Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 606,407,693.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of RegulationS-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☐☒ No ☒☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or anon-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule12b-2 of the Exchange Act. (Check one):

Large Accelerated filer ☒ Accelerated filer ☐

| Large Accelerated filer ☒ | Accelerated filer ☐ | Non-Accelerated filer ☐ | |

| Emerging Growth Company ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule12b-2 of the Exchange Act). Yes ☐ No ☒

i

Throughout this annual report on Form20-F we make numerous references to “LATAM”. Unless the context otherwise requires, references to “LATAM Airlines Group” are to LATAM Airlines Group S.A., the unconsolidated operating entity, and references to “LATAM,” “we,” “us” or the “Company” are to LATAM Airlines Group S.A. and its consolidated affiliates: Transporte Aéreo S.A. (which does business under the name “LATAM(“LATAM Airlines Chile”), LATAM Airlines Peru S.A. (f/k/a LAN Perú S.A. (“LATAMPeru S.A, “LATAM Airlines Peru”), Aerolane, Líneas Aéreas Nacionales del Ecuador S.A. (“LATAM Airlines Ecuador”), LAN Argentina S.A. (“LATAM Airlines Argentina,” previously Aero 2000 S.A.), Aerovías de Integración Regional, Aires S.A. (which does business under the name “LATAM(“LATAM Airlines Colombia”), TAM S.A. (“TAM” or “LATAM Airlines Brazil”), LAN Cargo S.A. (“LATAM Cargo”) and its threetwo regional affiliates: Aero Transportes Mas de Carga S.A. de C.V. (“MasAir”) in Mexico, Linea Aerea Carguera de Colombia S.A. (“LANCO”) in Colombia and Aerolinhas Brasileiras S.A. (“ABSA”) in Brazil. Other references to “LATAM”, however,as the context requires, are to the LATAM brand which was launched in 2016 and brings together, under one internationally recognized name, all of the affiliate brands such as LATAM Airlines Chile, LATAM Airlines Peru, LATAM Airlines Argentina, LATAM Airlines Colombia, LATAM Airlines Ecuador and LATAM Airlines Brazil.

References to “LATAM” and all references to “LAN” are to LAN Airlines S.A., currently known as LATAM Airlines Group S.A., and its consolidated affiliates, in connection with circumstances and facts occurring prior to the completion date of the combination between LAN Airlines S.A. and TAM S.A. See “Item 4. Information on the Company—A. History and Development of the Company—Combination of LAN and TAM.Company.”

In this annual report on Form20-F, unless the context otherwise requires, references to “TAM” are to TAM S.A., and its consolidated affiliates, including TAM Linhas Aereas S.A. (“TLA”), which does business under the name “LATAM Airlines Brazil”, Multiplus S.A. (“Multiplus”), Fidelidade Viagens e Turismo Limited (“TAM Viagens”) and Transportes Aéreos Del Mercosur S.A. (“TAM Mercosur”).

LATAM Airlines Group and the majority of our affiliates maintain their accounting records and prepare their financial statements in U.S. dollars. Some of our other affiliates, however, maintain their accounting records and prepare their financial statements in Chilean pesos, Argentinean pesos, Colombian pesos or Brazilian reais.real. In particular, TAM maintains its accounting records and prepares its financial statements in Brazilian reais.real. Our audited consolidated financial statements include the results of these affiliates translated into U.S. dollars. International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”), require assets and liabilities to be translated atperiod-end exchange rates, while revenue and expense accounts are translated at each transaction date, although a monthly rate may also be used if exchange rates do not vary widely.

In this annual report on Form20-F, all references to “Chile” are references to the Republic of Chile. This annual report contains conversions of certain Chilean peso and Brazilian real amounts into U.S. dollars at specified rates solely for the convenience of the reader. These conversions should not be construed as representations that the Chilean peso and the Brazilian real amounts actually represent such U.S. dollar amounts or could be converted into U.S. dollars at the rate indicated. Unless we specify otherwise, all references to “$”, “US$”, “U.S. dollars” or “dollars” are to United States dollars, references to “pesos,” “Chilean pesos” or “Ch$” are to Chilean pesos. References to “reais,“real,” “Brazilian reais”real” or “R$” are to Brazilian reais,real, and references to “UF” are toUnidades de Fomento, a daily indexed Chilean peso-denominated monetary unit that takes into account the effect of the Chilean inflation rate. Unless we indicate otherwise, the U.S. dollar equivalent for information in Chilean pesos used in this annual report and in our audited consolidated financial statements is based on the “dólar observado” or “observed” exchange rate published byBanco Central de Chile (which we refer to as the Central Bank of Chile) on December 31, 2016,2019, which was Ch$669.47744.62 = US$1.00. The observed exchange rate on, February 28, 2017,March 18, 2020, was Ch$645.19=855.09 = US$1.00. Unless we indicate otherwise, the U.S. dollar equivalent for information in Brazilian reaisreal used in this annual report and in our audited consolidated financial statements is based on the average “bid and offer rate”published by Banco Central do Brasil (which we refer to as the Central Bank of Brazil) on December 31, 2016,2019, which was R$3.2594.03 = US$1.00. The observed exchange rate on February 28, 2017March 18, 2020, was $R$3.099R$5.11 = US$1.00. The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos or Brazilian reais.real.

LATAM has a single series of shares of Common Stock, without par value, listed on Chilean Stock Exchange and American Depositary Shares (evidenced by American Depositary Receipts), each representing one share of Common Stock, that are listed on the New York Stock Exchange under the Symbol “LTM”

We have rounded percentages and certain U.S. dollar, Chilean peso and Brazilian reaisreal amounts contained in this annual report for ease of presentation. Any discrepancies in any table between totals and the sums of the amounts listed are due to rounding.

LATAM’s audited consolidated financial statements for the periods ended December 31, 2012, 2013, 2014, 2015, 2016, 2017, 2018 and 20162019 were prepared in accordance with IFRS.

This annual report contains certain terms that may be unfamiliar to some readers. You can find a glossary of these terms on page 42 of this annual report.

1

This annual report contains forward-looking statements. Such statements may include words such as “anticipate,” “could” “estimate,” “expect,” “project,” “intend,” “plan,” “believe” or other similar expressions. Forward-looking statements, including statements about our beliefs and expectations, are not statements of historical facts. These statements are based on current plans, estimates and projections, and, therefore, you should not place undue reliance on them. There is no assurance that the expected events, trends or results will actually occur. Forward-looking statements involve inherent risks and uncertainties. We caution you that a number of important factors could cause actual results to differ materially from those contained in any forward-looking statement. These factors include, but are not limited to:

| ● | the factors described in “Item 3. Key Information—Risk Factors”; |

| ● | our ability to service our debt and fund our working capital requirements; |

| ● | future demand for passenger and cargo air services in Chile, Brazil, other countries in Latin America and the rest of the world; |

| ● | the determination of relationships with customers; |

| ● | the state of the Chilean, Brazilian, other Latin American and world economies and their impact on the airline industry; |

| ● | the effects of competition in the airline industry; |

| ● | future terrorist incidents, cyberattacks or related activities affecting the airline industry; |

| ● | future outbreak of diseases, or the spread of already existing diseases, affecting travel behavior and/or exports; |

| ● | natural disasters affecting travel behavior and/or exports; |

| ● | the relative value of the Chilean peso and other Latin American currencies compared to other world currencies; |

| ● | inflation; |

| ● | competitive pressures on pricing; |

| ● | our capital expenditure plans; |

| ● | changes in labor costs, maintenance costs and insurance premiums; |

| ● | fluctuation of crude oil prices and its effect on fuel costs; |

| ● | cyclical and seasonal fluctuations in our operating results; |

| ● | defects or mechanical problems with our aircraft; |

| ● | our ability to successfully implement our growth strategy; |

| ● | our plans relative to acquisitions, joint ventures, strategic alliances or divestitures; |

| ● | increases in interest rates; and |

| ● | changes in regulations, including regulations related to access to routes in which we operate and environmental regulations. |

Forward-looking statements speak only as of the date they are made, and we undertake no obligation to publicly update publicly any of them, whether in light of new information, future events or otherwise. You should also read carefully the risk factors described in “Item 3. Key Information—Risk Factors.”

The following terms, as used in this annual report, have the meanings set forth below.

| Consolidated Affiliates of LATAM: | ||||

| ||||

| “ABSA” | Aerolinhas Brasileiras S.A., incorporated in Brazil. | |||

| “LANCO” | Línea Aérea Carguera de Colombia S.A., incorporated in Colombia. | |||

| “LATAM Airlines Argentina” | LAN Argentina S.A., incorporated in Argentina. | |||

| “LATAM Airlines Chile” | Transporte Aéreo S.A., incorporated in Chile. | |||

| “LATAM Airlines Colombia” | Aerovías de Integración Regional, Aires S.A., incorporated in Colombia. | |||

| “LATAM Airlines Ecuador” | LATAM-Airlines Ecuador S.A., incorporated in Ecuador. | |||

| “LATAM Airlines Peru” | LATAM Airlines Peru S.A. (f/ka LAN Peru S.A.), incorporated in Peru. | |||

| “LATAM Cargo” | LAN Cargo S.A., incorporated in Chile. | |||

| “TAM” | TAM S.A., incorporated in Brazil. | |||

| Capacity Measurements: | ||

| “available seat kilometers” or “ASKs” | The sum, across our network, of the number of seats made available for sale on each flight multiplied by the kilometers flown by the respective flight. | |

| “available ton kilometers” or “ATKs” | The sum, across our network, of the number of tons available for the transportation of revenue load (cargo) on each flight multiplied by the kilometers flown by the respective flight. | |

| Traffic Measurements: | ||

| “revenue passenger kilometers” or “RPKs” | The sum, across our network, of the number of revenue passengers on each flight multiplied by the number of kilometers flown by the respective flight. | |

| “revenue ton kilometers” or “RTKs” | The sum, across our network, of the load (cargo) in tons on each flight multiplied by the kilometers flown by the respective flight. | |

| “traffic revenue” | Revenue from passenger and cargo operations. | |

| Yield Measurements: | ||

| “cargo yield” | Revenue from cargo operations divided by RTKs. | |

| “passenger yield” | Revenue from passenger operations divided by RPKs. | |

| Load Factors: | ||

| “cargo load factor” | RTKs expressed as a percentage of ATKs. | |

| “passenger load factor” | RPKs expressed as a percentage of ASKs. | |

| Other: | ||

| “Airbus A320-Family Aircraft” | The Airbus | |

| “m²” | Square meters. | |

| “ton” | A metric ton, equivalent to 2,204.6 pounds. | |

| “utilization rates” | The actual number of | |

| “operating expenses” | Operating expenses, which are calculated in accordance with IFRS, comprise the sum of the line items “cost of sales” plus “distribution costs” plus “administrative expenses” plus “other operating expenses,” as shown on our consolidated statement of comprehensive income. These operating expenses include: wages and benefits, fuel, depreciation and amortization, commissions to agents, aircraft rentals, other rental and landing fees, passenger services, aircraft maintenance and other operating expenses. | |

“MiSchDynamicDT” | Market Intelligence Schedule Dynamic Table. | |

| “Diio Mi” | Data In Intelligence Out Market Intelligence. | |

| “CO2” | ||

| “PIS/COFINS” | “Program of Social Integration” and “Contribution for the Financing of Social Security” federal taxes in Brazil | |

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| ITEM 3. | KEY INFORMATION |

A. Selected Financial Data

LATAM’s Historical Financial Information

The summary consolidated annual financial information of LATAM as of December 31, 2019, 2018, 2017, 2016, 2015, 2014, 2013 and 20122015 has been prepared in accordance with IFRS(*)IFRS. In 2019, the Company adopted IFRS 16,Leases, retrospectively; restating the comparative figures as of December 31, 2018 and for the years ended December 31, 2018 and 2017, in accordance with the provisions of IAS 8,Accounting Policies, Changes in Accounting Estimates and Errors. On June 22, 2012, LATAM Airlines Group was formed throughThe selected Statement of Income Data for the business combinationyears ended 2016 and 2015 and the selected Balance Sheet Data as of LANDecember 31, 2017, 2016 and TAM. Following the combination, LAN Airlines S.A. became “LATAM Airlines Group S.A.” and TAM continues to exist as a subsidiary of LATAM Airlines Group. Financial statements for LATAM fully consolidate TAM’s results since June 23, 2012.2015 have not been restated.

LATAM’s Annual Financial Information

| Year ended December 31, | ||||||||||||||||||||

| 2016 | 2015 | 2014 | 2013 | 2012 | ||||||||||||||||

| (in US$ millions, except per share and capital stock data) | ||||||||||||||||||||

The Company(1)(2) | ||||||||||||||||||||

Statement of Income Data: | ||||||||||||||||||||

Operating revenues | ||||||||||||||||||||

Passenger | 7,877.7 | 8,410.6 | 10,380.1 | 11,061.5 | 7,966.8 | |||||||||||||||

Cargo | 1,110.6 | 1,329.4 | 1,713.4 | 1,863.0 | 1,743.6 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total operating revenues | 8,988.3 | 9,740.0 | 12,093.5 | 12,924.5 | 9,710.4 | |||||||||||||||

Cost of sales | (6,967.0 | ) | (7,636.7 | ) | (9,624.5 | ) | (10,054.2 | ) | (7,634.5 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Gross margin | 2,021.3 | 2,103.3 | 2,469.0 | 2,870.3 | 2,075.9 | |||||||||||||||

Other operating income(3) | 538.7 | 385.8 | 377.6 | 341.6 | 220.2 | |||||||||||||||

Distribution costs | (747.4 | ) | (783.3 | ) | (957.1 | ) | (1,025.9 | ) | (803.6 | ) | ||||||||||

Administrative expenses | (873.0 | ) | (878.0 | ) | (980.7 | ) | (1,136.1 | ) | (888.7 | ) | ||||||||||

Other expenses | (373.7 | ) | (324.0 | ) | (401.0 | ) | (408.7 | ) | (311.8 | ) | ||||||||||

Other gains/(losses) | (72.6 | ) | (55.3 | ) | 33.5 | (55.4 | ) | (45.8 | ) | |||||||||||

Financial income | 74.9 | 75.1 | 90.5 | 72.8 | 77.5 | |||||||||||||||

Financial costs | (416.3 | ) | (413.4 | ) | (430.0 | ) | (462.5 | ) | (294.6 | ) | ||||||||||

Equity accounted earnings | 0.0 | 0.0 | (6.5 | ) | 2.0 | 1.0 | ||||||||||||||

Exchange rate differences | 121.7 | (467.9 | ) | (130.2 | ) | (482.2 | ) | 66.6 | ||||||||||||

Result of indexation units | 0.3 | 0.6 | 0.1 | 0.3 | 0.0 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Income (loss) before income taxes | 273.9 | (357.1 | ) | 65.2 | (283.8 | ) | 96.7 | |||||||||||||

Income (loss) tax expense/benefit | (163.2 | ) | 178.4 | (292.4 | ) | 20.0 | (102.3 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net (loss) income for the period | 110.7 | (178.7 | ) | (227.2 | ) | (263.8 | ) | (5.6 | ) | |||||||||||

Income (loss) attributable to the parent company’s equity holders | 69.2 | (219.3 | ) | (260.0 | ) | (281.1 | ) | (19.1 | ) | |||||||||||

Income (loss) attributable tonon-controlling interests | 41.5 | 40.5 | 32.8 | 17.3 | 13.5 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) for the year | 110.7 | (178.7 | ) | (227.2 | ) | (263.8 | ) | (5.6 | ) | |||||||||||

Earnings per share | ||||||||||||||||||||

Average number of Shares | 549,559,559 | 545,547,819 | 545,547,819 | 487,930,977 | 412,267,624 | |||||||||||||||

Basic earnings (loss) per share (US$) Diluted earnings (loss) per share (US$) Balance Sheet Data: Cash, and cash equivalents Other current assets in operation Non-current assets and disposal groups held for sale Total current assets Property and equipment Othernon-current assets Totalnon-current assets Total assets Total current liabilities Totalnon-current liabilities Total liabilities Issued capital Net equity attributable to the parent company’s equity holders Non-controlling interest Total net equity Shares Outstanding Year ended December 31, 2016 2015 2014 2013 2012 (in US$ millions, except per share and capital stock data) 0.12665 (0.40193 ) (0.47656 ) (0.57613 ) (0.0463 ) 0.12665 (0.40193 ) (0.47656 ) (0.57613 ) (0.0463 ) At December 31, 2016 2015 2014 2013 2012 (in US$ millions, except per share and capital stock data) 949.3 753.5 989.4 1,984.9 650.3 2,340.3 2,067.4 2,644.1 2,992.2 2,626.2 337.2 2.0 1.1 2.4 47.7 3,626.8 2,822.9 3,634.6 4,979.5 3,324.2 10,498.1 10,938.7 10,773.1 10,982.8 11,807.1 5,073.3 4,339.8 6,076.7 6,668.8 7,195.0 15,571.4 15,278.5 16,849.8 17,651.6 19,002.1 19,198.2 18,101.4 20,484.4 22,631.1 22,326.3 6,222.2 5,641.0 5,829.7 6,509.1 6,297.5 8,790.7 9,522.9 10,151.0 10,795.6 10,808.1 15,012.9 15,163.9 15,980.7 17,304.7 17,105.6 3,149.6 2,545.7 2,545.7 2,389.4 1,501.0 4,096.7 2,856.5 4,401.9 5,238.8 5,112.1 88.6 81.0 101.8 87.7 108.6 4,185.3 2,937.5 4,503.7 5,326.5 5,220.7 606,407,693 545,547,819 545,547,819 535,243,229 479,107,860 Year ended December 31, 2019 2018

restated 2017

restated 2016 2015 (in US$ millions, except per share and capital stock data) The Company Statement of Income Data(1)(2)(3): Operating revenues Passenger 9,005.6 8,709.0 8,494.5 7,877.7 8,410.6 Cargo 1,064.4 1,186.5 1,119.4 1,110.6 1,329.4 Total operating revenues 10,070.1 9,895.5 9,613.9 8,988.3 9,740.0 Cost of sales (7,951.3 ) (7,773.4 ) (7,279.4 ) (6,967.0 ) (7,636.7 ) Gross margin 2,118.8 2,122.0 2.334,5 2,021.3 2,103.3 Other operating income(4) 360.9 472.8 549.9 538.7 385.8 Distribution costs (580.0 ) (615.2 ) (696.8 ) (747.4 ) (783.3 ) Administrative expenses (735.2 ) (736.3 ) (952.8 ) (873.0 ) (878.0 ) Other expenses (422.8 ) (356.3 ) (365.5 ) (373.7 ) (324.0 ) Other gains/(losses) 11.5 53.5 (7.8 ) (72.6 ) (55.3 ) Financial income 26.3 53.3 78.7 74.9 75.1 Financial costs (589.9 ) (539.1 ) (579.2 ) (416.3 ) (413.4 ) Equity accounted earnings 0.0 0.0 0.0 0.0 0.0 Foreign exchange gains/losses (32.6 ) (38.1 ) (48,5 ) 121.7 (467.9 ) Result of indexation units (15.0 ) (0.9 ) 0.7 0.3 0.6 Income (loss) before income taxes 141.9 415.7 313.4 273.9 (357.1 ) Income (loss) tax expense/benefit 53.7 (73.9 ) (159.0 ) (163.2 ) 178.4 Net (loss) income for the year 195.6 341.8 154.4 110.7 (178.7 ) Income (loss) attributable to owners of the parent 190.4 309.8 108.9 69.2 (219.3 ) Income (loss) attributable to non-controlling interests 5.2 32.0 45.5 41.5 40.5 Net income (loss) for the year 195.6 341.8 154.4 110.7 (178.7 ) Earnings per share Average number of Shares 606,407,693 606,407,693 606,407,693 546,559,599 545,547,819 Basic earnings (loss) per share (US$) 0.31403 0.51090 0.17958 0.12665 (0.40193 ) Diluted earnings (loss) per share (US$) 0.31403 0.51090 0.17958 0.12665 (0.40193 )

| As of December 31, | ||||||||||||||||||||

| 2019 | 2018 restated | 2017 | 2016 | 2015 | ||||||||||||||||

| (in US$ millions, except per share and capital stock data) | ||||||||||||||||||||

| Balance Sheet Data: | ||||||||||||||||||||

| Cash, and cash equivalents | 1,072.6 | 1,081.6 | 1,142.0 | 949.3 | 753.5 | |||||||||||||||

| Other current assets in operation | 2,460.5 | 2,188.5 | 2,312.4 | 2,340.3 | 2,067.4 | |||||||||||||||

| Non-current assets and disposal groups held for sale | 485.2 | 5.8 | 291.1 | 337.2 | 2.0 | |||||||||||||||

| Total current assets | 4,018.2 | 3,275.9 | 3,745.5 | 3,626.8 | 2,822.9 | |||||||||||||||

| Property and equipment | 12,919.6 | 12,501.8 | 10,065.3 | 10,498.1 | 10,938.7 | |||||||||||||||

| Other non-current assets | 4,150.0 | 4,301.1 | 4,987.2 | 5,073.3 | 4,339.8 | |||||||||||||||

| Total non-current assets | 17,069.6 | 16,802.9 | 15,052.5 | 15,571.4 | 15,278.5 | |||||||||||||||

| Total assets | 21,087.8 | 20,078.7 | 18,798.0 | 19,198.2 | 18,101.4 | |||||||||||||||

| Total current liabilities | 6,960.9 | 5,932.2 | 5,842.7 | 6,222.2 | 5,641.0 | |||||||||||||||

| Total non-current liabilities | 10,997.7 | 10,705.9 | 8,688.0 | 8,790.7 | 9,522.9 | |||||||||||||||

| , | ||||||||||||||||||||

| Total liabilities | 17,958.6 | 16,638.1 | 14,530.7 | 15,012.9 | 15,163.9 | |||||||||||||||

| Share capital | 3,146.3 | 3,146.3 | 3,146.3 | 3,149.6 | 2,545.7 | |||||||||||||||

| Net equity attributable to the parent company’s equity holders | 3,130.8 | 3,360.7 | 4,176.1 | 4,096.7 | 2,856.5 | |||||||||||||||

| Non-controlling interest | (1.6 | ) | 79.9 | 91.1 | 88.6 | 81.0 | ||||||||||||||

| Total equity | 3,129.2 | 3,440.6 | 4,267.2 | 4,185.3 | 2,937.5 | |||||||||||||||

| Shares Outstanding | 606,407,693 | 606,407,693 | 606,407,693 | 606,407,693 | 545,547,819 | |||||||||||||||

| (1) | For more information on the |

| (2) | The addition of the items may differ from the total amount due to rounding. |

| (3) | For the effects of the adoption of IFRS 15 and IFRS 16 see Note 2.1 to the Fnancial Statements” |

| (4) | Other operating income included in this Statement of Income Data is equivalent to the sum of income derived from |

(*)Law No. 20,780 issued on September 29, 2014, introduced modifications to the income tax system in Chile and other tax matters. On October 17, 2014 the Chilean Superintendence of Securities and Insurance (the “SVS”) issued Circular No. 856, which established that the effects of the change in the income tax rates on deferred tax assets and liabilities must be recognized directly on the Balance Sheet within “Retained earnings” instead of on the Income Statement as required by IAS 12. In order to comply with IAS 12, the financial statements in this document for the period ended December 31, 2014 are different from those presented to the SVS as the modifications introduced by Law No. 20,780 have been recognized within the income statement. For more information on the reconciliation of such differencessee Note 2.1 and Note 18 to our audited consolidated financial statements.

The table below presents LATAM’s unaudited operating data as of and for the year ended December 31, 2012 (which includes TAM’s data since June 23, 2012), and as of and for the years ended2015, December 31, 2013,2016, December 31, 2014,2017, December 31, 20152018 and December 31, 2016.2019. LATAM believes this operating data is useful in reporting the operating performance of its business and may be used by certain investors in evaluating companies operating in the global air transportation sector. However, these measures may differ from similarly titled measures reported by other companies, and should not be considered in isolation or as a substitute for measures of performance in accordance with IFRS. This unaudited operating data is not included in or derived from LATAM’s financial statements.

| Year ended December 31, | ||||||||||||||||||||

| Operating Data: | 2019 | 2018 | 2017 | 2016 | 2015 | |||||||||||||||

| ASKs (million) | 149,111.9 | 143,264.7 | 136,398.4 | 134,967.7 | 134,167.1 | |||||||||||||||

| RPKs (million) | 124,521.1 | 119,077.4 | 115,692.7 | 113,626.9 | 111,509.9 | |||||||||||||||

| ATKs (million) | 6,356.7 | 6,497.6 | 6,230.3 | 6,704.1 | 7,082.8 | |||||||||||||||

| RTKs (million) | 3,526.0 | 3,582.5 | 3,421.3 | 3,465.9 | 3,797.0 | |||||||||||||||

Operating Data: ASKs (million) RPKs (million) ATKs (million) RTKs (million) ASK Equivalent (million) For the year ended and as of December 31, 2016 2015 2014 2013 2012 134,967.7 134,167.1 130,200.9 131,690.9 132,186.0 113,626.9 111,509.9 108,534.0 106,466.5 103,886.1 6,704.1 7,082.8 7,219.7 7,651.9 7,645.9 3,465.9 3,797.0 4,317.2 4,466.7 4,488.3 205,537.5 208,722.5 206,197.9 212,237.0 212,669.6

Dividend Policy

In accordance with theLey sobre Sociedades Anónimas No. 18,046 (“Chilean Corporation Act”) and theReglamento de Sociedades Anónimas(“Regulation to the Chilean Corporation Act”) (collectively,, and together with the Chilean Corporation Act, the “Chilean Corporation Law”), we must pay annual cash dividends equal to at least 30.0% of our annual consolidated net income for the prior year, subject to limited exceptions. LATAM Airlines Group’s board of directors has the authority to declare interim dividends.Year-end dividends, if any, are declared by our shareholders at our annual meeting. For a description of our dividend policy, see “Item 8. Financial Information—Consolidated Financial Statements and Other Financial Information—Dividend Policy” and “Item 10. Additional Information—Dividend and Liquidation Rights”. LATAM did not pay dividends in 2014, 2015 or 2016. DividendOn May 18, 2017, LATAM paid US$20,766,119 in dividends in respect of the year ended December 31, 2016. On May 17, 2018, LATAM paid US$46,591,193 in dividends in respect of year ended December 31, 2017. On May 17, 2019, LATAM paid US$54,580,443 in dividends in respect of year ended December 31, 2018. In addition, dividend reserves of US$20,766,199 have been57,129,120 were set aside in 2016,for 2019, to be paid in 2017.2020.

We declare cash dividends in U.S. dollars, but make dividend payments in Chilean pesos, converted from U.S. dollars at the observed exchange rate two business days prior to the day we first make payment to shareholders. Payments of cash dividends to holders of ADSs, if any, are made in Chilean pesos to the custodian, whichwho converts those Chilean pesos into U.S. dollars and delivers U.S. dollars to the depositary for distribution to holders.holders of ADS. The amount of U.S. dollars distributed to holders of ADSs may be adversely affected by a devaluation of the Chilean currency that may occur before such dividends are converted and remitted.

Chilean Peso Exchange RatesLATAM’s Dividend Payments

The following table below sets forth the cash dividends per common share and per ADS paid by LATAM, as well as the number of common shares entitled to such dividends, for the periods indicated,years indicated. Dividends per common share amounts reflect common share amounts outstanding immediately prior to the high, low, average andperiod-end observed exchange rate for the purchasedistribution of U.S. dollars, expressed in Chilean pesos per U.S. dollar. The rates have not been restated in constant currency units. On February 28, 2017 the observed exchange rate was Ch$645.19 = US$1.00.such dividend.

| Daily Observed Exchange Rate | ||||||||||||||||

Year Ended December 31, | High | Low | Average(1) | Period-End | ||||||||||||

| Ch$ per US$ | ||||||||||||||||

2012 | 519.69 | 469.65 | 486.75 | 478.60 | ||||||||||||

2013 | 533.95 | 466.50 | 495.00 | 523.76 | ||||||||||||

2014 | 621.41 | 524.61 | 570.01 | 607.38 | ||||||||||||

2015 | 715.66 | 597.10 | 654.25 | 707.34 | ||||||||||||

2016 | 730.31 | 645.22 | 676.83 | 669.47 | ||||||||||||

2016 | ||||||||||||||||

October | 670.88 | 651.65 | 663.92 | 651.65 | ||||||||||||

November | 679.24 | 650.72 | 666.12 | 675.48 | ||||||||||||

December | 677.11 | 649.40 | 667.17 | 669.47 | ||||||||||||

2017 | ||||||||||||||||

Year Ended December 31, January February Daily Observed Exchange Rate High Low Average(1) Period-End Ch$ per US$ 673.36 648.31 661.19 648.87 646.97 638.35 643.21 645.19 Dividend for year: Payment date(s) Total dividend

payment Number of

common

shares

entitled to

dividend Cash

dividend per

common

share Cash

dividend per

ADS (U.S. dollars) (in millions) (U.S. dollars) (U.S. dollars) 2016 May 18, 2017 $ 20,766,119 606.41 $ 0.03424 $ 0.03424 2017 May 17, 2018 $ 46,591,193 606.41 $ 0.07683 $ 0.07683 2018 May 16, 2019 $ 54,580,443 606.41 $ 0.09001 $ 0.09001

Source: Central Bank of Chile

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

The following important factors, and those important factors described in other reports we submit to or file with the Securities and Exchange Commission (“SEC”), could affect our actual results and could cause our actual results to differ materially from those expressed in any forward-looking statements made by us or on our behalf. In particular, as we are anon-U.S. company, there are risks associated with investing in our ADSs that are not typical for investments in the shares of U.S. companies. Prior to making an investment decision, you should carefully consider all of the information contained in this document, including the following risk factors.

Risk Factors Relating to our Company

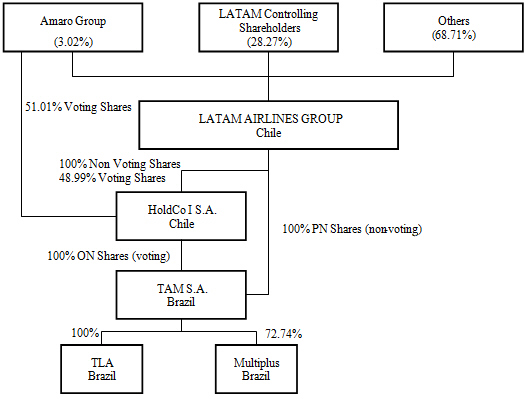

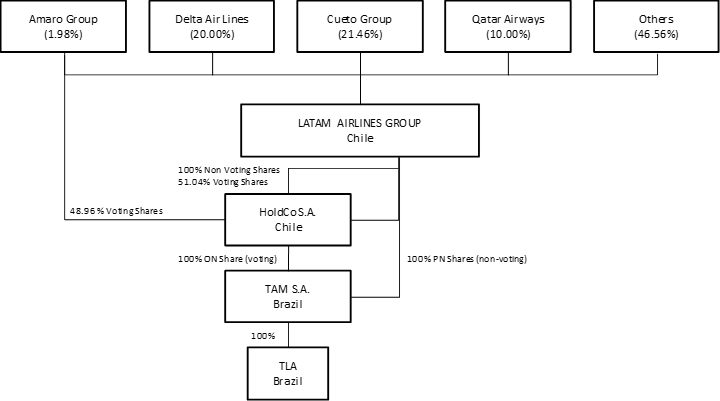

LATAM does not control the voting shares or board of directors of TAM

Due to Brazilian law restrictions on foreign ownership of Brazilian airlines, LATAM does not control the voting shares or board of directors of TAM. As of February 28, 2017, the ownership structure of TAM is as follows:

As a result of this ownership structure:

LATAM Airlines Group and TEP Chile and other parties have entered into shareholders’ agreements that establish agreements and restrictions relating to corporate governance with respect to TAM. Certain specified actions require supermajority approval, which in turn means they require the prior approval of both LATAM and TEP Chile. Examples of actions requiring supermajority approval by the board of directors of Holdco I or TAM include, among others, entering into acquisitions or business collaborations, amending or approving budgets, business plans, financial statements and accounting policies, incurring indebtedness, encumbering assets, entering into certain agreements, making certain investments, modifying rights or claims, entering into settlements, appointing executives, creating security interests, issuing, redeeming or repurchasing securities and voting on matters as a shareholder of affiliates

of TAM. Actions requiring supermajority shareholder approval of Holdco I or TAM include, among others, certain changes to theby-laws of Holdco I, TAM or TAM’s affiliates or any dissolution/liquidation, corporate reorganization, payment of dividends, issuance of securities, disposal or encumbrance of certain assets, creation of security interests or entering into guarantees and agreements with related parties. For more information on the shareholders’ agreements, see “Item 7. Controlling Shareholders and Related Party Transactions—Shareholders’ Agreements.”

Our assets include a significant amount of goodwill.

Our assets included US$2,710.42,209.6 million of goodwill as of December 31, 2016, US$2,582.5 million of which results from the combination of LAN and TAM.2019. Under IFRS, goodwill is subject to an annual impairment test and may be required to be tested more frequently if events or circumstances indicate a potential impairment. In 2016,2019, mainly as a result of the appreciationdepreciation of the Brazilian real against the U.S. dollar, the value of our goodwill increaseddecreased by 18.8%3.7% as compared with 2015.2018. Any impairment could result in the recognition of a significant charge to earnings in our statement of income, which could materially and adversely impact our consolidated results for the period in which the impairment occurs.

A failure to successfully implement our strategy or a failure adjusting the strategy to the current economic situation would harm our business and the market value of our ADSs and common shares.

We have developed a strategic plan with the goal of becoming one of the bestmost admired airlines in the world and renewing our commitment to sustained profitability and superior returns to shareholders. Our strategy requires us to identify value propositions that are attractive to our clients, to find efficiencies in our daily operations, and to transform ourselves into a stronger and more risk-resilient company. A tenet of our strategic plan is the continuing adoption of a new travel model for domestic and international services in the six countries where we have domestic operations to address the changing dynamics of customers and the industry, and to increase our competitiveness. The new travel model is based on a continued reduction in air fares that makes air travel accessible to a wider audience, and in particular to those wish to fly more frequently. This model requires continued cost reduction efforts and in order to achieve thisincreasing revenues from ancillary activities. In connection with these efforts, the Company is implementingcontinues to implement a series of initiatives to reduce cost per ASK in all its domestic operations.operations as well as developing new ancillary revenue initiatives.

Difficulties in implementing our strategy may adversely affect our business, results of operation and the market value of our ADSs and common shares.

A failure to successfully transfer the value proposition of the LAN and TAM brands to a new single brand, may adversely affect our business and the market value of our ADSs and common shares.

Following the combination in 2012, LAN and TAM continued to operate with their original brands. During 2016, we began the transition of LAN and TAM into a single brand. LAN and TAM had different value propositions, and there can be no assurances that we will be able to fully transfer the value of the original LAN and TAM brands to our new single brand “LATAM”. Difficulties in implementing our single brand may prevent us from consolidating as a customer preferred carrier and may adversely affect our business and results of operations and the market value of our ADSs and common shares.

It may take time to combine the frequent flyer programs of LAN and TAM.

We have integrated the separate frequent flyer programs of LAN and TAM so that passengers can use frequent flyer miles earned with either LAN or TAM interchangeably. During 2016, LAN and TAM announced their revamped frequent flyer programs, which have new names: LATAM Pass and LATAM Fidelidade, respectively. The change is part of the process of consolidating the airline group’s new brand identity (LATAM) and the evolution of the programs, which enhances existing benefits and introduces new benefits for program members. However, there is no guarantee that full integration of the two plans will be completed in the near term or at all. Even if the integration occurs, the successful integration of these programs will involve some time and expense. Moreover, during 2016, LATAM Pass and LATAM Fidelidade approved changes in their mileage earning policy which may impact the attractiveness of the programs to passengers. Until we effectively combine these programs, passengers may prefer frequent flyer programs offered by other airlines, which may adversely affect our business.

Our financial results are exposed to foreign currency fluctuations.

We prepare and present our consolidated financial statements in U.S. dollars. LATAM and its affiliates operate in numerous countries and face the risk of variation in foreign currency exchange rates against the U.S. dollar or between the currencies of these various countries. Changes in the exchange rate between the U.S. dollar and the currencies in the countries in which we operate could adversely affect our business, financial condition and results of operations..operations. If the value of the Brazilian real, Chilean peso or other currencies in which revenues are denominated declines against the U.S. dollar, our results of operations and financial condition will be affected. The exchange rate of the Chilean peso, Brazilian real and other currencies against the U.S. dollar may fluctuate significantly in the future.

Changes in Chilean, Brazilian and other governmental economic policies affecting foreign exchange rates could also adversely affect our business, financial condition, results of operations and the return to our shareholders on their common shares or ADSs. For further information, see “Item 11. Quantitative and Qualitative Disclosures About Market Risk—Risk of Variation in Foreign Exchange Rates.”

We depend on strategic alliances or commercial relationships in many of the countries in which we operate, and our business may suffer if any of our strategic alliances or commercial relationships terminates.

We maintain a number of alliances and other commercial relationships in many of the jurisdictions in which LATAM and its affiliates operate. These alliances or commercial relationships allow us to enhance our network and, in some cases, to offer our customers services that we could not otherwise offer. If any of our strategic alliances or commercial relationships deteriorates, or any of these agreements are terminated, our business, financial condition and results of operations could be adversely affected.

Our business and results of operations may suffer if we fail to obtain and maintain routes, suitable airport access, slots and other operating permits. Also, technical and operational problems with the airport infrastructure of cities in which we have a focus may have a material adverse effect on us.

Our business depends upon our access to key routes and airports. Bilateral aviation agreements between countries, open skies laws and local aviation approvals frequently involve political and other considerations outside of our control. Our operations could be constrained by any delay or inability to gain access to key routes or airports, including:

| ● | limitations on our ability to process more passengers; |

| ● | the imposition of flight capacity restrictions; |

| ● | the inability to secure or maintain route rights in local markets or under bilateral agreements; or |

| ● | the inability to maintain our existing slots and obtain additional slots. |

We operate numerous international routes subject to bilateral agreements, and also internalas well as domestic flights within Chile, Peru, Brazil, Argentina, Ecuador Colombia and other countries,Colombia, subject to local route and airport access approvals. See “Item 4. Information on the Company—B. Business Overview—Regulation.”

There can be no assurance that existing bilateral agreements with the countries in which our companies are based and permits from foreign governments will continue. A modification, suspension or revocation of one or more bilateral agreements could have a material adverse effect on our business, financial condition and results of operations. The suspension of our permission to operate in certain airports, destinations or slots, or the imposition of other sanctions could also have a material adverse effect. A change in the administration of current laws and regulations or the adoption of new laws and regulations in any of the countries in which we operate that restrict our route, airport or other access may have a material adverse effect on our business, financial condition and results of operations.

Moreover, our operations and growth strategy are dependent on the facilities and infrastructure of key airports, including Santiago’s International Airport, São Paulo’s Guarulhos International and Congonhas Airports, Brasilia’s International Airport and Lima’s Jorge Chavez International Airport.

Santiago’s Comodoro Arturo Merino Benítez International Airport is currently facing an important expansion, which is expected to be completed by 2021. If the expansion continues to be delayed, this will likely impact our operations and may affect our ability to remain competitive.

One of the major operational risks we face on a daily basis at Lima’s Jorge Chavez International Airport is the limited number of parking positions. Additionally, the indoor infrastructure of the airport limits our ability to manage connections and launch new flights due to the lack of gates and increasing security and immigration controls. Lima’s Jorge Chavez International Airport is currently undergoing an expansion, which is expected to be completed by 2024. Any delays could negatively impact our operations limit our ability to grow and affect our competitiveness in the country and in the region.

Brazilian airports, such as the Brasilia, and São Paulo (Guarulhos) International Airports, have limited the number of takeoff and landing slots per day due to infrastructural limitations. Any condition that would prevent or delay our access to airports or routes that are vital to our strategy, or our inability to maintain our existing slots and obtain additional slots, could materially adversely affect our operations.

7

A significant portion of our cargo revenue comes from relatively few product types and may be impacted by events affecting their production, trade or demand.

Our cargo demand, especially from Latin American exporters, is concentrated in a small number of product categories, such as exports of fish, sea products and fruits from Chile, and asparagus from Peru and exports of fresh flowers from Ecuador and Colombia. Events that adversely affect the production, trade or demand for these goods may adversely affect the volume of goods that we transport and may have a significant impact on our results of operations. Future trade protection measures by or against the countries for which we provide cargo services may have an impact in cargo traffic volumes and adversely affect our financial results. Some of our cargo products are sensitive to foreign exchange rates and, therefore, traffic volumes could be impacted by the appreciation or depreciation of local currencies.

Our operations are subject to fluctuations in the supply and cost of jet fuel, which could adversely impact our business.

Higher jet fuel prices could have a materially adverse effect on our business, financial condition and results of operations. Jet fuel costs have historically accounted for a significant amount of our operating expenses, and accounted for 23.0%30.2% of our operating expenses in 2016.2019. For additional information, see “Item 4. Information on the Company—B. Business Overview—Fuel Supplies”. Both the cost and availability of fuel are subject to many economic and political factors and events that we can neither control nor predict.predict, including international political and economic circumstances such as the political instability in major oil-exporting countries. Any future fuel supply shortage (for example, as a result of production curtailments by the Organization of the Petroleum Exporting Countries, or “OPEC”), a disruption of oil imports, supply disruptions resulting from severe weather or natural disasters, labor actions such as the 2018 trucking strike in Brazil, the continued unrest in the Middle East or other events could result in higher fuel prices or reductions in scheduled airline services. We cannot ensure that we would be able to offset any increases in the price of fuel by increasing our fares. In addition, lower fuel prices may result in lower fares through the reduction or elimination of fuel surcharges. We have entered into fuel hedging arrangements, but there can be no assurance that such arrangements will be adequate to protect us from an increase in fuel prices in the near future or in the long term. Also, while these hedging arrangements are designed to limit the effect of an increase in fuel prices, our hedging methods may also limit our ability to take advantage of any decrease in fuel prices, as was the case in 2015 and, to a lesser extent, in 2016. Although we have implemented measures to pass a portionSee “Item 11. Quantitative and Qualitative Disclosures About Market Risk—Risk of incremental fuel costs to our customers, our ability to lessen the impact of any increaseVariation in fuel costs using these types of mechanisms may be limited.Fuel Prices.”

We rely on maintaining a high aircraft utilization rate to increase our revenues and absorb our fixed costs, which makes us especially vulnerable to delays.

A key element of our strategy is to maintain a high daily aircraft utilization rate, which measures the number of flight hours we use our aircraft per day. High daily aircraft utilization allows us to maximize the amount of revenue we generate from our aircraft and

absorb the fixed costs associated with our fleet and is achieved, in part, by reducing turnaround times at airports and developing schedules that enable us to increase the average hours flown per day. Our rate of aircraft utilization could be adversely affected by a number of different factors that are beyond our control, including air traffic and airport congestion, adverse weather conditions, unanticipated maintenance and delays by third-party service providers relating to matters such as fueling and ground handling. If an aircraft falls behind schedule, the resulting delays could cause a disruption in our operating performance.performance and have a financial impact on our results.

We fly and depend upon Airbus and Boeing aircraft, and our business could suffer if we do not receive timely deliveries of aircraft, if aircraft from these companies becomesbecome unavailable or if the public negatively perceives our aircraft.

As our fleet has grown, our reliance on Airbus and Boeing has also grown. As of December 31, 2016,2019, LATAM Airlines Group has a total fleet of 250263 Airbus and 8279 Boeing aircraft. Risks relating to Airbus and Boeing include:

| ● | our failure or inability to obtain Airbus or Boeing aircraft, parts or related support services on a timely basis because of high demand, aircraft delivery backlog or other factors; |

| ● | the interruption of fleet service as a result of unscheduled or unanticipated maintenance requirements for these aircraft; |

| ● | the issuance by the Chilean or other aviation authorities of directives restricting or prohibiting the use of our Airbus or Boeing aircraft, or requiring time-consuming inspections and maintenance; |

| ● | adverse public perception of a manufacturer as a result of safety concerns, negative publicity or other problems, whether real or perceived, in the event of an accident; or |

| ● | delays between the time we realize the need for new aircraft and the time it takes us to arrange for Airbus and Boeing or for a third-party provider to deliver this aircraft. |

The occurrence of any one or more of these factors could restrict our ability to use aircraft to generate profits, respond to increased demands, or could otherwise limit our operations and adversely affect our business. For further information, related to current contractual obligations, see “Item 5. Operating and Financial Review and Prospects—F. Long term Indebtedness—Tabular Disclosure of Contractual Obligations.”

8

If we are unable to incorporate leased aircraft into our fleet at acceptable rates and terms in the future, our business could be adversely affected.

A large portion of our aircraft fleet is subject to long-term operating leases. Our operating leases typically run from three to 12 years from the date of delivery.execution. We may face more competition for, or a limited supply of, leased aircraft, making it difficult for us to negotiate on competitive terms upon expiration of our current operating leases or to lease additional capacity required for our targeted level of operations. If we are forced to pay higher lease rates in the future to maintain our capacity and the number of aircraft in our fleet, our profitability could be adversely affected.

Our business may be adversely affected if we are unable to service our debt or meet our future financing requirements.

We have a high degree of debt and payment obligations under our aircraft operating leases and financial debt arrangements. We require significant amounts of financing to meet our aircraft capital requirements and may require additional financing to fund our other business needs. We cannot guarantee that we will have access to or be able to arrange for financing in the future on favorable terms. Following the combination of LAN and TAM, Fitch Ratings Inc. and Standard and Poor’s downgraded LATAM Airlines Group S.A.’s credit rating to levels that are below investment grade. Any further securities rating agencies downgrades could increase our financing costs. Higher financing costs could affect our ability to expand or renew our fleet, which in turn could adversely affect our business.

In addition, the majority of our property and equipment is subject to liens securing our indebtedness. In the event that we fail to make payments on secured indebtedness, creditors’ enforcement of liens could limit or end our ability to use the affected property and equipment to fulfill our operational needs and thus generate revenue. For further information, related to current contractual obligations, see “Item 5. Operating and Financial Review and Prospects—F. Long term Indebtedness—Tabular Disclosure of Contractual Obligations.”

Moreover, external conditions in the financial and credit markets may limit the availability of funding at particular times or increase its costs, which could adversely affect our profitability, our competitive position and result in lower net interest margins, earnings and cash flows, as well as lower returns on shareholders’ equity and invested capital. Factors that may affect the availability of funding or cause an increase in our funding costs include global macro-economic crises, reductionreductions in our credit rating or in that of our credit rating,issuances, and other potential market disruptions.

We have significant exposure to LIBOR and other floating interest rates; increases in interest rates will increase our financing costs and may have adverse effects on our financial condition and results of operations.

We are exposed to the risk of interest rate variations, principally in relation to the U.S. dollar London Interbank Offer Rate (“LIBOR”). Many of our operating and financial leases are denominated in U.S. dollars and bear interest at a floating rate. 36.9%38.4% of our outstanding consolidated debt as of December 31, 20162019 bears interest at a floating rate after(after giving effect to interest rate hedging agreements.agreements). Volatility in LIBOR or other reference rates could increase our periodic interest and lease payments and have an adverse effect on our total financing costs. We may be unable to adequately adjust our prices to offset any increased financing costs, which would have an adverse effect on our revenues and our results of operations.

On July 27, 2017, the Financial Conduct Authority (the authority that regulates LIBOR) announced that it intends to stop compelling banks to submit rates for the calculation of LIBOR after 2021. It is unclear whether new methods of calculating LIBOR will be established such that it continues to exist after 2021. The U.S. Federal Reserve, in conjunction with the Alternative Reference Rates Committee, is considering replacing U.S. dollar LIBOR with a newly created index, calculated based on repurchase agreements backed by treasury securities. The impact of such a transition away from LIBOR could be significant for us because of our substantial indebtedness. It is not possible to predict the effect of these changes, other reforms or the establishment of alternative reference rates in the United Kingdom, the United States or elsewhere. See also the discussion of interest rate risk in “Item 11. Quantitative and Qualitative Disclosures About Market Risk—”Risk of Fluctuations in Interest Rates.”

Increases in insurance costs and/or significant reductions in coverage could harm our financial condition and results of operations.

Major events affecting the aviation insurance industry (such as terrorist attacks, hijackings or airline crashes) may result in significant increases of airlines’ insurance premiums or in significant decreases of insurance coverage, as occurred after the September 11, 2001 terrorist attacks. IncreasesFurther increases in insurance costs and/or significant reductions in available insurance coverage could harmhave an adverse impact on our financial conditionresults and results of operations and increasesincrease the risk that we experience uncovered losses.

Problems with air traffic control systems or other technical failures could interrupt our operations and have a material adverse effect on our business.business

Our operations, including our ability to deliver customer service, are dependent on the effective operation of our equipment, including our aircraft, maintenance systems and reservation systems. Our operations are also dependent on the effective operation of domestic and international air traffic control systems and the air traffic control infrastructure by the corresponding authorities in the markets in which we operate. Equipment failures, personnel shortages, air traffic control problems and other factors that could interrupt operations could adversely affect our operations and financial results as well as our reputation.

9

We depend on a limited number of suppliers for certain aircraft and engine parts.

We depend on a limited number of suppliers for aircraft, aircraft engines and many aircraft and engine parts. As a result, we are vulnerable to any problems associated with the supply of those aircraft, parts and engines, including design defects, mechanical problems, contractual performance by the suppliers, or adverse perception by the public that would result in unscheduled maintenance requirements, in customer avoidance or in actions by the aviation authorities resulting in an inability to operate our aircraft. During the year 2019, LATAM Airline’s main suppliers were aircraft manufacturers Airbus and Boeing.

In addition to Airbus and Boeing, LATAM Airlines has a number of other suppliers, primarily related to aircraft accessories, spare parts, and components, including Pratt & Whitney, MTU Maintenance, Rolls-Royce, and Pratt and Whitney Canada.

During 2019, Airbus experienced delays in the delivery of A320neo aircraft worldwide. LATAM is currently expecting delivery of three A320neo family aircraft during 2020, but any delivery delays could adversely affect operations.

Rolls-Royce continues to face delays with its Trent 1000 engine program, used to power LATAM’s Boeing 787 fleet, with increased demand for inspections and maintenance. This has affected the availability and the operational flexibility of this aircraft for operators worldwide, with the impact for LATAM reaching its peak in July 2018. LATAM currently has three aircraft on ground awaiting for engines. While the situation has improved considerably, there is no guarantee that this will not continue and therefore reduce the availability of Boeing 787 aircraft, thus negatively affecting operations and financial results.

Our business relies extensively on third-party service providers. Failure of these parties to perform as expected, or interruptions in our relationships with these providers or in their provision of services to us, could have an adverse effect on our financial position and results of operations.

We have engaged a significant number of third-party service providers to perform a large number of functions that are integral to our business, including regional operations, operation of customer service call centers, distribution and sale of airline seat inventory, provision of information technology infrastructure and services, performance of business processes, including purchasing and cash management, provision of aircraft maintenance and repairs, catering, ground services, and provision of various utilities and performance of aircraft fueling operations, among other vital functions and services. We do not directly control these third-party service providers, although we do enter into agreements with many of them that define expected service performance. Any of these third-party service providers, however, may materially fail to meet their service performance commitments, may suffer disruptions to their systems that could impact their services, or the agreements with such providers may be terminated. For example, flight reservations booked by customers and/or travel agencies via third-party GDSs (Global Distribution Systems) may be adversely affected by disruptions in our business relationships with GDS operators.operators or by issues in the GDS’s operations. Such disruptions, including a failure to agree upon acceptable contract terms when contracts expire or otherwise become subject to renegotiation, may cause the carriers’ flight information to be limited or unavailable for display, significantly increase fees for both us and GDS users, and impair our relationships with customers and travel agencies. The failure of any of our third-party service providers to adequately perform their service obligations, or other interruptions of services, may reduce our revenues and increase our expenses or prevent us from operating our flights and providing other services to our customers. In addition, our business, financial performance and reputation could be materially harmed if our customers believe that our services are unreliable or unsatisfactory.

Disruptions or security breaches of our information technology infrastructure or systems could interfere with our operations, compromise passenger or employee information, and expose us to liability, possibly causing our business and reputation to suffer.

A serious internal technology error, failure, or failurecybersecurity incident impacting systems hosted internally at our data centers, or externally at third-party locations or cloud providers, or large-scale interruption in technology infrastructure we depend on, such as power, telecommunications or the internet, may disrupt our technology network with potential impactonimpact on our operations. Our technology systems and related data may also be vulnerable to a variety of sources of interruption, including natural disasters, terrorist attacks, telecommunications failures, computer viruses, hackerscyber attacks and other security issues. While we have in place,These systems include our computerized airline reservation system, flight operations system, telecommunications systems, website, customer, self-service applications (“apps”), maintenance systems, check-in kiosks, in-flight entertainment systems and continue to invest in, technology security initiatives and disaster recovery plans, these measures may not be adequate or implemented properly so as to prevent a business disruption and its adverse financial and reputational consequences to our business.data centers.

In addition, as a part of our ordinary business operations, we collect and store sensitive data, including personal information of our passengers and employees and information of our business partners. The secure operation of the networks and systems on which this type of information is stored, processed and maintained is critical to our business operations and strategy. Unauthorized parties may attempt to gain access to our systems or information through fraud, deception, or deception.cybersecurity incident. Hardware or software we develop or acquire

may contain defects that could unexpectedly compromise information security. The compromise of our technology systems resulting in the loss, disclosure, misappropriation of, or access to, customers’, employees’ or business partners’ information could result in legal claims or proceedings, liability or regulatory penalties under laws protecting the privacy of personal information, disruption to our operations and damage to our reputation, any or all of which could adversely affect our business.

10

Increases in our labor costs, which constitute a substantial portion of our total operating expenses, could directly impact our earnings.

Labor costs constitute a significant percentage of our total operating expenses (21.8%(18.5% in 2016)2019) and at times in our operating history we have experienced pressure to increase wages and benefits for our employees. A significant increase in our labor costs could result in a material reduction in our earnings.

Collective action by employees could cause operating disruptions and adversely impact our business.

Certain employee groups such as pilots, flight attendants, mechanics and our airport personnel have highly specialized skills. As a consequence, actions by these groups, such as strikes, walk-outs or stoppages, could severely disrupt our operations and adversely impact our operating and financial performance, as well as our image.

A strike, work interruption or stoppage or any prolonged dispute with our employees who are represented by any of these unions could have an adverse impact on our operations. These risks are typically exacerbated during periods of renegotiation with the unions, which typically occurs every two to four years depending on the jurisdiction and the union. Any renegotiated collective bargaining agreement could feature significant wage increases and a consequent increase in our operating expenses. Any failure to reach an agreement during negotiations with unions may require us to enter into arbitration proceedings, use financial and management resources, and potentially agree to terms that are less favorable to us than our existing agreements. Employees who are not currently members of unions may also form new unions that may seek further wage increases or benefits.

Our business may experience adverse consequences if we are unable to reach satisfactory collective bargaining agreements with our unionized employees.

As of December 31, 2016,2019, approximately 72.9%46% of our employees, including administrative personnel, cabin crew, flight attendants, pilots and maintenance technicians are members of unions and have contracts and collective bargaining agreements which expire on a regular basis. Our business, financial condition and results of operations could be materially adversely affected by a failure to reach agreement with any labor union representing such employees or by an agreement with a labor union that contains terms that are not in line with our expectations or that prevent us from competing effectively with other airlines. For further information regarding the unions representing our employees in each country in which we operate and with which we have established collective bargaining agreements, see “Item 6. Directors, Senior Management and Employees—D. Employees—Labor Relations.”

Collective action by employees could cause operating disruptions and adversely impact our business.

Certain employee groups such as pilots, flight attendants, mechanics and our airport personnel have highly specialized skills. As a consequence, actions by these groups, such as strikes, walk-outs or stoppages, could severely disrupt our operations and adversely impact our operating and financial performance, as well as our image.

We may experience difficulty finding, training and retaining employees.

Our business is labor intensive. We employ a large number of pilots, flight attendants, maintenance technicians and other operating and administrative personnel. The airline industry has, from time to time, experienced a shortage of qualified personnel, especially pilots and maintenance technicians. In addition, as is common with most of our competitors, we may, from time to time, face considerable turnover of our employees. Should the turnover of employees, particularly pilots and maintenance technicians, sharply increase, our training costs will be significantly higher. AWe cannot assure you that we will be able to recruit, train and retain the managers, pilots, technicians and other qualified employees that we need to continue our current operations or replace departing employees. An increase in turnover or failure to recruit, train and retain qualified employees at a reasonable cost could materially adversely affect our business, financial condition, and results of operations.

Risks Related to the Airline Industry and the Countries in Which We Operate

Our performance is heavily dependent on economic conditions in the countries in which we do business. Negative economic conditions in those countries could adversely impact our business and results of operations and cause the market price of our common shares and ADSs to decrease.

Passenger and cargo demand is heavily cyclical and highly dependent on global and local economic growth, economic expectations and foreign exchange rate variations, among other things. In the past, our business has been adversely affected by global economic recessionary conditions, weak economic growth in Chile, recession in Brazil and Argentina and poor economic performance in certain emerging market countries in which we operate. The occurrence of similar events in the future could adversely affect our business. We plan to continue to expand our operations based in Latin America and our performance will, therefore, continue to depend heavily on economic conditions in the region.

Any of the following factors could adversely affect our business, financial condition and results of operations in the countries in which we operate:

| ● | changes in economic or other governmental policies; |

| ● | changes in regulatory, legal or administrative practices; |

| ● | weak economic performance, including, but not limited to, a slowdown in the Brazilian economy, political instability low economic growth, low consumption and/or investment rates, and increased inflation rates; or |

| ● | other political or economic developments over which we have no control. |

No assurance can be given that capacity reductions or other steps we may take in response to weakened demand will be adequate to offset any future reduction in our cargo and/or air travel demand in Brazil or in other markets in which we operate. Sustained weakenedweak demand may adversely impact our revenues, results of operations or financial condition.

An adverse economic environment, whether global, regional or in a particular country, could result in a reduction in passenger traffic, as well as a reduction in our cargo business, and could also impact our ability to raise fares, which in turn would materially and negatively affect our financial condition and results of operations.

We are exposed to increases in landing fees and other airport service charges that could adversely affect our margin and competitive position. Also, it cannot be assured that in the future we will have access to adequate facilities and landing rights necessary to achieve our expansion plans.

Airlines

We must pay fees to airport operators for the use of their facilities. Any substantial increase in airport facilities.charges, including at Guarulhos International Airport in São Paulo, Jorge Chavez International Airport in Lima or Comodoro Arturo Merino Benitez International Airport in Santiago, could have a material adverse impact on our results of operations. Passenger taxes and airport charges have increased substantially in recent years. We cannot assure you that the airports in which we operate will not increase or maintain high passenger taxes and service charges in the future. Any substantial increase in airport chargessuch increases could have an adverse effect on our financial condition and results of operations.

Certain airports that we serve (or that we plan to serve in the future) are subject to capacity constraints and impose various restrictions, including takeoff and landing slot restrictions during certain periods of the day and limits on aircraft noise levels. We cannot be certain that we will be able to obtain a materialsufficient number of slots, gates and other facilities at airports to expand our services in line with our growth strategy. It is also possible that airports not currently subject to capacity constraints may become so in the future. In addition, an airline must use its slots on a regular and timely basis or risk having those slots re-allocated to others. Where slots or other airport resources are not available or their availability is restricted in some way, we may have to amend our schedules, change routes or reduce aircraft utilization. It is also possible that aviation authorities in the countries in which we operate, change the rules for the assignment of takeoff and landing slots, as it was the case with the São Paulo airport (Congonhas) in 2019 where the slots previously operated by Avianca Brazil were reassigned. Any of these alternatives could have an adverse financial impact on our results of operations. In addition, anyWe cannot ensure that airports at which there are no such restrictions may not implement restrictions in the future or that, where such restrictions exist, they may not become more onerous. Such restrictions may limit our ability to continue to provide or to increase in passenger taxes could negatively impact demand for air travel and affect our results.services at such airports.

Our business is highly regulated and changes in the regulatory environment in the countries in which we operate may adversely affect our business and results of operations.

Our business is highly regulated and depends substantially upon the regulatory environment in the countries in which we operate or intend to operate. For example, price controls on fares may limit our ability to effectively apply customer segmentation profit maximization techniques (“passenger revenue management”) and adjust prices to reflect cost pressures. High levels of government regulation may limit the scope of our operations and our growth plans. The possible failure of aviation authorities to maintain the required governmental authorizations or our failure to comply with applicable regulations, may adversely affect our business and results of operations.

Our business, financial condition, results of operations and the price of preferred shares and ADSs may be adversely affected by changes in policy or regulations at the federal, state or municipal level in the countries in which we operate, involving or affecting factors such as:

| ● | interest rates; |

| ● | currency fluctuations; |

| ● | monetary policies; |

| ● | inflation; |

| ● | liquidity of capital and lending markets; |

| ● | tax and social security policies; |

| ● | labor regulations; |

| ● | energy and water shortages and rationing; and |

| ● | other political, social and economic developments in or affecting Brazil, Chile, Peru, and the United States, among others. |

For example, the Brazilian federal government has frequently intervened in the domestic economy and made drastic changes in policy and regulations to control inflation and affect other policies and regulations. This required the federal government to increase interest rates, change taxes and social security policies, implement price controls, currency exchange and remittance controls, devaluations, capital controls and limits on imports.

Uncertainty over whether the Brazilian federal government will implement changes in policy or regulation affecting these or other factors may contribute to economic uncertainty in Brazil and to heightened volatility in the Brazilian securities markets and securities issued abroad by Brazilian companies. These and other developments in the Brazilian economy and governmental policies may adversely affect us and our business and results of operations and may adversely affect the trading price of our preferred shares and ADSs.

We are also subject to international bilateral air transport agreements that provide for the exchange of air traffic rights between the countries where we operate, and we must obtain permission from the applicable foreign governments to provide service to foreign destinations. There can be no assurance that such existing bilateral agreements will continue, or that we will be able to obtain more route rights under those agreements to accommodate our future expansion plans. Certain bilateral agreements also include provisions that require substantial ownership or effective control. Any modification, suspension or revocation of one or more bilateral agreements could have a material adverse effect on our business, financial condition and results of operations. The suspension of our permits to operate to certain airports or destinations, the inability for us to obtain favorable take-off and landing authorizations at certain high-density airports or the imposition of other sanctions could also have a negative impact on our business. We cannot be certain that a change in ownership or effective control or in a foreign government’s administration of current laws and regulations or the adoption of new laws and regulations will not have a material adverse effect on our business, financial condition and results of operations.

Losses and liabilities in the event of an accident involving one or more of our aircraft could materially affect our business.

We are exposed to potential catastrophic losses in the event of an aircraft accident, terrorist incident or any other similar event. There can be no assurance that, as a result of an aircraft accident or significant incident:

| ● | we will not need to increase our insurance coverage; |

| ● | our insurance premiums will not increase significantly; |

| ● | our insurance coverage will fully cover all of our liability; or |

| ● | we will not be forced to bear substantial losses. |

Substantial claims resulting from an accident or significant incident in excess of our related insurance coverage could have a material adverse effect on our business, financial condition and results of operations. Moreover, any aircraft accident, even if fully insured, could cause the negative public perception that our aircraft are less safe or reliable than those operated by other airlines, or by other flight operators, which could have a material adverse effect on our business, financial condition and results of operations.

Insurance premiums may also increase due to an accident or incident affecting one of our alliance partners or other airlines.airlines, or due to a perception of increased risk in the industry related to concerns about war or terrorist attacks, the general industry, or general industry safety.

High levels of competition in the airline industry, such as the presence of low-cost carriers in the markets in which we operate, may adversely affect our level of operations.