As filed with the Securities and Exchange Commission on July 7, 2006January 26, 2007

Registration No. 333-134669333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

AIRCASTLE LIMITED

(Exact name of registrant as specified in its charter)

| Bermuda | 7359 | 98-0444035 | ||||

| (State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) | ||||

c/o Aircastle Advisor LLC

300 First Stamford Place

5th Floor

Stamford, Connecticut 06902

(203) 504-1020

(Address, Including Zip Code, and Telephone Number,

Including Area Code, of Registrant'sRegistrant’s Principal Executive Offices)

David Walton, Esq.

Chief Operating Officer and General Counsel

c/o Aircastle Advisor LLC

300 First Stamford Place

5th Floor

Stamford, Connecticut 06902

(203) 504-1020

(Name, Address, Including Zip Code, and Telephone

Number, Including Area Code, of Agent For Service)

Copies to:

| Joseph A. Coco, Esq. Skadden, Arps, Slate, Meagher & Flom LLP Four Times Square New York, New York 10036-6522 (212) 735-3000 | Edward F. Petrosky, Esq. J. Gerard Cummins, Esq. Sidley Austin LLP 787 Seventh Avenue New York, New York 10019 (212) 839-5300 | ||

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ![]()

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of earlier effective registration statement for the same offering. ![]()

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ![]()

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ![]()

Calculation of Registration Fee

| TITLE OF EACH CLASS OF SECURITIES TO BE REGISTERED | AMOUNTS TO BE REGISTERED(1) | PROPOSED MAXIMUM PER SHARE OFFERING PRICE(2) | PROPOSED MAXIMUM AGGREGATE OFFERING PRICE(1)(2) | AMOUNT OF REGISTRATION FEE | ||||||||||||||||||||

| Common Shares, par value $.01 per share | 15,525,000 | $ | 29.70 | $ | 461,092,500 | $ | 49,337 | |||||||||||||||||

| (1) | Includes 2,025,000 common shares which may be issued upon the exercise of the underwriters over-allotment option |

| (2) | Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(c) under the Securities Act of 1933, as amended, and based upon the average high and low prices on the New York Stock Exchange on January 25, 2007. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and we are not soliciting offers to buy these securities, in any state or jurisdiction where the offer or sale is not permitted.

Subject to completion,Completion, dated July 7, 2006.January 26, 2007

Prospectus

13,500,000 shares

Aircastle Limited

Common shares

ThisAircastle Limited is an initial public offering of13,500,000 common shares of Aircastle Limited.

All of the common shares are being sold by Aircastle.in this offering. After this offering, funds managed by affiliates of Fortress Investment Group LLC will beneficially own approximately %62.0% of Aircastle'sAircastle’s common shares. These funds are not selling any shares in this offering.

Prior to this offering, there has been no public market for theAircastle’s common shares. It is currently estimated that the public offering price per share will be between $ and $ . Aircastle intends to list the common shares are listed on the New York Stock Exchange under the symbol ‘‘ ’’AYR’’. The closing sale price of our common shares on the New York Stock Exchange on February , 2007, was $ per share.

| Per Share | Total | |||||||||||

| Public offering price | $ | $ | ||||||||||

| Underwriting discounts and commissions | $ | $ | ||||||||||

| Proceeds to Aircastle (before expenses) | $ | $ | ||||||||||

We have granted the underwriters a 30-day option to purchase up to 2,025,000 additional common shares at the public offering price less underwriting discounts and commissions for the purpose of covering over-allotments, if any.

Investing in our common shares involves a high degree of risk. See ‘‘Risk factors’Factors’’ beginning on page 10.11.

Neither the Securities and Exchange Commission, state securities regulators, the Minister of Finance and the Registrar of Companies in Bermuda, the Bermuda Monetary Authority nor any other regulatory body has approved or disapproved of these securities or determined if this prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares against payment in New York, New York on , 2006.2007.

| JPMorgan | Bear, Stearns & Co. Inc. | Citigroup | ||||

| Goldman, Sachs & Co. | Morgan Stanley | Jefferies & Company | ||||

, 20062007

Table of Contents

We have not authorized anyone to provide you with different information or to make representations as to matters not stated in this prospectus. You must not rely on unauthorized information. This prospectus may be used only where it is legal to sell these securities. The information in this prospectus is only accurate on the date of this prospectus.

Consent under the Exchange Control Act 1972 (and its related regulations) has been obtained from the Bermuda Monetary Authority for the issue and transfer of our common shares to and between non-residents of Bermuda for exchange control purposes, provided our shares remain listed on an appointed stock exchange, which includes the New York Stock Exchange, or NYSE. This prospectus will be filed with the Registrar of Companies in Bermuda in accordance with Bermuda law. In granting such consent and in accepting this prospectus for filing, neither the Bermuda Monetary Authority nor the Registrar of Companies in Bermuda accepts any responsibility for our financial soundness or the correctness of any of the statements made or opinions expressed in this prospectus.

Prospectus Summary

This summary highlights information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including the section entitled ‘‘Risk Factors’’ and our financial statements and the related notes included elsewhere in this prospectus, before making an investment decision to purchase common shares. Unless the context suggests otherwise, references in this prospectus to ‘‘Aircastle,’’ the ‘‘Company,’’ ‘‘we,’’ ‘‘us,’’ and ‘‘our’’ refer to Aircastle Limited and its subsidiaries. References in this prospectus to ‘‘AL’’ refer only to Aircastle Limited. References in this prospectus to ‘‘Aircastle Bermuda’’ refer to Aircastle Holding Corporation Limited and its subsidiaries. References in this prospectus to ‘‘Fortress’’ refer to Fortress Investment Group LLC, affiliates of which manage the Fortress shareholders,funds, and certain of its affiliates and references to the ‘‘Fortress shareholders’funds’’ refer to AL shareholders which are managed by affiliates of Fortress. Throughout this prospectus, when we refer to our aircraft, we include aircraft that we have transferred into grantor trusts or similar entities for purposes of financing such assets through securitization. These grantor trusts or similar entities are consolidated for purposes of our financial statements. All amounts in this prospectus are expressed in U.S. dollars and the financial statements have been prepared in accordance with U.S. generally accepted accounting principles (‘‘GAAP’’).

Aircastle Limited

We are a global company that acquires and leases high-utility commercial jet aircraft to passenger and cargo airlines throughout the world. High-utility aircraft are generally modern, operationally efficient jets with a large operator base and long useful lives. As of March 31,September 30, 2006, our aircraft portfolio consisted of 4265 aircraft that were leased to 2432 lessees located in 1623 countries and managed through our offices in the United States, Ireland and Singapore. All of our aircraft are subject to net operating leases whereby the lessee is generally responsible for maintaining the aircraft and paying operational and insurance costs and,although, in somea majority of cases, we are obligedobligated to pay a portion of specified maintenance or modification costs. We also make investments in other aviation assets, including debt securities secured by commercial jet aircraft. As of May 22, 2006,January 25, 2007, we had acquired and committed to acquire aviation assets having an aggregate purchase price equal to $1.2$1.9 billion and $244.2 million,$1.8 billion, respectively, for a total of approximately $1.4 billion.$3.7 billion, including our commitment to acquire 38 aircraft from affiliates of Guggenheim Aviation Fund, LP, or GAIF. See ‘‘Recent Developments — Guggenheim.’’ Our revenues and income from continuing operations for the quarternine months ended March 31,September 30, 2006 were $33.0$128.2 million and $7.8$28.0 million, respectively.

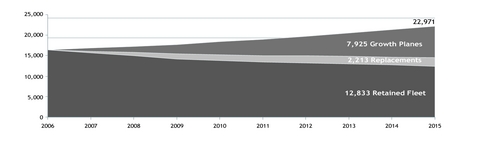

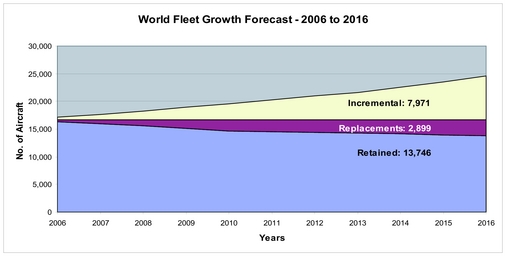

We expect to benefit from the size and growth of the commercial aircraft market and to increase our revenues and earnings by acquiring additional aviation assets. The current worldwide commercial aircraft fleet consists of more than 17,000 aircraft with an aggregate estimated value in excess of $330$360 billion and is expected to grow at a compound annual growth rate of 6.1%5.5% to a total value of $620 billion through 2015.2016. The market is highly fragmented, with over 1,800 owners. Operating lessors, including us, own approximately 30.1%30.9% of the global fleet. The continued growth in air traffic, driven in large part by emerging markets with strong economic growth and rising levels of per capita air travel, has increased the demand, and lease rates, for certain high-utility aircraft types.

On January 22, 2007, we entered into an Asset Purchase Agreement, which we refer to as the Acquisition Agreement, with affiliates of GAIF pursuant which we agreed to acquire 38 aircraft for an aggregate base purchase price of approximately $1.595 billion, subject to certain agreed adjustments. The aircraft we will acquire under the Acquisition Agreement are scheduled to be

delivered to us between January 2007 and February 2009, with 28 of these aircraft scheduled for delivery in 2007. Four of the aircraft are Boeing Model 747-400ERF freighter aircraft to be delivered new from the manufacturer, seven are Boeing Model 747-400 aircraft converted or to be converted from passenger to freighter specification and one is a McDonnell Douglas Model MD11SF. The remaining 26 aircraft are passenger aircraft. We refer to this acquisition in this prospectus as the Aircraft Acquisition.

We intend to pay regular quarterly dividends to our shareholders. We plan to grow our dividends per share through the acquisition of additional aviation assets using cash on hand and available credit facilities. We expect to finance our acquisitions on a long-term basis using low-cost, non-recourse securitizations. Securitizations allow companiesus to raise long-term capital by pledging cash flows of an asset pool, such as aircraft leases. In June 2006, we closed our first securitization which we refer to as Securitization No. 1, a $560 million transaction comprising 40 aircraft and related leases which we refer to as SecuritizationPortfolio No. 1. On , 2006,

The table below is a summary of our board of directors declared an ordinary

dividend of $ per common share for the three months ended , 2006, which is payable on , 2006. This dividendhistory. These dividends may not be indicative of the amount of any future dividends.

| Dividend Period | Pay Date | Dividend Per Share ($) | Total Dividend ($ in thousands) | ||||||||||||

| Three months ended June 30, 2006 | July 31, 2006 | $ | 0.35 | $ | 14,367 | ||||||||||

| Three months ended September 30, 2006 | November 15, 2006 | $ | 0.35 | $ | 16,395 | (1) | |||||||||

| Three months ended December 31, 2006 | January 15, 2007 | $ | 0.4375 | $ | 22,584 | ||||||||||

| (1) | Dividends for the three months ended September 30, 2006 were paid in two installments. A dividend of $0.156 per share was paid on August 15, 2006 for the period July 1, 2006 to August 12, 2006 for the period prior to our initial public offering. A dividend of $0.194 per share was paid on November 15, 2006 for the period after our initial public offering. |

Competitive Strengths

We believe that the following competitive strengths will allow us to capitalize on the growth opportunities in the global aviation industry:

| • | Diversified portfolio of high-utility aircraft.We have a portfolio of |

| • | Disciplined acquisition approach and broad sourcing |

| • | Scaleable business |

| • | Experienced management team with significant technical |

| • | Innovative long-term debt financing |

Growth Strategy

We plan to grow our business and increase our dividends per share by employing the following business strategies:

| • | Selectively acquire commercial jet aircraft and other aviation |

| • | Reinvest amounts approximately equal to non-cash depreciation expense in additional aviation |

| • | Maintain an efficient capital |

Industry Trends

The following industry dynamics create a favorable environment in which to expand our business, including:

| • | Large and growing commercial aircraft fleet. The current worldwide commercial aircraft fleet consists of more than 17,000 aircraft with an aggregate estimated value in excess of |

| • | Increasing use of operating |

| 18.8% to |

| • | Increasing air traffic and demand for commercial |

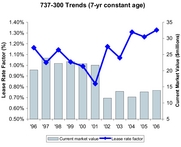

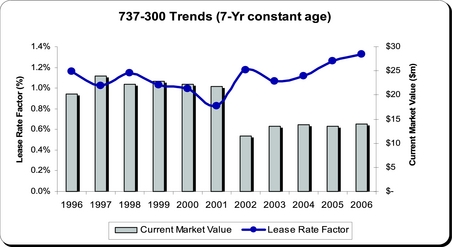

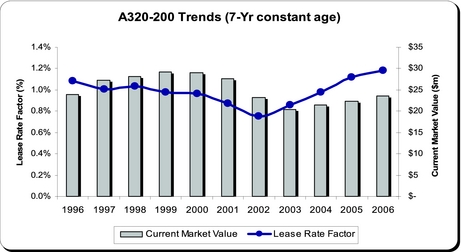

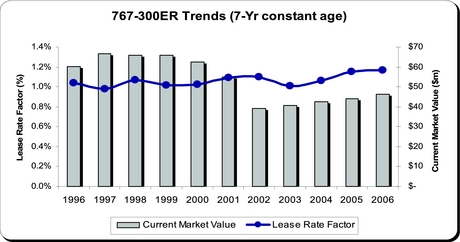

| • | Improving lease rates.Following a downturn from 2001 to 2003, the global commercial aviation industry has experienced a broad based recovery of aircraft values and lease rates. The relative increase in lease rates, however, has exceeded the increase in values for certain aircraft types. As a result, lease rate factors, or the ratio between lease rates and current market values, have been increasing for popular aircraft models such as 737 classics, A320s and 767-300ERs. It is possible, however, that higher lease rates could drive demand toward other aircraft models, new aircraft orders or other financing alternatives, and away from operating leasing for one or more of these popular aircraft models. |

Recent Developments

Securitization

On June 15, 2006 we closed Securitization No. 1. The securitization generated gross proceeds of $560 million through the issuance of floating-rate aircraft lease-backed securities. We expect to refinance the securitization on or prior to June 2011. We have entered into a series of interest

rate hedging contracts which result in a fixed-rate financing cost of 6.6% per annum, including recurring administrative costs and amortization of issuance expenses. The obligations under the aircraft lease-backed securities are secured by the ownership interests in our subsidiaries that own 40 of our aircraft, or Portfolio No. 1, and the related aircraft leases. A portion of the proceeds from Securitization No. 1 were used to repay amounts outstanding under our $525 million senior secured credit facility, which we refer to as Credit Facility No.1.

The aircraft in Portfolio No. 1 had an aggregate initial appraised value, or Initial Appraised Value, of $1.022 billion, based on the lesser of the mean and the median of the base values with respect to such aircraft determined in three base value appraisals from three internationally recognized appraisal firms as of dates from October to December 2005.

SecondFourth Quarter Financial Results

Our net income for the quarter ended June 30, 2006 was $ . Revenues for the quarter ended JuneDecember 31, 2006 were $61.2 million. Of this amount, $58.7 million were aircraft lease rental revenues and $2.5 million was interest income on our debt investments. Fourth quarter aircraft lease rental revenues of $58.7 million included a full quarter of revenue earned on the 65 aircraft owned as of September 30, 2006 were $ . EBITDAand a partial quarter of revenue on the four aircraft purchased during the fourth quarter.

Guggenheim

On January 22, 2007, we entered into the Acquisition Agreement with affiliates of GAIF pursuant to which we agreed to acquire 38 aircraft for the quarter ended June 30, 2006 was $ . Our basican aggregate base purchase price of approximately $1.595 billion, subject to certain agreed adjustments. See ‘‘Management’s Discussion and diluted income per share from net income for the quarter ended June 30, 2006 was $Analysis of Financial Condition and $ , respectively.Results of Operations—Acquisitions and Dispositions’’.

Fortress

Fortress is a leading global alternative investment management firm founded in 1998 with over $21approximately $29.7 billion of equity capital currently under management. Fortress is headquartered in New York City and has affiliates with offices in Dallas, Frankfurt, Geneva, Hong Kong,San Diego, Toronto, London, Rome, San Diego, SydneyFrankfurt, and Toronto.Sydney. Fortress manages capital for a diverse group of investors, including pension funds, university endowments and foundations, financial institutions, funds-of-funds and high-net-worth individuals. To date, the Fortress funds have contributed approximately $400.0 million in equity capital to us.

Additional Information

We are a Bermuda exempted company and were incorporated on October 29, 2004 under the provisions of Section 14 of the Companies Act 1981 of Bermuda. To date, Fortress has contributed approximately $400 million in equity capital to us. Our registered office is located

at Clarendon House, 2 Church Street, Hamilton HM 11, Bermuda, and our principal executive offices are located at c/o Aircastle AdvisorsAdvisor LLC, 300 First Stamford Place, 5th Floor, Stamford, Connecticut 06902. Our subsidiaries also maintain offices at Harcourt Centre, Harcourt Road,8 Fitzwilliam Place, Dublin 2, Ireland; and 6 Battery Road, #30-00, Singapore, 049909. Our main telephone number is 203-504-1020. Our internet address is www.aircastle.com. Information on our website does not constitute part of this prospectus.

The Offering

| Common shares offered by us in this offering | 13,500,000 shares | ||

| Common shares to be issued and outstanding after this offering | 65,121,279 shares | ||

| Use of proceeds | We expect to use the net proceeds from this offering to repay approximately $ million of the amount outstanding | |

| Dividend policy | On | |

| ‘‘AYR’’ | ||

| Risk factors | Please read the section entitled ‘‘Risk Factors’’ beginning on page | |

| Important tax considerations | We expect that we will be treated as a passive foreign investment company, or PFIC, for U.S. federal income tax purposes. In order to avoid possible deferred tax and interest charges under the U.S. Internal Revenue Code and regulations thereunder, you will need to make a ‘‘qualified electing fund,’’ or QEF, election, with respect to your investment in common shares and with respect to each of our PFIC subsidiaries. Investors who are U.S. persons should consult with their tax advisors as to whether or not to make such election and the related consequences and should carefully review the information set forth under ‘‘Material Tax Considerations — Material United States Federal Income Tax Considerations — Consequences to U.S. Holders — Passive Foreign Investment Company Status and Related Tax Consequences’’ for additional information. | |

The number of common shares to be issued and outstanding after this offering is based on 40,992,00051,621,279 common shares issued and outstanding as of , 2006,January 25, 2007, and excludes an additional 3,138,0002,950,698 common shares which remain available for issuance under our equity and incentive plan. See ‘‘Management — Equity Incentive Plan.’’

Except as otherwise indicated, all information in this prospectus:prospectus assumes no exercise by the underwriters of their option to purchase an additional 2,025,000 common shares from us to cover over-allotments.

Summary Consolidated Financial Information

The following tables summarize the consolidated financial information for our business. You should read these tables along with ‘‘Management'sManagement’s Discussion and Analysis of Financial Condition and Results of Operations,’’ ‘‘Business’’ and our consolidated historical financial statements and the related notes included elsewhere in this prospectus.

We derived the summary historical consolidated statements of operations data and consolidated statements of cash flows data for the period from inception through December 31, 2004 and the year ended December 31, 2005 and the summary historical consolidated balance sheets data as of December 31, 2004 and 2005, set forth below, from our audited consolidated financial statements included elsewhere in this prospectus. AL was incorporated and commenced operations on October 29, 2004. The statements of operations data and consolidated statements of cash flows data for the threenine months ended March 31,September 30, 2005 and 2006 and the balance sheets data as of March 31,September 30, 2006 are derived from our unaudited consolidated interim financial statements included elsewhere in this prospectus. The results for any interim period are not necessarily indicative of the results that may be expected for a full fiscal year.

| Period from October 29 (Commencement of Operations) Through December 31, | Year Ended December 31, | Three Months Ended March 31, | Period from October 29, 2004 (Commencement of Operations) Through December 31, | Year Ended December 31, | Nine Months Ended September 30, | |||||||||||||||||||||||||||||||||||||||||||

| 2004 | 2005 | 2005 | 2006 | 2004 | 2005 | 2005 | 2006 | |||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands, except per share data) | (Dollars in thousands, except per share data) | |||||||||||||||||||||||||||||||||||||||||||||||

| Consolidated Statements of Operations Data: | ||||||||||||||||||||||||||||||||||||||||||||||||

| Total revenues | $ | 78 | $ | 36,026 | $ | 2,187 | $ | 33,012 | $ | 78 | $ | 36,026 | $ | 15,337 | $ | 128,154 | ||||||||||||||||||||||||||||||||

| Selling, general and administrative expenses | 1,117 | 12,595 | 1,548 | 5,954 | ||||||||||||||||||||||||||||||||||||||||||||

| Selling, general and administrative expenses (including non-cash share based payment expense of $249 and $7,729 for the nine months ended September 30, 2005 and 2006, respectively) | 1,117 | 12,595 | 7,950 | 21,219 | ||||||||||||||||||||||||||||||||||||||||||||

| Depreciation | 390 | 14,460 | 1,462 | 9,915 | 390 | 14,460 | 6,644 | 38,182 | ||||||||||||||||||||||||||||||||||||||||

| Interest expense, net | (9) | 7,739 | 313 | 7,717 | ||||||||||||||||||||||||||||||||||||||||||||

| Interest (income) expense, net | (9 | ) | 7,739 | 3,217 | 35,058 | |||||||||||||||||||||||||||||||||||||||||||

| Income (loss) from continuing operations | (1,465) | (879) | (1,374) | 7,781 | (1,465 | ) | (879 | ) | (3,856 | ) | 28,013 | |||||||||||||||||||||||||||||||||||||

| Discontinued operations | — | 1,107 | — | 3,399 | — | 1,107 | — | 3,399 | ||||||||||||||||||||||||||||||||||||||||

| Net income (loss) | (1,465) | 228 | (1,374) | 11,180 | (1,465 | ) | 228 | (3,856 | ) | 31,412 | ||||||||||||||||||||||||||||||||||||||

| Basic income (loss) per share: | ||||||||||||||||||||||||||||||||||||||||||||||||

| Income (loss) from continuing operations | $ | (.04) | $ | (.02) | $ | (.03) | $ | .19 | $ | (.04 | ) | $ | (.02 | ) | $ | (.10 | ) | $ | .64 | |||||||||||||||||||||||||||||

| Discontinued operations | $ | — | $ | .03 | $ | — | $ | .08 | $ | — | $ | .03 | $ | — | $ | .08 | ||||||||||||||||||||||||||||||||

| Net income (loss) | $ | (.04) | $ | .01 | $ | (.03) | $ | .27 | $ | (.04 | ) | $ | .01 | $ | (.10 | ) | $ | .72 | ||||||||||||||||||||||||||||||

| Diluted earnings (loss) per share: | ||||||||||||||||||||||||||||||||||||||||||||||||

| Income (loss) from continuing operations | $ | (.04) | $ | (.02) | $ | (.03) | $ | .19 | $ | (.04 | ) | $ | (.02 | ) | $ | (.10 | ) | $ | .63 | |||||||||||||||||||||||||||||

| Discontinued operations | $ | — | $ | .03 | $ | — | $ | .08 | $ | — | $ | .03 | $ | — | $ | .08 | ||||||||||||||||||||||||||||||||

| Net income (loss) | $ | (.04) | $ | .01 | $ | (.03) | $ | .27 | $ | (.04 | ) | $ | .01 | $ | (.10 | ) | $ | .71 | ||||||||||||||||||||||||||||||

| Other Operating Data: | ||||||||||||||||||||||||||||||||||||||||||||||||

| EBITDA(1) | (1,084) | 22,260 | 570 | 26,417 | (1,054 | ) | 22,994 | 7,017 | 102,613 | |||||||||||||||||||||||||||||||||||||||

| Consolidated Statements of Cash Flows Data: | ||||||||||||||||||||||||||||||||||||||||||||||||

| Cash flows provided by (used in) operating activities | $ | 4,290 | $ | 20,562 | $ | (1,886) | $ | 13,904 | ||||||||||||||||||||||||||||||||||||||||

| Cash flows provided by operating activities | $ | 4,290 | $ | 20,562 | $ | 766 | $ | 87,433 | ||||||||||||||||||||||||||||||||||||||||

| Cash flows used in investing activities | (97,405) | (742,144) | (51,313) | (255,159) | (97,405 | ) | (742,144 | ) | (198,566 | ) | (820,960 | ) | ||||||||||||||||||||||||||||||||||||

| Cash flows provided by financing activities | 93,115 | 801,525 | 96,656 | 188,866 | 93,115 | 801,525 | 259,886 | 692,554 | ||||||||||||||||||||||||||||||||||||||||

| As of December 31, | As of March 31, | As of December 31, | As of September 30, | |||||||||||||||||||||||||||||||||

| 2004 | 2005 | 2006 | 2004 | 2005 | 2006 | |||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | |||||||||||||||||||||||||||||||||||

| Consolidated Balance Sheets Data: | ||||||||||||||||||||||||||||||||||||

| Flight equipment held for lease, net of accumulated depreciation | $ | 94,430 | $ | 746,124 | $ | 941,692 | $ | 94,430 | $ | 746,124 | $ | 1,509,443 | ||||||||||||||||||||||||

| Debt securities, available for sale | — | 26,907 | 120,558 | — | 26,907 | 120,271 | ||||||||||||||||||||||||||||||

| Total assets | 104,981 | 967,532 | 1,218,462 | 104,981 | 967,532 | 1,808,459 | ||||||||||||||||||||||||||||||

| Borrowings under credit facilities | — | 490,588 | 568,859 | — | 490,588 | 351,226 | ||||||||||||||||||||||||||||||

| Borrowings under securitization | — | — | 554,733 | |||||||||||||||||||||||||||||||||

| Repurchase agreements | — | 8,665 | 84,434 | — | 8,665 | 83,839 | ||||||||||||||||||||||||||||||

| Shareholders' equity (2) | 99,235 | 410,936 | 475,800 | |||||||||||||||||||||||||||||||||

| Shareholders’ equity(2) | 99,235 | 410,936 | 648,361 | |||||||||||||||||||||||||||||||||

| Other Data: | ||||||||||||||||||||||||||||||||||||

| Number of aircraft (at end of period) | 3 | 32 | 42 | 3 | 32 | 65 | ||||||||||||||||||||||||||||||

| Total debt to total capitalization | N/A | 54.9 | % | 57.9 | % | N/A | 54.9 | % | 60.4 | % | ||||||||||||||||||||||||||

(1) EBITDA is a measure of operating performance that is not calculated in accordance with GAAP. EBITDA should not be considered a substitute for net income, income from operations or cash flows provided by or used in operations, as determined in accordance with GAAP. EBITDA is a key measure of our operating performance used by management to focus on consolidated operating performance exclusive of income and expense that relate to the financing and capitalization of the business.

We define EBITDA as income (loss) from continuing operations before income taxes, interest expense and depreciation and amortization. We use EBITDA to assess our consolidated financial and operating performance, and we believe this non-GAAP measure, is helpful in identifying trends in our performance. This measure provides an assessment of controllable expenses and affords management the ability to make decisions which are expected to facilitate meeting current financial goals as well as achieve optimal financial performance. It provides an indicator for management to determine if adjustments to current spending decisions are needed. EBITDA provides us with a measure of operating performance because it assists us in comparing our operating performance on a consistent basis as it removes the impact of our capital structure (primarily interest charges on our outstanding debt) and asset base (primarily depreciation and amortization) from our operating results. Accordingly, this metric measures our financial performance based on operational factors that management can impact in the short-term, namely the cost structure or expenses of the organization. EBITDA is one of the metrics used by senior management and our board of directors to review the consolidated financial performance of the business.

| (1) | EBITDA is a measure of operating performance that is not calculated in accordance with GAAP. EBITDA should not be considered a substitute for net income, income from operations or cash flows provided by or used in operations, as determined in accordance with GAAP. EBITDA is a key measure of our operating performance used by management to focus on consolidated operating performance exclusive of income and expense that relate to the financing and capitalization of the business. |

| We define EBITDA as income (loss) from continuing operations before income taxes, interest expense and depreciation and amortization. We use EBITDA to assess our consolidated financial and operating performance and we believe this non-GAAP measure is helpful in identifying trends in our performance. This measure provides an assessment of controllable expenses and affords management the ability to make decisions which are expected to facilitate meeting current financial goals as well as achieve optimal financial performance. It provides an indicator for management to determine if adjustments to current spending decisions are needed. EBITDA provides us with a measure of operating performance because it assists us in comparing our operating performance on a consistent basis as it removes the impact of our capital structure (primarily interest charges on our outstanding debt) and asset base (primarily depreciation and amortization) from our operating results. Accordingly, this metric measures our financial performance based on operational factors that management can impact in the short-term, namely the cost structure or expenses of the organization. EBITDA is one of the metrics used by senior management and our board of directors to review the consolidated financial performance of the business. |

The table below shows the reconciliation of net income (loss) to EBITDA for the threenine months ended March 31,September 30, 2005 and 2006 and the period from October 29 through December 31, 2004 and the year ended December 31, 2005.

| Period from October 29, 2004 (Commencement of Operations) Through December 31, 2004 | Year Ended December 31, 2005 | Three Months Ended March 31, | Period from October 29, 2004 (Commencement of Operations) Through December 31, 2004 | Year Ended December 31, | Nine Months Ended September 30, | |||||||||||||||||||||||||||||||||||||||||||

| 2005 | 2006 | 2005 | 2005 | 2006 | ||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||

| Net income (loss) | $ | (1,465 | ) | $ | 228 | $ | (1,374 | ) | $ | 11,180 | $ | (1,465 | ) | $ | 228 | $ | (3,856 | ) | $ | 31,412 | ||||||||||||||||||||||||||||

| Depreciation | 390 | 14,460 | 1,462 | 9,915 | 390 | 14,460 | 6,644 | 38,182 | ||||||||||||||||||||||||||||||||||||||||

| Interest, net | (9 | ) | 7,739 | 313 | 7,717 | |||||||||||||||||||||||||||||||||||||||||||

| Amortization(a) | 30 | 734 | 551 | (3,093 | ) | |||||||||||||||||||||||||||||||||||||||||||

| Interest, (income) expense, net | (9 | ) | 7,739 | 3,217 | 35,058 | |||||||||||||||||||||||||||||||||||||||||||

| Income tax provision | — | 940 | 169 | 1,004 | — | 940 | 461 | 4,453 | ||||||||||||||||||||||||||||||||||||||||

| Earnings from discontinued operations, net taxes | — | (1,107 | ) | — | (3,399 | ) | ||||||||||||||||||||||||||||||||||||||||||

| Earnings from discontinued operations, net of taxes | — | (1,107 | ) | — | (3,399 | ) | ||||||||||||||||||||||||||||||||||||||||||

| EBITDA | $ | (1,084 | ) | $ | 22,260 | $ | 570 | $ | 26,417 | $ | (1,054 | ) | $ | 22,994 | $ | 7,017 | $ | 102,613 | ||||||||||||||||||||||||||||||

(2) The following table sets forth (a) our capitalization at March 31, 2006, (b) our capitalization as of such date as adjusted to give effect to: (i) the use of a portion of proceeds from Securitization No. 1 to repay $487.0 million of indebtedness under Credit Facility No. 1 and to return $36.9 million to Fortress in exchange for the cancellation of 3,693,200 common shares; (ii) the payment of an ordinary dividend from cash on hand in the amount of $ per common share, or an aggregate of $ million, declared by our board of directors on , 2006 and paid on , 2006; and (iii) the purchase of 277,000 common shares by employees and a director nominee in May, 2006 and (c) our capitalization as of such date as further adjusted to give effect to this offering and the use of proceeds therefrom.

| (a) | Includes amortization of lease premiums and discounts and excludes amortization of deferred financing costs which are included in interest expense. |

| (2) | The following table sets forth our capitalization at September 30, 2006 and our capitalization as of such date as adjusted to give effect to this offering and repayment of certain outstanding amounts under Amended Credit Facility No. 2 and the Revolving Credit Facility using a portion of the net proceeds of this offering. |

| Actual | Adjusted | As further Adjusted | Actual | As Adjusted | ||||||||||||||||||||||||||

| Borrowings under credit facilities | $ | 568,859 | $ | $ | $ | 351,226 | $ | 73,332 | ||||||||||||||||||||||

| Securitization debt | — | |||||||||||||||||||||||||||||

| Borrowings under securitization | 554,733 | 554,733 | ||||||||||||||||||||||||||||

| Repurchase agreements | 84,434 | 83,839 | 83,839 | |||||||||||||||||||||||||||

| Common shares | 444 | 515 | ||||||||||||||||||||||||||||

| Additional paid-in capital | 438,189 | 629,238 | ||||||||||||||||||||||||||||

| Retained earnings | 9,943 | 9,405 | ||||||||||||||||||||||||||||

| Accumulated other comprehensive income | 27,224 | 9,203 | ||||||||||||||||||||||||||||

| Total shareholders' equity | 475,800 | |||||||||||||||||||||||||||||

| Total shareholders’ equity | 648,361 | |||||||||||||||||||||||||||||

| Total capitalization | $ | 1,129,093 | $ | $ | $ | 1,638,159 | ||||||||||||||||||||||||

Risk Factors

Investing in our common shares involves a high degree of risk. You should carefully consider the following risk factors, as well as other information contained in this prospectus, before deciding to invest in our common shares. Generally, the risks facing us fall into five categories –— Risks Related to Our Business, Risks Related to the Aviation Industry, Risks Related to Our Organization and Structure, Risks Related to this Offering, and Risks Related to Taxation. The occurrence of any of the following risks could materially and adversely affect our business, prospects, financial condition, results of operations and cash flow, in which case, the trading price of our common shares would decline and you could lose all or part of your investment.

Risks Related to Our Business

Risks related to our operations

We have limited operating history and we are therefore subject to the risks generally associated with the formation of any new business.

We were incorporated in October 2004, prior to which we had no operations or assets. We are therefore subject to the risks generally associated with the formation of any new business, including the risk that we will not be able to implement our business strategies. Because of our limited operating history, it will be difficult for investors to assess the quality of our management team and our results of operations, and our financial performance to date may not be indicative of our long-term future performance. Furthermore, due to the lack of comparative annual historical financial statements, investors will find it more difficult to evaluate our performance and assess our future prospects than it would be were such information available. In addition, over our brief history we have incurred net losses of approximately $1.5 million for the period from October 29, 2004 through December 31, 2004, net income of only $228,000 for the year ended December 31, 2005, and net income of approximately $11.2$31.4 million for the threenine months ended March 31,September 30, 2006. We may not be able to achieve, maintain and/or increase profitability in the future. In addition, although we have grown substantially since our inception, there can be no assurance that we will be able to continue to effectively integrate acquired aircraft, including significant acquisitions such as the Aircraft Acquisition.

We have significant customer concentration and the loss ofdefaults by one or more of our major customers could have a material adverse effect on our cash flow and earnings and our ability to meet our debt obligations and pay dividends on our common shares.

Lease rental revenue from our four largest customers, US Airways, Inc., Hainan Airlines, Swiss International and Air India,Europa, accounted for 50.1%41% of our total revenue for the threenine months ended March 31,September 30, 2006. The lease rental revenue, as a percent of our total revenue, for these four customers for that period was 28.1%approximately 24%, 11.5%9%, 5.5%4% and 5.0%4%, respectively. These customers operate under 1317 operating lease agreements that have terms ranging from 1.5five months to 8.0eight years. In addition, US Airways, Inc. reorganized under Chapter 11 in August 2002 and exited bankruptcy in March 2003. US Airways, Inc. again reorganized in September 2004 and, in September 2005, exited bankruptcy and merged with America West Airlines. The loss of one or more of these customers or their inability to make operating lease payments due to financial difficulties, bankruptcy or otherwise could have a material adverse effect on our cash flow and earnings and our ability to meet our debt obligations and pay dividends on our common shares.

Under our current business model, we will need additional capital to finance our growth, and we may not be able to obtain it on terms acceptable to us, or at all, which may limit our ability to grow and compete in the aviation market.

Continued expansion of our business through the acquisition of additional aircraft and other aviation assets will require additional capital, particularly if we were to accelerate our acquisition plans. Financing may not be available to us or may be available to us only on terms that are not favorable. Furthermore, Amended Credit Facility No. 2 may be used to finance only 65% of the purchase price of the aircraft financed with proceeds from the facility. In addition, the terms of certain of our outstanding indebtedness restrict, among other things, our ability to incur additional debt. OurAmended Credit Facility No. 2 and the Revolving Credit Facility, subject to certain limited exceptions, prohibitseach prohibit us from incurring additional recourse debt or guaranteeing the indebtedness of our subsidiaries. If we are unable to raise additional funds or obtain capital on terms acceptable to us, we may have to delay, modify or abandon some or all of our growth strategies. Further, if additional capital is raised through the issuance of additional equity securities, the percentage ownershipinterests of our then current common shareholders would be diluted. Newly issued equity securities may have rights, preferences or privileges senior to those of our common shares. See ‘‘Description of Share Capital.’’

We may not be able to issue aircraft lease-backed securities on attractive terms, which may require us to seek more costly or dilutive financing for our investments or to liquidate assets.

We intend to continue to finance our aircraft portfolio on a long-term basis through the aircraft securitization market. We primarily use short-term credit facilities to finance the acquisition of aircraft until we accumulate a sufficient quantity, quality and diversity of aircraft, at which time we intend to refinance these facilities through a securitization, such as an issuance of aircraft lease-backed securities, or other long-term financing. As a result, we are subject to the risk that we will not be able to acquire, during the period that our credit facilities are available, a sufficient amount of eligible aircraft to maximize the efficiency of an issuance of aircraft lease-backed securities. We also may not be able to obtain additional credit facilities or may not be able to renew or refinance any of our existing credit facilities should we need more time to acquire aircraft necessary for a long-term securitization financing. In addition, we anticipate refinancing our securitization transactions within five years of closing each such transaction. The inability to renew or refinance our credit facilities may require us to seek more costly or dilutive financing for our aircraft or to liquidate assets. In addition, conditions in the capital markets may make the issuance of aircraft lease-backed securities more costly or otherwise less attractive to us when we do have a sufficient pool of aircraft or during the period of time when we anticipate refinancing a securitization portfolio. We also may not be able to structure any future securitizations to allow for distributions of excess securitization cash flows to us. If we are unable to access the securitization market to finance these assets, we may be required to seek other forms of more costly, dilutive or otherwise less attractive financing or otherwise to liquidate the assets.

An increase in our borrowing costs may adversely affect our earnings and cash available for distribution to our shareholders.

We enter into repurchase agreements to finance a portion of the purchase price of our debt securities. Our repurchase agreements typically have initial terms to maturity of between six months2007 and one year.2008. We utilize credit facilities to finance a portion of the purchase price of our aircraft. Our credit facilities have had initial terms to maturity ranging from December 31, 2007, in the case of between one and two years.the Revolving Credit Facility, to December 31, 2008, in the case of Amended Credit Facility No. 2. As our repurchase agreements and credit facilities mature, we will be required to either refinance

these instruments by entering into new repurchase agreements or credit facilities, which could result in higher borrowing costs, or repay them by using cash on hand or cash from the sale of our assets.

Our repurchase agreements and credit facilities are primarily LIBOR-based floating-rate obligations and the interest expense we incur will vary with changes in the applicable LIBOR reference rate. As a result, an increaseto the extent we are not sufficiently hedged, changes in short-terminterest rates willmay increase our interest costs and may reduce the spread between the returns on our portfolio investments and the cost of our borrowings. An increase in interest rates would adversely affect the market value of our debt investments that are fixed-rate and/or subject them to prepayment or extension risk, which may adversely affect our earnings and cash available for distribution to our shareholders.

As of March 31,September 30, 2006, if interest rates were to increase by 1%, we would expect to incur an increase in interest expense on our repurchase agreements of approximately $25,000$89,400 on an annualized basis, net of amounts received from our interest rate hedges. Also, as of March 31,September 30, 2006, on a pro forma basis, after giving effect to the use of a portion of the proceeds of Securitization No. 1 to pay down a portion of the outstanding obligations on our credit facilities, if interest rates were to increase by 1%, we would expect to incur an increasea decrease in annual interest expense on our credit facilities of approximately $46,000$1.5 million on an annualized basis, net of amounts received from our interest rate hedges.

Departure of key officers could harm our business and financial results.

Our senior management'smanagement’s reputations and relationships with lessees and sellers of aircraft are a critical element of our business. We encounter intense competition for qualified employees from other companies in the airlineaircraft leasing industry, and we believe there are only a limited number of available qualified executives in our industry. Our future success depends, to a significant extent, upon the continued service of our senior management personnel, particularly: Ron Wainshal, our Chief Executive Officer; Mark Zeidman, our Chief Financial Officer; and David Walton, our Chief Operating Officer and General Counsel, each of whose services are critical to the successful implementation of our growth strategies. These key officers have been with us as we have substantially grown our operations since the end of 2005 and as a result have been critical to our development. If we were to lose the services of any of these individuals, our business and financial results could be adversely affected. See ‘‘Management.’’

We may not be able to pay or maintain dividends and the failure to do so would adversely affect our share price.

On , 2006, our board of directors declared an ordinaryJanuary 15, 2007, we paid a regular quarterly dividend of $$0.4375 per common share, or an aggregate of $ ,approximately $22.6 million, for the three months ended ,December 31, 2006, which is payable on ,to shareholders of record as of December 29, 2006. This dividendThese dividends may not be indicative of the amount of any future dividends. We intend to continue to pay regular quarterly dividends to our shareholders; however, our ability to pay, maintain or expand cash dividends to our shareholders and to execute our dividend payment strategy is subject to the discretion of our board of directors and will depend on many factors, including our ability to make and finance acquisitions, our ability to negotiate favorable lease and other contractual terms, the level of demand for our aircraft, the economic condition of the commercial aviation industry generally, the financial condition and liquidity of our lessees, the lease rates we are able to charge and realize, our leasing costs, unexpected or increased expenses, the level and timing of capital expenditures, principal repayments and other capital needs, the value of our aircraft portfolio, our results of operations, financial condition and liquidity, general business conditions, restrictions imposed by our securitizations or other financing arrangements (including our credit facilities), legal restrictions on the payment of dividends and other factors that our board of directors deems relevant. Some of the factors are beyond our control and a change in any such factor could affect

our ability to pay dividends on our common shares. In the future we may not be able to pay or maintain dividends. We also may not be able to maintain our current level of dividends or increase them over time. Increases in demand for our aircraft and operating lease payments may not occur, and may not increase our actual cash

available for dividends to our common shareholders. See ‘‘Dividend Policy.’’ The failure to maintain or pay dividends would adversely affect our share price.

We are subject to risks related to our indebtedness that may limit our operational flexibility, our ability to compete with our competitors and our ability to pay dividends on our common shares.

General Risks.Our indebtedness subjects us to certain risks, including:

| • | substantially all of our aircraft leases serve as collateral for our secured indebtedness and the terms of certain of our indebtedness require us to use proceeds from sales of aircraft, in part, to repay amounts outstanding under such indebtedness; |

| • | we may be required to dedicate a substantial portion of our cash flows from operations, if available, to debt service payments, thereby reducing the amount of our cash flow available to pay dividends, fund working capital, make capital expenditures and satisfy other needs; |

| • | our failure to comply with the terms of our indebtedness, including restrictive covenants contained therein, may result in additional interest being due or defaults that could result in the acceleration of the principal, and unpaid interest on, the defaulted debt, as well as the forfeiture of the aircraft pledged as collateral; and |

| • | we are not permitted to pay dividends on our common shares to the extent a default or an event of default exists under the Revolving Credit |

Risks relating to Securitization No. 11.. The terms of Securitization No. 1 require us to satisfy certain financial covenants, including the maintenance of debt service coverage ratios. Our compliance with these covenants depends substantially upon the timely receipt of lease payments from our lessees. In particular, during the first five years from issuance, Securitization No. 1 has an amortization schedule that requires that lease payments be applied to reduce the outstanding principal balance of the indebtedness so that such balance remains at 54.8% of the assumed future depreciated value of the portfolio. If the debt service coverage ratio requirements are not met on two consecutive monthly payment dates in the fourth and fifth year following the closing date of Securitization No. 1, and in any month following the fifth anniversary of the closing date, all excess securitization cash flow is required to be used to reduce the principal balance of the indebtedness and will not be available to us for other purposes, including paying dividends to our shareholders.

In addition, under the terms of Securitization No. 1, certain transactions will require the consent or approval of one or more of the securitization trustees, the rating agencies that rated the Portfolio 1 certificates and the financial guaranty insurance policy issuer for the securitization, including (i) sales of aircraft at prices below certain scheduled minimum amounts or, in any calendar year, in amounts in excess of 10% of the portfolio value at the beginning of that year, (ii) the re-leasingleasing of aircraft to the extent not in compliance with the lessee and geographic concentration limits, and the other operating covenants, pursuant to the terms of the securitization (iii) modifying an aircraft if the cost thereof would exceed certain amounts or (iv) entering into any transaction between us and the Securitization No. 1 entities not already contemplated in the securitization. Absent the aforementioned consent, which we may not receive, the lessee and geographic concentration limits under Securitization No. 1 will require us to re-lease the aircraft to a diverse set of customers, and may place limits on our ability to re-leaselease

the 40 aircraft, or Portfolio No. 1, aircraftwhich are the security for Securitization No. 1, to certain customers in certain jurisdictions, even if to do so would provide the best risk-adjusted returns at that time.

Risks relating to our credit facilitiesfacilities.. The terms of our credit facilities restrict our ability to:

| • | create liens on assets; |

| • | incur additional indebtedness; |

| • | sell assets; |

| • | make certain investments or capital expenditures; |

| • | engage in mergers, amalgamations or consolidations; |

| • | engage in certain transactions with affiliates; |

| • | incur secured indebtedness; and |

| • | receive payments or excess cash flows from subsidiaries. |

Amended Credit Facility No. 2 requires us to make principal payments to the extent that amounts outstanding under the facility exceed 85%65% of the depreciated book valuepurchase price or, in the case of a loan that financed the acquisition of an aircraft that has been outstanding more than twelve months, 65% of 95% of the purchase price, of the aircraft financed with proceeds from the facility. In addition, upon completion of this offering, we will be requiredour Revolving Credit Facility requires us to maintain a minimum consolidated net worth of at least $500 million under the terms of Credit Facility No. 2.$550.0 million.

The restrictions described above may impair our ability to operate and compete with our direct and indirect competitors.competitors and to pay dividends on our common shares.

Failure to close the Aircraft Acquisition could negatively impact our share price and financial results.

On January 22, 2007 we entered into the Acquisition Agreement pursuant to which we agreed to acquire 38 aircraft for an aggregate base purchase price of approximately $1.595 billion, subject to certain agreed adjustments. The aircraft we will acquire under the Acquisition Agreement are scheduled to be delivered to us between January 2007 and February 2009. If we are unable to obtain the necessary financing or various conditions to the Aircraft Acquisition are not satisfied, we will be unable to close some or all of the aircraft under the Acquisition Agreement. If the Aircraft Acquisition is not closed for these or other reasons, we will be subject to several risks, including the following:

| • | having to pay and expense certain significant costs relating to the Aircraft Acquisition, such as liquidated damages, legal, accounting and financial advisory, without realizing any of the benefits of having the transactions completed; and |

| • | the focus of our management having been spent on the Aircraft Acquisition instead of on pursuing other opportunities that could have been beneficial to us, without realizing any of the benefits of having the transaction completed. |

These risks could materially and adversely affect our share price and financial results.

Risks Related to Our Aviation Assets

The variability of supply and demand for aircraft could depress lease rates for our aircraft, which would have an adverse effect on our financial results and growth prospects and on our ability to meet our debt obligations and to pay dividends on our common shares.

The aircraft leasing and sales industry has experienced periods of aircraft oversupply and undersupply. The oversupply of a specific type of aircraft in the market is likely to depress aircraft lease rates for and the value of that type of aircraft.

The supply and demand for aircraft is affected by various cyclical and non-cyclical factors that are not under our control, including:

| • | passenger and air cargo demand; |

| • | fuel costs and general economic conditions affecting our lessees’ operations; |

| • | geopolitical events, including war, prolonged armed conflict and acts of terrorism; |

| • | outbreaks of communicable diseases and natural disasters; |

| • | governmental regulation; |

| • | interest rates; |

| • | airline restructurings and bankruptcies; |

| • | the availability of credit; |

| • | manufacturer production levels and technological innovation; |

| • | retirement and obsolescence of aircraft models; |

| • | manufacturers merging or exiting the industry or ceasing to produce aircraft types; |

| • | reintroduction into service of aircraft previously in storage; and |

| • | airport and air traffic control infrastructure constraints. |

These factors may produce sharp decreases or increases in aircraft values and lease rates, which would impact our cost of acquiring aircraft, and may result in lease defaults and also prevent the aircraft from being re-leased or, if desired, sold on favorable terms. This would have an adverse effect on our financial results and growth prospects and on our ability to meet our debt obligations and to pay dividends on our common shares.

Other factors that increase the risk of decline in aircraft value and lease rates could have an adverse affect on our financial results and growth prospects and on our ability to meet our debt obligations and to pay dividends on our common shares.

In addition to factors linked to the aviation industry generally, other factors that may affect the value and lease rates of our aircraft include:

| • | the particular maintenance and operating history of the airframe and engines; |

| • | the number of operators using that type of aircraft; |

| • | whether the aircraft is subject to a lease and, if so, whether the lease terms are favorable to the lessor; |

| • | any renegotiation of a lease on less favorable terms; |

| • | any regulatory and legal requirements that must be satisfied before the aircraft can be purchased, sold or re-leased; and |

| • | compatibility of our aircraft configurations or specifications with other aircraft owned by operators of that type. |

Any decrease in the values of and lease rates for commercial aircraft which may result from the above factors or other unanticipated factors may have a material adverse effect on our financial results and growth prospects and on our ability to meet our debt obligations and to pay dividends on our common shares.

The concentration of aircraft types in our aircraft portfolio could lead to adverse effects on our business and financial results should any difficulties specific to these particular types of aircraft occur.

As of March 31,September 30, 2006, our aircraft portfolio included 1415 aircraft types, the three highest concentrations of which together represented 51.8%49.9% of our aircraft by net book value:

| • | A310-300F constitute |

| • | A319-100 constitute |

| • | A320-200 constitute |

| • | A330-200 constitute |

| • | A330-300 constitute |

| • | 737-300 constitute |

| • | 737-300QC constitute |

| • | 737-400 constitute |

| • | 737-500 constitute |

| • | 737-700 constitute |

| • | 737-800 constitute |

| • | 747-400PC constitute 2.1%; |

| • | 757-200 constitute 2.6%; |

| • | 767-200ER constitute |

| • | 767-300ER constitute |

Should any of these aircraft types (or other types we acquire in the future) or Airbus or Boeing encounter technical, financial or other difficulties, a diminution in value of such aircraft, an inability to lease the aircraft on favorable terms or at all, or a potential grounding of such aircraft could occur. As a result, the inability to lease the affected aircraft types maywould likely have an adverse effect on our financial results, to the extent the affected aircraft types comprise a significant percentage of our aircraft portfolio. The composition of our aircraft portfolio may therefore adversely affect our business and financial results. In addition, the abandonment or rejection of the lease of any of the aircraft listed above by one or more carriers in reorganization proceedings under Chapter 11 of the U.S. Bankruptcy Code or comparable statutes in non-U.S. jurisdictions may diminish the value of such aircraft and will subject us to re-leasing risks.

The advanced age of some of our aircraft may expose us to higher than anticipated maintenance related expenses, which could adversely affect our financial results and our ability to pursue additional acquisitions.

As of March 31,September 30, 2006, the average age of our aircraft portfolio calculated from the date of delivery by manufacturer, and weighted by net book value, was 8.78.6 years. In general, the costs of operating an aircraft, including maintenance expenditures, increase with the age of the aircraft. Also, older aircraft typically are less fuel-efficient than newer aircraft and may be more difficult to re-lease or sell. Variable expenses like fuel, crew size or aging aircraft corrosion control or modification programs and related airworthiness directives could make the operation of older aircraft less economically feasible and may result in increased lessee defaults. We may also incur some of these increased maintenance expenses and regulatory costs upon acquisition or releasing of our aircraft. Any of these expenses or costs will have a negative impact on our financial results and our ability to pursue additional acquisitions.

We operate in a highly competitive market for investment opportunities in aviation assets and for the leasing of aircraft.

A number of entities compete with us to make the types of investments that we plan to make. We compete with public partnerships, investors and funds, commercial and investment banks and commercial finance companies with respect to our investments in debt securities. We compete with other operating lessors, airlines, aircraft manufacturers, financial institutions (including those seeking to dispose of repossessed aircraft at distressed prices), aircraft brokers and other investors with respect to aircraft acquisitions and aircraft leasing. The aircraft leasing industry may be divided into two leasing segments: (i) leasing of new aircraft acquired directly or indirectly from manufacturers and (ii) leasing or re-leasing of aircraft in the secondary market. Currently, we compete primarily in the latter segment, and our competition is comprised of other aircraft leasing companies, including GE CapitalCommercial Aviation Services, International Lease Finance Corp., CIT Group, AerCap, Aviation Capital Group, Pegasus, GATX Air,Macquarie Aircraft Leasing, RBS Aviation Capital, AWAS, Babcock & Brown and Singapore Aircraft Leasing Enterprise.

Many of our competitors are substantially larger and have considerably greater financial, technical and marketing resources than we do. Some competitors may have a lower cost of funds and access to funding sources that are not available to us. In addition, some of our competitors may have higher risk tolerances or different risk assessments, which could allow them to consider a wider variety of investments, establish more relationships than us and bid more aggressively on aviation assets available for sale and offer lower lease rates than us. For instance, we may not be able to grant privileged rental rates to airlines in return for equity investments or debt financings in order to lease aircraft and minimize the number of aircraft on the groundoff lease (unless such equity investments or debt financings are in connection with the bankruptcy, reorganization or similar process of a lessee in settlement of expected or already delinquent obligations, as permitted under the terms of certain of our indebtedness). Certain of our competitors, however, may enter

into similar arrangements with troubled lessees to restructure the obligations of those lessees while maximizing the number of aircraft remaining on viable leases to such lessees and minimizing their overall cost. Such disparity could make our acquisitions more costly, impair our ability to effectively compete in the marketplace, maximize our revenues and grow our business. In addition, some competitors may provide financial services, maintenance services or other inducements to potential lessees that we cannot provide. As a result of competitive pressures, we may not be able to take advantage of attractive investment opportunities from time to time, and we may not be able to identify and make investments that are consistent with our investment objectives. Additionally, we may not be able to compete effectively against present and future competitors in the aircraft leasing market. The competitive pressures we face may have a material adverse effect on our business, financial condition and results of operations.

We may not realize gains or income from our debt investments.

We seek to generate both current income and capital appreciation.appreciation on our debt securities. The debt securities in which we invest may not appreciate in value, and, in fact, may decline in value and default on interest and/or principal payments. As of March 31,September 30, 2006, all of the obligors under our debt investments are U.S. airlines. During the past 15 years a number of North American passenger airlines, including US Airways, Inc, filed Chapter 11 bankruptcy proceedings and several major U.S. airlines ceased operations altogether.

As in Europe, North America has experienced the development of low-cost carriers and the resultant increased competition among such carriers and between such carriers and traditional carriers. This evolution in the North American airline industry may have a material adverse effect on the ability of North American lessees to meet their financial and other obligations under our leases. Accordingly, we may not be able to realize gains or income from our debt investments. Any gains that we do realize may not be sufficient to offset any other losses we experience. Any income that we realize may not be sufficient to offset our expenses.

Declines in the market values of our debt investments may adversely affect periodic reported results and credit availability, which may reduce earnings and, in turn, cash available for distribution to our shareholders.

Our debt investments are, and we believe are likely to continue to be, classified for accounting purposes as available for sale. Changes in the market values of those assets will be directly charged or credited to shareholders'shareholders’ equity. As a result, a decline in values may reduce the book value of our assets. Moreover, if the decline in value of an available for sale security is considered by our management to be other than temporary, such decline will reduce our earnings.

A decline in the market value of our debt investments may adversely affect us particularly in instances where we have borrowed money based on the market value of those debt investments. If the market value of those assets declines, the lender may require us to post additional collateral to support the loan. If we were unable to post the additional collateral, we would have to sell those assets or other assets at a time when we might not otherwise choose to do so. A reduction in available credit may reduce our earnings and, in turn, cash available for distribution to shareholders.

Market values of our debt investments may decline for a number of reasons, such as causes related to changes in prevailing market rates, increases in defaults, increases in voluntary prepayments for any debt investments that we have that are subject to prepayment risk, and widening of credit spreads.

Risks related to our leases

We generally will need to re-lease or sell aircraft as current leases expire to continue to generate sufficient funds to meet our debt obligations, to finance our growth and operations and to pay dividends on our common shares, and we may not be able to re-lease or sell such aircraft on favorable terms, or at all.

Our business strategy entails the need to re-lease aircraft as our current leases expire in order to continue to generate sufficient revenues to meet our debt obligations, to finance our growth and operations and to pay dividends on our common shares. In certain cases, including the Aircraft Acquisition, we may acquire aircraft that are not leased at the time. The ability to re-lease aircraft at attractive rates will depend on general market and competitive conditions.conditions at the particular time. If we are not able to re-lease an aircraft at favorable rates, including aircraft acquired pursuant to the Aircraft Acquisition, we may need to attempt to sell the aircraft to

provide adequate funds for debt payments and to otherwise finance our growth and operations. Further, our ability to re-lease, lease or sell aircraft on favorable terms or at all or without significant off-lease time is likely to be adversely impacted by risks affecting the airline industry.

A schedule of contractual lease expirations by year and aircraft type is presented in the table below. Leases subject to extension options are shown at the expiration of the current lease term. The table assumes that, except as indicated, no lease terminates prematurely, no substitute aircraft are delivered, no aircraft are sold and no additional aircraft are purchased.purchased, even though we acquired aircraft subsequent to September 30, 2006 and are currently committed to purchase additional aircraft as part of the Aircraft Acquisition. Contractual revenues represented by expiring leases totaled $2.6 millionlease revenue earned in 2006 $4.0 millionon leases expiring in the fourth quarter of 2006 totaled $1.3 million. Contractual lease revenues earned in 2006 on leases expiring in 2007 and $11.72008 totaled $16.4 million in 2008.and $29.7 million, respectively. More aircraft will need to be re-leased to the extent leases terminate prematurely.

Lease Expiration by Year, for aircraft we owned at March 31,September 30, 2006

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | |||||||||||||||||||||||||||||||||||||

| A310-300F | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||||||

| A319-100 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||||||

| A320-200 | 1 | 1 | 0 | 2 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 3 | 2 | 2 | 0 | 3 | 0 | 0 | ||||||||||||||||||||||||||||||||||||

| A330-200 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||||||

| A330-300 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 4 | 0 | 0 | ||||||||||||||||||||||||||||||||||||

| 737-300 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||||||

| 737-300QC | 0 | 0 | 1 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||||||

| 737-400 | 0 | 2 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 | 2 | 1 | 0 | 1 | 0 | 0 | ||||||||||||||||||||||||||||||||||||

| 737-500 | 0 | 0 | 0 | 1 | 3 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 3 | 0 | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||||||

| 737-700 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 7 | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||||||

| 737-800 | 0 | 1 | 0 | 0 | 0 | 2 | 0 | 0 | 2 | 0 | 1 | 1 | 0 | 0 | 2 | 0 | 0 | 2 | ||||||||||||||||||||||||||||||||||||

| 747-400PC | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||||||

| 757-200 | 0 | 3 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||||||||||||||||

| 767-200ER | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||||||

| 767-300ER | 0 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 1 | 1 | 0 | 1 | 0 | ||||||||||||||||||||||||||||||||||||

| Total | 2 | 6 | 9 | 10 | 5 | 3 | 5 | 0 | 2 | 1 | 9 | 14 | 10 | 9 | 11 | 8 | 1 | 2 | ||||||||||||||||||||||||||||||||||||

If lessees are unable to fund their maintenance requirements on our aircraft, our cash flow and our ability to meet our debt obligations or to pay dividends on our common shares could be adversely affected.

The standards of maintenance observed by the various lessees and the condition of the aircraft at the time of sale or lease may affect the future values and rental rates for our aircraft.

Under our leases, the relevant lessee is primarilygenerally responsible for maintaining the aircraft and complying with all governmental requirements applicable to the lessee and the aircraft,

including, without limitation, operational, maintenance, and registration requirements and airworthiness directives (although in certain cases we have agreed to share the cost of complying with certain airworthiness directives). Failure of a lessee to perform required maintenance with respect to an aircraft during the term of a lease could result in a diminution in value of such aircraft, an inability to lease the aircraft at favorable rates or at all, or a potential grounding of such aircraft, and will likely require us to incur maintenance and modification costs upon the expiration or earlier termination of the applicable lease, which could be substantial, to restore such aircraft to an acceptable condition prior to sale or re-leasing.

As of March 31,September 30, 2006, 2537 of our leases provide that the lessee is required to make periodic payments to us during the lease term in order to provide cash reserves for the payment of

maintenance tied to the usage of the aircraft. In these leases there is an associated liability for us to reimburse the lessee for such scheduled maintenance performed on the related aircraft, based on formulas tied to the extent of any of the lessee’s maintenance reserve payments. In some cases, we are obligated and in the future may incur additional obligations pursuant to the terms of the leases to contribute to the cost of maintenance work performed by the lessee in addition to maintenance reserve payments.

Our operational cash flow and available liquidity may not be sufficient to fund our maintenance requirements, particularly as our aircraft age. Actual rental and maintenance payments by lessees and other cash that we receive may be significantly less than projected as a result of numerous factors, including defaults by lessees and our potential inability to obtain satisfactory maintenance terms in leases. SeventeenAt September 30, 2006, 26 of our leases at March 31, 2006 do not provide for any periodic maintenance reserve payments to be made by lessees to us in respect of their maintenance obligations, and it is possible that future leases will not contain such requirements. Maintenance reservesTwo of our leases require that the lessee make both a monthly maintenance payment and an additional maintenance payment to us at the end of the lease term in certain circumstances. Even if we are entitled to maintenance reserve payments, they may not cover the entire expense of the scheduled maintenance they are intended to fund. In addition, maintenance reserves typically cover only certain scheduled maintenance requirements and do not cover all required maintenance and all scheduled maintenance. Furthermore, lessees may not meet their obligations to pay maintenance reserves or perform required scheduled maintenance. Any significant variations in such factors may materially adversely affect our business and particularly our cash position, which would make it difficult for us to meet our debt obligations or to pay dividends on our common shares.

Failure to pay certain potential additional operating costs could result in the grounding or arrest of our aircraft and prevent the re-lease, sale or other use of our aircraft, which would negatively affect our financial condition and results of operations.

As in the case of maintenance costs, we may incur other operational costs upon a lessee default or where the terms of the lease require us to pay a portion of those costs. Such costs include:

| • | the costs of casualty, liability and political risk insurance and the liability costs or losses when insurance coverage has not been or cannot be obtained as required or is insufficient in amount or scope; |

| • | the costs of licensing, exporting or importing an aircraft, airport taxes, customs duties, air navigation charges, landing fees and similar governmental or quasi-governmental impositions, which can be substantial; and |

| • | penalties and costs associated with the failure of lessees to keep the aircraft registered under all appropriate local requirements or obtain required governmental licenses, consents and approvals. |

The failure to pay certain of these costs can result in liens on the aircraft and the failure to register the aircraft can result in a loss of insurance. These matters could result in the grounding

or arrest of the aircraft and prevent the re-lease, sale or other use of the aircraft until the problem is cured, which would negatively affect our financial condition and results of operations.

Our lessees may have inadequate insurance coverage or fail to fulfill their respective indemnity obligations, which could result in us not being covered for claims asserted against us and may negatively affect our business, financial condition and results of operations.

While we do not directly control the operation of any of our aircraft, by virtue of holding title to the aircraft (directly or through a securitization related special purpose entity), in certain

jurisdictions around the world, aircraft lessors are held strictly liable for losses resulting from the operation of aircraft or may be held liable for those losses on other legal theories.