Use these links to rapidly review the document

TABLE OF CONTENTS

TABLE OF CONTENTS 2

As filed with the Securities and Exchange Commission on November 25,December 7, 2009.

Registration No. 333- 333-163372

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

COWEN GROUP, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) | 6211 (Primary Standard Industrial Classification Code Number) | 27-0423711 (I.R.S. Employer Identification No.) |

599 Lexington Avenue

New York, New York 10022

(212) 845-7900

(Address, including zip code, and telephone number, including

area code, of registrant's principal executive offices)

J. Kevin McCarthy

General Counsel

Cowen Group, Inc.

599 Lexington Avenue

New York, New York 10022

(212) 845-7900

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

David K. Boston, Esq. Laura L. Delanoy, Esq. Willkie Farr & Gallagher LLP 787 Seventh Avenue New York, New York 10019 (212) 728-8000 | Michael T. Kohler, Esq. Bartholomew A. Sheehan, III, Esq. Sidley Austin LLP 787 Seventh Avenue New York, New York 10019 (212) 839-5300 | |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

CALCULATION OF REGISTRATION FEE

| Title of Securities to be Registered | Shares to be Registered | Proposed Maximum Aggregate Offering Price(1)(2) | Amount of Registration Fee(3) | Shares to be Registered | Proposed Maximum Aggregate Offering Price(1)(2) | Amount of Registration Fee(3) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

Class A common stock, par value $0.01 | 17,250,000 | $112,642,500 | $6,286 | 17,480,000 | $114,098,400 | $6,368(4) | ||||||

|

|

| ||||||||||

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS (Subject to Completion) | Dated | |

15,000,00015,200,000 Shares

COWEN GROUP, INC.

Class A common stock

This is a public offering of shares of Class A common stock of Cowen Group, Inc. All of theCowen Group, Inc. is offering 15,000,000 shares of Class A common stock arestock. The selling stockholder identified in this prospectus is offering an additional 200,000 shares of Class A common stock. Cowen Group, Inc. will not receive any of the proceeds from the sale of the shares being sold by Cowen Group, Inc.the selling stockholder.

Our Class A common stock is presently traded on the NASDAQ Global Market under the symbol "COWND"."COWN." On November 24,December 4, 2009, the last reported sale price of our Class A common stock was $6.72$6.32 per share.

An investment in our Class A common stock involves a high degree of risk. See "Risk Factors" beginning on page 11 of this prospectus to read about factors you should consider before buying shares of our Class A common stock.

Neither the Securities and Exchange Commission nor any state securities commission or other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| | Per Share | Total | |||||

|---|---|---|---|---|---|---|---|

Public offering price | $ | $ | |||||

Underwriting discount | $ | $ | |||||

Proceeds, before expenses, to Cowen Group, Inc. | $ | $ | |||||

Proceeds, before expenses, to the selling stockholder | $ | $ | |||||

We have granted the underwriters an option to purchase up to an additional 2,250,0002,280,000 shares of our Class A common stock to cover any over-allotments, at the public offering price less the underwriting discount.

The underwriters expect to deliver the shares against payment in New York, New York on December , 2009.

| Cowen and Company | ||||||||||||

| BofA Merrill Lynch | ||||||||||||

Credit Suisse | ||||||||||||

Sandler O'Neill + Partners, L.P. | ||||||||||||

Keefe, Bruyette & Woods

December , 2009

Prospectus Summary | 1 | |

Risk Factors | 11 | |

Cautionary Statement Regarding Forward-Looking Statements | 37 | |

Use of Proceeds | 38 | |

Capitalization | 39 | |

Market Price of Class A Common Stock | 39 | |

Dividend Policy | 39 | |

Unaudited Pro Forma Condensed Combined Financial Statements | 40 | |

Selected Consolidated Historical Financial Data of the Company | 53 | |

Supplemental Quarterly Consolidated Financial Information | ||

Selected Consolidated Historical Financial Data of Cowen Holdings | ||

Management's Discussion and Analysis of Financial Condition and Results of Operations of the Company | ||

Management's Discussion and Analysis of Financial Condition and Results of Operations of Cowen Holdings | ||

Business | ||

Board and Management of Cowen Group | ||

Corporate Governance | ||

Certain Relationships and Related Transactions | ||

Compensation Discussion and Analysis | ||

Description of Capital Stock | ||

Security Ownership of Certain Beneficial Owners, the Selling Stockholder and Management | ||

Shares Eligible for Future Sale | ||

Material United States Tax Consequences | ||

Underwriting (Conflicts of Interest) | ||

Legal Matters | ||

Experts | ||

Where You Can Find More Information | ||

Index to Financial Statements | F-1 |

You should rely only on the information contained in this prospectus. Neither of uswe or the selling stockholder nor the underwriters hashave authorized anyone to provide you with information different from or in addition to that contained in this prospectus. If anyone provides you with additional or different information, you should not rely on it. We, the selling stockholder and the underwriters are offering to sell, and seeking offers to buy, shares of our Class A common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, unless the information specifically indicates that another date applies, regardless of the time of delivery of this prospectus or of any sale of our Class A common stock.

i

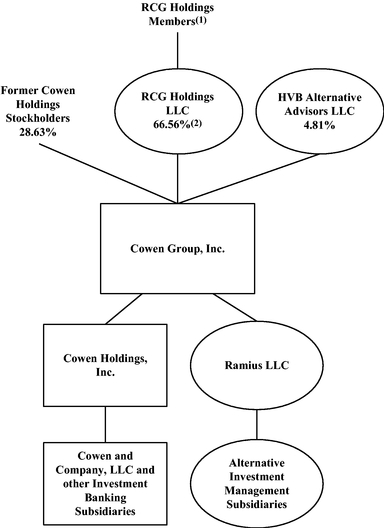

In this prospectus, references to "the Company," "Cowen Group," "we," "our" and "us" are to Cowen Group, Inc. and, except as the context otherwise requires, its consolidated subsidiaries. In this prospectus, references to "Ramius" refer to Ramius LLC, a wholly owned subsidiary of the Company, references to "Cowen Holdings" refer to Cowen Holdings, Inc., a wholly owned subsidiary of the Company, and references to "RCG" refer to RCG Holdings LLC, an entity which holds approximately 66.56% of our Class A common stock, in each case unless the context indicates otherwise. References to "Cowen and Company" refer to Cowen and Company, LLC, a wholly owned subsidiary of Cowen Holdings and the Company's primary broker-dealer, and to the Company's investment banking operations generally.

On November 2, 2009, the transactions (which we refer to collectively with the fund of funds asset exchange, described in the section titled "Prospectus Summary" below, as the Transactions) contemplated by the Transaction Agreement and Agreement and Plan of Merger, dated as of June 3, 2009 (which we refer to as the Transaction Agreement), by and among the Company, Ramius, Cowen Holdings, RCG and Lexington Merger Corp., were consummated including (1) the merger of Lexington Merger Corp. with and into Cowen Holdings, pursuant to which each outstanding share of common stock of Cowen Holdings Inc. was converted into one share of Class A common stock of the Company and (2) the transfer by RCG of substantially all of its assets and liabilities to Ramius in exchange for the Company's issuance to RCG of 37,536,826 shares of Class A common stock of the Company.

Prior to the consummation of the Transactions, the Company did not conduct any material activities other than those incidental to its formation and the matters contemplated by the Transaction Agreement. All financial statements and related financial information of the Company presented in this prospectus relate to the historical information of Ramius (the business of which was operated by RCG, the Company's accounting predecessor, prior to the consummation of the Transactions), unless the context indicates otherwise.

ii

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all of the information that may be important to you and is qualified in its entirety by, and should be read in conjunction with, the more detailed information contained elsewhere in this prospectus and our financial statements and the related notes appearing elsewhere in this prospectus before you decide to invest in our Class A common stock. This prospectus contains forward-looking statements, which involve risks and uncertainties. Our actual results could differ materially from those anticipated in such forward-looking statements as a result of certain factors, including those discussed in "Risk Factors" and other sections of this prospectus.

Our Business

Cowen Group is a diversified financial services firm providing alternative investment management, investment banking, research, and sales and trading services through its business units, Ramius and Cowen and Company. Its alternative investment management products include hedge funds, fund of funds, real estate, healthcare royalty funds and cash management services, offered primarily under the Ramius name. Cowen and Company offers industry focused investment banking services for growth-oriented companies, domain knowledge-driven research and a sales and trading platform for institutional investors.

Cowen Group, a Delaware corporation, is a new holding company, formed in connection with the business combination of Ramius and Cowen Holdings. On November 2, 2009, the Transactions were consummated in which RCG received approximately 66.56% of our Class A common stock in exchange for the Ramius business and former Cowen Holdings shareholders received approximately 28.63% of our Class A common stock in exchange for the Cowen Holdings business. Following the consummation of the Transactions, each of Ramius and Cowen Holdings became a wholly owned subsidiary of the Company.

Industry Overview

The financial market dislocation, which began in the fourth quarter of 2007 and accelerated into 2008, has created new opportunities for firms that are able to adapt to the changing landscape. In the past 24 months, many financial institutions in the United States either failed outright or were acquired by other financial institutions in distressed sales. Many of those that survived the dislocation found that their operating strategies had become greatly altered by the federal government, which became a major stakeholder in a number of financial institutions through various guarantee and support programs.

We believe the firms that have navigated this dislocation and are unencumbered by government obligations will have advantages going forward. Such firms should have opportunities to develop new client relationships and to build and improve their talent base and product offerings.

Competitive Strengths

We believe that the recent combination of Ramius's and Cowen and Company's businesses creates a firm with the breadth and depth to take advantage of the current market dislocation. The Company's global alternative investment management business (hedge funds, fund of funds, real estate, healthcare royalty funds and cash management services) complements the Company's established financial services practice (investment banking, research and sales and trading) in the following ways:

Diversified Platform of Complementary Businesses. The combination of our alternative investment management and investment banking businesses adds significant diversity to our sources of revenue. We believe that revenue diversification provides us with greater financial stability through market cycles when compared to other firms with a narrower product, sector or regionally-focused business model.

Top-Tier Management Team. We have a team of senior professionals led by seasoned executives with decades of experience building and managing financial services organizations and a track record of generating positive risk-adjusted returns. Additionally, the reputation of our senior management and their global network of relationships provides us with competitive advantages in identifying transactions and securing investment opportunities.

Strong Balance Sheet with a Long-Term, Proprietary Track Record of Outperformance. On a pro forma basis as of September 30, 2009, we had $408.6 million of total equity, a significant portion of which is invested or available for new investment opportunities. Since Ramius began investing its own capital on a proprietary basis in 1999, we generated a compounded annualized return on our invested capital through September 30, 2009 that significantly exceeds the S&P 500 return for the same period.

Team-Oriented Culture. Our senior management encourages collaboration and fosters a partnership culture in which highly-motivated team members can seek to build successful businesses together. We believe this enables us to identify and respond to new opportunities as they emerge and ultimately helps us to better identify, attract and retain talented, results-oriented people.

Alignment of Interests. One of our fundamental philosophies is to align the interests of our management and employees with those of our shareholders and investors. Employees, our executive officers and members of our board of directors own over 30% of our outstanding Class A common stock, including through their ownership of RCG. The equity held by certain Ramius principals through RCG is subject to transfer restrictions for at least 30 months from November 2, 2009. In addition, the Company's own capital is invested alongside our investors in many of our investment products.

Institutionalized Operational Processes and Infrastructure. We have developed highly institutionalized products, risk management, operational and information technology processes and controls. We believe that this infrastructure is scalable and important in attracting institutional investors, third-party distribution platforms and brokerage clients who demand portfolio transparency and deep insight into investment processes, as well as high quality research, execution and advisory services.

Opportunities for Growth

The business combination of Ramius and Cowen and Company brought together two like-minded, collaborative cultures. We believe the open exchange of ideas and the leveraging of relationships across both organizations will lead to greater revenue opportunities in our existing business lines. Moreover, our balance sheet should allow us to pursue opportunistic expansion either organically, through the hiring of talented individuals or teams, or through acquisitions, investments and strategic partnerships for both our alternative investment management and investment banking businesses.

Additional business line initiatives include:

Alternative Investment Management Business

Extend strong investment track record. Historically, our hedge fund and fund of funds platforms have sought to deliver consistent, risk-adjusted returns to our investors throughout market cycles. In these platforms, we seek positive performance with minimal correlation to directional market indices. As we seek to increase our assets under management, our focus remains to provide our clients with strong investment performance through our current strategies.

Grow assets under management by expanding our global distribution network. We are focused on developing a more significant global presence and intend to expand our client relationships and distribution capabilities in key regions of the world through new distribution channels and joint ventures. In addition, we are seeking to become a preferred alternative investment service provider to

financial intermediaries who will distribute our alternative investment management products through their distribution platforms.

Expand investment products and strategies. We are an alternative investment solutions provider that focuses on evolving client needs. We have consistently developed and added new products and strategies to our business and will continue to selectively expand our products, strategies and service offerings through acquisition, strategic partnership or the addition of new investment talent.

Investment Banking Business

Enhance our investment banking relationships. We believe that the combination of Ramius's network of investors and partners and Cowen and Company's corporate and institutional relationships coupled with our capital markets capabilities should enable us to be retained for more and a wider variety of investment banking transactions.

Leverage our sales and trading distribution into broader firm relationships. The institutional knowledge and expertise of our sales and trading teams are highly valued by our clients. We will seek to leverage this knowledge and expertise into increased levels of dialogue with our clients to generate value added capital markets and portfolio management ideas that we can execute on their behalf.

Hire additional senior professionals and add new industry verticals. We anticipate adding financial professionals and coverage of new sectors on an opportunistic basis. We have recently hired individuals in two new industry verticals—financial institutions and REITs—that have the potential for strong transaction activity.

Our Alternative Investment Management Business

We operate our alternative investment management business primarily through Ramius LLC, our wholly owned subsidiary. Our alternative investment management business had approximately $7.9 billion of assets under management as of October 1, 2009, after giving pro forma effect to the consummation of the Transactions. The predecessor to this business was founded in 1994 and, through one of its subsidiaries, has been a registered investment adviser under the Investment Advisers Act since 1997. Our alternative investment management products and services include hedge funds, fund of funds, real estate, healthcare royalty funds and cash management services. Our institutional investors include pension funds, insurance companies, banks, foundations and endowments, wealth management organizations and family offices.

Our Investment Banking Business

We operate our investment banking business primarily through Cowen and Company, LLC, our primary broker-dealer. Cowen and Company, LLC is an international investment bank dedicated to providing superior research, brokerage and investment banking services to companies and institutional investor clients primarily in the healthcare, technology, media and telecommunications, consumer, aerospace and defense, financial institutions, REITs and alternative energy sectors. We provide research and brokerage services to over 1,000 domestic and international clients seeking to trade equity and equity-linked securities, principally in our target sectors. We focus our investment banking efforts, principally equity and equity-linked capital raising and strategic advisory services, on growth-oriented public companies as well as private companies.

Risk Factors

Investing in our Class A common stock involves substantial risk. You should carefully consider all of the information set forth in this prospectus and, in particular, should evaluate the specific factors set

forth under "Risk Factors" in deciding whether to invest in our Class A common stock. Some of the most important risks are summarized below.

Recent Developments

Consummation of the Transactions

On November 2, 2009, the Transactions were consummated including (1) the conversion of each outstanding share of Cowen Holdings's common stock of into one share of our Class A common stock

and (2) RCG's transfer of substantially all of its assets and liabilities to Ramius, our wholly owned subsidiary, in exchange for 37,536,826 shares of our Class A common stock.

Fund of Funds Asset Exchange

On November 2, 2009, concurrently with the consummationas part of the Transactions, Cowen Holdings purchased from HVB the 50% interest in the Ramius fund of funds business, which is known as Ramius Alternative Solutions LLC (which we refer to as Ramius Alternative Solutions) that HVB owned in exchange for (1) the Company's issuance to HVB of 2,713,882 shares of our Class A common stock and (2) approximately $10.4 million in cash. This exchange resulted in Ramius Alternative Solutions becoming an indirect wholly-ownedwholly owned subsidiary of the Company.

The diagram below shows the structure of the Company as of November 2, 2009 following completion of the Transactions:

this offering and will distribute the net proceeds to satisfy withdrawals of certain of its other, non-affiliate members who are withdrawing one-third of their capital in RCG as of December 31, 2009.

Credit Facility

On November 2, 2009, the Company entered into a Secured Revolving Credit Agreement (which we refer to as the HVB Credit Facility) with Bayerische Hypo- und Vereinsbank AG, which we refer to as HVB AG, as Administrative Agent, and another lender. The credit agreement provides for a secured revolving loan facility of up to $50 million (which automatically reduces to $25 million on January 4, 2010), with a maturity date of September 29, 2011.

Principal Executive Offices

Our principal executive offices are located at 599 Lexington Avenue, New York, New York 10022, and our telephone number is (212) 845-7900. Our website address ishttp://www.cowen.com/. Our website and the information contained on, or that can be accessed through, the website are not part of this prospectus.

Class A common stock offered by us | 15,000,000 shares | |

Class A common stock offered by the selling stockholder | 200,000 shares. These shares are held by RCG and are attributable to certain of its non-affiliate members who are withdrawing one-third of their capital in RCG as of December 31, 2009. RCG is selling these shares and will distribute the net proceeds to those members to satisfy such withdrawals. | |

Over-allotment option granted by us to the underwriters |

| |

Common stock to be outstanding after this offering |

| |

Use of proceeds | We estimate that we will receive net proceeds from this offering of approximately $ million, after deducting the underwriting discounts and other estimated offering expenses payable by us. | |

We anticipate that we will use approximately $25 million of the net proceeds received by us from this offering to repay indebtedness and the remainder for working capital and general corporate purposes. | ||

We will not receive any proceeds from the sale of any shares in this offering by the selling stockholder. | ||

See "Use of Proceeds." | ||

Listing | Our Class A common stock is currently | |

Dividend Policy | We have never declared or paid any cash dividends on the Class A common stock and have no intent to do so for the foreseeable future. Any payment of cash dividends on Class A common stock in the future will be at the discretion of our board of directors and will depend upon our results of operations, earnings, capital requirements, financial condition, future prospects, applicable law, contractual restrictions and other factors deemed relevant by our board of directors. See "Dividend Policy." |

References in this prospectus to the number of shares of our Class A common stock to be outstanding after this offering are based on 56,397,41157,437,136 shares of Class A common stock outstanding on November 23,December 4, 2009 and exclude:

Except as otherwise noted, all information in this prospectus:

SUMMARY HISTORICAL AND PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION

The following summarizes our historical and pro forma consolidated financial information. We derived the historical financial information from our accounting predecessor's audited consolidated financial statements for the years ended December 31, 2008, 2007 and 2006 and the unaudited consolidated financial statements for the nine months ended September 30, 2009 and 2008 included elsewhere in this prospectus. The unaudited pro forma consolidated statement of operations data and pro forma consolidated statements of financial condition data give effect to the Transactions as if they were completed on January 1, 2008 and include all adjustments which give effect to the events that are directly attributable to the Transactions, as long as the impact of such events are expected to continue and are factually supportable.

This information should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations of the Company," "Management's Discussion and Analysis of Financial Condition and Results of Operations of Cowen Holdings," "Unaudited Pro Forma Condensed Combined Financial Statements," "Unaudited Selected Pro Forma Condensed Combined Financial Information,"Statements" and the financial statements and related notes of RCG and Cowen Holdings appearing elsewhere in this prospectus.

| | Pro Forma | | | | | | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Nine Months Ended | | | | | | | |||||||||||||||||

| | Year Ended | Nine Months Ended September 30, | | | | |||||||||||||||||||

| | Year Ended December 31, | |||||||||||||||||||||||

| | September 30, 2009 | December 31, 2008 | ||||||||||||||||||||||

| | 2009 | 2008 | 2008 | 2007 | 2006 | |||||||||||||||||||

| | (in thousands) | |||||||||||||||||||||||

Consolidated Statements of Operations Data: | ||||||||||||||||||||||||

Revenues | ||||||||||||||||||||||||

Management fees | $ | 38,125 | $ | 83,391 | $ | 31,408 | $ | 56,443 | $ | 70,818 | $ | 73,950 | $ | 65,635 | ||||||||||

Incentive income | 177 | — | 177 | — | — | 60,491 | 81,319 | |||||||||||||||||

Interest and dividends | 592 | 5,355 | 225 | 1,443 | 1,993 | 16,356 | 17,189 | |||||||||||||||||

Reimbursement from affiliates | 7,832 | 16,330 | 7,832 | 11,675 | 16,330 | 7,086 | 4,070 | |||||||||||||||||

Investment banking | 28,917 | 50,937 | — | — | — | — | — | |||||||||||||||||

Brokerage | 103,773 | 149,901 | — | — | — | — | — | |||||||||||||||||

Other Revenues | 4,173 | 7,404 | 2,265 | 4,737 | 6,853 | 5,086 | 8,038 | |||||||||||||||||

Consolidated Ramius Funds and certain real estate entities revenues | 12,312 | 31,739 | 12,312 | 26,165 | 31,739 | 25,253 | 35,897 | |||||||||||||||||

Total revenues | 195,901 | 345,057 | 54,219 | 100,463 | 127,733 | 188,222 | 212,148 | |||||||||||||||||

Expenses | ||||||||||||||||||||||||

Employee compensation and benefits | 158,474 | 228,910 | 50,869 | 67,703 | 84,769 | 123,511 | 112,433 | |||||||||||||||||

Non-compensation expense (excluding goodwill impairment) | 103,760 | 152,640 | 38,070 | 37,929 | 54,856 | 79,020 | 54,277 | |||||||||||||||||

Goodwill impairment | — | 10,200 | — | — | 10,200 | — | — | |||||||||||||||||

Consolidated Ramius Funds and certain real estate entities expenses | 11,831 | 34,268 | 11,831 | 27,040 | 34,268 | 21,014 | 39,300 | |||||||||||||||||

Total expenses | 274,065 | 426,018 | 100,770 | 132,672 | 184,093 | 223,545 | 206,010 | |||||||||||||||||

Other income (loss) | ||||||||||||||||||||||||

Net gain (loss) on securities, derivatives and other investments | (2,702 | ) | (2,006 | ) | (2,702 | ) | 800 | (2,006 | ) | 94,078 | 54,765 | |||||||||||||

Gain on exchange memberships | — | 751 | — | — | — | — | — | |||||||||||||||||

Consolidated Ramius Funds and certain real estate entities net gains (losses) | 25,268 | (198,485 | ) | 25,268 | (85,523 | ) | (198,485 | ) | 84,846 | 78,656 | ||||||||||||||

Total other income (loss) | 22,566 | (199,740 | ) | 22,566 | (84,723 | ) | (200,491 | ) | 178,924 | 133,421 | ||||||||||||||

Income (loss) before income taxes | (55,598 | ) | (280,701 | ) | (23,985 | ) | (116,932 | ) | (256,851 | ) | 143,601 | 139,559 | ||||||||||||

Income tax provision (benefit) | (5,413 | ) | 10,486 | (5,978 | ) | 738 | (1,301 | ) | 1,397 | 4,814 | ||||||||||||||

Net income (loss) | (50,185 | ) | (291,187 | ) | (18,007 | ) | (117,670 | ) | (255,550 | ) | 142,204 | 134,745 | ||||||||||||

Net Income (loss) attributable to non-controlling interests | 13,247 | (108,537 | ) | 13,888 | (52,176 | ) | (113,786 | ) | 66,343 | 74,189 | ||||||||||||||

Special allocation to the Managing Member | — | — | — | — | — | 26,551 | 21,195 | |||||||||||||||||

Net income (loss) available to all Redeemable Members | $ | (63,432 | ) | $ | (182,650 | ) | $ | (31,895 | ) | $ | (65,494 | ) | (141,764 | ) | 49,310 | 39,361 | ||||||||

SUMMARY HISTORICAL AND PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION (Continued)

| | As of September 30, | As of December 31, | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2009 | 2008 | 2007 | 2006 | |||||||||

| | (in thousands) | ||||||||||||

Consolidated Statements of Financial Condition Data: | |||||||||||||

Total assets | $ | 681,895 | $ | 797,831 | $ | 2,113,532 | $ | 2,468,195 | |||||

Total liabilities | 113,025 | 182,003 | 1,430,029 | 1,657,992 | |||||||||

Redeemable non-controlling interests in consolidated subsidiaries | 267,242 | 284,936 | 203,523 | 514,761 | |||||||||

Total redeemable members' capital | $ | 301,628 | $ | 330,892 | $ | 479,980 | $ | 295,442 | |||||

| | Pro Forma | |||

|---|---|---|---|---|

| | As of September 30, 2009 | |||

Consolidated Statements of Financial Condition Data: | ||||

Total assets | $ | 869,977 | ||

Total liabilities | 207,996 | |||

Total redeemable group equity | 253,359 | |||

Total equity | $ | 408,622 | ||

Cowen and Company, LLC, a wholly owned subsidiary of Cowen Group, is a member of the Financial Industry Regulatory Authority, Inc. (formerly known as the National Association of Security Dealers, Inc., or the NASD), or FINRA, and will participate in the distribution of the shares of our Class A common stock. We control Cowen and Company and this relationship is defined as a "conflict of interest" under Conduct Rule 2720 of the NASD. RCG also indirectly controls Cowen and Company and will sell shares of our Class A common stock in the offering. This relationship would also be defined as a "conflict of interest" under Conduct Rule 2720 of the NASD. BA Alpine Holdings, Inc., an affiliate of HVB, is a member of RCG and therefore considered an affiliate of Cowen and Company. In excess of 5% of the net offering proceeds are intended to be paid to HVB to repay amounts outstanding under the HVB Credit Facility. This is also defined as a "conflict of interest" under Conduct Rule 2720 of the NASD. Because of this relationship,those relationships, the offering will be conducted in accordance with NASD Rule 2720. This rule requires, among other things, that a qualified independent underwriter has participated in the preparation of, and has exercised the usual standards of "due diligence" in respect to, the registration statement and this prospectus. Merrill Lynch, Pierce, Fenner & Smith Incorporated has agreed to act as qualified independent underwriter for the offering and to undertake the legal responsibilities and liabilities of an underwriter under the Securities Act of 1933, as amended (or the "Securities Act"), specifically including those inherent in Section 11 of the Securities Act. We have agreed to indemnify Merrill Lynch, Pierce, Fenner & Smith Incorporated against liabilities in connection with acting as a qualified independent underwriter, including liabilities under the Securities Act.

An investment in our Class A common stock involves a high degree of risk. You should carefully consider the following information, together with the other information in this prospectus, prior to making a decision to purchase shares of our Class A common stock. This prospectus contains, in addition to historical information, forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those discussed herein. If any of the following risks occur or if any additional risks and uncertainties not presently known to us or not currently believed to be material occur, our business, results of operations, financial condition or prospects could be materially adversely affected.

Risks Related to the Company's Businesses and Industry

For purposes of the following risk factors, references made to Ramius's funds include hedge funds and other alternative investment management products offered by the Company and funds in the Ramius fund of funds business and real estate funds.

The Company

Difficult market conditions, market disruptions and volatility have adversely affected and may in the future continue to adversely affect the Company's businesses, results of operations and financial condition.

The Company's businesses, by their nature, do not produce predictable earnings, and all of the Company's businesses may be materially affected by conditions in the global financial markets and by global economic conditions, such as interest rates, the availability of credit, inflation rates, economic uncertainty, changes in laws, commodity prices, asset prices (including real estate), currency exchange rates and controls and national and international political circumstances (including wars, terrorist acts or security operations). Recently, global credit and other financial markets have suffered and continue to suffer substantial stress, volatility, illiquidity and disruption. Market turbulence reached unprecedented levels during the third and fourth quarters of 2008, as loss of investor confidence in the financial system resulted in an historically unprecedented lack of liquidity, decline in asset values (including real estate assets), and the bankruptcy or acquisition of, or government assistance to, several major domestic and international financial institutions. These factors, combined with volatile commodity prices and foreign exchange rates, have contributed to recessionary economic conditions globally and a deterioration in consumer and corporate confidence and could further exacerbate the overall market disruptions and risks to market participants, including the Ramius funds and managed accounts. These market conditions may affect the level and volatility of securities prices and the liquidity and the value of investments in the Ramius funds (including Ramius Enterprise L.P. (which we refer to as Enterprise) in which the Company has an investment of approximately $276 million of its own capital as of September 30, 2009) and managed accounts, and the Company may not be able to effectively manage its alternative investment management business's exposure to these market conditions. Losses in Enterprise could adversely affect our results of operations.

In addition, industry-wide declines in the size and number of underwritings and mergers and acquisitions have had an adverse effect on revenues of Cowen and Company due to the decrease in equity underwritings and the decline in both announced and completed mergers and acquisitions. Continued weakness in equity markets and diminished trading volume of securities could further adversely impact Cowen and Company's brokerage business, from which Cowen Holdings historically generated a significant portion of its revenues. In addition, reductions in the trading prices for equity securities also tend to reduce the dollar value of investment banking transactions, such as underwriting and merger and acquisition transactions, which in turn would likely reduce the fees that Cowen and Company earns from these transactions. As the Company may be unable to reduce expenses correspondingly, its profits and profit margins of its investment banking business may decline. During 2008, the adverse market conditions impacted Cowen and Company's investment banking business, and

there can be no assurance that these conditions will improve in the near term. Until they do, the Company expects its results of operations to be negatively impacted.

The Company is expected to incur substantial expenses related to the integration of Ramius and Cowen Holdings.

The Company expects to continue to incur substantial expenses in connection with the integration of the business, policies, procedures, operations, technologies and systems of Ramius and Cowen Holdings. There are a large number of functions that must be integrated, including but not limited to information technology, finance, human resources, audit, corporate communications, risk management and legal and compliance. Furthermore, the Company expects to move its employees in New York to a single office location, which will likely result in the Company incurring additional costs for rent and capital expenditures. While the Company has calculated an estimate of expenses, there are a number of factors beyond the Company's control that could affect the total amount or the timing of all of the expected integration expenses. Moreover, many of the expenses that will be incurred, by their nature, are difficult to estimate accurately at the present time. These expenses could, particularly in the near term, exceed the savings that the Company expects to achieve from the elimination of duplicative expenses and the realization of economies of scale, cost savings and revenue synergies related to the integration of the businesses as a result of the Transactions.

Although the Company expects that the combination of the businesses of Ramius and Cowen and Company will result in benefits to the Company, the Company may not realize those benefits because of integration difficulties and other challenges.

The success of the combination of the businesses of Ramius and Cowen and Company will depend in large part on the success of the management of the Company in integrating the operations, strategies, technologies and personnel of the two predecessor companies. The Company may fail to realize some or all of the anticipated benefits of the Transactions if the integration process takes longer or is more costly than expected. The failure of the Company to meet the challenges involved in successfully integrating the operations of Ramius and Cowen and Company or to otherwise realize any of the anticipated benefits of the Transactions, including additional revenue opportunities, could impair the operations of the Company. In addition, the Company anticipates that the overall integration of the companies will be a complex, time-consuming and expensive process that, without proper planning and effective and timely implementation, could significantly disrupt the business of Ramius and Cowen and Company.

Potential difficulties the Company may encounter in the integration process include the following:

The anticipated benefits and synergies include the combination of offices in various locations and the elimination of numerous technology systems, duplicative personnel and duplicative market and other data sources. However, these anticipated benefits and synergies assume a successful integration and are based on projections and other assumptions, which are inherently uncertain. Furthermore, the combination of the Company's offices in New York will likely result in the Company initially incurring additional costs for rent and capital expenditures.

Ramius and Cowen and Company operate in different business segments. Ramius's business is alternative investment management. Ramius's investment products and services include hedge funds, fund of funds, real estate funds, healthcare royalty funds and cash management services. Cowen and Company has a financial services practice, including investment banking, equity research, sales and trading and alternative investment management services. Although the management of the Company includes executives from both Ramius and Cowen and Company, the Company cannot guarantee that it will integrate and operate the business lines of Ramius and Cowen and Company to achieve the cost savings and other benefits that are anticipated to result from the Transactions. Even if integration is successful, anticipated benefits and synergies may not be achieved.

The Company's alternative investment management and investment banking businesses have incurred losses in recent periods and may incur losses in the future.

The Company's alternative investment management and investment banking businesses have incurred losses in several recent periods and also recorded net losses in certain quarters within other fiscal years. The Company may incur losses in any of its future periods. Future losses may have a significant effect on the Company's liquidity as well as our ability to operate.

In addition, we may incur significant expenses in connection with any expansion, strategic acquisition or investment with respect to our businesses. Accordingly, the Company will need to increase its revenues at a rate greater than its expenses to achieve and maintain profitability. If the Company's revenues do not increase sufficiently, or even if its revenues increase but it is unable to manage its expenses, the Company will not achieve and maintain profitability in future periods. As an alternative to increasing its revenues, the Company may seek additional capital the sale of additional common stock or through other forms of financing. Particularly in light of current market conditions, the Company cannot be certain that it would have access to such financing on acceptable terms.

The Company depends on its key senior personnel and the loss of their services would have a material adverse effect on the Company's businesses and results of operations, financial condition and prospects.

The Company depends on the efforts, skill, reputations and business contacts of its principals, Peter A. Cohen, David M. Malcolm, Jeffrey M. Solomon, Morgan B. Stark and Thomas W. Strauss and other key senior personnel, the information and investment activity these individuals generate during the normal course of their activities and the synergies among the diverse fields of expertise and knowledge held by the Company's senior professionals. Accordingly, the Company's continued success will depend on the continued service of these individuals. Key senior personnel may leave the Company in the future, and we cannot predict the impact that the departure of any key senior personnel will have on our ability to achieve our investment and business objectives. The loss of the services of any of them could have a material adverse effect on the Company's revenues, net income and cash flows and could harm our ability to maintain or grow assets under management in existing funds or raise additional funds in the future. Ramius historically relied in part on the interests of certain of these professionals in a special allocation to Ramius's managing member to discourage them from leaving Ramius's employ. However, in connection with the Transactions, the special allocation was terminated

and will no longer act as incentive for them to continue to be employed at the Company. Our senior and other key personnel possess substantial experience and expertise and have strong business relationships with investors in its funds, clients and other members of the business community. As a result, the loss of these personnel could have a material adverse effect on the Company's businesses and results of operations, financial condition and prospects.

The Company's ability to retain its senior professionals is critical to the success of its businesses, and its failure to do so may materially affect the Company's reputation, business and results of operations.

Our people are our most valuable resource. Our success depends upon the reputation, judgment, business generation capabilities and project execution skills of our senior professionals. The Company's employees' reputations and relationships with our clients are critical elements in obtaining and executing client engagements. Ramius and Cowen and Company encounter intense competition for qualified employees from other companies inside and outside of their industries. From time to time, Ramius and Cowen and Company have experienced departures of professionals. Losses of key personnel have occurred and may occur in the future. In addition, if any of our client-facing employees or executive officers were to join an existing competitor or form a competing company, some of our clients could choose to use the services of that competitor instead of the services of Ramius and Cowen and Company. The consummation of the Transactions caused all unvested RCG equity and Cowen Holdings equity held by our employees prior to the Transactions to vest. There is no guarantee that the compensation arrangements and share lock-up agreements we may have entered into with our senior professionals are sufficiently broad or effective to prevent them from resigning to join our competitors.

The success of our businesses is based largely on the quality of our employees and we must continually monitor the market for their services and seek to offer competitive compensation. In challenging market conditions, such as have occurred over the past two years, it may be difficult to pay competitive compensation without the ratio of our compensation and benefits expense to revenues becoming higher.

Volatility in the value of the Company's investments and securities portfolios or other assets and liabilities could adversely affect the financial condition or operations of the Company.

The Company is subject to the provisions of Accounting Standards Codification (ASC) Topic 820 (which we refer to as ASC 820) which RCG, as the accounting predecessor of the Company, adopted on January 1, 2008. ASC 820 defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. ASC 820 also establishes a framework for measuring fair value and a valuation hierarchy based upon the transparency of inputs used in the valuation of an asset or liability. Changes in fair value are reflected in the statement of operations at each measurement period. Therefore, continued volatility in the value of the Company's investments and securities portfolios or other assets and liabilities, including funds, will result in volatility of the Company's results. As a result, the changes in value may have an adverse effect on the Company's financial condition or operations in the future.

Limitations on the access to capital by the Company and its subsidiaries could impair its liquidity and its ability to conduct its businesses.

Liquidity, or ready access to funds, is essential to financial services firms. Failures of financial institutions have often been attributable in large part to insufficient liquidity. Liquidity is of particular importance to Cowen and Company's trading business and perceived liquidity issues may affect the Company's investment banking clients' and counterparties' willingness to engage in brokerage transactions with Cowen and Company. Cowen and Company's liquidity could be impaired due to circumstances that the Company may be unable to control, such as a general market disruption or an operational problem that affects Cowen and Company's trading clients, third parties or Cowen and

Company. Further, Cowen and Company's ability to sell assets may be impaired if other market participants are seeking to sell similar assets at the same time.

The Company is a holding company and primarily depends on dividends from its subsidiaries to funds its operations. Cowen and Company is subject to the net capital requirements of the SEC and various self-regulatory organizations of which it is a member. These requirements typically specify the minimum level of net capital a broker-dealer must maintain and also mandate that a significant part of its assets be kept in relatively liquid form. CIL,Cowen International Limited (which we refer to as CIL), the Company's U.K. registered broker-dealer subsidiary, is subject to the capital requirements of the FSA.Financial Services Authority of the United Kingdom (which we refer to as the FSA). Cowen Latitude Advisors Limited (which we refer to as CLAL) is subject to the financial resources requirements of the SFCSecurities and Futures Commission of Hong Kong.Kong (which we refer to as the SFC). Any failure to comply with these capital requirements could impair the Company's ability to conduct its investment banking business.

Ramius and its funds and/or Cowen and Company may become subject to additional regulations which could increase the costs and burdens of compliance or impose additional restrictions which could have a material adverse effect on the Company's businesses and the performance of the funds in its alternative investment management business.

Firms in the financial services industry have been subject to an increasingly regulated environment. The industry has experienced increased scrutiny from a variety of regulators, including the United States Securities and Exchange Commission (which we refer to as the SEC), the Financial Industry Regulatory Authority (which we refer to as FINRA), the New York Stock Exchange (which we refer to as NYSE), and state attorneys general. Penalties and fines sought by regulatory authorities have increased substantially over the last several years. In light of current conditions in the global financial markets and the global economy, regulators have increased their focus on the regulation of the financial services industry. The Company may be adversely affected by changes in the interpretation or enforcement of existing laws and rules by these governmental authorities and self-regulatory organizations. The Company also may be adversely affected as a result of new or revised legislation or regulations imposed by the SEC, other United States or foreign governmental regulatory authorities or self-regulatory organizations that supervise the financial markets. Among other things, the Company could be fined, prohibited from engaging in some of its business activities or subjected to limitations or conditions on its business activities. In addition, the Company could incur significant expense associated with compliance with any such legislation or regulations or the regulatory and enforcement environment generally. Substantial legal liability or significant regulatory action against the Company could have material adverse financial effects or cause significant reputational harm to the Company, which could seriously affect its business prospects.

The Company may need to modify the strategies or operations of its alternative investment management business, face increased constraints or incur additional costs in order to satisfy new regulatory requirements or to compete in a changed business environment. The Company's alternative investment management business is subject to regulation by various regulatory authorities that are charged with protecting the interests of investors. The activities of certain of the Company's subsidiaries are regulated primarily by the SEC, FINRA, and the National Futures Association, as well as various state agencies, within the United States and are also subject to regulation in the various other jurisdictions in which they operate, including the Financial Services Authority of the United Kingdom,FSA, the Financial Services Agency of Japan, the Securities and Futures Commission of Hong Kong,SFC, the German Federal Financial Supervisory Authority and the Commission of the Surveillance of the Financial Sector in Luxembourg. The activities of Ramius LLC, Ramius Securities LLC, Ramius Advisors, LLC, Ramius Asia, LLC, Ramius Alternative Solutions, Ramius Structured Credit Group LLC and RCG Starboard Advisors, LLC are all regulated by the SEC due to their registrations as U.S. investment advisers. In addition, the funds in the Company's alternative investment

management business are subject to regulation in the jurisdictions in which they are organized. These

and other regulators in these jurisdictions have broad regulatory powers dealing with all aspects of financial services including, among other things, the authority to make inquiries of companies regarding compliance with applicable regulations, to grant permits and to regulate marketing and sales practices and the maintenance of adequate financial resources. The Company is also subject to applicable anti-money laundering regulations and net capital requirements in the jurisdictions in which it operates. Additionally, the regulatory environment in which the Company operates frequently changes and has seen significant increased regulation in recent years and it is possible that this trend may continue. The Company may be materially adversely affected as a result of new or revised legislation or regulations or by changes in the interpretation or enforcement of existing laws and regulations. Such additional regulation could, among other things, increase compliance costs or limit our ability to pursue investment opportunities and strategies.

The regulatory environment continues to be turbulent as regulators globally respond to the recent financial crisis. There is an extraordinary volume of regulatory discussion papers, draft directives and proposals being issued globally and these initiatives are not always coordinated. The European Commission has issued a draft Directive on Alternative Investment Fund Managers, recommendations on directors' pay and pay for the financial services sector and proposals on packaged retail investment products. In addition, the Financial Services Authority of the United Kingdom has issued a discussion paper entitled "A Regulatory Response to the Global Banking Crisis" as well as undertaken an exercise to collect data to assess the systemic risk that hedge funds may or may not pose. The Bank of England is also collecting data on the systemic risk of hedge funds. Recent rulemaking by the SEC and other regulatory authorities outside the United States have imposed trading restrictions and reporting requirements on short selling, which have impacted certain of the investment strategies of the Company's investment funds and managed accounts, and continued restrictions on or further regulations of short sales could negatively impact the performance of the investment funds and managed accounts.

In addition, financial services firms are subject to numerous perceived or actual conflicts of interest, which have drawn scrutiny from the SEC and other federal and state regulators. For example, the research areas of investment banks have been and remain the subject of heightened regulatory scrutiny, which has led to increased restrictions on the interaction between equity research analysts and investment banking personnel at securities firms. While the Company maintains various policies, controls and procedures to address or limit actual or perceived conflicts and regularly seeks to review and update such policies, controls and procedures, appropriately dealing with conflicts of interest is complex and difficult, and our reputation could be damaged if it fails to do so. Such policies and procedures to address or limit actual or perceived conflicts may also result in increased costs, additional operational personnel and increased regulatory risk. Failure to adhere to these policies and procedures may result in regulatory sanctions or client litigation.

Cowen and Company, Ramius and the Company are subject to third party litigation risk and regulatory risk which could result in significant liabilities and reputational harm which, in turn, could materially adversely affect their business, results of operations and financial condition.

As an investment banking firm, Cowen and Company depends to a large extent on its reputation for integrity and high-caliber professional services to attract and retain clients. As a result, if a client is not satisfied with Cowen and Company's services, it may be more damaging in its business than in other businesses. Moreover, Cowen and Company's role as advisor to clients on important underwriting or merger and acquisition transactions involves complex analysis and the exercise of professional judgment, including rendering "fairness opinions" in connection with mergers and other transactions. Such activities may subject the Company to the risk of significant legal liabilities to clients and aggrieved third parties, including stockholders of clients who could commence litigation against Cowen

and Company and/or the Company. Although Cowen and Company's investment banking engagements

typically include broad indemnities from its clients and provisions to limit exposure to legal claims relating to such services, these provisions may not protect the Company or may not be enforceable in all cases. As a result, the Company may incur significant legal and other expenses in defending against litigation and may be required to pay substantial damages for settlements and/or adverse judgments. Substantial legal liability or significant regulatory action against the Company could have a material adverse effect on our results of operations or cause significant reputational harm, which could seriously harm our business and prospects.

In connection with Cowen Holdings' initial public offering in July 2006 (which we refer to as the Cowen Holdings' IPO), Cowen Holdings entered into an Indemnification Agreement with Société Générale (which we refer to as SG), wherein, among other things, Société GénéraleSG agreed to indemnify Cowen Holdings for all liability arising out of all known, pending or threatened litigation (including the cost of such litigation) and arbitrations and certain known regulatory matters, in each case, that existed prior to the date of Cowen Holdings' IPO. Société Générale,SG, however, will not indemnify Cowen Holdings, and Cowen Holdings will instead indemnify Société Générale,SG, for most litigation, arbitration and regulatory matters that may occur in the future but were unknown at the time of Cowen Holdings' IPO and certain known regulatory matters.

In general, the Company is exposed to risk of litigation by investors in its alternative investment management business if the management of any of its funds is alleged to constitute negligence or dishonesty. Investors could sue to recover amounts lost by the Company's funds due to any alleged misconduct, up to the entire amount of the loss. We may also be exposed to litigation by investors in the Ramius fund of funds platform for losses resulting from similar conduct at an underlying fund. Furthermore, the Company may be subject to litigation arising from investor dissatisfaction with the performance of the Ramius funds and the funds invested in by the Ramius fund of funds platform. In addition, the Company is exposed to risks of litigation or investigation relating to transactions which presented conflicts of interest that were not properly addressed. In the majority of such actions the Company would be obligated to bear legal, settlement and other costs, which may be in excess of any available insurance coverage. In addition, although the Company is indemnified by the Ramius funds, our rights to indemnification may be challenged. If the Company is required to incur all or a portion of the costs arising out of litigation or investigations as a result of inadequate insurance proceeds, if any, or fails to obtain indemnification from its funds, our business, results of operations and financial condition could be materially adversely affected. In its alternative investment management business, the Company is exposed to the risk of litigation if a fund suffer catastrophic losses due to the failure of a particular investment strategy or due to the trading activity of an employee who has violated market rules or regulations. Any litigation arising in such circumstances is likely to be protracted, expensive and surrounded by circumstances which are materially damaging to Ramius's and the Company's reputations and businesses. In addition, the Company faces the risk of litigation from investors in the Ramius funds if restrictions applicable to such funds are violated.

As a result of the Transactions, there exists the potential for conflicts of interest, and a failure to appropriately identify and deal with conflicts of interest could adversely affect our businesses.

With the combination of our alternative investment management and investment banking businesses, we will likely face an increasing potential for conflicts of interest, including situations where our services to a particular client, investor or our own interests in our investments conflict with the interests of another client. Such conflicts may also arise if our investment banking business has access to material non-public information that may not be shared with our alternative investment management business or vice versa. Additionally, our regulators have the ability to scrutinize our activities for potential conflicts of interest, including through detailed examinations of specific transactions.

We have developed and implemented procedures and controls that are designed to identify and address conflicts of interest, including those designed to prevent the improper sharing of information

among our businesses. However, appropriately identifying and dealing with conflicts of interest is complex and difficult, and the willingness of clients to enter into transactions or engagements in which such a conflict might arise may be affected if we fail to identify and deal appropriately with potential conflicts of interest. In addition, potential or perceived conflicts could give rise to litigation or enforcement actions.

Employee misconduct could harm Ramius, Cowen and Company and the Company by, among other things, impairing the Company's ability to attract and retain investors and subjecting the Company to significant legal liability, reputational harm and the loss of revenue from its own invested capital.

It is not always possible to detect and deter employee misconduct. The precautions that the Company takes to detect and prevent this activity may not be effective in all cases, and we may suffer significant reputational harm and financial loss for any misconduct by our employees. The potential harm to the Company's reputation and to our business caused by such misconduct is impossible to quantify.

There is a risk that the Company's employees or partners, or the managers of funds invested in by the Ramius fund of funds platform, could engage in misconduct that materially adversely affects the Company's business, including a decrease in returns on its own invested capital. The Company is subject to a number of obligations and standards arising from its alternative investment management business. The violation of these obligations and standards by any of the Company's employees could materially adversely affect the Company and its investors. For instance, the Company's businesses require that the Company properly deal with confidential information. If the Company's employees were improperly to use or disclose confidential information, we could suffer serious harm to our reputation, financial position and current and future business relationships. It is not always possible to detect or deter misconduct, and the extensive precautions we take to detect and prevent this activity may not be effective in all cases. If one of the Company's employees were to engage in misconduct or were to be accused of such misconduct, the business and reputation of the Company could be materially adversely affected.

Required reductions in the available credit under the Company's secured revolving loan facility may limit our ability to maintain sufficient liquidity and any additional financing that we may need may not be available on favorable terms, or at all.

Under the terms of the Company's secured revolving loan facility the amount of capital available is to be reduced to $25 million from $50 million on January 4, 2010, requiring us to reduce the outstanding balance to $25 million as of or prior to such date. The total amount outstanding as of the date hereof was approximately $43.0 million plus an outstanding letter of credit of approximately $7 million. As discussed under "Use of Proceeds", we intend to use a portion of the net proceeds of the offering to repay amounts outstanding under the secured revolving loan facility so that the remaining balance plus outstanding letters of credit will not exceed $25 million. Such reduction in our available liquidity could have a material adverse impact on our future financial position and results of operations and we may be required to obtain additional financing from other sources. There can be no assurance that we can find such financing in the amounts required or that the terms, covenants and the cost of such financing will be as favorable as those which were available under our existing secured revolving loan facility. If we are unable to obtain additional capital, we may have to change our business and capital expenditure plans, which would have a materially adverse effect on our future results of operations.

The Company may be unable to successfully identify, manage and assimilate future acquisitions, investments and strategic alliances, which could adversely affect our results of operations.

We intend to continually evaluate potential acquisitions, investments and strategic opportunities to expand our alternative investment management and investment banking businesses. In the future, we may seek additional acquisitions, investments, strategic alliances or similar arrangements, which may expose us to risks such as:

Furthermore, any future acquisitions of businesses could entail a number of risks, including:

There can be no assurance that we would successfully overcome these risks or any other problems encountered with these acquisitions, investments, strategic alliances or similar arrangements.

As a result of RCG's majority ownership interest in the Company, RCG controls matters requiring stockholder approval and its ownership could affect the liquidity in the market for our Class A common stock.

RCG's majority ownership stake in the Company gives it control over matters requiring approval by the Company's stockholders, including the election of directors and approval of significant corporate transactions. Furthermore, RCG's managing member is controlled by certain members of our senior management, including Peter A. Cohen, our Chairman and Chief Executive Officer. Corporate action may be taken even if other stockholders, including those who purchase shares in this offering, oppose such action. RCG's concentration of ownership and ability to determine the composition of the Company's board of directors may discourage a third party from proposing a change of control or other strategic transaction concerning the Company or otherwise have the effect of delaying or preventing a change of control of the Company that other stockholders may view as beneficial. As a result, the Company's Class A common stock could trade at prices that do not reflect a "control premium" to the same extent as do the stocks of similarly situated companies that do not have any single stockholder with an ownership interest as large as RCG's ownership interest.

The Company is a "controlled company" within the meaning of the NASDAQ rules and, as a result, will qualify for, and rely on, exemptions from certain corporate governance standards, which may limit the presence of independent directors on the board of directors or board committees of the Company.

RCG beneficially owns shares of the Company's capital stock which represent approximately 66%65.4% of the outstanding voting power of the Company's capital stock.stock (or approximately 51.5% after giving effect to this offering, assuming no exercise of the underwriters' over-allotment option and approximately 49.97% assuming the underwriters' over-allotment option is exercised in full). Accordingly, the Company is a majority-owned subsidiary of RCG and RCG has the ability to elect the Company's board of directors and thereby control the management and affairs of the Company. Therefore, the Company is deemed to be a "controlled company" for purposes of NASDAQ Rule 5615(c)(2). Under this rule, a company of which more than 50% of the voting power for the election of directors is held by an individual, a group or another company is a "controlled company" and is exempt from certain corporate governance requirements, including requirements that (1) a majority of the board of directors consist of independent directors, (2) compensation of officers be determined or recommended to the board of directors by a majority of its independent directors or by a compensation committee that is composed entirely of independent directors and (3) director nominees be selected or recommended for selection by a majority of the independent directors or by a nominating committee composed solely of independent directors. Accordingly, the Company's stockholders may not have the same protections afforded to stockholders of other companies that are required to fully comply with the NASDAQ rules. Solely for the purpose of including the director designated by BA Alpine Holdings, Inc. as a member of each of the compensation committee and the nominating and governance committee, the Company has elected to be treated as a "controlled company" for purposes of NASDAQ Rule 5615(c)(2). Even though the Company is treated as a "controlled company," a majority of the Company's board of directors consists of independent directors and each member of each of the compensation committee and the nominating and governance committee other than the director designated by BA Alpine Holdings, Inc. is independent. If the underwriters' over-allotment option is exercised in full, RCG will own approximately 49.97% of the outstanding voting power of the Company's capital stock and the Company would no longer be treated as a "controlled company" for purposes of NASDAQ Rule 5615(c)(2).

The market price of the Company's Class A common stock may decline in the future as a result of the Transactions.

The market price of the Company's Class A common stock may decline in the future as a result of the Transactions for a number of reasons, including:

The unaudited pro forma financial data for the Company included in this prospectus are preliminary, and the Company's actual financial position and operations may differ materially from the unaudited pro forma financial data included in this document.

The unaudited pro forma financial data for the Company in this prospectus are presented for illustrative purposes only and are not necessarily indicative of what the Company's actual financial position or operations would have been had the Transactions been completed on the dates indicated.

The Company's future results will suffer if the Company does not effectively manage its expanded operations following the Transactions.

The Company may continue to expand its operations through new product and service offerings and through additional strategic investments, acquisitions or joint ventures, some of which may involve complex technical and operational challenges. The Company's future success depends, in part, upon its ability to manage its expansion opportunities, which pose numerous risks and uncertainties, including the need to integrate new operations into its existing business in an efficient and timely manner, to combine accounting and data processing systems and management controls and to integrate

relationships with customers and business partners. In addition, future acquisitions or joint ventures may involve the issuance of additional shares of common stock of the Company, which may dilute the ownership of the Company's stockholders.

In 2008, Cowen Holdings expanded its investment banking business in China with the acquisition of Cowen Latitude Capital Group. The continued expansion of the Company's investment banking business in China may require significant resources and/or may result in significant unanticipated losses, costs or liabilities. In addition, geographic and other expansion, acquisitions or joint ventures may require significant managerial attention, which may be diverted from other operations. These capital, equity and managerial commitments may impair the operation of the Company's businesses.

BA Alpine Holdings, Inc., its designee on the Company's board of directors and RCG may have interests that conflict with your interests.

BA Alpine Holdings, Inc., its designee on the Company's board of directors and RCG may have interests that conflict with, or are different from, the Company's and your own. Conflicts of interest between BA Alpine Holdings, Inc. and/or RCG and the Company may arise, and such conflicts of interest may not be resolved in a manner favorable to the Company, including potential competitive business activities (in the case of BA Alpine Holdings, Inc.), corporate opportunities, indemnity arrangements, registration rights and sales or distributions by RCG, BA Alpine Holdings, Inc. or their respective affiliates of Class A common stock. The Company's amended and restated certificate of incorporation and by-laws do not contain any provisions designed to facilitate resolution of actual or potential conflicts of interest, or to ensure that potential business opportunities that may become available to BA Alpine Holdings, Inc. and the Company will be reserved for or made available to the Company. Pertinent provisions of law will govern any such matters if they arise. In addition, RCG, as the holder of the majority of the Company's issued and outstanding shares of Class A common stock, could delay or prevent an acquisition or merger even if such a transaction would benefit other stockholders.

The Company's failure to maintain effective internal control over financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act could have a material adverse effect on the Company's financial condition, results of operations, business and price of our Class A common stock.

The Sarbanes-Oxley Act and the related rules require our management to conduct annual assessment of the effectiveness of our internal control over financial reporting and require a report by our independent registered public accounting firm addressing our internal control over financial reporting. To comply with Section 404 of the Sarbanes-Oxley Act, we have documented formal policies, processes and practices related to financial reporting that are necessary to comply with Section 404. Such policies, processes and practices are important to ensure the identification of key financial reporting risks, assessment of their potential impact and linkage of those risks to specific areas and activities within our organization.

If we fail for any reason to comply with the requirements of Section 404 in a timely manner, our independent registered public accounting firm may issue an adverse report regarding the effectiveness

of our internal control over financial reporting. Matters impacting our internal controls may cause us to be unable to report our financial information on a timely basis and thereby subject us to adverse regulatory consequences, including sanctions by the SEC or violations of applicable stock exchange listing rules. There could also be a negative reaction in the financial markets due to a loss of investor confidence in us and the reliability of our financial statements. Any such event could adversely affect our financial condition, results of operations and business, and lead to a decline in the price of our Class A common stock.

Risks Related to the Company's Alternative Investment Management Business

Ramius's profitability and, thus, the Company's profitability may be adversely affected by decreases in revenue relating to changes in market and economic conditions.