries), in each case as of March 31, 2015. See Exhibit 8.1 to this annual report for a complete list of our subsidiaries, their respective countries of incorporation, and our percentage of ownership in each.2017.

Graph 2 – Ecopetrol Corporate Structure

The following organization chart illustrates the relationships betweenstock ownership percentage listed refers to Ecopetrol S.A. and its’s direct and indirect subsidiariesparticipation. The data in this structure shows neither the whole ownership nor its decimal figures, so they will be used only for information purposes.

The so-called shareholding (Ecopetrol S.A.’s direct participation), affiliated, subsidiary companies are listed, as well as the stock interest of March 31, 2015.Ecopetrol S.A.’s subordinate companies.

We are in the process of selling some of our non-core shareholdings:

| · | We currently own 0.31% of the total outstanding shares of Empresa de Energía de Bogotá. As approved by Decrees 2305 of November 13, 2014 and 2110 of December 22, 2016, we are authorized to offer our remaining 0.31% of total outstanding shares of Empresa de Energía de Bogotá to the general public using the most appropriate mechanism for the volume and value of the remaining shares. The first stage of the divestment plan took place during the second quarter of 2015, in which we placed 352,872,414 shares at COP$1,740 per share. In 2016, Ecopetrol placed 249,760,551 ordinary shares of Empresa de Energía de Bogotá at COP$1,815 per share. The operation was executed in accordance with the procedures defined by the Law 226 of 1995 and the Decree 2305 of November 13, 2014. On December 22, 2016, the Colombian Government issued Decree 2110 extending the duration of the divestment program until December 31, 2017. |

| · | In 2016, Ecopetrol completed the divestment of its stake in Interconexión Eléctrica S.A. E.S.P. ISA for a total of COP$513 billion. The operation was carried out in accordance with the procedures defined by the Law 226 of 1995 and the Decree 1800 of September 9, 2015. |

| · | We currently own 100% of the total outstanding shares of Propilco. On January 27, 2016, the Board of Directors of Ecopetrol approved the commencement of a divestment plan to sell Ecopetrol’s shares in Propilco. On June 13, 2016, the divestment program was approved by the Council of Ministers of Colombia. The next step in the process is the issuance of a Decree with the final approval to begin the divestiture process under Law 226 of 1995, which has not yet been provided and therefore we are not yet accounting this as a discontinued operation. |

| · | On November 25 of 2016, Ecopetrol conducted an auction to divest 20 non-core producing and non-producing assets. As a result of the bidding process, Ecopetrol received offers for US$53.4 million in six non-core assets, out of which three are currently producing 1.8 mbod and the rest are not in operation. |

| 8 |

| Our Business |

We are a vertically integrated oil company with a presence primarily in Colombia and with activities in Peru, Brazil Angola and the U.S. Gulf Coast. The Nation currently controls 88.49% of our voting capital stock. We are among the top 5036 oil and gas companies in the world based on the Petroleum Intelligence Weekly Top 50 Ranking and in the top 5 in Latin America based on production volume.- 2016. We are the largest corporation in Colombia as measured by revenues, Ebitda, shareholders’ equity, net income and net worth, and we play a key role in the local hydrocarbon market.

| Exploration and Production |

Our Explorationexploration and Productionproduction business segment includes exploration, development and production activities in Colombia and abroad. We began local exploration in 1955 and international exploration in 2006. We conduct exploration and production activities directly in Ecopetrol S.A., through some of our subsidiaries, and through joint ventures with third parties. As of December 31, 2014,2016, we were the largest operator and the largest producer of crude oil and natural gas in Colombia, and we maintainedmaintaining the largest acreage under exploration position in Colombia.

| 3.4.1 | Exploration Activities |

OurEcopetrol is planning to incorporate about 1 billion barrels of contingent resources by 2020, through exploration planactivities in the following areas: (i) offshore Colombia, (ii) near field exploration in Colombia, is focused on(iii) consolidation of exploration of: (1) production sites in close proximity to existing ones and (2) currently producing basins and exploration of frontier areas including off-shore areas primarily operated by our business partners, which we believe have the potential for large discoveries. Our exploration strategy outside of Colombia, such as the Gulf of Mexico, Brazil and other areas in America.

During 2016 our exploration activities focused in three work fronts: onshore Colombia, Colombia and the US Gulf of Mexico offshore and near field exploration in Colombia.

On January15, 2016 Hocol Petroleum Limited - HPL, subsidiary of Ecopetrol S.A. and owned 100% by Ecopetrol, constituted and registered before the Chamber of Commerce in Colombia the company Ecopetrol Offshore (“Ecopetrol Costa Afuera”or “ECAS”). ECAS and Hocol S.A. are subsidiaries of HPL.

ECAS´ purpose is focused on locating prospectsto develop oil and establishing joint venturesgas activities in offshore Colombia by taking advantage of offshore free trade zones regime. These activities include exploration, exploitation, production, transport, distribution, export, sales and commercialization of oil and gas and any other hydrocarbon products or derivatives.

During 2016 bidding rounds were not launched by the National Hydrocarbons Agency to offer licenses for exploratory activities in Colombia.

Ecopetrol signed farmout agreements with experienced operators.the following companies: Parex Resouces Colombia Ltd (acquired 50% of the working interest in Convenio Playón and 50% of the working interest in Convenio de Mares), Talisman Colombia Oil & Gas Ltd (acquired 49% of the working interest in Convenio Upar) and Hupecol Operating Co LLC (acquired 100% of the working interest in CPO-11 E&P Contract).

Additionally, Ecopetrol carried out its Onshore Round 1-2016 offering working interest in the onshore blocks LLA-38, LLA-39, LLA-52, PUT 13 and VMM-32 located in Colombia.

For purposes of this exploration section, “we” refers to Ecopetrol S.A., its subsidiaries and partnerships in which Ecopetrol has an interest. Unless otherwise stated, all figures are given before deductions for royalties.

| 3.4.1.1 | Exploration Activities in Colombia |

WeCurrently we have exploration activities in allmost of the sedimentary basins in Colombia, in which active oil and gas operations are found.

| 9 |

The following map shows the basins where we conductEcopetrol has been conducting its main exploration activities.

Source: ANH

We conduct exploration activities in Colombia on our own and through joint ventures with regional and global oil and gas companies. In 2014 Ecopetrol S.A. acquired 6,607 equivalent kilometers of seismic data, both directly and through business partners.

Seismic

During 2016, two 2D seismic programs were acquired in Colombia: Cardon (106.5 Km) and Nogal (44 Km).These seismic programs are intended to increase the knowledge of the Caguan-Putumayo basin.

Additionally, our subsidiary Hocol S.A. successfully completed the acquisition of 294.9 km2 of 3D seismic in the exploratory blocks GUA2 (213.5 km2) and YDSN1 (81.4 km2) in Middle Magdalena Basin and Llanos Basin, respectively.

Exploratory Wells

During 2016, onshore drilling operations were started in five wells by Ecopetrol and its subsidiary Hocol S.A. in the Lower Magdalena Basin and Llanos Basin. Additionally Hocol finalized drilling operations in the Payero well (Piedemonte basin), which started in December 2015 and was operated by Equion. In terms of offshore Colombia, drilling operations started at the Purple-Angel 1 well (following the discovery announced at the Kronos-1 well in July 2015) and at the Gorgon-1 prospect. Our joint venture partner Anadarko operates both wells. On March 8, 2017, we announced the discovery of a gas presence at Purple-Angel 1.

| 10 |

The following table sets forth for the periods indicated, the number of gross and net productive and dry exploratory wells drilled by us and our joint venture partners and the exploratory wells drilled by third parties pursuant to sole risk contracts with us.

| For the year ended December 31, | ||||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| COLOMBIA | ||||||||||||

| Ecopetrol S.A. | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Owned and operated by Ecopetrol | ||||||||||||

| Productive(1) | 3 | 4 | 4 | |||||||||

| Dry(2) | 9 | 2 | 2 | |||||||||

| Total | 12 | 6 | 6 | |||||||||

| Operated by Partner in Joint Venture | ||||||||||||

| Productive(3) | 1 | 3 | - | |||||||||

| Dry | 2 | 2 | - | |||||||||

| Total | 3 | 5 | - | |||||||||

| Operated by Ecopetrol in Joint Venture | ||||||||||||

| Productive | 1 | - | - | |||||||||

| Dry | - | - | - | |||||||||

| Total | 1 | - | - | |||||||||

| Net Exploratory Wells(4) | ||||||||||||

| Productive | 4.1 | 5.5 | 3.3 | |||||||||

| Dry | 10.7 | 3.0 | 2.0 | |||||||||

| Total | 14.8 | 8.5 | 5.3 | |||||||||

| Sole Risk | ||||||||||||

| Productive | - | - | - | |||||||||

| Dry | - | - | 1 | |||||||||

| Total | - | - | 1 | |||||||||

| Equion | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Productive | - | - | - | |||||||||

| Dry | - | - | 1 | |||||||||

| Total | - | - | 1 | |||||||||

| Hocol | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Productive | - | 1 | 4 | |||||||||

| Dry | 4 | 6 | 4 | |||||||||

| Total | 4 | 7 | 8 | |||||||||

| Net Exploratory Wells(4) | ||||||||||||

| Productive | - | 0.5 | 3 | |||||||||

| Dry | 3 | 5.0 | 4 | |||||||||

| Total | 3 | 5.5 | 7 | |||||||||

Table 4 – Exploratory Drilling in Colombia

| For the year ended December 31, | ||||||||||||

| 2016 | 2015 | 2014 | ||||||||||

| (number of wells) | ||||||||||||

| COLOMBIA | ||||||||||||

| Ecopetrol S.A. | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Owned and operated by Ecopetrol | ||||||||||||

| Productive(1) | – | – | 3.0 | |||||||||

| Dry(2) | 1.0 | 1.0 | 9.0 | |||||||||

| Total | 1.0 | 1.0 | 12.0 | |||||||||

| Operated by Partner in Joint Venture | ||||||||||||

| Productive | – | 1.0 | 1.0 | |||||||||

| Dry | – | 1.0 | 2.0 | |||||||||

| Total | – | 2.0 | 3.0 | |||||||||

| Operated by Ecopetrol in Joint Venture | ||||||||||||

| Productive | – | – | 1.0 | |||||||||

| Dry | – | – | – | |||||||||

| Total | – | – | 1.0 | |||||||||

| Net Exploratory Wells(3) | ||||||||||||

| Productive | – | 0.5 | 4.1 | |||||||||

| Dry | 1.0 | 1.5 | 10.7 | |||||||||

| Total | 1.0 | 2.0 | 14.8 | |||||||||

| Sole Risk | ||||||||||||

| Productive | – | – | – | |||||||||

| Dry | – | – | – | |||||||||

| Total | – | – | – | |||||||||

| Equion | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Productive | – | – | – | |||||||||

| Dry | – | – | – | |||||||||

| Total | – | – | – | |||||||||

| Hocol | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Productive | 1.0 | 1.0 | – | |||||||||

| Dry | – | – | 4.0 | |||||||||

| Total | 1.0 | 1.0 | 4.0 | |||||||||

| Net Exploratory Wells | ||||||||||||

| Productive | 0.5 | 0.5 | – | |||||||||

| Dry | – | – | 3.0 | |||||||||

| Total | 0.5 | 0.5 | 3.0 | |||||||||

| (1) | A productive well is an exploratory well that has evidence of hydrocarbons. |

| (2) | A dry well or hole is an exploratory well found to be incapable of producing either crude oil or natural gas in sufficient quantities to justify completion as a crude oil or natural gas well. |

| (3) |

| Net exploratory wells are calculated according to our percentage of ownership in these wells. |

| 11 |

Ecopetrol S.A. drilled two wells in 2016: (i) Chimú-1 St-1 well, where Ecopetrol holds a total of 17 wildcat exploratory wells (A3-A2) in 2014, including the QFN-CS1100% working interest at Caño Sur Block, which was a dry well, and (ii) Boranda well, in which Ecopetrol holds a 40%50% working interest and Parex holds the remaining 50% working interest, as block operator. As of March 30, 2017 we announced that the presence of crude was discovered at this well.

Our subsidiary Hocol S.A. drilled three wells in partnership with Metrapetroleum (operator)2016: (i) Payero E1 well, located at Niscota Block and whichoperated by Equión. Total holds a 50% working interest, Repsol holds a 30% working interest and Hocol S.A. holds a 20% working interest, this well was declared temporarily suspended; (ii) Bullerengue Sur-1 well, located at SSJN1 Block. Hocol S.A. holds a 50% working interest and Lewis Energy holds the remaining 50%, this one is a productive well, and (iii) Pegaso well, located at CPO 16 Block where Hocol S.A. holds a 100% working interest, this well was under evaluation as of December 31, 2014. There was evidence of hydrocarbons in five wells: Orca-1 the first discovery in deep waters of the Colombian Caribbean, in which Ecopetrol holds a 30% working interest, in partnership with Petrobras (operator, 40%) and Repsol (30%); Nueva Esperanza in block CPO09, operated by Ecopetrol (55%) in partnership with Talisman Colombia Oil & Gas Ltd. (45%) and in Tibirita-1A, Cacica-1 and Golosa, each of which are 100% owned by Ecopetrol. Eleven wells were dry. Hocol drilled four A3 wells, all of which were dry.

During 2014, Ecopetrol S.A. participated in the bidding round launched by the National Hydrocarbons Agency to offer licenses for exploratory activities in Colombia, and was awarded one exploration block located in the Colombian Caribbean (Sin Off-7) with an extension area of approximately 173 thousand hectares. Ecopetrol S.A. has a 35% stake in this contract. Hocol S.A. submitted the best offer for four blocks in the Sinu San Jacinto Basin: Blocks SN-8, SN-15, SN-18 and YDSN1.2016.

| 3.4.1.2 | Exploration Activities Outside of Colombia |

Our international exploration strategy is focused on participating in bidding rounds to secure blocks available for exploration and entering into joint ventures with international and regional oil companies. We believe exploring outside Colombia allows us to diversify our risks and improve the possibilities of increasing our crude oil and natural gas reserves.

In association withWith respect to our business partners,seismic data outside of Colombia, during 2016, our subsidiary Ecopetrol Brasil bought 854 Km2 of seismic data on the Potiguar basin, POT-M-567, in which Ecopetrol Brasil holds a 100% working interest.

With respect to our exploratory drilling outside of Colombia, during 2016, we have undertaken deep water exploratory drilling in the U.S. Gulf Coast Angolain association with our business partners. The following table sets forth information on our exploratory drilling in the years 2016, 2015 and in Brazil.2014.

| For the year ended December 31, | ||||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| INTERNATIONAL | ||||||||||||

| Ecopetrol America Inc. | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Productive(1) | 2 | - | 2 | |||||||||

| Dry(2) | 3 | 2 | 1 | |||||||||

| Total | 5 | 2 | 3 | |||||||||

| Net Exploratory Wells(3)(4) | ||||||||||||

| Productive | 0.7 | - | 0.3 | |||||||||

| Dry | 0.5 | 0.5 | 0.6 | |||||||||

| Total | 1.2 | 0.5 | 0.9 | |||||||||

| Ecopetrol Óleo e Gás do Brasil Ltda. | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Productive | - | - | - | |||||||||

| Dry | - | 1 | 3 | |||||||||

| Total | - | 1 | 3 | |||||||||

| Net Exploratory Wells(3) | ||||||||||||

| Productive | - | - | - | |||||||||

| Dry | - | 0.3 | 1 | |||||||||

| Total | - | 0.3 | 1 | |||||||||

| Ecopetrol Germany(5) | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Productive | - | - | - | |||||||||

| Dry | 2 | - | - | |||||||||

| Total | 2 | - | - | |||||||||

| For the year ended December 31, | ||||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| Net Exploratory Wells(3) | ||||||||||||

| Productive | - | - | - | |||||||||

| Dry | 0.2 | - | - | |||||||||

| Total | 0.2 | - | - | |||||||||

| Savía Perú(6) | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Productive | - | 1 | - | |||||||||

| Dry | - | - | 3 | |||||||||

| Total | - | 1 | 3 | |||||||||

| Net Exploratory Wells(3) | ||||||||||||

| Productive | - | 0.5 | - | |||||||||

| Dry | - | - | 1.5 | |||||||||

| Total | - | 0.5 | 1.5 | |||||||||

| 12 |

Table 5 – Exploratory Drilling Outside Colombia

| For the year ended December 31, | ||||||||||||

| 2016 | 2015 | 2014 | ||||||||||

| (number of wells) | ||||||||||||

| INTERNATIONAL | ||||||||||||

| Ecopetrol America Inc. | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Productive(1) | 1.0 | – | 2.0 | |||||||||

| Dry(2) | – | 1.0 | 3.0 | |||||||||

| Total | 1.0 | 1.0 | 5.0 | |||||||||

| Net Exploratory Wells(3)(4) | ||||||||||||

| Productive | 0.2 | – | 0.7 | |||||||||

| Dry | – | 0.5 | 0.5 | |||||||||

| Total | 0.2 | 0.5 | 1.2 | |||||||||

| Ecopetrol Óleo e Gás do Brasil Ltda. | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Productive | – | – | – | |||||||||

| Dry | – | – | – | |||||||||

| Total | – | – | – | |||||||||

| Net Exploratory Wells | ||||||||||||

| Productive | – | – | – | |||||||||

| Dry | – | – | – | |||||||||

| Total | – | – | – | |||||||||

| Ecopetrol Germany | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Productive | – | – | – | |||||||||

| Dry | – | – | 2.0 | |||||||||

| Total | – | – | 2.0 | |||||||||

| Net Exploratory Wells | ||||||||||||

| Productive | – | – | – | |||||||||

| Dry | – | – | 0.2 | |||||||||

| Total | – | – | 0.2 | |||||||||

| Savia Perú | ||||||||||||

| Gross Exploratory Wells | ||||||||||||

| Productive | – | – | – | |||||||||

| Dry | – | – | – | |||||||||

| Total | – | – | – | |||||||||

| Net Exploratory Wells | ||||||||||||

| Productive | – | – | – | |||||||||

| Dry | – | – | – | |||||||||

| Total | – | – | – | |||||||||

| (1) | A productive well is an exploratory well that has evidence of hydrocarbons. |

(2) | A dry well or hole is an exploratory well found to be incapable of producing either crude oil or natural gas in sufficient quantities to justify completion as a crude oil or natural gas well. |

| (3) | Net exploratory wells are calculated according to our percentage of ownership in these wells. |

| (4) | None of our international wells were dug pursuant to a sole risk contract. |

In 2014, weAs set forth in the table above, in 2016, our subsidiary Ecopetrol America Inc. drilled seven international grossin the United States Gulf of Mexico the Warrior exploratory wells through our subsidiaries and partners as follows:

Three wells were declared dry holes: the Deep Nansen well, in which Ecopetrol America hadInc. holds a 20% working interest and our partners Anadarko (operator) holds a 65% working interest and MCX Gulf of Mexico LLC holds the remaining 15% working interest,interest. The well was declared productive. This oil discovery is the result of our new exploratory strategy, which wasincludes partnerships with leading companies to diversify risk, undertake further exploration activities and increase contingent resources. The Warrior well is the fifth oil discovery of the Ecopetrol Group in this prosperous oil region and contributes with increasing our contingent resources.

Ecopetrol America Inc. also drilled a successful appraisal well in Leon discovery (León 2 BP4), operated by Repsol, which holds a 60% working interest. Ecopetrol America Inc. holds the remaining 40% working interest.The result of this well adds contingent resources to those initially discovered with the León 1 exploratory well in 2014.

During 2016, Ecopetrol S.A. did not participate in bidding rounds in the Gulf of Mexico.

With regards to ECP Oil and Gas Germany GmbH´s operations in Angola, we reached an agreement with our partners Anadarko Petroleum Corporation (operator), Conoco Phillips, Marubeni Oil & Gas (USA) Inc.on the terms upon which we will withdraw from Block 38/11 and Venari Resources;Block 39/11. This agreement was sent for approval of the Titan well, in which Ecopetrol America hasNational Concessionaire, Sonangol EP, followed by the issuance of a 30% working interest, which was drilled with our partners Murphy Oil Corporation (operator) and Venari Resources; anddecree from the K2 Exploration Tail well in which Ecopetrol America has a 9.21% working interest, which was drilled with our partners Anadarko Petroleum Corporation (operator), Eni Petroleum, ConocoPhillips, Nippon Oil Expl. and MCX GOM.Ministry of Petroleum. We expect the withdrawal process to be concluded by mid-year of 2017.

| 3.4.2 | Production Activities |

Our consolidated average production was 755.4717.9 thousand bpdboepd in 2014, 332016, a decrease of approximately 43 thousand bpd below thatboepd as compared to 2015. This decrease is mainly the result of the previous year. The main factors affecting this result were: 1) the operational difficulties associated with our community relations, including blockades which delayed the start-up of new facilities and new wells in several fields (approximately 22 thousand bpd), 2) the water disposal limitations, essentially in the Rubiales field (9.5 thousand bpd), 3) attacks on our infrastructure, which forced the temporary closure of somenatural production decline of our fields (5 thousand bpd), and 4) the temporarya reduction in productionthe upstream investments during 2016, as a consequence of the drop in the Guajira gas fields due to the start of GACE IV recovery factor improvement project, which required a temporary stop in production. These factors were partially offset by the increase in production by Ecopetrol S.A.’s affiliates and subsidiaries (3.5 thousand bpd).oil prices.

| 13 |

Despite these difficulties, we managed to reverse the trend of decreasing production experienced at the beginning of the year such that we were on a path of production growth in the last two quarters of 2014. This reversal was driven mainly by the results of our direct operations in fields like Chichimene, where we reached production records, and the increase in production of the Castilla field. In addition we made progress on the Akacias field project located in the Llanos Region, where production increased to 10.5 mbpoed by year-end.

The following table summarizes the results of our oil and gas production activities for the periods indicated:

| For the year ended December 31, | ||||||||||||||||||||||||||||||||||||

| 2014 | 2013 | 2012 | ||||||||||||||||||||||||||||||||||

| (thousand bpoed) | ||||||||||||||||||||||||||||||||||||

| Oil(2) | Gas(1) | Total | Oil(2) | Gas(1) | Total | Oil(2) | Gas(1) | Total | ||||||||||||||||||||||||||||

| Total production in Colombia | 610.9 | 133.3 | 744.2 | 643.9 | 136.6 | 780.5 | 626.5 | 118.5 | 745 | |||||||||||||||||||||||||||

| Total International production | 8.6 | 2.6 | 11.2 | 7.2 | 0.5 | 7.7 | 8.2 | 0.9 | 9.1 | |||||||||||||||||||||||||||

| Total production of Ecopetrol Group | 619.5 | 135.9 | 755.4 | 651.1 | 137.1 | 788.2 | 634.7 | 119.4 | 754.1 | |||||||||||||||||||||||||||

Table 6 – Ecopetrol Group’s Oil and Gas Production

| For the year ended December 31, | ||||||||||||||||||||||||||||||||||||

| 2016 | 2015 | 2014 | ||||||||||||||||||||||||||||||||||

| Oil | Gas(1) | Total | Oil | Gas(1) | Total | Oil | Gas(1) | Total | ||||||||||||||||||||||||||||

| (thousand boepd) | ||||||||||||||||||||||||||||||||||||

| Total production in Colombia(2) | 582.5 | 123.3 | 705.8 | 619.2 | 130.4 | 749.6 | 610.9 | 133.3 | 744.2 | |||||||||||||||||||||||||||

| Total International production(3) | 9.6 | 2.5 | 12.1 | 7.3 | 3.8 | 11.1 | 8.6 | 2.6 | 11.2 | |||||||||||||||||||||||||||

| Total production of Ecopetrol Group | 592.1 | 125.8 | 717.9 | 626.5 | 134.2 | 760.7 | 619.5 | 135.9 | 755.4 | |||||||||||||||||||||||||||

| (1) |

| Conversion between mcfpd and boepd is performed at 5,700 mcfpd to 1 boepd. |

| (2) | Total production in Colombia corresponds to Ecopetrol S.A., Hocol and Equion. |

| (3) | Total International production corresponds to Savia Perú and Ecopetrol America Inc. |

| 3.4.2.1 | Production Activities in Colombia |

| 3.4.2.1.1. | Ecopetrol S.A.’s Production Activities in Colombia |

For the year ended December 31, 2014,2016, Ecopetrol S.AS.A. was the largest participant in the Colombian hydrocarbons industry, accounting for approximately 58%62% of crude oil production (according to calculations made by Ecopetrol based on information from the Ministry of Mines and Energy) and approximately 63%61% of natural gas production.

In 2014, weproduction (according to calculations made by Ecopetrol based on information from the Ministry of Mines and Energy). Also during 2016, Ecopetrol S.A. carried out development drilling mainly in all our producingthe Oriente and Orinoquia regions, in Colombia, drilling 761133 development wells; 17783 of those through our direct operations and 58450 through our joint ventures. As part

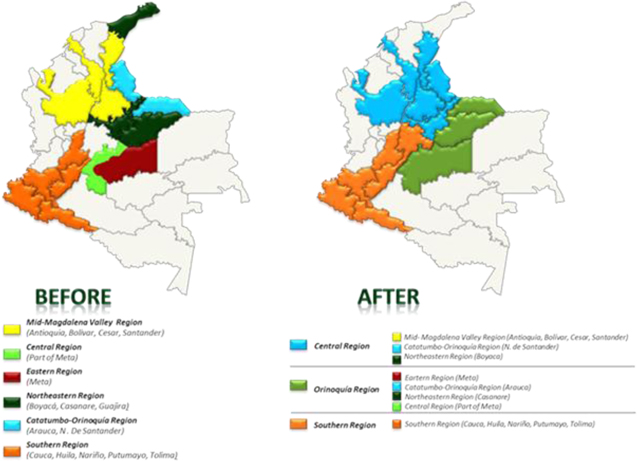

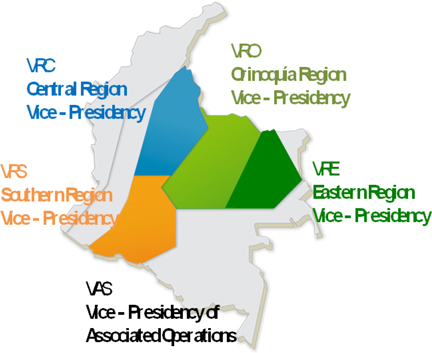

In terms of an internal administrative restructuring process we recently reorganized the management of theoperational structure, Ecopetrol S.A. manages its production activities of Ecopetrol S.A., which will allow us to improve our control on operations while at the same time giving usthrough a closer and more effective interaction with communities and partners. Beginning onregional organization. Since July 1, 2014, our fully owned fieldsthree regional Vice-Presidencies were divided into three main Vice-presidencies or administrativecreated: Central, Orinoquia and Southern. After the company took over the operations of the Rubiales field in July of 2016, a new Vice-Presidency, the Eastern Region, was incorporated to this scheme. Our operating assets are distributed in the following regions:

| · | Central Region: comprising |

| · |

| · | Southern Region: comprising |

| · | Eastern Region: comprising 4 fields with active production in 2016. |

A fourth Vice-presidency,fifth Vice-Presidency, the Vice-presidencyVice-Presidency of Associated Assets, will beOperations, is responsible for all of the production activities in which a partner is involved, regardless of the location of such activities in Colombia. This Vice- Presidency is comprised of 137 fields with active production in 2016.

The map below indicates the locations of ourEcopetrol S.A´s operations in Colombia. Productionwith production information for each of the newour administrative regions is includedfollowing in the discussion following the maps.subsequent paragraphs.

| 14 |

Graph 4 – Ecopetrol S.A. Operations in Colombia

Note: VAS is the countrywide Vice-presidency.

Crude Oil Production

The average daily production of crude oil in Colombia by Ecopetrol S.A. (excluding its subsidiaries), was 579.7 thousand bpd552.1 mbod in 2014, 33 thousand bpd less2016, 34.1 mbod lower than in 2013,2015, which represents a year-to-year decrease of 5.4%6%. The drop

However, it is important to highlight that since July of 2016 we took over the operations of the Rubiales and Cusiana fields. A plan was set up with more than two years in advance, which allowed us to successfully transition between operators, without technical, operational or communities’ issues in any of the two fields. In the case of the Rubiales field, it is important to highlight that we restarted investments in the average dailyasset with new development drilling during the last quarter of the year 2016, which helped us mitigate the production is mainly due to a 10.5% reduction in production in at our associated operations, and the above-described restrictions in our direct operations, mainly in the Orinoquía region where our production dropped by 2.2% as compared to 2013.decline observed during 2015.

The following chart summarizes Ecopetrol S.A.’s average daily crude oil production in Colombia by Region, prior to deducting royalties, for the periods indicated.

| For the year ended December 31, | ||||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| (thousand bpd) | ||||||||||||

| Central Region | ||||||||||||

| 1) La Cira – Infantas | 24.6 | 23.5 | 21.7 | |||||||||

| 2) Casabe | 22.0 | 22.8 | 23.1 | |||||||||

| 3) Yarigui | 16.7 | 14.9 | 14.3 | |||||||||

| 4) Other | 21.0 | 20.3 | 22.4 | |||||||||

| Total Central Region | 84.3 | 81.4 | 81.5 | |||||||||

| Orinoquía Region | ||||||||||||

| 1) Castilla | 104.4 | 112.9 | 111.4 | |||||||||

| 2) Chichimene | 56.2 | 53.1 | 44.1 | |||||||||

| 3) Cupiagua | 16.4 | 18.5 | 20.8 | |||||||||

| 4) Other | 26.0 | 23.8 | 22.8 | |||||||||

| Total Orinoquia Region | 203.0 | 208.3 | 199.2 | |||||||||

| Southern Region | ||||||||||||

| 1) San Francisco | 9.2 | 10.0 | 6.9 | |||||||||

| 2) Huila Area | 8.2 | 7.9 | 9.4 | |||||||||

| 3) Tello | 4.3 | 4.4 | 4.7 | |||||||||

| 4) Other | 11.8 | 11.8 | 12.1 | |||||||||

| Total Southern Region | 33.6 | 34.2 | 33.1 | |||||||||

| Associated Operations | ||||||||||||

| 1) Rubiales | 104.3 | 120.0 | 102.0 | |||||||||

| 3) Quifa | 33.0 | 33.5 | 22.1 | |||||||||

| 4) Caño Limon | 30.0 | 36.4 | 39.2 | |||||||||

| 5) Cusiana | 7.0 | 8.8 | 10.0 | |||||||||

| 6) Other | 83.9 | 89.8 | 101.8 | |||||||||

| Total Associated Operations | 258.2 | 288.5 | 275.1 | |||||||||

| Production tests* | 0.7 | 0.2 | 2.06 | |||||||||

| Total average daily crude oil production Ecopetrol S.A. (Colombia) | 579.7 | 612.6 | 591.0 | |||||||||

| 15 |

Table 7 – Ecopetrol S.A.’s Average Daily Crude Oil Production in Colombia by Region Vice-Presidency

| For the year ended December 31, | ||||||||||||

| 2016 | 2015 | 2014 | ||||||||||

| (thousand bpd) | ||||||||||||

| Central Region | ||||||||||||

| 1) La Cira – Infantas | 19.1 | 22.9 | 24.6 | |||||||||

| 2) Casabe | 17.8 | 21.9 | 22.0 | |||||||||

| 3) Yarigui | 16.6 | 17.8 | 16.7 | |||||||||

| 4) Other | 21.3 | 23.7 | 21.0 | |||||||||

| Total Central Region | 74.8 | 86.3 | 84.3 | |||||||||

| Orinoquía Region | ||||||||||||

| 1) Castilla | 121.3 | 122.5 | 104.4 | |||||||||

| 2) Chichimene | 74.0 | 78.0 | 56.2 | |||||||||

| 3) Cupiagua | 11.3 | 14.0 | 16.4 | |||||||||

| 4) Other | 18.3 | 21.1 | 26.0 | |||||||||

| Total Orinoquía Region | 224.9 | 235.6 | 203.0 | |||||||||

| Eastern Region | ||||||||||||

| 1) Rubiales(1) | 61.5 | 0 | 0 | |||||||||

| 2) Caño Sur(2) | 0.4 | 0 | 0 | |||||||||

| Total Eastern Region | 61.9 | 0 | 0 | |||||||||

| Southern Region | ||||||||||||

| 1) San Francisco | 6.5 | 8.1 | 9.2 | |||||||||

| 2) Huila Area | 7.4 | 7.8 | 8.2 | |||||||||

| 3) Tello | 4.4 | 4.5 | 4.3 | |||||||||

| 4) Other | 9.4 | 11.0 | 11.8 | |||||||||

| Total Southern Region | 27.7 | 31.4 | 33.5 | |||||||||

| Associated Operations | ||||||||||||

| 1) Rubiales(1) | 41.4 | 94.3 | 104.3 | |||||||||

| 2) Quifa | 19.6 | 24.2 | 33.0 | |||||||||

| 3) Caño Limon | 23.3 | 25.6 | 30.0 | |||||||||

| 4) Cusiana(3) | 2.6 | 5.2 | 7.0 | |||||||||

| 5) Other | 75.9 | 83.6 | 84.6 | |||||||||

| Total Associated Operations | 162.8 | 232.9 | 258.9 | |||||||||

| Total average daily crude oil production Ecopetrol S.A. (Colombia) | 552.1 | 586.2 | 579.7 | |||||||||

| (2) | In the first half of 2016, the Caño Sur field was part of the Orinoquia Region. Since July 1, 2016, it became a part of the Eastern Region. |

| (3) | In the first half of 2016, the Cusiana field was part of the Vice-Presidency of Associated Operations. Since July 3, 2016, it became a part of the Orinoquia Region. |

ECOPETROLTable 8 – Ecopetrol S.A. PRODUCTION PER TYPE OF CRUDE (IN MBOD):Production per Type of Crude