As filed with Securities and Exchange Commission on June 24, 2011April 29, 2013

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20102012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number: 001-14714

(Exact name of Registrant as specified in its charter)

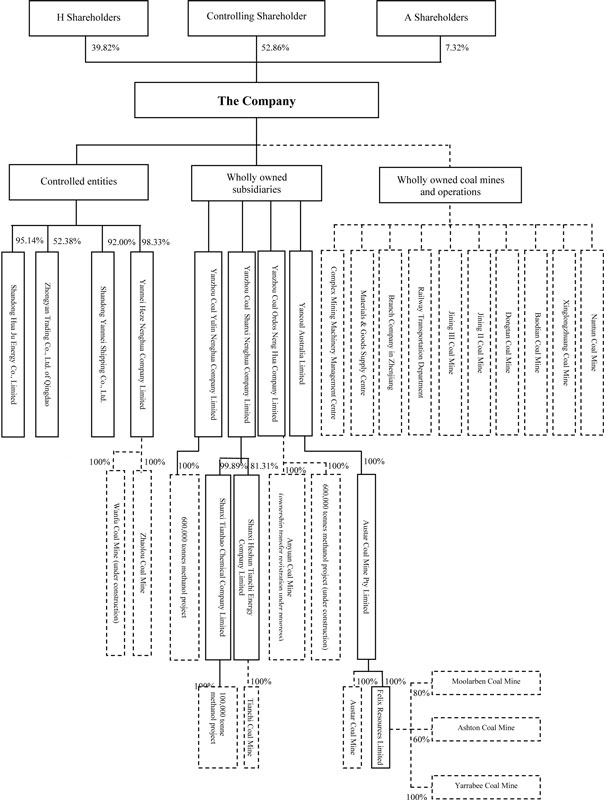

Yanzhou Coal Mining Company Limited

(Translation of Registrant’s name into English)

People’s Republic of China

(Jurisdiction of incorporation or organization)

298 Fushan South Road

Zoucheng, Shandong Province

People’s Republic of China

(Address of principal executive offices)

Zhang Baocai

298 South Fushan Road

Zoucheng, Shandong Province

People’s Republic of China (273500)

Tel: (86)537 5382319

Fax: (86)537 5383311

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

Title of each class | Name of each exchange on which registered | |

| American Depositary Shares | New York Stock Exchange | |

| Class H Ordinary Shares | New York Stock Exchange* | |

| * | Not for trading in the United States, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission. |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

2,960,000,000 Domestic Shares, par value RMB1.00 per share

1,958,400,000 H Shares, par value RMB1.00 per share, including H Shares that were represented by 13,933,698 ADSs

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this Chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files.) Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ¨ | International Financial Reporting Standards as issued by the International Accounting Standards Board x | Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This annual report includes statements of our expectations, intentions, plans and beliefs that constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and are intended to come within the safe harbor protection provided by those sections. The statements relate to future events or our financial performance, including, but not limited to, projections and estimates concerning the timing and success of specific projects and acquisitions. We use words such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “forecast,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “will” and the negatives of such terms or other similar expressions to identify forward-looking statements.

Without limiting the foregoing, all statements relating to our future operating results and anticipated capital expenditures, borrowings and sources of funding are forward-looking statements and speak only as of the date of this annual report. These statements are based on numerous assumptions that we believe are reasonable, but are subject to a wide range of risks, uncertainties and contingencies, which may cause actual results to differ materially from those discussed in these statements. Among the factors that could cause actual results to differ materially are:

|

price volatility for our coal and other related products;

demand for coal in the PRC and overseas markets;

difficulty in managing our rapid growth, business diversification, geographic expansion and integrating our acquisitions;

changes in legislation, regulations and policies;

the recovery offactors affecting the methanol industry and methanol prices;

our ability to reduce costs and compete effectively;

our need for, and ability to obtain, capital to finance our future expansion plans and capital expenditures;

expected increases in production capacity and utilization of new facilities;

intensity of competition;competitive landscape;

uncertainties in estimating our proven and probable coal reserves and our ability to replace and develop coal reserves;

effects of land reclamation and other liabilities;

geologic, equipment and operational risks related to mining;

changes in economic strength and political stability of countries in which we have operations or serve customers;

our ability to realize the anticipated benefits of our acquisition of equity interests or assets of coal mines;

obtaining governmental permits and approvals for our operations;

proximity of our coal resources to end-markets and costcosts of transportation;

availability, timing of delivery and cost of key supplies;

impacts of natural disasters, epidemics and safety accidents; and

other factors, including, but not limited to, those discussed in the section headed Risk Factors,under “Risk Factors”, set forth in Part D of Item 3 of this annual report.

All of the forward-looking statements made in this annual report are qualified by this cautionary statement. We cannot assure you that the actual results or developments anticipated by us will be realized or, even if substantially realized, that they will have the expected effect on us, our business or our operations. We caution you not to place undue reliance on any such forward-looking statements. Unless we are required to do so under U.S. federal securities laws or other applicable laws, we do not intend to update or revise any forward-looking statements.

DEFINITIONS AND SUPPLEMENTAL INFORMATION

As used in this annual report, references to “Yanzhou Coal,” “we,” “our,” “our Company,” “the Group” or “us” refer to Yanzhou Coal Mining Company Limited and its subsidiaries, which have been consolidated into its accounts for the purpose of the consolidated financial statements, unless the context indicates otherwise. References to “the Company” refer to Yanzhou Coal as a stand-alone statutory entity.

“ADSs” are to the American depositary shares of the Company.

“A Shares” refersare to domestic shares in the ordinary share capital of the Company, with nominal value of RMB1.00 each, which are listed on the Shanghai Stock Exchange.

“Articles of Association” refersare to our Articles of Association, as amended from time to time.

“ASX” are to ASX Limited or, as the context requires, the financial market known as the Australian Securities Exchange operated by it.

“Austar Company” refersare to Austar Coal Mine Pty Limited, a wholly owned subsidiary of Yancoal Australia Limited incorporated in Australia, which mainly engages in the mining, processing and sale of coal in Australia.

“Australia” are to the Commonwealth of Australia.

“BBSY” are to the Australian Bank Bill Swap Rate.

“Beisheng Industry and Trade” are to Zoucheng Yankuang Beisheng Industry and Trade Co., Ltd., a limited liability company incorporated in the PRC.

“Beisu Company” are to Yankuang Group Beisu Coal Mine Co., Ltd., a limited liability company incorporated in the PRC, which is a wholly owned subsidiary of Yankuang Group.

“CAGR” are to the compound annual growth rate.

“CASs” refersare to Accounting Standard for Business Enterprises (2006) and the relevant regulations and explanations issued by the Ministry of Finance of the PRC.

“CBRC” refersChina” or the “PRC” are to the People’s Republic of China, Bankingexcluding, for purposes of this annual report, the Hong Kong Special Administrative Region (“Hong Kong”), Macau Special Administrative Region and Taiwan.

“CSRC” are to the China Securities Regulatory Committee.Commission.

“CVR Shares” are to fully paid shares in the share capital of Yancoal Australia as defined in the amended merger proposal deed for the Gloucester acquisition.

“Directors” as used herein refer to our directors as discussed in Item 6 herein.

“eastern China” are collectively to Shandong Province, Jiangsu Province, Anhui Province, Zhejiang Province, Fujian Province, Jiangxi Province and Shanghai Municipality; “southern China” are to Guangdong Province, Hunan Province and Guangxi Zhuang Autonomous Region; “northern China” are to Beijing Municipality, Tianjin Municipality, Hebei Province, Shanxi Province and the Inner Mongolia Autonomous Region; and “northwestern China” are to Shaanxi Province, Gansu Province, Qinghai Province, Xinjiang Uyghur Autonomous Region and Ningxia Hui Autonomous Region.

“Excluded Assets” are the following assets which are excluded from Yancoal Australia prior to the merger with Gloucester and currently held by Yancoal International (Holding):

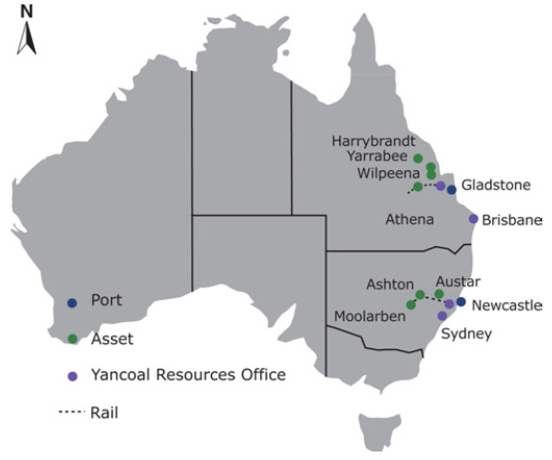

all of the issued shares in Tonford Pty Limited and as a result a 100% interest in the Harrybrandt Project tenements near Nebo in Queensland’s Bowen Basin (“Harrybrandt”);

all of the issued shares in Athena Coal Pty Limited and as a result a 51% interest in the Athena Coal Project joint venture in Queensland (“Athena”);

100% interest in certain Wilpeena tenements held by Yarrabee Coal Company Pty Limited in Queensland (“Wilpeena”);

all of the issued shares in each of Syntech Holdings Pty Limited and Syntech Holdings II Pty Limited and as a result a 100% interest in the Cameby Downs open-pit mine located approximately 30 kilometers from the town of Chinchilla in the Surat Basin, Queensland (“Syntech”);

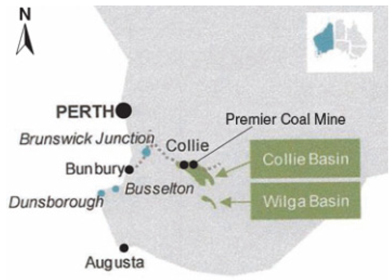

all of the issued shares in Premier Coal Limited (“Premier Coal”) and Premier Char Pty Limited (“Premier Char”) and thereby, among other things, a 100% interest in the Premier Coal Mine (together, “Premier”);

all of the issued shares in Yancoal Technology Development Pty Limited; and

all of the issued shares in UCC Energy Pty Limited.

“Felix” refersare to Yancoal Resources (formerly Felix Resources Limited,Limited).

“FOB” are to Free on Board, meaning the risk passes to the buyer, including payment of all transportation and insurance costs, once goods are delivered on board of the ship by the seller, as defined in the latest edition of the International Rules for the Interpretation of Trade Terms as published by ICC Publishing SA, 38 cours Albert 1er, 75008 Paris, France from time to time or such official rules for interpretation of trade terms as issued by the ICC in substitution therefore as amended from time to time.

“Gloucester” are to Gloucester Coal Ltd., a wholly owned subsidiary of Yancoal Australia Limitedcompany incorporated in Australia, which mainly engages infocuses on the exploration, mining and sale of coal in Australia. We completed the merger with Gloucester in June 2012, which turned Gloucester a wholly-owned subsidiary of Yancoal Australia.

“Grant Thornton” refersare to a registered firm of certified public accountants in the People’s Republic of China and is the principal auditor for the purpose of reporting to the United States Securities and Exchange Commission and other relevant U.S. regulatory bodies.

“Grant Thornton Hong Kong” refersare to a firm of certified public accountants in Hong Kong, Special Administrative Region which wasoriginally practised as a former member firmpartnership under the name of Grant Thornton International LtdJingdu Tianhua and has since changed itsnow operates as a corporate practice under the name to JBPB & Co as of December 10, 2010. (original official name in Hong Kong: Grant Thornton)

“Grant Thornton Jingdu Tianhua” refers to a firm of certified public accountants in Hong Kong Special Administrative Region, which has been a member firm of Grant Thornton International Ltd since November 2010.Hong Kong Limited. This firm is the auditor for the purpose of the Hong Kong H Share listing only.

“H Shares” refersare to overseas listed foreign invested shares in the ordinary share capital of the Company, with nominal value of RMB1.00 each, which are listed on the Hong Kong Stock Exchange.HKSE.

“Haosheng Company” refersare to Inner Mongolia Haosheng Coal Mining Company Limited, a 61% ownedCompany incorporated in the PRC and a 74.82%-owned subsidiary of the Company, which engages in applying for project development and mining rights for Shilawusu Coal Field in the Inner Mongolia Autonomous Region.

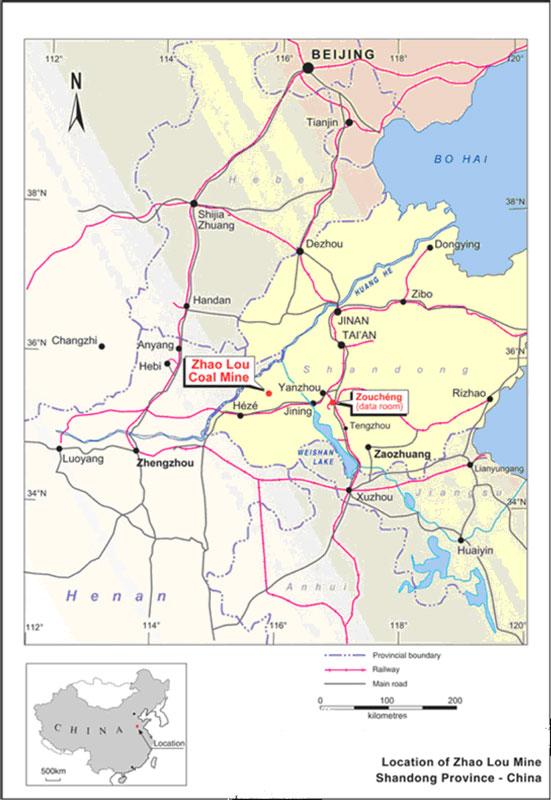

“Heze Nenghua” refersare to Yanmei Heze Nenghua Company Limited, a Company incorporated in the PRC and a 98.33% owned-owned subsidiary of the Company, thatwhich manages our exploration for coal resources at the Juye Mine in Heze City, Shandong Province.

“Hong Kong Listing Rules” are to the Rules Governing the Listing of Securities on the HKSE.

“Hong Kong Stock Exchange” refersor “HKSE” are to The Stock Exchange of Hong Kong Limited.

“Hua Ju Energy” refersare to ShangdongShandong Hua Ju Energy Co., Limited, a Company incorporated in the PRC and a 95.14% owned-owned subsidiary of the Company, thatwhich engages in the generation of electric power from coal gangue and coal slurry, which are by-productsbyproducts of our coal mining process.

“IFRS” refersare to International Financial Reporting Standards, as issued by the International Accounting Standard Board.Board (“IASB”).

“JBPB” refersIndustry Guide 7” are to JBPB &the United States Securities and Exchange Commission Industry Guide 7.

“Inner Mongolia Xintai” are to Inner Mongolia Xintai Coal Mining Company Limited, a company incorporated in the PRC that is a 80%-owned subsidiary of Ordos Neng Hua, which operates the Wenyu Coal Mine in Inner Mongolia Autonomous Region.

“Jiemei Wall Materials” are to Jining Jiemei New Wall Materials Co., Ltd., a firmlimited liability company incorporated in the PRC.

“JORC Code” are to the 2004 Australasian Code for Reporting Exploration Results, Mineral Resources and Ore Reserves prepared by the Joint Ore Reserves Committee of certified public accountantsthe Australasian Institute of Mining and Metallurgy, Australian Institute of Geoscientists and Minerals Council of Australia.

“LIBOR” are to the London Interbank Offered Rate.

“MEP” are to the Ministry of Environmental Protection of the PRC.

“MLR” are to the Ministry of Land and Resources of the PRC.

“MOC” are to the Ministry of Commerce of the PRC.

“MOT” are to the Ministry of Transportation of the PRC.

“MRRT” are to the Minerals Resource Rent Tax, a tax on assessable profits generated from the extraction of coal and iron ore in Hong Kong Special Administrative Region formerly known as Grant Thornton in Hong Kong.Australia.

“NDRC” refersare to the National Development and Reform Commission of the PRC.

“NYSE” refersare to the New York Stock Exchange.Exchange, Inc.

“Ordos Neng Hua” refersare to Yanzhou Coal Ordos Neng Hua Company Limited, a wholly owned subsidiary of the Company that mainly engagesincorporated in the constructionPRC that is principally engaged in the development of a 600,000-tonne methanol project in Ordos Citycoal resources and the development of coal resourceschemical business in the Inner Mongolia Autonomous Region.

“PBOC” refersare to the People’s Bank of China.

“PRC” refersPRC government” are to the People’s Republiccentral, provincial or municipal government of China.the PRC.

“PRC Standards” are to the standards in the Solid Mineral Resource/Reserve Classification of the PRC (GB/T17766-1999).

“Promoter Shares” refersare to the domestic legal person shares held by Yankuang Group.

“SAFE” are to the State Administration of Foreign Exchange of the PRC.

“SASAC” are to the State-owned Assets Supervision and Administration Commission.

“SAT” are to the State Administration of Taxation of the PRC.

“SEC” are to the United States Securities and Exchange Commission.

“SERC” are to the State Electricity Regulatory Commission of the PRC.

“Shanxi Nenghua” refersare to Yanzhou Coal Shanxi Nenghua Company Limited, a wholly owned subsidiary of the Company incorporated in the PRC that manages our investment projects in Shanxi Province.

“Shares” refers collectively to our (i) domestic invested shares listed on the Shanghai Stock Exchange, par value RMB1.00 each (the “Domestic Shares” or “A Shares”), (ii) foreign-invested shares issued and traded in HK dollars and listed on the Hong Kong Stock Exchange, par value RMB1.00 each (the “H Shares”) and (iii) American Depositary Shares, (the “ADSs”), each of which represents ten H Shares.

“Shengyang Wood” are to Shandong Shengyang Wood Co., Ltd., a limited liability company incorporated in the PRC.

“significant subsidiary” are to a significant subsidiary as defined in Rule 1-02 of Regulation S-X under the U.S. Securities Act of 1933.

“SSE” are to the Shanghai Stock Exchange.

“Tianhao Chemicals” refersare to Shanxi Tianhao Chemicals Company Limited, a 99.89% owned-owned subsidiary of Shanxi Nenghua that mainly engagesand a Company incorporated in the PRC, which is principally engaged in the operation of a 100,000 tonne methanol project in Shanxi Province.

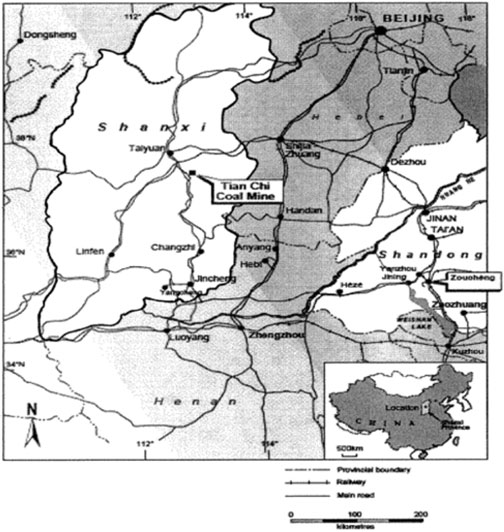

“Tianchi Energy” refers to Shanxi Heshun Tianchi Energy Company Limited, an 81.31% owned subsidiary of Shanxi Nenghua that mainly engages in the operation of Tianchi Coal Mine.

“Tonne” meansare to metric tonne, which is equivalent to 1,000 kilograms or approximately 2,205 pounds.

“Twelfth Five-Year Plan” refersare to the Twelfth Five-Year Plan (2011 to 2015) for National Economic and Social Development in the PRC.

“Yancoal Australia” refersare to Yancoal Australia Limited, an ASX-listed subsidiary of the Company incorporated in Australia that manages our investment projects in Australia, which is 78%-owned by the Company.

“Yancoal Canada” are to Yancoal Canada Resources Co., Ltd., a wholly owned subsidiary of the Company that manages our investment projects in Australia.Canada.

“Yancoal Resources” are to Yancoal Resources Limited, formerly known as Felix Resources Limited (“Felix”), a limited company incorporated under the laws of Australia and an indirect wholly owned subsidiary of Yancoal Australia, which mainly engages in coal mining, sales and exploration of coal.

“Yancoal International (Holding)” are to Yancoal International (Holding) Co., Limited, a wholly owned subsidiary of the Company.

“Yankuang Finance” is Yankuang Group Finance Company Limited, a joint venture established by the Yankuang Group, China Credit Trust Co., Ltd. and Yanzhou Coal Mining.

“Yankuang Group” or “Controlling Shareholder” refersare to Yankuang Group Corporation Limited (formerly known as Yanzhou Mining (Group) Corporation Limited)., a wholly state-owned enterprise established in the PRC, and the Controlling Shareholder of our Company.

“Yulin Nenghua” refersare to Yanzhou Coal Yulin Nenghua Company Limited, a wholly owned subsidiary of the Company that mainly engagesincorporated in the PRC, which is principally engaged in the operation of a 600,000-tonne methanol project in Shaanxi Province.

“Yushuwan Coal Mine Company” refers to Shaanxi Yushuwan Coal Mine Company Limited, a joint venture among the Company, Chia Tai Energy & Chemicals Company Limited and Yushen Coal Company Limited, of which we will hold a 41% equity interest. As of the date of this annual report, the establishment of Yushuwan Coal Mine Company is still pending regulatory approval.

For purpose of this annual report, “Eastern China” refers collectively to Shandong Province, Jiangsu Province, Anhui Province, Zhejiang Province, Fujian Province, Jiangxi Province and Shanghai Municipality; “Southern China” refers to Guangdong Province and Hunan Province and Guangxi Autonomous Region; and “Northern China” refers to Beijing Municipality, Tianjin Municipality, Hebei Province, Shanxi Province and the Inner Mongolia Autonomous Region.

Certain mining terms used in this annual report are defined in the “Glossary of Mining Terms”, which was included as Appendix B to our registration statement on Form F-l that we filed with the U.S. Securities and Exchange Commission. A copy of the “Glossary of Mining Terms” may be obtained upon written request to the Company.

Unless otherwise specified, all references in this annual report to “U.S. dollars”, “USD” or “US$” are to United States dollars, the lawful currency of the United States of America; all references to “HK dollars”, “HKD” or “HK$” are to Hong Kong dollars, the lawful currency of Hong Kong; all references to “AUD” or “A$” are to Australian dollars, andthe lawful currency of Australia; all references to “RMB” are to Renminbi, the lawful currency of the PRC.PRC; all references to “Euro” or “€” are to Euro, the lawful currency of the European Union; and all references to “British Pound” or “£” are to British Pound, the lawful currency of the British Kingdom. Our financial statements are denominated in RMB and, except as otherwise stated, all monetary amounts in this annual report are presented in RMB.

Solely for your convenience, certain items in this annual report contain translations of Renminbi amounts into U.S. dollars, which have been made at the rate of RMB6.6000RMB6.2301 to US$1.00, being the certified exchange rate as set forth in the H.10 weekly statistical release of the Board of Governors of the Federal Reserve BoardSystem of the United States on December 31, 2012. All such translations in this annual report are provided solely for December 30, 2010. Noyour convenience and no representation is made that the Renminbi amounts could have been or could be converted into U.S. dollars at that rate, or at all.

In this annual report, where information has been presented in percentages, or thousands or millions or billions of units, amounts may have been rounded up or down. Accordingly, the amounts identified as total amounts in tables may not be equal to the apparent sum of the amounts listed therein.

In this annual report, business taxes and surcharges have been reclassified as corresponding costs of each category of revenue to provide a more appropriate presentation. The same adjustments have been made to the corresponding prior year. The reclassification has no impact on our overall results. The attention of Shareholders and potential investors is drawn to such adjustments.

Coal resources and reserves are key elements in our Company’s investment decision-making process. The term “resources” describes a concentration or occurrence of material of intrinsic economic interest in or on the Earth’s crust in such form, quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade, geological characteristics and continuity of a mineral resource are known, estimated or interpreted from specific geological evidence and knowledge. The term “reserves” describes the recoverable quantity of coal that is commercially viable for development given the prevailing economic situation, particularly with respect to the prices of coal at the time of estimation. Reserves are estimated using a deterministic method, in which a single best estimate is made based on known geological, engineering and economic data, or a probabilistic method, in which known geological, engineering and economic data are used to generate a range of estimates and their associated probabilities. All coal reserves data are estimates, which are revised when additional information becomes available (for example, when additional coal mines commence operations or when actual coal production or extraction commences). “Proven reserves” refers to estimated quantities of coal that geological and engineering data demonstrate have reasonable certainty of being recovered in future years from known deposits under existing economic and operating conditions (that is, prices and costs at the date the estimate is made). “Probable reserves” refers to the estimated quantities of coal that geological and engineering data demonstrate have fair to good probability of being recovered in future years from known deposits under existing economic and operating conditions. To qualify as proven reserves, there should be at least a 90% probability that the quantities actually recovered will equal or exceed the proven estimate. To qualify as probable reserves, there should be at least a 50% probability that the quantities actually recovered will equal or exceed the proven plus probable estimate. Our total in-place proven and probable reserves are presented to include all mining and preparation losses that occur during the processing of coal after it is mined. Recoverable reserves refer to the amount of in-place proven and probable reserves but exclude all mining and preparation losses that occur during the processing of coal after it is mined. Our estimates of recoverable reserves are reported after deduction of actual production volume and nonaccessibe reserves up to December 31, 2012. Unless otherwise specified, coal reserves and resources are presented on a 100% basis.

A majority of our Company’s total estimated proven coal reserves are located in China and Australia. The coal reserves data in this annual report represent estimates of our Company that were calculated by its internal reserves system, which includes, among others, procedures for classifying and estimating reserves. Our Company believes that the methods it uses to estimate these reserves are consistent with definitions and classifications in Securities Act Industry Guide 7, the JORC Code and the PRC Standards, as applicable, to its PRC and Australian mines. Our Company’s internal geological team focuses on periodically estimating reserves information based on geological data obtained from various geological, geophysical and engineering studies. Estimates of net reserves are based on numerous assumptions and estimates relating to technical factors such as initial coal reserves, initial production rates, production decline rates, ultimate recovery of reserves, as well as commercial factors such as future coal prices, timing and amount of capital expenditures, and operating costs that may occur during the production life of the coal reserves.

Unless otherwise indicated, information regarding our Company’s coal production in this annual report refers to our Company’s share of production based on its percentage of equity interest in the relevant subsidiaries or coal mining projects.

PART I

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| ITEM 3. | KEY INFORMATION |

| A. | Selected Financial Data |

Historical Financial Data

The following table sets forth selected financial data as of and for the years ended December 31, 2006, 2007, 2008, 2009, 2010, 2011 and 2010.2012. The selected income statement and cash flow data for the years ended December 31, 2008, 20092010, 2011 and 20102012 and the selectedsummary balance sheet data as of December 31, 20092010, 2011 and 20102012 have been derived from our audited consolidated financial statements included elsewhere in this annual report and should be read in conjunction with those financial statements and the accompanying notes. Unless otherwise indicated, the financial statements have been prepared and presented in accordance with IFRS, as issued by the International Accounting Standards Board. Our selected income statement and cash flow data for the years ended December 31, 2006 and 2007 and our selected balance sheet data as of December 31, 2006, 2007 and 2008 have been derived from our audited consolidated financial statements for those periods and dates, which are not included in this annual report.IASB.

| As of and for the Year Ended December 31, | ||||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | 2010 | |||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | US$ | |||||||||||||||||||

| (in millions except per Share and per ADS data) | ||||||||||||||||||||||||

INCOME STATEMENT DATA | ||||||||||||||||||||||||

Total revenue(1) | 13,224.3 | 15,403.7 | 25,287.4 | 20,677.1 | 33,944.3 | 5,143.1 | ||||||||||||||||||

Gross sales of coal | 13,058.8 | 15,193.0 | 24,933.3 | 19,947.8 | 32,590.9 | 4,938.0 | ||||||||||||||||||

Railway transportation services income | 165.5 | 210.7 | 255.7 | 267.3 | 513.3 | 77.8 | ||||||||||||||||||

Gross sales of electricity power | — | — | 59.8 | 187.5 | 185.5 | 28.1 | ||||||||||||||||||

Gross sales of methanol | — | — | 38.6 | 258.9 | 629.3 | 95.3 | ||||||||||||||||||

Gross sales of heat supply | — | — | — | 15.6 | 25.2 | 3.8 | ||||||||||||||||||

Transportation costs of coal | (936.6 | ) | (549.8 | ) | (508.7 | ) | (403.3 | ) | (1,160.5 | ) | (175.8 | ) | ||||||||||||

Cost of sales and service provided(1) | (6,470.4 | ) | (7,625.2 | ) | (12,201.1 | ) | (10,590.0 | ) | (16,801.3 | ) | (2,545.7 | ) | ||||||||||||

Cost of electricity power | — | — | (88.3 | ) | (190.8 | ) | (195.5 | ) | (29.6 | ) | ||||||||||||||

Cost of methanol | — | — | (37.8 | ) | (352.9 | ) | (716.8 | ) | (108.6 | ) | ||||||||||||||

Cost of heat supply | — | — | — | (9.7 | ) | (12.5 | ) | (1.9 | ) | |||||||||||||||

Gross profit | 5,817.3 | 7,228.7 | 12,451.5 | 9,130.4 | 15,057.6 | 2,281.5 | ||||||||||||||||||

Selling, general and administrative expenses | (2,230.1 | ) | (2,854.7 | ) | (3,832.0 | ) | (3,820.2 | ) | (5,093.9 | ) | (771.8 | ) | ||||||||||||

Share of income (loss) of an associate | — | (2.4 | ) | (67.4 | ) | 109.8 | 8.9 | 1.3 | ||||||||||||||||

Other income | 165.8 | 198.9 | 351.5 | 311.0 | 3,108.1 | 470.9 | ||||||||||||||||||

Interest expense | (26.3 | ) | (27.2 | ) | (38.4 | ) | (45.1 | ) | (603.3 | ) | (91.4 | ) | ||||||||||||

Profit before income taxes | 3,726.7 | 4,543.3 | 8,865.2 | 5,685.8 | 12,477.3 | 1,890.5 | ||||||||||||||||||

Income taxes | (1,354.7 | ) | (1,315.5 | ) | (2,385.6 | ) | (1,553.3 | ) | (3,171.0 | ) | (480.5 | ) | ||||||||||||

Profit for the year | 2,372.0 | 3,227.8 | 6,479.6 | 4,132.5 | 9,306.3 | 1,410.0 | ||||||||||||||||||

Profit attributable to our equity holders | 2,373.0 | 3,230.5 | 6,488.9 | 4,117.3 | 9,281.4 | 1,406.3 | ||||||||||||||||||

Earnings per Share | 0.48 | 0.66 | 1.32 | 0.84 | 1.89 | 0.3 | ||||||||||||||||||

Earnings per ADS | 4.82 | 6.56 | 13.19 | 8.37 | 18.87 | 2.9 | ||||||||||||||||||

Operating income per Share before income tax | 0.76 | 0.92 | 1.80 | 1.16 | 2.54 | 0.4 | ||||||||||||||||||

Profit from continuing operation per ADS before income tax | 7.58 | 9.24 | 18.02 | 11.56 | 25.37 | 3.8 | ||||||||||||||||||

CASH FLOW DATA | ||||||||||||||||||||||||

Net cash from operating activities | 3,767.2 | 4,558.6 | 7,095.5 | 6,520.1 | 5,399.8 | 818.2 | ||||||||||||||||||

Net cash from (used in) investing activities | (3,625.5 | ) | (3,790.9 | ) | (2,091.5 | ) | (24,842.9 | ) | (5,884.4 | ) | (891.6 | ) | ||||||||||||

Net cash from (used in) financing activities | (1,291.5 | ) | (1,018.7 | ) | (921.7 | ) | 18,503.7 | 1,360.5 | 206.1 | |||||||||||||||

BALANCE SHEET DATA | ||||||||||||||||||||||||

Total current assets | 9,871.9 | 9,908.2 | 14,994.4 | 20,000.9 | 24,281.4 | 3,679.0 | ||||||||||||||||||

Total current liabilities | 3,828.0 | 4,099.5 | 5,297.0 | 10,410.4 | 10,133.9 | 1,535.4 | ||||||||||||||||||

Net current assets | 6,043.9 | 5,808.7 | 9,697.4 | 9,590.5 | 14,147.5 | 2,143.6 | ||||||||||||||||||

Property, plant and equipment | 12,139.9 | 13,524.6 | 14,149.4 | 18,877.1 | 19,874.6 | 3,011.3 | ||||||||||||||||||

Total assets | 23,458.7 | 26,187.4 | 32,338.6 | 62,432.6 | 72,755.9 | 11,023.6 | ||||||||||||||||||

Long-term bank borrowing | 330.0 | 258.0 | 176.0 | 20,911.7 | 22,400.8 | 3,394.1 | ||||||||||||||||||

Equity attributable to our equity holders | 18,931.8 | 21,417.5 | 26,755.1 | 29,151.8 | 37,331.9 | 5,656.3 | ||||||||||||||||||

DIVIDEND DECLARED PER SHARE | ||||||||||||||||||||||||

A and H Shares | 0.22 | 0.20 | 0.17 | 0.40 | 0.59 | 0.09 | ||||||||||||||||||

ADSs | 2.20 | 2.00 | 1.70 | 4.00 | 5.9 | 0.9 | ||||||||||||||||||

| As of and for the Year Ended December 31, | ||||||||||||||||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | 2012 | |||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | US$ | |||||||||||||||||||

| (in millions except per Share and per ADS data) | ||||||||||||||||||||||||

INCOME STATEMENT DATA | ||||||||||||||||||||||||

Total revenue1 | 25,287.4 | 20,677.1 | 33,944.3 | 47,065.8 | 58,146.2 | 9,333.1 | ||||||||||||||||||

Gross sales of coal | 24,933.3 | 19,947.8 | 32,590.9 | 45,181.2 | 56,200.6 | 9,020.8 | ||||||||||||||||||

Railway transportation service income | 255.7 | 267.3 | 513.3 | 476.9 | 464.1 | 74.5 | ||||||||||||||||||

Gross sales of electricity power | 59.8 | 187.5 | 185.5 | 328.0 | 323.6 | 51.9 | ||||||||||||||||||

Gross sales of methanol | 38.6 | 258.9 | 629.3 | 1,059.3 | 1,118.0 | 179.5 | ||||||||||||||||||

Gross sales of heat supply | — | 15.6 | 25.2 | 20.5 | 39.9 | 6.4 | ||||||||||||||||||

Transportation costs of coal | (508.7 | ) | (403.3 | ) | (1,160.5 | ) | (1,248.3 | ) | (2,104.2 | ) | (337.7 | ) | ||||||||||||

Cost of sales and service provided | (12,201.1 | ) | (10,590.0 | ) | (16,801.3 | ) | (25,725.3 | ) | (41,961.5 | ) | (6,735.3 | ) | ||||||||||||

Cost of electricity power | (88.3 | ) | (190.8 | ) | (195.5 | ) | (362.5 | ) | (330.8 | ) | (53.1 | ) | ||||||||||||

Cost of methanol | (37.8 | ) | (352.9 | ) | (716.8 | ) | (930.2 | ) | (911.2 | ) | (146.3 | ) | ||||||||||||

Cost of heat supply | — | (9.7 | ) | (12.5 | ) | (13.8 | ) | (25.1 | ) | (4.0 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Gross profit | 12,451.5 | 9,130.4 | 15,057.6 | 18,785.8 | 12,813.3 | 2,056.7 | ||||||||||||||||||

Selling, general and administrative expenses | (3,832.0 | ) | (3,820.2 | ) | (5,093.4 | ) | (6,570.2 | ) | (7,987.6 | ) | (1,282.1 | ) | ||||||||||||

Share of profit of associates | (67.4 | ) | 109.8 | 8.9 | 68.9 | 142.0 | 22.8 | |||||||||||||||||

Share of loss of jointly controlled entities | — | — | (0.5 | ) | — | (103.2 | ) | (16.6 | ) | |||||||||||||||

Other income | 351.5 | 311.0 | 3,108.1 | 1,075.8 | 2,930.4 | 470.4 | ||||||||||||||||||

Interest expense | (38.4 | ) | (45.1 | ) | (603.3 | ) | (839.3 | ) | (1,448.7 | ) | (232.5 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Profit before income taxes | 8,865.2 | 5,685.8 | 12,477.3 | 12,521.0 | 6,346.2 | 1,018.6 | ||||||||||||||||||

Income taxes | (2,385.6 | ) | (1,553.3 | ) | (3,171.0 | ) | (3,545.4 | ) | (123.9 | ) | (19.9 | ) | ||||||||||||

Profit for the year | 6,479.6 | 4,132.5 | 9,306.3 | 8,975.6 | 6,222.2 | 998.7 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Profit attributable to our equity holders | 6,488.9 | 4,117.3 | 9,281.4 | 8,928.1 | 6,219.0 | 998.2 | ||||||||||||||||||

Earnings per Share | 1.32 | 0.84 | 1.89 | 1.82 | 1.26 | 0.2 | ||||||||||||||||||

Earnings per ADS | 13.19 | 8.37 | 18.87 | 18.15 | 12.64 | 2.0 | ||||||||||||||||||

Operating income per Share before income tax | 1.80 | 1.16 | 2.54 | 2.55 | 1.29 | 0.21 | ||||||||||||||||||

Profit from continuing operation per ADS before income tax | 18.02 | 11.56 | 25.37 | 25.46 | 12.90 | 2.07 | ||||||||||||||||||

CASH FLOW DATA | ||||||||||||||||||||||||

Net cash from operating activities | 7,095.5 | 6,520.1 | 5,399.8 | 17,977.3 | 6,503.6 | 1,043.9 | ||||||||||||||||||

Net cash from (used in) investing activities | (2,091.5 | ) | (24,842.9 | ) | (5,884.4 | ) | (25,611.1 | ) | (3,187.4 | ) | (511.6 | ) | ||||||||||||

Net cash from (used in) financing activities | (921.7 | ) | 18,503.7 | 1,360.5 | 9,441.1 | 1,145.1 | 183.8 | |||||||||||||||||

BALANCE SHEET DATA | ||||||||||||||||||||||||

Total current assets | 14,994.4 | 20,000.9 | 24,281.4 | 30,431.1 | 30,282.4 | 4,860.7 | ||||||||||||||||||

Total current liabilities | 5,297.0 | 10,410.4 | 10,133.9 | 34,721.5 | 28,622.7 | 4,594.3 | ||||||||||||||||||

Net current assets/(liabilities) | 9,697.4 | 9,590.5 | 14,147.5 | (4,290.4 | ) | 1,659.7 | 266.4 | |||||||||||||||||

Property, plant and equipment | 14,149.4 | 18,877.1 | 19,874.6 | 31,273.8 | 39,503.1 | 6,340.7 | ||||||||||||||||||

Total assets | 32,338.6 | 62,432.6 | 72,755.9 | 97,151.6 | 122,702.3 | 19,695.1 | ||||||||||||||||||

Long-term bank borrowing | 176.0 | 20,911.7 | 22,400.8 | 14,869.3 | 33,283.8 | 5,342.4 | ||||||||||||||||||

Equity attributable to our equity holders | 26,755.1 | 29,151.8 | 37,331.9 | 42,634.5 | 45,826.4 | 7,355.6 | ||||||||||||||||||

DIVIDEND PER SHARE | ||||||||||||||||||||||||

A and H Shares | 0.40 | 0.25 | 0.59 | 0.57 | 0.36 | 0.06 | ||||||||||||||||||

ADS | 4.0 | 2.5 | 5.9 | 5.7 | 3.6 | 0.58 | ||||||||||||||||||

| In this annual report, business taxes and surcharges have been reclassified as corresponding costs of each category of revenue to provide a more appropriate presentation. The same adjustments have been made to the corresponding prior year. The reclassification has no impact on the overall results of the Group. The attention of Shareholders and potential investors is drawn to such adjustments. For details, please see Note 2 of the consolidated financial statements attached to this annual report. |

Number of Shares Outstanding

The following table sets forth the number of our A Shares, H Shares and ADSs outstanding as of the dates indicated.

| As of December 31, | ||||||||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||

A Shares | 2,960,000,000 | 2,960,000,000 | 2,960,000,000 | 2,960,000,000 | 2,960,000,000 | |||||||||||||||

H Shares | 1,958,400,000 | 1,958,400,000 | 1,958,400,000 | 1,958,400,000 | 1,958,400,000 | |||||||||||||||

ADSs | 5,461,179 | 3,338,368 | 18,919,105 | 19,403,533 | 19,744,158 | |||||||||||||||

A Shares H Shares ADS As of December 31, 2008 2009 2010 2011 2012 2,960,000,000 2,960,000,000 2,960,000,000 2,960,000,000 2,960,000,000 1,958,400,000 1,958,400,000 1,958,400,000 1,958,400,000 1,958,400,000 18,919,105 19,403,533 19,744,158 13,933,698 12,915,380

Exchange Rate Information

The following table sets forth information concerning exchange rates between the Renminbi and the U.S. dollar for the periods indicated. These rates are provided solely for your convenience and are not necessarily the exchange rates that we use in this annual report or will use in the preparation of our periodic reports or any other information to be provided to you. The source of these rates is the Federal Reserve H.10 Statistical Release.

Period | Period End | Average(1) | High | Low | ||||||||||||

| (expressed in RMB per US$) | ||||||||||||||||

2005 | 8.0702 | 8.1826 | 8.2765 | 8.0702 | ||||||||||||

2006 | 7.8041 | 7.9579 | 8.0702 | 7.8041 | ||||||||||||

2007 | 7.2946 | 7.5806 | 7.8127 | 7.2946 | ||||||||||||

2008 | 6.8225 | 6.9193 | 7.2946 | 6.7800 | ||||||||||||

2009 | 6.8259 | 6.8295 | 6.8470 | 6.8176 | ||||||||||||

2010 | 6.6000 | 6.7603 | 6.8330 | 6.6000 | ||||||||||||

October | 6.6707 | 6.6678 | 6.6912 | 6.6397 | ||||||||||||

November | 6.6670 | 6.6538 | 6.6892 | 6.6330 | ||||||||||||

December | 6.6000 | 6.6497 | 6.6745 | 6.6000 | ||||||||||||

2011 | ||||||||||||||||

January | 6.6017 | 6.5964 | 6.6364 | 6.5809 | ||||||||||||

February | 6.5713 | 6.5761 | 6.5965 | 6.5520 | ||||||||||||

March | 6.5483 | 6.5645 | 6.5743 | 6.5483 | ||||||||||||

April | 6.4900 | 6.5224 | 6.5477 | 6.4900 | ||||||||||||

May | 6.4786 | 6.4957 | 6.5073 | 6.4786 | ||||||||||||

June (through June 17, 2011) | 6.4700 | 6.4785 | 6.4830 | 6.4700 | ||||||||||||

Period | Period End | Average(1) | High | Low | ||||||||||||

| (expressed in RMB per US$) | ||||||||||||||||

2006 | 7.8041 | 7.9579 | 8.0702 | 7.8041 | ||||||||||||

2007 | 7.2946 | 7.5806 | 7.8127 | 7.2946 | ||||||||||||

2008 | 6.8225 | 6.9193 | 7.2946 | 6.7800 | ||||||||||||

2009 | 6.8259 | 6.8295 | 6.8470 | 6.8176 | ||||||||||||

2010 | 6.6000 | 6.7603 | 6.8330 | 6.6000 | ||||||||||||

2011 | 6.2939 | 6.4475 | 6.6364 | 6.2939 | ||||||||||||

2012 | 6.2301 | 6.3093 | 6.3449 | 6.2221 | ||||||||||||

October | 6.2265 | 6.2338 | 6.2454 | 6.2221 | ||||||||||||

November | 6.2301 | 6.2328 | 6.2502 | 6.2251 | ||||||||||||

December | 6.2186 | 6.2215 | 6.2303 | 6.2134 | ||||||||||||

2013 | ||||||||||||||||

January | 6.2213 | 6.2323 | 6.2438 | 6.2213 | ||||||||||||

February | 6.2301 | 6.3093 | 6.3449 | 6.2221 | ||||||||||||

March | 6.2108 | 6.2154 | 6.2246 | 6.2105 | ||||||||||||

April (through April 19, 2013) | 6.1772 | 6.1926 | 6.2078 | 6.1720 | ||||||||||||

| (1) | Determined by averaging the rates on the last business day of each month during the respective period, except for monthly averages, which are determined by averaging the rates on each business day of the month. |

On June 17, 2011,April 19, 2013, the noon buying rate was US$1.00 = RMB6.4700.RMB6.1772.

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

Our business, financial condition and results of operations are subject to various changing business, industry, competitive, economic, political and social conditions in China and worldwide. In addition to the factors discussed elsewhere in this annual report, the following are some of the important factors that could cause our actual results to differ materially from those projected in any forward-looking statements.

Risks Relating to Our Business and Industry

Our business and profitability are affected by global economic conditions.

The coal industry depends on general economic conditions, including the strengthconditions of global and local economies. In 2008 and 2009,For the past several years, the economies of the United States, Europe and certain countries in Asia experienced a severe and prolonged recession and China experienced a slowdown in overall economic growth, which has led to a reduction in economic activity. Moreover, the economic conditions in Europe remain uncertain. In 2010,this regard, following GDP growth of 9.2% in 2011 and 7.8% in 2012, according to statistics published by the average selling priceNational Bureau of Statistics of the PRC, the PRC maintained its GDP growth target for 2013 at approximately 7.5% in the face of continuing global turbulence and pressing domestic demand for economic restructuring. In the first quarter of 2013, the PRC’s GDP grew at an annualized rate of 7.7%, according to statistics published by the National Bureau of Statistics of the PRC. Australia’s overall economy, as well as its export-oriented coal industry, has also been adversely affected by these developments. Australia experienced GDP growth of 3.4% in 2012 and, according to the Reserve Bank of Australia, Australia’s GDP was expected to grow by 3.0% in 2013, lower than its actual growth in 2012. From late 2008 to mid-2009, the export prices of thermal coal in the PRC experienced fluctuations dueand Australia each decreased significantly. Since late 2009, the export prices of thermal coal in China and Australia have recovered but continue to globalfluctuate. In addition, in the period from February 2011 to April 2012, demand for semi-hard coking coal declined considerably and local economic conditions. In spitedemand for semi-soft coking coal also declined.

We expect that the export coal market and, in particular, the semi-soft coking coal segment of certainthe market, will remain weak for the balance of the current financial year. Despite policies and initiatives implemented by the PRC government to alternately stimulate and then moderate economic conditions, we cannot assure you that another recession would not occur or that a decline in overall economic conditions would notmay recur in the future. In the event of such a recession or decline in economic conditions, whether globally, locally in the PRC or Australia or in our other major markets, our business and profitability may be materially and adversely affected. We cannot assure you thatIn addition, increases in inflation and the consumer price index may put pressure on governments to maintain caps on the price of coal and to subsidize power generation companies. At various times, the PRC government will notor Australian governments may implement tightening policies to managestimulate or slow the growth of the economy or to control an overheated economy in the future which may, in turn, affect coal prices. In the event that this occurs, our business, results of operations and profitabilityfinancial condition may be materially and adversely affected.

Our business, and results of operations and financial condition depend on the volatile domestic and international coal markets.

Coal sales accounted for 96.0%, 96.0% and 96.7% of our revenues in 2010, 2011 and 2012, respectively, and we expect our coal sales to continue to account for a substantial portion of our revenue. As we derive a substantial portion of our revenue from sales of coal and coal-related products, our business and operating results depend heavily upon supply and demand for coal and coal-related products in the domestic and international coal markets. Accordingly, we are vulnerable to downturns in the demand for coal, increases in supply of coal through new or expanded coal production and declines in coal prices.

The prices of coal and coal-related products have historically been historically volatile and fluctuate in response to general economic conditions, supply and demand and the level of global inventories. FromIn 2012, the fourth quarter of 2008 through early 2009, the demand for coal decreased significantly as a result of thesluggish global financial crisis. Since 2009,economy has led to weak demand for coal in Chinaboth the PRC and worldwide, alongthe overseas markets and the average selling price of our coal products decreased as compared with coal prices, has substantially recovered.that of 2011. The average selling price of our coal products was RMB663.9, RMB529.2RMB663.5, RMB707.7 and RMB663.5RMB599.3 per tonne in 2008, 20092010, 2011 and 2010, respectively. However, we2012, respectively, representing a drop of RMB108.4 per tonne from 2011 to 2012, which in turn had a direct and adverse impact on our sales income. Our operating profit also decreased by 30.7% from 2011 to 2012. We cannot assure you that demand for and prices of coal will not further decline, again, the occurrence of which may adversely affect our business, results of operations.operations and financial condition.

Global coal demand correlates strongly with the global economy and the performance of coal-consuming industries, including but not limited to the power generation, chemical, metallurgy and construction materials industries. In addition, the availability and prices of alternative energy sources to coal, as well as international shipping costs, also affect coal demand. Coal supply on the other hand, is primarily affected by the geographicalgeographic location of coal reserves, transportation capacity, the level of domestic and international coal supplies and the type, quality and price of coal from othervarious producers. Developments in the international coal market may adversely affect our overseas sales, which we expect to increase following the expansion of our Australian operations.sales. A significant increase in global coal supply or reduction in demand for coal from key consuming industries may decrease coal prices, which in turn may significantly reduce our profitability and adversely affect our business, and results of operations.operations and financial condition.

The PRC government’s new policy on removing state-sponsored contracts and ceasing to reserve allocations of railway capacity for thermal coal transportation may materially and adversely affect our business, results of operations, financial condition and prospects.

Historically, power utilities purchased coal either on the spot market or through the annual NDRC coordinated contracts. The prices negotiated under this system were lower than prevailing market prices on the spot market and many producers were unwilling to fulfill their contracts when market prices were higher than contract prices. In December 2012, the NDRC announced a policy to change the Chinese domestic thermal coal pricing mechanism. The stated goal of the policy is to eliminate the state-controlled annual contracts which currently govern a large share of domestic coal sales. At the same time, the NDRC has also ceased reserving allocations of railway capacity for thermal coal transportation. Similarly, the stated aim of the new railway capacity ruling is to force coal producers and power utilities to compete with other railway users and negotiate directly with local railway departments.

By removing these state-sponsored contracts, the intended aim of the NDRC policy change is to expose domestic thermal coal pricing to market forces and encourage coal suppliers and power utilities to reach medium- to long-term contracts. The policy change of thermal coal transportation capacity reservation is intended to encourage sales to local customers and stable supply agreements between miners and power plants. However, we cannot assure you that we will obtain enough coal sale contracts without the coordination of the NDRC, or obtain sufficient railway capacity for thermal coal transportation under the new policy, to sustain our historical operating results. As a result, our business, results of operations, financial condition and prospects may be materially and adversely affected.

OurWe derive a significant portion of our revenue from a limited number of customers, and the loss of, or a significant reduction in, sales to any of these customers could materially and adversely affect our business, results of operations and financial condition.

For the years ended December 31, 2010, 2011 and 2012, our top five customers accounted for 24.7%, 19.4% and 19.4% of our revenue, respectively, and sales to our largest customer accounted for 13.0%, 8.5% and 6.3% of our revenue, respectively. We expect that our results of operations will continue to depend on sales to a limited number of customers for the foreseeable future. We may not be able to rely on these customers for revenue generation in the future. We may lose these customers due to the intensified competition. See “— Competition in the PRC and the international coal industry is dependentintensifying, and we may not be able to maintain our competitiveness.” We may also experience reduction, delay or cancellation of orders from one or more of our significant customers, and any decline in the businesses of our customers could also reduce their purchases of our products. The loss of sales to any of these customers could have a material adverse effect on short-termour business, results of operations and financial condition.

We face risks associated with our sales contracts and lettersstrategic framework agreements, which may materially and adversely affect our business, results of intent.operations and financial condition.

In 2008, 2009 and 2010, the majoritySales of our coal produced in China are made primarily on the spot market or pursuant to strategic framework agreements and to a lesser extent, pursuant to sales income (the invoiced amountcontracts. Sales of our coal sold net of returns and discounts) of coal was derived from short-term sales contracts or letters of intent. Theseproduced in Australia are made pursuant to sales contracts and lettersspot market sales. Our PRC sales contracts generally have terms of intentone year and specify the price, quantity and quality of coal and delivery schedule of coal. Our Australian sales contracts generally have terms of one year and specify the quantity and quality of coal and delivery schedule of purchases for a termcoal, while the purchase price is determined every month or quarter by our customer and us, subject to market conditions. In 2012, due to the volatile international coal markets, customers purchasing our coal produced in Australia generally not exceeding one year. Ifentered into quarterly contracts with us. As such, if we experience a weak coal pricing environment that results in a decline in coal prices at the time of actual sale,delivery, our revenue and profitability wouldmay be reduced.

Historically,materially and adversely affected. In addition, our customers have performed a significant majority of their purchase obligations under the sales contracts and letters of intent with us. However, a significant increase in the proportion of unperformed sales contracts and letters of intent or unrealized sales could have a material adverse impact on our results of operations ifare not automatically renewable. If we are not able to locate alternative purchasersmaintain our sales contracts with our major customers on terms commercially acceptable to us or at all, our business, results of operations and financial condition may be adversely affected.

In addition, the strategic framework agreements used in the sales of our coal produced in China generally only specify the quantity and quality of coal, while the purchase price is determined in the annual or monthly sales contracts we enter into under the strategic framework agreements. As a result, we are subject to market conditions at the similar leveltime of profitability. Furthermore, any changes in the cost or availability of labor, raw materials or transportation or volatility in foreign exchange rates during the period between the formation and performance of these sales contracts andactual delivery. Moreover, as letters of intent are not legally binding, customers entering into letters of intent with us are not obligated to purchase the agreed quantity of products, or any products at all. In addition, in accordance with industry practice, our customers do not enter into long-term contracts (those exceeding one year) with us. Therefore, we do not have long-term commitments from our customers to purchase our products, and our customers may reduce or stop purchasing products from us for various reasons, which may also materially and adversely affect our ability to perform our contractual obligations or our profitability.business, results of operations and financial condition.

Our products may be subjectWe rely primarily on ports, highways and third party operated railway systems in the PRC and Australia to governmental price control measures,deliver our coal, any major disruption of which may adversely affect our profitability.business, results of operations and financial condition.

Although the PRC government has implemented measures to overhaul historical price and supply controls and continues to support the development of a market-orientated PRC coal market, it may intervene in the domestic coal market from time to time through the use of macroeconomic measures to stabilize the market and achieve national social and economic goals. For example, the State Council of China and the NDRC published announcements in November and December 2010, respectively, imposing price caps on coal sold pursuant to key thermal coal supply agreements imposed with reference to the coal prices of the agreements entered into by the relevant enterprises in 2010. Such price caps were reemphasized by the NDRC in announcements issued in April 2011. These price-intervention measures may limit the degree of control we have over certain aspects of our business and may have a negative impact on our operations, pricing and profitability.

We rely primarily on the PRC nationalhighways and our own railway network, as well as third party operated railway system, to deliver our products.

We rely on the PRC national railway system, as well as our railway network, to deliver coal to customers.customers in China. We generated approximately 33.6%, 32.1% and 22.7% of our sales income (the invoiced amountalso deliver small volumes of coal sold net of returnsthrough ports and discounts) ofcanals. Coal resources and production in China are mainly located in northern and northwestern China, while coal products soldconsumption is primarily in eastern and transported on the PRC state-ownedsouthern China. As a result, coal suppliers must transport coal via third party operated railway system (exclusive of coal transported on our own railway network) in 2008, 2009 and 2010, respectively.systems from major supply areas to major demand areas. Although the PRC government has taken steps to upgrade and expand the national railway system,systems, its current capacity is not sufficient to meet the entire domestic coal transportation requirement.demand resulting from regional imbalances. Even though our domestic customers are mainly located in Easterneastern China, where the railway system is relatively more developed than other regions of China, our ability to deliver coal is still restricted by the transportation capacity. Pursuant to the Twelfth Five-Year Plan, the PRC government plans to construct several railways for coal transportation in cities in northern China and northwestern China, such as Shanxi Province, Shaanxi Province and the Inner Mongolia Autonomous Region. However, as it will take a significant amount of time for the relevant PRC authorities to grant approvals and permits and to complete the construction of the railway, we anticipate that we will continue to face challenges with respect to access to railway transportation. In addition to railway transportation, we use major coal shipping ports along the coast of China to deliver coal to customers located along the coastal regions of China. However, we cannot assure you that we willmay not be able to continue securing sufficient railway andor port capacity to deliver our coal or that we will notand may experience any material delivery delays or substantial increases in transportation costs as a result of insufficient railway capacity. For details about

In Australia, we rely substantially on third party operated railway networks to deliver coal to ports in New South Wales and Queensland, for onward shipping to our sales incomecustomers. We generally enter into transportation agreements with national and privately operated railway networks, rail haulage operators and ports to secure transportation capacity, generally for terms of coal, please referfive to “Item 5. Operatingten years and Financial Review and Prospects — Coal Business”.

The coal reserve data in this annual report are only estimates, which may differ materially from actual results.

Our coal reserve data are only estimates, which may differ materially from actual reserves. Our reserve estimates may change substantially if new information becomes available. There are inherent uncertainties in estimating reserves, which requiregenerally on a “take or pay” basis. As the consideration of a number of factors, assumptions and variables, many of which may be beyond our control and cannot be ascertained despite due investigation. Our actual results of operations may differ materially from our long-term business and operational plans, which aretransportation capacity secured by these agreements is based on assumed production volume, we may not have sufficient capacity if our actual production volume exceeds our estimated production volume. Conversely, we may have excess transportation capacity (which, in the case of “take or pay” agreements, we will have to pay for even if unused) if our actual production volume is lower than our estimated production volume. In 2012, the sluggish global economy led to weak demand for coal reserve estimates.in both the PRC and overseas markets. We expect that global economic conditions will remain uncertain and international coal markets to continue to be volatile in 2013, and as a result, we cannot assure you that we will fully use the transportation capacity secured on a “take or pay” basis. In addition, we may not adjustbe able to secure sufficient transportation capacity to deliver our coal reserve estimates downward in the future and may experience material delivery delays or substantial increases in such event,transportation costs as a result of insufficient transportation capacity, which may also adversely affect our long-term productionbusiness, results of operations and the useful life of our mines may be materially and adversely affected.financial condition.

Competition in the PRC and the international coal industry is intensifying, and we may not be able to maintain our competitiveness.

We face competition in all aspects of our business, including pricing, production capacity, coal quality and specifications, transportation capacity, cost structure and brand recognition. Our coal business competes in the domestic and international markets with other large domestic and international coal producers. OngoingThe ongoing consolidation in the PRC and Australian coal industry has increased the level of competition we face in China.our core business. In addition, countries such as Mongolia and U.S. have significantly increased their coal exports, which has intensified the competition among international coal exporters. Our competitors may have higher production capacities, stronger brand names and more financial, marketing, distribution and other resources than we do.

We may not be able to maintain our competitiveness if changes or developments in the market weaken our existing competitive advantages. We cannot assure you that efforts takenEfforts by our competitors to improve the quality of their coal will not erode themay render obsolete or irrelevant any quality advantage we have over them. Continual improvements in China’s transportation infrastructure, particularly the national railway transportation network, may diminish our proximity advantage of being located in Eastern China, the region with the highest coal demand in the PRC. Our principal competitors are located predominately in Shanxi Province, Shaanxi Province and the Inner Mongolia Autonomous Region, where there have been occasional rail capacity shortages and the costs of transporting coalfailure to Eastern China are more significant. However, the PRC government has constructed and plans to continue constructing additional railways to transport coal from northern and northwestern China to Eastern China. The completion of these railway projects may increase the supply of coal to customers in Eastern China, increasing the effective supply of coal, whichcompete effectively may have a material adverse impact on our business, results of operations and financial condition.

We may not be able to meet our capital expenditure requirements or secure additional external financing in the future.

Our business is capital intensive and will require substantial expenditures for, among other things, the acquisition of equity interests in and assets of coal mines as well as mining rights, purchase of and investment in properties, machinery and equipment and operational capital expenditures. In 2010, 2011 and 2012, our total capital expenditures were approximately RMB3,785.3 million, RMB23,336.4 million and RMB20,809.2 million, respectively, largely due to investment in our core coal businesses. We intend to use cash on hand, funds from operations and additional debt and equity financing to finance our capital expenditures going forward. However, we may not be able to obtain sufficient amounts of capital in a timely manner, on terms acceptable to us, or at all, which could result in a material adverse effect on our business, results of operations and financial condition.

In recent years, the size of our interest-bearing debt obligations has increased along with our expansion plans. In May and July 2012, we issued U.S. dollar and RMB denominated corporate bonds in aggregate principal amounts of US$1.0 billion and RMB5.0 billion, respectively. As of December 31, 2012, we had approximately RMB40,996.4 million in bank borrowings, of which approximately RMB7,712.6 million is due within a year and approximately RMB33,283.8 million is due after one year. In the first quarter of 2013, we entered into several U.S. dollar and RMB denominated loan agreements for aggregate amounts of US$601.4 million and RMB700 million. This level of debt could have significant consequences for our operations, including reducing the availability of our cash flow to fund working capital, capital expenditures, acquisitions and other general corporate purposes as a result of our debt servicing obligations, limiting our flexibility in planning for, or reacting to, and increasing our vulnerability to, changes in our business, our industry and the general economy and potentially limiting our ability to obtain, or increasing the cost of, any additional financing. In addition, our business plans may change from time to time due to changing circumstances, new opportunities or unforeseen contingencies. If we change our business plans, we may need to obtain additional external financing which may include bank borrowings or issuances of debt securities to meet our capital expenditure plans. If we raise additional funds through debt financing, our interest and debt repayment obligations will increase and we may be subject to additional covenants that could limit our ability to access cash flows from operations. We may not be able to raise sufficient financing to fund our future capital expenditures and service our debt obligations or at all. Failure to obtain sufficient financing could cause delays or abandonment of business development plans and have a material adverse effect on our business, results of operations and financial condition.

The coal reserve data in this annual report are only estimates, which may differ materially from actual reserve amounts.

Our coal reserve data are only estimates, which may differ materially from actual reserve amounts. There are inherent uncertainties in estimating reserves, which require the consideration of a number of factors, assumptions and variables, many of which may be beyond our control and cannot be ascertained despite due investigation. Our reserve estimates may change substantially if new information becomes available.

In addition, reserve data for certain of our PRC mines are estimated in accordance with Industry Guide 7 for proven and probable reserves and the JORC Code for reserves. Reserve data for our Australian mines are typically estimated in accordance with the JORC Code. As the mining standards and mining terminology of the JORC Code may differ substantially from Industry Guide 7, our reserve data may materially vary when we compile and present such data. As such, our actual results of operations may differ materially from our long-term business and operational projections, which are based on our coal reserve estimates. We may adjust our coal reserve estimates downward in the future, and in such event, our long-term production and the useful lives of our mines may be materially and adversely affected.

Our business, results of operations and financial condition depend on in part our ability to continue acquiring or developing suitable coal reserves.

The recoverable coalCoal reserves in our existing mines decline as we produce coal.coal is produced. Due to the limitation on our ability tolimitations in significantly increaseincreasing our production capacity at existing mines, such as Jining II Coal Mine, Jining III Coal Mine and Tianchi Coal Mine, the increase inour ability to expand our coal production capacity depends on theour development of coal reserves, we developed recently or will develop in the future, as well as our newly acquired coal resources.

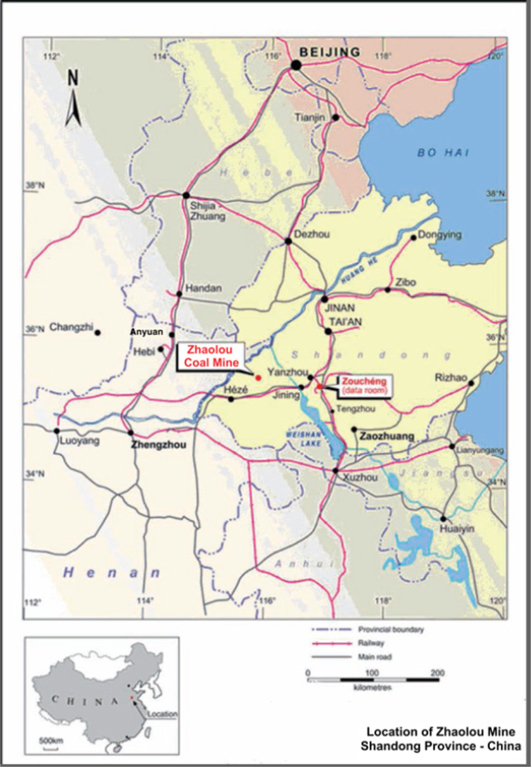

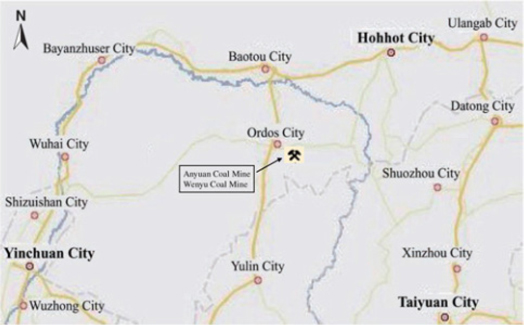

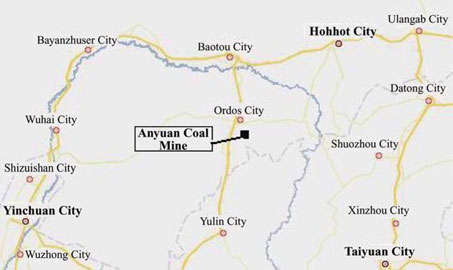

We acquired the mining rights of Zhaolou Coal Mine through Heze Nenghua in May 2008,reserves and commenced production at Zhaolou Coal Mine in December 2009. On December 23, 2009, we completed the acquisition of the entire equity interest in Felix, which had an equity interest in three operational minesresources domestically and three exploratory mines. In December 2009, we established Ordos Neng Hua to manage our investments in the Inner Mongolia Autonomous Region, including a coal mining project. In 2010, Ordos Neng Hua acquired a 100% equity interest in a 600,000 tonnes methanol project. We acquired the entire assets of Anyuan Coal Mine in December 2010, which has commenced production in early 2011. We also obtained a 61% equity interest in Haosheng Company as of the date of this annual report. We are also in the process of establishing an associate company for a coal mining project in Yushuwan, Shaanxi Province. For more information about the development and acquisition of our coal resources, please refer to “Item 4. Information on the Company — History and Development of Our Company” in this annual report.overseas.

The acquisition of new mines by PRC coal companies, either within China or overseas, and the procurement of related licenses and permits are subject to PRC government approval.approvals. Delays or failures in securing or failure to secure relevantthe required PRC government approvals, licenses or permits, as well as any adverse change in government policies, may hinder our expansion plans, which may materially and adversely affect our future profitability and growth prospects. In connection with overseas acquisitions and expansion, we may encounter challenges due to our unfamiliarity with local laws and regulations, and may suffer foreign exchange losses on overseas investments or face political or regulatory obstacles to acquisitions. We cannot assure you thatAs a result of these challenges, our overseas expansion plans and investments willmay not be successful.successful and may not achieve our anticipated results.

We cannot assure you thatIn addition, the acquisition of new mines or the grant of mining leases in Australia are subject to approval under Australia’s foreign acquisition legislation and policy, including the Foreign Acquisitions and Takeovers Act 1975, which is administered by the Treasurer of Australia acting through the Foreign Investment Review Board. Such foreign investment approvals may be granted subject to conditions imposed by the Treasurer of Australia. This foreign investment regime subjects us to additional risks and uncertainties, and may adversely impact our ongoing and potential expansion plans in Australia.

Moreover, we willmay not be able to continue to identify suitable acquisition targets or acquire these targets on competitive terms, andat an acceptable cost or in a timely manner. We may not be able to successfully develop new coal mines or expand our existing ones in accordance with our development plans, or at all. Failure to successfully acquire suitable targets on competitive terms, develop new coal mines or expand our existing coal mines could have an adverse effect on our competitiveness and growth prospects.

We may experience difficulty integrating our acquisitions, which could result in a material adverse effect on our business, results of operations and financial condition.

We may from time to time expand our business through acquisitions of other coal mining companies, assets or other coal or mining-related businesses. We are devoting significant resources to the integration of our operations in order to achieve the anticipated synergies and benefits of the acquisitions and expansion.

Acquisitions and expansion involve uncertainties and a number of risks, including:

difficulty in integrating the assets, operations and technologies of the acquired companies or assets, including their employees, corporate cultures, managerial systems, processes and procedures and management information systems and services;

complying with the laws, regulations and policies applicable to the acquired businesses;

failure to achieve the objectives or benefits, or to generate sufficient revenue to recover the costs and expenses, resulting from the acquisition and integration of such companies or assets;

managing relationships with employees, customers and business partners during the course of integrating new businesses;

integrating other acquired employee groups with our employee groups and on maintaining productive employee relations;

attracting, training and motivating members of our management and workforce;

accessing our capital resources and internally generated funds to fund acquisitions, which may divert financial resources otherwise available for other purposes;

strengthening our operational, financial and management controls, particularly those of our newly acquired assets and subsidiaries, to maintain the reliability of our reporting processes;

difficulty in exercising control and supervision over the newly acquired operations, including failure to implement and communicate our safety management procedures resulting in additional safety hazards and risks;

potential ongoing financial obligations and unforeseen or hidden liabilities of the acquired companies or coal or potash-related businesses; and

failure to diversify our operations to include new products or successfully manage our operations in new markets, such as potash.

In the event that we are unable to efficiently and effectively integrate newly acquired companies or coal or potash-related businesses into our Company, we may be unable to achieve the objectives or anticipated benefits of such acquisitions, which may adversely impact our business, results of operations and financial condition. In addition, we may have to write down the carrying value of the intangible assets associated with any acquired companies, which could adversely affect our earnings.

Our merger with Gloucester may not strengthen our coal mining operations and market profile, globally and in Australia, as we expect.

In June 2012, Gloucester became a wholly owned subsidiary of Yancoal Australia, and the Company and Gloucester shareholders held 78% and 22%, respectively, of the ordinary share capital of Yancoal Australia. However, as a condition of the foreign investment approval for our merger with Gloucester, we are required by the Treasurer of Australia to reduce our economic ownership in Yancoal Australia to less than 70% by December 31, 2013, and our economic ownership must not exceed 70% thereafter. In addition, we must reduce our economic ownership in Yancoal Resources’s underlying assets to no more than 50% by December 31, 2013.

Although we believe this transaction has significantly increased our total resource base and strengthened our coal mining operations and market profile in Australia and globally, we may face difficulty integrating the operations of Gloucester. The continued integration of Yancoal Resources and Gloucester into Yancoal Australia specifically may be affected by uncertain mining conditions.