Importance of Informed Judgment To help ensure that our compensation program is appropriately aligned with our long-term strategy, stakeholder expectations and the safety and soundness of our firm, our Compensation Committee, within the structure of its Assessment Framework and in the context of the inputs and factors described below, uses its informed judgment to evaluate, and structured discretion to set, executive compensation. We believe this balanced approach which is consistent with industry practice, is appropriate for our firm, and that a more formulaic compensation program would not be in the long-term best interests of our firm, our shareholders and other stakeholders. | ∎ | | Avoids Unintended Consequences and Mitigates Compensation-Related Risk. Our business is dynamic and requires us to respond rapidly to changes in our operating environment. As such, our annual compensation program is designed to encourage appropriate prudence by our senior leaders, on behalf of our shareholders and our clients, regardless of prevailing market conditions. | |

| » | | We use a Performance Our Compensation Committee utilizes an Assessment Framework to provide greater definition to, and transparency regarding, the pre-established financial and nonfinancial factors considered by the Compensation Committee to assessit considers in its assessment of the firm’s performance in connection with compensation decisions for our NEOs and other senior leaders. However, a strictly formulaic compensation program would not permit adjustments based on less quantifiable factors, such as unexpected external events or individual performance.

| |

| ∎ | | Performance-Based Pay Provides Alignment. Alignment.While annual compensation decisions are based on our Compensation Committee’s informed judgment and use of structured discretion, the amounts ultimately realized by our NEOs (who received 100% of year-end equity-based pay in PSUs) are subject to ongoing performance metrics and tied to the firm’s longer-term stock price (settlement of PSUs and Shares at Risk delivered in respect of PSUs). | |

Our Compensation Principles (available atwww.gs.com/corpgov) underpin all of our compensation decisions, including the Compensation Committee’s determination of NEO compensation. The Committee recently undertook a review of our long-standing Compensation Principles, reaffirming the key elements contained therein as well as formally documenting in the principles our existing commitment and practice that compensation should promote a strong risk management and control environment. Key elements of our Compensation Principles (which were reviewed and updated in 2023) include: | | | | | | | | | | | Paying for Performance | | Encouraging Firmwide Orientation & Culture | | Discouraging Imprudent Risk-Taking | | Attracting & Retaining Talent | | | | | | Paying for Performance | | Encouraging Firmwide Orientation & Culture | | Discouraging Imprudent Risk-Taking | | Attracting & Retaining Talent | | | | | Firmwide compensation should directly relate to firmwide performance over the cycle. | | Employees should think and act like long-term shareholders, and compensation should reflect the performance of the firm as a whole. | | Compensation should be carefully designed to be consistent with the safety and soundness of our firm. Risk profiles must be taken into account in annual performance reviews, and factors like liquidity risk and cost of capital should also be considered. | | Compensation should reward an employee’s ability to identify and create value, and the recognition of individual performance should also

be considered in the context of the competitive market for talent. | | | Promoting a Strong Risk Management and Control Environment |

| | | | | | 36 | | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERSGoldman Sachs | GOLDMAN SACHSProxy Statement for the 2024 Annual Meeting of Shareholders | | | 35

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS HOW OUR COMPENSATION COMMITTEE MAKES DECISIONS

Firmwide Performance  Taking into account our pay-for-performance philosophy, our Compensation Committee places substantial importance on the assessment of firmwide performance when determining NEO compensation. This includes not only financial performance, but how these results are achieved, including how our most senior leaders are investing in the future of our firm and demonstrating an appropriate commitment to a strong control environment and effective financial and nonfinancial risk management practices. | Taking into account our pay-for-performance philosophy, our Compensation Committee places substantial importance on the assessment of firmwide performance when determining NEO compensation.

|

| | ∎ | | During 2019, we developed our initial Performance Assessment Framework to provide greater definition to and transparency regarding the key factors considered by the Compensation Committee to assess the firm’s performance in connection with compensation decisions for our NEOs and our Management Committee. |

| » | | The Assessment Framework includes an assessment of pre-established financial metrics and nonfinancial factors on a firmwide basis. It also includes information and metrics on business metricsperformance in the context of our strategic priorities that underpin firmwide performance and serve to inform compensation decisions for the firm’s business leaders. |

| » | | The Assessment Framework aligns performance metrics and goals across our most senior leaders and provides a structure to help ensure that our compensation program for our NEOs and Management Committee continues to be appropriately aligned with our long-term strategy, our financial targets and stakeholder expectations as well as promotes the strength of our risk management and control environment and the safety and soundness of our firm. The Framework continues to evolve, as appropriate, to help ensure this purpose is served. |

| | ∎ | | In February 2022,The Assessment Framework is reviewed annually, with metrics and factors updated as needed. For example, in 2023, the Compensation Committee, taking into account Board and stakeholder feedback, adopted changes to enhance the types of metrics and the nature of information provided to the Committee adopted financial metricsin connection with the risk management and nonfinancial factors, each as described below, that informedcontrol pillar of the 2022 compensation decisions for our NEOs.Assessment Framework.

|

For 2023, the assessment of firmwide performance to inform compensation decisions for our NEOs and other Management Committee members included: | The assessment of firmwide performance takes into account a number of factors, including:

|

| | ∎ | | 20222023 financial performance, focused on the key metrics set forth in the Performance Assessment Framework, both on an absolute basis and relative to our Peers;Peers.

|

| | ∎ | | Progress towards achievingAdditional information regarding the firm’s strategic objectives through a review of a dashboard of KPIs that support our medium-term financial targets; and

|

| ∎ | | Nonfinancialnonfinancial factors that underpin how our financial results are achieved and support appropriate investment in the firm’s future.future, including with respect to progress towards our strategic priorities, One Goldman Sachs and client-centricity, risk management and control considerations, and execution of our people strategy.

|

| | | | | | | | | | Overview of Performance Assessment Framework | | | | | | | |

| | | | How the Results are Achieved/Investment in the Future | | | | | | | | | Financial Performance | | Strategic Priorities & Clients | | Risk Management & Controls | | People | | | | | |

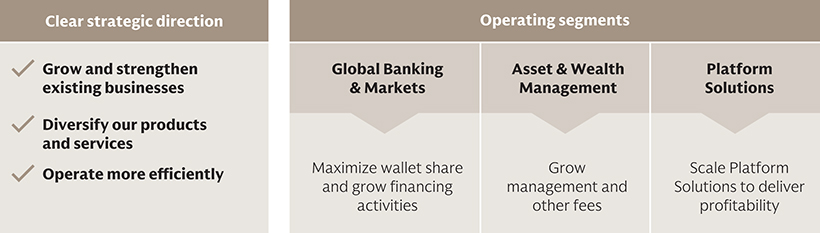

| | ∎ ROE ∎ ROTE ∎ Efficiency ratio ∎ TSR ∎ CET1 ratio ∎ BVPS growth ∎ Pre-tax earnings ∎ Net revenues / revenue net of provisions ∎ EPS ∎ Strategic priorities and KPIs:

» Grow and strengthen existing businesses

» Diversify our products and services

» Operate more efficiently

| | ∎ Collaboration across the firmProgress towards our strategic objectives ∎ Cross-business strategy / collaboration in support of One Goldman Sachs ∎ Strength of client feedback ∎ Broadening share of addressable market ∎ Progress towards sustainable finance commitments | | ∎ Managing reputational risk ∎ Compliance

∎ Standing with regulators ∎ Governance and controls

∎ ManagingRisk – including: » Management across categories (market, credit, liquidity & funding, operational, model) » Strategic & business environment risk » Residual risks identified ∎ Managing risk violations/ exceptionsInternal Audit findings ∎ CapitalCompliance, conduct and liquiditydisciplinary matters ∎ 360° feedback on risk management, firm reputation and compliance

| | ∎ Core Values ∎ Compliance and conduct matters

∎ Diversity, equity & inclusionEquity and Inclusion (e.g., hiring and representation) ∎ Attrition ∎ Leadership pipeline health ∎ Return to office

∎ Strategic location headcount and hiring |

We will continue to evolve the Assessment Framework, as appropriate, to help ensure its purposes are served. To this end, in February 2024, the Compensation Committee adopted amendments to the Assessment Framework to further align it with our announced strategic priorities and 2024 execution focus areas. | | | | | | | 36 | Proxy Statement for the 2024 Annual Meeting of Shareholders | Goldman Sachs | | GOLDMAN SACHS | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERS 37

| | |

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS HOW OUR COMPENSATION COMMITTEE MAKES DECISIONS | | |  Individual Performance Individual Performance

Individual Performance An assessment of each NEO’s individual performance and achievements is critical to our Compensation Committee’s decision-making process, including how each of our NEOs helped to contribute to firmwide performance based on the metrics and other criteria set forth in the Assessment Framework and other factors, in each case as applicable depending on the NEO’s role. Individual performance is also evaluated through our annual feedback processes, which are designed to solicit and provide individual performance feedback, including on strengths and development opportunities. These processes include confidential input from employees, including those who are senior to, peers of and junior to the employee being reviewed, as applicable. Individual performance is assessed across a variety of factors, including client focus and driving growth, risk management, firm reputation, culture contributions and manager effectiveness. An assessment of each NEO’s individual performance and achievements is critical to our Compensation Committee’s decision-making process, including how each of our NEOs helped to contribute to firmwide performance based on the criteria set forth in the Performance Assessment Framework and other factors, in each case as applicable depending on the NEO’s role.

The performance of each of our NEOs is considered against the criteria in the Performance Assessment Framework, as well as evaluated under our 360° Review Process. The 360° Review Process includes confidential input from employees, including those who are senior to (other than for our CEO), peers of and junior to the employee being reviewed. Through the 360° Review Process,

| | 360o Revew Process  | our NEOs’ performance is assessed across a variety of factors, including risk management and firm reputation, control-side empowerment, judgment, compliance with firm policies, culture contributions, diversity and inclusion, and client focus. |

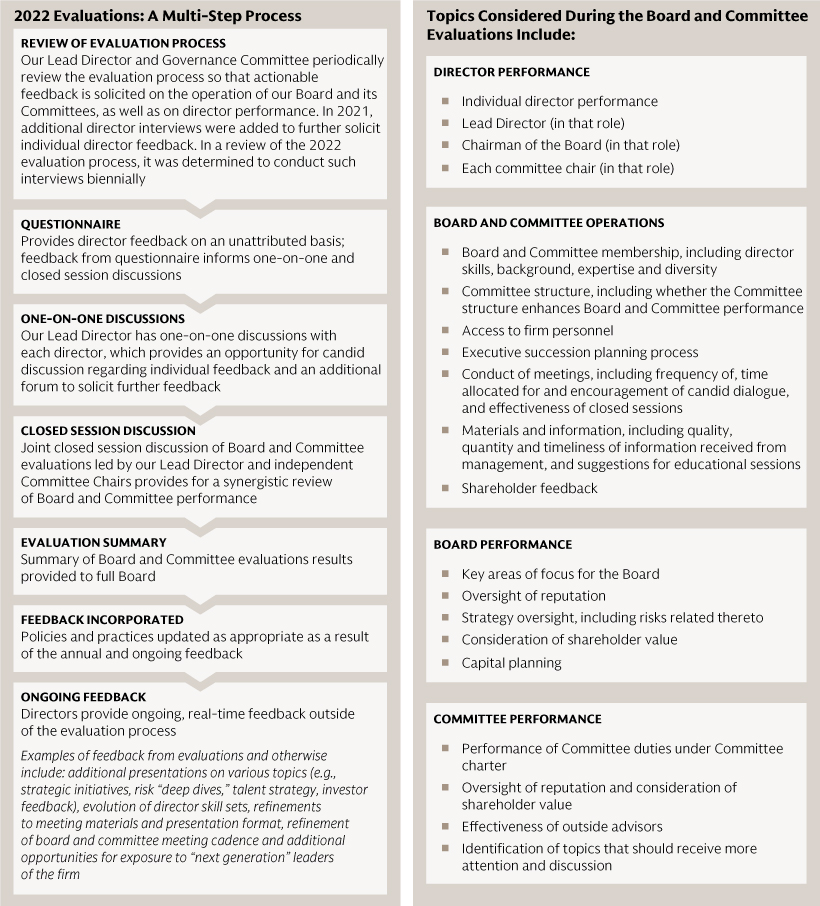

| | ∎ | | Our CEO:Under the direction of our Lead Director, our Governance Committee evaluated the performance of Mr. Solomon including consideration of performance pursuant to the Performance Assessment Framework, as well as a summary of his evaluation under the 360° Review Process (see Corporate Governance—Board Oversight of our Firm—Key Areas of Board Oversight—CEO Performance). Our Compensation Committee considered this evaluation and discussed Mr. Solomon’s performance, including pursuant to the Assessment Framework, as part of its discussions to determine his compensation. |

| | ∎ | | Other NEOs:Mr. Solomon discussed with the Governance Committee the performance of our COO, CFO and CFO, including consideration of Messrs. Waldron’sCLO and Coleman’s performance pursuant to the Performance Assessment Framework, as well as a summary of their evaluations under the 360° Review Process. The Compensation Committee similarly considered these evaluationsGeneral Counsel, and discussed the performance of Messrs. Waldron and Coleman as part of its discussions to determine their compensation. Messrs. Solomon and Waldron also discussed with the Compensation Committee the performance of our other NEOs, includingGlobal Treasurer, in respect of the metrics included in the Framework,each case taking into account results from our annual feedback processes. The Compensation Committee considered these individual performance evaluations, as well as a summary ofmetrics and other criteria set forth in the Assessment Framework, in connection with their evaluations under the 360° Review Process.discussions to determine NEO compensation. In this context, theyMessrs. Solomon and Waldron submitted variable compensation recommendations to the Compensation Committee for our NEOs, but did not make recommendations about their own compensation. |

Our Compensation Committee broadly reviewsconsiders the competitive market for talent as part of its review of our compensation program’s effectiveness in attracting and retaining talent, including to help determine NEO compensation. | | ∎ | | Wherever possible, our goal is to be in a position to appoint people from within the firm to our most senior leadership positions.roles. Our executive compensation program is intended to incentivize our people to stay at Goldman Sachs and to aspire to these senior roles. |

To this end, the Committee regularly evaluates our NEO compensation program using benchmarking to help ensure that our senior roles are properly valued, taking into account compensation program design and structure, as well as multi-year financial performance and quantum of NEO pay at our Peers. The Committee may also receive additional benchmarking information with respect to other companies with which the firm competes for talent (e.g., alternative and other asset managers, S&P 100 companies). | | ∎ | | The Committee performs this evaluation with information and assistance from HCM and the Committee’s independent compensation consultant, Meridian Compensation Partners, LLC (Meridian)Frederic W. Cook & Co., Inc. (FW Cook). |

| | ∎ | | Benchmarking information provided by HCM is obtained from an analysis of public filings, by our Controllers and HCM functions, as well as surveys conducted by Willis Towers Watson regarding incentive compensation practices. |

| | | | | | 38 | | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERSGoldman Sachs | GOLDMAN SACHSProxy Statement for the 2024 Annual Meeting of Shareholders | | | 37

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS HOW OUR COMPENSATION COMMITTEE MAKES DECISIONS | | | | Our Peers | | | U.S. Peers | | European Peers | | | | Bank of America Corporation Our

Peers | | Barclays PLC U.S. Peers

| | | Bank of America Corporation Citigroup Inc. | | Credit Suisse Group AG | | | JPMorgan Chase & Co. | | Deutsche Bank AG | | | Morgan Stanley | | UBS Group AG | | | The Bank of New York Mellon Corporation | | | | | Wells Fargo & Company | | European Peers* Barclays PLC Deutsche Bank AG UBS Group AG |

| | ∎* | | In addition,Credit Suisse was removed from the Compensation Committee (and other Committees as may be applicable inPeer group following the context of their respective oversight) also receives and considers information on non-executive employee compensation, including information on aggregate compensation, attrition and retention. Annually, the Compensation Committee reviews and approves the equity award terms, including deferral levels, for equity-based awards granted to employees at all levels across the firm. Consistentmerger with our Compensation Principles, employees at certain compensation thresholds receive a portion of their compensation in the form of equity-based awards, which increases as compensation increases, in order to help support employee share ownership and align employee interests with those of long-term shareholders.UBS Group AG.

|

In addition, the Compensation Committee (and other Committees as may be applicable in the context of their respective oversight) also receives and considers information on non-executive employee compensation, including information on aggregate compensation, benchmarking (for certain populations), attrition and retention. Annually, the Compensation Committee reviews and approves the equity award terms, including deferral levels, for equity-based awards granted to employees at all levels across the firm. Consistent with our Compensation Principles, employees at certain compensation thresholds receive a portion of their compensation in the form of equity-based awards, which increases as compensation increases, in order to help support employee share ownership and align employee interests with those of long-term shareholders.

Engagement has been and continues to be a priority for our Board and management. To this end, we engage extensively with our stakeholders each year (seeStakeholder Engagement). This feedback, together with feedback received over the last several years and the results of our annual Say on Pay vote, continues to informVote, informs our Board and Compensation Committee actions. | ∎ | | Feedback from the Say on Pay voteVote at the 2022our 2023 Annual Meeting (approximately 82%94% support), includingas well as stakeholder engagement in connection with our 20222023 Annual Meeting, reflected continued support for our: |

|  | Pay-for-performance philosophy |  Pay-for-performance philosophy

|

| | 100% deferralof year-end equity-based pay in PSUs for all NEOs and broader Management Committee

|

| | PSUs that tie compensation for senior leaders to ongoing performance conditions

|

| | Rigorous structure of previously granted Shareholder Value Creation Awards (SVC Awards); commitment to maintaining award thresholds despite change in operating environment

Robust risk-balancing features in the compensation program

|

| | | Program alignment across senior leadership |

| ∎ | | In determining the form, structure and amount of 2022 annual compensation, the Committee tookTaking into account thisthe strong feedback and discussed and evaluated that a core element of our Compensation Principles—as well as of stakeholder feedback—is paying-for-performance. In light of this,received, the Compensation Committee and the Board determined to keep the form and structure of annualour executive compensation program consistent year-over-year, while lowering 2022 annual variableyear-over-year. More information on 2023 year-end compensation in consideration of the firm’s 2022 performance. In doing so, we have continueddecisions and our commitment to various best practices (asis described below).below.

|

| | Over the last several years, we have made a number of enhancements to our compensation program and affirmed our commitments to various best practices, including paying for performance and using performance-based equity awards to closely link pay to longer-term results. |

| | | | | | | 38 | Proxy Statement for the 2024 Annual Meeting of Shareholders | Goldman Sachs | | GOLDMAN SACHS | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERS 39

| | |

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS HOW OUR COMPENSATION COMMITTEE MAKES DECISIONS | | | | In response to stakeholder feedback | | Over the last several years, we have made a number of enhancements to our compensation program and restated our commitments to various best practices, including paying-for-performance and using performance-based equity awards to further link pay to longer-term results

|

| | | | | Stakeholder Feedback | |

Compensation Committee Action | | |  Pay-for-Performance Philosophy | |

| | | All pay other than salary is variable and  Pay-for-Performance Philosophy Limit use Pay-for-Performance Philosophy Limit useat least 60% of Time-Based RSUs in Executive Compensation | | Continually increased over time the portion of deferral in PSUs. For 2022, all NEOs and continuing Management Committee members continued to receive 100% of deferral in PSUsNEO variable compensation is subject to performance conditions

| | |  Limit Use of Time-Based RSUs in Executive Compensation | | For 2023, all NEOs and other senior leaders continued to receive 100% of year-end equity in the form of PSUs | | | Support for High Percentage of Performance-Based Pay and Rigor of Design | | 100% of year-end equity for NEOs granted as PSUs, which are subject to ongoing performance conditions Granted rigorousRigorous five-year SVC Awardsin late 2021 or early 2022 (as applicable) previously granted to our senior leaders, who have the greatest ability to influence long-term shareholder returns; maintained award thresholds despite change in operating environmentreturns

| | | | |  Support for High Percentage Support for High PercentageComposition of Performance-Based Pay and Rigor of Design High Protection of European Peers in Peer Group | | Conducted Peer group analysis in 2020 and expanded Peer group with two additional U.S. Peers for PSUs and compensation benchmarking

Relative metricsbenchmarking; Peer group continues to be regularly reassessed (most recently in SVC Awards based on U.S. Peers only2023)

| | | | |  Support for Robust Risk-Balancing Features | | Continued use of risk-adjusted metrics, transfer restrictions, retention requirements and recapture provisions and program alignment across our senior leaders

| | |  Support for Robust Risk-Balancing Features Support for Robust Risk-Balancing Features Transparency Regarding Compensation Committee's Committee’s Use of Discretion | | MadeRegular enhancements to Performance Assessment Framework. Framework, which is reviewed annually. In 2020, added a dashboard for the Compensation Committee to assess progress against key strategic goals2023, pillar covering risk management and in 2021, added a People Scorecard to enhance consideration of leadership, culture and values. Framework and metrics reviewed annually and all NEOs individually evaluated pursuant to Frameworkcontrol-related reporting was enhanced

ExpandedRobust proxy disclosureregarding the Committee’s use of informed judgment and structured discretion on pay decisions and the factors considered by the Committee in making its decisions Eliminated ability for Compensation Committee to make certainNo discretionary adjustments to ROE in year-end PSUs; ROE based on as reported metrics | | | | | |  Support for Robust Stakeholder Engagement | | Continuedcommitment to engagementby Lead Director and Compensation Committee Chair

|

| | | | | | 40 | | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERSGoldman Sachs | GOLDMAN SACHSProxy Statement for the 2024 Annual Meeting of Shareholders | | | 39

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS HOW OUR COMPENSATION COMMITTEE MAKES DECISIONS

CRO Input CRO InputRisk ManagementControls

Effective risk management underpins everything we do, and ourOur compensation program is carefully designed to be consistent with the safety and soundness of our firm.firm and to help promote the strength of our risk management and control environment.

| | ∎ | | Our CRO presented the annual risk assessment jointly to our Compensation Committee and our Risk CommitteeCommittees in order to assist with the evaluation of our program’s design. |

| » This assessment, which is also reviewed by our independent compensation consultant, is focused on whether our program is consistent with regulatory guidance providing that financial services firms should ensure that variable compensation does not encourage imprudent risk-taking.risk taking. » Our Compensation Committee and our CRO believe that the various components of our compensation program, including compensation plans, policies and practices, as well as our Committee’s use of informed judgment, work together to balance risk and reward in a manner that does not encourage imprudent risk-taking.risk taking. For example: |

| | | | | | | | | | | | | | | | | | | | Compensation is

considered based on

risk-adjusted metrics,

such as net revenues and

ROE (which are reflected

in our Performance Assessment

Framework) | | | | Significant portion of pay

in equity-based awards

aligns with long-term

shareholder interests | | | | Transfer Restrictions, Retention Requirements restrictions,

retention requirements

and Stock Ownership Guidelinesstock ownership

guidelines work together

to align compensation with

long-term performance

and discourage imprudent

risk-taking | | | | Recapture provisions

provisions mitigate imprudent

risk-taking; misconduct

or improper risk

analysis could result

in clawback or forfeiture

of compensation |

| ∎ | | In addition, as described under —Firmwide Performance, in 2023 the Assessment Framework was updated to include enhanced risk management and control-related reporting and enhanced engagement with senior leaders across Legal, Compliance, Risk and Internal Audit to inform compensation decisions for our NEOs and other senior leaders. |

Our Compensation Committee also considers regulatory matters and the views of our regulators when determining NEO compensation. To this end, the Committee receives briefings on relevant regulatory developments.developments, feedback and expectations. See also ——CRO InputRisk Management & Risk ManagementControls..

Input

Our Compensation Committee recognizes the importance of using an independent compensation consulting firm that is appropriately qualified and that provides services solely to our Board and its Committees and not to our firm. | | ∎ | | For 2022,2023, our Compensation Committee received the advice of Meridian. MeridianFW Cook. FW Cook reviewed our Assessment Framework and provided input on our Performance Assessment Framework, our incentive compensation program structure and terms and other compensation matters generally. In addition, theyFW Cook reviewed our CRO’s compensation-related risk assessment and our 20222023 NEO annual compensation program, including with respect to market context and, expectations for Peer compensation, and they providedas needed, may provide additional benchmarking information to the Committee. |

| | ∎ | | Our Compensation Committee determined that MeridianFW Cook had no conflicts of interest in providing services to the Committee and was independent under the factors set forth in the NYSE rules for compensation committee advisors. |

| | | | | | | 40 | Proxy Statement for the 2024 Annual Meeting of Shareholders | Goldman Sachs | | GOLDMAN SACHS | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERS 41

| | |

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS OVERVIEW OF ANNUAL COMPENSATION ELEMENTS AND KEY PAY PRACTICES | | Overview of Annual Compensation Elements and Key Pay Practices |

Our Compensation Committee believes the design of our executive compensation program is integral to further our Compensation Principles, including paying-for-performancepaying for performance and effective risk management.management and controls. In addition, our variable compensation frameworks more broadly govern the variable compensation process for employees who could expose the firm to material amounts of risk (such as our NEOs). | | | | | | | | | | | | | Pay Element | | Characteristics | | Purpose | | 20222023 Annual Compensation | | | | | Base Salary | | Annual fixed cash compensation | | Provides our executives with a predictable level of income that is competitive to salary at our Peers | | For 2022,2023, NEOs received the following annual base salaries: $2.0 million for our CEO, $1.85 million for our COO and CFO and $1.5 million for our other NEOs | | | | | Annual Variable Compensation(a) | | Cash | | Motivates and rewards achievement of company performance and strategic and operational objectives | | In 2022, each of our NEOs received a portion of their annual variable compensation (no more than 40%) in the form of a cash bonus | | | | | | | Equity-Based: PSUs | | Aligns our executives’ interests with those of our shareholders and motivates executives to achieve longer-term performance, and strategic and operational objectives | | Each of our NEOs received at least 60% of their annual variable compensation in the form of PSUs | | | | | | | Cash | | Motivates and rewards achievement of company performance and strategic and operational objectives | | In 2023, each of our NEOs received a portion of their annual variable compensation (no more than 40%) in the form of a cash bonus |

| (a) | Our NEOs participate in the Goldman Sachs Partner Compensation Plan (PCP), under which we determine variable compensation for all of our PMDs. Previously granted SVC Awards are not part of annual compensation. For more information on these one-time, performance-based stock awards, see —Shareholder Value Creation Awards—A Detailed Look. |

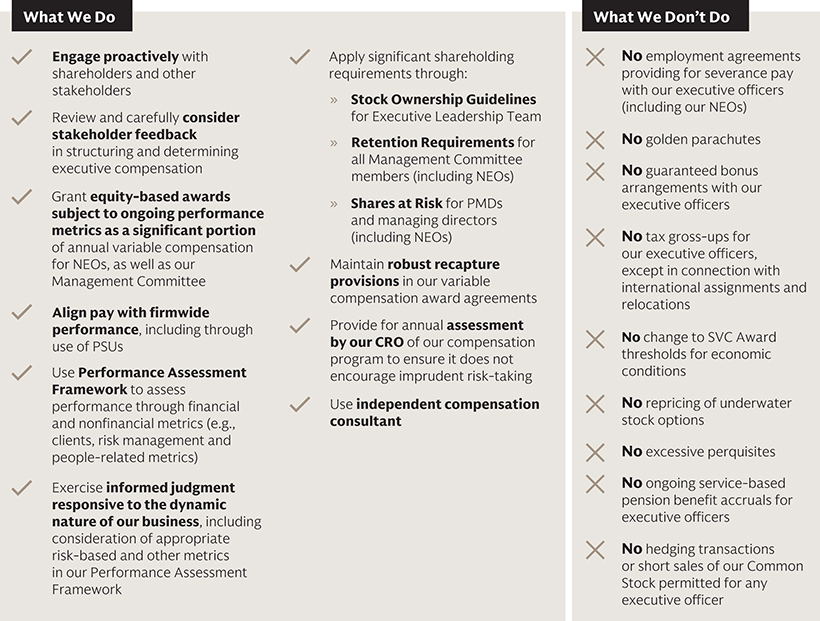

What We Do

as well as our Management Committee

Align pay with firmwide performance, including through use of PSUs

Performance Assessment Framework to assess performance through financial and nonfinancial metrics, (e.g., clients,including with respect to risk management and people-related metrics)

control-related information Exercise informed judgment responsive to the dynamic nature of our business, including consideration of appropriate risk-based and other metrics in our Performance Assessment Framework

Ownership Guidelinesownership guidelines for our Executive Leadership Team

Requirementsrequirements for all Management Committee members (including NEOs)

risk-taking

risk taking and engagement with senior control side leaders on risk and control matters Use independent compensation consultant

Don'tDont Do

(including our NEOs)

No golden parachutes

No change to SVC Award thresholds for economic conditions

| | | | | | 42 | | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERSGoldman Sachs | GOLDMAN SACHSProxy Statement for the 2024 Annual Meeting of Shareholders | | | 41

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS 20222023 ANNUAL COMPENSATION

| | 20222023 Annual Compensation

|

Our Compensation Committee made its annual compensation determinations for our NEOs in the context of our Compensation Principles, which encompass a pay-for-performance philosophy, and after consideration of the factors set forth in —How —How our Compensation Committee Makes its DecisionsDecisions.. | | CompensationOur compensation program reflects our pay-for-performance culture and incentivizes long-term shareholder alignment without undue emphasis on shorter-term resultsresults.

|

| | | | 2022 Annual2023 NEO Compensation for NEOs Reflects Pay-for-Performance PhilosophyReflects:

| | Solid results despite a challenging

economic backdrop

| Strong individual performance

| | | ∎ Second highest net revenuesDecisive leadership in recognizing the need to clarify and full-year EPS as well as double digit returnssimplify our forward strategy ∎ Year-over-year decline in firm performance, including due to impactsSwift execution on a series of challenging operating environmentactions that narrowed our strategic focus and strengthened our platform for 2024 and beyond ∎ Continued progress on strategic priorities in many of our strategic initiatives, with more work needed to fully realize longer-term ambitions | | ∎ Effective leadershipcore franchises: Global Banking & Markets and set appropriate tone from the topAsset & Wealth Management

∎ Led ongoing execution of our strategic priorities, including business realignmentOngoing emphasis on delivering long-term value for shareholders ∎ CommitmentSteadfast focus on client centricity and One Goldman Sachs as foundational to our people strategy, includingfirm ∎ Dedicated commitment to our culture, Core Values and advancing our culture, diversitypeople strategy ∎ Demonstrated investment to promote the strength of our risk management and talent developmentcontrol environment |

20222023 Firmwide Performance: Delivered Solid Results Despite a Challenging Economic BackdropStrong Execution on our Narrowed Strategic Focus and Progress on Other Strategic Priorities

Our Compensation Committee places key importance on the assessment of annual firmwide performance when determining NEO compensation, which is core to our pay-for-performance philosophy. | | ∎ | | Performance is assessed in a holistic manner and was guided by our Performance Assessment Framework (using metrics determined by our Compensation Committee in February 2022)early 2023), without ascribing specific weight to any single factor or metric, as we continue to believe that a formulaic compensation program would not be in the best interests of our firm or our shareholders. |

| | ∎ | | In reviewingThe Committee considered the firm’s 2023 financial performance, for 2022, the Committee receivedboth on an absolute basis and relative financial metrics and considered the comparison to the firm’s record 2021 performance. They also took into account a variety of other firmwide and business specific metrics,peer results, as well as in the context of the broader2023 operating environment and longer-term results. The Compensation Committee recognized that these results were affected by a number of factors, including our strong client franchise performance (as described below) but also the challenging economic backdrop during 2022.execution of the firm’s own initiatives to narrow its strategic focus. While these strategic actions negatively impacted short-term performance, the Compensation Committee believes that the actions of senior management were critical to reorienting the firm with a much stronger platform for 2024 and beyond.

|

| | ∎ | | In addition, the Committee also considered how 20222023 results were achieved, including how the firm continued to invest in its future and how each NEO and each business contributed to the various client, risk management and control, and people-related strategies and goals set forth in the Assessment Framework, including as described in ——20222023 Individual PerformancePerformance.. |

The execution of our narrowed strategic focus and evolution of the firm’s long-term growth strategyprogress on our broader strategic priorities was also central to our Compensation Committee decisions for 20222023 compensation. These actions reinforced the firm’s commitment to serve our clients with excellence and further strengthen our client franchise, which is reflected in the firm’s achievements over the past year. | | ∎ | | Our NEOs, and in particular our Executive Leadership Team, droverecognized the continued execution ofneed to clarify and simplify our forward strategy and swiftly executed on actions to narrow our strategic plan throughout 2022 and made important decisions to evolve the firm’s strategy in line with our long-term goals.focus, including: While continued progress was made, there is more work needed to fully realize our longer-term ambitions. Pursuant to the Performance Assessment Framework, the Committee considered progress towards achieving our strategic goals in 2022 by reviewing a dashboard of progress across various KPIs. |

| | » | | In this regard,The exit of our Marcus lending business and sale of substantially all of our Marcus loan portfolio; |

| » | | The sale of our Personal Financial Management business; |

| » | | The announcement of the Committee took into accountsale of GreenSky, and the sale of the majority of our NEOs’ clear focusGreenSky loan portfolio; |

| | | | | | | Proxy Statement for the 2024 Annual Meeting of Shareholders | Goldman Sachs | | 43 |

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS 2023 ANNUAL COMPENSATION | » | | An agreement with General Motors regarding a process to transition their credit card program to another issuer; and |

| » | | Continued progress on our strategic realignment, which is intended to strengthen our businessespriorities in Global Banking & Markets and improve our efficiency.Asset & Wealth Management. |

| | ∎ | | Each of our NEOs also focused on the continued implementation ofcommitment to an operating approach that deliversOne Goldman Sachs to our clients, is underscored by a multi-year financial-planning process, invests in new and existing businessescapabilities and enhances accountability and transparency. |

| | | | | 42 | | GOLDMAN SACHS | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERS

| | |

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS

2022 ANNUAL COMPENSATION

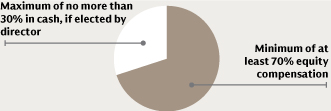

The Committee continues to focus on ensuring that the structure and amount of our NEO compensation appropriately incentivizes our NEOs to continue to build long-term, sustainable growth and to achieve our financial targets, without undue emphasis on shorter-term results. | | ∎ | | For example, each of our NEOs receives at least 60% of his or her variable compensation in equity-based awards that promote alignment with long-term shareholder interests.

| | ∎ | | Further, equity-based awards for our continuing Management Committee members, including for our NEOs, are all in the form of PSUs, resulting in a significant portion of compensation for our most senior leaders being subject to ongoing performance metrics.

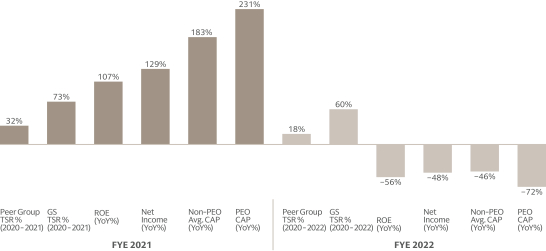

| | | | | | | | | | | | Assessment of 20222023 Firmwide Performance | | | | | | | | | | | Financial performance | | ROE 10.2%7.5%

(+2.6 percentage points Ex. Selected Items and FDIC Special Assessment Fee)(a) | | ROTE(a)(b) 11.0%8.1%

| | Net Revenues $47.446.3 billion | | (2nd highest full-yearRevenues Net of Provisions

net revenues)

$45.2 billion | | EPS $30.0622.87 (2nd highest full-year EPS)+$8.04 Ex. Selected Items and FDIC Special Assessment Fee)(a)

| | | | | | | | | Pre-Tax Earnings $13.510.7 billion (+$3.4 billion Ex. Selected Items and FDIC Special Assessment Fee)(a) | | Efficiency Ratio 65.8%74.6%

| | 1-Year TSR -7.9%15.9%

| | Standardized CET1 Capital Ratio 14.4% | | BVPS Growth 6.7%3.3% YoY

| | | | Progress Across our 2023 Strategic GoalsPriorities | | | | | | | | Grow and

strengthen

existing

businessesGlobal Banking & Markets

| | ∎ Reported record net revenues in FICC financing and Equities financing, enhancing durability of revenues

∎ Ranked #1 in worldwide announced and completed M&A(b); grew wallet share across Global Banking & Marketsmergers and acquisitions, equity and equity-related offerings, and common stock offerings for 2023(c) ∎ Increased AUS by $77 billionRecord total financing revenues across FICC and Equities businesses in 2023 ∎ Top 3 with 117 of the Top 150 FICC & Equities clients in 1H23 vs. 77 in 2019(d) in 2022, including long-term net inflows of $50 billion, resulting in record AUS of $2.5 trillion | | | Diversify our

products and

servicesAsset & Wealth Management

| | ∎ Continued building Transaction banking capabilities, with $70Record Management and other fees of $9.5 billion in deposits at 2022 year-end2023, up 8% YoY, and AUS of $2.8 trillion ∎ Continued to drive third-party alternatives fundraising, with gross third-party alternatives fundraising across strategies24 consecutive quarters of $72 billion in 2022long-term fee-based net inflows ∎ Focus on Workplace and Personal Wealth channelSurpassed our five-year $225 billion alternatives fundraising target, one year ahead of schedule ∎ Net interest income increased 19% year-over-year for 2022 | | | Operate more

efficiently

| | ∎ Diversified funding mix; increased depositsReduced historical principal investments by approximately $23$13 billion year-over-year, reflecting growth in private bank and consumer deposits and transaction banking deposits

∎ Continued to expand presence in strategic locations and make ongoing investments in automation and infrastructureduring the year(e)

|

| (a) Represents the impact from selected items that the firm has sold or is selling related to the firm’s narrowing of its ambitions in consumer-related activities and related to Asset & Wealth Management, including its transition to a less capital-intensive business, as well as the firm’s recognition of the FDIC special assessment fee. For additional information about these items, please see Annex A: Calculation of Non-GAAP Measures and Other Information. (b) For a reconciliation of this non-GAAP measure to the corresponding GAAP measure, please seeAnnex A: Calculation of Non-GAAP Measures and Other Information. (b)(c) Source: Dealogic.

(c) 2022 wallet share vs. 2019 wallet share. Based on reported revenues for Advisory, Equity underwriting, Debt underwriting, FICC(d) Top 150 client list and Equities. Total wallet includesrankings compiled by GS JPM, C, MS, BAC, UBS, BARC, CS, DB.through Client Ranking / Scorecard / Feedback and / or Coalition Greenwich 1H23 and FY19 Institutional Client Analytics ranking.

(d) Includes net inflows(e) Historical principal investments include consolidated investment entities and other legacy investments the firm intends to exit over the medium term (medium term refers to a three to five year time horizon from acquisitions/(dispositions) of $316 billion, substantially all from the acquisition of NN Investment Partners.year-end 2022).

|

20222023 Individual Performance

| | ∎ | | The Committee assesses how each NEO’s individual performance (highlights of which are set forth below) contributed to the firm’s overall performance, including execution of our long-term strategy, as well as how each NEO exhibited effective leadership and set the tone-at-the-top in the stewardship of our culture and Core Values. |

| | ∎ | | The Committee also considers the metrics and factors described in our Performance Assessment Framework, (e.g., clients, risk management and people-related metrics), including assessmentsan assessment of each NEO against the criteria in the Assessment Framework and other factors, in each case as applicable dependent on each NEO’s role. |

| | | | | | 44 | | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERSGoldman Sachs | GOLDMAN SACHSProxy Statement for the 2024 Annual Meeting of Shareholders | | | 43

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS 20222023 ANNUAL COMPENSATION

| | |

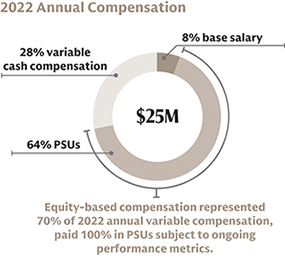

| | David Solomon Chairman and CEO |

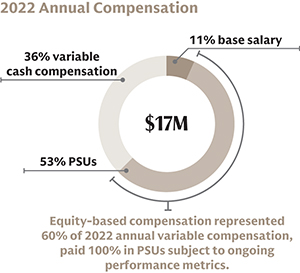

| | | Key Responsibilities | As Chairman and CEO, Mr. Solomon is responsible for leading our business operations and overseeing our firm, leading development and implementation of corporate policy and strategy and serving as primary liaison between our Board and our firm and as a primary public face of our firm. | 20222023 Annual Compensationcash compensation28% variabl8%Compensation cash compensation 28% variabl 6% base salary64% PSUs$25MEquity-basedsalary 65% PSUs $31M Equity-based compensation represented70%represented 70% of 20222023 annual variable compensation,paid 100% in PSUs subject to ongoingperformanceongoing performance metrics.   | | | | | | |

| * | | | | | | | | Percentages do not sum to 100% due to rounding. |

| Key Performance Highlights Mr. Solomon displayed strongdecisive and effective leadership of our firm during 2022, exhibiting relentless2023, demonstrating an unwavering focus on our forwardits long-term strategy, including recognizing the announced evolution thereof, driving strong financial performance despite a challenging operating environmentneed for, and displayingswiftly executing on, the actions to narrow our strategic focus, and an authentic commitment to our people and culture, clients, shareholders and broader stakeholders. Mr. Solomon’s 20222023 dashboard: | | | Strategic Priorities & Clients | ∎ Actively drove our forwardLed the firm through the initial phases of its strategic plan,evolution, including to:by: » Champion client centricity,Championing transparency with external stakeholders about our strategy, including ongoing execution of our One Goldman Sachs approachby hosting the firm’s 2023 Investor Day » Strategically realign and re-organize revenue businessesSwiftly executing on the decisions made to narrow our strategic focus » Narrow the firm’s ambitions for its direct-to-consumer strategy » ContinueContinuing to capitalize on opportunities to expand addressable markets and provide differentiated client service

»∎ ExhibitDisplayed ongoing commitment to ongoing transparencyclient centricity and One Goldman Sachs, including by promoting collaboration across our businesses and through extensive engagement with 2023 Investor Dayour clients around the world

∎ Displayed unwavering commitment to client engagement, delivering consistent, personal engagement with leadersContinued sponsorship of clients across the globe and regularly participating in group client and industry events ∎ Droveour sustainability strategy, in particular to further accelerate and operationalize associated commercial capabilities to serve our clients

| Risk Management | ∎ EmphasizingDemonstrated the importancestrategic imperative of an appropriateregular reinvestment in our enterprise risk management framework to maintain a strong and effective risk management and control environment ∎» Instilling a strongContinued focus on the management of financial and nonfinancial risks

» Engaged actively throughout the year with leaders of our control, finance

and operating functions, including Legal, Risk and Compliance, as well as Internal Audit ∎ Continued strong engagement with our regulatorsActed promptly to direct and top government officials, bothmanage oversight of the firm’s exposures to, and further bolster the firm’s liquidity positions in light of, the Spring 2023 regional banking crisis in the U.S. and globallyEurope ∎ Worked closelyMaintained ongoing engagement with the Boardour key regulators and CRO to manage the firm’s Russia exposure, including with respect to our commitment to unwind our onshore business in response to Russia’s invasion of Ukrainegovernment

leaders worldwide | People | ∎ ContinuedDemonstrated commitment to reinforce our culture and Core Values and continued to advance our people strategy, including by: » Reinvigorating focus onPrioritizing engagement with the firm’s culturepeople across all levels in our offices across the globe, through meetings, small group roundtables and continued emphasis on our employees’ responsibility to protecttownhalls as well as hosting and foster integrity, encourage escalation and hold themselves and others toparticipating in nearly all Cultural Stewardship events during the highest standards of conductyear » SponsoringServing as a senior sponsor of our people and talent initiatives, including progressing towards aspirational diversity goals, developing next generation talent, promoting internal mobility efforts, focusing on aspirational diversity goals, and enhancing wellnesscontinuing investments in our benefits offerings and performance management processes » Leading firmwideInvesting in the leadership of our businesses and external dialoguecontrol, finance and operating functions » Providing thought leadership on important social topics such asand personally demonstrating the firm’s diversity, equity and inclusion strategy and commitment to sustainable financemaintaining a safe and climate transition » Visitingsupportive environment in which all of our offices across the globepeople have an equal opportunity to host internal eventssucceed, grow and underscore the value of “Return to Office” and the firm’s people and culture

» Recruiting various strategic hires and appointing key PMDs to focus on innovation and execution of the firm’s strategybuild a fulfilling career

|

| | | | | | 44 | Proxy Statement for the 2024 Annual Meeting of Shareholders | Goldman Sachs | | GOLDMAN SACHS | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERS 45 |

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS 20222023 ANNUAL COMPENSATION

| | |

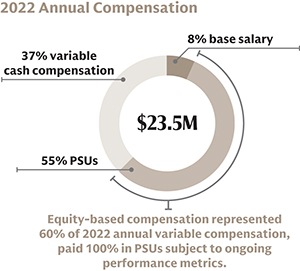

| | John Waldron President and COO |

| | | Key Responsibilities | As President and COO, Mr. Waldron’s responsibilities include managing our day-to-day business, executing our firmwide strategy and other priorities and closely collaborating with our senior management team across the breadth of the firm’s operations, as well as engaging with, and serving as a liaison to, our clients.clients and other stakeholders. | 20222023 Annual Compensationcash compensation37% variable8%compensation38% variable6% base salary$23.5M55%30M56% PSUsEquity-based compensation represented60%represented 60% of 20222023 annual variable compensation,paid 100% in PSUs subject to ongoingperformanceongoing performance metrics.   | | | | | | | | | | | | | | | |

| Key Performance Highlights During 2022,2023, Mr. Waldron displayed dedicateda strong and active focus on the execution and evolution of our firm’s forward strategy, and driving progress towards our executionnarrowed focus and other strategic priorities with a continued attention to further enhancing our expense discipline. In doing so, he provided robustdedicated leadership forof the firm’s businesses and operations while continuing extensivemaintaining significant client engagement. Mr. Waldron’s 20222023 dashboard: | | | Strategic Priorities & Clients | ∎ Continued dedicated focus on our One Goldman Sachs strategy, including by promoting collaboration access our businesses and actively engaging with clients ∎ Actively assessed key client franchises across the firm and established working groups to drive progress for key cross-business client channels

∎ DroveLed execution and evolution of our forward strategy,strategic priorities, including by:

» Actively managing revenue, control, finance and operating functions in pursuit of the firm’s strategy

» Driving execution priorities, growth initiatives and achievement of KPIs in close partnership with business and functional leaders across the firm » Overseeing operating efficiency initiatives, including continued optimization of organizational structure and progressing automation efforts » Overseeing firmwide integration efforts in respectDriving significant focus on the reduction of our historical principal investments » Engaging with internal and external stakeholders on our strategic realignmentpriorities ∎ Continued focus on our One Goldman Sachs strategy, including by promoting collaboration across our businesses and new operating segmentsassessing key client franchises across the firm, establishing working groups under our Firmwide Client Franchise Committee to drive progress for key cross-business client channels, and maintaining high levels of client engagement | Risk Management | ∎ Collaborated closely with control, financing and operating teams with aMaintained focus on the management of financial and nonfinancial risks as well as efficient management of resources firmwide. In doing so, closely collaborated with control, finance and operating functions and demonstrated a commitment to a strong risk management and efficient management of resource consumption and capital allocation firmwide, as well as to sponsor assessments of first-line controls, roles and responsibilitiescontrol environment ∎ Assumed co-chair roleServed as Co-Chair (alongside CRO) of the Enterprise Risk Committee with a focus on enhancing the monitoring and review of risk across the firm ∎ Oversaw reputational risk management as chairChair of the Firmwide Reputational Risk Committee

∎ Significant attention to evolution of our China strategyengagement around regional strategies in the context of an evolving market and geopolitical landscape ∎ Maintained ongoing dialogue with key regulators and government leaders globally | People | ∎ Drove continued focus on the firm’s location strategyEngaged regularly with our people and fostered collaboration through individual meetings, small group roundtables and townhalls throughout our offices globally ∎ Sponsored major people and talent initiatives, including: » Continuing to enhance the firm’s leadership pipeline review process and related leadership development educationinitiatives to increase transparency, governance and other initiativesrigor around

succession planning » Sponsoring Pine Street and Partnership Committee efforts to invest in culture, connectivity and talent development » Sponsoring diversity, equity and inclusion networks and initiatives

across the firm » Leading PMD selectionmanaging director promotion process ∎ Drove efforts related to the firm’s location and real estate strategy |

| | | | | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERS | GOLDMAN SACHS 46 | | 45 Goldman Sachs | Proxy Statement for the 2024 Annual Meeting of Shareholders | | |

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS 20222023 ANNUAL COMPENSATION

| | |

| | Denis Coleman CFO |

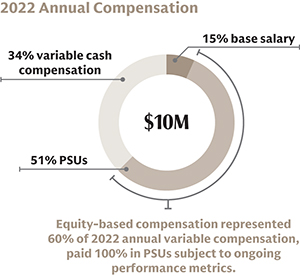

| | | Key Responsibilities | As CFO, Mr. Coleman is responsible for managing the firm’s overall financial condition, as well as financial analysis and reporting. In addition, he oversees various control functions, operations and technology and closely collaborates across our senior management team, including on issues relating to risk management and firmwide operations. | 20222023 Annual Compensation36%Compensation 36% variable cash compensation11%compensation 9% base salary53% PSUs$17MEquity-basedsalary 54% PSUs $20M Equity-based compensation represented60%represented 60% of 20222023 annual variable compensation,paid 100% in PSUs subject to ongoingperformanceongoing performance metrics.   | | | | | |

| * | Percentages do not sum to 100% due to rounding. |

| Key Performance Highlights In 2022,2023, Mr. Coleman successfully transitioned to his role as CFO, providingprovided strong oversight of the firm’s capital, liquidity and balance sheet to support the execution of the firm’s strategic and operational goals with an enduring focus on ensuring the financial safety and soundness of the firm.firm and the strength of our risk management and control environment. Mr. Coleman’s 20222023 dashboard: | | | Strategic Priorities & Clients | ∎ Actively engaged with clients in partnership with business leaders ∎ Focused on ensuringSuccessfully navigated market volatility to ensure the firm had appropriate capital, liquidity and balance sheet to prudently deploy towards franchise activity as well as future growth

∎ Closely collaborated with our CEO and COO on the execution of our strategic priorities, with regular stakeholder engagement related thereto and concerted focus on deepening relationships with investors aimed at raising greater awareness around our firm’s strategy and performance ∎ Engaged with clients in partnership with business leaders | Risk Management | ∎ Actively managedDemonstrated a strong commitment to investing in and promoting the strength of our risk management and control environment and maintained focus on the management of both financial and nonfinancial risks ∎ Managed the firm’s financial resources, including to: » Manage capital and liquidity through market volatility, while ensuringincluding the regional banking crisis and U.S. debt ceiling negotiations, maintaining sufficient capacity to meet internal and regulatory requirements » Focus on enhancing expense disciplinemanagement across our businesses » Deploy resources to strategic opportunities

∎ Engaged in ongoing dialogue with key regulators and strategic government officials, including with respect to the firm’s navigation of global macro events ∎ Collaborated with the CEO and COO on the execution of our strategic realignment, including oversight of implications for our financial reporting

∎ Drove significant focus on maintaining and further enhancing the strength of the firm’s control functions and emphasized the importance of an appropriate control environment

∎ Oversaw the firm’s efforts to manage the firm’s Russia exposure in response to Russia’s invasion of Ukraineleaders

∎ Served as Vice Chair of the Enterprise Risk Committee and as Co-Chair of the Firmwide Asset Liability Committee | People | ∎ Engaged with our people across the firm in support ofand continued his transition to CFO ∎ Regularly convened leadershipfocus on convening leaders across control, finance and operating functions to enhancefoster greater alignment and collaboration

∎ Championed the firm’s people cultural and talent initiatives, including through participation in the PMDmanaging director selection process, leadership pipeline reviews and various other key programs ∎ Advanced the firm’s culture through participation in the firm’s Cultural Stewardship Program and Culture Connect Forums |

| | | | | | 46 | Proxy Statement for the 2024 Annual Meeting of Shareholders | Goldman Sachs | | GOLDMAN SACHS | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERS 47 |

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS 20222023 ANNUAL COMPENSATION

| | |

| | Kathryn Ruemmler CLO and General Counsel |

| | | Key Responsibilities | As CLO and General Counsel, Ms. Ruemmler leads the firm’s Legal division, providing oversight for the firm’s legal affairs worldwide, and oversees the Compliance division and Conflicts Resolution Group, which oversight serves to enhance collaboration across these disciplines and ensure a consistent approach to addressing the legal, compliance and reputational risk issues facing the firm. | 2023 Annual Compensation*9% base salary cash compensation 36% variable$16M54% PSUsEquity-based compensation represented 60% of 2023 annual variable compensation, paid 100% in PSUs subject to ongoing performance metrics.2023 Annual Compensation* 9% base salary cash compensation 36% variable $16M 54% PSUs Equity-based compensation represented 60% of 2023 annual variable compensation, paid 100% in PSUs subject to ongoing performance metrics.  * Percentages do not sum to 100% due to rounding. | | | | | | | | | | | | |

| Key Performance Highlights In 2023, Ms. Ruemmler continued to serve as an invaluable advisor to firm leadership across a broad range of legal, reputational and regulatory matters with a strong track record of exceptional judgment and informed and sound counsel. She also brought certain long-standing litigation matters to successful resolution while continuing to enhance collaboration and synergies across the Legal, Compliance and Conflicts Resolution functions. Ms. Ruemmler’s 2023 dashboard: | | Strategic Priorities & Clients | ∎ Regularly provided counsel to senior management on the development and execution of our strategic priorities | Risk Management | ∎ Championed the ongoing investment in our risk management and control environment, serving as a sponsor and leader of our efforts to strategically enhance our enterprise risk management framework ∎ Provided informed and sound counsel to leaders across the firm on a broad range of legal, reputational and regulatory matters ∎ Significant focus and leadership on the firm’s litigation strategy, bringing several key matters to a successful resolution in 2023 ∎ Enhanced the firm’s engagement model with key regulators by pursuing a more centralized and robust approach to engagement, exam management, responses and, where applicable, remediation ∎ Significant focus on the management of reputational risk, including as Co-Vice Chair of the Firmwide Reputational Risk Committee | People | ∎ Invested substantial time and thought leadership as Chair of the Firmwide Conduct Committee, including emphasizing the importance of integrity as an expectation of our people and leaders ∎ Focused on supporting and implementing the firm’s people strategy goals across Compliance, Legal and Conflicts Resolution functions, including furthering issues of equity, diversity and inclusion across all areas of the firm ∎ Led continued efforts to refine and improve our organizational structure, including with ongoing focus on enhancing collaboration and synergies across the Legal, Compliance and Conflicts Resolution functions |

| | | | | 48 | | Goldman Sachs | Proxy Statement for the 2024 Annual Meeting of Shareholders | | |

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS 2023 ANNUAL COMPENSATION | | |

| | Philip Berlinski Global Treasurer |

| | | Key Responsibilities | As Global Treasurer, Mr. Berlinski is responsible for overseeing the firm’s Corporate Treasury function, which manages the firm’s liquidity, payments, funding, balance sheet and capital to maximize net interest income and return on equity through liability planning and execution, financial resource allocation, asset liability management and liquidity portfolio management. Mr. Berlinski also serves as CEO of Goldman SachsGS Bank USA.and as interim Co-Head or Head of Platform Solutions. | 20222023 Annual Compensation34%Compensation 35% variable cash compensation15%compensation 12% base salary$10M51% PSUsEquity-basedsalary $13M 53% PSUs Equity-based compensation represented60%represented 60% of 20222023 annual variable compensation,paid 100% in PSUs subject to ongoingperformanceongoing performance metrics.   | | | | | | | | | | | | | | | |

| Key Performance Highlights During 2022,2023, Mr. Berlinski effectively managed the firm’s liquidity position through continued market volatility, appropriately balancing his technical responsibilities while supporting business growth in our core franchises, as well as focusing on enhancingfranchises. He also successfully assumed the firm’s strategy for conducting activity in our banking entities.role of interim Co-Head or Head of Platform Solutions, with significant engagement and oversight of the Enterprise Platforms and Transaction Banking businesses. Mr. Berlinski’s 20222023 dashboard: | | | Strategic Priorities & Clients | ∎ Focused on ensuring the firm hasmaintaining appropriate liquidity to support franchise activity as well asand future growth ∎ Engaged with a range of firmPlatform Solutions clients and strategic partners as well as fixed income investors | Risk Management | ∎ Maintained strong tone-at-the-top with demonstrated commitment to the strength of our risk management and control environment across his various responsibilities ∎Successfully managed the firm’s liquidity position throughand navigated continued market volatility throughout the year, including in connection with Russia’s invasion of Ukraine,during the regional banking crisis and U.S. debt ceiling negotiations, and ensured sufficient liquidity to meet internal and regulatory needs ∎ Progressed criticalPartnered with Risk to strengthen the firm’s liquidity and funding management processes, including to enhance the firm’s liquidity stress testing and intraday liquidity risk model and capabilities ∎ Continued to progress liquidity optimization management initiatives, including to: » Achieve medium-term target of optimizing the firm’s unsecured funding mix via deposit growth channels » Reduce need for benchmark issuances

»Deliver enhanced liquidity projections

∎» Reduced interest expense throughAdd new funding diversification, product innovation and efficiency optimizationchannels to enable the firm to bolster funding in times of stress

∎ Continued progress on theto lead efforts to facilitate growth and migration of businesses to Bank entities with a focus on enhancing GS Bank governance and oversight and on GS Bank risk management and controls ∎ Represented the firm by leading G-SIB Treasurer discussions on markets, liquidity and regulations with key regulators and policy-makerspolicy makers ∎ Served as Chair of the GS Bank Management Committee and Co-Chair of the Firmwide Asset Liability Committee | People | ∎ Focused on supporting and implementing the firm’s people strategy goals in Corporate Treasury.Treasury and Platform Solutions. In doing so, he partnered with HCM to invest in our people develop our managers as coaches, strengthen ourand culture and advance diversity, equity and inclusion |

| | | | | | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERS | GOLDMAN SACHS | 47 |

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS

2022 ANNUAL COMPENSATION

| | |

Proxy Statement for the 2024 Annual Meeting of Shareholders | Goldman Sachs | | Kathryn Ruemmler49

CLO and General Counsel

|

| | | Key Responsibilities

| As CLO and General Counsel, Ms. Ruemmler leads the firm’s Legal department, providing oversight for the firm’s legal affairs worldwide, and oversees the Compliance and Conflicts Resolution Group, which oversight serves to enhance collaboration across these disciplines and ensure a consistent approach to addressing the legal, compliance and reputational risk issues facing the firm.

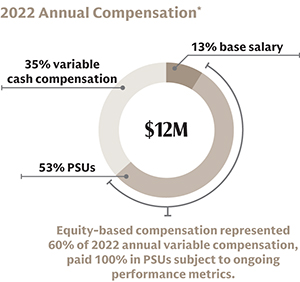

| 2022 Annual Compensation*13% base salary cash compensation 35% variable$12M53% PSUsEquity-based compensation represented60% of 2022 annual variable compensation,paid 100% in PSUs subject to ongoingperformance metrics.

* Percentages do not sum to 100% due to rounding.

| | | | | | | | | | | | |

| Key Performance Highlights

In 2022, Ms. Ruemmler exhibited exceptional judgment and provided sound counsel to the firm across a breadth of matters, utilizing decisive decision-making over various legal and regulatory matters of importance to the firm and enhancing collaboration and synergies across the Legal, Compliance and Conflicts Resolution functions.

Ms. Ruemmler’s 2022 dashboard:

| | Risk Management

| ∎ Key advisor to the firm across a broad range of legal, reputational and regulatory matters, including in her oversight of the firm’s litigation and enforcement strategy

∎ Leader of continued efforts to refine and improve our organizational structure and fulfill our ongoing responsibility to continually enhance the control functions, including by bringing together and enhancing collaboration and synergies across the Legal, Compliance and Conflicts Resolution functions

∎ Significant focus on the management of reputational risk, including as Co-Vice Chair of the Firmwide Reputational Risk Committee

∎ Continued responsibility for executive oversight of the firm’s 1MDB-related remediation program, including providing updates to the 1MDB Remediation Special Committee

| People

| ∎ Invested substantial time and thought leadership as chair of the Firmwide Conduct Committee, focusing on ensuring that our cultural expectations are well communicated across the firm and developing and launching leadership, culture and values educational programs for all PMDs and managing directors

∎ Focused on supporting and implementing the firm’s people strategy goals across Compliance, Legal and Conflicts Resolution, including with respect to “Return to Office” and diversity, equity and inclusion matters

|

| | | 48 | | GOLDMAN SACHS | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERS |

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS EQUITY-BASED ANNUAL VARIABLE COMPENSATION ELEMENTS OF ANNUAL COMPENSATION—A MORE DETAILED LOOKCOMPENSATION: PSUS | | Equity-Based Annual Variable Compensation Elements of Annual Compensation—A More Detailed LookCompensation: PSUs |

We believe it is important to pay a significant portion of our annual variable compensation in equity-based awards. To this end, for 20222023 annual compensation, 70% of Mr. Solomon’s and 60% of all other NEOs’ variable compensation was paid 100% in PSUs. The use of PSUs as a consistent form of equity-based compensation across our NEOs and our broader Management Committee serves to align the compensation structure across our most senior leaders and further ties compensation for this population to ongoing performance metrics.

Our equity-based variable compensation is subject to various robust risk-balancing features, as described more fully in —Other —Other Compensation Policies and Practices. Treatment upon a termination of employment or change in control is described more fully in —Executive —Executive Compensation—Potential Payments upon Termination or Change in Control. | | | | | | | | | | | Year-End PSUs—Overview of Material Terms | | | | | | | | | | | | | | | | | | | | | | | |

| ∎ PSUs provide recipients with annual variable compensation that has a metrics-based outcome. The ultimate value paid to the NEO is subject to firm performance both through stock price and a metrics-based structure. ROE is used because it is a risk-based metric that is an important indicator of the firm’s operating performance and is viewed by many stakeholders as a key performance metric. ∎ PSUs will be paid at 0-150% of the initial award based on our average ROE over 2023-2025,2024-2026, using absolute and relative metrics as described in the below table. |

| | | | | | | | | | | | | | | | | | | | | | | 3-Year Average Absolute ROE | | % Earned | | | | | | | | | | | | 3-Year Average Relative ROE | | % Earned(a) | | | | | <5% | | 0% | | | | | |

| | | | | | <25th percentile | | 25% | | | | | 5% to <16% | | Based on relative ROE; see scale at right | | | | | | | | | | 25th percentile | | 50% | | | | | | | | | | | | | 60th percentile | | 100% | | | | | ≥16% | | 150% | | | | | | | | | | ≥75th percentile | | 150% | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | 3-Year Average Absolute ROE | | % Earned | | | | | | | | 3-Year Average Relative ROE | | % Earned(a) | | | | | <5% | | 0% | | | | | |

| | <25th percentile | | 25% | | | | | 5% to <16% | | Based on relative ROE; see scale at right | | | | | | 25th percentile | | 50% | | | | | | | | | 60th percentile | | 100% | | | | | ≥16% | | 150% | | | | | | ≥75th percentile | | 150% | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (a) %Percentage earned is scaled if performance is between specified thresholds; payout is automatically capped at 100% if 3-year average GS ROE is between 5% and 6%. ∎ PSU performance thresholds for PSUs granted in January 2024 (for 2023 (for 2022 year-end compensation) were unchanged year-over-year. Our Compensation Committee continues to believe these thresholds are appropriate to incentivize senior management to achieve our strategic goals and enhance long-term shareholder value. ThresholdsPSU design, including performance thresholds, will continue to be reviewed annually in connection with annual compensation decisions. ∎ PSUs granted in January 20232024 will be settledsettle in 2026.2027. For the CEO, COO and CFO, PSUs will be settledsettle 50% in cash based on the average closing price of our Common Stock over a ten-trading-day period and 50% in Shares at Risk. For our other NEOs, PSUs will settle 100% in shares of Common Stock, substantially in the form of Shares at Risk. |

| | ∎ | | For purposes of the relative ROE metric, for PSUs granted in January 2023,2024, our Peers consist of Bank of America Corporation; Citigroup, Inc.; JPMorgan Chase & Co.; Morgan Stanley; The Bank of New York Mellon Corporation; Wells Fargo & Company; Barclays PLC; Credit Suisse Group AG; Deutsche Bank AG;AG and UBS Group AG. Our Compensation Committee believes that these Peers appropriately and comprehensively reflect those firms that have a major presence across our collection of scaled businesses and that have regulatory requirements (such as with respect to capital) similar to ours. |

| | ∎ | | Average ROE is the average of the annual ROE for each year during the performance period. |

| | » | | Annual ROE for the firm is calculated as annualized net earnings applicable to common shareholders divided by average common shareholders’ equity, as publicly reported by Goldman Sachs in its annual report, and rounded to one decimal place. |

| | » | | For purposes of determining ROE of our Peers with respect to the PSUs’ relative metrics, annual ROE is as reported in the Peer company’s publicly disclosed annual report, rounded to one decimal place. |

| | | | | | 50 | | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERSGoldman Sachs | GOLDMAN SACHSProxy Statement for the 2024 Annual Meeting of Shareholders | | | 49

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS EQUITY-BASED LONG-TERM INCENTIVE: SHAREHOLDER VALUE CREATION AWARDS—A DETAILED LOOKAWARDS | | ∎ | | In certain circumstances (e.g., a merger, change in corporate structure or other similar corporate transaction) that result in a substantial change in a Peer company’s business or revenue mix, the Committee mayshall adjust the Peer group and/or make such other equitable adjustments as the Committee deems appropriate. |

| » | | Following the Credit Suisse merger with UBS Group AG in 2023, the Compensation Committee amended the peers for outstanding PSUs (those granted in respect of 2020-2022 year-end compensation) to reflect this transaction. |

| » | | For purposes of relative ROE calculations, Credit Suisse ROE will be included only when there is a full year of reported ROE available (2021 and 2022 ROE only, as applicable). Accordingly, Credit Suisse has been removed from the Peer group for the 2022 Year-End PSUs (2023-2025 performance period) and for PSUs going forward. |

| | ∎ | | Certain adjustments (e.g., to a Peer company’s ROE for purposes of the relative ROE calculation) will be based on publicly disclosed financial information. |

| | ∎ | | Each PSU granted to our NEOs includes a cumulative dividend equivalent right payable only if and when that PSU is earned. |

| | ∎ | | PSUs granted to our NEOs who meet certain age and service requirements on the grant date have no additional service-based vesting requirement; however, all PSUs are subject to various robust risk-balancing features, as described in —Other —Other Compensation Policies and Practicesbelow. |

| | ∎ | | For information on the vesting and settlement of Messrs. Solomon’sSolomon and Waldron’s 2018 2019 year-end PSUs during 2022,2023, see —Executive Compensation—20222023 Stock Vested. |

| | Equity-Based Long-Term Incentive: Shareholder Value Creation Awards—A Detailed LookAwards |

As previously disclosed, the non-employee members of our Board, upon the recommendation of our independent Compensation Committee, granted SVC Awards to Messrs. Solomon and Waldron in October 2021 and, in response to shareholder feedback regarding the importance of broadening the scope of these awards’ key objectives across our senior leadership team, more broadly to members of our Management Committee, including Messrs. Coleman and Berlinski and Ms. Ruemmler, in January 2022. SVC Awards were designed to addressthree key objectivesandalign the incentive structureacross our most senior leaders. | | | | | | | | | | | | | | | 1  | | Align compensation with rigorous performance thresholds that drive long-term shareholder value creation | | | 2  | | | | | | | | | | | | | | | | | | 1 | | Align compensation with rigorous performance thresholds that drive long-term shareholder value creation | | 2 | | Ensure leadership continuity over the next phase of our growth strategy | | 3 | | Enhance retention in response to the increasing competition for talent in the current environment | | | | | | | | | | | | | | | | | | | | |

| | Ensure leadership continuity over the next 5+ years in the next phase of our growth strategy | | | 3  |

| | Enhance retention in response to the increasing competition for talent in the current environment | | | | | | | | | » Even at maximum payout, awards represent ~55 basis points of the total shareholder value (from the time of grant) that would be created by achieving the TSR goals

| | | | | | »The Board believes that senior management’s leadership and vision will continue to be critical in driving the firm’s progress

| | | | | | » Recent experience shows significant opportunities for our senior leadership in less traditional sectors of the financial industry

|

| ∎ | | While SVC Awards were originally granted to only Messrs. Solomon and Waldron in October 2021, the Board expanded these awards more broadly to members of the Management Committee in January 2022 in response to shareholder feedback regarding the importance of broadening the scope of the awards’ key objectives across our senior leadership team. We believe this will further enhance collaboration and teamwork.

|

As we already committed, the previously granted SVC Awards were not part of annual compensation and will not be awarded on a regularly recurring basis. 2022 2023 annual compensation was determined based on the factors described in—How —How our Compensation Committee Makes Decisions and—2022 —2023 Annual Compensation above.

| | | | | | | 50 | Proxy Statement for the 2024 Annual Meeting of Shareholders | Goldman Sachs | | GOLDMAN SACHS | PROXY STATEMENT FOR THE 2023 ANNUAL MEETING OF SHAREHOLDERS 51

| | |

COMPENSATION MATTERS—COMPENSATION DISCUSSION AND ANALYSIS OTHER COMPENSATION POLICIES AND PRACTICES | | | | | | | | | | | | | | | Key Terms of our NEOs’ SVC Awards | | | | Grant Details | | Form: Performance stock units Amount of Award/Grant Date(a) ∎ October 21, 2021: Mr. Solomon - $30 million ($17.0 million grant date fair value; 73,264 performance stock units); Mr. Waldron - $20 million ($11.4 million grant date fair value; 48,843 performance stock units) ∎ January 28, 2022: Mr. Coleman - $10 million ($3.3 million grant date fair value; 24,422 performance stock units); Mr. Berlinski and Ms. Ruemmler - $7 million each ($2.3 million grant date fair value; 17,095 performance stock units) Conversion Price: The number of performance stock units was calculated using a conversion price of $409.48, the 5-day average closing price from October 15 - 21, 2021 | | | | | | | | TSR Thresholds

(Absolute & Relative) | | | | Cumulative