As filed with the Securities and Exchange Commission on January 10,24, 2011

Registration No. 333-170203

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 24

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

BankUnited, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) | 6035 (Primary Standard Industrial Classification Code Number) | 27-0162450 (I.R.S. Employer Identification Number) |

14817 Oak Lane

Miami Lakes, Florida 33016

(305) 569-2000

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

John A. Kanas

Chairman, President and Chief Executive Officer

BankUnited, Inc.

14817 Oak Lane

Miami Lakes, Florida 33016

(305) 569-2000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

Richard B. Aftanas, Esq. Skadden, Arps, Slate, Meagher & Flom LLP Four Times Square New York, New York 10036 (212) 735-3000 | Richard D. Truesdell, Jr., Esq. Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 (212) 450-4000 | |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 of the Securities Act of 1933 check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Securities Exchange Act of 1934.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) | Smaller reporting company o |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file an amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. Neither we nor the selling stockholders may sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion. Dated January 10,24, 2011

PROSPECTUS

26,250,000 Shares

![]()

BankUnited, Inc.

Common Stock

This is the initial public offering of our common stock. We are offering 4,000,000 shares of our common stock. The selling stockholders identified in this prospectus are offering an additional 22,250,000 shares. We will not receive any of the proceeds from the sale of the shares being sold by the selling stockholders.

Prior to this offering there has been no public market for our common stock. It is currently estimated that the public offering price per share of our common stock will be between $$23.00 and $$25.00 per share. We intend to apply to list ourOur common stock has been approved for listing on the New York Stock Exchange under the symbol "BKU."

See "Risk Factors" on page 13 to read about factors you should consider before buying our common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| | Per Share | Total | |||||

|---|---|---|---|---|---|---|---|

Initial public offering price | $ | $ | |||||

Underwriting discounts | $ | $ | |||||

Proceeds, before expenses, to us | $ | $ | |||||

Proceeds, before expenses, to the selling stockholders | $ | $ | |||||

To the extent that the underwriters sell more than 26,250,000 shares of our common stock, the underwriters have the option to purchase up to an additional 3,937,500 shares of our common stock from the selling stockholders at the initial public offering price less the underwriting discount, within 30 days from the date of this prospectus, to cover over-allotments.

The underwriters expect to deliver the shares of our common stock against payment in New York, New York on , 2011.

| Morgan Stanley | BofA Merrill Lynch | |

Deutsche Bank Securities | Goldman, Sachs & Co. |

Keefe, Bruyette & Woods | RBC Capital Markets | UBS Investment Bank |

Prospectus dated , 2011

We, the selling stockholders and the underwriters have not authorized anyone to provide any information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We, the selling stockholders and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are not, and the selling stockholders and underwriters are not, making an offer of these securities in any jurisdiction where the offer is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front of this prospectus.

TABLE OF CONTENTS

PROSPECTUS SUMMARY | 1 | |

RISK FACTORS | 13 | |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS | 26 | |

REORGANIZATION | 27 | |

USE OF PROCEEDS | 29 | |

DIVIDEND POLICY | 30 | |

CAPITALIZATION | 31 | |

DILUTION | 32 | |

SELECTED HISTORICAL CONSOLIDATED FINANCIAL INFORMATION | 34 | |

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 38 | |

BUSINESS | ||

REGULATION AND SUPERVISION | ||

MANAGEMENT | ||

COMPENSATION DISCUSSION AND ANALYSIS | ||

CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS | 148 | |

PRINCIPAL AND SELLING STOCKHOLDERS | 150 | |

DESCRIPTION OF OUR CAPITAL STOCK | 155 | |

SHARES ELIGIBLE FOR FUTURE SALE | ||

CERTAIN MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES FOR NON-U.S. HOLDERS OF COMMON STOCK | ||

UNDERWRITERS | ||

LEGAL MATTERS | ||

EXPERTS | ||

WHERE YOU CAN FIND MORE INFORMATION | ||

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS | F-1 |

The shares of our common stock that you purchase in this offering will not be a bank deposit and will not be insured or guaranteed by the FDIC or any other government agency. Your investment will be subject to investment risk, and you must be capable of affording the loss of your entire investment.

For investors outside the United States: None of we, the selling stockholders or any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

MARKET AND INDUSTRY DATA AND FORECASTS

This prospectus includes market and industry data and forecasts that we have developed from independent research firms, publicly available information, various industry publications, other

i

published industry sources or our internal data and estimates. Independent research reports, industry publications and other published industry sources generally indicate that the information contained therein was obtained from sources believed to be reliable, but do not guarantee the accuracy and completeness of such information. Although we believe that the publications and reports are reliable, none of we, the selling stockholders or the underwriters have independently verified the data. Our internal data, estimates and forecasts are based on information obtained from our investors, trade and business organizations and other contacts in the markets in which we operate and our management's understanding of industry conditions. Although we believe that such information is reliable, we have not had such information verified by any independent sources.

ii

This summary highlights selected information contained elsewhere in this prospectus. This summary may not contain all of the information that you should consider before investing in our common stock. You should read the entire prospectus carefully, including the section entitled "Risk Factors," our financial statements and the related notes thereto and management's discussion and analysis thereof included elsewhere in this prospectus, before making an investment decision to purchase our common stock. Unless we state otherwise or the context otherwise requires, references in this prospectus to "we," "our," "us," and the "Company" for all periods subsequent to the Acquisition (as defined below) refer to BankUnited, Inc., a Delaware corporation, and its consolidated subsidiaries. References in this prospectus to "BankUnited" and the "Bank" for all periods beginning May 22, 2009 refer to BankUnited, a federal savings association, formed to acquire substantially all of the assets (including loans, employees and certain operations), and assume all of the non-brokered deposits and substantially all other liabilities, of the Failed Bank (as defined below).

Summary

BankUnited, Inc. is a savings and loan holding company with two wholly-owned subsidiaries: BankUnited, which is one of the largest independent depository institutions headquartered in Florida by assets, and BankUnited Investment Services, Inc., or BankUnited Investment Services, a Florida insurance agency which provides comprehensive wealth management products and financial planning services. BankUnited is a federally-chartered, federally-insured savings association headquartered in Miami Lakes, Florida, with $11.2 billion of assets, more than 1,100 professionals and 78 branches in 13 counties at September 30, 2010. Our goal is to build a premier, large regional bank with a low-risk, long-term value-oriented business model focused on small and medium sized businesses and consumers. We endeavor to provide personalized customer service and offer a full range of traditional banking products and financial services to both our commercial and consumer customers, who are predominantly located in Florida.

BankUnited, Inc. was organized by a management team led by our Chairman, President and Chief Executive Officer, John A. Kanas, on April 28, 2009 and was initially capitalized with $945.0 million by a group of investors. On May 21, 2009, BankUnited was granted a savings association charter and the newly formed bank acquired substantially all of the assets and assumed all of the non-brokered deposits and substantially all other liabilities of BankUnited, FSB, or the Failed Bank, from the Federal Deposit Insurance Corporation, or the FDIC, in a transaction which we refer to as the Acquisition. Concurrently with the Acquisition, we entered into two loss sharing agreements, or the Loss Sharing Agreements, which cover certain legacy assets, including the entire legacy loan portfolio and other real estate owned, or OREO, and certain purchased investment securities, including private-label mortgage-backed securities and non-investment grade securities. We refer to assets covered by the Loss Sharing Agreements as Covered Assets (or, in certain cases, Covered Loans or Covered Securities).

Since the Bank's establishment in May 2009, we have pursued our new strategy and as part of this strategy we have recruited a new executive management team, substantially enhanced our middle management team, redesigned the Bank's underwriting functions, and have begun the process of improving the Bank's information technology systems and optimizing our existing branch network. For the nine months ended September 30, 2010, the Company was one of the most profitable and well-capitalized bank holding companies in the United States, having earned 1.9% on its average assets and 17.7% on its average common stockholder's equity, and achieved a 41.9% efficiency ratio. BankUnited's tier 1 leverage ratio was 10.1% and its tier 1 risk-based capital ratio was 42.5% at September 30, 2010. The Company's tangible common equity ratio was 10.7% at September 30, 2010.

We intend to invest our excess capital to grow opportunistically both organically and through acquisitions.

Our management team is led by Mr. Kanas, a veteran of the banking industry who built North Fork Bancorporation, or North Fork, into a leading regional bank based in New York. At the time of its sale to Capital One Financial Corporation, or Capital One, in December 2006, North Fork was one of the top 25 bank holding companies in the United States. Mr. Kanas served as the Chairman of North Fork from 1986 to 2006 and President and Chief Executive Officer of North Fork from 1977 to 2006. Through organic growth and over 15 acquisitions, Mr. Kanas oversaw the growth and expansion of North Fork from less than $1 billion in assets in 1977 to nearly $60 billion in assets by 2006. According to FactSet Research Systems, while for the five-year period prior to its sale to Capital One, North Fork generated a total annualized return of 11.2%, which equaled the median total annualized return of the top fifty U.S. bank holding companies (excluding North Fork) by assets, for the ten-year period, North Fork generated a total annualized return of 20.5%, compared to a median total annualized return of 14.5%. North Fork distinguished itself as one of the most efficient banking companies in the United States through Mr. Kanas' vision of safe and prudent expansion, cost control and capital management. North Fork was sold to Capital One in December 2006 for $13.2 billion, or 4.0 times tangible equity, a transaction multiple higher than both the median transaction multiple of 3.2 for sales of banks with assets between $10 billion and $30 billion and the median transaction multiple of 3.0 for sales in the banking industry during the period from 2000 to 2006.

The Acquisition

On May 21, 2009, BankUnited entered into a purchase and assumption agreement, or the Purchase and Assumption Agreement, with the FDIC, Receiver of the Failed Bank, to acquire substantially all of the assets and assume all of the non-brokered deposits and substantially all other liabilities of the Failed Bank. Excluding the effects of acquisition accounting adjustments, BankUnited acquired $13.6 billion of assets and assumed $12.8 billion of liabilities. The fair value of the assets acquired was $10.9 billion and the fair value of the liabilities assumed was $13.1 billion. BankUnited received a net cash consideration from the FDIC in the amount of $2.2 billion.

The Acquisition consisted of assets with a fair value of $10.9 billion, including $5.0 billion of loans (with a corresponding unpaid principal balance, or UPB, of $11.2 billion), a $3.4 billion FDIC indemnification asset, $538.9 million of investment securities, $1.2 billion of cash and cash equivalents, $177.7 million of foreclosed assets, $243.3 million of Federal Home Loan Bank, or FHLB, stock and $347.4 million of other assets. Liabilities with a fair value of $13.1 billion were also assumed, including $8.3 billion of non-brokered deposits, $4.6 billion of FHLB advances, and $112.2 million of other liabilities.

Concurrently with the Acquisition, the Bank entered into the Loss Sharing Agreements with the FDIC that cover certain legacy assets, including the entire loan portfolio and OREO, and certain purchased investment securities, including private-label mortgage-backed securities and non-investment grade securities. The Bank acquired other BankUnited, FSB assets that are not covered by the Loss Sharing Agreements with the FDIC including cash, certain investment securities purchased at fair market value and other tangible assets. The Loss Sharing Agreements do not apply to subsequently acquired, purchased or originated assets. At September 30, 2010, the Covered Assets consisted of assets with a book value of $4.3 billion. The total UPB (or, for investment securities, unamortized cost basis) of the Covered Assets at September 30, 2010 was $8.9 billion.

Pursuant to the terms of the Loss Sharing Agreements, the Covered Assets are subject to a stated loss threshold whereby the FDIC will reimburse the Bank for 80% of losses up to the $4.0 billion stated threshold and 95% of losses in excess of the $4.0 billion stated threshold, calculated, in each case, based on UPB (or, for investment securities, unamortized cost basis) plus certain interest and

expenses. The carrying value of the FDIC indemnification asset at September 30, 2010 was $2.7 billion. The Bank will reimburse the FDIC for its share of recoveries with respect to losses for which the FDIC paid the Bank a reimbursement under the Loss Sharing Agreements. The FDIC's obligation to reimburse the Company for losses with respect to the Covered Assets began with the first dollar of loss incurred. We have received $997.2 million from the FDIC in reimbursements under the Loss Sharing Agreements for claims filed for losses incurred as of September 30, 2010. See "Business—The Acquisition—Loss Sharing Agreements."

Several elements of our Acquisition are favorable relative to other FDIC-assisted transactions and position the Company to generate significant value. At the time of the Acquisition, bank failures were on the rise and the U.S. Treasury's unprecedented Supervisory Capital Assessment Program for the largest U.S. bank holding companies was underway. Due in part to the distress in the banking system, economic uncertainty and poor capital markets conditions, the Covered Loans and OREO were purchased by the Bank in a bidding process for 76.5% of their $11.4 billion in UPB as of the Acquisition date, which represented the fair market value for those assets at that time. The discount was one of the largest relative to other FDIC-assisted transactions and reflected, in addition to the abovementioned factors, the poor quality of the assets acquired as noted by the ratio of non-performing assets to total assets of 23.5% at May 21, 2009. In addition, our bid included the granting of a warrant to the FDIC, allowing the FDIC to participate in the economic upside of the transaction if certain performance levels are achieved. Along with the pricing terms, the Loss Sharing Agreements and the size of the transaction enable the Company to generate significant capital even in severe loss scenarios. For example, in the worst case scenario of a 100% credit loss on all Covered Loans and OREO, we would recover no less than 89.7% of the UPB as of the Acquisition date, assuming compliance with the terms of the Loss Sharing Agreements.

Furthermore, the Loss Sharing Agreements include attractive provisions that optimize our flexibility and reduce our risk associated with the Covered Assets, including the following:

We view our relationship with the FDIC as a long-term partnership in which both parties are economically aligned to minimize credit losses on the Covered Assets.

Our Competitive Strengths

We believe that we are especially well positioned to create value for our stockholders.

experience and a history of high performance at nationally recognized mid- to large-cap financial institutions. Many of our management team members have extensive experience working together at North Fork and have successfully executed operating business models similar to ours in the past. In addition, our management has a successful track record of growing bank franchises both organically and through acquisitions.

Risks We Face

There are a number of risks that you should consider before buying our common stock. These risks are discussed more fully in the section entitled "Risk Factors" beginning on page 13. These risks include, but are not limited to:

ability to foreclose and hence delay the collection of payments for single family residential loans under the Loss Sharing Agreements; and

Our Business

Our primary business is to offer a full range of traditional banking products and financial services coupled with high-touch, personalized customer service to both our commercial and consumer customers, who are predominantly located in Florida. We offer a full array of lending products to cater to our customers' needs, including, but not limited to, small business loans, commercial real estate loans, equipment loans, term loans, asset-backed loans, letters of credit, commercial lines of credit, residential mortgage loans, home equity and consumer loans. We also offer traditional depository products, including checking accounts, money market deposit accounts, savings accounts and certificates of deposit, repo products and cash management services. Through dedicated financial consultants and licensed bankers, BankUnited Investment Services provides comprehensive wealth management products and services, including mutual funds, annuities, life insurance, individual securities and succession, estate and financial planning services. We believe that our customers are attracted to us because we offer the resources and sophistication of a large bank as well as the responsiveness and relationship-based approach of a community bank.

Our Market Area

We view our market as the southeast region of the United States with a current focus on Florida, and in particular the Miami metropolitan statistical area, or MSA. We believe Florida represents a long-term attractive banking market. According to estimates from SNL Financial, from June 30, 2000 to June 30, 2010, Florida added 2.9 million new residents, the third most of any U.S. state, and, at June 30, 2010, had a total population of 18.9 million and a median household income of $49,910. Additionally, the state has 1.9 million active businesses. We believe Florida's population provides tremendous opportunities for us to grow our business. At June 30, 2010, BankUnited ranked 11th in deposit market share in Florida and 6th in the Miami MSA, according to SNL Financial.

Florida's economy and banking industry continue to face significant challenges. Since 2007, many Florida banks have experienced capital constraints and liquidity challenges as a result of significant losses from loans with poor credit quality and investments that have had sizeable decreases in value or realized losses. The undercapitalization and increased regulation of the banking sector have caused many banks to reduce lending to new and existing clients and focus primarily on improving their balance sheets, putting pressure on commercial borrowers to look for new banking relationships. As of September 30, 2010, 40 banks with $31.8 billion in assets have failed since 2008 in Florida. Given our competitive strengths, including an experienced management team, robust capital position and scalable platform, we believe these challenges present significant acquisition and organic growth opportunities for us.

Over time, we will look to expand our branch network outside of Florida in selected markets such as New York, where our management team has had significant experience and has the competitive advantage of having managed one of the most successful regional banks in that market. However, for a limited period of time, certain of our executive officers are subject to non-compete agreements which may restrict them from operating in New York, New Jersey and Connecticut.

Our Business Strategy

Since the Acquisition, we have focused on the financial needs of small and medium sized businesses and consumers throughout Florida. Through BankUnited, we deliver a comprehensive range

of traditional depository and lending products, online services and cash management tools for businesses. We also offer on a national basis commercial lease financing services and municipal leasing services. Through our non-bank subsidiary, BankUnited Investment Services, we offer a suite of products including mutual funds, annuities, life insurance, individual securities and other wealth management services.

Our goal is to build a premier, large regional bank in attractive growth markets, employing the following key elements:

With the changes implemented as discussed above, we have increased our core deposits (defined as total deposits less certificates of deposit, or CDs) since the Acquisition to September 30, 2010 from $2.1 billion to $3.8 billion and lowered our cost of deposits (excluding the impact of accretion from fair value adjustments due to acquisition accounting) from 3.5% to 1.6%. In addition, since the Acquisition to September 30, 2010, we have generated $429.5 million of new commercial and commercial real estate loan commitments.

Additional Information

Our principal executive offices are located at 14817 Oak Lane, Miami Lakes, Florida 33016. Our telephone number is (305) 569-2000. Our Internet address is www.bankunited.com. Information on, or accessible through, our website is not part of this prospectus.

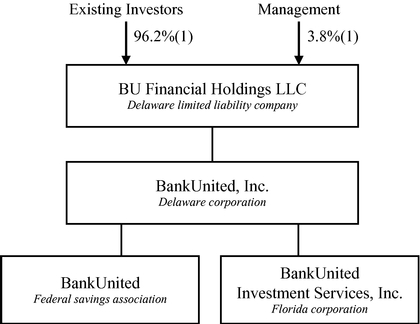

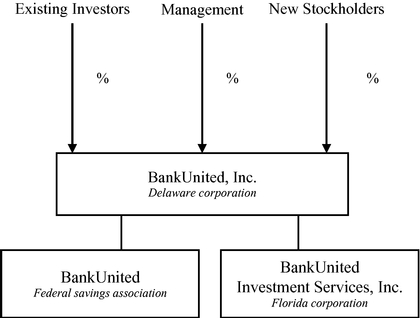

We are currently a direct, wholly-owned subsidiary of BU Financial Holdings LLC, or the LLC, a Delaware limited liability company, and whose common equity interests are referred to herein as units. Prior to the completion of this offering, we will effect a reorganization so that our investors, our named executive officers and all other members of the LLC will hold equity interests in us directly rather than indirectly through the LLC. Immediately prior to the consummation of this offering, the LLC will be liquidated and all interests in the registrant, BankUnited, Inc., a Delaware corporation, will be distributed to the members of the LLC in accordance with its amended and restated limited liability company agreement dated as of May 21, 2009, or the LLC Agreement. There are currently 36 holders of units in the LLC. All of the transactions necessary to effect the liquidation are collectively referred to herein as the "Reorganization." For additional information, see "Compensation Discussion and Analysis—Executive Officer Compensation—Equity-Based Compensation."

The Offering

Common stock offered by us | 4,000,000 shares of common stock | |

Common stock offered by the selling stockholders | 22,250,000 shares of common stock | |

Over-allotment option | 3,937,500 shares of common stock from the selling stockholders | |

Common stock to be outstanding after this offering | 96,971,850 shares of common stock | |

Use of proceeds | We estimate that the net proceeds to us from this offering after deducting estimated underwriting discounts and commissions and offering expenses will be approximately | |

Dividend policy | We initially anticipate paying a quarterly dividend of | |

New York Stock Exchange symbol | BKU | |

Risk factors | Please read the section entitled "Risk Factors" beginning on page 13 for a discussion of some of the factors you should consider before buying our common stock. |

References in this section to the number of shares of our common stock to be outstanding after this offering are based on 92,971,850 shares of our common stock outstanding and excludesas of January 10, 2011. Such references exclude:

Unless otherwise indicated, the information presented in this prospectus:

Summary Historical Consolidated Financial Data

You should read the summary historical consolidated financial information set forth below in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations," "Capitalization" and the consolidated financial statements and the related notes thereto included elsewhere in this prospectus. The summary historical consolidated financial information set forth below at and for the nine months ended September 30, 2010 is derived from our unaudited interim condensed consolidated financial statements included elsewhere in this prospectus and includes all adjustments (consisting of normal recurring adjustments) that we considered necessary for a fair presentation of the financial position and the results of operations for these periods. Operating results for the nine months ended September 30, 2010 are not necessarily indicative of the results that may be expected for the year ended December 31, 2010. The summary historical consolidated financial information set forth below at December 31, 2009 and for the period from April 28, 2009 (date of inception) to December 31, 2009 has been derived from our audited consolidated financial statements included elsewhere in this prospectus. The summary historical consolidated financial information set forth below for each of the periods from October 1, 2008 to May 21, 2009 and at and for the fiscal years ended September 30, 2008 and 2007 has been derived from the audited consolidated financial statements of the Failed Bank included elsewhere in this prospectus.

Although we were incorporated on April 28, 2009, neither we nor the Bank had any substantive operations prior to the Acquisition on May 21, 2009. Results of operations of the Company for the post-Acquisition periods are not comparable to the results of operations of the Failed Bank for the pre-Acquisition periods. Results of operations for the post-Acquisition periods reflect, among other things, the acquisition method of accounting. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Periods Presented and Factors Affecting Comparability."

| | BankUnited, Inc. | Failed Bank | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | At September 30, 2010 | | At September 30, | ||||||||||||||

| | Actual | As Adjusted(1) | At December 31, 2009 | 2008 | 2007 | ||||||||||||

| | (unaudited) | | | | | ||||||||||||

| | (dollars in thousands, except per share data) | ||||||||||||||||

Consolidated Balance Sheet Data: | |||||||||||||||||

Cash and cash equivalents | $ | 494,586 | $ | 356,215 | $ | 1,223,346 | $ | 512,885 | |||||||||

Investment securities available for sale, at fair value | 3,088,504 | 2,243,143 | 755,225 | 1,098,665 | |||||||||||||

Loans held in portfolio, net | 4,079,234 | 4,588,898 | 11,249,367 | 12,561,693 | |||||||||||||

FDIC indemnification asset | 2,723,059 | 3,279,165 | — | — | |||||||||||||

Goodwill and other intangible assets | 60,759 | 60,981 | 28,353 | 28,353 | |||||||||||||

Total assets | 11,151,301 | 11,129,961 | 14,088,591 | 15,107,310 | |||||||||||||

Deposits | 7,300,460 | 7,666,775 | 8,176,817 | 7,305,788 | |||||||||||||

Federal Home Loan Bank advances | 2,260,006 | 2,079,051 | 5,279,350 | 6,234,360 | |||||||||||||

Total liabilities | 9,908,462 | 10,035,701 | 13,689,821 | 13,904,508 | |||||||||||||

Total stockholder's equity | 1,242,839 | 1,094,260 | 398,770 | 1,202,802 | |||||||||||||

| | BankUnited, Inc. | Failed Bank | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | At September 30, 2010 | | At September 30, | ||||||||||||||

| | Actual | As Adjusted(1) | At December 31, 2009 | 2008 | 2007 | ||||||||||||

| | (unaudited) | | | | | ||||||||||||

| | (dollars in thousands, except per share data) | ||||||||||||||||

Consolidated Balance Sheet Data: | |||||||||||||||||

Cash and cash equivalents | $ | 494,586 | 580,763 | $ | 356,215 | $ | 1,223,346 | $ | 512,885 | ||||||||

Investment securities available for sale, at fair value | 3,088,504 | 3,088,504 | 2,243,143 | 755,225 | 1,098,665 | ||||||||||||

Loans held in portfolio, net | 4,079,234 | 4,079,234 | 4,588,898 | 11,249,367 | 12,561,693 | ||||||||||||

FDIC indemnification asset | 2,723,059 | 2,723,059 | 3,279,165 | — | — | ||||||||||||

Goodwill and other intangible assets | 60,759 | 60,759 | 60,981 | 28,353 | 28,353 | ||||||||||||

Total assets | 11,151,301 | 11,237,478 | 11,129,961 | 14,088,591 | 15,107,310 | ||||||||||||

Deposits | 7,300,460 | 7,300,460 | 7,666,775 | 8,176,817 | 7,305,788 | ||||||||||||

Federal Home Loan Bank advances | 2,260,006 | 2,260,006 | 2,079,051 | 5,279,350 | 6,234,360 | ||||||||||||

Total liabilities | 9,908,462 | 9,908,462 | 10,035,701 | 13,689,821 | 13,904,508 | ||||||||||||

Total stockholder's equity | 1,242,839 | 1,329,016 | 1,094,260 | 398,770 | 1,202,802 | ||||||||||||

| | BankUnited, Inc. | Failed Bank | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | Period from April 28, 2009 to December 31, 2009(2) | Period from October 1, 2008 to May 21, 2009(2) | At September 30, | |||||||||||||

| | Nine Months Ended September 30, 2010 | ||||||||||||||||

| | 2008 | 2007 | |||||||||||||||

| | (unaudited) | | | | | ||||||||||||

| | (dollars in thousands, except per share data) | ||||||||||||||||

Consolidated Income Statement Data: | |||||||||||||||||

Interest income | $ | 414,959 | $ | 335,524 | $ | 339,068 | $ | 834,460 | $ | 957,897 | |||||||

Interest expense | 127,495 | 83,856 | 333,392 | 555,594 | 604,558 | ||||||||||||

Net interest income | 287,464 | 251,668 | 5,676 | 278,866 | 353,339 | ||||||||||||

Provision for loan losses | 45,157 | 22,621 | 919,139 | 856,374 | 31,500 | ||||||||||||

Net interest income (loss) after provision for loan losses | 242,307 | 229,047 | (913,463 | ) | (577,508 | ) | 321,839 | ||||||||||

Non-interest income (loss) | 237,520 | 252,828 | (81,431 | ) | (128,859 | ) | 28,367 | ||||||||||

Non-interest expense | 220,048 | 282,454 | 238,403 | 246,480 | 185,634 | ||||||||||||

Income (loss) before income taxes | 259,779 | 199,421 | (1,233,297 | ) | (952,847 | ) | 164,572 | ||||||||||

Provision (benefit) for income before taxes | 102,857 | 80,375 | — | (94,462 | ) | 55,067 | |||||||||||

Net income (loss) | $ | 156,922 | $ | 119,046 | $ | (1,233,297 | ) | $ | (858,385 | ) | $ | 109,505 | |||||

Share Data: | |||||||||||||||||

Earnings (loss) per common share, basic and diluted | $ | 1.69 | $ | 1.29 | $ | (12,332,970 | ) | $ | (8,583,850 | ) | $ | 1,095,054 | |||||

Weighted average common shares outstanding | 92,943,620 | 92,664,910 | 100 | 100 | 100 | ||||||||||||

Other Data (unaudited): | |||||||||||||||||

Financial ratios | |||||||||||||||||

Return on average assets(3) | 1.86 | % | 1.69 | % | (14.26) | % | (5.94) | % | 0.78 | % | |||||||

Return on average common stockholder's equity(3) | 17.72 | % | 18.98 | % | (2,041.04) | % | (75.43) | % | 10.04 | % | |||||||

Yield on earning assets(3) | 7.16 | % | 7.42 | % | 3.91 | % | 5.91 | % | 6.96 | % | |||||||

Cost of interest bearing liabilities(3) | 1.82 | % | 1.39 | % | 3.94 | % | 4.36 | % | 4.91 | % | |||||||

Equity to assets ratio | 11.15 | % | 9.83 | % | (7.25) | % | 2.83 | % | 7.96 | % | |||||||

Interest rate spread(3) | 5.34 | % | 6.03 | % | (0.03) | % | 1.55 | % | 2.05 | % | |||||||

Net interest margin(3) | 4.95 | % | 5.58 | % | 0.06 | % | 1.98 | % | 2.57 | % | |||||||

Loan to deposit ratio | 56.67 | % | 60.15 | % | 128.73 | % | 146.33 | % | 172.74 | % | |||||||

Asset quality ratios | |||||||||||||||||

Non-performing loans to total loans(4)(6) | 0.68 | % | 0.38 | % | 24.58 | % | 11.98 | % | 1.59 | % | |||||||

Non-performing assets to total assets(5) | 1.99 | % | 1.24 | % | 23.53 | % | 11.13 | % | 1.51 | % | |||||||

Allowance for loan losses to total loans | 1.40 | % | 0.49 | % | 11.14 | % | 5.98 | % | 0.46 | % | |||||||

Allowance for loan losses to non-performing loans | 206.28 | % | 130.22 | % | 45.33 | % | 49.96 | % | 29.15 | % | |||||||

Net charge-offs to average loans(3) | 0.31 | % | 0.00 | % | 5.51 | % | 1.58 | % | 0.08 | % | |||||||

| | BankUnited, Inc. | Failed Bank | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | At September 30, | |||||||||||

| | At September 30, 2010 | At December 31, 2009(2) | ||||||||||||

| | 2008 | 2007 | ||||||||||||

| | (unaudited) | | | | ||||||||||

Capital ratios(7) | ||||||||||||||

Tangible common equity to tangible assets(8) | 10.66 | % | 9.33 | % | 2.63 | % | 7.79 | % | ||||||

Tier 1 common capital to total risk weighted assets | 42.46 | % | 40.42 | % | 4.90 | % | 14.64 | % | ||||||

Tier 1 risk-based capital | 42.46 | % | 40.42 | % | 4.90 | % | 14.64 | % | ||||||

Total risk-based capital | 43.27 | % | 40.55 | % | 6.21 | % | 15.37 | % | ||||||

Tier 1 leverage | 10.09 | % | 8.78 | % | 2.89 | % | 7.84 | % | ||||||

A $1.00 increase (decrease) in the assumed initial public offering price of $$24.00 per share would increase (decrease) additional cash and cash equivalents, total assets and total stockholder's equity by $$3.8 million, assuming that the number of shares offered by us, as set forth on the cover of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions and offering expenses.

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors, as well as all of the other information contained in this prospectus including our consolidated financial statements and the related notes thereto, before deciding to invest in our common stock. The occurrence of any of the following risks could materially and adversely affect our business, prospects, financial condition, results of operations and cash flow. In such case, the trading price of our common stock could decline and you could lose all or part of your investment.

Risks Related to Our Business

Failure to comply with the terms of our Loss Sharing Agreements with the FDIC may result in significant losses.

In May 2009, we purchased substantially all of the assets and assumed all of the non-brokered deposits and substantially all other liabilities of the Failed Bank in an FDIC-assisted transaction, and presently a substantial portion of BankUnited's revenue is derived from such assets. The purchased loans, commitments, foreclosed assets and certain securities are covered by the Loss Sharing Agreements with the FDIC, which provide that a significant portion of the losses related to the Covered Assets will be borne by the FDIC. Under the Loss Sharing Agreements, we are obligated to comply with certain loan servicing standards, including requirements to participate in government-sponsored loan modification programs. As these standards evolve, we may experience difficulties in complying with the requirements of the Loss Sharing Agreements, which could result in Covered Assets losing some or all of their coverage. BankUnited is subject to audits with the terms of the Loss Sharing Agreements by the FDIC through its designated agent. The required terms of the agreements are extensive and failure to comply with any of the guidelines could result in a specific asset or group of assets losing their loss sharing coverage. See "Business—The Acquisition—Loss Sharing Agreements."

The geographic concentration of our markets in the coastal regions of Florida makes our business highly susceptible to local economic conditions and natural disasters.

Unlike larger financial institutions that are more geographically diversified, our branch offices are primarily concentrated in the coastal regions of Florida. Additionally, a significant portion of our loans secured by real estate are secured by commercial and residential properties in Florida. The Florida economy and our market in particular have been affected by the downturn in commercial and residential property values, and the decline in real estate values in Florida during the downturn has been higher than the national average. Additionally, the Florida economy relies heavily on tourism and seasonal residents, which have also been affected by recent market disruptions. Continued deterioration in economic conditions in the markets we serve or the occurrence of a natural disaster, such as a hurricane, or a man-made catastrophe, such as the Gulf of Mexico oil spill, could result in one or more of the following:

Hurricanes and other catastrophes to which our markets in the coastal regions of Florida are susceptible also can disrupt our operations, result in damage to our properties, reduce or destroy the value of collateral and negatively affect the local economies in which we operate, which could have a material adverse effect on our results of operations.

A decline in existing and new real estate sales decreases lending opportunities, may delay the collection of our cash flow from the Loss Sharing Agreements, and negatively affects our income. We

do not anticipate that the real estate market will improve in the near-term and, accordingly, this could lead to additional valuation adjustments on our loan portfolios.

Delinquencies and defaults in residential mortgages have recently increased, creating a backlog in courts and an increase in the amount of legislative action that might restrict or delay our ability to foreclose and hence delay the collection of payments for single family residential loans under the Loss Sharing Agreements.

For the single family residential loans covered by the Loss Sharing Agreements, we cannot collect loss share payments until we liquidate the properties securing those loans. These loss share payments could be delayed by an extended foreclosure process, including delays resulting from a court backlog, local or national foreclosure moratoriums or other delays, and these delays could have a material adverse effect on our results of operations. Home ownerHomeowner protection laws may also delay the initiation or completion of foreclosure proceedings on specified types of residential mortgage loans. Any such limitations are likely to cause delayed or reduced collections from mortgagors. Any restriction on our ability to foreclose on a loan, any requirement that we forgo a portion of the amount otherwise due on a loan or any requirement that we modify any original loan terms could negatively impact our business, financial condition, liquidity and results of operations.

Our loan portfolio has and will continue to be affected by the ongoing correction in residential and commercial real estate prices and reduced levels of residential and commercial real estate sales.

Soft residential and commercial real estate markets, higher delinquency and default rates, and increasingly volatile and constrained secondary credit markets have affected the mortgage industry generally, and Florida in particular, which is where our business is currently most heavily concentrated. Our financial results may be adversely affected by changes in real estate values. We make credit and reserve decisions based on the current conditions of borrowers or projects combined with our expectations for the future. If the slowdown in the real estate market continues, we could experience higher charge-offs and delinquencies beyond that which is provided in the allowance for loan losses. Although we have the Loss Sharing Agreements with the FDIC, these agreements do not cover 100% of the losses attributable to Covered Assets. In addition, the Loss Sharing Agreements will not mitigate any losses on our non-Covered Assets and our earnings could be adversely affected through a higher than anticipated provision for loan losses on such assets.

Our business is highly susceptible to credit risk on our non-Covered Assets.

As a lender, we are exposed to the risk that our customers will be unable to repay their loans according to their terms and that the collateral securing the payment of their loans (if any) may not be sufficient to assure repayment. Similarly, we have credit risk embedded in our securities portfolio. Our credit standards, procedures and policies may not prevent us from incurring substantial credit losses, particularly in light of market developments in recent years. Recent economic and market developments and the potential for continued economic disruption present considerable risks to us and it is difficult to determine the depth and duration of the economic and financial market problems and the many ways in which they may impact our business in general. The Loss Sharing Agreements only cover certain legacy assets, and credit losses on assets not covered by the Loss Sharing Agreements could have a material adverse effect on our operating results.

Changes in interest rates could have an adverse impact on our results of operations and financial condition.

Our earnings and cash flows depend to a great extent upon the level of our net interest income. Changes in interest rates can increase or decrease our net interest income, because different types of assets and liabilities may react differently, and at different times, to market interest rate changes. Net interest income is the difference between the interest income we earn on loans, investments and other interest earning assets, and the interest we pay on interest bearing liabilities, such as deposits and borrowings. When interest bearing liabilities mature or reprice more quickly than interest earning assets

in a period, an increase in interest rates could reduce net interest income. Similarly, when interest earning assets mature or reprice more quickly than interest bearing liabilities, falling interest rates could reduce net interest income. Additionally, an increase in interest rates may, among other things, reduce the demand for loans and our ability to originate loans and decrease loan repayment rates. A decrease in the general level of interest rates may affect us through, among other things, increased prepayments on our loan and mortgage-backed securities portfolios and increased competition for deposits. Accordingly, changes in the level of market interest rates affect our net yield on interest earning assets, loan origination volume, loan and mortgage-backed securities portfolios, and our overall results. Interest rates are highly sensitive to many factors beyond our control, including general economic conditions and policies of various governmental and regulatory agencies, particularly the Federal Reserve.

We attempt to manage our risk from changes in market interest rates by adjusting the rates, maturity, repricing, and balances of the different types of interest-earning assets and interest bearing liabilities; however, interest rate risk management techniques are not precise, and we may not be able to successfully manage our interest rate risk. As a result, a rapid increase or decrease in interest rates could have an adverse effect on our net interest margin and results of operations.

We depend on our executive officers and key personnel to continue the implementation of our long-term business strategy and could be harmed by the loss of their services.

We believe that our continued growth and future success will depend in large part on the skills of our senior management team. We believe our senior management team possesses valuable knowledge about and experience in the banking industry and that their knowledge and relationships would be very difficult to replicate. Although our senior management team has entered into employment agreements with us, they may not complete the term of their employment agreements or renew them upon expiration. Our success also depends on the experience of our branch managers and lending officers and on their relationships with the customers and communities they serve. The loss of service of one or more of our executive officers or key personnel, or the inability to recruit and retain qualified personnel in the future, could have an adverse effect on our business, financial condition or operating results and the value of our common stock.

Our allowance for credit losses may not be adequate to cover actual credit losses.

We maintain an allowance for loan losses that represents management's estimate of probable losses inherent in our credit portfolio. This estimate requires management to make certain assumptions and involves a high degree of judgment, particularly as our originated loan portfolio is not yet seasoned and has not yet developed an observable loss trend and Covered Loans that did not exhibit evidence of deterioration in credit quality at acquisition, or non-ACI loans, have limited delinquency statistics. Management considers numerous factors, including, but not limited to, internal risk ratings, loss forecasts, collateral values, geographic location, borrower FICO scores, delinquency rates, the proportion of non-performing and restructured loans in the loan portfolio, origination channels, product mix, underwriting practices, industry conditions, economic trends and net charge-off trends.

If management's assumptions and judgments prove to be incorrect, our current allowance may be insufficient and we may be required to increase our allowance for loan losses. In addition, federal and state regulators periodically review our allowance for loan losses and may require us to increase our provision for loan losses or recognize further loan charge-offs, based on judgments different than those of our management. Continued adverse economic conditions could make management's estimate even more complex and difficult to determine. Any increase in our allowance for loan losses will result in a decrease in net income and capital and could have a material adverse effect on our financial condition and results of operations. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Analysis of the Allowance for Loan Losses" and "Management's Discussion

and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies and Estimates—Accounting for Covered Loans."

We may not be able to find suitable acquisition candidates and may be unable to manage our growth due to acquisitions.

A key component of our growth strategy is to pursue acquisitions of complementary businesses. As consolidation of the banking industry continues, the competition for suitable acquisition candidates may increase. We compete with other banking companies for acquisition opportunities and there are a limited number of candidates that meet our acquisition criteria. Consequently, we may not be able to identify suitable candidates for acquisitions. If we are unable to locate suitable acquisition candidates willing to sell on terms acceptable to us, our net income could decline and we would be required to find other methods to grow our business.

Even if suitable candidates are identified and we succeed in consummating future acquisitions, acquisitions involve risks that the acquired business may not achieve anticipated revenue, earnings or cash flows. There may also be unforeseen liabilities relating to the acquired institution or arising out of the acquisition, asset quality problems of the acquired entity, difficulty operating in markets in which we have had no or only limited experience and other conditions not within our control, such as adverse personnel relations, loss of customers because of change in identity, and deterioration in local economic conditions.

In addition, the process of integrating acquired entities will divert significant management time and resources. We may not be able to integrate successfully or operate profitably any financial institutions we may acquire. We may experience disruption and incur unexpected expenses in integrating acquisitions. Any acquisitions we do make may not enhance our cash flows, business, financial condition, results of operations or prospects and may have an adverse effect on our results of operations, particularly during periods in which the acquisitions are being integrated into our operations.

We face significant competition from other financial institutions and financial services providers, which may decrease our growth or profits.

The primary market we serve is Florida. Consumer and commercial banking in Florida is highly competitive. Our market contains not only a large number of community and regional banks, but also a significant presence of the country's largest commercial banks. We compete with other state and national financial institutions located in Florida and adjoining states as well as savings and loan associations, savings banks and credit unions for deposits and loans. In addition, we compete with financial intermediaries, such as consumer finance companies, mortgage banking companies, insurance companies, securities firms, mutual funds and several government agencies as well as major retailers, all actively engaged in providing various types of loans and other financial services.

The financial services industry could become even more competitive as a result of legislative, regulatory and technological changes and continued consolidation. Banks, securities firms and insurance companies can merge under the umbrella of a financial holding company, which can offer virtually any type of financial service, including banking, securities underwriting, insurance (both agency and underwriting) and merchant banking. Increased competition among financial services companies due to the recent consolidation of certain competing financial institutions may adversely affect our ability to market our products and services. Also, technology has lowered barriers to entry and made it possible for banks to compete in our market without a retail footprint by offering competitive rates, as well as non-banks to offer products and services traditionally provided by banks. Many of our competitors have fewer regulatory constraints and may have lower cost structures. Additionally, due to their size, many competitors may offer a broader range of products and services as well as better pricing for certain products and services than we can.

Our ability to compete successfully depends on a number of factors, including:

Failure to perform in any of these areas could significantly weaken our competitive position, which could adversely affect our growth and profitability, which, in turn, could harm our business, financial condition and results of operations.

Since we engage in lending secured by real estate and may be forced to foreclose on the collateral property and own the underlying real estate, we may be subject to the increased costs and risks associated with the ownership of real property, which could have an adverse effect on our business or results of operations.

A significant portion of our loan portfolio is secured by real property. During the ordinary course of business, we may foreclose on and take title to properties securing certain loans, in which case, we are exposed to the risks inherent in the ownership of real estate. The amount that we, as a mortgagee, may realize after a default is dependent upon factors outside of our control, including:

Certain expenditures associated with the ownership of real estate, principally real estate taxes and maintenance costs, may also adversely affect our operating expenses.

We are dependent on our information technology and telecommunications systems and third-party servicers, and systems failures, interruptions or breaches of security could have an adverse effect on our financial condition and results of operations.

Our business is highly dependent on the successful and uninterrupted functioning of our information technology and telecommunications systems and third-party servicers. We outsource our major systems including our electronic funds transfer, or EFT, transaction processing, cash management and online banking services. We rely on these systems to process new and renewal loans, gather deposits, provide customer service, facilitate collections and share data across our organization. The failure of these systems, or the termination of a third-party software license or service agreement on

which any of these systems is based, could interrupt our operations. Because our information technology and telecommunications systems interface with and depend on third-party systems, we could experience service denials if demand for such services exceeds capacity or such third-party systems fail or experience interruptions. If sustained or repeated, a system failure or service denial could result in a deterioration of our ability to process new and renewal loans, gather deposits and provide customer service, compromise our ability to operate effectively, damage our reputation, result in a loss of customer business, and/or subject us to additional regulatory scrutiny and possible financial liability, any of which could have a material adverse effect on our financial condition and results of operations.

We are currently in the process of implementing substantial changes to our core deposit platform. We may not be able to successfully implement this new core system in an effective manner. In addition, we may incur significant increases in costs and encounter extensive delays in the implementation and rollout of our new operating system. If there are technological impediments, unforeseen complications, errors or breakdowns in implementing this new core operating system or if this new core operating system does not meet the requirements of our customers, our business, financial condition, results of operations or customer perceptions may be adversely affected.

In addition, we provide our customers the ability to bank remotely, including online and over the telephone. The secure transmission of confidential information over the Internet and other remote channels is a critical element of remote banking. Our network could be vulnerable to unauthorized access, computer viruses, phishing schemes and other security breaches. We may be required to spend significant capital and other resources to protect against the threat of security breaches and computer viruses, or to alleviate problems caused by security breaches or viruses. To the extent that our activities or the activities of our customers involve the storage and transmission of confidential information, security breaches and viruses could expose us to claims, litigation and other possible liabilities. Any inability to prevent security breaches or computer viruses could also cause existing customers to lose confidence in our systems and could adversely affect our reputation and our ability to generate business.

BankUnited is a de novo bank, which could be mistaken for the Failed Bank, and this and other reputational risks could affect our results.

BankUnited was established as ade novo federal savings association in order to participate in the FDIC-assisted acquisition of the Failed Bank. There is a reputational risk in being incorrectly associated with the Failed Bank. Our ability to originate and maintain accounts is highly dependent upon consumer and other external perceptions of our business practices and/or our financial health. Adverse perceptions regarding our business practices and/or our financial health could damage our reputation in both the customer and funding markets, leading to difficulties in generating and maintaining accounts as well as in financing them. Adverse developments with respect to the consumer or other external perceptions regarding the practices of our competitors, or our industry as a whole, may also adversely impact our reputation. In addition, adverse reputational impacts on third parties with whom we have important relationships may also adversely impact our reputation. Adverse reputational impacts or events may also increase our litigation risk. We carefully monitor internal and external developments for areas of potential reputational risk and have established governance structures to assist in evaluating such risks in our business practices and decisions.

Three material weaknesses were identified in the first audit period following the Acquisition. Existing or future material weaknesses in our internal controls, if not properly corrected, could result in material misstatements in our financial statements.

We are not yet required to comply with Section 404 of the Sarbanes-Oxley Act of 2002, or to make an assessment of the effectiveness of our internal control over financial reporting under the Sarbanes-Oxley Act of 2002. Furthermore, our independent auditors have not been engaged to express, nor have they expressed, an opinion on the effectiveness of our internal control over financial reporting in

accordance with Sarbanes-Oxley Act of 2002. However, in connection with the audit of our consolidated financial statements for the period from May 22, 2009 through December 31, 2009, which we refer to as the period ended or ending December 31, 2009, we identified three material weaknesses in our system of internal control over financial reporting. A material weakness is a deficiency, or combination of deficiencies in internal controls over financial reporting, that results in a reasonable possibility that a material misstatement of our annual or interim financial statements will not be prevented or detected on a timely basis.

The first material weakness identified relates to the fact that management did not design effective controls over its loan modeling process in order to account for certain loans in accordance with the requirements of Accounting Standards Codification, or ASC, Subtopic 310-30,Loans and Debt Securities Acquired with Deteriorated Credit Quality. A material weakness existed due to the fact that the design of internal control did not provide for an independent review or approval and validation of the loan cash flow model and related assumptions. In addition, the design of internal control over the loan cash flow model did not provide for adequate access, change management, and end-user computing controls including spreadsheets. Furthermore, management's controls were not designed to reflect on a timely basis the impact of changes in market conditions on the loan cash flow model and related assumptions. The second material weakness relates to the fact that management did not maintain effective internal controls over the valuation and resulting writedown to fair market value of OREO properties. Specifically, a material weakness existed due to the fact that the control over the timely recording of OREO values by the Collateral Valuation Department in the Company's sub-ledger system was not operating effectively. The third material weakness relates to the fact that BankUnited did not design effective controls over its financial reporting process in order to ascertain the complete, accurate, and timely preparation of its consolidated financial statements, including the applicable disclosures and footnotes, or design effective review controls to provide for proper accounting of nonroutine transactions. A material weakness existed due to the fact that the design of internal control did not provide for a comprehensive review of interim financial information and the consolidated financial statements to ensure the completeness and accuracy of information supporting various financial statement components.

Steps we are taking to address the identified material weaknesses may not be sufficient to remediate the identified material weaknesses or prevent additional material weaknesses from occurring. If we fail to remediate the material weaknesses or if additional material weaknesses are discovered in the future, we may fail to meet our future reporting obligations and our financial statements may contain material misstatements. Any such failure could also adversely affect the results of the periodic management evaluations and annual auditor attestation reports regarding the effectiveness of our internal controls over financial reporting, and could negatively impact our business, results of operations and reputation.

BankUnited Investment Services offers third-party products including mutual funds, annuities, life insurance, individual securities and other wealth management services which could experience significant declines in value subjecting us to reputational damage and litigation risk.

Through our subsidiary BankUnited Investment Services, we offer third-party products including mutual funds, annuities, life insurance, individual securities and other wealth management products and services. If these products do not generate competitive risk-adjusted returns that satisfy clients in a variety of asset classes, we will have difficulty maintaining existing business and attracting new business. Additionally, our investment services businesses involve the risk that clients or others may sue us, claiming that we have failed to perform under a contract or otherwise failed to carry out a duty owed to them. Our investment services businesses are particularly subject to this risk and this risk may be heightened during periods when credit, equity or other financial markets are deteriorating in value or are particularly volatile, or when clients or investors are experiencing losses. Significant declines in the performance of these third-party products could subject us to reputational damage and litigation risk.

Risks Relating to the Regulation of Our Industry

The enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 may have a material effect on our operations.

On July 21, 2010, President Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, or the Dodd-Frank Act, which imposes significant regulatory and compliance changes. The key effects of the Dodd-Frank Act on our business are:

The changes resulting from the Dodd-Frank Act may impact the profitability of our business activities, require changes to certain of our business practices, impose upon us more stringent capital, liquidity and leverage requirements or otherwise adversely affect our business. These changes may also require us to invest significant management attention and resources to evaluate and make any changes necessary to comply with new statutory and regulatory requirements. Failure to comply with the new requirements or with any future changes in laws or regulations may negatively impact our results of operations and financial condition. For a more detailed description of the Dodd-Frank Act, see "Regulation and Supervision—The Dodd-Frank Act."

We operate in a highly regulated environment and the laws and regulations that govern our operations, corporate governance, executive compensation and accounting principles, or changes in them, or our failure to comply with them, may adversely affect us.

We are subject to extensive regulation, supervision, and legislation that govern almost all aspects of our operations. Intended to protect customers, depositors and deposit insurance funds, these laws and regulations, among other matters, prescribe minimum capital requirements, impose limitations on the business activities in which we can engage, limit the dividend or distributions that BankUnited can pay to us, restrict the ability of institutions to guarantee our debt, and impose certain specific accounting requirements on us that may be more restrictive and may result in greater or earlier charges to earnings or reductions in our capital than generally accepted accounting principles. Compliance with laws and regulations can be difficult and costly, and changes to laws and regulations often impose additional compliance costs. Our failure to comply with these laws and regulations, even if the failure follows good faith effort or reflects a difference in interpretation, could subject us to restrictions on our business activities, fines and other penalties, any of which could adversely affect our results of operations, capital base and the price of our securities. Further, any new laws, rules and regulations could make compliance more difficult or expensive or otherwise adversely affect our business and financial condition.

In addition, as a public company, we will incur significant legal, accounting, insurance and other expenses. Compliance with other rules of the United States Securities and Exchange Commission, or the SEC, and the rules of the stock exchange on which our common stock is listed will increase our legal and financial compliance costs and make some activities more time consuming and costly.

The FDIC's restoration plan and the related increased assessment rate could adversely affect our earnings.

Market developments have significantly depleted the deposit insurance fund, or DIF, of the FDIC and reduced the ratio of reserves to insured deposits. As a result of recent economic conditions and the enactment of the Dodd-Frank Act, the FDIC has increased the deposit insurance assessment rates and thus raised deposit premiums for insured depository institutions. If these increases are insufficient for the DIF to meet its funding requirements, further special assessments or increases in deposit insurance premiums may be required. We are generally unable to control the amount of premiums that we are required to pay for FDIC insurance. If there are additional bank or financial institution failures, we may be required to pay even higher FDIC premiums than the recently increased levels. Any future additional assessments, increases or required prepayments in FDIC insurance premiums may materially adversely affect results of operations.

Federal banking agencies periodically conduct examinations of our business, including compliance with laws and regulations, and our failure to comply with any supervisory actions to which we are or become subject as a result of such examinations may adversely affect us.

Federal banking agencies, including the Office of Thrift Supervision, or OTS, periodically conduct examinations of our business, including compliance with laws and regulations. If, as a result of an examination, a federal banking agency were to determine that the financial condition, capital resources, asset quality, earnings prospects, management, liquidity or other aspects of any of our operations had become unsatisfactory, or that the Company or its management was in violation of any law or regulation, it may take a number of different remedial actions as it deems appropriate. These actions include the power to enjoin "unsafe or unsound" practices, to require affirmative actions to correct any conditions resulting from any violation or practice, to issue an administrative order that can be judicially enforced, to direct an increase in BankUnited's capital, to restrict our growth, to assess civil monetary penalties against our officers or directors, to remove officers and directors and, if it is concluded that such conditions cannot be corrected or there is an imminent risk of loss to depositors, to terminate BankUnited's deposit insurance. If we become subject to such regulatory actions, our business, results of operations and reputation may be negatively impacted.

Many of our new activities and expansion plans require regulatory approvals, and failure to obtain them may restrict our growth.

We intend to complement and expand our business by pursuing strategic acquisitions of banks and other financial institutions. We must generally receive federal regulatory approval before we can acquire an institution or business. In determining whether to approve a proposed acquisition, federal bank regulators will consider, among other factors, the effect of the acquisition on the competition, our financial condition, and our future prospects. The regulators also review current and projected capital ratios and levels, the competence, experience, and integrity of management and its record of compliance with laws and regulations, the convenience and needs of the communities to be served (including the acquiring institution's record of compliance under the Community Reinvestment Act, or CRA) and the effectiveness of the acquiring institution in combating money laundering activities. Such regulatory approvals may not be granted on terms that are acceptable to us, or at all. We may also be required to sell branches as a condition to receiving regulatory approval, which condition may not be acceptable to us or, if acceptable to us, may reduce the benefit of any acquisition.

In addition to the acquisition of existing financial institutions, as opportunities arise, we plan to continuede novo branching as a part of our internal growth strategy and possibly enter into new markets throughde novo branching.De novo branching and any acquisition carries with it numerous risks, including the inability to obtain all required regulatory approvals. The failure to obtain these regulatory approvals for potential future strategic acquisitions andde novo branches may impact our business plans and restrict our growth.

Financial institutions, such as BankUnited, face a risk of noncompliance and enforcement action with the Bank Secrecy Act and other anti-money laundering statutes and regulations.

The federal Bank Secrecy Act, the USA PATRIOT Act, and other laws and regulations require financial institutions, among other duties, to institute and maintain an effective anti-money laundering program and file suspicious activity and currency transaction reports as appropriate. The federal Financial Crimes Enforcement Network, established by the U.S. Treasury Department to administer the Bank Secrecy Act, is authorized to impose significant civil money penalties for violations of those requirements, and has recently engaged in coordinated enforcement efforts with the individual federal banking regulators, as well as the U.S. Department of Justice, Drug Enforcement Administration, and Internal Revenue Service. There is also increased scrutiny of compliance with the rules enforced by the Office of Foreign Assets Control.

In order to comply with regulations, guidelines and examination procedures in this area, we have enhanced our anti-money laundering program by adopting new policies and procedures and selecting a new, robust automated anti-money laundering software solution that is scheduled to be implemented in early 2011. If our policies, procedures and systems are deemed deficient or the policies, procedures and systems of the financial institutions that we have already acquired or may acquire in the future are deficient, we would be subject to liability, including fines and regulatory actions such as restrictions on our ability to pay dividends and the necessity to obtain regulatory approvals to proceed with certain aspects of our business plan, including our acquisition plans.

We are subject to the CRA and fair lending laws, and failure to comply with these laws could lead to material penalties.

The CRA, the Equal Credit Opportunity Act, the Fair Housing Act and other fair lending laws and regulations impose nondiscriminatory lending requirements on financial institutions. The Department of Justice and other federal agencies are responsible for enforcing these laws and regulations. A successful challenge to an institution's performance under the CRA or fair lending laws and regulations could result in a wide variety of sanctions, including the required payment of damages and civil money penalties, injunctive relief, imposition of restrictions on mergers and acquisitions activity, and restrictions on expansion activity. Private parties may also have the ability to challenge an institution's performance under fair lending laws in private class action litigation.

Risks Related to this Offering and Ownership of Our Common Stock

There is no prior public market for our common stock and one may not develop.

Prior to this offering, there has not been a public trading market for our common stock. An active trading market may not develop or be sustained after this offering. If an active trading market does not develop, you may have difficulty selling your shares of common stock at an attractive price, or at all. The initial public offering price for our common stock sold in this offering will be determined by negotiations among us, the selling stockholders and the underwriters. This price may not be indicative of the price at which our common stock will trade after this offering. The market price of our common stock may decline below the initial offering price, and you may not be able to sell your common stock at or above the price you paid in this offering, or at all.

Our stock price may be volatile, and you could lose all or part of your investment as a result.

You should consider an investment in our common stock to be risky, and you should invest in our common stock only if you can withstand a significant loss and wide fluctuation in the market value of your investment. The market price of our common stock could be subject to wide fluctuations in

response to, among other things, the factors described in this "Risk Factors" section, and other factors, some of which are beyond our control. These factors include:

Furthermore, the stock markets have experienced price and volume fluctuations that have affected and continue to affect the market price of equity securities of many companies. These fluctuations have often been unrelated or disproportionate to the operating performance of these companies. These broad market fluctuations, as well as general economic, systemic, political and market conditions, such as recessions, loss of investor confidence, interest rate changes, or international currency fluctuations, may negatively affect the market price of our common stock.