|

|

|

|

| For the Year Ended December 31, |

| |||||||||||||

| 2020 |

| 2019 (3) |

| 2018 (2) |

| 2017 |

| 2016 |

| |||||

| (in US$ thousands, except for earnings per share) |

| |||||||||||||

Income Statement Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue | $ | 313,564 |

| $ | 338,160 |

| $ | 425,940 |

| $ | 425,215 |

| $ | 384,565 |

|

Costs of sales |

| (279,686 | ) |

| (313,373 | ) |

| (389,692 | ) |

| (385,527 | ) |

| (352,957 | ) |

Gross profit |

| 33,878 |

|

| 24,787 |

|

| 36,248 |

|

| 39,688 |

|

| 31,608 |

|

Other operating income |

| 814 |

|

| 385 |

|

| 805 |

|

| 5,084 |

|

| 5,441 |

|

Selling, general & administrative expenses |

| (27,006 | ) |

| (25,051 | ) |

| (26,924 | ) |

| (27,248 | ) |

| (26,325 | ) |

Other operating expenses |

| (129 | ) |

| (770 | ) |

| (1,445 | ) |

| (909 | ) |

| (3,386 | ) |

Operating profit/(loss) |

| 7,557 |

|

| (649 | ) |

| 8,684 |

|

| 16,615 |

|

| 7,338 |

|

Finance costs |

| (744 | ) |

| (1,012 | ) |

| (1,378 | ) |

| (1,221 | ) |

| (1,147 | ) |

Finance income |

| 320 |

|

| 506 |

|

| 482 |

|

| 876 |

|

| 1,045 |

|

Share of loss of associates |

| (1 | ) |

| (3 | ) |

| (3 | ) |

| (3 | ) |

| (710 | ) |

Impairment of investment in associates |

| — |

|

| — |

|

| — |

|

| — |

|

| (126 | ) |

Loss on liquidation of a subsidiary |

| — |

|

| — |

|

| — |

|

| (261 | ) |

| — |

|

Exchange (loss)/gain |

| (579 | ) |

| 1,550 |

|

| 1,741 |

|

| 2,784 |

|

| (38 | ) |

Other income |

| 1,173 |

|

| 717 |

|

| 1,817 |

|

| 214 |

|

| 267 |

|

Other expense |

| (1 | ) |

| (3 | ) |

| (11 | ) |

| (336 | ) |

| (94 | ) |

Profit before taxes |

| 7,725 |

|

| 1,106 |

|

| 11,332 |

|

| 18,668 |

|

| 6,535 |

|

Income taxes expense |

| (4,016 | ) |

| (2,057 | ) |

| (3,886 | ) |

| (5,140 | ) |

| (510 | ) |

Profit/(Loss) for the year | $ | 3,709 |

| $ | (951 | ) | $ | 7,446 |

| $ | 13,528 |

| $ | 6,025 |

|

Attributable to: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Equity holders of APWC | $ | (552 | ) | $ | (1,632 | ) | $ | 2,928 |

| $ | 8,720 |

| $ | 2,853 |

|

Non-controlling interests | $ | 4,261 |

| $ | 681 |

| $ | 4,518 |

| $ | 4,808 |

| $ | 3,172 |

|

Earnings per share (1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic and diluted (loss)/profit for the year attributable to equity holders of the parent | $ | (0.04 | ) | $ | (0.12 | ) | $ | 0.21 |

| $ | 0.63 |

| $ | 0.21 |

|

5

| As of December 31, |

| |||||||||||||

| 2020 |

| 2019 (3) |

| 2018 (2) |

| 2017 |

| 2016 |

| |||||

| (in US$ thousands) |

| |||||||||||||

Balance Sheet Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents | $ | 52,237 |

| $ | 53,673 |

| $ | 60,778 |

| $ | 46,093 |

| $ | 48,231 |

|

Working capital |

| 180,323 |

|

| 185,855 |

|

| 182,410 |

|

| 181,752 |

|

| 157,012 |

|

Total assets |

| 338,119 |

|

| 298,911 |

|

| 305,798 |

|

| 334,843 |

|

| 293,596 |

|

Total debts |

| 13,781 |

|

| 11,356 |

|

| 24,814 |

|

| 42,688 |

|

| 29,762 |

|

Net assets |

| 234,875 |

|

| 228,435 |

|

| 221,816 |

|

| 222,826 |

|

| 197,175 |

|

Capital stock |

| 138 |

|

| 138 |

|

| 138 |

|

| 138 |

|

| 138 |

|

Total APWC shareholders’ equity |

| 157,860 |

|

| 153,854 |

|

| 150,028 |

|

| 153,328 |

|

| 135,950 |

|

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

Exchange Rate Information

Unless otherwise noted, for the convenienceyear ended December 31, 2023. For the year ended December 31, 2022, it was based on 20,020,364 basic and diluted weighted Common Shares issued and outstanding; and was based on 13,819,669 basic and diluted weighted Common Shares issued and outstanding for each of the reader, translations of amounts from Baht, Singapore dollars, Renminbi and Australian dollars to U.S. dollars have been made at the respective noon buying rates in New York City for cable transfers in those currencies as certified for customs purposes by the Federal Reserve Bank of New York (the “Noon Buying Rate”) onyear ended December 31, 2020. The respective Noon Buying Rates on December 31,2021, 2020, were US$ 1.00 = Bt 30.02; S$ 1.321; RMB 6.525; and A$ 1.297. The respective Noon Buying Rates on March 31, 2021,2019.

Sources: Federal Reserve Bulletin, Board of Governorsimpact of the Federal Reserve System. Federal Reserve Statistical Release H.10, from the websiteapplication of the Board of Governors of the Federal Reserve System at http://www.federalreserve.gov.

Thailand

The Thai Baht is convertible into foreign currenciesIFRS 16.

Year Ended December 31, | At Period End |

| Average(1) |

| High |

| Low |

| ||||

| (Bt per $1.00) |

| ||||||||||

2016 |

| 35.81 |

|

| 35.22 |

|

| 36.33 |

|

| 34.54 |

|

2017 |

| 32.56 |

|

| 33.75 |

|

| 35.89 |

|

| 32.49 |

|

2018 |

| 32.31 |

|

| 32.27 |

|

| 33.44 |

|

| 31.11 |

|

2019 |

| 29.75 |

|

| 30.89 |

|

| 32.26 |

|

| 29.75 |

|

2020 |

| 30.02 |

|

| 31.32 |

|

| 33.04 |

|

| 29.79 |

|

|

|

6

The high and low exchange rates for the six months preceding the date of this Annual Report were:

Month | High |

| Low |

| ||

October 2020 |

| 31.56 |

|

| 31.02 |

|

November 2020 |

| 31.13 |

|

| 30.18 |

|

December 2020 |

| 30.27 |

|

| 29.79 |

|

January 2021 |

| 30.14 |

|

| 29.89 |

|

February 2021 |

| 30.46 |

|

| 29.86 |

|

March 2021 |

| 31.30 |

|

| 30.21 |

|

Sources: Federal Reserve Bulletin, Board of Governors of the Federal Reserve System. Federal Reserve Statistical Release H.10, from the website of the Board of Governors of the Federal Reserve System at http://www.federalreserve.gov.

Singapore

The Singapore dollar is convertible into foreign currencies and floats against a trade-weighted basket of foreign currencies, the composition of which is not made public by Singapore’s central bank, the Monetary Authority of Singapore, but of which the U.S. dollar is a component. The following tables set forth, for the periods indicated, certain information concerning the Noon Buying Rate of the Singapore dollar. No representation is made that the Singapore dollar or U.S. dollar amounts referred to herein could have been or could be converted into U.S. dollars or Singapore dollars, as the case may be, at any particular rate or at all.

Year Ended December 31, | At Period End |

| Average(1) |

| High |

| Low |

| ||||

| (S$ per $1.00) |

| ||||||||||

2016 |

| 1.447 |

|

| 1.382 |

|

| 1.452 |

|

| 1.337 |

|

2017 |

| 1.336 |

|

| 1.373 |

|

| 1.450 |

|

| 1.336 |

|

2018 |

| 1.362 |

|

| 1.350 |

|

| 1.384 |

|

| 1.304 |

|

2019 |

| 1.345 |

|

| 1.363 |

|

| 1.391 |

|

| 1.345 |

|

2020 |

| 1.321 |

|

| 1.337 |

|

| 1.461 |

|

| 1.321 |

|

|

|

The high and low exchange rates for the six months preceding the date of this Annual Report were:

Month | High |

| Low |

| ||

October 2020 |

| 1.368 |

|

| 1.353 |

|

November 2020 |

| 1.366 |

|

| 1.340 |

|

December 2020 |

| 1.338 |

|

| 1.321 |

|

January 2021 |

| 1.329 |

|

| 1.318 |

|

February 2021 |

| 1.337 |

|

| 1.320 |

|

March 2021 |

| 1.350 |

|

| 1.329 |

|

Sources: Federal Reserve Bulletin, Board of Governors of the Federal Reserve System. Federal Reserve Statistical Release H.10, from the website of the Board of Governors of the Federal Reserve System at http://www.federalreserve.gov.

7

China

The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of Renminbi into foreign currencies, including the conversion rate limitations on capital transfers and through restrictions on foreign trade and other regulatory impediments to the free transferability of capital. The following tables set forth, for the periods indicated, certain information concerning the Noon Buying Rate of the Renminbi. No representation is made that the Renminbi or U.S. dollar amounts referred to herein could have been or could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all.

Year Ended December 31, | At Period End |

| Average(1) |

| High |

| Low |

| ||||

| (RMB per $1.00) |

| ||||||||||

2016 |

| 6.943 |

|

| 6.655 |

|

| 6.958 |

|

| 6.448 |

|

2017 |

| 6.506 |

|

| 6.735 |

|

| 6.958 |

|

| 6.477 |

|

2018 |

| 6.876 |

|

| 6.629 |

|

| 6.974 |

|

| 6.265 |

|

2019 |

| 6.962 |

|

| 6.901 |

|

| 7.179 |

|

| 6.682 |

|

2020 |

| 6.525 |

|

| 6.888 |

|

| 7.168 |

|

| 6.521 |

|

|

|

The high and low exchange rates for the six months preceding the date of this Annual Report were:

Month | High |

| Low |

| ||

October 2020 |

| 6.790 |

|

| 6.650 |

|

November 2020 |

| 6.690 |

|

| 6.556 |

|

December 2020 |

| 6.571 |

|

| 6.521 |

|

January 2021 |

| 6.482 |

|

| 6.428 |

|

February 2021 |

| 6.487 |

|

| 6.434 |

|

March 2021 |

| 6.572 |

|

| 6.465 |

|

Sources: Federal Reserve Bulletin, Board of Governors of the Federal Reserve System. Federal Reserve Statistical Release H.10, from the website of the Board of Governors of the Federal Reserve System at http://www.federalreserve.gov.

Australia

The following tables set forth, for the periods indicated, certain information concerning the Noon Buying Rate of the Australian dollar. No representation is made that the Australian dollar or U.S. dollar amounts referred to herein could have been or could be converted into U.S. dollars or Australian dollars, as the case may be, at any particular rate or at all.

Year Ended December 31, | At Period End |

| Average(1) |

| High |

| Low |

| ||||

| (A$ per $1.00) |

| ||||||||||

2016 |

| 1.383 |

|

| 1.346 |

|

| 1.459 |

|

| 1.279 |

|

2017 |

| 1.280 |

|

| 1.301 |

|

| 1.383 |

|

| 1.239 |

|

2018 |

| 1.419 |

|

| 1.344 |

|

| 1.425 |

|

| 1.234 |

|

2019 |

| 1.423 |

|

| 1.438 |

|

| 1.493 |

|

| 1.373 |

|

2020 |

| 1.297 |

|

| 1.448 |

|

| 1.738 |

|

| 1.297 |

|

|

|

8

The high and low exchange rates for the six months preceding the date of this Annual Report were:

Month | High |

| Low |

| ||

October 2020 |

| 1.427 |

|

| 1.382 |

|

November 2020 |

| 1.419 |

|

| 1.359 |

|

December 2020 |

| 1.360 |

|

| 1.297 |

|

January 2021 |

| 1.306 |

|

| 1.284 |

|

February 2021 |

| 1.318 |

|

| 1.257 |

|

March 2021 |

| 1.321 |

|

| 1.278 |

|

Sources: Federal Reserve Bulletin, Board of Governors of the Federal Reserve System. Federal Reserve Statistical Release H.10, from the website of the Board of Governors of the Federal Reserve System at http://www.federalreserve.gov.

|

|

Not applicable

|

|

Not applicable.

|

|

Risks Relating to Our Business

COVID-19 Could Have a Material Adverse Effect on Our Business, Financial Condition and Results of Operations

The outbreak of the Coronavirus Disease 2019 (“COVID-19”), which has been declared by the World Health Organization to be a “public health emergency of international concern,” has spread across the globe and is impacting worldwide economic activity and financial markets. We are facing significant adverse risks related to the spread of COVID-19, and the recent developments surrounding the global pandemic have had, and are expected to continue to have, significant adverse effects onadversely affect our business, financial condition, results of operations and cash flows. Asflows, and could result in a result,loss of all or part of your investment.

DuePRC can change quickly with little advance notice. Uncertainties exist with respect to the measures institutedinterpretation and implementation of the PRC laws regarding foreign investment, cybersecurity, personal data protection and anti-monopoly, and any change in Chinagovernment interpretation or enforcement could implicate our PRC subsidiaries and have a material adverse effect on us.

which could materially and adversely affect our corporate governance.

The Singapore government implemented a partial lockdown, also known

The impact of COVID-19 is constantly changing. Our operations in Thailand and Australia could be materially and adversely affected if an outbreak recurs in these regions. Although we are monitoring the situation, the extent to which COVID-19 impacts our business will depend on future developments, which are uncertain and unpredictable in nature.

We are facing increased operational challenges as we take measures to support and protect employee health and safety as a result of COVID-19. For example, in order to protect the employees from COVID-19, the Company has taken measures to protect its employees, including temperature checks before entering the workplace, mandatory mask-wearing, social distancing, and work from home. We have also implemented staggered work hours to lower the risk that our employees might get infected on public transportations if they commute during peak hours. In particular, our remote work arrangements, coupled with stay-at-home orders and quarantines, pose challenges to our employees and our IT systems, and the extension of remote work arrangements could increase operational risk, including cyber security and IT systems management risks, and impair our ability to manage our business. The increased operational challenges could have a material and adverse effect on our business, financial conditions, and, results of operations.

If COVID-19 continues to adverselyseverity, could materially affect our business, operationsfinancial condition, and financial results the probability of the occurrence of other risks describedoperations.

Risks Relating to Copper

Company’s profitability.

10

periodic intervals to the then net realizable value, which could be below cost. Copper prices have been subject to considerable volatility, and it is not always possible to manage our copper purchases and inventory so as to neutralize the impact of copper price volatility. In addition, an excessive increase in the price of copper could result in fewer orders from customers or increased cost of sales given agreed sales prices, and negatively impact theour Company. Accordingly, significant volatility in copper prices could have a material adverse effect on our business, financial condition and results of operations.

Competition

transmission technologies, such as wireless telecommunications, could materially reduce sales of our telecommunications products.

highly concentrated end markets.

11

PEWC May

Agreement.

our business risks.

Employees’ Unions

Some of APWC’s operating subsidiaries have a large

Employees

retain qualified personnel.

12

Environmental Liabilities

operations.

Cyber security Because there is no unified framework for administering information systems amongst APWC’s subsidiaries, our competitors with a unified framework for administering information systems across their subsidiaries may have a competitive advantage over us and may be able to more efficiently administer such systems and respond to incidents and minimize risk to their business.

13

make any such payment could have a material adverse effect on our liquidity, business, financial condition and results of operations.

In addition our debt agreements contain restrictive covenants and default provisions. Covenants in the agreements governing our existing debt, and debt we may incur in the future, may materially restrict our operations, including our ability to incur debt, pay dividends, make certain investments and payments, and encumber or dispose of assets. In addition, any global economic deterioration may cause us to incur significant net losses or force us to assume considerable liabilities. We cannot assure youmake assurances that we will be able to remain in compliance with our financial covenants, which, as a result, may lead to a default. ThisAny such default may thereby restrict our ability to access unutilized credit facilities or the global capital markets to meet our liquidity needs. Furthermore, a default under any agreementcertain debt agreements by APWC or APWC’s subsidiaries may trigger cross-defaults under our other debt agreements. In the event of default, we may not be able to cure the default or obtain a waiver on a timely basis.waiver. An event of default under any agreement timely governing our existing or future debt, if not cured or timely waived, could have a material adverse effect on our liquidity, business, financial condition and results of operations. Please see Section 5.b.5.B. (“Liquidity and Capital Resources”) of this Annual Report and Note 27(c) of our consolidated financial statements referenced in Item 18 of this Annual Report for a further discussion of our secured and unsecured indebtedness, including with respect to the loan agreement pursuant to which APWC borrowed $6 million from PEWC (which loan is secured by a pledge of APWC’s 98.3% ownership interest inindebtedness.

We Face Uncertainties Relating to the Phasing Out of LIBOR

In July 2017, the U.K. Financial Conduct Authority, which regulates the London interbank offered rate (LIBOR), announced that it intends to phase out LIBOR by the end of 2021. Discontinuation of LIBORfinancial performance and uncertainty as to the nature of such potential changes, alternative reference rates or other reforms may adversely affect the amounts of interest we pay under our debt arrangements and materially adversely affect our business, financial condition and results of operations.

Risks Relating to Our Exposure to Foreign Exchange Fluctuations

condition.

The

14

Impairment Charges

Risks Relating

our operations in Thailand.

Our auditor’ In addition, our Thai operations could be materially adversely impacted if low margin wire and cable manufacturers from China, affiliate, like other independent registered public accounting firm operating in China,including SOEs, were to enter the Thailand market.

Our auditor, the independent registered public accounting firm that issued the audit report included elsewhere in this annual report, as auditor of companies that are traded publiclyenforce agreements in the United StatesPRC with third parties; and firm registered withchanges in policies, laws, rules and regulations in the Public Company Accounting Oversight Board (United States), or PCAOB, isPRC could adversely affect us.

In December 2020, the United States enacted the Holding Foreign Companies Accountable Act (the “HFCAA”). The HFCAA requires that the SEC identify issuers that retain an auditor that has a branch or office that is located in a foreign jurisdiction and that the PCAOB determines it is unable to inspect or investigate completely because of a position taken by an authority in that foreign jurisdiction. Amongst other things, the HFCAA also requires the SEC to prohibit the securities of any issuer from being traded on any of the U.S. national securities exchanges, such as Nasdaq, or on the U.S. “over-the-counter” markets, if the auditor of the issuer’s financial statements is not subject to PCAOB inspections for three consecutive “non-inspection” years after the law became effective.

15

On April 5, 2021, the SEC’s interim final rule to implement the disclosure and submission requirements of the HFCAA was published in the U.S. Federal Register, along with the SEC’s request for public comment on the interim final rule. Regarding how the term “retain” should be interpreted for purposes of determining whether an issuer has retained an auditor that has a branch or office that is located in a foreign jurisdiction and that the PCAOB determines it is unable to inspect or investigate completely because of a position taken by an authority in that foreign jurisdiction, the SEC noted in the interim final rule that the HFCAA does not define the term “retain”, and requested comment on how the term “retain” should be understood for purposes of the HFCAA.

The auditor of our PRC-based subsidiaries is located in the PRC and that auditor is an affiliate of APWC’s Taiwan-based auditor that signs APWC’s audit report. Given the current question as to how “retain” should be understood for purposes of the HFCAA, we cannot assure you that we will not be identified by the SEC as an issuer that has retained an auditor that has a branch or office that is located in a foreign jurisdiction that the PCAOB determines it is unable to inspect or investigate completely because of a position taken by an authority in that foreign jurisdiction as a result of the fact that the auditor of our China affiliates is located in, and organized under the laws of, the PRC. In addition, there can be no assurance that, if we have a “non-inspection” year, we will be able to take remedial measures in response thereto. Given the foregoing, we cannot assure you that we will be able to maintain the listing of the Common Shares on Nasdaq or that you will be allowed to trade the Common Shares in the United States on the “over-the-counter” markets or otherwise. Should the Common Shares not be listed or tradeable in the United States, the value of the Common Shares could be materially affected.

This lack of PCAOB inspections in China prevents the PCAOB from fully evaluating audits and quality control procedures of our independent registered public accounting firm. As a result, we and investors in the Common Shares are deprived of the benefits of such PCAOB inspections. The inability of the PCAOB to conduct inspections of auditors in China makes it more difficult to evaluate the effectiveness of our independent registered public accounting firm’s China affiliate’s audit procedures or quality control procedures as compared to auditor outside of China that are subject to PCAOB inspections, which could cause investors and potential investors in the Common Shares to lose confidence in our audit procedures and reported financial information and the quality of our financial statements.

The PRC Legal System May Limit the Company’s Remedies

China. The PRC legal system is a civil law system based on written statutes. Prior court decisions may be cited for reference but have limited precedential value. Since the late 1970s, the PRC central government has promulgated a comprehensive system of laws, rules and regulations governing economic matters. However, China has not developed a fully integrated legal system. Recentlysystem and enacted laws, rules and regulations may not sufficiently cover all aspects of economic activities or may be subject to a significant degree of interpretation by PRC regulatory agencies and courts

On January 1, 2020, theGovernance.

16

Regulations are relatively new, uncertainties still exist in relation to its interpretation and implementation. The Foreign Investment Law andOld FIL Laws were repealed at the Implementation Regulations may affect our relevant corporate governance practices and increase our compliance costs. For instance,same time the Foreign Investment Law and the Implementation Regulations require thatFIL became effective, foreign-invested enterprises established before the Foreign Investment Law(“

In addition, the Foreign Investment Law and the Implementation Regulations imposedomestic investors alike. The FIL imposes information reporting requirements on foreign investors and foreign-invested enterprises. Any foreign investors or foreign-invested enterprisesFIEs and any found to be non-compliant with these reporting obligations may be subject to fines or administrative liabilities.

business.

operations.

17

unpredictable actions by PRC government officials. For example, APWC’s principal office is located in Taipei, Taiwan, and any escalation in political tensions between the PRC and the government of Taiwan could materially adversely impact our ability to manage our operations in the PRC efficiently or without third party interference. The PRC government has long advocated a one-China policy with regard to the Republic of China. Any overtly aggressive actions by the PRC towards Taiwan could have a materially destabilizing impact on Taiwan generally, and on our business in particular, and could materially and adversely affect our business, financial condition and results of operations.

SOEs have competitive advantages and our business and operations may be materially and adversely affected in the event we must compete with such SOEs.

18

delisted, APWC expects its Common Shares would be quoted on an over-the-counter market. If this were to occur, APWC’s shareholders could face significant material adverse consequences, including the need to receive permission from the BMA to transfer the Common Shares, limited availability of market quotations for the Common Shares and reduced liquidity for the trading of the Common Shares. In addition, APWC could experience a decreased ability to issue additional securities and obtain additional financing in the future.

decrease.

may not be liquid, which could cause volatility and adversely affect our prevailing market price.

19

APWC May Not Be Able

leadership arising from an activist campaign could cause our stock price to experience periods of enhanced volatility or harm our ability to raise capital.

Holding Company Structure; Potential Restrictions

dividends could materially adversely affect our market price.

Corporate Matters; Limited Recourse; Limited Enforceability

Such restrictions on payments involving entities organized in PRC could adversely affect our liquidity, our business results and thus, the price of our Common Shares.

20

The Common Shares currently remain tradedAPWC relies on Nasdaq. However, as APWC has aNasdaq’s controlled company and foreign private issuer exemptions, all of which could materially and adversely affect our corporate governance.

directors could adversely affect our corporate governance.

21

cost-effective control system, misstatements due to error or fraud may occur and not be detected. As a result, even effective internal controls are able to provide only reasonable assurance with respect to the preparation and fair presentation of financial statements. Any failure in our internal control could result in a material adverse effect on our business and a decline of investor confidence in the reliability of our financial statements, which could materially adversely affect the market price of the Common Shares.

financial condition.

International Business Risks

|

|

|

|

22

States is Pacific Holdings Group, with an address at 2901 Dallas Parkway, Suite 360, Plano, Texas 75093.

North Asia in 2023.

The

|

|

|

|

Theour Company is principally engaged in the manufacture and distribution of telecommunications (primarily copper, but also fiber optic),enameled wire, power cable, and enameled wiretelecommunications products in Thailand, Singapore, Australia, PRC, Hong Kong and certain other markets in the Asia Pacific region, primarily in Thailand, China, Singapore and Australia. Theregion. Our Company also provides project engineering services in supply, delivery and installation of power cable (“SDI”). Our Company’s major customers include appliance component manufacturers, electrical contracting firms, state owned entities, wire and cable dealers and factories.

holders of our Common Shares since 2019, APWC’s ability to pay any dividends in the future, as well as to meet its other obligations and to fund operations, depends upon the amount of distributions, if any, received from its direct and indirect operating subsidiaries and other holdings and investments. APWC’s operating subsidiaries and other holdings and investments, from time to time, may be subject to restrictions on their ability to make distributions to APWC, including as a result of restrictive covenants contained in loan agreements, restrictions on the conversion of local currency earnings into U.S. dollars or other hard currency and other regulatory restrictions applicable to the countries in which our subsidiaries are formed and conduct their business. For further discussion of the risks created by these restrictions and limitations, see “Risk Factors-Risks Related to our Financial Activities” and “Risk Factors-Risks Relating to the Regions in which We Operate.”

| Year ended December 31, 2023 | North Asia | Thailand | ROW | Total segments Consolidated | |||||||||||||||||||

| US$’000 | US$’000 | US$’000 | US$’000 | ||||||||||||||||||||

| Revenue from external customers | |||||||||||||||||||||||

| Power | 9 | 80,564 | 140,501 | 221,075 | |||||||||||||||||||

| Enamel | 55,959 | 79,510 | 1,972 | 137,441 | |||||||||||||||||||

| SDI | 2,667 | — | 55,028 | 57,695 | |||||||||||||||||||

| Others* | 14 | 6,851 | 2,697 | 9,562 | |||||||||||||||||||

| 58,649 | 166,925 | 200,198 | 425,772 | ||||||||||||||||||||

| Year ended December 31, 2022 | North Asia | Thailand | ROW | Total segments Consolidated | |||||||||||||||||||

| US$’000 | US$’000 | US$’000 | US$’000 | ||||||||||||||||||||

| Revenue from external customers | |||||||||||||||||||||||

| Power | 92 | 46,340 | 135,739 | 182,171 | |||||||||||||||||||

| Enamel | 76,002 | 102,122 | — | 178,124 | |||||||||||||||||||

| SDI | 1,209 | — | 44,722 | 45,931 | |||||||||||||||||||

| Others* | 26 | 23,379 | 4,262 | 27,667 | |||||||||||||||||||

| 77,329 | 171,841 | 184,723 | 433,893 | ||||||||||||||||||||

| Year ended December 31, 2021 | North Asia | Thailand | ROW | Total segments Consolidated | |||||||||||||||||||

| US$’000 | US$’000 | US$’000 | US$’000 | ||||||||||||||||||||

| Revenue from external customers | |||||||||||||||||||||||

| Power | — | 63,629 | 127,891 | 191,520 | |||||||||||||||||||

| Enamel | 107,027 | 105,749 | — | 212,776 | |||||||||||||||||||

| Fabrication | — | — | 39,476 | 39,476 | |||||||||||||||||||

| Others* | 5 | 28,401 | 4,481 | 32,887 | |||||||||||||||||||

| 107,032 | 197,779 | 171,848 | 476,659 | ||||||||||||||||||||

23

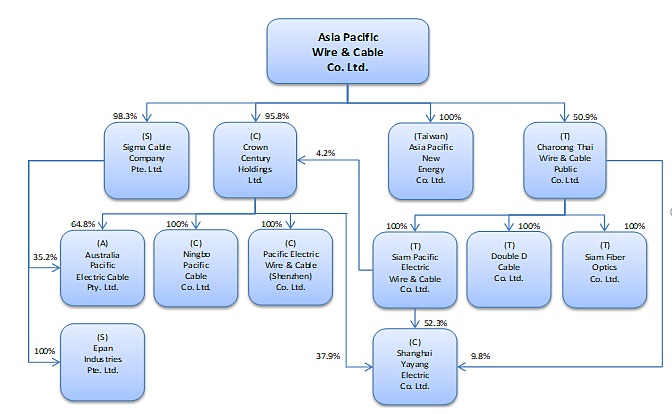

During 2020, the Company’sAPWC has four principal operations in North Asia were conducted through four business entities – subsidiaries:

The Company has an effective holding of 97.93% (including holdings through Siam Pacific) of the capital stock of CCH HK, a Hong Kong registered company, and its wholly-owned subsidiary company, PEWSC. PEWSC manufactures enameled wires for electric, video and audio products for the south China market.

Ningbo is currently a dormant entity. TheOur Company continues to indirectly own the equity of Ningbo, which still holds its government-granted business license. TheOur Company has disposed of all of the buildings and most of the equipment and the land use rights for the property where Ningbo’s operations had been situated. The principal machinery utilized at the Ningbo facility has either been sold or stored at other operating facilities of our Company.

TheROW, APWC has three principal subsidiaries:

24

dividends paid by a company to any individual or corporate payee overseas are subject to a withholding tax of 10%. Under the current Singapore corporate tax system, dividends paid by a Singapore resident company are tax exempt, and are not subject to withholding taxes. In Australia, dividends paid to non-residents are exempt from dividend withholding taxes except when dividends are paid out of profit that is not taxed by Australian income tax.

Charoong Thai is a publicly-traded Thai corporation, the shares of which are listed on the Stock Exchange of Thailand (“SET”). It manufactures aluminum and copper electric wire, medium and high voltage power cables and telecommunications cables. It has subsidiaries and affiliates in the businesses of fiber optic cable manufacturing and telecommunication and network services. Charoong Thai was established in Thailand in 1967 as a limited public company. As of December 31, 2020, the Company effectively owned 50.93% of the issued and outstanding shares of Charoong Thai. The Company’s present intention is to maintain majority ownership of the voting securities of Charoong Thai. The board of directors of Charoong Thai may authorize the issuance of additional shares of common stock of Charoong Thai. The Company has preemptive rights to purchase its pro rata share of any additional authorized shares, less amounts reserved for Charoong Thai’s directors, officers or employees. In the event the board of Charoong Thai decides to cause it to issue additional shares, the Company may decide not to exercise the Company’s preemptive rights, in which case its interest may be diluted.

Siam Pacific was established in 1988 as a joint venture between PEWC and Italian-Thai Development Plc. Siam Pacific is now a 100%-owned subsidiary of Charoong Thai and focuses on the manufacture of telecommunications cables, and enameled wires.

Rest of the World (“ROW”) Region

The Company’s ROW region currently consists of its Singapore and Australian operations.

The Company’s Singapore operations are principally conducted through“Siam Pacific” trade name. Products manufactured by Sigma Cable Company (Private) Limited (“Sigmaare sold under the “Sigma Cable”), an indirectly 98.3%-owned subsidiary of the Company. The Company believes that Sigma Cable is one of the major suppliers of power cable products in Singapore. Sigma Cable manufactures brand.

Sigma Cable also has project engineering operations in Singapore to supply, deliver and install (referred to as “SDI”) primarily medium and high voltage cables to power transmission projects. While the Company currently obtains its supply of medium and high voltage power cables for its SDI operations from PEWC, other suppliers are also available if necessary.

Sigma Cable owns 100% of the capital stock of Epan Industries Pte. Ltd. (“Epan”) a Singaporean Company. Currently, Epan is acting as the distributor of Sigma Cable products and those of other third party suppliers.

The Company’s business in Australia is conducted by Australia Pacific Electric Cable Pty. Ltd. (“APEC”). The Company’s indirect ownership interest in APEC is 98.06%. APEC is located near Brisbane and is one of three major wire and cable manufacturers in Australia. APEC possesses a substantial marketing and distribution infrastructure with a network of sales offices and warehouses in the cities of Brisbane, Sydney, Melbourne and Perth.

25

Services

|

|

Across theour Company’s three reporting segments, the Company engages in three principal business lines that consist of manufacturing and distributing wire and cable products and providing fabrication or project engineering services to certain customers. Theour Company manufactures and sells a wide variety of wire and cable products in primarily three general categories: enameled wire, power cable, and telecommunications cables, power transmission cables, and enameled wires. The Company’s telecommunications and power cables are used in a range of infrastructure projects and in commercial and residential developments. Thecable. Our Company’s enameled wires are used in the manufacturing of components and sub-components of a number of household appliances and small machinery. Our Company’s telecommunications and power cables are used in a range of infrastructure projects and in commercial and residential developments. In addition, theour Company acts as a distributor in Singapore of wire and cable products manufactured by PEWC and other third party suppliers in Singapore. ThePEWC. Our Company also offers SDI project engineering services of medium and high voltage cables for power transmission projects in Singapore.

Services

Fabrication

The Company performs fabrication services for its customers, converting raw materials to wire and cable products. Raw materials, such as copper, aluminum, polyvinyl chloride, polyethylene and optic fibers, are commodities traded on global markets with anticipated price fluctuations and currency risk. Given these risks, the Company provides fabrication services using customer-owned materials in order to limit exposure to these risks.

SDI Project Engineering Services

Given government and private sector infrastructure projects and residential and commercial buildings activity in Singapore, the Company anticipates modest demand for medium and high voltage power and for value added services in the power supply industry. To take advantage of these opportunities, the Company has developed an SDI project engineering capability. This SDI project engineering involves supply, delivery and installation of primarily medium and high voltage cables to power transmission projects in Singapore. In entering into a contract to supply, deliver and install cables for a power transmission project, the Company delivers medium and high voltage cables and enters into subcontracting agreements with local companies to install the cables as required by the project

The

26

Power Cable

The

Production of unarmored cables begins by drawing and annealingimpact of copper rods. The drawn copper wires are then stranded or “bunched” into round or sector-shaped conductors in sizes ranging from 1.5 square millimeters to 1000 square millimeters. The copper conductors are then covered in an extrusion process with a plastic insulator such as PVC, after which 2-5 conductors are twisted into a circular cable core in a cabling process and covered by a plastic outer cover.

Unarmored cables are composed of one or more cores of copper wire, insulated by substances such as PVC. Armored cables are produced in the same manner and the same range of configurations as unarmored cables, but with the addition of an outer layer of galvanized steel or iron wires to protect the cables from damage.

Enameled Wire

The Company also produces several varieties of enameled wires. Enameled wires are copper wires varnished, in an enameling process, by insulating materials. The enameling process makes the wires more resistant to oil, heat, friction and fusion, and therefore suitable for use in machinery and components and sub-components of manufactured goods. The Company manufactures enameled wires in sizes that range from 0.02 mm to 4.00 mm in diameter, varnished by various types of petroleum insulation materials including polyvinyl formal, polyurethane wires and polyester. Enameled wire products are used in the assembly of a wide range of electrical products, including oil-filled transformers, refrigerator motors, telephones, radios, televisions, fan motors, air conditioner compressors and other electric appliances.

27

|

|

Copper is the principal raw material used by the Company for copper-based products. Theprice fluctuations, our Company typically purchases copper at prices based on the average prevailing international spot market prices on the LME for copper for the one month prior to purchase. The price of copper is influenced heavily by global supply and demand as well as speculative trading. As with other costs of production, changes in the price of copper can affect theour Company’s cost of sales. Whether this has a material impact on theour Company’s operating margins and financial results depends primarily on theour Company’s ability to adjust selling prices to its customers, such that increases and decreases in the price of copper are reflected in those selling prices. In the cases when we enter into a long-term sales contract at fixed selling prices, rising copper prices could render this contract onerous and our Company would be required to recognize losses from this onerous contract in the income statement. Most sales of theour Company’s manufactured products reflect copper prices prevailing at the time the products are ordered. A long-term decrease in the price of copper would require theour Company to revalue the value of its inventory at periodic intervals to the then net realizable value, which could be below cost.

The

The Company imports both copper cathodes and copper rods in Thailand, with copper cathodes subjected to lower import duty than copper rods. The

The (See Item 3D: Risk Factors-Risks Relating to our Business: “The ability of suppliers to deliver raw materials, parts and components and energy resources could affect our Company’s ability to manufacture products without disruption and in turn negatively affect our operations.”).

28

|

|

UL Solutions.

|

|

The Company’s telecommunications cable and power cable products are primarily sold in the domestic markets of the countries where they are manufactured, whereas a portion of the enameled wires manufactured by the Company in Thailand are exported, primarily to customers throughout Southeast Asia. The following table sets forth the Company’s sales revenues for the periods indicated in its three reporting segments – North Asia region, Thailand region and ROW region for its three principal product lines, i.e., power, enameled and others together with their respective percentage share of total sales by reporting segment for such periods.

Year ended December 31, 2020 | North Asia |

| Thailand |

| ROW |

| Total segments Consolidated |

| ||||

| US$’000 |

| US$’000 |

| US$’000 |

| US$’000 |

| ||||

Revenue from external customers |

|

|

|

|

|

|

|

|

|

|

|

|

Power |

| — |

|

| 48,851 |

|

| 78,779 |

|

| 127,630 |

|

Enamel |

| 73,179 |

|

| 57,971 |

|

| — |

|

| 131,150 |

|

Fabrication |

| — |

|

| 33,101 |

|

| — |

|

| 33,101 |

|

Others* |

| 20 |

|

| 3,724 |

|

| 17,939 |

|

| 21,683 |

|

|

| 73,199 |

|

| 143,647 |

|

| 96,718 |

|

| 313,564 |

|

*include revenues from SDI service contracts (which amounted to US$15.6 million in 2020), and sale of other wires and cables products.

Year ended December 31, 2019 | North Asia |

| Thailand |

| ROW |

| Total segments Consolidated |

| ||||

| US$’000 |

| US$’000 |

| US$’000 |

| US$’000 |

| ||||

Revenue from external customers |

|

|

|

|

|

|

|

|

|

|

|

|

Power |

| — |

|

| 49,493 |

|

| 78,686 |

|

| 128,179 |

|

Enamel |

| 76,575 |

|

| 102,997 |

|

| — |

|

| 179,572 |

|

Others* |

| — |

|

| 19,889 |

|

| 10,520 |

|

| 30,409 |

|

|

| 76,575 |

|

| 172,379 |

|

| 89,206 |

|

| 338,160 |

|

*include revenues from SDI service contracts (which amounted to US$7.6 million in 2019), fabrication service contracts, and sale of other wires and cables products.

29

Year ended December 31, 2018 | North Asia |

| Thailand |

| ROW |

| Total segments Consolidated |

| ||||

| US$’000 |

| US$’000 |

| US$’000 |

| US$’000 |

| ||||

Revenue from external customers |

|

|

|

|

|

|

|

|

|

|

|

|

Power |

| — |

|

| 64,771 |

|

| 92,130 |

|

| 156,901 |

|

Enamel |

| 103,647 |

|

| 114,247 |

|

| — |

|

| 217,894 |

|

Others* |

| — |

|

| 34,406 |

|

| 16,739 |

|

| 51,145 |

|

|

| 103,647 |

|

| 213,424 |

|

| 108,869 |

|

| 425,940 |

|

* include revenues from SDI service contracts (which amounted to US$16.7 million in 2018), fabrication service contracts, and sale of other wires and cables products.

APWC’s operating subsidiaries are also responsible for sales planning, marketing strategy and customer liaison. The Company’s sales staff is knowledgeable about the Company’s products and also renders technical assistance, consulting services and repair and maintenance services to the Company’s customers. The Company does not conduct sales through independent sales agents on a commission basis but uses its own sales employees located at APWC’s operating subsidiaries.

As copper constitutes the most significant component of the Company’s wire and cable products, the price of the Company’s products depends primarily upon the price of copper. In order to minimize the impact of copper price fluctuations, the Company attempts to determine the prices of its products based on the prevailing market price of copper. The Company may be affected by significant fluctuations in the price of copper.

Payment methods for the Company’s products vary with markets and customers. The majority of sales by the Company requires payment within 90 days, but may vary depending on the customer and payment record. Sales pursuant to a successful project tender or sales to governmental or public utilities are conducted in accordance with the tender or other applicable regulations. In connection with the distribution of medium and high voltage power cables manufactured by PEWC, the Company is required to pay PEWC 90% of the cost of the products either within 30 days of receipt of the product or, in the case of SDI products, upon installation, with the remaining 10% in either case to be paid within one year. In connection with a purchase of copper rod, the Company is required to pay PEWC the cost of the copper rod within 30 days from obtaining the products from PEWC. For the export market, payment is usually made by prior delivery of an irrevocable letter of credit. Neither APWC nor its operating subsidiaries offers financing for purchases of the Company’s products. Company employees engaged in sales and marketing are paid a salary and may also receive a bonus based on performance.

Products are marketed under the respective names of the operating subsidiaries. For instance, products manufactured by Siam Pacific are marketed under the “Siam Pacific” trade name. Products manufactured by Sigma Cable are sold under the “Sigma Cable” brand.

North Asia

The Company produces and sells enameled wires in China. The Company’s principal China operations are conducted through China-based business entities. The Company generally sells enameled wires directly to manufacturers of electric motors for use in various consumer appliances.

Thailand

The Company produces and sells telecommunication cables, enameled wires and power cables in Thailand. Charoong Thai is one of the leading cable manufacturers in Thailand. Our distribution channels include both direct sales to government entities and private sector participants in the infrastructure sector, and sales to agents for governmental entities. Sales within the Thailand region are made directly by the sales department of the APWC’s operating subsidiaries in accordance with terms and pricing set by the local subsidiaries. The major customers of the Company include clients working with the government and its contractors.

30

ROW

The Company produces and sells low voltage power cables in Singapore and Australia. In addition, the Company sells a wide range of wire and cable products produced by third party suppliers and PEWC. The Company also offers SDI project engineering services for medium and high voltage power cables to power transmission projects in Singapore. SP Power Assets Ltd. has historically been the principal customer for the Company’s SDI services, accounting for nearly all of our SDI sales. Sales to SP Power Assets Ltd. are under a comprehensive contract, with purchase orders placed from time to time.

|

|

The wire and cable industry in the Asia Pacific region is highly competitive. TheOur Company’s competitors include a large number of independent domestic and foreign suppliers. Certain competitors in each of theour Company’s markets have substantially greater manufacturing, sales, research and financial resources than the Company. Theus. Our Company and other wire and cable producers primarily compete on the basis of product quality and performance, reliability of supply, customer service, and price.

31

| Regional Considerations |

The

| Insurance |

The

32

| Environmental Regulations |

The

|

|

|

|

The

presently encumbered.

The loan agreements were renewed for one year and are set to expire in March 2024.

|

|

33

|

|

|

|

5.a.1.Disclosures of Critical Accounting Policies

The critical

5.a.2.Report, which are prepared in accordance with IFRS as issued by the IASB.

| For the year ended December 31, | |||||||||||||||||

| 2023 | 2022 | 2021 | |||||||||||||||

| (US$’000 except for percentages) | |||||||||||||||||

| Net Sales: | |||||||||||||||||

| North Asia region | $ | 58,649 | $ | 77,329 | $ | 107,032 | |||||||||||

| Thailand region | 166,925 | 171,841 | 197,779 | ||||||||||||||

| ROW region | 200,198 | 184,723 | 171,848 | ||||||||||||||

| Total | $ | 425,772 | $ | 433,893 | $ | 476,659 | |||||||||||

| Operating profit/(loss): | |||||||||||||||||

| North Asia region | $ | 1,794 | $ | 241 | $ | 4,523 | |||||||||||

| Thailand region | (2,119) | 2,636 | (13,537) | ||||||||||||||

| ROW region | 8,628 | 7,768 | 6,690 | ||||||||||||||

| Corporate expenses & adjustments | (6,755) | (2,578) | (2,649) | ||||||||||||||

| Total operating (loss)/profit | $ | 1,548 | $ | 8,067 | $ | (4,973) | |||||||||||

| Operating profit/(loss) margin: | |||||||||||||||||

| North Asia region | 3.06 | % | 0.31 | % | 4.23 | % | |||||||||||

| Thailand region | (1.27) | % | 1.53 | % | (6.84) | % | |||||||||||

| ROW region | 4.31 | % | 4.21 | % | 3.89 | % | |||||||||||

|

|

| For the year ended December 31, |

| |||||||

| 2020 |

| 2019 |

| 2018 |

| |||

| (US$’000 except for percentages) |

| |||||||

Net Sales: |

|

|

|

|

|

|

|

|

|

North Asia region | $ | 73,199 |

| $ | 76,575 |

| $ | 103,647 |

|

Thailand region |

| 143,647 |

|

| 172,379 |

|

| 213,424 |

|

ROW region |

| 96,718 |

|

| 89,206 |

|

| 108,869 |

|

Total | $ | 313,564 |

| $ | 338,160 |

| $ | 425,940 |

|

Operating profit (loss): |

|

|

|

|

|

|

|

|

|

North Asia region | $ | 3,087 |

| $ | 1,237 |

| $ | 5,234 |

|

Thailand region |

| 11,250 |

|

| 3,042 |

|

| 9,539 |

|

ROW region |

| (4,492 | ) |

| (1,659 | ) |

| (2,306 | ) |

Corporate expenses & adjustments |

| (2,288 | ) |

| (3,269 | ) |

| (3,783 | ) |

Total operating profit (loss) | $ | 7,557 |

| $ | (649 | ) | $ | 8,684 |

|

Operating profit (loss) margin: |

|

|

|

|

|

|

|

|

|

North Asia region |

| 4.22 | % |

| 1.62 | % |

| 5.05 | % |

Thailand region |

| 7.83 | % |

| 1.76 | % |

| 4.47 | % |

ROW region |

| (4.64 | )% |

| (1.86 | )% |

| (2.12 | )% |

December 31, 2023, APWC is approximately 75.5%80.96% beneficially owned and is controlled by PEWC, a Taiwanese company. Thewith the remaining approximately 24.5%19.04% of the issued and outstanding Common Shares arebeing publicly-traded in the United States and listed on Nasdaq. Based upon a review of Schedule 13D and 13G filings made with the SEC by shareholders, and a review of the share register maintained by APWC’s transfer agents in Bermuda and the U.S., the Company iswe are not aware of any shareholders residentresiding in the jurisdictions where theour Company has business operations. While theour Company’s operations and results are impacted by economic, fiscal, monetary and political policies of the respective governments in the countries where theour Company operates, that impact is not a function of APWC’s shareholder base.

34

|

|

| For the Year Ended December 31, |

|

|

|

|

|

|

| ||||

| 2020 |

| 2019 |

| Changes |

| Changes |

| ||||

| US$’000 |

| US$’000 |

| US$’000 |

| % |

| ||||

Income Statement Data: |

|

|

|

|

|

|

|

|

|

|

|

|

Revenue | $ | 313,564 |

| $ | 338,160 |

| $ | (24,596 | ) |

| (7.3 | ) |

Costs of sales |

| (279,686 | ) |

| (313,373 | ) |

| 33,687 |

|

| 10.7 |

|

Gross profit |

| 33,878 |

|

| 24,787 |

|

| 9,091 |

|

| 36.7 |

|

Other operating income |

| 814 |

|

| 385 |

|

| 429 |

|

| 111.4 |

|

Selling, general and administrative expenses |

| (27,006 | ) |

| (25,051 | ) |

| (1,955 | ) |

| (7.8 | ) |

Other operating expenses |

| (129 | ) |

| (770 | ) |

| 641 |

|

| 83.2 |

|

Operating profit /(loss) |

| 7,557 |

|

| (649 | ) |

| 8,206 |

|

| 1,264.4 |

|

Finance costs |

| (744 | ) |

| (1,012 | ) |

| 268 |

|

| 26.5 |

|

Finance income |

| 320 |

|

| 506 |

|

| (186 | ) |

| (36.8 | ) |

Share of loss of associates |

| (1 | ) |

| (3 | ) |

| 2 |

|

| 66.7 |

|

Exchange (loss)/gain |

| (579 | ) |

| 1,550 |

|

| (2,129 | ) |

| (137.4 | ) |

Other income |

| 1,173 |

|

| 717 |

|

| 456 |

|

| 63.6 |

|

Other expense |

| (1 | ) |

| (3 | ) |

| 2 |

|

| 66.7 |

|

Profit before tax |

| 7,725 |

|

| 1,106 |

|

| 6,619 |

|

| 598.5 |

|

Income taxes expense |

| (4,016 | ) |

| (2,057 | ) |

| (1,959 | ) |

| (95.2 | ) |

Profit/(Loss) for the year |

| 3,709 |

|

| (951 | ) |

| 4,660 |

|

| 490.0 |

|

Attributable to: |

|

|

|

|

|

|

|

|

|

|

|

|

Equity holders of APWC |

| (552 | ) |

| (1,632 | ) |

| 1,080 |

|

| 66.2 |

|

Non-controlling interests |

| 4,261 |

|

| 681 |

|

| 3,580 |

|

| 525.7 |

|

| For the Year Ended December 31, | |||||||||||||||||||||||

| 2023 | 2022 | Changes | Changes | ||||||||||||||||||||

| US$’000 | US$’000 | US$’000 | % | ||||||||||||||||||||

| Income Statement Data: | |||||||||||||||||||||||

| Revenue | $ | 425,772 | $ | 433,893 | $ | (8,121) | (1.9) | ||||||||||||||||

| Costs of sales | (395,545) | (401,363) | 5,818 | (1.4) | |||||||||||||||||||

| Gross profit | 30,227 | 32,530 | (2,303) | (7.1) | |||||||||||||||||||

| Other operating income | 433 | 1,026 | (593) | (57.8) | |||||||||||||||||||

| Selling, general and administrative, research and development expenses | (24,472) | (24,978) | 506 | (2.0) | |||||||||||||||||||

| Other operating expenses | — | (3) | 3 | (100.0) | |||||||||||||||||||

| Net impairment loss on financial and contract assets | (4,640) | (508) | (4,132) | 813.4 | |||||||||||||||||||

| Operating profit | 1,548 | 8,067 | (6,519) | (80.8) | |||||||||||||||||||

| Finance costs | (2,527) | (1,650) | (877) | 53.2 | |||||||||||||||||||

| Finance income | 205 | 120 | 85 | 70.8 | |||||||||||||||||||

| Share of loss of associates | (2) | (1) | (1) | 100.0 | |||||||||||||||||||

| Exchange gain | 679 | 143 | 536 | 374.8 | |||||||||||||||||||

| Other income | 570 | 889 | (319) | (35.9) | |||||||||||||||||||

| Other expense | (9) | (3) | (6) | 200.0 | |||||||||||||||||||

| Profit before tax | 464 | 7,565 | (7,101) | (93.9) | |||||||||||||||||||

| Income taxes expense | (162) | (2,808) | 2,646 | (94.2) | |||||||||||||||||||

| Profit for the year | 302 | 4,757 | (4,455) | (93.7) | |||||||||||||||||||

| Attributable to: | |||||||||||||||||||||||

| Equity holders of APWC | 3,867 | 3,874 | (7) | (0.2) | |||||||||||||||||||

| Non-controlling interests | (3,565) | 883 | (4,448) | (503.7) | |||||||||||||||||||

2022.

|

| 2020 |

| 2019 |

| ||

Average LME copper price ($/Ton) | Q1 |

| 5,638 |

|

| 6,220 |

|

| Q2 |

| 5,341 |

|

| 6,114 |

|

| Q3 |

| 6,521 |

|

| 5,798 |

|

| Q4 |

| 7,174 |

|

| 5,888 |

|

| Year |

| 6,169 |

|

| 6,005 |

|

| 2023 | 2022 | ||||||||||

| Average LME copper price ($/Ton) | Q1 | 8,929 | 9,984 | ||||||||

| Q2 | 8,478 | 9,525 | |||||||||

| Q3 | 8,355 | 7,741 | |||||||||

| Q4 | 8,169 | 8,005 | |||||||||

| Year | 8,483 | 8,814 | |||||||||

35

Total sales in

a decline in sales compared with the previous period.

the decrease in government spending on infrastructure and delay in government projects.

the completion of public sector projects in Singapore.

onerous contracts in the Thailand region.

2022.

our products.

volume in enameled wire as well as loss from onerous contracts.

the increased loss allowance provided for the delinquent accounts.

increase in interest rates in various countries.

Finance

both 2022 and 2023.

The

36

| As of December 31, |

| ||||||||||||||||||||||||||

| 2020 |

| 2019 |

| ||||||||||||||||||||||||

| As of December 31, | As of December 31, | |||||||||||||||||||||||||||

| 2023 | 2023 | 2022 | ||||||||||||||||||||||||||

Foreign currency to US$1: |

|

|

|

|

|

| ||||||||||||||||||||||

| Thai Baht | ||||||||||||||||||||||||||||

| Thai Baht | ||||||||||||||||||||||||||||

Thai Baht |

| 30.02 |

| 29.75 |

| |||||||||||||||||||||||

Singapore $ |

| 1.321 |

| 1.345 |

| |||||||||||||||||||||||

Australian $ |

| 1.297 |

| 1.423 |

| |||||||||||||||||||||||

Chinese RMB |

| 6.525 |

| 6.962 |

| |||||||||||||||||||||||

|

|

| For the Year Ended December 31, |

|

|

|

|

|

|

| ||||

| 2019 |

| 2018 |

| Changes |

| Changes |

| ||||

| US$’000 |

| US$’000 |

| US$’000 |

| % |

| ||||

Income Statement Data: |

|

|

|

|

|

|

|

|

|

|

|

|

Revenue | $ | 338,160 |

| $ | 425,940 |

| $ | (87,780 | ) |

| (20.6 | ) |

Costs of sales |

| (313,373 | ) |

| (389,692 | ) |

| 76,319 |

|

| 19.6 |

|

Gross profit |

| 24,787 |

|

| 36,248 |

|

| (11,461 | ) |

| (31.6 | ) |

Other operating income |

| 385 |

|

| 805 |

|

| (420 | ) |

| (52.2 | ) |

Selling, general and administrative expenses |

| (25,051 | ) |

| (26,924 | ) |

| 1,873 |

|

| 7.0 |

|

Other operating expenses |

| (770 | ) |

| (1,445 | ) |

| 675 |

|

| 46.7 |

|

Operating (loss)/profit |

| (649 | ) |

| 8,684 |

|

| (9,333 | ) |

| (107.5 | ) |

Finance costs |

| (1,012 | ) |

| (1,378 | ) |

| 366 |

|

| 26.6 |

|

Finance income |

| 506 |

|

| 482 |

|

| 24 |

|

| 5.0 |

|

Share of loss of associates |

| (3 | ) |

| (3 | ) |

| — |

|

| — |

|

Exchange gain |

| 1,550 |

|

| 1,741 |

|

| (191 | ) |

| (11.0 | ) |

Other income |

| 717 |

|

| 1,817 |

|

| (1,100 | ) |

| (60.5 | ) |

Other expense |

| (3 | ) |

| (11 | ) |

| 8 |

|

| 72.7 |

|

Profit before tax |

| 1,106 |

|

| 11,332 |

|

| (10,226 | ) |

| (90.2 | ) |

Income taxes expense |

| (2,057 | ) |

| (3,886 | ) |

| 1,829 |

|

| 47.1 |

|

(Loss)/Profit for the year | $ | (951 | ) | $ | 7,446 |

|

| (8,397 | ) |

| (112.8 | ) |

Attributable to: |

|

|

|

|

|

|

|

|

|

|

|

|

Equity holders of APWC |

| (1,632 | ) |

| 2,928 |

|

| (4,560 | ) |

| (155.7 | ) |

Non-controlling interests |

| 681 |

|

| 4,518 |

|

| (3,837 | ) |

| (84.9 | ) |

| For the Year Ended December 31, | |||||||||||||||||||||||

| 2022 | 2021 | Changes | Changes | ||||||||||||||||||||

| US$’000 | US$’000 | US$’000 | % | ||||||||||||||||||||

| Income Statement Data: | |||||||||||||||||||||||

| Revenue | $ | 433,893 | $ | 476,659 | $ | (42,766) | (9.0) | ||||||||||||||||

| Costs of sales | (401,363) | (455,508) | 54,145 | 10.7 | |||||||||||||||||||

| Gross profit | 32,530 | 21,151 | 11,379 | 53.8 | |||||||||||||||||||

| Other operating income | 1,026 | 587 | 439 | 74.8 | |||||||||||||||||||

| Selling, general and administrative expenses | (24,978) | (26,484) | 1,506 | (7.8) | |||||||||||||||||||

| Other operating expenses | (3) | (7) | 4 | 83.2 | |||||||||||||||||||

| Net impairment loss on financial and contract assets | (508) | (220) | (288) | 130.9 | |||||||||||||||||||

| Operating (loss)/profit | 8,067 | (4,973) | 13,040 | 1264.4 | |||||||||||||||||||

| Finance costs | (1,650) | (1,251) | (399) | 26.5 | |||||||||||||||||||

| Finance income | 120 | 123 | (3) | (2.4) | |||||||||||||||||||

| Share of loss of associates | (1) | (1) | — | 66.7 | |||||||||||||||||||

| Exchange gain/(loss) | 143 | (4,425) | 4,568 | (103.2) | |||||||||||||||||||

| Other income | 889 | 671 | 218 | 32.5 | |||||||||||||||||||

| Other expense | (3) | (1) | (2) | 66.7 | |||||||||||||||||||

| Profit before tax | 7,565 | (9,857) | 17,422 | (176.7) | |||||||||||||||||||

| Income taxes expense | (2,808) | 1,345 | (4,153) | (95.2) | |||||||||||||||||||

| Profit/(loss) for the year | 4,757 | (8,512) | 13,269 | 490.0 | |||||||||||||||||||

| Attributable to: | |||||||||||||||||||||||

| Equity holders of APWC | 3,874 | (2,642) | 6,516 | 66.2 | |||||||||||||||||||

| Non-controlling interests | 883 | (5,870) | 6,753 | (115.0) | |||||||||||||||||||

37

2021.

Copper prices indicated in this Annual Report are quoted from the index published by the LME. The 20192022 and 20182021 average copper prices were as follows:

|

| 2019 |

| 2018 |

| ||

Average LME copper price ($/Ton) | Q1 |

| 6,220 |

|

| 6,959 |

|

| Q2 |

| 6,114 |

|

| 6,872 |

|

| Q3 |

| 5,798 |

|

| 6,103 |

|

| Q4 |

| 5,888 |

|

| 6,168 |

|

| Year |

| 6,005 |

|

| 6,525 |

|

| 2022 | 2021 | ||||||||||

| Average LME copper price ($/Ton) | Q1 | 9,984 | 8,479 | ||||||||

| Q2 | 9,525 | 9,711 | |||||||||

| Q3 | 7,741 | 9,371 | |||||||||

| Q4 | 8,005 | 9,697 | |||||||||

| Year | 8,814 | 9,314 | |||||||||

The average copper price in March 2020 on the LME was $5,179 per metric ton.

Total sales in

world economy.

Revenue fromdemand for cables decreased the ROW region decreasedrevenues in Australia.

Gross Profit

While fluctuations in raw material acquisition are preferably placed upon the customer, limiting factors reduced the effects of this strategycopper price fluctuations, which decreased loss on onerous contracts and impacted Gross Profit. A decreasediminution in average copper prices per metric tonthe value of 7.97% plusinventory in 2022 in the intense competition and market slowdown primarily due to the trade war between USA and China all led to the material change in GrossThailand region.

Operating (Loss)

Operating (loss) for 20192022 was $(0.6)$8.1 million, representing a decrease by $9.3an increase of $13 million, or (107.5)%262.2%, from the operating profitloss of $8.7$(5) million in 2018.

2021.

copper prices.

2021.

38

Singapore.

the required working capital due to the decrease in revenue.

The

both 2021 and 2022.

The

| As of December 31, |

| ||||||||||

| 2019 |

| 2018 |

| ||||||||

| As of December 31, | ||||||||||||

| 2022 | ||||||||||||

| 2022 | ||||||||||||

| 2022 | ||||||||||||

| Foreign currency to US$1: | ||||||||||||

| Foreign currency to US$1: | ||||||||||||

Foreign currency to US$1: |

|

|

|

|

|

| ||||||

Thai Baht |

| 29.75 |

| 32.31 |

| |||||||

| Thai Baht | ||||||||||||

| Thai Baht | ||||||||||||

| Singapore $ | ||||||||||||

| Singapore $ | ||||||||||||

Singapore $ |

| 1.345 |

| 1.362 |

| |||||||

Australian $ |

| 1.423 |

| 1.419 |

| |||||||

| Australian $ | ||||||||||||

| Australian $ | ||||||||||||

Chinese RMB |

| 6.962 |

| 6.876 |

| |||||||

| Chinese RMB | ||||||||||||

| Chinese RMB | ||||||||||||

39

better earnings in Thailand in 2022.

|

|

For details of our Company’s bank loans and borrowings, see Note 11(b) to our consolidated financial statements. As of December 31, 2023, a majority of the short-term bank loans and borrowings were held at variable interest rates, whereas the long-term bank loans were held at a fix interest rate.

shares pledged as collateral are unencumbered.

several factors, including decreased net profit, and increased trade receivables, compared to 2022.

40

2021.

equipment in 2023.

equipment in 2022.

Net cash used in financing activities was $17.9 million in 2019. In 2019, net cash used in financing activities reflected primarily the repayment of borrowings.

|

|

The

| Payments due by period | |||||||||||||||||||||||

Contractual obligations (In thousands of US$) | Total | Less than 1 year | 1-5 years | More than 5 years | |||||||||||||||||||

| Interest-bearing loans and borrowings | $ | 57,170 | 57,170 | — | — | ||||||||||||||||||

| Lease obligations | 2,090 | 676 | 1,059 | 355 | |||||||||||||||||||

| Capital commitment relating to factory building improvement and acquisition of machinery | 735 | 725 | 10 | — | |||||||||||||||||||

| Purchase obligations for raw materials | 146,839 | 146,839 | — | — | |||||||||||||||||||

| $ | 206,834 | 205,410 | 1,069 | 355 | |||||||||||||||||||

|

|

•Uncertainty arising from the volatility in the cost of copper, our principal raw material. In 2020, the The yearly average copper price went upper ton decreased from $6,005 (yearly average for 2019) per metric ton$9,314 in 2021 to $6,169 per metric ton (yearly average for 2020).$8,814 in 2022, and to $8,483 in 2023. Under our business model, theour Company, like other companies in the industry, is affected by movements in the price of copper, our principal raw material.

•Fluctuations in the demand for our products in the markets in which we do business. Demand for our products in the markets in which we do business fluctuates based upon variations in the level of governmental and private investments in communications, power and industrial projects and programs that utilize our products. We are not an end-user of our products and, therefore, we depend upon the requirements of our customers to generate sales.

41

|

|

|

|

The following table sets forth the Company’s contractual obligations asNote 3.23 of December 31, 2020:

| Payments due by period |

| ||||||||||

Contractual obligations (In thousands of US$) | Total |

| Less than 1 year |

| 1-5 years |

| More than 5 years |

| ||||

Interest-bearing loans and borrowings | $ | 15,428 |

|

| 10,279 |

|

| 925 |

|

| 4,224 |

|

Lease obligations |

| 2,621 |

|

| 613 |

|

| 1,015 |

|

| 993 |

|

Capital commitment relating to factory building improvement and acquisition of machinery |

| 2,541 |

|

| 2,520 |

|

| 21 |

|

| — |

|

Purchase obligations for raw materials |

| 251,001 |

|

| 251,001 |

|

| — |

|

| — |

|

| $ | 271,591 |

|

| 264,413 |

|

| 1,961 |

|

| 5,217 |

|

For more details on financial commitments and contingencies, please refer to our audited consolidated financial statements and the notes thereto referenced in Item 18: “Financial Statements”.

|

|

Please see the section18 of this report entitled “Cautionary Statement Regarding Forward-Looking Statements”

|

|

|

|

There is only

| Name | Date of Birth | Position | ||||||||||||

Ocorian Services (Bermuda) Limited. | N/A | Resident Assistant | ||||||||||||

Anson Chan | November 3, 1963 | Independent director, Audit Committee Chairman | ||||||||||||

|

|

| ||||||||||||

|

|

| ||||||||||||

|

|

| ||||||||||||

Lambert L. Ding | October 12, 1959 | Independent director, Audit Committee Member | ||||||||||||

42

|

|

| ||||||||||||

Yichin Lee | January 4, 1961 | Independent director, Audit Committee Member | ||||||||||||

|

|

| ||||||||||||

David Sun | December 22, 1953 | Director | ||||||||||||

George Sun | April 4, 1951 | Director | ||||||||||||

| Lee Gai Poo | February 28, 1957 | Director | ||||||||||||

| Yuan Chun Tang | November 26, 1960 | Director, Chief Executive Officer | ||||||||||||

|

|

| ||||||||||||

Ivan Hsia | August 14, 1973 | Chief Financial Officer | ||||||||||||

| Daphne Hsu | August 12, 1962 | Financial Controller | ||||||||||||

Mr. Andy C.C. Cheng was a member of APWC’s Board of Directors from 2004 to 2005 and was re-elected in 2007. Mr. Cheng was appointed as Chairman of the Board in 2009. From 1987 to 2003, Mr. Cheng served as Vice President in charge of procurement at PEWC. Mr. Cheng has been an Executive Vice President at PEWC since 2004 and Chairman of each of the investment divisions of PEWC, Tai Ho Investment Co., Ltd. and You Chi Investment Co., Ltd., since June 2008. Mr. Andy C.C. Cheng is not related to Mr. Fang Hsiung Cheng. Mr. Cheng currently is also a member of PEWC’s Board of Directors.

Mr. Fang Hsiung Cheng has been a member of APWC’s Board of Directors since 2006. He also serves as Assistant Vice President of PEWC. Mr. Fang Hsiung Cheng is not related to Mr. Andy C.C. Cheng.

Ms. Daphne Hsu has been Financial Controller of APWC since March 2005, prior to which she served as Financial Controller for ten years in Taiwan and China at a Thomson SA joint venture.

Mr. Michael C. Lee has been a member of APWC’s Board of Directors since 2004 and is also Chief Executive Officer of PEWC and Chairman of Pacific USA Holdings, Ltd. Mr. Michael C. Lee is not related to Dr. Yichin Lee. Mr. Lee currently is also a member of PEWC’s Board of Directors.

Compensation Committee.

Mr. Alex Chen has beenLee, a member of APWC’sformer Board of Directors since 2015. He also served as Chief Marketing Officer of APWC from July 1, 2015 until December 31, 2019. Mr. Chen was first assigned to PEWC as Engineer, Assistant to General Manager, and later Manager of Quality Assurance Department from 1983 to 2008. He was Managing Director of Siam Pacific Electric Wire & Cable Co. Ltd. in Thailand from 2008 to 2015. Mr. Chen also serves as Vice President and General Division Manager of the General Sales Division of PEWC, and as a Director of the Taiwan Electric Research & Testing Center.

member.

43

Mr. George Sun are siblings.