As filed with the Securities and Exchange Commission on August 30,November 8, 2004

Registration No. 333-105202

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

AMENDMENT NO. 34 TO

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

streetTRACKS® GOLD TRUST

SPONSORED BY WORLD GOLD TRUST SERVICES, LLC

(Exact name of Registrant as specified in its charter)

| New York | 6189 | • | ||||||||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) | ||||||||

c/o World Gold Trust Services, LLC

444 Madison Avenue, 3rd Floor

New York, New York 10022

(212) 317-3800

(Address, including zip code, and telephone number, including area code, of Registrant's principal executive offices)

Steven J. Glusband, Esq.

Kathleen H. Moriarty, Esq.

Carter Ledyard & Milburn LLP

2 Wall Street

New York, New York 10005

(212) 732-3200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Mr. J. Stuart Thomas World Gold Trust Services, LLC 444 Madison Avenue, 3rd Floor New York, New York 10022 (212) 317-3800 | ||||||||||

and

| Kevin W. Kelley, Esq. Gibson, Dunn & Crutcher LLP 200 Park Avenue New York, New York 10166 (212) 351-4000 | John Altorelli, Esq. Paul, Hastings, Janofsky & Walker LLP 75 East 55th Street New York, New York 10022 (212) 318-6000 | |||||

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ![]()

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ![]()

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ![]()

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ![]()

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. ![]()

Calculation of Registration Fee

| Title of each class of securities to be registered | Title of each class of securities to be registered | Amount to be registered | Proposed maximum offering price per Share(1) | Proposed maximum aggregate offering price(1) | Amount of registration fee | Title of each class of securities to be registered | Amount to be registered | Proposed maximum offering price per Share(1) | Proposed maximum aggregate offering price(1) | Amount of registration fee | |||||||||||||||||||||||||||||||||||||

| streetTRACKS® Gold Shares | 60,400,000 | $ | 33.14 | $ | 2,001,656,000 | $ | 161,933.97 | (2) | |||||||||||||||||||||||||||||||||||||||

| streetTRACKS® Gold Shares | streetTRACKS® Gold Shares | 120,000,000 | $ | 42.35 | $ | 4,525,716,000 | $ | 481,732.37 | (2) | ||||||||||||||||||||||||||||||||||||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(d) under the Securities Act of 1933. The initial amount of gold required for deposit with the |

| (2) |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. WeThese securities may not sell these securitiesbe sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and wethe Sponsor and the Trust are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | Subject to Completion |

60,400,000120,000,000 Shares

[INSERT LOGO]

streetTRACKS®streetTRACKS® Gold Shares

The streetTRACKS® Gold Trust (Trust) will issue streetTRACKS® Gold Shares (Shares) which represent units of fractional undivided beneficial interest in and ownership of the Trust. World Gold Trust Services, LLC is the sponsor of the Trust (Sponsor), The Bank of New York is the trustee of the Trust (Trustee), HSBC Bank USA, N.A. is the custodian of the Trust (Custodian) and State Street Global Markets, LLC is the marketing agent of the Trust (Marketing Agent). The Trust intends to issue additional Shares on a continuous basis through its Trustee.

The Shares may be purchased from the Trust only in one or more blocks of 100,000 Shares (a block of 100,000 Shares is called a Basket). The Trust will issue Shares in Baskets to certain authorized participants (Authorized Participants) on an ongoing basis as described in "Plan of Distribution." Baskets will be offered continuously at the net asset value (NAV) for 100,000 Shares on the day that an order to create a Basket is accepted by the Trustee.

Prior to this offering, there has been no public market for the Shares. The Sponsor has applied for approval to list the Shares on the New York Stock Exchange (NYSE) under the symbol "GLD."

Investing in the Shares involves significant risks. See "Risk Factors" starting on page 7.

Neither the Securities and Exchange Commission (SEC) nor any state securities commission has approved or disapproved of the securities offered in this prospectus, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The Shares are neither interests in nor obligations of the Sponsor, the Trustee or the Marketing Agent.

streetTRACKS® is a registered service mark of State Street Corporation, an affiliate of the Marketing Agent.

The Trust will issue Shares from time to time in Baskets, as described in "Creation and Redemption of Shares." It is expected that the Shares will be sold to the public at varying prices to be determined by reference to, among other considerations, the price of gold and the trading price of the Shares on the NYSE at the time of each sale.

Shares

Of the total number of Shares which are the subject of this prospectus, theThe Trust is offering Shares (Underwritten Shares) through UBS Securities LLC, also called the Purchaser, as underwriter. The Purchaser has, subject to conditions, agreed to purchase the Underwritten Shares at a per Share price equal to one-tenth (1/10) of an ounce of gold, as described in "Plan of Distribution." Total proceeds to the Trust from the sale of the Underwritten Shares are expected towill be ounces of gold. Delivery of the Underwritten Shares is expected to be made on or abouta date between November and , 2004.

UBS Investment BankThe public offering price of the Underwritten Shares will be determined as described above and such Shares could be sold at different prices if sold by the Purchaser at different times. In connection with the offering and sale of the Underwritten Shares, the Purchaser will be paid an aggregate fee by the Sponsor of $ . The Purchaser may also receive an advisory fee payable by the Sponsor within one month after the initiation of trading in the Shares (to be paid in the sole discretion of the Sponsor depending on the success of the Trust at such time) in the amount of $ million for advice provided by the Purchaser in the original structuring of the Trust. In addition to such fees, the Purchaser may receive commissions/fees from investors through their commission/fee-based brokerage accounts, in amounts between $ and $ ..

UBS Investment Bank

This prospectus contains information you should consider when making an investment decision about the Shares. You may rely on the information contained in this prospectus. The Trust and the Sponsor have not authorized any person to provide you with different information and, if anyone provides you with different or inconsistent information, you should not rely on it. This prospectus is not an offer to sell the Shares in any jurisdiction where the offer or sale of the Shares is not permitted.

The Shares are not registered for public sale in any jurisdiction other than the United States.

TABLE OF CONTENTS

| Statement Regarding Forward-Looking Statements | ii | |||||

| Glossary of Defined Terms | iii | |||||

| Prospectus Summary | 1 | |||||

| Risk Factors | 7 | |||||

| Use of Proceeds | ||||||

| Overview of the Gold Industry | ||||||

| Operation of the Gold Bullion Market | ||||||

| Analysis of Movements in the Price of Gold | ||||||

| Business of the Trust | ||||||

| Description of the Trust | ||||||

| The Sponsor | ||||||

| The Trustee | ||||||

| The Custodian | ||||||

| The Marketing Agent | ||||||

| Description of the Shares | ||||||

| Custody of the Trust's Gold | ||||||

| Description of the Custody Agreements | ||||||

| Creation and Redemption of Shares | ||||||

| Description of the Trust Indenture | ||||||

| United States Federal Tax Consequences | ||||||

| ERISA and Related Considerations | ||||||

| Plan of Distribution | ||||||

| Legal Proceedings | ||||||

| Legal Matters | ||||||

| Experts | ||||||

| Where You Can Find More Information | ||||||

| Statement of Financial Condition | F-2 | |||||

streetTRACKS® Gold Trust and streetTRACKS® Gold Shares are service marks owned by State Street Corporation.

Until , 2004 (25 days after the date of this prospectus), all dealers effecting transactions in the offered Shares, whether or not participating in this distribution, may be required to deliver a prospectus. This requirement is in addition to the obligations of dealers to deliver a prospectus when acting as underwriters and with respect to unsold allotments or subscriptions.

The information contained in the sections captioned "Overview of the Gold Industry," "Operation of the Gold Bullion Market" and "Analysis of Movements in the Price of Gold" is based on information obtained from sources that the Sponsor believes are reliable. This prospectus summarizes certain documents and other information in a manner we believethe Sponsor believes to be accurate. In making an investment decision, you must rely on your own examination of the Trust, the gold industry, the operation of the gold bullion market and the terms of the offering and the Shares, including the merits and risks involved. Although the Sponsor believes this information to be reliable, the accuracy and completeness of this information is not guaranteed and has not been independently verified.

i

Statement Regarding Forward-Looking Statements

This prospectus includes "forward-looking statements" which generally relate to future events or future performance. In some cases, you can identify forward-looking statements by terminology such as "may," "will," "should," "expect," "plan," "anticipate," "believe," "estimate," "predict," "potential" or the negative of these terms or other comparable terminology. All statements (other than statements of historical fact) included in this prospectus that address activities, events or developments that will or may occur in the future, including such matters as changes in commodity prices and market conditions (for gold and the Shares), the Trust's operations, the Sponsor's plans and references to the Trust's future success and other similar matters are forward-looking statements. These statements are only predictions. Actual events or results may differ materially. These statements are based upon certain assumptions and analyses the Sponsor made based on its perception of historical trends, current conditions and expected future developments, as well as other factors appropriate in the circumstances. Whether or not actual results and developments will conform to the Sponsor's expectations and predictions, however, is subject to a number of risks and uncertainties, including the special considerations discussed in this prospectus, general economic, market and business conditions, changes in laws or regulations, including those concerning taxes, made by governmental authorities or regulatory bodies, and other world economic and political developments. See "Risk Factors." Consequently, all the forward-looking statements made in this prospectus are qualified by these cautionary statements, and there can be no assurance that the actual results or developments the Sponsor anticipates will be realized or, even if substantially realized, that they will result in the expected consequences to, or have the expected effects on, the Trust's operations or the value of the Shares. Moreover, neither the Sponsor nor any other person assumes responsibility for the accuracy or completeness of the forward-looking statements. Neither the Trust nor the Sponsor is under a duty to update any of the forward-looking statements to conform such statements to actual results or to reflect a change in the Sponsor's expectations or predictions.

ii

Glossary of Defined Terms

In this prospectus, each of the following quoted terms have the meanings set forth after such term:

"Allocated Bullion Account Agreement" — The agreement between the Trustee and the Custodian which establishes the Trust Allocated Account. The Allocated Bullion Account Agreement and the Unallocated Bullion Account Agreement are sometimes referred to together as the "Custody Agreements."

"ANAV" — Adjusted NAV. See "Description of the Trust Indenture — Valuation of Gold, Definition of Net Asset Value and Adjusted Net Asset Value" for a description of how the ANAV of the Trust is calculated. The ANAV of the Trust is used to calculate the fees of the Trustee, the Sponsor and the Marketing Agent.

"Authorized Participant" — A person who (1) is a registered broker-dealer or other securities market participant such as a bank or other financial institution which is not required to register as a broker-dealer to engage in securities transactions, (2) is a participant in DTC, (3) has entered into a Participant Agreement with the Trustee and (4) has established an Authorized Participant Unallocated Account with the Custodian. Only Authorized Participants may place orders to create or redeem one or more Baskets.

"Authorized Participant Unallocated Account" — An unallocated gold account established with the Custodian by an Authorized Participant. Each Authorized Participant's Authorized Participant Unallocated Account will be used to facilitate the transfer of gold deposits and gold redemption distributions between the Authorized Participant and the Trust in connection with the creation and redemption of Baskets.

"Basket" — A block of 100,000 Shares. Multiple blocks of 100,000 Shares are called "Baskets."

"BNY" — The Bank of New York, a banking corporation organized under the laws of the State of New York with trust powers. BNY is the trustee of the Trust.

"Book Entry System" — The Federal Reserve Treasury Book Entry System for United States and federal agency securities.

"CEA" — Commodity Exchange Act of 1936, as amended.

"CFTC" — Commodity Futures Trading Commission, an independent agency with the mandate to regulate commodity futures and option markets in the United States.

"Clearing Agency" — Any clearing agency or similar system other than the Book Entry System or DTC.

"Code" — The United States Internal Revenue Code of 1986, as amended.

"Creation Basket Deposit" — The total deposit required to create a Basket. The deposit will be an amount of gold and cash, if any, that is in the same proportion to the total assets of the Trust (net of estimated accrued but unpaid fees, expenses and other liabilities) on the date an order to purchase one or more Baskets is properly received as the number of Shares comprising the number of Baskets to be created in respect of the deposit bears to the total number of Shares outstanding on the date such order is properly received.

"Custodian" — HSBC Bank USA, N.A., a national banking association and a market maker, clearer and approved weigher under the rules of the LBMA.

"Custody Agreements" — The Allocated Bullion Account Agreement together with the Unallocated Bullion Account Agreement.

"Custody Rules" — The rules, regulations, practices and customs of the LBMA, the Bank of England or any applicable regulatory body which apply to gold made available in physical form by the Custodian.

"DTC" — The Depository Trust Company. DTC is a limited purpose trust company organized under New York law, a member of the US Federal Reserve System and a clearing agency registered with the SEC. DTC will act as the securities depository for the Shares.

"DTC Participant" — Participants in DTC, such as banks, brokers, dealers and trust companies.

iii

Glossary of Defined Terms

"Evaluation Time" — The time at which the Trustee will evaluate the gold held by the Trust and determine both the NAV and the ANAV of the Trust, which is currently the time of the London PM Fix on each day when the NYSE is open for regular trading or, if there is no London PM Fix on such day or the London PM Fix has not been announced by 12:00 PM New York time on such day, 12:00 PM New York time on such day.

"FSA" — The Financial Services Authority, an independent non-governmental body which exercises statutory regulatory power under the FSM Act and which regulates the major participating members of the LBMA in the United Kingdom.

"FSM Act" — The Financial Services and Markets Act 2000.

"HSBC" — HSBC Bank USA, N.A., a national banking association and a market maker, clearer and approved weigher under the rules of the LBMA. HSBC is the custodian of the Trust's gold.

"Indirect Participants" — Those banks, brokers, dealers, trust companies and others who maintain, either directly or indirectly, a custodial relationship with a DTC Participant.

"LBMA" — The London Bullion Market Association. The LBMA is the trade association that acts as the coordinator for activities conducted on behalf of its members and other participants in the London bullion market. In addition to coordinating market activities, the LBMA acts as the principal point of contact between the market and its regulators. A primary function of the LBMA is its involvement in the promotion of refining standards by maintenance of the "London Good Delivery Lists," which are the lists of LBMA accredited melters and assayers of gold. Further, the LBMA coordinates market clearing and vaulting, promotes good trading practices and develops standard documentation. The major participating members of the LBMA are regulated by the FSA in the United Kingdom under the FSM Act.

"London Good Delivery Bar" — A bar of gold meeting the London Good Delivery Standards.

"London Good Delivery Standards" — The specifications for weight, dimensions, fineness (or purity), identifying marks and appearance of gold bars as set forth in "The Good Delivery Rules for Gold and Silver Bars" published by the LBMA. The London Good Delivery Standards are described in "Operation of the Gold Bullion Market — The London Bullion Market."

"London PM Fix" — The afternoon session of the twice daily fix of the price of an ounce of gold which starts at 3:00 PM London, England time and is performed in London by the five members of the London gold fix. See "Operation of the Gold Bullion Market – The London Bullion Market" for a description of the operation of the London PM Fix.

"Marketing Agent Agreement" — The agreement amongbetween the Sponsor the Trustee on behalf of the Trust and the Marketing Agent under which, among other things, the Marketing Agent will assist the Sponsor with certain marketing activities.

"Marketing Agent" — State Street Global Markets, LLC, a Delaware limited liability company and a wholly-owned subsidiary of State Street Corporation.

"NAV" — Net asset value. See "Description of the Trust Indenture — Valuation of Gold, Definition of Net Asset Value and Adjusted Net Asset Value" for a description of how the NAV of the Trust and the NAV per Share are calculated.

"OTC" — The global Over-the-Counter market for the trading of gold which consists of transactions in spot, forwards, and options and other derivatives.

"Participant Agreement" — An agreement entered into by each Authorized Participant, the Sponsor and the Trustee which provides the procedures for the creation and redemption of Baskets and for the delivery of the gold and any cash required for such creations and redemptions.

"Participant Unallocated Bullion Account Agreement" — The agreement between an Authorized Participant and the Custodian which establishes the Authorized Participant Unallocated Account.

"Purchaser" — the purchaser of the Underwritten Shares, as described on the front page of this prospectus.

"Seed Baskets" — The three Baskets issued to the Specialist in exchange for the deposit into the Trust of 30,000 ounces of gold in connection with the formation of the Trust.

iv

Glossary of Defined Terms

"Seed Baskets" — The Baskets issued in exchange for the deposit into the Trust of ounces of gold in connection with the formation of the Trust.

"Shareholders" — Owners of beneficial interests in the Shares.

"Shares" — Units of fractional undivided beneficial interest in and ownership of the Trust which are issued by the Trust and named "streetTRACKS® Gold Shares."

"Specialist" — Bear Hunter Structured Products, LLC, the designated NYSE specialist firm for the Shares and the purchaser of the Seed Baskets.

"Sponsor" — World Gold Trust Services, LLC, a Delaware limited liability company wholly-owned by the WGC.

"tonne" — One metric tonne which is equivalent to 1,000 kilograms or 32,150.7465 troy ounces.

"Trust" — The streetTRACKS® Gold Trust, an investment trust, formed on November , 2004 under New York law pursuant to the Trust Indenture.

"Trust Allocated Account" — The allocated gold account of the Trust established with the Custodian by the Allocated Bullion Account Agreement. The Trust Allocated Account will be used to hold the gold deposited with the Trust in allocated form (i.e., as individually identified bars of gold).

"Trustee" — The Bank of New York, a banking corporation organized under the laws of the State of New York with trust powers.

"Trust Indenture" — The agreement entered into by the Sponsor and the Trustee under which the Trust is formed and which sets forth the rights and duties of the Sponsor, the Trustee and Custodian.

"Trust Unallocated Account" — The unallocated gold account of the Trust established with the Custodian by the Unallocated Bullion Account Agreement. The Trust Unallocated Account will be used to facilitate the transfer of gold deposits and gold redemption distributions between Authorized Participants and the Trust in connection with the creation and redemption of Baskets and the sales of gold made by the Trustee for the Trust.

"Unallocated Bullion Account Agreement" — The agreement between the Trustee and the Custodian which establishes the Trust Unallocated Account. The Allocated Bullion Account Agreement and the Unallocated Bullion Account Agreement are sometimes referred to together as the "Custody Agreements."

"Underwritten Shares" — The Shares purchased by the Purchaser as described on the front page of this prospectus.

"US Shareholder" — A Shareholder that is (1) an individual who is treated as a citizen or resident of the United States for US federal income tax purposes; (2) a corporation or partnership created or organized in or under the laws of the United States or any political subdivision thereof; (3) an estate, the income of which is includible in gross income for US federal income tax purposes regardless of its source; or (4) a trust, if a court within the United States is able to exercise primary supervision over the administration of the trust and one or more US persons have the authority to control all substantial decisions of the trust.

"WGC" — World Gold Council, a not-for-profit association registered under Swiss law and the sole member of the Sponsor.

"WGTS" — World Gold Trust Services, LLC, a Delaware limited liability company wholly-owned by the WGC. WGTS is the sponsor of the Trust.

v

Prospectus Summary

This is only a summary of the prospectus and, while it contains material information about the Trust and its Shares, it does not contain or summarize all of the information about the Trust and the Shares contained in this prospectus which is material and/or which may be important to you. You should read this entire prospectus, including "Risk Factors" beginning on page 7, before making an investment decision about the Shares.

TRUST STRUCTURE

The Trust is an investment trust, formed on November , 2004 under New York law pursuant to a trust indenture (Trust Indenture). The Trust holds gold and is expected from time to time to issue Baskets in exchange for deposits of gold and to distribute gold in connection with redemptions of Baskets. The investment objective of the Trust is for the Shares to reflect the performance of the price of gold bullion, less the Trust's expenses. The Sponsor believes that, for many investors, the Shares will represent a costcost- effective investment in gold. The material terms of the Trust Indenture are discussed in greater detail under the section "Description of the Trust Indenture". The Shares represent units of fractional undivided beneficial interest in and ownership of the Trust and are expected to be traded under the ticker symbol GLD on the NYSE.

The Trust's Sponsor is World Gold Trust Services, LLC (WGTS), which is wholly-owned by the World Gold Council (WGC), a not-for-profit association registered under Swiss law. The Sponsor is a Delaware limited liability company and was formed on July 17, 2002. Under the Delaware Limited Liability Company Act and the governing documents of the Sponsor, the WGC, the sole member of the Sponsor, is not responsible for the debts, obligations and liabilities of the Sponsor solely by reason of being the sole member of the Sponsor.

The Sponsor is responsible for establishing the Trust and for the registration of the Shares. The Sponsor will generally oversee the performance of the Trustee and the Trust's principal service providers, but will not exercise day-to-day oversight over the Trustee and such service providers. The Sponsor may remove the Trustee and appoint a successor (1) if the Trustee commits certain willful bad acts in performing its duties or willfully disregards its duties, (2) if the Trustee acts in bad faith in performing its duties, (3) if the Trustee's creditworthiness has materially deteriorated or (4) if the Trustee's negligent acts or omissions have had a material adverse effect on the Trust or the interests of Shareholders and the Trustee has not cured the material adverse effect within a certain period of time and established that the material adverse effect will not recur. The Sponsor will remove the Trustee if the Trustee does not meet the qualifications for a trustee under the Trust Indenture. See "Description of the Trust Indenture — The Trustee — Resignation, discharge or removal of Trustee; successor trustees" for more information. The Sponsor may direct the Trustee to employ one or more other custodians in addition to or in replacement of the Custodian, provided that the Sponsor may not appoint a successor custodian without the consent of the Trustee if the appointment has a material adverse effect on the Trustee's ability to perform its duties. To assist the Sponsor in marketing the Shares, the Sponsor will enter into a marketing agent agreement with the Marketing Agent and the Trustee on behalf of the Trust (Marketing Agent Agreement). The Sponsor will maintain a public website on behalf of the Trust, containing information about the Trust and the Shares. The internet address of the Trust's website is [ ].will be www.streettracksgoldshares.com. This internet address is only provided here as a convenience to you, and the information contained on or connected to the Trust's website is not considered part of this prospectus. The general role, responsibilities of the Sponsor are further discussed in "The Sponsor."

The Trustee is The Bank of New York (BNY). The Trustee is generally responsible for the day-to-day administration of the Trust. This includes (1) selling the Trust's gold as needed to pay the Trust's expenses (gold sales are expected to occur approximately monthly in the ordinary course), (2) calculating the NAV of the Trust and the NAV per Share, (3) receiving and processing orders from Authorized Participants to create and redeem Baskets and coordinating the processing of such orders with the Custodian and The Depository Trust Company (DTC) and (4) monitoring the Custodian. The general role, responsibilities and regulation of the Trustee are further described in "The Trustee."

The Custodian is HSBC Bank USA, N.A. (HSBC). The Custodian is responsible for the safekeeping of the Trust's gold deposited with it by Authorized Participants in connection with the creation of Baskets. The Custodian also facilitates the transfer of gold in and out of the Trust through gold accounts it will maintain for Authorized Participants and the Trust. The Custodian is a market maker, clearer and approved weigher under the rules of the London Bullion Market Association (LBMA). The general role, responsibilities and regulation of the Custodian are further described in "The Custodian" and "Custody of the Trust's Gold."

Detailed descriptions of certain specific rights and duties of the Trustee and the Custodian are set forth in "Description of the Trust Indenture" and "Description of the Custody Agreements."

The Marketing Agent will assist the Sponsor in (1) developing a marketing plan for the Trust on an ongoing basis, (2) preparing marketing materials regarding the Shares, including the content of the Trust's website, (3) executing the marketing plan for the Trust, (4) providing marketincorporating gold into its strategic and tactical exchange-traded fund research, in respect of gold,and (5) reviewing the performance of the Trust and (6) licensing the "streetTRACKS® Gold Trust" and "streetTRACKS®" trademarks.trademark. The general role and responsibilities of the Marketing Agent are further described in "The Marketing Agent."

TRUST OVERVIEW

The investment objective of the Trust is for the Shares to reflect the performance of the price of gold bullion, less the expenses of the Trust's operations. The Shares are designed for investors who want a cost effectivecost-effective and convenient way to invest in gold. Advantages of investing in the Shares include:

| • | Ease and Flexibility of Investment. The Sponsor has applied to list the Shares on the NYSE. The Shares are expected to be exchange-listed equity instruments providing institutional and retail investors with indirect access to the gold bullion market. The Shares are expected upon listing on the NYSE to be bought and sold on the NYSE like any other exchange-listed securities, except that the Shares will regularly trade until 4:15 PM instead of 4:00 |

| • | Expenses. The Sponsor expects that, for many investors, costs associated with buying and selling the Shares in the secondary market and the payment of the Trust's ongoing expenses will be lower than the costs associated with buying and selling gold bullion and storing and insuring gold bullion in a traditional allocated gold bullion account. |

Investing in the Shares does not insulate the investor from certain risks, including price volatility. See "Risk Factors."

PRINCIPAL OFFICES

The Trust's office is located at 444 Madison Avenue, 3rd Floor, New York, New York 10022 and its telephone number is (212) 317-3800. The Sponsor's office is located at 444 Madison Avenue, 3rd Floor, New York, New York 10022. The Trustee has a trust office at 2 Hanson Place, Brooklyn, New York 11217. The Custodian is located at 8 Canada Square, London, E14 5HQ, United Kingdom. The Marketing Agent's office is located at State Street Financial Center, One Lincoln Street, Boston, Massachusetts 02111.

The Offering

| Offering | The Shares represent units of fractional undivided beneficial interest in and ownership of the Trust. | |

| Use of proceeds | Proceeds received by the Trust from the issuance and sale of Baskets, including the Seed Baskets | |

| New York Stock Exchange symbol | GLD | |

| CUSIP | ||

| Creation and redemption | The Trust expects to create and redeem the Shares from time to time, but only in one or more Baskets (a Basket equals a block of 100,000 Shares). The creation and redemption of Baskets requires the delivery to the Trust or the distribution by the Trust of the amount of gold and any cash represented by the Baskets being created or redeemed, the amount of which will be based on the combined NAV of the number of Shares included in the Baskets being created or redeemed. The initial amount of gold required for deposit with the Trust to create Shares is 10,000 ounces per Basket. The number of ounces of gold required to create a Basket or to be delivered upon the redemption of a Basket will gradually decrease over time, due to the accrual of the Trust's expenses and the sale of the Trust's gold to pay the Trust's expenses. See "Business of the Trust — Trust Expenses — Pro Forma Impact of Trust Expenses." Baskets may be created or redeemed only by Authorized Participants, who will pay a transaction fee for each order to create or redeem Baskets and may sell the Shares included in the Baskets they create to other investors. See "Creation and Redemption of Shares" for more details. | |

| Net Asset Value | The NAV of the Trust is the aggregate value of the Trust's assets less its liabilities (which include estimated accrued but unpaid fees and expenses). In determining the NAV of the Trust, the Trustee will value the gold held by the Trust on the basis of the price of an ounce of gold as set by the afternoon session of the twice daily fix of the price of an ounce of gold which starts at 3:00 PM London, England time and is performed by the five members of the London gold fix (London PM Fix). See "Operation of the Gold | |

| Bullion Market — The London Bullion Market" for a description of the operation of the London gold price fix. The Trustee will determine the NAV of the Trust on each day | ||

| the NYSE is open for regular trading, at the earlier of the London PM Fix for the day or 12:00 PM New York time. If no London PM Fix is made on a particular evaluation day or if the London PM Fix has not been announced by 12:00 PM New York time on a particular evaluation day, the next most recent London gold price fix (AM or PM) will be used in the determination of the NAV of the Trust, unless the Trustee, in consultation with the Sponsor, determines that such price is inappropriate to use as basis for such determination. The Trustee will also determine the NAV per Share, which equals the NAV of the Trust, divided by the number of outstanding Shares. | ||

| Trust expenses | The Trust's ordinary operating expenses are accrued daily and are reflected in the NAV of the Trust. The Trust's expenses include fees and expenses of the Trustee (which include fees and expenses paid to the Custodian by the Trustee for the custody of the Trust's gold), the fees and expenses of the Sponsor, certain taxes, the fees of the Marketing Agent, printing and mailing costs, legal and audit fees, registration fees and NYSE listing fees. In order to pay the Trust's expenses, the Trustee will sell gold held by the Trust on an as-needed basis. Each sale of gold by the Trust will be a taxable event to Shareholders. See "United States Federal Tax Consequences — Taxation of US Shareholders." | |

| Sponsor's and Marketing Agent's fees | The Sponsor's fee is payable monthly in arrears and is accrued daily at an annual rate equal to 0.15% of the daily ANAV of the Trust. The Marketing Agent's fee is payable monthly in arrears and is accrued daily at an annual rate equal to 0.15% of the daily ANAV of the Trust. If at the end of any month during the period ending seven years from the | |

| date of the Trust Indenture or upon the earlier termination of the Marketing Agent Agreement the estimated ordinary expenses of the Trust exceed an amount equal to 0.40% per | ||

| reduction. See "Business of the Trust — Trust Expenses — Fee Reduction." | ||

| Termination events | The Sponsor may, and it is anticipated that the Sponsor will, direct the Trustee to terminate and liquidate the Trust at any time after the first anniversary of the Trust's formation when the NAV of the Trust is less than $350 million (as adjusted for inflation). The Sponsor may also direct the Trustee to terminate the Trust if the Commodity Futures Trading Commission (CFTC) determines that the Trust is a commodities pool under the Commodity Exchange Act of 1936, as amended (CEA). The Trustee may also terminate the Trust upon the agreement of the owners of beneficial interests in the Shares (Shareholders) owning at least 66 2/3% of the outstanding Shares. | |

| The Trustee will terminate and liquidate the Trust if one of the following events occurs: | ||

| → | DTC, the securities depository for the Shares, is unwilling or unable to perform its functions under the Trust Indenture and no suitable replacement is available; | ||

| → | The Shares are de-listed from the NYSE and are not listed for trading on another US national securities exchange or through the Nasdaq Stock Market within five business days from the date the Shares are de-listed; | ||

| → | The NAV of the Trust remains less than $50 million for a period of 50 consecutive business days at any time after the first 90 days of the Shares being traded on the NYSE; | ||

| → | The Sponsor resigns or is unable to perform its duties or becomes bankrupt or insolvent and the Trustee has not appointed a successor and has not itself agreed to act as sponsor; | ||

| → | The Trustee resigns or is removed and no successor trustee is appointed within 60 days; | ||

| → | The Custodian resigns and no successor custodian is appointed within 60 days; | ||

| → | The sale of all of the Trust's assets; | ||

| → | The Trust fails to qualify for treatment, or ceases to be treated, for US federal income tax purposes, as a grantor trust; or | ||

| → | The maximum period for which the Trust is allowed to exist under New York law ends. | ||

| Upon the termination of the Trust, the Trustee will, within a reasonable time after the termination of the Trust, sell the | ||

| Trust's gold and, after paying or making provision for the Trust's liabilities, distribute the proceeds to the Shareholders. See "Description of the Trust Indenture — Termination of the Trust." | ||

| Authorized Participants | Baskets may be created or redeemed only by Authorized Participants. Each Authorized Participant must (1) be a registered broker-dealer or other securities market participant such as a bank or other financial institution which is not required to register as a broker-dealer to engage in securities transactions, (2) be a participant in DTC, (3) have entered into an agreement with the Trustee and the Sponsor (Participant Agreement) and (4) have established an unallocated gold account with the Custodian (Authorized Participant Unallocated Account). The Participant Agreement provides the procedures for the creation and redemption of Baskets and for the delivery of gold and any cash required for such creations or redemptions. A list of the current Authorized Participants can be obtained from the Trustee or the Sponsor. See "Creation and Redemption of Shares" for more details. | |

| Clearance and settlement | The Shares will be evidenced by | |

Summary of Financial Condition

As of the openingdate of businessthe formation of the Trust on , 2004, the NAV of the Trust, which represents the value of the gold deposited into the Trust in exchange for the Seed Baskets, was $ and the NAV per Share was $ . See "Statement of Financial Condition" elsewhere in this prospectus.

Risk Factors

You should consider carefully the risks described below before making an investment decision. You should also refer to the other information included in this prospectus, including the Trust's financial statements and the related notes.

The value of the Shares relates directly to the value of the gold held by the Trust and

fluctuations in the price of gold could materially adversely affect an investment in the Shares.

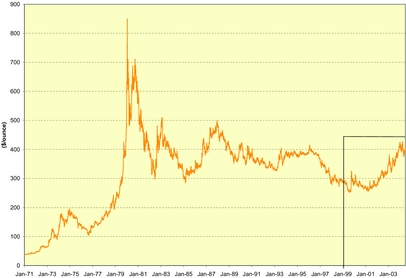

The Shares are designed to mirror as closely as possible the performance of the price of gold bullion, and the value of the Shares relates directly to the value of the gold held by the Trust, less the Trust's liabilities (including estimated accrued but unpaid expenses). The price of gold has fluctuated widely over the past several years. Several factors may affect the price of gold, including:

In addition, investors should be aware that there is no assurance that gold will maintain its long-term value in terms of purchasing power in the future. In the event that the price of gold declines, the Sponsor expects the value of an investment in the Shares to decline proportionately.

The Shares may trade at a price which is at, above or below the NAV per Share and any discount or premium in the trading price relative to the NAV per Share may widen as a result of non-concurrent trading hours between the COMEX and the NYSE.

The Shares may trade at, above or below the NAV per Share. The NAV per Share will fluctuate with changes in the market value of the Trust's assets. The trading price of the Shares will fluctuate in accordance with changes in the NAV per Share as well as market supply and demand. The amount of the discount or premium in the trading price relative to the NAV per Share may be influenced by non-concurrent trading hours between the COMEX division of the New York Mercantile Exchange and the NYSE. While the Shares will trade on the NYSE until 4:15 PM New York time, liquidity in the global gold market will be reduced after the close of the COMEX division of the New York Mercantile Exchange at 1:30 PM New York time. As a result, during this time, trading spreads, and the resulting premium or discount, on the Shares may widen.

The sale of gold by the Trust to pay expenses will reduce the amount of gold represented by each Share on an ongoing basis irrespective of whether the trading price of the Shares rises or falls in response to changes in the price of gold.

Each outstanding Share will represent a proportionalfractional, undivided interest in the gold held by the Trust. As the Trust will not generate any income and as the Trust will regularly sell gold over time to pay for its ongoing expenses, the amount of gold represented by each Share will gradually decline over time. This is true even if additional Shares are issued in exchange for additional deposits of gold into the Trust, as the amount of gold required to create Shares will proportionately reflect the amount of gold represented by the Shares outstanding at the time of creation. Assuming a constant gold price, the trading price of the Shares is expected to gradually decline relative to the price of gold as the amount of gold represented by the Shares gradually declines. The Shares will only maintain their original price if the price of gold increases.

Investors should be aware that the gradual decline in the amount of gold represented by the Shares will occur regardless of whether the trading price of the Shares rises or falls in response to changes in the price of gold.

Risk Factors

of gold. The estimated ordinary operating expenses of the Trust, which accrue daily commencing after the first day of trading of the Shares on the NYSE, are described in "Business of the Trust — Trust Expenses" and "Description of the Trust Indenture — Expenses of the Trust."

When the fee reduction under the Trust Indenture terminates or expires, the estimated ordinary expenses payable by the Trust may increase, thus reducing the NAV of the Trust more rapidly and adversely affecting an investment in the Shares.

Under the Trust Indenture, for the period endingFor seven years from the date of the Trust Indenture or uponuntil the earlier termination of the Marketing Agent Agreement, if at the end of any month during suchthis period the estimated ordinary expenses of the Trust exceed an amount equal to 0.40% per annumyear of the daily ANAV of the Trust for such month, the fees payable to the Sponsor and the Marketing Agent from the assets of the Trust for such month will be reduced by the amount of such excess in equal shares up to the amount of their fees. Investors should be aware that if the gross value of the Trust's assets is less than approximately $388 million, the ordinary expenses of the Trust will be accrued at a rate greater than 0.40% per year of the daily ANAV of the Trust, even after the Sponsor and the Marketing Agent have completely reduced their combined fees of 0.30% per year of the daily ANAV of the Trust. This amount is based on the estimated ordinary expenses of the Trust described in "Business of the Trust — Trust Expenses" and may be higher if the Trust's actual ordinary expenses exceed those estimates. Additionally, if the Trust incurs unforeseen expenses that cause the total ordinary expenses of the Trust to exceed 0.70% per year of the daily ANAV of the Trust, the ordinary expenses will accrue at a rate greater than 0.40% per year of the daily ANAV of the Trust, even after the Sponsor and the Marketing Agent have completely reduced their combined fees of 0.30% per year of the daily ANAV of the Trust.

Upon the end of the seven year period or the earlier termination of the Marketing Agent Agreement, the fee reduction will expire and the estimated ordinary expenses of the Trust which are payable from the assets of the Trust each month may be more than they would have been during the period when the fee reduction is in effect, thus reducing the NAV of the Trust more rapidly than if the fee reduction was in effect and adversely affecting the value of the Shares.

The estimated ordinary operating expenses of the Trust, which accrue daily, are described in "Business of the Trust — Trust Expenses" and "Description of the Trust Indenture — Expenses of the Trust." For details on the calculation of the ANAV of the Trust, see "Description of the Trust Indenture — Valuation of Gold, Definition of Net Asset Value and Adjusted Net Asset Value."

The sale of the Trust's gold to pay expenses at a time of low gold prices could adversely affect the value of the Shares.

The Trustee will sell gold held by the Trust to pay Trust expenses on an as-needed basis irrespective of then-current gold prices. The Trust is not actively managed and no attempt will be made to buy or sell gold to protect against or to take advantage of fluctuations in the price of gold. Consequently, the Trust's gold may be sold at a time when the gold price is low, resulting in a negative effect on the value of the Shares.

Purchasing activity in the gold market associated with the purchase of Baskets from the Trust may cause a temporary increase in the price of gold. This increase may adversely affect an investment in the Shares.

Purchasing activity associated with acquiring the gold required for deposit into the Trust in connection with the creation of Baskets may temporarily increase the market price of gold, which will result in higher prices for the Shares. Temporary increases in the market price of gold may also occur as a result of the purchasing activity of other market participants. Other market participants may attempt to benefit from an increase in the market price of gold that may result from increased purchasing activity of gold connected with the issuance of Baskets. Consequently, the market price of gold may decline immediately after Baskets are created. If the price of gold declines, the trading price of the Shares will also decline.

As the Sponsor and its management have no history of operating an investment vehicle like the Trust, their experience may be inadequate or unsuitable to manage the Trust.

The Sponsor was expressly formed to be the sponsor of the Trust and has no history of past performance. The past performances of the Sponsor's management in other positions are no indication of their ability

Risk Factors

to manage an investment vehicle such as the Trust. If the experience of the Sponsor and its management is not adequate or suitable to manage an investment vehicle such as the Trust, the operations of the Trust may be adversely affected.

The Shares are a new securities product and their value could decrease if unanticipated operational or trading problems arise.

The mechanisms and procedures governing the creation, redemption and offering of the Shares have been developed specifically for this securities product. Consequently, there may be unanticipated problems or issues with respect to the mechanics of the Trust's operations and the trading of the Shares that could have a material adverse effect on an investment in the Shares. In addition, although the Trust is not actively "managed" by traditional methods, to the extent that unanticipated operational or trading problems or issues arise, the Sponsor's past experience and qualifications may not be suitable for solving these problems or issues.

Risk Factors

Shareholders will not have the protections associated with ownership of shares in an investment company registered under the Investment Company Act of 1940 or the protections afforded by the Commodity Exchange Act of 1936.

The Trust is not registered as an investment company under the Investment Company Act of 1940 and is not required to register under such act. Consequently, Shareholders will not have the regulatory protections provided to investors in investment companies. The Trust will not hold or trade in commodity futures contracts regulated by the CEA, as administered by the CFTC. Furthermore, the Trust is not a commodity pool for purposes of the CEA, and none of the Sponsor, the Trustee or the Marketing Agent is subject to regulation by the CFTC as a commodity pool operator or a commodity trading advisor in connection with the Shares. Consequently, Shareholders will not have the regulatory protections provided to investors in CEA-regulated instruments or commodity pools.

The Trust may be required to terminate and liquidate at a time that is disadvantageous to Shareholders.

If the Trust is required to terminate and liquidate, such termination and liquidation could occur at a time which is disadvantageous to Shareholders, such as when gold prices are lower than the gold prices at the time when Shareholders purchased their Shares. In such a case, when the Trust's gold is sold as part of the Trust's liquidation, the resulting proceeds distributed to Shareholders will be less than if gold prices were higher at the time of sale. See "Description of the Trust Indenture — Termination of the Trust" for more information about the termination of the Trust, including when the termination of the Trust may be triggered by events outside the direct control of the Sponsor, the Trustee or the Shareholders.

The lack of a market for the Shares may limit the ability of Shareholders to sell the Shares.

Prior to the date of this prospectus, there has been no market for the Shares, and there can be no assurance that an active public market for the Shares will develop. If an active public market for the Shares does not exist or continue, the market prices and liquidity of the Shares may be adversely affected.

The operations of the Trust and the Sponsor depend on support from the WGC. This support may not be available in the future and, if such support is not available, the operations of the Trust may be adversely affected.

The Sponsor is a subsidiary of the WGC, a not-for-profit association that represents members of the gold mining industry through international marketing programs directed at stimulating demand for gold in all forms.

The ongoing operations of the Trust depend on the financial and management support of the Sponsor. The operations of the Sponsor, in turn, depend on the financial and management support of the WGC. See "The Sponsor" for more information on the funding of the Sponsor. If the WGC limits or ends its support of the Sponsor for any reason, the operations of the Trust and an investment in the Shares may be adversely affected. As a result, the Trust may be required to terminate.

The WGC's members determine the financial plan of the WGC. The WGC's current and reasonably foreseeable operational costs and expenses are underwritten by the WGC's members through the end of

Risk Factors

2004. The WGC's members have agreed to fundfunded the estimated ordinary operating expenses of the Sponsor which include expensesthrough 2004, including the costs associated with the marketinginitial registration of the Shares for the two year period beginning after the effectiveness of the Trust's registration statement and the listing of the Shares on the NYSE. The WGC has provided $3 million in funding to cover the estimated ordinary expenses of the Sponsor for 2005 and 2006. There is no assurance that the WGC's members will fund the WGC or the Sponsor thereafter. The lack of such funding could adversely affect the ability of the Sponsor to support the Trust.

Shareholders will not have the rights enjoyed by investors in certain other vehicles.

As interests in an investment trust, the Shares have none of the statutory rights normally associated with the ownership of shares of a corporation (including, for example, the right to bring "oppression" or "derivative" actions). In addition, the Shares have limited voting and distribution rights (for example, Shareholders do not have the right to elect directors and will not receive dividends). See "Description of the Shares" for a description of the limited rights of holders of Shares.

Risk Factors

An investment in the Shares may be adversely affected by competition from other methods of investing in gold.

The Trust is a new, and thus untested, type of investment vehicle. It will compete with other financial vehicles, including traditional debt and equity securities issued by companies in the gold industry and other securities backed by or linked to gold, direct investments in gold and investment vehicles similar to the Trust. Market and financial conditions, and other conditions beyond the Sponsor's control, may make it more attractive to invest in other financial vehicles or to invest in gold directly, which could limit the market for the Shares and reduce the liquidity of the Shares.

Crises may motivate large-scale sales of gold which could decrease the price of gold and

adversely affect an investment in the Shares.

The possibility of large-scale distress sales of gold in times of crisis may have a short-term negative impact on the price of gold and adversely affect an investment in the Shares. For example, the 1998 Asian financial crisis resulted in significant sales of gold by individuals which depressed the price of gold. Crises in the future may impair gold's price performance which would, in turn, adversely affect an investment in the Shares.

Substantial sales of gold by the official sector could adversely affect an investment in the Shares.

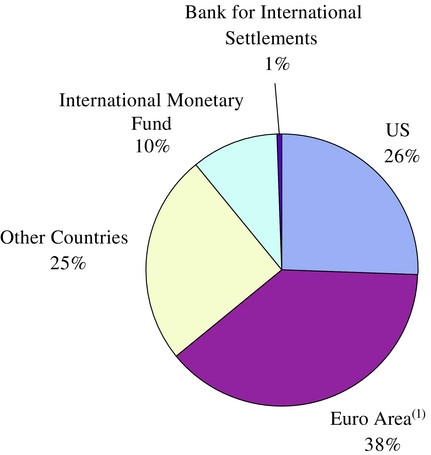

The official sector consists of central banks, other governmental agencies and multi-lateral institutions that buy, sell and hold gold as part of their reserve assets. The official sector holds a significant amount of gold, most of which is static, meaning that it is held in vaults and is not bought, sold, leased or swapped or otherwise mobilized in the open market. A number of central banks have sold portions of their gold over the past 10 years, with the result that the official sector, taken as a whole, has been a net supplier to the open market. Since 1999, most sales have been made in a coordinated manner under the terms of the Central Bank Gold Agreement, under which 15 of the world's major central banks (including the European Central Bank) agreed to limit the level of their gold sales and lending to the market for the following five years. The European Central Bank announced in March 2004 that the agreement would be extended for a further five-year period starting on September 27, 2004. The new agreement is similar to the existing agreement, although the ceiling for gold sales is 25% higher and the Bank of Greece replaces the Bank of England as a signatory to the agreement. UK Treasury indicated at the time of the announcement of the new agreement that the UK government had no plans to sell gold from its reserves and therefore would not participate in the new agreement. See "Overview of the Gold Industry — Sources of Gold Supply" and "Analysis of Movements in the Price of Gold" for more details. As before, the new agreement will be reviewed after five years. It is possible that the new agreement may not be renewed when it expires in September 2009. In the event that future economic, political or social conditions or pressures require members of the official sector to liquidate their gold assets all at once or in an uncoordinated manner, the demand for gold might not be sufficient to accommodate the sudden increase in the supply of gold to the market. Consequently, the price of gold could decline significantly, which would adversely affect an investment in the Shares.

Risk Factors

A widening of interest rate differentials between the cost of money and the cost of gold could negatively affect the price of gold which, in turn, could negatively affect the price of the Shares.

A combination of rising money interest rates and a continuation of the current low cost of borrowing gold could improve the economics of selling gold forward. This could result in an increase in hedging by gold mining companies and short selling by speculative interests, which would negatively affect the price of gold. Under such circumstances, the price of the Shares would be similarly affected.

Risk Factors

The Trust's gold may be subject to loss, damage, theft or restriction on access.

There is a risk that part or all of the Trust's gold could be lost, damaged or stolen. Access to the Trust's gold could also be restricted by natural events (such as an earthquake) or human actions (such as a terrorist attack). Any of these events may adversely affect the operations of the Trust and, consequently, an investment in the Shares.

The Trust may not have adequate sources of recovery if its gold is lost, damaged, stolen or destroyed.destroyed and recovery may be limited, even in the event of fraud, to the market value of the gold at the time the fraud is discovered.

Shareholders' recourse against the Trust, the Trustee the Custodian, any subcustodians and the Sponsor, under New York law, the Custodian, under English law, and any subcustodians under the law governing their custody operations is limited. The Trust will not insure its gold. The Custodian will maintain insurance with regard to its business on such terms and conditions as it considers appropriate. The Trust will not be a beneficiary of any such insurance and does not have the ability to dictate the existence, nature or amount of coverage. Therefore, Shareholders cannot be assured that the Custodian will maintain adequate insurance or any insurance with respect to the gold held by the Custodian on behalf of the Trust. In addition, the Custodian and the Trustee will not require any direct or indirect subcustodians to be insured or bonded with respect to their custodial activities or in respect of the gold held by them on behalf of the Trust. Consequently, a loss may be suffered with respect to the Trust's gold which is not covered by insurance and for which no person is liable in damages.

The liability of the Custodian for losses affectingis limited under the gold is limited.Custody Agreements. Under the agreements between the Trustee and the Custodian which establish the Trust's unallocated gold account (Unallocated Bullion Account Agreement) and the Trust's allocated gold account (Allocated Bullion Account Agreement), the Custodian is notonly liable for losses that are not the direct result of its own negligence, fraud or willful default in the performance of its duties. Any such liability is further limited, in the case of the Allocated Bullion Account Agreement, to the market value of the gold held in the Trust Allocated Account at the time such negligence, fraud or willful default is discovered by the Custodian and, in the case of the Unallocated Bullion Account Agreement, to the amount of gold credited to the Trust Unallocated Account at the time such negligence, fraud or willful default is discovered by the Custodian. Under each Participant Unallocated Bullion Account Agreement (between the Custodian and an Authorized Participant), the Custodian is not contractually or otherwise liable for any losses suffered by any Authorized Participant or Shareholder that are not the direct result of its own gross negligence, fraud or wilfulwillful default in the performance of its duties under such agreements,agreement, and in no event will its liability exceed the market value of the balance in its Authorized Participant Unallocated Account at the time such gross negligence, fraud or willful default is discovered by the Custodian. In addition, the Custodian will not be liable for any delay in performance or any non-performance of any of its obligations under the Allocated Bullion Account Agreement, the Unallocated Bullion Account Agreement or the Participant Unallocated Bullion Account Agreement by reason of any cause beyond its reasonable control, including acts of God, war or terrorism. As a result, the recourse of the Trustee or the investor, under English law, is limited. Furthermore, under English common law, the Custodian or any subcustodian will not be liable for any delay in the performance or any non-performance of its custodial obligations by reason of any cause beyond its reasonable control.

Under the Allocated Bullion Account Agreement, except for an obligation on the part of the Custodian to use commercially reasonable efforts to obtain delivery of the Trust's gold from any subcustodians appointed by the Custodian, the Custodian is not liable for the acts or omissions of its subcustodians unless the selection of such subcustodians was made negligently or in bad faith. There are expected to be no written contractual arrangements between subcustodians that hold the Trust's gold and the Trustee or

Risk Factors

the Custodian. Therefore,Custodian, because traditionally such arrangements are based on the LBMA's rules and on the customs and practices of the London bullion market. In the event of a legal dispute with respect to or arising from such arrangements, it may be difficult to define such customs and practices. The LBMA's rules may be subject to change outside the control of the Trust. Under English law, neither the Trustee, andnor the Custodian may notwould have a supportable breach of contract claim against a subcustodian for losses relating to the safekeeping of gold. If the Trust's gold is lost or damaged while in the custody of a subcustodian, the Trust may not be able to recover damages from the Custodian or the subcustodian. Whether a subcustodian will be liable for the failure of subcustodians appointed by it to exercise due care in the safekeeping of the Trust's gold will depend on the facts and circumstances of the particular situation. Shareholders cannot be assured that the Trustee will be able to recover damages from subcustodians whether appointed by athe Custodian or by another subcustodian for any losses relating to the safekeeping of gold by such subcustodian.

The obligations of the Custodian under the Allocated Bullion Account Agreement, the Unallocated Bullion Account Agreement and the Participant Unallocated Bullion Account Agreement are governed by English law. The Custodian may enter into arrangements with English subcustodians, which arrangements may also be governed by English law. The Trust is a New York investment trust. Any United States, New York or other court situated in the United States may have difficulty interpreting English law (which, insofar as it relates to custody arrangements, is largely derived from court rulings rather than statute), LBMA rules or the customs and practices in the London custody market. It may be difficult or impossible for the Trust to sue a subcustodian in a United States, New York or other court situated in the United States. In addition, it may be difficult, time consuming and/or expensive for the Trust to enforce in a foreign court a judgment rendered by a United States, New York or other court situated in the United States.

If the Trust's gold is lost, damaged, stolen or destroyed under circumstances rendering a party liable to the Trust, the responsible party may not have the financial resources sufficient to satisfy the Trust's claim. For example, as to a particular event of loss, the only source of recovery for the Trust might be limited to the Custodian or one or more subcustodians or, to the extent identifiable, other responsible third parties (e.g., a thief or terrorist), any of which may not have the financial resources (including liability insurance coverage) to satisfy a valid claim of the Trust.

Neither the Shareholders nor any Authorized Participant will have a right under the Custody Agreements to assert a claim of the Trustee against the Custodian or any subcustodian; claims under the Custody Agreements may only be asserted by the Trustee on behalf of the Trust.

Gold bullion allocated to the Trust in connection with the creation of a Basket may not meet the London Good Delivery Standards and, if a Basket is issued against such gold, the Trust may suffer a loss.

Neither the Trustee nor the Custodian independently confirms the fineness of the gold allocated to the Trust in connection with the creation of a Basket. The gold bullion allocated to the Trust by the

Risk Factors

CustodiantheCustodian may be different from the reported fineness or weight required by the LBMA's standards for gold bars delivered in settlement of a gold trade (London Good Delivery Standards), the standards required by the Trust. If the Trustee nevertheless issues a Basket against such gold, and if the Custodian fails to satisfy its obligation to credit the Trust the amount of any deficiency, the Trust may suffer a loss. The London Good Delivery Standards are described in "Operation of the Gold Bullion Market — The London Bullion Market." The Custodian's responsibility for the allocation to the Trust of gold meeting LBMA standards is described in "Description of the Custody Agreements — Transfers from the Trust Unallocated Account."

Because neither the Trustee andnor the Custodian do not overseeoversees or monitormonitors the activities of subcustodians who may hold the Trust's gold, there can be no assurance thatfailure by the subcustodians willto exercise due care in the safekeeping of the Trust's gold.gold could result in a loss to the Trust.

Under the Allocated Bullion Account Agreement described in "Description of the Custody Agreements," the Custodian may appoint from time to time one or more subcustodians to hold the Trust's gold. The subcustodians which the Custodian currently uses are the Bank of England and LBMA market-making members that provide bullion vaulting and clearing services to third parties. The Custodian is required

Risk Factors

under the Allocated Bullion Account Agreement to use reasonable care in appointing its subcustodians.subcustodians but otherwise has no other responsibility in relation to the subcustodians appointed by it. These subcustodians may in turn appoint further subcustodians, but the Custodian is not responsible for the appointment of these further subcustodians. The Custodian does not undertake to monitor the performance by subcustodians of their custody functions or their selection of further subcustodians. The Trustee does not undertake to monitor the performance of any subcustodian. Furthermore, the Trustee may have no right to visit the premises of any subcustodian for the purposes of examining the Trust's gold or any records maintained by the subcustodian, and no subcustodian will be obligated to cooperate in any review the Trustee may wish to conduct of the facilities, procedures, records or creditworthiness of such subcustodian. In addition, the ability of the Trustee to monitor the performance of the Custodian may be limited because under the Allocated Bullion Account Agreement and the Unallocated Bullion Account Agreement (together, the Custody Agreements) the Trustee has only limited rights to visit the premises of the Custodian for the purpose of examining the Trust's gold and certain related records maintained by the Custodian. See "Custody of the Trust's Gold" for more information about subcustodians that may hold the Trust's gold.

The ability of the Trustee and the Custodian to take legal action against subcustodians may be limited, which increases the possibility that the Trust may suffer a loss if a subcustodian does not use due care in the safekeeping of the Trust's gold.

If any subcustodian does not exercise due care in the safekeeping of the Trust's gold, the ability of the Trustee or the Custodian to recover damages against such subcustodian may be limited to only such recourse, if any, as may be available under applicable English law or, if the subcustodian is not located in England, under other applicable law. This is because there are expected to be no written contractual arrangements between subcustodians who may hold the Trust's gold and the Trustee or the Custodian, as the case may be. If the Trustee's or the Custodian's recourse against the subcustodian is so limited, the Trust may not be adequately compensated for the loss. For more information on the Trustee's and the Custodian's ability to seek recovery against subcustodians and the subcustodian's duty to safekeep the Trust's gold, see "Custody of the Trust's Gold."

If the Custodian becomes insolvent, goldGold held in the Trust's unallocated gold account orand any Authorized Participant's unallocated gold account would represent an unsecured claim againstwill not be segregated from the Custodian's assets. If the Custodian and the Custodian'sbecomes insolvent, its assets may not be adequate to satisfy a claim by the Trust or any Authorized Participant. In addition, in the event of the Custodian's insolvency, there may be a delay and costs incurred in identifying the bullion held in the Trust's allocated gold account.

Gold which is part of a deposit for a purchase order or part of a redemption distribution will be held for a time in the Trust's unallocated gold account (Trust Unallocated Account) and, previously or subsequently in, the unallocated gold accountAuthorized Participant Unallocated Account of the purchasing or redeeming Authorized Participant. During those times, the Trust and the Authorized Participant, as the case may be, will have no proprietary rights to any specific bars of gold held by the Custodian and will each be an unsecured creditor of the Custodian with respect to the amount of gold held in such unallocated accounts. In addition, if the Custodian fails to allocate the Trust's gold in a timely manner, in the proper amounts or otherwise in accordance with the terms of the Unallocated Bullion Account Agreement, or if a subcustodian fails to so held.segregate gold held by it on behalf of the Trust, unallocated gold will not be segregated from the Custodian's assets, and the Trust will be an unsecured creditor of the Custodian with respect to the amount so held in the event of the insolvency of the Custodian. In the event the Custodian becamebecomes insolvent, the Custodian's assets might not be adequate to satisfy a claim by the Trust or the Authorized Participant for the amount of gold held in their respective unallocated gold accounts.

In the case of the insolvency of the Custodian, a liquidator may seek to freeze access to the gold held in all of the accounts held by the Custodian, including the Trust's allocated account (Trust Allocated Account). Although the Trust would be able to claim ownership of properly allocated gold, the Trust could incur expenses in connection with asserting such claims, and the assertion of such a claim by the liquidator could delay creations and redemptions of Baskets.

Risk Factors

In issuing Baskets, the Trustee will rely on certain information received from the Custodian which is subject to confirmation after the Trustee has relied on the information. If such information turns out to be incorrect, Baskets may be issued in exchange for an amount of gold which is more or less than the amount of gold which is required to be deposited with the Trust.

The Custodian's definitive records are prepared after the close of its business day. However, when issuing Baskets, the Trustee will rely on information reporting the amount of gold credited to the Trust's accounts which it receives from the Custodian during the business day and which is subject to correction during the preparation of the Custodian's definitive records after the close of business. If the information relied upon by the Trustee is incorrect, the amount of gold actually received by the Trust may be more or less than the amount required to be deposited for the issuance of Baskets.

The Trust's obligation to reimburse the Purchaser, and the Marketing Agent and the Authorized Participants for certain liabilities in the event the Sponsor fails to indemnify the Purchaser, or the Marketing Agent or the Authorized Participants could adversely affect an investment in the Shares.

The Sponsor has agreed to indemnify the Purchaser and the Marketing Agent, their partners, directors and officers, and any person who controls the Purchaser or the Marketing Agent, and their respective successors and assigns, against any loss, damage, expense, liability or claim that may be incurred by the Purchaser and the Marketing Agent in connection with (1) any untrue statement or alleged untrue statement of a material fact contained in the registration statement of which this prospectus forms a part (including this prospectus, any preliminary prospectus, any prospectus supplement and any exhibits thereto) or any omission or alleged omission to state a material fact required to be stated therein or necessary to make the statements therein not misleading, (2) any untrue statement or alleged untrue statement of a material fact made by the Sponsor with respect to any representations and warranties or any covenants under (A) the distribution agreement between the Sponsor and the Purchaser, dated November , 2004 or (B) the Marketing Agent Agreement, or failure of the Sponsor to perform any agreement or covenant therein, (3) any untrue statement or alleged untrue statement of a material fact contained in any materials used in connection with the marketing of the Shares, (4) circumstances surrounding the third party allegations relating to patent and contract disputes as described in "Risk Factors—Competing claims over ownership of intellectual property rights related to the Trust could adversely affect the Trust and an Investment in the Shares," "Business of the Trust—License Agreement" and "Legal Proceedings," or (5) the Marketing Agent's performance of its duties under the Marketing Agent Agreement, and to contribute to payments that the Purchaser or the Marketing Agent may be required to make in respect thereof or (5) the Marketing Agent's performance of its duties under the Marketing Agent Agreement.thereof. The TrustTrustee has agreed to reimburse the Purchaser and the Marketing Agent, in respectsolely from and to the extent of anythe Trust's assets, for indemnification and contribution amounts due from the Sponsor arising under the preceding sentence and the Purchaser for indemnification and contribution amounts due from the Sponsor in respect of the items identified in subsections (1), (2), (3) and (3)(4) of the preceding sentence to the extent the Sponsor has not paid such amounts directly when due. Under the Participant Agreement, the Sponsor also has agreed to indemnify the Authorized Participants against certain liabilities, including liabilities under the Securities Act of 1933, as amended (Securities Act) and to contribute to payments that the Authorized Participants may be required to make in respect of such liabilities. The Trustee has agreed to reimburse the Authorized Participants, solely from and to the extent of the Trust's assets, for indemnification and contribution amounts due from the Sponsor in respect of such liabilities to the extent the Sponsor has not paid such amounts when due. In the event the Trust is required to pay any such amounts, the Trustee would be required to sell assets of the Trust to cover the amount of any such payment and the NAV of the Trust would be reduced accordingly, thus adversely affecting an investment in the Shares.