QuickLinks-- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on February 9,May 16, 2007

Registration No. 333-________333-142653

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1 to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

ALLEGIANT TRAVEL COMPANY

(Exact name of registrant as specified in charter)

NEVADA

(State or other jurisdiction of

incorporation or organization) |

| 4512

(Primary Standard Industrial

Classification Code Number) |

| 20-4745737

(I.R.S. Employer

Identification Number) |

3301 N. Buffalo Drive, Suite B-9

Las Vegas, Nevada 89129

(702) 851-7300

(Address, including zip code, and telephone number, including

area code, of registrant's principal executive offices) |

Andrew C. Levy

Managing Director and Secretary

3301 N. Buffalo Drive, Suite B-9

Las Vegas, Nevada 89129

(702) 851-7300

(Name, address, including zip code, and telephone number,

including area code, of agent for service of process) |

With copies to: |

Robert B. Goldberg

Ellis Funk, P.C.

3490 Piedmont Road, Suite 400

Atlanta, Georgia 30305

(404) 233-2800 | | Daniel P. Raglan

Greenberg Traurig, LLP

Met Life Building

200 Park Avenue

New York, New York 10166

(212) 801-2251 | | Mark C. Smith

Skadden, Arps, Slate, Meagher & Flom LLP

Four Times Square

New York, New York 10036

(212) 735-3000 |

3301 N. Buffalo Drive, Suite B-9

Las Vegas, Nevada 89129

(702) 851-7300

(Address, including zip code, and telephone number, including

area code, of registrant’s principal executive offices)

Andrew C. Levy

Managing Director and Secretary

3301 N. Buffalo Drive, Suite B-9

Las Vegas, Nevada 89129

(702) 851-7300

(Name, address, including zip code, and telephone number,

including area code, of agent for service of process)

With copies to:

Robert B. Goldberg

Ellis Funk, P.C.

3490 Piedmont Road, Suite 400

Atlanta, Georgia 30305

(404) 233-2800

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ox

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

CALCULATION OF REGISTRATION FEE

| Title of each class of

Securities to be Registered | | | Amount to be

Registered | | Proposed Maximum

Offering Price

Per Share(1) | | Proposed Maximum

Aggregate

Offering Price(1) | | Amount of

Registration Fee | |

Common Stock, $0.001 par value | | 1,750,000 | | $ | 35.39 | _ | $ | 61,932,500 | | $ | 6,626.78 | |

| | | | | | | | | | | | | | |

|

Title of each class of

Securities to be Registered

| | Amount to be

Registered

| | Proposed Maximum

Offering Price

Per Share(1)

| | Proposed Maximum

Aggregate

Offering Price(1)

| | Amount of

Registration Fee

|

|---|

|

| Common Stock, $0.001 par value | | 5,175,000 | | $31.64 | | $163,737,000 | | $5,027(2) |

|

- (1)

Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(a)457(c) under the Securities Act of 1933, as amended, based on $35.39$31.64 per share, the average of the high and low sales prices of the Common Stock as reported on the Nasdaq Global Market on February 5,April 30, 2007.

(2)Previously paid.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective time until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. TheseThese securities may not be sold until the registration statement filed with the Securities and Exchange Commission is declared effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated February 9,May 16, 2007

P R O S P E C T U S

1,750,0003,600,000 Shares

Common Stock

This prospectus relates to shares of common stock of Allegiant Travel Company being sold by the selling stockholder described under “Principalus and Selling Stockholders”. We are not selling any shares under this prospectus. The manner in which the shares of common stock will be offered from time to time by the selling stockholder is discussedstockholders described under “Plan of Distribution”.

Investing in our common stock involves risks that are described in the “Risk Factors” section beginning on page 11 of this prospectus.

The selling stockholder"Principal and Selling Stockholders." We will not receive any underwriter, broker-dealer or agent that participates inproceeds from the sale of shares by the common stock or interests therein may be deemed “underwriters” within the meaning of Section 2(11) of the Securities Act of 1933, as amended. Any discounts, commissions, concessions, profit or other compensation any of them earns on any sale or resale of the shares, directly or indirectly, may be underwriting discounts and commissions under the Securities Act of 1933. A selling stockholder who is an “underwriter” within the meaning of Section 2(11) of the Securities Act of 1933 will be subject to the prospectus delivery requirements of the Securities Act of 1933.stockholders.

Expenses of this offer, estimated to be $50,000, other than any discounts, commissions or similar fees charged in connection with the sale of any shares of common stock offered hereby, will be borne by us.

Our common stock currently trades on the Nasdaq Global Market under the symbol “ALGT.”"ALGT." On February 5,May 15, 2007, the last reported sale price of our common stock was $35.20$27.76 per share.

Investing in our common stock involves risks that are described in the "Risk Factors" section beginning on page 10 of this prospectus.

| | Per Share

| | Total

|

|---|

| Public offering price | | $ | | $ |

| Underwriting discount | | $ | | $ |

| Proceeds, before expenses, to Allegiant | | $ | | $ |

| Proceeds, before expenses, to selling stockholders | | $ | | $ |

The underwriters may also purchase up to an additional 540,000 shares from us, at the public offering price, less the underwriting discount, within 30 days from the date of this prospectus to cover overallotments.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares will be ready for delivery on or about , 2007.

| Merrill Lynch & Co. | | |

Bear, Stearns & Co. Inc. |

|

|

Raymond James |

The date of this prospectus is , 2007.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus. We have not authorized any other person to provide you with information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not making an offer to sell those securities in any jurisdiction where the offer and sale is not permitted. The information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

i

SPECIAL NOTE ABOUT FORWARD-LOOKING STATEMENTS

We have made forward-looking statements in this prospectus, including the sections entitled “Management’s"Management's Discussion and Analysis of Financial Condition and Results of Operations”Operations" and “Business,”"Business," that are based on our management’smanagement's beliefs and assumptions and on information currently available to our management. Forward-looking statements include the information concerning our possible or assumed future results of operations, business strategies, financing plans, competitive position, industry environment, potential growth opportunities, the effects of future regulation and the effects of competition. Forward-looking statements include all statements that are not historical facts and can be identified by the use of forward-looking terminology such as the words “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate”"believe," "expect," "anticipate," "intend," "plan," "estimate" or similar expressions.

Forward-looking statements involve risks, uncertainties and assumptions. Actual results may differ materially from those expressed in the forward-looking statements. We do not have any intention or obligation to update forward-looking statements after we distribute this prospectus.

3

You should understand that many important factors, in addition to those discussed elsewhere in this prospectus, could cause our results to differ materially from those expressed in the forward-looking statements. These factors include, without limitation, increases in fuel prices, terrorist attacks, risks inherent to airlines, demand for air services to Las Vegas, Orlando and Tampa/St. Petersburg from the markets served by us, our ability to implement our growth strategy, our fixed obligations, our dependence on the Las Vegas, Orlando and Tampa/St. Petersburg markets, our ability to add, renew or replace gate leases, our competitive environment, problems with our aircraft, dependence on fixed fee customers, economic and other conditions in markets in which we operate, governmental regulation, increases in maintenance costs and insurance premiums and cyclical and seasonal fluctuations in our operating results.

ii

SUMMARY

SUMMARY

This section summarizes material information that appears later in this prospectus and is qualified in its entirety by the more detailed information and financial statements included elsewhere in this prospectus. In this prospectus, we consider Alaska Airlines, Inc., American Airlines, Inc., Continental Airlines, Inc., Delta Air Lines, Inc., Northwest Airlines, Inc., United Air Lines Inc., Trans World Airlines, Inc. (prior to its acquisition by AMR Corp.) and US Airways, Inc. (prior to 2005) as U.S. legacy carriers, and we consider AirTran Airways, Inc., America West Airlines, Inc., Frontier Airlines, Inc., JetBlue Airways Corporation, Southwest Airlines Co., and US Airways, Inc. (starting in 2005) as U.S. low-cost carriers. This summary may not contain all of the information that may be important to you. As an investor or prospective investor, you should carefully review the entire prospectus, including the risk factors and the more detailed information that appears later.

In this prospectus, we use the terms “Allegiant,” “we,” “us”"Allegiant," "we," "us" and “our”"our" to refer to Allegiant Travel Company and its subsidiaries.

Business Overview

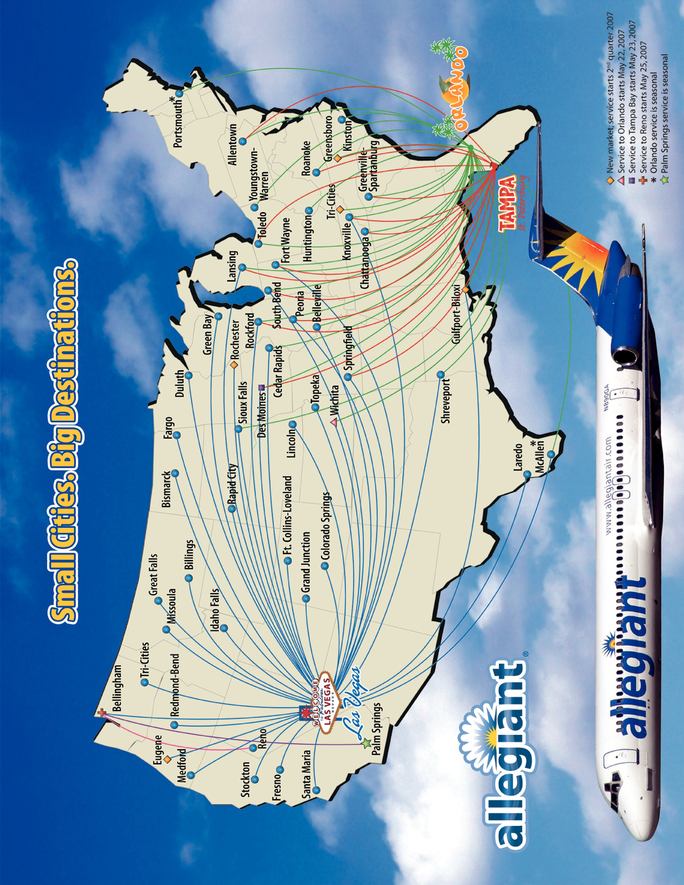

We are a leisure travel company focused on linking travelers in small cities to world-class leisure destinations such as Las Vegas, Nevada, Orlando, Florida and Tampa/St. Petersburg, Florida. We operate a low-cost passenger airline marketed to leisure travelers in small cities, allowing us to sell air travel both on a stand-alone basis and bundled with hotel rooms, rental cars and other travel related services. Our route network, pricing philosophy, advertising and diversified product offering built around relationships with premier leisure companies are all intended to appeal to leisure travelers and make it attractive for them to purchase air travel and related services from us.

Our business model provides for diversified revenue streams, which we believe distinguishes us from other U.S. airlines and other travel companies.

- •

·Scheduled service revenues currently consist of nonstop flights between our leisure destinations and our small city markets.

- •

·Fixed fee contract revenues consist largely of fixed fee flying agreements with affiliates of Harrah’sHarrah's Entertainment Inc. and Apple Vacations West, Inc. that provide for a predictable revenue stream.

- •

·Ancillary revenues are generated from the sale of hotel rooms, rental cars, advance seat assignments, in-flight products and other items sold in conjunction with our scheduled air service. We recognize our ancillary revenues on a net basis, net of amounts paid to wholesale providers, travel agent commissions and credit card processing fees.

Our business strategy has evolved as our experienced management team has taken a different approach to the traditional way business has been conducted in the airline industry. In contrast to the traditional airline strategy, we focus primarily on the leisure traveler, provide low frequency nonstop service from small cities in larger jet aircraft, sell direct to travelers, do not offer connections, do not code-share, and provide amenities at a small charge to our passengers. We have developed relationships with many premier leisure companies to generate revenue beyond just air fares. We generated $11.55 of ancillary revenue per scheduled service passenger in 2005, and $16.11 per scheduled service passenger in 2006.2006 and $18.98 per scheduled service passenger in first quarter 2007.

As of January 31,May 1, 2007, we provide scheduled air service to customers in 46 small cities (including seasonal service) and have announced service from twosix additional small cities to commence in firstbefore the end of second quarter 2007. These 4852 cities have an aggregate population of over 50 million within a 50-mile radius of the airports in those cities. We have identified at least 5248 additional cities in the United States, Canada and CanadaMexico with similar characteristics and where we do not presently have any

arrangements for service. These cities represent an estimated population of over 50 million people we could potentially serve primarily to our Las Vegas, Orlando and Tampa/St. Petersburg destinations.

Our business model has allowed us to grow rapidly and to achieve attractive rates of profitability, even during the present climate of high fuel costs. For the year ended December 31, 2006, we had revenue of $243.3 million, representing substantial growth of 83.7% over the year ended December 31, 2005, while maintaining an operating margin of 9.3% which was higher than the U.S. legacy carriers and U.S. low-cost carriers other than Southwest Airlines Co. We had operating income of $8.5 million in 2005 and $22.6 million in 2006. Our net income was $7.3 million in 2005 and, despite a $6.4 million one-time non-cash tax charge resulting from our reorganization to a C-corporation, $8.7 million in 2006. In first quarter 2007, we had revenue of $84.3 million, operating income of $14.3 million and net income of $9.7 million, reflecting significant growth over revenue of $59.6 million, operating income of $7.4 million and net income of $6.8 million in first quarter 2006.

Our Competitive Strengths

We have developed a unique business model that focuses on leisure travelers in small cities. We believe the following strengths allow us to maintain a competitive advantage in the markets we serve:

Focus on Linking Small Cities to World-Class Leisure Destinations. As of January 31,May 1, 2007, we provide nonstop low fare scheduled air service from 46 small cities (including seasonal service) primarily to the world-class leisure destinations of Las Vegas, Nevada, Orlando, Florida, and Tampa/St. Petersburg, Florida. We have announced service from twosix new small cities to commence in firstbefore the end of second quarter 2007. Frequently, when we enter a new market, we introduce nonstop service to our leisure destinations which previously did not exist. We believe this nonstop service, combined with our pricing philosophy and premier leisure company relationships, makes it attractive for leisure travelers to purchase air travel and related services from us. As a result, we believe we stimulate new traffic. By focusing on underserved small cities, we believe we avoid the overcapacity and intense competition presently seen in high traffic domestic air corridors. On 6265 of our 6670 routes as of January 31,May 1, 2007, we are the only carrier providing nonstop service. Of the 7079 routes we will be serving by the end of firstsecond quarter 2007, there are only fivenine routes with existing or announced nonstop service by other airlines.

We believe it would be difficult for potential competitors to profitably contest our market positions with nonstop service as our markets are generally too small to support either two carriers or the high frequency service provided by most U.S. legacy carriers and U.S. low-cost carriers (“LCCs”("LCCs"). In addition, leisure routes from small cities are generally too low-yielding to be a priority for most carriers. Moreover, while some of these markets may be suitable for service with regional jets,aircraft, we believe our unit costs are significantly less than the unit costs for most regional jets,aircraft, making it difficult for regional jetsaircraft to effectively compete.

Low Operating Costs. We believe low costs are essential to competitive success in the airline industry today. Our cost per available seat mile, or “CASM,”"CASM," was 6.92¢7.51¢ for first quarter 2007 and 7.69¢ and 7.41¢ for the years ended December 31, 20042006 and 2005, respectively. Our CASM for 2006 increased only 3.8% to 7.69¢over the prior year despite significantly higher fuel costs. Excluding the cost of fuel, our CASM was 4.63¢4.17¢ for first quarter 2007, 4.15¢ for the year ended December 31, 2004,2006, and 4.27¢ for the year ended December 31, 20052005. We believe our CASM for the year ended December 31, 2006 was approximately 45.6% lower than the average of the U.S. legacy carriers, and 4.15¢ for 2006.was approximately 23.9% lower than the average of the LCCs.

Our low operating costs are the result of our focus on the following factors:

- •

·Cost-Driven Schedule. We design our flight schedule to concentrate most of our aircraft each night at our leisure destinations. This concentration allows us to better utilize our personnel,

airport facilities, aircraft, spare parts inventories and other assets. As a result, we are able to reduce costs associated with maintenance, airport operations, and flight crews staying overnight away from home.

- •

·Low Aircraft Ownership Costs. We believe we properly balance low aircraft ownership costs and low operating costs to minimize our total costs. We currently operate one fleet type consisting of 26 MD80 series aircraft. Used MD80 series equipment is widely available today, and we believe the ownership costs of the used MD80s sought by us are more than 80% lower than that of comparably sized new Airbus A320 and Boeing 737 aircraft. While used MD80 aircraft are less fuel efficient than new aircraft, we believe the ownership cost advantages of the MD80 currently outweigh the operating cost savings of new equipment for our type of operation.

- •

·Highly Productive Workforce. We believe we have one of the most productive workforces in the U.S. airline industry with approximately 33.435.8 full-time equivalent employees per aircraft as of January 31,May 1, 2007, which compares to an industry range of greater than 60from 57 to more than 100 full-time equivalent employees per aircraft, based on publicly available information. Our high level of employee productivity is created by fleet commonality, fewer unproductive labor work rules, cost-driven scheduling, and the effective use of automation and part-time employees.

- •

·Simple Product. We believe offering a simple product is critical to low operating costs. As such, we do not sell connections; we do not code-share or interline with other carriers; we have a single class cabin; we do not have any frequent flyer or other loyalty programs; we do not provide any free catered items—everything on board is for sale; we do not overbook our flights; we do not provide cargo or mail services; and we do not offer other perks such as airport lounges.

- •

·Low Distribution Costs. We do not sell our product through outside sales channels and, as such, avoid the fees charged by travel web sites (such as Expedia, Orbitz or Travelocity) and the traditional global distribution systems (such as Sabre or Worldspan). Our customers can only purchase travel at our airport ticket counters or, for a fee, through our telephone reservations center or website. We actively encourage sales on our website. This is the least expensive form of distribution and accounted for 85.1%85.9% of our scheduled service revenue during 2006.2006 and 87.6% of our scheduled servicerevenue during first quarter 2007. We believe our percentage of direct website sales is among the highest in the U.S. airline industry.

Growing Ancillary Revenues. Ancillary revenues are earned in conjunction with our sale of scheduled air service and represent a significant, growing revenue stream. On a per scheduled service passenger basis, our ancillary revenues increased by 96.8% from $5.87 per scheduled service passenger in 2004, to $11.55 in 2005 and increased further to $16.11 in 2006.2006 and $18.98 in first quarter 2007. Ancillary revenue is derived from the sale of vacation packages including hotels, rental cars, show tickets, night club packages and other attractions; the sale of advance seat assignments; the sale of beverages, snacks and other products on board the aircraft; charging a fee for using our reservation center or website to purchase air travel; the collection of checked bag and overweight bag charges; and several other revenue streams. The largest component of our ancillary revenue is from the sale of hotel rooms packaged with air travel. As of January 31,May 1, 2007, we have agreements with 3840 hotels in Las Vegas, including hotels managed by MGM MIRAGE, Harrah’sHarrah's Entertainment Inc., Boyd’sBoyd's Gaming Corp., Wynn Resorts, Limited, and Las Vegas Sands Corp., 1819 hotels in Orlando (plus 17 additional hotels in nearby Daytona Beach, Florida), 10 and 11 hotels in Tampa/St. PetersburgPetersburg. We have also recently begun to sell rooms at four hotels in Gulfport-Biloxi serving passengers from Florida and eightseven hotels in Palm Springs, California.Reno

serving passengers from Bellingham. During 2006, we generated revenue from the sale of more than 344,000 hotel room nights.

Strong Financial Position. We have a strong financial position with significant cash balances. As of DecemberMarch 31, 2006,2007, we had $136.1$175.3 million (unaudited) of cash and cash equivalents, and short-term investments, total debt of $72.8$68.5 million (unaudited) and a debt to total capitalization ratio of 32.2%29.5%. We also have a history of growing profitably, having generated net income in 1314 of the last 1617 quarters. We believe our strong financial

position allows us to have greater financial flexibility to grow the business and weather sudden industry disruptions.

Proven Management Team and Financial Sponsors.Team. We have a strong management team comprised of experienced and motivated individuals. Our management team is led by Maurice J. Gallagher, Jr., who has an extensive background in the airline industry. Mr. Gallagher was the president of WestAir Holdings, Inc. and built WestAir into one of the largest regional airlines in the U.S., prior to its sale in 1992 to Mesa Air Group. He was also one of the founders of ValuJet, Inc., known today as AirTran Holdings, Inc., which we believe was one of the most successful start-ups of a low-cost carrier in industry history. Three of our other executive officers are former managers of ValuJet or WestAir. Our pre-public offering investorsdirectors also have significant experience in the airline industry and were intimately involved in several airline successes. These include Robert L. Priddy, a founder and former chairman and chief executive officer of ValuJet, Inc. and Declan F. Ryan, a co-founder and former chief executive officer of Ryanair, the successful European low-cost carrier.

Our Business Strategy

To continue the growth of our business and increase our profitability, our strategy will be to continue to offer a single class of air travel service at low fares, while maintaining high quality standards, keeping our operating costs low and pursuing ways to make our operations more efficient. We intend to grow by adding flights on existing routes, entering additional small cities, expanding our relationships with premier leisure companies, and providing service to more world-class leisure destinations.

The following are the key elements of our strategy:

Capitalize on Significant Growth Opportunities in Linking Small Cities to Leisure Destinations. We believe small cities represent a large untapped market, especially for leisure travel. We believe small city travelers have limited options to world-class leisure destinations as existing carriers are generally focused on connecting small city “spokes”"spokes" to their business hubs. We aim to become the premier travel brand for leisure travelers in small cities. We have identified at least 5248 additional small cities in the U.S. and Canada where we could potentially offer our low fare nonstop service to Las Vegas, Orlando or Tampa/St. Petersburg. We also believe there are several other world-class leisure destinations we could serve that share many of the same characteristics as Las Vegas, Orlando and Tampa/St. Petersburg. These potential markets include several popular vacation destinations in the U.S., Mexico and the Caribbean.

Develop New Sources of Revenue. We have identified three key areas where we believe we can grow our ancillary revenues:

- •

·Unbundling the Traditional Airline Product. We believe most leisure travelers are concerned primarily with purchasing air travel for the least expensive price and do not value many of the amenities provided by most other airlines for free. As such, we have created new sources of revenue by charging fees for services most U.S. airlines currently bundle in their product offering. We believe by offering a simple base product at an attractive low fare we can drive demand and generate incremental revenue as customers pay additional amounts for conveniences they value. We aim to continue to create new revenue sources by further unbundling our product.

- •

·Expand and Add Partnerships with Premier Leisure Companies.We currently work with many premier leisure companies in Las Vegas, Orlando and Tampa/St. Petersburg that provide ancillary products and services we sell to our customers. By expanding our existing relationships and seeking additional partnerships with premier leisure

companies, we believe we can increase the number of products and services offered to our customers and generate more ancillary revenue.

- •

·Leverage Direct Relationships With Our Customers. Since approximately 85%85.9% of our scheduled service revenue iswas purchased directly through our website in 2006, we are able to establish direct relationships with our customers by capturing their email addresses for our database. This information provides us multiple opportunities to market products and services, including: at the time they purchase their travel, between the time they purchase and initiate their travel, and after they have completed their travel. In addition, we market products and services to our customers during the flight. We believe the breadth of options we can offer them allows us to provide a “one-stop”"one-stop" shopping solution.

Continue to Reduce Our Operating Costs. We intend to continue to focus on lowering our costs to remain one of the lowest cost airlines in the world, which we believe is instrumental to increasing profitability. We will drive operational efficiency and lower costs principally by growing our network. We will expand our network by increasing the frequency of our flights in existing markets, expanding the number of small cities we serve, and serving additional world-class leisure destinations, all of which permits us to increase the utilization of our employees and assets, spreading our fixed costs over a larger number of available seat miles. In 2005, we averaged 184.7 block hours per aircraft per month while during 2006, we averaged 202.5 block hours per aircraft per month.

Minimize Fixed Costs to Increase Strategic Flexibility. We believe our low aircraft ownership costs and the lower fixed costs associated with our small city market strategy provide us with a lower level of fixed costs than other U.S. airlines. We believe minimizing our level of fixed costs will provide us with added flexibility in scheduling our services and controlling our profitability. For example, with lower fixed costs we are better able to enter or exit markets as well as match the size and utilization of our fleet to limit unprofitable flying and maximize profitability. We match our frequency with the market demand on a daily and seasonal basis.

Recent Developments

On December 1, 2006, we purchased three MD83 aircraft with seller financing. The aircraft were previously operated by us under operating leases. The purchase price was paid with cash and $16.5 million notes payable to the seller. The notes bear interest at 8.5% and are payable in monthly installments through 2011.

On December 4, 2006, the National Mediation Board reported the vote by our flight attendants. The flight attendants rejected the proposal to be represented by a union.

On December 13, 2006, we completed the initial public offering of our common stock. We issued 5,750,000 shares at $18.00 per share resulting in net proceeds to us of approximately $94.5 million.

On December 21, 2006, we took delivery of two MD80 series aircraft under short term lease agreements. The leases provide for an 18 month term.

On January 30, 2007, we announced unaudited earnings for 2006. For 2006, we reported $243.3 million of revenues, $22.6 million of operating income, $15.8 million of income before taxes and $8.7 million of net income or $0.52 per fully diluted share. For the quarter ended December 31, 2006, we reported $63.1 million of revenue, $7.4 million of operating income, $5.5 million of income before taxes and a net loss of $1.5 million or $0.17 per share.

In January 2007, we purchased two aircraft previously under operating leases. The purchase price was paid in cash.

Our principal executive offices are located at 3301 N. Buffalo Drive, Suite B-9 Las Vegas, Nevada 89129. Our telephone number is (702) 851-7300. Our website’swebsite's address is http://www.allegiantair.com. We have not incorporated by reference into this prospectus the information on our website and you should not consider it to be a part of this document. Our website address is included in this document for reference only.

Allegiant Travel Company, Allegiant Air and Allegiant Vacations are service marks of Allegiant Travel Company in the U.S. This prospectus also contains trademarks and tradenames of other companies.

In May 2005, we completed a private placement under which ComVest Allegiant Holdings, Inc., Viva Air Limited and Timothy P. Flynn invested $34.5 million in preferred shares of our limited liability company predecessor. Simultaneously, Maurice J. Gallagher, Jr., our chief executive officer, converted $5.0 million of debt owed to him into preferred shares. All of our current directors were selected by these shareholders. The representation of these shareholders on our board of directors and the ownership by these shareholders of more than 48% of our stock will allow these shareholders to exert significant control over our business in the future.

We previously conducted our business through a limited liability company, Allegiant Travel Company, LLC, and its consolidated subsidiaries. Immediately prior to the closing of our initial public offering, we completed a merger under which we succeeded to the business of Allegiant Travel Company, LLC and its consolidated subsidiaries. For further details on these transactions, see “Company History and Reorganization”.

The Offering

Common stock offered by us | None

| 155,714 shares |

Common stock offered by selling stockholders

| 1,750,000

|

3,444,286 shares |

Shares outstanding before and after the offering

| 19,795,933

|

20,034,407 shares |

Use of proceeds

|

|

We are not selling any shares of common stock underintend to use the net proceeds from this prospectus andoffering for general corporate purposes. |

|

|

We will not receive any of the proceeds from the sale of common stock by the selling stockholders. |

Risk Factors

|

|

See “Risk Factors”"Risk Factors" and other information included in this prospectus for a discussion of factors you should carefully consider before deciding to invest in shares of our common stock. |

Nasdaq Global Market Symbol

| “ALGT”

|

"ALGT" |

The number of shares outstanding before and after this offering:

·

- •

- excludes

414,000326,500 shares of common stock reserved for issuance upon exercise of outstanding stock options at a weighted average exercise price of $4.66$4.97 per share; and·

- •

- excludes 162,500 shares of common stock subject to issuance upon exercise of outstanding warrants at an exercise price of $4.40 per

share;share.

Certain Unless we specifically state otherwise, the information in this prospectus does not reflect the sale of our existing stockholders sold 1,750,000 shares of our common stockup to PAR Investment Partners, L.P. (“PAR”) on December 13, 2006, simultaneously with the closing of our initial public offering. We agreed to register the shares purchased by PAR for resale. This prospectus relates to shares of our common stock being offered solely by PAR. The manner in which the540,000 shares of common stock will be offeredwhich the underwriters have the option to purchase from timeus upon exercise of the underwriters' overallotment option.

SUMMARY FINANCIAL AND OPERATING DATA

The following financial information for each of the five years ended December 31, 2006 and for the quarters ended March 31, 2007 and 2006, has been derived from our consolidated financial statements. You should read the selected consolidated financial data set forth below along with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes.

| | For the year ended December 31,

| | For the three months ended March 31,

| |

|---|

| | 2006

| | 2005

| | 2004

| | 2003

| | 2002

| | 2007

| | 2006

| |

|---|

| |

| |

| |

| |

| | (unaudited)

| | (unaudited)

| | (unaudited)

| |

|---|

| | (in thousands, except per share data)

| |

|---|

| STATEMENT OF OPERATIONS DATA: | | | | | | | | | | | | | | | |

| Operating revenue: | | | | | | | | | | | | | | | |

| | Scheduled service revenues | | $178,349 | | $90,664 | | $46,236 | | $22,515 | | $6,007 | | $58,231 | | $42,693 | |

| | Fixed fee contract revenues | | 33,743 | | 30,642 | | 40,987 | | 26,569 | | 16,081 | | 13,348 | | 11,286 | |

| | Ancillary revenues | | 31,258 | | 11,194 | | 3,142 | | 886 | | 89 | | 12,770 | | 5,655 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| | | 243,350 | | 132,500 | | 90,365 | | 49,970 | | 22,177 | | 84,349 | | 59,634 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| Operating expenses: | | | | | | | | | | | | | | | |

| | Aircraft fuel | | 101,561 | | 52,568 | | 27,914 | | 11,755 | | 4,761 | | 31,179 | | 24,367 | |

| | Salary and benefits | | 34,950 | | 21,718 | | 15,379 | | 8,176 | | 4,320 | | 11,324 | | 7,653 | |

| | Station operations | | 24,866 | | 14,090 | | 13,608 | | 8,042 | | 2,852 | | 8,635 | | 6,180 | |

| | Maintenance and repairs | | 19,482 | | 9,022 | | 9,367 | | 6,136 | | 2,589 | | 6,527 | | 3,701 | |

| | Sales and marketing | | 9,293 | | 5,625 | | 3,548 | | 2,385 | | 632 | | 3,032 | | 2,429 | |

| | Aircraft lease rentals | | 5,102 | | 4,987 | | 3,847 | | 3,137 | | 3,033 | | 651 | | 1,629 | |

| | Depreciation and amortization | | 10,584 | | 5,088 | | 2,183 | | 1,181 | | 260 | | 3,660 | | 2,226 | |

| | Other | | 14,959 | | 10,901 | | 8,441 | | 6,258 | | 4,661 | | 5,040 | | 4,030 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| Total operating expenses | | 220,797 | | 123,999 | | 84,287 | | 47,070 | | 23,108 | | 70,048 | | 52,215 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| Operating income (loss) | | 22,553 | | 8,501 | | 6,078 | | 2,900 | | (931 | ) | 14,301 | | 7,419 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| Other (income) expense: | | | | | | | | | | | | | | | |

| | (Gain)/loss on fuel derivatives, net | | 4,193 | | (612 | ) | (4,438 | ) | (314 | ) | — | | (1,524 | ) | (268 | ) |

| | Gain from joint venture | | — | | — | | — | | — | | — | | (67 | ) | — | |

| | Other (income) expense, net | | — | | — | | — | | (913 | ) | (9 | ) | 63 | | — | |

| | Interest income | | (2,973 | ) | (1,225 | ) | (30 | ) | (9 | ) | — | | (1,884 | ) | (552 | ) |

| | Interest expense | | 5,517 | | 3,009 | | 1,399 | | 831 | | 367 | | 1,408 | | 1,405 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| Total other (income) expense | | 6,737 | | 1,172 | | (3,069 | ) | (405 | ) | 358 | | (2,004 | ) | 585 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| Income (loss) before income taxes | | 15,816 | | 7,329 | | 9,147 | | 3,305 | | (1,289 | ) | 16,305 | | 6,834 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| Provision for income taxes | | 7,076 | | 37 | | 12 | | 1 | | 1 | | 6,558 | | 1 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| Net income (loss) | | $8,740 | | $7,292 | | $9,135 | | $3,304 | | $(1,290 | ) | $9,747 | | $6,833 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| Earnings (loss) per share: | | | | | | | | | | | | | | | |

| | Basic | | $1.23 | | $1.11 | | $1.36 | | $0.49 | | $(0.14 | ) | $0.49 | | $1.06 | |

| | Diluted(1) | | $0.52 | | $0.56 | | $1.36 | | $0.49 | | $(0.14 | ) | $0.48 | | $0.41 | |

- (1)

- The number of weighted average diluted shares outstanding for purposes of calculating 2005 earnings per share includes our redeemable convertible preferred shares as if converted on a one-for-one basis into common shares. The dilutive effect of common stock subject to

timeoutstanding options and warrants to purchase shares of common stock for 2005 is not material.

| OTHER FINANCIAL DATA: | | | | | | | | | | | | | | | |

| Operating margin | | $22,553 | | $8,501 | | $6,078 | | $2,900 | | $(931 | ) | $14,301 | | $7,419 | |

| Operating margin % | | 9.3 | % | 6.4 | % | 6.7 | % | 5.8 | % | (4.2 | )% | 17.0 | % | 12.4 | % |

| EBITDA (unaudited) | | $28,944 | | $14,201 | | $12,699 | | $5,308 | | $(662 | ) | $19,489 | | $9,913 | |

Net cash provided by (used in): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| | Operating activities | | $34,746 | | $44,027 | | $10,484 | | $4,172 | | $1,686 | | $53,384 | | $34,895 | |

| | Investing activities | | (1,607 | ) | (47,706 | ) | (9,675 | ) | (7,380 | ) | (1,844 | ) | (3,996 | ) | (32,260 | ) |

| | Financing activities | | 75,875 | | 23,369 | | 480 | | 3,380 | | 201 | | (4,322 | ) | (2,135 | ) |

| | As of December 31,

| | As of

March 31,

|

|---|

| | 2006

| | 2005

| | 2004

| | 2003

| | 2002

| | 2007

| | 2006

|

|---|

| |

| |

| |

| |

| | (unaudited)

| | (unaudited)

| | (unaudited)

|

|---|

| | (in thousands, except per share data)

|

|---|

| BALANCE SHEET DATA: | | | | | | | | | | | | | | |

| Cash, cash equivalents and short-term investments | | $136,081 | | $53,325 | | $1,569 | | $280 | | $108 | | $175,339 | | $75,046 |

| Total assets | | 305,726 | | 170,083 | | 65,474 | | 32,689 | | 5,840 | | 354,430 | | 197,992 |

| Long term debt (including capital leases) | | 72,765 | | 59,747 | | 31,992 | | 18,981 | | 3,915 | | 68,467 | | 57,614 |

| Redeemable convertible preferred shares | | — | | 39,540 | | — | | — | | — | | — | | 39,540 |

| Shareholders'/members' equity (deficit) | | 153,471 | | 14,607 | | 9,493 | | 355 | | (2,951 | ) | 163,445 | | 21,850 |

| | For the year ended December 31,

| | For the three months ended March 31,

| |

|---|

| | 2006

| | 2005

| | 2004

| | 2003

| | 2002

| | 2007

| | 2006

| |

|---|

| |

| |

| |

| |

| | (unaudited)

| | (unaudited)

| | (unaudited)

| |

|---|

| Operation statistics (unaudited): | | | | | | | | | | | | | | | |

| Total system statistics: | | | | | | | | | | | | | | | |

| Passengers | | 2,179,367 | | 1,199,547 | | 840,939 | | 472,078 | | 200,872 | | 753,239 | | 521,324 | |

| Revenue passenger miles (RPMs) (thousands) | | 2,251,341 | | 1,295,633 | | 914,897 | | 436,740 | | 149,158 | | 749,237 | | 583,525 | |

| Available seat miles (ASMs) (thousands) | | 2,871,071 | | 1,674,376 | | 1,218,560 | | 614,280 | | 222,216 | | 932,530 | | 736,628 | |

| Load factor | | 78.4 | % | 77.4 | % | 75.1 | % | 71.1 | % | 67.1 | % | 80.3 | % | 79.2 | % |

| Operating revenue per ASM (cents) | | 8.48 | | 7.91 | | 7.42 | | 8.13 | | 9.98 | | 9.05 | | 8.10 | |

| Operating expense per ASM (cents) | | 7.69 | | 7.41 | | 6.92 | | 7.66 | | 10.40 | | 7.51 | | 7.09 | |

| Operating expense per ASM, excluding fuel (cents) | | 4.15 | | 4.27 | | 4.63 | | 5.75 | | 8.26 | | 4.17 | | 3.78 | |

| Departures | | 20,074 | | 11,646 | | 8,369 | | 5,307 | | 3,308 | | 6,767 | | 4,740 | |

| Block hours | | 50,584 | | 29,472 | | 20,784 | | 11,160 | | 5,486 | | 16,560 | | 12,863 | |

| Average stage length (miles) | | 966 | | 977 | | 948 | | — | | — | | 930 | | 1,048 | |

| Average number of operating aircraft during period | | 20.8 | | 13.3 | | 8.0 | | 4.8 | | 2.8 | | 25.9 | | 19.3 | |

| Total aircraft in service end of period | | 24 | | 17 | | 9 | | 7 | | 3 | | 26 | | 21 | |

| Full-time equivalent employees at period end | | 846 | | 596 | | 391 | | 282 | | 107 | | 915 | | 677 | |

| Fuel gallons consumed (thousands) | | 47,984 | | 28,172 | | 19,789 | | 10,490 | | 4,548 | | 15,848 | | 12,282 | |

| Average fuel cost per gallon | | $2.12 | | $1.87 | | $1.41 | | $1.12 | | $1.05 | | $1.97 | | $1.98 | |

Scheduled service statistics: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Passengers | | 1,940,456 | | 969,393 | | 535,602 | | 260,850 | | 83,779 | | 672,840 | | 453,479 | |

| Revenue passenger miles (RPMs) (thousands) | | 1,996,559 | | 1,029,625 | | 517,301 | | 202,997 | | 33,687 | | 641,479 | | 496,073 | |

| Available seat miles (ASMs) (thousands) | | 2,474,285 | | 1,294,064 | | 694,949 | | 274,036 | | 57,566 | | 777,141 | | 607,552 | |

| Load factor | | 80.7 | % | 79.6 | % | 74.4 | % | 74.1 | % | 58.5 | % | 82.5 | % | 81.7 | % |

| Departures | | 16,634 | | 8,388 | | 4,803 | | 2,553 | | 1,433 | | 5,674 | | 3,814 | |

| Block hours | | 43,391 | | 22,465 | | 11,827 | | 5,141 | | 1,897 | | 13,847 | | 10,583 | |

| Yield (cents) | | 8.93 | | 8.81 | | 8.94 | | 11.09 | | 17.83 | | 9.08 | | 8.61 | |

| Scheduled service revenue per ASM (cents) | | 7.21 | | 7.01 | | 6.65 | | 8.22 | | 10.43 | | 7.49 | | 7.03 | |

| Ancillary revenue per ASM (cents) | | 1.26 | | 0.87 | | 0.45 | | 0.32 | | 0.15 | | 1.64 | | 0.93 | |

| Total revenue per ASM (cents) | | 8.47 | | 7.87 | | 7.11 | | 8.54 | | 10.59 | | 9.14 | | 7.96 | |

| Average fare—scheduled service | | $91.91 | | $93.53 | | $86.33 | | $86.31 | | $71.70 | | $86.55 | | $94.15 | |

| Average fare—ancillary | | $16.11 | | $11.55 | | $5.87 | | $3.40 | | $1.06 | | $18.98 | | $12.47 | |

| Average fare—total | | $108.02 | | $105.07 | | $92.19 | | $89.71 | | $72.76 | | $105.52 | | $106.61 | |

| Average state length (miles) | | 1,006 | | 1,045 | | 913 | | 725 | | 403 | | 926 | | 1,075 | |

| Percent of sales through website during period | | 85.9 | % | 81.0 | % | 68.4 | % | 53.2 | % | — | | 87.6 | % | 84.7 | % |

The following terms used in this section and elsewhere in this prospectus have the meanings indicated below:

"Available seat miles" or "ASMs" represents the number of seats available for passengers multiplied by the selling stockholdersnumber of miles the seats are flown.

"Average fuel cost per gallon" represents total aircraft fuel costs divided by the total number of fuel gallons consumed.

"Average stage length" represents the average number of miles flown per flight.

"EBITDA" represents earnings before interest expense, income taxes, depreciation, and amortization. EBITDA is discussed under “Plannot a calculation based on generally accepted accounting principles and should not be considered as an alternative to net income (loss) or operating income (loss) as indicators of Distribution.”our financial performance or to cash flow as a measure of liquidity. In addition, our calculation may not be comparable to other similarly titled measures of other companies. EBITDA is included as a supplemental disclosure because we believe it is a useful indicator of our operating performance. Further, EBITDA is a well recognized performance measurement in the airline industry that is frequently used by securities analysts, investors and other interested parties in comparing the operating performance of companies in our industry. We believe EBITDA is useful in evaluating our operating performance compared to our competitors because its calculation generally eliminates the effects of financing and income taxes and the accounting effects of capital spending and acquisitions, which items may vary between periods and for different companies for reasons unrelated to overall operating performance. The following represents the reconciliation of EBITDA to net income (loss) for the periods indicated below.

| | Year ended December 31,

| | Three months ended March 31,

| |

|---|

| | 2006

| | 2005

| | 2004

| | 2003

| | 2002

| | 2007

| | 2006

| |

|---|

| | (unaudited)

| |

| |

| |

|---|

| | (in thousands, except share and per share data)

| |

|---|

| EBITDA Reconciliation: | | | | | | | | | | | | | | | |

| Net income (loss) | | $8,740 | | $7,292 | | $9,135 | | $3,304 | | $(1,290 | ) | $9,747 | | $6,833 | |

| Plus (minus): | | | | | | | | | | | | | | | |

| Interest income | | (2,973 | ) | (1,225 | ) | (30 | ) | (9 | ) | — | | (1,884 | ) | (552 | ) |

| Interest expense | | 5,517 | | 3,009 | | 1,399 | | 831 | | 367 | | 1,408 | | 1,405 | |

| Provision for income taxes | | 7,076 | | 37 | | 12 | | 1 | | 1 | | 6,558 | | 1 | |

| Depreciation and amortization | | 10,584 | | 5,088 | | 2,183 | | 1,181 | | 260 | | 3,660 | | 2,226 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| EBITDA | | $28,944 | | $14,201 | | $12,699 | | $5,308 | | $(662 | ) | $19,489 | | $9,913 | |

| | |

| |

| |

| |

| |

| |

| |

| |

Aircraft lease rentals expense represents a significant operating expense of our business. Because we leased aircraft during the periods presented, we believe that when assessing EBITDA you should also consider the impact of our aircraft lease rentals expense, which was (in thousands) $5,102 in 2006, $4,987 in 2005, $3,847 in 2004, $3,137 in 2003 and $3,033 in 2002, $651 in first quarter 2007, and $1,629 in first quarter 2006.

"Load factor" represents the percentage of aircraft seating capacity that is actually utilized (revenue passenger miles divided by available seat miles).

"Operating expense per ASM" represents operating expenses divided by available seat miles.

"Operating expense per ASM, excluding fuel" represents operating expenses, less aircraft fuel, divided by available seat miles. This statistic provides management and investors the ability to measure and monitor our cost performance absent fuel price volatility. Both the cost and availability of fuel are subject to many economic and political factors and therefore are beyond our control.

"Operating revenue per ASM" represents operating revenue divided by available seat miles.

"Revenue passengers" represents the total number of passengers flown on all flight segments.

"Revenue passenger miles" or"RPMs" represents the number of miles flown by revenue passengers.

"Yield" represents scheduled service revenue divided by scheduled service revenue passenger miles.

RISK FACTORS

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below before making an investment decision. The risks described below are not the only ones facing our company. Additional risks not presently known to us or that we currently deem immaterial may also impair our business and operations. Our business, financial condition or results of operations could be materially and adversely affected by any of these risks. The trading price of our common stock could decline due to any of these risks, and you may lose all or part of your investment.

Risks Related to Allegiant

Increases in fuel prices or unavailability of fuel would harm our business and profitability.

Fuel costs constitute a significant portion of our total operating expenses (46.0% during 2006). Significant increases in fuel costs would harm our financial condition and results of operations.

Our MD80 series aircraft are less fuel efficient than new aircraft. An increase in the price of aircraft fuel would therefore result in a disproportionately higher increase in our average total costs than our competitors using more fuel efficient aircraft.

Historically, fuel costs have been subject to wide price fluctuations. Aircraft fuel availability is also subject to periods of market surplus and shortage and is affected by demand for heating oil, gasoline and other petroleum products. Because of the effect of these events on the price and availability of aircraft fuel, the cost and future availability of fuel cannot be predicted with any degree of certainty. A fuel supply shortage or higher fuel prices could result in the curtailment of our service. Some of our competitors may be better positioned to obtain fuel in the event of a shortage. We cannot assure you increases in the price of fuel can be offset by higher revenue.

In addition, although we implemented a fuel derivatives program in 2003 to partially protect against fuel price volatility, our hedging program does not protect us against ordinary course price increases and is limited in fuel volume and duration. We cannot assure you our fuel hedging program is sufficient to protect us against increases in the price of fuel.

We carry limited fuel inventory and we rely heavily on our fuel suppliers. We cannot assure you we will always have access to adequate supplies of fuel in the event of shortages or other disruptions in the fuel supply. We were recently notified by our fuel supplier in Las Vegas that they will be limiting fuel purchases of all airlines supplied by them in that market. This will result in a reduction of our fuel supply by approximately 21% of our usage at this time. We do not know how long this restriction will last or whether further cuts may be imposed at a later time. During the period of this restriction, we will seek to reduce its effect on our operations by various means, but the restriction could result in a higher fuel cost to service our Las Vegas market or restrict our ability to grow our Las Vegas operations if the restriction continues for an extended period of time.

If our credit card processing company were to require significant holdbacks for processing credit card transactions for the purchase of air travel and other services, our cash flow would be adversely affected.

Credit card companies frequently require significant holdbacks when future air travel and other future services are purchased through credit card transactions. We rely on a single credit card processing company at this time, and our agreement is terminable on 30 days notice. As virtually all of our scheduled service and ancillary revenue is paid with credit cards and our credit card processing agreement does not require a significant holdback, our cash flow would suffer in the event the terms of our current agreement were changed or terminated. Although we believe that we would be able to secure a replacement credit

card processing agreement if our current agreement is terminated, the terms of any new agreement may not be as favorable to us. These cash flow issues could be

exacerbated during periods of rapid growth as we would be incurring additional costs associated with our growth, but our receipt of these revenues would be delayed.

Our failure to successfully implement our growth strategy and generate demand for our services could harm our business.

Successfully implementing our growth strategy is critical for our business to achieve economies of scale and to sustain or increase our profitability. Increasing the number of small city markets we serve depends on our ability to identify and effectively evaluate new target markets and then access suitable airports located in these markets in a manner consistent with our cost strategy.

Most of our scheduled air service is sold to customers traveling from our small city markets to our leisure destinations of Las Vegas, Orlando or Tampa/St. Petersburg. While we seek to generate demand for our services in these markets, the smaller size of these markets makes it more difficult to create this demand. If we are unable to do so in a particular market, our revenues could be negatively affected and our ability to grow could be constrained. Under those circumstances, we may decide to reduce or terminate service to that market, which could result in additional costs.

We will also need to obtain additional gates in Las Vegas, Orlando and Tampa/St. Petersburg, and obtain access to markets we seek to serve in the future. Any condition that would deny, limit or delay our access to airports we seek to serve in the future would constrain our ability to grow. Opening new markets may require us to commit a substantial amount of resources, even before the new services commence, including additional skilled personnel, equipment and facilities. An inability to hire and retain skilled personnel or to secure the required equipment and facilities efficiently and cost-effectively may affect our ability to implement our growth strategy. We cannot assure you we will be able to successfully establish new markets and our failure to do so could harm our business.

We have recently commenced service from 12 small cities to In November 2006, we added Tampa/St. Petersburg.Petersburg as a new leisure destination. As we do not have any significant historical data on the performance of Tampa/St. Petersburg as one of our leisure destinations, we may not be able to profitably operate these routes.routes on a year-round basis.

We expect to serve other leisure destinations, in addition to Las Vegas, Orlando and Tampa/St. Petersburg, which we believe are attractive to small city markets. However, if we fail to successfully implement service to additional leisure destinations, our growth prospects will be limited and our profitability could be adversely impacted.

Expansion of our markets and services may also strain our existing management resources and operational, financial and management information systems to the point they may no longer be adequate to support our operations, requiring us to make significant expenditures in these areas. We expect we will need to develop further financial, operational and management controls, reporting systems and procedures to accommodate future growth. We cannot assure you we will be able to develop these controls, systems or procedures on a timely basis and the failure to do so could harm our business.

Additionally, we are subject to regulation by the Federal Aviation Administration (“FAA”("FAA") and must receive its approval to add aircraft to our operating certificate. If the FAA does not grant us approval

to add aircraft to our fleet as quickly as we desire, our growth may be limited and our profitability could be adversely impacted.

Any inability to acquire and maintain additional compatible aircraft, engines or parts on favorable terms or at all would increase our operating costs and could harm our profitability.

Our fleet currently consists of MD80 series aircraft equipped with Pratt & Whitney JT8D-200 series engines. Although our management believes there is currently an adequate supply of suitable MD80 series aircraft available at favorable prices and terms, we are unable to predict how long these conditions will continue. Any increase in demand for the MD80 aircraft or the Pratt & Whitney

JT8D-200 series engine could restrict our ability to obtain additional MD80 aircraft, engines and spare parts. Because the aircraft and the engine are no longer being manufactured, we may be unable to obtain additional suitable aircraft, engines or spare parts on satisfactory terms or at the time needed for our operations or for our implementation of our growth plan.

In April 2006, the FAA indicated it intends to issue regulations limiting the age of aircraft that may be flown in the U.S. The announcement did not indicate the maximum age that would be allowed, the effective date of the regulation or any grandfathering provisions. These regulations, if and when implemented, may have a material effect on our future operations.

We cannot assure you we will be able to purchase additional MD80s on favorable terms, or at all. Instead, we may be required to lease MD80s from current owners. Because, in our experience, the cost of leasing generally exceeds the ownership costs associated with the purchase of the MD80, our operating costs would increase if we are required to lease, instead of purchase, additional MD80 aircraft, and this could harm our profitability.

If the available MD80 series aircraft, whether by purchase or lease, are not compatible with the rest of our fleet in terms of takeoff weight, avionics, engine type or other factors, the costs of operating and maintaining our fleet would likely increase. Similarly, our aircraft ownership costs will likely increase if we decide to acquire aircraft which are not MD80 series aircraft.

There is also a greater risk with acquiring used aircraft because we may incur additional costs to remedy any mechanical issues not found in our inspection and acceptance process and, generally, the cost to maintain used aircraft exceeds the cost to maintain new aircraft.

Any inability to obtain financing for additional aircraft could harm our growth plan.

We typically finance our aircraft through either mortgage debt or lease financing. Although we believe debt and/or lease financing will be available for the aircraft we will acquire, we cannot assure you we will be able to secure such financing on terms attractive to us or at all. To the extent we cannot secure such financing on acceptable terms or at all, we may be required to modify our aircraft acquisition plans, incur higher than anticipated financing costs or use more of our cash balances for aircraft acquisitions than we currently expect.

Aircraft lenders often require that they receive the benefit of Section 1110 protection under the U.S. Bankruptcy Code. It is more difficult to provide lenders Section 1110 protection for aircraft manufactured before 1994. Most MD80s, and almost all of our MD80s, were manufactured before 1994. As a result, we may face difficulty obtaining financing for aircraft transactions.

13

Our maintenance costs will increase as our fleet ages.

Our aircraft range from 1011 to 2021 years old, with an average age of 1617 years. Our aircraft are significantly older than the U.S. industry average. In general, the cost to maintain aircraft increases as they age and exceeds the cost to maintain new aircraft. FAA regulations require additional maintenance inspections for older aircraft. For example, a repair assessment program must be implemented for each of our aircraft once they reach 60,000 cycles. A cycle is defined as one take-off and landing. The average cycles on our fleet is approximately 25,50026,000 cycles and the highest number of cycles on any of our aircraft is approximately 43,500. Based on our current and expected aircraft utilization rates of approximately 1,000 cycles per year, we will not have to comply with the repair assessment program for several years. We will also need to comply with other programs which require enhanced inspections of aircraft including Aging Aircraft Airworthiness Directives, which typically increase as an aircraft ages and vary by aircraft or engine type depending on the unique characteristics of each aircraft and/or engine.

In addition, we may be required to comply with any future aging aircraft issues, law changes, regulations or airworthiness directives. We cannot assure you our maintenance costs will not exceed our expectations.

We believe our aircraft are and will be mechanically reliable based on the percentage of scheduled flights completed. We cannot assure you our aircraft will continue to be sufficiently reliable over longer periods of time. Furthermore, given the age of our fleet, any public perception that our aircraft are less than completely reliable could have an adverse effect on our profitability.

We may be subject to unionization, work stoppages, slowdowns or increased labor costs.

Unlike most airlines, we have a non-union workforce. If our employees unionize, it could result in demands that may increase our operating expenses and adversely affect our profitability. Our pilots have formed an in-house pilot association. Our flight attendants are in the process of also forming an in-house association to negotiate matters of concern with us. Although we have negotiated a mutually acceptable arrangement with our pilots, our costs could be adversely affected by the cumulative results of discussions with employee groups in the future.

Each of our different employee groups could unionize at any time and would require separate collective bargaining agreements. If any group of our employees were to unionize and we were unable to agree on the terms of their collective bargaining agreement or we were to experience widespread employee dissatisfaction, we could be subject to work slowdowns or stoppages. In addition, we may be subject to disruptions by organized labor groups protesting our non-union status. Any of these events would be disruptive to our operations, could harm our business, and therefore have an adverse effect on our future results.

Our reputation and financial results could be harmed in the event of an accident or incident involving our aircraft or other MD80 aircraft.

Although we have not had any accidents or material incidents to date, an An accident or incident involving one of our aircraft could involve repair or replacement of a damaged aircraft and its consequential temporary or permanent loss from service, and significant potential claims of injured passengers and others. Although we believe we currently maintain liability insurance in amounts and of the type generally consistent with industry practice, the amount of such coverage may not be adequate and

we may be forced to bear substantial losses from an accident. Substantial claims resulting from an accident in excess of our related insurance coverage would harm our business and financial results. Moreover, any aircraft accident or incident, even if fully insured, could cause a public perception that we are less safe or reliable than other airlines, which would harm our business. Because we are a relatively new company and because we are smaller than most airlines, an accident would be likely to adversely affect us to a greater degree than a larger, more established airline.

In March 2007, the nose landing gear failed to deploy on a flight to Orlando Sanford International Airport. The aircraft landed safely with only minor injuries to ten passengers. Although the FAA and National Transportation Safety Board ("NTSB") have conducted their usual investigation, they have yet to release their final report. The damage to the aircraft is covered by our insurance, but we will be responsible for the $250,000 deductible. The aircraft will be out of service for two months.

Additionally, our dependence on this single type of aircraft and engine for all of our flights makes us particularly vulnerable to any problems that might be associated with this aircraft type or these engines. Our business would be significantly harmed if a mechanical problem with the MD80 series aircraft or the Pratt & Whitney JT8D-200 series engine were discovered causing our aircraft to be grounded while any such problem is being corrected, assuming it could be corrected at all. The FAA could also suspend or restrict the use of our aircraft in the event of any actual or perceived mechanical problems, whether involving our aircraft or another U.S. or foreign airline’sairline's aircraft, while it conducts its own investigation. Our business would also be significantly harmed if the public avoids flying our

aircraft due to an adverse perception of the MD80 series aircraft or the Pratt & Whitney JT8D-200 series engine because of safety concerns or other problems, whether real or perceived, or in the event of an accident involving an MD80 aircraft.

We depend on our ability to maintain existing and develop new relationships with hotels and other providers of travel related services. Any adverse changes in these relationships could adversely affect our business, financial condition and results of operations, as well as our ability to provide air-hotel packages in our leisure destination markets.

An important component of our business success depends on our ability to maintain our existing, as well as build new, relationships with hotels and other travel suppliers in our leisure destination markets. We do not currently have long-term contracts with any of our hotel room suppliers, nor do we anticipate entering into long-term contracts with them in the future. Adverse changes in or the failure to renew existing relationships, or our inability to enter into arrangements with new hotel suppliers on favorable terms, if at all, could reduce the amount, quality and breadth of attractively priced travel products and services we are able to offer, which could adversely affect our business, financial condition and results of operations. Our ability to continue to grow and enter new markets also depends on our ability to obtain a sufficient supply of suitable hotel rooms on favorable terms in our existing and new leisure destinations.

Hotels and other travel suppliers are increasingly seeking to lower their distribution costs by promoting direct online bookings through their own websites, and we expect this trend to continue. Hotels and travel suppliers may choose not to make their travel products and services available through our distribution channels. To the extent consumers increase the percentage of their travel purchases through supplier direct websites and/or if travel suppliers choose not to make their products and services available to us, our business may suffer.

We have a significant amount of fixed obligations and we expect to incur significantly more fixed obligations which could hurt our ability to meet our strategic goals.

As of December 31, 2006, maturities of our long-term debt (including capital leases) were $14.9 million in 2007, $14.2 million in 2008, $16.8 million in 2009, $14.3 million in 2010 and $12.6 million in 2011. All of our long-term and short-term debt has fixed interest rates. In addition to long-term debt, we have a significant amount of other fixed obligations under operating leases related to our aircraft,

airport terminal space, other airport facilities and office space. As of December 31, 2006, future minimum lease payments under noncancelable operating leases with initial or remaining terms in excess of one year were approximately $2.3$3.9 million in 2007, $1.7$1.9 million in 2008, $0.8$0.6 million in 2009 and $0.6$0.1 million in 2010. We expect to incur additional debt and other fixed obligations as we take delivery of additional aircraft and other equipment and continue to expand into new markets.

The amount of our debt and other fixed obligations could:

·

- •

- limit our ability to obtain additional financing to support capital expansion plans and for working capital and other purposes;

·

- •

- divert substantial cash flow from our operations and expansion plans to service our fixed obligations;

·

- •

- limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we compete; and

·

- •

- place us at a possible competitive disadvantage compared to less leveraged competitors and competitors with better access to capital resources.

Our ability to make scheduled payments on our debt and other fixed obligations will depend upon our future operating performance and cash flow, which in turn will depend upon prevailing

economic and political conditions and financial, competitive, regulatory, business and other factors, many of which are beyond our control. We cannot assure you we will be able to generate sufficient cash flow from our operations to pay our debt and other fixed obligations as they become due, and our failure to do so could harm our business. If we are unable to make payments on our debt and other fixed obligations, we could be forced to renegotiate those obligations or obtain additional equity or debt financing. To the extent we finance our activities or future aircraft acquisitions with additional debt, we may become subject to financial and other covenants that may restrict our ability to pursue our growth strategy. We cannot assure you any renegotiation efforts would be successful or timely or that we could refinance our obligations on acceptable terms, if at all.

Our lack of an established line of credit or borrowing facility makes us highly dependent upon our cash balances and operating cash flows.

We have no lines of credit and rely on operating cash flows to provide working capital. Unless we secure a line of credit or borrowing facility, we will be dependent upon our operating cash flows and cash balances to fund our operations and to make scheduled payments on our debt and other fixed obligations. If we fail to generate sufficient funds from operations to meet these cash requirements or do not secure a line of credit, other borrowing facility or equity financing, we could default on our debt and other fixed obligations. Our inability to meet our obligations as they become due would materially restrict our ability to grow and seriously harm our business and financial results.

Our business is heavily dependent on the the attractiveness of our leisure destinations and a reduction in demand for air travel to these markets would harm our business.

Almost all of our scheduled flights have Las Vegas, Orlando or Tampa/St. Petersburg as either their destination or origin. Our business would be harmed by any circumstances causing a reduction in demand for air transportation to the Las Vegas, Orlando or Tampa/St. Petersburg markets, such as adverse

changes in local economic conditions, negative public perception of the particular city, significant price increases, or the impact of past or future terrorist attacks.

We serve Orlando Sanford International Airport, which is not the principal airport in the Orlando market. A refusal by passengers to view Orlando Sanford International Airport as a reasonable alternative to Orlando International Airport, the main airport serving Orlando, could harm our business.

We serve St. Petersburg-Clearwater International Airport, which is not the principal airport in the Tampa Bay market. A refusal by passengers to view the St. Petersburg-Clearwater International Airport as a reasonable alternative to Tampa International Airport, the main airport serving the Tampa Bay area, could harm our business.

We may face increased competition in our markets which could harm our business.

The small cities we serve on a scheduled basis have traditionally attracted considerably less attention from our potential competitors than larger markets, and in most of our markets, we are the only provider of nonstop service to Las Vegas, Orlando or Tampa/St. Petersburg. It is possible other airlines will begin to provide nonstop services to and from these markets or otherwise target these markets. An increase in the amount of direct or indirect competition could harm our business.

We may be unable to renew our lease or increase our facilities at Las Vegas’Vegas' McCarran International Airport.

McCarran International Airport was the 911th busiest airport in the world in 20052006 and its gate space, terminal space, aircraft parking space and facilities in general are constrained. To meet our growth plan, we will require additional facilities at McCarran. However, we may not be able to maintain sufficient or obtain additional facilities at McCarran on favorable terms, or at all. In addition,

our present agreement can be terminated at any time upon 30 days’days' notice. Since Las Vegas is one of our principal destinations, our inability to maintain sufficient facilities or to obtain additional facilities as needed would harm our business by limiting our ability to grow and increasing our costs.

We also currently rely on the availability of overnight aircraft parking space at McCarran. However, due to anticipated airport growth, we may find it difficult to obtain sufficient overnight aircraft parking space in the future. Over time, this may result in our having to overnight aircraft in other cities, which wouldcould increase our costs and could adversely impact our business and results of operations.

Our business could be harmed if we lose the services of our key personnel.

Our business depends upon the efforts of our chief executive officer, Maurice J. Gallagher, Jr., and a small number of management and operating personnel. We do not currently have an employment agreement with or maintain key-man life insurance on Mr. Gallagher. We may have difficulty replacing management or other key personnel who leave and, therefore, the loss of the services of any of these individuals could harm our business.

Our results of operations will fluctuate.

We expect our quarterly operating results to fluctuate in the future based on a variety of factors, including:

·

- •

- the timing and success of our growth plans as we enter new markets;

·

- •

- changes in fuel, security and insurance costs;

·

- •

- mark-to-market adjustments attributable to our fuel hedging transactions;

·

- •

- increases in personnel, marketing, aircraft ownership and other operating expenses to support our anticipated growth; and

·

- •

- the timing and amount of maintenance expenditures.

In addition, seasonal variations in traffic, the timing of significant repair events and weather affect our operating results from quarter to quarter. Quarter-to-quarter comparisons of our operating results may not be good indicators of our future performance. In addition, it is possible our operating results in any future quarter could be below the expectations of investors and any published reports or analyses regarding Allegiant. In that event, the price of our common stock could decline, perhaps substantially.

Due to our limited fleet size, if any of our aircraft becomes unavailable, we may suffer greater damage to our service, reputation and profitability than airlines with larger fleets.