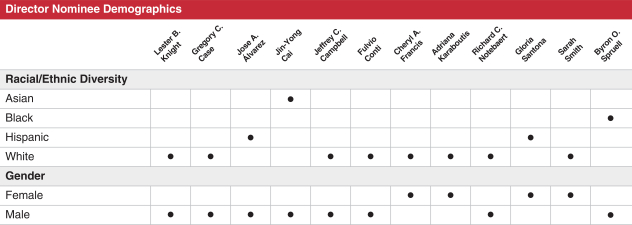

| | The Compensation Committee’s report is provided by the Organization and Compensation Committee, which is composed entirely of the following independent directors: | | | | | Richard C. Notebaert, Chair Jin-Yong Cai Jeffrey C. Campbell | | Cheryl A. Francis | Jin-Yong CaiByron O. Spruell

| | Richard B. Myers

| Jeffrey C. Campbell

| | Carolyn Y. Woo | | | | | | | | | |

2022

2024 Aon Proxy Statement 3941

Executive Compensation The executive compensation disclosure contained in this section reflects compensation information for the years ended December 31, 2021,2023, December 31, 2020,2022, and December 31, 20192021, with respect to our NEOs for all years in which each NEO served in that capacity. The following Summary Compensation Table contains compensation information for the following NEOs: (1) Mr. Case, who served as our Chief Executive Officer during 2021,2023, (2) Ms. Davies, who served as our Chief Financial Officer during 2021,2023, and (3) Mr. Andersen, Ms. Stevens, and Mr. Zeidel, who were our three other most highly compensated executive officers serving as of December 31, 2021. No compensation prior to 2021 is included for Ms. Stevens or Mr. Zeidel because they were not named executive officers for those years.2023. Summary Compensation Table for Fiscal Years 2021, 20202023, 2022 and 20192021 | | Name and Principal Position | | Name and Principal Position | | Name and Principal Position | | Name and Principal Position | | Name and Principal

Position | | Year | | Salary

(S) | | Bonus

($) | | Stock

Awards

($)(1) | | Option

Awards

($) | | Non-Equity

Incentive Plan

Awards

($)(2) | | Change in

Pension Value

and

Nonqualified

Deferred

Compensation

Earnings

($) | | All Other

Compensation

($) | | Total ($) | | | Year | | Salary

($) | | Bonus

($) | | Stock

Awards

($)(1) | | Option

Awards

($) | | Non-Equity

Incentive Plan

Awards

($)(2) | | Change in

Pension Value

and

Nonqualified

Deferred

Compensation

Earnings

($) | | All Other

Compensation

($)(3) | | Total ($) | Gregory C. Case | | | 2021 | | | | 1,500,000 | | | | — | | | | 15,262,436 | | | | — | | | | 2,437,500 | | | | — | | | | 668,448 | | | | 19,868,384 | | | | 2023 | | | | 1,500,000 | | | | — | | | | 21,487,348 | | | | — | | | | — | | | | — | | | | 674,485 | | | | 23,661,834 | | Chief Executive | | 2020 | | | 1,500,000 | | | | — | | | 15,880,566 | | | | — | | | 2,242,500 | | | | — | | | 671,430 | | | 20,294,496 | | | Officer | | | 2019 | | | | 1,500,000 | | | | — | | | | 13,705,798 | | | | — | | | | — | | | | — | | | | 802,045 | | | | 16,007,843 | | Officer | | Officer | | Officer | | Officer | | Christa Davies | | | 2021 | | | | 1,000,000 | | | | — | | | | 8,313,103 | | | | — | | | | 1,365,000 | | | | — | | | | 4,536,093 | | | | 15,214,195 | | | | 2023 | | | | 1,250,000 | | | | — | | | | 25,042,451 | | | | — | | | | — | | | | — | | | | 5,340,367 | | | | 31,632,818 | | Executive Vice President | | 2020 | | | 1,000,000 | | | | — | | | 6,779,055 | | | | — | | | 1,300,000 | | | | — | | | 3,164,888 | | | 12,243,943 | | | and Chief Financial Officer | | and Chief Financial Officer | | and Chief Financial Officer | | and Chief Financial Officer | | and Chief Financial Officer | | | 2019 | | | | 975,000 | | | | — | | | | 5,024,842 | | | | — | | | | — | | | | — | | | | 1,739,576 | | | | 7,739,418 | | Eric Andersen | | | 2021 | | | | 1,000,000 | | | | — | | | | 6,381,328 | | | | — | | | | 1,218,750 | | | | — | | | | 43,450 | | | | 8,643,528 | | | | 2023 | | | | 1,250,000 | | | | — | | | | 23,356,614 | | | | — | | | | — | | | | 108,811 | | | | 50,022 | | | | 24,765,447 | | President | | 2020 | | | 1,000,000 | | | | — | | | 4,358,044 | | | | — | | | 975,000 | | | 307,284 | | | 33,975 | | | 6,674,303 | | | | | | 2019 | | | | 975,000 | | | | — | | | | 3,261,849 | | | | — | | | | — | | | | 417,424 | | | | 47,384 | | | | 4,701,657 | | | | | | | | | | | | | | Lisa Stevens | | | 2021 | | | | 900,000 | | | | — | | | | 2,106,188 | | | | — | | | | 780,000 | | | | — | | | | 34,960 | | | | 3,821,148 | | | | 2023 | | | | 1,000,000 | | | | — | | | | 5,269,440 | | | | — | | | | — | | | | — | | | | 36,446 | | | | 6,305,886 | | Chief People Officer and Head of Human Capital Solutions | | | | | | | | | | | | | | | | | | | Executive Vice President | | | and Chief People Officer | | and Chief People Officer | | and Chief People Officer | | and Chief People Officer | | and Chief People Officer | | Darren Zeidel | | | 2021 | | | | 750,000 | | | | — | | | | 1,534,728 | | | | — | | | | 585,000 | | | | — | | | | 29,100 | | | | 2,898,828 | | | | 2023 | | | | 900,000 | | | | — | | | | 2,573,886 | | | | — | | | | 250,000 | | | | — | | | | 37,695 | | | | 3,761,581 | | EVP, General Counsel and Company Secretary | | | | | | | | | | | | | | | | | | | Executive Vice President, | | General Counsel and | | Company Secretary | |

| (1) | The amounts shown reflect the aggregate grant date fair value (determined in accordance with Financial Accounting Standards Board Accounting Standards Codification Topic 718, Compensation—Stock Compensation (“ASC Topic 718”)) of restricted share unit awards (paid in satisfaction of 35%all or part of each NEO’s annual incentive award for the previous performance year) and performance share unit awards granted to our NEOs pursuant to our Shareholder-Approved Plan in 20212023 and, where applicable, 2020,2022, and 2019.2021. These amounts disregard adjustments for forfeiture assumptions and do not reflect amounts actually paid to, or realized by, the NEOs in the years shown, or any prior years. |

In 2019-2021, each of our NEOs received awards of performance share units under the LPP with a grant date fair value

| LPP Awards. In 2021-2023, each of our NEOs received awards of PSUs under the LPP (and, in the case of Mr. Case, also in satisfaction of a portion of his annual incentive from the previous year) with grant date fair values as set forth in the table below. |

| | | | | | | | | | | | | | Name | | Year | | | Grant Date Fair Value of

Performance Share Unit Awards

Assuming Probable Outcomes

Under LPP

($) | | | Grant Date Fair Value of

Performance Share Unit Awards

Assuming Achievement of

Maximum Performance Levels

Under LPP

($) | | Gregory C. Case | | | 2021 | | | | 14,054,964 | | | | 28,109,929 | | | | | 2020 | | | | 15,880,566 | | | | 31,761,131 | | | | | 2019 | | | | 13,005,880 | | | | 26,011,760 | | Christa Davies | | | 2021 | | | | 7,613,019 | | | | 15,226,039 | | | | | 2020 | | | | 6,779,055 | | | | 13,558,110 | | | | | 2019 | | | | 4,464,926 | | | | 8,929,852 | | Eric Andersen | | | 2021 | | | | 5,856,437 | | | | 11,712,874 | | | | | 2020 | | | | 4,358,044 | | | | 8,716,089 | | | | | 2019 | | | | 2,911,923 | | | | 5,823,846 | | Lisa Stevens | | | 2021 | | | | 1,756,260 | | | | 3,512,521 | | Darren Zeidel | | | 2021 | | | | 1,219,656 | | | | 2,439,312 | |

| | | | | | | | | | | | | | Name | | Year | | | Grant Date Fair Value of

Performance Share Unit Awards

Assuming Probable Outcomes

Under LPP

($) | | Grant Date Fair Value of

Performance Share Unit Awards

Assuming Achievement of

Maximum Performance Levels

Under LPP

($) | | | Gregory C. Case | | | 2023 | | | 19,293,739 | | 38,587,479 | | | | | | 2022 | | | 17,497,455 | | 34,994,910 | | | | | | 2021 | | | 14,054,964 | | 28,109,929 | | | Christa Davies | | | 2023 | | | 7,839,084 | | 15,678,167 | | | | | | 2022 | | | 6,873,311 | | 13,746,622 | | | | | | 2021 | | | 7,613,019 | | 15,226,039 | | | Eric Andersen | | | 2023 | | | 6,369,181 | | 12,738,362 | | | | | | 2022 | | | 5,400,548 | | 10,801,096 | | | | | | 2021 | | | 5,856,437 | | 11,712,874 | | | Lisa Stevens | | | 2023 | | | 3,919,542 | | 7,839,084 | | | | | | 2022 | | | 2,945,838 | | 5,891,676 | | | | | | 2021 | | | 1,756,260 | | 3,512,521 | | | Darren Zeidel | | | 2023 | | | 1,763,823 | | 3,527,647 | | | | | | 2022 | | | 1,570,927 | | 3,141,854 | | | | | | 2021 | | | 1,219,656 | | 2,439,312 |

40 202242 2024 Aon Proxy Statement

| July 2023 PSUs. On July 26, 2023, the Compensation Committee approved special grants of PSUs to each of Ms. Davies and Mr. Andersen with grant date fair values, assuming probable outcomes, of $14,737,500 each. |

| | For awards granted under the LPP and the July 2023 PSUs, the grant date fair value of performance share unitsPSUs is calculated in accordance with ASC Topic 718 based on the probable outcome of the performance conditions at the time of grant. See Note 12 “Share-Based Compensation Plans” of the Notes to Consolidated Financial Statements in Part II, Item 8 of the Company’s Form 10-K for the year ended December 31, 2023 for information regarding assumptions underlying the valuation of equity awards. Set forth above are the grant date fair values of the performance share unit awardsPSUs granted under the LPP and the July 2023 PSUs, calculated assuming (i) the probable outcome of the performance conditions for each program, which amount is included in the “Stock Awards” column of this Summary Compensation Table and (ii) for units granted under the LPP, achievement of the maximum levels of performance (which is the dollar value attributed to the original award multiplied by 200% for each year shownperformance. No maximum amounts are reflected for the LPP).July 2023 PSUs because the threshold performance level has not been achieved. The amounts shown in the tabletables above reflect the aggregate grant date fair value for these awards computed in accordance with ASC Topic 718, and do not correspond to the actual value that will be recognized by our NEOs. |

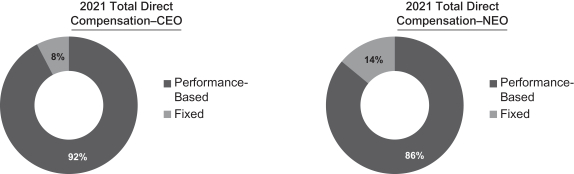

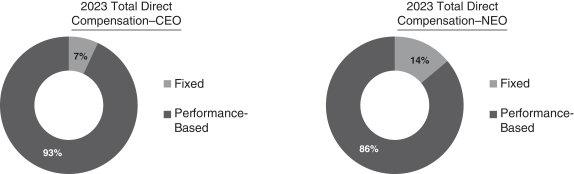

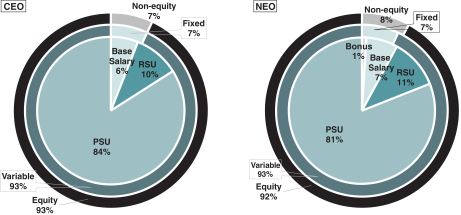

| (2) | The amounts shown in the “Non-Equity Incentive Plan Compensation” column for each of 2021, 2020,2023, 2022, and 20192021 reflect the cash portion of the annual incentive awards earned by the NEOs for performance in those years (generally, underyears. For 2021, 65% was paid in the termsform of those awards,cash and 35% has beenwas paid in the form of restricted share units (reported in the “Stock Awards Column”), andexcept that Mr. Case received 35% in the form of PSUs. For 2022, 100% was paid in the form of restricted share units, except that Mr. Case received 65% in the form of cash; provided, however, that Mr. Case receivedrestricted share units and 35% of his 2021 annual incentive award in the form of performancePSUs. For 2023, other than for Mr. Zeidel, 100% was paid in the form of PSUs with terms similar to LPP 19 awards, except that such units are also subject to attainment of a share units under LPP 17). Theseprice hurdle. For Mr. Zeidel, in addition to the PSUs, he received a portion ($250,000) of his annual incentive in cash. All amounts shown in this column were actually paid or granted to the NEOs in the first quarter of the year following the relevant performance year, which, for annual awards settled in share units, causes the amounts to be reflected as stock awards in the Summary Compensation Table two years following the relevant performance year. |

| (3) | For 2021,2023, the amounts reported as “All Other Compensation” consist of the following components: |

| | Name | | Company

Contributions

($)(a) | | Perquisites

($)(b) | | Other

($)(c) | | Tax

Reimbursements

($)(d) | | Total ($) | | Company

Contributions

($)(a) | | Perquisites

($)(b) | | Other

($)(c) | | Tax

Reimbursements

($)(d) | | Total ($) | | Gregory C. Case | | | 31,450 | | | | 22,485 | | | | 614,513 | | | | — | | | | 668,448 | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | | Christa Davies | | Christa Davies | | Christa Davies | | Christa Davies | | Christa Davies | | | 29,350 | | | | 52,035 | | | | 527,510 | | | | 3,927,197 | | | | 4,536,093 | | | Eric Andersen | | | 31,450 | | | | 12,000 | | | | — | | | | — | | | | 43,450 | | Eric Andersen | | Eric Andersen | | Eric Andersen | | Eric Andersen | | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | | 25,150 | | | | 9,810 | | | | — | | | | — | | | | 34,960 | | | Darren Zeidel | | | 27,250 | | | | 1,850 | | | | — | | | | — | | | | 29,100 | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | |

| | (a) | The amounts shown in the “Company Contributions” column represent, for each of our NEOs, (i) a contribution by Aon of $18,850$21,450 for each of Mr. Case, Ms. Stevens, and Mr. Zeidel, and $18,450$21,150 for each of Ms. Davies and Mr. Andersen to the Aon Savings Plan, our qualified defined contribution plan; and (ii) a contribution by Aon of $12,600 to$10,200 for Mr. Case, $10,900 to$10,500 for each of Ms. Davies $13,000 forand Mr. Andersen, $6,300$6,800 for Ms. Stevens, and $8,400$8,500 for Mr. Zeidel to the Aon Supplemental Savings Plan, a nonqualified defined contribution plan. |

| | (b) | In connection with the 2012 Redomestication, certain of our NEOsMr. Case and Ms. Davies have agreed to relocate toprovide services primarily at Aon’s London, U.K. Theheadquarters. They are each provided relocation packages that are intended to keep the transferred executivesthem “whole” on a total rewards basis, be transparent and equitable, and reflect competitive practices and benchmarks of industry counterparts. This column also includes amounts Aon paid to third parties for Ms. Davies’ eligible dependents’ schooling or assistance in preparing her tax returns in connection with the 2012 Redomestication.her international assignment.

|

| | | In 2021,2023, the Company provided perquisites to Ms. Davies related to the relocationassignment of $44,128$54,914 for schooling assistance and $6,057$31,346 for tax preparation services. |

| | | For a description of cash allowances and cash bonuses paid to our NEOs in connection with the relocation,international assignments, see footnote (c) below. |

| | | Mr. Case,All NEOs except Ms. Davies Ms. Stevens and Mr. Zeidel each participated in Aon’s executive health screening program in 2021.2023. The actual cost to Aon of the NEO’s use of this program was $1,850 per NEO.$7,687 for Mr. Case, $5,000 for Mr. Andersen, $4,356 for Ms. Stevens, and $6,620 for Mr. Zeidel.

|

| | | As part of Mr. Case’s employment agreement, Aon provides him with life insurance coverage in the amount no less than $5,000,000 during the term of his agreement. This amount reflects the cost above and beyond the cost of life insurance that is provided to a typical Aon employee. For 2021,2023, the cost was $20,635. |

| | | Ms. Stevens received reimbursement for club dues of $7,960.$3,840. Mr. Andersen received an annual car allowance of $12,000. |

| | | We maintain an arrangement with NetJets for use of chartered aircraft and associated ground travel as necessary. Infrequently, a NEO will use a NetJets flight for personal purposes, or the spouse or guests of a NEO may accompany the executive when a NetJets flight is already going to a specific destination for a business purpose. In the case of a personal flight, the cost to the Company of such flight is reimbursed to the Company by the NEO. In the case of a spouse or other guest on a business flight, this has a minimal cost to the Company and, where applicable, the variable costs associated with the additional passenger are included in determining the aggregate incremental cost to the Company. No amounts were included in the Summary Compensation Table this year with respect to such aircraft. |

2024 Aon Proxy Statement 43

| | (c) | In connection with their relocationinternational assignment to London, U.K., certain NEOsMr. Case and Ms. Davies are entitled to additional cash compensation in accordance with the terms of their international assignment letters and our relocation programs. Allowances became payable to the NEOs beginning on the date the NEO’s foreign assignment began and will terminate at the end of the foreign assignment. The following table sets forth the additional compensation received by the NEOsthem with respect to 20212023 service: |

| | Name | | Housing

Allowance

($) | | Cost of

Living

Allowance ($) | | Foreign

Service

Allowance

($) | | Transportation

Allowance ($) | | Total ($) | | Housing

Allowance ($) | | Cost of

Living

Allowance ($) | | Foreign

Service

Allowance ($) | | Transportation Allowance ($) | | Total ($) | | Gregory C. Case | | | 382,013 | | | | 97,500 | | | | 135,000 | | | | — | | | | 614,513 | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | | Christa Davies | | | 286,510 | | | | 97,500 | | | | 120,000 | | | | 23,500 | | | | 527,510 | | Christa Davies | | Christa Davies | | Christa Davies | | Christa Davies | |

2022 Aon Proxy Statement 41

| | (d) | In connection with her relocation to London, U.K.,international assignment, Ms. Davies is entitled to receive a tax equalization benefit designed to equalize the income tax paid by her so that her total income and social tax costs related to any earnings from the Company while on the international assignment |

| | (including (including earnings related to granting or vesting of equity-based awards) will be no more than an amount she would have paid had all of the earnings been taxable solely pursuant to U.S. income and social tax laws.

|

| | | The tax equalization benefit caps the executive’s total income and social tax exposure to what she would be taxed on earnings from the Company under the U.S. tax laws (as compared to the U.K. tax laws as in existence from time to time). This policy is designed and intended to yield neither an economic benefit nor detriment to Ms. Davies as a result of her international assignment. |

| | | For Ms. Davies, any applicable schooling assistance and allowances for foreign service, housing, cost of living, home leave, and transportation are grossed up for applicable U.S. taxes. |

| | | The amounts shown in the “All Other Compensation” table represent Aon’s calculation of the excess U.K. taxes paid above the hypothetical tax that Ms. Davies would have paid had she not been relocated to London, U.K. and the amount paid by Aon to neutralize the tax impact on Ms. Davies with respect to eligible relocation compensation. |

Employment Agreements and Other Compensation Agreements Mr. Case’s Employment Agreement We are party to an Amended and Restated Employment Agreementemployment agreement with Gregory C.Mr. Case pursuant to which he serves as our Chief Executive Officer. The current term of Mr. Case’s agreement continues through April 1, 2026,2028, unless terminated earlier or extended. The agreement also provides that Mr. Case will be nominated for re-election as a member of the Board at each annual general meeting of shareholders during the period of his employment. Mr. Case’s employment agreement provides for an initial base salary of $1,500,000, subject to adjustment at the discretion of the Board, and a target annual incentive bonus of not less than 200% of base salary, subject to the provisions of our Shareholder-Approved Plan. The Board retains the discretion to determine Mr. Case’s actual bonus payment. In the first quarter of 2022, the Compensation Committee performed its annual compensation review (as described above under “The Executive Compensation Process”) and adjusted Mr. Case’s target annual incentive to 250% of base salary. In addition, Mr. Case’s agreement provides that he will be provided with life insurance coverage in an amount equal to no less than $5,000,000 during the term of the agreement. Under the agreement, Mr. Case has also agreed to maintain an investment position in Aon Class A Ordinary Shares equal to no less than 20 times his annual base salary. Ms. Davies’s Employment Agreement We are party to an Employment Agreementemployment agreement with ChristaMs. Davies pursuant to which she serves as our Executive Vice President and Chief Financial Officer. The current term of Ms. Davies’s agreement continues through April 1, 2026, unless terminated earlier or extended. The agreement provides for an initial base salary which has subsequently been adjusted by our Compensation Committee as permitted under the agreement, and a target annual incentive bonus of 150% of her base salary and foreign service allowance. In the first quarter of 2022, the Compensation Committee performed its annual compensation review (as described above under “The Executive Compensation Process”) and adjusted Ms. Davies’s base salary to $1,250,000 and target annual incentive to 200% of base salary. On April 1, 2024, Ms. Davies notified the Company of her intention to retire from the position of Chief Financial Officer. Ms. Davies will continue to serve as Chief Financial Officer into the third quarter of 2024 and will thereafter remain at the Company as a senior advisor for a transition period into 2025. Mr. Andersen’s Employment Agreement and Letter We have provided Eric Andersenare party to an employment letteragreement with Mr. Andersen, effective July 1, 2023, pursuant to which he serves as our President.President of the Company and Aon Corporation. The letter provides thatcurrent term of Mr. Andersen’s continuedagreement continues until June 30, 2026, unless earlier terminated or extended. The employment with us is on an at-will basis, and that he is eligible to participate in our Combined Severance Plan.agreement supersedes Mr. Andersen’s employment letter also 44 2024 Aon Proxy Statement

confirming certain terms and conditions of his at-will employment dated as of May 11, 2018. Mr. Andersen’s agreement provides for an initial base salary of no less than $1,250,000 per year, and an initial target annual bonus, both of which have been adjusted by the Compensation Committee as permitted under the letter. In early 2021, the Compensation Committee approved an increase to Mr. Andersen’sa target annual incentive from 100% to 150%. In the first quarter of 2022, the Compensation Committee performed its annual compensation review (as described above under “The Executive Compensation Process”) and adjusted Mr. Andersen’s target annual incentive tono less than 200% of his base salary. The agreement also provides for the grant of the July 2023 PSUs. Ms. Stevens’s Employment Letter We have provided LisaMs. Stevens an employment letter pursuant to which she serves as our Executive Vice President and Chief People Officer and Head of Human Capital Solutions.Officer. The letter provides that Ms. Stevens’s continued employment with us is on an at-will basis, and that she is eligible to participate in our Combined Severance Plan. Ms. Stevens’s letter also provides for an initial base salary, which has subsequently been adjusted to $1,000,000 by our Compensation Committee as permitted under the letter, a target annual bonus 42 2022 Aon Proxy Statement

of 100% of her base salary, which has subsequently been adjusted to 150% by our Compensation Committee as permitted under the letter, and an initial target long-term incentive award of 150% of her base salary. In the first quarter of 2022, the Compensation Committee performed its annual compensation review (as described above under “The Executive Compensation Process”) and adjusted Ms. Stevens’s target annual incentive to 150% of her base salary. Mr. Zeidel’s Employment Letter We have provided DarrenMr. Zeidel an employment letter pursuant to which he serves as our Executive Vice President, General Counsel, and Company Secretary. The letter provides that Mr. Zeidel’s continued employment with us is on an at-will basis, and that he is eligible to participate in our Combined Severance Plan. Mr. Zeidel’s letter also provides for an initial base salary, which has subsequently been adjusted to $900,000 by our Compensation Committee as permitted under the letter, a target annual bonus of 100% of his base salary, and an initial target long-term incentive award of 150% of his base salary. International Assignment Letters In connection with the Company’s 2012 Redomestication,their agreeing to provide services primarily at Aon’s London global operational headquarters, we entered into international assignment letters with each of Mr. Case and Ms. Davies. These letters describe the international assignments and set forth the relocation benefits to the executives, which are described below. The letters are not intended to diminish the rights of the executives under their current employment arrangements; however, the letters provide by their terms that the executives’ acceptance of their international assignments, and repatriation thereafter, will not give rise to any right to terminate for good reason (as such term is defined in the applicable executive’s employment agreement, if applicable). The letters for Mr. Case and Ms. Davies were amended and extended in July 2014 for an additional two years, onin July 1, 2016 for an additional two years, and on each July 1 of 2018 through 20212023 for an additional year. Depending on each executive’s personal circumstances, and as disclosed in the tables above, the relocation packages, as amended, generally provide some or all of the following benefits: a monthly housing allowance of approximately $31,834 for Mr. Case and $23,876 for Ms. Davies;

| • | | a monthly housing allowance of approximately $31,834 for Mr. Case and $23,876 for Ms. Davies; |

a monthly cost of living differential of $8,125;

| • | | a monthly cost of living differential of $8,125; |

a monthly foreign service allowance of $11,250 for Mr. Case, and $10,000 for Ms. Davies;

| • | | a monthly foreign service allowance of $11,250 for Mr. Case, and $10,000 for Ms. Davies; |

a monthly car allowance of approximately $1,958 for Ms. Davies;

| • | | a monthly car allowance of approximately $1,958 for Ms. Davies; |

eligible dependents’ schooling assistance, including tuition and application fees, for Ms. Davies;

| • | | eligible dependents’ schooling assistance, including tuition and application fees, for Ms. Davies; |

a tax equalization benefit for Ms. Davies, designed to equalize the income tax paid by her so that her total income and social tax costs related to any earnings from the Company while on the international assignment (including earnings related to granting or vesting of equity-based awards) will be no more than an amount she would have paid had all of the earnings been taxable solely pursuant to the U.S. income and social tax laws;

| • | | a tax equalization benefit for Ms. Davies, designed to equalize the income tax paid by her so that her total income tax costs related to any earnings from the Company while on the international assignment (including earnings related to granting or vesting of equity-based awards) will be no more than an amount she would have paid had all of the earnings been taxable solely pursuant to the U.S. income tax laws; |

a tax gross-up for Ms. Davies on schooling assistance and on allowances related to housing, cost of living, home leave, and transportation; and

| • | | a tax gross-up for Ms. Davies on schooling assistance and on allowances related to housing, cost of living, home leave, and transportation; and |

enhanced tax preparation and planning and expatriate services for the tax years covered by the international assignment or for which international earnings are taxed by the U.K. or Ireland.

| • | | enhanced tax preparation and planning and expatriate services for the tax years covered by the international assignment or for which international earnings are taxed by the U.K. or Ireland. |

All of the relocation benefits are subject to recoupment if the executive officer resigns employment with the Company within two years of commencing the international assignment, or 12 months after the end of the assignment, and becomes employed by a direct competitor of the Company. 20222024 Aon Proxy Statement 4345

Grants of Plan-Based Awards in Fiscal Year 20212023 The following table provides information on non-equity incentive plan compensation, restricted share unit awards, and performance share unit awards granted in 20212023 to each of the NEOs. | | | Name | | Grant

Date | | Estimated Possible

Payouts Under

Non-Equity Incentive

Plan Awards (1) | | | | Estimated Future Payouts Under

Equity Incentive Plan Awards (2) | | All

Other

Stock

Awards:

Number

of

Shares

of Stock

or Units

(#)(3) | | All Other

Option

Awards:

Number of

Securities

Underlying

Options

(#) | | Exercise

or Base

Price of

Option

Awards

($/Sh) | | Grant

Date Fair

Value of

Stock and

Option

Awards

($)(4) | | Target

($) | | Maximum

($) | | | | Threshold

(#) | | Target

(#) | | Maximum

(#) | | Name | | | | Name | | Name | | Grant

Date | | Estimated Possible

Payouts Under

Non-Equity Incentive

Plan Awards (1) | | | | Estimated Future Payouts Under Equity Incentive Plan Awards (2) | | All

Other

Stock

Awards:

Number

of

Shares

of

Stock

or Units

(#)(3) | | All Other

Option

Awards:

Number of

Securities

Underlying Options

(#) | | Exercise

or Base

Price of

Option

Awards

($/Sh) | | Grant

Date Fair

Value of

Stock and

Option

Awards

($)(4) | | Target

($) | | Maximum

($) | | | | Threshold

(#) | | Target

(#) | | Maximum

(#) | | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | | 2/12/2021 | | | | 3,000,000 | | | | 6,000,000 | | | | — | | | | — | | | | — | | | | 5,295 | | | | — | | | | — | | | | 1,207,472 | | | | | 3/26/2021 | | | | — | | | | — | | | | | | 31,536 | | | | 63,072 | | | | 126,144 | | | | — | | | | — | | | | — | | | | 14,054,964 | | | Christa Davies | | Christa Davies | | Christa Davies | | Christa Davies | | Christa Davies | | | 2/11/2021 | | | | 1,680,000 | | | | 3,360,000 | | | | — | | | | — | | | | — | | | | 3,053 | | | | — | | | | — | | | | 700,083 | | | | | 3/25/2021 | | | | — | | | | — | | | | 11,776 | | | | 23,552 | | | | 47,104 | | | | — | | | | — | | | | — | | | | 5,171,077 | | | | | 8/6/2021 | | | | — | | | | — | | | | | | 4,780 | | | | 9,559 | | | | 19,118 | | | | — | | | | — | | | | — | | | | 2,441,942 | | | | | | | | | | | | | | | | | Eric Andersen | | Eric Andersen | | Eric Andersen | | Eric Andersen | | Eric Andersen | | | 2/11/2021 | | | | 1,500,000 | | | | 3,000,000 | | | | — | | | | — | | | | — | | | | 2,289 | | | | — | | | | — | | | | 524,891 | | | | | 3/25/2021 | | | | — | | | | — | | | | 8,888 | | | | 17,775 | | | | 35,550 | | | | — | | | | — | | | | — | | | | 3,902,679 | | | | | 8/6/2021 | | | | — | | | | — | | | | | | 3,824 | | | | 7,648 | | | | 15,296 | | | | — | | | | — | | | | — | | | | 1,953,758 | | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | | 2/11/2021 | | | | 900,000 | | | | 1,800,000 | | | | — | | | | — | | | | — | | | | 1,526 | | | | — | | | | — | | | | 349,927 | | | | | 3/25/2021 | | | | — | | | | — | | | | | | 4,000 | | | | 7,999 | | | | 15,998 | | | | — | | | | — | | | | — | | | | 1,756,260 | | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | | | 2/11/2021 | | | | 750,000 | | | | 1,500,000 | | | | — | | | | — | | | | — | | | | 1,374 | | | | — | | | | — | | | | 315,072 | | | | | 3/25/2021 | | | | — | | | | — | | | | 2,778 | | | | 5,555 | | | | 11,110 | | | | — | | | | — | | | | — | | | | 1,219,656 | |

| (1) | The amounts shown relate to potential annual incentive plan awards for 20212023 service for each NEO under our Shareholder-Approved Plan. The amounts shown as “Target” represent the target payment level of 200%250% for Mr. Case, 150%200% for Ms. Davies and Mr. Andersen, 150% for Ms. Stevens, and 100% for each of Ms. Stevens and Mr. Zeidel, of their respective base salaries (after giving effect to annual increases), and the amounts shown in “Maximum” reflect the maximum payment level of two times the target incentive amount, as provided by the terms of our Shareholder-Approved Plan. For Ms. Davies, the annual foreign service allowance is included with base salary in determining her bonus target. |

| Our Shareholder-Approved Plan does not contain a threshold payment level for any of the NEOs. If pre-establishedOur Shareholder-Approved Plan does not contain a threshold payment level for any of the NEOs. If pre-established performance measures are not met, no payments are made.

|

| (2) | The amounts shown in columns titled “Threshold,” “Target,” and “Maximum” represent the threshold, target, and maximum number of performance share units(a) PSUs granted to our NEOs pursuant to Aon’s LPP 1618 (and, for Mr. Case, in respect of 35% of his 2022 annual incentive award) that will be earned and settled in Class A Ordinary Shares if certain performance criteria are achieved during the 20212023 to 2025 performance period, and (ii) for Ms. Davies and Mr. Andersen, PSUs granted to them on July 26, 2023 performance period.(the July 2023 PSUs). As the potential payments for these units are dependent on achieving certain performance criteria, actual payouts could differ by a significant amount. For more information regarding the terms of these performance share units andthe PSUs granted pursuant to LPP 16,18, see the section titled “Leadership Performance Program under Our Shareholder-Approved Plan” in the CD&A. For more information regarding the terms of the July 2023 PSUs, see the section titled “July 2023 Long-Term Performance-Based Awards” in the CD&A. |

| (3) | The amounts shown in this column represent the number of restricted share units granted to each NEO in 20212023 in satisfaction of 35%100% of the annual incentive award earned by such NEO for 2020 performance.2022 performance, other than Mr. Case, who received 65% in the form of restricted share units. Within the framework of our Shareholder-Approved Plan, the target amount of each NEO’s annual incentive award for 20202022 performance (calculated as a percentage of base salary and, with respect to Ms. Davies, her annual foreign service allowance) was 200% for Mr. Case, 150% for each of Ms. Davies and Mr. Andersen, 150% for Ms. Stevens, and 100% for each of Ms. Stevens and Mr. Zeidel; the bonus range was capped at 400% for Mr. Case, 300% for each of Ms. Davies and Mr. Andersen, 300% for Ms. Stevens, and 200% for each of Ms. Stevens and Mr. Zeidel. The determination of the actual incentive amount payable was determined based, among other things, on Aon’s overall performance and an individual performance assessment. These restricted share units will vest in installments of 331/3% on the first through third anniversaries of the date of grant. DividendEffective with grants in 2023 onward, dividend equivalents are paid quarterly in cash on unvestedwill accumulate and pay when the restricted share units and votingunit vests. Voting rights do not attach to any unvested restricted share units. |

| (4) | The amounts shown in this column are the grant date fair values of the restricted share units and performance share units.PSUs. The grant date fair value reflects the aggregate grant date fair value computed in accordance with ASC Topic 718 and, with respect to the performance share unit awards granted under the LPP and the July 2023 PSUs, is based on the probable outcome of the performance-based conditions at the time of grant. These amounts do not correspond to the actual value (if any) that may be recognized by the NEOs. For additional information about the applicable assumptions for determining the grant date fair value of restricted share unit awards, see footnote (1) to the Summary Compensation Table. |

44 202246 2024 Aon Proxy Statement

Outstanding Equity Awards at 20212023 Fiscal Year-End The following table sets forth information regarding outstanding restricted share units and performance share unitsPSUs held by each of our NEOs on December 31, 2021.2023. See “Potential Payments and Benefits on Termination or Change in Control” for information regarding the impact of certain employment termination scenarios on outstanding equity awards. | | | | | | Stock Awards | | Stock Awards | | Name | | Grant

Date | | Number of Shares or

Units of Stock That

Have Not Vested

(#) | | Market Value of

Shares or Units

of Stock That

Have Not Vested

($)(4) | | Equity Incentive Plan

Awards: Number of

Unearned Shares,

Units or Other Rights

That Have Not Vested

(#) | | Equity Incentive Plan

Awards: Market or

Payout Value of

Unearned Shares,

Units or Other Rights

That Have Not Vested

($)(4) | | Grant

Date | | Number of Shares or

Units of Stock That

Have Not Vested

(#) | | Market Value of

Shares or Units

of Stock That

Have Not Vested

($)(5) | | Equity Incentive Plan

Awards: Number of

Unearned Shares,

Units or Other Rights

That Have Not Vested

(#) | | Equity Incentive Plan

Awards: Market or

Payout Value of

Unearned Shares,

Units or Other Rights

That Have Not Vested

($)(5) | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | | 2/15/2019 | (1) | | | 1,357 | | | | 407,860 | | | | — | | | | — | | | | | 3/29/2019 | (2) | | | 157,000 | | | | 47,187,920 | | | | — | | | | — | | | | | 3/27/2020 | (3) | | | — | | | | — | | | | 198,284 | | | | 59,596,239 | | | | | 2/12/2021 | (1) | | | 5,295 | | | | 1,591,465 | | | | — | | | | | 3/26/2021 | (3) | | | — | | | | — | | | | 126,144 | | | | 37,913,841 | | | | | Christa Davies | | Christa Davies | | Christa Davies | | Christa Davies | | Christa Davies | | | 2/14/2019 | (1) | | | 1,101 | | | | 330,917 | | | | — | | | | — | | | | | 3/28/2019 | (2) | | | 54,384 | | | | 16,345,655 | | | | — | | | | — | | | | | 3/26/2020 | (3) | | | — | | | | — | | | | 84,490 | | | | 25,394,314 | | | | | 2/11/2021 | (1) | | | 3,053 | | | | 917,610 | | | | — | | | | — | | | | | 3/25/2021 | (3) | | | — | | | | — | | | | 47,104 | | | | 14,157,578 | | | | | 8/6/2021 | (3) | | | — | | | | — | | | | 19,118 | | | | 5,746,106 | | | | | | | | Eric Andersen | | Eric Andersen | | Eric Andersen | | Eric Andersen | | Eric Andersen | | | 2/14/2019 | (1) | | | 688 | | | | 206,785 | | | | — | | | | — | | | | | 3/28/2019 | (2) | | | 35,468 | | | | 10,660,262 | | | | — | | | | — | | | | | 3/26/2020 | (3) | | | — | | | | — | | | | 54,316 | | | | 16,325,217 | | | | | 2/11/2021 | (1) | | | 2,289 | | | | 687,982 | | | | | | 3/25/2021 | (3) | | | — | | | | — | | | | 35,550 | | | | 10,684,908 | | | | | 8/6/2021 | (3) | | | — | | | | — | | | | 15,296 | | | | 4,597,366 | | | | | | | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | | 2/22/2019 | (1) | | | 1,917 | | | | 576,174 | | | | — | | | | — | | | | | 3/28/2019 | (2) | | | 3,546 | | | | 1,065,786 | | | | — | | | | — | | | | | 2/13/2020 | (1) | | | 746 | | | | 224,218 | | | | — | | | | — | | | | | 3/26/2020 | (3) | | | — | | | | — | | | | 14,484 | | | | 4,353,311 | | | | | 2/11/2021 | (1) | | | 1,526 | | | | 458,655 | | | | — | | | | — | | | | | 3/25/2021 | (3) | | | — | | | | — | | | | 15,998 | | | | 4,808,359 | | | | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | | | 5/19/2017 | (1) | | | 157 | | | | 47,188 | | | | — | | | | — | | | | | 3/15/2019 | (1) | | | 148 | | | | 44,483 | | | | — | | | | — | | | | | 3/28/2019 | (2) | | | 4,848 | | | | 1,457,115 | | | | — | | | | — | | | | | 5/21/2019 | (1) | | | 132 | | | | 39,674 | | | | — | | | | — | | | | | 2/13/2020 | (1) | | | 224 | | | | 67,325 | | | | — | | | | — | | | | | 3/26/2020 | (3) | | | — | | | | — | | | | 13,880 | | | | 4,171,773 | | | | | 2/11/2021 | (1) | | | 1,374 | | | | 412,969 | | | | — | | | | — | | | | | 3/25/2021 | (3) | | | — | | | | — | | | | 11,110 | | | | 3,339,222 | |

2022 Aon Proxy Statement 45

| (1) | The vesting schedule for the restricted share units, other than performance share units,PSUs, held by each NEO is as follows: |

| | | | | | | | | | | | | | | | | | | | | | | | | | | Vesting Date | | Gregory

C. Case | | Christa

Davies | | Eric

Andersen | | Lisa

Stevens | | Darren

Zeidel | 2/11/2022 | | | | | | | | | 1,017 | | | | | 763 | | | | | 508 | | | | | 458 | | 2/12/2022 | | | | 1,765 | | | | | | | | | | | | | | | | | | | | | | 2/13/2022 | | | | | | | | | | | | | | | | | | | 373 | | | | | 112 | | 2/14/2022 | | | | | | | | | 1,101 | | | | | 688 | | | | | | | | | | | | 2/15/2022 | | | | 1,357 | | | | | | | | | | | | | | | | | | | | | | 2/22/2022 | | | | | | | | | | | | | | | | | | | 639 | | | | | | | 3/15/2022 | | | | | | | | | | | | | | | | | | | | | | | | 148 | | 5/19/2022 | | | | | | | | | | | | | | | | | | | | | | | | 157 | | 5/21/2022 | | | | | | | | | | | | | | | | | | | | | | | | 44 | | 2/11/2023 | | | | | | | | | 1,018 | | | | | 763 | | | | | 509 | | | | | 458 | | 2/12/2023 | | | | 1,765 | | | | | | | | | | | | | | | | | | | | | | 2/13/2023 | | | | | | | | | | | | | | | | | | | 373 | | | | | 112 | | 2/22/2023 | | | | | | | | | | | | | | | | | | | 639 | | | | | | | 5/21/2023 | | | | | | | | | | | | | | | | | | | | | | | | 44 | | 2/11/2024 | | | | | | | | | 1,018 | | | | | 763 | | | | | 509 | | | | | 458 | | 2/12/2024 | | | | 1,765 | | | | | | | | | | | | | | | | | | | | | | 2/22/2024 | | | | | | | | | | | | | | | | | | | 639 | | | | | | | 5/21/2024 | | | | | | | | | | | | | | | | | | | | | | | | 44 | | | | | | | | Total | | | | 6,652 | | | | | 4,154 | | | | | 2,977 | | | | | 4,189 | | | | | 2,035 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | Vesting Date | | Gregory

C. Case | | Christa

Davies | | Eric

Andersen | | Lisa

Stevens | | Darren

Zeidel | | | 2/11/2024 | | | | | | | | | 1,018 | | | | | 763 | | | | | 509 | | | | | 458 | | | | 2/12/2024 | | | | 1,765 | | | | | | | | | | | | | | | | | | | | | | | | 2/16/2024 | | | | | | | | | 2,649 | | | | | 2,417 | | | | | 1,450 | | | | | 870 | | | | 2/17/2024 | | | | 2,356 | | | | | 872 | | | | | 778 | | | | | 498 | | | | | 374 | | | | 2/22/2024 | | | | | | | | | | | | | | | | | | | 639 | | | | | | | | | 5/21/2024 | | | | | | | | | | | | | | | | | | | | | | | | 44 | | | | 2/16/2025 | | | | | | | | | 2,649 | | | | | 2,417 | | | | | 1,450 | | | | | 870 | | | | 2/17/2025 | | | | 2,357 | | | | | 872 | | | | | 779 | | | | | 498 | | | | | 374 | | | | 2/16/2026 | | | | | | | | | 2,650 | | | | | 2,418 | | | | | 1,451 | | | | | 871 | | | | 2/17/2026 | | | | 2,357 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | Total | | | | 8,835 | | | | | 10,710 | | | | | 9,572 | | | | | 6,495 | | | | | 3,861 | |

2024 Aon Proxy Statement 47

| (2) | The performance share units convert into Class A Ordinary Shares on a one-to-one basis after the conclusion of a three-year performance period. For performance share units with a March 28, 2019 or March 29, 2019 grant date, the three-year performance period ended on December 31, 2021. These performance share units were subsequently settled in Class A Ordinary Shares on February 17, 2022. |

(3) | The performance share units,PSUs, to the extent earned, convert into Class A Ordinary Shares on a one-to-one basis after the conclusion of a three-year performance period. For PSUs with a March 25, 2021, March 26, 2021, or August 6, 2021 grant date, the three-year performance period ended on December 31, 2023. These PSUs were subsequently settled in Class A Ordinary Shares on February 16, 2024.

|

| (3) | The PSUs, to the extent earned, convert into Class A Ordinary Shares on a one-to-one basis after the conclusion of a three-year performance period. A pre-established cumulative adjusted diluted earnings per share target as certified by the Compensation Committee in the first quarter of the year after the performance period must be met. For LPP performance share unitsPSUs with a March 26, 202024, 2022 or March 27, 202025, 2022 grant date, the three-year performance period ends on December 31, 2022.2024. For LPP performance share unitsPSUs with a March 25, 2021,23, 2023 or March 26, 2021, or August 6, 202124, 2023 grant date, the three-year performance period ends on December 31, 2023.2025. If the minimum or threshold performance is not attained, the performance share unitsPSUs will be forfeited. In this table, the maximum number of performance share unitsPSUs is shown for outstanding awards for all LPP cycles as awards granted under these cycles are currently tracking at or above target payout levels. If Aon does not attain the maximum cumulative target over the three-year period, the number of Class A Ordinary Shares received by the NEOs upon settlement will be reduced. |

| (4) | The July 2023 PSUs, to the extent earned, convert into Class A Ordinary Shares on a one-to-one basis, with 0% to 200% of the target number of July 2023 PSUs (50,000) eligible to vest on the Vesting Date, as follows: (a) no July 2023 PSUs will vest if the average closing price of a Class A Ordinary Share for the 90 consecutive trading days ending on the Vesting Date is below the Performance Hurdle; and (b) subject to achieving the Performance Hurdle, the percentage of July 2023 PSUs to vest will be based upon the Average Share Price, as follows—(i) 50% if the Average Share Price is $475 (threshold), (ii) 100% if the Average Share Price is $500 (target), and (iii) 200% if the Average Share Price is at least $550 (max), with straight line vesting if the Average Share Price is between the threshold, target, and max levels. In this table, the threshold number of July 2023 PSUs is shown, as the share price Performance Hurdle has not been achieved due to the fact that these awards are intended to vest based on share price increases over a five-year period. |

| (5) | The market value is calculated using $300.56,$291.02, the closing price of a Class A Ordinary Share on the NYSE on December 31, 202129, 2023 (the last trading day of 2021)2023). |

Stock Vested in Fiscal Year 20212023 The following table sets forth (1) the number of Class A Ordinary Shares acquired during 20212023 by our NEOs upon the vesting of restricted share unit awards and the settlement of performance share unit awards, and (2) the value realized upon such vesting or settlement. | | | | Stock Awards | | Stock Awards | | Name | | Number of Shares

Acquired

on Vesting (#)(1) | | Value Realized

on Vesting

($)(2) | | Number of Shares

Acquired

on Vesting (#)(1) | | Value Realized on Vesting ($)(2) | | Gregory C. Case | | | 143,042 | | | | 32,794,145 | | Gregory C. Case | | | 200,049 | | 62,076,563 | | Christa Davies | | Christa Davies | | | 46,769 | | | | 10,721,220 | | | 86,379 | | 26,805,945 | | Eric Andersen | | | 31,936 | | | | 7,321,199 | | Eric Andersen | | | 55,857 | | 17,334,867 | | Lisa Stevens | | Lisa Stevens | | | 1,013 | | | | 231,430 | | | 16,503 | | 5,124,486 | | Darren Zeidel | | | 6,162 | | | | 1,445,005 | | Darren Zeidel | | | 14,867 | | 4,617,807 |

| (1) | Represents (a) the vesting of restricted share units granted under theour Shareholder-Approved Plan and (b) the settlement of performance share unit awards granted under the LPP in March 20182020 for the three-year performance period ending on December 31, 2020,2022, which were converted into Class A Ordinary Shares on February 11, 2021.16, 2023. Of the amounts shown, the following aggregate number of Class A Ordinary Shares were withheld to pay taxes due in connection with the vesting: Mr. Case, 63,29688,578 shares; Ms. Davies, 18,35033,990 shares; Mr. Andersen, 14,95527,998 shares; Ms. Stevens, 3637,720 shares; and Mr. Zeidel, 2,7336,588 shares. |

| (2) | Calculated by multiplying (a) the fair market value of Class A Ordinary Shares on the vesting date, which was determined using the closing price on the NYSE of a Class A Ordinary Share on the vesting date or, if such day is a holiday, on the immediately preceding working day, by (b) the number of Class A Ordinary Shares acquired upon vesting. |

46 2022 Aon Proxy Statement

Pension Benefits in Fiscal Year 20212023 The table below provides information regarding the benefits expected to be paid from the Company’s defined benefit pension plans, as well as a supplemental contractual arrangement, for Mr. Andersen, the only NEO who participates in these plans. | | Name | | Plan Name | | Number of Years

of Credited Service (#) | | Present Value of

Accumulated Benefit

($)(1) | | Payments During Last

Fiscal Year ($) | | Plan Name | | Number of Years

of Credited Service (#) | | Present Value of

Accumulated Benefit

($)(1) | | Payments During Last Fiscal Year ($) | | Eric Andersen | | Eric Andersen | | Aon Pension Plan | | 12 | | 487,038 | | — | | Aon Pension Plan | | 12 | | 371,723 | | — | | | | Excess Benefit Plan | | 12 | | 720,558 | | — | | | | Excess Benefit Plan | | 12 | | 540,553 | | — | | | Supplemental Contractual Pension | | 5 | | 686,583 | | — | | | | | | | Supplemental Contractual Pension | | 5 | | 520,874 | | — |

| (1) | Reflects the actuarial present value of benefits accumulated under the respective plans from service and compensation through December 31, 2021,2023, in accordance with the assumptions disclosed in Note 11 to the audited financial statements included in the Company’s Annual Report on Form 10-K as filed with for the SEC on February 18, 2022.year ended December 31, 2023. |

48 2024 Aon Proxy Statement

Mr. Andersen commenced participation in the Aon Pension Plan on May 16, 1997. Under the Aon Pension Plan, a participant is generally entitled to an annual pension benefit commencing at the normal retirement age of 65, calculated based on the participant’s years of service, compensation, and Social Security benefits. Participants are fully vested after completing five years of service. Eligible compensation under the plan is subject to applicable IRS limits; accordingly, the maximum eligible compensation under the plan was $245,000 up to April 1, 2009, the date that the Aon Pension Plan was frozen. The pension formula for service after January 1, 1998, through December 31, 2006, is 1.15% of the participant’s final average earnings multiplied by years of service on or after January 1, 1998, plus 0.45% of the participant’s final average earnings in excess of covered compensation multiplied by years of service on or after January 1, 1998 (not in excess of 35 years). “Final average earnings” is the average of the participant’s base salary and certain eligible bonus payments for the five consecutive calendar years within the last 10 calendar years of employment for which the average was the highest. “Covered compensation” is the average of the Social Security Taxable Wage Base for the 35-year period prior to the participant’s normal retirement age. Effective January 1, 2007, the prior plan benefit was frozen and a career average formula of 1.15% of each year’s earnings plus 0.45% of earnings in excess of covered compensation is effective for service after December 31, 2006. The default form of benefit payment for married participants is a 50% joint and survivor pension; other actuarially equivalent payment options are also available. The Aon Pension Plan was frozen as to benefit accrual effective April 1, 2009, and was previously closed to newly hired employees effective January 1, 2004. Effective January 1, 2020, a portion of the liabilities of the Aon Pension Plan was spun-off to a mirror plan, the Aon Retirement Pension Plan, and Mr. Andersen’s pension plan participation continues under the Aon Retirement Pension Plan as of that date. The Excess Benefit Plan was established in 1989 as an unfunded deferred compensation plan for a select group of management or highly compensated employees and was intended to replace benefits lost under the Aon Pension Plan due to application of certain IRS compensation limits. To be eligible for a benefit under this plan, participants must have attained age 50 and at least 10 years of benefit accrual service. Mr. Andersen satisfied those requirements as of February 3, 2015. The benefit under this plan is determined based on amount of the monthly benefit payable under the Aon Pension Plan had such plan not applied the maximum annual benefit limitation imposed by Section 415 of the Code. Effective for the 2002 plan year and thereafter, the Excess Benefit Plan was amended to provide that earnings in excess of $500,000 would not be taken into account for purposes of calculating the plan benefit. Effective January 1, 2006, the Excess Benefit Plan was further amended to incorporate an alternative benefit formula that provides a benefit of 1% of final average compensation multiplied by total years of service, subject to a maximum annual pension benefit of $500,000. Upon retirement, a participant will receive the greater of the pension from the basic formula (1.15%/0.45%) or the 1% formula. With respect to plan benefits that were earned and vested after December 31, 2004, the form of benefit is an actuarially equivalent term certain annuity for five years, payable monthly. With respect to plan benefits earned and vested on or before December 31, 2004, the form of benefit is the same that would apply under the Aon Pension Plan (subject to certain exceptions). The Excess Benefit Plan was frozen as to benefit accrual effective April 1, 2009. Mr. Andersen and the Company entered into a Supplemental Pension Agreement effective January 19, 2010, in connection with the Company’s decision to freeze further benefit accruals under the Aon Pension Plan and the Excess Benefit Plan in 2009. Under this supplemental agreement, Mr. Andersen is entitled to a supplemental pension benefit upon termination of employment equal to the aggregate pension benefit earned under the Aon Pension Plan and the Excess Benefit Plan for the 2008 plan year, multiplied by five (effectively giving Mr. Andersen an additional five years of pension service). Mr. Andersen became fully vested in this 2022 Aon Proxy Statement 47

benefit upon his continuous employment with the Company through the later of December 31, 2014, or attainment of age 50 and completion of 10 years of benefit accrual service. This benefit is payable in the form of a 100% joint and survivor annuity commencing following termination of employment or, if later, attaining age 55. Nonqualified Deferred Compensation in Fiscal Year 20212023 The table below shows any executive contributions, contributions by Aon, earnings, withdrawals, and account balances for the NEOs with respect to our Supplemental Savings Plan. None of our NEOs participate in the Aon Deferred Compensation Plan. See the section titled “Executive and Relocation Benefits” in the CD&A and the narratives set forth below the following table for additional information on these plans.

2024 Aon Proxy Statement 49

Nonqualified Deferred Compensation in FY 2021Fiscal Year 2023 | | Name | | Name of Plan | | Executive

Contributions

in Last Fiscal

Year ($) | | Aon

Contributions

in Last Fiscal

Year ($)(1) | | Aggregate

Earnings in

Last Fiscal

Year ($) | | Aggregate

Withdrawals/

Distributions

($) | | Aggregate

Balance at

Last Fiscal

Year End

($)(2) | | Name of Plan | Name of Plan | | Executive Contributions

in Last Fiscal

Year ($) | Executive Contributions

in Last Fiscal

Year ($) | | Aon

Contributions

in Last Fiscal

Year ($)(1) | Aon

Contributions

in Last Fiscal

Year ($)(1) | | Aggregate

Earnings in

Last Fiscal

Year ($) | Aggregate

Earnings in

Last Fiscal

Year ($) | | Aggregate

Withdrawals/

Distributions

($) | Aggregate

Withdrawals/

Distributions

($) | | Aggregate Balance at Last Fiscal Year End ($)(2) | Aggregate Balance at Last Fiscal Year End ($)(2) | | Gregory C. Case | | Supplemental Savings Plan | | | — | | | | 12,600 | | | | 3,442 | | | | — | | | | 198,028 | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | | Christa Davies | | Christa Davies | | Christa Davies | | Christa Davies | | Christa Davies | | Supplemental Savings Plan | | | — | | | | 10,900 | | | | 3,288 | | | | — | | | | 210,106 | | | Eric Andersen | | Supplemental Savings Plan | | | — | | | | 13,000 | | | | 143,316 | | | | — | | | | 879,478 | | Eric Andersen | | Eric Andersen | | Eric Andersen | | Eric Andersen | | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | Supplemental Savings Plan | | | — | | | | 6,300 | | | | 114 | | | | — | | | | 12,864 | | | Darren Zeidel | | Supplemental Savings Plan | | | — | | | | 8,400 | | | | 1,578 | | | | — | | | | 86,397 | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | |

| (1) | These amounts are included in “All Other Compensation” for 20212023 in the Summary Compensation Table. |

| (2) | The following table provides the amount reported in the “Aggregate Balance at Last Fiscal Year End” column for each NEO that has been previously reported as compensation in the Summary Compensation Tables for 2021, 2020,2023, 2022, and 2019.2021. |

| | Name | | Name of Plan | | Amount Included

in 2021

Compensation in

Summary

Compensation

Table ($) | | Amount Included

in 2020

Compensation in

Summary

Compensation

Table ($) | | Amount Included

in 2019

Compensation in

Summary

Compensation

Table ($) | | Name of Plan | Name of Plan | | Amount Included

in 2023

Compensation in

Summary

Compensation

Table ($) | Amount Included

in 2023

Compensation in

Summary

Compensation

Table ($) | | Amount Included

in 2022

Compensation in

Summary

Compensation

Table ($) | Amount Included

in 2022

Compensation in

Summary

Compensation

Table ($) | | Amount Included in 2021 Compensation in Summary Compensation Table ($) | Amount Included in 2021 Compensation in Summary Compensation Table ($) | | Gregory C. Case | | Supplemental Savings Plan | | | 12,600 | | | | 13,125 | | | | 11,300 | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | Gregory C. Case | | | Christa Davies | | Christa Davies | | Christa Davies | | Christa Davies | | Christa Davies | | Supplemental Savings Plan | | | 10,900 | | | | 2,642 | | | | 11,300 | | | Eric Andersen | | Supplemental Savings Plan | | | 13,000 | | | | 3,125 | | | | 13,500 | | Eric Andersen | | Eric Andersen | | Eric Andersen | | Eric Andersen | | | Lisa Stevens(a) | | Supplemental Savings Plan | | | 6,300 | | | | N/A | | | | N/A | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | Lisa Stevens | | | Darren Zeidel(a) | | Supplemental Savings Plan | | | 8,400 | | | | N/A | | | | N/A | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | | Darren Zeidel | |

| (a) | The compensation of Ms. Stevens and Mr. Zeidel was not reported in our Summary Compensation Table in 2019 and 2020 because they were not named executive officers for those years.

|

Aon Supplemental Savings Plan The Aon Supplemental Savings Plan was created to provide matching and other company allocations similar to what participants in the Aon Savings Plan (our qualified 401(k) plan) would have received had the Code limits not restricted contributions under the Aon Savings Plan. Participants eligible for Aon Savings Plan company contributions who are active at the end of the plan year and who attain the IRS 401(k) contribution limit and compensation limit (or participate in the Aon Deferred Compensation Plan) receive supplemental allocations to the Supplemental Savings Plan based on their years of service and their match eligible compensation in excess of the IRS limit or Deferred Compensation Plan deferrals (to a combined plan limit of $500,000). Distributions from the Supplemental Savings Plan must begin at the earlier of retirement or age 65. Each NEO participated in the Supplemental Savings Plan in 2021.2023. If an executive officer contributes on a match-eligible basis to the Aon Savings Plan an amount equal to the annual contribution limit imposed by the Code ($19,50022,500 in 2021)2023), the Supplemental Savings Plan provides for a company allocation as a percentage of eligible compensation deferred under the Aon Deferred Compensation Plan and of eligible compensation in excess of the IRS limit ($290,000330,000 in 2021)2023). The combined 48 2022 Aon Proxy Statement

total annual eligible compensation for the Aon Savings and Aon Supplemental Savings Plans is capped at $500,000. The percentage allocation varies by length of service. In the first four years of employment the Company allocation percentage is 3% and that percentage increases incrementally to 6% after 15 years of service. Potential Payments and Benefits on Termination or Change in Control During 2021,2023, each NEO was party to either an employment agreement with Aon that addresses the payments and benefits that he or she will receive under various termination of employment scenarios or an employment letter that provides for participation in the Combined Severance Plan. Non-competition and non-solicitation covenants apply to each NEO for a period of two years following the termination of employment of such executive without regard to the reason for such termination. Each NEO other than Mr. Case is entitled to participate in our the Combined Severance Plan, which provides certain severance benefits upon a qualifying termination of employment in connection with or during the two years following a change in control of Aon. Mr. Case is party to his ownan individual change of control severance agreement with the Company providing certain severance benefits in connection with a qualifying termination of employment in connection with a change in control.control of Aon. 50 2024 Aon Proxy Statement

The tables below outline the potential payments to the NEOs upon the occurrence of various termination of employment events, including a termination in connection with a change in control of Aon. The following assumptions apply with respect to the tables below and any termination of employment of ana NEO: Each NEO was terminated on December 31, 2021, and the price per Class A Ordinary Share is $300.56 per share, the closing market price per share on December 31, 2021 (the last trading day of 2021). Accordingly, the tables set forth amounts as of December 31, 2021 and include estimates of amounts that would be paid to the NEO upon the occurrence of a termination event.

| • | | Each NEO was terminated on December 31, 2023, and the price per Class A Ordinary Share is $291.02 per share, the closing market price per share on December 29, 2023 (the last trading day of 2023). Accordingly, the tables set forth amounts as of December 31, 2023, and include estimates of amounts that would be paid to the NEO upon the occurrence of a termination of employment event. |

Each NEO is entitled to receive amounts earned during the term of his or her employment regardless of the manner of termination. These amounts include accrued base salary, accrued vacation time, and other employee benefits to which the NEO was entitled on the date of termination and are not shown in the tables below. Under each NEO’s employment agreement, other than Mr. Case’s, or by virtue of the NEO’s eligibility for the Combined Severance Plan, the NEO is entitled to 365 days’ notice in the event that the Company terminates his or her employment without cause, during which period the NEO would continue to receive base salary and remain eligible for the Company’s standard benefit plans.

| • | | Each NEO is entitled to receive amounts earned during the term of his or her employment regardless of the manner of termination. These amounts include accrued base salary, accrued vacation time, and other employee benefits to which the NEO was entitled on the date of termination and are not shown in the tables below. Under each NEO’s employment agreement, other than Mr. Case’s, or by virtue of the NEO’s eligibility for the Combined Severance Plan, the NEO is entitled to 365 days’ notice in the event that the Company terminates his or her employment without cause, during which period the NEO would continue to receive base salary and remain eligible for the Company’s standard benefit plans. |

The specific definitions of (i) “good reason” applicable to “Involuntary—Good Reason” and (ii) “cause” applicable to “Involuntary—For Cause,” and (iii) “without cause” or “not for cause” applicable to “Involuntary—Without Cause” for each of the NEOs can be found, to the extent applicable, in their respective employment agreements or the Combined Severance Plan. In addition, the specific definitions of “qualifying termination” applicable to “Qualifying After Change in Control” can be found in the Combined Severance Plan or, with respect to Mr. Case, in his change in control severance agreement.

The definition of “retirement” applicable to “Retirement” means a voluntary termination of employment upon or after the individual’s attainment of age 55. The LPP provides for pro rata vesting in the event of retirement on the same terms that apply to a termination “without cause” or for “good reason.”

| • | | The specific definitions of (i) “good reason” applicable to “Involuntary—Good Reason” and (ii) “cause” applicable to “Involuntary—For Cause,” and (iii) “without cause” or “not for cause” applicable to “Involuntary—Without Cause” for each of the NEOs can be found, to the extent applicable, in their respective employment agreements or the Combined Severance Plan. In addition, the specific definitions of “qualifying termination” applicable to “Qualifying After Change in Control” can be found in the Combined Severance Plan or, with respect to Mr. Case, in his change in control severance agreement. |

20222024 Aon Proxy Statement 4951

| • | | The definition of “retirement” applicable to “Retirement” means a voluntary termination of employment upon or after the individual’s attainment of age 55. The LPP provided in 2023 for pro rata vesting in the event of retirement on the same terms that apply to a termination “without cause” or for “good reason.” |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | Name | | Termination Reason

| | Total Cash

Payment

($)(1) | | Accelerated

Share

Vesting

($)(2) | | Welfare,

Retirement

and Other

Benefits

($) | | Severance

Cutback

($)(3) | | Total ($) | Gregory C. Case | | Retirement | | | | — | | | | $ | 75,371,632 | | | | | | | | | | | | | | $ | 75,371,632 | | | | Involuntary-Good Reason | | | $ | 12,000,000 | | | | $ | 75,371,632 | | | | $ | 232,016 | | | | | | | | | $ | 87,603,648 | | | | Death | | | $ | 3,000,000 | | | | $ | 97,942,285 | | | | $ | 5,000,000 | | | | | | | | | $ | 105,942,285 | | | | Disability | | | $ | 3,000,000 | | | | $ | 97,942,285 | | | | | — | | | | | | | | | $ | 100,942,285 | | | | Involuntary-Without Cause | | | $ | 12,000,000 | | | | $ | 75,371,632 | | | | $ | 232,016 | | | | | | | | | $ | 87,603,648 | | | | Qualifying After Change in Control | | | $ | 15,316,667 | | | | $ | 97,942,285 | | | | $ | 430,045 | | | | | | | | | $ | 113,688,996 | | Christa Davis | | Involuntary-Good Reason | | | $ | 2,680,000 | | | | $ | 29,376,233 | | | | | | | | | | | | | | $ | 32,056,233 | | | | Death | | | $ | 3,932,055 | | | | $ | 40,243,181 | | | | | | | | | | | | | | $ | 44,175,235 | | | | Disability | | | $ | 4,932,055 | | | | $ | 40,243,181 | | | | | | | | | | | | | | $ | 45,175,235 | | | | Involuntary-Without Cause | | | $ | 4,360,000 | | | | $ | 29,376,233 | | | | | | | | | | | | | | $ | 33,736,233 | | | | Qualifying After Change in Control | | | $ | 5,200,000 | | | | $ | 40,243,181 | | | | $ | 79,064 | | | | | | | | | $ | 45,522,245 | | Eric Andersen | | Retirement | | | | — | | | | $ | 19,543,814 | | | | | | | | | | | | | | $ | 19,543,814 | | | | Involuntary-Good Reason | | | $ | 1,000,000 | | | | $ | 19,543,814 | | | | | | | | | | | | | | $ | 20,543,814 | | | | Death | | | | — | | | | $ | 27,358,775 | | | | | | | | | | | | | | $ | 27,358,775 | | | | Disability | | | | — | | | | $ | 27,358,775 | | | | | | | | | | | | | | $ | 27,358,775 | | | | Involuntary-Without Cause | | | $ | 1,000,000 | | | | $ | 19,543,814 | | | | | | | | | | | | | | $ | 20,543,814 | | | | Qualifying After Change in Control | | | $ | 4,333,333 | | | | $ | 27,358,775 | | | | $ | 107,196 | | | | ($ | 6,798,980 | ) | | | $ | 25,000,324 | | Lisa Stevens | | Involuntary-Good Reason | | | $ | 900,000 | | | | $ | 4,165,261 | | | | | | | | | | | | | | $ | 5,065,261 | | | | Death | | | | — | | | | $ | 6,493,599 | | | | | | | | | | | | | | $ | 6,493,599 | | | | Disability | | | | — | | | | $ | 6,493,599 | | | | | | | | | | | | | | $ | 6,493,599 | | | | Involuntary-Without Cause | | | $ | 900,000 | | | | $ | 4,165,261 | | | | | | | | | | | | | | $ | 5,065,261 | | | | Qualifying After Change in Control | | | $ | 4,425,000 | | | | $ | 6,493,599 | | | | $ | 91,999 | | | | | | | | | $ | 11,010,598 | | Darren Zeidel | | Involuntary-Good Reason | | | $ | 750,000 | | | | $ | 3,929,021 | | | | | | | | | | | | | | $ | 4,679,021 | | | | Death | | | | — | | | | $ | 5,737,390 | | | | | | | | | | | | | | $ | 5,737,390 | | | | Disability | | | | — | | | | $ | 5,737,390 | | | | | | | | | | | | | | $ | 5,737,390 | | | | Involuntary-Without Cause | | | $ | 750,000 | | | | $ | 3,929,021 | | | | | | | | | | | | | | $ | 4,679,021 | | | | Qualifying After Change in Control | | | $ | 3,069,667 | | | | $ | 5,737,390 | | | | $ | 73,156 | | | | | | | | | $ | 8,880,213 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | Name | | Termination Reason | | Total Cash

Payment

($)(1) | | Accelerated

Share

Vesting

($)(2) | | Welfare,

Retirement

and Other

Benefits

($) | | Severance

Cutback

($)(3) | | Total ($) | | | | | | | | Gregory C. Case | | Retirement | | | | — | | | | | 56,158,323 | | | | | — | | | | | — | | | | | 56,158,323 | | | | Involuntary-Good Reason | | | | 14,250,000 | | | | | 56,158,323 | | | | | 96,000 | | | | | — | | | | | 70,504,323 | | | | Death | | | | 3,750,000 | | | | | 73,860,003 | | | | | 5,000,000 | | | | | — | | | | | 82,610,003 | | | | Disability | | | | 3,750,000 | | | | | 73,860,003 | | | | | — | | | | | — | | | | | 77,610,003 | | | | Involuntary-Without Cause | | | | 14,250,000 | | | | | 56,158,323 | | | | | 96,000 | | | | | — | | | | | 70,504,323 | | | | Qualifying After Change in Control | | | | 17,310,000 | | | | | 73,860,003 | | | | | 238,950 | | | | | — | | | | | 91,408,952 | | | | | | | | | Christa Davies | | Involuntary-Good Reason | | | | 3,990,000 | | | | | 29,229,273 | | | | | — | | | | | — | | | | | 33,219,273 | | | | Death | | | | 3,055,068 | | | | | 36,491,580 | | | | | — | | | | | — | | | | | 39,546,648 | | | | Disability | | | | 4,555,068 | | | | | 36,491,580 | | | | | — | | | | | — | | | | | 41,046,648 | | | | Involuntary-Without Cause | | | | 6,730,000 | | | | | 29,229,273 | | | | | — | | | | | — | | | | | 35,959,273 | | | | Qualifying After Change in Control | | | | 4,753,333 | | | | | 36,491,580 | | | | | 90,066 | | | | | | | | | | 41,334,979 | | | | | | | | | Eric Andersen | | Retirement | | | | — | | | | | 23,026,181 | | | | | — | | | | | — | | | | | 23,026,181 | | | | Involuntary-Good Reason | | | | 9,369,863 | | | | | 23,026,181 | | | | | 65,567 | | | | | — | | | | | 32,461,612 | | | | Death | | | | 2,500,000 | | | | | 28,869,475 | | | | | — | | | | | — | | | | | 31,369,475 | | | | Disability | | | | 2,500,000 | | | | | 28,869,475 | | | | | — | | | | | — | | | | | 31,369,475 | | | | Involuntary-Without Cause | | | | 9,369,863 | | | | | 28,869,475 | | | | | 65,567 | | | | | — | | | | | 38,304,905 | | | | Qualifying After Change in Control | | | | 4,450,000 | | | | | 28,869,475 | | | | | 115,754 | | | | | (1,958,844 | ) | | | | 31,476,385 | | | | | | | | | Lisa Stevens | | Involuntary-Good Reason | | | | 1,000,000 | | | | | 9,633,538 | | | | | — | | | | | — | | | | | 10,633,538 | | | | Death | | | | — | | | | | 13,138,971 | | | | | — | | | | | — | | | | | 13,138,971 | | | | Disability | | | | — | | | | | 13,138,971 | | | | | — | | | | | — | | | | | 13,138,971 | | | | Involuntary-Without Cause | | | | 1,000,000 | | | | | 9,633,538 | | | | | — | | | | | — | | | | | 10,633,538 | | | | Qualifying After Change in Control | | | | 3,256,667 | | | | | 13,138,971 | | | | | 107,326 | | | | | — | | | | | 16,502,963 | | | | | | | | | Darren Zeidel | | Involuntary-Good Reason | | | | 900,000 | | | | | 5,906,251 | | | | | — | | | | | — | | | | | 6,806,251 | | | | Death | | | | — | | | | | 7,552,842 | | | | | — | | | | | — | | | | | 7,552,842 | | | | Disability | | | | — | | | | | 7,552,842 | | | | | — | | | | | — | | | | | 7,552,842 | | | | Involuntary-Without Cause | | | | 900,000 | | | | | 5,906,251 | | | | | — | | | | | — | | | | | 6,806,251 | | | | Qualifying After Change in Control | | | | 2,775,000 | | | | | 7,552,842 | | | | | 101,154 | | | | | — | | | | | 10,428,996 | |

50 202252 2024 Aon Proxy Statement

| (1) | The Total Cash Payment is calculated in accordance with the terms of the agreements and plans described below. The components of the Total Cash Payment are set forth in the following table: |

| | Name | | Termination

Reason

(a) | | Base

Salary

($) | | Base

Salary

Multiple | | Bonus

($) | | Bonus

Multiple | | Average

Annual

Cash Bonus

($) | | Total

Severance

($) | | Pro Rata

Bonus

($) | | Total Cash

Payment

($) | | Termination

Reason

(a) | | Base

Salary

($) | | Base

Salary

Multiple | | Bonus

($) | | Bonus

Multiple | | Average

Annual

Cash Bonus

($) | | Total

Severance

($) | | Pro Rata

Bonus

($) | | Total

Cash

Payment