0001877787 iiac:MonterubelloAndCompaniesControlledByMonterubelloOritsShareholdersZegnaDirectorsOrSeniorManagementMember iiac:PkbPrivateBankAgMember 2021-01-01 2021-12-31 0001877787 iiac:ThomBrowneCanadaMember iiac:ThomBrowneTradingSaMember 2021-12-310001877787zgn:IndustrialAndCommercialEquipmentMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2022-12-31

SECURITIES AND EXCHANGE COMMISSION

☐ | ☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

☒ | ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2021

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D)☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

☐ | ☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number:

001-41180

(Exact name of Registrant as specified in its charter)

| | | | | |

| | |

(Translation of Registrant’s name into English)

| | (Jurisdiction of incorporation or organization)

|

Not applicable The Netherlands

(Translation of Registrant’s name into English) (Jurisdiction of incorporation or organization)

Viale Roma 99/100

13835 Valdilana loc. Trivero

(Address of principal executive offices)

Gianluca Ambrogio Tagliabue

Viale Roma 99/100, 13835 Valdilana loc. Trivero, Italy

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| | Trading Symbol(s) | | | |

Ordinary Shares, nominal value €0.02 per share | | ZGN | | | |

Warrants, each whole warrant exercisable for one Ordinary Share at an exercise price of $11.50 per share

| | | | |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

OnAt December 31, 2021,2023, the issuer had 242,343,659250,310,263 ordinary shares, nominal value €0.02 per share, and 154,981,350 special voting shares A, nominal value €0.02 per share, outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of RegulationS-T

(§ (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐ Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a

non-accelerated

filer, or an emerging growth company. See

definitionthe definitions of

“accelerated“large accelerated filer,”

“large accelerated“accelerated filer,” and “emerging growth company” in Rule

12b-2

of the Exchange Act.

(Check one):

| | | | | | | | | | | |

| Large accelerated filer | | ☐ | ☒ | Accelerated filer | | ☐ |

| | | |

| Non-accelerated filer | | ☒ | ☐ | Emerging growth company | | ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| | | | | | | | | | | | | | |

U.S. GAAP ☐ | | International Financial Reporting Standards as issued | | | | Other ☐ |

| | �� by the International Accounting Standards Board ☒ | | | | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule12b-2

of the Exchange Act). Yes ☐ No ☒

| | | | | |

| | 102 | |

| | | 102 | |

| | | 102 | |

| | | 102 | |

| | | 115 | |

| |

| E. Taxation | | 115 | |

| | | 115 | |

| | | 138 | |

| | | 138 | |

| | | 138 | |

| | | 138 | |

| | | 138 | |

| | | 139 | |

| | | 139 | |

| | | 139 | |

| | | 139 | |

| | | 139 | |

| | | | |

| | | 140 | |

| | | 140 | |

| | | 140 | |

| | | 140 | |

| | | 141 | |

| | | 141 | |

| | | 141 | |

| | | 142 | |

| | | 142 | |

| | | 142 | |

| | | 142 | |

| | | 143 | |

| | | 143 | |

| |

| |

| | | 144 | |

| | | 144 | |

| | | 144 | |

| | | 144 | |

Table of Contents

In this report, unless otherwise specified, the terms “Zegna”, “”, “”, and the “”, the “” and “” refer to the Registrant, Ermenegildo Zegna N.V., a Dutch public limited liability company (), following(naamloze vennootschap); the Conversionterms “Ermenegildo Zegna Group” and priorthe “Group” refer to the Conversion, to Ermenegildo Zegna Holditalia S.p.A., a joint stock company incorporated under Italian law, in each caseCompany together with its consolidated subsidiaries,subsidiaries. Unless otherwise specified, the terms “we,”“our” and “us,” refer to the Group or any one or more of them,the Company, as the context may require. “” means, with respect to any Person, any other Person who directly or indirectly, through one or more intermediaries, controls, is controlled by, or is under common control with, such Person. The term “control” means the possession, directly or indirectly, of the power to direct or cause the direction of the management and policies of a Person, whether through the ownership of voting securities, by contract or otherwise, and the terms “controlled” and “controlling” have meanings correlative thereto. “Articles of Association” means the articles of association of the Company.

” means the audit committee of the Zegna Board.“Board” means the Company’s board of directors.

“Board Regulations” means the regulations of the Board, as amended or supplemented from time to time.

“Business Combination

Zegnathe Company and IIAC, which was completed on December 17, 2021.“Business Combination Agreement

Zegna,the Company, and Zegna Merger Sub, as amended or supplemented from time to time. “” means a return of capital distribution under Cayman Islands law whereby, on the Closing Date, immediately following the PIPE Financing and prior to the Share Repurchase, IIAC distributed the Capital Distribution Amount to Zegna.the Company. “Capital Distribution Amount

“” means an amount of €455,000,000. “” means the Class A ordinary shares, par value $0.0001 per share, of IIAC prior to the Merger. “” means the Class B ordinary shares, par value $0.0001 per share, of IIAC prior to the Merger. “” means the closing of the Business Combination. “” means December 17, 2021. “” means the compensation committee of the Zegna Board. “” means the cross-border conversion whereby, on December 17, 2021, Zegna,the Company, by means of the execution of a Dutch notarial deed of cross-border conversion and amendment of its articles of association, converted into a Dutch public limited liability company ()(naamloze vennootschap) and transferred its legal seat from Italy to the Netherlands and amended its articles of association, as a result of which Zegnathe Company assumed its current legal name “Ermenegildo Zegna N.V.” “” means the Dutch Corporate Governance Code. “” has the meaning set forth in “Item 5.A—Operating Results—Trends, Uncertainties and Opportunities—Disposition of certain businesses.” “Item 5—Operating and Financial Review and Prospects1

”.

“Director” means an Executive Director or a Non-Executive Director.

” has the meaning set forth in“Item 5—5.A—Operating Results—Trends, Uncertainties and Financial Review and Prospects

.“” means directly operated stores. “”means direct-to-consumer.

“” means the time the Merger became effective on the Closing Date. “” means 50%the portion of the Ordinary Shares that were issued to the IIAC Initial Shareholders in(in exchange for their Class B Shares,Shares) which Ordinary Shares are currently held in escrow subject to the release conditions described in the prospectus.Business Combination Agreement. “” means the Securities Exchange Act of 1934, as amended. “Executive Director” means an executive member of the Board.

” means the transactions contemplated by the Forward Purchase Agreement.“Forward Purchase Agreement

“” means Strategic Holding Group S.à r.l., an affiliate of the IIAC Sponsor. “General Meeting” means the corporate body that consists of the shareholders of the Company and all other Persons with meeting rights and also the meeting in which shareholders of the Company and all other Persons with meeting rights assemble, as the case may be.

“Governance and Sustainability Committee

Zegna Board.“” means the hedging positions and arrangements that effectively transfer the economic interest of any member of the Sponsor Group in Zegnathe Company to a third party (e.g., forward sale contracts); provided, that the definition of “Hedged Positions” shall not include hedging positions and arrangements (a) in which the economic interest of any member of the Sponsor Group in Zegnathe Company is retained (e.g., pledges and margin loans), (b) that minimize exposure to certain risks independent of the business operations of Zegnathe Company (e.g., currency exchange swaps) or (c) that marginally cap or limit the upside/downside risk of any member of the Sponsor Group while maintaining material economic exposure (e.g., puts, calls and collars), as determined in good faith by the Zegna Board and such member of the Sponsor Group. “” means Investindustrial Acquisition Corp., a Cayman Islands exempted company. “IIAC Initial Shareholders

”Shareholders” means the FPA Purchaser, Sergio P. Ermotti, Audeo Advisors Limited, Jose Joaquin Guell Ampuero, Dante Roscini and Tensie Whelan. “” means collectively the Class A Shares and the Class B Shares prior to the Merger. “IIAC Private Placement Warrants

“” means warrants to acquire Class A Shares, issued as part of units in the IIAC initial public offering consummated on November 23, 2020, at an initial exercise price of $11.50 per share. “” means the IIAC Private Placement Warrants and the IIAC Public Warrants. “” means Investindustrial Acquisition Corp. L.P., a limited partnership incorporated in England and Wales.“IIAC SponsorLock-Up

Agreement lock-up

agreement, entered into at the Closing, by and among Zegna,the Company, IIAC Sponsor and the IIAC Initial Shareholders.

“IIAC Warrants” means the IIAC Private Placement Warrants and the IIAC Public Warrants.

“Insider PIPE Subscribers

“LeadNon-Executive

Director Zegna Director serving as lead non-executive director. “” means the separate part of Zegna’sthe Company’s shareholder register instrumental to Zegna’sthe Company’s loyalty voting structure. “” means the merger of Zegna Merger Sub with and into IIAC, with IIAC being the surviving company. “Minimum Holding Requirement

”Requirement” means the beneficial ownership (as such term is defined inRule 13d-3 under

the Exchange Act) by the Sponsor Group, of at least 5% of the issued and outstanding Ordinary Shares, excluding (i) any Hedged Positions as evidenced by the IIAC Sponsor in writing and (ii) any Escrowed Shares that have not been released from escrow to the applicable Sponsor Group member.

“” means Monterubello s.s., an Italian.semplice. “Non-Executive Director” means a non-executive member of the Warrant Agreement entered into concurrently with the Closing, by and between Zegna, Computershare Trust Company, N.A., and Computershare Inc.Board. “” means the New York Stock Exchange. “” means the private placement of 12,500,000 Ordinary Shares to the Offset PIPE Investors, for gross proceeds to Zegnathe Company in an aggregate amount of $125,000,000, pursuant to the Offset Subscription Agreements. “” means investors in the Offset PIPE Financing pursuant to the Redemption Offset Agreements and the Offset Subscription Agreements. “Offset Subscription Agreements

Zegnathe Company and the Offset PIPE Investors named therein. “” means the ordinary shares, nominal value €0.02 per share, of Zegna.the Company. “” means an individual, partnership, corporation, limited liability company, joint stock company, unincorporated organization or association, trust, joint venture or other similar entity, whether or not a legal entity. “” means the private placement of 25,000,000 Ordinary Shares to the PIPE Investors, for gross proceeds to Zegnathe Company in an aggregate amount of approximately $250,000,000, pursuant to the PIPE Subscription Agreements. “” means the investors (including the Insider PIPE Subscribers) in the PIPE Financing pursuant to the PIPE Subscription Agreements. “” means the 37,500,000 Ordinary Shares that were issued to certain securityholders in connection with the closing of a private placement offering concurrent with the Closing. “” means those certain subscription agreements entered into on July 18, 2021, among IIAC, Zegnathe Company and the PIPE Investors named therein relating to the PIPE Financing.“Private Placement Warrants

“” means warrants to acquire Ordinary Shares on the same contractual terms and conditions as the IIAC Public Warrants. “Redemption Offset Agreements

Zegnathe Company and the Offset PIPE Investors named therein relating to the offset of redemptions of Class A Shares by IIAC public shareholders up to a certain level.

“Registration Rights Agreement

Zegna,the Company, in each case, on the terms and subject to the conditions in such registration rights agreement.“” means the Sarbanes-Oxley Act of 2002, as amended. “” means the United States Securities and Exchange Commission. “” means the Securities Act of 1933, as amended. “Senior Management Team” means the Group’s senior management.

“Share Repurchase” means the repurchase by the Company of 54,600,000 Ordinary Shares from Monterubello in exchange for the Cash Consideration.

“Shareholders Agreement

” means the shareholders agreement entered into at Closing by and among Zegna,the Company, the IIAC Sponsor, Monterubello and Mr. ErmenegildoGildo Zegna.“Special Voting Shares” means, collectively, the Special Voting Shares A, the Special Voting Shares B and the Special Voting Shares C.

“Special Voting Shares A” means the repurchase by Zegnaspecial voting shares class A, nominal value of 54,600,000 Ordinary€0.02 per share, of the Company.“Special Voting Shares from Monterubello in exchange forB” means the Cash Consideration.special voting shares class B, nominal value of €0.08 per share, of the Company.

“Sponsor

Special Voting Shares C” means the special voting shares class C, nominal value of €0.18 per share, of the Company.

“” means theZegna Non-Executive Director

to be nominated by the IIAC Sponsor in accordance with the Zegna Articles of Association. “” means IIAC following the Merger. “Terms and Conditions of the Zegna Special Voting Shares

Zegna Special Voting Shares and certain aspects of the registration of the Ordinary Shares in the Loyalty Register. “TFI Acquisition”means the acquisition of Tom Ford International (“TFI”), as further described in “Item 4.A—History and Development of the Company—TFI Acquisition.”

Redemption” means the Warrant Agreement,redemption of all our outstanding Warrants, which was completed on February 27, 2023 and as described in the notice of redemption dated as of November 23, 2020, between IIAC and Continental Stock Transfer & Trust Company, as subsequently amended by the Warrant Agreement Amendment and the Warrant Assumption and Amendment Agreement.January 26, 2023.“Warrant Agreement Amendment

” means the Warrant Agreement Amendment, entered into immediately prior to the Effective Time, by and between IIAC and Continental Stock Transfer & Trust Company. “Warrant Assumption and Amendment Agreement

” means the Warrant Assumption and Amendment Agreement, entered into concurrently with the Closing, by and among IIAC, Zegna, Continental Stock Transfer & Trust Company, Computershare Trust Company, N.A. and Computershare Inc.“” means, collectively, the Public Warrants and the Private Placement Warrants.“Zegna Articles of Association

” means the articles of association of Zegna. “” means Zegna’s board of directors.“” means the regulations of the Zegna Board, as amended or supplemented from time to time.“” means a Zegna Executive Director or aZegna Non-Executive Director.

“” means an executive member of the Zegna Board.“” means the corporate body that consists of the shareholders of Zegna and all other Persons with meeting rights and also the meeting in which shareholders of Zegna and all other Persons with meeting rights assemble, as the case may be.“Zegna Initial Shareholders

“” means EZ Cayman, a Cayman Islands exempted company. “” meansa non-executive member

of the Zegna Board. “Zegna ShareholdersLock-Up

Agreement lock-up

agreement, entered into at the Closing, by and among Zegnathe Company and the Zegna Initial Shareholders.“” means, collectively, the Zegna Special Voting Shares A, the Zegna Special Voting Shares B and the Zegna Special Voting Shares C.“Zegna Special Voting Shares A

” means the special voting shares class A, nominal value of €0.02 per share, of Zegna.“Zegna Special Voting Shares B

” means the special voting shares class B, nominal value of €0.08 per share, of Zegna.“Zegna Special Voting Shares C

” means the special voting shares class C, nominal value of €0.18 per share, of Zegna.

Table of Contents

This document includes the consolidated financial statements of Ermenegildo Zegna N.V. as ofat December 31, 20212023 and 2020,2022, and for each of the three years in the period ended December 31, 2021,2023, prepared in accordance with International Financial Reporting Standards (“”) as issued by the International Accounting Standards Board (“”), as well as IFRS as adopted by the European Union. There is no effect on these consolidated financial statements resulting from differences between IFRS as issued by the IASB and IFRS as adopted by the European Union. We refer to these consolidated financial statements collectively as the “Consolidated Financial Statements

Basis of Preparation of the Consolidated Financial Statements

As explained in Item 4.A of this report, onOn December 17, 2021 we closed the previously announced Business Combination pursuant to the Business Combination Agreement, dated as of July 18, 2021, as amended, by and among us, IIAC and Zegna Merger Sub, our wholly owned subsidiary. For more information on the Business Combination, see “Item 4.A—History and Development of the Company.

The Group’s financial information is presented in Euro. In certain instances, information is presented in U.S. Dollars. All references in this document to “”“Euro” and ““€” refer to the currency introduced at the start of the third stage of European Economic and Monetary Union pursuant to the Treaty on the Functioning of the European Union, as amended, and all references to “” “US$” and ““$” refer to the currency of the United States of America (the “”). The language of this document is English. Certain legislative references and technical terms have been cited in their original language in order that the correct technical meaning may be ascribed to them under applicable law.

Certain totals in the tables included in this document may not add due to rounding.

TRADEMARKS, SERVICE MARKS AND TRADE NAMES

This report includes trademarks, tradenamestrade names and service marks, certain of which belong to Zegnathe Group and others that are the property of other organizations. Solely for convenience, some of the trademarks, service marks, logos and trade names referred to in this report are presented without the®

and™

symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks and trade names. This report contains additional trademarks, service marks and trade names of others. All trademarks, service marks and trade names appearing in report are, to our knowledge, the property of their respective owners. We do not intend our use or display of other companies’ trademarks, service marks, copyrights or trade names to imply a relationship with, or endorsement or sponsorship of us by, any other companies. MARKET AND INDUSTRY INFORMATION

Information contained in this report concerning the market and the industry in which we compete, including our market position, general expectations of market opportunity and market size, is based on information from various third party sources, assumptions made by us based on such sources and our knowledge of the personal luxury goods market. This information and any estimates provided herein involve numerous assumptions and limitations, and you are cautioned not to give undue weight to such information. Third partyThird-party sources generally state that the information contained in such source has been obtained from sources believed to be reliable but that there can be no assurance as to the accuracy or completeness of such information. We have not independently verified any third partythird-party information. The industry in which we operate is subject to a high degree of uncertainty and risk. As a result, the estimates and market and industry information provided in this report are subject to change based on various factors, including those described in the sections entitled “Cautionary Note Regarding Forward-Looking Statements

Item 4.B—Business Overview—Industry

, unless otherwise indicated, has been based on the Bain-Altagamma Luxury Goods Worldwide Market Study, Fall 2021,2023, dated November 11, 2021.14, 2023.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements. Forward-looking statements provide the current expectations or forecasts of future events of Zegna.the Company. Forward-looking statements include statements about Zegna’sthe Company’s expectations, beliefs, plans, objectives, intentions, assumptions and other statements that are not historical facts. Words or phrases such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “objective,” “ongoing,” “plan,” “potential,” “predict,” “project,” “should,” “will” and “would,” or similar words or phrases, or the negatives of those words or phrases, may identify forward-looking statements, but the absence of these words does not necessarily mean that a statement is not forward-looking. Examples of forward-looking statements in this report include, but are not limited to, statements regarding Zegna’s disclosure concerning Zegna’sthe Group’s operations, cash flows, financial position and dividend policy.

Forward-looking statements are subject to known and unknown risks and uncertainties and are based on potentially inaccurate assumptions that could cause actual results to differ materially from those expected or implied by the forward-looking statements. The risks and uncertainties include, but are not limited to:

the impact ofCOVID-19

or similar public health crises on Zegna’s business;disruptions arising from political, social and economic instability, geopolitical tensions or civil unrest, including the current conflict in Ukraine;

the effect of the consummation of the Business Combination on Zegna’s business, cash flows, financial condition or results of operations;

•the ability of Zegnathe Group to safeguard the recognition, integrity and reputation of its brands and to identify and respond to new and changing customer preferences;

•the impact of COVID-19 or similar public health crises on the Group’s business;

•disruptions arising from political, social and economic instability, geopolitical tensions or civil unrest, including the current conflict in Ukraine and sanctions imposed onto Russia; •the ability of Zegnathe Group to successfully implement its strategy;

•the ability of the Group to achieve the expected benefits of businesses we may acquire;

•disruptions to Zegna’sthe Group’s manufacturing and logistics facilities, as well as DOSs, including as a result of theCOVID-19

pandemic; DOSs;•risks related to the operation of Zegna’sthe Group’s DOSs, including as a result of difficulties in renewing the existing lease agreements, an increase in rental charges or a decline in sales, and the operation of points of sale by third parties in the wholesale channel;

•fluctuations in the price or quality of, or disruptions in the availability of, raw materials used by Zegnathe Group for its products or of commodities such as energy, which could cause Zegnathe Group to incur increased costs, disrupt its manufacturing processes or prevent or delay Zegnathe Group from meeting its customers’ demand;

•the ability of Zegnathe Group to negotiate, maintain or renew license or co-branding agreements with high end third party brands;

•shifts in travel patterns or declines in travel volumes, including as a result of theCOVID-19

pandemic; volumes;•the ability to attract and retain key senior and skilled personnel and preserve craftmanshipcraftsmanship skills;

Zegna’s•the Group’s ability to protect its intellectual property rights;

•disruptions or breaches compromising Zegna’sin the Group’s information technology systems compromising the Group’s business operations or the personal information of Zegna’s customers;

Zegna’s ability to maintain Zegna’s securities’ listing on the NYSE;

•the fact that the market price of Zegna’sthe Company’s securities may be volatile due to a variety of factors;

•the ability to develop and maintain effective internal controls;

•the Company has identified material weaknesses have been identified in Zegna’sits internal control over financial reporting andreporting; if Zegnathe Company fails to remediate these material weaknesses or maintain an effective system of internal controls, it may not be able to produce timely and accuratethis could result in a material misstatement in the Company’s consolidated financial statements or comply with applicable laws and regulations;

may subject us to adverse regulatory

consequences and affect investor confidence in us and, as a result, the price of our securities and our ability to access the capital markets and other forms of financing in the future may be impaired;

•changes in local economic, business, regulatory, social and political conditions, as well as changes in general economic conditions (such as significant inflation) and in demand for luxury goods;

•exchange rate fluctuations, interest rate changes, credit risk and other market risks;

•the high levels of competition in the luxury goods market;

•compliance with laws, including laws and regulation related to intellectual property, competition, product safety, packaging and labeling, import and processing of certain raw materials and finished goods, data protection and privacy, limits on cash payments, workersanctions, workers’ health and safety, human rights and the environment;

•risks related to climate change and other environmental impacts, as well as an increased focus by regulators and stakeholders on environmental, social and governance matters;

•changes in trade policy, the imposition of tariffs, the enactment of tax reforms and other changes in laws and regulations; and

•other factors discussed elsewhere in this report in the section “.”. Actual results could differ materially from those anticipated in forward-looking statements for many reasons, including the factors described in the section “” of this report. Accordingly, you should not rely on such forward-looking statements, which speak only as ofat the date of this report. ZegnaThe Company undertakes no obligation to publicly revise any forward-looking statement to reflect circumstances or events after the date of this report or to reflect the occurrence of unanticipated events. You should, however, review the factors and risks Zegnathe Company describes in the reports it will file from time to time with the SEC. Although Zegnathe Company believes the expectations reflected in the forward-looking statements were reasonable at the time made, it cannot guarantee future results, level of activity, performance or achievements. Moreover, neither Zegna,the Company, nor any other person assumes responsibility for the accuracy or completeness of such forward-looking statements. You should carefully consider the cautionary statements contained or referred to in this section in connection with the forward-looking statements contained in this report and any subsequent written or oral forward-looking statements that may be issued by Zegnathe Company or persons acting on its behalf.

Table of Contents

| ITEM 1 IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2 OFFER STATISTICS AND EXPECTED TIMETABLE |

ITEM 3 KEY INFORMATION

A. [Reserved]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Summary of Risk Factors

The following is a summary of the principal risk factors that could have a material adverse effect on our business, results of operations and financial condition. Please carefully consider all of the information discussed in this “Item 3.D—Risk Factors” for a detailed description of such risks.

•Our business depends on the recognition, integrity and reputation of our brands and on our ability to identify and respond to new and changing customer preferences.

•The resurgence of the COVID-19 pandemic or similar public health crises may materially and adversely affect our business.

•Disruptions arising from political, social and economic instability, geopolitical tensions or civil unrest, including the current conflict in Ukraine and sanctions imposed onto Russia, may adversely affect our business.

•We may not be able to successfully implement our strategy, including the further enhancement of the ZEGNA brand, the successful integration of the TOM FORD FASHION business and Thom Browne’s international expansion.

•Disruptions to our manufacturing and logistics facilities, as well as DOSs, may adversely affect our business.

•The sale of our products through our DTC channel and directly operated stores is subject to certain risks, including as a result of difficulties in renewing the existing lease agreements, increases in rental charges or declines in sales, which may adversely affect our business.

•In the wholesale channel, we are subject to certain risks arising from points of sale operated by third parties, and we are dependent on our local partners to sell products in certain markets.

•Fluctuations in the price or quality of, or disruptions in the availability of, raw materials used in our products or of commodities such as energy, could cause us to incur increased costs, disrupt our manufacturing processes or prevent or delay us from meeting our customers’ demands.

•We could be adversely affected if we are unable to negotiate, maintain or renew our license or co-branding agreements.

•The loss or unavailability of certain key senior personnel as well as skilled personnel could adversely affect our business.

•We could be adversely affected by fluctuations in exchange rates.

Risk factors relating to Zegna’sthe Group’s business, strategy and operations

Our business depends on the recognition, integrity and reputation of our brands.

We design, manufacture, promote and sell luxury goods under a number of brands, including ZegnaZEGNA and Thom Browne and, untilBrowne. Pursuant to a long-term license agreement with The Estée Lauder Companies, we also operate the full implementation of our rebranding strategy, our Ermenegildo Zegna, Z Zegna and Ermenegildo Zegna XXX brands.TOM FORD FASHION (“TFF”) business. Our sales and our ability to achieve premium pricing depend on the perception, recognition and reputation of our brands, which, in turn, depend on factors such as product design, the distinctive character and the quality of our products and customer service, the image of our stores and those of our franchisees and other wholesale customers, the success of our advertising and communication activities and our general corporate profile.

The recognition, integrity and reputation of our brands are among our most valuable assets, which are influenced by several factors, some of which are outside of our control. Factors that may adversely affect our brands’ image include our inability to respond adequately to the needs and expectations of our customers with regard to the quality, style and design, as well as the social and environmental sustainability, of our products, the service we provide in our stores, the dissemination by third parties of information that is untrue or defamatory, the commencement of litigation proceedings against us, as well as factors attributable to the parallel distribution and counterfeiting of our products.

As we expand into new marketing channels, we may pursue new collaborations with designers, artists, promoters and influencers to attract new customers and drive engagement with existing customers. Such collaborators could engage in behavior, make statements or use their platforms in a manner that reflects poorly on our brand or otherwise adversely affect us. We may be unable prevent such actions, and the actions we take to address them may not be effective in all cases. Each of these factors could harm the recognition, integrity and reputation of our brands, causing us to lose existing customers or fail to attract new customers, or otherwise having a material adverse effect on our business, results of operations and financial condition.

Our reputation may also suffer as a result of facts depending onfactors or actions attributable to our suppliers. While we closely monitor our suppliers to ensure that they comply with all applicable laws and regulations, if suppliers fail to comply with applicable law, including those relating to labor, social security, health and safety, human rights, or if they deliver products that are defective or differ from our specifications or quality standards or do not comply with applicable law, this could have adverse effects on our production cycle and cause delays in product deliveries to our customers, which in turnand could damage our reputation, with possible adverse effects on our business, results of operations and financial condition.

Our success depends on our ability to anticipate trends and to identify and respond to new and changing consumer preferences.

Our continued success depends in part on our ability to set and define product and fashion trends, and in part on our ability to identify and respond to changing consumer preferences in a timely manner. Our products must appeal to an evolving customer base whose preferences cannot be predicted with certainty and are subject to increasingly rapid change, while preserving the image and recognition of our brands. Although we dedicate considerable resources to market analysis and the identification of new fashion trends, we may not be able to promptly anticipate fashion trends or to quickly adapt to these trends during the design and manufacturing stages. If we fail to identify or promptly respond to new trends or changing consumer preferences, including concerns or perceptions regarding the sustainability and environmental impact of our products, our brands’ reputation may be affected, which could result in unsold products, a decline in sales to customers and could have a material adverse effect on our business, results of operations and financial condition.

Table of Contents

We are subject to risks related to the

COVID-19

pandemic or similar public health crises that may materially and adversely affect our business.

Public health crises such as pandemics could adversely impact our business. The global spread of

COVID-19,

including

more recently the highly transmissible Delta and Omicron variants thereof,

led to governments around the world mandating restrictive measures, including quarantine, social distancing, “shelter in place” or similar orders, travel restrictions and suspension ofnon-essential

business activities. TheCOVID-19

pandemic has caused significant disruption to the global economy, consumer spending and behavior, tourism, supply chains and financial

markets, leadingmarkets.The COVID-19 pandemic, the ensuing government-mandated restrictive measures and the responsive actions adopted by the private sector and individual consumers adversely impacted our business operations, store traffic, employee availability, supply chain, financial condition, liquidity and cash flows, primarily in 2020 at the onset of the pandemic and in 2022 due to a global economic slowdown and a severe recession in severalnew wave of the marketsvirus and the resulting lockdown restrictions in which we operate, whichcertain parts of the Greater China Region, the Group’s largest geographical market. The continuation or reintroduction of these restrictions or any new restrictions may persist even after all restrictions are lifted.adversely affect our business, results of operations and financial condition.

In connection with theCOVID-19

pandemic and related government measures, we experienced suspension or slowdown of our production at our manufacturing and logistics facilities in 2020 and 2021, as well as delays in deliveries of raw materials from suppliers and of our products to wholesale customers, temporary closures of our DOSs and our distribution partners’ stores, as well as running costs related to our workforce, despite furlough or reduced hours schemes we implemented with respect to certain of our employees. While we continued to serve our customers through our remote selling and onlinee-commerce

websites during the periods in which our DOSs were closed, the store closures resulted in a significant decline in our revenues and ability to generate cash flows from operations. For further information on the impact of theCOVID-19

pandemic on our results of operations and liquidity, see “Item 5—5.A—Operating and Financial Review and Prospects—Results—Trends, Uncertainties and Opportunities.”

” TheGlobal trade conditions and consumer trends that originated during the COVID-19

pandemic continue to persist and may also have long-lasting adverse impacts on our business independently of the progress of the pandemic. For instance, the pandemic has alsoled to shifts in tourism patterns and the emerging of new tourist destinations, thus reshaping the geographical landscape of our store and distribution network. These shifts have resulted in a decline inincreased expenditure associated with the levelphysical and logistical expansion of consumer purchases of discretionary itemsour distribution network, as well as the need to adjust distribution strategies and luxury retail products, including our products, caused by lower disposable income levels, travel restrictions, the prevalence oflogistics. Moreover, increasing remote working arrangements may result in lower luxury purchases.Although COVID-19-related restrictions have generally been lifted across the markets where we operate, our businesses may continue to experience impacts from a resurgence of COVID-19 or other widespread public health crises, such as incremental health and

other factors. As a result of storesafety measures and related increased expenses, capacity restrictions and closures,

and lower consumer demand, we experienced abuild-up

of inventory. While the overallCOVID-19

situation appears to have improved in countries that have rolled out vaccination campaigns, our business and operating results may be negatively impacted if the virus worsensas well as new shutdowns or

mutates, if vaccination efforts are unsuccessful or if regions or countries implement further restrictions to contain the virus. We may experience a new shutdown or slowdownslowdowns of all or part of our manufacturing and logistics

facilities,operations and of our stores.

InA resurgence of the

first monthsCOVID-19 pandemic or the occurrence of

2022 we experienced minor delays in production in certain countries where a significant number of our and our suppliers’ employees had to stay at home after becoming infected withCOVID-19.

Since March 2022, dueother widespread public health crises may contribute to a

new wave of the virus in certain parts of the Greater China Regionrecession, depression or global economic downturn, reduce store traffic and

the resulting lockdown restrictions, we have been required to close certain of our DOSs in the Greater China Region, and DOSs that remained open have experienced significantly lower customer traffic. Management time and resources were required to be, and in the future may need to be, spent onCOVID-19

related matters, distracting them from the implementation of our strategy. In addition, the prophylactic measures we are required to adopt at our facilities may be costly and may affect production levels.Our suppliers, customers and other contractual counterparties may be restricted or prevented from conducting business activities for indefinite or intermittent periods of time. TheCOVID-19

pandemic mayconsumer spending, lead to financial distress for our suppliers or wholesale customers, as a result of which they may have to permanently discontinue or substantially reduce their operations. Any of the foregoing could

disrupt our supply chain and/or limit customer demand or our capacity to meet customer demand,

disrupt our supply chain and have a material adverse effect on our business, results of operations and financial condition.

The impact of the

COVID-19

pandemic on our business, results of operations and financial condition will

ultimately depend largely on future events outside of our control, including ongoing developments in the pandemic

(including the appearance of new variants of the virus), the success of containment measures, vaccination campaigns and other actions taken by governments around the world, as well as the overall condition and outlook of the global economy. However, the effects on our business, results of operations and financial condition may be material and adverse.

TheCOVID-19

pandemic or other widespread public health crises may also exacerbate other risks disclosed in this “Item 3.D—3.D.—Risk Factors,

, including, but not limited to, our competitiveness, demand for our products, shifting consumer preferences, exchange rate fluctuations, and availability and price of raw materials.

We operate in many countries around the world and, accordingly, we are exposed to various international business, regulatory, social and political risks.

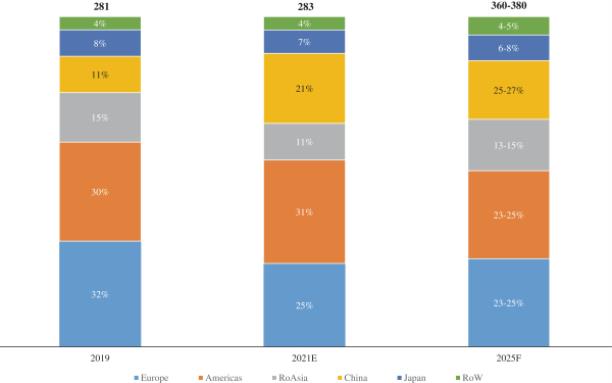

We operate in over 80approximately 85 countries worldwide through a direct and indirect distribution network. For the year ended December 31, 2021, 54%2023, 41% of our revenues were generated in APAC, 29%35% were generated in EMEA, 15%22% were generated in North America and 2% were generated in Latin America.

Our operations in various international markets expose us to various risks, including those arising from: competition with local competitors (which may have greater resources and/or more favorable market positions); the diversity of consumers’ tastes and preferences and our ability to anticipate or respond to such tastes and preferences; changes in the political and economic environments in the countries where we operate; changes in regulations, including tax regulations, and the imposition of new duties or other protectionist measures; strict regulations affecting the import and processing of certain

raw materials and finished goods; the occurrence of acts of terrorism or similar events, conflicts,

geopolitical tensions, civil unrest or situations of political instability; parallel imports of goods at terms inconsistent with our guidelines and distribution of our products, in violation of exclusive territorial rights granted to other importers and licensees (the

so-called

“gray “gray market”)

., which may force us to reposition our pricing in certain countries and erode our profitability. These or other factors may harm our business in international markets or cause us to incur significant costs in these markets, which could have a material adverse effect on our business, results of operations and financial condition.

The conflict in Ukraine and sanctions imposed onto Russia may adversely affect our business.

Due toThe ongoing conflict in Ukraine and resulting geopolitical tensions

manyhave had an abrupt impact on the global economy resulting in a sharp increase in energy prices and higher prices for certain raw materials and goods and services, which in turn have contributed to higher inflation around the world. The extent and duration of the military action, sanctions and resulting market disruptions are impossible to predict, but could be material and adverse. Many governments around the world, including those of the United States, the European Union, the United Kingdom and other jurisdictions, have

recently announced the imposition of sanctions on certain industries and parties in Russia,

Belarus and the Ukrainian regions of Donetsk and Luhansk, as well as export controls on certain industries and products,

including luxury goods, and the exclusion of certain Russian financial institutions from the SWIFT system. On March 11, 2022, the President of the United States issued an executive order prohibiting exports to Russia of luxury goods (including,

, apparel, footwear and certain accessories with a per unit wholesale price of $1,000 or more).

Shortly thereafter, onOn March 15, 2022, the Council of the European Union imposed new sanctions on Russia prohibiting the export of luxury goods having a value in excess of €300 per item (including clothing, footwear, leather and fashion accessories). These and any additional sanctions or export controls, as well as any counter responses by the governments of Russia or other countries, are adversely affecting, and will continue to adversely affect, directly or indirectly, our supply chain and customers, as well as the global financial markets and financial services industry.

The Russian market represented 1.5%0.01%, 2.0%0.3% and 1.5% of our revenues in 2021, 20202023, 2022 and 2019,2021, respectively. Our business operations in such market areused to be conducted through franchisees and distribution partners. Pursuant to the aforementioned sanctions, we are required to suspendsuspended indefinitely deliveries to our franchisees and distributors in Russia. Accordingly, we haveeither suspended production of products forstarting with the Fall/Winter 2022 collection ordered by our Russian franchisees and distributors or redirected any products ordered by Russian franchises and itdistributors for the Fall/Winter 2022 collection to our DOSs in other regions or to other franchisees and distributors. It is uncertain whether and when we will be able to resume such production. As we have already purchased raw materials for such production, we may be unable to repurpose all of the excess materials, which may therefore become obsolete. In light of the current crisis there is also no assurance that we will be able to collect from our franchisees and distributors in Russia certain outstanding receivable amounts for completed sales of the Spring/Summer 2022 collection; as of the date of this report, such amounts were not material. Finally, several of the agreements with our wholesale customers in Russia are due to expire during the course of 2022 and 2023. It is uncertain whether, when and at what terms and conditions such agreements will be renewed. Any of the foregoing factors could have a material adverse effect on our business, results of operations and financial condition.

In general, the banking, economic and monetary crisis, as well as the escalating energy prices triggered by the conflict may reduce customers’ interest for, and financial ability to buy, luxury products. An expansion of the conflict to other European countries, the United States or other parts of the world, or the worsening of the world economic situation in terms of inflation, energy costsprices and purchase power, is likely to translate into a lower propensity to spend on luxury good products and potentially impact our business.

Developments in Greater China and other growth and emerging markets may adversely affect our business.

We operate in a number of growth and emerging markets, both directly and through our distribution partners. In particular, a significant proportion of our sales are in the Greater China Region (which for Zegna’sour reporting purposes includes the Chinese mainland, Hong Kong S.A.R., Macau S.A.R. and Taiwan), representing 46%31%, 43%33% and 35%46% of our revenuerevenues in 2021, 20202023, 2022 and 2019,2021, respectively, where we have had a direct retail presence since 1991. While demand in these markets has increased in recent years due to sustained economic growth and growth in personal income and wealth, economic growth in these markets may not be sustained in the future. For example, rising geopolitical tensions and potential slowdown in the rate of growth there and in other emerging markets (such as the recent decline in investments in the real estate market in the Greater China Region) could cause a decline in our sales there, or limit the opportunity for us to increase sales of our products and revenues in those regions in the near term.

Economic and political developments in emerging markets, including economic crises, or political instability or geopolitical tensions, have had and could have in the future material adverse effects on our business, results of operations and financial condition. Government actions may also impact the market for luxury goods in these markets, such as tax changes, measures aiming at limiting the import of foreign goods or the active discouragement of luxury purchases. Consumer

spending habits in these markets may also change due to other factors that are outside of our control. For instance, starting from the end of August 2021, the President of the People’s Republic of China has repeatedly signaled the government’s intention to regulate excessively high incomes and encourage high-income groups and enterprises to return more to society. While noResulting regulatory action has been taken to date,or similar statements by governmental authorities may affect the social acceptability of spending on luxury goods.

Maintaining our position in these growth and emerging markets is a key component of our global strategy. However, initiatives from several global luxury goods manufacturers have increased competitive pressures for luxury goods in several emerging markets. As these markets continue to grow, we anticipate that additional competitors, both international and domestic, will seek to enter these markets and that existing market participants will try to aggressively protect or increase their sales. Increased competition may result in pricing pressure, reduced margins and our inability to increase or maintain our sales levels, which could have a material adverse effect on our results of operations and financial condition. See also “—Risk factors relating to the industry in which Zegnathe Group operates—The markets in which we operate are highly competitive.

Failure to implement our strategy could adversely affect our results of operations.

Our ability to increase our revenues, and pursue growth and development objectives and generate profits and cash flows depends, in part, upon our success in carrying out our strategic plan. As part of our strategy, we are pursuing, among other things, the further enhancement of the ZEGNA brand (including through our One Brand strategy), the successful consolidationintegration of the TOM FORD FASHION business and Thom Browne’s international expansion. See “Item 4.B—Business Overview—Strategy” for a description of our shift toward luxury leisurewear,strategy.

If our One Brand strategy proves unsuccessful, the successful designpositioning of the ZEGNA brand may suffer and introductionwe may have to undertake markdown activities, which could impact our prestige and reputation, as well as profitability. In addition, as a result of our ZEGNA brand strategy relating to iconic products, we could become significantly exposed to certain specific products and, should they lose their appeal, it may be difficult to replace the revenues generated therefrom.

Our initiatives to grow the direct to consumers channel through the opening of new iconic products,stores involve significant investments and the preservationselection of the exceptional qualityappropriate locations and personnel. If the execution of the stores roll-out plan is not successful we are known for andmay not realize the use of digital tools to strengthen our processes, attract new customers and retain our existing customer base, andreturn on investment or the growth and profitability that we anticipate.

Our initiatives to develop an increasingly sustainable business and leverage on our Made in Italy textiles and manufacturing platform involve significant investments and possible operational changes. If the implementation of such initiatives is not successful, or we do not realize the Thom Browne brand, which dependsreturn on the brand’s positive momentum and successful customer proposition. See “our investments in these initiatives that we anticipate, our results of operations could be adversely affected.

Item 4—Information on the Company—Strategy.”

Our strategy is premised upon certain assumptions about the global economy and the evolution of demand for luxury goods in various regions of the world in which we operate or seek to operate our competitive position and the ability of our management team to carry out our strategic plan. If we fail to implement our strategic plan, if our assumptions prove to be incorrect or if the geopolitical situation triggers an economic crisis or a conflict situation in the

European Union,regions where we operate, our ability to increase our revenues and profitability could be affected, which could have a material adverse effect on our business, results of operations and financial condition.

We are exposed to risks relating to recent and potential future acquisitions.

Our growth strategy may, from time to time, include acquisitions. Such acquisitions may cause us to face uncertainties concerning the economic and financial outcomes of such transactions. With respect to both past and future acquisitions (including the TFI Acquisition which closed on April 28, 2023), we may be exposed to liabilities (including tax liabilities) not detected during the due diligence process or not covered by contractual provisions. Furthermore, other assessments of the acquired business made at the time of the initial investment could prove to be incorrect. The achievement of the anticipated benefits of an acquisition is subject to a number of uncertainties, including general competitive factors in the marketplace, our ability to integrate the businesses in an efficient and effective manner and establish and implement effective operational principles and procedures. We may also encounter unexpected difficulties and costs if we are unable to retain certain key employees and achieve minimal unplanned attrition, which could increase our hiring and training costs and disrupt our business, or in connection with hiring new senior managers. The process of coordinating and integrating businesses acquired by the Group has required and will continue to require significant management and financial resources that may otherwise have been focused on the ordinary course management of our activities. The integration process also

requires the application of financial reporting and management control systems to the acquired companies, as well as the integration of IT systems, compliance and risk management policies (which may apply different standards, procedures and tools), and the training of new personnel. Each of these needs could require considerable resources from us, entailing significant costs. If we incur liabilities as a result of acquisitions and these liabilities exceed the contractual indemnification caps, or if indemnification is not available for any other reason, this could have a material adverse effect. Furthermore, we are exposed to the risk that the evaluations and assumptions underlying investment decisions could turn out to be incorrect, which could lead to unexpected difficulties in the process of integrating the acquired assets or companies with our business, or costs and other unforeseen liabilities for the Group, and we may not obtain the benefits and synergies expected from such transactions. Any of the above circumstances could have adverse effects on our business, results of operations and financial condition.

Acquisitions of new businesses may also expose us to other risks relating specifically to the business being acquired. For example, pursuant to the arrangements governing the TFI Acquisition (and subject to its closing), Mr. Tom Ford, Founder and CEO of Tom Ford International, served as the brand’s creative visionary until the end of 2023. His departure following many years at the helm of the TOM FORD brand could ultimately have a material adverse effect on the TOM FORD FASHION business, and therefore on our results of operations and financial condition.

We depend on our manufacturing and logistics facilities, which are subject to disruption.

We operate manufacturing and logistics facilities in Italy, Switzerland and Turkey and logistics facilities in the People’s Republic of China, Japan and the United States. These facilities are subject to operational risks, including mechanical and information technology system failure, work stoppage, civil unrest, increases in transportation costs, natural disasters, fire, government imposed shutdowns and disruption to supplies of raw materials.materials or of commodities such as energy. Any interruption of activity in our manufacturing or logistics facilities due to these or other similar events outside of our control could result in disruption to our operations and a reduction in sales, which could have an adverse effect on our business, results of operations and financial condition. See “—“—We are subject to risks related to theCOVID-19

pandemic or similar public health crises that may materially and adversely affect our business.” ” We are subject to certain risks related to the sale of our products through our DTC channel and in particular our directly operated stores.

In our distribution model, the DTC channel consists of single branded stores managed directly by us, or DOSs, outlets, concessions within department stores, as well as a directly managed online boutique and other

e-commerce

platforms through which we sell directly to our customers.

As ofAt December 31,

2021,2023, we operated

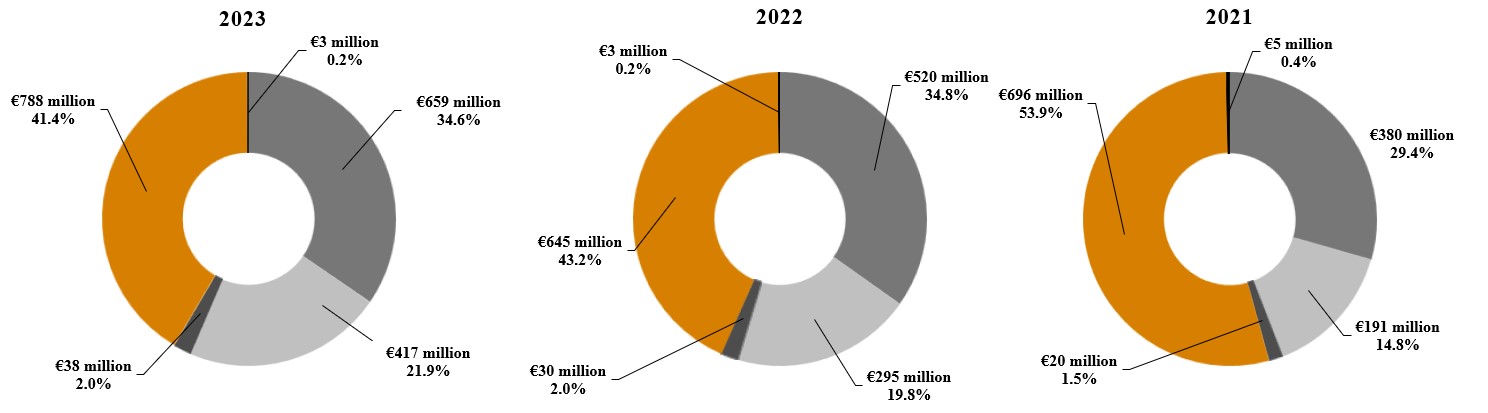

245 Zegna DOSs and 52253 ZEGNA, 86 Thom Browne

DOSs.and 51 TOM FORD FASHION DOSs (239 ZEGNA and 63 Thom Browne DOSs at December 31, 2022). The DTC channel generated revenues of

€851€1,265 million in

20212023 (or 66% of our consolidated revenues in such period). The risks related to managing currently existing DOSs mainly relate to possible difficulties in renewing the existing lease agreements, an increase in rental charges and a decline in sales.

Our DOSs are all located in properties that we lease from third parties. There is significant competition among retail operators in our industry to obtain commercial spaces in prestigious locations in major cities, towns and resort destinations worldwide. Accordingly, to renew our lease agreements, we may have to compete with other operators, including those in our same industry, some of which have greater economic and financial resources than ours or otherwise more bargaining power. If we are unable to renew our lease agreements with economic terms consistent or more beneficial than those currently applicable, or if we are forced to accept rental charges which are substantially higher than the existing ones, this could have a material adverse effect on our business, results of operations and financial condition.

Our DOSs have a high level of fixed costs, which affect profits from the retail channel. A reduction in sales or a decrease in revenues from the retail channel could, in light of the high level of fixed costs, have a material adverse effect on our business, results of operations and financial condition.

We analyze the performance of each of our DOSs and market trends in order to assess whether to open new DOSs (or move DOSs to a different location), renew existing leases, or close DOSs that are underperforming. If our analysis is inadequate or based on the wrong assumptions, we could select

sub-optimal

locations for our stores, or keep or open underperforming stores, which could have a material adverse effect on our business, results of operations and financial condition. In the event we decide to close an underperforming DOS, the terms of the lease may not allow us to terminate the lease without significant penalties (such as payment of rent until the expiry of the contractual term).

In addition, although we have adopted internal policies and training initiatives to ensure that the staff in our DOSs operate in a manner consistent with the image and prestige of our brands, there can be no assurance that such staff will abide by such policies or that inappropriate or illicit behavior by certain employees will not occur. If there is any allegation brought against us as a result of negligence or other impermissible conduct by our DOS staff, we may be exposed to legal or other proceedings or increased public scrutiny, which may result in substantial costs, diversion of resources and management’s attention and potential harm to our reputation.

The operations of our retail channel and DOSs are also subject to risks such as information technology system failure, work stoppage, wars, conflicts, civil unrest, natural disasters, fire and government imposed shutdowns. Any interruption of activity in our retail channel and DOSs due to these or other similar events out of our control could result in disruption to our operations and a reduction in sales, which could have an adverse effect on our business, results of operations and financial condition.

In the wholesale channel, we are subject to certain risks arising from points of sale operated by third parties, and we are dependent on our local partners to sell our products in certain markets.

In the wholesale channel, we sell our products to franchisees, specialty stores, department stores and online retailers. InFor the year ended December 31, 2021,2023, revenues attributable to the wholesale channel for the Zegna Branded Products andZEGNA branded products, Thom Browne and TOM FORD FASHION (after the closing of the TFI Acquisition) amounted to €259€458.4 million (or 20%24% of our consolidated revenues in the same period).The termination or loss of existing commercial relationships with our primary wholesale customers, the failure to develop new commercial relationships on economically favorable terms (or at all) or a significant decrease in wholesale channel revenues could have a material adverse effect on our business, results of operation and financial condition. In addition, any failure by retail storesretailers not directly operated by us to manage their stores, or by our local partners to act, in a manner consistent with the image and prestige of our brands or in line with any agreed contractual commitments (including in terms of sale prices), or failure by online retailers to comply with consumer protection laws or provide accurate product descriptions, could damage the competitive position and image of our brand, with potential material adverse effects on our business, results of operations and financial condition. See “—“—Our business depends on the recognition, integrity and reputation of our brands.brands.”

In certain of the geographic markets in which we operate, the distribution of our products is carried out, sometimes exclusively, through franchising agreements with local operators. Although we generally have not experienced significant problems in the past with such wholesale customers, the loss of one or more important commercial relationships with, or the occurrence of material disagreements with, our distribution partners or a failure to renew or develop commercial relationships on economically favorable terms (or at all) with them could have a material adverse effect on our business, results of operations and financial condition.

Our operations are also subject to the risk of insolvency of our wholesale customers. Despite our efforts to mitigate such risk, there can be no assurance that we will be able to do so successfully, and our business, results of operations and financial condition could be materially adversely affected.

Fluctuations in the price or quality of, or disruptions in the availability of, raw materials used in our products could cause us to incur increased costs, disrupt our manufacturing processes or prevent or delay us from meeting our customers’ demands.

We require high quality raw materials in order to produce our products. The market price of the raw materials that we require for our production depends on many factors that are largely out of our control and which are difficult to predict. The primary raw materials we use are fibers and yarns (in particular,of wool, yarns), silk, cotton, linen, cashmere and fabrics andof the same composition, as well as leather. The availability of wool and silk depends on unpredictable factors which are outside our control, including weather conditions in the areas where these raw materials originate (mainly Australia and New Zealand for wool, Greater China and Mongolia for cashmere, Turkey and Egypt for cotton, Europe and the Caribbean for linen and Greater China for silk), as well as diseases and pests affecting livestock.livestock and plants and, as a result, fiber quality. We also use rare raw materials, such as vicuna yarns and fabrics and specially selected calf leather, which are only available in a very limited quantity and subject to strict export and processing regulations, which may change. Possible legislative, political and economic developments, potential social instability or the introduction of export restrictions or tariffs in the countries in which our suppliers operate, or the introduction of import restrictions on products from such countries, could have a negative impact on our procurement activities. These and other factors could affect the availability and price of the raw materials required for our production. For instance, the price of cashmere raised significantly through 2021.

fiber prices continued to grow as a result of various factors, including droughts that reduced the available quantity high quality flax. The price of other raw materials was also recently affected by the global high inflationary environment.

If the supply of such raw materials decreases (including due to shortages or to a decrease in the number of producers or suppliers of raw materials), we may face difficulties in obtaining sufficient supplies of high quality raw materials, and the relevant prices may increase. Thus, we could face supply shortages in the medium term and rising costs of purchasing, which we may be unable to pass on to our customers. In addition, our suppliers could cancel or delay the delivery of raw materials to us, or may fail to provide raw materials that meet our high quality standards.standards or may fail to comply with our increasingly stringent sustainability and traceability requirements. This could delay our manufacturing process or cause us to incur increased costs to obtain raw materials of the quality we require. Any of the foregoing factors could have a material adverse effect on our business, results of operations or financial condition. Suppliers’ actions may also damage our reputation. See “—Our business depends on the recognition, integrity and reputation of our brands”.

We could be adversely affected if we are unable to negotiate, maintain or renew our license or co-branding agreements with high end third party brands.

We are a party to various agreements with third party brands, as licensee or supplier, and license agreements, as licensor.

In particular, we have been acting as licenseeaccordance with the definitive agreements for the productionacquisition of TFI, which closed on April 28, 2023, TFI entered into a license agreement, pursuant to which TFI is the licensee of The Estée Lauder Companies for all TOM FORD men’s and distributionwomen’s fashion as well as accessories and underwear, fine jewelry, childrenswear, textile and home design products, for a term of Tom Ford menswear since 200820 years, subject to renewal at TFI’s option for one further 10-year period subject to certain minimum performance conditions (the “TFF License”). Under the TFF License, we are required to pay royalties to the licensor. If we are unable to run the licensed business efficiently (considering the royalties and upon expiryother costs), our profitability may be adversely affected. In addition, the TFF License provides for certain minimum guaranteed royalties payable to The Estée Lauder Companies regardless of the existing license following the completionlevel of the production and distribution activities for the Fall/Winter 2022 collection, we willsales actually achieved.

We act as an exclusive supplier for certain Tom Ford products starting from the Spring/Summer 2023 season. We are also supplier of menswear for several brands such as Dunhill and for Gucci.During the year ended December 31, 2021,2023, we recorded revenues of €75€25.3 million from these agreements with third party brands (after eliminations). See “Item 4—Information on the Company—Brands, Collections and Products—4.B—Business Overview—Zegna Segment—segment—Third Party Brands Product Line

or amend in a manner adverse to us the existing arrangements, or initiate legal proceedings against the Group, which may have material adverse consequences on our business, results of operations and financial condition. We are also party to certain license agreements whereby we grant, for a certain period of time, the use of our brand to third parties for the production of products in adjacent luxury sectors (including fragrances, glasses and sunglasses, cufflinks, and beachwear and underwear). For the year ended December 31, 2021,2023, royalties relating to these arrangements were €4.5€3.0 million. If any of these licensees were not to perform their obligations towards Zegnathe Group (including by failing to ensure the required quality, sustainability or traceability standards, complynot complying with our directions with respect to distribution channels and after sale services)services, breaching obligations related to our intellectual property rights, or failing to comply with the timeline for product launches), we may be unable, in a commercially reasonable time, to replace such licensee with another producer capable of ensuring equivalent quality and production standards, or procure its services upon the same or substantially the same financial terms. Our inability to maintain a presence in these adjacent luxury sectors or to provide products in these sectors of a quality comparable to that of our other products may reflect negatively on the reputation and integrity of our brands.

We are also pursuing the negotiationsFrom time to time, we enter into co-branding projects with different brands

to enter intoco-branding

projects for the design, production and

marketingsale of certain selected

co-branded

products, as we did

in the past with

Maserati, Leica CameraThe Elder Statesman. We also enter into collaborations with other brands to offer new products lines (as we did with Norda and

Fear of God.Baccarat). If we fail to

conclude the negotiationsnegotiate, enter into or renew such relationships in a mutually satisfactory manner for both brands, in particular with respect to the distribution of the

co-branded

products and the ownership and protection of the intellectual property rights related to these projects, we may be unable to replace the revenues generated in the past from these collaborations.

If any of the foregoing licensing agreements or

agreements orco-branding

projects with third party brands are terminated for any reason, not renewed upon their expiration or renewed but with less favorable terms and conditions, this could have a material adverse effect on our business, results of operations and financial condition.

Our business depends on tourist traffic and demand.

A substantial amount of our sales is generated by customers who purchase products while travelling. Consequently, adverse economic conditions (such as financial crises), global political developments, other social and geopolitical sources of unrest,tensions, instability, disorders, riots, civil wars or military conflicts, natural disasters such as fire, floods, blizzards, global pandemics such as theCOVID-19

pandemic and earthquakes or other events, as well as travel restrictions imposed by governments, which result in a shift in travel patterns or a decline in travel volumes, have had in the past, and may have in the future, an adverse effect on our business, results of operations and financial condition. See also “—“—We are subject to risks related to theCOVID-19

pandemic or similar public health crises that may materially and adversely affect our business. , “—Global economic conditions and macro events may adversely affect us.

The conflict in Ukraine and sanctions imposed onto Russia may adversely affect our business.business.”

”

Our business success depends on certain key personnel.senior personnel as well as skilled personnel, and their loss or unavailability could adversely affect our business.

The performance of our business depends significantly on the efforts and abilities of some key senior personnel, including, without being limited tolimitation, our Chairperson and Chief Executive Officer, Mr. Ermenegildo (Gildo) Zegna. Such key personnel have substantial experience and expertise in the luxury goods business and have made significant contributions to the success of our business.

If suchAlthough we have a succession planning process in place for certain key roles, if any key personnel were to leave us abruptly, or become otherwise unable or unwilling to continue in their roles, we may not be able to replace them in a timely fashion.fashion or with individuals of equivalent experience and capabilities. The failure to retain or replace such key personnel with other skilled personnel capable of integrating into our operations efficiently could lead to delays in the development of collections, inefficiencies in management of our business, and, accordingly, could have a material adverse effect on our business, results of operations and financial condition.

In addition, our future success depends on our ability to continue to attract, retain and motivate skilled employees. Competition for employees is becoming more intense. The ability to attract, hire and retain skilled personnel depends on our ability to provide meaningful work at competitive compensation. The inability to do so effectively would constrain our ability to timely complete certain projects, which could adversely affect our business, results of operations and financial condition.

We depend on highly specialized craftsmanship and skills.