Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on July 23,August 27, 2010

Registration No. 333-166550

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 34

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Rhino Resource Partners LP

(Exact Name of Registrant as Specified in Its Charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) | 1221 (Primary Standard Industrial Classification Code Number) | 27-2377517 (I.R.S. Employer Identification Number) |

424 Lewis Hargett Circle, Suite 250

Lexington, Kentucky 40503

(859) 389-6500

(Address, Including Zip Code, and Telephone Number, Including

Area Code, of Registrant's Principal Executive Offices)

David G. Zatezalo

424 Lewis Hargett Circle, Suite 250

Lexington, Kentucky 40503

(859) 389-6500

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

| Copies to: | ||

Mike Rosenwasser Brenda K. Lenahan Vinson & Elkins L.L.P. 666 Fifth Avenue, 26th Floor New York, New York 10103 Tel: (212) 237-0000 Fax: (212) 237-0100 | Charles E. Carpenter Sean T. Wheeler Latham & Watkins LLP 885 Third Avenue New York, New York 10022 Tel: (212) 906-1200 Fax: (212) 751-4864 | |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) | Smaller reporting company o |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission becomes effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, Dated July 23,August 27, 2010

PROSPECTUS

3,750,0003,244,000 Common Units

Representing Limited Partner Interests

This is our initial public offering. We are offering 3,750,0003,244,000 common units. We have been approved to list our common units on the New York Stock Exchange under the symbol "RNO."

Prior to this offering, there has been no public market for our common units. We anticipate that the initial public offering price will be between $19.00 and $21.00 per common unit.

You should consider the risks which we have described in "Risk Factors" beginning on page 23 before buying our common units.

These risks include the following:

In order to comply with certain U.S. laws relating to the ownership of interests in mineral leases on federal lands, we require an owner of our units to be an "eligible citizen." If you are not an eligible citizen, your common units will be subject to redemption. Please read "The Partnership Agreement—Ineligible Citizens; Redemption."

| | Per Common Unit | Total | |||||

|---|---|---|---|---|---|---|---|

Public offering price | $ | $ | |||||

Underwriting discount | $ | $ | |||||

Proceeds, before offering expenses, to us | $ | $ | |||||

The underwriters may purchase up to an additional 562,500486,600 common units from us at the public offering price, less the underwriting discount, within 30 days from the date of this prospectus to cover over-allotments.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the common units to purchasers on or about , 2010.

RAYMOND JAMES

RBC CAPITAL MARKETS

STIFEL NICOLAUS WEISEL

The date of this prospectus is , 2010.

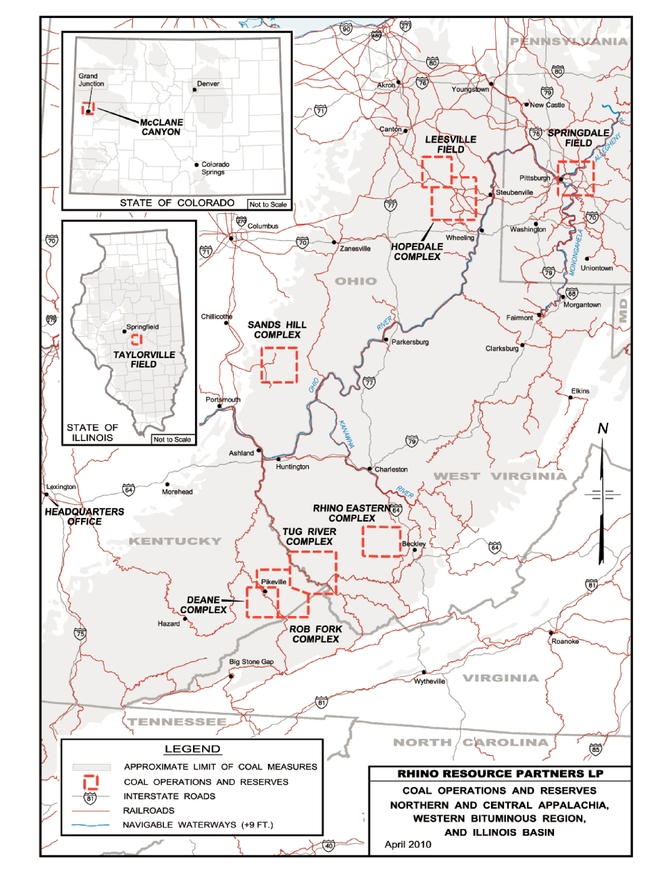

The map above does not reflect our acquisition in August 2010 of certain mining assets located in Emery and Carbon Counties, Utah.

Summary | 1 | |

Risk Factors | 23 | |

Use of Proceeds | ||

Capitalization | ||

Dilution | ||

Cash Distribution Policy and Restrictions on Distributions | ||

Provisions of Our Partnership Agreement Relating to Cash Distributions | 77 | |

Selected Historical Consolidated and Pro Forma Condensed Consolidated Financial and Operating Data | 94 | |

Management's Discussion and Analysis of Financial Condition and Results of Operations | 98 | |

The Coal Industry | ||

Business | ||

Management | ||

Executive Officer Compensation | 194 | |

Security Ownership of Certain Beneficial Owners and Management | 210 | |

Certain Relationships and Related Party Transactions | 211 | |

Conflicts of Interest and Fiduciary Duties | 214 | |

Description of the Common Units | 224 | |

The Partnership Agreement | 227 | |

Units Eligible for Future Sale | 244 | |

Material Tax Consequences | 246 | |

Investment in Rhino Resource Partners LP by Employee Benefit Plans | 269 | |

Underwriting | 271 | |

Validity of Our Common Units | 276 | |

Experts | 276 | |

Where You Can Find More Information | 277 | |

Forward-Looking Statements | 277 | |

Index to Financial Statements | F-1 | |

Appendix A—Form of First Amended and Restated Agreement of Limited Partnership of Rhino Resource Partners LP | A-1 | |

Appendix B—Application for Transfer of Common Units | B-1 | |

Appendix C—Glossary of Terms | C-1 |

You should rely only on the information contained in this prospectus, any free writing prospectus prepared by or on behalf of us or any other information to which we have referred you in connection with this offering. We have not, and the underwriters have not, authorized any other person to provide you with information different from that contained in this prospectus. Neither the delivery of this prospectus nor sale of our common units means that information contained in this prospectus is correct after the date of this prospectus. This

i

prospectus is not an offer to sell or solicitation of an offer to buy our common units in any circumstances under which the offer or solicitation is unlawful.

Until , 2010 (25 days after the date of this prospectus), all dealers that buy, sell or trade our common units, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers' obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

ii

This summary highlights information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including the historical and pro forma consolidated financial statements and the notes to those financial statements, before investing in our common units. The information presented in this prospectus assumes that the underwriters' option to purchase additional common units is not exercised unless otherwise noted. You should read "Risk Factors" beginning on page 23 for information about important risks that you should consider before buying our common units.

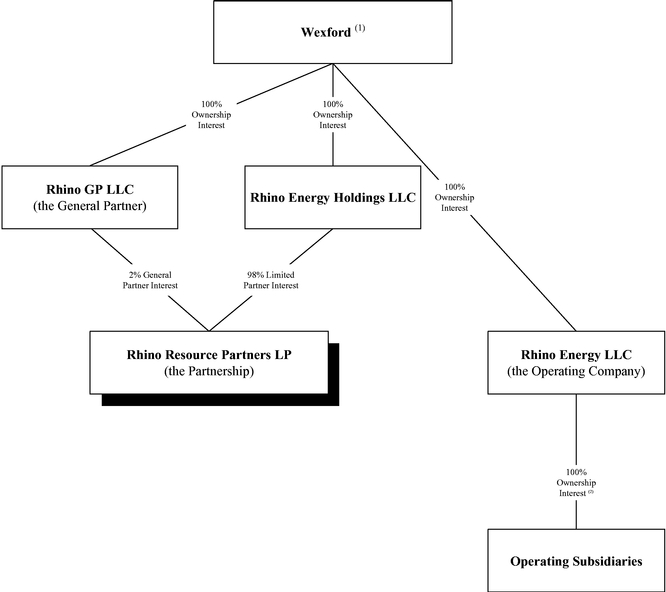

References in this prospectus to "Rhino Resource Partners LP," "we," "our," "us" or like terms when used in a historical context refer to the business of our predecessor, Rhino Energy LLC and its subsidiaries, that is being contributed to Rhino Resource Partners LP in connection with this offering, except that, unless otherwise specified, references to our proven and probable reserves, non-reserve coal deposits and coal production do not include the reserves and deposits owned by or the production of Rhino Eastern LLC, a joint venture in which we have a 51% membership interest and for which we serve as manager. When used in the present tense or prospectively, those terms refer to Rhino Resource Partners LP and its subsidiaries. References in this prospectus to "Wexford" refer to Wexford Capital LP, our sponsor, and its affiliates and principals. We include a glossary of some of the terms used in this prospectus as Appendix C.

Rhino Resource Partners LP

We are a growth-oriented Delaware limited partnership formed to control and operate coal properties and related assets. We produce, process and sell high quality coal of various steam and metallurgical grades. We market our steam coal primarily to electric utility companies as fuel for their steam-powered generators. Customers for our metallurgical coal are primarily steel and coke producers who use our coal to produce coke, which is used as a raw material in the steel manufacturing process.

Our primary business objective is to make quarterly cash distributions to our unitholders at our minimum quarterly distribution and, over time, increase our quarterly cash distributions. Initially, we will pay our common unitholders distributions of $0.445 per common unit per quarter, or $1.78 per common unit annually, to the extent we have sufficient cash from our operations after establishment of cash reserves and payment of fees and expenses, including payments to our general partner and its affiliates, before we pay any distributions to our subordinated unitholders.

For the year ended December 31, 2009, we generated revenues of approximately $419.8 million and net income of approximately $19.5 million. For the threesix months ended March 31,June 30, 2010, we generated revenues of approximately $66.6$145.0 million and net income of approximately $6.5$13.7 million. As of July 13,August 23, 2010, we had sales commitments for approximately 99%97% and 80%69% of our estimated coal production (including purchased coal to supplement production and excluding results from the joint venture) for the year ending December 31, 2010 and the twelve months ending JuneSeptember 30, 2011, respectively.

We have a geographically diverse asset base with coal reserves located in Central Appalachia, Northern Appalachia, the Illinois Basin and the Western Bituminous region. As of March 31, 2010, we controlled an estimated 285.4 million tons of proven and probable coal reserves, consisting of an estimated 272.9 million tons of steam coal and an estimated 12.5 million tons of metallurgical coal. In addition, as of March 31, 2010, we controlled an estimated 122.2 million tons of non-reserve coal deposits. As of March 31, 2010, Rhino Eastern LLC, a joint venture in which we have a 51% membership interest and for which we serve as manager, controlled an estimated 22.4 million tons of proven and probable coal reserves at the Rhino Eastern mining complex located in Central Appalachia, consisting entirely of premium mid-vol and low-vol metallurgical coal, and an estimated 34.3 million tons of non-reserve coal deposits. Our and the joint venture's proven and probable coal reserves and non-reserve coal deposits were the same in all material respects as of December 31, 2009. We currently operate twelveeleven mines, including sevensix underground and five surface mines, located in Kentucky, Ohio, Colorado and West Virginia. In addition, our joint venture currently operates one underground mine in West Virginia. The number of mines that we operate may vary from time to time depending on a number of factors, including the existing demand for and price of coal, depletion of economically recoverable reserves and availability of experienced labor. Excluding results from the joint venture, for the year ended December 31, 2009, we produced approximately 4.7 million tons of coal, purchased approximately 2.0 million tons of coal and sold approximately 6.7 million tons of coal, approximately 99% of which were pursuant to supply contracts. Excluding results from the joint venture, for the threesix months ended March 31,June 30, 2010, we produced approximately 1.02.1 million tons of coal and sold approximately 0.92.0 million tons of coal, approximately 99%97% of which were pursuant to supply contracts. Additionally, the joint venture produced and sold approximately 0.2 million tons and approximately 0.1 million tons of premium mid-vol metallurgical coal for the year ended December 31, 2009 and the threesix months ended March 31,June 30, 2010, respectively.

Since our predecessor's formation in 2003, we have significantly grown our coal reserves. Since April 2003, we have completed numerous coal asset acquisitions with a total purchase price of approximately $208.3 million. Through these acquisitions and coal lease transactions, we have substantially increased$223.3 million, including our proven and probable coal reserves and non-reserve coal deposits. We expect to complete the acquisition in August 2010 of certain mining assets of C.W. Mining Company out of bankruptcy for approximately $15.0 million.bankruptcy. The assets to be acquired are located in Emery and Carbon Counties, Utah and include coal reserves and non-reserve coal deposits, underground mining equipment and infrastructure, an overland belt conveyor system, a loading facility and support facilities. We intend to fund the asset acquisition with borrowings underThrough these acquisitions and coal lease transactions, we have substantially increased our credit agreement.proven and probable coal reserves and non-reserve coal deposits.

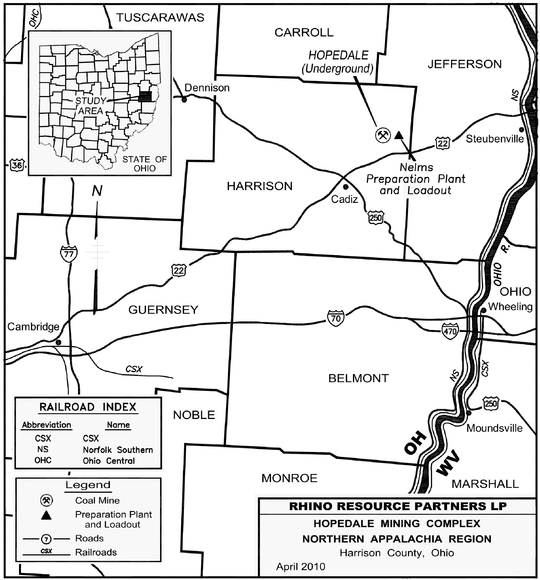

In addition, we have successfully grown our production through internal development projects. Between 2004 and 2006, we invested approximately $19.0 million in the Hopedale mine located in Northern Appalachia to develop the estimated 18.5 million tons of proven and probable coal reserves at the mine. The Hopedale mine produced approximately 1.5 million tons of coal for the year ended December 31, 2009 and approximately 0.30.7 million tons of coal for the threesix months ended March 31,June 30, 2010. In 2007, we completed initial development of Mine 28, a new underground high-vol metallurgical coal mine at the Rob Fork mining complex located in Central Appalachia. We finished additional development work on Mine 28 in 2009, which completes all major foreseen development projects for the life of these reserves. Mine 28 produced approximately 0.4 million tons of metallurgical coal for the year ended December 31, 2009 and approximately 0.10.2 million tons of metallurgical coal for the threesix months ended March 31,June 30, 2010. As of March 31, 2010, we also controlled or managed a significant amount of

undeveloped proven and probable coal reserves. These reserves can be developed and produced over time as

industry and regional conditions permit. We believe our existing asset base will continue to provide attractive internal growth projects.

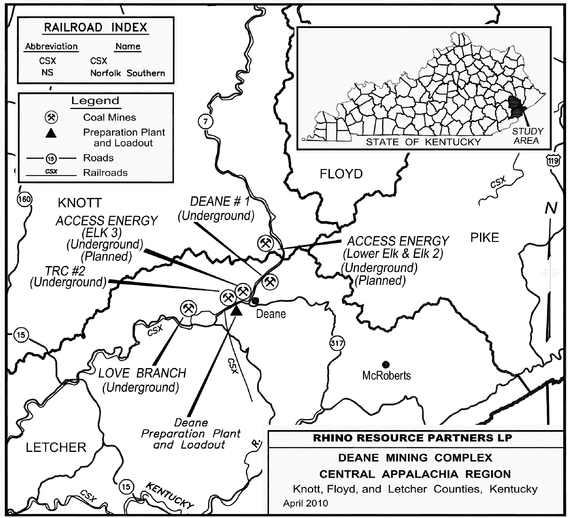

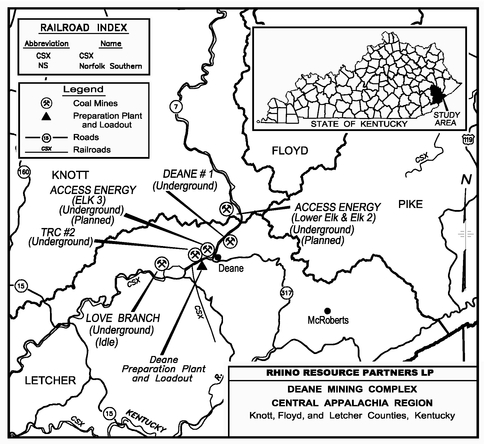

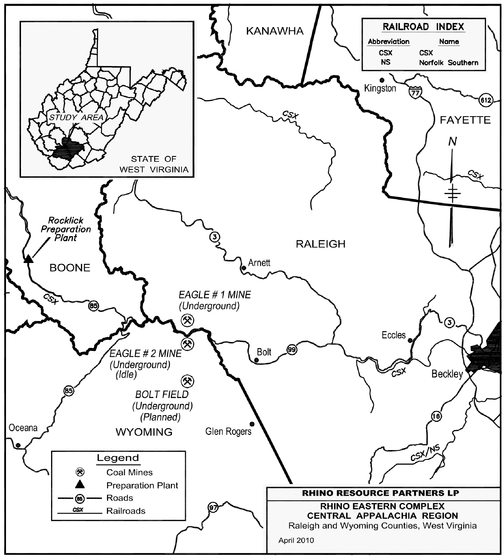

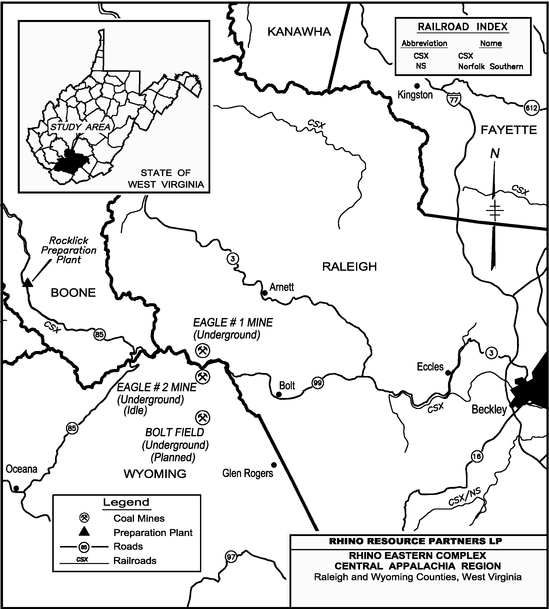

The following table summarizes our and the joint venture's mining complexes, production and reserves by region:

| | | | Production for the (2) | Proven and Probable Reserves as of March 31, 2010 (3) | | | Production for the (2) | Proven and Probable Reserves as of March 31, 2010 (3) | ||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | Type of Production (1) | Year Ended December 31, 2009 | Three Months Ended March 31, 2010 | | Type of Production (1) | Year Ended December 31, 2009 | Six Months Ended June 30, 2010 | ||||||||||||||||||||||||||||||

| Region | Region | Total | Steam | Metallurgical | Region | Total | Steam | Metallurgical | ||||||||||||||||||||||||||||||

| | | | (in million tons) | | | (in million tons) | ||||||||||||||||||||||||||||||||

Central Appalachia | Central Appalachia | Central Appalachia | ||||||||||||||||||||||||||||||||||||

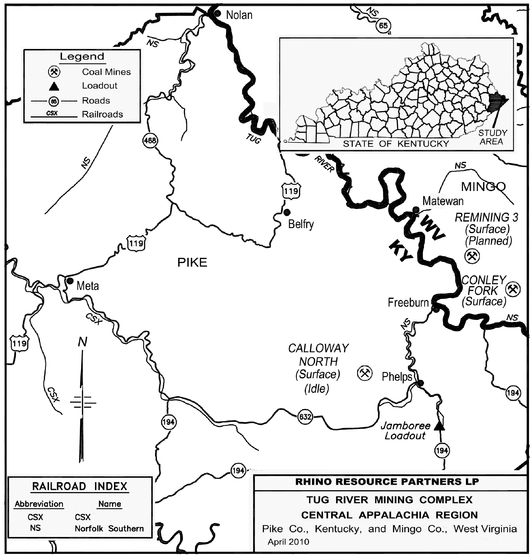

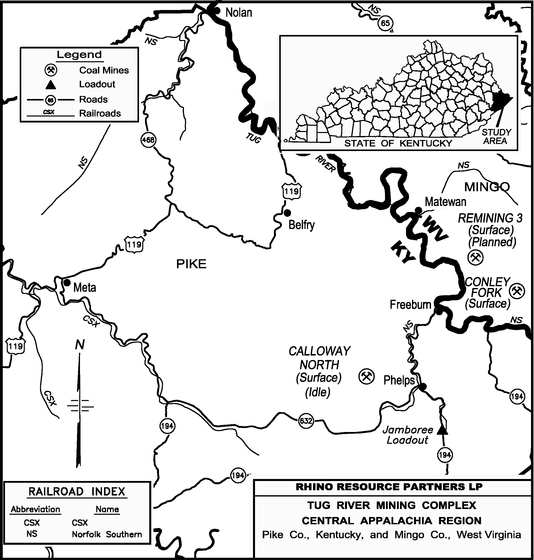

Tug River Complex (KY, WV) | Tug River Complex (KY, WV) | U, S | 0.5 | 0.1 | 34.8 | 28.8 | 6.0 | Tug River Complex (KY, WV) | U, S | 0.5 | 0.2 | 34.8 | 28.8 | 6.0 | ||||||||||||||||||||||||

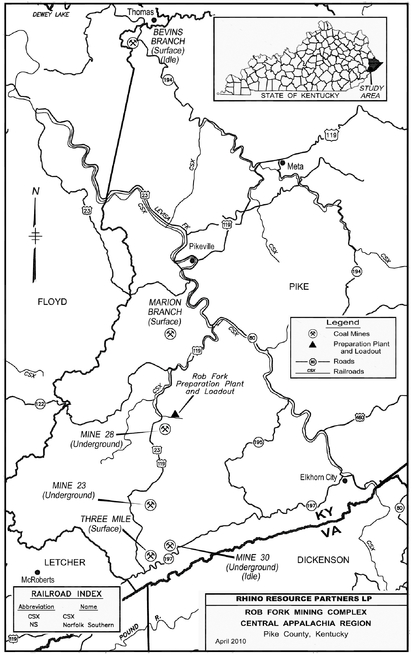

Rob Fork Complex (KY) | Rob Fork Complex (KY) | U, S | 1.2 | 0.3 | 26.2 | 19.7 | 6.5 | Rob Fork Complex (KY) | U, S | 1.2 | 0.5 | 26.2 | 19.7 | 6.5 | ||||||||||||||||||||||||

Deane Complex (KY) | Deane Complex (KY) | U | 0.6 | 0.1 | 40.8 | 40.8 | — | Deane Complex (KY) | U | 0.6 | 0.2 | 40.8 | 40.8 | — | ||||||||||||||||||||||||

Northern Appalachia | Northern Appalachia | Northern Appalachia | ||||||||||||||||||||||||||||||||||||

Hopedale Complex (OH) | Hopedale Complex (OH) | U | 1.5 | 0.3 | 18.5 | 18.5 | — | Hopedale Complex (OH) | U | 1.5 | 0.7 | 18.5 | 18.5 | — | ||||||||||||||||||||||||

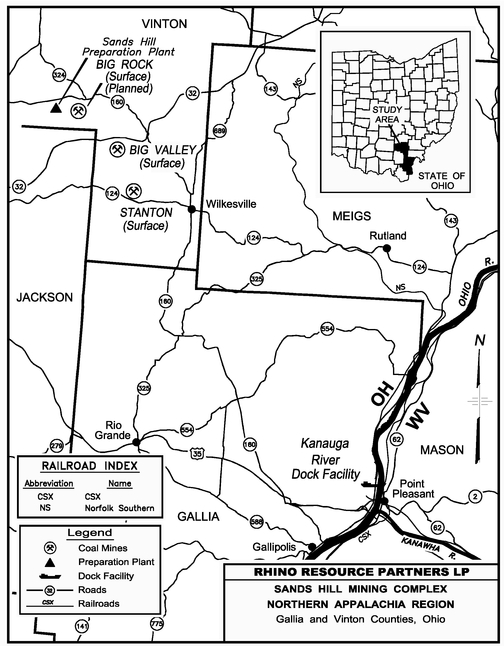

Sands Hill Complex (OH) | Sands Hill Complex (OH) | S | 0.7 | 0.2 | 8.6 | 8.6 | — | Sands Hill Complex (OH) | S | 0.7 | 0.3 | 8.6 | 8.6 | — | ||||||||||||||||||||||||

Leesville Field (OH) | Leesville Field (OH) | U | — | — | 26.8 | 26.8 | — | Leesville Field (OH) | U | — | — | 26.8 | 26.8 | — | ||||||||||||||||||||||||

Springdale Field (PA) | Springdale Field (PA) | U | — | — | 13.8 | 13.8 | — | Springdale Field (PA) | U | — | — | 13.8 | 13.8 | — | ||||||||||||||||||||||||

Illinois Basin | Illinois Basin | Illinois Basin | ||||||||||||||||||||||||||||||||||||

Taylorville Field (IL) | Taylorville Field (IL) | U | — | — | 109.5 | 109.5 | — | Taylorville Field (IL) | U | — | — | 109.5 | 109.5 | — | ||||||||||||||||||||||||

Western Bituminous | Western Bituminous | Western Bituminous | ||||||||||||||||||||||||||||||||||||

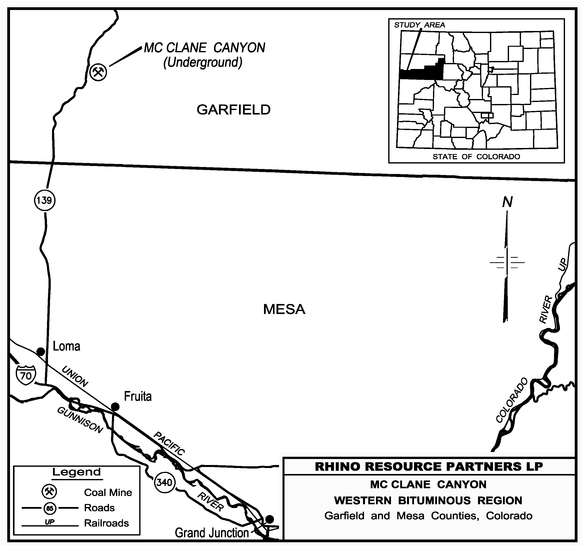

McClane Canyon Mine (CO) | McClane Canyon Mine (CO) | U | 0.3 | 0.1 | 6.4 | 6.4 | — | McClane Canyon Mine (CO) | U | 0.3 | 0.1 | 6.4 | 6.4 | — | ||||||||||||||||||||||||

Total | 4.7 | 1.0 | 285.4 | 272.9 | 12.5 | Total | 4.7 | 2.1 | 285.4 | 272.9 | 12.5 | |||||||||||||||||||||||||||

Central Appalachia | Central Appalachia | Central Appalachia | ||||||||||||||||||||||||||||||||||||

Rhino Eastern Complex (WV) (4) | Rhino Eastern Complex (WV) (4) | U | 0.2 | 0.1 | 22.4 | — | 22.4 | Rhino Eastern Complex (WV) (4) | U | 0.2 | 0.1 | 22.4 | — | 22.4 | ||||||||||||||||||||||||

Our principal business strategy is to safely, efficiently and profitably produce and sell both steam and metallurgical coal from our diverse asset base in order to maintain and, over time, increase our quarterly cash distributions. Our plan for executing this strategy includes the following key components:

We believe the following competitive strengths will enable us to successfully execute our business strategy:

For a more detailed description of our business strategies and competitive strengths, please read "Business—Our Business Strategy" and "—Our Competitive Strengths."

Our consolidated financial statements forcovering the three monthsone month ended and six months ended June 30,July 31, 2010 are not prepared yet.yet prepared. Our expectations with respect to our results for the periods discussed belowthat period are based upon management estimates. Our actual results may differ from these estimates.

We expect to reportgenerate total revenues and net income for the threeone month ended July 31, 2010 that are similar to our average monthly total revenues and net income during the six months ended June 30, 2010 that were slightly higher than for the three months ended March 31, 2010, due to slight increases in total coal sales volumes and coal prices. We expect that our costs of operations have increased slightly as a result of an increase in purchased coal costs, which we incurred in order to2010.

supplement production while transitioning underground operations in Central Appalachia to better enable us to take advantage of favorable pricing for metallurgical coal. Nonetheless, we expect that our increased revenues will offset our increased costs, resulting in greater net income for three months ended June 30, 2010 than for the three months ended March 31, 2010.

Risk Factors

An investment in our common units involves risks. You should carefully consider the following risk factors, those other risks described in "Risk Factors" and the other information in this prospectus, before deciding whether to invest in our common units. The following risks are discussed in more detail in "Risk Factors" beginning on page 23.

We are managed and operated by the board of directors and executive officers of our general partner, Rhino GP LLC. Following this offering, approximately 69.8%73.8% of our outstanding common units and all of our outstanding subordinated units and incentive distribution rights will be owned by Wexford. As a result of owning our general partner, Wexford will have the right to appoint all members of the board of directors of our general partner, including the independent directors. Our unitholders will not be entitled to elect our general partner or its directors or otherwise directly participate in our management or operation. For more information about the executive officers and directors of our general partner, please read "Management."

Following the consummation of this offering, neither our general partner nor Wexford will receive any management fee or other compensation in connection with our general partner's management of our business, but webusiness. Our general partner, however, may receive incentive fees resulting from holding the incentive distribution rights. Please see "Provisions of our Partnership Agreement Relating to Cash Distributions—Distributions of Available Cash—General Partner Interest and Incentive Distribution Rights." We will reimburse our general partner and its affiliates, including Wexford, for all expenses they incur and payments they make on our behalf. Our partnership agreement does not set a limit on the amount of expenses for which our general partner and its affiliates may be reimbursed. These expenses include salary, bonus, incentive compensation and other amounts paid to persons who perform services for us or on our behalf and expenses allocated to our general partner by its affiliates. Our partnership agreement provides that our general partner will determine in good faith the expenses that are allocable to us.

In order to maximize operational flexibility, our operations will be conducted through, and our operating assets will be owned by, our wholly owned subsidiary, Rhino Energy LLC, and its subsidiaries. Rhino Resource Partners LP does not have any employees. All of the employees that conduct our business are employed by our general partner or our subsidiaries.

Wexford Capital LP, or Wexford Capital, is a Securities and Exchange Commission, or SEC, registered investment advisor. Wexford Capital, which was formed in 1994, manages a series of investment funds and has over $6.0 billion of assets under management.

Conflicts of Interest and Fiduciary Duties

Our general partner has a legal duty to manage us in a manner beneficial to holders of our common and subordinated units. This legal duty is commonly referred to as a "fiduciary duty." However, the officers and directors of our general partner also have fiduciary duties to manage our general partner in a manner beneficial to Wexford. As a result, conflicts of interest may arise in the future between us and our unitholders, on the one hand, and Wexford and our general partner, on the other hand.

Delaware law provides that Delaware limited partnerships may, in their partnership agreements, restrict or expand the fiduciary duties owed by the general partner to limited partners and the partnership. Our partnership agreement limits the liability of, and reduces the fiduciary duties owed by, our general partner to our common unitholders. Our partnership agreement also restricts the remedies available to our unitholders for actions that might otherwise constitute a breach of fiduciary duty by our general partner. By purchasing a common unit, a unitholder is treated as having consented to various actions and potential conflicts of interest contemplated in the partnership agreement that might otherwise be considered a breach of fiduciary or other duties under applicable state law.

For a more detailed description of the conflicts of interest and the fiduciary duties of our general partner, please read "Conflicts of Interest and Fiduciary Duties." For a description of other relationships with our affiliates, please read "Certain Relationships and Related Party Transactions."

Our principal executive offices are located at 424 Lewis Hargett Circle, Suite 250, Lexington, Kentucky. Our phone number is (859) 389-6500. Our website address will behttp://rhinolp.com. We intend to make our periodic reports and other information filed with or furnished to the SEC available, free of charge, through our website, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference into this prospectus and does not constitute a part of this prospectus.

We are a Delaware limited partnership formed in April 2010 by Wexford to own and operate the business that has historically been conducted by Rhino Energy LLC.

In connection with the closing of this offering, the following will occur:

562,500486,600 common units to Rhino Energy Holdings LLC at the expiration of the option. If the underwriters exercise their option to purchase up to 562,500486,600 additional common units, the number of common units purchased by the underwriters pursuant to such exercise will be sold to the public instead of being issued to Rhino Energy Holdings LLC. The net proceeds from any exercise of the underwriters' option to purchase additional common units (approximately $10.5$9.1 million based on an assumed initial offering price of $20.00 per common unit, if exercised in full, after deducting the estimated underwriting discount and offering expenses payable by us) will be used to reimburse Rhino Energy Holdings LLC for capital expenditures it incurred with respect to the assets contributed to us.

The following is a simplified diagram of our ownership structure before this offering.

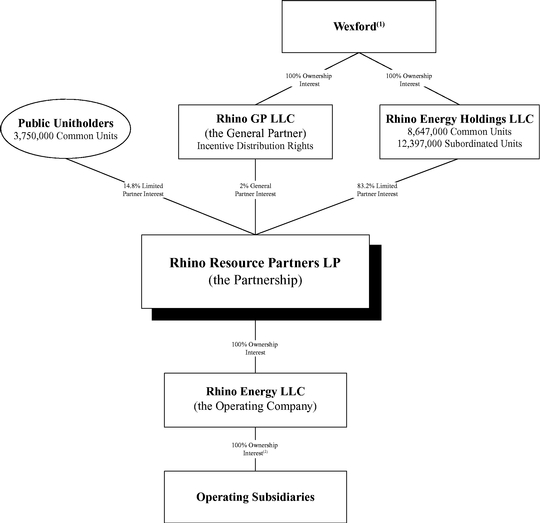

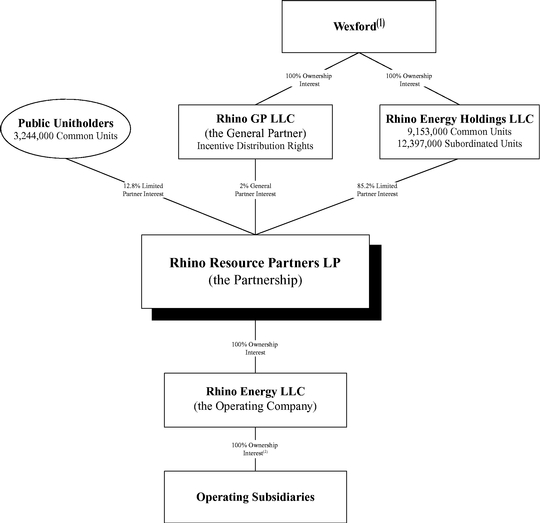

The following is a simplified diagram of our ownership structure after giving effect to this offering and the related transactions.

Public Common Units | % | ||||

Interests of Wexford: | |||||

Common Units | % | ||||

Subordinated Units | 49.0 | % | |||

General Partner Interest | 2.0 | % | |||

| 100.0 | % | ||||

The Offering

| Common units offered to the public | ||

Units outstanding after this offering | 12,397,000 common units and 12,397,000 subordinated units, each representing a 49.0% limited partner interest in us. If the underwriters do not exercise their option to purchase additional common units, we will issue | |

Use of proceeds | We intend to use the estimated net proceeds of approximately | |

The net proceeds from any exercise of the underwriters' option to purchase additional common units (approximately | ||

Please read "Use of Proceeds." |

| Cash distributions | We will make a minimum quarterly distribution of $0.445 per common unit (or $1.78 per common unit on an annualized basis) to the extent we have sufficient cash from operations after establishment of cash reserves and payment of costs and expenses, including reimbursement of expenses to our general partner and its affiliates. These expenses include salary, bonus, incentive compensation and other amounts paid to persons who perform services for us or on our behalf and expenses allocated to our general partner by its affiliates. Our partnership agreement does not set a limit on the amount of cash reserves that our general partner may establish or the amount of expenses for which our general partner and its affiliates may be reimbursed. Our ability to pay cash distributions at the minimum quarterly distribution rate is subject to various restrictions and other factors described in more detail under "Cash Distribution Policy and Restrictions on Distributions." | |

For the first quarter that we are publicly traded, we will pay investors in this offering a prorated distribution covering the period from the completion of this offering through September 30, 2010, based on the actual length of that period. | ||

Our partnership agreement requires us to distribute all of our available cash each quarter in the following manner: | ||

• first, 98.0% to the holders of common units and 2.0% to our general partner, until each common unit has received the minimum quarterly distribution of $0.445 plus any arrearages from prior quarters; | ||

• second, 98.0% to the holders of subordinated units and 2.0% to our general partner, until each subordinated unit has received the minimum quarterly distribution of $0.445; and | ||

• third, 98.0% to all unitholders, pro rata, and 2.0% to our general partner, until each unit has received a distribution of $0.51175. | ||

If cash distributions to our unitholders exceed $0.51175 per unit in any quarter, our unitholders and our general partner will receive distributions according to the following percentage allocations: |

| | Marginal Percentage Interest in Distributions | |||||||

|---|---|---|---|---|---|---|---|---|

| Total Quarterly Distribution | | General Partner | ||||||

| Target Amount | Unitholders | |||||||

above $0.51175 up to $0.55625 | 85.0 | % | 15.0 | % | ||||

above $0.55625 up to $0.6675 | 75.0 | % | 25.0 | % | ||||

above $0.6675 | 50.0 | % | 50.0 | % | ||||

| The percentage interests shown for our general partner include its 2.0% general partner interest. We refer to the additional increasing distributions to our general partner as "incentive distributions." We view these distributions as an incentive fee providing our general partner with a direct financial incentive to expand the profitability of our business to enable us to increase distributions to our limited partners. Please read "Provisions of Our Partnership Agreement Relating to Cash Distributions—Distributions of Available Cash—General Partner Interest and Incentive Distribution Rights." | ||

Pro forma cash available for distribution generated during the year ended December 31, 2009 and the twelve months ended | ||

We believe, based on our financial forecast and related assumptions included in "Cash Distribution Policy and Restrictions on Distributions—Pro Forma and Forecasted Results of Operations and Cash Available for Distribution," that we will have sufficient available cash to pay the minimum quarterly distribution of $0.445 on all of our units and the corresponding distribution on our general partner's 2.0% interest for each quarter in the twelve months ending |

| Subordinated units | Wexford will initially own all of our subordinated units. The principal difference between our common and subordinated units is that in any quarter during the subordination period, the subordinated units will not be entitled to receive any distribution until the common units have received the minimum quarterly distribution plus any arrearages in the payment of the minimum quarterly distribution from prior quarters. Subordinated units will not accrue arrearages. | |

Conversion of subordinated units | The subordination period will end on the first business day after we have earned and paid at least (1) $1.78 (the minimum quarterly distribution on an annualized basis) on each outstanding unit and the corresponding distribution on our general partner's 2.0% interest for each of three consecutive, non-overlapping four quarter periods ending on or after | |

The subordination period also will end upon the removal of our general partner other than for cause if no subordinated units or common units held by the holders of subordinated units or their affiliates are voted in favor of that removal. | ||

When the subordination period ends, all subordinated units will convert into common units on a one-for-one basis, and all common units thereafter will no longer be entitled to arrearages. Please read "Provisions of Our Partnership Agreement Relating to Cash Distributions—Subordination Period." | ||

Ineligible citizens and redemption | Only eligible citizens (meaning a person or entity qualified to hold an interest in mineral leases on federal lands) will be entitled to receive distributions or be allocated income or loss from us. If a transferee or a unitholder, as the case may be, does not properly complete the transfer application or any required recertification, for any reason, the transferee or unitholder will have no right to vote its units on any matter and we have the right to redeem such units at a price which is equal to the lower of the transferee's or unitholder's purchase price or the then-current market price of such units. The redemption price will be paid in cash or by delivery of a promissory note, as determined by our general partner. Please read "Description of the Common Units—Transfer of Common Units" and "The Partnership Agreement—Ineligible Citizens; Redemption." |

| General partner's right to reset the target distribution levels | Our general partner, as the initial holder of our incentive distribution rights, has the right, at any time when there are no subordinated units outstanding and it has received incentive distributions at the highest level to which it is entitled (48.0%, in addition to distributions paid on its 2.0% general partner interest) for each of the prior four consecutive fiscal quarters, to reset the initial target distribution levels at higher levels based on our cash distributions at the time of the exercise of the reset election. If our general partner transfers all or a portion of our incentive distribution rights in the future, then the holder or holders of a majority of our incentive distribution rights will be entitled to exercise this right. The following assumes that our general partner holds all of the incentive distribution rights at the time that a reset election is made. Following a reset election, the minimum quarterly distribution will be adjusted to equal the reset minimum quarterly distribution, and the target distribution levels will be reset to correspondingly higher levels based on the same percentage increases above the reset minimum quarterly distribution. | |

If our general partner elects to reset the target distribution levels, it will be entitled to receive common units and to retain its then-current general partner interest. The number of common units to be issued to our general partner will equal the number of common units which would have entitled the holder to an average aggregate quarterly cash distribution in the prior two quarters equal to the average of the distributions to our general partner on the incentive distribution rights in the prior two quarters. Please read "Provisions of Our Partnership Agreement Relating to Cash Distributions—General Partner's Right to Reset Incentive Distribution Levels." | ||

Issuance of additional units | Our partnership agreement authorizes us to issue an unlimited number of additional units without the approval of our unitholders. Please read "Units Eligible for Future Sale" and "The Partnership Agreement—Issuance of Additional Interests." |

| Limited voting rights | Our general partner will manage and operate us. Unlike the holders of common stock in a corporation, our unitholders will have only limited voting rights on matters affecting our business. Our unitholders will have no right to elect our general partner or its directors on an annual or other continuing basis. Our general partner may not be removed except by a vote of the holders of at least 662/3% of the outstanding units, including any units owned by our general partner and its affiliates, voting together as a single class. Upon consummation of this offering, Wexford will own an aggregate of | |

Limited call right | If at any time our general partner and its affiliates own more than 90% of the outstanding common units, our general partner has the right, but not the obligation, to purchase all of the remaining common units at a price equal to the greater of (1) the average of the daily closing price of the common units over the 20 trading days preceding the date three days before notice of exercise of the call right is first mailed and (2) the highest per-unit price paid by our general partner or any of its affiliates for common units during the 90-day period preceding the date such notice is first mailed. If our general partner and its affiliates reduce their ownership percentage to below 70% of the outstanding common units, the ownership threshold to exercise the limited call right will be reduced to 80%. Please read "The Partnership Agreement—Limited Call Right." | |

Estimated ratio of taxable income to distributions | We estimate that if you own the common units you purchase in this offering through the record date for distributions for the period ending December 31, 2012, you will be allocated, on a cumulative basis, an amount of federal taxable income for that period that will be approximately 40.0% of the cash distributed to you with respect to that period. For example, if you receive an annual distribution of $1.78 per unit, we estimate that your average allocable federal taxable income per year will be no more than approximately $0.72 per unit. Thereafter, the ratio of allocable taxable income to cash distributions to you could substantially increase. Please read "Material Tax Consequences—Tax Consequences of Unit Ownership—Ratio of Taxable Income to Distributions" for the basis of this estimate. |

| Material federal income tax consequences | For a discussion of the material federal income tax consequences that may be relevant to prospective unitholders who are individual citizens or residents of the United States, please read "Material Tax Consequences." | |

Exchange listing | We have been approved to list our common units on the New York Stock Exchange, or NYSE, under the symbol "RNO." |

Summary Historical Consolidated and Condensed Consolidated and Pro Forma Condensed Consolidated Financial and Operating Data

The following table presents summary historical consolidated financial and operating data of our predecessor, Rhino Energy LLC, as of the dates and for the periods indicated. The summary historical consolidated financial data presented as of December 31, 2007 is derived from the audited historical consolidated statement of financial position of Rhino Energy LLC that is not included in this prospectus. The summary historical consolidated financial data presented as of December 31, 2008 and 2009 and for the years ended December 31, 2007, 2008 and 2009 is derived from the audited historical consolidated financial statements of Rhino Energy LLC that are included elsewhere in this prospectus. The historical consolidated financial data as of and for the year ended December 31, 2008 was restated to reflect certain selling, general and administrative expenses within the statement of operations, rather than as a distribution to members in the statement of financial position. The summary historical consolidated financial data presented as of March 31,June 30, 2010 and for the threesix months ended March 31,June 30, 2009 and 2010 is derived from the unaudited historical condensed consolidated financial statements of Rhino Energy LLC that are included elsewhere in this prospectus. The summary historical condensed consolidated financial data presented as of March 31,June 30, 2009 is derived from our predecessor's accounting records, which are unaudited.

The summary pro forma condensed consolidated financial data presented for the year ended December 31, 2009 and as of and for the threesix months ended March 31,June 30, 2010 is derived from our unaudited pro forma condensed consolidated financial statements included elsewhere in this prospectus. Our unaudited pro forma condensed consolidated financial statements give pro forma effect to:

The unaudited pro forma condensed consolidated statement of financial position assumes the items listed above occurred as of March 31,June 30, 2010. The unaudited pro forma condensed consolidated statements of operations data for the year ended December 31, 2009 and for the threesix months ended March 31,June 30, 2010 assume the items listed above occurred as of January 1, 2009. We have not given pro forma effect to incremental selling, general and administrative expenses of approximately $3.0 million that we expect to incur as a result of being a publicly traded partnership.

For a detailed discussion of the summary historical consolidated financial information contained in the following table, please read "Management's Discussion and Analysis of Financial Condition and Results of Operations." The following table should also be read in conjunction with "Use of Proceeds," "Business—Our History" and the audited historical consolidated financial statements of Rhino Energy LLC and our unaudited pro forma condensed consolidated financial statements included elsewhere in this prospectus. Among other things,

the historical consolidated and unaudited pro forma condensed consolidated financial

statements include more detailed information regarding the basis of presentation for the information in the following table.

The following table presents a non-GAAP financial measure, EBITDA, which we use in our business as it is an important supplemental measure of our performance and liquidity. EBITDA represents net income before interest expense, income taxes and depreciation, depletion and amortization. This measure is not calculated or presented in accordance with generally accepted accounting principles, or GAAP. We explain this measure under"—Non-GAAP Financial Measure" and reconcile it to its most directly comparable financial measures calculated and presented in accordance with GAAP.

| | | Rhino Energy LLC Historical | | | | Rhino Energy LLC Historical | | | ||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | Consolidated | Condensed Consolidated | Rhino Resource Partners LP Pro Forma Condensed Consolidated | | Consolidated | Condensed Consolidated | Rhino Resource Partners LP Pro Forma Condensed Consolidated | ||||||||||||||||||||||||||||||||||||||

| | | Year Ended December 31, | Three Months Ended March 31, | Year Ended December 31, | Three Months Ended March 31, | | Year Ended December 31, | Six Months Ended June 30, | Year Ended December 31, | Six Months Ended June 30, | ||||||||||||||||||||||||||||||||||||

| | | | 2008 (as restated) | | | | 2008 (as restated) | | ||||||||||||||||||||||||||||||||||||||

| | | 2007 | 2009 | 2009 | 2010 | 2009 | 2010 | | 2007 | 2009 | 2009 | 2010 | 2009 | 2010 | ||||||||||||||||||||||||||||||||

| | | (in thousands, except per unit data) | | (in thousands, except per unit data) | ||||||||||||||||||||||||||||||||||||||||||

Statement of Operations Data: | Statement of Operations Data: | Statement of Operations Data: | ||||||||||||||||||||||||||||||||||||||||||||

Total revenues | Total revenues | $ | 403,452 | $ | 438,924 | $ | 419,790 | $ | 116,706 | $ | 66,603 | $ | 419,790 | $ | 66,603 | Total revenues | $ | 403,452 | $ | 438,924 | $ | 419,790 | $ | 226,095 | $ | 145,031 | $ | 419,790 | $ | 145,031 | ||||||||||||||||

Costs and expenses: | Costs and expenses: | Costs and expenses: | ||||||||||||||||||||||||||||||||||||||||||||

Cost of operations (exclusive of depreciation, depletion and amortization shown separately below) | 318,405 | 364,912 | 336,335 | 98,317 | 46,352 | 336,335 | 46,352 | Cost of operations (exclusive of depreciation, depletion and amortization shown separately below) | 318,405 | 364,912 | 336,335 | 183,518 | 104,192 | 336,335 | 104,192 | |||||||||||||||||||||||||||||||

Freight and handling costs | 4,021 | 10,223 | 3,990 | 938 | 673 | 3,990 | 673 | Freight and handling costs | 4,021 | 10,223 | 3,990 | 1,976 | 1,444 | 3,990 | 1,444 | |||||||||||||||||||||||||||||||

Depreciation, depletion and amortization | 30,750 | 36,428 | 36,279 | 9,974 | 7,765 | 36,279 | 7,765 | Depreciation, depletion and amortization | 30,750 | 36,428 | 36,279 | 19,872 | 15,803 | 36,279 | 15,803 | |||||||||||||||||||||||||||||||

Selling, general and administrative (exclusive of depreciation, depletion and amortization shown separately above) | 15,370 | 19,042 | 16,754 | 4,376 | 3,678 | 16,754 | 3,678 | Selling, general and administrative (exclusive of depreciation, depletion and amortization shown separately above) | 15,370 | 19,042 | 16,754 | 8,989 | 7,604 | 16,754 | 7,604 | |||||||||||||||||||||||||||||||

(Gain) loss on sale of assets | (944 | ) | 451 | 1,710 | — | (1 | ) | 1,710 | (1 | ) | (Gain) loss on sale of assets | (944 | ) | 451 | 1,710 | 1,288 | (47 | ) | 1,710 | (47 | ) | |||||||||||||||||||||||||

Income from operations | Income from operations | 35,849 | 7,868 | 24,721 | 3,101 | 8,136 | 24,721 | 8,136 | Income from operations | 35,849 | 7,868 | 24,721 | 10,452 | 16,035 | 24,721 | 16,035 | ||||||||||||||||||||||||||||||

Interest and other income (expense): | Interest and other income (expense): | Interest and other income (expense): | ||||||||||||||||||||||||||||||||||||||||||||

Interest expense | (5,579 | ) | (5,501 | ) | (6,222 | ) | (1,170 | ) | (1,471 | ) | (4,291 | ) | (992 | ) | Interest expense | (5,579 | ) | (5,501 | ) | (6,222 | ) | (2,891 | ) | (2,781 | ) | (4,271 | ) | (1,875 | ) | |||||||||||||||||

Interest income | 317 | 149 | 71 | 87 | 8 | 71 | 8 | Interest income | 317 | 149 | 71 | 69 | 18 | 71 | 18 | |||||||||||||||||||||||||||||||

Equity in net income (loss) of unconsolidated affiliate(1) | — | (1,587 | ) | 893 | (43 | ) | (130 | ) | 893 | (130 | ) | Equity in net income (loss) of unconsolidated affiliate(1) | — | (1,587 | ) | 893 | (268 | ) | 414 | 893 | 414 | |||||||||||||||||||||||||

Total interest and other income (expense) | Total interest and other income (expense) | (5,263 | ) | (6,939 | ) | (5,259 | ) | (1,125 | ) | (1,592 | ) | (3,327 | ) | (1,114 | ) | Total interest and other income (expense) | (5,263 | ) | (6,939 | ) | (5,259 | ) | (3,089 | ) | (2,349 | ) | (3,307 | ) | (1,443 | ) | ||||||||||||||||

Income tax benefit | Income tax benefit | (126 | ) | — | — | — | — | — | — | Income tax benefit | (126 | ) | — | — | — | — | — | — | ||||||||||||||||||||||||||||

Net income | Net income | $ | 30,714 | $ | 929 | $ | 19,462 | $ | 1,976 | $ | 6,544 | $ | 21,394 | $ | 7,023 | Net income | $ | 30,714 | $ | 929 | $ | 19,462 | $ | 7,362 | $ | 13,686 | $ | 21,413 | $ | 14,592 | ||||||||||||||||

Net income per limited partner unit, basic: | Net income per limited partner unit, basic: | Net income per limited partner unit, basic: | ||||||||||||||||||||||||||||||||||||||||||||

Common units | $ | 1.306 | $ | 0.360 | Common units | $ | 1.306 | $ | 0.581 | |||||||||||||||||||||||||||||||||||||

Subordinated units | $ | 0.385 | $ | 0.196 | Subordinated units | $ | 0.387 | $ | 0.573 | |||||||||||||||||||||||||||||||||||||

Net income per limited partner unit, diluted: | Net income per limited partner unit, diluted: | Net income per limited partner unit, diluted: | ||||||||||||||||||||||||||||||||||||||||||||

Common units | $ | 1.304 | $ | 0.358 | Common units | $ | 1.305 | $ | 0.578 | |||||||||||||||||||||||||||||||||||||

Subordinated units | $ | 0.385 | $ | 0.196 | Subordinated units | $ | 0.387 | $ | 0.573 | |||||||||||||||||||||||||||||||||||||

Weighted average number of limited partner units outstanding, basic: | Weighted average number of limited partner units outstanding, basic: | Weighted average number of limited partner units outstanding, basic: | ||||||||||||||||||||||||||||||||||||||||||||

Common units | 12,397,000 | 12,397,000 | Common units | 12,397,000 | 12,397,000 | |||||||||||||||||||||||||||||||||||||||||

Subordinated units | 12,397,000 | 12,397,000 | Subordinated units | 12,397,000 | 12,397,000 | |||||||||||||||||||||||||||||||||||||||||

Weighted average number of limited partner units outstanding, diluted: | Weighted average number of limited partner units outstanding, diluted: | Weighted average number of limited partner units outstanding, diluted: | ||||||||||||||||||||||||||||||||||||||||||||

Common units | 12,411,479 | 12,447,417 | Common units | 12,410,073 | 12,445,073 | |||||||||||||||||||||||||||||||||||||||||

Subordinated units | 12,397,000 | 12,397,000 | Subordinated units | 12,397,000 | 12,397,000 | |||||||||||||||||||||||||||||||||||||||||

| | | Rhino Energy LLC Historical | | | | Rhino Energy LLC Historical | | | ||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | Consolidated | Condensed Consolidated | Rhino Resource Partners LP Pro Forma Condensed Consolidated | | Consolidated | Condensed Consolidated | Rhino Resource Partners LP Pro Forma Condensed Consolidated | ||||||||||||||||||||||||||||||||||||||

| | | Year Ended December 31, | Three Months Ended March 31, | Year Ended December 31, | Three Months Ended March 31, | | Year Ended December 31, | Six Months Ended June 30, | Year Ended December 31, | Six Months Ended June 30, | ||||||||||||||||||||||||||||||||||||

| | | | 2008 (as restated) | | | | 2008 (as restated) | | ||||||||||||||||||||||||||||||||||||||

| | | 2007 | 2009 | 2009 | 2010 | 2009 | 2010 | | 2007 | 2009 | 2009 | 2010 | 2009 | 2010 | ||||||||||||||||||||||||||||||||

| | | (in thousands, except per ton data) | | (in thousands, except per ton data) | ||||||||||||||||||||||||||||||||||||||||||

Statement of Cash Flows Data: | Statement of Cash Flows Data: | Statement of Cash Flows Data: | ||||||||||||||||||||||||||||||||||||||||||||

Net cash provided by (used in): | Net cash provided by (used in): | Net cash provided by (used in): | ||||||||||||||||||||||||||||||||||||||||||||

Operating activities | $ | 52,493 | $ | 57,211 | $ | 41,495 | $ | 3,274 | $ | 4,555 | Operating activities | $ | 52,493 | $ | 57,211 | $ | 41,495 | $ | 20,222 | $ | 24,871 | |||||||||||||||||||||||||

Investing activities | $ | (28,098 | ) | $ | (106,638 | ) | $ | (27,345 | ) | $ | (11,732 | ) | $ | (6,541 | ) | Investing activities | $ | (28,098 | ) | $ | (106,638 | ) | $ | (27,345 | ) | $ | (19,424 | ) | $ | (11,588 | ) | |||||||||||||||

Financing activities | $ | (21,192 | ) | $ | 47,781 | $ | (15,401 | ) | $ | 7,028 | $ | 1,647 | Financing activities | $ | (21,192 | ) | $ | 47,781 | $ | (15,401 | ) | $ | (2,292 | ) | $ | (13,781 | ) | |||||||||||||||||||

Other Financial Data: | Other Financial Data: | Other Financial Data: | ||||||||||||||||||||||||||||||||||||||||||||

EBITDA | EBITDA | $ | 66,917 | $ | 42,858 | $ | 61,964 | $ | 13,119 | $ | 15,779 | $ | 61,964 | $ | 15,779 | EBITDA | $ | 66,917 | $ | 42,858 | $ | 61,964 | $ | 30,125 | $ | 32,270 | $ | 61,964 | $ | 32,270 | ||||||||||||||||

Capital expenditures (1) | Capital expenditures (1) | $ | 32,773 | $ | 92,741 | $ | 29,657 | $ | 10,965 | $ | 6,637 | $ | 29,657 | $ | 6,637 | Capital expenditures (1) | $ | 32,773 | $ | 92,741 | $ | 29,657 | $ | 18,825 | $ | 11,498 | $ | 29,657 | $ | 11,498 | ||||||||||||||||

Balance Sheet Data (at period end): | Balance Sheet Data (at period end): | Balance Sheet Data (at period end): | ||||||||||||||||||||||||||||||||||||||||||||

Cash and cash equivalents | Cash and cash equivalents | $ | 3,583 | $ | 1,937 | $ | 687 | $ | 508 | $ | 347 | $ | 687 | $ | 347 | Cash and cash equivalents | $ | 3,583 | $ | 1,937 | $ | 687 | $ | 443 | $ | 188 | $ | 188 | ||||||||||||||||||

Property and equipment, net | Property and equipment, net | $ | 211,657 | $ | 282,863 | $ | 270,680 | $ | 283,685 | $ | 269,603 | $ | 270,680 | $ | 269,603 | Property and equipment, net | $ | 211,657 | $ | 282,863 | $ | 270,680 | $ | 278,124 | $ | 266,357 | $ | 266,357 | ||||||||||||||||||

Total assets | Total assets | $ | 275,992 | $ | 352,536 | $ | 339,985 | $ | 369,112 | $ | 347,488 | $ | 339,985 | $ | 347,488 | Total assets | $ | 275,992 | $ | 352,536 | $ | 339,985 | $ | 350,652 | $ | 340,897 | $ | 340,897 | ||||||||||||||||||

Total liabilities | Total liabilities | $ | 158,152 | $ | 234,225 | $ | 201,584 | $ | 248,825 | $ | 202,543 | $ | 134,634 | $ | 135,593 | Total liabilities | $ | 158,152 | $ | 234,225 | $ | 201,584 | $ | 225,027 | $ | 188,811 | $ | 121,178 | ||||||||||||||||||

Total debt | Total debt | $ | 83,954 | $ | 138,027 | $ | 122,137 | $ | 145,107 | $ | 123,833 | $ | 55,187 | $ | 56,883 | Total debt | $ | 83,954 | $ | 138,027 | $ | 122,137 | $ | 137,146 | $ | 108,454 | $ | 40,821 | ||||||||||||||||||

Members'/partners' equity | Members'/partners' equity | $ | 117,841 | $ | 118,311 | $ | 138,401 | $ | 120,287 | $ | 144,944 | $ | 205,351 | $ | 211,894 | Members'/partners' equity | $ | 117,841 | $ | 118,311 | $ | 138,401 | $ | 125,625 | $ | 152,086 | $ | 219,719 | ||||||||||||||||||

Operating Data (2): | Operating Data (2): | Operating Data (2): | ||||||||||||||||||||||||||||||||||||||||||||

Tons of coal sold | Tons of coal sold | 8,159 | 7,977 | 6,699 | 1,939 | 949 | 6,699 | 949 | Tons of coal sold | 8,159 | 7,977 | 6,699 | 3,696 | 2,042 | 6,699 | 2,042 | ||||||||||||||||||||||||||||||

Tons of coal produced/purchased | Tons of coal produced/purchased | 8,024 | 8,017 | 6,732 | 1,991 | 1,044 | 6,732 | 1,044 | Tons of coal produced/purchased | 8,024 | 8,017 | 6,732 | 3,742 | 2,176 | 6,732 | 2,176 | ||||||||||||||||||||||||||||||

Coal revenues per ton (3) | Coal revenues per ton (3) | $ | 48.30 | $ | 51.25 | $ | 59.98 | $ | 58.33 | $ | 65.98 | $ | 59.98 | $ | 65.98 | Coal revenues per ton (3) | $ | 48.30 | $ | 51.25 | $ | 59.98 | $ | 59.06 | $ | 66.96 | $ | 59.98 | $ | 66.96 | ||||||||||||||||

Cost of operations per ton (4) | Cost of operations per ton (4) | $ | 39.02 | $ | 45.75 | $ | 50.21 | $ | 50.69 | $ | 48.82 | $ | 50.21 | $ | 48.82 | Cost of operations per ton (4) | $ | 39.02 | $ | 45.75 | $ | 50.21 | $ | 49.66 | $ | 51.02 | $ | 50.21 | $ | 51.02 | ||||||||||||||||

| | | Rhino Energy LLC Historical | | Rhino Energy LLC Historical | ||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | Consolidated | Condensed Consolidated | | Consolidated | Condensed Consolidated | ||||||||||||||||||||||||||||

| | | Year Ended December 31, | Three Months Ended March 31, | | Year Ended December 31, | Six Months Ended June 30, | ||||||||||||||||||||||||||||

| | | 2007 | 2008 | 2009 | 2009 | 2010 | | 2007 | 2008 | 2009 | 2009 | 2010 | ||||||||||||||||||||||

| | | (in thousands) | | (in thousands) | ||||||||||||||||||||||||||||||

Reconciliation of total capital expenditures to net cash used for capital expenditures: | Reconciliation of total capital expenditures to net cash used for capital expenditures: | Reconciliation of total capital expenditures to net cash used for capital expenditures: | ||||||||||||||||||||||||||||||||

Additions to property, plant and equipment | Additions to property, plant and equipment | $ | 14,599 | $ | 78,076 | $ | 27,836 | $ | 9,144 | $ | 6,637 | Additions to property, plant and equipment | $ | 14,599 | $ | 78,076 | $ | 27,836 | $ | 17,004 | $ | 11,440 | ||||||||||||

Acquisitions of coal companies and coal properties | Acquisitions of coal companies and coal properties | 18,174 | 14,665 | 1,821 | 1,821 | — | Acquisitions of coal companies and coal properties | 18,174 | 14,665 | — | — | 58 | ||||||||||||||||||||||

Acquisition of roof bolt manufacturing company | Acquisition of roof bolt manufacturing company | — | — | 1,821 | 1,821 | — | ||||||||||||||||||||||||||||

Net cash used for capital expenditures | Net cash used for capital expenditures | 32,773 | 92,741 | 29,657 | 10,965 | 6,637 | Net cash used for capital expenditures | 32,773 | 92,741 | 29,657 | 18,825 | 11,498 | ||||||||||||||||||||||

Plus: | Plus: | Plus: | ||||||||||||||||||||||||||||||||

Additions to property, plant and equipment financed through long-term borrowings | — | — | — | — | — | Additions to property, plant and equipment financed through long-term borrowings | — | — | — | — | — | |||||||||||||||||||||||

Total capital expenditures | Total capital expenditures | $ | 32,773 | $ | 92,741 | $ | 29,657 | $ | 10,965 | $ | 6,637 | Total capital expenditures | $ | 32,773 | $ | 92,741 | $ | 29,657 | $ | 18,825 | $ | 11,498 | ||||||||||||

EBITDA is used as a supplemental financial measure by management and by external users of our financial statements, such as investors, to assess:

EBITDA should not be considered an alternative to net income, income from operations, cash flows from operating activities or any other measure of financial performance or liquidity presented in accordance with GAAP. EBITDA excludes some, but not all, items that affect net income, income from operations and cash flows from operating activities, and these measures may vary among other companies.

EBITDA as presented below may not be comparable to similarly titled measures of other companies. The following table presents a reconciliation of EBITDA to the most directly comparable GAAP financial measures, on a historical basis and pro forma basis, as applicable, for each of the periods indicated.indicated:

| | | Rhino Energy LLC Historical | | | | Rhino Energy LLC Historical | | | ||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | Consolidated | Condensed Consolidated | Rhino Resource Partners LP Pro Forma Condensed Consolidated | | Consolidated | Condensed Consolidated | Rhino Resource Partners LP Pro Forma Condensed Consolidated | ||||||||||||||||||||||||||||||||||||||

| | | Year Ended December 31, | Three Months Ended March 31, | Year Ended December 31, | Three Months Ended March 31, | | Year Ended December 31, | Six Months Ended June 30, | Year Ended December 31, | Six Months Ended June 30, | ||||||||||||||||||||||||||||||||||||

| | | | 2008 (as restated) | | | | 2008 (as restated) | | ||||||||||||||||||||||||||||||||||||||

| | | 2007 | 2009 | 2009 | 2010 | 2009 | 2010 | | 2007 | 2009 | 2009 | 2010 | 2009 | 2010 | ||||||||||||||||||||||||||||||||

| | | (in thousands) | | (in thousands) | ||||||||||||||||||||||||||||||||||||||||||

Reconciliation of EBITDA to net income: | Reconciliation of EBITDA to net income: | Reconciliation of EBITDA to net income: | ||||||||||||||||||||||||||||||||||||||||||||

Net income | Net income | $ | 30,714 | $ | 929 | $ | 19,462 | $ | 1,976 | $ | 6,544 | $ | 21,394 | $ | 7,023 | Net income | $ | 30,714 | $ | 929 | $ | 19,462 | $ | 7,362 | $ | 13,686 | $ | 21,413 | $ | 14,592 | ||||||||||||||||

Plus: | Plus: | Plus: | ||||||||||||||||||||||||||||||||||||||||||||

Depreciation, depletion and amortization | 30,750 | 36,428 | 36,279 | 9,974 | 7,765 | 36,279 | 7,765 | Depreciation, depletion and amortization | 30,750 | 36,428 | 36,279 | 19,872 | 15,803 | 36,279 | 15,803 | |||||||||||||||||||||||||||||||

Interest expense | 5,579 | 5,501 | 6,222 | 1,170 | 1,471 | 4,291 | 992 | Interest expense | 5,579 | 5,501 | 6,222 | 2,891 | 2,781 | 4,271 | 1,875 | |||||||||||||||||||||||||||||||

Less: | Less: | Less: | ||||||||||||||||||||||||||||||||||||||||||||

Income tax benefit | 126 | — | — | — | — | — | — | Income tax benefit | 126 | — | — | — | — | — | — | |||||||||||||||||||||||||||||||

EBITDA | EBITDA | $ | 66,917 | $ | 42,858 | $ | 61,964 | $ | 13,119 | $ | 15,779 | $ | 61,964 | $ | 15,779 | EBITDA | $ | 66,917 | $ | 42,858 | $ | 61,964 | $ | 30,125 | $ | 32,270 | $ | 61,964 | $ | 32,270 | ||||||||||||||||

| | | Rhino Energy LLC Historical | | Rhino Energy LLC Historical | ||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | Consolidated | Condensed Consolidated | | Consolidated | Condensed Consolidated | ||||||||||||||||||||||||||||

| | | Year Ended December 31, | Three Months Ended March 31, | | Year Ended December 31, | Six Months Ended June 30, | ||||||||||||||||||||||||||||

| | | | 2008 (as restated) | | | | 2008 (as restated) | | ||||||||||||||||||||||||||

| | | 2007 | 2009 | 2009 | 2010 | | 2007 | 2009 | 2009 | 2010 | ||||||||||||||||||||||||

| | | (in thousands) | | (in thousands) | ||||||||||||||||||||||||||||||

Reconciliation of EBITDA to net cash provided by operating activities: | Reconciliation of EBITDA to net cash provided by operating activities: | Reconciliation of EBITDA to net cash provided by operating activities: | ||||||||||||||||||||||||||||||||

Net cash provided by operating activities | Net cash provided by operating activities | $ | 52,493 | $ | 57,211 | $ | 41,495 | $ | 3,274 | $ | 4,555 | Net cash provided by operating activities | $ | 52,493 | $ | 57,211 | $ | 41,495 | $ | 20,222 | $ | 24,871 | ||||||||||||

Plus: | Plus: | Plus: | ||||||||||||||||||||||||||||||||

Increase in net operating assets | 10,553 | — | 17,190 | 9,601 | 10,828 | Increase in net operating assets | 10,553 | — | 17,190 | 10,290 | 5,827 | |||||||||||||||||||||||

Decrease in provision for doubtful accounts | 175 | — | — | — | — | Decrease in provision for doubtful accounts | 175 | — | — | — | — | |||||||||||||||||||||||

Gain on sale of assets | 944 | — | — | — | 1 | Gain on sale of assets | 944 | — | — | 47 | ||||||||||||||||||||||||

Gain on retirement of advance royalties | 115 | — | — | — | — | Gain on retirement of advance royalties | 115 | — | — | 77 | — | |||||||||||||||||||||||

Interest expense | 5,579 | 5,501 | 6,222 | 1,170 | 1,471 | Interest expense | 5,579 | 5,501 | 6,222 | 2,891 | 2,781 | |||||||||||||||||||||||

Settlement of litigation | — | — | 1,773 | — | — | Settlement of litigation | — | — | 1,773 | — | — | |||||||||||||||||||||||

Equity in net income of unconsolidated affiliate | — | — | 893 | — | — | Equity in net income of unconsolidated affiliate | — | — | 893 | — | 414 | |||||||||||||||||||||||

Less: | Less: | Less: | ||||||||||||||||||||||||||||||||

Decrease in net operating assets | — | 10,440 | — | — | — | Decrease in net operating assets | — | 10,440 | — | — | — | |||||||||||||||||||||||

Accretion on interest-free debt | 360 | 569 | 200 | 44 | 49 | Accretion on interest-free debt | 360 | 569 | 200 | 193 | 98 | |||||||||||||||||||||||

Amortization of advance royalties | 700 | 471 | 215 | 83 | 276 | Amortization of advance royalties | 700 | 471 | 215 | 156 | 374 | |||||||||||||||||||||||

Increase in provision for doubtful accounts | — | — | 19 | — | — | Increase in provision for doubtful accounts | — | — | 19 | — | — | |||||||||||||||||||||||

Loss on sale of assets | — | 451 | 1,710 | — | — | Loss on sale of assets | — | 451 | 1,710 | 1,288 | — | |||||||||||||||||||||||

Loss on retirement of advance royalties | — | 45 | 712 | — | 78 | Loss on retirement of advance royalties | — | 45 | 712 | — | 113 | |||||||||||||||||||||||

Income tax benefit | 126 | — | — | — | — | Income tax benefit | 126 | — | — | — | — | |||||||||||||||||||||||

Accretion on asset retirement obligations | 1,757 | 2,709 | 2,753 | 756 | 542 | Accretion on asset retirement obligations | 1,757 | 2,709 | 2,753 | 1,450 | 1,085 | |||||||||||||||||||||||

Equity in net loss of unconsolidated affiliate | — | 1,587 | — | 43 | 130 | Equity in net loss of unconsolidated affiliate | — | 1,587 | — | 268 | — | |||||||||||||||||||||||

Payment of abandoned public offering expenses (a) | — | 3,582 | — | — | — | Payment of abandoned public offering expenses (a) | — | 3,582 | — | — | — | |||||||||||||||||||||||

EBITDA | EBITDA | $ | 66,917 | $ | 42,858 | $ | 61,964 | $ | 13,119 | $ | 15,779 | EBITDA | $ | 66,917 | $ | 42,858 | $ | 61,964 | $ | 30,125 | $ | 32,270 | ||||||||||||

Limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. You should carefully consider the following risk factors together with all of the other information included in this prospectus in evaluating an investment in our common units.

If any of the following risks were to occur, our business, financial condition, results of operations and cash available for distribution could be materially adversely affected. In that case, we might not be able to make distributions on our common units, the trading price of our common units could decline, and you could lose all or part of your investment.

Risks Inherent in Our Business

We may not have sufficient cash to enable us to pay the minimum quarterly distribution on our common units following establishment of cash reserves and payment of costs and expenses, including reimbursement of expenses to our general partner.

We may not have sufficient cash each quarter to pay the full amount of our minimum quarterly distribution of $0.445 per unit, or $1.78 per unit per year, which will require us to have available cash of approximately $11.3 million per quarter, or $45.0 million per year, based on the number of common and subordinated units and the general partner interest to be outstanding after the completion of this offering. The amount of cash we can distribute on our common and subordinated units principally depends upon the amount of cash we generate from our operations, which will fluctuate from quarter to quarter based on, among other things:

For a description of additional restrictions and factors that may affect our ability to pay cash distributions, please read "Cash Distribution Policy and Restrictions on Distributions."

We must generate approximately $45.0 million of available cash from operating surplus to pay the minimum quarterly distribution for four quarters on all of our common units and subordinated units that will be outstanding immediately after this offering and the corresponding distribution on our general partner interest. For the year ended December 31, 2009 and the twelve months ended March 31,June 30, 2010, we would have generated approximately $33.4$11.6 million and $39.3$1.5 million, respectively, less than the amount of available cash from operating surplus respectively, and would have been ableneeded to pay the full minimum quarterly distribution on all of our common units, but only approximately 48.3% and 74.8%, respectively, of the minimum quarterly distribution on ouras a whole, including subordinated units, during those periods.

We must generate approximately $45.0 million (or approximately $11.3 million per quarter) of available cash to pay the minimum quarterly distribution for four quarters on all of our common units and subordinated units that will be outstanding immediately after this offering and the corresponding distribution on our general partner interest. We did not generate $45.0 million of available cash from operating surplus during the year ended December 31, 2009 or the twelve months ended March 31,June 30, 2010. The amount of available cash from operating surplus we generated with respect to those periods was approximately $33.4 million and $39.3$43.6 million, respectively. Asrespectively, or approximately $11.6 million and $1.5 million, respectively, less than the amount needed to pay the full minimum quarterly distribution on all units as a result, forwhole, including subordinated units. For those periods, we would have generated aggregate available cash sufficient to pay 100% of the aggregate minimum quarterly distribution on our common units, but only approximately 48.3%48.4% and 74.8%93.5%, respectively, of the minimum quarterly distribution on our subordinated units during those periods. We have not usedcalculated available cash on a quarter-by-quarter estimatesbasis for each quarter in the year ended December 31, 2009 andor the twelve months ended March 31,June 30, 2010 to determine if we would have generated available cash sufficient to pay the minimum quarterly distribution for each quarter during those periods.

The assumptions underlying our forecast of cash available for distribution included in "Cash Distribution Policy and Restrictions on Distributions" are inherently uncertain and subject to significant business, economic, financial, regulatory and competitive risks and uncertainties that could cause cash available for distribution to differ materially from those estimated.

We would have generated sufficient cash available for distribution to pay 100% of the minimum quarterly distribution on all of our common units during the year ended December 31, 2009 and the twelve months ended March 31,June 30, 2010, but only approximately 48.3%48.4% and 74.8%93.5%, respectively, of the minimum quarterly distribution on our subordinated units during those periods. The forecast of cash available for distribution set forth in "Cash Distribution Policy and Restrictions on Distributions" includes our forecast of our results of operations and cash available for distribution for the twelve months ending JuneSeptember 30, 2011. Our ability to pay the full minimum quarterly distribution in the forecast period is based on a number of assumptions that

may not prove to be correct, which are discussed in "Cash Distribution Policy and Restrictions on Distributions." These assumptions include, but are not limited to, the following:

Our forecast of cash available for distribution has been prepared by management, and we have not received an opinion or report on it from any independent registered public accountants. The assumptions underlying our forecast of cash available for distribution are inherently uncertain and are subject to significant business, economic, financial, regulatory and competitive risks and uncertainties that could cause cash available for distribution to differ materially from that which is forecasted. If we do not achieve our forecasted results, we may not be able to pay the minimum quarterly distribution or any amount on our common units or subordinated units, in which event the market price of our common units may decline materially. Please read "Cash Distribution Policy and Restrictions on Distributions."

A decline in coal prices could adversely affect our results of operations and cash available for distribution to our unitholders.

Our results of operations and the value of our coal reserves are significantly dependent upon the prices we receive for our coal as well as our ability to improve productivity and control costs. The prices we receive for coal depend upon factors beyond our control, including:

Any adverse change in these factors could result in weaker demand and lower prices for our products. In addition, the recent global economic downturn, particularly with respect to the U.S. economy, coupled with the global financial and credit market disruptions, have had an impact on the coal industry generally and may continue to do so until economic conditions improve. The demand for electricity in the United States decreased during 2009 as compared to 2008, which led to a decline in the demand for and prices of coal. The demand for electricity may remain at low levels or further decline if economic conditions remain weak. If these trends continue, we may not be able to sell all of the coal we are capable of producing or sell our coal at prices comparable to recent years. Recent low prices for natural gas, which is a substitute for coal generated power, may also lead to continued decreased coal consumption by electricity-generating utilities. A substantial or extended decline in the prices we receive for our coal supply contracts could materially and adversely affect our results of operations.

We could be negatively impacted by the competitiveness of the global markets in which we compete and declines in the market demand for coal.

We compete with coal producers in various regions of the United States and overseas for domestic and international sales. The domestic demand for, and prices of, our coal primarily depend on coal consumption patterns of the domestic electric utility industry and the domestic steel industry. Consumption by the domestic electric utility industry is affected by the demand for electricity, environmental and other governmental regulations, technological developments and the price of competing coal and alternative fuel sources, such as natural gas, nuclear, hydroelectric power and other renewable energy sources. Consumption by the domestic steel industry is primarily affected by economic growth and the demand for steel used in construction as well as appliances and automobiles. In recent years, the competitive environment for coal was impacted by sustained growth in a number of the largest markets in the world, including the United States, China, Japan and India, where demand for both electricity and steel have supported prices for steam and metallurgical coal. The economic stability of these markets has a significant effect on the demand for coal and the level of competition in supplying these markets. The cost of ocean transportation and the value of the U.S. dollar in relation to foreign currencies significantly impact the relative attractiveness of our coal as we compete on price with foreign coal producing sources. During the last several years, the U.S. coal industry has experienced increased consolidation, which has contributed to the industry becoming more competitive. Increased competition by coal producers or producers of alternate fuels could decrease the demand for, or pricing of, or both, for our coal, adversely impacting our results of operations and cash available for distribution.

Portions of our coal reserves possess quality characteristics that enable us to mine, process and market them as either metallurgical coal or high quality steam coal, depending on prevailing market conditions. A decline in the metallurgical market relative to the steam market could cause us to shift coal from the metallurgical market to the steam market, potentially reducing the price we could obtain for this coal and adversely impacting our cash flows, results of operations and cash available for distribution.

Our mining operations are subject to extensive and costly environmental laws and regulations, and such current and future laws and regulations could materially increase our operating costs or limit our ability to produce and sell coal.

The coal mining industry is subject to numerous and extensive federal, state and local environmental laws and regulations, including laws and regulations pertaining to permitting and

licensing requirements, air quality standards, plant and wildlife protection, reclamation and restoration of mining properties, the discharge of materials into the environment, the storage, treatment and disposal of wastes, protection of wetlands, surface subsidence from underground mining and the effects that mining has on groundwater quality and availability. The costs, liabilities and requirements associated with these laws and regulations are significant and time-consuming and may delay commencement or continuation of our operations. Moreover, the possibility exists that new laws or regulations (or new judicial interpretations or enforcement policies of existing laws and regulations) could materially affect our mining operations, results of operations and cash available for distribution to our unitholders, either through direct impacts such as those regulating our existing mining operations, or indirect impacts such as those that discourage or limit our customers' use of coal. Although we believe that we are in substantial compliance with existing laws and regulations, we may, in the future, experience violations that would subject us to administrative, civil and criminal penalties and a range of other possible sanctions. The enforcement of laws and regulations governing the coal mining industry has

increased substantially. As a result, the consequences for any noncompliance may become more significant in the future.