The substantial share ownership position of Kibbutz Sdot-Yam and Tene will limit your ability to influence corporate matters.

This concentration of ownership of our ordinary shares could delay or prevent proxy contests initiated by other shareholders, mergers, tender offers, open-market purchase programs or other purchases of our ordinary shares that might otherwise give you the opportunity to realize a premium over then-prevailing market price of our ordinary shares. The interests of the Kibbutz or Tene may not always coincide with the interests of our other shareholders. This concentration of ownership may also lead to proxy contests. For example, prior to the voting arrangement between Tene and the Kibbutz, in connection with our annual general meeting of shareholders held in December 2015, the Kibbutz issued a proxy to our shareholders, in which it opposed the independent nominees our board of directors proposed to nominate to the board and suggested two alternative nominees. Such initiatives, which may not coincide with the interests of our other shareholders, result in us incurring unexpected costs and could divert our management’s time and attention. This concentration of ownership may also materially and adversely affect our share price.

In recent years, Israeli issuers listed on securities exchanges in the United States have also been faced with governance-related demands from activist shareholders, unsolicited tender offers and proxy contests. Responding to these types of actions by activist shareholders could be costly and time-consuming for management and our employees and could disrupt our operations or business model in a way that would interfere with our ability to execute our strategic plan.

As a foreign private issuer whose shares are listed on the Nasdaq Global Select Market, we may follow certain home country corporate governance practices instead of certain Nasdaq requirements.

As a foreign private issuer whose shares are listed on the Nasdaq Global Select Market, we are permitted to follow certain home country corporate governance practices instead of certain requirements of the rules of Nasdaq. As permittedWe rely on this “home country practice exemption” with respect to the quorum requirement for shareholder meetings. Whereas under the Israeli Companies Law,listing rules of the Nasdaq Stock Market, a quorum requires the presence, in person or by proxy, of holders of at least 331/3% of the total issued outstanding voting power of our shares at each general meeting of shareholders, pursuant to our articles of association, provide thatand as permitted under the Companies Law, the quorum required for any ordinarya general meeting of shareholders shall be the presenceconsists of at least two shareholders present in person or by proxy in accordance with the Companies Law, who hold or represent at least 33 1/3% of the total outstanding voting power of our shares, except if (i) any such general meeting of shareholders was initiated by and convened pursuant to a resolution adopted by the board of directors and (ii) at the time of such general meeting, we qualify to use the forms and rules of a “foreign private issuer,” the requisite quorum will consist of two or more shareholders present in person or by a voting instrument,proxy who hold or represent at least 25% of the total outstanding voting power of our shares instead(and if the meeting is adjourned for a lack of 33 1/3% ofquorum, the issued share capital required under Nasdaq requirements. At anquorum for such adjourned meeting will be, subject to certain exceptions, any number of shareholders constitutes a quorum.shareholders).

In the future, we may also choose to follow Israeli corporate governance practices instead of Nasdaq requirements with regard to, among other things, the composition of our board of directors, compensation of officers and director nomination procedures. In addition, we may choose to follow Israeli corporate governance practice instead of Nasdaq requirements with respect to shareholder approval for certain dilutive events (such as for issuances that will result in a change of control of the company, certain transactions other than a public offering involving issuances of a 20% or more interest in the company and certain acquisitions of the stock or assets of another company) and for the adoption of, and material changes to, equity incentive plans. Accordingly, our shareholders may not be afforded the same protection as provided under Nasdaq corporate governance rules. Following our home country governance practices, as opposed to the requirements that would otherwise apply to a U.S. company listed on the Nasdaq Global Select Market, may provide less protection than is accorded to investors of domestic issuers. See “ITEM 16G: Corporate Governance.”

As a foreign private issuer, we are not subject to the provisions of Regulation FD or U.S. proxy rules and are exempt from filing certain Exchange Act reports.

As a foreign private issuer, we are exempt from the rules and regulations under the Exchange Act related to the furnishing and content of proxy statements, and our officers, directors and principal shareholders are exempt from the reporting and short-swing profit recovery provisions contained in Section 16 of the Exchange Act. In addition, we are not required under the Exchange Act to file annual and current reports and financial statements with the SEC as frequently or as promptly as U.S. domestic companies whose securities are registered under the Exchange Act, we are permitted to disclose limited compensation information for our executive officers on an individual basis and we are generally exempt from filing quarterly reports with the SEC under the Exchange Act. Moreover, we are not required to comply with Regulation FD, which restricts the selective disclosure of material nonpublic information to, among others, broker-dealers and holders of a company’s securities under circumstances in which it is reasonably foreseeable that the holder will trade in the company’s securities on the basis of the information. These exemptions and leniencies reduce the frequency and scope of information and protections to which you may otherwise have been eligible in relation to a U.S. domestic issuer.

We would lose our foreign private issuer status if (a) a majority of our outstanding voting securities were either directly or indirectly owned of record by residents of the United States and (b)(i) a majority of our executive officers or directors were United States citizens or residents, (ii) more than 50% of our assets were located in the United States or (iii) our business were administered principally in the United States. Our loss of foreign private issuer status would make U.S. regulatory provisions mandatory. The regulatory and compliance costs to us under U.S. securities laws as a U.S. domestic issuer may be significantly higher. If we are not a foreign private issuer, we will be required to file periodic reports and registration statements on U.S. domestic issuer forms with the SEC, which are more detailed and extensive than the forms available to a foreign private issuer. We would also be required to follow U.S. proxy disclosure requirements, including the requirement to disclose, under U.S. law, more detailed information about the compensation of our senior executive officers on an individual basis. We may also be required to modify certain of our policies to comply with accepted governance practices associated with U.S. domestic issuers. Such conversion and modifications will involve additional costs. In addition, we would lose our ability to rely upon Nasdaq exemptions from certain corporate governance requirements that are available to foreign private issuers.

Our operations may be affected by negative economic conditions or labor unrest in Israel.

Since none of our employees work under any collective bargaining agreements, extension orders issued by the IMEI apply to us and affect matters such as cost of living adjustments to salaries, length of working hours and work week, recuperation pay, travel expenses, and pension rights. Any labor disputes over such matters could result in a work stoppage or strikes by employees that could delay or interrupt our output of products. Any strike, work stoppages or interruption in manufacturing could result in a failure to meet contractual obligations or in delays, including in our ability to manufacture and deliver products to our customers in a timely manner, and could have a materially adverse effect on our relationships with our distributors and on our financial results.

If a union of our employees is formed in the future, we may enter into a collective bargaining agreement with our employees, which may increase our costs and limit our managerial freedom, and if we are unable to reach a collective bargaining agreement, we may become subject to strikes and work stoppages, all of which may materially and adversely affect our business.

The tax benefits that are available to us require us to continue to meet various conditions and may be terminated or reduced in the future, which could increase our costs and taxes.

Our Israeli facilities have been granted “Preferred Enterprise” status by the Israeli Authority for Investment and Development of the Industry and Economy (“Investment Center”), which provides us with investment grants (in respect of certain Approved Enterprise programs) and makes us eligible for tax benefits under the Investment Law.

In order to remain eligible for the tax benefits of a “Preferred Enterprise” we must continue to meet certain conditions stipulated in the Investment Law and its regulations, as amended, and in certificates of approval issued by the Investment Center (in respect of Approved Enterprise programs), which may include, among other things, selling more than 25% of our products to markets of over 14 million residents in 2012 (such export criteria will further be increased in the future by 1.4% per annum) in a specific tax year, making specified investments in fixed assets and equipment, financing a percentage of those investments with our capital contributions, filing certain reports with the Investment Center, complying with provisions regarding intellectual property and the criteria set forth in the specific certificate of approval issued by the Investment Center or the ITA. If we do not meet these requirements, the tax benefits could be canceled and we could be required to refund any tax benefits and investment grants that we received in the past adjusted to the Israeli consumer price index and interest, or other monetary penalties. Further, in the future, these tax benefits may be reduced or discontinued. If these tax benefits are cancelled, our Israeli taxable income would be subject to regular Israeli corporate tax rates. The standard corporate tax rate for Israeli companies has been 23% since 2018.

Historically, some portions of income were tax exempt, but that is no longer the case. In the event of a distribution of a dividend from the tax-exempt income described above, we will be subject to tax at the corporate tax rate applicable to our Approved Enterprise’s and Beneficiary Enterprise’s income on the amount distributed (grossed-up to reflect the pre-tax income that it would have had to earn in order to distribute the dividend) in accordance with the effective corporate tax rate that would have been applied had we not relied on the exemption. In addition to the reduced tax rate, a distribution of income attributed to an “Approved Enterprise” and a “Beneficiary Enterprise” will be subject to 15% withholding tax (or a reduced rate under an applicable double tax treaty, subject to the receipt in advance of a valid certificate from the ITA allowing for a reduced tax rate). As for a “Preferred Enterprise,” dividends are generally subject to 20% withholding tax from 2014 (or a reduced rate under an applicable double tax treaty, subject to the receipt in advance of a valid certificate from the ITA allowing for a reduced tax rate). However, because we announced our election to apply the provisions of Amendment No. 68 prior to June 30, 2015, we will be entitled to distribute exempt income generated by any Approved/Beneficiary Enterprise to our Israeli corporate shareholders tax free (See “ITEM 10.E: Additional Information—Taxation—Israeli tax considerations and government programs—Law for the Encouragement of Capital Investments, 1959”).

It may be difficult to enforce a U.S. judgment against us, our officers and directors in Israel or the United States, or to assert U.S. securities laws claims in Israel or serve process on our officers and directors.

We are incorporated in Israel. Other than one director, none of our directors, or our independent registered public accounting firm, is a resident of the United States. None of our executive officers is resident in the United States. The majority of our assets and the assets of these persons are located outside the United States. Therefore, it may be difficult for an investor, or any other person or entity, to enforce a U.S. court judgment based upon the civil liability provisions of the U.S. federal securities laws against us or any of these persons in a U.S. or Israeli court, or to effect service of process upon these persons in the United States. Additionally, it may be difficult for an investor, or any other person or entity, to assert U.S. securities law claims in original actions instituted in Israel. Israeli courts may refuse to hear a claim based on a violation of U.S. securities laws on the grounds that Israel is not the most appropriate forum in which to bring such a claim. Even if an Israeli court agrees to hear a claim, it may determine that Israeli law and not U.S. law is applicable to the claim. If U.S. law is found to be applicable, the content of applicable U.S. law must be proved as a fact, which can be a time-consuming and costly process. Certain matters of procedure will also be governed by Israeli law. There is little binding case law in Israel addressing the matters described above.

Your rights and responsibilities as our shareholder will be governed by Israeli law which may differ in some respects from the rights and responsibilities of shareholders of United States corporations.

Since we are incorporated under Israeli law, the rights and responsibilities of our shareholders are governed by our articles of association and Israeli law. These rights and responsibilities differ in some respects from the rights and responsibilities of shareholders in U.S.-based corporations. In particular, a shareholder of an Israeli company has a duty to act in good faith and in a customary manner in exercising its rights and performing its obligations towards the company and other shareholders and to refrain from abusing its power in the company, including, among other things, in voting at the general meeting of shareholders on certain matters, such as an amendment to the company’s articles of association, an increase of the company’s authorized share capital, a merger of the company and approval of related party transactions that require shareholder approval. A shareholder also has a general duty to refrain from discriminating against other shareholders. In addition, a controlling shareholder or a shareholder who knows that it possesses the power to determine the outcome of a shareholders’ vote or to appoint or prevent the appointment of an office holder in the company or has another power with respect to the company, has a duty to act in fairness towards the company. However, Israeli law does not define the substance of this duty of fairness. See “ITEM 6.C: Directors, Senior Management and Employees—Board Practices—Board Practices—Fiduciary duties and approval of specified related party transactions under Israeli law—Duties of shareholders.” Additionally, the parameters and implications of the provisions that govern shareholder behavior have not been clearly determined by the Israeli courts. These provisions may be interpreted to impose additional obligations and liabilities on our shareholders that are not typically imposed on shareholders of United States corporations.

These provisions of Israeli law could have the effect of delaying or preventing a change in control and may make it more difficult for a third party to acquire us or our shareholders to elect different individuals to our board of directors, even if doing so would be beneficial to our shareholders, and may limit the price that investors may be willing to pay in the future for our ordinary shares.

Under the Israeli Economic Competition law (formerly, the Restrictive Trade Practices Law, 1988) (the “Israeli Competition Law”), a company that either supplies more than 50% of any asset or service in Israel or, in some cases, in a specific geographical area in Israel, or holds significant market power in a relevant market, is deemedsubject to be a monopoly. The determination of monopoly status depends on an analysis of the relevant product or service market, but it does not require a positive declaration, and the status is achieved by virtue of such market share threshold being crossed or the existence of market power.

If we do not manage our inventory effectively, our results of operations could be materially adversely affected.

We must manage our inventory effectively in order to meet the demand for our products. If our forecasts for any Specific Stock Keeping Unit (“SKU”) exceed actual demand, we could experience excess inventory, resulting in increased logistic costs. If we ultimately determine that we have excess inventory, we may have to reduce our prices and write-down inventory which could have an adverse effect on our business, financial condition and results of operations. If we have insufficient inventory levels, we may not be able to respond to the market demand for our products, resulting in reduced sales and market share.

We depend on our senior management team and other skilled and experienced personnel to operate our business effectively, and the loss of any of these individuals could materially and adversely affect our business and our future financial condition or results of operations.

We are dependent on the skills and experience of our senior management team and other skilled and experienced personnel. These individuals possess strategic, managerial, sales, marketing, operational, manufacturing, logistical, financial and administrative skills that are important to the operation of our business. During 2021There have been, and from time to time, there may continue to be, changes in our management team resulting from the hiring or departure of executives and key employees, or the transition of executives within our business. For example, Mr. Shiran replaced Yuval Dagim as our Chief Executive Officer on March 16, 2023, and six of our current 14 members of the management team have joined since such date. Such changes and transitions in our executive management team may divert resources and focus away from the operation of our business. Furthermore, in recent years we have experienced a significant increasetrend of relatively high turnover in turnover across our operationssome sites and challenges in recruiting and retaining employees as labor markets change around the world post-COVID-19.

Retention of institutional knowledge and the ability to attract, motivate and retain personnel, as well as the ability to successfully onboard our senior management as a team comprised of several new members, are crucial for implementing our business strategy, without which our business and our future financial condition or results of operations could suffer materially and adversely. We do not carry key man insurance with respect to any of our executive officers or other employees. We cannot assure you that we will be able to retain all our existing senior management personnel and key personnel or to attract additional qualified personnel when needed.

The market for qualified personnel is competitive in the geographies in which we operate. Moreover, the COVID-19 pandemic has also caused a shift to virtual or hybrid recruiting and employment, which has increased the difficulty in timely attracting new employees, integrating, and introducing them into our corporate culture and retaining them for the longer term. Companies with whom we compete have expended and will likely continue to expend more resources than we do on employee recruitment and are often better able to offer more favorable compensation and incentive packages than we can. We seek to retain and motivate existing personnel through our compensation practices, company culture, and career development opportunities. If we are unable to attract and retain qualified personnel when and where they are needed, our ability to operate and grow our business could be impaired. Moreover, if we are not able to properly balance investment in personnel with sales, our profitability may be adversely affected.

In addition, factors beyond our control may damage or disrupt the ability of our senior management or key employees to perform their critical roles in the Company. In particular, the ongoing COVID-19 pandemic may affect the health and livelihood of our management and employees. The pandemic has led governments in the jurisdictions in which we operate, including the location of our headquarters and manufacturing facilities, to implement reductions in onsite workforce, travel restrictions and individual quarantines. Such limitations may lead to significant changes in the operations of our business, such as reduction in number of shifts at our plants, reduced sales activity and lack of back office support, and materially adversely affect our business and financial condition. See also “—The COVID-19 pandemic could further impact end-consumers and the global economy in general, lower demand for our products, disrupt our operations and materially and adversely affect our business and financial results” and “—Disturbances to our operations or the operations of our suppliers, distributors, customers, consumers or other third parties could materially adversely affect our business.”

Labor shortages and increased turnover or increases in employee and employee-related costs could have adverse effects on our profitability.

We have recently experienced increased difficulties in recruitment at some of our production facilities and other locations. While we have historically experienced some level of ordinary course turnover of employees, the COVID-19 pandemic and resulting actions and impacts have exacerbated labor shortages and increased turnover. A number of factors have had and may continue to have adverse effects on the labor force available to us, including reduced employment pools, unemployment subsidies, including unemployment benefits offered in response to the COVID-19 pandemic, and other government regulations, which include laws and regulations related to workers’ health and safety, and wage and hour practices. Labor shortages and increased turnover rates within our team members have led to and could in the future lead to increased costs, such as increased overtime to meet demand and increased wage rates to attract and retain employees and could negatively affect our ability to efficiently operate our production facilities or otherwise operate at full capacity. An overall or prolonged labor shortage, lack of skilled labor, increased turnover or labor inflation could have a material adverse impact on our operations, results of operations, liquidity or cash flows.

ITEM 4: Information on the Company

| A. | History and Development of the Company |

Our History

Caesarstone Ltd. was founded in 1987 and incorporated in 1989 in the State of Israel. We began as a leading manufacturer of high-end quartz based engineered surfaces used primarily as countertops in residential and commercial buildings, and we are now a global multi material, multi-application designer, producer, and reseller of countertops.surfaces. We design, develop produce and source engineered quartz,stone, natural stone and porcelain products that offer aesthetic appeal and functionality through a distinct variety of colors, styles, textures, and finishes used primarily as countertops surfaces, vanities, and other interior and exterior spaces.

Our products are currently sold in over 5060 countries through a combination of direct sales in certain markets performed by our subsidiaries and indirectly through a network of independent distributors in other markets. We acquired the businesses of our former Australian, Canadian, U.S. and Singaporean distributors, and established such businesses within our own subsidiaries in such countries. In March 2012, we listed our shares on the Nasdaq Global Select Market. In 2017, we started selling our products in the U.K. directly through our U.K. subsidiary, Caesarstone (UK) Ltd. In October 2020, we acquired a majority stake in Lioli, an India-based producer of porcelain slabs, which also sells its porcelain products in India and other markets. In December 2020, we acquired Omicron, a premier stone supplier which operated several locations across Florida, Ohio, Michigan, and Louisiana. We now generate a substantial portion of our revenues in the United States, Australia, and Canada from direct distribution of our products. In addition,July 2022, we also acquired our distributor in October 2020,Sweden and established Caesarstone Scandinavia.

During 2023, our manufacturing network has been undergoing restructuring, with the focus of optimizing our global production footprint. As part of this strategic plan, we acquired a majority stakeshifted our focus from production activities and discontinued production operations in Lioli, an India-based producer of porcelain slabs, which also sells its porcelain products in Indiaour Sdot Yam, Israel, and other markets.Richmond Hill, GA, USA, production facilities.

We are a company limited by shares organized under the laws of the State of Israel. We are registered with the Israeli Registrar of Companies in Jerusalem. Our registration number is 51-143950-7. Our principal executive offices are located at Kibbutz Sdot-Yam, MP Menashe, 3780400, Israel, and our telephone number is +972 (4) 610-9368. We have irrevocably appointed Caesarstone USA as our agent for service of process in any action against us in any United States federal or state court. The address of Caesarstone USA is 1401 W. Morehead Street, Suite 100, Charlotte, NC, 28208. The SEC maintains an internet site at http:/www.sec.gov that contains reports and other information regarding issues that file electronically with the SEC. Our securities filings, including this annual report and the exhibits thereto, are available on the SEC’s website. For more information about us, our website is www.caesarstone.com. The information contained in, or connected with, our SEC filings on the SEC internet site and our website shall not be deemed to be incorporated by reference in this annual report.

Principal Capital Expenditures

Our capital expenditures for fiscal years 2021, 20202023, 2022 and 20192021 amounted to $31.5$11.2 million, $19.8$17.8 million, and $23.6$31.5 million, respectively. The majority of our investment activities have historically been related to the purchase of manufacturing equipment and components for our production lines. For additional information on our capital expenditures, see “ITEM 5.B: Liquidity and Capital Resources–Capital expenditures.”

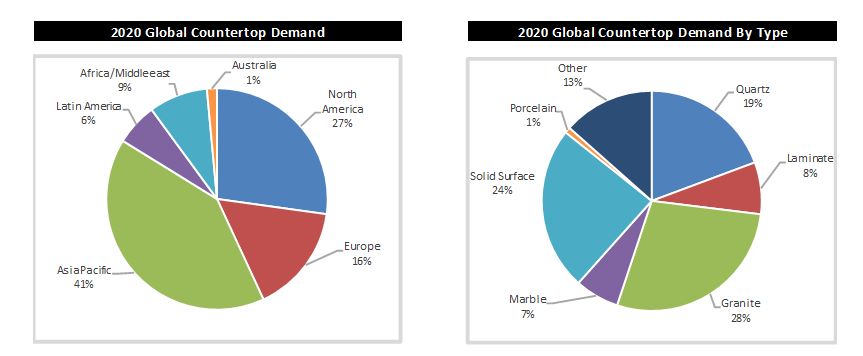

We are a multi material designer, producer and reseller of countertops used in residential and commercial buildings globally. Based on the Freedonia Report The global countertop industry generated approximately $117$160.6 billion in sales to end consumers in 20202022 based on average installed price, which includes fabrication, installation and other service relatedservice-related costs, as per the following charts:

The majority of our sales are at the wholesale level to fabricators and distributors and exclude fabrication, installation and other service relatedservice-related costs.

The engineered quartz countertop is a growing category in the countertop market and continues to take market share from other materials, such as granite, manufactured solid surfaces and laminate. Between 1999 and 2020,2022, global engineered quartz sales to end-consumers grew at a compound annual growth rate of 16.6%16.2% compared to a 5.0%6.0% compound annual growth rate in total global countertop sales to end-consumers during the same period. FollowingIn 2022, we successfully launched the Lioli Acquisition, we intend to commence marketing and sales of porcelain countertops under ourthe Caesarstone brand.brand following the Lioli Acquisition. Porcelain represents one of the fastest growing categories in the global countertop market.market and between 20142016 and 2020,2022, the porcelain sales to end-consumers grew at a compound annual growth rate of 14.9%36%.

In recent years, quartz penetration rate, by volume, other than in Israel, increased in our key markets, as detailed in the following chart:

Quartz penetration in our key markets

| | | For the year ended December 31, | |

| For the year ended December 31, | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Region | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| United States | | | 20 | % | | | 14 | % | | | 8 | % | | | 6 | % | | | 5 | % | | | 21 | % | | | 20 | % | | | 14 | % | | | 8 | % | | | 6 | % |

| Australia (not including New Zealand) | | | 47 | % | | | 45 | % | | | 39 | % | | | 35 | % | | | 32 | % | | | 48 | % | | | 47 | % | | | 45 | % | | | 39 | % | | | 35 | % |

| Canada | | | 28 | % | | | 24 | % | | | 18 | % | | | 12 | % | | | 9 | % | | | 27 | % | | | 28 | % | | | 24 | % | | | 18 | % | | | 12 | % |

| Israel (*) | | | 67 | % | | | 87 | % | | | 86 | % | | | 85 | % | | | 82 | % | | | 53 | % | | | 67 | % | | | 87 | % | | | 86 | % | | | 85 | % |

(*) In Israel, quartz lost market share mainly to porcelain, which increased its market share from a de-minimis rate in 2016 to over 20%34% in 2020, a trend we estimate continued thorugh 2022.

Our products consist primarily of engineered quartz,stone fabrication and installation related services, natural stone and porcelain slabs that are currently sold in over 5060 countries through a combination of direct sales in certain markets and indirectly through a network of independent distributors in other markets. Our products are primarily used as indoor & outdoor kitchen countertops in the renovation and remodeling and residential construction end markets. Other applications for our products include vanity tops, back splashes, furniture, and other interior and exterior surfaces that are used in a variety of residential and non-residential applications. High quality engineered quartzstone offers durability, non-porous characteristics, superior scratch, stains and heat resistance levels, making it durable and ideal for kitchen and other applications relative to competing products such as granite, manufactured solid surfaces and laminate. Porcelain is characterized by its hardness and its stain resistance, as well as extreme heat and UV resistance. Through our design and manufacturing processes we can offer a wide variety of compositions, colors, styles, designs, and textures.

From 2010 to 2021,2023, our revenue grew at a compound annual growth rate of 11.3%8.4%. From 20202022 to 2021,2023, our revenue increaseddecreased at an annual rate of 32.4%18.2%. In 2021,2023, we generated revenue of $643.9$565.2 million, net incomeloss of $107.7 million attributable to controlling interest, which included a one-time non-cash impairment charge of $47.9 million, an adjusted EBITDA loss of $9.4 million and adjusted net loss attributable to controlling interest of $19.0 million, adjusted EBITDA of $68.2 million and adjusted net income attributable to controlling interest of $28.6$46.4 million. Adjusted EBITDA and adjusted net income attributable to controlling interest are non-GAAP financial measures. See “ITEM 8.B: 4.B: Information on the Company—Business Overview—Non-GAAP Financial Measures” below for a description of how we define adjusted EBITDA and adjusted net income attributable to controlling interest and reconciliations of net income to adjusted EBITDA and net income attributable to controlling interest to adjusted net income attributable to controlling interest.

Not as projected by the Freedonia report, our primary markets, and potentially engineered stone penetration have slowed down during 2023, which we believe is attributable to macroeconomics with higher global interest rates and inflation, as well as uncertainties relating to the changes in the Australian market that may further affect the realization of such projections during 2024.

Our Products

Our products are generally marketed under the Caesarstone brand. Currently, our porcelain products manufactured in India are marketed either under the Caesarstone brand, mainly for counter-top applications in selected markets, and under the existing Lioli brand mainly for flooring and cladding applications. Most of our engineered stone and ceramicPorcelain products are installed as countertops in residential kitchens. Other applications of our products include vanity tops, back splashes, and exterior surfaces.surfaces for outdoor kitchens. In addition, we sell natural stone, sinks and various ancillary fabrication tools and materials. Our standard size engineered quartzstone slabs constituting the majority of our products measure 120 inches long by 56 1/2 inches wide, andwith a thickness option of 1/2, 3/4, or 1 1/4 inches. Our jumbo slabs, constituting the majority of our products, measure 131 1/2 inches long by 64 1/2 inches wide, for the jumbo slabs, with a thickness of 1/2 of an inch, 3/4 of an inch or 1 1/4 inches, and 3/4 of an inch or 1 1/4 inches for the jumbo slabs.inches. On average engineered quartzstone surfaces are comprised on average of 85% quartzminerals blended with polyester, and pigments. Our engineered quartzstone products’ manufacturing processes and composition gives them superior strength and resistance levels to heat impact, scratches, cracks and chips. Polyester, which acts as a binding agent in our engineered quartz products, make such products non-porous and highly resistant to stains. Pigments act as a dyeing agent to vary our products’ colors and patterns. Our standard size porcelain countertop slabs measure 126 inches long by 63 inches wide, 9494.5 inches long by 47 inches wide and 47 inches by 47 inches mm, with a thickness of 1/2 inches, 1/3 inches and 1/4 inches, in a range of matt and polished finishes. Porcelain surfaces are typically comprised of clay minerals, natural minerals, and chemical additives, and offer non-porous characteristics as well as scratch and heat resistance.

We design our products with a wide range of colors, finishes, textures, thicknesses, and physical properties, which help us meet the different functional and aesthetic demands of end-consumers. Our designs range from fine-grained patterns to coarse-grained color blends with a variegated visual texture. Through offering new designs, we capitalize on Caesarstone’s brand name and foster our position as a leading innovator in the counter-top space.

Our product offerings consist of foura few collections (Classico, Supernatural, Metropolitan, Outdoor and recently Porcelain), each of which is designed to have a distinct aesthetic appeal. We use a multi-tiered pricing model across our products and within each product collection ranging from lower price points to higher price points. Each product collection is designed, branded, and marketed with the goal of reinforcing our products’ premium quality.

We introduced our original product collection, Classico, in 1987, and today, this collection still generates more revenue than our other collections.1987. Launched in 2012, our Supernatural collection, which is marketed as specialty high-end, offers designs inspired by natural stone and which are manufactured using proprietary technology. In 2018, we launched our new Metropolitan collection, inspired by the rough and unpolished textures found in industrial architecture. In 2020, we introduced our Outdoor collection, an innovative product category, which comprises stain resistant easy-to-clean surfaces, made of a highly durable material, proven to withstand UV-rays and the most extreme environmental conditions over a long term, intended for use in outdoor cookingkitchens spaces. Following the Lioli Acquisition we began offering porcelain products as well for countertops as well as flooring and cladding applications.

We regularly introduce new colors and designs to our product collections based on consumer trends. We offer over 70 different colors of quartzengineered stone products, with five textures and three thicknesses generally available for each collection. Each year we typically introduce between four to eight new colors and models.

In 2018, we began to offer porcelain slabs sourced through OEMs and following the Lioli Acquisition, from Lioli as well.

In addition, following the Omicron Acquisition, we now offer to our customers in the United States resale of natural stone, as well as various ancillaries and fabrication and installation accessories.

A key focus of our product development is a commitment to substantiating our claim of our products’ superior quality, strength, and durability. Our products undergo regularongoing tests for durability and flexural strength internally by our internal laboratory operations group and by external accreditation laboratories and organizations. Products in our portfolio are accredited by organizations overseeing safety, Food contact and environment performance, such as the NSF International and GREENGUARD Indoor Air Quality. Generally, our products support green building projects and allow contractors to receive Leadership in Energy and Design (“LEED”) points for projects incorporating our products.

Distribution

Our four largest markets based on sales are currently the United States, Australia (including New Zealand), Canada and Israel. In 2021,2023, sales of our products in these markets accounted for 47.4%48.1%, 18.4%18.8%, 13.1%13.4% and 6.1%4.2% of our revenues, respectively. Total sales in these markets accounted for 85.1%84.2% of our revenues in 2021.2023. For a breakdown of revenues by geographic market for the last three fiscal years, see “ITEM 5.A: Operating Results and Financial Review and Prospects—Operating Results.”

Direct Markets

We currently have direct sales channels in the United States, Australia, Canada, Israel, the United Kingdom (“U.K.”), Sweden (Scandinavia), India, and Singapore. Our direct sales channels allow us to maintain greater control over the entire sales channel within a market. As a result, we gain greater insight into market trends, receive feedback more readily from end-consumers, fabricators, architects and designers regarding new developments in tastes and preferences, and have greater control over inventory management. Our subsidiaries’ warehouses in each of these countries maintain inventories of our products and are connected to each subsidiary’s sales department. We supply our products primarily to wholesalers, resellers and fabricators, who in turn resell them to contractors, developers, builders and consumers, who are generally advised by architects and designers. In certain market channels in the U.S., Canada Israel and Australis,Australia, we also provide, together with our products, fabrication and installation services, which we source from third party fabricators. We believe that our supply of a fabricated and installed Caesarstone countertop is a competitive advantage in such channels, which enables us to better control our products’ prices as well as to promote a full solution to our customers, while in some of these cases our products are sold under different brands.

In Israel, whereDuring the second half of 2022, we made changes to our headquarters are located, we distribute our products directly to several local distributors who in turn sell them to fabricators. This arrangement reduces our financial exposure and simplifies our logisticsdistribution strategic in the Israeli market.market, and began selling directly to major fabricators, in addition to selling through a handful of local distributers Although we still sell our products to distributors in this market, we consider this a direct market due to the warranty we provide to end-consumers, as well as our fabricator technical and health and safety instruction programs and our local sales and marketing activities. In the United States, Australia, Canada, the United Kingdom, Sweden (Scandinavia) and Singapore we have established direct distribution channels with distribution locations in major urban centers complemented by arrangements with various third parties, sub-distributors or stone suppliers in certain areas of the United States.

Indirect Markets

We distribute our products in other territories in which we do not have a direct sales channel through third-party distributors, who generally distribute our products to fabricators on an exclusive or non-exclusive basis in a specific country or region. Fabricators sell our products to contractors, developers, builders and consumers. In some cases, our distributors operate their own fabrication facilities. Additionally, our distributors may sell to sub-distributors located within the territory who in turn sell to fabricators.

In most cases, we engage one or more distributors to serve a country or territory. Today, we sell our products in over 4550 countries through third-party distributors, and to over 5060 countries in total. Sales to third-party distributors in such indirect markets accounted for approximately 10%11% of our revenues in 2021.2023. This strategy often allows us to accelerate our penetration into multiple new markets. Our distributors typically have prior stone surface experience and close relationships with fabricators, builders and contractors within their respective territory.

We work closely with our distributors to assist them in preparing and executing a marketing strategy and comprehensive business plan. Ultimately, however, our distributors are responsible for the sales and marketing of our products and providing technical support to their customers within their respective territories. To assist some of our distributors in the promotion of our brand in these markets, we provide marketing materials and in certain cases, monetary participation in marketing activities. Our distributors devote significant effort and resources to generating and maintaining demand for our products along all levels of the product supply chain in their territory. To this end, distributors use our marketing products and strategies to develop relationships with local builders, contractors, developers, kitchen and bath retailers, architects and designers. Certain distributors, as well as sub-distributors, do not engage in brand promotion activities and their activities are limited to sales promotion, warehousing and distributing to fabricators or other customers.

We do not control the pricing terms of our distributors’distributors or sub-distributors’ sales to customers.customers, nor do we control their purchasing and inventory policy. As a result, prices for our products may vary.vary and their inventory policies may affect their purchases.

Sales and Marketing

Sales

We manufacture or source our products based upon our rolling projections of the demand for our products.

SinceFrom 2019 and through 2023, we have operated under a regional structure which consists of North America, APAC, EMEA and Israel. Under this structure,Commencing 2024 each region managesof our subsidiaries is responsible for its direct revenues, with the directresponsibility of the majority of third-party distribution channels and focuses on penetrating new markets within its territory, as well as further develops its key growth indirect sales markets.partners handled by our Rest of World team.

We believe our products still have significant growth opportunities in the United States, Canada and Europe. For information on sales trends in the markets in which we operate, see “ITEM 5: Operating and Financial Review and Prospects—Components of statement of income”. In 2016, we established a direct sales channel in the United Kingdom and starting in January 2017 we have been selling and distributing our products in the U.K. directly through our U.K. subsidiary. In December 2020, we acquired Omicron, a premier stone supplier servicing the Florida, Ohio, Michigan, and Louisiana markets in the U.S. In July 2022, we acquired a leading distributor in Sweden, establishing first direct Go-To-Market presence in E.U. under Caesarstone Scandinavia AB. We intend to continue to invest resources to further strengthen and increase our penetration in our existing markets. We are also exploring alternative sales channels and methodologies to further enhance our presence in each market.

Marketing

We position our engineered quartz,stone, porcelain and natural stone surfaces as premium branded products in terms of their designs, quality and pricing. Through our marketing, we seek to convey our products’ ability to elevate the overall design and quality of an entire kitchen or other setting. Our marketing strategy is to deliver this message every time our end-consumers, customers, fabricators, architects and designers meet our brand. We also aim to communicate our position as a design-oriented global leader in engineered surfaces innovation and technology.

The goal of our marketing activities is to drive marketing and sales efforts across the regions, while creating demand for our products from end-consumers, kitchen and bath retailers, fabricators, contractors, architects and designers, which we refer to as a “push-and-pull demand strategy.” We combine both pushing our brand and products through all levels of the product supply chain while generating demand from end-consumers as a complementary strategy.

We implement a multi-channel marketing strategy in each of our territories and market not only to our direct customers, but to the entire product supply chain, including fabricators, developers, contractors, kitchen retailers, builders, architects and designers. We use multipleSuch marketing channels includinginclude, among others: advertisements in home interior magazines and websites, the placement of our display stands and sample books in kitchen retails stores and our company’s website and social media presence. We share professional knowledge with fabricators about our products and their capabilities, installation methods and safety requirements through manuals, seminars and webinars. In addition, our “Master of Stone” program operates as an online training platform, with content aimed at educating fabricators on the topics of Health & Safety, professional know-how and added value content for fabrication plant managers and making safety and professional working guidelines accessible to our fabricators worldwide.

Our marketing materials are developed by our global marketing department in Israel and are used globally.globally, in addition to local marketing initiatives in the regions. In 2021,2023, we spent $15.3$15.7 million on direct advertisingmarketing and promotional activities.

Our digital platforms’ websites are a key part of our marketing strategy enabling us to create data-driven personal relationship,relationships, on and off site, in order to increase engagement and conversion to sale. Our websites enable our business partners, customers and end-consumers to view currently available designs, photo galleries of installations of our products in a wide range of settings, instructions with respect to the correct usage of our products and offer an innovative cutting-edge experience with rich content and interactive tools to empower and guide consumers at any stage of their renovation journey. We also conduct marketing activity in the social media arena mainly to increase our brand awareness among end-consumers, architects and designers.

During 2020, we opened a new Israeli showroom named “Caesarstone Concept House” where we introduced innovative technology-driven consumer experience.

We also seek to increase awareness of our brand and products through a range of other methods, such as trade shows, home design shows, design competitions, media campaigns and through our products’ use in high profile projects and iconic buildings. In recent years, we have collaborated with renowned designers, who created exhibitions and particles from our products. Our design initiatives attracted press coverage around the world.

Research and Development

Our research and development (“R&D”) department is primarily located in Israel. As of December 31, 2021,2023, our corporate R&D department was comprised of 1619 employees, all of whom have extensive experience in engineered quartzstone and porcelain surface manufacturing, polymer science, engineering, product design and engineered quartz surfacesurfaces applications. In addition, our R&D for porcelain manufacturing is conducted by eight dedicated employee located in India. In 2021,2023, R&D costs accounted for approximately 0.7%0.9% of our revenues.

The strategic mission of our R&D team is to develop and maintain innovative and leading technologies and top-quality designs, develop new and innovative products according to our marketing department’s roadmap, increase the cost-effectiveness of our manufacturing processes and raw materials, and generate and protect company intellectual property in order to enhance our position in the engineered quartzstone surface industry. We also study and evaluate consumer trends by attending industry exhibitions and hosting international design workshops with market and design specialists from various regions.

Customer Service

We believe that our ability to provide outstanding customer service is a strong competitive differentiator. Our relationships with our customers are established and maintained through the coordinated efforts of our sales, marketing, production and customer service personnel. In our direct markets, the warranty period varies. We provide end-consumers with various warranties depending on the relevant markets ranging from a ten-year limited warranty to limited lifetime warranties in selected markets such as the United States, Canada and Israel. In our indirect markets, end-consumers, warranty issues on our products are addressed by our local distributor. We provide all our distributors with a limited direct manufacturing defect warranty and our distributors are responsible for providing warranty coverage to end-customers. The warranties provided by our distributors vary in term. In our direct markets, following an end-consumer call, our technicians are sent to the product site within a short time. We provide readily accessible resources and tools regarding the fabrication, installation, care and maintenance of our products. We believe our comprehensive global customer service capabilities and the sharing of our service-related know-how differentiate our company from our competitors.

Raw Materials and Service Provider Relationships

Quartz,Minerals, clay, polyester and pigment are the primary raw materials used in the production of our engineered quarts products.surfaces. We acquire raw materials from third-party suppliers. Suppliers ship raw materials for our engineered quartzstone products and porcelain to our manufacturing facilities in Israel and the U.S.India primarily by sea. Our raw materials are generally inspected at the suppliers’ facilities and upon arrival at our manufacturing facilities in Israel and the U.S. The cost of our raw materials consists of the purchase prices of such materials and costs related to the logistics of delivering the materials to our manufacturing facilities. Our raw materials costs are also impacted by changes in foreign currency exchange rates.

Quartz is theMinerals are our main raw material component used in our engineered quartzsurface products. Raw quartzminerals must be processed into finer grades of sand and powder before we can use itthem in our manufacturing process. We purchase quartzminerals from our quartz suppliers after it was already processed by them.some process. We acquire quartzminerals from suppliers primarily in Turkey, Belgium, India, Portugal, the U.S. and Israel. In 2021,2023, approximately 62%69% of our quartz,minerals, including mainly quartzite, which is used across all of our engineered quartzstone products, was imported from several suppliers in Turkey. Approximately 40%63% of the imported quartzminerals from Turkey (or 25%44% of our total quartz) wasdirect mineral consumption) were acquired from Mikroman Madencilik San ve TIC.LTD.STI (“Mikroman”) and approximately 33%32% of the imported quartz from Turkey (or 20%22% of our total quartz) wasmineral consumption) were acquired from Polat Maden Sanayi veEkom Eczacibasi Dis Ticaret A.SA.Ş. (“PolatEkom”). Our current supply arrangementsIn light of market volatility and our changing raw material needs, while we have long lasting mutually beneficial relationships with Polatour suppliers, we do not currently have an annual framework agreement in place and Mikroman are set forth in letter agreements.purchasing materials from them based on spot purchase orders.

Similar to our arrangements with Mikroman and PolatEkom described above, we typically transact business with ourother quartz suppliers on an annual framework basis, under which weand execute purchase orders from them from time to time. Quartz imported from Turkey, Europe and Israel for our U.S. manufacturing facility entails higher transportation costs.

In most cases, we acquire polyester from several suppliers, on an annual framework basis or purchase order basis based on our projected needs for the subsequent one to three months. Typically, suppliers are unwilling to agree to preset prices for periods longer than a quarter and suppliers’ prices may vary during a quarter as well.

Pigments for our engineered quartzstone production in Israel are purchased from Israel and suppliers abroad. Pigments for our U.S. engineered quartzstone production are primarily purchased from U.S. vendors.

The principal raw materials for our porcelain products are clay minerals (such as Ukraine clay bentonite), natural minerals (such asand feldspar) and chemical additives. While we acquire feldspar locally from Indian suppliers, Ukraine clay and bentonite are imported from the relevant regions. We typically transact business with our suppliers of raw materials for porcelain products on an annual framework basis, under which we execute purchase orders from time to time.

Our strategy is to maintain, whenever practicable, multiple sources for the purchase of our raw materials to achieve competitive pricing, provide flexibility and protect against supply disruption.

See “ITEM 3.D. Key Information—Risk Factors—We may encounter significant delays in manufacturing if we are required to change the suppliers for the raw materials used in the production of our products.” For our cost of raw materials in 20212023 and prior years, see “ITEM 5.A: Operating Results and Financial Review and Prospects—Operating Results—Cost of revenues and gross profit margin.”

Manufacturing and Facilities

OurFollowing the closure of our Sdot-Yam and Richmond-Hill facilities during 2023, our products are now manufactured at our fourtwo manufacturing facilities located in Kibbutz Sdot-Yam in central Israel, Bar-Lev Industrial Park in northern Israel, Richmond Hill, Georgia in the U.S. and following the Lioli Acquisition, in Morbi, Gujarat in India. Our Sdot-Yam facility includesIndia and by our first two production lines.third party PBP partners. We completed our Bar-Lev manufacturing facility in 2005, which included our then third production line, and we established our fourth production line at this facility in 2007 and our fifth production line at this facility in 2013. We completed our U.S. manufacturing facility in 2015, where we began to operate our sixth production line in the second quarter of 2015 and our seventh line in the fourth quarter of 2015. In addition to a $135 million as an initial investment, we have the option to further invest and expand in Richmond Hill to accommodate additional manufacturing capacity in the future as needed to satisfy potential demand. During 2020, in response to the pandemic impact on our business we reduced the utilization of our production facilities in Israel and the U.S and currently we are still only partially utilizing our U.S. production facility. As part of the Lioli Acquisition, in 2020 we acquired a porcelain slab manufacturing facility, which is comprised of one production line currently in operation.

Finished slabs are shipped from our facilities in Israel and the U.S.India, or from our PBP, to our distribution centers worldwide, directly to customers and to third-party distributors worldwide. Finished porcelain slabs manufactured at our Morbi facility are distributed via third-party distributors and are shipped from Indiaor directly to customers worldwide. For further discussion of our facilities, see “ITEM 4.D: Information on the Company—Property, plants, and equipment.”

The manufacturing process for our engineered quartz products typically involves the blending of quartzminerals (85% on average) with polyester and pigments. Using machinery acquired primarily from Breton, the leading supplier of engineered stone manufacturing equipment, together with our proprietary manufacturing enhancements, this mixture is compacted into slabs by a vacuum and vibration process. The slabs are then moved to a curing kiln where the cross-linking of the polyester is completed. Lastly, the slabs are gauged, calibrated and polished to enhance shine.

The manufacturing process for our porcelain products typically involves blending of clay, natural minerals (such as feldspar) and chemical additives required for the shaping process. The multi-ingredient mixture is fed to a ball mill, together with water, to achieve fine grinding. The excess water is then removed, and the resulting powder is shaped into slabs. Slabs are first moved to dryers and then passed through a glaze line, where they are decorated with different applicators. Decorated slabs are passed through digital printing machines and then go into a curing kiln for the final firing process. Lastly, the slabs are gauged, calibrated and polished to enhance shine.

We maintain strict quality control and safety standards for our products and manufacturing process.processes both in our facilities as well as with our PBP. Our manufacturing facilities have severalfacility in Israel holds ISO45001 safety certifications from third-party organizations, including an OHSAS 18001 safetyThe Standards Institution of Israel, while our facility in India, is in the process of obtaining the same certification from the International Quality Network for superior manufacturing safety operations.TUV).

In addition, since 2018 we have increased our outsourcing capabilities and currently purchase a certain portion of our product from our PBPs including natural stone, engineered quartz slabs from third-party quartz manufacturers that meet our specifications.stone, porcelain and ancillaries. We conduct quality control and quality assurance processes with respect to such outsourcing of our products. In 2021, OEMs2023, products produced by third parties accounted for less than 10%approximately 22.4% of revenues, and we are aiming to increase purchases from OEMsPBPs in 2022.2024. For more information, see ITEM 3.D: Key Information - Operational Risks.

Seasonality

For a discussion of seasonality, please refer to “ITEM 5.A: Operating and Financial Review and Prospects—Operating Results—Factors impacting our results of operations” and “ITEM 5.A: Operating and Financial Review and Prospects—Operating Results—Quarterly results of operations and seasonality.Seasonality.”

Competition

We believe that we compete principally based upon product quality, breadth of colors and designs offering and innovation, brand awareness and position, pricing and customer service. We believe that we differentiate ourselves from competitors on the basis of our premium brand, our signature product designs, our products and designs innovation, our ability to directly offer our products in major markets globally, our focus on the quality of our product offerings, our customer service-oriented culture, our high involvement in the product supply chain and our leading distribution partners.

The dominant surface materials used by end-consumers in each market vary. Our products compete with a number of other surface materials as well as similar materials offered by other producers and re-sellers. The manufacturers of these products consist of a number of regional as well as global competitors. Some of our competitors may have greater resources than we have and may adapt to changes in consumer preferences and demand more quickly, expand their materials offering, devote greater resources to design innovation and establishing brand recognition, manufacture more versatile slab sizes and implement processes to lower costs.

The engineered quartzstone and porcelain surface market is highly fragmented and is also served by a number of regional and global competitors. We also face growing competition from low-cost manufacturers from Asia and Europe. Large multinational companies have also invested in their engineered quartzstone and porcelain surface production capabilities. For more information, see “ITEM 3.D. Key Information—Risk Factors—We face intense competitive pressures from manufacturers of other surface materials, which could materially and adversely affect our results of operations and financial condition” and “ITEM 3.D. Key Information—Risk Factors—Competition from manufacturers of lower priced products may reduce our market share, alter consumer preferences and materially and adversely affect our results of operations and financial condition”.

Information Technology Systems

We believe that an appropriate information technology infrastructure is important in order to support our daily operations and the growth of our business.

We implemented various IT systems to support our business and operations. Our Enterprise Resource Planning (“ERP”) software enables us to manage our day-to-day business activities and provides us with accessible quality data that support our forecasting, planning and reporting. Accurate planning is important in order to support sales and optimize working capital and cost as our products can be built in a number of combinations of sizes, colors, textures and finishes. Given our global expansion, we implemented a global ERP based on an Oracle platform. Our MES systems manage work processes on the production floor in our facilities and Salesforce enhances our Customer Relationship Management (“CRM”) infrastructure.

We are implementing a digital transformation withindigitalization across our organization to better streamline processes and support our business strategy. We continuedare investing in our digital transformation projects for betterto enhance consumer engagement and customer experience. Our technological and digital investments will be geared towards operational enhancements in inventory management and production, along with transforming our go-to-market tools. We seek to update our IT infrastructure to enhance our ability to prevent and respond to cyber threats and conduct trainingtrainings for our employees in this respect. For further details, see “ITEM 3.D. Key Information—Risk Factors—Disruptions to or our failure to upgrade and adjust our information technology systems globally, may materially impair our operations, hinder our growth and materially and adversely affect our business and results of operations.”

Intellectual Property

Our Caesarstone brand is central to our business strategy, and we believe that maintaining and enhancing the Caesarstone brand is critical to expanding our business.

We have obtained trademark registrations in certain jurisdictions that we consider material to the marketing of our products, including CAESARSTONE® and our Caesarstone logo. We have obtained trademark registrations for additional marks that we use to identify certain product collections, as well as other marks used for certain of our products. While we expect our current and future applications to mature into registrations, we cannot be certain that we will obtain such registrations. In many of our markets we also have trademarks, including registered and unregistered marks, on the colors and models of our products. We believe that our trademarks are important to our brand, success and competitive position. In order to mitigate the risk of infringement, we conduct an ongoing review process before applying for registration. However, we cannot be certain that third parties will not oppose our application or that the application will not be rejected in whole or in part. In the past, some of our trademark applications for certain classes of our products’ applications have been rejected or opposed in certain markets and may be rejected for certain classes in the future, in all or parts of our markets, including without limitation, for flooring and wall cladding. We are currently subject to oppositionvarious proceedings with respect toregarding our Caesarstone trademark applications for registration of our trademark Caesarstone in certainvarious jurisdictions.

To protect our know-how and trade secrets, we customarily require our employees and managers to execute confidentiality agreements or otherwise agree to keep our proprietary information confidential. Typically, our employment contracts also include clauses requiring these employees to assign to us all inventions and intellectual property rights they develop in the course of their employment and agree not to disclose our confidential information. We limit access to our trade secrets and implement certain protections to allow our know-how and trade secret to remain confidential.

In addition to confidentiality agreements, we seek patent protection for some of our latest technologies. We have obtained patents for certain of our technologies and have pending patent applications that were filed in various jurisdictions, including the United States, Europe, Australia, Canada, China and Israel, which relate to our manufacturing technology and certain products. No patent application of ours is material to the overall conduct of our business. There can be no assurance that pending applications will be approved in a timely manner or at all, or that such patents will effectively protect our intellectual property. There can be no assurance that we will develop patentable intellectual property in the future, and we have chosen and may further choose not to pursue patents for innovations that are material to our business.

Environmental and Other Regulatory Matters

Environmental and Health and Safety Regulations

Our manufacturing facilitiesfacility and operations in Israel, our manufacturing facility in Georgia, United States and our manufacturing facility in Gujarat, India are subject to numerous Israeli U.S. and Indian environmental and workers’ health and safety laws and regulations, respectively, and our supply chain operations are subject to applicable local laws and regulations. For instance, applicable U.S. laws and regulations include federal, state and local laws and regulations, including Georgia state laws. Laws and regulations in the U.S. and other countries govern, among other things, exposure to pollutants, protection of the environment; setting standards for emissions; generation, treatment, import, purchase, use, storage, handling, disposal and transport of hazardous wastes, chemicals and materials, including sludge; discharges or releases of hazardous materials into the environment, soil or water; permissible exposure levels to hazardous materials; product specifications; nuisance prevention;; soil, water or other contamination from hazardous materials and remediation requirements arising therefrom; and protection of workers’ health and safety.

In addition to being subject to regulatory and legal requirements, our manufacturing facilities in Israel the United States and India operate under applicable permits, licenses and approvals with terms and conditions containing a significant number of prescriptive limits and performance standards. Business licenses for our facilitiesfacility in Israel contain conditions related to a number of requirements, including with respect to dust emissions, air quality, the disposal of effluents and process sludge, and the handling of waste, chemicals and hazardous materials. Subject to certain terms, the business license for our Sdot-Yam plant is in effect until December 31, 2025. The business license for our Bar-Lev plant is in effect until June 30, 2022,2024, and the Company is in the process of seeking an extension. The business license for our U.S. facility is renewed every year subject to a fee paid to the city and county. Our site in India has a Factory License which is a basic license issued by the Inspectorate of Factories, which is in effect until December 31, 2023.2028. The site in India has also obtained a Consent to Operate (the “CTO”) from the State Pollution Control Board, which is a permit issued to any factory in India with all the compliance requirements related to environmental aspects, such as air emission, water and wastewater management, waste management. The CTO is valid until September 28, 2023.2023, and following a renewal process we believe we are to receive an extended CTO in the coming weeks. We operate in Israel under poison permits that regulate our use of poisons and hazardous materials. Our current poison permits are valid until January 202326, 2025, for both our Israeli facilities. In addition, we dispose of wastewater from our Israeli manufacturing facilities to a treatment plant pursuant to permits obtained from the Israeli Ministry of Environmental Protection (“IMEP”), which are effective until March 31, 2022 and the Company is in process of its extension. Our facility in the United States is required to obtain and follow a General Permit for Storm Water Discharges Associated with Industrial Activity of the Georgia Environmental Protection Division (“GEPD”), an air quality permit from GEPD and other requirements and regulations including among others specific limitations on emission levels of hazardous substances, such as styrene, specific limitations on RCS levels inside our plant, allowable wastewater discharge limits, oil spill prevention rule, hazardous waste handling requirements and fire protection measures requirements.Bar-Lev facility. Our site in India is required to comply with all applicable conditions, including with respect to water consumption, wastewater discharge, air emission monitoring and pollution control devices, hazardous wastes storage and disposal, specified in the CTO. We are currently in the process of renewing the plant’s Fire NOC (No Objection Certification), which expired in July 2021 due to a requirement to install a Fire Hydrant system in the entire plant area. In all our manufacturing facilities, we are implementing measures on an ongoing basis in order to achieve and maintain compliance with dust and styrene environmental and occupational emissions standards and to reduce such emissions to minimum thresholds.

Each of these permits, licenses and standards require a significant amount of monitoring, record-keeping and reporting in order for us to demonstrate compliance therewith.

Official representatives of the health and safety and environment authorities in Israel, the States of Georgia and Gujarat visit our facilities from time to time, to inspect issues such as workplace safety, industrial hygiene, monitoring lockout tag out programs, exposure and emissions, water treatment, noise and others. Such inspections may result in citations, penalties, revocation of our business license or limitation or shut down of our facilities’ operations. It may also require us to make further investments in our facilities.

From time to time, we face environmental, and health and safety compliance issues related to our manufacturing facilitiesfacilities:

| • | Emissions - Israel. InOn March 2018 and later on December 2019 the IMEP issued the additional terms to thefor business license for ourthe Bar-Lev facility, which require among others, performing a constant monitoring of styrene emission. Accordingly, weand the Company has implemented all the required terms, including an online styrene emission monitoring system that was installed at our Bar-Lev facility during September 2020.with certain implementing of cyber related requirements underway. The IMEP closely monitors our Bar-Lev facility’s implementation of the additional terms and emissions, specifically of styrene. During July 2021, the Company received a warning letter from the IMEP in which our Bar-Lev plant was notified of violations of the Clean Air Act and the plant’s business license terms, following an unannounced styrene emission sampling that revealed several cases of deviations from the styrene emission standard under the Clean Air Act in Israel. The IMEP has ordered the Company to take corrective and preventive actions, including reducing the expected timeframe for installation of additional Regenerative Thermal Oxidizer (“RTO”) system and to implement a continuous (online) monitoring device on the Bar-Lev plant’s fence. We are cooperating with the IMEP and are currently in the process of implementing all its requirements and remaining additional terms. Similarly, in October 2020 we received fromterms, such process is currently behind schedule, since the IMEP the final version of the additional terms to the business license for our Sdot-Yam facility, which required, among others, implementation of a continuous monitoring of the facility’s styrene emission. Accordingly, we implemented the required terms, including an online styrene emission monitoring system that was installed at Sdot-Yam plant in May 2021. The IMEP closely monitors our Sdot-Yam facility emissions, specifically for its styrene emissions. During January 2021 we were informed of several cases of deviations from the styrene emission standard under the Clean Air Actcurrent geopolitical circumstances in Israel at our Sdot-Yam plant, which were identified in an unannounced continuous monitoring inspection that was conducted onprevents the Sdot-Yam plant’s fence byarrival of experts needed to conclude the municipal supervisory authority. Recently the municipal supervisory authority advised (but did not order) that a continuous monitoring system on the Sdot-Yam plant’s fence should be installed, and that advice is being reviewed.project. In February 2022, Israel adopted a long termlong-term goal for the reduction of environmental styrene emissions. Although such goal is not expected to impact our current operations, the adoption of new regulations could create an additional burden for any future investment in our Israeli facilities. We are constantly in the process of taking the required corrective actions in order to comply with the business license terms, the styrene emission standard and the IMEP instructionsinstructions. |

| • | Workers’ safety and health. The Israeli Ministry of Economics, Labor Division (“IMOE”) in Israel the U.S. Occupational Safety and Health Administration (“OSHA”) in the U.S. and the Indian Ministry of Labor and Employment, conduct audits of our plants, in which, among other things, it examinesthey examine if there were any deviations from permitted ambient levels of RCS, styrene and acetone in the plants. We seek, on an ongoing basis, to continue reducing the level of exposure of our employees to RCS, styrene and acetone, while enforcing our employees’ use of personal protection equipment. A fatal accident occurred at the Company’s facility in Richmond Hill in February 2023. The accident was investigated by local law enforcement and OSHA and the matter is now closed. |

| • | Australian Market. On December 13, 2023, Australian federal, state and territory governments announced a joint decision to ban the use, supply and manufacture of engineered stone slabs containing crystalline silica (including our quartz-based products) in Australia. Subject to the formal adoption of the legislation and regulations, the ban will go into effect on July 1, 2024, in most Australian states and territories. While we disagree with this decision, we believe that the focus should be aimed at improving occupational health and safety, and has communicated its position to Australian governments, it is taking the necessary steps to ensure supply of alternative materials to its Australian customers in line with its high standards. This process may negatively impact our sales in the near-term in the Australian market, which accounted for approximately 18.8% of revenue during the fiscal year ended December 31, 2023. |

Other Regulations

We are subject to the Israeli Rest Law, which, among other things, prohibits the employment of Jewish employees on Saturdays and Jewish holidays, unless a permit is obtained from the IMEI. We received a permit from the IMEI to employ Jewish employees on Saturdays and Jewish holidays in connection with most of the production machinery in our Sdot-Yam facility, effective until December 31, 2022.

If we are deemed to be in violation of the Rest Law, we may be required to halt operations of our manufacturing facilities on Saturdays and Jewish holidays, we and our officers may be exposed to administrative and criminal liabilities, including fines, and our operational and financial results could be materially and adversely impacted. For more information, see “Item 3.D. Key Information—Risk Factors—Risks relating to our incorporation and location in Israel—If we fail to comply with Israeli law restrictions concerning employment of Jewish employees on Saturdays and Jewish holidays, we and our office holders may be exposed to administrative and criminal liabilities and our operational and financial results may be materially and adversely impacted.”

For information on other regulations applicable, or potentially applicable, to us, see the following risks factors in “ITEM 3.D. Key Information—Risk Factors”:

“Risks related to our business and industry—We may have exposure to greater-than-anticipated tax liabilities.”