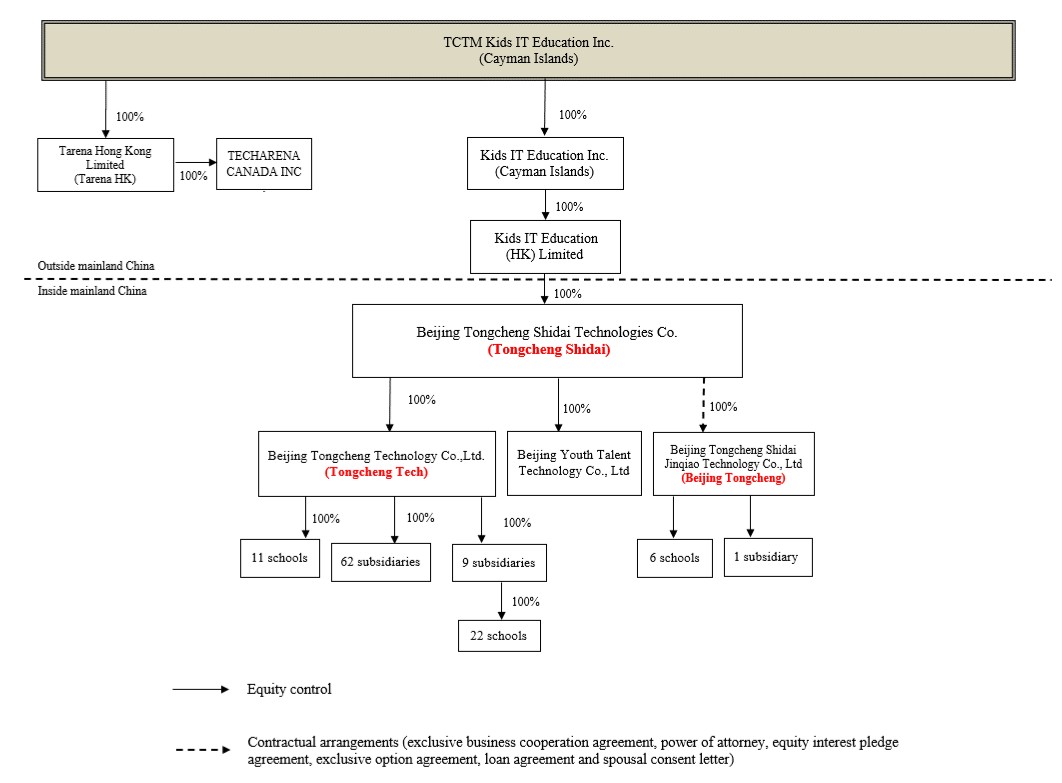

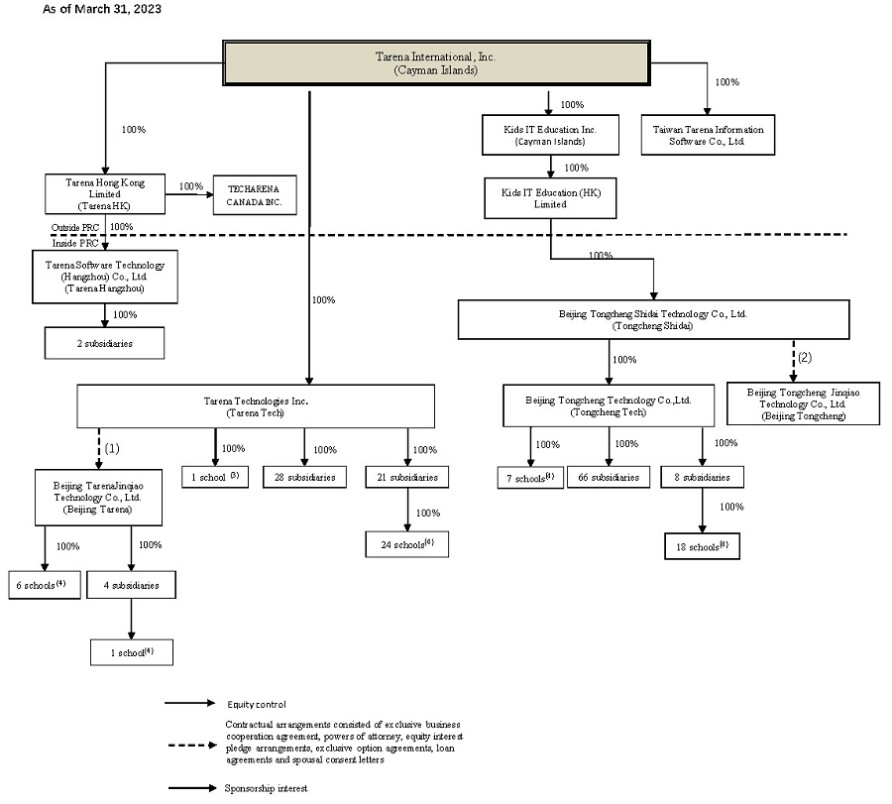

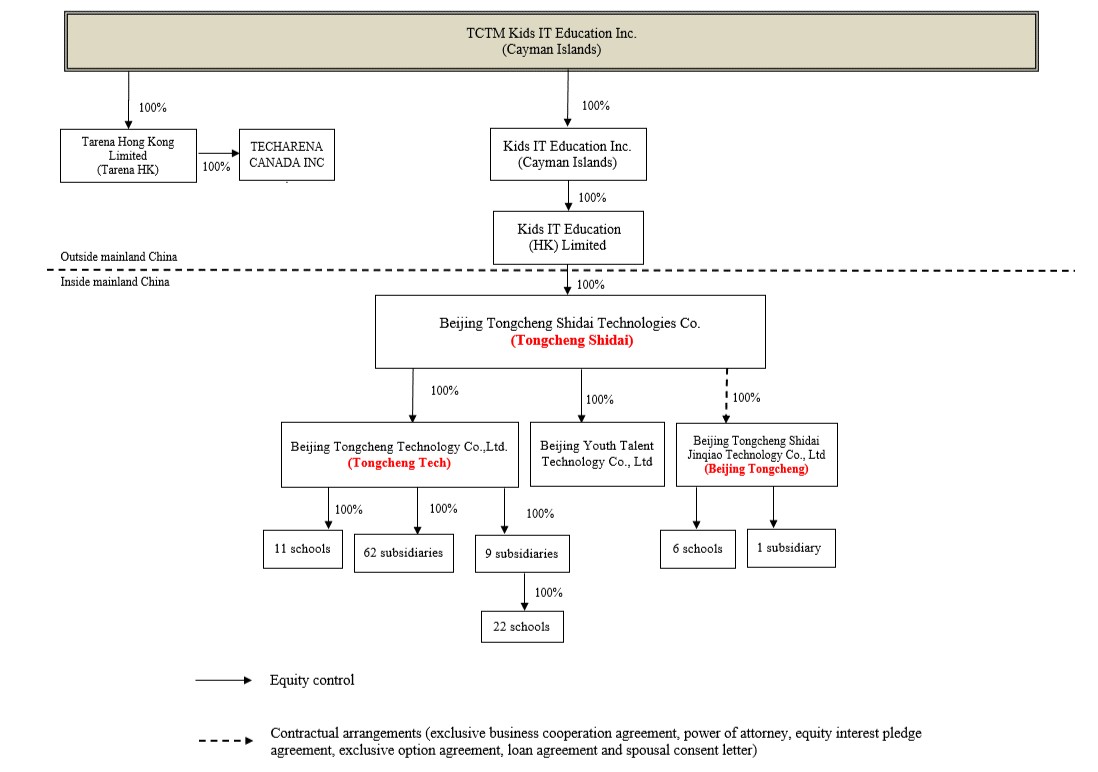

The following diagram illustrates our corporate structure, including our principal subsidiaries, the principal VIEs and other entities that are material to our business, as of the date of this annual report:

5

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20222023.

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report ___________

For the transition period from ___________ to ___________

Commission file number: 001-36363

Tarena International,TCTM Kids IT Education Inc.

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

Cayman Islands

(Jurisdiction of incorporation or organization)

6/F, No. 1 Andingmenwai Street, Litchi Tower,

Chaoyang District, Beijing 100011,

People’s Republic of China

(Address of principal executive offices)

1/F, Block A, Training Building,

65 Kejiyuan Road, Baiyang Jie Dao,

Economic Development District,

Hangzhou 310000, People’s Republic of China

(Address of principal executive offices)

Ping WeiXiaobo Shao, Chief Financial Officer

Email: bjweiping@tedu.cnshaoxiaobo@tedu.cn

6/F, No. 1 Andingmenwai Street, Litchi Tower,

Chaoyang District, Beijing 100011,

People’s Republic of China

Telephone: +86 10-6213 5687

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol |

| Name of each exchange on which registered |

American Depositary Shares, each |

|

| | The NASDAQ Stock Market LLC |

representing five Class A ordinary shares, |

| | | (The NASDAQ |

par value US$0.001 per share |

| | | |

Class A ordinary shares, |

| | |

|

par value US$0.001 per share |

| | | (The NASDAQ |

* | Not for trading, but only in connection with the listing on The NASDAQ |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report. As of December 31, 2022,2023, there were 53,773,95153,962,196 ordinary shares outstanding, par value $0.001 per share, being the sum of 46,567,89246,756,137 Class A ordinary shares (excluding 10,608,95011,105,190 Class A ordinary shares issued to our depositary bank for bulk issuance of ADSs reserved for issuances upon the exercise or vesting of awards under our share incentive plan) and 7,206,059 Class B ordinary shares.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒ No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “accelerated filer,” “large accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ | Accelerated filer ☐ |

Non-accelerated filer ☒ | Emerging growth company ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☒ | International Financial Reporting Standards as issued by | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

TABLE OF CONTENTS

| | |

| Page | |

1 | ||

| | |

| ||

| ||

| ||

| ||

3 | ||

| ||

| ||

| ||

| ||

| ||

| ||

| ||

| ||

| ||

| ||

129 | ||

| ||

| ||

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

| |

| ||

133 | ||

| ||

| ||

| ||

| ||

PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

| |

| ||

| ||

| ||

DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS |

| |

135 | ||

135 | ||

| ||

| ||

| ||

| ||

| 138 | |

F-1 | ||

i

INTRODUCTION

In this annual report, except where the context otherwise requires and for purposes of this annual report only:

· | “ |

· | “current VIE” refers to Beijing Tongcheng Shidai Jinqiao Technology Co., |

· | “China” or “PRC” refers to the People’s Republic of China, including Hong Kong, Macau and |

· | “Divestiture” refers to the equity transfer transaction entered into in December 2023 to divest our professional education business. The Divestiture had been consummated at the |

· | “former VIE” refers to Beijing Tarena Jinqiao Technology Co., Ltd., or Beijing |

· | “Hong Kong” or “HK” or “Hong Kong S.A.R.” refers to the Hong Kong Special Administrative Region of the PRC; |

· | “IT” refers to information technology; |

· | “our company” refers to TCTM Kids IT Education Inc. (formerly known as Tarena International, Inc.), which is not a PRC operating company but a Cayman Islands holding company with operations primarily conducted through (i) our subsidiaries in mainland China and (ii) contractual arrangements with the VIEs based in mainland China. This structure entails unique risks to investors, see “Item 3. Key Information—D. Risk Factors—Risks Related to our Corporate Structure” for more details; |

· | “shares” or “ordinary shares” |

· | “ |

· | “student enrollments” for a certain period |

· | “U.S. GAAP” refers to generally accepted accounting principles in the United States; |

· | “variable interest |

· | “we,” “us,” “our” or |

· | “RMB” or “Renminbi” |

We present our financial results in RMB. We make no representation that any RMB or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or RMB, as the case may be, at any particular rate, or at all. The PRC government in mainland China imposes control over its foreign currency reserves in part through direct regulation of the conversion of RMB into foreign exchange and through restrictions on foreign trade. This annual report contains translations of certain foreign currency amounts into U.S. dollars for the convenience of the reader. Unless otherwise stated, all translations of Renminbi into U.S. dollars were made at the rate of RMB6.8972RMB7.0999 to US$1.00, the exchange rate as set forth in the H.10 statistical release of the Board of Governors of the Federal Reserve System in effect as of December 30, 202229, 2023 (except the cash dividend, which is translated at the rate on the exercise date).

1

FORWARD-LOOKING INFORMATION

This annual report on Form 20-F contains forward-looking statements that involve risks and uncertainties. All statements other than statements of historical facts are forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements.

You can identify these forward-looking statements by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “likely to” or other similar expressions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements include, but are not limited to, statements about:

| ● | our goals and growth strategies, and our ability to implement such strategies; |

| ● | our expectations regarding demand for and market acceptance of our courses; |

1

| ● | our ability to retain and increase our |

| ● | our ability to maintain and increase the utilization rate of our learning centers; |

| ● | our ability to offer new courses in existing and new subject areas; |

| ● | our ability to maintain and increase the tuition fees of our courses; |

| ● | our future business development, results of operations and financial condition; |

| ● | the expected growth of, and trends in, the markets for our services in mainland China; |

| ● |

| ● | assumptions underlying or related to any of the foregoing. |

You should read thoroughly this annual report and the documents that we refer to in this annual report with the understanding that our actual future results may be materially different from and worse than what we expect. Other sections of this annual report include additional factors which could adversely impact our business and financial performance. Moreover, we operate in an evolving environment. New risk factors and uncertainties emerge from time to time and it is not possible for our management to predict all risk factors and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We qualify all of our forward-looking statements by these cautionary statements.

You should not rely upon forward-looking statements as predictions of future events. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

2

PART I.

ITEM 1.IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

ITEM 2.OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

2

ITEM 3.KEY INFORMATION

Our Holding Company Structure and Contractual Arrangements with the Variable Interest Entities

Tarena International, Inc.TCTM is not ana PRC operating company incorporated in mainland China, but rather a Cayman Islands holding company with no equity ownership in its variable interest entities. Our Cayman Islands holding company does not conduct business operations directly. We conduct our operations in mainland Chinaprimarily conducted through (i) our subsidiaries incorporated in mainland China, or mainland China subsidiaries, and (ii) contractual arrangements with the variable interest entities with which we have maintained contractual arrangements and their subsidiaries.based in mainland China. Laws and regulations of mainland China restrict and impose conditions on foreign investment in certain internet value-added businesses. Accordingly, we operate these businesses in mainland China through the variable interest entities in order to comply with these laws and regulations, and rely on contractual arrangements among our subsidiaries in mainland China subsidiaries, the variable interest entities, and their nominee shareholders to control the business operations of the variable interest entities. The variable interest entities are consolidated for accounting purposes, but are not entities in which our Cayman Islands holding company, or our investors, own equity. Revenues from continuing operations contributed by the variable interest entities accounted for 6.7%1.3%, 5.9%2.9% and 6.4%6.6% of our totalnet revenues from continuing operations for the years of 2020, 2021, 2022 and 2022,2023, respectively. As used in this annual report, “we,” “us,” “our company” and “our” or “TCTM” refers to TCTM Kids IT Education Inc. (formerly known as Tarena International, Inc. and), its subsidiaries, and, in the context of describing our operations and consolidated financial information, the variable interest entities in mainland China, including but are not limited to, Beijing Tarena Jinqiao Technology Co., Ltd., orand Beijing Tarena, whichTongcheng for the effective period of their respective contractual arrangements with us. The current VIE, Beijing Tongcheng, holds our ICP license as an internet information provider and operates our TMOOC.cn website,a permit for the production and Beijing Tongcheng Shidai Jinqiao Technology Co., Ltd., or Beijing Tongcheng, which holds our ICP license as an internet information provideroperation of radio and television programs, and operates our 61it.cn website. website and Tongcheng Online App. Our variable interest entities are domestic companies incorporated in mainland China in which we do not have any equity ownership but whose financial results have been consolidated into our consolidated financial statements based solely on contractual arrangements in accordance with U.S. GAAP. Investors in our ADSs are not purchasing any equity interest in the variable interest entities in mainland China, but instead are purchasing equity interest in a holding company incorporated in the Cayman Islands.

AIn December 2023, we entered into an equity transfer agreement to dispose of our equity interests in the professional education business to a buyer consortium led by Tarena Weishang Technology (Hainan) Co., Ltd, or the Divestiture. Ms. Lijuan Han, sister of our founder and chairman Mr. Shaoyun Han, is a member of the buyer consortium and has an interest in the Divestiture. The Divestiture had been consummated at the end of March 2024. Upon the consummation of the Divestiture, the professional education business, including the business operated by the former VIE, had been divested, and the STEM education business operated by the former VIE had been transferred to the current VIE. The Divestiture represented a strategic shift that has a major effect on our company’s operations and financial results. As a result of the Divestiture, the professional education business has been reclassified as discontinued operations and our remaining business after the Divestiture has been reclassified as continuing operations. For detailed information regarding all material financial impacts related to the Divestiture, see “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Financial Impact by the Divestiture” and notes 1 and 3 to our consolidated financial statements, which are included in this annual report.

3

We, through our mainland China subsidiaries, the variable interest entities, and their shareholders entered into a series of contractual agreements. These contractual arrangements, during the respective effective period:

| ● | enable us to receive the economic benefits that could potentially be significant to the variable interest entities in consideration for the services provided by our mainland China subsidiaries; |

| ● | effectively assigned all of the voting rights underlying the nominee shareholders’ equity interest in the variable interest entities to us; and |

| ● | enable us to hold an exclusive option to purchase all or part of the equity interests in the variable interest entities when and to the extent permitted by the laws of mainland China. |

These contractual agreements includingamong our mainland China subsidiaries, the variable interest entities and their shareholders include exclusive business cooperation agreement,agreements, power of attorney, equity interest pledge agreements, exclusive option agreements, and loan agreements, have been entered into by and among our subsidiaries,agreements. As a result of the variable interest entities and their respective shareholders. Despitecontractual arrangements, the lack of legal majority ownership, our Cayman Island holding company is considered the primary beneficiaryshareholders of the variable interest entities and consolidateseffectively assigned all of their voting rights underlying their equity interest in the variable interest entities as required by Accounting Standards Codification topic 810, Consolidation. Accordingly, we treatto us, which gives our company or its subsidiaries the power to direct the activities that most significantly impact the variable interest entities as our consolidated entities under U.S. GAAP, and we consolidate the financial resultsentities’ economic performance. The nominee shareholders of the variable interest entities inare directors and members of our consolidated financial statements in accordancemanagement body. We consider such people suitable to act as the nominee shareholders of the variable interest entities because of, among other considerations, their contribution to us, their competence, and their length of service with U.S. GAAP.and loyalty to us. For more details onof these contractual arrangements, see “Item 4. Information on the Company—A. History and Development of the Company.”

However,

4

The following diagram illustrates our corporate structure, including our principal subsidiaries, the principal VIEs and other entities that are material to our business, as of the date of this annual report:

5

This type of corporate structure may affect investors and the value of their investment. The contractual arrangements may not be as effective as direct ownership in providing us with control over the variable interest entities, and we may incur substantial costs to enforce the terms of the arrangements. Uncertainties in the PRC legal system may limit our ability, as a Cayman Islands holding company, to enforce these contractual arrangements. Meanwhile, there are very few precedents as to whether contractual arrangements would be judged to form effective control overIf the variable interest entities throughor the nominee shareholders fail to perform their respective obligations under the contractual arrangements, or howwe could be limited in our ability to enforce the contractual arrangements inthat effectively assigned us the context of variable interest entities should be interpreted or enforced by the PRC courts. Should legal actions become necessary, we cannot guarantee that the court will rulevoting rights in favor of the enforceability of the variable interest entities contractual arrangements. In the event we are unable to enforce these contractual arrangements, or if we suffer significant delay or other obstacles in the process of enforcing these contractual arrangements, we may not be able to exert effective control over the variable interest entities, and these agreements have not been tested in the courts of mainland China. Furthermore, if we are unable to maintain such effective assignment, we would not be able to continue to consolidate the financial results of these entities in our ability to conduct our business may be materially adversely affected.financial statements. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—Any failure by Beijing Tarena or Beijing Tongcheng or theirits shareholders to perform their obligations under our contractual arrangements with them would have an adverse effect on our business” and “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—The shareholders of Beijing Tarena and Beijing Tongcheng may have potential conflicts of interest with us, which may materially and adversely affect our business and financial condition.”

If the PRC government deems that our contractual arrangements with the variable interest entities do not comply with PRC regulatory restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations change or are interpreted differently in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations. Our holding company, our subsidiaries and variable interest entities in mainland China, and investors of our company face uncertainty about potential future actions by the PRC government that could affect the enforceability of the contractual arrangements with the variable interest entities and, consequently, significantly affect the financial performance of the variable interest entities and our company as a whole. For a detailed description of the risks associated with our corporate structure, please refer to risks disclosed under “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure.”

3

Other Risks Related to Our Business Operationsin Mainland China

There are also substantial uncertainties regarding the interpretation and application of current and future laws, regulations and rules of mainland China regarding the status of the rights of our Cayman Islands holding company with respect to its contractual arrangements with the variable interest entities and their nominee shareholders. It is uncertain whether any new laws or regulations of mainland China relating to variable interest entitiesentity structures will be adopted or if adopted, what they would provide. If we or the variable interest entities are found to be in violation of any existing or future laws or regulations of mainland China, or fail to obtain or maintain any of the required permits or approvals, the relevant PRC regulatory authorities would have broad discretion in accordance with the applicable laws and regulations to take action in dealing with such violations or failures. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—If the relevantPRC government finds that the agreements that establish the structure for holding our ICP license do not comply with applicable laws and regulations of mainland China, or if these laws and regulations or the interpretation of existing laws and regulations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations” and “—If the PRC authorities determine that we can no longer own and operate certain of our learning centers through our subsidiaries in mainland China, we may need to restructure the ownership and operation of these learning centers (including possibly transferring these learning centers to the consolidated VIEs)variable interest entities), our business may be disrupted and we may be exposed to increased risks associated with the contractual arrangements relating to the variable interest entities.”

Our operations are primarily conducted in mainland China through (i) our mainland China subsidiaries and (ii) contractual arrangements with the variable interest entities based in mainland China, and revenues are substantially generated from mainland China. Though the PRC Foreign Investment Law does not explicitly classify contractual arrangements as a form of foreign investment, the definition of “foreign investment” thereunder is relatively wide and contains a catch-all provision which includes investments made by foreign investors through means stipulated in laws or administrative regulations or other methods prescribed by the State Council. Therefore, there is no assurance that foreign investment via contractual arrangement would not be interpreted as a type of indirect foreign investment activities in the future. If the variable interest entities were deemed as a foreign-invested enterprise under any such future laws, administrative regulations or provisions and any of our business would be included in any negative list or other form of restrictions on foreign investment, we may need to take further actions to comply with such future laws, administrative regulations or provisions. Such actions may have a material and adverse impact on our business, financial condition, result of operations and prospects. In addition, if the PRC regulatory authorities were to find our legal structure and contractual arrangements to be in violation of any laws, administrative regulations or provisions of mainland China, we are uncertain what impact of above PRC regulatory authorities’ actions would have on us and our ability to consolidate the variable interest entities in the consolidated VIEs” andfinancial statements. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—Any failure by Beijing Tarena or Beijing Tongcheng or their shareholdersDoing Business in China—Uncertainties exist with respect to perform their obligations underthe interpretation and implementation of the PRC Foreign Investment Law and its implementation regulations and how it may impact the viability of our contractual arrangements with them would have an adverse effect on our business.current corporate structure, corporate governance and business operations.”

WeOur company and the variable interest entities face various risks and uncertainties related to doing business in China. Our business operations are primarily conducted in mainland China, and we are subject to complex and evolving laws and regulations of mainland China. For example, we face risks associated with regulatory approvals on offshore offerings, anti-monopolyantimonopoly regulatory actions, and oversight on cybersecurity and data privacy, which may impact our ability to conduct certain businesses, accept foreign investments, or list on a United States or other foreign exchange.privacy. These risks could result in a material adverse change in our operations and the value of our ADSs, significantly limit or completely hinder our ability to continue to offer securities to investors, or may cause the value of such securities to significantly decline.decline or become worthless. For a detailed description of risks related to doing business in China, please refer to risks disclosed undersee “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China.”

The 6

PRC government’s significant authoritycertain administrative measures in regulating (i) our operations and its oversight and control over(ii) offerings conducted overseas by, and foreign investment in, China-based issuers, could significantly limit or completely hinder our ability to offer or continue to offer securities to investors. Implementation of industry-wide regulations, including data security or anti-monopoly related regulations, of this nature may cause the value of such securities to significantly decline or become worthless. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Our Business—Our business is subject to complex and evolving Chinese laws and regulations regarding cybersecurity, information security, privacy and data protection. Many of these laws and regulations are subject to change and uncertain interpretation, and any failure or perceived failure to comply with these laws and regulations could result in claims, changes to our business practices, negative publicity, legal proceedings, increased cost of operations, or declines in student base, or otherwise harm our business” and “Item 3. Key Information—D. Risk Factors—“—Risks Related to Doing Business in China—The approval of and filing with the CSRC or other PRC government authorities may be required in connection with our offshore offerings under the laws of mainland China, and, if required, we cannot predict whether or for how long we will be able to obtain such approval or complete such filing.”

Risks and uncertainties arising from the PRC legal system, in China, including risks and uncertainties regarding the enforcement of laws and quickly evolving rules and regulations in mainland China, could result in a material adverse change in our operations and cause the value of our ADSs.ADSs to significantly decline or become worthless. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Uncertainties in the interpretation and enforcement of laws and regulations of mainland China could limit the legal protections available to you and us” and “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—We face risks and uncertainties with respect to the licensing requirement for value-added telecommunication services, internet audio-video programs, radio or television programs production and operation, internet publication, human resources intermediary service and filing requirements for commercial franchise.us.”

4

Permissions Required from the PRC Government Authorities for Our Operations

We conduct our business primarily through our subsidiaries and the variable interest entities in mainland China. Our operations in mainland China are governed by laws and regulations of mainland China. As of the date of this annual report, our subsidiaries and the variable interest entities in mainland China have obtained the requisite licenses and permits from the PRC government authorities that are material for the business operations of our holding company, its subsidiaries, and the variable interest entities in mainland China, including, among others, an ICP licenses.license, a permit for the production and operation of radio and television programs and permits for school operation. Given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by relevantthe government authorities, we may be required to obtain additional licenses, permits, filings or approvals for the functions and services of our platform in the future. For more detailed information, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—We face risks and uncertainties with respect to the licensing requirement for value-added telecommunication services, internet audio-video programs, radio or television programs production and operation, internet publication, human resources intermediary service and filing requirements for commercial franchise.”

Furthermore, under current laws, regulations and regulatory rulesin connection with our historical issuance of securities to foreign investors, we, our mainland China we, our subsidiaries and the variable interest entities, in mainland China may be(i) are not required to fulfill filing proceduresobtain permission from the China Securities Regulatory Commission, or the CSRC, in connection with our future offering and listing in an overseas market, and may be(ii) are not required to go through a cybersecurity review by the Cyberspace Administration of China, or the CAC. As of the date of this annual report, weand (iii) have not been subjectasked to obtain permission by any filling procedures required byPRC government authority.

However, the PRC government has promulgated certain regulations and rules to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers. On February 17, 2023, the CSRC released the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies and five supporting guidelines, or, any cybersecurity review made bycollectively, the CAC. If we failFiling Rules, which took effect on March 31, 2023. According to obtain the relevant approval or complete relevant filing procedures for any future offshore offering or listing, we may face sanctions by the CSRC or other PRC regulatory authorities, which may include fines and penalties on our operationsFiling Rules, domestic companies in mainland China limitations onthat directly or indirectly offer or list their securities in an overseas market are required to file with the CSRC. In addition, an overseas listed company must also submit the filing with respect to its follow-on offerings, issuance of convertible corporate bonds and exchangeable bonds, and other equivalent offering activities, within a specific time frame requested under the Filing Rules. Therefore, we will be required to file with the CSRC for our operating privilegesoverseas offering of equity and equity linked securities in mainland China, restrictions on or prohibitionthe future within the applicable scope of the payments or remittance of dividends by our subsidiaries in mainland China, restrictions on or delays to our future financing transactions offshore, or other actions that could have a material and adverse effect on our business, financial condition, results of operations, reputation and prospects, as well as the trading price of our ADSs.Filing Rules. For more detailed information, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The approval of and filing with the CSRC or other PRC government authorities may be required in connection with our offshore offerings under the laws of mainland China, and, if required, we cannot predict whether or for how long we will be able to obtain such approval or complete such filing” and “Item 3. Key Information—D. Risk Factors—“—Risks Related to Our Business—Our business is subject to complex and evolving Chinese laws and regulations regarding cybersecurity, information security, privacy and data protection. Many of these laws and regulations are subject to change and uncertain interpretation, and any failure or perceived failure to comply with these laws and regulations could result in claims, changes to our business practices, negative publicity, legal proceedings, increased cost of operations, or declines in student base, or otherwise harm our business.”

7

Cash and Asset Flows through Our Organization

Tarena International, Inc.TCTM is a holding company with no operations of its own. We conduct our operations in mainland China primarily through our subsidiaries and the variable interest entities.entities in mainland China. As a result, although other means are available for us to obtain financing at the holding company level, Tarena International, Inc.’sTCTM’s ability to pay dividends to the shareholders and to service any debt it may incur may depend upon dividends paid by our subsidiaries in mainland China and service fees paid by the variable interest entities and their subsidiaries.entities. If any of our subsidiaries incurs debt on its own behalf in the future, the instruments governing such debt may restrict its ability to pay dividends to Tarena International, Inc.TCTM. In addition, our subsidiaries in mainland China are permitted to pay dividends to Tarena International, Inc.TCTM only out of their retained earnings, if any, as determined in accordance with accounting standards and regulations of mainland China. Further, our subsidiaries and the variable interest entities in mainland China are required to make appropriations to certain statutory reserve funds or may make appropriations to certain discretionary funds, which are not distributable as cash dividends except in the event of a solvent liquidation of the companies. For more details, see “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Holding Company Structure.”

Under the laws of mainland China, Tarena International, Inc.TCTM may provide funding to our subsidiaries in mainland China only through capital contributions or loans, and to the variable interest entities only through loans or payment for inter-groupintergroup transactions, subject to satisfaction of applicable government registration and approval requirements. Prior to December 31, 2018, Tarena International, Inc., through its intermediate holding companies, provided capital contribution of RMB448.0 million accumulatively to its subsidiaries in mainland China. Subsequently, there was no additional capital contribution from Tarena International, Inc. to its subsidiaries or variable interest entities. For the years ended December 31, 2020, 2021, 2022 and 2022, Tarena International,2023, there was no capital contribution from TCTM Kids IT Education Inc. to its subsidiaries or the variable interest entities, and TCTM did not extend any loans to, or receive any repayments from, its intermediate holding companies and subsidiaries or itsthe variable interest entities.

5

The variable interest entities may transfer cash to Tarena International, Inc.TCTM by paying service fees according to the exclusive business cooperation agreements.agreement. For the years ended December 31, 2020, 2021, 2022 and 2022,2023, no such service fees were paid by the variable interest entities. If there is any amount payable to Tarena International, Inc.TCTM under the exclusive business cooperation agreements,agreement, we intend to settle them accordingly, but do not intend to otherwise distribute earnings.

For the years ended December 31, 2020, 2021, 2022 and 2022,2023, no dividends or distributions were made to Tarena International, Inc.TCTM by ourits subsidiaries or the variable interest entities. Under laws and regulations of mainland China, our subsidiaries and the variable interest entities in mainland China are subject to certain restrictions with respect to paying dividends or otherwise transferring any of their net assets to us. Remittance of dividends by a wholly foreign-owned enterprise, or WFOE, out of mainland China is also subject to examination by the banks designated by State Administration of Foreign Exchange, or the SAFE. The amounts restricted include the paid-up capital and the statutory reserve funds of our subsidiaries in mainland China and the net assets of the variable interest entities in which we have no legal ownership, totaling RMB1,483.4 million, RMB1,523.2 million, and RMB1,558.9 million and RMB1,228.2 million (US$226.0173.0 million) as of December 31, 2020, 2021, 2022 and 2022,2023, respectively. For risks related to the fund flows of our operations in mainland China, see “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—We may rely on dividends and other distributions on equity paid by our subsidiaries in mainland China to fund any cash and financing requirements we may have, and any limitation on the ability of our subsidiaries in mainland China to make payments to us could have a material and adverse effect on our ability to conduct our business.”

For the years ended December 31, 2020, 2021, 2022 and 2022,2023, no assets other than cash were transferred through our organization.

Tarena International, Inc.TCTM has not declared or paid any cash dividends since the beginning of 2019, nor does it have any present plan to pay any cash dividends on our ordinary shares in the foreseeable future. We currently intend to retain most, if not all, of our available funds and any future earnings to operate and expand our business. See “Item 8. Financial Information—A. Consolidated Statements and Other Financial Information—Dividend Policy.” For the Cayman Islands, PRCmainland China and United States federal income tax considerations of an investment in our ADSs, see “Item 10. Additional Information—E. Taxation.”

For purposes of illustration, the following discussion reflects the hypothetical taxes that might be required to be paid within mainland China, assuming that: (i) we have taxable earnings, and (ii) we determine to pay a dividend in the future:

| | | |

|

| Tax calculation (1) |

|

Hypothetical pre-tax earnings(2) |

| 100 | % |

Tax on earnings at statutory rate of 25%(3) |

| (25) | % |

Net earnings available for distribution |

| 75 | % |

Withholding tax at standard rate of 10%(4) |

| (7.5) | % |

Net distribution to Parent/Shareholders |

| 67.5 | % |

Notes:

8

| (1) | For purposes of this example, the tax calculation has been simplified. The hypothetical book pre-tax earnings amount, not considering timing differences, is assumed to equal taxable income in mainland China. |

| (2) | Under the terms of |

| (3) | Certain of our mainland China subsidiaries qualify for |

6

| (4) | TheImplementation Regulations for PRC Enterprise Income Tax Law imposes a withholding income tax of 10% on dividends distributed by a foreign invested enterprise |

The table above has been prepared under the assumption that all profits of the variable interest entities will be distributed as fees to our subsidiaries in mainland China under tax neutral contractual arrangements. If, in the future, the accumulated earnings of the variable interest entities exceed the service fees paid to our subsidiaries in mainland China (or if the current and contemplated fee structure between the intercompany entities is determined to be non-substantive and disallowed by Chinese tax authorities), the variable interest entities could make a non-deductible transfer to our subsidiaries in mainland China for the amounts of the stranded cash in the variable interest entities. This would result in such transfer being non-deductible expenses for the variable interest entities but still taxable income for the subsidiaries in mainland China. Such a transfer and the related tax burdens would increase our after-tax loss by less than 1%approximately 28% of the pre-tax loss.profit. Our management believes that there is only a remote possibility that this scenario would happen.

Financial Information Related to the Consolidated Variable Interest Entities

Disposal of subsidiary

Gaohuiqiangxue Software (Hainan) Co., Ltd. was a wholly-owned subsidiary of the former VIE, Beijing Tarena, through the cooperation with universities and colleges in mainland China to offer joint-major degree programs and related peripheral services to colleges and students, or the Target Business, in accordance with the higher education reform policies of each province. On April 28, 2023, we entered into agreements to dispose of our controlling interest in the Target Business to a consortium led by Beijing Weike Xinneng Education Technology Ltd, or Beijing Weike Mr. Shaoyun Han is member of the investor consortium and has an interest in the disposal of the Target Business. The separatedTarget Business accounted for an insignificant portion of our revenues and assets during the recent fiscal years before the disposal, and therefore, we do not expect the disposal to have any material impact on our business operations and financial performance.

Discontinued operations

In December 2023, we entered into an equity transfer agreement to dispose of our equity interests in the professional education business to a buyer consortium led by Tarena Weishang Technology (Hainan) Co., Ltd, or the Divestiture. The Divestiture had been consummated at the end of March 2024. Upon the consummation of the Divestiture, the professional education business, including the business operated by the former VIE, had been divested, and the STEM education business operated by the former VIE had been transferred to the current VIE. The Divestiture represented a strategic shift that has a major effect on our company’s operations and financial results. As a result of the Divestiture, the professional education business has been reclassified as discontinued operations and our remaining business after the Divestiture has been reclassified as continuing operations. The following tables present the condensed consolidating schedules for our consolidated variable interest entities and other entities for the years and as of the dates indicated.

9

The following tables provide financial information depicting the financial position, cash flows and results of operations of the parent, subsidiaries, the VIEs, and Non-VIE financial informationany eliminating adjustments and consolidated totals (in thousands of RMB) as of and for the yearyears ended December 31, 2021, 2022 was as follows:and 2023.

Selected Condensed Consolidated Statements of Income, Balance Sheets, and Cash Flows Information

| | | | | | | | | | | | | | | | | | | | | | | | |

|

| For the Year Ended December 31, 2022 |

| For the Year Ended December 31, 2023 | ||||||||||||||||||||

| | | | VIE and VIE | | Non-VIE | | | | Other Inter- | | | | | | | | Non-VIE | | | | Other Inter- | | |

| | Parent | | Subsidiaries | | Subsidiaries | | VIE | | Company | | Group | | Parent | | VIEs | | Subsidiaries | | VIE | | Company | | Group |

|

| Company |

| Consolidated |

| Consolidated |

| Elimination |

| Elimination |

| Consolidation |

| Company |

| Consolidated |

| Consolidated |

| Elimination |

| Elimination |

| Consolidation |

| | RMB | ||||||||||||||||||||||

| | (In thousands) | ||||||||||||||||||||||

| | | | | | | | | | | | | ||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| | RMB | ||||||||||||||||||||||

| | (In thousands) | ||||||||||||||||||||||

Cash and cash equivalents | | 1,844 |

| 29,567 |

| 324,826 |

| — |

| — |

| 356,237 | | 5,251 |

| 2,520 |

| 212,918 |

| — |

| — |

| 220,689 |

Inter-Group balances due from the VIEs and their subsidiaries/Non-VIE | | 437,987 |

| 106,922 |

| 342,338 |

| (106,922) |

| (780,325) |

| — | ||||||||||||

Inter-Group balances due from the VIEs/Non-VIE subsidiaries | | 380,470 |

| 104,642 |

| 406,637 |

| (11,259) |

| (880,490) |

| — | ||||||||||||

Other current assets | | 550 |

| 10,606 |

| 310,183 |

| (23) |

| (10,000) |

| 311,316 | | 225 |

| 62,550 |

| 22,344 |

| — |

| (20,815) |

| 64,304 |

Equity method investments | | 140,025 |

| — |

| — |

| — |

| (140,025) |

| — | | 142,399 |

| — |

| — |

| — |

| (142,399) |

| — |

Investment deficit in the VIEs and their subsidiaries and Non-VIE | | (1,714,999) |

| — |

| — |

| — |

| 1,714,999 |

| — | ||||||||||||

Non-current assets | | — |

| 39,394 |

| 630,553 |

| — |

| — |

| 669,947 | ||||||||||||

Investment deficit in the VIEs and Non-VIE subsidiaries | | (1,702,776) |

| — |

| — |

| — |

| 1,702,776 |

| — | ||||||||||||

Other non-current assets | | — |

| 46,371 |

| 411,276 |

| — |

| — |

| 457,647 | ||||||||||||

Total assets of discontinued operations held for sale | | — | | 36,779 | | 249,639 | | — | | (10,815) | | 275,603 | ||||||||||||

Total Assets | | (1,134,593) |

| 186,489 |

| 1,607,900 |

| (106,945) |

| 784,649 |

| 1,337,500 | | (1,174,431) |

| 252,862 |

| 1,302,814 |

| (11,259) |

| 648,257 |

| 1,018,243 |

Inter-Group balances due to the VIEs and their subsidiaries/Non-VIE | | 334,909 |

| 7,631 |

| 544,909 |

| (7,631) |

| (879,818) |

| — | ||||||||||||

Inter-Group balances due to the VIEs/Non-VIE subsidiaries | | 319,197 |

| 23,676 |

| 130,159 |

| (11,259) |

| (461,773) |

| — | ||||||||||||

Other current liabilities | | 30,392 |

| 206,458 |

| 2,420,096 |

| — |

| — |

| 2,656,946 | | 4,155 |

| 152,969 |

| 1,712,121 |

| — |

| (18,680) |

| 1,850,565 |

Non-current liabilities | | — |

| 4,433 |

| 182,802 |

| — |

| — |

| 187,235 | | — |

| 4,252 |

| 103,985 |

| — |

| — |

| 108,237 |

Total liabilities of discontinued operations held for sale | | — | | 100,392 | | 471,214 | | — | | (10,815) | | 560,791 | ||||||||||||

Total liabilities | | 365,301 |

| 218,522 |

| 3,147,807 |

| (7,631) |

| (879,818) |

| 2,844,181 | | 323,352 |

| 281,289 |

| 2,417,479 |

| (11,259) |

| (491,268) |

| 2,519,593 |

Equity | | (1,499,894) |

| (32,033) |

| (1,539,907) |

| 7,065 |

| 1,558,088 |

| (1,506,681) | | (1,497,783) |

| (28,427) |

| (1,114,665) |

| (2,060) |

| 1,141,585 |

| (1,501,350) |

Net Revenue | | — |

| 158,347 |

| 2,326,221 |

| — |

| (16,494) |

| 2,468,074 | ||||||||||||

Net profit/(loss) | | 83,520 |

| 1,255 |

| 482 |

| 17,064 |

| (17,088) |

| 85,233 | ||||||||||||

Net revenues from continuing operations | | — |

| 90,661 |

| 1,284,531 |

| — |

| — |

| 1,375,192 | ||||||||||||

Net income/(loss) | | 8,928 |

| 3,606 |

| (6,530) |

| 7,939 |

| (3,589) |

| 10,354 | ||||||||||||

Net cash provided by/(used in) operating activities | | (5,699) |

| 7,722 |

| (29,753) |

| 17,088 |

| (16,886) |

| (27,528) | | 4,902 |

| (17,817) |

| 317,788 |

| (3,220) |

| (420,588) |

| (118,935) |

Net cash provided by/(used in) investing activities | | — |

| 19,975 |

| (37,684) |

| (5,000) |

| — |

| (22,709) | ||||||||||||

Net cash provided by/(used in) financing activities | | (16,996) |

| 5,762 |

| 4,331 |

| 14,238 |

| (9,440) |

| (2,105) | ||||||||||||

Net cash provided by investing activities | | — |

| — |

| 72,048 |

| — |

| — |

| 72,048 | ||||||||||||

Net cash (used in)/provided by financing activities | | (2,201) |

| (7,192) |

| (456,123) |

| 7,192 |

| 422,543 |

| (35,781) | ||||||||||||

710

| | | | | | | | | | | | | | | | | | | | | | | | |

|

| For the Year Ended December 31, 2021 |

| For the Year Ended December 31, 2022 | ||||||||||||||||||||

| | | | VIE and VIE | | Non-VIE | | | | Other Inter- | | | | | | | | Non-VIE | | | | Other Inter- | | |

| | Parent | | Subsidiaries | | Subsidiaries | | VIE | | Company | | Group | | Parent | | VIEs | | Subsidiaries | | VIE | | Company | | Group |

|

| Company |

| Consolidated | | Consolidated |

| Elimination |

| Elimination |

| Consolidation |

| Company |

| Consolidated |

| Consolidated |

| Elimination |

| Elimination |

| Consolidation |

| | RMB | ||||||||||||||||||||||

| | (In thousands) | ||||||||||||||||||||||

| | | | | | | | | | | | | ||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| | RMB | ||||||||||||||||||||||

| | (In thousands) | ||||||||||||||||||||||

Cash and cash equivalents | | 23,506 |

| 8,204 |

| 392,056 |

| — |

| — |

| 423,766 | | 1,844 |

| 16,031 |

| 180,654 |

| — |

| — |

| 198,529 |

Inter-Group balances due from the VIEs and their subsidiaries/Non-VIE | | 407,795 |

| 141,104 |

| 365,293 |

| (141,104) |

| (773,088) |

| — | ||||||||||||

Inter-Group balances due from the VIEs/Non-VIE subsidiaries | | 437,987 |

| 64,604 |

| 280,273 |

| (50,780) |

| (732,084) |

| — | ||||||||||||

Other current assets | | 24 |

| 27,439 |

| 186,523 |

| — |

| (18,420) |

| 195,566 | | 550 |

| 1,191 |

| 47,030 |

| (23) |

| (10,000) |

| 38,748 |

Equity method investments | | 128,185 |

| — |

| — |

| — |

| (128,185) |

| — | | 140,025 |

| — |

| — |

| — |

| (140,025) |

| — |

Investment deficit in the VIEs and their subsidiaries and Non-VIE | | (1,828,408) |

| — |

| — |

| — |

| 1,828,408 |

| — | ||||||||||||

Investment deficit in the VIEs and Non-VIE subsidiaries | | (1,714,999) |

| — |

| — |

| — |

| 1,714,999 |

| — | ||||||||||||

Other non-current assets | | — |

| 44,846 |

| 977,604 |

| — |

| — |

| 1,022,450 | | — |

| 37,704 |

| 445,457 |

| — |

| — |

| 483,161 |

Total assets of discontinued operations held for sale | | — | | 66,959 | | 654,486 | | (56,142) | | (48,241) | | 617,062 | ||||||||||||

Total Assets | | (1,268,898) |

| 221,593 |

| 1,921,476 |

| (141,104) |

| 908,715 |

| 1,641,782 | | (1,134,593) |

| 186,489 |

| 1,607,900 |

| (106,945) |

| 784,649 |

| 1,337,500 |

Inter-Group balances due to the VIEs and their subsidiaries/Non-VIE | | 309,241 |

| 56,052 |

| 548,899 |

| (56,052) |

| (858,140) |

| — | ||||||||||||

Inter-Group balances due to the VIEs/Non-VIE subsidiaries | | 334,909 |

| (48,511) |

| 598,854 |

| (7,631) |

| (877,621) |

| — | ||||||||||||

Other current liabilities | | 5,781 |

| 195,882 |

| 2,756,383 |

| (17,960) |

| — |

| 2,940,086 | | 30,392 |

| 134,191 |

| 1,755,328 |

| — |

| — |

| 1,919,911 |

Non-current liabilities | | — |

| 6,209 |

| 287,907 |

| — |

| — |

| 294,116 | | — |

| 4,176 |

| 105,685 |

| — |

| — |

| 109,861 |

Total liabilities of discontinued operations held for sale | | — | | 128,666 | | 687,940 | | — | | (2,197) | | 814,409 | ||||||||||||

Total liabilities | | 315,022 |

| 258,143 |

| 3,593,189 |

| (74,012) |

| (858,140) |

| 3,234,202 | | 365,301 |

| 218,522 |

| 3,147,807 |

| (7,631) |

| (879,818) |

| 2,844,181 |

Equity | | (1,583,920) |

| (36,550) |

| (1,671,713) |

| 12,960 |

| 1,686,803 |

| (1,592,420) | | (1,499,894) |

| (32,033) |

| (1,539,907) |

| 7,065 |

| 1,558,088 |

| (1,506,681) |

Net Revenue | | — |

| 140,541 |

| 2,262,538 |

| — |

| (16,559) |

| 2,386,520 | ||||||||||||

Net profit/(loss) | | (474,547) |

| (39,072) |

| 37,839 |

| 16,559 |

| (16,559) |

| (475,780) | ||||||||||||

Net revenues from continuing operations | | — |

| 40,755 |

| 1,360,680 |

| — |

| (1,591) |

| 1,399,844 | ||||||||||||

Net income/(loss) | | 83,520 |

| 1,255 |

| 482 |

| 17,064 |

| (17,088) |

| 85,233 | ||||||||||||

Net cash provided by/(used in) operating activities | | 14,458 |

| 10,308 |

| (16,156) |

| (161) |

| 161 |

| 8,610 | | (5,699) |

| 7,722 |

| (29,753) |

| 17,088 |

| (16,886) |

| (27,528) |

Net cash provided in investing activities | | — |

| — |

| 33,693 |

| — |

| — |

| 33,693 | ||||||||||||

Net cash provided by/(used in) financing activities | | 3,947 |

| (3,437) |

| 22,727 |

| 3,437 |

| (3,437) |

| 23,237 | ||||||||||||

Net cash provided by/(used in) investing activities | | — |

| 19,975 |

| (37,684) |

| (5,000) |

| — |

| (22,709) | ||||||||||||

Net cash (used in)/provided by financing activities | | (16,996) |

| 5,762 |

| 4,331 |

| 14,238 |

| (9,440) |

| (2,105) | ||||||||||||

811

| | | | | | | | | | | | | | | | | | | | | | | | |

|

| For the Year Ended December 31, 2020 |

| For the Year Ended December 31, 2021 | ||||||||||||||||||||

| | | | VIEs and VIE | | Non-VIE | | | | Other Inter- | | | | | | | | Non-VIE | | | | Other Inter- | | |

| | Parent | | Subsidiaries | | Subsidiaries | | VIE | | Company | | Group | | Parent | | VIEs | | Subsidiaries | | VIE | | Company | | Group |

|

| Company |

| Consolidated |

| Consolidated |

| Elimination |

| Elimination |

| Consolidation |

| Company |

| Consolidated |

| Consolidated |

| Elimination |

| Elimination |

| Consolidation |

| | RMB | ||||||||||||||||||||||

| | (In thousands) | ||||||||||||||||||||||

| | | | | | | | | | | | | ||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| | RMB | ||||||||||||||||||||||

| | (In thousands) | ||||||||||||||||||||||

Cash and cash equivalents | | 3,793 |

| 1,332 |

| 315,054 |

| — |

| — |

| 320,179 | | 23,506 |

| 1,226 |

| 98,085 |

| — |

| — |

| 122,817 |

Inter-Group balances due from the VIEs and their subsidiaries/Non-VIE | | 410,910 |

| 113,021 |

| 330,187 |

| (113,021) |

| (741,097) |

| — | ||||||||||||

Inter-Group balances due from the VIEs/Non-VIE subsidiaries | | 407,795 |

| 39,712 |

| 130,130 |

| (39,712) |

| (537,925) |

| — | ||||||||||||

Other current assets | | 699 |

| 4,480 |

| 219,187 |

| (161) |

| (8,131) |

| 216,074 | | 24 |

| 14,175 |

| 47,605 |

| — |

| (18,421) |

| 43,383 |

Equity method investments | | 131,184 |

| — |

| — |

| — |

| (131,184) |

| — | | 128,185 |

| — |

| — |

| — |

| (128,185) |

| — |

Investment deficit in the VIEs and their subsidiaries and Non-VIE | | (1,372,593) |

| — |

| — |

| — |

| 1,372,593 |

| — | ||||||||||||

Investment deficit in the VIEs and Non-VIE subsidiaries | | (1,828,408) |

| — |

| — |

| — |

| 1,828,408 |

| — | ||||||||||||

Other non-current assets | | — | | 56,011 | | 1,366,985 | | — | | — | | 1,422,996 | | — | | 36,700 | | 575,062 | | — | | — | | 611,762 |

Total assets of discontinued operations held for sale | | — | | 129,780 | | 1,070,594 | | (101,392) | | (235,162) | | 863,820 | ||||||||||||

Total Assets | | (826,007) | | 174,844 | | 2,231,413 | | (113,182) | | 492,181 | | 1,959,249 | | (1,268,898) | | 221,593 | | 1,921,476 | | (141,104) | | 908,715 | | 1,641,782 |

Inter-Group balances due to the VIEs and their subsidiaries/Non-VIE | | 298,782 | | 31,405 | | 523,932 | | (31,405) | | (822,714) | | — | ||||||||||||

Inter-Group balances due to the VIEs /Non-VIE subsidiaries | | 309,241 | | 56,052 | | 548,898 | | (56,051) | | (858,140) | | — | ||||||||||||

Other current liabilities | | 7,213 | | 156,137 | | 2,514,067 | | (8,131) | | (161) | | 2,669,125 | | 5,781 | | 50,068 | | 1,970,157 | | (17,961) | | — | | 2,008,045 |

Non-current liabilities | | — | | 1,791 | | 427,602 | | — | | — | | 429,393 | | — | | 2,126 | | 195,111 | | — | | — | | 197,237 |

Total liabilities of discontinued operations held for sale | | — | | 149,897 | | 879,023 | | — | | — | | 1,028,920 | ||||||||||||

Total liabilities | | 305,995 | | 189,333 | | 3,465,601 | | (39,536) | | (822,875) | | 3,098,518 | | 315,022 | | 258,143 | | 3,593,189 | | (74,012) | | (858,140) | | 3,234,202 |

Equity | | (1,132,002) | | (14,489) | | (1,234,188) | | 3,131 | | 1,238,279 | | (1,139,269) | | (1,583,920) | | (36,550) | | (1,671,713) | | 12,960 | | 1,686,803 | | (1,592,420) |

Net Revenue | | — | | 127,043 | | 1,780,038 | | (156) | | (9,042) | | 1,897,883 | ||||||||||||

Net profit/(loss) | | (766,643) | | 32,869 | | (37,419) | | (34,515) | | 34,515 | | (771,193) | ||||||||||||

Net revenues from continuing operations | | — | | 16,673 | | 1,219,600 | | — | | — | | 1,236,273 | ||||||||||||

Net income/(loss) | | (474,547) | | (39,072) | | 37,839 | | 16,559 | | (16,559) | | (475,780) | ||||||||||||

Net cash provided by/(used in) operating activities | | (8,010) | | 112,106 | | 1,034,589 | | (7,970) | | (1,239,536) | | (108,821) | | 14,458 | | 10,308 | | (16,156) | | (161) | | 161 | | 8,610 |

Net cash provided in investing activities | | — | | — | | (657) | | — | | — | | (657) | ||||||||||||

Net cash provided by investing activities | | — | | — | | 33,693 | | — | | — | | 33,693 | ||||||||||||

Net cash provided by/(used in) financing activities | | 3,354 | | (110,985) | | (1,155,394) | | 120,274 | | 1,074,452 | | (68,299) | | 3,947 | | (3,437) | | 22,727 | | 3,437 | | (3,437) | | 23,237 |

912

Selected Consolidated Financial DataA.[Reserved]

The following selected consolidated statements of comprehensive income data for the years ended December 31, 2020, 2021, 2022 and 2022,2023, and the selected consolidated balance sheet data as of December 31, 20212022 and 2022,2023, have been derived from our audited consolidated financial statements included elsewhere in this annual report. The following selected consolidated statements of comprehensive income data for the years ended December 31, 2018 and 2019, and the selected consolidated balance sheet data as of December 31, 2018, 20192021 is based on the unaudited and 2020 have beenunreviewed financial data derived from our audited consolidated financial statementsmanagement accounts, which are not included in this annual report.were adjusted to retrospectively present discontinued operations. Our historical results for any period are not necessarily indicative of results to be expected for any future period. The selected consolidated financial data should be read in conjunction with, and are qualified in their entirety by reference to, our audited consolidated financial statements and related notes and “Item 5. Operating and Financial Review and Prospects” below. Our consolidated financial statements are prepared and presented in accordance with generally accepted accounting principles in the United States, or U.S. GAAP.

| | | | | | | | | | | | | | | | | | | | |

| | For the Year ended December 31, | | For the Year ended December 31, | ||||||||||||||||

| | 2018 | | 2019 | | 2020 | | 2021 | | 2022 | | 2022 | | 2021 | | 2022 | | 2023 | | 2023 |

|

| RMB |

| RMB |

| RMB |

| RMB |

| RMB |

| USD |

| RMB |

| RMB |

| RMB |

| USD |

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| | (in thousands, except for share and per share) | | (in thousands, except for share and per share) | ||||||||||||||||

Selected Consolidated Statements of Comprehensive Income Data: | | | | | | | | | | | | | | | | | | | | |

Net revenues | | 2,085,371 |

| 2,051,354 |

| 1,897,883 |

| 2,386,520 |

| 2,468,074 |

| 357,837 |

| 1,236,273 |

| 1,399,844 |

| 1,375,192 |

| 193,692 |

Cost of revenues(1) | | (918,549) |

| (1,173,834) |

| (1,066,842) |

| (1,201,419) |

| (1,056,043) |

| (153,112) |

| (795,669) |

| (728,416) |

| (750,840) |

| (105,754) |

Gross profit | | 1,166,822 |

| 877,520 |

| 831,041 |

| 1,185,101 |

| 1,412,031 |

| 204,725 |

| 440,604 |

| 671,428 |

| 624,352 |

| 87,938 |

Selling and marketing expenses(1) | | (1,047,632) |

| (1,119,698) |

| (906,337) |

| (878,130) |

| (642,937) |

| (93,217) |

| (437,487) |

| (280,093) |

| (268,399) |

| (37,803) |

General and administrative expenses(1) | | (546,568) |

| (723,306) |

| (630,618) |

| (569,985) |

| (604,028) |

| (87,576) |

| (359,453) |

| (397,440) |

| (330,848) |

| (46,599) |

Research and development expenses(1) | | (167,254) |

| (132,672) |

| (100,466) |

| (106,098) |

| (72,028) |

| (10,443) |

| (40,311) |

| (20,248) |

| (11,654) |

| (1,641) |

Operating (loss) income | | (594,632) |

| (1,098,156) |

| (806,380) |

| (369,112) |

| 93,038 |

| 13,489 |

| (396,647) |

| (26,353) |

| 13,451 |

| 1,895 |

Interest income (expenses) | | 26,200 |

| 15,859 |

| (199) |

| 2,335 |

| 2,700 |

| 391 | ||||||||

Other (loss) income | | (33,583) |

| 246 |

| 5,201 |

| 5,572 |

| 11,283 |

| 1,636 | ||||||||

Foreign currency exchange gains (loss) | | 4,951 |

| 1,614 |

| (4,849) |

| (518) |

| (954) |

| (138) | ||||||||

Interest income, net |

| 2,611 |

| 1,962 |

| 1,089 |

| 153 | ||||||||||||

Other income, net |

| 1,466 |

| 8,150 |

| 723 |

| 102 | ||||||||||||

Foreign currency exchange loss |

| (267) |

| (325) |

| (901) |

| (127) | ||||||||||||

(Loss) income before income taxes | | (597,064) |

| (1,080,437) |

| (806,227) |

| (361,723) |

| 106,067 |

| 15,378 |

| (392,837) |

| (16,566) |

| 14,362 |

| 2,023 |

Net (loss) income from continuing operations | | (509,288) | | (2,062) | | 22,334 | | 3,146 | ||||||||||||

Net income (loss) from discontinued operations | | 33,508 | | 87,295 | | (11,980) | | (1,687) | ||||||||||||

Net (loss) income | | (592,199) |

| (1,038,878) |

| (771,193) |

| (475,780) |

| 85,233 |

| 12,357 |

| (475,780) |

| 85,233 |

| 10,354 |

| 1,459 |

Net (loss) income attributable to Class A and Class B ordinary shareholders | | (590,174) |

| (1,036,086) |

| (766,643) |

| (474,547) |

| 83,520 |

| 12,109 |

| (474,547) |

| 83,520 |

| 8,926 |

| 1,258 |

Cash dividend declared per share(2) | | 0.76 |

| — |

| — |

| — |

| — |

| — | ||||||||

Weighted average number of class A and class B ordinary shares outstanding(3): | | |

| |

| |

| |

| |

| | ||||||||

Weighted average number of class A and class B ordinary shares outstanding(2): |

| |

| |

| |

| | ||||||||||||

Basic | | 54,929,910 | | 53,386,075 | | 54,341,213 | | 56,260,925 | | 54,657,222 | | 54,657,222 | | 56,260,925 | | 54,657,222 | | 53,873,945 | | 53,873,945 |

Diluted | | 54,929,910 |

| 53,386,075 |

| 54,341,213 |

| 56,260,925 |

| 57,730,672 |

| 57,730,672 |

| 57,630,365 |

| 57,730,672 |

| 55,334,574 |

| 55,334,574 |

Net income/(loss) per ADS | | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

Basic | | (53.72) | | (97.04) | | (70.54) | | (42.17) | | 7.64 | | 1.11 | ||||||||

Diluted | | (53.72) |

| (97.04) |

| (70.54) |

| (42.17) |

| 7.23 |

| 1.05 | ||||||||

Basic (loss) income per ADS attributable to ordinary shareholder from continuing operations | | (45.15) | | (0.35) | | 1.94 | | 0.27 | ||||||||||||

Diluted (loss) income per ADS attributable to ordinary shareholder from continuing operations |

| (45.15) |

| (0.35) |

| 1.89 |

| 0.27 | ||||||||||||

Basic income (loss) per ADS attributable to ordinary shareholder from discontinued operations | | 2.98 | | 7.99 | | (1.11) | | (0.16) | ||||||||||||

Diluted income (loss) per ADS attributable to ordinary shareholder from discontinued operations | | 2.91 | | 7.56 | | (1.11) | | (0.16) | ||||||||||||

10

Notes:

| (1) | Share-based compensation expenses were allocated in cost of revenues and operating expenses as follows: |

| | | | | | | | | | | | |

| | For the Year ended December 31, | ||||||||||

| | 2018 | | 2019 | | 2020 | | 2021 | | 2022 | | 2022 |

|

| RMB |

| RMB |

| RMB |

| RMB |

| RMB |

| USD |

| | (in thousands) | ||||||||||

Cost of revenues |

| 2,265 |

| 983 |

| 379 |

| 70 |

| 325 | | 47 |

Sales and marketing expenses |

| 8,866 |

| 6,502 |

| 1,842 |

| 2,785 |

| 1,388 |

| 201 |

General and administrative expenses |

| 84,645 |

| 36,719 |

| 26,242 |

| 14,840 |

| 12,296 |

| 1,783 |

Research and development expenses |

| 28,477 |

| 14,968 |

| 7,783 |

| 1,408 |

| 2,528 |

| 367 |

13

| | | | | | | | |

| | For the Year ended December 31, | ||||||

| | 2021 | | 2022 | | 2023 | | 2023 |

|

| RMB |

| RMB |

| RMB |

| USD |

| | (in thousands) | ||||||

Cost of revenues |

| 18 |

| 244 |

| 19 | | 3 |

Sales and marketing expenses |

| 206 |

| 227 |

| 24 |

| 3 |

General and administrative expenses |

| 13,514 |

| 10,179 |

| 2,551 |

| 359 |

Research and development expenses |

| 375 |

| 734 |

| 149 |

| 21 |

| (2) |

| The weighted average number of ordinary shares represents the sum of the weighted average number of Class A and Class B ordinary shares. See Note |

| Each ADS represents five Class A ordinary shares. The weighted average number of ADS and earnings per ADS have been retrospectively adjusted to reflect the ADS ratio change from one ADS representing one Class A ordinary share to one ADS representing five Class A shares, which became effective on December 23, 2021. |

The following table presents our selected consolidated balance sheet data as of the dates indicated.

| | | | | | | | | | | | | | | | | | | | |

| | As of December 31, | | As of December 31, | ||||||||||||||||

| | 2018 | | 2019 | | 2020 | | 2021 | | 2022 | | 2022 | | 2021 | | 2022 | | 2023 | | 2023 |

|

| RMB |

| RMB |

| RMB |

| RMB |

| RMB |

| USD |

| RMB |

| RMB |

| RMB |

| USD |

| | (in thousands) | ||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| | (in thousands) | ||||||||||||||||||

Selected Consolidated Balance Sheet Data: | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

|

Cash and cash equivalents |

| 530,984 |

| 537,701 |

| 320,179 |

| 423,766 |

| 356,237 |

| 51,650 |

| 122,817 |

| 198,529 |

| 220,689 |

| 31,083 |

Time deposits, including non-current portion |

| 159,102 |

| 83,487 |

| 6,257 |

| 6,380 |

| 6,505 |

| 943 | ||||||||

Time deposits, including noncurrent portion |

| 102 |

| 104 |

| 300 |

| 42 | ||||||||||||

Restricted cash |

| 14,700 |

| — |

| 38,369 |

| 255 |

| 17,730 |

| 2,571 |

| — |

| — |

| 6,575 |

| 926 |

Accounts receivable, net of allowance for doubtful accounts |

| 39,901 |

| 31,442 |

| 32,790 |

| 48,458 |

| 68,733 |

| 9,965 | ||||||||

Current assets held for sale associated with discontinued operations | | 453,132 | | 430,276 | | 275,603 | | 38,818 | ||||||||||||

Property and equipment, net |

| 626,068 |

| 576,633 |

| 464,490 |

| 299,441 |

| 122,834 |

| 17,809 |

| 118,005 |

| 77,996 |

| 66,064 |

| 9,305 |

Long-term investments |

| 59,651 |

| 67,773 |

| 67,592 |

| 46,449 |

| 46,183 |

| 6,696 |

| 43,569 |

| 46,183 |

| 41,860 |

| 5,896 |

Non-current assets held for sale associated with discontinued operations | | 410,688 | | 186,786 | | — | | — | ||||||||||||

Total assets |

| 1,878,047 |

| 2,512,020 |

| 1,959,249 |

| 1,641,782 |

| 1,337,500 |

| 193,919 |

| 1,641,782 |

| 1,337,500 |

| 1,018,243 |

| 143,417 |

Deferred revenue, including non-current portion |

| 830,019 |

| 1,585,970 |

| 1,998,198 |

| 2,024,852 |

| 1,702,661 |

| 246,862 | ||||||||

Deferred revenue |

| 1,424,216 |

| 1,314,877 |

| 1,210,536 |

| 170,500 | ||||||||||||

Total liabilities |

| 1,306,404 |

| 2,915,084 |

| 3,098,518 |

| 3,234,202 |

| 2,844,181 |

| 412,367 |

| 3,234,202 |

| 2,844,181 |

| 2,519,593 |

| 354,878 |

Total equity (deficit) attributable to the shareholders of Tarena International, Inc. |

| 572,618 |

| (400,047) |

| (1,132,002) |

| (1,583,920) |

| (1,499,894) |

| (217,464) | ||||||||

Total equity (deficit) |

| 571,643 |

| (403,064) |

| (1,139,269) |

| (1,592,420) |

| (1,506,681) |

| (218,448) | ||||||||

Total deficit attributable to the shareholders of TCTM Kids IT Education Inc. |

| (1,583,920) |

| (1,499,894) |

| (1,497,783) |

| (210,959) | ||||||||||||

Total deficit |

| (1,592,420) |

| (1,506,681) |

| (1,501,350) |

| (211,461) | ||||||||||||

| B. | Capitalization and Indebtedness |

Not Applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not Applicable.

11

| D. | Risk Factors |

Summary of Risk Factors

An investment in our ADSs involves significant risks. Below is a summary of material risks we face, organized under relevant headings. With respect to the legal risks associated with being based in and having operations in mainland China, the laws, regulations and the discretion of mainland China governmental authorities discussed in this annual report are expected to apply to mainland China entities and businesses, rather than entities or businesses in Hong Kong which operate under a different set of laws from mainland China. These risks are discussed more fully in Item 3. Key Information—D. Risk Factors.

14

Risks Related to Our Business

· | Uncertainties and risks accompany our strategy to divest our professional education business. Our strategy to divest is largely based on our management’s assessment of our core strengths, business objectives, resource allocation, and likelihood of success for different business models. However, our judgment could be inaccurate, and we may not achieve the desired strategic and financial benefits from the divestiture transaction. |

· | We incurred net losses from |

· | We rely on IT-focused supplementary STEM education programs for a substantial part of our net revenues upon the consummation of the Divestiture, and a decrease in the popularity of IT-focused supplementary STEM education courses, such as childhood & adolescent robotics programming and computer programming courses, would have a material adverse effect on our business and results of operations. |