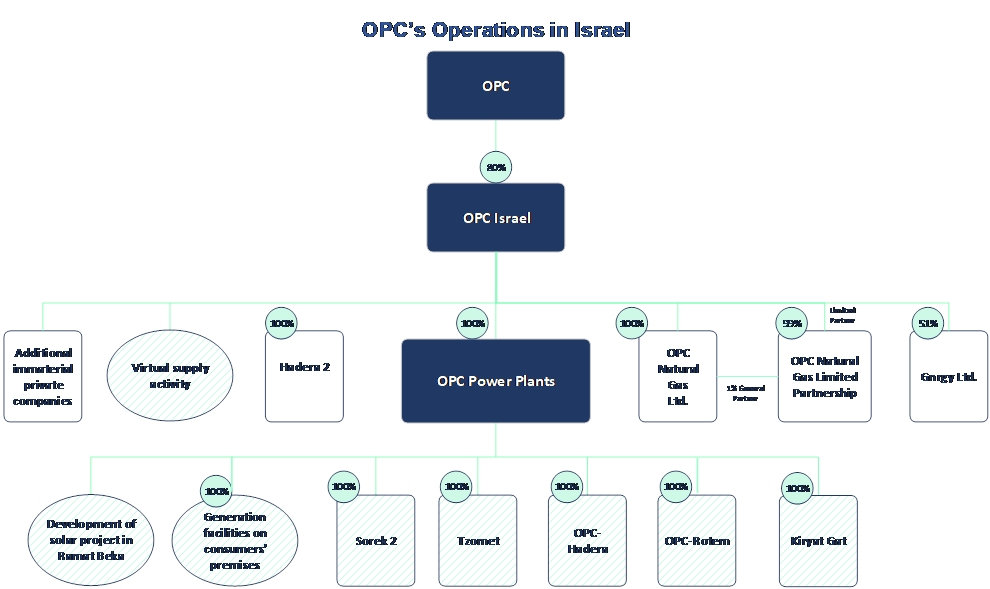

Real estate held through Rotem | Land on which the Rotem Power Plant was built | | Mishor Rotem | | Lease | | About 55 dunams |

Real estate held through Hadera | Hadera Energy Center and the Hadera power plant (including emergency road) | | Hadera | | Rental | | About 30 dunams (Power Plant and Hadera Energy Center) |

Real estate (including options for land) held by Hadera for Hadera 2 Hadera Expansion – Expansion—Land near the area of the Hadera Power Plant | | Hadera | | Rental option through the end of 2028 | | About 68 dunams |

Rotem 2’s land agreement

Land Agreement of Rotem 2 | Land near to space on which Rotem Power Plant was built | | Mishor Rotem | | Lease | | About 55 dunams |

Land held by Tzomet (through Tzomet HLH General Partner Ltd. and Tzomet Netiv Limited Partnership) | Land on which Tzomet is situated | | Plugot Intersection | | Tzomet Netiv Limited Partnership – (byPartnership—(by force of a development agreement with Israel Lands Authority) – —Lease | | About 85 dunams |

Right-of-use of the land for Sorek

Right-of-use of the land for Sorek 2 | Land on which Sorek 2 is being constructed | | Sorek 2 Desalination Facility | | Right of use | | About 2 dunams | | Land held through Kiryat Gat | | Land on which Kiryat Gat is being constructed | | Kiryat Gat | | Ownership | | About 12 dunams |

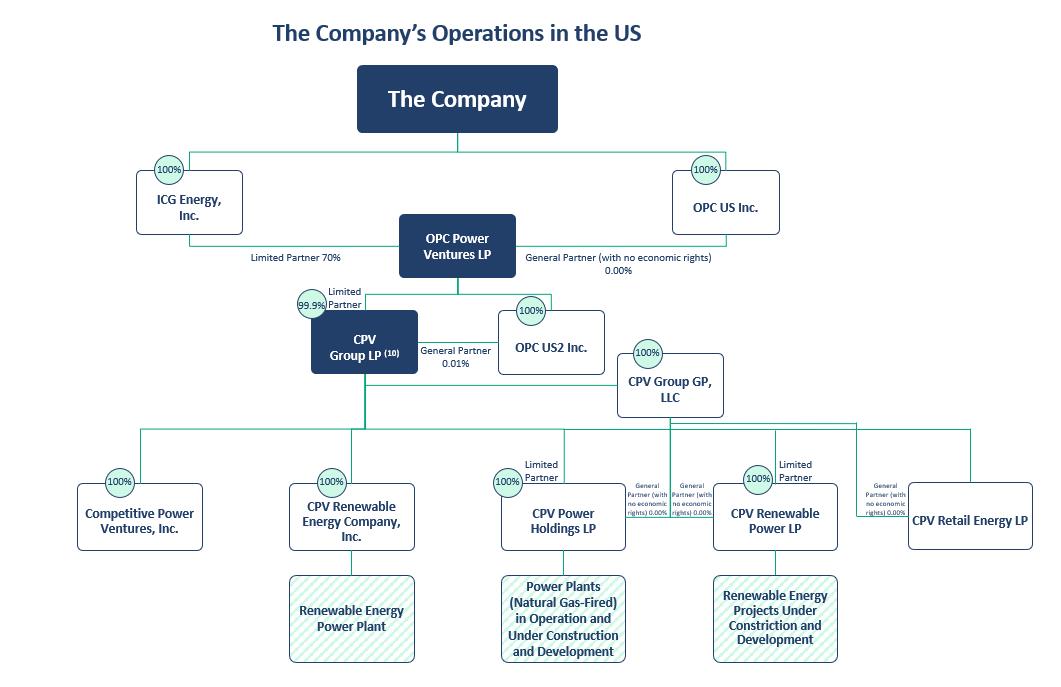

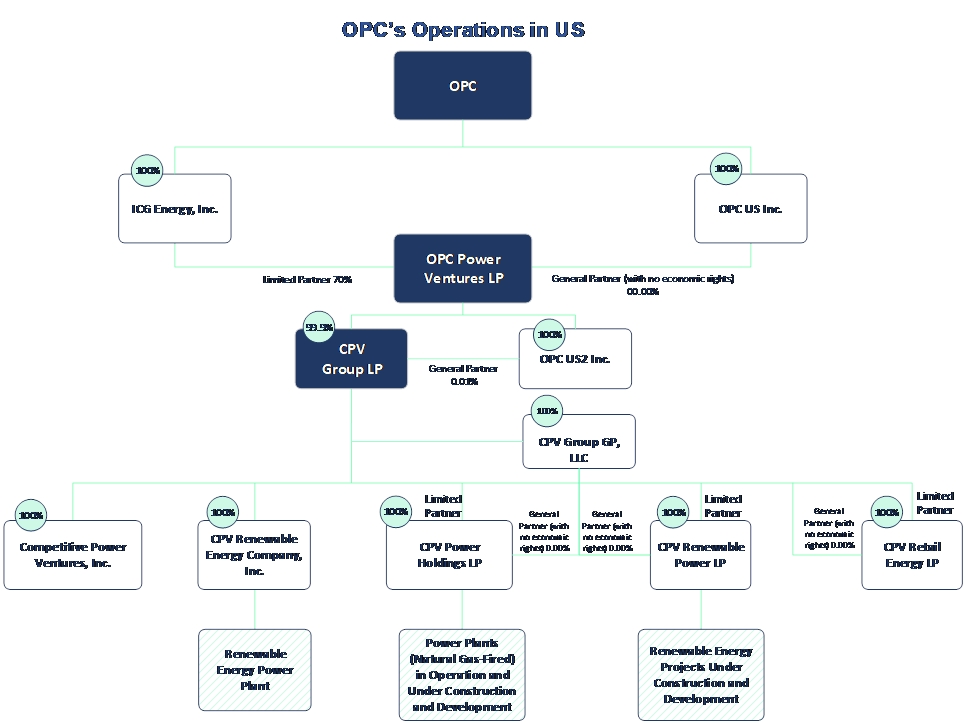

United States In general, the land on which the projects are situated (both the active projects and the projects under construction) is held in a number of ways – ways—ownership, lease with use right, under a permit and licenses. In some cases, the facilities themselves are located on owned land, where there are easements in land surrounding the facility for purposes of connectioninterconnection and transmission. In addition to the project lands, CPV leases office space for use by the headquarters in Silver Spring, Maryland, Sugar Land, Texas, and in Braintree, Massachusetts pursuant to multiyearmulti-year lease agreements. CPV plants in commercial operation | | | | The right in the property | | | | |

Conventional Energy Projects

| Shore | | Land on which the Shore power plant was constructed | | Middlesex County, New Jersey | | Ownership | | About 111,290 square meters (28 acres) | | N/A |

| Maryland | | Land on which the Maryland power plant was constructed | | Charles County, Maryland | | Ownership / easements / licenses and permits / authority | | About 308,290 square meters (76 acres) | | N/A |

| Valley | | Land on which the Valley power plant was constructed | | Wawayanda, Orange County, New York | | Substantive Ownership(1) / easements or permits | | About 121,406 square meters (30 acres) | | N/A |

Towantic

| Towantic | | Land on which the Towantic power plant was constructed | | New Haven County, Connecticut | | Ownership / easements | | About 107,242 square meters (26 acres) | | N/A |

| Fairview | | | | | | | | | | | Land on which the Fairview power plant was constructed | | Cambria County, Jackson Township, Pennsylvania | | Ownership / easements | | About 352,077 square meters (87 acres) | | N/A |

| Three Rivers | | Land on which the Three Rivers power plant was constructed | | Grundy County, Illinois | | Ownership / easements | | About 485,623 square meters (120 acres) | | N/A |

Renewable Energy Projects

| Keenan II | | Land on which the Keenan II wind farm was constructed | | Woodward County, Oklahoma | | Contractual easements | | Rights to land and the equipment | | December 31, 2040 |

Maple Hill

| Mountain Wind | Land on which the CPV Mountain Wind wind farms were constructed (information is aggregated for the four wind farms of Mountain Wind) | Franklin, Oxford and Waldo Counties, Maine | | Contractual easements and leases | | Approx. 15,000,000 square meters (3,700 acres) | | Forty years (Thirty years for 20% of Spruce Mountain) Various 2046—2055 | | Maple Hill | Land on which the Maple Hill power plant is beingwas constructed | | Cambria County, Jackson Township, Pennsylvania | | Ownership / easements | | About 3,063,470 square meters (757 acres, of which 11 acres are leased) | | With regard to the leased area December 1, 20612058 |

| Stagecoach | | Land on which the Stagecoach power plant is being built | | Macon County, Georgia | | Lease Agreement | | Approx. 2,541,426 m² (628 acres) | | May 22, 2042 with option to extend for an additional 20 years | | Land on which the Backbone power plant will be built | | Garrett County, Maryland | | Lease agreement | | Approximately 2,559 acres | | The earlier of March 31, 2025 or commencement of the operating period, plus an option to extend by five consecutive periods of seven years during operations. |

_______________________________________________________________________

| (1) | This land is held for the benefit of Valley, which is entitled to transfer it to its name. |

Insurance OPC and its subsidiaries, including CPV, hold various insurance policies in order to reduce the damage for various risks, including “all-risks” insurance. OPC’s sites (similar to most private business activities in Israel) could be exposed to physical damage as a result of the War in Israel. The existing insurance policies maintained by OPC and its subsidiaries may not cover certain types of damages or may not cover the entire scope of damage caused (and such policies include deductibles and exceptions as customary in the areas of activity). In addition, OPC or CPV may not be able to obtain insurance on comparable terms in the future. Insurance policies for OPC-Rotem, OPC-Hadera will expire at the end of July 2024. Insurance policies for Tzomet will expire at the end of May 2024 and for Kiryat Gat—at the end of April 2024. OPC and its subsidiaries, including CPV, may be adversely affected if they incur losses that are not fully covered by their insurance policies. Employees Israel As of December 31, 2022,2023, in Israel, OPC had a total of 150169 employees, of which 108114 employees are in the OPC Israel division (including plant operation, corporate management, finance, commercial and other), and 4255 are at OPC’s headquarters. Substantially all of OPC’s employees are employed on a full-time basis. The table below sets forth breakdown of employees in Israel by main category of activity as of the dates indicated: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | Number of employees by category of activity: | | | | | | | | | | | | | | | | | | | | Headquarters | | | 42 | | | | 34 | | | | 66 | | | | 55 | | | | 50 | | | | 34 | | | Plant operation, corporate management, finance, commercial and other | | | 108 | | | | 86 | | | | 50 | | | | 114 | | | | 100 | | | | 86 | | | OPC Total (in Israel) | | | 150 | | | | 120 | | | | 116 | | | | 169 | | | | 150 | | | | 120 | |

Most of OPC-Rotem and OPC-Hadera power plants’ operations employees are employed under collective employment agreements. OPC-Rotem is currently negotiating with its employees the engagement in a revised collective agreement to come into force immediately upon the end of the term of the said agreement. .The term of the OPC-Rotem collective agreement ended on March 31, 2023, and a revised collective agreement was signed in respect of OPC-Rotem’s employees for a period of four years until March 31, 2027. Approximately 70 of the employees in OPC-Hadera are employed under a collective agreement which was signed in December 2022 and will be in effect through March 2026. United States As of December 31, 2022,2023, CPV had a total of 131150 employees. In general, CPV does not enter into employment contracts with its employees. All employees of CPV are “at-will” employees and are typically not physically present at the project companies facilities. Rather, day-to-day operations at the project facilities are performed by contractors who are employed directly by the applicable O&M service providers. Shareholders’ Agreements OPC Israel Upon completion of the Veridis transaction, aA shareholders’ agreement is in place between OPC and Veridis regarding OPC Israel entered into force. This agreement replaced shareholder arrangements made between the parties regarding OPC-Rotem and which were in effect until the completion of the Veridis transaction.

Israel. The shareholders’ agreement regarding OPC Israel includes customary terms and conditions, including, inter alia provisions regarding shareholder meetings, rights to appoint directors (such that OPC, as the controlling shareholder, has the right to appoint the majority of directors), shareholder rights in case of share allocation, and more.allocation. In addition, the shareholders’ agreement grants Veridis veto rights in connection with certain material decisions regarding OPC Israel, including: (i) changing the incorporation papers so as to adversely affect or change Veridis’ rights and obligations; (ii) liquidation; (iii) extraordinary transactions (as the term is defined by the Israeli Companies Law -1999, or the Companies Law)-1999) with related parties, with the exception of the exceptions set forth; (iv) entry into new substantial projects that are not included in OPC Israel’s area of activity; (v) restructuring or a merger as a result of which OPC Israel is not the surviving company, subject to the exception set forth in the case of a drag-along sale; (vi) appointing an independent auditor to OPC Israel or a material subsidiary thereof that is not one of the “Big Five” CPA firms; and (vii) approval of a transaction or project in which the planned investment amount is highly material, in accordance with criteria set forth, and subject to exceptions set forth. The agreement provides for additional rights in the event of the sale of OPC Israel’Israel’s shares held by any of the parties, such as the right of first refusal, the tag-along right, the drag-along right – right—all in accordance with the terms and conditions set forth. UnderAn amendment to the shareholders’ loan agreement was signed as part of the Veridis transaction, an amount ofsuch that OPC Israel provided to OPC-Rotem (whether directly or indirectly) NIS 400 million was used by OPC-Rotem(approximately $118 million) for repayment purposes as stated above, and provisions were set regarding the partial repayment of shareholder loans that were advanced to OPC-Rotemthe Shareholder Loans in 2021 (in lieu of Rotem’s project financing). Following the partial repayment and the balance of shareholders’ loans, divided (pro rata) between OPC and Veridis, amounts to approximately NIS 545 million, such that OPC’s share is approximately NIS 436 million (the “Shareholder Loans”). The Shareholders Loans are unlinked and bear interest (representing market conditions) at a rate of 2.65% or interest according to Section 3(J) of the Income Tax Ordinance, whichever is higher. The loans shall be repaid in quarterly unequal paymentsfuture, taking into account OPC-Rotem’s free cash flow in accordance with provisions of the mechanism set in the Shareholder Loans agreement, and in any case no later than October 2031.agreement. CPV-related OPC Partnership Agreement In October 2020, OPC signed a partnership agreement with three institutional investors in connection with the formation of OPC Power (the “Partnership”) and acquisition of CPV by the Partnership. OPC is the general partner and owns 70% of the Partnership interests. The limited partners of the Partnership are: OPC (70% interest; directly or through a subsidiary), Clal Insurance Group (12.75% interest), Migdal Insurance Group (12.75% interest) and a company from the PoalimHapoalim Capital Markets Group (4.5% interest) (together, these three investors, the “Financial Investors”). The percentages above do not include participation rights in the profits allocated to the CPV managers. The total investment commitments and shareholder loans of all the partners amount to $815$1,215 million, based on their respective ownership interests, representing commitments for acquisition consideration, as well as funding of additional investments in CPV for implementation of certain new projects being developed by CPV. In September 2021, the Financial Investors in the Partnership confirmed their participation in an additional undertaking to invest in developing and expanding CPV’s operations, each according to their proportional share, an additional investment of $400 million. During 2022, OPCIn 2023, CPV and the Financial Investors invested in the equity of the Partnership OPC Power (both directly and shareholders’ loans at theindirectly) a total amount of $122approximately $150 million, and $38extended it approximately $45 million in loans, respectively, based on their stake in accordance with their proportionate share in Partnership’s ownership interests.the Partnership. As of March 2023,22, 2024, total investments in the total amountPartnership’s equity and the outstanding balance of the investment is $1,156loans (including accrued interest) amount to approximately $927 million, (net of accrued interest, which – as of December 31, 2022 stood at $29 million).and approximately $339 million, respectively. In March 2023, OPCCPV and the Financial Investors approved their participation in a facility for an additional investment commitment for backing guarantees that were or will be provided for the purpose of development and expansion of projects –- each based on its pro rataproportionate share, as outlined above, for a total of approximately $75 million. In September 2023, after utilizing the entire investment commitment and the shareholder loans advanced, the facility was increased by $100 million, in accordance with each partner’s proportionate share (the CPV’s share in the facility is $70 million). As of March 22, 2024, the total balance of investment undertakings and shareholders’ loans advanced by all partners under the facility is estimated at approximately $100 million (excluding the guarantee facility). The general partner of the Partnership, an entity wholly-owned by OPC, manages the ownership of CPV, with certain material actions (or actions which may involve a conflict of interest between the general partner and the limited partners) requiring approval of a majority or special majority (according to the specific action) of the institutional investors which are limited partners. The general partner is entitled to management fees and success fees subject to meeting certain achievements. There are limits on transfers of partnership interests, with OPC not permitted to sell its interest in the Partnership for a period of three years (except in the case of a public offering by the Partnership), tag along rights for the Financial Investors, drag along rights, and rights of first offer (ROFO) for OPC and the Financial Investors in the case of transfers by the other party. OPC and the Financial Investors have entered into put and call arrangements, with the Financial Investors being granted put options and OPC being granted a call option (if the put options are not exercised), with respect to their holdings in the Partnership. These options are exercisable after 10 years from the date of the CPV acquisition and to the extent that up to such time the Partnership rights are not traded on a recognized stock exchange. Legal Proceedings For a discussion of other significant legal proceedings to which OPC’s businesses are party, see Note 1718 to our financial statements included in this annual report. Industry Overview Overview of Israeli Electricity Generation Industry Electricity generation and supply in Israel In general, the Israeli electricity market is divided into four sectors: the (i) generation sector, (ii) transmission sector (transmitting electricity from generation facilities to switching stations and substations through the electricity transmission grid), (iii) distribution sector (transmitting electricity from substations to consumers through the distribution grid including high voltage and low voltage lines), and the supply sector (sale of electricity to private customers). None of the actions provided in the Electricity Sector Law shall be carried out except pursuant to a license, subject to legal restrictions, and in accordance with activity in each of the segments requiring a relevant license. As of December 31, 2022, the installed electricity production capacity in Israel (of the IEC and independent producers) was 17,434 MW excluding renewable energies, and approximately 4,800 MW of renewable energies, with actual generation constituting approximately 10.1% of total actual consumption in the economy in 2022. According to publications of the EA, the annual rate of increase in demand for electricity in 2023 is expected to be at less than 1%. According to the Electricity Sector Status Report, in 2022 the sectoral generation amounted to 76.9 TWh; in 2025, the annual generation forecast is expected to be 81.7 TWh. In 2023, the EA reviewed key points of progress in the renewable energy market, and stated that at the end of 2023 the rate of actual consumption of renewable energy in the Israeli economy was 12.5%; the rate of renewable energy installed capacity out of total capacity in Israel as of the end of 2023 was 24.4%. The Israeli electricity market includes a number of key players: the EA, the IEC, Noga, the Ministry of Energy and Infrastructures (the “Ministry of Energy”), independent power producers and suppliers and electricity consumers. The Ministry of Energy oversees of the energy and natural resources markets of Israel, including electricity, fuel, cooking gas, natural gas, energy conservation, oil and gas exploration, etc. The Ministry of Energy regulates the public and private entities involved in these fields. In addition, the Minister of Energy has powers under the Electricity Sector Law, including regarding licenses and policy setting on matters regulated under the Law. The EA reports to the Ministry of Energy and operates in accordance with its policy. The EA has the power to issue licenses in accordance with the Electricity Sector Law, to supervise license holders (including private license holders), to set tariffs and criteria for the level and quality of service required from an “essential service provider” license holder. Accordingly, the EA supervises both the IEC and Noga as well as independent power producers and suppliers. According to the Electricity Sector Law, the EA is authorized to determine the electricity tariffs in the market (including the generation component) based, among other things, on the IEC’s costs that are recognized by the EA. The IEC supplies electricity to most of the customers in Israel in accordance with licenses granted to it under the Electricity Sector Law, and transmits and distributes almost all of the electricity in Israel. In general, the IEC is responsible for the installation and reading of the electricity meters of electricity consumers and generators and for transfer of the information to Noga and suppliers in accordance with the decisions of the EA. Noga is a government company, whose operations commenced in November 2021, and is in charge of the management of the electricity system in the generation and transmission segments, including constant balancing out between the supply of electricity and the demand for planning of the transmission system, including, among other things, drawing up a development plan for the transmission and generation segments. Pursuant to the Electricity Sector Law, the IEC and Noga are each defined as an “essential service provider” and as such, they are subject to the criteria and tariffs set by the EA. As of 2022, the IEC’s share amounted to 51.5% in the generation segment and 69% in the supply segment. According to the Electricity Market Report, as of 2022, independent power producers (including OPC power plants), including those using renewable energy, active in Israel have an aggregate generation capacity of approximately 11,706 MW, constituting 53% of the total installed generation capacity in Israel. According to Electricity Market Report, at the end of 2025 (the end of the IEC Reform), the market share of the independent power producers, including renewable energies, is expected to amount to approximately 66% of the total installed capacity in the sector. In generation terms, in 2025 the market share of the independent power producers (including OPC power plants), and including renewable energies, is expected to amount to approximately 60% of the total generation in the market.

The generation component and changes in the IEC’s costs In accordance with the Electricity Sector Law, the EA determines the tariffs, including the rate of the IEC electricity generation component, in accordance with the costs principle and the other considerations provided for in the Electricity Sector Law, as applied by the EA. The generation component is based on, inter alia, the IEC’s fuel costs, comprising mainly of the IEC’s gas and coal costs, the costs of purchasing electricity from independent producers, the IEC’s capital costs, and the EA’s policy on classification of costs to either the generation component and the IEC’s system costs or the recognition of such costs of the IEC. The generation component may also change based on the IEC’s other expenses and revenues and may also be affected by other factors, such as, sale of power plants as part of the IEC Reform. Under the agreements with the private customers, OPC charges its customers the load and time tariff (the “DSM Tariff”), net of the generation component discount. Since the electricity price in the agreements between OPC-Rotem, OPC-Hadera and Kiryat Gat (and of the generation facilities) and their customers is impacted directly by the generation component (such that a decline in the generation component would generally decrease the profitability and vice versa) and the generation component is the linkage base for the natural gas price in accordance with the gas supply agreements of OPC in Israel (subject to a minimum price), OPC is exposed to changes in the generation component, including, among other things, changes in the generation costs and the energy acquisition costs of the IEC, including the price of coal and the IEC’s gas cost. In addition, OPC is exposed to changes in the methodology for determining the generation component and recognizing IEC costs by the EA. In general, an increase in the generation component has a positive effect on OPC’s results. In Israel, the TAOZ tariffs are supervised (controlled) and published by the EA. Generally, the electricity tariffs in Israel in the summer and the winter are higher than those in the transition seasons. Acquisition of the gas, which constitutes the main cost in this business operations, is not impacted by seasonality of the TAOZ (or the demand hours’ brackets). The hourly demand brackets change the breakdown of OPC revenues over the quarters in such a manner that it increases the summer months (and mainly the third quarter) at the expense of the other quarters, and particularly the first and fourth quarters. The summer on-peak (August) high voltage tariff for 2023 indicates that the generation component in 2023 accounted for about 91% of TAOZ. In addition, the TAOZ includes system costs at the rate of 7% and public utilities at the rate of about 2%. On January 1, 2023, an annual update of the tariff for 2023 came into effect for the IEC’s electricity consumers. In accordance with the resolution, the high cost of coal was the main reason for the increase in electricity tariffs. In accordance with the update, the generation component stood at NIS 0.312 per kWh, a 0.6% decrease compared to the generation component that applied in the last few months of 2022. On February 1, 2023, the EA resolution to revise the costs recognized to the IEC and Noga and the tariffs paid by electricity consumers came into effect. This came into effect after the Ministry of Finance signed, on January 23, 2023, orders that extend the reduction in the purchase tax and excise tax rates applicable to coal, such that the reduction shall be in effect through the end of 2023. Pursuant to the resolution, a further update to the generation component for 2023 came into effect, whereby the generation component was changed to NIS 0.3081 per kWh, approximately 1.2% decrease compared to the tariff set on January 1, 2023. At the beginning of March 2023, a hearing was published in connection with the revision of the costs recognized to the IEC and the tariffs paid by electricity consumers, following the decline in coal prices, and increase in other costs. The tariff of NIS 0.3081 which came into effect on April 1, 2023 was reduced by approximately 1.4% from the tariff set in February 2023 to NIS 0.3039. An update to the hourly demand brackets, which became effective from January 2023, had a negative impact on our results from Israel activities and caused a change in the seasonality of our revenues, which resulted in a significant increase in our results during the summer period at the expense of the other months of the year (particularly the first quarter). On February 1, 2024, an annual update of the tariff for 2024 came into effect for the IEC’s electricity consumers. According to the decision, the generation component was updated to NIS 0.3007 per KWh, a decline of 1.1%, mainly due to the excess proceeds expected from the sale of the Eshkol power plant, which led to a reduction in the generation segment. Furthermore, as part of the resolution regarding the updating of the tariff, and according to a decision about the designation of proceeds from the sale of Eshkol, the surplus proceeds from the sale will be first used to cover costs incurred during the War, including diesel fuel costs, and only then will the surplus proceeds be used to cover past one-off costs. Updates in the demand hour clusters On August 28, 2022, the EA also published a resolution amending the demand hour clusters in order to, according to the publication, adjust the structure of the DSM tariff, such that it integrates a significant portion of solar energy and storage. According to the published resolution, the following key revisions were set: (i) changing peak hours from the afternoon to the evening; (ii) increasing the number of months during which peak time applies in the summer to from two months to four months; (iii) increasing the difference between peak time and off-peak time; and (iv) defining a maximum of two clusters for each day of the year (without the mid-peak cluster that was in force until the resolution went into effect). Changing the hour categories in accordance with the decision is expected to increase the tariffs paid by the household consumers and decrease the tariffs paid by DSM tariff consumers. In accordance with the resolution, the revised tariff structure came into force with the revision of the tariff for consumers for 2023. The resolution also stipulated that in view of the frequent changes in the sector and the need to reflect the appropriate sectoral cost, the hour clusters shall be updated more frequently, in accordance with actual changes. The revision of the demand hour clusters had a negative effect on OPC’s results, mainly in view of the consumption profile of OPC’s customers (who are mostly industrial and commercial customers), which generally have low level of consumption fluctuations during the day compared to the sectoral consumption profile as reflected in the tariffs and regulations set as part of the revision for off-peak and on-peak hours. In addition, a change of the demand hour clusters changes the breakdown of OPC’s revenues and profits from its operations in Israel between the different quarters, such that revenues and profits in the summer (June-September), and mainly the third quarter, increase at the expense of the other quarters. The IEC Reform and development of the private electricity market in Israel The entrance of the independent power producers and suppliers has led to a significant decrease in the IEC’s market share in the sale of electricity to large electricity consumers (high and medium voltage consumers). The market share of independent producers in the generation and supply segments is expected continue to grow in coming years as a result of, inter alia, construction of power plants by independent producers (using natural gas and renewable energies), and as a result of the IEC Reform, which includes the sale of power plants and their transfer from the IEC to independent producers, and imposed limitations on the IEC with respect to construction of new power plants, as well as a result of opening the supply segment to competition, including providing licenses to suppliers without generation means and the resolution regarding smart meters installation rules. The following table presents data on the share of independent power producers and the IEC in the electricity market, as well as renewable energy production in 2021 and 2022, as published by the EA. | | | | | | | | | | | | | | % of Total Installed Capacity in the Market | | | | | | % of Total Installed Capacity in the Market | | | IEC | | | 11,615 | | | | 54 | % | | | 10,527 | | | | 47 | % | | Independent power producers (without renewable energy) | | | 6,231 | | | | 29 | % | | | 6,907 | | | | 31 | % | | Renewable energy (independent power producers) | | | | | | | | | | | | | | | | | | Total in the market | | | 21,502 | | | | 100 | % | | | 22,233 | | | | 100 | % |

| | | Energy generated (thousands of MWh) | | | % of total energy produced in Israel | | | Energy generated (thousands of MWh) | | | % of total energy produced in Israel | | | IEC | | | 38,223 | | | | 52 | % | | | 39,224 | | | | 51 | % | | Independent power producers (without renewable energy) | | | 30,077 | | | | 41 | % | | | 30,155 | | | | 39 | % | | Renewable energy (independent power producers) | | | | | | | | | | | | | | | | | | Total in the market | | | 73,975 | | | | 100 | % | | | 76,886 | | | | 100 | % |

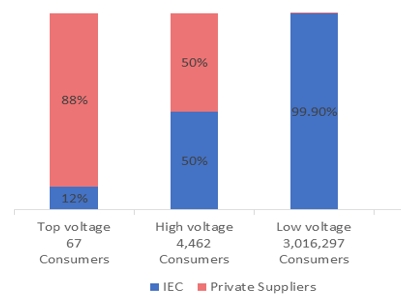

Set forth below are data about the distribution of consumers between private suppliers and the default supplier (in accordance with the IEC’s data): Pursuant to the IEC Reform, an 8-year plan was formed, under which the IEC was required, among other things, to sell certain generation sites (including the Eshkol, which is under a process of completing a sale to an independent producer)), and the system operation activities will be spun off from the IEC and executed by a separate government company. Accordingly, Noga started operating as an entity separate to the IEC in November 2021. The Reading power plant, was also supposed to be sold as part of the IEC Reform; a government taskforce was set up, which considered alternatives to such power plant in order to secure the supply of electricity to Gush Dan. A final decision as to the selected alternative is expected to be made in July 2024. In May 2023, OPC submitted, through a joint special-purpose corporation, held in equal parts by OPC Power Plants and a corporation held by the Noy Fund ("OPC Eshkol"), a bid to purchase the Eshkol Power Plant as part of an IEC tender. In June 2023, OPC was notified that the Tenders Committee declared that an offer submitted by Eshkol Power Energies Ltd. is the winning offer in the Tender, and that OPC Eshkol was declared a "second qualifier" according to the tender documents. Since the winning bidder did not complete the signing of the acquisition agreement, in July 2023, the IEC announced the cancellation of the tender, and its decision to hold a new tender between the bidders that took part in the first bid (and which includes a minimum price of NIS 9 billion (approximately $2 billion) (the "Tender"). In August 2023, OPC Eshkol filed an administrative petition to the Tel Aviv Administrative Court. On September 14, 2023, the Administrative Court rejected the petition. OPC Eshkol did not submit a bid as part of the tender that took place on October 30, 2023. Forecast of potential growth in natural gas in the Israeli electricity market According to the hearings and resolutions of the EA, four gas-powered conventional generation units are expected to be constructed, including the unit that is expected to be constructed as part of the Sorek tender, with a capacity of up to 900 MW, the replaced generation unit in the Eshkol site with a capacity of up to 850 MW, and two conventional units with a capacity of up to 900 MW each. The assessment as to the growth potential in natural gas generation units in the upcoming decade is conditional upon compliance with the renewable energy targets. According to external data available to OPC, OPC believes new natural gas generation capacity of 5,400 to 9,000 MW will be required between 2030 and 2040. In September 2022, Noga published a long-term demand forecast for 2022-2050, according to which the demand is expected to increase by 3.1% per year by 2030 and 3.7% in 2030-2040, based mainly on growth forecasts in connection with the introduction of electric vehicles into Israel. Virtual supply—Opening of the supply segment to suppliers without means of generation and to household consumers In February 2021, the EA reached a resolution to regulate virtual supply license, which allows suppliers who do not have means of production to purchase energy from the System Operator to sell to their customers (the “Virtual Supply”). Suppliers who did not have means of production had been restricted by certain a quota set by the EA. In July 2021, OPC was awarded a virtual supply license. OPC began entering into virtual supply agreements with customers for a total capacity of 50 MW. OPC also entered into a virtual supply agreement with Noga. In March 2022, the EA removed all quotas that were set for virtual supply, and amended the tariff for acquisition of electricity from the System Operator. Overview of United States Electricity Generation Industry Overview The electricity market in the United States, in which CPV operates, is the largest private electricity market in the world with installed capacity of approximately 1,300 gigawatts of generation facilities. The generation mix has changed significantly over the last several years. In 2016, natural gas overtook coal as the primary fuel source for electricity production in the United States, after coal comprised over 50% of the electricity supply since the 1980s. These changes have been driven by federal and state environmental policies, as well as the relative cost of the fuel sources and the advancement in technologies. These factors also have greatly contributed to the growth in renewable technologies over the last several years. Alongside the increasing demand for renewable energy, environmental goals of large commercial and industrial customers are driving demand for renewable energy. The wholesale electric marketplace in the United States operates within the framework of several FERC-approved regional or state market operators, including RTO or ISO. RTO/ISOs are responsible for the day-to-day operation of the transmission system, the administration of the wholesale markets in the regions in which they operate, and for the long-term transmission planning and resource adequacy functions. In most cases the ISO’s and RTO’s powers are concentrated under a single entity. The RTOs and ISOs are supervised by FERC, except for ERCOT (the Texas electricity market). In addition to FERC, other state regulators regulate the sale and transmission of electricity, within each state, and the RTOs/ISOs, which are the key players in the wholesale electricity markets in the United States, in which the CPV Group operates, include other electricity producers and local utility companies, that serve both wholesale and retail customers. Most of the other electricity producers (especially producers that joined recently), and local electricity companies operating in these wholesale markets, are privately owned entities; however, those market players include a number of publicly held cooperatives, government utility companies and federal system administrators. Each of the ISOs and RTOs operates energy markets and related services, and buyers and sellers can submit in those markets bids to sell or supply electricity and related services, such as capacity services, frequency stabilization, backup, etc. Some of the ISOs and RTOs also operate capacity markets. ISOs and RTOs operating in advanced markets use a demand-based electricity selling system, and a marginal price set by electricity producers to meet the regional consumption needs. In large parts of the United States, the electricity management system has a more traditional structure where the local electric utility company is in charge of load management and the production mix. The CPV Group operates mainly in advanced markets managed by ISOs or RTOs. In addition to revenues from the sale of energy, related services and availability, manufacturers of renewable energy and manufacturers of low-carbon energies benefit from government mechanisms and incentives. Both U.S. federal and state governments offer incentives to suppliers in order to meet the renewable energy targets. A number of states require the local electric utility company to acquire a certain quantity of RECs in accordance with the total consumption of their consumers. In addition, there are federal tax incentives in connection with production of and investment in renewable energies and other low-carbon technologies, which also constitute a financial incentive to develop specific production technologies. Furthermore, each state has in place environmental protection regulations, which may provide incentives and encourage the closure of existing production facilities that use fossil fuels. While each of the ISOs and RTOs has the same function on the federal level, there are significant differences between markets in terms of their structure and activity; those differences may affect the execution and the economic feasibility of new projects, and promote or delay investments in new projects. The CPV Group operates mainly in advanced markets managed by ISOs or RTOs. Market Developments The increasing demand for renewable energy led to an unprecedented increase in interconnection applications by projects, and to an increase in interconnection survey applications by solar projects. These demands may affect the planning functions of ISOs or RTOs and utility and electric distribution companies, and lead to delays in interconnection approvals; the demand may also affect the process and pace of promoting the CPV Group’s projects under development. In addition, projects under construction and development are affected by disruptions or delays in supply chains. Some of the CPV’s projects under development or construction have signed certain agreements including PPAs and capacity agreements, as well as RECs, which include provisions relating to delays in commercial operation. If the delays are longer than certain periods, the other parties to the agreements may terminate the agreements, and the CPV Group’s compensation shall be limited to the collateral provided under the agreements. The amount of collateral provided in connection with development projects (including pre-construction) which were provided due to various needs and purposes in the execution stages may increase or decrease pursuant to the terms of applicable agreements in connection with certain milestones being reached for the development projects. The transition in the United States to renewable energy and low-carbon emission generation has been accelerating in recent years. Hydroelectric generation has been a mainstay of the industry from its early days, and certain parts of the country have a significant resource base thereto. During the past decade there has been a significant decrease in the less efficient, less flexible coal fired generation, mainly due to introduction of carbon capture power plants but coal still constitutes more than 17% of the total electricity generation in the United States. While in recent years there has been a significant increase in the capacity of power plants powered by wind and solar energy, the build out of these facilities in the northeast has been slower than expected. A key factor driving the increase in renewable technologies are state policies supporting the decarbonization of the economy which includes energy, transportation, and heating. Twenty-three states (including Maryland, New York, New Jersey, Connecticut and Illinois, states in which the CPV Group operates), the District of Columbia and Puerto Rico have adopted mandatory generation targets using renewable energy to support state demand, and others have policy targets aimed at reducing CO2 emissions over time. Plans implemented by states for renewable energy development require local utility companies to acquire a certain rate of electricity from renewable sources through plans commonly referred to as RECs, which are tradable on a number of exchanges throughout the country. Federal regulations require the reporting of greenhouse gas emissions under the federal Clean Air Act (“CAA”). Federal regulations also impose limits on CO2 emissions from new (commenced construction after January 8, 2014) or reconstructed (commenced reconstruction after June 8, 2014) combined-cycle power plants. States may also impose additional regulations or limitations on such emissions. For example, CPV’s conventional, natural gas-fired power plants in Connecticut, New York, New Jersey and Maryland are subject to the Regional Greenhouse Gas Initiative (“RGGI”), which requires CPV’s natural gas-fired plants to obtain, either through auctions or trading, greenhouse gas emission allowances to offset each facility’s emission of CO2. Pennsylvania may also adopt the RGGI regulation pending the outcome of legal proceedings challenging its implementation. Under RGGI, an independent market monitor provides oversight of the auctions for CO2 allowances, as well as activity on the secondary market, to ensure integrity of, and confidence in, the market. In 2023, the price of carbon dioxide allowances averaged $11.92 per allowance in the four quarterly RGGI auctions. In addition, federal and state tax policies have incentivized investment in certain low or no carbon technologies through PTC, which provide a tax benefit for every kWh generated by renewables during a ten-year period and through ITC, which provide tax benefits based upon the amount of investment made in a renewable or a battery storage project; and tax credit for carbon emissions that either used or sequestered. In 2022, the IRA was signed into law by President Biden. Among other things, this law awards significant tax benefits to renewable energies and technologies aimed at reducing carbon emissions. One of the IRA’s key objective is to increase the production of electricity using renewable energies and to increase regulatory stability in this sector. For more information on the IRA, see “Item 4.B Business Overview—Regulatory, Environmental and Compliance Matters—United States—The Inflation Reduction Act of 2022.” For information on the PJM market, see “Item 4.B Business Overview—Regulatory, Environmental and Compliance Matters—United States—The PJM market.” Regulatory, Environmental and Compliance Matters Israel The IEC generates and supplies most of the electricity in Israel in accordance with licenses granted by virtue of the Israeli Electrical Market Law, and distributes and supplies almost all of the electricity in Israel. In June 2020, the System Operator was granted a license to manage the Israeli electricity system (which was revised in November 2020), pursuant to which the Minister of Energy and the EA approved commencement of gradual activities of the System Operator in two stages. The System Operator’s Technological Planning and Development Unit is responsible for planning the transmission system and, among other things, preparing a development plan for the transmission and generation of electricity, determining criteria for development of the electricity system, formulating forecasts, engineering and statutory planning of the transmission system, and performing studies with respect to connection to generation facilities. The System Operators’ Market Statistic Unit is responsible for the current ongoing operation of the transmission system and is intended to, among other things, maintain a balance in levels of supply and demand in the electricity market, manage the transmission of energy from power stations to substations at the reliability and quality required (by passing through the power grids), timing and performing maintenance works in production units and in transmission systems, managing commerce in Israel under competitive, equal and optimal terms, including performing agreements to purchase available capacity and energy from private electricityindependent power producers and for planning and developing the transmission and distribution systems. Pursuant to the Electricity Sector Law, the IEC and the System OperatorNoga are each defined as an “essential service provider” and as such they are subject to the criteria and tariffs provided by the EA. In addition, the IEC was declared a monopoly by the Israeli Antitrust Authority in the electricity sector, in the field of power supply — electricity production and sale, transmission and distribution of electricity and providing backup services to electricity consumers and producers. IEC Reform Pursuant to the Israeli Government’s electricity sector reform, the IEC will bewas required to sell five of its power plants through a tender process over the 7 years. The IEC will be permitted to build and operate two new gas-powered stations (through a subsidiary), but will not be authorized to construct any new stations or recombine existing stations. The IEC will also cease acting as the System Operator. Following the Israeli Government’s electricity sector reform, as part of which the IEC is expected to sell five of its sites, the Israel Competition Authority issued guiding principles for sector concentration consultation in such sale process. According to such principles, which are subject to change and review considering the relevant circumstances: An entity may not hold more than 20% of the total planned installed capacity on the date of sale of all the sites being sold. The generation capacity of an entity’s related parties with generation licenses will be counted towards such entity’s capacity for purposes of this 20% limitation. In addition, the EA published proposed regulations in respect of maximum holdings in generation licenses which are not identical to the Competition Authority principles. The Competition Authority has stated that the relevant limit is 20% of 10,500 MW (which is the anticipated capacity in the market held by private players by 2023, excluding capacity of the IEC), while, the EA has proposed regulation whereby the relevant limit is 20% of 16,000 MW (including capacity of the IEC). OPC may be subject to a more restrictive interpretation. The MW currently attributable to OPC, including Oil Refineries Ltd., or ORL, and Israel Chemicals Ltd. as parties with generation licenses that are related to OPC, is approximately 1,480 MW; and An entity holding a right to a fuel venture may not acquire any of the sites being sold. OPC participated in the tenders of the Alon Tabor plant and Ramat Hovav plants — the first two plants that have been sold out of the five plants to be sold by the IEC — but was not the winning bidder. Ministry of Energy and EA The Ministry of Energy regulates the energy and natural resources markets of the State of Israel: electricity, fuel, cooking gas, natural gas, energy conservation, water, sewerage, oil exploration, minerals, scientific research of the land and water, etc. The Ministry of Energy regulates public and private entities involved in these fields, and operates to ensure the markets’ adequate supply under changing energy and infrastructure needs, while regulating the markets, protecting consumers and preserving the environment. According to publications of the Ministrypolicy principles set by the Minister of Energy from November 2019, by the Ministryend of Energy’s multi-year goals include diversified energy resources2025, production units 5-6 at the Orot Rabin site in Hadera and ensuring reliability of supply during peacetime and emergency, developing effective and significantgeneration units 1-4 at the “Rutenberg” site in Ashkelon will be converted to natural gas and determining long-terms policies and appropriate regulationsthe use of coal will cease. In accordance with information published by the EA, the first combined cycle in “Orot Rabin” is expected to start operations in May 2024. After its operation, the two units are expected to be decommissioned (units 3-4 in “Orot Rabin”). In addition, the project for the conversion of the market’s electricity. 109

The Ministry of Energy’s main objectives in the electricity field are securing a reliable supply of electricity to the Israeli market, formulating development procedures to the electricity production sections, energy transmission and distribution, promoting policies to integrate renewable energies in electricity production in accordance with governmental decisions, formulating policies changing the market’s electricity structure, performing control and supervision of the implementation of the IEC’s and private producers’ development plans, performing control, supervision and enforcement of implementing safety regulations according to the Electricity Law, 5714-1954, and handling legislature in the electricity market fields, rules of performing electricity works and security in electricity. The main objectives of the Ministry of Energy in its workplan for 2019 included achieving an efficient and competitive electricity sector by focusing on the reform of the sector through the initiation of tenders for the sale of the IEC power plants and the transfer of system management activities from the IEC to the new System Operator. Energy Sector Targets for 2050 In April 2021, the Ministry of Energy published the roadmap for a low-carbon energy sector by 2050. The Ministry of Energy has set four “primary targets” that will reflect the strategic goal of reducing emissions, and also supportive sectoral objectives which will help to achieve them. The “super target” is defined as a reduction of greenhouse gas emissions from the energy sector by 80%at least 85% compared to the 2015 reference year, by 2050. The targets and indices for the energy sector are presented by the Ministry of Energy in the following table. | | | | | | | | | | Reducing greenhouse gas in the energy sector | | Percentage reduction of greenhouse gas over 2015 | | 0% | | 22% | | 80% | | Reducing greenhouse gas in the electricity sector | | Percentage reduction of greenhouse gas over 2015 | | 7.5% | | 30% | | 75%-85% | | Energy efficiency | | Percentage of annual improvement in energy intensity (TW/NUS million) | | 0.7% | | Annual improvement of 1.3% in energy intensity | | Annual improvement of 1.3% in energy intensity | | Use of coal | | Percentage of coal in the electricity generation mix | | 30% | | 0% | | 0% |

| | | | | | | | | | Reducing greenhouse gas emissions in the energy sector | | Percentage reduction of greenhouse gas emissions compared with 2015 | | 0% | | 22% | | 80% | | Reducing greenhouse gas emissions in the electricity sector | | Percentage reduction of greenhouse gas emissions compared with 2015 | | 7.5% | | 30% | | 75%-85% | | Energy efficiency | | Average annual improvement in energy intensity (TW/NIS million) | | 0.7% | | Annual improvement of 1.3% in energy intensity | | Annual improvement of 1.3% in energy intensity | | Use of coal | | Percentage of coal in the electricity generation mix | | 30% | | 0% | | 0% |

In February 2022, Israeli Knesset discussedFurther to Government Decision No. 171 from July 2021 regarding a transition to a low carbon economy, in January 2024, the Climate Law bill,Government passed Government Resolution No. 1261 regarding the objectivepricing of which is to preventemissions of local pollutants and reduce greenhouse gas emissions andgases, for the damages of global warming in Israel, as partimplementation of the State of Israel’s commitmentprinciple that requires polluting entity to take steps for tackling global warming, including setting targets and drawing up plans for reducing greenhouse gas emissions.pay. As part of the bill, it was suggestedresolution, the Minister of Finance will revise the Excise Tax on Fuel Order (Imposition of Excise Tax), 2004 (“the Excise Tax on Fuel Order”) and the Customs Tariff and Exemptions and Purchase Tax of Goods Order, 2017, to ensure a gradual charge to an entity for the external and environmental costs of carbon emissions, commencing from 2025, within the scope of the resolution. The Minister of Finance has yet not approved the Excise Tax on Fuel Order within the scope of the resolution. OPC believes that the amendment of the Excise Tax on Fuel Order pursuant to the government will take stepsresolution (if advanced) would increase OPC’s costs of acquiring natural gas (renewable energy projects are not exposed to reduce annualthe natural gas costs), where this impact is expected to be offset, partly or fully, to the extent the costs deriving from the resolution are included in the generation component. In September 2023, the Israeli Ministerial Legislation Committee approved the government Climate Bid, which specifies a strategic national net-zero target by 2050, and an interim target of a 30% reduction in greenhouse gas emissions such that emissions willby 2030. The law sets government implementation mechanisms, national plans, and transparency, monitoring and reporting duties to secure compliance with the targets. To the best of OPC’s knowledge, the law has not exceedyet been passed and the following targets (in relation to 2015 asfinal wording of the base year):legislation is uncertain.

| (1) | In 2030 and through 2049 – no more than 73% of the annual quantity measured in the base year. |

| (2) | In 2050 and thereafter – no more than 15% of the annual quantity measured in the base year. |

Closure of the IEC’s Coal-Fired Production Units As of March 19, 2023, theThe IEC’s generation units run on coal, natural gas, fuel oil or diesel fuel as their secondary or primary fuel, as the case may be. The power plants operated by the independent electricity producers are powered by natural gas as primary fuel and diesel fuel as backup. Use of natural gas for power generation reduces air pollution and greenhouse gas emissions in the power generation process compared to the use of coal.

According to Government Decision 4080, by June 2022, the generation of electricity in units 1-4 will bewas stopped, subject to the existence of two cumulative conditions: (i) connection of a third gas reservoir (Karish Tanin reservoir) to the national gas transmission system, (ii) commencement of operation of the first combined cycle with a capacity of 600 MW at the “Orot Rabin” site in Hadera. As of March 19, 2023, theThe generation units of units 1-44-1 at the Orot Rabin site has not yet terminated and there is no certainty regarding compliance with the conditions and the cessation of generation in these units. According to the policy principles set by the Minister of Energy from November 2019, untilby the end of 2025, production units 5-6 at the Orot Rabin site in Hadera and generation units 1-4 at the “Rutenberg” site in Ashkelon will be converted to natural gas and the use of coal will cease. In accordance with information published by the EA, as part of the tariff update, the first combined cycle in “Orot Rabin” is expected to start operations in July 2023.May 2024. After theits operation, of the combined cycle, the two units are expected to be decommissioned.decommissioned (3-4 in “Orot Rabin”). In addition, the project for the conversion of the coal-fired power plants is delayed and is expected to be completed onlystarted in April 2023.the first unit in January 2024. The EA The EA, which is subordinated to the Ministry of Energy and operates in accordance with its policy, was established in January 2016, and replaced the Public Utility Authority (“PUAE”), which operated until that time by virtue of the Electricity Sector Law. The EA has the authority to grant licenses in accordance with the Electricity Sector Law, to supervise license holders, to set electricity tariffs and criteria for them, including the level and quality of services required from an “essential service provider” license holder, supply license holder, a transmission and distribution license holder, an electricity producer and a private electricityan independent power producer. Thus, the EA supervises both the IEC and private producers. The Minister of Energy can dispute EA rulings and request a renewed discussion on specific rulings, except in the matter of the electricity tariffs, which the EA has full authority to set. In addition, the Minister of Energy has the authority to propose the appointment of some of the members of the EA board, as well as the authority to rule on electricity market policy on the subjects defined in the Electricity Sector Law. According to the Electricity Sector Law, the EA may set the power rates in the market, based, among others, on the IEC costs that the EA elects to recognize, and yield on capital. The EA sets different rates for different electricity sectors. According to the Electricity Sector Law, the IEC shall charge customers in accordance with rates set by the EA and shall pay another license holder or a customer in accordance with the relevant rates. In addition, the EA sets the tariffs paid by private electricityindependent power producers to the IEC for various services provided by the IEC, including measurement and meter services, system services, and infrastructure services. In 2022, the EA continued to publish resolutions intended to promote the construction of solar facilities, storage facilities, and installation of EV charging stations in the land divisions, updated the demand hours clusters and underlying tariffs, revised the criteria for promoting competition in the supply segment, established principles for installing smart meters, and approved virtual supply licenses. In addition, the EA published a resolution to amend criteria for the purpose of applying the market model to existing private electricity generation.

For further information on related EA tariffs, see “—Industry Overview— Overview of Israeli Electricity Generation Industry.” For further information on the effect of EA tariffs on OPC’s revenues and margins, see “Item 5. Operating and Financial Review and Prospects—Material Factors Affecting Results of Operations—OPC— Revenue—EA Tariffs.” Independent Power Producers (IPPs) Activity by IPPs, including the construction of private power stations and the sale of electricity produced therein, is regulated by IPP Regulations and the Cogeneration Regulations, as well as the rules, decisions, and standards established by the EA. OPC-Rotem has a unique regulation by virtue of a tender, as detailed below. According to the Electricity Sector Law, none of the actions set in the Electricity Sector Law shall be carried out by anyone other than a license holder. The Licenses Regulations include provisions and conditions in the matter of issuing licenses, rules for operating under such licenses and the obligations borne by license holders. In order to obtain a production license, an applicant must file a request in accordance with the relevant regulations, and meet the threshold conditions. Among others, the manufacturer bears the burden to prove that the corporation requesting the license has a link to the land relevant to the facility. According to EA rulings, subject to meeting the terms (and with the approval of the Minister of Energy for licenses exceeding 100 MW), the developer is granted a conditional license and, upon completion of construction of the facility and successful compliance with acceptance tests, a generation license. The conditional license holder must meet certain milestones for constructing its facility as detailed in the conditional license, and must also prove financial closing. Only after meeting these milestones and the commercial operation of the facility, the developer is granted a generation license (or Permanent License) determined by the EA for the period determined in such license (for licenses exceeding 100 MW, the license must be approved by the Minister of Energy).

This model, which is based on receiving a conditional license followed by a permanent license (subject to meeting the regulatory and statutory milestones), is applicable to both the production of electricity using all types of technology, with the exception of facilities with an installed capacity under 16 MW, for which no license is required for their operation. A party requesting a supply license must demonstrate compliance with the shareholders’ equity requirements as provided by the EA as a condition for receipt of a supply license for suppliers without means of generation.

According to the 20212022 Electricity MarketSector Status Report, as of 2021,2022, IPPs (including OPC-Rotem and OPC-Hadera)OPC power plants), including those using renewable energy, active in Israel have an aggregate generation capacity of 9,887approximately 11,706 MW, constituting 46%53% of the total installed generation capacity in the country. According to the Electricity Sector Status Report for 2021,2022, by the end of the IEC Reform period, the market share of the independent electricitypower producers (including OPC-Rotem and OPC-Hadera), including renewable energies, is expected to amount to approximately 69%66% of the total installed capacity in the sector. In generation terms, in 2025, the market share of the independent electricitypower producers (including OPC-Rotem and OPC-Hadera), including renewable energies, is expected to amount to approximately 62%60% of the total generation in the market. The regulatory arrangements applicable to IPPs were determined while distinguishing between the different generation technologies they use and the various levels of voltage they will be connected to (according to installed capacity). The following are the key electricity production technologies used by private producers in Israel:

| • | Conventional technology – —electricity generation using fossil fuel (natural gas, diesel oil or carbon). As of December 31, 2021,2022, the total installed capacity in this technology which is primarily held by the independent producers, is about 5,931 megawatts.6,607 MW. Gas-fired combined cycle generation facilities are planned to be operational during most hours over the year. Conventional open cycle power plants (the “peaker power plants”) are generally planned to operate for a number of hours during the day; these power plants are operated when the demand for electricity exceeds the supply supply–- whether due to demand peaks, as backup in case of malfunctions in other generation facilities, or as a supplement when solar energy is unavailable – unavailable—whether in the early morning hours or at night. |

| • | Cogeneration technology – —electricity generation using facilities that simultaneously generate both electrical energy and useful thermal energy (steam) from a single source of energy. Exercise of the quota of generatorsfor producers using this technology amounts to approximately 990 MW assigned under the current regulation.is fully utilized. |

| • | Renewable energy – —generation of electric power the source of energy of which includes, inter alia, sun, wind, water or waste. In November 2020, the Israeli government updated the generation targets for renewable energy to 30% of the consumption up to 2030. As of the end of 2022, the installed capacity of renewable energy generation facilities was 4,795 MW. In recent years, there has been an uptick in the entrance of electricity producers and generation facilities that use renewable energies in to the electricity generation market, including solar energy, wind energy, and storage; that use the grid resources. MostIn 2023, most of the renewable energy generation activities arewas sold to the System Operator or for producer’s own consumption and to the onsite consumers. |

| • | Pumped storage energy – —generation of electricity using an electrical pump connected to the power grid in order to pump water from a lower water reservoir to an upper water reservoir, while taking advantage of the height differences between them in order to power an electric turbine. The capacity of one of the production facilities (which is in operation) using this technology amounts to 300 MW, with two additional facilities using this technology with capacity of approximately 800 MW are under construction. |

| • | Energy storage – —this is possible through a range of technologies, including, among others, pumped storage, mechanical storage (for example compressed air) and chemical storage (for example batteries). Considering the Israeli government decision that provides a target for generation of electricity using renewable energies (mainly solar energy) at the rate of 30% out of the generation up to 2030, the EA estimates that the electricity sector in Israel will need to prepare for construction of facilities for energy storage. The use of this technology is currently negligible; however, it is expected to increase significantly in the upcoming years due to the need for storage facilities as a result of the anticipated increase in renewable energies.energies, due to, among other things, the renewable energies generation targets. In particular, based on study conducted by EA, publications, compliance with the target for renewable energies up to 2030 will require construction of storage facilities with a capacity of thousands of MWh, deriving from the readiness of the technology and the economic feasibility of its use. OPC takes steps to integrate energy storage. For example, OPC entered into a number of agreements for generation of electricity at the consumers’ premises, which allow OPC to build storage facilities.facilities as well as in the Ramat Beka Solar Project. |

According to the Electricity Sector Law, the IEC, as an essential service provider, is committed to purchasing electricity from IPPs at the rates and under the conditions set in the Electricity Sector Law and the regulations and standards promulgated thereunder (and, in relation to OPC-Rotem, by virtue of the tender and OPC-Rotem’s PPA with the IEC). In addition, the IEC is committed to connecting the IPPs facilities to the distribution and transmission grid and providing them with infrastructure services in order to allow IPPs to provide power to private customers and system administration service. In accordance with the EA’s resolution entitled “Principles for the Integration of the IEC into the Field of Energy Storage in the Transmission and Distribution Grid” of January 18, 2023, the IEC’s market share in the field of storage shall not exceed 15% of the market share of the private market. The deployment plan that will be filed by the IEC for the construction of storage facilities will be coordinated with the System Operator and approved by the EA in view of the purpose of the storage facilities it will build, for system-wide purposes. The facilities will be operated by the IEC under the directives of the System Operator, and its supervision and control. Independent Electricity Suppliers The electricity suppliers operate through supply licenses, by virtue of which they are allowed to sell–- to consumers or to suppliers–- electricity they generate or purchase, in accordance with the terms and conditions of the licenses and the regulations that apply to them. During 2023, following EA regulations in respect of the suppliers without means of production, the private activity in the supply segment expanded, including offers to sell electricity to household consumers. Further to the above, in February 2024, the EA published a hearing regarding the incorporation of basic meters in the competition in the supply segment; according to the EA, in order to remove barriers and promote competition in the supply segment, to allow household consumers to belong to independent suppliers regardless of the installation of a smart meter. Accordingly, the proposed resolution regulates the netting procedure of suppliers with the System Operator, and the latter’s netting with the IEC, such that a household consumer without a smart meter will be able to join the competitive supply segment, allowing private electricity suppliers to be able to sell electricity to consumers who own a basic meter, as part of the virtual supply activity. Electricity Consumers In recent years more so than in the past, due to the Israeli government’s targets with respect to renewable energies and the targets of the Minister of Energy for decentralized generation, the impact of electricity consumers on the market has strengthened. In recent years, there is a global trend of transition from generation of electricity using fossil fuels to generation using renewable energy technologies due to, among other things, the increasing awareness of the climate change crisis, as well as in light of the decline in the construction costs of the renewable energy facilities, particularly the photovoltaic generation facilities. In addition, recently, including due to technology developments, including the introduction of electric vehicles, and the definition of the renewable energy targets set by the Israeli government and the targets set by the Ministry of Energy for decentralized generation, the status of the electricity consumers consumers–- as active stakeholders stakeholders–- has strengthened. In accordance with the regulations forecast as per the EA’s decision to deploy smart meters, in 2023, the number of smart meters will reach 300,000. OPC believes, the steps taken by the EA to open up the supply segment to competition, including decisions regarding installation of smart meters and licensing suppliers without means of production, are expected to expandincreased the number of entities operating in the households consumption segment, and the scope of consumption associated with independent suppliers and in a manner that is expected to enhance the growing competition in this segment. For example, in June 2023, the EA approved a plan to expand the deployment of the smart meters, where an essential service provider shall complete the replacement of the meters of all Israeli consumers to smart meters by December 31, 2028. The deployment plan is expected to include the replacement of approximately 2.7 million meters, including the installation of smart meters with new connections. The number of smart meters in Israel in 2029 is expected to reach approximately 3.5 million. In February 2024 the EA published a hearing on the “incorporation of basic meters in the supply competition,” pursuant to which the supply of electricity to household consumers will be allowed also through a uniform meter, regardless of installation of a smart meter. Market model for generation and storage facilities connected to or integrated into the distribution grid In September 2022, the EA published a resolution on “market model for generation and storage facilities connected to or integrated into the distribution grid.” The resolution regulates the generation activity of generation (all(using all different technologies) and storage facilities in the distribution grid, and determines their option to sell electricity directly to virtual suppliers as from January 2024. The resolution allows forAs a practical matter, the decision permits opening of the supply segmentsector to competition while removing the quotas that were previously setprovided regarding this matter. The main goalprinciples of the resolution is: (i)are: allowing the possibility of sale of energy from a generation facility to a private virtual provider assupplier commencing from January 2024, and (ii)2024; allowing the transferpossibility of transitioning from other existing regulations forwith respect to the generation facility tounder this regulation; implementationand acceptance of a generation plan forof high voltagetension facilities by the distributor and provision of a load plan. AsProducers connected to the distribution grid may also sell to consumers (through virtual suppliers) as part of the resolution, the formula for acquiring electricity through the virtual supplier was amended such that the difference between the cost of acquiring the supplier’s energy and the cost of selling the energy to IEC’s consumers was minimized, and a unified tariff was set (which is based on an economy-wide profile) in respect of acquisition of electricity during peak demand hours net. In fact, the resolution allows for the opening of the supply segment to competition, while removing the quotas that were previously set regarding this matter.market distribution model. OPC expects that, in the short term, the resolution reduces the economic viability of the virtual supply activity, compared to the conditions prior to the resolution, and in the long term, the resolution encourages increased competition in the supply segment while integrating generation facilities and storage facilities. Regulatory Framework for Conventional IPPs The regulatory framework for current and under construction conventional IPPs was set by the PUAE in 2008. An IPP may choose to allocate its generation capacity, as “permanently available capacity,” or PAC, or as “variable available capacity,” or VAC. PAC refers to capacity that is allocated to the IEC and is dispatched according to the IEC’s instructions. PAC receives a capacity payment for the capacity allocated to the IEC, as well as energy payment to cover the energy costs, in the event that the unit is dispatched. VAC refers to capacity that is allocated to private consumers, and sold according to an agreement between the IPP and a third party. Under VAC terms, IPP shall be entitled to receive availability payments for excess energy not sold to private customers. In addition, the IEC can purchase electricity allocated to it at variable availability, on a price quote basis. Within this regulatory framework, a private electricity producer can choose to allocate between 70% and 90% of their production capacity at high availability, and the rest at variable availability. Upon the development of the electricity sector and the full utilization of EA Regulation 241 quotas, the EA published a follow-up arrangement for conventional producers, and implemented dispatch of IPPs according to the economic dispatch order. According to this regulation, the production units shall be dispatched in accordance with an economic dispatch principle and independent of PPAs between producers and customers, and shall apply to producers with an installed capacity higher than 16 MW and up to a total output of 1,224 MW. This regulation is referred to as “Regulation 914.” In May 2017, the EA amended Regulation 914. Under the amendment, a higher tariff was adopted for production facilities that comply with certain flexible requirements. The amendment also offers open-cycle producers several alternatives including receiving surplus gas from the gas agreementsas part of other producers.Regulation 914. The total quota for new facilities pursuant to this arrangement was limited to 1,100 MW distributed across various plants (at least 450 MW and up to 700 MW for combined cycle facilities, at least 400 MW and up to 650 MW for flexible open cycle facilities). Furthermore, under the amendment the EA prohibits entry into bilateral transactions by open-cycle facilities and demands that combined-cycle facilities sell at least 15% of their capacity to private consumers. For example, Tzomet operates in accordance with Regulation 914. Finally, in order to grant IPPs sufficient time to reach financial closing, Regulation 914 was extended to apply to producers who will receive licenses no later than January 1, 2020. In November 2018, the EA published a decision regarding the activity arrangement of natural gas generation facilities connected to the distribution network. Pursuant to this decision, generators under 16 MW are encouraged to construct power plants within customers’ facilities. These power plants will only be permitted to sell electricity to customers within the facility (and not other private customers) and the System Operator. In 2019, the EA announced a tender to establish and allot the capacity tariff for facilities connected to the distribution grid producing electricity with natural gas. In March 2019, the EA published a decision regarding the establishment of generators connected to the high-voltage network without a tender process. This decision would permit the establishment of generation facilities that are connected to the transmission grid or integrated in the connection of a consumer connected to the transmission grid (excluding renewable energy) for a maximuman aggregate installed capacity of 500 MW and provided they receive tariff approval by May 1, 2024 as extended by EA resolution on November 29, 2023 which postponed the enddeadlines for construction of 2023.electricity generation facilities due to the security condition. These generation facilities will only be permitted to sell electricity to customers within the facility (and not other private customers) and to provide the rest of their available capacity to the System Operator, that will upload the capacity to the grid according to central upload system. The EA has stated that it intends to publish information on the tender process for construction of such generation facilities in the future.