The Board of Directors seeks to ensure that the Board of Directors is composed of members whose particular experience, qualifications, attributes and skills, when taken together, will allow the Board of Directors to satisfy its oversight responsibilities effectively. As discussed below under “Corporate Governance and Nominating Committee” beginning on page 7,8, a slate of Directors to be nominated for election at the annual shareholders’ meeting each year is approved by the Board of Directors after recommendation by the Corporate Governance and Nominating Committee. In the case of a vacancy on the Board of Directors (other than one resulting from removal by shareholders), the Corporate Governance and Nominating Committee will identify individuals believed to be qualified candidates to serve on the Board of Directors approvesand will recommend any director nominees to the full Board of Directors for election. The Board of Directors will then approve a Directordirector nominee to fill the vacancy followingon the recommendationBoard of a candidate by the Chairman of the Board.Directors. In identifying candidates for Director, the Corporate Governance and Nominating Committee and the Board of Directors take into account (1) the comments and recommendations of board members regarding the qualifications and effectiveness of the existing Board orof Directors or additional qualifications that may be required when selecting new board members that may be made in connection with the self-examinations described below under “Corporate Governance and Nominating Committee” beginning on page 7,8, (2) the requisite expertise and sufficiently diverse backgrounds of the Board of Directors’ overall membership composition, (3) the independence of outside Directors and other possible conflicts of interest of existing and potential members of the Board of Directors and (4) all other factors it considerssuch bodies consider appropriate. Although the Company has no formal policy regarding diversity, the charter of the Corporate Governance and Nominating Committee includes a statement that it and the Board of Directors believe that diversity is an important component of a board of directors, including such factors as background, skills, experience, expertise, gender, race and culture. As mentioned above, the Corporate Governance and Nominating Committee and the Board of Directors include diversity as one of several criteria that they consider in connection with selecting candidates for the Board.Board of Directors. The Board of Directors seeks to ensure that the Boardit is composed of members whose particular background, expertise, qualifications, attributes and skills, when taken together, allow the Board of Directors to satisfy its oversight responsibilities effectively.

| Mr. Hovnanian has been Chief Executive Officer since July 1997 after being appointed President in 1988 and Executive Vice President in 1983. Mr. Hovnanian joined the Company in 1979 and has been a Director of the Company since 1981 and was Vice Chairman from 1998 through November 2009. In November 2009, he was elected Chairman of the Board following the death of Kevork S. Hovnanian, the chairman and founder of the Company and the father of Mr. Hovnanian. |

| |

| Mr. Coutts retired from the position of Executive Vice President of Lockheed Martin Corporation (NYSE), which he held from 2000 to 2008. Mr. Coutts was President and COO of the former Electronics Sector of Lockheed Martin. He was elected an officer by the Board of Directors of Lockheed Martin in December 1996. Mr. Coutts held management positions with General Electric Corporation (NYSE) from 1972-1993,1972 to 1993, and was with GE Aerospace when it became part of Lockheed Martin in 1993. Mr. Coutts is the retired Chairman of Sandia Corporation, a subsidiary of Lockheed Martin Corp., and is on the Board of Directors of Stanley Black and Decker (NYSE) and is the Chairman of the Governance and Nominating Committee,, as well as the Pall Corporation (PLL)(NYSE), and is also a member of the Board of Overseers, College of Engineering, Tufts University. He is a Member of the Chapter of the National Cathedral. He was elected as a Director of Hovnanian Enterprises, Inc. in March 2006 and is a member of the Company’s Compensation Committee. |

| Mr. Kangas was the Global Chairman and Chief Executive Officer of Deloitte Touche Tohmatsu from December 1989 to May 2000, when he retired. He also serves on the Boards of Directors of United Technologies Corp. (NYSE), AllScripts, Inc. (NASDAQ), Tenet Healthcare Corporation, Inc. (NYSE), and Intuit, Inc. (NASDAQ). He was on the Board of Directors of Electronic Data Systems, Inc. (NYSE) from 2004 to 2008.2008 and AllScripts, Inc. (NASDAQ) (and, prior to its merger with AllScripts, Inc., Eclipsys Corporation (NASDAQ)) from 2004 to 2012. Mr. Kangas is the past Chairman of the Board of the National Multiple Sclerosis Society. Mr. Kangas was elected as a Director of Hovnanian Enterprises, Inc. in September 2002, is Chairman of the Company’s Audit Committee and a member of the Company’s Compensation Committee and Corporate Governance and Nominating Committee. |

| | |

| Mr. Marengi, sincefrom July 2007 servesto March 2012, served as a Venture Partner for Austin Ventures. Prior to that date, Mr. Marengi served as senior vice president for Dell Inc.’s (NASDAQ)the Commercial Business Group.Group of Dell Inc. (NASDAQ). In this role, Mr. Marengi was responsible for the Dell units serving medium business, large corporate, government, education and healthcare customers in the United States. Mr. Marengi joined Dell in July 1997 from Novell Inc. (NASDAQ), where he was president and chief operating officer. He joined Novell in 1989 and moved through successive promotions to become executive vice president of worldwide sales and field operations. He is also an outside Director for Quantum Corporation (NYSE) and is a member of the Compensation Committee and se rves as Chairman ofsits on the Board forof Entorian Technologies, Inc. (NASDAQ)(formerly, the OTC Markets). Mr. Marengi was elected Directorto the Board of Directors of Hovnanian Enterprises, Inc. in March 2006 and is member of the Company’s Corporate Governance and Nominating Committee. |

| | |

| Mr. RobbinsPagano was a managingpartner at Simpson Thacher & Bartlett LLP until his retirement at the end of 2012. He was the head of the firm’s capital markets practice from 1999 to 2012, and, before that, administrative partner of the New York office of Kenneth Leventhal & Company and executive committee partner, retiring from the firm in 1992. He was made a partner of Kenneth Leventhal & Company in 1973. Mr. Robbins was a Trustee of Keene Creditors Trust from 1996 until July 2009.to 1999. He was Director and the Chairman of the Audit Committee of Raytech Corporation from May 2003 until March 2007, and was a Director and Chairman of the Audit Committee of Texas Petrochemicals Inc. from May 2006 until December 2009. Mr. Robbins was elected as a Director of Hovnanian Enterprises, Inc. in January 2001, and is a member of the Company’s Audit Committee.firm’s executive committee during nearly all of that period. He also serves on the Board of Directors of Cheniere Energy Partners GP, LLC, the general partner of Cheniere Energy Partners (NYSE MKT). Mr. Pagano serves on the Engineering Advisory Council of Lehigh University. |

| | |

| Mr. Sorsby has been Chief Financial Officer of Hovnanian Enterprises, Inc. since 1996, and Executive Vice President since November 2000. Mr. Sorsby was also Senior Vice President from March 1991 to November 2000 and was elected as a Director of the Company in 1997. He is Chairman of the Board of Visitors for Urology at The Children’s Hospital of Philadelphia (“CHOP”) and also serves on the Institutional Advancement Committee at CHOP. |

| | |

| Mr. Weinroth is a partner in Coral Reef Capital Partners, a private equity fund and was from 2003 untilto mid-2008 a Managing Member of Hudson Capital Advisors, LLC and since then he has been an advisor to Coral Reef Capital Partners, a private equity and merchant banking firm. From 1989successor firm to 2003, he served as co-Chairman and headsome of the Investment Committee at First Britannia Mezzanine N.V., a European private investment firm. Hudson Capital employees. He is Chairman of the Board Emeritus(Emeritus) of Core Laboratories, N.V. (NYSE), a global oil field service company where he had previously been Chairman from 1994 through 2001. From l989 to 2003, he served as Co-Chairman and head of the Board from 1994 to 2001.Investment Committee of First Britannia Mezzanine, N.V., a European private investment firm. He was Vice Chairis presently Chairman of the Central Asian AmericanAsia Education Foundation, a successor to the Central Asian-American Enterprise Fund, to which he was appointed by the President of the United States, and is Chairman of its successor, the US Central Asia Education Foundation. HeStates. Mr. Weinroth has been Chairman of four NYSE listedNYSE-listed companies and chief executiveChief Executive of three of them. He is also a Trustee and the immediate past Chairman of The Joyce Theatre Foundation, Inc., and a Trustee of the Paul Taylor Dance Foundation as well as a recently retired TrusteeBoard member of the Horace Mann School.Flea Theater. Mr. Weinroth has been a Director of Hovnanian Enterprises, Inc. since 1982, is a member of the Company’s Audit Committee, and Chairman of the Company’sCompany's Compensation Committee and Corporate Governance and Nominating Committee, and is a member of its Audit Committee. |

MEETINGS OF THE BOARD OF DIRECTORS AND COMMITTEES OF THE BOARD OF DIRECTORS

During the year ended October 31, 2010,2012, the Board of Directors held four regularly scheduled meetings and fourone telephonic meetings.meeting. In addition, Directors considered Company matters and had communications with the Chairman of the Board of Directors and others outside of formal meetings. During the fiscal year ended October 31, 2010,2012, each Director attended 100% of the meetings of the Board of Directors and at least 75%95% of the meetings of its Committees on which such Director served. Directors are expected to attend the Annual Meeting of Shareholders, but the Company does not have a formal policy with respect to attendance. All of the members of the Board of Directors attended the Annual Meeting of Shareholders held on March 16, 2010.27, 2012.

Audit Committee

TheFor fiscal 2012, the members of the Audit Committee of the Board of Directors arewere Messrs. Kangas, Robbins and Weinroth. Weinroth. The Board of Directors has determined that all of the members of the Audit Committee meet the standards for independence in our Certificate of Incorporation, which is available on our website at www.khov.com under “SEC Filings/Quarterly Filings/09-08-08 Filing Date,” and the independence requirements mandated by the NYSE listing standards.

The Audit Committee is currently chaired by Mr. Kangas and is responsible for reviewing and approving the scope of the annual audit undertaken by the Company’s independent registered public accounting firm and meeting with them to review the results of their work as well as their recommendations. The Audit Committee selects the Company’s independent registered public accounting firm and also approves and reviews their fees. The duties and responsibilities of the Audit Committee are set forth in its charter, which may be found at www.khov.com under “Investor Relations/Corporate Governance.” During the fiscal year ended October 31, 2010,2012, the Audit Committee met on fourthree occasions and held eight telephonic meetings. The Audit Committee also authorizes staffing and compensation of the Internal Audit Department. The Vice President of Internal Audit for the Company reports directly to the Audit Committee on, among other things, the Company’s compliance w ithwith certain Company procedures which are designed to enhance management’s understanding of operating issues and the results of the Audit Department’s annual audits of the various aspects of the Company’s business. In fiscal 2010,2012, the Audit Department issued 13eight traditional audit reports and performed 2316 reviews pursuant to Section 404 of the Sarbanes-Oxley Act of 2002. For additional information related to the Audit Committee, see “The Audit Committee” below.

Compensation Committee

The members of the Compensation Committee of the Board of Directors areduring fiscal 2012 were Messrs. Weinroth, Kangas and Coutts. The Board of Directors has determined that all of the members of the Compensation Committee meet the standards for independence in our Certificate of Incorporation and the independence requirements mandated by the NYSE listing standards. The duties and responsibilities of the Compensation Committee are set forth in its charter, which may be found on our website at www.khov.com under “Investor Relations/Corporate Governance.”

The Compensation Committee is currently chaired by Mr. Weinroth and is responsible for reviewing salaries, bonuses and other forms of executive compensation for the Company’s senior executives, key management employees and non-employee Directors, and is active in other compensation and personnel areas as the Board of Directors from time to time may request. In addition, all members of the Compensation Committee qualify as “non-employee directors” for purposes of Rule 16b-3 of the Exchange Act, and as “outside directors” for purposes of Section 162(m) (“Section 162(m)”) of the Internal Revenue Code of 1986, as amended. For a discussion of the criteria used and factors considered by the Compensation Committee in reviewing and determining executive compensation, see “The Compensation Committee” and “Compensation Discussion and Analysis” below. During the fiscal year ended October 31, 2010,2012, the Compensation Committee met on fivefour occasions and held no telephonic meetings.

Corporate Governance and Nominating Committee

The Company has established a Corporate Governance and Nominating Committee, although the Company is not required to have such committee because it is a controlled company under the rules of the NYSE. The members of the Corporate Governance and Nominating Committee of the Board of Directors areduring fiscal 2012 were Messrs. Weinroth, Kangas and Marengi. The Board of Directors has determined that all of the members of the Corporate Governance and Nominating Committee meet the standards for independence in our Certificate of Incorporation and the independence requirements mandated by the NYSE listing standards.

The Corporate Governance and Nominating Committee is currently chaired by Mr. Weinroth. The Corporate Governance and Nominating Committee is responsible for corporate governance matters, and reviewing and recommending nominees for the Board of Directors, succession planning and other Board-related policies. The Corporate Governance and Nominating Committee also oversees the annual performance evaluation of the Board of Directors and its Committees, the Board’s periodic review of the Company’s Corporate Governance Guidelines (“Guidelines”) and compliance with the Company’s Related Person Transaction Policy. During the fiscal year ended October 31, 2010,2012, the Corporate Governance and Nominating Committee met on twothree occasions and held twono telephonic meetings.

The Guidelines require that annually each Director prepares annually an assessment of each Board committee on which hesuch Director serves as well as of the full Board of Directors as to the effectiveness of each committee and the full Board of Directors and any recommendations for improvement.

The duties and responsibilities of the Corporate Governance and Nominating Committee are set forth in its charter, which may be found at www.khov.com under “Investor Relations/Corporate Governance,” and the Guidelines may be found at the same website address under “Investor Relations/Corporate Governance.”

In conducting its nomination function, among other factors, the Board of DirectorsCorporate Governance and Nominating Committee generally considers the size of the Board of Directors best suited to fulfill its responsibilities, the Board of Directors’ overall membership composition to ensure the Board of Directors has the requisite expertise and consists of persons with sufficiently diverse backgrounds, the independence of outside directors and other possible conflicts of interest of existing and potential members of the Board of Directors.Directors as more fully described under “Election of Directors – Board of Directors – Composition” above.

The Company does not have a specific policy regarding shareholder nominations of potential directors to the Board of Directors, other than through the process described under “Shareholder Proposals for the 20122014 Annual Meeting” below. The Corporate Governance and Nominating Committee will consider director candidates recommended by shareholders. Possible nominees to the Board of Directors may be suggested by any Director and given to the Corporate Governance and Nominating Committee. The Corporate Governance and Nominating Committee may seek potential nominees and engage search consultants to assist it in identifying potential nominees. The Corporate Governance and Nominating Committee adopted an amendment to its charter in November 2009 affirming its belief that d iversitydiversity is an important factor to consider in evaluating potential nominees. The Corporate Governance and Nominating Committee recommends to the Board of Directors a slate of nominees for the Board of Directors for inclusion in the matters to be voted upon at the Annual Meeting. The Company’s Restated By-laws provide that Directors need not be shareholders. Vacancies on the Board of Directors, other than those resulting from removal by shareholders, may be filled by action of the Board of Directors.

As of the 120th calendar day prior to February 1, 2011,March 27, 2013, the Board of Directors had not received any recommendation for the nomination of a candidate to the Board of Directors by any shareholder or group of shareholders that at such time held more than 5% of the Company’s voting stock for at least one year.

VOTE REQUIRED

The election of the nominees to the Company’s Board of Directors for the ensuing year, to serve until the next Annual Meeting of Shareholders of the Company, and until their respective successors may be elected and qualified, requires that each director be elected by a majority of the votes cast by the shareholders of Class A Common Stock and Class B Common Stock, voting together, represented in person or by proxy at the 20112013 Annual Meeting. In determining whether each director has received the requisite number of affirmative votes, abstentions and broker non-votes will have no impact on such matter because such shares are not votes cast.

Mr. Hovnanian and others with voting power over the shares held by the Estate of Kevork S. Hovnanian, the Limited Partnership and certain family trusts have informed the Company that they intend to vote in favor of the nominees named in this proposal. Because of their collective voting power, this proposal is assured passage.

Our Board of Directors recommends that shareholders vote FOR the election of the nominees named in this proposal to the Company’s Board of Directors.

(2) RATIFICATION OF THE SELECTION OF AN INDEPENDENT

REGISTERED PUBLIC ACCOUNTING FIRM

On January 5, 2009, the Audit Committee of the Board of Directors of the Company terminated its relationship with Ernst & Young LLP as the independent registered public accounting firm for the Company. Ernst & Young LLP’s reports on the financial statements of the Company for the fiscal years ended October 31, 2007 and 2008 did not contain any adverse opinion or a disclaimer of opinion, nor were such reports qualified or modified as to uncertainty, audit scope or accounting principle. During the fiscal years ended October 31, 2007 and 2008, and through January 5, 2009, (1) there were no disagreements with Ernst & Young LLP on any matter of accounting principles or practices, financial statement disclosure, or auditing scope or procedure, which, if not resolved to the sati sfaction of Ernst & Young LLP, would have caused Ernst & Young LLP to make reference thereto in its reports on the financial statements of the Company for such years, and (2) there have been no “reportable events” as defined in Item 304(a)(1)(v) of Regulation S-K.

Also on January 5, 2009, the Audit Committee of the Company’s Board of Directors appointed Deloitte & Touche LLP as the independent registered public accounting firm for the Company as of and for the fiscal year ending October 31, 2009. This appointment followed a solicitation and review process conducted by the Company’s Audit Committee.

During the fiscal years ended October 31, 2007 and 2008, and through January 4, 2009, (1) Deloitte & Touche LLP had not been engaged as the principal accountant of the Company to audit its financial statements or as an independent accountant to audit a significant subsidiary of the Company, and (2) the Company had not consulted with Deloitte & Touche LLP regarding (a) the application of accounting principles to any completed or proposed transaction, (b) the type of audit opinion that might be rendered on the Company’s financial statements for such periods, or (c) any other accounting, auditing or financial reporting matter described in Items 304(a)(2)(i) and (ii) of Regulation S-K.

The selection of an independent registered public accounting firm to examine financial statements of the Company to be made available or transmitted to shareholders and to be filed with the SEC for the fiscal year ending October 31, 20112013 is submitted to this Annual Meeting of Shareholders for ratification. Deloitte & Touche LLP has been selected by the Audit Committee of the Company to examine such financial statements. In the event that the shareholders fail to ratify the appointment, the Audit Committee will consider the view of the shareholders in determining its selection of the Company’s independent registered public accounting firm for the subsequent fiscal year. Even if the selection is ratified, the Audit Committee may, in its discretion, direct the appointment of a new independ entindependent registered public accounting firm at any time during the fiscal year if the Audit Committee determines that such a change would be in the best interests of the Company and our stockholders.its shareholders.

The Company has been advised that representatives of Deloitte & Touche LLP will attend the Annual Meeting of Shareholders to respond to appropriate questions and will be afforded the opportunity to make a statement if the representativerepresentatives so desires.desire.

VOTE REQUIRED

Ratification of the selection of Deloitte & Touche LLP as the Company’s independent registered public accounting firm to examine financial statements of the Company for the year ending October 31, 2011,2013 requires the majority of the votes cast by the shareholders of Class A Common Stock and Class B Common Stock, voting together, present in person or by proxy at the 20112013 Annual Meeting. In determining whether the proposal has received the requisite number of affirmative votes, abstentions will have no impact on such matter because such shares are not considered votes cast.

Mr. Hovnanian and others with voting power over the shares held by the Estate of Kevork S. Hovnanian, the Limited Partnership and certain family trusts have informed the Company that they intend to vote in favor of this proposal. Because of their collective voting power, this proposal is assured passage.

Our Board of Directors recommends that shareholders vote FOR ratification of the selection of Deloitte & Touche LLP as the Company’s independent registered public accounting firm.

(3) APPROVAL OF AN AMENDMENT TO THE COMPANY’S CERTIFICATE OF INCORPORATION TO INCREASE THE NUMBER OF AUTHORIZED SHARES OF CLASS A COMMON STOCK

On December 14, 2012, subject to shareholder approval, the Board authorized an amendment to our Certificate of Incorporation to increase the number of authorized shares of Class A Common Stock (the “Class A Common Stock”) from 200,000,000 shares to 400,000,000 shares (the “Class A Amendment”). Pursuant to Proposal 4, we are separately proposing an increase to our authorized Class B Common Stock, but we are not proposing an increase to the number of authorized shares of Preferred Stock.

If approved by shareholders, the Class A Amendment would be reflected in an Amended and Restated Certificate of Incorporation of Hovnanian Enterprises, Inc., and the first paragraph of paragraph Fourth of our Certificate of Incorporation would be amended to provide as follows:

“FOURTH: The total number of shares of all classes of stock which the Corporation shall have the authority to issue is 430,100,0001 shares, of which 400,000,000 shares shall be Class A Common Stock having a par value of one cent ($0.01) per share, 30,000,0002 shares shall be Class B Common Stock having a par value of one cent ($0.01) per share and 100,000 shares shall be Preferred Stock having a par value of one cent ($0.01) per share.” If the shareholders approve the proposed amendment, it will become effective upon filing of an Amended and Restated Certificate of Incorporation with the Delaware Secretary of State, which the Company anticipates doing as soon as practicable following shareholder approval.

The newly authorized shares of Class A Common Stock will have all the rights and privileges of the shares of Class A Common Stock presently authorized. Therefore, approval of this proposal and any subsequent issuance of additional shares of Class A Common Stock would not affect your current rights as a shareholder, except for any dilutive effects of a potential increase in the number of outstanding shares of Class A Common Stock to, among other things, earnings per share, book value per share and the voting power of current holders of our Class A Common Stock.

Reasons for the Proposal

Our Board believes that the number of shares of Class A Common Stock that is available for issuance is not sufficient. We are currently authorized to issue 200,000,000 shares of Class A Common Stock. As of November 1, 2012, 118,362,931 shares of Class A Common Stock were issued and outstanding and 73,181,095 shares of Class A Common Stock were reserved (1) for conversions of our Class B Common Stock into shares of Class A Common Stock, (2) for the issuance upon exercise of outstanding stock options and stock awards, (3) for stock options and stock awards that may be granted in the future under our stock option or other incentive programs and (4) for stock that may be issued upon settlement or exchange of our outstanding equity-linked securities. As a result, there are currently only 8,455,974 shares of Class A Common Stock available, including shares held in Treasury, for other purposes.

The Board believes that it is advisable and in the Company’s and its shareholders’ best interests to have a greater number of authorized shares of Class A Common Stock in order to maintain the Company’s flexibility to use its capital stock for business and financing purposes in the future. The additional shares will be available for issuance from time to time at the discretion of the Board, normally without further shareholder action (except as may be required for a particular transaction by applicable law, requirements of regulatory agencies or by NYSE rules), for any proper corporate purpose including, among other things, capital-raising and deleveraging transactions, investment opportunities, to issue under stock option or other incentive programs, to attract and retain talented personnel and for other value-creating opportunities and strategic transactions. The Board believes that the proposed increase in the Company’s authorized Class A Common Stock will provide a sufficient number of shares available to maintain the flexibility necessary to pursue the foregoing and other opportunities in the foreseeable future.

The Board believes that prudent corporate governance includes the Company having a sufficient number of authorized but unissued shares of Class A Common Stock available for various purposes, and the Board regularly evaluates the Company’s needs and opportunities to utilize shares of the Company’s Class A Common Stock. In recent years, the Company has been focused on evaluating its debt profile, capital structure and various financing and refinancing alternatives and has successfully completed several deleveraging transactions, including with issuances of Class A Common Stock and securities which may be settled or exchanged for Class A Common Stock. These issuances represent the primary use of the Class A Common Stock over the past few years.

The Company has no current plans, and there are currently no agreements or arrangements to issue any of the additional shares of Class A Common Stock that would be authorized by the proposed Class A Amendment. However, if shareholders approve the proposed Class A Amendment, the additional authorized shares would give the Board more flexibility in responding to a variety of corporate opportunities, including those discussed above, which, if they become available, are likely to require prompt action on our part. The Board believes that the increase in the authorized number of shares of Class A Common Stock will enable the Company to take timely advantage of market conditions and the availability of favorable opportunities without the delay and expense associated with convening a special meeting to obtain shareholder approval at that time (unless otherwise required by regulatory agencies or by NYSE rules).

1 The Company will have the authority to issue a total of 460,100,000 shares of all classes of stock if Proposal 4 is also approved.

2 The Company will have the authority to issue a total of 60,000,000 shares of Class B Common Stock if Proposal 4 is approved.

Possible Effects of the Increase in Class A Common Stock

The Company has not proposed the increase in the number of authorized shares of Class A Common Stock with the intent of using the additional shares to prevent or discourage any actual or threatened takeover of the Company. The Company currently has in effect a shareholder approved rights plan that is not designed to protect shareholders against the possibility of a hostile takeover. Instead, it is meant to preserve shareholder value and the value of certain tax assets primarily associated with net loss carryforwards and built-in losses under Section 382 of the Internal Revenue Code of 1986, as amended. The proposed Class A Amendment does not change any of the existing terms of the rights plan.

The increase in the authorized number of shares of Class A Common Stock and the subsequent issuance of such shares could, however, have the effect of delaying or preventing a change of control of the Company without further action by shareholders. Shares of authorized and unissued Class A Common Stock could (within the limits imposed by applicable law) be issued in one or more transactions that could make a change of control of the Company less likely. The additional authorized shares could be used to discourage persons from attempting to gain control of the Company by diluting the voting power of shares then outstanding or by increasing the voting power of persons who would support the Board in a potential takeover scenario. However, this proposal is not made in response to any effort of which we are aware to accumulate our stock or to obtain control of us, nor do we have a present intent to use the additional shares of authorized Class A Common Stock to oppose a hostile takeover attempt or to delay or prevent changes in control of management. In addition, members of the Hovnanian family, including Ara Hovnanian, the Chairman of our Board, President and Chief Executive Officer, have the power to cast a majority of the votes that can be cast by the holders of all our currently outstanding common stock, voting together, through personal holdings, the Limited Partnership, family trusts and shares held by the Estate of Kevork S. Hovnanian.

You will not realize any dilution in your percentage ownership or your voting rights as a result of increasing our authorized Class A Common Stock. In the absence of future issuances of our Class A Common Stock to you, issuances of additional shares of our Class A Common Stock in the future would dilute your percentage ownership and the voting power of the outstanding shares of our Class A Common Stock. In addition, the issuance of additional shares of our Class A Common Stock (or even the potential issuance) may have a depressive effect on the market price of our Class A Common Stock. Shareholders do not have preemptive rights, which means that they do not have the right to purchase shares in any future issuance of Class A Common Stock in order to maintain their proportionate equity interests in the Company.

VOTE REQUIRED

Approval of the proposed amendment to the Certificate of Incorporation to increase the number of authorized shares of Class A Common Stock requires the affirmative vote of the holders, represented in person or by proxy at the 2013 Annual Meeting, of (1) a majority of the votes cast by the shareholders of Class A Common Stock and Class B Common Stock, voting together, and (2) a majority of the votes cast by the shareholders of Class A Common Stock. In determining whether this proposal has received the requisite number of affirmative votes, abstentions will have no effect on the outcome because they are not considered votes cast. Approval of the Class A Amendment is not conditioned on the approval of the Class B Amendment described in Proposal 4.

If our shareholders approve the proposed Class A Amendment, it will become effective upon filing of an Amended and Restated Certificate of Incorporation with the Delaware Secretary of State, which we anticipate doing as soon as practicable following shareholder approval. However, if our shareholders approve the proposed Class A Amendment, our Board retains discretion under Delaware law not to implement the proposed amendment. If our Board were to exercise such discretion, the number of authorized shares of Class A Common Stock would remain at current levels.

Mr. Hovnanian and others with voting power over the shares held by the Estate of Kevork S. Hovnanian, the Limited Partnership and certain family trusts have informed the Company that they intend to vote in favor of this proposal.

Our Board of Directors recommends that shareholders vote FOR the approval of the proposed amendment to our Certificate of Incorporation to increase the number of authorized shares of Class A Common Stock.

(4) APPROVAL OF AN AMENDMENT TO THE COMPANY’S CERTIFICATE OF INCORPORATION TO INCREASE THE NUMBER OF AUTHORIZED SHARES OF CLASS B COMMON STOCK

On December 14, 2012, subject to shareholder approval, the Board authorized an amendment to our Certificate of Incorporation to increase the number of authorized shares of Class B Common Stock (the “Class B Common Stock”) from 30,000,000 shares to 60,000,000 shares (the “Class B Amendment”). Pursuant to Proposal 3, we are separately proposing an increase to our authorized Class A Common Stock, but we are not proposing an increase to the number of authorized shares of Preferred Stock.

If approved by shareholders, the Class B Amendment would be reflected in an Amended and Restated Certificate of Incorporation of Hovnanian Enterprises, Inc., and the first paragraph of paragraph Fourth of our Certificate of Incorporation would be amended to provide as follows:

“FOURTH: The total number of shares of all classes of stock which the Corporation shall have the authority to issue is 260,100,0003 shares, of which 200,000,0004 shares shall be Class A Common Stock having a par value of one cent ($0.01) per share, 60,000,000 shares shall be Class B Common Stock having a par value of one cent ($0.01) per share and 100,000 shares shall be Preferred Stock having a par value of one cent ($0.01) per share.” If the shareholders approve the proposed amendment, it will become effective upon filing of an Amended and Restated Certificate of Incorporation with the Delaware Secretary of State, which the Company anticipates doing as soon as practicable following shareholder approval.

The newly authorized shares of Class B Common Stock will have all the rights and privileges of the shares of Class B Common Stock presently authorized. Therefore, approval of this proposal and any subsequent issuance of additional Class B Common Stock would not affect your current rights as a shareholder, except for any dilutive effects of a potential increase in the number of outstanding shares of Class B Common Stock to, among other things, earnings per share, book value per share and the voting power of holders of our Class B Common Stock.

Reasons for the Proposal

The Company is a family enterprise that has been in operation since 1959, and the Company has maintained a shareholder approved dual-class capital structure since 1992. The Board established this structure as part of its philosophy to foster continuity and stability in the Company’s operations.

The Board continues to believe that it important to the Company’s continued and future development to provide for continuity of direction and management and to maintain stability in the Company’s relationships with its lenders, suppliers, contractors and others who are important to the conduct of the Company’s business. The Board also believes that the Hovnanian family’s direction and management of the Company and the stability in the Company’s relationships with others fostered by their control have been crucial to the growth and success of the Company over its history and will continue to be so in the future.

In light of the benefits to the Company of the continuity of share ownership and control of the Hovnanian family, the Board believes that it is advisable and in the best interests of the Company and its shareholders to maintain the relative proportion of the Class B Common Stock to the Class A Common Stock. If Proposal 3 is approved, we would be authorized to issue 400,000,000 shares of Class A Common Stock. Therefore, approval of the Class B Amendment would maintain the proportion of authorized Class A Common Stock and Class B Common Stock as it currently stands and enable the Company to pursue the initiatives described in Proposal 3.

3 The Company will have the authority to issue a total of 460,100,000 shares of all classes of stock if Proposal 3 is also approved.

4 The Company will have the authority to issue a total of 400,000,000 shares of Class A Common Stock if Proposal 3 is approved.

The Company has historically issued Class B Common Stock to the Hovnanian family in connection with equity awards and with the anticipation that the Class B Common Stock would be held for investment. Under the terms of the Company’s Certificate of Incorporation, transfers of Class B Common Stock are restricted to certain permitted transferees (otherwise each share of Class B Common Stock would be converted into Class A Common Stock on a share-for-share basis) and, if the Class B Common Stock is held in nominee name, the beneficial owner of the Class B Common Stock is required to make representations that such holder has held continuously since the date of issuance in order to receive the benefit of the Class B Common Stock voting. Absent such representations, each share of Class B Common Stock would carry the same number of votes as a share of Class A Common Stock.

Possible Effects of the Increase in Class B Common Stock

The Company has not proposed the increase in the number of authorized shares of Class B Common Stock with the intent of using the additional shares to prevent or discourage any actual or threatened takeover of the Company. The Company currently has in effect a shareholder approved rights plan that is not designed to protect shareholders against the possibility of a hostile takeover. Instead, it is meant to preserve shareholder value and the value of certain tax assets primarily associated with net loss carryforwards and built-in losses under Section 382 of the Internal Revenue Code of 1986, as amended. The proposed Class B Amendment does not change any of the existing terms of the rights plan.

The increase in the authorized number of shares of Class B Common Stock and the subsequent issuance of such shares could, however, have the effect of delaying or preventing a change of control of the Company without further action by shareholders. Shares of authorized and unissued Class B Common Stock could (within the limits imposed by applicable law) be issued in one or more transactions that could make a change of control of the Company less likely. The additional authorized shares could be used to discourage persons from attempting to gain control of the Company by diluting the voting power of shares then outstanding or by increasing the voting power of persons who would support the Board in a potential takeover scenario. However, this proposal is not made in response to any effort of which we are aware to accumulate our stock or to obtain control of us, nor do we have a present intent to use the additional shares of authorized Class B Common Stock to oppose a hostile takeover attempt or to delay or prevent changes in control of management. In addition, members of the Hovnanian family, including Ara Hovnanian, the Chairman of our Board, President and Chief Executive Officer, have the power to cast a majority of the votes that can be cast by the holders of all our currently outstanding common stock, voting together, through personal holdings, the Limited Partnership, family trusts and shares held by the Estate of Kevork S. Hovnanian.

You will not realize any dilution in your percentage ownership or your voting rights as a result of increasing our authorized Class B Common Stock. Issuances of additional shares of our Class B Common Stock in the future would dilute your percentage ownership and the voting power of the outstanding shares of our Class A Common Stock. In addition shareholders do not have preemptive rights.

VOTE REQUIRED

Approval of the proposed amendment to the Certificate of Incorporation to increase the number of authorized shares of Class B Common Stock requires the affirmative vote of the holders, represented in person or by proxy at the 2013 Annual Meeting, of (1) a majority of the votes cast by the shareholders of Class A Common Stock and Class B Common Stock, voting together, and (2) a majority of the votes cast by the shareholders of Class B Common Stock. In determining whether this proposal has received the requisite number of affirmative votes, abstentions will have no effect on the outcome because they are not considered votes cast. Approval of the Class B Amendment is not conditioned on the approval of the Class A Amendment described in Proposal 3.

If our shareholders approve the proposed Class B Amendment, it will become effective upon filing of an Amended and Restated Certificate of Incorporation with the Delaware Secretary of State, which we anticipate doing as soon as practicable following shareholder approval. However, if our shareholders approve the proposed Class B Amendment, our Board retains discretion under Delaware law not to implement the proposed amendment. If our Board were to exercise such discretion, the number of authorized shares of Class B Common Stock would remain at current levels.

Mr. Hovnanian and others with voting power over the shares held by the Estate of Kevork S. Hovnanian, the Limited Partnership and certain family trusts have informed the Company that they intend to vote in favor of this proposal. Because of their collective voting power, this proposal is assured passage.

Our Board of Directors recommends that shareholders vote FOR the approval of the proposed amendment to our Certificate of Incorporation to increase the number of authorized shares of Class B Common Stock.

(5) ADVISORY VOTE ON EXECUTIVE COMPENSATION

In accordance with the requirements of Section 14A of the Exchange Act (which was added by the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”)) and the related rules of the SEC, we are including in these proxy materials a separate resolution subject to shareholder vote to approve, in a non-binding vote, the compensation of our named executive officers as disclosed on pages 1318 to 38.50.

In light of the voting results with respect to the frequency of shareholder votes on executive compensation at the 2011 Annual Meeting of Shareholders in which a substantial majority of our shareholders (96.3% of the votes cast by shareholders of Class A Common Stock and Class B Common Stock, voting together) voted for “say-on-pay” proposals to occur every three years, the Board of Directors initially decided that the Company would hold, in accordance with the vote of an overwhelming majority, a triennial advisory vote on the compensation of named executive officers, which vote would next take place at the Company’s 2014 Annual Meeting of Shareholders. However, we have voluntarily elected to hold our next “say-on-pay” vote at this 2013 Annual Meeting of Shareholders.

In considering their vote, shareholders may wish to review with care the information on the Company’s compensation policies and decisions regarding the named executive officers presented in Compensation Discussion and Analysis on pages 1318 to 27,36, as well as the discussion regarding the Compensation Committee on pages 1116 and 12.17.

TheAs we discuss in the Compensation Discussion and Analysis begins at page 13. As we discuss in Compensation Discussion and Analysis,section, the Board of Directors believes that the Company’s long-term success depends in large measure on the talents of the Company’s employees. The Company’s compensation system plays a significant role in the Company’s ability to attract, retain and motivate the highest quality associates in a difficult market. The principal underpinnings of the Company’s compensation system are an acute focus on performance, shareholder alignment, sensitivity to the relevant market place, and a long-term orientation.

The Compensation Committee ties increases or decreases in overall compensation with the overall financial performance of the Company. During fiscal years when the Company’s profitability has been higher, total compensation has been higher. During more recent years when the Company’s performance has been lower due in part to the economic downturn and recession particularly in the housing industry, the Compensation Committee’s policies and actions have significantly lowered overall compensation in recent years relative to profitable periods.compensation. These policies and actions include:

| | · | Significant reductions in annual bonus opportunity, where, on average, the maximum award for all named executive officers is approximately 92% lower than the maximum award during the last ten years and approximately 45%39% lower than the maximum award during the last threefour years; |

| | · | Focus on lowering net debt levelsimproving EBITDA through a bonus component for our Chairman of the Board, President and Chief Executive Officer, and our Executive Vice President and Chief Financial Officer and our Chief Operating Officer that is only earned if net debtEBITDA improvement performance goals are met; |

| | · | Focus on a return to profitability and lowering net debt over a three-year performance period through a long-term incentive award for all named executive officers in fiscal 2010; |

| | · | Continued policyPolicy of generally targeting a fixed guideline number of stock options rather than a specific option value as part of the annual compensation program (since the guideline number of stock options generally was not increased as stock prices in the homebuilding industry declined, the value of stock option grants to our named executive officers has declined significantly); and |

| | · | Reduction in shareholder dilution through the Compensation Committee actions to cancel stock optionsCommittee’s active management of both equity award levels and not return the cancelled shares to the poolnumber of shares available for new awards under the Amended and Restated 2008 Hovnanian Enterprises, Inc. Stock Incentive Plan.equity awards. |

The text of the resolution in respect of this proposal is as follows:

“Resolved, that the compensation paid to the Company’s named executive officers as disclosed pursuant to Item 402 of Regulation S-K in the Proxy Statement relating to the Company’s Annual Meeting of Shareholders to be held on March 15, 2011,12, 2013, including the Compensation Discussion and Analysis, compensation tables, and narrative discussion, is hereby approved.”

The Board recommends that shareholders vote FOR approval of this resolution.

(4) ADVISORY VOTE ON THE FREQUENCY OF

SHAREHOLDER VOTE ON EXECUTIVE COMPENSATION

In accordance with the requirements of Section 14A of the Exchange Act (which was added by the Dodd-Frank Act) and the related rules of the SEC, we are including in these proxy materials a separate resolution subject to shareholder vote to recommend, in a non-binding vote, whether a non-binding shareholder vote to approve the compensation of our named executive officers (that is, votes similar to the advisory vote in the preceding proposal on pages 9 and 10) should occur every one, two or three years.

In considering their vote, shareholders may wish to review with care the information presented in connection with the preceding proposal, the information on the Company’s compensation policies and decisions regarding the named executive officers presented in Compensation Discussion and Analysis on pages 13 to 27, as well as the discussion regarding the Compensation Committee on pages 11 and 12.

We believe a three-year frequency is most consistent with our approach to executive compensation. Our reasons include:

| · | The homebuilding industry is cyclical in nature and, accordingly, the best way for shareholders to evaluate how executive compensation relates to our performance is over a multi-year time frame; |

| · | The Committee has focused executives on long-term results through regular awards of stock options, which generally vest over a multi-year period up to five years and expire only after ten years; |

| · | Our recently adopted Long Term Incentive Program is specifically designed to incentivize performance, and to position the Company for future growth, over a three-year performance period; and |

| · | We do not make significant changes to the structure of our compensation programs frequently, although we tailor the performance objectives for each executive officer each year to focus on the areas deemed critical to the Company’s current and future success and long-term shareholder value. |

The text of the resolution in respect of this proposal is as follows:

“Resolved, that the shareholders recommend, in a non-binding vote, whether a non-binding shareholder vote to approve the compensation of the Company’s named executive officers should occur every one, two or three years.”

The Board recommends that shareholders vote for THREE YEARS with respect to how frequently an advisory shareholder vote to approve the compensation of our named executive officers should occur.

THE COMPENSATION COMMITTEE

The Compensation Committee of the Board of Directors (the “Committee”) is the principal overseer of the Company’s various policies and procedures related to executive compensation. The Committee meets at least threefour times a year to discuss industry trends with regard to overall compensation issues and consults with outside compensation consultants as needed. The Committee is governed by its Charter which is available on the Company’s public website (www.khov.com)(www.khov.com).

Areas of Responsibility

The Committee, in conjunction with the Board of Directors and with management’s input, shapes the Company’s executive compensation philosophy and objectives. In particular, the Committee is charged with:

| | · | Reviewing, at least annually, the salaries, bonuses and other forms of compensation, including stock option grants, for the Company’s senior executives (which include the Chairman of the Board, President and Chief Executive Officer (the "CEO"“CEO”), the Executive Vice President and Chief Financial Officer (the “CFO”), the Chief Operating Officer (the “COO”) and the other named executive officers (“NEOs”) for whom compensation is reported in the tables below); |

| | · | Reviewing, at least annually, compensation paid to the Company’s non-employee Directors; |

| | · | Participating in the review of compensation of other designated key employees of the Company as may be directed by the Board of Directors or by management;Company; |

| | · | Periodically reviewing the Company’s policies and procedures pertaining to the Company’s equity award plans and forms of equity grants to all employees and non-employee Directors, employee benefit plans (for example, the 401(k) plan and deferred compensation plans), the Chief Executive Officer’s severance agreement,agreements, executive perquisites, and forms of equity grants to all employees and non-employee directors; |

| | · | Fostering good corporate governance practices as they relate to executive compensation; and |

| | · | Reviewing, at least annually, as part of the Board'sBoard of Directors’ oversight responsibilities, the Company's compensation program to assessand reports from the Company’s CFO regarding his assessment of whether there are any compensation risks that are reasonably likely to result in a material adverse effect on the Company (see "Oversight of Risk Management") below). In addition, the Committee regularly considers business and compensation risks as part of its process for establishing performance goals and determining incentive awards for each of the NEOs. |

These areas of responsibilities are discussed in more detail below under “Compensation Discussion and Analysis.” During the fiscal year ended October 31, 2010,2012, the members of the Committee were all independent, non-employee Directors.“non-employee directors” for purposes of Rule 16b-3 of the Exchange Act, and “outside directors” for purposes of Section 162(m) of the Internal Revenue Code of 1986, as amended.

Compensation Review Process for the Named Executive Officers

The Committee, in conjunction with the Board of Directors and with management’s input, is responsible for making decisions related to the overall compensation of the NEOs.

At least annually, the Committee establishes objective financial measures for determining bonus awards to the NEOs. The Committee also considers salary, employee benefits and discretionary bonus awards, if any, for the NEOs.

In determining overall compensation for the NEOs, the Committee may consult with other members of the Board of Directors, including the CEO and the CFO. TheseEach of these individuals often provideprovides the Committee with insight on the individual and overall performance of executives (other than with respect to himself), including the achievement of personal objectives, if any, rather than relying solely on the Company’s financial performance measures in determining their compensation. The CEO and CFO are not present for the Committee’s evaluation of their individual performance. The Committee also engages an outside compensation specialist related to various compensation issues.

Outside Compensation Consultant

Since October 2003, the Committee has engaged Pearl Meyer & Partners (“PM&P”) as the Committee’s independent outside compensation consultant to provide services related to executivereviews and non-employee Director compensation. PM&P does not provide any other services to the Company unless approved by the Committee and no such services were provided in fiscal 2010. In fiscal 2010, PM&P assisted the Committee with its review and design of the Company’s annual bonus and long-term incentive plans for the NEOs in order to reflect modifications and realignment of priorities in the Company’s objectives due to declining market conditions in the homebuilding industry. The analysis also included a review ofanalyzes the compensation of chiefthe named executive officers and chief financial officers amongof the Company’s peer group of 11 publicly-traded homebuilding companies (the “Peer Group”). See “Peer Group Considerations”, discussed further below. The Committee may engage outside compensation consultants in the Compensation Discussion and Analysis below for a list of the companies in the Company’s Peer Group.

The Committee’s primary objective in engaging PM&P isrelation to obtain advice and feedback related to maintaining programs that providevarious compensation opportunities for executives within the median range of the competitive homebuilder Peer Group for comparable financial performance.issues. The Committee may also instruct PM&Pa compensation consultant to provide assistance in fostering an overall compensation program that aligns with its compensation philosophy to guide, motivate, retain and reward its executives for the achievement of the Company’s financial performance, strategic initiatives and individual goals, including increased long-term shareholder value in the context of a challenging business environment. The Company also periodically participates in a homebuilding industry groupNotwithstanding any input from compensation consultants, the Committee has the sole discretion to make all final decisions related to NEO compensation.

Outside Compensation Consultant and No Conflicts of Interest

For fiscal 2012, the Committee engaged Pearl Meyer & Partners (“PM&P”) as the Committee’s outside compensation consultant to provide certain services related to executive compensation s urvey that is conducted byand non-employee Director compensation. PM&P does not provide any other services to the Company unless approved by the Committee, and which provides valuable informationno such services were provided in fiscal 2012. After considering the relevant factors, the Company has determined that no conflicts of interest have been raised in connection with the services PM&P performed for the Company in fiscal 2012. In fiscal 2012, PM&P assisted the Committee with its review of the Company’s annual bonus and long-term incentive plans for the NEOs as well as its review of the compensation program for the non-employee directors.

The Committee’s primary objective in engaging PM&P has been to obtain advice and feedback related to maintaining programs that provide compensation opportunities for executives within the median range of the competitive homebuilder Peer Group for comparable financial performance and PM&P also provided assistance to the Committee in assessing its competitive pay levels. An abbreviated edition of the homebuilding industry survey was conducted by PM&P during fiscal 2010 at no charge to any participants, including the Company.fostering an overall compensation program as discussed above.

The Committee weighs the information gatheredadvice and feedback from PM&Pits compensation consultant and the members of the Board of Directors, as well as the views of and information gathered by the members of management it has consulted in conjunction with its review of other information itthe Committee considers relevant when making decisions or making recommendations to the full Board of Directors regarding executive compensation.

Board Communication

The Company’s Board of Directors is updated at least quarterly of any compensation decisions or recommendations made by the Committee and the Committee requests feedback from the Board of Directors regarding specific compensation issues as it deems necessary.

Compensation Committee Report

The Committee has reviewed and discussed the Compensation Discussion and Analysis provided below with the Company’s management. Based on itsthis review and discussion, the Compensation Committee recommended to the Board of Directors that the Compensation Discussion and Analysis be included in this proxy statement.statement and in the Company’s Annual Report on Form 10-K for the fiscal year ended October 31, 2012.

COMPENSATION COMMITTEE

Stephen D. Weinroth, Chair

Robert B. Coutts

Edward A. Kangas

Compensation Committee Interlocks and Insider Participation

During the fiscal year ended October 31, 2010,2012, the members of the Compensation Committee were Messrs. Weinroth, Kangas, and Coutts. Each of Messrs. Weinroth, Kangas, and Coutts are non-employee Directors, and were never officers or employees of the Company or any of its subsidiaries.subsidiaries and did not have any relationships requiring disclosure under Item 404 of Regulation S-K during fiscal 2012. None of our executive officers served on the board of directors or compensation committee of any other entity that has or had one or more executive officers who served on our Board of Directors or our Compensation Committee during fiscal 2012.

COMPENSATION DISCUSSION AND ANALYSIS

1. EXECUTIVE SUMMARY

Company Performance in Fiscal 2012

Beginning in the second quarter of fiscal 2012, the Company began to see positive operating trends, which continued into the third and fourth quarters of fiscal 2012. Below are some highlights for fiscal 2012:

| · | Total revenues for fiscal 2012 were $1.5 billion, up 30.9% from $1.1 billion during all of fiscal 2011; |

| · | During fiscal 2012, the dollar value of net contracts, including unconsolidated joint ventures, increased 43.9% to $1.9 billion compared with $1.3 billion for fiscal 2011, and the number of net contracts increased 30.1% to 5,838 homes compared with 4,488 homes in the previous year; |

| · | During fiscal 2012, deliveries, including those in our unconsolidated joint ventures, were 5,356 homes compared with 4,216 homes during fiscal 2011, representing an increase of 27.0%; |

| · | Contract backlog as of October 31, 2012, including that in our unconsolidated joint ventures, was $742.2 million for 2,145 homes, which was an increase of 34.4% and 29.0%, respectively, compared to October 31, 2011; |

| · | During all of fiscal 2012, homebuilding gross margin percentage, before interest expense included in cost of sales, was 17.8% compared with 15.6% in 2011; |

| · | During all of fiscal 2012, total selling, general and administrative expenses were $190.3 million, or 12.8% of total revenues, compared with $211.4 million, or 18.6% of total revenues, for fiscal 2011; |

| · | The Company refinanced $797 million of secured senior notes during the fourth quarter of fiscal 2012, which reduces annual cash interest payments by approximately $17 million and extends the maturity of the refinanced debt from 2016 until 2020; and |

| · | The fiscal year-end closing price of a share of Class A Common Stock increased 199% compared to 2011. |

Best Practices

| | · | ·Pay-for-Performance:

| Pay-for-Performance: The Compensation Committee (“Committee”) ties increases or decreases in overall compensation with the overall financial performance of the Company. During fiscal years when the Company’s profitability has been higher, total compensation has been higher. During more recent years when the Company’s performance has been lower due in part to the economic downturn and recession, which is particularly significant in the housing industry, the overall compensation has been lower than during profitable periods.lower. The Committee seeks to motivate management to achieve enhancedimproved financial performance of the Company through bonus plans that reward higher performance with increased bonus opportunities. In its selection of metrics to measure bonus achievement, the Committee has selected metrics to correspond to the financial needs of the Company during the relevant period. During periods of profitability, the bonus metrics were focused on profitability and return on shareholder’sshareholders’ equity measures. During recent periods when there was little or no likelihood of profits, bonus metrics were focused on opportunities that would reduce the Company’s debt obligations that wouldand improve cash flow and liquidity to enable the Company to weather the difficult economic conditions and return to profitability. |

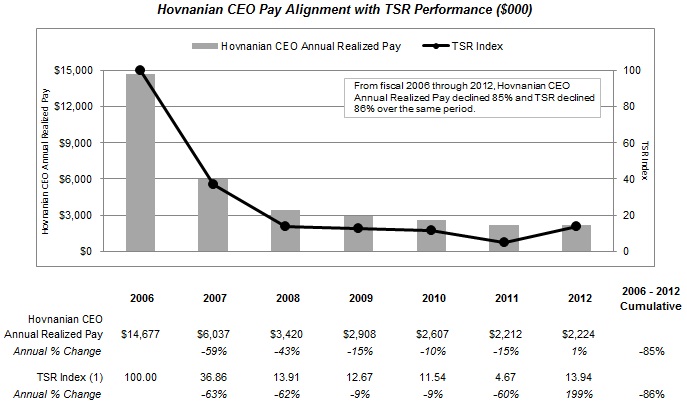

| | | The following graph demonstrates the link between the CEO’s annual realized pay and the Company’s Total Shareholder Return (“TSR”). Annual realized pay includes salary, annual bonus, perquisites and other compensation plus the realized value of options exercised and shares vesting during the fiscal year. |

| (1) | The TSR Index measures the change in the Company's stock price relative to fiscal 2006. The index for each fiscal year is determined by comparing the fiscal year-ending stock price to the ending stock price in fiscal 2006 which is set at 100. |

| · | ·

| Emphasis on Long-Term Value Creation and Retention: The Committee attemptsseeks to align the interests of management with the long-term interests of the shareholders through theby granting of a significant portion of the total compensation in the form of stock options that increase in value as the Company’s financial performance improves. The Committee also seeks to retain management through the utilization of compensation methods that require executives to be employed through various vesting periods in order to receive the full financial benefits of stock option grants that vest over multiple years, deferred shares as part of an annual bonus, and the recently adopted Long TermLong-Term Incentive Plan.Program implemented in fiscal 2010. |

| | · | ·

| Reduction in Dilution: In recent years, the Committee also focused on reducing the dilution of shareholder value by not returning 2,528,251 cancelled stock options to the pool of shares available for stock options in the Amended and Restated 2008 Hovnanian Enterprises, Inc. Stock Incentive Plan (the "Stock Incentive Plan"). |

| | Maintaining Appropriate Peer Group: In constructing the Peer Group, the Committee selected those companies that compete directly with the Company in the homebuilding industry, are of comparable size and complexity in operations to the Company and are generally in the markets where we compete.in which the Company competes. The Committee reviews the composition of the Peer Group on an annual basis and makes adjustments, if needed. For example, in fiscal 2010, the Committee determined that Meritage Homes Corporation should be added to the Peer Group. The Committee reviews the executive compensation of the Peer Group companies and seeks to award total compensation opportunity for our NEOs near the median of the Peer Group.Group, with variation in actual compensation earned both above and below the median, depending on performance. |

| | · | ·

| No Employment Agreements, Excise Tax Gross-Ups, SERPs or Defined Benefit Plans: The Company does not maintain employment or other agreements that provide contractual rights to employees upon termination of employment (other than upon death or disability), except for the change in control severance agreements the Company entered into with Messrs. O’Connor and itValiaveedan in January 2012 discussed below and in footnote (5) to the “Potential Payments Upon Termination Or Change-In-Control Table,” and the Company does not provide excise tax gross-ups, supplemental executive retirement plans or defined benefit pension plans for any NEOs. |

| | · | ·

| Maintenance and Enforcement of Stock Ownership Guidelines: The Board of Directors has established stock ownership guideline’s requiringguidelines pursuant to which the CEO, CFO and CFOCOO are requested to achieve and maintain recommended minimum levels of stock ownership as set forth on pages 26 and 27.below under “Stock Ownership Guidelines.” |

| | · | ·Perquisites:

| Perquisites: The Compensation Committee has provided NEOs only a few perquisites in addition to typical medical, dental and life insurance benefits. The Company limits the personal use of Company automobiles and its fractional aircraft share, reimbursement for country club dues and personal income tax preparation and accounting services to the CEO. In addition,Our perquisites aredo not grossed up for personal income taxes.include any tax gross-ups. |

Overall Compensation Decisions for Fiscal 2012

The Committee’s compensation decisions for fiscal 2012 reflected a conservative approach to fixed pay elements (base salary), the achievement of pre-established goals (annual bonuses) and long-term equity awards well below median of the Peer Group in view of the challenging business environment and the Company’s stock performance in such environment.

| | · | ·

| Base Salaries: Three of the four NEOs who were also NEOs for fiscal 2009 The CEO and CFO received no base salary increase infor fiscal 2010. Our newly appointed COO, upon his promotion at the end of the first quarter of fiscal 2010,2012. The remaining three NEOs received a base salary increaseincrease. In December 2011, the Committee approved fiscal 2012 increases for Messrs. Pellerito, Valiaveedan and O’Connor. The increases for Messrs. Pellerito and Valiaveedan were approved in order to compensate him for his elevated set of responsibilities. In addition, based on a review of externalmove them closer to the Peer Group data, our CFO received a base salary increasemedian and, in fiscal 2010, which was intendedthe case of Mr. Valiaveedan, to bringfurther align him towith the median level for the broad-based compensation survey data (as described further under “Compensation Philosophy and Objectives – Peer Group Considerations”). Mr. O’Connor received an increase as a result of the Peer Group.his promotion to Vice President — Chief Accounting Officer and Corporate Controller. See “Details of Compensation Elements – Base Salaries” below for additional information on base salaries. |

| | · | ·

| Annual Bonuses: Consistent with the achievement of specified financial andor personal objectives, fiscal 20102012 bonuses were paid out to all NEOs. Bonuses for the CEO, CFO and COO were the same as for fiscal 2011. Bonuses for the other NEOs increased in proportion to the amount of their annual salary increases, as their bonus calculations are a percentage of base salary. Additional details are described below under “Details of Compensation Elements – Annual Bonuses – Regular Bonuses.” |

| | · | ·

| Discretionary Bonuses: None Discretionary bonuses were madeawarded to Mr. O’Connor and Mr. Valiaveedan in fiscal 2010 to any NEO while he was an executive officer.2013 in respect of their performance in fiscal 2012, as described further under “Details of Compensation Elements – Annual Bonuses – Discretionary Bonuses.” |

| | · | ·

| Long TermLong-Term Awards, including stock options and participation in the 2011-2013 LTIP:Long-Term Incentive Program (described below): Grants of equity awards made to NEOs forin fiscal 20102012 and the annualized target value of the Company’s Long-Term Incentive Program fell considerably below median Peer Group long-term incentive compensation levels, includinglevels. The Long-Term Incentive Program was implemented in fiscal 2010 as a multi-year award with a three-year performance period (fiscal 2011-2013), with additional vesting conditions in fiscal 2014 and 2015. In fiscal 2012, the targetCommittee determined that stock options granted in June 2012 to the CEO, CFO and COO would have an exercise price 33 1/3% above the closing stock price on the grant date. In determining to grant options with an exercise price at this premium level, the Committee sought to provide a stronger link with increased shareholder value, as these executives have more significant responsibility for the Company’s long-term strategy as compared to the other NEOs. The Committee also determined to increase the number of options awarded in recognition of the premium pricing and its determination that the CEO, CFO and COO’s long-term incentive values on the grant date (including recent annual option grants and the annualized fiscal 2010 value of the Long-Term Incentive Program annualizedLTIP at target, discussed below) were considerably below the median value of long-term incentive awards granted to the endPeer Group chief executive officers, chief financial officers and chief operating officers. Additional details are described below under “Details of its three-year performance period.Compensation Elements – Stock Grants.” |

| · | Change in Control and Severance Agreements: In January 2012, the Company entered into change in control severance protection agreements with Messrs. O’Connor and Valiaveedan. The Committee considers the continued services of these key executives whose skills are not specifically tied to the homebuilding industry to be in the best interests of the Company and its shareholders. The agreements are designed to reinforce and encourage their continued attention and dedication to their duties of employment without personal distraction or conflict of interest in circumstances which could arise from the occurrence of a change in control of the Company. These agreements provide benefits following a change in control only if the executive is terminated involuntarily or terminates with Good Reason. Neither of these agreements provide for excise tax gross-ups. The provisions of such agreements are described below under “Potential Payments Upon Termination Or Change-In-Control Table.” |

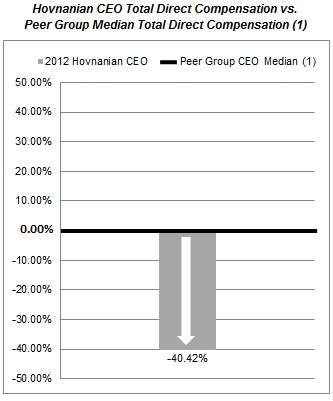

| · | Impact on CEO Total Direct Compensation: The following graphs compare fiscal 2012 CEO total direct compensation (the sum of base salary, annual bonus/incentive and long-term incentive awards, excluding all other compensation elements) to the most recently published Peer Group median data available to the Committee when finalizing fiscal 2012 CEO compensation. |

| (1) | Reflects the most recently published Peer Group Median data available to the Committee when finalizing fiscal 2012 CEO compensation. Note that the annual incentive and long-term incentive compensation levels for two of the eleven peer group CEOs reflected in the Peer Group Median were substantially lower than their prior year levels because these CEOs were no longer serving in such positions during or just after the end of the year for which the data was gathered. Had these two CEOs been excluded from the Peer Group CEO Median, the Peer Group CEO Median would have been higher and, consequently, the CEO’s Total Direct Compensation would have been further below the Peer Group CEO Median Total Direct Compensation. |

| (1) | Reflects the most recently published Peer Group Median data available to the Committee when finalizing fiscal 2012 CEO compensation. Note that the annual incentive and long-term incentive compensation levels for two of the eleven peer group CEOs reflected in the Peer Group Median were substantially lower than their prior year levels because these CEOs were no longer serving in such positions during or just after the end of the year for which the data was gathered. Had these two CEOs been excluded from the Peer Group CEO Median, the Peer Group CEO Median would have been higher and, consequently, the CEO’s Total Direct Compensation would have been further below the Peer Group CEO Median Total Direct Compensation. |

2. COMPENSATION PHILOSOPHY AND OBJECTIVES

The Compensation Committee, in conjunction with the Board of Directors and with senior management, has been instrumental in shaping the Company’s compensation philosophy and objectives because of its responsibilities and oversight of the Company’s various policies and procedures concerning executive compensation.

The six primary objectives that the Committee consideredconsiders in making compensation decisions are discussed below.below, as are our other philosophies and mechanisms for determining compensation. In making compensation-related decisions, the Committee also considered its role in promoting good corporate governance practices.

Primary Objectives for the Compensation Program

The Company’s primary objectives for compensating its executives are as follows:

| | 1. | To fairly compensate its executives in a manner that is appropriate with respect to their performance, level of responsibilities, abilities and skills; |

| | 2. | To offer compensation that guides, motivates, retains and rewards its executives for the achievement of the Company’s financial performance, strategic initiatives and individual goals; |

| | 3. | To align the executive’s interests with the interests of the shareholders; |

| | 4. | To maintain competitive pay opportunities for its executives so that it retains its talent pool and, at the same time, has the ability to attract new and highly-qualified individuals to join the organization as it grows or in the event of succession or replacement of an executive; |

| | 5. | To safeguard that the reward system is appropriately designed in the context of a challenging business environment; and |

| | 6. | To ensure that compensation plans do not incentivize a level of risk that is reasonably likely to have a material adverse effect on the Company. |

Tailored Compensation

Consistent with these objectives, the Company’s compensation philosophy also takes into consideration the very unique roles played by each of the named executive officersNEOs for whom compensation is reported in the tables below, (“NEOs”), and the Committee seeks to individually tailor their compensation packages to align their pay mix and pay levels with their contributions to, and positions within, the Company. For example:

| | · | CEO,: CFO and COO: The compensation package of the CEO,, Mr. Ara K. Hovnanian, differsthe CFO, Mr. J. Larry Sorsby, and the COO, Mr. Thomas J. Pellerito, differ from that of the other NEOs due to histheir unique roleroles and elevated set of responsibilities. Because the CEO, makesCFO and COO make executive decisions that influence the direction, stability and profitability of the Company, histheir overall compensation is intended to strongly align with objective financial measures of the Company. |

| | |