UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

or

or | |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 31, |

or

or | |

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

or

or | |

¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report______________ | |

| |

For the transition period from ___________________ to ___________________ |

Commission File Number 0-15688

CORAL GOLD RESOURCES LTD. |

(Exact name of Registrant as specified in its charter) |

Not Applicable

(Translation of Registrant'sRegistrant’s name into English)

British Columbia, Canada

(Jurisdiction of incorporation or organization)

570 Granville Street, Suite 900, Vancouver, British Columbia V6C 3P1, Canada

(Address of principal executive offices)

David Wolfin, Tel: 604 682-3701, Email: dwolfin@coralgold.com

570 Granville Street, Suite 900, Vancouver, British Columbia V6C 3P1, Canada

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Not Applicable | Not Applicable | |

Title of Each Class | Name of each exchange on which registered |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

Common Shares, without Par Value

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

Not Applicable

(Title of Class)

Indicate the number of outstanding shares of each of the issuer'sissuer’s classes of capital or common stock as of the close of the period covered by the annual report.

There were 47,825,33748,043,337 common shares, without par value, issued and outstanding as of January 31, 2016.2019.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [Not applicable to the registrant]¨x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer.filer, or an emerging growth company. See definition of “large accelerated filer”, "accelerated filer,” and large accelerated filer""emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated File | ¨ |

| |

Non-Accelerated Filer | x | ||

Accelerated Filer | ¨ | Emerging Growth Company | ¨ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP¨ | International Financial Reporting Standards as issued by the International Accounting Standards Boardx | Other¨ |

If "Other"“Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ¨ No ¨

Item |

| ||||

Page | |||||

|

| ||||

|

| ||||

|

| ||||

3 | |||||

| |||||

EXPLANATORY NOTE REGARDING PRESENTATION OF FINANCIAL INFORMATION |

| ||||

|

| ||||

|

| 4 | |||

| 4 | ||||

| |||||

| |||||

| |||||

| |||||

| |||||

|

| ||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

|

| 37 | |||

| |||||

| |||||

| |||||

| |||||

Material Modifications to the Rights of Security Holders and Use of Proceeds |

| ||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

Purchases of Equity Securities by the Issuer and Affiliated Purchasers |

| ||||

|

|

| |||

|

|

| |||

|

|

| |||

|

| 40 | |||

40 | |||||

40 | |||||

40 | |||||

41 | |||||

41 | |||||

42 | |||||

| 2 | ||||

|

|

| ||

|

|

| ||

|

|

|

Nomenclature

In this Annual Report on Form 20-F, which we refer to as the "Annual Report"“Annual Report”, except as otherwise indicated or as the context otherwise requires, the "Company"terms “Company”, "Coral"“we”, "we", "our"“our” or "us"“us” refers to Coral Gold Resources Ltd. and its subsidiaries.

You should rely only on the information contained in this Annual Report. We were organized under the Company Act of the Province of British Columbia, Canada on January 22, 1981 under the name of Carol Energy Corporation, which name was changedhave not authorized anyone to Coral Energy Corporation on March 3, 1982, and to Coral Gold Corp. on September 9, 1987. On September 14, 2004, we changed our name to Coral Gold Resources Ltd. in conjunctionprovide you with a 10 to 1 share consolidation and transitioned to the British Columbia Business Corporations Act on July 15, 2004. The principal executive office of the Companyinformation that is located at 570 Granville Street, Suite 900, Vancouver, British Columbia, V6C 3P1, and its telephone number is 604-682-3701.

different. The information in this Annual Report may only be accurate on the date of this Annual Report or on or as at any other date provided with respect to specific information herein.information.

Unless otherwise indicated in this Annual Report, all references to "Canadian Dollars"“Canadian Dollars”, "CDN$"“CDN$”, "dollars"“dollars” or "$"“$” are to the lawful currency of Canada and all references to "U.S. Dollars"“U.S. Dollars”, or "US$"“US$” are to the lawful currency of the United States.

Certain statements in this Annual Report, including those appearing under Item 5, constitute "forward-looking statements"“forward-looking statements”, including, without limitation, those concerning the economic outlook for the mining industry, expectations regarding mineral prices, potential production, cash costs and other operating results, growth prospects and outlook of the Company'sCompany’s operations, individually or in the aggregate, including the completion and commencement of commercial operations of certain of the Company'sCompany’s exploration and production projects, the Company'sCompany’s liquidity and capital resources and capital expenditures, the outcome and consequences of any potential or pending litigation or regulatory proceedings, and the Company'sCompany’s plan to conduct drilling operations. Additionally, forward-looking statements are generally identifiable by the terminology used such as "plans"“plans”, "expects"“expects”, "estimates"“estimates”, "budgets"“budgets”, "intends"“intends”, "anticipates"“anticipates”, "believes"“believes”, "projects"“projects”, "indicates"“indicates”, "targets"“targets”, "objective"“objective”, "could"“could”, "may"“may”, or other similar words.

The forward-looking statements are subject to known and unknown risks and uncertainties and other factors that may cause actual results, levels of activity and achievements to differ materially from those expressed or implied by such statements. Such factors include, among others: market prices for metals; the results of exploration and development drilling and related activities; economic conditions in the countries and provinces in which we carry on business, especially economic slowdown; actions by governmental authorities including increases in taxes, changes in environmental and other regulations, and renegotiations of contracts; political uncertainty, including actions by insurgent groups or other conflict; the negotiation and closing of material contracts; and the other factors discussed in Item 3 Key Information – "Risk Factors"“Risk Factors”, and in other documents that we file with the SEC. The impact of any one factor on a particular forward-looking statement is not determinable with certainty as such factors are interdependent upon other factors; our course of action would depend upon our assessment of the future considering all information then available. In that regard, any statements as to future production levels, if any; capital expenditures; the allocation of capital expenditures to exploration and development activities; sources of funding of our capital program; drilling; expenditures and allowances relating to environmental matters; anticipated dates by which certain areas will be developed or will come on-stream; expected finding and development costs; future production rates; ultimate recoverability of reserves; dates by which transactions are expected to close; cash flows; uses of cash flows; collectability of receivables; availability of trade credit; expected operating costs; expenditures and allowances relating to environmental matters; debt levels; and changes in any of the foregoing are forward-looking statements, and theret There can be no assurances that the expectations conveyed by such forward-looking statements will, in fact, be realized.

Although we believe that the expectations conveyed by the forward-looking statements are reasonable based on information available to us on the date such forward-looking statements were made, no assurances can be given as to future results, levels of activity, achievements or financial condition.

Readers should not place undue reliance on any forward-looking statement and should recognize that the statements are predictions of future results, which may not occur as anticipated. Actual results could differ materially from those anticipated in the forward-looking statements and from historical results, due to the risks and uncertainties described above, as well as others not now anticipated. The foregoing statements are not exclusive and further information concerning the Company, including factors that could materially affect its financial results, may emerge from time to time. The Company does not intend to update forward-looking statements to reflect actual results or changes in factors or assumptions affecting such forward-looking statements.

| 3 |

| Table of Contents |

In Canada, an issuer is required to provide technical information with respect to mineralization, including reserves and resources, if any, on its mineral exploration properties in accordance with Canadian requirements, which differ significantly from the requirements of the Securities and Exchange Commission (the "SEC"“SEC”) applicable to registration statements and reports filed by United States companies pursuant to the United States Securities Act of 1933, as amended (the "Securities Act"“Securities Act”), or the United States Securities Exchange Act of 1934, as amended (the "Exchange Act"“Exchange Act”). As such, information contained in this annual reportAnnual Report concerning descriptions of mineralization under Canadian standards may not be comparable to similar information made public by United States companies subject to the reporting and disclosure requirements of the SEC. In particular, this annual report on Form 20-F includes the terms "mineral resource," "measured mineral resource," "indicated mineral resource" and "inferred mineral resource". Investors are advised that these terms are defined under Canadian rules under National Instrument 43-101 ("NI 43-101"). Investors are cautioned not to assume that any part of the mineral deposits in these categories will ever be converted into reserves. However, these terms are not defined terms under SEC Industry Guide 7 and are not permitted to be used in reports and registration statements filed with the SEC by U.S. domestic issuers. In addition, NI 43-101 permits disclosure of "contained ounces" of mineralization. In contrast, the SEC only permits issuers to report mineralization as in place tonnage and grade without reference to unit measures.

The definitions of proven and probable reserves used in NI 43-101 differ from the definitions in SEC Industry Guide 7. Under SEC Industry Guide 7 (under the Exchange Act), as interpreted by the staff of the SEC, mineralization may not be classified as a "reserve" for United States reporting purposes unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. Among other things, all necessary permits would be required to be in hand or issuance imminent in order to classify mineralized material as reserves under the SEC standards.

Investors are cautioned not to assume that any part or all of the mineral deposits identified as an "indicated mineral resource," "measured mineral resource" or "inferred mineral resource" will ever be converted to reserves as defined in NI 43-101 or SEC Industry Guide 7. Further, "inferred mineral resources" have a great amount of uncertainty as to their existence and economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian securities legislation, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, or economic studies. Investors are cautioned not to assume that part or all of an inferred mineral resource exists, or is economically or legally mineable.

EXPLANATORY NOTE REGARDING PRESENTATION OF FINANCIAL INFORMATION

The annual audited consolidated financial statements contained in this annual report on Form 20-F are reported in Canadian dollars. For the years ended January 31, 20122019 through January 31, 20162015, inclusive we have prepared our consolidated financial statements in accordance with International Financial Reporting Standards ("IFRS"(“IFRS”) as issued by the International Accounting Standards Board ("IASB"(“IASB”).

GLOSSARY OF TECHNICAL TERMS

| ||

| The elemental symbol for gold. | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

| A fracture in a rock where there has been displacement of the two sides. | |

| The concentration of each ore metal in a rock sample, usually given as weight percent. Where extremely low concentrations are involved, the concentration may be given in grams per tonne (g/t or gpt) or ounces per ton (oz/t). The grade of an ore deposit is calculated, often using sophisticated statistical procedures, as an average of the grades of a very large number of samples collected from throughout the deposit. | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

|

|

| Usually implies minerals of value occurring in rocks. |

| Payment of a percentage of net mining profits after deducting applicable smelter charges. |

|

|

|

|

| A natural aggregate of one or more minerals which may be mined and sold at a profit, or from which some part may be profitably separated. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Imperial measurement of weight equivalent to 2,000 pounds. |

| Metric measurement of weight equivalent to 1,000 kilograms (or 2,204.6 pounds). |

|

A long, narrow excavation dug through overburden, or blasted out of rock, to expose a vein or ore structure.

veins

The mineral deposits that are found filling openings in rocks created by faults or replacing rocks on either side of faults.

wenban limestone

Devonian limestones best exposed on the western flank of Wenban Peak south of the town of Cortez, Nevada.

| 4 |

| Table of Contents |

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

| A. Selected Financial Data For the years ended January 31, 2019, 2018, 2017, 2016 and 2015, we have prepared our consolidated financial statements in accordance with IFRS, as issued by the IASB.

|

The selected historical consolidated financial information set forth below has been derived from our annual audited consolidated financial statements for each of the years in the five-year period ended January 31, 2016.

For the years ended January 31, 2016, 2015, 2014, 2013, and 2012 we have prepared our consolidated financial statements in accordance with IFRS, as issued by the IASB.2019.

The selected historical consolidated financial information presented below is condensed and may not contain all of the information that you should consider. This selected financial data should be read in conjunction with our annual audited consolidated financial statements, the notes thereto and the section entitled ''Item 5 — Operating‘‘Item 5-Operating and Financial Review and Prospects.''’’

|

| Years Ended January 31, |

| |||||||||||||||||

| 2019 |

|

| 2018 |

|

| 2017 |

|

| 2016 |

| 2015 |

| |||||||

Operations |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Revenue |

| $ | - |

|

| $ | - |

|

| $ | - |

|

| $ | - |

|

| $ | - |

|

Expense |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating and Administrative |

|

| 878,566 |

|

|

| 1,375,982 |

|

|

| 580,066 |

|

|

| 642,193 |

|

|

| 538,469 |

|

Net Income (Loss) |

|

| 704,296 |

|

|

| 2,015,340 |

|

|

| (981,139 | ) |

|

| 50,521 |

|

|

| 527 |

|

Earnings (Loss) Per Share - Basic |

|

| 0.01 |

|

|

| 0.04 |

|

|

| (0.02 | ) |

|

| 0.00 |

|

|

| 0.00 |

|

Earnings (Loss) Per Share – Diluted |

|

| 0.01 |

|

|

| 0.04 |

|

|

| (0.02 | ) |

|

| 0.00 |

|

|

| 0.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted Average Number of Shares Outstanding - Basic |

|

| 48,672,608 |

|

|

| 47,570,158 |

|

|

| 48,396,734 |

|

|

| 44,200,953 |

|

|

| 42,016,049 |

|

Weighted Average Number of Shares Outstanding – Diluted |

|

| 49,826,429 |

|

|

| 50,519,282 |

|

|

| 48,396,734 |

|

|

| 44,200,953 |

|

|

| 42,741,915 |

|

In accordance with IFRS

|

| As at January 31, |

| |||||||||||||||||

Balance Sheet |

| 2019 |

|

| 2018 |

|

| 2017 |

|

| 2016 |

|

| 2015 |

| |||||

Working Capital (deficit) |

|

| 15,094,434 |

|

| $ | 15,296,877 |

|

| $ | (117,528 | ) |

| $ | 470,078 |

|

| $ | 11,324 |

|

Total Assets |

|

| 22,222,757 |

|

|

| 21,937,782 |

|

|

| 19,641,035 |

|

|

| 20,088,148 |

|

|

| 20,275,844 |

|

Liabilities |

|

| 2,966,800 |

|

|

| 2,881,168 |

|

|

| 1,793,502 |

|

|

| 1,413,790 |

|

|

| 2,011,063 |

|

Equity |

|

| 19,255,957 |

|

|

| 19,056,614 |

|

|

| 17,837,213 |

|

|

| 18,674,358 |

|

|

| 18,264,781 |

|

The tables below set forth selected consolidated financial data under IFRS for the years ended January 31, 2016, 2015, 2014, 2013B. Capitalization and 2012. The information has been derived from our annual audited consolidated financial statements.Indebtedness

Years Ended January 31, 2016 2015 2014 2013 2012 Operations Revenue Expense Operating and Administrative Net Income (loss) Net Earnings (loss) Per Share Weighted Average Number of Shares Outstanding $ - $ - $ - $ - $ - 642,193 538,469 860,517 1,365,288 772,587 50,521 527 (50,871 ) (1,542,564 ) (773,813 ) 0.00 0.00 (0.00 ) (0.05 ) (0.02 ) 44,200,953 42,016,049 36,024,532 33,563,649 33,483,650

|

| As at January 31, |

| |||||||||||||||||

| 2016 |

|

| 2015 |

|

| 2014 |

|

| 2013 |

|

| 2012 |

| ||||||

Balance Sheet | ||||||||||||||||||||

Working Capital (deficit) |

| $ | 470,078 |

|

| $ | 11,324 |

|

| $ | (486,109 | ) |

| $ | (539,814 | ) |

| $ | 1,166,663 |

|

Total Assets |

|

| 20,088,148 |

|

|

| 20,275,844 |

|

|

| 19,856,395 |

|

|

| 20,330,548 |

|

|

| 20,756,599 |

|

Liabilities |

|

| 1,413,790 |

|

|

| 2,011,063 |

|

|

| 2,750,713 |

|

|

| 3,435,002 |

|

|

| 2,719,920 |

|

Equity |

|

| 18,674,358 |

|

|

| 18,264,781 |

|

|

| 17,105,682 |

|

|

| 16,895,546 |

|

|

| 18,036,679 |

|

Exchange Rates

The following table sets forth information as to the period end, average, the high and the low exchange rate for Canadian Dollars and U.S. Dollars for the periods indicated based on the noon buying rate in New York City for cable transfers in Canadian Dollars as certified for customs purposes by the Federal Reserve Bank of New York (Canadian dollar = US$1).

Year Ended January 31, |

| Average |

|

| Period End |

|

| High |

|

| Low |

| ||||

2012 |

|

| 0.9970 |

|

|

| 1.0052 |

|

|

| 1.0604 |

|

|

| 0.9449 |

|

2013 |

|

| 0.9978 |

|

|

| 0.9973 |

|

|

| 1.0299 |

|

|

| 0.9599 |

|

2014 |

|

| 1.0389 |

|

|

| 1.1138 |

|

|

| 1.1178 |

|

|

| 0.9955 |

|

2015 |

|

| 1.1151 |

|

|

| 1.2711 |

|

|

| 1.2711 |

|

|

| 1.0639 |

|

2016 |

|

| 1.2964 |

|

|

| 1.4080 |

|

|

| 1.4223 |

|

|

| 1.2185 |

|

The following table sets forth the high and low exchange rate for the past six months based on the noon buying rate. As of June 9, 2016, the exchange rate was CDN$1.2731 for each US$1.

Month |

| High |

|

| Low |

| ||

December 2015 |

|

| 1.3990 |

|

|

| 1.3360 |

|

January 2016 |

|

| 1.4589 |

|

|

| 1.3969 |

|

February 2016 |

|

| 1.4040 |

|

|

| 1.3523 |

|

March 2016 |

|

| 1.3468 |

|

|

| 1.2962 |

|

April 2016 |

|

| 1.3170 |

|

|

| 1.2544 |

|

May 2016 |

|

| 1.3136 |

|

|

| 1.2548 |

|

|

Not Applicable.

|

| Table of |

C. Reasons for the Offer and Use of Proceeds

Not Applicable.

| D. Risk Factors

|

In addition to the other information presented in this Annual Report, the following should be considered carefully in evaluating the Company and its business. This Annual Report contains forward forward‑looking statements that involve risks and uncertainties. The Company'sCompany’s actual results may differ materially from the results discussed in the forward forward‑looking statements. Factors that might cause such a difference include, but are not limited to, those discussed below and elsewhere in this Annual Report.

WeAlthough the Company recognized net income for the years ended January 31, 2018 and 2019, the Company does not anticipate any revenues in the near future and will be requiredincur losses.During the year ended January 31, 2019, the Company recognized net income from positive movements in foreign exchange, which fluctuates from period to raise additional capitalperiod based on the value of the Canadian dollar in relation to mine our properties.the US dollar. The Company is currentlyCompany’s remaining properties are in the exploration stage of its properties. Ifstage. Therefore until such properties can develop or the Company determines, based on its most recent information,can acquire properties that it is feasible to begin operations on its properties,can be development and revenues can be derived therefrom, the Company will incur losses.

As of January 31, 2019, our internal controls over financial reporting were ineffective, and if we continue to fail to improve such controls and procedures, investors could lose confidence in our financial and other reports, the price of our shares of common stock may decline, and we may be requiredsubject to raise additional capital in orderincreased risks and liabilities.As a public company, we are subject to developthe reporting requirements of the United States Securities Exchange Act of 1934, as amended, and bring the properties into production.Sarbanes-Oxley Act of 2002. The Company's abilityExchange Act requires, among other things, that we file annual reports with respect to raise funds will depend on several factors, including, butour business and financial condition. Section 404 of the Sarbanes-Oxley Act requires, among other things, that we include certifications of our management regarding the effectiveness of our disclosure controls and procedures. For the year ended January 31, 2019, our management has concluded that our disclosure controls and procedures were not limitedeffective to current economic conditions, its properties, its prospects, metal prices, businesses competing for financingprovide reasonable assurance that material information relating to the Company and its consolidated subsidiaries is made known to management and disclosed in accordance with applicable securities regulations. Further, management concluded the Company’s internal control over financial condition. Thereporting was not effective as at January 31, 2019, due to the following material weaknesses: (i) due to the limited number of staff resources, the Company believes there are instances where a lack of segregation of duties exist to provide effective controls; and (ii) due to the limited number of staff resources, the Company may not be ablehave the necessary in-house knowledge to raise funds, oraddress complex accounting and tax issues that may arise. If we cannot effectively and efficiently improve our controls and procedures, we could suffer material misstatements in our financial statements and other information we report and fail to raise funds on commercially reasonable terms. Ifmeet our reporting obligations, which would likely cause investors to lose confidence in our reported financial and other information. This could lead to a decline in the Company is unable to raise additional funds, it may not be able to develop its properties or any of its business plans as described in this Annual Report.trading price for our common shares.

The commercial quantities of ore cannot be accurately predicted. Whether an ore body will be commercially viable depends on a number of factors including the particular attributes of the deposit, such as size, grade and proximity to infrastructure, as well as mineral prices and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in a mineral deposit being unprofitable.

The mining industry is highly speculative and involves substantial risks. The mining industry, from exploration, development and production is a speculative business, characterized by a number of significant risks including, among other things, unprofitable efforts resulting not only from the failure to discover mineral deposits but from finding mineral deposits which, though present, are insufficient in quantity and quality to return a profit from production. The marketability of minerals acquired or discovered by the Company may be affected by numerous factors which are beyond the control of the Company and which cannot be accurately predicted, such as market fluctuations, the proximity and capacity of milling facilities, mineral markets and processing equipment, and government regulations, including regulations relating to royalties, allowable production, importing and exporting of minerals, and environmental protection. The combination of such factors may result in the Company not receiving any or an adequate return on investment capital.

The Company'sCompany’s properties are all at the exploration stage and have no proven reserves. All of the Company'sCompany’s properties are in the exploration stage only and are without a known body of ore. If the Company does not discover a body of ore in its properties, the Company will search for other properties where it can continue similar work.

| 6 |

| Table of Contents |

The Company'sCompany’s mineral exploration efforts may be unsuccessful. Despite exploration work on its mineral claims, no known bodies of commercial ore or economic deposits have been established on any of the Company's properties. In addition, theThe Company is at the exploration stage on all of its properties and substantial additional work will be required in order to determine if any economic deposits occur on the Company'sCompany’s properties. Even in the event commercial quantities of minerals are discovered, the exploration properties might not be brought into a state of commercial production. Finding mineral deposits is dependent on a number of factors, including the technical skill of exploration personnel involved. The commercial viability of a mineral deposit once discovered is also dependent on a number of factors, some of which are particular attributes of the deposit, such as size, grade and proximity to infrastructure, as well as metal prices.

Competition for mineral land. There is a limited supply of desirable mineral lands available for acquisition, claim staking or leasing in the areas where the Company contemplates expanding its operations and conducting exploration activities. Many participants are engaged in the mining business, including large, established mining companies. Accordingly, there can be no assurance that the Company will be able to compete successfully for new mining properties.

Uncertainty of exploration and development programs. The Company'sCompany’s results of operations are significantly affected by the costs and results of its exploration and development programs. Exploration for minerals is highly speculative in nature, involves many risks and is frequently unsuccessful. Among the many uncertainties inherent in any gold and silver exploration and development program are the location of economic ore bodies, the development of appropriate metallurgical processes, the receipt of necessary governmental permits and the construction of mining and processing facilities. Assuming the discovery of an economic deposit, depending on the type of mining operation involved, several years may elapse from the initial phases of drilling until commercial operations are commenced and, during such time, the economic feasibility of production may change. Accordingly, the Company'sCompany’s exploration and development programs may not result in any new economically viable mining operations or yield new mineral reserves to expand current mineral reserves.

Licenses and permits. The operations of the Company require licenses and permits from various governmental authorities. The Company believes that it holds all necessary licenses and permits required under applicable laws and regulations and believes that it is presently complying in all material respects with the terms of such licenses and permits. However, such licenses and permits are subject to change in various circumstances. There can be no guarantee that the Company will be able to obtain or maintain all necessary licenses and permits as are required to explore and develop its properties, commence construction or operation of mining facilities and properties under exploration or development or to maintain continued operations that economically justify the cost.

Litigation. Although the Company is not currently subject to litigation, it may become involved in disputes with other parties in the future which may result in litigation. Any litigation could be costly and time consuming and could divert the Company's management from the Company's business operations. In addition, if the Company is unable to resolve any litigation favorably, it may have a material adverse impact on the Company's financial performance, cash flow and results of operations.

Acquisitions. The Company undertakes evaluations of opportunities to acquire additional mining properties. Any resultant acquisitions may be significant in size, may change the scale of the Company's business, and may expose the Company to new geographic, political, operating, financial and geological risks. The Company's success in its acquisition activities depends on its ability to identify suitable acquisition candidates, acquire them on acceptable terms, and integrate their operations successfully. Any acquisitions would be accompanied by risks, such as a significant decline in the price of gold or silver, the ore body proving to be below expectations, the difficulty of assimilating the operations and personnel of any acquired companies, the potential disruption of the Company's ongoing business, the inability of management to maximize the financial and strategic position of the Company through the successful integration of acquired assets and businesses, the maintenance of uniform standards, controls, procedures and policies, the impairment of relationships with customers and contractors as a result of any integration of new management personnel and the potential unknown liabilities associated with acquired mining properties. In addition, the Company may need additional capital to finance an acquisition. Historically, the Company has raised funds through equity financing and the exercise of options and warrants. However, the market prices for natural resources are highly speculative and volatile. Accordingly, instability in prices may affect interest in resource properties and the development of and production from such properties that may adversely affect the Company's ability to raise capital to acquire and explore resource properties. There can be no assurance that the Company would be successful in overcoming these risks or any other problems encountered in connection with such acquisitions.

Conflict of interest. Certain directors and officers of the Company are officers and/or directors of, or are associated with, other natural resource companies that acquire interests in mineral properties. Such associations may give rise to conflicts of interest from time to time. The directors are required by law, however, to act honestly and in good faith with a view to the best interests of the Company and its shareholders and to disclose any personal interest which they may have in any material transaction which is proposed to be entered into with the Company and to abstain from voting as a director for the approval of any such transaction.

Uncertainty of continuing as a going concern. The continuation of the Company and the recoverability of mineral property costs depends upon its ability to discover economically recoverable mineral reserves, attain profitable operations and generate cash flow from operations and/or to raise equity capital through the sale of its securities. The Company's consolidated financial statements do not include the adjustments that would be necessary if the Company were unable to continue as a going concern.

Limited and volatile trading volume.volume. Although the Company'sCompany’s common shares are listed on the TSX Venture Exchange (the "TSX-V"“TSX-V”), the Frankfurt Stock Exchange (the "FSE"“FSE”), and the Berlin-Bremen Stock Exchange and quoted in the United States on the OTCPink,OTCQX, the volume of trading has been limited and volatile in the past and is likely to continue to be so in the future, reducing the liquidity of an investment in the Company'sCompany’s common shares and making it difficult for investors to readily sell their shares in the open market. Without a liquid market for the Company'sCompany’s common shares, investors may be unable to sell their shares at favorable times and prices and may be required to hold their shares in declining markets or to sell them at unfavorable prices.

Volatility of share price.price. In recent years, securities markets in Canada have experienced a high level of price volatility. The market price of many resource companies, particularly those, like the Company, that are considered speculative exploration companies, have experienced wide fluctuations in price, resulting in substantial losses to investors who have sold their shares at a low price point. These fluctuations are based only in part on the level of progress of exploration, and can reflect general economic and market trends, world events or investor sentiment, and may sometimes bear no apparent relation to any objective factors or criteria. During the 20162019 fiscal year, the Company'sCompany’s common share price fluctuated on the TSX-V between a low of $0.06$0.32 and a high of $0.18.$0.44. Significant fluctuations in the Company'sCompany’s common share price isare likely to continue, and could potentially increase in the future.

| 7 |

| Table of Contents |

Difficulty for United States investors to effect service of process against the Company.Company. The Company is incorporated under the laws of the Province of British Columbia, Canada. Consequently, it will be difficult for United States investors to effect service of process in the United States upon the directors or officers of the Company, or to realize in the United States uponCanada judgments of United States courts predicated upon civil liabilities under the Exchange Act. The majority of the Company'sCompany’s directors and officers are residents of Canada. A judgment of a United States court predicated solely upon such civil liabilities would likely be enforceable in Canada by a Canadian court if the United States court in which the judgment was obtained had jurisdiction, as determined by the Canadian court, in the matter. There is substantial doubt whether an original action could be brought successfully in Canada against any of such persons or the Company predicated solely upon such civil liabilities.

The Company is subject to foreign currency fluctuations. The Company operates in more than one country and the Company's functional currency is the Canadian Dollar. The Company's offices are located in Canada, all of its mining exploration properties are located in United States, and the Company's financial results are reported in Canadian Dollars. The Company's currency fluctuation exposure is primarily to the U.S. Dollar and the Canadian Dollar. The Company reported a foreign exchange loss of $9,714 during the year ended January 31, 2016. The Company does not use derivative financial instruments for speculative trading purposes, nor does the Company hedge its foreign currency exposure to manage the Company's foreign currency fluctuation risk. Fluctuations in and among the various currencies in which the Company operates could have a material effect on the Company's operations and its financial results.

The Company has incurred net losses since its inception and expects losses to continue. The Company has not been profitable since its inception. For the fiscal year ended January 31, 2016, the Company had net income of $50,521 due to deferred income tax recovery and an accumulated deficit on January 31, 2016 of $27,829,911. As the Company is currently at the exploration stage and has no reserves of precious metals, there is no assurance that the Company will be profitable in the future.

There are no assurances that we will discover minerals on a commercially viable basis. The Company'sCompany’s ability to generate revenues and profits is expected to occur through exploration, development and production of its existing properties as well as through acquisitions of interests in new properties. Substantial expenditures will be incurred in an attempt to establish the economic feasibility of mining operations by identifying mineral deposits and establishing ore reserves through drilling and other techniques, developing metallurgical processes to extract metals from ore, designing facilities and planning mining operations. The economic feasibility of a project depends on numerous factors, including the cost of mining and production facilities required to extract the desired minerals, the total mineral deposits that can be mined using a given facility, the proximity of the mineral deposits to a user of the minerals, and the market price of the minerals at the time of sale. There is no assurance that existing or future exploration programs or acquisitions will result in the identification of deposits that can be mined profitably.

The Company'sCompany’s exploration activities are subject to various federal, state and local laws and regulations. Laws and regulations govern various aspects of the Company'sCompany’s business including the following: taxes; labor standards; occupational health; waste disposal; protection of the environment; mine safety; toxic substances; and the exploration, development, mining, production, importing and exporting of minerals. In many cases, licenses and permits are required to conduct mining operations. Amendments to current laws and regulations governing operations and activities of mining companies or more stringent implementation thereof could have a substantial adverse impact on the Company. Applicable laws and regulations will require the Company to make certain capital and operating expenditures to initiate new operations. Under certain circumstances, the Company may be required to stop its exploration activities once it is started until a particular problem is remedied or to undertake other remedial actions.

Market price is highly speculative.speculative. The market prices of metals are highly speculative and volatile. Instability in metal prices may affect the interest in mining properties and the exploration, development and production of such properties. If gold prices substantially decline, this may adversely affect the Company'sCompany’s ability to raise capital to explore for existing and new mineral properties.

The Company operates in a highly competitive industry. The Company competes with other developmental resource companies which have similar operations, and many competitors have operations and financial resources and industry experience greater than those of the Company. The Company may encounter increasing competition from other mining companies in its efforts to acquire mineral properties and hire experienced resource industry professionals. Increased competition in the Company'sCompany’s business could adversely affect its ability to attract necessary capital funding or acquire suitable producing properties or prospects for mineral exploration in the future.

Penny stock rules may make it more difficult to trade the Company'sCompany’s common shares. The SEC has adopted regulations which generally define a "penny stock"“penny stock” to be any equity security that has a market price of less than US$5.00 per share or an exercise price of less than US$5.00 per share, subject to certain exceptions. The Company'sCompany’s securities may be covered by the penny stock rules, which impose additional sales practice requirements on broker-dealers who sell to persons other than established customers and accredited investors such as institutions with assets in excess of US$5,000,000 or an individual with net worth in excess of US$1,000,000 or annual income exceeding US$200,000 or US$300,000 jointly with his or her spouse. For transactions covered by this rule, the broker-dealers must make a special suitability determination for the purchase and receive the purchaser'spurchaser’s written agreement of the transaction prior to the sale. Consequently, the rule may affect the ability of broker-dealers to sell the Company'sCompany’s securities and also affect the ability of its investors to sell their shares in the secondary market.

| 8 |

| Table of Contents |

FINRA rules will make it more difficult to trade the Company'sCompany’s common shares.shares. The Financial Industry Regulatory Authority, or FINRA, has adopted sales practice requirements which may limit a stockholder'sstockholder’s ability to buy and sell our stock. In addition to the "penny stock"“penny stock” rules described above, FINRA has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer'scustomer’s financial status, tax status, investment objectives and other information. Under interpretations of these rules, FINRA believes that there is a high probability that speculative low priced securities will not be suitable for at least some customers. FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may limit your ability to buy and sell our stock and have an adverse effect on the market for our shares.

Item 4. Information on the Company

| A. History and Development of the Company

|

The Company was incorporated under the Company Act of the Province of British Columbia, Canada on January 22, 1981 under the name of Carol Energy Corporation, which name was changed to Coral Energy Corporation on March 3, 1982, and to Coral Gold Corp. on September 9, 1987. On September 14, 2004, the Company changed its name to Coral Gold Resources Ltd. in conjunction with a 10 to 1 share consolidation. On July 17, 2007, the shareholders of the Company amended the share structure by subdividing the Company'sCompany’s issued share capital of 8,267,360 common shares into 24,802,080 common shares, every one common share being subdivided into three common shares. On July 15, 2004, the Company transitioned to the British Columbia Business Corporations Act. The principal executive office of the Company is located at 570 Granville Street, Suite 900, Vancouver, British Columbia V6C 3P1, and its telephone number is 604-682-3701.

The Company is a natural resource company primarily engaged in the exploration and development of natural resource properties. Its principal business activities have been the exploration of certain mineral properties located in the statesstate of Nevada and California in the United States. The carrying value of the Company's mineral property acquisition and exploration expenditures at January 31, 2016 is $19,192,353.

Please refer to Note 46 of the financial statements (Item 18) for information regarding the Company's principal expenditures on its mineral properties.Company’s exploration and evaluation assets.

B. Business Overview |

Operations and Principal Activities

Presently, the Company'sCompany’s principal business activity is the care and maintenance, and, where warranted, the exploration thereof, three mineral properties consisting of the Norma Sass claims, JDN claims and development of mineral properties.Ludlow property. The Company is in the process of exploring itsthese mineral properties and has not yet determined whether its mineral properties contain ore reserves that are economically recoverable. There is no assurance that a commercially viable mineral deposit exists on any of the Company'sCompany’s properties, and future exploration will be required before final evaluation as to the economic and legal feasibility is determined.

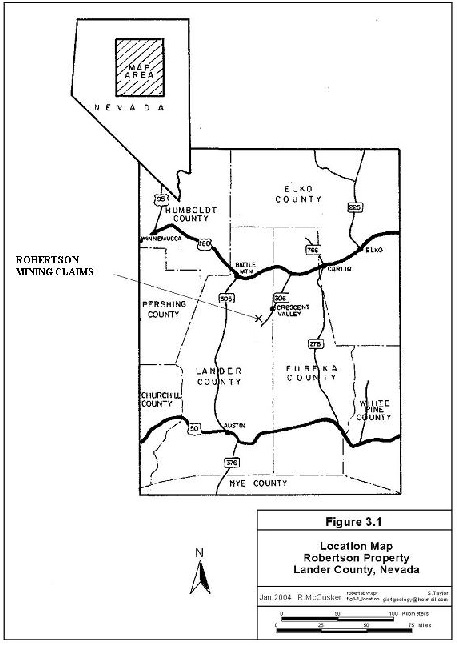

The Company's mining claims are located in the states of Nevada and California in the United States. The Company's present principal exploration activities have been focusedCompany also has a net smelter returns royalty on its former property, the Robertson Mining Claims located in Crescent Valley, Nevada.claims, sold to Barrick Cortez Gold Corp. on June 8, 2017.

Competition

The mining industry in which the Company is engaged and is highly competitive. Competitors include well-capitalized mining companies, independent mining companies and other companies having financial and other resources far greater than those of the Company. The companies competeCompany competes with other mining companies in connection with the acquisition of gold and other precious metal properties. In general, properties with a higher grade of recoverable mineral and/or which are more readily minable afford the owners a competitive advantage in that the cost of production of the final mineral product is lower. Thus, a degree of competition exists between those engaged in the mining industries to acquire the most valuable properties. As a result, the Company may eventually be unable to acquire attractive gold mining properties.

Seasonality

Due to the climate in the States of Nevada, and California, the Company is generally not affected by seasonality.

Dependence on Customers and Suppliers

The Company is not dependent upon a single or few customers or suppliers for revenues or its operations.

Government Regulation

We are subject to various federal and state laws and regulations including environmental laws and regulations. Environmental regulations impose, among other things, restrictions, liabilities and obligations in connection with the generation, handling, use, storage, transportation, treatment and disposal of hazardous substances and waste and in connection with spills, releases and emissions of various substances to the environment. Environmental regulation also requires that facility sites and other properties associated with our operations be operated, maintained, abandoned and reclaimed to the satisfaction of applicable regulatory authorities. In addition, certain types of operations, including exploration and development projects and changes to certain existing projects, may require the submission and approval of environmental impact assessments or permit applications. Compliance with environmental regulation can require significant expenditures, including expenditures for clean up costs and damages arising out of contaminated properties and failure to comply with environmental regulations may result in the imposition of fines and penalties. We believe that we are in substantial compliance with such laws and regulations; however, such laws and regulations may change in the future in a manner which will increase the burden and cost of compliance.

Certain laws and governmental regulations may impose liability on us for personal injuries, clean-up costs, environmental damages and property damages, as well as administrative, civil and criminal penalties. We maintain limited insurance coverage for sudden and accidental environmental damages, but do not maintain insurance coverage for the full potential liability that could be caused by sudden and accidental environmental damage. Accordingly, we may be subject to liability or may be required to cease production from properties in the event of such damages.

Environmental Regulations

The Company'sCompany’s exploration programs in Nevada and California are subject to state and federal regulations regarding environmental considerations. All operations involving the exploration for the production of minerals are subject to existing laws and regulations relating to exploration procedures, safety precautions, employee health and safety, air quality standards, pollution of streams and fresh water sources, odor, noise, dust and other environmental protection controls adopted by federal, state and local governmental authorities as well as the rights of adjoining property owners. The Company may be required to prepare and present to federal, state or local authorities data pertaining to the effect or impact that any proposed exploration for or production of minerals may have upon the environment. All requirements imposed by any such authorities may be costly, time consuming and may delay commencement or continuation of exploration or production operations. Future legislation may significantly emphasize the protection of the environment, and, as a consequence, the activities of the Company may be more closely regulated to further the cause of environmental protection. Such legislation, as well as further interpretation of existing laws in the United States, may require substantial increases in equipment and operating costs to the Company and delays, interruptions, or a termination of operations, the extent of which cannot be predicted. Environmental problems known to exist at this time in the United States may not be in compliance with regulations that may come into existence in the future. This may have a substantial impact upon the capital expenditures required of the Company in order to deal with such problem and could substantially reduce earnings. At the present time, the Company'sCompany’s exploration activities in Nevada and California are in compliance with all known environmental requirements.

The primary regulatory bodies that directly regulate the Company'sCompany’s activities are the Bureau of Land Management (Federal), Lander County and the Lander County Recorder’s Office and the Nevada Department of Environmental Protection (State).Protection.

|

| Table of Contents |

C. Organizational Structure

The Company has two wholly-owned subsidiaries: Coral Energy Corporation of California, a California corporation which holdspreviously held title to the Company'sproperty in California, property, and Coral Resources, Inc., a Nevada corporation, which holds title to the Company'sCompany’s mining claims located in Nevada. In the 2006 fiscal year, theThe Company completed the purchase of 1,391,860 shares, representingalso owns 98.49% of the issued shares, of

Marcus Corporation, which is a Nevada Corporation that owns the Marcus mining claims, consisting of 39 unpatented lode claims and two placer claims, and which comprise a portion of the Company's Robertson Property.corporation.

| D. Property, Plant and Equipment

|

Presently, the Company is an "exploration“exploration stage company"company”, as all of the Company'sCompany’s properties are currently in the exploratory stage of development. In order to determine if a commercially viable mineral deposit exists in any of the Company'sCompany’s properties, further geological work will need to be done and a final evaluation based upon the results obtained to conclude economic and legal feasibility.

The Company's primary focus has been on the Robertson Mining Claims, in Nevada, United States.

Prior Property - Robertson Mining Claims, Nevada, U.S.A.

Completed Sale of Robertson Properties

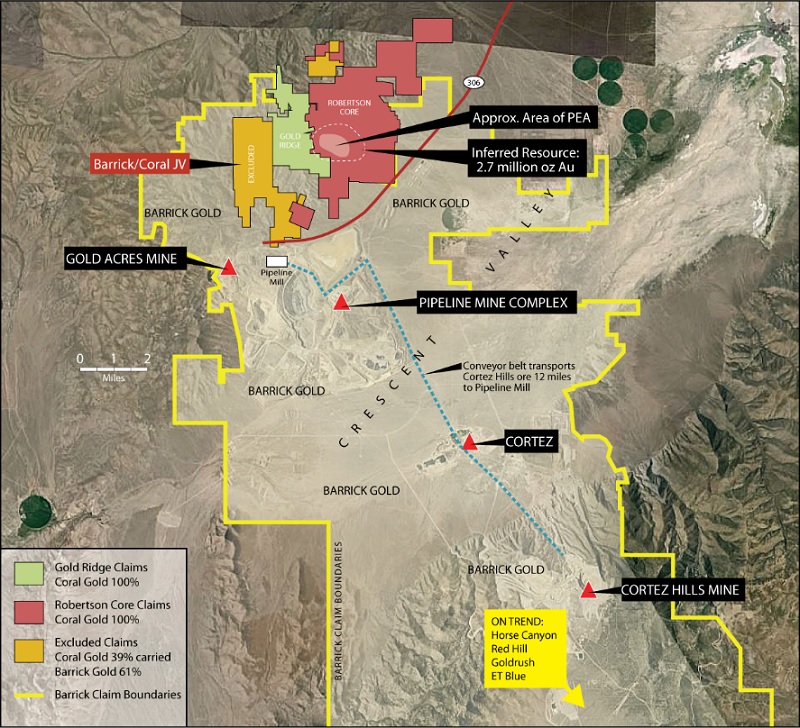

On June 8, 2017, Coral completed the purchase and sale agreement with Barrick Cortez Inc. (“Barrick”), a subsidiary of Barrick Gold Corp., for the sale of the Robertson Property in Lander County, Nevada, to Barrick in consideration of:

| 1. | The payment to Coral of US$15.75 million (Cdn $21.84 million based on the closing exchange rate) in cash ; | |

| 2. | The return of 4,150,000 common shares of Coral held by Barrick (which represent approximately 8.5% of the Company’s basic common shares outstanding as of June 8, 2017) for cancellation by the Company ; and | |

| 3. | A sliding scale 1% to 2.25% net smelter returns royalty (the “NSR”) on the Robertson Property, payable quarterly, subject to potential advance royalty payments as outlined below, as well as a right of first refusal enabling Barrick to acquire the NSR in the event that the Company wishes to sell the NSR to any third party . |

The sliding scale NSR rate will be determined based on the observed gold price during each quarterly period based on the average LBMA Gold Price PM during the quarterly period, as follows:

Average Gold Price/Oz During the Quarter (USD) | Applicable NSR Royalty Rate |

Up to and including $1,200.00 $1,200.01 to $1,400.00 $1,400.01 to $1,600.00 $1,600.01 to $1,800.00 $1,800.01 to $2,000.00 Over $2,000.00 | 1.00% 1.25% 1.50% 1.75% 2.00% 2.25% |

Pursuant to the agreement, as amended, and due to the delay in closing, in the event that the Robertson Property is not placed into production by Barrick by December 31, 2024, then beginning on January 1, 2025, and continuing on an annual basis thereafter until the earlier of (i) the date commercial production commences and (ii) January 2, 2034, Barrick will make advance royalty payments to Coral Gold of US$0.5M, which will be non-refundable and fully credited against any future obligations under the NSR. These dates have all been extended by one year from the dates in Coral’s earlier announcement.

Barrick will also assume all liabilities relating to the Robertson Property, and will provide replacement security for the reclamation bond.

The Robertson Mining Claims areProperty includes the properties also known as the Core, Gold Ridge, Excluded and the Ruf mining claims, but does not include the properties known as the Norma Sass, Eagle, and JDN mining claims. The Robertson Property is located in Crescent Valley, Nevada on the western flanks of the Shoshone Range, 28 miles to the southeast of Battle Mountain, Nevada, which lies approximately 230 miles northeast of Reno, Nevada. The Robertson Mining Claims comprise approximately 9,200 acres in the Bullion Mining District,eastern Lander County, Nevada, and currently include 435 unpatented Federal claims and 9 patented lode claims.sixty miles southwest of Elko.

As a result of the sale, the Company recorded a gain of $5,871,719, net of transaction costs during the fiscal year ended January 31, 2018.

| 11 |

| Table of Contents |

These mining claims have been acquired over a period of several years from different sources. The entire Robertson Mining Claims are subject to a 3% net smelter royalty to Geomex Development Eighth Partnership ("Geomex 8"), which royalty shall cease at such time as the sum of US$1,250,000 has been paid to Geomex 8, and various mining leases requiring minimum annual advanced royalties ranging from 4% to 10% of net smelter returns.

There is no underground or surface plant or equipment located on the Robertson Mining Claims and the following figures provide location details with respect to the Robertson Mining Claims.

|

The Robertson Property is the subject of four technical reports dated January 15, 2004, April 25, 2006, January 27, 2008 and January 18, 2012. The first two technical reports were prepared by Robert McCusker, P.Geol. in accordance with NI 43-101 ("McCusker Reports"). The third and fourth reports were prepared by Beacon Hill Consultants (1988) Ltd. ("Beacon Hill") of Vancouver, British Columbia (the "Beacon Hill Report"). The first Beacon Hill report was a NI 43-101 resource estimate that included the zones located within the Robertson's Core claims only. The Company's other claim blocks, including Norma Sass, Lander Ranch, Ruf, Blue Nugget and the Excluded (Carve Out) claims (joint ventured with Cortez Gold Mines ("Cortez"), a joint venture owned by Barrick Gold Corporation), were not part of the estimate. The 2012 report was an NI 43-101 compliant preliminary economic assessment of the advanced stage Altenburg Hill, Porphyry and Gold Pan zones analyzing a combination of open pit mining methods and cyanide heap leach.Existing Properties

Property Description and Location(i) Norma Sass Claims, Nevada

The Robertson Property is an advanced-stage gold exploration project located in eastern Lander County, Nevada, 60 miles southwest of Elko. Coral Resources, Inc., a wholly owned subsidiary of the Company, acquired control of the Robertson Property in 1986. The core property consists of 300 unpatented federal lode claims, mill sites, and nine patented lode claims covering over 6,200 acres of public lands administered by the U.S. Bureau of Land Management (the "BLM"). The Company controls an additional 31 claims through a series of mineral leases and option agreements.

In 2001, a boundary agreement between the Company and Cortez resolved claim boundary overlaps and seniority issues along the east and southwest sides of the Robertson claim block. This agreement required both parties to amend and/or abandon certain claims in order to achieve the agreed upon boundary. This was completed during the 2002-2003 assessment year.

Approximately 31 of the 300 of the claims that comprise the Robertson Property are controlled by the Company through 4 mining leases and option agreements. The Core Claims held by the Company under lease or option agreements require minimum advance royalty payments and production royalties in the event of production. Total annual payments for the various leases and minimum advance royalties are approximately US$51,600.

A summary compilation of the terms of these agreements are presented in the table below:

Mining Lease and Option Agreements

Company/Date |

| Number of Claims |

| Option Payment |

| Production Royalty | Advance Royalty Payment | |||||||

Core: Tenabo Gold Mining Co. Nov. 30, 1975 |

| 13 |

| US$ | 2,000,000 |

| 8% NSR | US$ | 12,000/yr | |||||

Northern Nevada Au, Inc. Sept. 30, 1986 |

| 12 |

| US$ | - |

| 4% GSR | US$ | 9,600/yr | |||||

Albany Gold Corp. (Geomex) |

| All |

| US$ | 1,250,000 |

| 3% NSR |

| Nil | |||||

Filippini/Breckon (June Claims) |

| 6 |

| US$ | 1,000,000 |

| 3% NSR | US$ | 30,000/yr | |||||

Annual federal rental fees of US$82,305 payable to the BLM, and Notice of Intent to Hold Mining Claims have been filed for the 2015-2016 assessment year.

History and Exploration

The Robertson Property is located in the Tenabo area, a sub-district of the Bullion mining district in Lander County, Nevada. Historic lode mining in this district dates from 1905 and placer gold was discovered in many of the dry washes in the Tenabo area in 1916. Between 1937 and 1939, a small dragline dredge and washing plant operated in the district, and a dredge was reported by Humphrey to be operating in lower Mill Gulch in 1945.

During 1966 through 1970, a number of companies explored the district in search of porphyry copper-style mineralization. In 1968, while drilling a series of shallow rotary holes near the Gold Pan mine, Superior Oil discovered a small, but relatively high-grade zone of gold at shallow depths in what is now known as the Gold Pan zone; however, with additional drilling, Superior Oil lost interest in the district. They were followed by a number of mining companies, including Placer Development (1974-75), Teck Corporation (1977), Aaron Mining Ltd. (1975-86), and E & B Exploration Ltd. (1980-81), all of which sporadically explored the Tenabo area with limited success.

Modern open pit mining and heap leaching began in 1974, when Aaron Mining Ltd. ("Aaron"), initiated a pilot leach operation on the Robertson Property. From 1978 through 1980, Aaron expanded its leaching operations and continued exploration and acquiring claims in the district.

In 1986, the Company acquired Aaron's interest in the Robertson Property and immediately began a series of major drilling programs beginning in 1986 and continuing until 1989. Mining operations on the Robertson Property commenced in 1988, but were suspended less than one year later. During the operating life of the Robertson Property mine approximately 350,000 tons of low-grade material was placed on leach pads from which about 6,200 ounces of gold were recovered.

During 1986 through 1989, the Company completed approximately 380 reverse circulation drill holes and seven diamond drill holes, totaling about 109,377 feet. Much of this drilling was focused in four resources areas: Gold Pan, Gold Quartz, Gold Quartz extension (also called Gold Quartz West) and the Triplet Gulch areas. The purpose of this drilling was to determine the limits and continuity of mineralization within these zones. Nearly all of the reverse circulation holes were drilled vertically to an average depth of about 300 feet.

In 1990, the Company and Amax Gold Exploration Inc. ("Amax") entered into an amended and restated option and earn-in agreement in which Amax could earn a 60% interest in the Robertson Property by producing a bankable feasibility study. Amax completed an exploration program that included drilling 338 reverse circulation holes and 62 diamond drill holes, totaling over 176,000 feet. As the feasibility study did not meet the requirements of the agreement, Amax returned the property to the Company in 1996.

During the fiscal year ended January 31, 1999, the Company entered into an option agreement dated October 8, 1998 (the "Option Agreement"), with Placer Dome U.S. Inc. ("Placer"), which was later assigned by Placer to Cortez. Under the agreement, Cortez could earn a 70% interest in the Robertson Property by producing a bankable feasibility study. The focus of Cortez's exploration was to expand the 39A zone and test a number of outlying targets. During 1999, Cortez completed 46 reverse circulation drill holes and a single flood rotary hole, totaling 57,000 feet. Of the 13 holes directed at expanding the 39A zone, only two holes, 99401 and 99413, encountered significant mineralization. This drilling program did little to expand the resource. Of the remaining holes drilled by Cortez, only two holes (99406 and 99419) encountered significant mineralization. Both holes were designed to offset and/or follow up existing drill intersections and surface gold anomalies.

After completing this drilling program, Cortez declared its interest in renegotiating the terms of the Option Agreement with the Company. When the Company declined, Cortez terminated the Option Agreement on December 30, 1999, and did not earn an interest in the Robertson Property.

During 2004 and 2005, the Company conducted three drilling programs consisting of 32 reverse circulation holes totaling 24,020 feet on the Robertson Property. The focus of this exploration was to expand and further define the 39A Zone, test the "deep" Gold Pan Zone for extensions of the 39A Zone and offset previous ore-grade intersections in the "distal target area".

A report entitled "Update of the Geological Report on the Robertson Property" April 25, 2006 on gold resources at the Robertson Property was submitted by Robert McCusker, Consulting Geologist, a "qualified person" in accordance with the requirements of NI 43-101.

During fiscal 2006, the Company completed a major drilling program on the Robertson Property. Drilling was completed in two phases. The drilling program totaled 35,615 feet of reverse circulation drilling in 46 holes. Depths ranged from 450 feet to 1,500 feet. Due to the relatively flat-lying nature of mineralization at the Robertson Property, all holes were drilled vertically. Phase Iconsisted of 14 reverse circulation (RC) drill holes, CR06-2 through CR06-15, totaling 11,355 feet which were completed in the immediate vicinity of the existing 39A Zone indicated mineral resource. Phase IIconsisted of 32 RC holes, CR06-16 through CR06-48A, totaling 24,260 feet which were completed in (1) the Distal Zone; (2) on the northeast flank of Altenburg Hill; (3) in the gravel-covered area between the Altenburg Hill and the Porphyry Zone mineral resource; and (4) along a northeast-striking structural zone in the Porphyry Zone. Drilling operations during Phase I and Phase II drilling were directly supervised by Robert McCusker.

In February 2008, the Company received an NI 43-101 compliant resource estimate titled Mineral Resource Estimate for the Robertson Property, Lander County, Nevada report dated January 27, 2008, prepared by Beacon Hill, Robert McCusker and Jasman Yee (updated in October 2009). This resource estimate is no longer considered current.

Later in 2008, the Company commissioned Beacon Hill to not only update the Robertson Property resource estimate but to also outline a program for continued development of the Core Claims in 2008 and beyond. Beacon Hill recommended a three-pronged development approach:

| ||

| ||

|

Beacon Hill recommended the following drilling on the Core Claims:

Phase I: 52 RC holes ranging in depth from 500 feet to 1,200 feet and totaling 37,600 feet, to focus on:

|

| |

|

| |

|

| |

|

|

Phase II: would consist of 21 diamond core holes (HQ diameter) ranging from 300 feet to 1,000 feet-deep and totaling 11,900 feet. The purpose of core drilling is to provide geological data on the controls of mineralization, acquire geotechnical data (RQD and specific gravity), confirm grade and continuity and provide material for metallurgical testing. Drilling has been recommended as follows:

|

| |

|

| |

|

| |

|

|

In March 2008, the Company announced that it had entered into a contract for 37,600 feet of reverse circulation drilling on Robertson Property. The agreement, signed with Lang Exploratory Drilling of Salt Lake City, Utah, began in April following permit approval from the BLM. Robert McCusker supervised the drill program as the "qualified person" under NI 43-101.

In September 2008, the Company completed its reverse circulation drilling program at Robertson. The program totaled 22,835 feet of drilling in 33 vertical holes which ranged in depth from 500 to 1200 feet. The holes were located on the Altenburg Hill, South Porphyry, 39A and Distal zones in order to increase the gold resource in these zones.

Both Phase I and Phase II were aimed at expanding and upgrading the Robertson Property inferred resource.

The planned 21 diamond drill holes of Phase II ranged from 300 to 1,000 feet in depth. It was anticipated that Phase II drilling would:

| ||

| ||

| ||

|

To help derive exploration priorities to expand the current resource with the 2008 drilling campaign, a series of in-house, draft open pit shapes were modeled around the 2008 NI 43-101 compliant inferred resource.

During the fiscal year ending January 31, 2008, the Company purchased 100% interest in the 72 claims comprising the Fanny Komp/Elwood Wright lease which forms part of the core area of the Robertson Property for US$250,000.

In October 2009, the Company received a revised resource for the Robertson Property from Beacon Hill utilizing lower cut-off grades to reflect the positive movement in the price of gold over the previous three years. The revised values were based on the NI 43-101 report titled Mineral Resource Estimate for the Robertson Property, Lander County, Nevada prepared by Beacon Hill in January 2008; this report is no longer considered current.

Despite the permitting setback, 12 RC holes at Triplet Gulch that were previously permitted under the 2007 PO were drilled in 2010.

A limited diamond drilling program at the Gold Pan and Altenburg Hill zones was also permitted under the 2007 PO. A program totaling 6,700 feet was conducted that represents the first phase of the diamond core drill program announced in the company's 2010 work plan and budget. The program was designed to verify the 2008 RC drilling assay results and provide material for metallurgical test work. The Gold Pan, Altenburg Hill and Porphyry zones represent near surface resources that could potentially be developed as an open pit/heap leach operation. Past metallurgical testing of Porphyry Zone mineralization returned favorable gold recoveries from the oxide material.

Also in 2010, Coral commissioned Beacon Hill to commence a Preliminary Economic Assessment ("PEA") that would meet the NI 43-101 standard on the Gold Pan, Altenburg Hill and Porphyry zones. The report was finalized and made public in late January 2012 and outlined steps to move the project towards pre-feasibility. (see section below titled Preliminary Economic Assessment for details)

In June 2011, the BLM accepted the fifth submission of the APO and a kick off meeting was held on July 20th, 2011. The meeting outlined the need for a new EA. In particular, the various categories to be studied in the EA including cultural, wild life, native religions, hazmat, paleontology, range management, noxious weeds, air quality, hydrology, riparian zones, migratory birds, environmental justice and socio economic issues.

Studies had been in progress since November 2010 but the EA did not officially start until July 2011. The cultural studies were done by Kautz and Co. of Reno, Nevada. Most of the other studies are by SRK out of Elko, Nevada who have overseen the entire environmental assessment.

As Coral anticipated, the work did not locate native religious sites or burial grounds etc. but the ghost mining town of Tenabo required detailed study.

Coral's cultural and wildlife surveys were sufficiently completed by the end of 2011 to allow the Company to demonstrate to the BLM that 13 proposed diamond core holes on the Porphyry zone would not impact on cultural or wildlife areas. The program consisted of 13 diamond drill core holes that twinned existing Amax Gold Inc. ("Amax") holes (circa 1990 -- 1996) and provided core for leach tests at McClelland Laboratories Inc. ("McClelland Labs") in Reno, Nevada. The holes were part of the Phase 1 drill program as proposed in the January 2012 PEA Assessmentand were designed to verify Amax's historic drilling data, and to upgrade the level of confidence in resources contained in the oxidized zones. The Phase 1 drill program represented Coral's first step towards pre-feasibility as defined by the PEA.

By July 13th, 2012 the baseline vegetation and wildlife field work had been completed and the baseline studies report was submitted to the BLM.

The BLM's response to Corals Baseline Studies was received July 27th and delivered to SRK Consultants who then supplied a response to the modifications to the Baseline Studies required by the BLM.

On September 24, 2012, Coral announced thatSRK had completed and submitted the EA to the BLM.

Compliance with the EA process was mandatory. The various categories studied were the subject of numerous Nevada State and US Federal laws. Fortunately not all are applicable to the Robertson property.

In September 2013, Coral received a notice from the BLM, which included the Decision on the Robertson Project Amendment to the Exploration Plan of Operations and Reclamation Permit Application and also the Finding of No Significant Impact ("FONSI").

On January 13, 2014, Coral announced that its US subsidiary, Coral Resources Inc. had received notice from the Bureau of Mining Regulation and Reclamation (BMRR) of the State of Nevada that it had approved the Plan of Amendment for Coral Resources Inc.'s Robertson Project.

The Amended Plan of Operations ("APO") was originally approved by the federal Bureau of Land Management (see news release dated Sept 16, 2013). Now that the APO has been approved by the State of Nevada (NDEP and subsidiary BMRR) Coral can proceed with drilling and other programs at Robertson.

Reclamation Activities