As filed with the Securities and Exchange Commission on July 8,October 7, 2016

Registration No. 333- 333-212449

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 4

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Forterra, Inc.

| Delaware | 3272 | 37-1830464 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

511 East John Carpenter Freeway, 6th Floor

Irving, TX 75062

(469) 458-7973

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Jeff Bradley

Chief Executive Officer

Forterra, Inc.

511 East John Carpenter Freeway, 6th Floor

Irving, TX 75062

tel: (469) 458-7973

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Jeffrey A. Chapman Peter W. Wardle Gibson, Dunn & Crutcher LLP 2100 McKinney Ave., Suite 1100 Dallas, TX 75201 tel: (214) 698-3100 fax: (214) 571-2900 | Joshua Davidson Samantha H. Crispin Baker Botts L.L.P. One Shell Plaza 910 Louisiana Street Houston, TX 77002 tel: (713) 229-1234 fax: (713) 229-1522 |

Approximate date of commencement of proposed sale to the public:As soon as practicable after this registration statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

CALCULATION OF REGISTRATION FEE

|

|

| ||||||||||

Title of Each Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price(1)(2) | Amount of Registration Fee | Amount to be Registered(1) | Proposed Maximum Offering Price Per Unit(2) | Proposed Maximum Aggregate Offering Price(1)(2) | Amount of Registration Fee | ||||||

Common Stock, $0.001 par value per share | $100,000,000 | $10,070 | 21,183,000 | $21.00 | $444,843,000 | $50,037.31(3) | ||||||

|

|

| ||||||||||

|

|

| ||||||||||

| (1) | Includes 2,763,000 shares that the underwriters have the option to purchase. See “Underwriting.” |

| (2) | Estimated solely for the purpose of calculating the registration fee under Rule |

| (3) | $10,070 previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 8,OCTOBER 7, 2016

18,420,000 Shares

Forterra, Inc.

Common Stock

$ per share

This is the initial public offering of our common stock. We are offering shares of our common stock and the selling stockholder identified in this prospectus is offering18,420,000 shares of our common stock. We will not receive any proceeds from the sale of shares by the selling stockholder. Prior to this offering, there has been no public market for our common stock. It is currently estimated that the initial public offering price per share will be between $$19.00 and $ .$21.00.

hasWe and the selling stockholder have each granted to the underwriters an option to purchase up to 1,381,500 additional shares of common stock. We will not receive any proceeds from the sale of shares by the selling stockholder.

We intend to applyhave applied to list our common stock on the NASDAQ Global Select Market under the symbol “ .”“FRTA.”

Investing in our common stock involves risks. See “Risk Factors” beginning on page 2223 to read about factors you should consider before buying shares of our common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

Initial public offering price | $ | $ | ||||||

Underwriting discount(1) | $ | $ | ||||||

Proceeds to us (before expenses) | $ | $ | ||||||

| ||||||||

| (1) | See “Underwriting” for a description of all underwriting compensation payable in connection with this offering. |

The underwriters expect to deliver the shares to purchasers on or about �� , 2016 through the book-entry facilities of The Depository Trust Company.

Joint Book-Running Managers

| Goldman, Sachs & Co. | Citigroup | Credit Suisse | ||

| Barclays | Deutsche Bank Securities | RBC Capital Markets | ||

Co-Managers

| Oppenheimer & Co. | Stephens Inc. | SunTrust Robinson Humphrey | ||

Prospectus dated , 2016

FORTERRA

US PIPE

HP LOK

FORTERRA

| Page | ||||

| 1 | ||||

Unaudited Pro Forma Condensed Combined Financial Information | ||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||||

| F-1 | ||||

We are responsible for the information contained in this prospectus, in any amendment or supplement to this prospectus and in any free-writing prospectus we prepare or authorize. We have not authorized anyone to provide you with different information, and we take no responsibility for and cannot provide any assurance as to the reliability of any other information others may give you. We are not, the selling stockholder is not and the underwriters are not, making an offer to sell shares of our common stock in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than its date.

i

GENERAL INFORMATION

Industry and Market Data

We use market data and industry forecasts throughout this prospectus and, in particular, in the sections entitled “Prospectus Summary” and “Business.” Unless otherwise indicated, statements in this prospectus concerning our industries and the markets in which we operate, including our general expectations, competitive position, business opportunity and market size, growth and share, are based on publicly available information, periodic industry publications and surveys, government surveys and reports, including from the U.S. Census Bureau and the U.S. Environmental Protection Agency, or EPA, and reports by market research firms.

In this prospectus, when we refer to:

We have not independently verified market data and industry forecasts provided by any of these or any other third-party sources referred to in this prospectus, although we believe such market data and industry forecasts included in this prospectus are reliable. This information cannot always be verified with complete certainty due to the limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in surveys of market size.

Management estimates are derived from the information and data referred to above, as well as our internal research, calculations and assumptions made by us based on our analysis of such information and data and our knowledge of our industries and markets, which we believe to be reasonable, although they have not been independently verified. While we believe that the market position information included in this prospectus is generally reliable, such information is inherently imprecise. Assumptions, expectations and estimates of our future performance and the future performance of the industries and markets in which we operate are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the sections entitled “Risk Factors” and “Forward-Looking Statements.” These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties and by us.

ii

Pro Forma Financial Information

In addition to our results presented under U.S. GAAP, or GAAP, in this prospectus we also present certain pro forma financial information that gives effect to the acquisition of our business from HeidelbergCement AG, certain acquisition transactions we have completed following the acquisition of our business from HeidelbergCement AG and certain other transactions, as discussed in greater detail in the section entitled “Unaudited Pro Forma Condensed Combined Financial Information.” As a result of these transactions, our historical financial results do not reflect any impact or the full impact, as applicable, of these transactions, and our management believes it is important to discuss our pro forma financial information because it provides investors with additional context regarding our business. However, our pro forma financial information should not be considered independent of our audited and unaudited combined financial statements and the related notes included elsewhere in this prospectus and the pro forma financial statements included in the section entitled “Unaudited Pro Forma Condensed Combined Financial Information.”

iii

The following is a summary of material information discussed in this prospectus. The summary is not complete and does not contain all of the information that you should consider before investing in our common stock. You should read this entire prospectus carefully, including the risks discussed in the section entitled “Risk Factors” and our audited and unaudited combined Predecessor and Successor financial statements and the related notes, and our unaudited pro forma condensed combined financial information and the related notes, each included elsewhere in this prospectus, before making an investment decision to purchase shares of our common stock. Some of the statements in this summary constitute forward-looking statements. See “Forward-Looking Statements.”

On March 13, 2015, through an indirect wholly owned subsidiary, Lone Star Fund IX (U.S.), L.P. acquired the building products business of HeidelbergCement AG in the United States and Eastern Canada. Unless otherwise specified or where the context otherwise requires, references in this prospectus to “our,” “we,” “us,” the “Company” and “our business” (i) for the Predecessor periods prior to the completion of the acquisition described above, refer to the building products business of HeidelbergCement AG in the United States and Eastern Canada, (ii) for the Successor periods after completion of the acquisition described above, but prior to the internal reorganization transaction described below, the building products business of LSF9 Concrete Holdings Ltd in the United States and Eastern Canada and (iii) for the Successor periods after completion of the internal reorganization transaction in which LSF9 Concrete Holdings Ltd will transfer its building products business in the United States and Eastern Canada to Forterra, Inc., the operations of Forterra, Inc., in each case together with its consolidated subsidiaries. We are a holding company controlled and indirectly owned by Lone Star Fund IX (U.S.), L.P. and have a relatively short operating history as a stand-alone company.

All amounts in this prospectus are expressed in U.S. dollars unless specifically noted otherwise and the financial statements have been prepared in accordance with GAAP.

Our Company

We are a leading manufacturer of pipe and precast products by sales volume in the United States and Eastern Canada for a variety of water-related infrastructure applications, including water transmission, distribution and drainage. We provide critical infrastructure components for a broad spectrum of construction projects across residential, non-residential and infrastructure markets. Our extensive suite of end-to-end products covers “the First Mile to the Last Mile” of the water infrastructure grid, ranging from large diameter pipe that transports water to and from treatment centers and manages drainage along major transportation corridors, to smaller diameter pipe that delivers potable water to, and removes wastewater from, end users in residential and commercial settings. We employ a specialized technical salesforce, including engineers and field service representatives, which enables us to deliver a high degree of customer service, create tailored solutions and ensure our products meet project specifications to maximize applications in the field. We believe that ourOur product breadth, footprint in the United States and Eastern Canada and significant scale help make us a one-stop shop for water-related pipe and products, and a preferred supplier to a wide variety of customers, including contractors, distributors and municipalities.

We are a market leader within eachboth of our three business segments: Drainage Pipe & Products and Water Pipe & Products and Bricks.Products. In 2015, approximatelymore than 75% of our pro forma net sales was generated from our concrete drainage pipe and precast products, ductile iron pipe, or DIP, and concrete pressure pipe products, product categories in which we hold a leading market share position by sales volume in the United States and Eastern Canada.

the United States and Eastern Canada. We are also one of the top manufacturers of bricks in the United States and operate the only commercial brick manufacturing plant in Eastern Canada.

Our manufacturing and distribution network is one of the most extensive in the industry, allowing us to serve most major U.S. and Eastern Canadian markets. We operate 11396 manufacturing facilities and currently have significant additional manufacturing capacity available in eachboth of our segments, providing substantial room to increase production to meet short-cycle demand with minimal incremental investment. These strategically located facilities, which have a significant replacement cost, and our broad distribution network provide us with a local presence and the necessary proximity to our customers to minimize delivery time and distribution costs.

As one of the only companies of scale in our industry that manufactures both water drainage pipe and precast structures (used primarily for stormwater and drainage applications) and water transmission and distribution pipe (used primarily to transport potable water and as a component of wastewater systems), our complementary product portfolio is well positioned to serve both the projected $10.4 billion stormwater and wastewater infrastructure market and the projected $7.9 billion potable water transmission and distribution market, each based on Freedonia projections of 2018 total U.S. market demand. AWWA estimates that nearly $1 trillion will need to be spent from 2010 to 2035 to repair and upgrade aging water infrastructure in the United States. In December 2015, the Fixing America’s Surface Transportation Act, or the FAST Act, was enacted by the U.S. federal government authorizing $305.0 billion of funding over the following five years to upgrade transportation-related infrastructure, more than 70% of which relates to highway spending, which supports a key end market for our Drainage Pipe & Products business due to the stormwater, drainage and related needs associated with highway construction and improvement projects. As “Buy America” provisions become increasingly prevalent under federal law, we believe our domestic manufacturing footprint will be a competitive advantage. Additionally, within the water transmission and distribution markets, Dodge market forecasts suggest that new residential and non-residential construction starts, which remain well below long-term historical averages, are expected to grow from 2015 levels. We believe that our exposure to each of the residential, non-residential and infrastructure end markets will allow us to benefit from both secular and cyclical growth across each of these end markets. The residential, non-residential and infrastructure end markets in the United States and Eastern Canada have different growth drivers and operating dynamics, and the cyclical performance of these markets has historically been staggered during different stages of the broader economic cycle.

For the Predecessor period from January 1, 2015 to March 13, 2015, we generated net sales of $132.6 million, a net loss of $5.8 million and Adjusted EBITDA of $3.3 million, and for the Successor period from March 14, 2015 to December 31, 2015, we generated net sales of $722.7 million, a net loss of $82.8 million and Adjusted EBITDA of $60.2 million. In 2015, we generated pro forma net sales of $1,733.4$1,663.4 million, pro forma net loss from continuing operations of $139.9$76.3 million and pro forma Adjusted EBITDA of $202.5$187.1 million. ProAdjusted EBITDA and pro forma Adjusted EBITDA is aare non-GAAP measure.measures. See the section entitled “Non-GAAP Financial Information” for a description of how we define and calculate Adjusted EBITDA and pro forma Adjusted EBITDA, a reconciliation thereof to pro forma net income (loss) and pro forma income (loss) from continuing operations, respectively, and a description of why we believe this measure isthese measures are important.

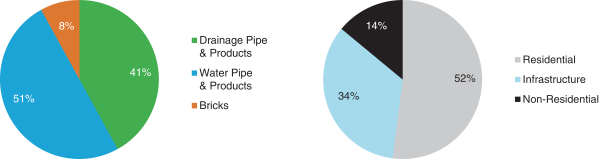

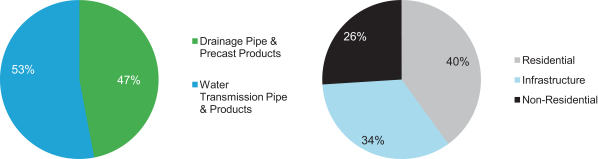

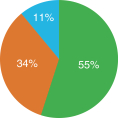

The following charts represent the pro forma net sales contribution by business segment for the 12 months ended December 31, 2015 and an estimated breakdown by end market for the same period. In 2015, excluding our corporate segment, 23% of both our Predecessor and Successor net sales and 53% of our pro forma net sales were generated by our Water Pipe & Products segment; and 61% and 60% of our Predecessor and Successor net sales, respectively, and 47% of our pro forma net sales were generated by our Drainage Pipe & Products segment. In 2015, we estimate that approximately 36% and 39% of our Predecessor and Successor net sales, respectively, and approximately 40% of our pro forma net sales were generated from residential construction activity; approximately 47% and 45% of our

Predecessor and Successor net sales, respectively, and approximately 34% of our pro forma net sales were generated from government-funded infrastructure projects; and approximately 17% and 16% of our Predecessor and Successor net sales, respectively, and approximately 26% of our pro forma net sales were generated from non-residential construction activity.

2015 Pro Forma Net Sales by Segment* and Estimated End Market | ||

| ||

* Excludes Corporate and Other business segment.

Since being acquired from HeidelbergCement AG in 2015, we have undergone a significant transformation to become a leading water infrastructure company throughout the United States and Eastern Canada. As part of this transformation, we have:

Our organic growth strategy is focused on leveraging our low-cost operations, high level of customer service and product innovation capabilities, as well as our product breadth and industry-leading scale, to cross-sell our products to existing customers to increase penetration and project wins and to gain market share through new customers. Operationally, we continue to focus on efficiency and productivity improvements to reduce costs and drive margin improvements.

We have built a strong operating platform and continuously evaluate acquisition opportunities to complement our organic growth and improve our market positions within the markets we serve. Over the past three years, sixseven strategic acquisitions (including three acquisitions completed by U.S. Pipe)

have provided meaningful, ongoing synergy benefits. We believe that our success in acquiring businesses has been the result of our highly disciplined approach, continuous monitoring of potential targets (with a focus on culture and people, among other things), and a market view that Forterra is a strong partner given our scale, culture and recent growth. We believe significant acquisition opportunities at attractive prices are still available given the relatively fragmented landscape in several of the sub-markets in which we operate.

Our Segments

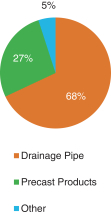

Drainage Pipe & Products. We are the largest producer of concrete drainage pipe and precast products by sales volume in the United States and Eastern Canada. We have 6870 manufacturing facilities across 30 states and two Canadian provinces. We believe our extensive product offering creates a compelling value proposition for our customers as it eliminates the need to engage multiple suppliers of stormwater and wastewater-related products for a single project, thereby maximizing efficiency and allowing our customers to meet more aggressive timetables. We also have the ability to custom-build products to complex specifications and regulations, further enhancing our ability to address customer needs. Our top ten Drainage Pipe & Products customers have an average tenure with us of approximately 17 years. Recently, we acquired concrete pipe and precast and related product manufacturers Cretex and Sherman-Dixie to further enhance our scale, geographic footprint and product portfolio.

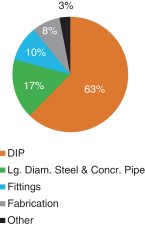

Water Pipe & Products. We are the largest producer of DIP and concrete pressure pipe by sales volume in the United States and Eastern Canada. We offer significant product breadth and depth and technical service, addressing our customers’ full range of water transmission and distribution needs. Our 2826 manufacturing facilities are strategically located across the United States and Eastern Canada, with ample swing capacity available to support increased production levels as demand in the construction industry continues to improve. Furthermore, we believe our expansive distribution network allows us to achieve lead times among the shortest in the industry. Our top ten Water Pipe & Products customers have an average tenure with us of approximately 24 years. Recently, we acquired U.S. Pipe, a market leader within DIP, to diversify our product portfolio and enhance our service offering. U.S. Pipe’s recent acquisition history includes the acquisitions of Griffin Pipe Products Co., LLC, or Griffin Pipe, a manufacturer of DIP, the operations of Metalfit S.A de C.V and Metalfit, Inc., collectively Metalfit, a manufacturer of waterworks fittings and industrial castings, and Custom Fab, Inc., or Custom Fab, a fabricator of pipe primarily for the waterworks industry.

Bricks. We are one of the largest manufacturers of bricks by capacity in the United States and Eastern Canada. We operate 17 manufacturing facilities, strategically located near large population centers or major census Metropolitan Statistical Areas, or MSAs, and raw material reserves. We offer more than 300 core styles of bricks to both residential and non-residential end markets. Our facilities are located in Ontario, Quebec, Kentucky, Michigan, North Carolina, South Carolina and Texas.

|

| |||

|    | |||

|

| |||

|

| |||

|

| |||

|

| |||

|  | |||

| ||||

| Key Segments | Drainage Pipe & Products | Water Pipe & Products | ||

| Products |  |  | ||

| Product Applications | Stormwater and wastewater infrastructure | Potable and wastewater transmission and distribution | ||

| 2018 Estimated U.S. Demand1 | $10.4bn | $7.9bn | ||

| Primary Market Channels | • Direct to Contractors • Distributors | • Distributors • Direct to Contractors, Municipalities and Utilities Waterworks | ||

| # of Manufacturing Facilities | 70 | 26 | ||

| 1 |

| Freedonia—Projected 2018 total market demand. |

Drainage Pipe & Products | Water Pipe & Products | |||

| 2015 Pro Forma Net Sales by Product |  |  | ||

| Primary Market Channels | • Direct to Contractors • Distributors | • Distributors • Direct to Contractors, Municipalities and Utilities Waterworks | ||

| # of Manufacturing Facilities | 68 | 28 | ||

Our Competitive Strengths

Leading Market Positions with Unmatched Scale and Footprint. We believe we are the largest manufacturer in the over $17.0 billion U.S. drainage and water transmission pipe market, as estimated by Freedonia. We believe we are a leader in the following major product categories: concrete drainage pipe and precast products, DIP and concrete pressure pipe. Our industry is relatively fragmented and local in nature due to the transportation costs associated with our products, particularly in the Drainage Pipe & Products business. Our industry has few participants of scale, and we are one of the only sizeable players with significant presence in both the Drainage Pipe & Products and Water Pipe & Products segments, with an extensive portfolio covering “the First Mile to the Last Mile” and a broad geographic footprint. Further, we believe we have one of the most extensive manufacturing and distribution networks in the water transmission and infrastructure industry. We believe our geographic footprint enables us to win more large business projects than our local or regional competitors, as we can provide services to contractors and distributors across geographies and product categories. Additionally, due to our scale, we have purchasing power with suppliers, which reduces our operating costs and enhances our ability to win business in competitive bidding processes.

Well-positioned to Benefit from Attractive Industry Fundamentals. Our exposure to each of the residential, non-residential and infrastructure end markets enables us to capitalize on the growth in demand and recovery in each of these end markets and diversifies our customer base. The construction industry is recovering, fueled by the continuing rebound in infrastructure, residential and non-residential activity. According to AWWA, water infrastructure in the United States will require nearly $1 trillion of investment for repairs and upgrades from 2010 to 2035. The U.S. and Canadian governments are committed to upgrading their aging infrastructure. The FAST Act allocates $305.0 billion to improving surface transportation infrastructure, and in its budget for 2016, the Canadian federal government proposed $11.9 billion (CAD) in infrastructure spending over the next

five years, with $2.0 billion (CAD) in a clean water and wastewater fund and $2.2 billion (CAD) towards water, wastewater and waste management infrastructure. Additional secular industry trends support further infrastructure construction growth, including the growing demand for precast structure products,

environmental regulations supporting on-site water management and continued urbanization. Furthermore, Dodge market forecasts suggest that both residential and non-residential construction starts will grow from 2015 levels, which remain well below the average of the most recent cyclical troughs, and significantly below the average annual starts since 1970. Lastly, we have a presence in each of the 40 most populous MSAs and ten most populous states, enabling us to benefit from the recovery in residential construction.

Complete Suite of Products to Serve Customers from “the First Mile to the Last Mile.” We believe we offer unmatched product breadth and depth compared to our competitors in the United States and Eastern Canada. In our Water Pipe & Products segment, our complementary product portfolio of concrete and steel pressure pipe and DIP addresses the broad range of our customers’ water transmission and distribution needs. Our comprehensive suite of products incorporates large diameter pipe that transports water to treatment plants as well as smaller diameter pipe for distribution to residential users. In our Drainage Pipe & Products segment, our diversified product offering creates a one-stop shop for water-related pipe and products. Our drainage offering creates a compelling value proposition for customers by eliminating the need to seek multiple bids for a single project, helping maximize efficiency for time sensitive orders. Finally, our extensive product offering also creates cross-selling opportunities for our segments due to our broad and diversified customer base.

Attractive and Expanding Margins and Strong Cash Flow Profile. Due to our increasing scale, cost cutting initiatives and our work toward integrating acquisitions, we have generated attractive and increasing margins, capitalizing on our low-cost operations and operating leverage. Our regional and local sales force, strategically located manufacturing facilities and broad distribution network allow us to serve our customers across the United States and Eastern Canada at a competitive cost with efficient procurement and operations. We expect to further increase our scale through acquisitions and, as a result, we expect to continue to generate purchasing power, operating leverage and cost saving opportunities. Furthermore, we have an ongoing strategy of implementing cost-cutting initiatives at our production plants. In the Water Pipe & Products segment, service, procurement and operational initiatives have reduced year to date operating costs by more than $1.5 million in DIP and $1.5 million in large diameter concrete and steel pipe, each asAs of MayAugust 31, 2016. In the Drainage Pipe & Products segment,2016, we have recognized year to date savings of more than $5.0$10 million, as of May 31, 2016 across three major plants due to purchasing initiatives.$9 million and $1 million from procurement, operational and commercial initiatives, respectively. We continue to roll out cost and productivity improvements at new sites and have identified new cost reduction opportunities in resale items, transportation, logistics and energy. Additionally, we have increased our margins and cash flow through operational improvement of acquired businesses. Our acquisition of Sherman-Dixie and U.S. Pipe’s acquisition of Griffin Pipe, specifically, provided consolidation opportunities with our existing plant network and improved the respective cost positions by reducing personnel and rationalizing older facilities.

Proven Ability to Identify, Close and Improve the Performance of Strategic Acquisitions. Over the last three years, we have acquired twothree businesses in our Drainage Pipe & Products segment and four businesses in our Water Pipe & Products segment (including three acquisitions by U.S. Pipe). Our acquisition strategy has been focusedfocuses on three main pillars: reinforce our position in existing markets, expand our product offeringtargets that meet a stringent set of criteria: leading market positions with attractive margins, high growth geographies, potential for synergies and expand our geographic footprint.consolidation, new products and a focus on people development. Acquisitions enable us to improve our product mix and expand our geographic scope, helping us to win business from new customers, cross-sell additional products to existing customers and optimize pricing through the enhanced value created by our differentiated product offering. We believe that our success in acquiring

businesses has been the result of our highly disciplined acquisition strategy, continuous monitoring of potential targets in an opportunity-rich landscape and focus on culture and people, among other things. We have effectively sourced and closed both smaller strategic transactions, and larger transformative deals. In both instances, we have successfully achieved meaningful cost and revenue synergies through the implementation of best practices and operational improvement initiatives in the acquired businesses.

In the instanceconnection with our acquisitions of Cretex, Sherman-Dixie and U.S. Pipe, and U.S. Pipe’s acquisition of Griffin Pipe and Custom Fab, we have realized in excess of $40$45 million of synergies through cost savings.

Experienced Management Team with Proven Ability to Grow Businesses and IntegrateAcquisitions. Our management team, led by Jeff Bradley, our Chief Executive Officer, has a proven track record of increasing shareholder value and generating profitable growth, attractive margins and cash flow. Mr. Bradley and other key executives, including Matt Brown, the Chief Financial Officer, have relevant history managing public companies, as well as extensive experience in the manufacturing industry. Our management team has proven their ability to execute on our acquisition strategy, leading us in growth from $816.2 million ofthrough three substantive acquisitions that almost doubled our 2015 historical net sales by us and our Predecessor on a combined basis (excluding net sales from Cretex) to $1,733.4 million in 2015on a pro forma net sales through three substantial acquisitions.basis. Further, Mr. Bradley and his team are continuing to execute a comprehensive program to drive commercial, operational and procurement excellence, as well as managing working capital to increase free cash flow.

Our Business Strategy

Our goal is to be our customers’ preferred provider of drainage pipe, water transmission pipe and related products. We intend to drive profitable growth in excess of the growth rates of the end markets in which we operate through the following key strategies:

Capitalize on Favorable, Multi-pronged Industry Growth Dynamics. The multi-pronged cyclical recovery in our construction-related end markets is well underway. We expect to benefit from increased demand generated by growth in both residential and non-residential construction activity. Further, there is a significant need to improve North America’s aging water and highway infrastructure. Operationally, we believe we are well positioned in the water transmission and distribution industry to capitalize on the increased funding allocated to water infrastructure improvement. The FAST Act will be a key underlying driver for our business as it dedicates more than 70% of its total budget to highway spending, supporting our key infrastructure end market. Secular industry trends, including the continued shift in product preference to rigid and zinc-coated pipe, environmental regulations in support of on-site water management and continued urbanization, support further incremental growth. Our reputation, extensive product offering and coast-to-coast distribution network provide us with competitive advantages that we expect will fuel growth in excess of that offered by already attractive market dynamics underlying our businesses.

Increase Market Share by Leveraging Our Scale, “the First Mile to the Last Mile” Suite of Products and Go-to-Market Strategy. Our scale enables us to be among the industry’s lowest cost producers, while our strategically located manufacturing facilities and broad distribution network allowus to meet the particular needs of our customers. Our existing swing capacity enables us to meet customer demand and well positions us to win small and large projects. Moreover, our large and scalable installed asset base will allow us to respond swiftly to growing demand without having to increase capacity.

Our “First Mile to the Last Mile” product portfolio enables us to be a complete solutions provider and to serve as a one-stop shop for water-related pipe and products, increasing our customers’ overall

spend on our products. Our ability to offer both pipe and precast products helps us better serve our infrastructure-related markets and differentiates us from our competitors.

Our go-to-market strategy is based on three main pillars. First, we incentivize our highly specialized technical salesforce to focus on profitable growth while offering our products and value-added services. Second, we target our key customers with a robust cross-selling sales organization,

marketing the benefits of ordering from one supplier. Lastly, we focus on the implementation of systematic pricing strategies across all of our product categories.

Leverage Our Commitment to Product Innovation and Technical Expertise to Optimize Product Mix and Capitalize on Market Opportunities. We continuously explore new applications for our existing product portfolio and develop new products and solutions that allow us to stay at the forefront of the needs of the drainage and water pipe and products markets. Our technical salesforce also proactively reaches out to our customers on a regular basis to ensure that our customers are satisfied and our products adhere to project specifications. We have a long history of developing and seeking out innovative products to bring to market across both water-related segments, which include the recent introductions of Oystercrete, duct bank and metallic zinc coating. We will continue our innovation efforts, optimizing our portfolio through research and development and strategic acquisitions to expand our positions in attractive products and markets. Along with these initiatives, our specialized technical salesforce will continue to promote and support our existing specialty products to drive differentiation and growth.

Enhance Margins, Free Cash Flow and Returns Through Operational and Commercial Excellence. We have successfully launched multiple operational initiatives focused on increasing plant efficiency and productivity. We expect to continue growing our margins through ongoing operational, commercial and cultural initiatives. We are working to leverage our information technology and financial systems to lower costs and implement systematic pricing across our business. We will continue to manage working capital and seek scale-driven procurement efficiency improvements through centralized purchasing and fixed overhead control and reduction. We intend to prioritize opportunities that generate attractive returns on invested capital. Further, our management team has emphasized a strong pay-for-performance culture that cultivates, challenges and compensates employees based on profitability and cash flow generation.

Accelerate Profitable Growth Through Strategic Acquisitions. We believe that the relative fragmentation of some of our sub-markets creates an environment in which we can continue to acquire companies at attractive valuations to increase our scale, product breadth and geographic diversity. Over the past three years, we have acquired sixseven businesses—both tuck-in and transformative in nature—within the water drainage and transmission industry (including three acquisitions by U.S. Pipe). We continuously monitor potential targets to develop and maintain a diversified and actionable acquisition pipeline. Additional acquisitions would enable us to add adjacent products to our portfolio that could help us further penetrate our existing markets and expand our geographic footprint. By integrating these businesses and implementing our culture and operational best practices, we believe we can achieve significant further growth. We are focused on driving synergies, including those achievable as a result of our recent acquisitions, to reduce costs and increase our margins. We are in the process of executing a plan associated with our acquisitions of Cretex, Sherman-Dixie and U.S. Pipe. We believe that we can achieve significant synergies associated with these acquisitions. We expect cost savings synergies to come from procurement, eliminating redundant selling, general and administrative functions, and optimizing our plant network through consolidations to achieve operational efficiencies and freight cost reductions. In addition, we believe the U.S. Pipe Acquisition creates opportunity to increase market share in large diameter DIP by leveraging our geographic scope, cross-selling capabilities and existing contractor relationships.

Our Industry

In the United States and Eastern Canada, we are a market leader in each of the following core product categories: concrete drainage pipe and precast, ductile iron pipe and concrete pressure pipe.

Core Products

Drainage Pipe & Products

Drainage pipe has residential, non-residential and infrastructure applications. It is primarily used for storm water applications such as storm drains for roads and highways and for residential and non-residential site developments. In addition, drainage pipe and concrete precast structures are used for sanitary sewers, low-pressure sewer force mains, tunneled systems, treatment plant piping and utility tunnels. Freedonia estimates U.S. total market demand for sewer and drainage pipe and wastewater concrete precast structures to grow at a compound annual growth rate, or CAGR, of 7.4% from $7.2 billion in 2013 to $10.4 billion in 2018. We serve these markets primarily through our diverse portfolio of concrete drainage pipe, U.S. demand for which is expected to increase at a CAGR of 5.9% from 2013 to 2018, according to Freedonia estimates. Further, we serve the aforementioned markets with various precast structures, the demand for which Freedonia estimates to grow at a CAGR of 6.4% from 2013 to 2018. Rebounding levels of construction activity, replacement of aging stormwater and highway infrastructure and committed government funding programs are expected to support this growth. We typically sell our drainage pipe and precast concrete products to contractors that perform construction work for governments, residential and non-residential building owners and developers in markets across the United States and Eastern Canada.

Water Pipe & Products

Water pipe and products are primarily used for potable and wastewater transmission. Water transmission pipe demand comes from water supply construction, especially within municipalities and residential construction. Among these applications, potable water is expected to maintain the largest portion of U.S. demand, with projected growth at a CAGR of 8.2% from $5.3 billion in 2013 to $7.9 billion in 2018, according to Freedonia estimates. We serve these markets primarily through our diverse offering of DIP, prestressed concrete cylinder pipe and bar-wrapped pipe, as well as fittings and fabricated products.

Ductile iron inhibits corrosion, retains strength and prevents fractures better than cast iron and most other materials. Ductile iron also improves water flow compared to other materials, particularly plastic. U.S. market volume for DIP shipments (less than 24” diameter pipe) is expected to increase at a CAGR of 6.1% from 2013 to 2018, based on the key drivers of housing starts and waterline infrastructure spend, according to Freedonia estimates.

In larger diameters (greater than 24” diameter pipe), steel and concrete pipe are sturdier and more cost effective. Plastic pipe structural integrity is more dependent on firm soil bedding than concrete or steel, which can make engineers reluctant to use plastic in large diameters due to the increased installation cost. U.S. market demand for large diameter steel and concrete pipe is expected to increase at a CAGR of 4.6% from 2013 to 2018, based on increasing government spending on water infrastructure, according to Freedonia estimates.

Bricks

Our Bricks operations primarily serve the residential markets. Recovery in single family housing construction represents the largest driver of overall brick demand growth. The estimated demand for bricks in the United States and Eastern Canada is expected to grow at a CAGR of 11% from $1.3 billion in 2013 to $2.1 billion in 2018, according to Freedonia estimates. We are well-positioned to benefit from expected increases in residential housing starts and attractive market dynamics due to our competitive positioning and broad geographic footprint.

Core End Markets

North American water infrastructure, aging and strained by a growing population, requires substantial, prolonged capital investment totaling nearly $1 trillion across the U.S. according to the AWWA. According to the EPA, the U.S. potable water and waste and storm water infrastructures require a cumulative $682 billion investment in repairs and expansions over the next 20 years, with pipe representing a substantial proportion of the total capital need. In Canada, per the Canadian Infrastructure Report Card, or CIRC, the replacement value for water infrastructure in “fair” to “very poor” condition areas totals $173.0 billion (CAD), where “fair” assets are defined as those with indicated deterioration and deficiencies and require attention and “very poor” assets are defined as near or beyond expected service life and unfit for sustained service, indicating that infrastructure reinvestment lags behind targeted levels.

We serve a range of infrastructure-related end markets. Based on the source of funding, we classify these construction markets into infrastructure, residential and non-residential.

Infrastructure

We estimate that 2015 sales to the infrastructure market represented 31%47% and 45% of our PredecessorandSuccessor net sales, respectively, and 34% of our pro forma net sales in fiscal year 2015.sales. Our main sales drivers in this market include the construction of streets, highways and storm and sanitary sewers. WeThough based on U.S. Census data and information from the CBO annual federal spending on transportation and water infrastructure hit a 30-year low on a per capita basis in 2014, we expect to benefit from several drivers in this market, as U.S. and Canadian federal funding dynamics and public infrastructure requirements support continued growth. At the U.S. federal level, the FAST Act demonstrates the U.S. government’s commitment to improving the country’s transportation infrastructure. More than 70% of the law’s budget is dedicated to highway spending, providing multi-year visibility on federal highway funding. As a U.S.-based company, we are well-positioned to benefit from this new spending, as the legislation steps up federal “Buy America” requirements from 60% in 2015 to 70% in 2020. In its budget for 2016, the Canadian federal government proposed $11.9 billion (CAD) in infrastructure spending over the next five years, with $2.0 billion (CAD) in a clean water and wastewater fund and $2.2 billion (CAD) towards water, wastewater and waste management infrastructure.

Residential Construction

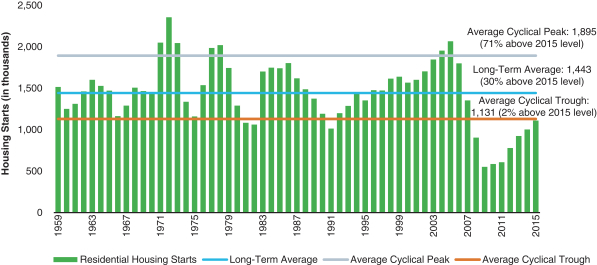

We estimate that 2015 sales to the residential construction market represented 51%36% and 39% of our PredecessorandSuccessor net sales, respectively, and 40% of our pro forma net sales in 2015.sales. These revenues were largely driven by new U.S. residential construction, which is recovering from historic lows reached during the financial crisis. Though new housing starts grew at a CAGR of 14% from 2010 to 2015, according to the U.S. Census Bureau, current levels remain substantially below long-term averages, as outlined in the graph below.

U.S. Residential Housing Starts

Source: U.S. Census Bureau.

The new residential construction market is expected to continue to grow at a robust pace over the next few years, with Fannie Mae and CMHC forecasting a CAGR of 8% from 2015 to 2017 across the United States and Canada.

Non-residential Construction

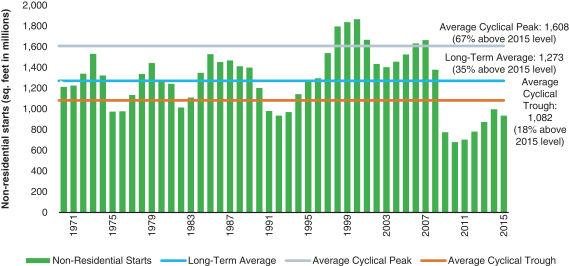

We estimate that 2015 sales to the non-residential construction market represented 18%17% and 16% of our PredecessorandSuccessor net sales, respectively, and 26% of our pro forma net sales in 2015.sales. These revenues were driven largely by new U.S. non-residential construction, and we believe we will continue to benefit from this market’s ongoing recovery from historical lows reached during the financial crisis. Though new non-residential construction starts grew, according to Dodge, at a CAGR of 7% from 2010 to 2015, current levels remain substantially below long-term average levels, as outlined in the graph below.

U.S. Non-Residential Starts

Source: Dodge and CMD Group

The non-residential construction market is expected to continue to grow at a CAGR of 8% from 2015 to 2017 across the United States and Canada, according to data from Dodge and CMD Group.

Recent Developments

Preliminary Financial Results for the Three Months Ending September 30, 2016

The following preliminary financial results for the three months ending September 30, 2016 do not include the results of J&G and Precast Concepts, which the Company entered into definitive agreements to acquire in September 2016, but which acquisitions have not closed; includes only partial results of Bio Clean, which the Company acquired on August 4, 2016; and includes results for the Company’s bricks business, which the Company will distribute to an affiliate prior to the consummation of this offering. See “—Our History—Recent Transactions.”

We estimate that for the three months ended September 30, 2016, we will generate net sales of between $464.0 million and $484.0 million, income from operations, including our corporate segment, of between $45.0 million and $50.0 million and Adjusted EBITDA, including our corporate segment, of between $80.0 million and $85.0 million. Results for the quarter ending September 30, 2016 were negatively affected by significant adverse weather, which caused certain deliveries to be delayed, and other project delays.

In our Drainage Pipe & Products segment, we estimate that for the three months ended September 30, 2016, we will generate net sales of between $211.0 million and $219.0 million, income from operations of between $36.0 million and $38.0 million and Adjusted EBITDA of between $46.0 million and $48.0 million.

In our Water Pipe & Products segment, we estimate that for the three months ended September 30, 2016, we will generate net sales of between $215.0 million and $223.0 million, income from operations of between $23.0 million and $25.0 million and Adjusted EBITDA of between $41.0 million and $43.0 million.

In our Bricks segment, we estimate that for the three months ended September 30, 2016, we will generate net sales of between $38.0 million and $42.0 million, income from operations of between $2.5 million and $3.5 million and Adjusted EBITDA of between $5.0 million and $6.0 million.

In addition to net sales, we have also presented an estimated range for Adjusted EBITDA for the periods referenced above. Adjusted EBITDA is a non-GAAP financial measure and is being presented as a supplemental measure of financial performance that is not required by, or presented in accordance with, GAAP. We calculate Adjusted EBITDA as net income (loss) before interest expense, income tax benefit (expense), depreciation and amortization, and further adjusted for impairment and restructuring charges, gains or losses on the sale of property, plant and equipment, acquisition-related costs and costs associated with disposed sites.

We believe providing an estimated range of Adjusted EBITDA is important to an investor’s understanding of our performance for the reasons described in “Non-GAAP Financial Information,” notwithstanding that we are not yet able to provide any estimate of our net income, the most directly comparable GAAP financial measure, for the relevant periods.

We are not able to provide a reconciliation of Adjusted EBITDA to net income because we cannot quantify certain materially significant amounts that are necessary to calculate net income without unreasonable efforts. Specifically, we are unable to estimate our income tax (expense) benefit for the period ended September 30, 2016 as we have not completed an estimate thereof because we have not completed our evaluation of the impact of recent transactions on income tax (expense) benefit for the period. We expect the variability of our income tax (expense) benefit could have a potentially significant impact on our future GAAP financial results.

We have presented ranges for net sales, income from operations and Adjusted EBITDA above, instead of specific numbers, as our results of operations for such period are not yet available. Our expected results above reflect our current estimates for such period based on information available as of the date of this prospectus, and management prepared such estimated financial information in good faith based upon our internal reporting. However, although we have not identified any unusual or unique events or trends that occurred during the period which might materially affect these estimates, our estimates of results are inherently uncertain and subject to change, and we undertake no obligation to update this information. These estimates are forward-looking statements. Actual results remain subject to the completion of management’s final review, other quarterly financial closing procedures and the completion of the preparation of our interim consolidated financial statements. Our actual consolidated financial statements and related notes as of and for the period ending September 30, 2016 are not expected to be filed with the SEC until after this offering is completed. During the course of the preparation of these actual consolidated financial statements and related notes, additional items that may require adjustments to the preliminary estimated financial results presented above could be identified, and such adjustments could be material. See “Risk Factors—Risks Relating to Our Business and Industry” and “Forward-Looking Statements.”

This preliminary financial data has been prepared by and are the responsibility of our management. Our independent registered public accounting firm, Ernst & Young LLP, has not audited, reviewed or performed any procedures with respect to the preliminary financial data. Accordingly, Ernst & Young LLP does not express an opinion or any other form of assurance with respect thereto.

Our History

The Acquisition

On March 13, 2015, through an indirect wholly owned subsidiary, Lone Star Fund IX (U.S.), L.P. acquired the building products business of HeidelbergCement AG, or HeidelbergCement in the United States and Eastern Canada, or the Acquisition, along with HeidelbergCement’s building products business in the United Kingdom for aggregate consideration of $1.33 billion. The aggregate purchase price is subject to a potential earn outearn-out capped at $100.0 million, which is subject to a dispute with HeidelbergCement as discussed in greater detail in the section entitled “Business—Legal Proceedings.” Following the Acquisition, the acquired businesses were operated by LSF9 Concrete Holdings Ltd, or Concrete Holdings, an indirect wholly owned subsidiary of Lone Star Fund IX (U.S.), L.P.

Recent Transactions

A number of strategic transactions have been completed since the Acquisition. These transactions include:

| • | Cretex Acquisition—On October 1, 2015, the Company acquired Cretex, a manufacturer of concrete pipe, box culverts, concrete precast drainage structures, pre-stressed bridge components and ancillary precast products in the Upper Midwestern United States, for aggregate consideration of $245.1 million, or the Cretex Acquisition. Cretex operates as part of our Drainage Pipe & Products segment. |

| • | Sherman-Dixie Acquisition—On January 29, 2016, the Company acquired Sherman-Dixie, a manufacturer of concrete pipe, box culverts, precast concrete utility products, storm and sanitary civil engineered systems and specialty engineered retainage systems in Kentucky, Tennessee, Alabama and Indiana, for aggregate consideration of $66.8 million, or the Sherman-Dixie Acquisition. Sherman-Dixie operates as part of our Drainage Pipe & Products segment. |

| • | Forterra UK IPO—On April 26, 2016, Concrete Holdings completed an initial public offering of the ordinary shares of Forterra, plc, the operator of HeidelbergCement’s former building products business in the United Kingdom, or Forterra UK. Though we and Forterra UK are both controlled by Lone Star Fund IX (U.S.), L.P., we have no relation to or affiliation with Forterra UK other than certain contractual arrangements regarding third-party IT services and the use of the “Forterra” name. |

| • | U.S. Pipe Acquisition—On April 15, 2016, the Company acquired U.S. Pipe, which manufactures ductile iron pipe products for water distribution and water management applications and distributes its products throughout the United States, for aggregate consideration of $775.1 million, subject to customary working capital adjustments, or the U.S. Pipe Acquisition. U.S. Pipe operates as part of our Water Pipe & Products segment. |

| • | Bio Clean Acquisition—On August 4, 2016, the Company acquired Bio Clean, which designs and sells storm water management systems that meet the requirements of local regulatory bodies regulating storm water quality, for aggregate consideration of $30.0 million, or the Bio Clean Acquisition. Bio Clean also owns or has applied for more than 20 patents for a variety of technologies relating to drainage and storm water management. Bio Clean operates as part of our Drainage Pipe & Products segment. |

| • | Bricks Disposition—On August 23, 2016, LSF9 Concrete Mid-Holdings Ltd, or Mid Holdings, which is wholly owned by Concrete Holdings, entered into an agreement with an unaffiliated third party to contribute our bricks business to a newly formed joint venture with the unaffiliated |

third party, or the Bricks Joint Venture. In exchange for the contribution of our bricks business, Mid Holdings will receive a 50% interest in the Bricks Joint Venture. In connection with this agreement, prior to the consummation of this offering, we will distribute our bricks business to Mid Holdings or its affiliate, or the Bricks Disposition. Though both our business and the 50% equity interest in the Bricks Joint Venture will be held by Mid Holdings or its affiliate, following the Bricks Disposition, we will no longer have any profit or other interest in our then-former bricks business or in the Bricks Joint Venture and we will have no relation to or business affiliation with our then-former bricks business or the Bricks Joint Venture other than contractual arrangements regarding certain limited transition services, the short-term loan described under “Certain Relationships and Related Party Transactions—Loan to Bricks Business” and the temporary use of the “Forterra” name. |

| • | J&G Acquisition—On September 6, 2016, we entered into a definitive agreement to acquire J&G Concrete Operations, LLC, or J&G, a manufacturer of concrete pipe, box culverts and special fittings in North Texas, for aggregate consideration of $32.0 million, subject to customary working capital adjustments, or the J&G Acquisition. The J&G Acquisition is subject to customary closing conditions and is expected to close in the fourth quarter of 2016. J&G will operate as part of our Drainage Pipe & Products segment following completion of the acquisition. |

| • | Precast Concepts Acquisition—On September 7, 2016, we entered into a definitive agreement to acquire the business of Precast Concepts, LLC, or Precast Concepts, a manufacturer of concrete pipe, box culverts, storm detention systems and other precast concrete and related products in Colorado, for aggregate consideration of $97.1 million, subject to customary working capital adjustments, or the Precast Concepts Acquisition. The Precast Concepts Acquisition is subject to regulatory approval and other customary closing conditions and is expected to close in the fourth quarter of 2016. Precast Concepts will operate as part of our Drainage Pipe & Products segment following completion of the acquisition. |

Each of the Company’s recent acquisition and disposition transactions is discussed in greater detail in the section entitled “Business—Our Recent Strategic Transactions.”

Reorganization

Forterra, Inc., the registrant whose name appears on the cover page of this prospectus, does not currently have any operations and was formed in 2016 for the purpose of an internal reorganization transaction. Prior to or concurrent with the consummation of this offering, Concrete Holdings will transfer its building products operations in the United States and Eastern Canada, the business which

is described in this prospectus and the business for which historical and pro forma financial information is included elsewhere in this prospectus, in an internal reorganization transaction, or the Reorganization, to Forterra, Inc. Following the Reorganization, Forterra, Inc. will be a wholly owned subsidiary of LSF9 Concrete Mid-Holdings Ltd, or MidForterra US Holdings, LLC, which is indirectly wholly owned by Concrete Holdings. Each of Concrete Holdings, MidForterra US Holdings, LLC and Forterra, Inc. are affiliates of Lone Star Fund IX (U.S.), L.P. Shares of common stock of Forterra, Inc. are being offered by the prospectus.

Our Sponsor

Lone Star Fund IX (U.S.), L.P., which we refer to in this prospectus, along with its affiliates and associates (including Concrete Holdings, and Mid Holdings and Forterra US Holdings, LLC, but excluding us and other companies that it owns as a result of its investment activity), as Lone Star or our sponsor, is part of a leading private equity firm that, since the establishment of its first fund in 1995, has organized 16 private equity funds with aggregate capital commitments totaling over $65.0 billion. The funds are structured as closed-end, private-equity limited partnerships, the limited partners of which

include corporate and public pension funds, sovereign wealth funds, university endowments, foundations, funds of funds and high net worth individuals. Immediately prior to this offering, Lone Star owned all of our outstanding common stock, and will own approximately %71.1% of our common stock immediately following consummation of this offering (or %67.5% if the underwriters exercise in full their option to purchase additional shares). Therefore, we expect towill be a “controlled company” under the applicable stock exchange corporate governance standards of the NASDAQ Global Select Market, or NASDAQ, and will take advantage of the related corporate governance exceptions for controlled companies.

Risks Affecting Our Business

Our business is subject to numerous risks and uncertainties, including, but not limited to, those arising from:

We are also subject to numerous risks relating to:

You should carefully consider all of the information set forth in this prospectus and, in particular, the information in the section entitled “Risk Factors” beginning on page 2223 of this prospectus prior to making an investment in our common stock. These risks could, among other things, prevent us from successfully executing our strategies and could have a material adverse effect on our business, financial condition and results of operations.

Principal Executive Offices

Our principal executive offices are located at 511 East John Carpenter Freeway, 6th Floor, Irving, TX 75062 and our telephone number is (469) 458-7973. Our website address is forterrabp.com. Information contained on our website or linked therein or otherwise connected thereto does not constitute part of nor is it incorporated by reference into this prospectus or the registration statement of which this prospectus forms a part. Forterra, U.S. Pipe and other trademarks or service marks of ours appearing in this prospectus are our property. Other trademarks and service marks appearing in this prospectus are the property of their respective holders.

THE OFFERING

Common stock offered by us | 18,420,000 shares (or 19,801,500 shares if the underwriters exercise in full their option to purchase additional shares) | |

Common stock offered by the selling stockholder | 1,381,500 shares if the underwriters exercise in full their option to purchase additional shares | |

Common stock to be outstanding immediately after this offering | 63,789,474 shares (or 65,170,974 shares if the underwriters exercise in full their option to purchase additional shares) | |

Use of proceeds | We estimate our proceeds from this offering will be approximately | |

We will not receive any of the proceeds from the sale of shares of common stock by the selling stockholder. See “Use of Proceeds,” “Principal and Selling Stockholders” and “Underwriting.” | ||

Dividend policy | We have no present intention to pay cash dividends on our common stock. Any determination to pay dividends to holders of our common stock will be at the discretion of our board of directors and will depend upon many factors, including our financial condition, results of operations, projections, liquidity, earnings, legal requirements, restrictions in our debt agreements and other factors that our board of directors deems relevant. See “Dividend Policy.” | |

Risk factors | You should carefully read and consider the information set forth in the section entitled “Risk Factors” beginning on page | |

Conflicts of interest | In connection with the repayment of the Junior Term Loan with the net proceeds from this offering, Credit Suisse Securities (USA) LLC, Citigroup Global Markets Inc. and Deutsche Bank Securities Inc., each an underwriter in this offering, or their affiliates, are expected to receive, in the aggregate, payments representing less than 5%, of the net proceeds of this offering. See “Use of Proceeds” and “Underwriting—Conflicts of Interest.” | |

NASDAQ symbol | “ | |

The number of shares of our common stock to be outstanding immediately after this offering as set forth above is based on the number of shares outstanding as of , 2016 and excludes 5,000,000 shares reserved for issuance under our equity incentive plan (under which no equity awards have been granted as of such date). We intend to grant equity awards representing an aggregate of approximately 498,490 shares of common stock to our executive officers and certain director nominees under our equity incentive plan at the time of the pricing of this offering.

Unless otherwise indicated, this prospectus:

SUMMARY HISTORICAL AND UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL AND OTHER INFORMATION

The following tables set forth, for the periods and dates indicated certain summary historical and unaudited pro forma condensed combined financial information. The accompanying historical audited financial statements are presented for the “Predecessor,” which are the combined financial statements of HeidelbergCement’s building products business in the United States and Eastern Canada for the period preceding the Acquisition, and the “Successor,” which are the combined audited and unaudited financial statements of the Company and subsidiaries for the period following the Acquisition. The Predecessor’s combined statements of operations data for the years ended December 31, 2013 and 2014 and the period from January 1, 2015 through March 13, 2015 and the Predecessor’s combined balance sheet data as of December 31, 2014 have been derived from the audited combined financial statements of HeidelbergCement’s building products business in the United States and Eastern Canada, which are included elsewhere in this prospectus. The Successor’s combined statements of operations data for the period from March 14, 2015 through December 31, 2015 and balance sheet data as of December 31, 2015 have been derived from our audited financial statements, which are included elsewhere in this prospectus. The Successor’s combined balance sheet data as of March 31,June 30, 2016 and condensed combined statements of operations data for the period from March 14, 2015 through March 31,June 30, 2015 and the threesix months ended March 31,June 30, 2016 are derived from our unaudited condensed combined financial statements, which are included elsewhere in this prospectus.

The Predecessor’s financial statements may not necessarily be indicative of the cost structure or results of operations that would have existed if HeidelbergCement’s building products business in the United States and Eastern Canada operated as a stand-alone, independent business. Accordingly, these historical results should not be relied upon as an indicator of our future performance. The Acquisition was accounted for as a business combination, which resulted in a new basis of accounting. The Predecessor’s and the Successor’s historical financial statements are not comparable as a result of applying a new basis of accounting. See the notes to the audited financial statements for additional information regarding the accounting treatment of the Acquisition. In the opinion of management, the unaudited interim financial statements include all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of our financial position and operating results for these periods and as of such date. Results from interim periods are not necessarily indicative of results that may be expected for the entire year and historical results are not indicative of the results to be expected in the future. The summary financial and operating data presented below represent portions of our financial statements and are not complete.

The unaudited pro forma condensed combined financial information set forth below presents certain unaudited pro forma condensed combined statements of operations data for the threesix months ended March 31,June 30, 2016 and 2015 and for the year ended December 31, 2015, and certain unaudited pro forma condensed combined balance sheet data as of March 31,June 30, 2016. The unaudited pro forma condensed combined financial information has been derived by aggregating our audited and unaudited historical combined financial statements, and the historical financial statements of U.S. Pipe, each included elsewhere in this prospectus, and making certain pro forma adjustments to such aggregated financial information to give effect to the transactions discussed in greater detail in the section entitled “Unaudited Pro Forma Condensed Combined Financial Information.”

The information presented below should be read in conjunction with the sections entitled “Capitalization,” “Selected Historical Financial Data,” “Unaudited Pro Forma Condensed Combined Financial Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited and unaudited combined financial statements and related notes included elsewhere in this prospectus.

| (in thousands) | (in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Pro forma Three months ended March 31, 2016 | Pro forma Three months ended March 31, 2015 | Pro forma Year ended December 31, 2015 | Successor | Predecessor | Successor | Predecessor | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

(in thousands) | Three months ended March 31, 2016 | For the period from March 14, 2015 to March 31, 2015 | For the period from March 14, 2015 to December 31, 2015 | For the period from January 1, 2015 to March 13, 2015 | Year ended December 31, 2014 | Year ended December 31, 2013 | Pro forma Six months ended June 30, 2016 | Pro forma Six months ended June 30, 2015 | Pro forma Year ended December 31, 2015 | Six months ended June 30, 2016 | For the period from March 14, 2015 to June 30, 2015 | For the period from March 14, 2015 to December 31, 2015 | For the period from January 1, 2015 to March 13, 2015 | Year ended December 31, 2014 | Year ended December 31, 2013 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Statement of Operations Data: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Statement of Operations Data | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Net sales | $ | 362,083 | $ | 340,654 | $ | 1,733,373 | $ | 217,334 | $ | 38,014 | $ | 722,664 | $ | 132,620 | $ | 736,963 | $ | 697,948 | $ | 783,112 | $ | 764,172 | $ | 1,663,363 | $ | 640,142 | $ | 251,315 | $ | 722,664 | $ | 132,620 | $ | 736,963 | $ | 697,948 | ||||||||||||||||||||||||||||||||||||||||||

Cost of goods sold | (295,772 | ) | (308,288 | ) | (1,474,743 | ) | (179,403 | ) | (35,324 | ) | (626,498 | ) | (117,831 | ) | (631,454 | ) | (611,660 | ) | 628,627 | 654,856 | 1,396,432 | 509,370 | 228,405 | 626,498 | 117,831 | 631,454 | 611,660 | |||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Gross profit | $ | 66,311 | $ | 32,366 | $ | 258,630 | $ | 37,931 | $ | 2,690 | $ | 96,166 | $ | 14,789 | $ | 105,509 | $ | 86,288 | $ | 154,485 | $ | 109,316 | $ | 266,931 | $ | 130,772 | $ | 22,910 | $ | 96,166 | $ | 14,789 | $ | 105,509 | $ | 86,288 | ||||||||||||||||||||||||||||||||||||||||||

Selling, general and administrative expenses | (60,415 | ) | (69,102 | ) | (271,253 | ) | (37,945 | ) | (18,722 | ) | (134,971 | ) | (21,683 | ) | (102,107 | ) | (87,393 | ) | (118,809 | ) | (129,692 | ) | (275,020 | ) | (98,622 | ) | (47,716 | ) | (134,971 | ) | (21,683 | ) | (102,107 | ) | (87,393 | ) | ||||||||||||||||||||||||||||||||||||||||||

Impairment and restructuring charges | — | — | — | — | 8 | (1,185 | ) | (542 | ) | (4,219 | ) | (250,577 | ) | — | — | — | (23 | ) | (343 | ) | (1,185 | ) | (542 | ) | (4,219 | ) | (250,577 | ) | ||||||||||||||||||||||||||||||||||||||||||||||||||

Earnings from equity method investee | — | — | — | 1,303 | 115 | 8,429 | 67 | 4,451 | (216 | ) | — | — | — | 4,868 | 3,772 | 8,429 | 67 | 4,451 | (216 | ) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Other operating income | 3,081 | 1,455 | 12,200 | 1,778 | 813 | 832 | 994 | 6,965 | 9,232 | 9,244 | 8,878 | 14,455 | 2,533 | 3,930 | 832 | 994 | 6,965 | 9,232 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Interest expense | (30,557 | ) | (30,562 | ) | (122,891 | ) | (17,290 | ) | (2,474 | ) | (45,953 | ) | (84 | ) | — | — | (30,413 | ) | (25,934 | ) | (53,305 | ) | (42,129 | ) | (15,551 | ) | (45,953 | ) | (84 | ) | — | — | ||||||||||||||||||||||||||||||||||||||||||||||

Other income (expense), net | 23 | (21 | ) | 981 | (81 | ) | — | (326 | ) | (39 | ) | (594 | ) | 947 | (1,003 | ) | (207 | ) | 1,205 | (1,179 | ) | (140 | ) | (326 | ) | (39 | ) | (594 | ) | 947 | ||||||||||||||||||||||||||||||||||||||||||||||||

Net income (loss) before taxes | (21,557 | ) | (65,864 | ) | (122,333 | ) | (14,304 | ) | (17,570 | ) | (77,008 | ) | (6,498 | ) | 10,005 | (241,719 | ) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Income (loss) from continuing operations before taxes | 13,504 | (37,639 | ) | (45,734 | ) | (3,780 | ) | (33,138 | ) | (77,008 | ) | (6,498 | ) | 10,005 | (241,719 | ) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Income tax (expense) benefit | 8,142 | 1,269 | (17,518 | ) | 10,368 | — | (5,778 | ) | 742 | (2,417 | ) | (2,561 | ) | 25,983 | (13,300 | ) | (30,545 | ) | 36,533 | (1,579 | ) | (5,778 | ) | 742 | (2,417 | ) | (2,561 | ) | ||||||||||||||||||||||||||||||||||||||||||||||||||

Income (loss) from continuing operations | (13,415 | ) | (64,595 | ) | (139,851 | ) | (3,936 | ) | (17,570 | ) | (82,786 | ) | (5,756 | ) | 7,588 | (244,280 | ) | 39,487 | (50,939 | ) | (76,279 | ) | 32,753 | (34,717 | ) | (82,786 | ) | (5,756 | ) | 7,588 | (244,280 | ) | ||||||||||||||||||||||||||||||||||||||||||||||

Discontinued operations | — | — | — | — | — | — | — | 1,260 | (3,018 | ) | — | — | — | — | 1,260 | (3,018 | ) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Net income (loss) | $ | (13,415 | ) | $ | (64,595 | ) | $ | (139,851 | ) | $ | (3,936 | ) | $ | (17,570 | ) | $ | (82,786 | ) | $ | (5,756 | ) | $ | 8,848 | $ | (247,298 | ) | $ | 32,753 | $ | (34,717 | ) | $ | (82,786 | ) | $ | (5,756 | ) | $ | 8,848 | $ | (247,298 | ) | ||||||||||||||||||||||||||||||||||||

Statements of Cash Flow Data: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Net cash provided by (used in): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Operating activities | $ | (35,834 | ) | $ | 19,891 | $ | 121,417 | $ | (48,224 | ) | $ | 25,918 | $ | 31,686 | $ | (6,366 | ) | $ | (37 | ) | $ | 121,417 | $ | (48,224 | ) | $ | 25,918 | $ | 31,686 | |||||||||||||||||||||||||||||||||||||||||||||||||

Investing activities | (73,501 | ) | (640,428 | ) | (898,039 | ) | (2,762 | ) | (1,901 | ) | (55 | ) | (858,201 | ) | (643,160 | ) | (898,039 | ) | (2,762 | ) | (1,901 | ) | (55 | ) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Financing activities | 77,809 | 660,410 | 822,580 | 60,907 | (23,990 | ) | (31,636 | ) | 861,868 | 665,629 | 822,580 | 60,907 | (23,990 | ) | (31,636 | ) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance Sheet Data (as of period end): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Cash and cash equivalents | $ | 66,060 | $ | 11,803 | $ | 43,590 | $ | 42 | $ | 5 | $ | 47,871 | $ | 41,817 | $ | 43,590 | $ | 42 | $ | 5 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Property, plant & equipment, net | 664,740 | 418,499 | 388,924 | 414,073 | 423,826 | 437,231 | 648,621 | 388,924 | 414,073 | 423,826 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||