| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Title of each class | Name of each exchange on which registered | |

American Depositary Shares, each representing the right to receive three ordinary shares, par value Ps.1.00 per share | New York Stock Exchange | |

Ordinary shares, par value Ps.1.00 per share | New York Stock Exchange* |

* | The ordinary shares are not listed for trading,but are listed only in connection with the registration of the American Depositary Shares, pursuant to requirements of the New York Stock Exchange. |

Title of class | Number of shares outstanding | |

Ordinary Shares, par value Ps.1.00 per share | 612,710,079 |

| Large accelerated filer | ☐ | Accelerated filer | ☒ | |||

| Non-accelerated filer | ☐ | Emerging growth company | ☐ | |||

| U.S. GAAP | ☐ | International Financial Reporting | ☒ | Other | ☐ |

Auditor firm ID: | 1449 | Auditor name: | Pistrelli, Henry Martin y Asociados S.R.L. | Auditor location: | Argentina | |||||

Auditor firm ID: | 1410 | Auditor name: | KPMG | Auditor location: | Argentina |

TABLE OF CONTENTS

| Page | |||||||||

| 1 | |||||||||

| 3 | |||||||||

| PART I | |||||||||

| 4 | |||||||||

| 4 | |||||||||

| 4 | |||||||||

| PART II | |||||||||

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | |||||||||

PURCHASES OF EQUITY SECURITIES BY | |||||||||

DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS | |||||||||

| 188 | |||||||||

| 189 | |||||||||

| PART III | |||||||||

FORWARD-LOOKING STATEMENTS

This Form 20-F contains words, such as “believe”, “expect”, “estimate”, “intend”, “plan”, “may” and “anticipate” and similar expressions that identify forward-looking statements, which reflect our views about future events and financial performance. Actual results could differ materially as a result of factors beyond our control, including but not limited to:

changes in general economic, business or political or other conditions in the Republic of Argentina (“Argentina” or “the Republic”) or changes in general economic or business conditions in Latin America;worldwide;

angovernmental intervention and regulation (including banking and tax regulations);

developments in the global financial markets;

deterioration in the Argentine financial system or regional business and economic conditions;

inflation;

the outbreak and spread of a new pandemic or the worsening of the ongoing Covid-19 pandemic;and other large-scale public health events;

changes in exchange rates or capital markets in general that may affect policies towards or lending to Argentina or Argentine companies;

increased costschanges in interest rates which may adversely affect our margins;

adverse legal or regulatory disputes or proceedings;

credit and decreased income related to macroeconomic variablesother risks of lending, such as exchange ratesincreases in defaults by borrowers and other delinquencies;

increase in the provisions for loan losses;

fluctuations and declines in the value of Argentine public debt;

decreases in deposits or in the number of our customers;

competition in the banking, financial services and related industries and the Consumer Price Index (“CPI”) in Argentina;loss of market share;

unanticipated increases in financing and other costs or the inability to obtain additional debt, equity or wholesale financing on attractive terms or at all; and

| • | the factors discussed under “Item 3. Key Information—D. Risk Factors”. |

Accordingly, readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Banco BBVA Argentina S.A. (“BBVA Argentina” or the “Bank”) undertakes no obligation to update or revise these forward-looking statements or to publicly release the results of any revisions to these forward-looking statements. The accompanying information in this annual report, including, without limitation, the information under “Item 4. Information on the Company”, “Item 5. Operating and Financial Review and Prospects” and “Item 11. Quantitative and Qualitative Disclosures About Market Risk” identifies important factors that could cause material differences between any forward-looking statements and actual results.

1

PRESENTATION OF FINANCIAL INFORMATION

General

The Bank’s audited consolidated financial statements as of December 31, 20222023 and 20212022 and for the years ended December 31, 2023, 2022 2021 and 20202021 included herein (the “Consolidated Financial Statements”) are prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS-IASB”).

All 2023, 2022 2021 and 20202021 data included in this report have been prepared in accordance with IFRS-IASB for the sole purpose of filing this annual report on Form 20-F with the U.S. Securities and Exchange Commission (“SEC”).

The statutory consolidated annual financial statements that the Bank prepares to comply with the requirements of the Argentine Central Bank (the “Central Bank” or “BCRA”) are prepared pursuant to the reporting framework established by the Central Bank requiring supervised entities to submit financial statements prepared pursuant to IFRS-IASB except for:

| (i) | the application of the expected credit loss model set forth under paragraph 5.5. of IFRS 9 for debt instruments issued by the public sector; |

| (ii) | for 2021, |

1

| (iii) | the treatment to be applied to uncertain tax positions, which follows the guidance prescribed by Memorandum No. 6/2017 Financial Reporting Framework Established by the BCRA issued on May 29, 2017. As of December 31, 2021, such provision had been reversed in the statutory consolidated financial statements. |

Because of such differences, our statutory consolidated annual financial statements for the fiscal years ended December 31, 2023, 2022 2021 and 20202021 are not comparable with the Consolidated Financial Statements included herein. In addition, we will continue to have differences during 20232024 between our statutory consolidated financial statements and the financial statements required by IFRS-IASB. We do not intend to report in accordance with IFRS-IASB on an interim basis during 2023.2024. Consequently, our interim financial information for 20232024 will not be comparable with the Consolidated Financial Statements and other information contained in this annual report on Form 20-F. We refer in this annual report on Form 20-F to IFRS-IASB as adjusted by the regulations of the BCRA as “IFRS-BCRA”.

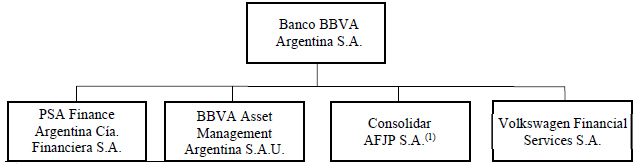

The Consolidated Financial Statements consolidate all the subsidiaries of the Bank in which the Bank holds direct or indirect control. See “Item 4. Information on the Company—C. Organizational Structure” for an organizational chart of BBVA Argentina and its subsidiaries.

In this annual report, references to “$”, “US$”, “U.S. dollars”, “US dollars” and “dollars” are to United States dollars and references to “Ps.”, “Pesos” and “pesos” are to Argentine pesos. Percentages and certain dollar and peso amounts have been rounded for ease of presentation. Unless otherwise stated, all market share and other industry information has been derived from information published by the Central Bank.

Unless otherwise indicated, financial information contained in this annual report reflects the consolidation of the following subsidiaries at the year end and for the fiscal years indicated below:

| As of and for the year ended December 31, | As of and for the year ended December 31, | |||||||||||

Entity | 2022 | 2021 | 2020 | 2023 | 2022 | 2021 | ||||||

Volkswagen Financial Services Compañía Financiera S.A. | X | X | X | X | X | X | ||||||

Consolidar AFJP S.A. (undergoing liquidation proceedings) | X | X | X | X | X | X | ||||||

BBVA Asset Management Argentina S.A.U. | X | X | X | X | X | X | ||||||

PSA Finance Argentina Compañía Financiera S.A. | X | X | X | X | X | X | ||||||

2

IAS 29 Financial Reporting in Hyperinflationary Economies requires that an entity whose functional currency is the currency of a hyperinflationary economy must state its assets, liabilities, income and expenses in terms of the measuring unit current at the end of the reporting period (December 31, 2022)2023). The Bank has applied IAS 29 as follows for purposes of the Consolidated Financial Statements:

Restated the consolidated statement of profit or loss, the consolidated statement of comprehensive income, the consolidated statement of changes in equity and consolidated statements of cash flow for the years ended December 31, 20212022 and 2020.2021.

Restated the consolidated statement of financial position as of December 31, 2021.2022.

Adjusted the consolidated statement of financial position as of December 31, 2022.2023.

Adjusted the consolidated statement of profit or loss, the consolidated statement of comprehensive income, the consolidated statement of changes in equity and consolidated statements of cash flow for the year ended December 31, 2022,2023, including the calculation and separate disclosure of the gain or loss on the net monetary position.

For further information regarding the methodology and criteria applied see Note 2.1.5 to the Consolidated Financial Statements.

See “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Exchange Rates” for information regarding the evolution of rates of exchange since 2018.2019.

All figures and percentages of variations in this annual report on Form 20-F, unless otherwise stated, are presented in the measuring unit current at December 31, 2022.2023. All comparisons of the financial system contained in this annual report on Form 20-F are presented in nominal terms.

2

CERTAIN TERMS AND CONVENTIONS

The terms below are used as follows throughout this report:

“BBVA Argentina”, the “Bank” or the “Company” and terms such as “we”, “us” and “our” mean Banco BBVA Argentina S.A. and its consolidated subsidiaries unless otherwise indicated or the context otherwise requires.

“BBVA” or the “BBVA Group” means Banco Bilbao Vizcaya Argentaria, S.A. and its consolidated subsidiaries unless otherwise indicated or the context otherwise requires.

“Consolidated Financial Statements” means our audited consolidated financial statements as of December 31, 2022 and 2021 and for the years ended December 31, 2022, 2021 and 2020, prepared in accordance with IFRS-IASB and included in this annual report on Form 20-F.

| • | “Consolidated Financial Statements” means our audited consolidated financial statements as of December 31, 2023 and 2022 and for the years ended December 31, 2023, 2022 and 2021, prepared in accordance with IFRS-IASB and included in this annual report on Form 20-F. |

3

- PART I -

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

| A. | Selected Financial Data |

Reserved.

| B. | Capitalization and indebtedness |

Not applicable.

| C. | Reasons for the offer and use of proceeds |

Not applicable.

| D. | Risk Factors |

The following summarizes some, but not all, of the risks provided below. Please carefully consider all of the information discussed in this Item 3.D. “Risk Factors” in this annual report for a more thorough description of these and other risks:

Risks Relating to Argentina

economic and political instability in Argentina;

current levels of inflation;

high levels of public spending;

the effects on the Argentine economy of economic events in other markets;

a decline in international prices for Argentina’s principal commodity exports;

exchange controls and restrictions on capital inflows and outflows;

the insufficiency of the measures adopted to resolve the crisis in the energy sector;

any failure to adequately address actual and perceived risks of institutional deterioration and corruption;

fluctuations in the value of the peso;

the inability of the Republic to obtain financing on satisfactory terms;

salary increases or additional employments benefits as a result of government measures or pressure from union sectors;

government intervention in the Argentine economy;

amendments to the Central Bank’s Charter and the Convertibility Law;

an outbreak of a new pandemic or the worsening of the ongoing Covid-19 pandemic; and

exposure to risks in connection with climate change.

Risks Relating to the Argentine Financial System and to BBVA Argentina

the short-term structure of the deposit base of the Argentine financial system, including the deposit base of the Bank, could lead to a reduction in liquidity levels and limit the long-term expansion of financial intermediation;

reduced spreads between interest rates received on loans and those paid on deposits;

volatility in interest rates;

a mismatch between UVA (“Unidad de Valor Adquisitivo”, in Spanish) loans and UVA deposits;

4

the inaccuracy and/or insufficiency of our estimates and established reserves for credit risk and potential credit losses;

increased competition in the banking industry;

activities across the BBVA Group could adversely affect us;

the dependency of our credit ratings on Argentine sovereign credit ratings;

the increasing dependency of the financial industry on information technology systems;

security risks;

an increase in fraud or transaction errors;

any insolvency proceeding against us that could subject us to the powers of, and intervention by, the Central Bank;

lawsuits brought against us outside Argentina;

class actions against financial institutions for an indeterminate amount;

the ability of BBVA, our controlling shareholder, to direct our business;

our ability to grow our business is dependent on our ability to manage our relationships with partners and grow our deposit base;

acquisitions that could adversely affect the value of the Bank;

any adverse consequences related to our calculation of income tax for the years ended December 31, 2018 and 2020;

the application of IAS 29 to our Consolidated Financial Statements; and

restrictions on our ability to pay dividends.

Legal, Regulatory and Compliance Risks

material weaknesses in our internal control over financial reporting;

our operations are conducted in a highly regulated environment;

the instability of the regulatory framework, in particular the regulatory framework affecting financial institutions;

our exposure to multiple provincial and municipal legislation and regulations;

limitations arising from the Consumer Protection Law and the Credit Card Law;

compliance risks;

differences between U.S. and Argentine corporate disclosure, governance and accounting standards; and

special rules that govern the priority of different stakeholders of financial institutions in Argentina.

Risks Relating to Argentina

economic and political instability in Argentina;

current levels of inflation;

high levels of public spending;

the Argentine economy could be adversely affected by economic events in other markets;

a decline in international prices for or in the amount of Argentina’s principal commodity exports;

exchange controls and restrictions on capital inflows and outflows;

the insufficiency of the measures adopted to resolve the crisis in the energy sector;

any failure to adequately address actual and perceived risks of institutional deterioration and corruption;

fluctuations in the value of the peso;

the inability of the Republic to obtain financing on satisfactory terms;

salary increases or additional employments benefits as a result of government measures or pressure from union sectors;

government intervention in the Argentine economy;

amendments to the Central Bank’s Charter and the Convertibility Law; and

the outbreak and spread of a pandemic and other large-scale public health events.

Risks Relating to the Argentine Financial System and to BBVA Argentina

the short-term structure of the deposit base of the Argentine financial system, including the deposit base of the Bank, could lead to a reduction in liquidity levels and limit the long-term expansion of financial intermediation;

reduced spreads between interest rates received on loans and those paid on deposits;

volatility in interest rates;

a mismatch between UVA (“Unidad de Valor Adquisitivo”, in Spanish) loans and UVA deposits;

4

the inaccuracy and/or insufficiency of our estimates and established reserves for credit risk and potential credit losses;

exposure to public sector debt;

increased competition in the banking industry;

activities across the BBVA Group could adversely affect us;

the dependency of our credit ratings on Argentine sovereign credit ratings;

the increasing dependency of the financial industry on information technology systems;

security risks;

an increase in fraud or transaction errors;

any insolvency proceeding against us that could subject us to the powers of, and intervention by, the Central Bank;

lawsuits brought against us outside Argentina;

class actions against financial institutions for an indeterminate amount;

the ability of BBVA, our controlling shareholder, to direct our business;

our ability to grow our business is dependent on our ability to manage our relationships with partners and grow our deposit base;

acquisitions that could adversely affect the value of the Bank;

any adverse consequences related to our calculation of income tax for the years ended December 31, 2018 and 2020;

the application of IAS 29 to our Consolidated Financial Statements;

restrictions on our ability to pay dividends; and

exposure to risks in connection with climate change.

Legal, Regulatory and Compliance Risks

material weaknesses in our internal control over financial reporting;

our operations are conducted in a highly regulated environment;

the instability of the regulatory framework, in particular the regulatory framework affecting financial institutions;

our exposure to multiple provincial and municipal legislation and regulations;

limitations arising from the Consumer Protection Law and the Credit Card Law;

compliance risks;

differences between U.S. and Argentine corporate disclosure, governance and accounting standards; and

special rules that govern the priority of different stakeholders of financial institutions in Argentina.

Risks Relating to Argentina

Overview

We are an Argentine corporation (sociedad anónima)public limited company), and the vast majority of our operations, properties and customers are located in Argentina. Accordingly, the quality of our assets, our financial condition and our results of operations are significantly affected by macroeconomic and political conditions prevailing in Argentina.

Economic and political instability in Argentina may adversely and materially affect our business, results of operations and financial condition.

The Argentine economy has experienced significant volatility in recent decades, characterized by periods of low or negative growth, high levels of inflation and currency devaluation. As a consequence, our business and operations have been, and could in the future be, affected from time to time to varying degrees by economic and political developments and other material events affecting the Argentine economy, such as inflation, price controls, foreign exchange controls, fluctuations in foreign currency exchange rates and interest rates, governmental policies regarding spending and investment, national, provincial or municipal tax increases and other initiatives increasing government involvement in business activities, and civil unrest and local security concerns.

InBetween 2001 and 2002,2015, the Argentine economy suffered awas very volatile combining periods of severe economic and political crisis. Among other consequences,crisis resulting, among others, in restrictions on deposit withdrawals and the crisis resulted in Argentina defaulting on its foreign debt obligations and introducing emergency measures and several changes in economic policies that affected utilities, financial institutions and many other sectors“pesification” of the economy. Argentina also suffered a significant real devaluation of thedeposits (which were reclassified as peso which in turn caused numerous Argentine private sector debtors with foreign currency

5

exposure to default on their outstanding debt. Restrictions on deposit withdrawals from the banking system were implemented, as dollar denominated loans and deposits were “pesified” (reclassified as peso denominated) and maturities reprogrammed. Following that crisis, Argentina substantially recovered its real gross domestic product (“GDP”), which grew by 8.9% in 2005, 8.0% in 2006, 9.0% in 2007 and 4.1% in 2008.with certain periods of recovery. In 2009, an extended drought, which reduced agricultural production, and the effects of the global economic crisis led to a 5.9% GDP contraction. GDP growth was strong in 2010 and 2011, increasing to 10.1% and 6.0%, respectively. However, the economy has not been able to attain sustained GDP growth since then, as the country has experienced several adverse economic cycles, currency crises and the impact of Covid-19. As a consequence, in 2020 real GDP was 12% below the 2011 level.

The economic and financial environment in Argentina was significantly influenced by the presidential elections held on November 22, 2015, which resulted in Mr. Mauricio Macri beingwas elected President of Argentina. Mr. Macri’sArgentina and his administration (the “Macri administration”) assumed office on December 10, 2015 and launched a wide array of measures intended to correct the longstanding fiscal and monetary policies that had resulted in recurrent public sector deficits,deficit, high inflation, pervasive foreign exchange controls and limited foreign investment. In 2016,

However, in 2018, the eliminationworsening of foreign exchange restrictionseconomic and rebalancing of utility rates led to an increasepolitic conditions worldwide and in inflation of 41% year-on-year according to the City of Buenos Aires index at year end and to a considerable declineArgentina particularly, resulted in consumption. As a result, GDP fell by 1.8% in 2016. Once the main imbalances were eliminated, the economy picked up again in 2017, with GDP growing 2.9% and inflation slowing to 24.8% year-on-year, though higher than the goal defined by the Central Bank.

The Macri administration carried out a gradual approach intended to reduce the significant fiscal and current account deficit and to correct the macroeconomic imbalances received from the previous administration. This gradual approach ended abruptly in the second quarter of 2018 due to a combination of domestic impacts (mainly a severe drought), a deterioration of the global financial environment (including an increase in US interest rates and the US-China trade war) coupled with policy errors (including a change to BCRA inflation targets and a capital gains tax), which brought about significant capital outflows from Argentina, and the closing of global credit markets for Argentine issuers. From April 30 to July 31, 2018,issuers and a strong devaluation of the Argentine peso (based on the reference exchange rate of the Central Bank) depreciated 32.1% despite frequent exchange market interventions. Even after a strong adjustment of monetary policy and assistance from the International Monetary Fund (“IMF”) in the form of a stand-by high-access agreement of US$50 billion signed in mid-June 2018, tensions in the foreign exchange market reemerged in August, with the peso devaluating by 35.8% during that month in a strong sell-off of Argentine assets. Between April and September 2018, nearly US$14 billion of international reserves were lost due to sales of U.S. dollars by the Central Bank in the foreign exchange market.

Monetary policy was highly influenced by the IMF plan, and bypeso. By the end of September 2018, a new monetary and foreign exchange scheme, highly influenced by the International Monetary Fund (“IMF”), was announced. This scheme was adoptedannounced and while economic conditions stabilized, in order to control exchange rate volatility by absorbing all excess liquidity in pesos, holding the nominal monetary base constant until December 2018. It also set wide bands within which the foreign exchange rate could float. It allowed currency to be stabilized until February 2019. The peso appreciated 5% between September 30, 2018 and February 28,October 2019, (from Ps.40.89/US$ to Ps.39.00/US$) and interest rates of Central Bank Liquidity Bills (Leliq) fell in that period more than 2,900 basis points from the peak. By the end of April 2019, the Central Bank changed its exchange rate scheme by eliminating intervention bands, which became exchange reference bands since intervention of the Central Bank in the exchange market was allowed at any level of the exchange rate of the peso, which led to the stability of the peso until the primary elections of August 11, 2019 (on August 9, 2019 the exchange rate closed at Ps.45.40/US$, 1.6% above the value as of April 29, 2019). However, the unexpected loss by a 15 points gap of President Macri lost the elections to Alberto Fernández in those elections caused the exchange market to react negatively, and the reference exchange rate rose 10.3 pesos on Monday, August 12, 2019, a 22.8% increase over the value recorded the prior Friday, and finished 2019 at Ps.59.89/US$ with high volatility. On August 28, 2019, Argentina announced a new schedule of payment on its short term local debt, including instruments like Lecap, Letes, Lecer and Lelink, where original dates of payment were postponed between three and six months.

During 2019, the IMF advanced disbursements planned to be made in 2020 and 2021 within the framework of a revised agreement that required an additional fiscal adjustment in 2019, including reaching the goal of a primary deficit of 0% of GDP, the strengthening of Central Bank reserves with the support of official creditors and the continuity of orthodox monetary and fiscal policies. This was part of a new program established in October 2018.

In October 2019, Alberto Fernández was elected president of Argentina and took office on December 10, 2019. Since then, his governmentFernandez, whose administration (the “Fernandez administration”) hastook office in December 2019. The Fernandez administration implemented a wide range of economic and political reforms, including limiting access to the exchange market for individuals (seeking to contain the exchange rate without losing reserves) and the adoption of Law No. 27,541 on Social Solidarity and Productive Reactivation (the “Solidarity Law”), which covers a wide range of political and economic areas and adopts measures that have had, and continue to have, a significant impact on the Argentine

6

economy, including the declaration of a public emergency in economic, financial, fiscal, administrative, pensions, utility rates and energy issues, as well as health and social services. The Solidarity Law also increased taxes, while providing incentives for production and benefits for the poorest and most vulnerable sectors. Moreover, the Solidarity Law also set up the “Tax for an Inclusive and Solidary Argentina” (the “PAIS Tax”) which will be in force for a five-year period since its enactment, which applies a 30% rate on banknotes purchases in foreign currency for hoarding purposes, the acquisition of foreign services, and cross-border transportation services.

The Fernández administration has also undertaken a sovereign debt restructuring designed to make Argentina’s debt sustainable including through the reschedulement of maturities of sovereign securities, some ofpursuant to which were held by the Bank. As of December 31, 2020, sovereign debt securities affected by these measures and held by the Bank represented 2.67% of the Bank’s total assets. Pursuant to such debt restructuring, investors agreed to exchange their defaulted bonds by new bonds. The “Net Present Value” paid for such securities was around US$53.5 for every US$100 of nominal value, discounted at an exit yield of 10% for those securities issued during 2015-2019bonds, and around US$59.5 for those previously issued in 2005 and 2010. Additionally, the Fernandez administration has also undertaken a restructuring of domestic debt.

Moreover, the Covid-19 crisis hasThe Argentine economy was adversely affected by the Argentine economy. The Metropolitan Area of Buenos Aires was under PreventiveCovid-19 pandemic and Mandatory Social Isolation (“PMSA”) from March 20, 2020 to November 8, 2020. Meanwhile, the rest of the country was subject to social distancing. These measures significantly affected the population’s ability to function normally, primarily labor intensive sectors, which significantly adversely affected the country’s economic performance in 2020. In this regard, GDP fell 9.9% in 2020 compared to 2019. However, this critical situation was partially reversedrecovered in 2021, as a result of eased mobility restrictions and a consequent increase in economic activity since the beginning of 2021 due to increased vaccination levels. See “An outbreak of a new pandemic or the worsening of the ongoing Covid-19 pandemic may have material adverse consequences on the Argentine economy.”

activity. In 2021, Argentina held mid-term elections, testing the Fernández Administration, which received only 33.5% of the votes (compared to 48% in the elections held in 2019), while the main opposition coalition obtained 41.9% of the votes.

Thereafter, the government presented to Congress a bill for a new agreement with the IMF which wouldto replace the Stand-Bystand-by agreement (“SBA”) signed in 2018. The bill was approved in March 2022 despite the lack of endorsement by the Kirchnerist wing of the ruling coalition. The newThis program is an Extended Fund Facility (“EFF”), for a ten-year term, (with a grace period of 4 and a half years), and it does not require any structural reforms. Compliance with the EFF is reviewed on a quarterly basis and compliance of the economic targets is necessary to cover the maturities of the SBA. The EFF contains the minimum requirements for fiscal convergence, reserve accumulation and reduction of monetary issuance for a path towards fiscal balance in 2025, an accumulation of USD US$15 billion of net international reserves in the next three years, and a reduction of the Treasury’s monetary financing to zero in 2024. Any failure to meet such targets could result in the termination of the EFF program, which could bring political, financial and exchange rate instability due to the government’s inability to access external financing. The EFF program may be subject to adjustments, mainly in terms of disbursements and structural reforms, but it is expected to remain in effect.

In 2022 political and economic instability has beenwas high, including with regards to the economic cabinet, which had three Ministers of Economy during the year. In July, following a month of very high economic and financial tensions, the Minister of Economy Martín Guzmán unexpectedly resigned being replaced by Silvina Batakis. She was appointed without the support of the entire ruling coalition, and in the midst of a failed attempt to calm financial tensions, she was replaced by Sergio Massa (a lawyer by profession and one of the main partners of the ruling coalition) only 24 days after taking office. His appointment brought calm to the markets, and sincesoon after his arrival he has implemented a slow but consistent reduction of the fiscal deficit, focused on the revision of subsidies to public services tariffs, and an accumulation of international reserves centered on a multiple exchange rate scheme, with benefits forbenefitting soybean exporters.

Finally, direct transfers from the Central Bank to the Treasury, which was one of the promises madeas promised by Minister Massa upon taking office, have ceased so far. The lack of fiscal-monetary consistency in the short term could demand a strong monetary issuance by the BCRA, which could increase inflation and have a negative impact on investment.ceased.

7

In addition to the instability caused by the successive changes in the Ministry of Economy, Vice-President Cristina Kirchner was the victim of an assasinationassassination attempt in Buenos Aires. Although Argentina had not experienced similar events in the last decades, violent political events may occur and have adverse effects on the political and social stability.

Massa’s management as Minister of Economy was based on three pillars: (i) avoiding an abrupt devaluation of the official exchange rate, for which a multiple exchange rate scheme was generated that allowed exporters to settle at a higher differential exchange rate, or partially access the parallel exchange rate, which is always higher than the official exchange rate. This task became especially difficult in the context of the severe drought suffered for the last three years which adversely affected the agricultural sector, resulting in an estimated reduction in dollar inflows of approximately US$20 billion in 2023; (ii) the containment and reduction of inflation, by implementing a variety of measures, such as price controls (through agreements and sanctions) and raising the monetary policy rate (which was generally not positive in real terms, although it was close to the inflation rate); and (iii) the containment of the gap between the parallel and official exchange rates, for which the government intervened to accommodate prices and prevent the gap from widening. Another objective, less relevant for the government than the previous ones, was to moderate the deviations with respect to the targets set forth in the EFF. In order to help the Treasury achieve its issuance target, the government continued to resort to the methodology already applied by former Minister Guzmán, whereby the Central Bank participated in the secondary debt market of the Treasury, so that the latter could take a greater volume of debt to

6

finance spending; for the fiscal target, Minister Massa undertook a partial price adjustment of utility tariffs, although this was set aside in the context of the Presidential elections. The Fernandez administration’s attemptreserve accumulation target was reduced as a result of the difficulties posed by the severe drought suffered in 2023.

Although the results were not as expected: inflation went from 71% year-on-year in July 2022 to stabilize114% year-on-year in May 2023, international reserves went from US$40 billion (monthly average) in July 2022 to US$26 billion (monthly average) in July 2023 and the exchange rate gap was still very high, the government chose Minister Massa as its candidate for President.

Primary elections took place on August 13, 2023. Javier Milei, candidate for La Libertad Avanza (LLA), was the most voted in the primary presidential elections with 30.0% of the total votes. The second most voted political party was Juntos por el Cambio, whose candidates achieved 28.3% of the votes, followed by the candidates of Unión por la Patria (Massa’s party) who achieved 27.3% of the votes. These results were surprising not only because of the parity between the main parties, but also because of the unexpected victory of Milei. The day after the elections, the government validated a 22% increase in the exchange rate and a 22 percentage points increase in the monetary policy rate. This devaluation jump was not accompanied by a stabilization plan, so the benefits of depreciating the real exchange rate were almost non-existent and monthly inflation accelerated to 12.4% and 12.7% in August and September 2023, respectively, the highest values (at that time) in more than 30 years.

After the primary elections, Minister Massa took a series of measures to improve the population’s income in the short term, including one-time bonuses and tax cuts. We estimate the fiscal impact of these measures at 1% of GDP. In the general elections, Sergio Massa obtained 36.7% of the votes, followed by Javier Milei who obtained 30.0% of the votes and Patricia Bullrich, a member of Mauricio Macri’s party, who obtained 23.8% of the votes. The new Congress is fragmented, which will force the new President to negotiate the approval of laws.

On November 19, 2023, Javier Milei was elected President of Argentina with 55.7% of the votes, and he took office on December 10, 2023 (the “Milei administration”). In the first months of the Milei administration, the Central Bank raised by 120% the value of the US$/Peso exchange rate, allowing for the acquisition of international reserves amounting to US$5,624 million from December 11, 2023 to February 15, 2024. At the same time, the Central Bank implemented a debt payment process with importers consisting of the subscription of US$-denominated bonds issued by the Central Bank but payable with Argentine peso, which allowed the Central Bank to withdraw pesos from the economy. Finally, the Central Bank also decided to lower the monetary policy rate -which was yielding 133% per annum- to 70% per annum, in order to reduce the interest payments that the Central Bank pays to banks for their interest-bearing liabilities. This measure is having a negative effect on the Bank as we are receiving lower remuneration on the money we lend to the Central Bank. On the political front, Milei’s government sent to Congress an extensive package of laws aimed at deregulating the economy, which was not approved given the insufficient support that the Milei administration has in Congress.

We cannot assure whether Milei will implement aggressive political and reduceeconomic policies, such as the fiscal deficit,dollarization of our economy, or whether his government will take a more moderate path. The implementation of aggressive political and economic policies could result in further uncertainty and the trade deficit, inflation, poverty and country risk have to date proved unsuccessful. Any furtherinstability of the Argentine economy, all of which could adversely result our results of operations. Additionally, the dollarization of the economy or other disruptive exchange rate measures could be detrimental to the economytrigger hyperinflation and adversely affecta banking crisis, damaging our business, results of operationsbalance sheet and financial condition.potentially reducing our net income.

If current levels of inflation continue, the Argentine economy and the Bank’s business, results of operations and financial condition could be adversely affected.

Argentina has been facing high inflation levels since 2007. According to information published by the National Institute of Statistics and Censuses (“INDEC”), the CPI increased 9.5% in 2011, 10.8% in 2012, 10.9% in 2013, 24% in 2014 and 11.9% in the ten-month period ended on October 31, 2015. INDEC stopped publishing the CPI in the period between November 2015 and April 2016, and resumed the publication of inflation rates with its new methodology for calculating the CPI as of June 2016, reflecting a cumulative increase of 16.9% from May to December 2016. The INDEC reported an annual variation of the CPI of 47.6%50.9%, 53.8%, 36.1%, 50.9% and 94.8 % and 211.4 % in 2018, 2019, 2020, 2021, 2022 and 2022,2023, respectively.

As a result of the devaluation of the Argentine Peso and the continuity of the process of adjustment of public service rates, as well as an unfavorable international context in terms of financing, the three-year accumulated inflation as of July 2018 was over 100%. Consequently, the Bank applied International Accounting Standard N° 29 (“IAS 29”) “Financial Reporting in Hyperinflationary Economies” as from July 1, 2018 in the preparation of the Consolidated Financial Statements accompanying this annual report, which requires the financial statements of any entity whose functional currency is the currency of a hyperinflationary economy, either based on the historical cost method or on the current cost method, be expressed in terms of the unit of measure that is in effect at the end of the reporting period. IAS 29 does not establish an absolute inflation rate above which hyperinflation is presumed.

Likewise since January 1, 2020, financial entities supervised by the BCRA, such as the Bank, are required to prepare their statutory financial statements in accordance with IAS 29 in the preparation of their financial statements as established by Communication “A” 6651.

During the first half of 2022, and as in 2021, the government tried to contain the inflationary acceleration produced by the monetary overhang derived from the monetary issuance in 2020 and 2021, with an appreciation of the real exchange rate and a freeze in the price of utility tariffs. This strategy was inefficient to reduce inflation, which averaged 5.3% per month in the first half of 2022. In July 2022, after the sudden departure of Minister Martín Guzmán, parallel exchange rates rose 20% in one week and determined a successive remarking of prices that accelerated the already very high inflation, leading to a 6.8% monthly average in the third quarter of the year. However, since the

7

The arrival of Minister Massa and withresulted in a decrease of inflation values; however the slight reduction of public spending and monetary issuance, the government has managed to decrease inflation values from the monthly peak of 7.4% in July 2022. The adjustment of regulated prices (mainly utility rates) was one of the main inflationary drivers of the last months of 2022 and the beginning of 2023. Monthly

As a result of the strong drought suffered in Argentina for the last three years; inflation decelerated sharply in November and December 2022 and then accelerated until April 2023. After the primary elections the government adjusted the exchange rate and approved a 22% rise of the parity exchange rate between the U.S. dollar and the Argentine peso. As a result, monthly inflation started to increase at double-digit and year-on-year inflation at December 2023 reached 211%. At the same time, the official exchange rate was 6%27% more appreciated than the average of the last 20 years. President Milei has already announced that a price stabilization plan will be launched with the aim to reach fiscal equilibrium but, as of the date of this annual report on Form 20-F, there is no certainty as to how this plan will be implemented and the effects it will have on the exchange rate market and/or the fiscal deficit. The Bank’s balance sheet is exposed to the interest-bearing liabilities of the Central Bank (both LELIQ, which is a 28-day instrument, and 1-day REPO), and if the government implements measures aimed to reduce the Central Bank’s interest-bearing issuance, including a rate reduction or a plan to exchange these instruments, the Bank’s balance sheet and net income will be adversely affected.

After the increase in the parity exchange rate, inflation increased from 12.8% per month in November 2023 to 25.5% per month in December 2023, 20.6% per month in January 2023, 6.6%2024 and 13.2% per month in February 20232024. At the same time, the new government announced the deregulation of a series of regulated prices (such as health insurance, transportation and 7.7%utility rates) that could continue to drive inflation in March, 2023.

the short term. We cannot predict whether any measures to be implemented by the FernandezMilei administration to control inflation will have the desired effect. Currently and in the past, inflation has adversely affected the Argentine economy and the government’s ability to create conditions leading to growth. An environment of high inflation rates also negatively affects Argentina’s international competitiveness, real wages, employment rates, the consumption rate, and interest rates. High levels of inflation and the high level of uncertainty regarding economic variables, have in the past, and may in the future, adversely affect economic activity, which could materially and adversely affect our business, results of operations and financial condition.

8

High levels of inflation adversely affect the financial sector’s ability to provide long-term loans because of the difficulty in establishing an appropriate interest rate, typically making lending more expensive for banks, including us.

A high level of public spending could negatively affect the Argentine economy and its access to financial markets.

DuringWhile the last years of the mandate of Fernández de Kirchner (the “Kirchner administration”), the governmentMacri administration had managed to significantly reduce fiscal deficit by 2019, increased public spending turning to the BCRA and the Argentine Social Security Office (“ANSES”) to cover partreduced revenue during 2020 as a result of the funding requirements of the public administration, generated in part by the policy of subsidies to certain public services such as electricity, gas, water and transportation, which together with an expansionary monetary policy led to a greater increase in prices, all of which adversely affected consumer purchasing power and economic activity levels.

The Macri administration adopted measures to mitigate the increase in the fiscal deficit and reduce its current level. For 2017 and 2018, the Macri administration set a fiscal deficit target of 4.2% and 2.7% of GDP, respectively, achieving a fiscal deficit of 3.9% and 2.4% of GDP, respectively. Although the objective of the Macri administration was to achieve a primary fiscal deficit equivalent to 1.3% of GDP in 2019, by virtue of negotiations with the IMF and in accordance with the National Budget Law for 2019, the fiscal deficit target was reduced to 0% of GDP in 2019 with a surplus of 1% in 2020. Subsequently, this target wasCovid-19 pandemic, significantly increased to 0.5% of GDP. The deficit in 2019 finally amounted to Ps 95,121 million, equivalent to 0.4% of GDP.

In 2020, in the face of the Covid-19 crisis, the Fernandez administration announced a package of fiscal stimulus measures to alleviate the effects of the recession, focused on sustaining the income of the most vulnerable families and companies most affected by social isolation. The combined effect of the increase in spending and the fall in revenue (due to the economic recession) produced a significant increase in the fiscal deficit in 2020. The 2020, primary fiscal deficit waswhich reached 6.4% of GDP, the highest in more than 40 years.GDP. Although the Treasury showed signs of fiscal austerity by the end of 2020, the inaccessibility to debt markets forced the government to finance its fiscal needs almost exclusively with monetary issuance from the Central Bank. As of December 31, 2021, the fiscal deficit accounted for 2.0%2.1% of GDP (3.0% if IMF’s special drawing rights (“SDRs”) were not taken into account), which showed that, even though the fiscal balance was not moving towards an equilibrium as fast as the economy demanded, the fiscal gap was lower in 2021 than in 2020. The lower fiscal deficit in 2021 was not only explained by a deceleration in public spending compared to 2020 but also by a significant increase in economic activity, higher export duties and a one-off tax on large fortunes.

The government had proposed a fiscal deficit of 3.3% of GDP for 2022 at the beginning of the year through the presentation of the revenue and expenditure budget for the national public sector. However, this bill was not approved, and the government had to negotiate a fiscal deficit target with the IMF without the consensus of the political opposition. The government finally agreed to a target of 2.5% of GDP, which was complied with. The tariffs adjustment and the additional revenues received by the Treasury from taxes levied on soybean exporters who liquidated commodities at a higher exchange rate, allowed the Treasury to improve the fiscal balance. We believe that it will be critical for the government to keep reducing the fiscal deficit to ensure less reliance on debt issuance and monetary financing in order to reduce the very high levels of inflation.

The Fernandez administration had proposed a primary fiscal deficit target of 1.9% of GDP for 2023, however, fiscal deficit reached Ps.5.1 trillion (accounting for approximately 2.7% of GDP pending publication of public official figures). The impact of the fiscal measures that took place between the primary and general elections was close to 1% of GDP. Milei’s stabilization plan aims to reduce the fiscal deficit to zero by ceasing money issuances by the Central Bank to assist the Treasury. It is uncertain how this stabilization plan will be implemented, if at all, and the effects it could have on the fiscal deficit. The Treasury had already reached fiscal surplus in January 2024, primarily as a result of expenses growing below inflation levels and expense cuts.

8

The Treasury will face high debt maturities in the upcoming months and, potentially, a higher demand for financing to fund next year’s fiscal deficit. Aany poor performance in the local debt market, with debt rollovers below 100%, could complicate the public sector’s sources of financing, increasing the possibility of requiring higher direct financing from the Central Bank, which would increase the already high level of inflation.

In addition, any deterioration in the government’s fiscal position negatively affects its ability to access debt markets in the future and could result in greater restrictions on accessing those markets by Argentine companies, including the Bank.

A weaker fiscal position could have a material adverse effect on the government’s ability to obtain long-term financing and adversely affect economic conditions in Argentina, which could adversely affect the business, results of operations and financial condition of the Bank.

The Argentine economy could be adversely affected by economic events in other markets.

Weak or no economic growth or recession or adverse situations that affect any of Argentina’s main trading partners could negatively affect the balance of payments and, therefore, the economic growth of Argentina. In recent years, several Argentine trading partners (such as Brazil, Europe and China) have experienced significant slowdowns or periods of recession in their economies. If these slowdowns or recessions were to occur again, this could impact the demand for products that come from Argentina and thus affect its economy.

9

Furthermore, the global economy faces significant challenges. There have been concerns about unrest and terrorist threats in the Middle East, Europe and Africa and conflicts involving Russia, Ukraine, Israel, Iran Syria and North Korea.Syria. Likewise, economic and social crises have emerged in several Latin American countries during 2019, asin recent years, including the economyrecent crisis in most of the region slowed down after almost a decade of sustained growth, among other factors.Ecuador. There has also been concern about the relationship between China and other Asian countries, which can result in or intensify potential conflicts in relation to territorial disputes, and the possibility of a trade war between the United States and China. Furthermore, the UK withdrew from the European Union (“Brexit”) on January 31, 2020. The medium and long-term implications of Brexit are uncertain and could adversely affect European and global market and economic conditions and could contribute to instability in global financial and currency markets. Additionally, Russia’s invasion of Ukraine, the largest military attack on a European state since World War II, has led to significant disruption, instability and volatility in global markets, as well as higher inflation ( including(including by contributing to further increases in the prices of energy, oil and other commodities and further disrupting supply chains) and lower growth. The EU, UK, U.S. and other governments have imposed significant sanctions and export controls against Russia and Russian interests and threatened additional sanctions and controls. The impact of such an invasion and these measures, as well as potential responses to such measures by Russia, is currently unknown and, whileWhile we have limited exposure to Ukraine and Russia, theythis or similar conflicts could significantly and adversely affect our business, financial condition and results of operations.

The Covid-19 pandemic led to economic contractions in most of the world’s economies in 2020, both developed and emerging. This affected the Argentine economy mainly through trade since the demand for its exports (mainly from Brazil and Europe) dropped substantially. In 2021, most economies experienced significant growth compared to 2020, which together with higher commodity prices (mostly soybean) during the second quarter of 2021 led to higher exports for Argentina. As a result, in 2021, the Argentine economy accumulated a US$14,750 million surplus, representing a 17.7% increase compared to 2020.

Additionally, the inflationary acceleration that has taken place in the United States and Europe has led central banks to tighten monetary policy, resulting in significant interest rate hikes. This fact restricts market access to emerging markets, including Argentina, since investors tend to invest in more stable economies.

In addition, recently,in early 2023, concerns have arisen with respect to the financial condition of a number of banking organizations in the United States and Europe, in particular those with exposure to certain types of depositors and large portfolios of investment securities. On March 10, 2023 Silicon Valley Bank was closed by the California Department of Financial Protection and Innovation and the Federal Deposit Insurance Corporation was appointed receiver of Silicon Valley Bank. On March 11, 2023, Signature Bank was similarly closed and placed into receivership and concurrently the Federal Reserve Board announced it would make available additional funding to eligible depository institutions to assist eligible banking organizations with potential liquidity needs. In Europe, on March 15, 2023 the National Swiss Bank announced several measures amounting to approximately 50 billion Swiss francs to provide Credit Suisse with liquidity and on March 20, 2023 UBS announced that it would acquire Credit Suisse for approximately US$3,250 million. While our business, balance sheet and depositor profile differ substantially from banking institutions such as SilliconSilicon Valley Bank and Signature Bank, the operating environment and public trading prices of financial services sector securities can be highly correlated, in particular in times of stress, which may adversely affect the trading price of our securities and potentially our results of operations.

9

If international and local economic conditions fail to improve or deteriorate even more, the Argentine economy could be negatively affected as a result of lower international demand and lower prices for its products and services, higher international interest rates, less capital inflow and greater aversion to risk. Any of the foregoing could also adversely affect the Bank’s business, results of operations and financial condition.

A decline in international prices for or in the amount of Argentina’s principal commodity exports could have a material adverse effect on Argentina’s economy and public finances, and, as a result, on our business.

Historically, the commodities market has been characterized by high volatility. Despite the volatility of prices of most of Argentina’s commodities exports, commodities significantly contributed to the government’s revenues during the 2000s due to the imposition of export duties on agricultural products in 2002. Although most duties were eliminated and the export tax on soy was reduced from 35% to 30% by the Macri administration in 2016, and was further reduced in 2018 by 0.5% per month, the Argentine economy is still relatively dependent on the price of its main agricultural exports, primarily soy. This dependence, in turn, renders the Argentine economy vulnerable to commodity prices fluctuations. International soybean prices decreased slightly

10

during 2017 and further in 2018 due to growing trade tensions between the United States and China. During 2019, soybean prices reached their lowest prices over the prior five years, but recovered from US$305.5 per ton in May 2019 to US$335.0 per ton in December 2019. During the last months of 2020 soybean prices showed an upward trend (due to purchases from China, the monetary stimulus of the main central banks of the world and the promising news regarding the Covid-19 vaccine) that continued until the second quarter of 2022 when they reached US$621 per ton, the higher value in 10 years. However, soybean prices have declined since then,after that, reaching US$507.0 per ton in October 2022. and have continued to decline since then, being close to US$455 per ton by the end of 2023, the lowest since December 2020.

In addition, theThe amount of agricultural products harvested in any given period may decrease due to adverse weather conditions. For example, as a drought or flood could adversely affect the performanceresult of the agricultural sectorsevere drought suffered during the last three years, Argentina experienced a significant water deficit, which resulted in soybean production being less than half as expected and worsenin an estimated reduction in dollar inflows of approximately US$20 billion. This has been, together with the appreciation of the official exchange rate, one of the main sourcescauses of foreign currency generationthe drop in Argentina.the Central Bank’s gross reserves from US$38 billion on November 30, 2022, to US$23.0 billion on December 31, 2023.

Declines in the prices or the amount of highly exported commodities may adversely affect the Argentine economy and the government’s fiscal revenues, which could in turn adversely impact the business, results of operations and financial condition of the Bank.

Exchange controls and restrictions on capital inflows and outflows could have a material adverse effect on Argentine public sector activity, and, as a result, on our business.

FromWith the exception of some limited periods of time, since 2011, to 2015, the different Argentine government introducedgovernments have implemented exchange controls and restrictions on the transfer and entry of foreign currency, that significantly limitedlimiting the ability of companies to hold foreign currency in Argentina or make payments abroad.

After taking office in 2015, the Macri administration substantially eliminated all exchange restrictions that had been implemented under the previous administration. Nevertheless, on September 1, 2019, due to the economic instability and the significant devaluation of the peso that took place in August 2019 after the primary elections, the government and the BCRA adopted a series of measures reinstating certain exchange controls limiting the access to the local exchange market in order to reduce the purchases of foreign currency. The payment of external financial debt, dividends in foreign currency and the payment of imports of goods and services were severely restricted and the obligation to enter and settle in pesos the funds from the export of goods and services, was reinstated, among other measures. Other financial transactions such as derivatives and transactions in securities are also limited by the new exchange regime.

The Fernandez administration extended the period during which these measures would apply and established additional measures through the Solidarity Law, including a tax on certain transactions that imply the acquisition of foreign currency by individuals and companies. During 2020, foreign exchange market regulations have been strengthened and made increasingly more complex. Towards the end of May 2020, the BCRA issued Communication “A” 7030 by means of which access to foreign currency to pay for imports was severely limited. After that, on September 15, 2020, the Central Bank tightened the foreign exchange market controls. First of all, companies with external financial maturities of more than US$1 million due before March 31, 2021 had to present a restructuring plan of at least 60% of the capital payment. Secondly, a 35% tax was added to individuals who buy dollars in the official market (already limited to US$200 per month, and on top of a 30% tax on the official exchange rate) and finally, Communication “A” 7106 banned non-residents from selling bonds for foreign currency. These decisions resulted in a notorious sell-off of sovereign bonds, which led to a 7% daily fall. The Central Bank sold US$1,318 million during the following five weeks, in order to keep the exchange rate depreciation at desirable levels. Due to this unsustainable situation, the government decided to partially ease the restrictions. The Central Bank purchased US$608 million in the spot market in December 2020.

During 2021, the government maintained the tightened restrictions on imports and financial transactions with bonds.bonds that had been implemented in previous years. In October 2021, the Central Bank reduced the minimum threshold above which imports required authorization (which resulted in less imports being automatically approved). Meanwhile, the monetary authority significantly reduced the allowed weekly trading amount for domestic-law bonds, resulting in blue chip swap transactions being required to be carried out with foreign-law bonds.

During 2022, the government not only maintained most of the restrictions imposed in 2020 and 2021, but also implemented an exchange rate regime with differential effective exchange rates for different sectors of the economy, which resulted in increased complexity. For instance, the government implemented the “soybean dollar”, a transitory exchange rate for exporters of the soybean sector, which was higher than the official exchange rate during the months of September and December, leading to higher dollar settlements related to the agricultural sector during those months and very low USDUS$ settlements from the agricultural sector in the others. At the same time, through taxes or withholdings, new exchange rates were created: for tourism and international artists, among others. Finally, a new import monitoring system with additional supervision of payments was set up.

1110

During 2023, new exchange rates continued to appear for certain sectors, similar to the soybean dollar in 2022 as the shortage of Central Bank reserves prevented the government’s ability to avoid a significant increase in the exchange rate between the U.S. dollar and the Argentine peso. In this sense, the Fernandez administration launched several campaigns allowing exporters to settle 30% of their exports through the parallel exchange rate market with the remaining 70% having to be liquidated at the official exchange rate. Initially, this campaign only applied to soybean exporters, but it was later extended to all types of exports. After the elections, and with an increased need to generate foreign currency inflows, the proportion of export dollars that could be liquidated at the parallel exchange rate was increased from 30% to 50%, which granted some short-term relief in the Central Bank’s stock of reserves. The Milei administration has modified these values and as of the date of this annual report, exporters are allowed to settle 20% of their exports in the parallel exchange rate market, while the remaining 80% needs to be settled in the official exchange rate market.

Milei has announced that all current exchange rate restrictions will be eliminated as soon as the fiscal deficit is reduced. There is no certainty as to the scope or timing for any of these measures and the effect they would have on the Bank. The lifting of these exchange rate restrictions could result in an acceleration of inflation, which could negatively affect our balance sheet and net income.

The establishment of new restrictions on foreign trade or related to the foreign exchange market, together with the application of new exchange rates, could require the Bank to allocate additional and unbudgeted resources to provide customers with the tools they require to carry out transactions under the new regulatory framework. Additionally, such tools may not be developed on a timely basis due to changing demands.

Any changes in the policies of the current government concerning economic, exchange and financial matters in order to preserve the balance of payments, the Central Bank’s reserves, a capital outflow or a significant depreciation of the Peso, such as the mandatory conversion into Pesos of obligations assumed by legal entities resident in Argentina in US dollars which could be due to a period of crisis and political, economic and social instability affecting Argentina, or otherwise, any of which could be exacerbated as a result of the Covid-19 pandemic, could have an adverse effect on Argentina’s economic activity and the Bank’s business, results of operations and financial condition.

The measures adopted to resolve the crisis in the energy sector may not be sufficient, which could affect the business, the results of operations and the financial condition of the Bank.

The economic policies applied since the Argentine crisis of 2001-2002 have had an adverse effect on the Argentine energy sector. The failure to reverse the freeze on electricity and natural gas rates imposed during the crisis became a barrier to investment in the energy sector. The government tried to encourage investment by subsidizing energy consumption but the policy proved ineffective and served to further discourage investment in the energy sector, causing oil and gas production and electricity generation, transmission and distribution to stagnate while consumption continued to rise. To address the power supply shortage that began in 2011, the government attempted to increase imports of electrical power, with adverse consequences for the trade balance and international reserves.

In response to the growing energy crisis, the Macri administration declared a state of emergency for the national electricity system, which ended on December 31, 2017. The state of emergency allowed the government to take measures to stabilize the supply of electricity to the country. In this context, subsidy policies were re-examined and new electricity rates were adopted.

However, utility rates were almost frozen from 2019 to 2022, which worsened the national energy situation by promoting higher demand and discouraging new investments from supplying companies, resulting in an energy deficit heightened by the lack of dollar inflows.

Although actions have been carried out to attempt to address the crisis in the energy sector, in recent months,2023, the partial removal of subsidies to fund utilities (particularly with respect to high income families), the lack of a definitive resolution of the negative effects on the generation, transport and distribution of electricity in Argentina with respect to residential and industrial supply could undermine confidence and adversely affect Argentina’s economic and financial condition, resulting in political instability, and adversely affecting the Bank’s business and results of operations.

Likewise, theThe Milei administration has continued to remove subsidies for utilities and public transportation and has decided to stop all public works until 2024. The elimination of subsidies and the progressive increase in prices could continue to generate social

11

unrest and be challenged in local courts. Additionally, the decision to stop all public works could result in the failure to progress on the construction of the gas pipeline that will take gas from Patagonia to Buenos Aires and generally result in lower investment and a lower need for funding to finance that investment, which would adversely affect the Bank. We can give no assurance that the measures adopted by the governmentMilei administration to deal with the energy crisis will be sufficient to restore energy production in Argentina in the short or medium term. Since the Fernandez administration took office, the rates of public services have been frozen, so a rise in energy demand is expected to generate deficit pressures on the trade balance due to the need to import gas to maintain the levels of domestic production and prevent it from declining as a result of the lack of investment driven by the capped prices.

12

The current lack of resolution on tariffs results in uncertainty regarding the future situation of the energy market in Argentina and constitutes a source of potential risk for the country’s economy and could lead to exchange rate volatility, either of which could adversely affect the Bank’s business, results of operations and financial condition.

Any failure to adequately address actual and perceived risks of institutional deterioration and corruption may adversely affect Argentina’s economy and financial condition.

The lack of a sound institutional framework and corruption have been identified as, and continue to be, critical problems for Argentina. Argentina ranked 9498 out of 180 countries in the 20222023 Corruption Perceptions Index published by Transparency International.

Failure to address these issues could increase the risk of political instability, distort decision-making processes and adversely affect Argentina’s international reputation and ability to attract foreign investment, and consequently, may negatively affect our business, financial condition and results of operations. Although the Argentine government has taken several measures aimed at strengthening Argentina’s institutions, these measures may be insufficient to ensure transparency and integrity in a highly polarized political context, which could have a material adverse effect on the business, the results of operations and the financial condition of the Bank.

Fluctuations in the value of the peso could adversely affect the Argentine economy and Argentine’s ability to service its debt obligations.

Fluctuations in the value of the peso may adversely affect the Argentine economy. A devaluation of the peso may adversely affect the government’s revenues (measured in U.S. dollars), fuel inflation and significantly reduce real wages. After several years of moderate variations in the nominal exchange rate, the peso lost 35.3% of its value in 2014 and 33.7% in 2015. Persistent high inflation during this period, with formal and “de facto” exchange controls, resulted in an increasingly overvalued real official exchange rate. Compounded by the effects of foreign exchange controls and restrictions on foreign trade, these highly distorted relative prices resulted in a loss of competitiveness of Argentine production, impeded investment and resulted in economic stagnation during this period.

After foreign exchange controls were lifted at the end of 2015, the peso depreciated by 38.5% in 2016 considering the average foreign exchange rate in December 2016 compared to the average foreign exchange rate in December 2015. In 2017, the depreciation of the peso fell to 11.8%, well below inflation, raising doubts about potential appreciation of the peso in real terms. In this scenario, the vulnerability of the Argentine economy due to a tightening of international financial conditions was reflected in a current account deficit of 4.9% of GDP in 2017 and a low level of international reserves compared to other countries in the region. When ten-year U.S. treasury rates began to rise and the U.S. dollar strengthened, these vulnerabilities resulted in a negative differentiation of Argentina compared to other emerging countries, which led to a prolonged run on the currency despite frequent interventions by the Central Bank and a sizeable loan from the IMF signed in June 2018. Finally, after another sell-off of Argentine assets in August 2018 and a strong depreciation of the peso, in early October 2018 a revised program with the IMF which further tightened fiscal and monetary policy managed to stabilize the foreign exchange market and the peso appreciated by 7.5% in the last quarter of 2018. Considering the full year, the peso depreciated by 50.3% in nominal terms in 2018. Together with the decline in economic activity, the real depreciation of the peso resulted in a strong reduction in imports and a correction of the external deficit in the fourth quarter of 2018.

According to a revision of the IMF agreement, the Argentine peso had to float freely within an accepted band of exchange rates, but the Central Bank could intervene to a limited extent in the foreign exchange market selling reserves if the exchange rate rose above a certain level, defined initially at Ps.44/US$ (and subsequently adjusted by inflation) which was the upper threshold of the accepted band in which the peso could float freely without intervention of the Central Bank. Conversely, the Central Bank was charged with purchasing reserves if the foreign exchange rate fell below the lower threshold of the non-intervention band. In early 2019, the peso crossed the lower threshold, prompting purchases by the Central Bank and a strong decline in interest rates pursuant to the monetary program.

13

By the end of April 2019, exchange rate tensions, together with negative inflation reports of March 2019, led the Central Bank to agree with the IMF the possibility of an intervention even within the (then) exchange reference zone. The announcement of the measure significantly reduced volatility in the exchange rate and helped to contain inflation expectations. It further deepened the contractive profile of the monetary policy since the pesos obtained from the sales of dollars were not re-injected and instead, the monetary base objective was reduced. Thus, the supply of foreign currency from exporters increased and demand decreased. In spite of this, the adverse reaction of the markets to the primary elections in August 2019 led to an increase in exchange rates, and an increase in the lack of confidence in Argentine assets. The prices of Argentine government securities fell by 20% while the value of local companies’ shares declined more than 40% over a few days. The U.S. dollar exchange rate exceeded Ps.60, which implied a depreciation of more than 25% in just four days. The Central Bank intervened in the market, with relatively little success, by selling foreign currency, which brought about a fall in the international reserves of around US$2 billion. For individuals, the Central Bank established a maximum limit of US$200 for the purchase of foreign currency per calendar month across all entities authorized to trade in foreign exchange, as well as for purposes of formation of foreign assets, family assistance remittances, and transactions with derivatives. This measure was enacted in order to help control the exchange rate without using reserves. However, due to the high money issuance and the resulting monetary overhang, the Central Bank sold international reserves in order to smooth the depreciation of the peso. Nevertheless, as the reserves stock is limited and the more the Central Bank uses them, the more the foreign exchange premium rises, the Central Bank decreed a series of measures during 2020 to avoid further loss of reserves, including, for example, Communication “A” 7030 and “A” 7106 (see, “—Exchange controls and restrictions on capital inflows and outflows could have a material adverse effect on Argentine public sector activity, and, as a result, on our business”).

The Central Bank has maintained the same exchange rate policy since December 2019, consisting of avoiding foreign exchange disruptions by applying more controls, selling foreign reserves and establishing multiple exchange rates. The Central Bank invested more than US$2.1 billion of reserves in the official exchange rate market from August 2021 to August 2022 to curb the depreciation of the Argentine peso. However, the Central Bank purchased US$5.8 billion of reserves in the official exchange rate market, between September 2022 and December 2022, thanks tofor a transitory differential exchange rate regime that allowed soybean exporters to sell dollars to the Central Bank at a higher exchange rate during the months of September and December.

The government seeksaimed to maintain the USD/US$/Peso parity to prevent the undesired effect that a devaluation would have on inflation, and validated a real appreciation of the official exchange rate in 2022. The nominal exchange rate rose 72.4% in 2022, while accumulated inflation in the same period was 94.8%. The December 2022 real exchange rate was 24% lower than the real exchange rate in December 2019.

The exchange rate premium arising from exchange controls further complicates the foreign exchange market due to the coexistence of an appreciated real exchange rate, and a parallel exchange rate that increases devaluation expectations, discouraging exports and encouraging imports. In this regard, between January 2022 and August 2022, the Central Bank only bought the equivalent of 1% of the stock of dollars it bought in the same period of the previous year. This situation, which jeopardized compliance with the IMF’s third quarter reserves target, led the government to apply a differential exchange rate for soybean exporters, which was 40% higher than the official exchange rate. This exchange rate was in effect in September 2022 and allowed the Central Bank to buy USD US$4,966 million in the official exchange market. The application of differential exchange rates adversely impactsimpacted the Central Bank’s balance sheet due to the difference between the higher price at which it buysbought dollars and the lower price at which it sellssold dollars to importers.

The

12