As filed with the Securities and Exchange Commission on [ ], 2012

Registration No. 333-183246

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment Number FORM S-1 | ||

| REGISTRATION STATEMENT | ||

| UNDER | ||

THE SECURITIES ACT OF 1933

|

STERLING CONSOLIDATED CORP.

(Exact Name of Registrant in its Charter)

| Nevada | 3050 | 45-1840913 | ||

| (State or other Jurisdiction of Incorporation) | (Primary Standard Industrial Classification Code) | (IRS Employer Identification No.) |

STERLING CONSOLIDATED CORP.

1105 Green Grove Road

Neptune, New Jersey 07753

Tel.: 732-918-8004

(Address and Telephone Number of Registrant’s Principal

Executive Offices and Principal Place of Business)

Copies of communications to:

Gregg E. Jaclin, Esq.

Anslow & Jaclin, LLP

195 Route 9 South, Suite204

Manalapan, NJ 07726

Tel. No.: (732) 409-1212

Fax No.: (732) 577-1188

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box.x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, please check the following box and list the Securities Act registration Statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |

| Non-accelerated filer | ¨ | Smaller reporting company | x |

CALCULATION OF REGISTRATION FEE

| Title of Each Class Of Securities to be Registered | Amount to be Registered | Proposed Maximum Aggregate Offering Price per share | Proposed Maximum Aggregate Offering Price | Amount of Registration fee | ||||||||||||

| Common Stock, $0.001 par value per share | 2,236,873 | (1) | $ | 0.30 | (2) | $ | 671,061.90 | (2) | $ | 91.54 | (2) | |||||

(1) This Registration Statement covers the resale by our selling shareholders of i) 797,373 shares sold to investors in our private offering pursuant to Regulation D Rule 506 completed in July 2012 at an offering price of $0.30 per share, ii)720,000shares issued to Lawrence Adams and an additional 559,500 shares to 17 other founders of Oceanview Acquisition Corp. iii) 150,000 shares issued to Delaney Equity Group for consulting services, and iv) 10,000 shares issued to Anslow & Jaclin, LLP for services rendered.

(2) The offering price has been estimated solely for the purpose of computing the amount of the registration fee in accordance with Rule 457(o). Our common stock is not traded on any national exchange and in accordance with Rule 457; the offering price was determined by the price of the shares that were sold to our shareholders in a private placement memorandum. The price of $0.30 is a fixed price at which the selling security holders may sell their shares until our common stock is quoted on the OTCBB at which time the shares may be sold at prevailing market prices or privately negotiated prices. There can be no assurance that a market maker will agree to file the necessary documents with the Financial Industry Regulatory Authority, which operates the OTC Bulletin Board, nor can there be any assurance that such an application for quotation will be approved.

THE REGISTRANT HEREBY AMENDS THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL THE REGISTRANT SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(a) OF THE SECURITIES ACT OR UNTIL THE REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE COMMISSION, ACTING PURSUANT TO SUCH SECTION 8(a), MAY DETERMINE.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the U.S. Securities and Exchange Commission (“SEC”) is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS

Subject to completion, dated __________, 2012

STERLING CONSOLIDATED CORP.

2,236,873SHARES OFCOMMON STOCK

The selling security holders named in this prospectus are offering all of the shares of common stock offered through this prospectus. We will not receive any proceeds from the sale of the common stock covered by this prospectus.

Our common stock is presently not traded on any market or securities exchange. The selling security holders have not engaged any underwriter in connection with the sale of their shares of common stock. Common stock being registered in this registration statement may be sold by selling security holders at a fixed price of $0.30 per share until our common stock is quoted on the OTC Bulletin Board (“OTCBB”) and thereafter at a prevailing market prices or privately negotiated prices or in transactions that are not in the public market. There can be no assurance that a market maker will agree to file the necessary documents with the Financial Industry Regulatory Authority (“FINRA”), which operates the OTCBB, nor can there be any assurance that such an application for quotation will be approved. We have agreed to bear the expenses relating to the registration of the shares of the selling security holders.

We are an “emerging growth company” as defined under the federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements. Investing in our common stock involves risks. See “Risk Factors” beginning on page 3 to read about factors you should consider before buying shares of our common stock.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

The Date of This Prospectus is: __________, 2012

TABLE OF CONTENTS

| PAGE | |

| Prospectus Summary | 1 |

| Risk Factors | 3 |

| Use of Proceeds | 12 |

| Determination of Offering Price | 13 |

| Dilution | 13 |

| Selling Shareholders | 13 |

| Plan of Distribution | 16 |

| Description of Securities to be Registered | 16 |

| Interests of Named Experts and Counsel | 17 |

| Description of Business | 18 |

| Description of Property | 21 |

| Legal Proceedings | 22 |

| Market for Common Equity and Related Stockholder Matters | 22 |

| Index to Financial Statements | F-1 |

| Management Discussion and Analysis of Financial Condition and Financial Results | 23 |

| Plan of Operations | 23 |

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 29 |

| Directors, Executive Officers, Promoters and Control Persons | 29 |

| Executive Compensation | 32 |

| Security Ownership of Certain Beneficial Owners and Management | 33 |

| Transactions with Related Persons, Promoters and Certain Control Persons | 33 |

ITEM 3. Summary Information, Risk Factors and Ratio of Earnings to Fixed Charges

PROSPECTUS SUMMARY

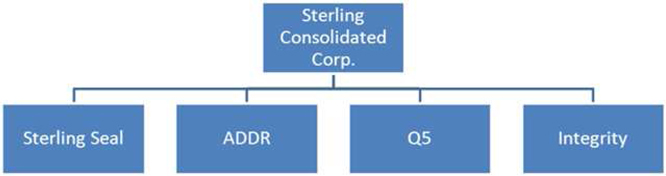

This summary highlights selected information contained elsewhere in this prospectus. This summary does not contain all the information that you should consider before investing in the common stock. You should carefully read the entire prospectus, including “Risk Factors”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the Financial Statements, before making an investment decision. In this Prospectus, the terms “Sterling Consolidated,” the “Company,” “we,” “us” and “our” refer to Sterling Consolidated Corp. Sterling Seal refers to our wholly-owned subsidiary Sterling Seal & Supply, Inc., a New Jersey corporation. ADDR refers to our wholly-owned subsidiary ADDR Properties, LLC. Q5 refers to our wholly-owned subsidiary Q5 Ventures, LLC.

Overview

We were incorporated in the State of Nevada as Oceanview Acquisition Corp. on January 31, 2011. On May 18, 2012, we amended our Articles of Incorporation to change our name to Sterling Consolidated Corp.

Our largest subsidiary is Sterling Seal & Supply, Inc. (“Sterling Seal”), a New Jersey corporation which was incorporated in 1997. Its predecessor was Sterling Plastic & Rubber Products, Inc., incorporated in New Jersey and was founded in 1970. Sterling Seal engages primarily in the distribution and sale of O-rings, rubber seals, oil seals, custom molded rubber parts, custom Teflon parts, Teflon rods, O-ring cord, bonded seals, O-ring kits, and stuffing box sealant.

We also own real property through our subsidiaries ADDR Properties, LLC (“ADDR”) and Q5 Ventures, LLC (“Q5”). ADDR owns a 28,000 square foot facility in Neptune, New Jersey, that is primarily used by Sterling Seal for its operations. ADDR also owns another property in Cliffwood Beach, New Jersey, that was previously occupied by Sterling Seal and is now rented out to tenants. Q5 owns a 5,000 square foot facility that is used by Sterling Seal in Florida.

In addition, our subsidiary Integrity Cargo Freight Corporation (“Integrity”) is a freight forwarding business. Integrity shares a facility with Sterling Seal and manages the importation of Sterling Seal’s products and exports products on behalf of Sterling Seal to various countries.

Risk Factors

Our ability to successfully operate our business and achieve our goals and strategies is subject to numerous risks as discussed in the section titled “Risk Factors,” beginning on page 3.

| 1 |

Emerging Growth Company Status

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act of 1933, or the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As such, we are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a non-binding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We have decided to take advantage of these exemptions. As a result, some investors may find our common stock less attractive as a result. The result may be a less active trading market for our common stock and our stock price may be more volatile.

In addition, Section 107 of the JOBS Act also provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an “emerging growth company” can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We intend to take advantage of the benefits of this extended transition period.

We could remain an “emerging growth company” for up to five years, or until the earliest of (a) the last day of the first fiscal year in which our annual gross revenues exceed $1 billion, (b) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, or (c) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three-year period.

Where You Can Find Us

Our principal executive office is located at 1105 Green Grove Road, Neptune, NJ 07753 and our telephone number is (732) 918-8004.

The Offering

| Common stock offered by selling security holders | 2,236,873 shares of common stock. This number represents | |

| Common stock outstanding before the offering | 37,074,040 | |

| Common stock outstanding after the offering | 37,074,040 shares of common stock as of January 16, 2013. | |

| Terms of the Offering | The selling security holders will determine when and how they will sell the common stock offered in this prospectus. | |

| Termination of the Offering | The offering will conclude upon the earliest of (i) such time as all of the common stock has been sold pursuant to the registration statement or (ii) such time as all of the common stock becomes eligible for resale without volume limitations pursuant to Rule 144 under the Securities Act, or any other rule of similar effect. | |

| Use of proceeds | We are not selling any shares of the common stock covered by this prospectus. | |

| Risk Factors | The Common Stock offered hereby involves a high degree of risk and should not be purchased by investors who cannot afford the loss of their entire investment. See “Risk Factors” beginning on page 3. |

(1) Based on 36,957,37337,074,040 shares of common stock outstanding as of January 16, 2013.

RISK FACTORS

The shares of our common stock being offered for resale by the selling security holders are highly speculative in nature, involve a high degree of risk and should be purchased only by persons who can afford to lose the entire amount invested in the common stock. Before purchasing any of the shares of common stock, you should carefully consider the following factors relating to our business and prospects. If any of the following risks actually occurs, our business, financial condition or operating results could be materially adversely affected. In such case, you may lose all or part of your investment. You should carefully consider the risks described below and the other information in this process before investing in our common stock.

Risks Related to Our Business and Industry

THE PRICES WE PAY AND CHARGE FOR THE PRODUCTS THAT WE SUPPLY, AND THE AVAILABILITY OF SUCH PRODUCTS GENERALLY, MAY FLUCTUATE DUE TO A NUMBER OF FACTORS BEYOND OUR CONTROL.

We purchase large quantities of O-rings and other rubber seals from our suppliers for distribution to our customers. At times pricing and availability of these products change depending on many factors outside of our control, such as general global economic conditions, competition, consolidation of seal producers, cost and availability of raw materials necessary to produce rubber and other materials found in the products we carry, production levels, labor costs, freight and shipping costs, natural disasters, political instability, import duties, tariffs and other trade restrictions, currency fluctuations and surcharges imposed by our suppliers.

We seek to maintain our profit margins by attempting to increase the prices we charge for the products we supply in response to increases in the prices we pay for them. However, demand for the products we supply, the actions of our competitors, our contracts with certain of our customers and other factors largely out of our control will influence whether, and to what extent, we can pass any such cost increases and surcharges on to our customers. If we are unable to pass on higher costs and surcharges to our customers, or if we are unable to do so in a timely manner, our business, financial condition, results of operations and liquidity could be materially and adversely affected.

Alternatively, if the price of the raw materials decreases significantly or if demand for the products we supply decreases because of increased customer, manufacturer or distributor inventory levels of O-rings and other seals, we may be required to reduce the prices we charge for the products we supply to remain competitive. These factors may affect our gross profit and cash flow and may also require us to write-down the value of inventory on hand that we purchased prior to the steel price decreases, which could materially and adversely affect our business, financial condition, results of operations and liquidity.

Our business could also be negatively impacted by the importation of lower-cost seals into the U.S. market. An increase in the level of imported lower-cost products could adversely affect our business to the extent that we then have higher-cost products in inventory or if prices and margins are driven down by increased supplies of such products. These events could also have a material adverse effect on our profit margins and results of operations.

In addition, the domestic and international O-ring industry has experienced consolidation in recent years. Further consolidation could result in a decrease in the number of our major suppliers or a decrease in the number of alternative supply sources available to us, which could make it more likely that termination of one or more of our relationships with major suppliers would result in a material adverse effect on our business, financial condition, results of operations or cash flows. Consolidation could also result in price increases for the products that we purchase. Such price increases could have a material adverse effect on our business, financial condition, results of operations or cash flows if we were not able to pass these price increases on to our customers.

WE MAY EXPERIENCE UNEXPECTED SUPPLY SHORTAGES.

We supply products from a wide variety of vendors and suppliers. In the future we may have difficulty obtaining the products we need from suppliers and manufacturers as a result of unexpected demand or production difficulties. Also, products may not be available to us in quantities sufficient to meet customer demand. Failure to fulfill customer orders in a timely manner could have an adverse effect on our relationships with these customers. Our inability to obtain products from suppliers and manufacturers in sufficient quantities to meet demand could have a material adverse effect on our business, results of operations and financial condition.

WE MAINTAIN AN INVENTORY OF PRODUCTS FOR WHICH WE DO NOT HAVE FIRM CUSTOMER ORDERS. AS A RESULT, IF PRICES OR SALES VOLUMES DECLINE, OUR PROFIT MARGINS AND RESULTS OF OPERATIONS COULD BE ADVERSELY AFFECTED.

Our profitability, margins and cash flows may be negatively affected if we are unable to sell our inventory in a timely manner. Because we maintain substantial inventories of specialty seal products for which we do not have firm customer orders, there is a risk that we will be unable to sell our existing inventory at the volumes and prices we expect.

OUR BUSINESS IS SENSITIVE TO ECONOMIC DOWNTURNS AND ADVERSE CREDIT MARKET CONDITIONS, WHICH COULD ADVERSELY AFFECT OUR BUSINESS, FINANCIAL CONDITION, RESULTS OF OPERATIONS AND LIQUIDITY.

Aspects of our business, including demand for and availability of the products we supply, are dependent on, among other things, the state of the global economy and adverse conditions in the global credit markets. Our business has been affected in the past and may be affected in the future by the following:

| · | our customers reducing or eliminating capital expenditures as a result of reduced demand from their customers; |

| · | our customers not being able to obtain sufficient funding at a reasonable cost or at all as a result of tightening credit markets, which may result in delayed or cancelled projects or maintenance expenditures; |

| · | our customers not being able to pay us in a timely manner, or at all, as a result of declines in their cash flows or available credit; |

| · | experiencing supply shortages for certain products if our suppliers reduce production as a result of reduced demand for their products or as a result of limitations on their ability to access credit for their operations; |

| · | experiencing tighter credit terms from our suppliers, which could increase our working capital needs and potentially reduce our liquidity; and |

| · | the value of our inventory declining if the sales prices we are able to charge our customers decline. |

As a result of these and other effects, economic downturns such as the one we recently experienced have, and could in the future, materially and adversely affect our business, financial condition, results of operations and liquidity.

In addition, market disruptions, such as the recent global economic recession, could adversely affect the creditworthiness of lenders under our debt facilities. Any reduced credit availability under our credit facilities could require us to seek other forms of liquidity through financing in the future and the availability of such financing will depend on market conditions prevailing at that time.

WE RELY ON OUR SUPPLIERS TO MEET THE REQUIRED SPECIFICATIONS FOR THE PRODUCTS WE PURCHASE FROM THEM, AND WE MAY HAVE UNREIMBURSED LOSSES ARISING FROM OUR SUPPLIERS’ FAILURE TO MEET SUCH SPECIFICATIONS.

We rely on our suppliers to provide mill certifications that attest to the specifications and physical and chemical properties of the seals that we purchase from them for resale. We generally do not undertake independent testing of any such seals but rely on our customers or assigned third-party inspection services to notify us of any products that do not conform to the specifications certified by the manufacturers. We may be subject to customer claims and other damages if products purchased from our suppliers are deemed to not meet customer specifications. These damages could exceed any amounts that we are able to recover from our suppliers or under our insurance policies. Failure to provide products that meet our customer’s specifications would adversely affect our relationship with such customer, which could negatively impact our business and results of operations.

| 4 |

LOSS OF KEY SUPPLIERS COULD DECREASE OUR SALES VOLUMES AND OVERALL PROFITABILITY.

For the year ended December 31, 2011, our ten largest suppliers accounted for approximately 54% of our purchases and our single largest supplier accounted for approximately 14% of our purchases. Consistent with industry practice, we do not have long-term contracts with any of our suppliers. Therefore, all of our suppliers have the ability to terminate their relationships with us or reduce their planned allocations of product to us at any time. The loss of any of these suppliers due to merger or acquisition, business failure, bankruptcy or other reason could put us at a competitive disadvantage by decreasing the availability or increasing the prices, or both, of products we supply, which in turn could result in a decrease in our sales volumes and overall profitability.

LOSS OF THIRD-PARTY TRANSPORTATION PROVIDERS UPON WHICH WE DEPEND, FAILURE OF SUCH THIRD-PARTY TRANSPORTATION PROVIDERS TO DELIVER HIGH QUALITY SERVICE OR CONDITIONS NEGATIVELY AFFECTING THE TRANSPORTATION INDUSTRY COULD INCREASE OUR COSTS AND DISRUPT OUR OPERATIONS.

We depend upon third-party transportation providers for delivery of products to our customers. Shortages of transportation vessels, transportation disruptions or other adverse conditions in the transportation industry due to shortages of truck drivers, strikes, slowdowns, piracy, terrorism, disruptions in rail service, closures of shipping routes, unavailability of ports and port service for other reasons, increases in fuel prices and adverse weather conditions could increase our costs and disrupt our operations and our ability to deliver products to our customers on a timely basis. We cannot predict whether or to what extent any of these factors would affect our costs or otherwise harm our business. In addition, the failure of our third-party transportation providers to provide high quality customer service when delivering product to our customers would adversely affect our reputation and our relationship with our customers and could negatively impact our business and results of operations.

SIGNIFICANT COMPETITION FROM A NUMBER OF COMPANIES COULD REDUCE OUR MARKET SHARE AND HAVE AN ADVERSE EFFECT ON OUR SELLING PRICES, SALES VOLUMES AND RESULTS OF OPERATIONS.

We operate in a highly competitive industry and compete against a number of other market participants, some of which have significantly greater financial, technological and marketing resources than we do. We compete primarily on the basis of pricing, availability of specialty products and customer service. We may be unable to compete successfully with respect to these or other competitive factors. If we fail to compete effectively, we could lose market share to our competitors. Moreover, our competitors’ actions could have an adverse effect on our selling prices and sales volume. To compete for customers, we may elect to lower selling prices or offer increased services at a higher cost to us, each of which could reduce our sales, margins and earnings. There can be no assurance that we will be able to compete successfully in the future, and our failure to do so could adversely affect our business, results of operations and financial condition.

THE DEVELOPMENT OF ALTERNATIVES TO SEAL PRODUCT DISTRIBUTORS IN THE SUPPLY CHAIN IN THE INDUSTRIES IN WHICH WE OPERATE COULD CAUSE A DECREASE IN OUR SALES AND RESULTS OF OPERATIONS AND LIMIT OUR ABILITY TO GROW OUR BUSINESS.

If our customers were to acquire or develop the capability and desire to purchase products directly from our suppliers in a competitive fashion, it would likely reduce our sales volume and overall profitability. Our suppliers also could expand their own local sales forces, marketing capabilities and inventory stocking capabilities and sell more products directly to our customers. Likewise, customers could purchase from our suppliers directly in situations where large orders are being placed and where inventory and logistics support planning are not necessary in connection with the delivery of the products. These and other actions that remove us from, limit our role in, or reduce the value that our services provide in the distribution chain could materially and adversely affect our business, financial condition and results of operations.

CHANGES IN THE PAYMENT TERMS WE RECEIVE FROM OUR SUPPLIERS COULD HAVE A MATERIAL ADVERSE EFFECT ON OUR LIQUIDITY.

The payment terms we receive from our suppliers are dependent on several factors, including, but not limited to, our payment history with the supplier, the supplier’s credit granting policies, contractual provisions, our credit profile, industry conditions, global economic conditions, our recent operating results, financial position and cash flows and the supplier’s ability to obtain credit insurance on amounts that we owe them. Adverse changes in any of these factors, many of which may not be wholly in our control, may induce our suppliers to shorten the payment terms of their invoices. Given the large amounts and volume of our purchases from suppliers, a change in payment terms may have a material adverse effect on our liquidity and our ability to make payments to our suppliers, and consequently may have a material adverse effect on our business, results of operations and financial condition.

WE ARE A HOLDING COMPANY WITH NO REVENUE GENERATING OPERATIONS OF OUR OWN. WE DEPEND ON THE PERFORMANCE OF OUR SUBSIDIARIES AND THEIR ABILITY TO MAKE DISTRIBUTIONS TO US.

We are a holding company with no business operations, sources of income or assets of our own other than our ownership interests in our subsidiaries. Because all of our operations are conducted by our subsidiaries, our cash flow and our ability to repay debt that we currently have and that we may incur after this offering and our ability to pay dividends to our stockholders are dependent upon cash dividends and distributions or other transfers from our subsidiaries.

Our subsidiaries are separate and distinct legal entities. Any right that we have to receive any assets of or distributions from any of our subsidiaries upon the bankruptcy, dissolution, liquidation or reorganization of any such subsidiary, or to realize proceeds from the sale of their assets, will be junior to the claims of that subsidiary’s creditors, including trade creditors and holders of debt issued by that subsidiary.

WE RELY UPON SEVERAL MAJOR CUSTOMERS; THE LOSS OF ANY OF THE MAIN CUSTOMERS WILL ADVERSELY AFFECT OUR BUSINESS PERFORMANCE.

We rely upon our major customers for a substantial portion of our sales. For the fiscal year ended December 31, 2011, our five (5) largest customers accounted for approximately 25% of the sales of Sterling Seal, our largest subsidiary. We have not entered into formal agreements with these customers. Loss of any of these customers could adversely affect our business performance and profitability.

Shortages or interruptions in the supply or delivery of our products could adversely affect our operating results.

We are dependent on frequent deliveries of products that meet our specifications. Shortages or interruptions in the supply of products caused by unanticipated demand, problems in production or distribution, inclement weather or other conditions could adversely affect the availability, quality and cost of supplies, which would adversely affect our operating results.

FAILURE TO COMPLY WITH THE LAWS ADMINISTERED BY THE U.S. FEDERAL MARITIME COMMISSION COULD SUBJECT US TO PENALTIES AND OTHER ADVERSE CONSEQUENCES.

Integrity Cargo is regulated by the Federal Maritime Commission. The Federal Maritime Commission (FMC) is an independent regulatory agency responsible for the regulation of ocean-borne transportation in the foreign commerce of the U.S. The principal statutes or statutory provisions administered by the Commission are: the Shipping Act of 1984, the Foreign Shipping Practices Act of 1988, section 19 of the Merchant Marine Act, 1920, and Public Law 89-777. Failure to comply with these laws could subject us to penalties and other adverse consequences.

OUR REAL ESTATE HOLDING COMPANIES AND FREIGHT FORWARDING BUSINESS RELY UPON STERLING SEAL FOR A MAJORITY OF THEIR REVENUE. LOSS OF CUSTOMERS BY STERLING SEAL WILL ADVERSELY AFFECT THE BUSINESS PERFORMANCE OF OUR OTHER CONSOLIDATING ENTITIES.

ADDR and Q5 rely on generating a majority of their respective revenues from Sterling Seal. In addition, 52% of the revenues of our freight forwarding business, Integrity Cargo, are derived from Sterling Seal. In the event that Sterling Seal has any material disruptions in business or its revenues or profits decrease substantially, our other subsidiaries may not be able to sustain operations.

DUE TO THE GLOBAL NATURE OF OUR BUSINESS, WE COULD BE ADVERSELY AFFECTED BY VIOLATIONS OF THE FCPA AND VARIOUS INTERNATIONAL TRADE AND EXPORT LAWS.

The global nature of our business creates various domestic and local regulatory challenges. The Foreign Corrupt Practices Act (“FCPA”) generally prohibits U.S.-based companies and their intermediaries from making improper payments to non-U.S. officials for the purpose of obtaining or retaining business. Our policies mandate compliance with these and other anti-bribery laws. We operate in parts of the world that experience corruption by government officials to some degree and, in certain circumstances, compliance with anti-bribery laws may conflict with local customs and practices. Our global operations require us to import from various countries, which geographically stretches our compliance obligations. To help ensure compliance, our anti-bribery policy and training on a global basis provide our employees with procedures, guidelines and information about anti-bribery obligations and compliance. However, such anti-bribery policies will not always protect us from reckless, criminal or unintentional acts committed by our employees, agents or other persons associated with us. If we are found to be in violation of the FCPA or other anti-bribery laws (either due to acts or inadvertence of our employees, or due to the acts or inadvertence of others), we could suffer criminal or civil penalties or other sanctions, which could have a material adverse effect on our business.

WE RELY ON OUR INFORMATION TECHNOLOGY SYSTEMS TO MANAGE NUMEROUS ASPECTS OF OUR BUSINESS AND CUSTOMER AND SUPPLIER RELATIONSHIPS, AND A DISRUPTION OF THESE SYSTEMS COULD ADVERSELY AFFECT OUR BUSINESS, FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

We depend on our information technology, or IT, systems to manage numerous aspects of our business transactions and provide analytical information to management. Our IT systems are an essential component of our business and growth strategies, and a disruption to our IT systems could significantly limit our ability to manage and operate our business efficiently. These systems are vulnerable to, among other things, damage and interruption from power loss, including as a result of natural disasters, computer system and network failures, loss of telecommunications services, operator negligence, loss of data, security breaches and computer viruses. Any such disruption could adversely affect our competitive position and thereby our business, financial condition and results of operations.

WE COULD BE SUBJECT TO PERSONAL INJURY, PROPERTY DAMAGE, PRODUCT LIABILITY, WARRANTY, ENVIRONMENTAL AND OTHER CLAIMS INVOLVING ALLEGEDLY DEFECTIVE PRODUCTS THAT WE SUPPLY.

The products we supply are often used in potentially hazardous applications that could result in death, personal injury, property damage, environmental damage, loss of production, punitive damages and consequential damages. Actual or claimed defects in the products we supply may result in our being named as a defendant in lawsuits asserting potentially large claims despite our not having manufactured the products alleged to have been defective. We may offer warranty terms that exceed those of the supplier, or we and the supplier may be financially unable to cover the losses and damages caused by any defective products that it manufactured and we supplied. Finally, the third-party supplier may be in a jurisdiction where it is impossible or very difficult to enforce our rights to obtain contribution in the event of a claim against us.

WE MAY NOT HAVE ADEQUATE INSURANCE FOR POTENTIAL LIABILITIES.

In the ordinary course of business, we may be subject to various product and non-product related claims, laws and administrative proceedings seeking damages or other remedies arising out of our commercial operations. We maintain insurance to cover our potential exposure for most claims and losses. However, our insurance coverage is subject to various exclusions, self-retentions and deductibles, may be inadequate or unavailable to protect us fully, and may be canceled or otherwise terminated by the insurer. Furthermore, we face the following additional risks under our insurance coverage:

| · | we may not be able to continue to obtain insurance coverage on commercially reasonable terms, or at all; |

| · | we may be faced with types of liabilities that are not covered under our insurance policies, such as damage from environmental contamination or terrorist attacks, and that exceed any amounts we may have reserved for such liabilities; |

| · | the amount of any liabilities that we may face may exceed our policy limits and any amounts we may have reserved for such liabilities; and |

| · | we may incur losses resulting from interruption of our business that may not be fully covered under our insurance policies. |

Even a partially uninsured claim of significant size, if successful, could materially and adversely affect our business, financial condition, results of operations and liquidity. However, even if we successfully defend ourselves against any such claim, we could be forced to spend a substantial amount of money in litigation expenses, our management could be required to spend valuable time in the defense against these claims and our reputation could suffer, any of which could harm our business and financial condition.

OUR FUTURE GROWTH MAY REQUIRE RECRUITMENT OF ADDITIONAL QUALIFIED EMPLOYEES.

In the event of our future growth in administration, marketing, and customer service, we may have to increase the depth and experience of our management team by adding new members. Our future success will depend to a large degree upon the active participation of our key officers and employees. There is no assurance that we will be able to employ qualified persons on acceptable terms. Lack of qualified employees may adversely affect our business development.

Risks Related To This Offering

WE MAY INCUR SIGNIFICANT COSTS TO BE A PUBLIC COMPANY TO ENSURE COMPLIANCE WITH U.S. CORPORATE GOVERNANCE AND ACCOUNTING REQUIREMENTS AND WE MAY NOT BE ABLE TO ABSORB SUCH COSTS.

We may incur significant costs associated with our public company reporting requirements, costs associated with newly applicable corporate governance requirements, including requirements under the Sarbanes-Oxley Act of 2002 and other rules implemented by the Securities and Exchange Commission. We expect all of these applicable rules and regulations to significantly increase our legal and financial compliance costs and to make some activities more time consuming and costly. We also expect that these applicable rules and regulations may make it more difficult and more expensive for us to obtain director and officer liability insurance and we may be required to accept reduced policy limits and coverage or incur substantially higher costs to obtain the same or similar coverage. As a result, it may be more difficult for us to attract and retain qualified individuals to serve on our board of directors or as executive officers. We are currently evaluating and monitoring developments with respect to these newly applicable rules, and we cannot predict or estimate the amount of additional costs we may incur or the timing of such costs. In addition, we may not be able to absorb these costs of being a public company which will negatively affect our business operations.

THE LACK OF PUBLIC COMPANY EXPERIENCE OF OUR MANAGEMENT TEAM COULD ADVERSELY IMPACT OUR ABILITY TO COMPLY WITH THE REPORTING REQUIREMENTS OF U.S. SECURITIES LAWS.

Our Chief Executive Officer (“CEO”) lacks public company experience, which could impair our ability to comply with legal and regulatory requirements such as those imposed by Sarbanes-Oxley Act of 2002. Our CEO has never been responsible for managing a publicly traded company. Such responsibilities include complying with federal securities laws and making required disclosures on a timely basis. Our management may not be able to implement programs and policies in an effective and timely manner that adequately respond to such increased legal, regulatory compliance and reporting requirements, including establishing and maintaining internal controls over financial reporting. Any such deficiencies, weaknesses or lack of compliance could have a materially adverse effect on our ability to comply with the reporting requirements of the Securities Exchange Act of 1934 which is necessary to maintain our public company status. If we were to fail to fulfill those obligations, our ability to continue as a U.S. public company would be in jeopardy in which event you could lose your entire investment in our company.

OUR FUTURE SUCCESS IS DEPENDENT, IN PART, ON THE PERFORMANCE AND CONTINUED SERVICE OF ANGELO AND DARREN DEROSA, OUR OFFICERS AND DIRECTORS.

We are presently dependent to a great extent upon the experience, abilities and continued services of Angelo DeRosa, our Chairman of the Board, and Darren DeRosa, our Chief Executive Officer. The loss of services of any of the management staff could have a material adverse effect on our business, financial condition or results of operation.

UPON THE COMPLETION OF THIS OFFERING, THE CONCENTRATION OF OUR CAPITAL STOCK OWNERSHIP WITH OUR FOUNDERS, EXECUTIVE OFFICERS, AND MEMBERS OF THE DEROSA FAMILY WILL LIKELY LIMIT AN INVESTOR’S ABILITY TO INFLUENCE CORPORATE MATTERS.

Upon completion of this offering, the executive officers and directors, Darren DeRosa and Angelo DeRosa will own approximately 88% of our outstanding common stock. In addition, members of the DeRosa family will own and control approximately 89.5% of our outstanding common stock. See “Certain Relationships and Related-Party Transactions.” As a result, these stockholders, acting individually or together, can exercise significant influence over our business policies and affairs, including the power to nominate a majority of the members of our board of directors. Because of such power and because our board of directors is responsible for appointing the members of our senior management team, our founders and key employees could affect any attempt by independent stockholders to replace current members of our management team. In addition, our founders and key employees and the DeRosa family in general can control any action requiring the general approval of our stockholders, including the adoption of amendments to our certificate of incorporation and bylaws and the approval of mergers or sales of substantially all of our assets. It is possible that the interests of certain of our founders and other key employees may, in certain circumstances, conflict with our interests, the interests of our other founders, key employees or minority stockholders, including you. For example, the concentration of ownership and voting power of our founders and key employees may delay, defer or even prevent an acquisition by a third party or other change of control involving us and may make some transactions more difficult or impossible without their support, even if such events are in the best interests of our minority stockholders. As a result, our founders and key employees could pursue transactions that may not be in our best interests which could have a material adverse effect on our business, financial condition or results of operations.

Risk Related To Our Capital Stock

WE MAY NEVER PAY ANY DIVIDENDS TO SHAREHOLDERS.

We have never declared or paid any cash dividends or distributions on our capital stock. We currently intend to retain our future earnings, if any, to support operations and to finance expansion and therefore we do not anticipate paying any cash dividends on our common stock in the foreseeable future.

The declaration, payment and amount of any future dividends will be made at the discretion of the board of directors, and will depend upon, among other things, the results of our operations, cash flows and financial condition, operating and capital requirements, and other factors as the board of directors considers relevant. There is no assurance that future dividends will be paid, and, if dividends are paid, there is no assurance with respect to the amount of any such dividend.

| 9 |

THE OFFERING PRICE OF THE COMMON STOCK WAS DETERMINED BASED ON THE PRICE OF OUR PRIVATE OFFERING, AND THEREFORE SHOULD NOT BE USED AS AN INDICATOR OF THE FUTURE MARKET PRICE OF THE SECURITIES. THEREFORE, THE OFFERING PRICE BEARS NO RELATIONSHIP TO OUR ACTUAL VALUE, AND MAY MAKE OUR SHARES DIFFICULT TO SELL.

Since our shares are not listed or quoted on any exchange or quotation system, the offering price of $0.30 per share for the shares of common stock was determined based on the price of our private offering. The facts considered in determining the offering price were our financial condition and prospects, our limited operating history and the general condition of the securities market. The offering price bears no relationship to the book value, assets or earnings of our company or any other recognized criteria of value. The offering price should not be regarded as an indicator of the future market price of the securities.

YOU WILL EXPERIENCE DILUTION OF YOUR OWNERSHIP INTEREST BECAUSE OF THE FUTURE ISSUANCE OF ADDITIONAL SHARES OF OUR COMMON STOCK AND OUR PREFERRED STOCK.

In the future, we may issue our authorized but previously unissued equity securities, resulting in the dilution of the ownership interests of our present stockholders. We are currently authorized to issue 200,000,000 shares of common stock, par value $0.001 per share, and 10,000,000 shares of preferred stock, par value $0.001 per share. We may also issue additional shares of our common stock or other securities that are convertible into or exercisable for common stock in connection with hiring or retaining employees or consultants, future acquisitions, future sales of our securities for capital raising purposes, or for other business purposes. The future issuance of any such additional shares of our common stock or other securities may create downward pressure on the trading price of our common stock. There can be no assurance that we will not be required to issue additional shares, warrants or other convertible securities in the future in conjunction with hiring or retaining employees or consultants, future acquisitions, future sales of our securities for capital raising purposes or for other business purposes, including at a price (or exercise prices) below the price at which shares of our common stock will be quoted on the OTCBB.

IN THE EVENT THAT THE COMPANY’S SHARES ARE TRADED, THEY WILL MOST LIKELY TRADE UNDER $5.00 PER SHARE AND THUS WILL BE A PENNY STOCK. TRADING IN PENNY STOCKS HAS MANY RESTRICTIONS AND THESE RESTRICTIONS COULD SEVERLY AFFECT THE PRICE AND LIQUIDITY OF THE COMPANY’S SHARES.

In the event that our shares are traded, and our stock will most likely trade below $5.00 per share, and our stock will therefore be known as a “penny stock”, which is subject to various regulations involving disclosures to be given to you prior to the purchase of any penny stock. The U.S. Securities and Exchange Commission (the “SEC”) has adopted regulations which generally define a “penny stock” to be any equity security that has a market price of less than $5.00 per share, subject to certain exceptions. Our common stock will probably be considered to be a “penny stock” and will subject to the additional regulations and risks of such a security. A penny stock is subject to rules that impose additional sales practice requirements on broker/dealers who sell these securities to persons other than established customers and accredited investors. For transactions covered by these rules, the broker/dealer must make a special suitability determination for the purchase of these securities. In addition, he must receive the purchaser’s written consent to the transaction prior to the purchase. He must also provide certain written disclosures to the purchaser. Consequently, the “penny stock” rules may restrict the ability of broker/dealers to sell our securities, and may negatively affect the ability of holders of shares of our common stock to resell them. These disclosures require you to acknowledge that you understand the risks associated with buying penny stocks and that you can absorb the loss of your entire investment. Penny stocks are low priced securities that do not have a very high trading volume. Consequently, the price of the stock is often volatile and you may not be able to buy or sell the stock when you want to.

INVESTING IN THE COMPANY IS A HIGHLY SPECULATIVE INVESTMENT AND COULD RESULT IN THE LOSS OF YOUR ENTIRE INVESTMENT.

A purchase of the offered shares is significantly speculative and involves significant risks. The offered shares should not be purchased by any person who cannot afford the loss of his or her entire purchase price. The business objectives of the Company are also speculative, and we may be unable to satisfy those objectives. The shareholders of the Company may be unable to realize a substantial return on their purchase of the offered shares, or any return whatsoever, and may lose their entire investment in the Company. For this reason, each prospective purchaser of the offered shares should read this prospectus and all of its exhibits carefully and consult with their attorney, business advisor and/or investment advisor.

THERE IS NO ASSURANCE OF A PUBLIC MARKET OR THAT OUR COMMON STOCK WILL EVER TRADE ON A RECOGNIZED EXCHANGE. THEREFORE, YOU MAY BE UNABLE TO LIQUIDATE YOUR INVESTMENT IN OUR STOCK.

There is no established public trading market for our common stock. Our shares have not been listed or quoted on any exchange or quotation system. There can be no assurance that a market maker will agree to file the necessary documents with FINRA, which operates the OTCBB, nor can there be any assurance that such an application for quotation will be approved or that a regular trading market will develop or that if developed, will be sustained. In the absence of a trading market, an investor may be unable to liquidate their investment.

WE ARE AN “EMERGING GROWTH COMPANY,” AND ANY DECISION ON OUR PART TO COMPLY ONLY WITH CERTAIN REDUCED DISCLOSURE REQUIREMENTS APPLICABLE TO “EMERGING GROWTH COMPANIES” COULD MAKE OUR COMMON STOCK LESS ATTRACTIVE TO INVESTORS.

We are an “emerging growth company,” as defined in the JOBS Act, and, for as long as we continue to be an “emerging growth company,” we may choose to take advantage of exemptions from various reporting requirements applicable to other public companies but not to “emerging growth companies,” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We could be an “emerging growth company” for up to five years, or until the earliest of (i) the last day of the first fiscal year in which our annual gross revenues exceed $1 billion, (ii) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, or (iii) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three year period.

In addition, Section 107 of the JOBS Act also provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an “emerging growth company” can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected to opt in to the extended transition period for complying with the revised accounting standards.

BECAUSE WE HAVE ELECTED TO DEFER COMPLIANCE WITH NEW OR REVISED ACCOUNTING STANDARDS, OUR FINANCIAL STATEMENT DISCLOSURE MAY NOT BE COMPARABLE TO SIMILAR COMPANIES.

We have elected to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(1) of the JOBS Act. This allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result of our election, our financial statements may not be comparable to companies that comply with public company effective dates.

OUR STATUS AS AN “EMERGING GROWTH COMPANY” UNDER THE JOBS ACT OF 2012 MAY MAKE IT MORE DIFFICULT TO RAISE CAPITAL AS AND WHEN WE NEED IT.

Because of the exemptions from various reporting requirements provided to us as an “emerging growth company” and because we will have an extended transition period for complying with new or revised financial accounting standards, we may be less attractive to investors and it may be difficult for us to raise additional capital as and when we need it. Investors may be unable to compare our business with other companies in our industry if they believe that our financial accounting is not as transparent as other companies in our industry. If we are unable to raise additional capital as and when we need it, our financial condition and results of operations may be materially and adversely affected.

WE MAY BE EXEMPT FROM THE REPORTING OBLIGATIONS PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT AND THEREFORE MAY NOT HAVE TO PROVIDE INVESTORS WITH PERIODIC REPORTS AS MAY BE REQUIRED PURSUANT TO SECTION 13 OF THE SECURITIES EXCHANGE ACT, FOLLOWING THE FORM 10K REQUIRED FOR THE FISCAL YEAR IN WHICH OUR REGISTRATION STATEMENT IS EFFECTIVE.

The requirement for an issuer that has filed a registration statement to file pursuant to Section 15(d) of the Securities Exchange Act is suspended for any fiscal year, except for the fiscal year in which such registration statement becomes effective, if, at the beginning of the fiscal year, the issuer has fewer than 300 shareholders. We currently have fewer than 300 shareholders and expect to maintain a fewer than 300 shareholder base. If we do continue to have fewer than 300 shareholders, we will be exempt from the filing requirements as required pursuant to Section 13 of the Securities Exchange Act and will not be required to file any periodic reports, including Form 10Q and 10K filings, with the SEC subsequent to the Form 10K required for the fiscal year in which our registration statement is effective. Further, disclosures in our Form 10K that we will be required to file for the fiscal year in which our registration statement is effective, is less extensive than the disclosures required of fully reporting companies. Specifically, we are not subject to disclose in our Form 10K risk factors, unresolved staff comments, or selected financial data, pursuant to Items 1A, 1B, 6, respectively.

UNTIL WE REGISTER A CLASS OF OUR SECURITIES UNDER SECTION 12 OF THE SECURITIES EXCHANGE ACT OF 1934 (“EXCHANGE ACT”), WE WILL ONLY BE SUBJECT TO THE PERIODIC REPORTING OBLIGATIONS IMPOSED BY SECTION 15(D) OF THE EXCHANGE ACT.

Until such time as we register a class of our securities under Section 12 of the Securities Exchange Act of 1934, we will only be subject to the periodic reporting obligations imposed by Section 15(d) of the Exchange Act. Accordingly, we will not be subject to the proxy rules, Section 16 short-swing profit provisions, beneficial ownership reporting, the bulk of the tender offer rules and the reporting requirements of Section 13 of the Exchange Act.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

The information contained in this report, including in the documents incorporated by reference into this report, includes some statement that are not purely historical and that are “forward-looking statements.” Such forward-looking statements include, but are not limited to, statements regarding our and their management’s expectations, hopes, beliefs, intentions or strategies regarding the future, including our financial condition, results of operations. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipates,” “believes,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “might,” “plans,” “possible,” “potential,” “predicts,” “projects,” “seeks,” “should,” “would” and similar expressions, or the negatives of such terms, may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements contained in this report are based on current expectations and beliefs concerning future developments and the potential effects on the parties and the transaction. There can be no assurance that future developments actually affecting us will be those anticipated. These that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements, including the following forward-looking statements involve a number of risks, uncertainties (some of which are beyond the parties’ control) or other assumptions.

Use of Proceeds

We will not receive any proceeds from the sale of common stock by the selling security holders. All of the net proceeds from the sale of our common stock will go to the selling security holders as described below in the sections entitled “Selling Security Holders” and “Plan of Distribution”. We have agreed to bear the expenses relating to the registration of the common stock for the selling security holders.

Determination of Offering Price

Since our common stock is not listed or quoted on any exchange or quotation system, the offering price of the shares of common stock was determined by the price of the common stock that was sold to our security holders pursuant to an exemption under Section 4(2) of the Securities Act of 1933 and Rule 506 of Regulation D promulgated under the Securities Act of 1933.

The offering price of the shares of our common stock does not necessarily bear any relationship to our book value, assets, past operating results, financial condition or any other established criteria of value. The facts considered in determining the offering price were our financial condition and prospects, our limited operating history and the general condition of the securities market.

Although our common stock is not listed on a public exchange, we will be filing to obtain a quotation on the OTCBB concurrently with the filing of this prospectus. In order to be quoted on the OTCBB, a market maker must file an application on our behalf in order to make a market for our common stock. There can be no assurance that a market maker will agree to file the necessary documents with FINRA, which operates the OTC Bulletin Board, nor can there be any assurance that such an application for quotation will be approved.

In addition, there is no assurance that our common stock will trade at market prices in excess of the initial offering price as prices for the common stock in any public market which may develop will be determined in the marketplace and may be influenced by many factors, including the depth and liquidity.

Dilution

The common stock to be sold by the selling shareholders as provided in the “Selling Security Holders” section is common stock that is currently issued. Accordingly, there will be no dilution to our existing shareholders.

Selling Security Holders

The common shares being offered for resale by the selling security holders consist of 2,236,873 shares of our common stock held by 59 shareholders, which consist of i) 797,373 shares sold to investors in our private offering pursuant to Regulation D Rule 506 completed in July 2012 at an offering price of $0.30 per share, ii) 720,000 shares issued to Lawrence Adams and an additional 559,500 to 17 other founders of Sterling Consolidated Corp. (f/k/a Oceanview Acquisition Corp.) that were issued as founders shares on January 31, 2011, iii) 150,000 shares issued to Delaney Equity Group for consulting services, and iv) 10,000 shares issued to Anslow & Jaclin, LLP for services rendered.

The following table sets forth the names of the selling security holders, the number of shares of common stock beneficially owned by each of the selling stockholders as of January 16, 2013 and the number of shares of common stock being offered by the selling stockholders. The shares being offered hereby are being registered to permit public secondary trading, and the selling stockholders may offer all or part of the shares for resale from time to time. However, the selling stockholders are under no obligation to sell all or any portion of such shares nor are the selling stockholders obligated to sell any shares immediately upon effectiveness of this prospectus. All information with respect to share ownership has been furnished by the selling stockholders.

| Name | Shares Beneficially Owned Prior to Offering | Shares to be Offered | Amount Beneficially Owned After Offering | Percent Beneficially Owned After Offering | Shares Beneficially Owned Prior to Offering | Shares to be Offered | Amount Beneficially Owned After Offering | Percent Beneficially Owned After Offering | ||||||||||||||||||||||||

| Ali Daneshmand | 100,000 | 100,000 | 0 | * | 100,000 | 100,000 | 0 | * | ||||||||||||||||||||||||

| Angelo C Porta | 21,040 | 21,040 | 0 | * | 21,040 | 21,040 | 0 | * | ||||||||||||||||||||||||

| Anna Khorosheva | 333 | 333 | 0 | * | 333 | 333 | 0 | * | ||||||||||||||||||||||||

| Chichester Associates, Inc. (1) | 288,333 | (20) | 288,333 | 0 | * | 288,333 | (20) | 288,333 | 0 | * | ||||||||||||||||||||||

| Chris Hussar | 10,000 | 10,000 | 0 | * | 10,000 | 10,000 | 0 | * | ||||||||||||||||||||||||

| Desiree Muzzicato | 3,337 | 3,337 | 0 | * | 3,337 | 3,337 | 0 | * | ||||||||||||||||||||||||

| Eugenia Fishbein (2) | 333 | 333 | 0 | * | 333 | 333 | 0 | * | ||||||||||||||||||||||||

| Frank Strain | 1,000 | 1,000 | 0 | * | 1,000 | 1,000 | 0 | * | ||||||||||||||||||||||||

| Fred Zink (3) | 35,000 | 35,000 | 0 | * | 35,000 | 35,000 | 0 | * | ||||||||||||||||||||||||

| Gary Lesock | 333 | 333 | 0 | * | 333 | 333 | 0 | * | ||||||||||||||||||||||||

| Gregory Schmitt | 1,000 | 1,000 | 0 | * | 1,000 | 1,000 | 0 | * | ||||||||||||||||||||||||

| Hannah Steinberg (4) | 1,667 | 1,667 | 0 | * | 1,667 | 1,667 | 0 | * | ||||||||||||||||||||||||

| Joe and Mary Orlando | 56,666 | 56,666 | 0 | * | 56,666 | 56,666 | 0 | * | ||||||||||||||||||||||||

| John Magoulis | 333 | 333 | 0 | * | 333 | 333 | 0 | * | ||||||||||||||||||||||||

| John Padian | 333 | 333 | 0 | * | 333 | 333 | 0 | * | ||||||||||||||||||||||||

| John Scoscia | 1,000 | 1,000 | 0 | * | 1,000 | 1,000 | 0 | * | ||||||||||||||||||||||||

| John Velisaris | 10,000 | 10,000 | 0 | * | 10,000 | 10,000 | 0 | * | ||||||||||||||||||||||||

| John Williamson | 333 | 333 | 0 | * | 333 | 333 | 0 | * | ||||||||||||||||||||||||

| Joseph Coccia | 333 | 333 | 0 | * | 333 | 333 | 0 | * | ||||||||||||||||||||||||

| Laura Frye | 1,000 | 1,000 | 0 | * | 1,000 | 1,000 | 0 | * | ||||||||||||||||||||||||

| Linda Ann Trufolo | 33,333 | 33,333 | 0 | * | 33,333 | 33,333 | 0 | * | ||||||||||||||||||||||||

| Lou Welfare | 667 | 667 | 0 | * | 667 | 667 | 0 | * | ||||||||||||||||||||||||

| Lynne and Keith Davis (5) | 116,667 | 116,667 | 0 | * | 116,667 | 116,667 | 0 | * | ||||||||||||||||||||||||

| Michael Angeloni | 333 | 333 | 0 | * | 333 | 333 | 0 | * | ||||||||||||||||||||||||

| Mike Mrotzek | 16,667 | 16,667 | 0 | * | 16,667 | 16,667 | 0 | * | ||||||||||||||||||||||||

| Maranz Inc. (19) | 175,000 | 175,000 | 0 | * | 175,000 | 175,000 | 0 | * | ||||||||||||||||||||||||

| Next Generation TS FBO Glenn Jaffe IRA 1343 (6) | 20,000 | 20,000 | 0 | * | 20,000 | 20,000 | 0 | * | ||||||||||||||||||||||||

| Rebecca Steinberg (7) | 1,667 | 1,667 | 0 | * | 1,667 | 1,667 | 0 | * | ||||||||||||||||||||||||

| Remy Fishbein (8) | 333 | 333 | 0 | * | 333 | 333 | 0 | * | ||||||||||||||||||||||||

| Robert and Inga Bliss | 34,000 | 34,000 | 0 | * | 34,000 | 34,000 | 0 | * | ||||||||||||||||||||||||

| Robert Wallace | 33,333 | 33,333 | 0 | * | 33,333 | 33,333 | 0 | * | ||||||||||||||||||||||||

| Sally Chichester (19) | 333 | 333 | 0 | * | ||||||||||||||||||||||||||||

| Sally Chichester (20) | 333 | 333 | 0 | * | ||||||||||||||||||||||||||||

| Sean Davis (9) | 1,667 | 1,667 | 0 | * | 1,667 | 1,667 | 0 | * | ||||||||||||||||||||||||

| Tim Walsh | 16,666 | 16,666 | 0 | * | 16,666 | 16,666 | 0 | * | ||||||||||||||||||||||||

| Timothy Davis (10) | 1,667 | 1,667 | 0 | * | 1,667 | 1,667 | 0 | * | ||||||||||||||||||||||||

| Troy Nowakowski | 333 | 333 | 0 | * | 333 | 333 | 0 | * | ||||||||||||||||||||||||

| Sheng-Chi and LiSheng T. Wu | 100,000 | 100,000 | 0 | * | 100,000 | 100,000 | 0 | * | ||||||||||||||||||||||||

| Rose Astorino | 333 | 333 | 0 | * | 333 | 333 | 0 | * | ||||||||||||||||||||||||

| Lawrence Adams | 1,293,500 | 720,000 | 561,500 | 1.52 | % | 1,293,500 | 720,000 | 561,500 | 1.52 | % | ||||||||||||||||||||||

| Delaney Equity Group (11) | 150,000 | 150,000 | 0 | 0 | 150,000 | 150,000 | 0 | 0 | ||||||||||||||||||||||||

| Bennett Weber | 50,000 | 50,000 | 0 | * | 50,000 | 50,000 | 0 | * | ||||||||||||||||||||||||

| Erik Langeland | 25,000 | 25,000 | 0 | * | 25,000 | 25,000 | 0 | * | ||||||||||||||||||||||||

| Frederick Kiechel III (12) | 25,000 | 25,000 | 0 | * | 25,000 | 25,000 | 0 | * | ||||||||||||||||||||||||

| Frederick Kiechel IV (13) | 5,000 | 5,000 | 0 | * | 5,000 | 5,000 | 0 | * | ||||||||||||||||||||||||

| Vivian Kiechel (14) | 25,000 | 25,000 | 0 | * | 25,000 | 25,000 | 0 | * | ||||||||||||||||||||||||

| K. Lee Kiechel Coles (15) | 5,000 | 5,000 | 0 | * | 5,000 | 5,000 | 0 | * | ||||||||||||||||||||||||

| Loretta Harrison | 10,000 | 10,000 | 0 | * | 10,000 | 10,000 | 0 | * | ||||||||||||||||||||||||

| Maria Brown | 10,000 | 10,000 | 0 | * | 10,000 | 10,000 | 0 | * | ||||||||||||||||||||||||

| Sara Fleischman-Stuven | 5,000 | 5,000 | 0 | * | 5,000 | 5,000 | 0 | * | ||||||||||||||||||||||||

| Gina Skurchak-Rossi (16) | 5,000 | 5,000 | 0 | * | 5,000 | 5,000 | 0 | * | ||||||||||||||||||||||||

| Ernest Rossi (17) | 5,000 | 5,000 | 0 | * | 5,000 | 5,000 | 0 | * | ||||||||||||||||||||||||

| Dr. Dominick Lembo | 30,000 | 30,000 | 0 | * | 30,000 | 30,000 | 0 | * | ||||||||||||||||||||||||

| Michael Selearis | 15,000 | 15,000 | * | 15,000 | 15,000 | * | ||||||||||||||||||||||||||

| Rafael Veloz | 5,000 | 5,000 | 0 | * | 5,000 | 5,000 | 0 | * | ||||||||||||||||||||||||

| Wendy Straker-Elie | 7,500 | 7,500 | 0 | * | 7,500 | 7,500 | 0 | * | ||||||||||||||||||||||||

| Elaine Friedman | 44,000 | 44,000 | 0 | * | 44,000 | 44,000 | 0 | * | ||||||||||||||||||||||||

| Anslow & Jaclin, LLP (18) | 9,000 | 9,000 | 0 | * | 9,000 | 9,000 | 0 | * | ||||||||||||||||||||||||

| Eric Stein (18) | 1,000 | 1,000 | 0 | * | 1,000 | 1,000 | 0 | * | ||||||||||||||||||||||||

| TOTAL: | 2,810,373 | 2,236,873 | 561,000 | 1.52 | % | 2,810,373 | 2,236,873 | 561,000 | 1.52 | % | ||||||||||||||||||||||

(1) Sally Chichester is the principal of Chichester Associates, Inc. Sally Chichester acting alone has voting and dispositive power over the shares owned by Chichester Associates, Inc.

(2) Eugenia Fishbein is the mother of Remy Fishbein.

(3) Fred Zink is the President of Sterling Seal & Supply, Inc.

(4) Hannah Steinberg is the daughter of Lynne Davis.

(5) Lynne and Keith Davis are husband and wife and are the parents of Sean Davis and Timothy Davis. Lynne Davis is the mother of Hannah Steinberg and Rebecca Steinberg.

(6)Next Generation TS FBO Glenn Jaffe IRA 1343 is the Individual Retirement Account of Glenn Jaffe, administered by Next Generation Trust Services. Glenn Jaffealone has voting and dispositive power over the shares owned by Next Generation TS FBO Glenn Jaffe IRA 1343.

(7) Rebecca Steinberg the daughter of Lynne Davis.

(8) Remy Fishbein is the son of Eugenia Fishbein.

(9) Sean Davis is the son of Lynne and Keith Davis.

(10) Timothy Davis is the son of Lynne and Keith Davis.

(11) David Delaney is the president of Delaney Equity Group, LLC acting alone has voting and dispositive power over the shares owned by Delaney Equity Group, LLC

(12) Frederick Kiechel III is the father of Frederick Kiechel IV and K. Lee Kiechel Coles. Frederick Kiechel III is the husband of Vivian Kiechel.

(13) Frederick Kiechel IV is the son of Frederick Kiechel III and Vivian Kiechel.

(14) Vivian Kiechel is the mother of Frederick Kiechel IV and K. Lee Kiechel Coles. Vivian Kiechel is the wife of Frederick Kiechel III.

(15) K. Lee Kiechel Coles is the daughter of Frederick Kiechel III and Vivian Kiechel.

(16) Gina Skurchak-Rossi is the wife of Ernest Rossi.

(17) Ernest Rossi is the husband of Gina Skurchak-Rossi

(18) Rich Anslow and Gregg Jaclin are principals of Anslow & Jaclin LLP and have shared voting and dispositive powers over its shares of our common stock. Eric Stein is an associate at Anslow & Jaclin LLP.

(19) George Halagas is the principal of Maranz, Inc. George Halagas acting alone has voting and dispositive power over the shares owned by Maranz, Inc.

(20) The shares owned by Chichester Associates, Inc. include (i) 288,000 shares issued as founders shares in Oceanview Acquisition Corp; and (ii) 333 shares issued in connection with the Regulation D Rule 506 completed in July 2012 at an offering price of $0.30 per share. The 333 shares that Sally Chichester owns in her own name are different than the 333 shares issued to Chichester Associates, Inc.

There are no agreements between the company and any selling shareholder pursuant to which the shares subject to this registration statement were issued.

Other than Angelo DeRosa, Darren DeRosa and Scott Chichester, noneNone of the selling shareholders or their beneficial owners:

| - | has had a material relationship with us other than as a shareholder at any time within the past three years; or |

| - | has ever been one of our officers or directors or an officer or director of our predecessors or affiliates |

| - | are broker-dealers or affiliated with broker-dealers. |

Angelo DeRosa is our current Chairman of the Board of Directors. Darren DeRosa is our current Chief Executive Officer. And, Scott Chichester is our current Chief Financial Officer and was, prior to the closing of the share exchange agreement, our sole officer and director.

Plan of Distribution

The selling security holders may sell some or all of their shares at a fixed price of $0.30 per share until our shares are quoted on the OTCBB and thereafter at prevailing market prices or privately negotiated prices. Prior to being quoted on the OTC Bulletin Board, shareholders may sell their shares in private transactions to other individuals. Although our common stock is not listed on a public exchange, we will be filing to obtain a quotation on the OTCBB concurrently with the filing of this prospectus. In order to be quoted on the OTC Bulletin Board, a market maker must file an application on our behalf in order to make a market for our common stock. There can be no assurance that a market maker will agree to file the necessary documents with FINRA, which operates the OTC Bulletin Board, nor can there be any assurance that such an application for quotation will be approved. However, sales by selling security holder must be made at the fixed price of $0.30 until a market develops for the stock.

Once a market has developed for our common stock, the shares may be sold or distributed from time to time by the selling stockholders, who may be deemed to be underwriters, directly to one or more purchasers or through brokers or dealers who act solely as agents, at market prices prevailing at the time of sale, at prices related to such prevailing market prices, at negotiated prices or at fixed prices, which may be changed. The distribution of the shares may be effected in one or more of the following methods:

| ● | ordinary brokers transactions, which may include long or short sales, |

| ● | transactions involving cross or block trades on any securities or market where our common stock is trading, market where our common stock is trading, |

| ● | through direct sales to purchasers or sales effected through agents, |

| ● | through transactions in options, swaps or other derivatives (whether exchange listed of otherwise), or exchange listed or otherwise), or |

| ● | any combination of the foregoing. |

In addition, the selling stockholders may enter into hedging transactions with broker-dealers who may engage in short sales, if short sales were permitted, of shares in the course of hedging the positions they assume with the selling stockholders. The selling stockholders may also enter into option or other transactions with broker-dealers that require the delivery by such broker-dealers of the shares, which shares may be resold thereafter pursuant to this prospectus. To our best knowledge, none of the selling security holders are broker-dealers or affiliates of broker dealers.

We will advise the selling security holders that the anti-manipulation rules of Regulation M under the Exchange Act may apply to sales of shares in the market and to the activities of the selling security holders and their affiliates. In addition, we will make copies of this prospectus (as it may be supplemented or amended from time to time) available to the selling security holders for the purpose of satisfying the prospectus delivery requirements of the Securities Act. The selling security holders may indemnify any broker-dealer that participates in transactions involving the sale of the shares against certain liabilities, including liabilities arising under the Securities Act.

Brokers, dealers, or agents participating in the distribution of the shares may receive compensation in the form of discounts, concessions or commissions from the selling stockholders and/or the purchasers of shares for whom such broker-dealers may act as agent or to whom they may sell as principal, or both (which compensation as to a particular broker-dealer may be in excess of customary commissions). Neither the selling stockholders nor we can presently estimate the amount of such compensation. We know of no existing arrangements between the selling stockholders and any other stockholder, broker, dealer or agent relating to the sale or distribution of the shares. We will not receive any proceeds from the sale of the shares of the selling security holders pursuant to this prospectus. We have agreed to bear the expenses of the registration of the shares, including legal and accounting fees, and such expenses are estimated to be approximately $68,000.

Notwithstanding anything set forth herein, no FINRA member will charge commissions that exceed 8% of the total proceeds of the offering.

Description of Securities to be Registered

General

We are currently authorized to issue 200,000,000 shares of common stock, par value $0.001 per share, and 10,000,000 shares of preferred stock, par value $0.001 per share.

Common Stock

We are currently authorized to issue 200,000,000 shares of common stock, par value $0.001 per share. Currently we have36,957,37337,074,040 shares of common stock issued and outstanding.

Each share of common stock shall have one (1) vote per share for all purpose. Our common stock does not provide a preemptive, subscription or conversion rights and there are no redemption or sinking fund provisions or rights. Our common stock holders are not entitled to cumulative voting for election of Board of Directors.

Preferred Stock

We are authorized to issue 10,000,000 shares of preferred stock, par value $0.001 per share. Currently, no shares of our preferred stock have been designated any rights and we have no shares of preferred stock issued and outstanding.

Dividends

We have not paid any cash dividends to our shareholders. The declaration of any future cash dividends is at the discretion of our board of directors and depends upon our earnings, if any, our capital requirements and financial position, our general economic conditions, and other pertinent conditions. It is our present intention not to pay any cash dividends in the foreseeable future, but rather to reinvest earnings, if any, in our business operations.

Warrants

There are no outstanding warrants to purchase our securities.

Options

There are no outstanding options to purchase our securities.

Transfer Agent and Registrar

The transfer agent and registrar for our common stock is VStock Transfer, LLC. The transfer agent’s address is 77 Spruce Street, Suite 201, Cedarhurst, New York 11516.

Interests of Named Experts and Counsel

No expert or counsel named in this prospectus as having prepared or certified any part of this prospectus or having given an opinion upon the validity of the securities being registered or upon other legal matters in connection with the registration or offering of the common stock was employed on a contingency basis, or had, or is to receive, in connection with the offering, a substantial interest, direct or indirect, in the registrant or any of its parents or subsidiaries. Nor was any such person connected with the registrant or any of its parents or subsidiaries as a promoter, managing or principal underwriter, voting trustee, director, officer, or employee.

Anslow & Jaclin, LLP located at 195 Route 9 South, Suite 204, Manalapan, NJ 07726 will pass on the validity of the common stock being offered pursuant to this registration statement.