XCYTE THERAPIES, INC.

As filed with the Securities and Exchange Commission on October 10, 20037, 2004

Registration No. 333-

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

XCYTE THERAPIES, INC.

(Exact name of Registrantregistrant as specified in its charter)

| Delaware | 2834 | 91-1707622 | ||

(State or incorporation or organization) | (Primary Standard Industrial | |||

Classification Code Number) | (I.R.S. Employer Identification Number) |

1124 Columbia Street, Suite 130

Seattle, Washington 98104

(206) 262-6200

(Address, including zip code, and telephone number, including

area code, of registrant’s principal executive offices)

Ronald J. Berenson, M.D.

President and Chief Executive Officer

Xcyte Therapies, Inc.

1124 Columbia Street, Suite 130

Seattle, Washington 98104

(206) 262-6200

(Name, address including zip code, and telephone number,

including area code, of agent for service)

Copies to:

| Sonya F. Erickson | Joanna | |||

| General Counsel & Vice President | ||||

| Xcyte Therapies, Inc. | ||||

| 1124 Columbia Street, Suite 130 | ||||

| Seattle, Washington 98104 | ||||

| (206) 262-6200 | Palo Alto, California 94306-2155 | |||

| (206) 447-0900 | (650) |

Approximate date of commencement of proposed sale to the public:As soon as practicable after the Registration Statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box.¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box.¨

CALCULATION OF REGISTRATION FEE(1)FEE

| Title of Each Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price(2) | Amount of Registration Fee(3) | Amount to be Registered(1) | Proposed Maximum Per Share | Proposed Maximum Aggregate Offering Price(1) | Amount of Registration Fee | |||||||||||||||

Convertible Exchangeable Preferred Stock, par value $0.001 | 1,725,000 | $ | 10.00 | $ | 17,250,000 | $ | 2,185.58 | ||||||||||||||

Convertible Subordinated Debentures | $ | 17,250,000 | (2) | — | (3) | — | (3) | — | (3) | ||||||||||||

Common Stock, par value $0.001 | $ | 75,000,000.00 | $6,067.50 | (4) | — | (3) | — | (3) | — | (3) | |||||||||||

Common Stock, par value $0.001 | 1,000,000 | (5) | $ | 3.33 | (6) | $ | 3,333,333.33 | $ | 421.92 | ||||||||||||

| (1) |

| Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933. |

| (2) | This number represents a total of $17,250,000 aggregate principal amount of Convertible Subordinated Debentures issuable if we elect to exchange all of the Convertible Exchangeable Preferred Stock for Convertible Subordinated Debentures. For purposes of estimating the number of debentures to be included upon exchange of the preferred stock, we calculated the amount of debentures issuable upon exchange based on an exchange price of $10 per share of preferred stock. |

| (3) |

| (4) | This number represents shares of common stock issuable upon conversion of the Convertible Exchangeable Preferred Stock or the Convertible Subordinated Debentures. In addition, the shares set forth in the table, pursuant to Rule 416 under the Securities Act of 1933, include an indeterminate number of shares of common stock issuable upon conversion of the preferred stock or the debentures, as these amounts may be adjusted as a result of stock splits, stock dividends and antidilution provisions, or in payment of such make-whole obligations. |

| (5) | This number represents the estimated maximum number of shares of our common stock issuable to satisfy the dividend make-whole payment and interest make-whole payment pursuant to the |

| (6) | Estimated solely for the purpose of calculating the registration fee, pursuant to Rule 457(c), based on |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

ThisThe information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we areit is not soliciting offersan offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECTTO COMPLETION, DATED OCTOBER 7, 2004

1,500,000 Shares

XCYTE THERAPIES, INC. | |

% Convertible Exchangeable Preferred Stock

(Cumulative Dividend, Liquidation Preference $10 Per Share)

· Xcyte Therapies, Inc. is offering 1,500,000 shares of % convertible exchangeable preferred stock, which is referred to · Dividends will be cumulative from the date of original issue at the annual rate of % of the liquidation preference of the convertible preferred stock, payable quarterly on the day of , , , and , commencing , 2005. Any dividends must be declared by our board of directors and must come from funds that are legally available for dividend payments. · You may convert each share of the convertible preferred stock into shares of our common stock based on the initial conversion price of $ , subject to certain adjustments. · We may elect to automatically convert the convertible preferred stock into our common stock if the closing price of our common stock has exceeded $ , which is 150% of the conversion price of the convertible preferred stock, for at least 20 trading days during any 30-day trading period, ending within five trading days prior to notice of automatic conversion. · If we elect to automatically convert, or you elect to voluntarily convert, some or all of the convertible preferred stock into our common stock prior to , 2007, we will make an additional payment on the convertible preferred stock equal to the aggregate amount of dividends that would have been payable on the convertible preferred stock through and including , 2007, less any dividends already paid on the convertible preferred stock. | · We may elect to redeem the convertible preferred stock after , 2007 on the terms described in this prospectus. · At our option, we may exchange the convertible preferred stock in whole, but not in part, on any dividend payment date beginning on , 2005 for our % convertible subordinated debentures. If we elect to exchange the convertible preferred stock for debentures, the exchange rate will be $10 principal amount of debentures for each share of the convertible preferred stock. The debentures, if issued upon exchange of the convertible preferred stock, will mature 25 years after the exchange date and will have terms substantially similar to those of the preferred stock. · The convertible preferred stock has no maturity date and no voting rights prior to conversion into common stock, except under limited circumstances. · Shares of our common stock are listed on the Nasdaq National Market under the symbol “XCYT.” The last reported sale price of our common shares on October |

Shares

Common Stock

This is the initial public offering of our common stock. No public market currently exists for our common stock. We are selling all of the shares of common stock offered by this prospectus. We expect the public offering price to be between $ and $ per share.

We have applied to have our common stock approved for quotation on The Nasdaq National Market under the symbol “XCYT.”

Investing in our common stockinvestment involves a high degree of risk. Before buying any shares, you should read the discussion of material risks of investing in our common stock inSee ““Risk factors”Factors” beginning on page 7.9.

| Per Share | Total | |||||

Public offering price | $ | $ | ||||

Underwriting discounts and commissions | $ | $ | ||||

Proceeds, before expenses, to Xcyte Therapies, Inc. | $ | $ | ||||

The underwriters have a 30-day option to purchase up to 225,000 additional shares of convertible preferred stock from us to cover over-allotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracydetermined if this prospectus is truthful or adequacy of this prospectus.complete. Any representation to the contrary is a criminal offense.

| ||||||||

| ||||||||

| ||||||||

| ||||||||

The underwriters may also purchase up to an additional shares of our common stock at the public offering price, less the underwriting discounts and commissions, to cover over-allotments, if any, within 30 days from the date of this prospectus. If the underwriters exercise the option in full, the total underwriting discounts and commissions will be $ , and our total proceeds, before expenses, will be $ .

The underwriters are offering the common stock as set forth under “Underwriting.” Delivery of the shares will be made on or about , 2003.

UBS Investment Bank

U.S. Bancorp Piper Jaffray

Wells Fargo Securities, LLC

The date of this prospectus is , 2003.2004.

| Page | ||

| 1 | ||

| 9 | ||

| 27 | ||

| 28 | ||

| 28 | ||

Ratio of Earnings to Fixed Charges and Preferred Stock Dividends | 29 | |

| 29 | ||

| 30 | ||

| 31 | ||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 32 | |

| 41 | ||

| 66 | ||

| 67 | ||

| 79 | ||

| 82 | ||

| 84 | ||

| 94 | ||

| 101 | ||

| 105 | ||

| 113 | ||

| 115 | ||

| 118 | ||

| 118 | ||

| 118 | ||

| F-1 |

You should rely only on the information contained in this prospectus. We have not, and the underwriters have not, authorized anyoneany other person to provide you with information different from that contained in this prospectus. We are offeringinformation. This prospectus is not an offer to sell, andnor is it seeking offersan offer to buy, shares of our common stock onlythese securities in jurisdictionsany state where offers and sales arethe offer or sale is not permitted. The information contained in this prospectus is complete and accurate only as of the date of this prospectus, regardless ofon the time of delivery of this prospectus or of any sale of shares of our common stock.

Through and including , 2003, federal securities lawsfront cover, but the information may require all dealershave changed since that effect transactions in our common stock, whether or not participating in this offering, to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.date.

XcyteTM, Xcyte TherapiesTM, XcellerateTM and Xcellerated T CellsTM are trademarks of Xcyte Therapies, Inc. All other trademarks appearing in this prospectus are the property of their respective holders.

Prospectus summaryPROSPECTUS SUMMARY

This summary highlights selected information appearing elsewhere in this prospectus and may not contain all ofprospectus. While this summary highlights what we consider to be the information that ismost important to you. This prospectus includes information about the shares we are offering as well as information regarding our business and detailed financial data. Youus, you should carefully read this prospectus and the registration statement of which this prospectus is a part in itstheir entirety before making an investment decision, especially the risks of investing in our commonthe convertible preferred stock, which we discuss under “Risk factors”Factors” beginning on page 7,9, and our financial statements and related notes beginning on page F-1.

Unless the context requires otherwise, the words “Xcyte,” “we,” “company,” “us” and “our” refer to Xcyte Therapies, Inc.

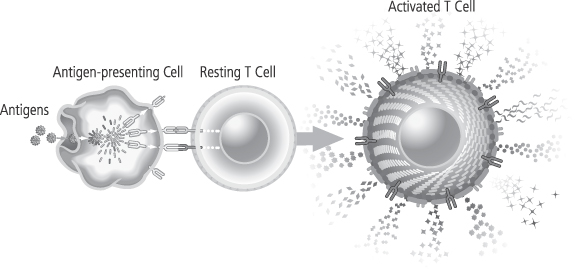

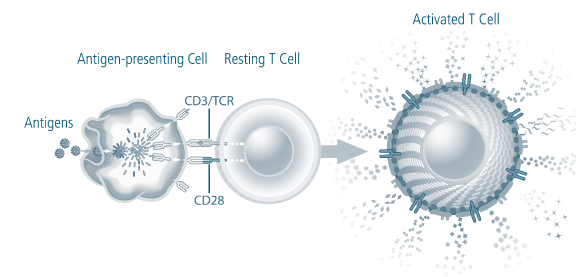

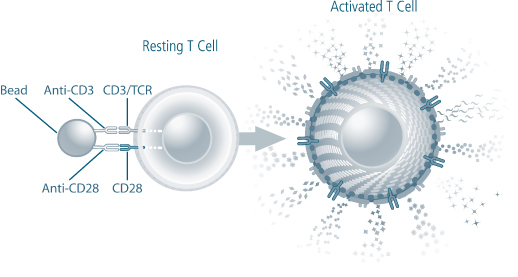

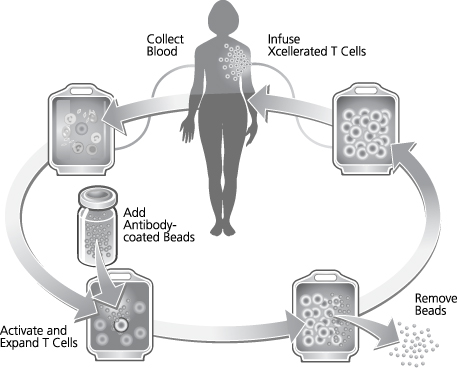

OUR BUSINESSOur Business

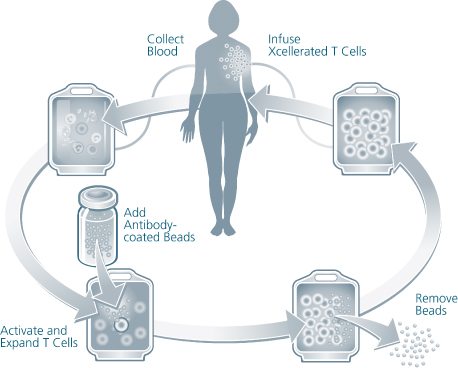

We are a biotechnology company developing a new class of therapeutic products thatdesigned to enhance the body’s natural immune responses to treat cancer, infectious diseases and other medical conditions associated with weakened immune systems. We producederive our therapeutic products which consist of activated, patient-specificfrom a patient’s own T cells, usingwhich are cells of the immune system that orchestrate immune responses and can detect and eliminate cancer cells and infected cells in the body. We use our patented and proprietary Xcellerate Technology. We use blood collected from the patientTechnology to generate activated T cells, which we call Xcellerated T Cells.Cells, from blood that is collected from the patient. Activated T cells are T cells that have been stimulated to carry out immune functions. Our Xcellerate Technology is designed to rapidly activatesactivate and expandsexpand the patient’s T cells outside of the body. These Xcellerated T Cells are subsequentlythen administered to the patient.

We believe, based on clinical trials to date, that our Xcellerate Technology can produce Xcellerated T Cells in sufficient numbers to generate rapid and potent immune responses to treat a variety of medical conditions.

We believe In our ongoing clinical studies using our Xcellerate Technology, allows us to consistentlywe have observed an increase in the quantity and restorea restoration of the quality and diversity of T cells fromin patients with weakened immune systems. We have submitted the findings on the increase in quantity of T cells to the FDA and plan to submit additional data in our next annual report. We believe we can efficiently manufacture Xcellerated T Cells for therapeutic applications. In addition, based on clinical studies to date, we believe the Xcellerated T Cells are safe and generally well tolerated and can be easily administered to patients in an outpatient clinical setting. We expect Xcellerated T Cells may be used alone or in combination with other complementary treatments.

Our clinical trials and independent clinical trials using an earlier version of our technology, to date, have involved small numbers of patients and we have not designed nor been required to design such trials to produce statistically significant results as to efficacy. These trials have neither been randomized nor blinded to ensure that the results are due to the effects of Xcellerated T Cells. Success in early clinical trials neither ensures that large-scale trials will be successful nor predicts final results. We and our scientific collaboratorsother clinical investigators have completed or are conducting clinical trials in the following indications:

Chronic lymphocytic leukemia, or CLL. In our ongoing Phase I/II clinical trial in CLL, treatment with Xcellerated T Cells resulted in a 50% to 100% reduction in the size of enlarged lymph nodes in 12 of 17 (71%) patients for whom data was available as of September 27, 2004. In addition, there was a 50% or greater reduction in spleen size as measured below the rib cage by physical examination in 10 of the 13 patients (77%) with enlarged spleens. These findings were submitted to the FDA in the Information Packet for a Type B End of Phase II meeting held on September 23, 2004. At this meeting we discussed with the FDA our plans for a Phase II/III clinical trial of Xcellerated T Cells in patients with CLL who have been previously treated with chemotherapy and have failed treatment with Campath, an FDA-approved drug used to treat CLL. Based on feedback from the FDA during |

this meeting, we intend to modify our planned protocol for this Phase II/III clinical trial to provide the FDA with data we believe will address the FDA’s concerns regarding the subcutaneous route of Campath administration and the dose and schedule of Xcellerated T |

| Multiple myeloma. In our ongoing Phase I/II clinical trial, we have shown that treatment with Xcellerated T Cells |

| Non-Hodgkin’s lymphoma. In an independent clinical trial, conducted by one of our scientific founders under a physician-sponsored |

|

1

an earlier version of our proprietary technology. We have been advised that these data have been submitted to the FDA for review. The results of this study were |

OUR SOLUTION

We have developed our proprietary Xcellerate Technology, which consistently activates and grows large numbers of T cellsex vivo, or outside of the body, for multiple therapeutic applications.

Benefits of Xcellerated T Cells

We believe Xcellerated T Cells may be an effective treatment for cancer and infectious diseases and may have the following clinical benefits:

Benefits of our Xcellerate Technology

We believe our Xcellerate Technology may have the following benefits:

2

OUR STRATEGYOur Strategy

Our goal is to be a leader in the field of T cell therapy and to leverage our expertise in T cell activation to develop and commercialize products to treat patients with cancer, infectious diseases and other medical conditions associated with weakened immune systems. We willplan to initially develop Xcellerated T Cells to treat life-threatening diseases, such as cancer and HIV, which currently have inadequate treatments. Key elements of our strategy include the following:

| Maximize speed to market. |

| Expand the |

| Leverage complementary technologies and therapies. |

| Retain |

| Enhance our manufacturing capabilities. |

| Expand and enhance our intellectual property. |

OUR CORPORATE INFORMATIONRisks Associated With Our Business

We are a development stage company. We are subject to numerous risks and obstacles, and we have highlighted the most important of them in “Risk Factors” beginning on page 9. In particular, we have a limited operating history and have incurred losses in each fiscal year since our inception. We incurred net losses of approximately $18.5 million for the year ended December 31, 2003 and $24.4 million for the six months ended June 30, 2004, and our deficit accumulated during the development stage was approximately $111.0 million as of June 30, 2004. We have no commercial products for sale, and we anticipate that we will incur substantial and increasing losses over the next several years as we expand our research, development and clinical trial activities, acquire or license technologies, scale up and improve our manufacturing operations, seek regulatory approval and, if we receive FDA approval, commercialize our products. Because of the numerous risks and uncertainties associated with our product development efforts, we are unable to predict whether or when we will achieve profitability. Our clinical trials and independent clinical trials using an earlier version of our technology, to date, have involved small numbers of patients, and we have not designed nor been required to design such trials to produce statistically significant results as to efficacy. These trials have neither been randomized nor blinded to ensure that the results are due to the effects of the Xcellerated T Cells. The results reported are preliminary and success in early clinical trials neither ensures that large-scale trials will be successful nor predicts final results.

Our Corporate Information

We were incorporated in Delaware as MolecuRx, Inc. in January 1996. We changed our name to CDR Therapeutics, Inc. in August 1996 and changed our name to Xcyte Therapies, Inc. in October 1997. Our principal executive offices are located at 1124 Columbia Street, Suite 130, Seattle, Washington 98104, and our telephone number is (206) 262-6200. Our web site address is www.xcytetherapies.com.www.xcytetherapies.com. The information contained on our web site is not incorporated by reference into and does not form any part of this prospectus.

3THE OFFERING

The offering

| 1,500,000 shares of % convertible exchangeable preferred stock, | par value $0.001 per share (1,725,000 shares |

|

|

|

| |

Dividends | Dividends will be cumulative from the date of original issue at the annual rate of % of the liquidation preference of the convertible preferred stock, payable quarterly on the day of , , , and , commencing , 2005. Any dividends must be declared by our board of directors and must come from funds which are legally available for dividend payments. | |

Conversion Rights | Unless we redeem or exchange the convertible preferred stock, the convertible preferred stock can be converted at your option at any time into shares of our common stock at an initial conversion price of $ (equivalent to a conversion rate of approximately shares of common stock for each share of convertible preferred stock). The initial conversion price with respect to the convertible preferred stock is subject to adjustment in certain events, including a non-stock fundamental change or a common stock fundamental change, which are explained in more detail under the section entitled “Description of Convertible Preferred Stock—Conversion—Conversion Price Adjustment—Merger, Consolidation or Sale of Assets.” | |

Automatic Conversion | Unless we redeem or exchange the convertible preferred stock, we may elect to automatically convert some or all of the convertible preferred stock into shares of our common stock if the closing sale price of our common stock has exceeded 150% of the conversion price for at least 20 out of 30 consecutive trading days ending within five trading days prior to the notice of automatic conversion. | |

Dividend Make-Whole Payment | If we elect to automatically convert, or you voluntarily convert, some or all of the convertible preferred stock into shares of our common stock prior to , 2007, we will make an additional payment on the convertible preferred stock equal to the aggregate amount of cumulative | |

| dividends that would have accrued and become payable on the convertible preferred stock from the date of original issue through and including , 2007, less any dividends already paid on the convertible preferred stock. This additional payment is payable by us in cash or, at our option, in shares of our common stock, or a combination of cash and shares of our common stock. | ||

Liquidation Preference | In the event of our voluntary or involuntary dissolution, liquidation or winding up, you will be entitled to be paid a liquidation preference equal to $10 per share of convertible preferred stock, plus accrued and unpaid dividends before any distribution of assets may be made to holders of capital stock ranking junior to the convertible preferred stock. | |

Optional Redemption | On or after , 2007, we may redeem the convertible preferred stock, in whole or in part, at our option at the redemption prices set forth in this prospectus, together with accrued dividends to, but excluding, the redemption date. See the section entitled “Description of Convertible Preferred Stock—Optional Redemption” below. | |

Voting Rights | Except as provided by law and in other limited situations described in this prospectus, you will not be entitled to any voting rights. However, you will, among other things, be entitled to vote as a separate class to elect two directors if we have not paid the equivalent of six or more quarterly dividends, whether or not consecutive. These voting rights will continue until we pay the full accrued but unpaid dividends on the convertible preferred stock. | |

Exchange Provisions | At our option, we may exchange the convertible preferred stock in whole, but not in part, on any dividend payment date beginning on , 2005 for our % convertible subordinated debentures. If we elect to exchange the convertible preferred stock for debentures, the exchange rate will be $10 principal amount of debentures for each share of convertible preferred stock. | |

Debentures | The debentures, if issued upon exchange of the convertible preferred stock, will have the following terms: | |

Interest Rate | The debentures will have an interest rate of % per year. Interest will be payable on and of each year, beginning on the first interest payment date after the exchange date. | |

Redemption | On or after , 2007 we may redeem the debentures at the redemption prices listed in this prospectus, plus accrued interest. | |

Maturity | The debentures will mature 25 years after the exchange date. | |

Conversion | The debentures may be converted at any time by the holder prior to maturity into shares of our common stock at the same conversion price applicable to the convertible preferred stock, subject to adjustment upon certain events. | |

Automatic Conversion | We may automatically convert the debentures into shares of our common stock at any time prior to maturity under the same terms applicable to the convertible preferred stock. | |

Interest Make-Whole Payment | If you voluntarily convert or we elect to automatically convert some or all of the debentures into shares of our common stock prior to , 2007, we will also make an additional payment on the debentures equal to the aggregate amount of interest that would have accrued and been payable from date of the original issuance of the debentures pursuant to the exchange through and including , 2007, less any interest paid with respect to such debentures. This additional payment is payable by us, in cash or, at our option, in shares of our common stock, or a combination of cash and shares of our common stock. | |

Subordination | The debentures are subordinated to all existing and future senior indebtedness and are effectively subordinated to all of the indebtedness and other liabilities (including trade and other payables, but excluding intercompany liabilities) of us and our subsidiaries. As of June 30, 2004, we had | |

| approximately $2.2 million of indebtedness outstanding that would have constituted senior indebtedness and approximately $4.6 million of indebtedness and other liabilities outstanding to which the debentures would have been effectively subordinated (including trade and other payables, but excluding intercompany liabilities). The indenture governing the debentures does not limit the amount of indebtedness, including senior indebtedness, that we and our subsidiaries may incur. See the section entitled “Description of Debentures—Subordination” below. | ||

Use of Proceeds | We expect to use the net proceeds | |

|

| |

The number of shares of our common stock outstanding at the closing of this offering is based on 8,402,636 shares of our common stock outstanding as of September 30, 2003 and excludes:

Our common stock |

Nasdaq National Market Symbol for our Convertible Preferred Stock | We will make an application to trade the convertible preferred stock on the Nasdaq National Market under the symbol “XCYTP.” | |

Listing of | ||

Debentures

Unless otherwise indicated, all information in this prospectus assumes the following:

Risk Factors | An investment in the | |

Unless we specifically state otherwise, the information in this prospectus assumes that the underwriters have not exercised their option to purchase up to additional shares of our common stock to cover over-allotments, if any.

4SUMMARY FINANCIAL DATA

Summary financial data

The following summary financial data for the years ended December 31, 19981999 through 2002 has2003 have been derived from our audited financial statements. The following summary financial data for the six-month periods ended June 30, 2003 and 2002,2004, and the summary balance sheet data as of June 30, 20032004 have been derived from our unaudited condensed financial statements. The unaudited condensed financial statements have been prepared on a basis consistent with our audited financial statements and include all adjustments we consider necessary for the fair presentation of the information. Operating results for the six months ended June 30, 20032004 are not necessarily indicative of the results that may be expected for the entire year ending December 31, 2003.2004. This information is only a summary and should be read together with the financial statements and the notes to those statements appearing elsewhere in this prospectus and the information under “Selected financial data”Financial Data” and “Management’s discussionDiscussion and analysisAnalysis of financial conditionFinancial Condition and resultsResults of operations.Operations.”

| Years ended December 31, | Six months ended June 30, | |||||||||||||||||||||||||||

| Statement of operations data | 1998 | 1999 | 2000 | 2001 | 2002 | 2002 | 2003 | |||||||||||||||||||||

| (in thousands, except per share data) | ||||||||||||||||||||||||||||

Total revenue | $ | — | $ | 16 | $ | 98 | $ | 30 | $ | — | $ | — | $ | 72 | ||||||||||||||

Operating expenses: | ||||||||||||||||||||||||||||

Research and development | 4,317 | 5,471 | 11,257 | 14,701 | 14,663 | 7,651 | 7,029 | |||||||||||||||||||||

General and administrative | 1,427 | 1,654 | 2,403 | 5,204 | 4,979 | 2,883 | 2,194 | |||||||||||||||||||||

Total operating expenses | 5,744 | 7,125 | 13,660 | 19,905 | 19,642 | 10,534 | 9,223 | |||||||||||||||||||||

Loss from operations | (5,744 | ) | (7,109 | ) | (13,562 | ) | (19,875 | ) | (19,642 | ) | (10,534 | ) | (9,151 | ) | ||||||||||||||

Other income (expense), net | 298 | 162 | 621 | 363 | 189 | 122 | (38 | ) | ||||||||||||||||||||

Net loss | (5,446 | ) | (6,947 | ) | (12,941 | ) | (19,512 | ) | (19,453 | ) | (10,412 | ) | (9,189 | ) | ||||||||||||||

Accretion of preferred stock | — | — | (8,411 | ) | (8,001 | ) | (8,001 | ) | — | |||||||||||||||||||

Net loss applicable to common stockholders | $ | (5,446 | ) | $ | (6,947 | ) | $ | (12,941 | ) | $ | (27,923 | ) | $ | (27,454 | ) | $ | (18,413 | ) | $ | (9,189 | ) | |||||||

Basic and diluted net loss per common share | $ | (0.86 | ) | $ | (1.15 | ) | $ | (2.16 | ) | $ | (4.03 | ) | $ | (3.52 | ) | $ | (2.45 | ) | $ | (1.13 | ) | |||||||

Shares used in basic and diluted net loss per share calculation | 6,355 | 6,050 | 6,003 | 6,936 | 7,809 | 7,523 | 8,144 | |||||||||||||||||||||

Pro forma net loss per common share (unaudited)(1) | $ | (0.44 | ) | $ | (0.20 | ) | ||||||||||||||||||||||

Shares used in pro forma net loss per common share calculation (unaudited)(1) | 44,550 | 45,427 | ||||||||||||||||||||||||||

| Years ended December 31, | Six months ended June 30, | |||||||||||||||||||||||||||

| 1999 | 2000 | 2001 | 2002 | 2003 | 2003 | 2004 | ||||||||||||||||||||||

| (in thousands, except per share data) | (unaudited) | |||||||||||||||||||||||||||

Statement of Operations Data | ||||||||||||||||||||||||||||

Total revenue | $ | 16 | $ | 98 | $ | 30 | $ | — | $ | 170 | $ | 72 | $ | 36 | ||||||||||||||

Operating expenses: | ||||||||||||||||||||||||||||

Research and development | 5,471 | 11,257 | 14,701 | 14,663 | 13,685 | 7,029 | 8,601 | |||||||||||||||||||||

General and administrative | 1,654 | 2,403 | 5,204 | 4,979 | 4,322 | 2,194 | 3,297 | |||||||||||||||||||||

Total operating expenses | 7,125 | 13,660 | 19,905 | 19,642 | 18,007 | 9,223 | 11,898 | |||||||||||||||||||||

Loss from operations | (7,109 | ) | (13,562 | ) | (19,875 | ) | (19,642 | ) | (17,837 | ) | (9,151 | ) | (11,862 | ) | ||||||||||||||

Other income (expense), net | 162 | 621 | 363 | 189 | (620 | ) | (38 | ) | (12,508 | ) | ||||||||||||||||||

Net loss | (6,947 | ) | (12,941 | ) | (19,512 | ) | (19,453 | ) | (18,457 | ) | (9,189 | ) | (24,370 | ) | ||||||||||||||

Accretion of preferred stock | — | — | (8,411 | ) | (8,001 | ) | — | — | (8,973 | ) | ||||||||||||||||||

Net loss applicable to common stockholders | $ | (6,947 | ) | $ | (12,941 | ) | $ | (27,923 | ) | $ | (27,454 | ) | $ | (18,457 | ) | $ | (9,189 | ) | $ | (33,343 | ) | |||||||

Basic and diluted net loss per common share | $ | (6.32 | ) | $ | (11.86 | ) | $ | (22.14 | ) | $ | (19.34 | ) | $ | (12.40 | ) | $ | (6.21 | ) | $ | (3.66 | ) | |||||||

Shares used in basic and diluted net loss per share calculation | 1,100 | 1,091 | 1,261 | 1,420 | 1,488 | 1,481 | 9,107 | |||||||||||||||||||||

5

The following table contains a summary of our balance sheet as of June 30, 2003:2004:

| on an actual basis; |

| on |

| As of June 30, 2003 | ||||||||||

| Balance sheet data | Actual | Pro forma | Pro forma as | |||||||

| (in thousands) | ||||||||||

Cash, cash equivalents and short term investments | $ | 8,892 | $ | 22,502 | $ | |||||

Working capital | 7,252 | 20,862 | ||||||||

Total assets | 12,695 | 26,305 | ||||||||

Long-term obligations, less current portion | 1,477 | 1,477 | ||||||||

Redeemable convertible preferred stock | 64,604 | — | ||||||||

Redeemable convertible preferred stock warrants | 1,069 | — | ||||||||

Total stockholders’ equity (deficit) | (56,589 | ) | 9,957 | |||||||

Balance Sheet Data Cash, cash equivalents and short-term investments Working capital Total assets Long-term obligations, less current portion Total stockholders’ equityThe above balance sheet data is based on 8,402,636 shares of our common stock outstanding as of June 30, 2003 and excludes: As of June 30, 2004 Actual As adjusted (unaudited, in thousands) $ 33,730 $ 47,315 30,838 44,423 39,860 53,445 2,594 2,594 33,097 46,682

6

Investing in our commonthe convertible preferred stock involves a high degree of risk. You should carefully consider the risks described below with all of the other information included in this prospectus before making an investment decision.deciding to invest in the convertible preferred stock. If any of the following risks actually occur, they may materially harm our business and our financial condition and results of operations. In this event, the market price of the convertible preferred stock and our common stock could decline and you could lose part or all of your investment. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also adversely affect our business.

RISKS RELATED TO OUR BUSINESSRisks Related To Our Business

We expect to continue to incur substantial losses, and we may never achieve profitability.

We are a development stage company with limited operating history. We have incurred significant operating losses since we began operations in 1996, including net losses of approximately $9.2$18.5 million for the year ended December 31, 2003 and $24.4 million for the six months ended June 30, 2003,2004, and we may never become profitable. As of June 30, 2003,2004, we had a deficit accumulated during the development stage of approximately $77.3$111.0 million. These losses have resulted principally from costs incurred in our research and development programs and from our general and administrative expenses. We also expect to incur significant costs to renovate our leased facility for the manufacture of Xcellerated T Cells for our planned clinical trials and, if we receive FDA approval, for initial commercialization activities. To date, we have derived no revenues from product sales or royalties. We do not expect to have any significant product sales or royalty revenue for a number of years. Our operating losses have been increasing during the past several years and will continue to increase significantly in the next several years as we expand our research and development, participate in clinical trial activities, acquire or license technologies, scale up and improve our manufacturing operations, seek regulatory approvals and, if we receive FDA approval, commercialize our products. These losses, among other things, have had and will continue to have an adverse effect on our stockholders’ equity and working capital. Because of the numerous risks and uncertainties associated with our product development efforts, we are unable to predict when we may become profitable, if at all. If we are unable to achieve and then maintain profitability, the market value of our common and convertible preferred stock will likely decline.

We will need to raise substantial additional capital to fund our operations, and our failure to obtain funding when needed may force us to delay, reduce or eliminate our product development programs or collaboration efforts.

Developing products and conducting clinical trials for the treatment of cancer and infectious diseases require substantial amounts of capital. To date, we have raised capital primarily through private equity financings, an initial public offering, the sale of convertible promissory notes and equipment leases. Currently, we anticipate that our cash, cash equivalents and investments will be adequate to satisfy our capital needs through at least the end of the second quarter of 2005 if we do not raise capital in this offering. If we are unable to timely obtain additional funding in a timely fashion, we may never conduct required clinical trials to demonstrate safety and clinical efficacy of Xcellerated T Cells, and we may never obtain FDA approval or commercialize any of our products. We will need to raise additional capital to, among other things:

| fund our clinical trials; |

| expand our research and development activities; |

| scale up and improve our manufacturing operations; |

| finance our general and administrative expenses; |

| acquire or license technologies; |

7

Risk factors

| prepare, file, prosecute, maintain, enforce and defend our patent and other proprietary rights; |

| pursue regulatory approval and commercialization of Xcellerated T Cells and any other products that we may develop; and |

| develop and implement sales, marketing and distribution capabilities. |

Our net cash used in operations has exceeded our cash generated from operations for each year since our inception. For example, we used approximately $8.0 million in operating activities for the six months ended June 30, 2003 and approximately $15.2 million in 2002. Based upon the current status of our product development and collaboration plans, we believe that the net proceeds of this offering, together with our cash, cash equivalents and investments, will be adequate to satisfy our capital needs through at least the next 18 months. However, changes in our business may occur that would consume available capital resources sooner than we expect. See “Management’s discussion and analysis of financial condition and results of operations—Liquidity and capital resources.” Our future funding requirements will depend on many factors, including, among other things:

| the progress, expansion and cost of our clinical trials and research and development activities; |

| any future decisions we may make about the scope and prioritization of the programs we pursue; |

| the development of new product candidates or uses for our Xcellerate Technology; |

| changes in regulatory policies or laws that affect our operations; and |

| competing technological and market developments. |

If we raise additional funds by issuing equity securities, further dilution to stockholders may result and new investors could have rights superior to holders of the shares issued in this offering.our current stockholders. In addition, debt financing, if available, may include restrictive covenants. If adequate funds are not available to us, we may have to liquidate some or all of our assets or delay, reduce the scope of or eliminate some portion or all of our development programs or clinical trials. We also may have to license to other companies our products or technologies that we would prefer to develop and commercialize ourselves.

WeDue to our limited resources and access to capital, we must prioritize our development programs and may decidechoose to pursue development programs for Xcellerated T Cells that may never receive regulatory approval or prove to be profitable.

Because we have limited resources and access to capital to fund our operations, our management must make significant prioritization decisions on which programs to pursue and how much of our resources to allocate to each program. We are currently focusing our research and development efforts on the use of Xcellerated T Cells to treat CLL, multiple myeloma, non-Hodgkin’s lymphoma kidney cancer, prostate cancer and HIV. Our management has broad discretion to suspend, scale down or discontinue any of these programs or to initiate new programs to treat other clinical indications. Xcellerated T Cells may never prove to be safe and clinically effective to treat any of these indications, and the market for these indications may never prove to be profitable even if we obtain regulatory approval for these indications. Accordingly, we cannot assure you that the programs we decide to pursue will lead to regulatory approval or will prove to be profitable.

If we are unable to protect our proprietary rights, we may not be able to compete effectively.

Our success depends in part on obtaining, maintaining and enforcing our patents and in-licensed and proprietary rights throughout the world. We believe we own, or have rights under licenses to, issued patents and pending patent applications that are necessary to commercialize Xcellerated T Cells. However, the patents on which we rely may be challenged and invalidated, and our patent applications may not result in issued patents. Moreover, our patents and patent applications may not be sufficiently broad to prevent others from practicing our technologies or developing competing products. We also face the risk that others may independently develop similar or alternative technologies or may design around our proprietary and patented technologies.

The patent positions of pharmaceutical and biotechnology companies can be highly uncertain and involve complex legal and factual questions for which important legal principles remain unresolved. No consistent policy regarding the breadth of claims allowed in biotechnology patents has emerged to date in the United States. Furthermore, the application and enforcement of patent laws and regulations in foreign countries is even more uncertain, particularly where, as here, patent rights are co-owned with others, thus requiring their consent to ensure exclusivity in the marketplace. Accordingly, we cannot assure you that we will be able to effectively file, protect or defend our proprietary rights in the United States or in foreign jurisdictions on a consistent basis.

Third parties may successfully challenge the validity of our patents. We will only be able to protect our technologies from unauthorized use by third parties to the extent that valid and enforceable patents or other

proprietary rights cover them. Because the issuance of a patent is not conclusive of its validity or enforceability, we cannot assure you how much protection, if any, will be given to our patents if we attempt to enforce them or if others challenge their validity in court. It is possible that a competitor may successfully challenge our patents or that a challenge will result in limiting the coverage of our patents. If the outcome of litigation is adverse to us, third parties may be able to use our technologies without payment to us.

In addition, it is possible that others may infringe upon our patents or successfully avoid them through design innovation. We may initiate litigation to police unauthorized use of our proprietary rights. However, the cost of litigation to uphold the validity of our patents and to prevent infringement could be substantial, particularly where patent rights are co-owned with others, thus requiring their participation in the litigation, and the litigation will consume time and other resources. Some parties may be better able to sustain the costs of complex patent litigation because they have substantially greater resources. Moreover, if a court decides that our patents are not valid, we will not have the right to stop others from using our inventions. There is also the risk that, even if the validity of our patents were upheld, a court may refuse to stop others on the grounds that their activities do not infringe upon our patents. Because protecting our intellectual property is difficult and expensive, we may be unable to prevent misappropriation of our proprietary rights.

We also rely on certain proprietary trade secrets and know-how, especially where we believe patent protection is not appropriate or obtainable. Trade secrets and know-how, however, are difficult to protect. We have taken measures to protect our unpatented trade secrets and know-how, including the use of confidentiality and invention assignment agreements with our employees, consultants and some of our contractors. It is possible, however, that these persons may unintentionally or willingly breach the agreements or that our competitors may independently develop or otherwise discover our trade secrets and know-how.

The clinical and commercial utility of our Xcellerate Technology is uncertain and may never be realized.

Our Xcellerate Technology is based on a novel approach to treat cancer and infectious diseases and is in an early stage of development. We have limitedOur clinical data or examplestrials and independent clinical trials using an earlier version of similarour technology, to conclude that our Xcellerate Technology may be safe and clinically effective.date, have involved small numbers of patients, which, unless otherwise stated, were not designed to produce statistically significant results as to efficacy. In addition, these trials have neither been randomized nor blinded to ensure the results are due to the effect of Xcellerated T Cells. Some of the data regarding

8

Risk factors

our Xcellerate Technology were derived from independent clinical trials, including physician-sponsored trials, which we do not control. In addition, data from these independent clinical trials were derived using T cells activated with an earlier version of our proprietary technology. Success in early clinical trials neither ensures that large-scale trials will be successful nor predicts final results. Acceptable results in early trials may not be repeated in later trials. In addition, we may not be able to treat patients if we cannot collect a sufficient quantity of T cells that meet our minimum specifications to enable us to produce Xcellerated T Cells. Also, some patients may be unable to tolerate the required procedures for blood collection and administration of Xcellerated T Cells.

We Finally, we only have limited data on the safety and efficacyexperience in treating patients with multiple doses of Xcellerated T Cells, which may be required to treatachieve optimal therapeutic effects.

Although we have observed few serious side effects in patients infused with very weakened immune systems, such as patients with HIV. AlthoughXcellerated T Cells in clinical trials conducted to date, we may not ultimately be able to provide the FDA with satisfactory data to support a claim of clinical safety and efficacy sufficient to enable the FDA to approve Xcellerated T Cells for commercialization. This may be because later clinical trials may fail to reproduce favorable data we may have obtained in earlier clinical trials, because the FDA may disagree with how we interpret the data from these clinical trials or because the FDA may not accept these therapeutic effects as valid endpoints in pivotal trials necessary for market approval. For example, although our studies to date have indicated that our Xcellerate Technology can lead to increased T cell and lymphocyte counts, the FDA will not accept increased T cell and lymphocyte counts as a valid endpoint in pivotal studies necessary for market approval. Instead, we would be required to show that Xcellerated T Cells lead to a significant clinical benefit. We will also need to demonstrate that Xcellerated T Cells are safe. We do not have data on possible harmful long-term effects of Xcellerated T Cells and will not

have any data on long-term effects in the near future. Furthermore,We also have limited data on the data from our clinical trials may be limited because these clinical trials generally do not involve a large numbersafety and efficacy of patients.Xcellerated T Cells to treat patients with very weakened immune systems, such as patients with HIV. For these and other reasons, the clinical effectiveness and commercialibility of our Xcellerate Technology is uncertain and may never be realized.

Our ability to initiate a pivotal trial in patients with CLL on our proposed protocol and timeline is uncertain and highly dependent on the FDA.

We cannot be sure that the FDA will accept the Phase II/III clinical trial protocol we plan to submit in the fourth quarter of 2004 for Xcellerated T Cells in patients with CLL, who have been previously treated with chemotherapy and have failed treatment with Campath. The FDA may conclude that we have not adequately addressed the issues they raised in our initial meeting on September 23, 2004 or they may propose additional modifications to address new concerns they have with our protocol. If the FDA does not accept the Phase II/III clinical trial protocol we plan to submit in the fourth quarter of 2004 or if the FDA requires us to conduct a separate clinical trial to address their concerns, then our plan to initiate a pivotal trial by the end of the second quarter of 2005 could be significantly delayed. Our clinical development plan for CLL is premised upon the continued existence of an unmet medical need in this population. FDA approval of another drug or biologic to treat Campath-refractory CLL could result in the FDA requiring that we conduct larger, controlled studies in more patients.

To date, Xcellerated T Cells have been shown in CLL patients to decrease lymph nodes and spleen size, but not leukemic blood counts. We cannot be sure that the FDA will accept two of these three major measurements of tumor response as sufficient to support product approval. In addition, although the FDA has accepted tumor response as a valid clinical endpoint in disease indications where there is an unmet clinical need such as CLL, we cannot be sure that the FDA will not require us to demonstrate patient survival in a pre-approval trial rather than a post-approval confirming trial that we plan to do. The Phase II/III clinical trial we plan to conduct is not randomized or powered statistically to demonstrate patient survival. To address decreases in leukemic counts in the blood in order to achieve all three major measurements of tumor response, we are planning to enroll CLL patients in our proposed Phase II/III clinical trial who have been recently treated with Campath, a drug that leads to decreases in leukemic counts in the blood. We have not previously tested the effects of using Xcellerated T Cells after use of Campath. We cannot be sure that patients’ leukemic counts will not rise again after the use of Campath or that we will observe a similar safety profile and treatment effects of our Xcellerated T Cells in CLL patients who have received Campath as we have observed in our previous clinical trials.

We may fail to obtain or may experience delays in obtaining regulatory approvalapprovals to market Xcellerated T Cells, which will significantly harm our business.

We do not have the necessary approvalapprovals to market or sell Xcellerated T Cells in the United States or any foreign market. Before marketing Xcellerated T Cells, we must successfully complete extensive preclinical studies and clinical trials and rigorous regulatory approval procedures. We cannot assure you that we will obtain the necessary regulatory approvalapprovals to commercialize Xcellerated T Cells.

Conducting clinical trials is uncertain and expensive and often takes many years to complete. The results from preclinical testing and early clinical trials are often not predictive of results obtained in later clinical trials. In conducting clinical trials, we may fail to establish the effectiveness of Xcellerated T Cells for the targeted indication or we may discover unforeseen side effects. Moreover, clinical trials may require the enrollment of large numbers of patients, and suitable patients may be difficult to identify and recruit. Clinical trials are also often subject to unanticipated delays. In addition, we are currently developing a custom bioreactor system in our manufacturing process, and we will not be able to obtain FDA approval to commercialize Xcellerated T Cells without the FDA’s acceptance of our manufacturing process using this bioreactor system. Also, patients participating in the trials may die before completion of the trial or suffer adverse medical effects unrelated to treatment with Xcellerated T Cells. This could delay or lead to termination of our clinical trials. A number of companies in the biotechnology industry have suffered significant setbacks in every stage of clinical trials, even in advanced clinical trials after positive results in earlier trials. In addition, we have developed a custom bioreactor system in our manufacturing process, and we will not be able to

obtain FDA approval to commercialize Xcellerated T Cells without the FDA’s acceptance of our manufacturing process using this bioreactor system.

To date, the FDA has approved only a few cell-based therapies for commercialization. The FDA recently formed a new division that will regulate biologic products, such as Xcellerated T Cells. The processes and requirements associated with this new division may cause delays and additional costs in obtaining regulatory approvals for our products. Because our Xcellerate Technology is novel, and cell-based therapies are relatively new, regulatory agencies may lack experience in evaluating product candidates like Xcellerated T Cells. This inexperience may lengthen the regulatory review process, increase our development costs and delay or prevent commercialization of Xcellerated T Cells.

In addition, the following factors may impede or delay our ability to obtain timely regulatory approvals, if at all:

| our limited experience in filing and pursuing the applications necessary to gain regulatory approvals; |

9

Risk factors

| any failure to satisfy efficacy, safety or quality standards; |

| any difficulty identifying, recruiting, enrolling and retaining a sufficient number of qualified patients for our clinical trials; |

| · | a decision by us or regulators to suspend or terminate our clinical trials if the participating patients are being exposed to unacceptable health risks; |

| regulatory inspections of our clinical trials or manufacturing facilities, which may, among other things, require us to undertake corrective action or suspend or terminate our clinical trials if investigators find us not to be in compliance with applicable regulatory requirements; |

| our ability to produce sufficient quantities of Xcellerated T Cells to complete our clinical trials; |

| varying interpretations of the data generated from our clinical trials; and |

| changes in governmental regulations or administrative |

Any delays in, or termination of, our clinical trials could materially and adversely affect our development and collaboration timelines, which may cause our stock price to decline. If we do not complete clinical trials for Xcellerated T Cells and obtain regulatory approvals, we will not be able to commercialize Xcellerated T Cells and we may not be able to recover any of the substantial costs we have invested in the development of Xcellerated T Cells.

We have limited manufacturing experience and may not be able to manufacture Xcellerated T Cells on a large scale or in a cost-effective manner.

We currently manufacture Xcellerated T Cells for research and development and our clinical activities in one manufacturing facility in Seattle, Washington. We have not demonstrated the ability to manufacture Xcellerated T Cells beyond quantities sufficient for research and development and limited clinical activities. We have no experience manufacturing Xcellerated T Cells at the capacity that will be necessary to support large clinical trials or commercial sales. We plan to relocate our manufacturing activities to our leased property in Bothell, Washington, which we plan to renovatehave recently renovated for the manufacture of Xcellerated T Cells for our planned clinical trials and, initial commercialization if we receive FDA approval.approval, initial commercialization. However, we may encounter difficulties in obtaining the approvals for and designing, constructing, validating and operating any newthis manufacturing facility. We may also be unable to hire the qualified personnel that we will require to accommodate the expansion of our operations and manufacturing capabilities. If we relocate our manufacturing activities to a new facility during or after a pivotal clinical trial, we will be required to demonstrate to the FDA similarity of the Xcellerated T Cells manufactured in the new facility to the Xcellerated T Cells manufactured in the prior facility to obtain FDA approval. If we cannot adequately demonstrate similarity to the FDA, we could be required to repeat clinical trials, which would be expensive and substantially delay regulatory approval.

Because our Xcellerate Technology is a patient-specific, cell-based product, the manufacture of Xcellerated T Cells is more complicated than the manufacture of most pharmaceuticals. Our present manufacturing process may not meet our initial expectations as to reproducibility, yield, purity or other measurements of performance. In addition, we have recently begunare using a custom bioreactor system in our manufacturing process and only have limited manufacturing experience using this bioreactor system to activate and expand T cells. Because this new manufacturing process is unproven, we may never successfully utilize our custom bioreactor system to commercialize our products. In addition, because some of our prior clinical trials were conducted using a prior version of the manufacturing system, which did not use the custom bioreactor, we may have to show comparability of the Xcellerated T Cells manufactured with the different versions of the manufacturing systems we have used. To show comparability, we may be required to conduct additional clinical trials. If we make additional modifications in our manufacturing process in the future, we may also have to show comparability of newer versions of the manufacturing process. We are currently negotiating a manufacturing and supply agreement with Wave Biotech LLC, the manufacturer of our bioreactor system. If we are unable to successfully negotiate this contract or are unable to procure a suitable alternative manufacturer in a timely manner, we wouldcould face a setback in the development of our manufacturing process. For these and other reasons, we may not be able to manufacture Xcellerated T Cells on a large scale or in a cost-effective manner.

We are the only manufacturer of Xcellerated T Cells. Although we are considering third partythird-party manufacturing options, we expect that we will conduct most of our manufacturing in our own facility for the next several years. Furthermore, because we are the only manufacturer of Xcellerated T Cells and we currently use only one manufacturing facility, any damage to or destruction of our manufacturing

10

Risk factors

facility or our equipment, prolonged power outage, contamination of our facility or shutdown by the

FDA or other regulatory authority could significantly impair or curtail our ability to produce Xcellerated T Cells. In addition, we store our patients’ cells in freezers at our manufacturing facility. If these cells are damaged at our facility, including by the loss or malfunction of these freezers or our back-up power systems, we would need to collect replacement patient cells, which would delay our patients’ treatments. If we are unable to collect replacement cells from our patients, we could incur liability and our business could suffer.

The government and other third-party payors may control the pricing and profitability of our products.

Our ability to commercialize Xcellerated T Cells successfully will depend in part on the extent to which governmental authorities, private health insurers and other organizations establish appropriate reimbursement levels for the cost of Xcellerated T Cells and related treatments. Increasing emphasis on managed care in the United States will continue to put pressure on the pricing of healthcare products. In addition, governmental authorities may establish pricing and reimbursement levels for some disease indications but not others, which may reduce the demand for Xcellerated T Cells and our profitability. Pricing and profitability of healthcare products are also subject to governmental control in some foreign markets. Cost control initiatives could:

| result in lower prices for Xcellerated T Cells or any future products or their exclusion from reimbursement programs; |

| reduce any future revenues we may receive from collaborators; |

| discourage physicians from delivering Xcellerated T Cells to patients in connection with clinical trials or future |

| · | limit off-label use of Xcellerated T Cells. |

We rely on third parties to conduct some of the clinical trials for Xcellerated T Cells, and their failure to timely and successfully perform their obligations to us, or their defective performance, could significantly harm our product development programs.programs and our business.

Because we rely on academic institutions, site management operationsorganizations and clinical research organizations to conduct, supervise or monitor some or all aspects of clinical trials involving our Xcellerate Technology, we have limited control over the timing and other aspects of these clinical trials. If these third parties do not successfully carry out their duties under their agreements with us, fail to inform us if these trials fail to comply with clinical

trial protocols or fail to meet expected deadlines, this may adversely affect our clinical trials and we may not be able to obtain regulatory approvals.

A third party on whom we rely to conduct clinical trials for Xcellerated T Cells could conduct those clinical trials defectively. This could lead to patients experiencing harmful side effects or could prevent us from proving that Xcellerated T Cells are effective, which may result in:

| · | our failure to obtain or maintain regulatory approval; |

| · | physicians not using or recommending our products; and |

| · | significant product liability. |

Xcellerated T Cells may never achieve market acceptance even if we obtain regulatory approvals.

We do not expect to receive regulatory approvals for the commercial sale of any products derived from our Xcellerate Technology for several years, if at all. Even if we do receive regulatory approvals, the future commercial success of Xcellerated T Cells will depend, among other things, uponon its acceptance by physicians, patients, health carehealthcare payors and other members of the medical community as a therapeutic and cost-effective alternative to commercially available products. Because only a few cell-based therapy products have been commercialized, we do not know to what extent cell-based immunotherapy products will be accepted as therapeutic alternatives. If we fail to gain market acceptance, we may not be able to earn sufficient revenues to continue our business. Market acceptance of and demand for any product that we may develop will depend on many factors, including:

| our ability to provide acceptable evidence of safety and efficacy; |

11

Risk factors

| convenience and ease of administration; |

| prevalence and severity of adverse side effects; |

| availability of alternative and competing treatments; |

| cost effectiveness; |

| effectiveness of our marketing and distribution strategy and the pricing of any product that we may develop; |

| publicity concerning our products or competitive products; and |

| our ability to obtain sufficient third-party coverage or reimbursement. |

If Xcellerated T Cells do not become widely accepted by physicians and patients, it is unlikely that we will ever become profitable.

Even if we obtain regulatory approvals for Xcellerated T Cells, those approvals and ongoing regulation of our products may limit how we manufacture and market our products, which could prevent us from realizing the full benefit of our efforts.

If we obtain regulatory approvals, Xcellerated T Cells, theour Xcellerate Technology and our manufacturing facilities will be subject to continual review, including periodic inspections, by the FDA and other USU.S. and foreign regulatory authorities. In addition, regulatory authorities may impose significant restrictions on the indicated uses or marketing of Xcellerated T Cells or other products that we may develop. These and other factors may significantly restrict our ability to successfully commercialize Xcellerated T Cells and theour Xcellerate Technology.

We and many of our vendors and suppliers are required to comply with current Good Manufacturing Practices, or cGMP, which include requirements relating to quality control and quality assurance as well as the corresponding maintenance of records and documentation. Furthermore, our manufacturing facilities must be approved by

regulatory agencies before these facilities can be used to manufacture Xcellerated T Cells, and they will also be subject to additional regulatory inspections. Any material changes we may make to our manufacturing process may require approvalapprovals by the FDA and state or foreign regulatory authorities. Failure to comply with FDA or other applicable regulatory requirements may result in criminal prosecution, civil penalties, recall or seizure of products, partial or total suspension of production or withdrawal of a product from the market.

We must also report adverse events that occur when our products are used. The discovery of previously unknown problems with Xcellerated T Cells or our manufacturing facilities may result in restrictions or sanctions on our products or manufacturing facilities, including withdrawal of our products from the market. Regulatory agencies may also require us to reformulate our products, conduct additional clinical trials, make changes in the labeling of our product or obtain re-approvals. This may cause our reputation in the market place to suffer or subject us to lawsuits, including class action suits.

We rely on third parties to administer Xcellerated T Cells to patients, and our business could be harmed if these third parties administer Xcellerated T Cells incorrectly.

We rely on the expertise of physicians, nurses and other associated medical personnel to administer Xcellerated T Cells to patients. Although our Xcellerate Technology employs mostly standard medical procedures, if these medical professionalspersonnel are not properly trained to administer, or are negligent in the administration of, Xcellerated T Cells, the therapeutic effect of Xcellerated T Cells may be diminished or the patient may suffer critical injury.

12

Risk factors

In addition, third-party medical personnel must thaw Xcellerated T Cells received from us. If this thawing is not performed correctly, the patient may suffer critical injury. While we intend to provide training materials and adequate resources to these third-party medical professionals,personnel, the thawing of Xcellerated T Cells will occur outside our supervision and may not be administered properly. If, due to a third-party error, people believe that Xcellerated T Cells are ineffective or harmful, the desire to use Xcellerated T Cells may decline, which will negatively impact our ability to generate revenue. We may also face significant liability even though we aremay not be responsible for the actions of these third parties.

There are risks inherent in our business that may subject us to potential product liability suits and other claims, which may require us to engage in expensive and time-consuming litigation or pay substantial damages and may harm our reputation and reduce the demand for our product.

Our business exposes us to potential product liability risks, which are inherent in the testing, manufacturing, marketing and sale of biopharmaceutical products. We will face an even greater risk of product liability if we commercialize Xcellerated T Cells. An individual may bring a product liability claim against us if Xcellerated T Cells cause, or merely appear to have caused, an injury. For example,In addition, we have been named as a defendantare licensing our Xcellerate Technology in connection with a clinical trial using technology similarthe field of HIV retroviral gene therapy to ours conducted at the University of Chicago Hospital. This proceeding is currently pending. Although we intendour collaborative partner, Fresenius Biotech GmbH, or Fresenius. We may incur liability and be exposed to vigorously defend this lawsuit, because of the nature of the complaint against us, we cannot predict the probability of a favorable or unfavorable outcome or estimate the amount or range of potential loss. See “Business—Legal proceedings.”claims for products manufactured by Fresenius.

Certain aspects of how Xcellerated T Cells are processed and administered may enhanceincrease our exposure to liability. Our Xcellerate Technology requires us to activate a patient’s T cellsex vivo, or outside of the body, using blood collected from patients. Third partythe patient. Third-party physicians or other medical personnel initially collect a patient’s blood through a process called leukapheresis, which may pose risks, such as bleeding and infection. The blood that we collect from our patients may contain infectious agents that may infect medical personnel or others with whom the blood comes in contact. Medical personnel administer Xcellerated T Cells to patients intravenously in an outpatient procedure. This procedure poses risks to the patient similar to those occurring with infusions of other frozen cell products, such as stem cells, including blood clots, infection and mild to severe allergic reactions.

It is possible that we or third parties may misidentify Xcellerated T Cells and deliver them to the wrong patient. If these misidentified Xcellerated T Cells are administered to the wrong patient, the patient could suffer irreversible injury or death.

The discovery of unforeseen side effects of Xcellerated T Cells could also lead to lawsuits against us. Regardless of merit or eventual outcome, product liability or other claims may, among other things, result in:

| injury to our reputation and decreased demand for Xcellerated T Cells; |

| withdrawal of clinical trial volunteers; |

| costs of related litigation; and |

| substantial monetary awards to plaintiffs. |

We currently have clinical trial insurance that covers our clinical trials up to $5.0 million per occurrence with a $5.0 million aggregate limit, and we intend to obtain product liability coverage in the future. However, due to factors outside of our control, including the risks discussed above as well as conditions in the relevant insurance coveragemarkets, we may not be availableable to us at anrenew or obtain such coverage on acceptable cost,terms, if at all. EvenFurthermore, even if we secure coverage,

13

Risk factors

we may not be able to obtain insurance coverage that will bepolicy limits adequate to satisfy any liability that may arise. If a successful product liability or other claim or series of claims is brought against us for uninsured liabilities or in excess of insured liabilities, our assets may not be sufficient to cover these claims and our business operations could suffer.

If Xcellerated T Cells or components of our Xcellerate Technology alone or in combination with complementary treatments cause unforeseen harmful side effects, physicians may not use our products and/or we may incur significant product liability, which will adversely affect our ability to operate our business.

Xcellerated T Cells or components of our Xcellerate Technology may cause unforeseen harmful side effects. For example, a patient receiving Xcellerated T Cells could have a severe allergic reaction or could develop an autoimmune condition. While we employ procedures to substantially remove the antibodies and beads used to generate Xcellerated T Cells, it is possible that residual antibodies or beads may be infused into patients and cause harmful effects.

In addition, we have not conducted studies on the long-term effects associated with the different types of media that we use to grow and freeze cells as part of our Xcellerate Technology. These media contain substances that have proved harmful if used in certain quantities. While we believe that we use sufficiently small quantities of these substances, harmful effects may still arise from our use of these media. As we continue to develop our Xcellerate Technology, we may encounter harmful side effects that we did not previously observe in our prior studies and clinical trials.

We believe Xcellerated T Cells may be used in combination with complementary treatments, including cancer vaccines, monoclonal antibodies, genes, cytokines or chemotherapy, and one or more of these other therapies could cause harmful side effects that could be attributed to Xcellerated T Cells. Any or all of these harmful side effects may occur at various stages of our product development, including the research stage, the development stage, the clinical stage or the commercial stage of our products. If people believe Xcellerated T Cells or any component of our Xcellerate Technology alone or in combination with complementary treatments causecauses harmful side effects, we may incur significant damages from product liability claims, which will adversely affect our ability to operate our business.

We rely on a limited number of manufacturers and suppliers for some of the key components of our Xcellerate Technology. The loss of these suppliers, or their failure to provide us with adequate quantities of these key components when needed, could delay our clinical trials and prevent or delay commercialization of Xcellerated T Cells.

We rely on third partythird-party suppliers for some of the key components used to manufacture Xcellerated T Cells. We rely on Lonza Biologics PLC, or Lonza, to develop and manufacture the antibodies that we use in our Xcellerate Technology. LonzaEither party may terminate our agreements with Lonza for breach or insolvency of the agreements we have with themother party or if we commit a breach. We are aware of few companies with the abilityLonza is unable to manufacture commercial grade antibodies.perform its obligations for scientific or technical reasons. Our current agreements with

Lonza only provide for manufacturing development and validation, and the creation and submission of materials required to obtain regulatory approval of the antibody manufacturing process. We are using the antibodies supplied by Lonza under the agreements to manufacture of these antibodies for usethe Xcellerated T Cells used in our clinical trials. We are currently negotiating an agreement with Lonza to manufacture the antibodies for commercial use. If we are unable to negotiate this contract with Lonza or are unable to procure a suitable alternative manufacturer in a timely manner and on favorable terms, if at all, we may incur significant costs and be unable to continue developing our Xcellerate Technology. We are aware of few companies with the ability to manufacture commercial-grade antibodies.

Our Xcellerate Technology also depends in part on the successful attachment of the antibodies to magnetic beads. We currently use magnetic beads developed and manufactured by Dynal S.A.A.S., or Dynal, in Oslo, Norway. Our contract with Dynal expires in August 2009, and eitherhas the right to terminate the agreement if we do not purchase a minimum quantity of beads. Either party may terminate the

14

Risk factors

contract agreement as of August 2009 for any reason, or earlier for the material breach.breach or insolvency of the other party. If the agreement is not terminated by August 2009, either party can elect to extend the term of the agreement for an additional 5 years. Otherwise, it will automatically renew on a year to year basis. We are contractually obligated to obtain our beads from Dynal as long asunless Dynal is ableunable to fill our orders.orders or certain other circumstances arise. If Dynal terminates our contract or if Dynal discontinues manufacturing our beads for any reason, we may be unable to find a suitable alternative manufacturer in a timely manner, or at all, which would delay our clinical trials and delay or prevent commercialization of Xcellerated T Cells.