As filed with the Securities and Exchange Commission on October 27, 2010March 2, 2012.

Registration No. 333-163867

333-______

333-______

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

INDIA GLOBALIZATION CAPITAL, INC.

(Exact Namename of Registrantregistrant as Specifiedspecified in Its Charter)its charter)

| Maryland | 1600 | 20-2760393 | ||

(State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

4336 Montgomery Ave.

Bethesda, Maryland 20814

(301) 983-0998

(Address, Including Zip Code, and Telephone Number,

Including Area Code, of Registrant’s Principal Executive Offices)

Ram Mukunda

Chief Executive Officer and President

India Globalization Capital, Inc.

4336 Montgomery Ave.

Bethesda, Maryland, 20814

(301) 983-0998

(Name, Address, Including Zip Code, and Telephone Number,

Including Area Code, of Agent for Service)

Copies of all communications to:

Approximate date of commencement of proposed sale to public: As soon as practicable, after this registration statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: þ

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company þ |

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Amount to be Registered (1) | Proposed maximum offering price | Proposed maximum aggregate offering price (2) | Amount of Registration Fee | ||||||||||||||

| Shares of Common Stock, $0.0001 par value per share, underlying IPO Warrants | 11,855,122 | $ | 5.00 | $ | 59,275,610 | $ | 6,792.98 | |||||||||||

| Shares of Common Stock, $0.0001 par value per share, underlying 2009 Warrants | 258,800 | 1.60 | 414,080 | 47.45 | (3) | |||||||||||||

| Shares of Common Stock, $0.0001 par value per share, underlying 2010 Warrants | 858,610 | 0.90 | 772,749 | 88.56 | (3) | |||||||||||||

| Shares of Common Stock, $0.0001 par value per share ,issued in the acquisition of Ironman | 31,500,000 | 0.35 | (4) | 11,025,000 | 1,263.47 | |||||||||||||

| Total | 44,472,532 | $ | $ | 71,487,439 | $ | 8,192.46 | ||||||||||||

| (1) | Pursuant to Rule 416 of the Securities Act of 1933, as amended, this Registration Statement also registers such additional shares of Common Stock as may become issuable to prevent dilution as a result of stock splits, stock dividends or similar transactions. |

| (2) | Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended. |

| (3) | The fee has been partially satisfied by applying, pursuant to Rule 457(p) under the Securities Act of 1933, a portion of the previously paid filing fees in connection with (i)$159.03 that was paid with respect to the same securities that were previously registered pursuant to the Registration Statement No. 333-160993 on Form S-3 in August 2009 and (ii) $698.74 that was paid with respect to the same securities that were previously registered pursuant to the Registration Statement No. 333-163867 on Form S-1 in October 2010. |

| (4) | Estimated solely for the purpose of computing the registration fee pursuant to Rule 457(c) under the Securities Act of 1933, as amended. |

The RegistrantCompany hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the RegistrantCompany shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

| Proposed | ||||||||||||||||

| Proposed | maximum | Amount of | ||||||||||||||

| Amount to be | maximum | aggregate | registration | |||||||||||||

| Title of each class of securities to be registered (1) | registered | offering price (2) | offering price | Fee | ||||||||||||

| Common Stock, $0.0001 par value | 7,500,000 | $ | 0.98 | $ | 7,350,000 | $ | 524.06 | |||||||||

| Warrants (3) | 2,500,000 | (3) | ||||||||||||||

| Shares of Common Stock, $0.0001 par value per share, underlying Warrants | 2,500,000 | 0.98 | 2,450,000 | 174.69 | ||||||||||||

| Total | 10,000,000 | $ | 0.98 | $ | 9,800,000 | $ | 698.74 | (4) | ||||||||

| The information in this |

SUBJECT TO COMPLETION, DATED OCTOBER 27, 2010MARCH 2, 2012

PRELIMINARY PROSPECTUS

India Globalization Capital, Inc.

This prospectus relates to purchase up to 2,500,000the offer and sale by India Globalization Capital, Inc. (“IGC” or the “Company”) of 12,972,532 shares of Common Stock

The warrants are exercisable at any time after [the closing date] and on or before the seventh anniversary of their initial exercise date at an exercise price of $ ____ per share. and $ per warrant . This prospectus also relates to the purchase of up to 2,500,00012,972,532 shares of our common stock that areCommon Stock issuable by the Company upon the exercise of the warrants offered hereunder.

(i) 11,855,122 shares of Common Stock issuable upon the exercise of 11,855,122 warrants offered by this prospectus. The placement agents are not purchasing any securities(the “IPO Warrants”) originally issued in our initial public offering pursuant to thisa prospectus nor are they requireddated March 3, 2006. In order to sell any specific number or dollar amountobtain the shares, the holders of the securities offered hereby, but will use their best efforts to arrangeIPO Warrants must pay an exercise price of $5.00 per share for the saleshares underlying the IPO Warrants.

(ii) 258,800 shares of Common Stock issuable upon the exercise of 258,800 warrants (the “2009 Warrants”) originally issued in a registered direct offering pursuant to a prospectus and prospectus supplement each dated September 16, 2009. In order to obtain the shares, the holders of the securities being offered. See2009 Warrants must pay an exercise price of $1.60 per share for the section entitled “Planshares underlying the 2009 Warrants.

(iii) 856,610 shares of Distribution” beginning on page 14Common Stock issuable upon the exercise of this858,610 warrants (the “2010 Warrants”) originally issued in a registered direct offering pursuant to a prospectus for more information regarding these arrangements. The placement agents will receive compensation for salesand prospectus supplement each dated November 30, 2010. In order to obtain the shares, the holders of the securities2010 Warrants must pay an exercise price of $0.90 per share for the shares underlying the 2010 Warrants.

The 31,500,000 shares of Common Stock are being offered hereby at a fixed commission rateand sold by the selling shareholders who acquired the shares in connection withthe Company’s acquisition of 7%H&F Ironman, Ltd. (“HK Ironman”). Pursuant to that acquisition, the Company sold an aggregate of 31,500,000 shares in exchange for the ownership of 100% of HK Ironman. The issuance of shares was approved by the shareholders of the gross proceeds of the offering, provided that the commission rate shall be reduced to 2% for sales to certain investors identified by us.Company on December 30, 2011.

Investing in the offered securities involves substantial risks. In reviewing this prospectus, you should carefully consider the matters described under the heading “Risk Factors,“Risk Factors.” and in other documents incorporated by reference, including our Annual Report on Form 10-K for our fiscal year ended March 31, 2010 and our Quarterly Report on Form 10-Q for the three month period ended June 30, 2010.

The date of this prospectus is __________, 2010.

| Page | |

| 1 | |

| Determination of Offering Price | 27 |

| 48 | |

| 53 | |

All references to “Company”, “IGC”, “IGC Inc.” “we,” “our,” “us,”, “we”, “our”, “us” and similar terms in this prospectus refer to India Globalization Capital, Inc.

hold a non-controlling interest.

We have not authorized anyone to provide any information other than that contained or incorporated by reference in this prospectus. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus and any applicable prospectus supplement are not offers to sell nor are they seeking an offer to buy these securities in any jurisdiction where the offer or sale is not permitted. The information contained in this prospectus and any applicable prospectus supplement is complete and correct only as of the date on the front cover of such documents, regardless of the time of the delivery of such documents or any sale of these securities.

For investors outside the United States: We have not taken any action to permit a public offering of the shares of our Common Stock or the possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement that we have filed with the Securities and Exchange Commission (the “SEC” or the “Commission”) utilizing a shelf registration process. Under this shelf registration process, we and the selling stockholders named herein may, from time to time, offer and sell shares of the Common Stock of the Company pursuant to this prospectus. It is important for you to read and consider all of the information contained in this prospectus and any applicable prospectus before making a decision whether to invest in the common stock.Common Stock. You should also read and consider the information contained in the documents that we have incorporated by reference as described in “Where You Can Find More Information”Information.”

ADDITIONAL INFORMATION

As permitted by SEC rules, this prospectus omits certain information that is included in the registration statement and “Incorporationits exhibits. Since the prospectus may not contain all of Certain Documents by Reference”the information that you may find important, you should review the full text of these documents. If we have filed a contract, agreement or other document as an exhibit to the registration statement, you should read the exhibit for a more complete understanding of the document or matter involved. Each statement in this prospectus.prospectus, regarding a contract, agreement other document is qualified in its entirety by reference to the actual document.

We file annual, quarterly and special reports and other information with the SEC. You may read and copy any document we file with the SEC at the SEC’s Public reference room located at 100 F Street, N.E., Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the public reference room. Our filings are also available to the public from the SEC’s web site at http://www.sec.gov.

We have three securities listed on the NYSE Amex: (1) Common Stock, $0.0001 par value (ticker symbol: IGC), (2) redeemable warrants to purchase Common Stock (ticker symbol: IGC.WT) and (3) units consisting of one share of Common Stock and two redeemable warrants to purchase Common Stock (ticker symbol: IGC.U).

We will make available on our website, www.indiaglobalcap.com, our annual reports, quarterly reports, proxy statements as well as up-to-date investor presentations. For information on HK Ironman, please visit www.hfironman.net. The registration statement and its exhibits, as well as our other reports filed with the SEC, can be inspected and copied at the SEC’s public reference room at 100 F Street, N.E., Washington, D.C 20549. The public may obtain information about the operation of the public reference room by calling the SEC at 1-800-SEC-0330 or visiting the SEC web site at http://www.sec.gov, which contains the Form S-1 and other reports, proxy and information statements and information regarding issuers that file electronically with the SEC. We do not intend to incorporate into this prospectus any of the information included on our website.

YOU SHOULD NOT ASSUME THAT THE INFORMATION CONTAINED IN THIS PROSPECTUS IS ACCURATE AS OF ANY DATE OTHER THAN THE DATE OF THIS PROSPECTUS AND THE MAILING OF THIS PROSPECTUS SHALL NOT CREATE AN IMPLICATION TO THE CONTRARY.

MARKET AND INDUSTRY DATA

The following is a summary of some of the information contained in this prospectus. In addition to this summary, we urge you to read the entire prospectus carefully, especially the risks relating to our business and common stockCommon Stock discussed under the heading “Risk Factors” and our financial statements.

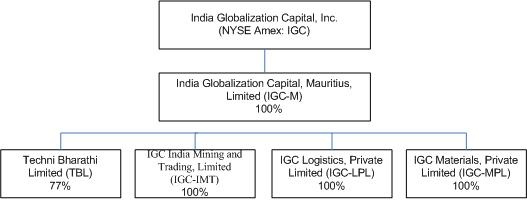

On February 19, 2009, IGC-M beneficially purchased 100% of IGC Mining and Trading Private Limited (IGC-IMT) based in Chennai, India. IGC-IMT was formed on December 16, 2008, as a privately held start-up company engaged in the business of mining and trading. Its current activity is to operate shipping hubs and to export iron ore to China from India. On July 4, 2009, IGC-M beneficially purchased 100% of IGC Materials, Private Limited (IGC-MPL based in Nagpur, India), which conducts IGC’s quarrying business, and 100% of IGC Logistics, Private Limited (IGC-LPL) based in Nagpur, India, which is involved in the transport and delivery of ore, cement, aggregate and other materials. Each of IGC-IMT, IGC-MPL and IGC-LPL were formed by third parties at the behest of IGC-M to facilitate the creation of the subsidiar ies.subsidiaries. The purchase price paid for each of IGC-IMT, IGC-MPL and IGC-LPL was equal to the expenses incurred in incorporating the respective entities with no premium paid. No officer or director of IGC had a financial interest in the subsidiaries at the time of their acquisition by IGC-M. India Globalization Capital, Inc. (the Registrant, the Company, or we) and its subsidiaries are significantly engaged in one segment,the sale of construction infrastructure.materials, mining, quarrying and construction.

On December 30, 2011, IGC acquired a 95% equity interest in Linxi HeFei Economic and 2009, we expanded our business offerings beyond construction to includeTrade Co. aka Linxi H&F Economic and Trade Co., a rapidly growing materials business. We have successfully repositioned the Company as a materials and construction firm, with construction activity in our TBL subsidiary and materials activity in our other subsidiaries. Rather than continue to owe Sricon $17.9 million, and more importantly, continue to fund two construction companies, we decreased our ownership in SriconPeople’s Republic of China-based company (“PRC Ironman”) by an amount proportionate to the loan. Effective October 1, 2009, we decreased our ownership in Sricon Infrastructure from 63% to 22.3%. The impactacquiring 100% of this is that we no longer owe Sricon $17.9 million and our corresponding ownership is a non-controlling interest. The deconsolidation of Sricon from the balance sheet of IGC r esulted in a smaller IGC balance sheet and a one-time charge to our P&L. Post deconsolidation, earnings and losses from Sricon are accounted for using the equity method of accounting.

Unless the context requires otherwise, all references in this reportprospectus to the “Company”, “IGC”, “IGC Inc.”, “we”, “our”, and “us” refer to India Globalization Capital, Inc., together with its wholly owned subsidiarysubsidiaries IGC-M and HK Ironman, Ltd. and its direct and indirect subsidiaries (TBL, IGC-IMT, IGC-MPL, IGC-LPL and IGC-LPL)PRC Ironman) and Sricon, in which we hold a non-controlling interest.

Our Business

IGC has identified the infrastructure materials business as a public (but not listedhigh growth business in both India and China as this is fundamental to the long-term development of Chinese and Indian infrastructure. In response to the increased demand for infrastructure-related construction in India and China, IGC’s focus is to supply construction materials in India and to China, as well as execute infrastructure projects. We do this entirely through our subsidiaries. We supply construction materials such as iron ore and rock aggregate to the construction industry. IGC operates rock aggregate quarries and exports iron ore to China. We build interstate highways, rural roads, and execute civil works in high temperature cement and steel plants. We are pursuing joint venture partnerships with mine owners and have applied for licenses to mine iron ore in India. We have customers in India and China and are exploring other regional opportunities. We also actively continue to pursue joint venture partnerships with mine owners for acquisition of mines and mining rights and have started materializing our efforts by acquiring PRC Ironman thru HK Ironman in China.

In March 2008, IGC completed the acquisition of interests in two companies in India, Sricon and TBL. Both companies are focused on the stock exchange) limited company on June 19, 1982 in Cochin, India.infrastructure industry. Currently, IGC owns 77% of TBL is an engineering and construction company engaged in the execution22% of civil construction, structural engineering projects and trading. TBL has a focus in the Indian states of Kerala, Karnataka, Assam and Tamil Nadu. Its present and past clients include various Indian government organizations.

Sricon. IGC Materials, Private Limited (“IGC-MPL”) and IGC Logistics, Private Limited (“IGC-LPL”) are based in Nagpur India and were incorporated in June 2009. The two companies focus on infrastructure materials like rock aggregate, bricks, concrete and other building materials, as well as, logistical support for the transportation of infrastructure materials. IGC India Mining and Trading (“IGC-IMT”) was incorporated in December 2008 in Chennai, India. IGC-IMT is focused on the export of iron ore to China.China, as well as the sale of iron ore to customers in India. IGC-MPL, IGC-LPL and IGC-IMT are all wholly-owned subsidiaries of IGC-M.

HK Ironman was incorporated as H&F Ironman Limited, a private limited company, on December 20, 2010 in Hong Kong to acquire PRC Ironman. Its registered office is at Room 17 6/F Shun on Commercial Building 112-114, Des Voeux Road Central, Hong Kong. HK Ironman’s sole asset is its ownership of a 95% equity interest in Linxi Hefei Economic and Trade Co., Ltd. (“PRC Ironman”), which was incorporated in China on January 8, 2008. HK Ironman was formed for the purpose of acquiring and owning PRC Ironman. HK Ironman acquired PRC Ironman in January 2011. As a result of that acquisition, PRC Ironman is now considered an equity joint venture (“EJV”) in view of its foreign ownership through HK Ironman. An EJV is a joint venture between a Chinese and a foreign company within the territory of China.

PRC Ironman is engaged in the processing and extraction of iron ore from sand and dirt at its beneficiation plant on 2.2 square kilometers of hills in southwest LinXi in the autonomous region of eastern Inner Mongolia, under the administration of Chifeng City, Inner Mongolia, which is located 250 miles from Beijing, 185 miles from Tianjin Port and 125 miles from Jinzhou Port and well connected by roads, planes and railroad. PRC Ironman is a Sino-foreign EJV established by both foreign and Chinese investors (i.e., Sino means “China” herein). HK Ironman, a Hong Kong-based company owns 95% of PRC Ironman, and Mr. Zhang Hua, a Chinese citizen owns the remaining 5%.

PRC Ironman’s technique for extracting ore consists of two processes. First, naturally occurring sand mixed with sparse amounts of iron ore is processed through a magnetic separator where magnets attracts the iron dust; the separation of iron from the sand is called a dry separation process. This is followed by mixing the material with water and processing the slurry through a wet magnetic separator, further purifying the material until it extracts ore that is 65-67% iron content. PRC Ironman currently mines the ore from the surrounding hills or buys sand and low-grade ore from Mongolia, processes the material to produce 66% Fe ore, and then sells the high-grade ore to steel mills and other traders in China. Its customers are mostly traders and steel mills located mostly around the port of Tianjin, China.

PRC Ironman has received a license to operate the beneficiation plant on a specific acreage of land in Inner Mongolia through August 2018. In addition, PRC Ironman has a business license, which was amended on November 28, 2011, to reflect HK Ironman’s new ownership of PRC Ironman, effective January 2011. PRC Ironman’s business objective is to operate and grow an environmentally friendly company that extracts and processes ore from barren hills and leaves in its place green acreage. PRC Ironman is located in southwest LinXi in the autonomous region of Inner Mongolia. PRC Ironman’s office is in the capital city of Chifeng. It has access via highways to Tianjin port, which gives us access to steel mills in the northeastern part of China. PRC Ironman customers come to its site to pick up the refined and processed high-grade ore. This acquisition of PRC Ironman will permit IGC to offer integrated solutions to our customers such as construction services to customers involving construction, as well as,combined with the sale and transportation of materials.

Core Business Competencies

| 1. | A sophisticated, integrated approach to project modeling, costing, management and monitoring. |

| 2. | In-depth knowledge of southern and central Indian infrastructure development as well as knowledge, history and ability to work in Inner Mongolia and Mongolia. |

| 3. | Knowledge of low cost logistics for moving commodities across long distances in specific parts of India as well as knowledge of logistics in the autonomous region of Inner Mongolia. |

| 4. | In-depth knowledge of the licensing process for mines in Inner Mongolia and southern and central India and for quarries in southern and central India. |

| 5. | Strong relationships with several important construction companies and mine operators in southern and central India and strong relationships at the appropriate levels of government in the autonomous region of Inner Mongolia. |

| 6. | Great access to the sand ore in the hills of Inner Mongolia |

Core Business Areas

Our core business areas include the following:are:

1. Mining and trading. Our mining and trading activity currently centers on the export of iron ore to China and the resale of iron ore to traders in India. India is the fourth largest producer of iron ore. The Freedonia Group projected in May 2010 that China’s $1.15 trillion construction industry would grow 9.1% every year until 2014. The Company expects that this growth may increase China’s already large demand for steel. China is a net importer of iron ore from Australia, Brazil, India and other countries. China is the largest mineral trader in the world accounting for 25% of the trading in 2010. The iron ore and steel global trade in 2010 was about $395 billion and China accounted for $83 billion or 21.1 % of the global trade. According to China’s new steel industry blueprint for its 12th 5-year plan, estimates China’s demand for iron ore could go as high as 1.13 billion tons over the next three years through 2012.

Global prices for iron ore are set through negotiations between China Steel and the large suppliers Rio Tinto, BHP Billiton and Vale. Once prices are set, the rest of the global markets follow that pricing. Prices for iron ore have increased about seven fold from 2003 to a high of $180 per metric ton at the end of 2010. In 2011, iron ore prices have been between $130 and $150 per metric ton. We believe that IGC is well positioned to provide some Chinese steel mills with the iron ore needed to meet their demand. Our subsidiary, IGC Mining and Trading Private Limited (IGC-IMT), based in Chennai, India, and our subsidiary Ironman are engaged in the iron ore business. The IGC-IMT has relationships and in some cases agreements with mine owners in Orissa and Karnataka, two of the largest ore mining belts in India. In addition, it operates facilities at seaports on the west coast of India and to a lesser extent on the east coast of India. The facilities consist of an office and a plot of land within the port to store iron ore. IGC-IMP services a customer in China by buying ore from Indian mine owners, transporting it to seaports and then subcontracting stevedores to load the ships.

Ironman is engaged in the processing and extraction of iron ore from sand and dirt at its beneficiation plant on 2.2 square kilometers of hills, which converts low-grade ore to high-grade ore through a dry and wet separation process, provides IGC with a platform in China to expand its business including to ship low-grade iron ore, which is available for export in India, to China and to convert the ore to higher-grade ore before selling it to customers in China. Ironman’s customers include local traders and steel mills near the port of Tianjin and steel mills located there. This area has excellent access roads consisting of multi-lane highways. Our staff is experienced in delivering and managing the logistics of ore transport. Even with the acquisition of Ironman, our share of the iron ore market is less than 1%. However, we have an opportunity to consolidate and grow our market share in a specific geographic area.

2. Quarrying rock aggregate. As Indian infrastructure modernizes, the demand for raw materials like rock aggregate, iron ore and similar resources is projected to increase greatly. In 2009, according to the Freedonia Group, India was the third largest stone aggregate market in the world. The report projected that Indian demand for crushed stone will increase to 770 million metric tons in 2013 and 1.08 billion metric tons in 2018. Our subsidiary, IGC Materials Private Limited (“IGC-MPL”), is responsible for our rock aggregate production. The subsidiary currently has two quarrying agreements with two separate partners. The two quarries mined near Nagpur, a city in the state of Maharashtra, India, have approximately 10-11 million metric tons of rock aggregate or about $40,000,000 of reserves at current prices. With the production of these two quarries, our subsidiary is one of the largest suppliers in the immediate area. Our share of the overall market in India is currently less than 1%. However, IGC-MPL has a growing regional presence in the Nagpur area.

All quarrying or mining activities in India require a license. IGC and its subsidiaries do not directly hold any mining or quarrying licenses and therefore there are no licenses or expenses in connection with acquiring the same being reflected in the consolidated financial statements. However, Sricon holds licenses and we operate under licenses held by our partners. For all quarries, the licenses are granted for two years. The licenses are automatically renewed for additional periods of two years, provided that all royalty payments and taxes to the Indian government are paid up to date. IGC-MPL has applied, on its own, for licenses for mining and quarrying. The process of obtaining a quarrying license is difficult and typically takes between 12-18 months. The process involves a competitive application process. As such, while we have applied for licenses, there is no assurance that we will be granted these licenses or that we will be permitted to continue to operate under partners’ licenses. IGC-MPL is also in active negotiations with other land and license owners to expand the number of producing quarries available to it.

3. Highway and heavy construction.

The Indian government has developed a plan to build and modernize Indian infrastructure. The Wall Street Journal reported on March 23, 2010 that the government plans to double infrastructure spending from $500 billion to $1 trillion. It will pay for the expansion and construction of rural roads, major highways, airports, seaports, freight corridors, railroads and townships. A significant number of our customers are engaged in highway and heavy construction.

4. Construction and maintenance of high temperature plants.

| Subsidiary | Nine months ended December 31, 2011 | Nine months ended December 31, 2010 | ||||||

TBL | 1 | % | 32 | % | ||||

IGC-IMT | 86 | % | 62 | % | ||||

IGC-MPL | 13 | % | 5 | % | ||||

IGC-LPL | 0 | % | 1 | % | ||||

PRC Ironman | - | % | - | % | ||||

Total | 100 | % | 100 | % | ||||

Customers

Our present and past customers include the National Highway Authority of India,NHAI, several state high way authorities, the Indian railways, private construction companies in India and several steel mills in China. In April 2010 we received a $160,000,000 contractChina, including local traders and steel mills near the port of Tianjin. Five of Ironman’s major customers accounted for supplying iron ore over five years to Jiya International, a large Chinese steel mill. This was followed by a $35,000,000 contract to supply ore to Tangshan Danyang Enterprises, another large customer in China. We currently92%, respectively of its total revenue for the fiscal year ended December 31, 2011 and 83%, respectively, of its total revenue for the fiscal year ended December 31, 2010. Non-renewal or/and termination of such relationship may have a backlogmaterial adverse effect on its revenue. No assurance can be given that Ironman’s business will not remain largely dependent on a limited number of approximately $200,000,000customers accounting for the supplya substantial part of iron ore to China.our revenue.

Construction contract bidding process. Contract Bidding Process

In order to create transparency, the Indian government has centralized the contract awarding process for building inter-stateinterstate roads. The new process is as follows: At the “federal” level, NHAI publishes a Statement of Work for an interstate highway construction project. The Statement of Work has a detailed description of the work to be performed, as well as, the completion time frame. The bidder prepares two proposals in response to the Statement of Work. The first proposal demonstrates technical capabilities, prior work experience, specialized machinery, manpower required, and other qualifications required to complete the project. The second proposal includes a financial bid. NHAI evaluates the technical bids and short-lists technically qualified companies. Next, the short li stlist of technically qualified companies are invited to place a detailed financial bid and show adequate financial strength in terms of revenue, net worth, credit lines, and balance sheets. Generally, the lowest bid wins the contract. Additionally, contract bidders must meet several requirements to demonstrate an adequate level of capital reserves:

1) An earnest money deposit between 2% to 10% of project costs,

2) aA performance guarantee of between 5% and 10%,

3) anAn adequate overall working capital, and

4) additionalAdditional capital available for plant and machinery.

Bidding qualifications for larger NHAI projects are set by NHAI and are imposed on each contractor. As the contractor actually executes larger highway projects, then the contractor may qualify for even larger projects.

Growth strategyStrategy and business model.Business Model

Industry reports indicate that Chinese steel consumption has continued to grow even through the global economic downturn, as China’s economy only modestly decelerated from its previous multi-year growth trajectory. Industry experts predict that growth in Chinese consumption is expected to remain a key driver for the global steel industry for a number of years to come. According to the World Steel Association, world crude steel production was 119 million metric tons (mmt) in January 2011, an increase of 5.3% from January 2010. In 2010, world crude steel production reached a record 1,414 mmt, up 15% year over year. China’s crude steel production for January 2011 was 52.8 mmt, up 0.5% year over year.

In China, the iron ore industry is broadly divided into mining and processing. The companies that hold mining licenses mine ore and sell it to steel mills directly or to processing plants. The processing plants convert ore into high-grade ore, like Ironman, or into pellets that are then sold to steel mills. Typically, low-grade ore is ore that has an iron (Fe) content of less than 52% and high-grade ore is ore with a Fe content of over 52%. The processing involves the extraction of iron ore from sand and dirt at beneficiation plants. The beneficiation process involves crushing and separating ore into valuable substances or waste by any of a variety of techniques. Ironman’s beneficiation plant extracts iron ore from a dry magnetic separation process followed by a wet separation process. PRC Ironman currently either mines ore from the hills of Inner Mongolia in their designated acreage or it buys sand and low-grade ore from Mongolia, processes the material to produce 66% Fe ore and then sells the high-grade ore to steel mills and other traders in China. Its customers are mostly traders and steel mills located mostly around the port of Tianjin, China. Our growth strategy and business model are to:

| 1) | Deepen our relationships with our existing construction customers by providing them infrastructure materials like iron ore, rock aggregate, concrete, coal and associated logistical support. |

| 2) | Expand our materials offering by expanding the number of rock aggregate quarries and other materials. |

| 3) | Leverage our expertise in the logistics and supply of iron ore by increasing the number of shipping hubs we operate from and continue to expand our offering into China and other Asian countries in order to take advantage of their expected strong infrastructure growth. |

| 4) | Consummate strategic acquisitions that would enable us to expand operations and markets in our identified areas of expertise. |

| 5) | Expand the number of recurring contracts for infrastructure build-out to customers that can benefit from our portfolio of offerings. |

Competition

We operate in an industry that is competitive. However, therethe industry is fragmented and while a large gap in the supplynumber of our competitors are well qualified and better financed contractors andthan we are, we believe that the demand for contractors.contractors in general will permit us to compete for projects and contracts that are appropriate for our size and capabilities. Large domestic and international firms compete for jumbo contracts over $250 million in size, while locally based contractors vie for contracts worth less than $5 million. We seek to compete in the gap between these two ends of the competitive spectrum. The recent capital markets crisis has made it more difficult for smaller companies to grow to mid-sized companies because their access to capital has been restrained. While we are also constrained by capital, we believe that we are in a better position to secure capital than a number of small, purely local competitors. Our construction business is positioned in the $5 million to $50 million contract range, above locally based contractors and below the large firms, creating a distinct technical and financial advantage in this market niche. niche assuming that we can maintain access to capital.

Rock aggregate is generally supplied to the industry through small crushing units, which supply low quali tyquality material. Frequently, high quality aggregate is unavailable, or is transported over large distances. We fill this gap by providing high quality material in large quantities. Further, we expect to install a large iron ore crusher that can grind ore pebbles into fine ore particles, providing a value added service to the smaller mine owners. We compete on price, quantity and quality. Iron ore is produced in India, where our core assets are located, and exported to China. While this is a fairly established business,and relatively efficient market, we compete by aggregating ore from smaller suppliers who do not have direct access to customers in China. Further, we expectAs mentioned before, Ironman’s beneficiation plant is located 185 miles from the port of Tianjin. Other than about 10 kilometers of dirt road leading over a bridge and over the hills, the access to install a large ironTianjin port and steel mills located there is excellent consisting of multi-lane highways. The competition in the immediate area consists of three other operators and is fairly limited mainly because demand for ore crusherwithin China is high and market can absorb almost any amount of ore that can grind ore pebbles into fine ore particles, providing a value added service to the smaller mine owners.is produced.

There is seasonality in our business as outdoor construction industriesactivity in India slows down during the Indian monsoons typically experienceexperiencing naturally recurring seasonal patterns throughout India. The Northeastnortheast monsoons historically arrive on June 1 annually, followed by the Southwestsouthwest monsoons, which usually continue intermittently until September. Historically, the business in the monsoon months is slower than in other months because of the heavy rains. Activities such as engineering and maintenance of high temperature plants are less susceptible to weather delays, while the iron ore export business slows down somewhat due to the rough seas. Flooding in the quarries can slow production in the stone aggregate industry during the monsoon season. However, our quarries build stone reserves prior to the monsoon season. The monsoon season has historically been used to bid and win contracts for construction and for the supply of ore and aggregate in preparation for work activity when the rains abate.

In 2011, the area of Chifeng and Inner Mongolia was subject to severe inclement weather. Typically, the months of May through September are rainy. On average, the rainfall is between 1.1 inches per month to a high of 4.7 inches per month, typically in July. This level of rainfall is not disruptive to the production of ore and in most cases the plant is operational. However, in 2011, the area received very heavy rainfall that caused significant flooding through the region and had a serious impact on PRC Ironman’s operations, as PRC Ironman could not operate the mines and the plant for more than four months. The heavy rains and flooding destroyed more than 16,000 houses and 6,000 hectares of farmland. It also destroyed the bridge connecting our production facilities to the main highways. No damage was sustained to the plant because the plant is located high in the hills. However, during that time PRC Ironman was unable to produce ore.

Employees and consultants.Consultants

As of June 30, 2010,December 31, 2011, we employed a work force of approximately 200251 employees and contract workers worldwide.in the US, India, China, Hong Kong and Mauritius. Employees are typically skilled workers including executives, engineers, accountants, sales personnel, welders, truck drivers and other specialized experts. Contract workers require less specialized skills. The truck drivers tend to be contract workers. We make diligent efforts to comply with all employment and labor regulations, including immigration laws in the many jurisdictions in which we operate. In order to attract and retain skilled employees, we have implemented a performance based incentive program, offered career development programs, improved working conditions and provided United States work assignments, technology training and other fringe benefits. Ironman tends to be the employer of choice as there are very few industries in the area it operates. We hope that our efforts will make our other companies more attractive. We are planning to provide vastly improved labor camps for our labor force. We hope that our efforts will make our companies the “employers of choice”. As of June 30, 2010 our Executive Chairman and Chief Executive Officer is Ram Mukunda and our Non-Executive Chairman is Ranga Krishna. Our Managing Director for Materials, Mining and Trading is P. M. Shivaraman. The General Manager of our rock aggregate and logistics business in India is Brigadier Kuljit Singh. Our Treasurer and Principal Accounting Officer is John Selvaraj. Our General Manager of Accounting based in India is Santhosh Kumar. We also utilize the services of several consultants who provide USGAAP systems and other expertise.

India hasand China have strict environmental, occupational, health and safety regulations. In most instances, the contracting agency regulates and enforces all regulatory requirements. As part of the mandate in the area, Ironman has undertaken a conservation effort as well as an effort to create a sustainable environment. Ironman actively plants grass and shrubs in the hills after they are excavated and uses the water from the processing plant to irrigate the grass and shrubs. We internally monitor and manage regulatory issues on a continuous basis. We believe that we are in compliance with all the regulatory requirements of the jurisdictions in which we operate. Furthermore, we do not believe that compliance will have a material adverse effect on our business activities.

Current Chinese currency revaluation.Currency Revaluation

Information and timely financial reporting.Timely Financial Reporting

Our operations are located in India and now China where the respective accepted accounting standard isstandards are the Indian GAAP which, inand the Chinese GAAP. In many cases, isthe Indian GAAP and the Chinese GAAP are not congruent with the USGAAP.U.S. GAAP. Indian and Chinese accounting standards are evolving toward IFRS (International Financial Reporting Standards). We annually conduct audits for the Company byengage independent public accounting firmfirms registered with the U.S. PCAOB. We acknowledge that thisU.S.Public Company Accounting Oversight Board (“PCAOB”) to conduct an annual audit of our financial statements. The process of producing financial statements is at times cumbersome and places significant demands upon our existing staff. We believe we are still six to twelve monthssome time away from having processes and adequately trained personnel in place to meet the reporting timetables set out by U.S. reporting requirements. Until then we may, on occasion, have to file for extensions to meet U.S. reporting timetables.timetables and it is possible that we may fail to meet these time tables. Failure to file our reports in a timely fashion can result in severe consequences including the potential delisting of our securities. In addition, our access to capital may become more difficult or limited if we fail to meet reporting deadlines. We will make our annual reports, quarte rlyquarterly reports, proxy statements and up-to-date investor presentations available on our Web site,website, www.indiaglobalcap.com, as soon as they are available. Our SEC filings are also available, free of charge, at www.sec.gov.

www.sec.gov. Please see “Risk Factors” for more information concerning the risks of investing in the Company.

Corporate Information

The mailing address of our company.principal executive office is 4336 Montgomery Avenue, Bethesda, MD 20814 and our telephone number is 301-983-0998.

| Securities offered upon the exercise of warrants: | 11,855,122 shares of common stock of IGC, par value $0.0001 per share (“Common Stock”) underlying 11,855,122 warrants having an exercise price of $5.00 per share (“IPO Warrants”). The warrants expire on March 8, 2013. | |

| 258,800 shares of Common Stock underlying 258,800 warrants having an exercise price of $1.60 per share (“2009 Warrants”). The warrants expire on September 18, 2012. | ||

| 858,610 shares of Common Stock underlying 858,610 warrants having an exercise price of$0.90 per share (“2010 Warrants”). The warrants expire on December 8, 2017. | ||

| Securities offered for Resale by Selling Stockholders: | 31,500,000 shares of Common Stock issued in connection with the acquisition of Ironman (aka “Exchange Shares”).We will not receive any proceeds from the sale by the selling shareholders of their shares of Common Stock. | |

| Shares of Common Stock outstanding before this offering: | 52,460,433 shares | |

| Shares of Common Stock to be outstanding after this offering: | 65,432,965 shares, assuming exercise of all of the currently outstanding warrants.1 | |

| IPO Warrant Terms | ||

| Exercisability: | Each warrant is exercisable for one share of Common Stock. | |

| Exercise price: | $5.00 | |

| Exercise period: | The warrants will expire at 5:00 p.m. EST on March 8, 2013 or earlier upon redemption. | |

| Redemption: | ||

We may redeem the outstanding warrants and the warrants issued to selling Stockholders, as follows: • in whole and not in part; • at a price of $.01 per warrant at any time after the warrants become exercisable; • upon a minimum of 30 days’ prior written notice of redemption; and • if, and only if, the last sales price of our Common Stock equals or exceeds $8.50 per share for any 20 trading days within a 30 trading day period ending three business days before we send the notice of redemption. | ||

| Exercisability: | Each warrant is exercisable for one share of Common Stock. | ||

| Exercise price: | $1.60 | ||

| Exercise period: | The warrants will expire at 5:00 p.m. EST on September 18, 2012. | ||

Redemption: | We do not have the right to redeem the outstanding 2009 Warrants. | ||

| 2010 Warrant Terms | |||

| Exercisability: | Each warrant is exercisable for one share of Common Stock. | ||

| Exercise price: | $0.90 | ||

| We | |||

| NYSE Amex | |||

| Units: | IGC-U | ||

| Common | IGC | ||

| IPO Warrants: | IGC-WT | ||

| Use of proceeds: | We estimate our net proceeds from this offering will be approximately $60,462,439, which assumes the exercise of all of the warrants, as set forth on the cover page of this prospectus. However, given the recent trading price of our Common Stock it is unlikely that such amounts will be realized. We intend to use any proceeds for working capital, operating expenses and other general corporate purposes. If at the time the warrants are exercised, we have incurred indebtedness, we may also use the proceeds to repay indebtedness. | ||

| Risk Factors: | Investment in our Common Stock involves substantial risks. You should read this prospectus carefully | ||

| 1 | Based on 52,460,433 shares outstanding as of March 2, 2012. Excludes 2,783,450 shares of our Common Stock issuable upon the exercise of options issued under our stock incentive plan and outstanding as of March 2, 2012, and 116,030 shares of Common Stock available for future issuance under our stock incentive plan as of March 2, 2012. |

RISK FACTORS

You should carefully consider the following risk factors, together with all of the other information included in this prospectus in evaluating us and our common stockCommon Stock and other securities. If any of the following risks and uncertainties developdevelops into actual events, they could have a material adverse effect on our business, financial condition or results of operations. In that case, the trading price of our common stockCommon Stock and other securities also could be adversely affected. We make various statements in this section, which constitute “forward-looking statements.” See “Forward-Looking Statements.”

PRC Ironman has a significant underpayment of taxes.

PRC Ironman is currently delinquent in its regulatory compliance in the People’s Republic of China due to its unpaid taxes for previous years stemming from underreported income. The taxes shown in the financial statements of PRC Ironman reflect what has been calculated as per U.S. GAAP rules, which for the financial year ended March 31, 2011, out of a total current liability of $7,300,917 was is a total of $6,763,485 in taxes payable. As of December 31, 2011, PRC Ironman had access to $2,678,119 in cash and $3,877,660 in receivables. Therefore, PRC Ironman has resources from which to pay these amounts in the event a favorable agreement is not reached with the tax authorities. IGC believes that PRC Ironman will be successful in negotiating a settlement or a concession based on oral representations made by the authorities though the resolution of this deficiency is not free from doubt. The authorities have offered concessions as part of an incentive to attract investment into a geographic area in China that needs trade, commerce, jobs and a sustainable environment. All taxes and penalties due prior to the Company’s acquisition of Ironman are the responsibility of Ironman and its stockholders before the closing of the acquisition. An unfavorable outcome could significantly reduce PRC Ironman’s cash reserves and even cause it to pay any shortfall from its current year income.

IGC may experience difficulty transferring money from China to the U.S.

Chinese currency is not freely convertible into other currencies in part because of its undervalued status. Therefore, profits made in China may have to be reinvested in China. While it is well reported in the news that China is seeking to make its currency convertible by 2015, there is no certainty that this will occur in the short-term. IGC has engaged legal counsel in China to advise on paths to move money between China and the U.S. or India, which includes the sale of PRC Ironman stock back to HK Ironman without dilution, a dividend payment or transfer pricing that involves USA overhead expenses paid out of the Chinese company.

Iron Ore Exports from India may be reduced by one-third in 2012 and beyond.

Iron ore exports from India, usually the world's third biggest supplier of the ingredient for steel, could fall a third into 2012. India's iron ore exports were already down 25 percent in April to October 2011 because of stalled shipments arising from a legal dispute in Karnataka, India and because of high transport costs. Karnataka, India normally accounts for a quarter of India’s exports. Most of India's iron ore exports go to China, which has the world's largest steel industry. India exported about half of China’s annual production until Karnataka introduced a ban on shipments in July 2010. IGC is aware of the export issues in Karnataka, India, which could cause (a) logistics pricing, (b) export bans similar to the Karnataka ban on exports elsewhere in India, and (c) increased in the export duty. If one or more of these risks materialize, IGC’s revenues could be adversely affected. IGC believes that low-grade ore remains readily available in other parts of India including both Orissa and Goa. Further, IGC’s established presence in China and India will facilitate its ability to export ore from India.

The failure to integrate Ironman’s business and operations successfully in the expected timeframe may adversely affect the combined company’s future results.

IGC believes that its acquisition of Ironman will result in certain benefits, synergies and operational efficiencies. However, to realize these anticipated benefits, the businesses of IGC and Ironman must be successfully combined. The success of the acquisition will depend on the combined company’s ability to realize these anticipated benefits from combining the businesses of IGC and Ironman. The combined company may fail to realize the anticipated benefits of the Acquisition for a variety of reasons, including:

• failure to successfully manage relationships with customers, distributors and suppliers;

• revenue attrition in excess of anticipated levels;

• failure to leverage the increased scale of the combined company quickly and effectively;

• potential difficulties integrating and harmonizing financial reporting systems;

• loss of one or more key employees;

• failure to effectively coordinate sales and marketing efforts to communicate the capabilities of the combined company; and

• failure to combine product and services offerings quickly and effectively.

The acquisition of Ironman has closed; however, the actual integration may result in additional and unforeseen expenses or delays. If the combined company is not able to integrate Ironman’s business and operations successfully, or if there are delays in combining the businesses, the anticipated benefits of the acquisition may not be realized fully or at all or may take longer to realize than expected.

The integration of IGC and Ironman may result in significant accounting charges that adversely affect the announced results of the combined company.

The financial results of the combined company may be adversely affected by cash expenses and non-cash accounting charges incurred in connection with the combination. These expenses have been preliminarily estimated to be approximately $500,000, which includes legal, accounting, due diligence and filing fee to date. In addition, under the stock purchase agreement (the “Stock Purchase Agreement”) between IGC and Ironman, Ironman’s shareholders, IGC has agreed to file a registration statement to register the shares of Common Stock issued to the Ironman stockholders for resale within 60 days of the closing of the acquisition on December 30, 2011, which will cause IGC to incur additional legal fees. The price of our Common Stock could decline to the extent our financial results are materially affected by the foregoing charges or if the foregoing charges are larger than anticipated.

IGC’s management lack’s experience in the iron ore industry.

IGC’s current officers and directors do not have experience operating a business in China and lack direct experience in the iron ore industry. IGC believes that the officers and directors of HK Ironman and PRC Ironman will remain with the companies at least one year following the closing of the Acquisition to facilitate the transition, though there is no guaranty of this result. The success of the acquisition of HK Ironman (the “Acquisition”) will depend in part on the ability of the combined company following the completion of the Acquisition to realize the anticipated benefits, including annual net operating synergies. Following the Acquisition, the size of the combined company’s business will be significantly larger than the current business of IGC. Our future success depends, in part, upon our ability to manage this expanded business, which will pose challenges for our management, including challenges related to the management and monitoring of new operations and associated increased costs and complexity. IGC cannot assure you that the combined company will be successful or that the combined company will realize the expected operating efficiencies, annual net operating synergies, revenue enhancements and other benefits currently anticipated resulting from the Acquisition. The failure to manage successfully the challenges presented after an Acquisition may result in the Company’s failure to achieve some of all of the anticipated benefits of the Acquisition. Consequently, our operations, earnings and ultimate financial success may suffer harm as a result.

Ironman has limited business insurance coverage.

Insurance companies in China currently do not offer as extensive array of insurance products as insurance companies do in the U.S. We do not have any business liability or disruption insurance to cover our operations. Any uninsured occurrence of business disruption may result in our incurring substantial costs, which could have an adverse effect on our results of operations and financial condition.

Our ability to operate effectively could be impaired if we lose key personnel or if we fail to attract qualified personnel.

We are managing our business, following the Acquisition, through a number of key personnel, including Mr. Danny Chang, Ironman’s managing director, Mr. Jianqun Dou, its deputy chairman and Mr. Wei Dong Qu, its general manager and chief operating officer. The loss of any of these key officers could have a material adverse effect on our operations. In addition, as business develops and expands, we believe that our future success will depend greatly on our continued ability to attract and retain highly skilled and qualified personnel. No assurance can be given that key personnel will continue to be employed by us or that we will be able to attract and retain qualified personnel in the future. Accordingly, if we are not able to retain these officers and/or personnel, or effectively fill vacancies created by departing key persons, our business may be impaired. The lack of key man insurance on any of these important personnel will also have an adverse effect on our financial conditions in case of the death of any of these important key personnel.

Material weaknesses in our internal controls and financial reporting, and our lack of a CFO at Ironman with sufficient U.S. GAAP experience may limit our ability to prevent or detect financial misstatements or omissions. As a result, our financial reports may not comply with U.S. GAAP and the Accounting Standards Codification. Any material weakness, misstatement or omission in our financial statements will negatively affect the market, and price of our stock which could result in significant loss to our investors.

None of the members of Ironman has experience managing and operating a public company and they rely in many instances on the professional experience and advice of third parties. While we are obligated to hire a qualified chief financial officer to enable us to meet our ongoing reporting obligations, we do not have a CFO with any significant U.S. GAAP experience for now with Ironman. Although we are actively seeking a new CFO, qualified individuals are often difficult to find, or the individual may not have all of the qualifications that we require. Therefore, we may experience “weakness” and potential problems in implementing and maintaining adequate internal controls as required under Section 404 of the Sarbanes-Oxley Act. This “weakness” also includes a deficiency, or combination of deficiencies, in internal controls over financial reporting, such that there is a reasonable possibility that a material misstatement of the company’s annual or interim financial statements will not be prevented or detected on a timely basis. Management has identified a weakness relating to the Company not having sufficient experienced personnel with the requisite technical skills and working knowledge of the application of U.S. GAAP. Projections of any evaluation of effectiveness to future periods are also subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate. This may result in significant deficiencies or material weaknesses in our internal controls, which could affect the reliability of our financial statements and prevent us from complying with SEC rules and regulations and the requirements of the Sarbanes-Oxley Act. Failure to comply or adequately comply with any laws, rules, or regulations applicable to our business may result in fines or regulatory actions, which may materially adversely affect our business, results of operation, or financial condition and could result in delays in achieving either the effectiveness of a registration statement or the development of an active and liquid trading market for our Common Stock. To the extent that the market place perceives that we do not have a strong financial staff and financial controls, the market for and price of our stock may be impaired.

Risks Related to Our Corporate Structure.

The PRC government may determine that HK Ironman’s ownership of PRC Ironman or PRC Ironman’s structure is not in compliance with applicable PRC laws, rules and regulations. If so, the relevant regulatory authorities would have broad discretion with respect to actions that could be taken in dealing with such non-compliance. Any of these actions could adversely affect our ability to manage, operate and gain the financial benefits of PRC Ironman, which would have a material adverse impact on our business, financial condition and results of operations.

IGC is conducting business in China through its subsidiary, PRC Ironman, a Sino-Foreign Equity Joint Venture (“EJV”), which is a corporation jointly invested and incorporated by foreign companies, other economic organizations or persons and Chinese companies or other economic organizations. An EJV typically is established by joint contribution, joint operation of all parties to the joint venture, and sharing of risk, profits and losses in proportion to their respective contributions towards the registered capital.

In the opinion of Gaopeng & Partners, our PRC legal counsel, PRC Ironman’s business is a foreign investment that is permitted in China. Chinese foreign investment policies classify various industries into four groups, which are encouraged, permitted, restricted and prohibited for foreign investment. Mining and processing of ferruginous sandstone and sale of refined iron powder is not in either the encouraged, restricted or prohibited groups explicitly stipulated by the Catalogue of Industries Guiding Foreign Investment, so such business is foreign investment permitted. HK Ironman entered into a share transfer agreement to purchase 95% shares of PRC Ironman from Mr. Zhang Hua and Mr. XU Jianjun in January 2011. On April 28, 2011, the share purchase was approved by the Department of Commerce of Inner Mongolia Autonomous Region. On the same day, HK Ironman was granted the Certificate of Approval for Establishment of Enterprises with Investment of Taiwan, Hong Kong, Macao and Overseas Chinese in the People’s Republic of China (Approval No. Shang Wai Zi Meng Wai Zi Shen 2011- 0023). Before the closing of the Acquisition, 95% shares of PRC Ironman is held by HK Ironman and 5% is held by Mr. Zhang Hua.

We have been advised by our PRC legal counsel that there are uncertainties regarding the interpretation and application of current and future PRC laws and regulations. If PRC Ironman were for any reason determined to be in breach of any future PRC laws or regulations, the relevant regulatory authorities would have broad discretion in dealing with such breach, including:

| · | imposing economic penalties: |

| · | discontinuing or restricting the operations of PRC Ironman; |

| · | imposing conditions or requirements with respect to HK Ironman or PRC Ironman with which HK Ironman or PRC Ironman may not be able to comply; |

| · | requiring our company to restructure the relevant ownership structure or operations; |

| · | taking other regulatory or enforcement actions that could adversely affect our company’s business; and |

| · | revoking the business licenses and/or the licenses or certificates of PRC Ironman. |

Any of these actions could adversely affect our ability to manage, operate and gain the financial benefits of PRC Ironman, which would have a material adverse impact on our business, financial condition and results of operations.

We rely on the approval certificates and business licenses held by HK Ironman and PRC Ironman. HK Ironman and PRC Ironman’s failure to renew its licenses and certificates when their terms expire with substantially similar terms as the ones it currently holds could result in our inability to operate our business.

We operate our business in China in reliance on approval certificates, business license and other requisite licenses held by HK Ironman and PRC Ironman. PRC Ironman has received a license, to operate the beneficiation plant on a specific acreage of land in Inner Mongolia through August 2018. In addition, PRC has a business license, which was amended on November 28, 2011 to reflect PRC Ironman’s new ownership by HK Ironman effective January 2011. The business license is valid through January 7, 2028. There is no assurance that HK Ironman will be able to renew its licenses and certificates in the future when their terms expire with substantially similar terms as the ones they currently hold. HK Ironman’s failure to renew its licenses and certificates when their terms expire with substantially similar terms as the ones it currently holds could result in our inability to operate our business.

Our future operating results and the market price of our Common Stock could be materially adversely affected if we are required to write down the carrying value of goodwill and investment associated with any of our businesses in the future.

We review our goodwill balance and investments for impairment on at least an annual basis through the application of a fair value-based test. Our estimate of fair value is based primarily on projected future results and cash flows and other assumptions. In addition, we review long-lived assets whenever events or changes in circumstances indicate that their carrying amounts may not be recoverable. In the fourth quarter of our 2011 fiscal year, we performed our annual test for goodwill and investment impairment and determined that our goodwill arising on account of the acquisition of TBL and our investment in Sricon was further impaired. Similarly, in the future, if our projected discounted cash flows or the recoverable value of the underlying assets associated with our businesses do not exceed the carrying value of their net assets, we may be required to record further write-downs of the carrying value of other long-lived assets associated with our businesses. If that is the case, then our operating results and the market price of our Common Stock may be adversely affected.

Our subsidiaries may become involved in litigation in the future.

Our construction and aggregate contracts are subject to the jurisdiction of the Indian courts. Our iron ore contracts frequently are subject to the jurisdiction of other foreign countries. Our subsidiaries may have to initiate actions in the Indian courts or in foreign courts to enforce their rights and may be drawn into litigation. The expenses of litigation and any judgments against us could have an adverse effect on us.

The audit report provided by Yoganandh and Ram (Y&R) will require a review by a U.S. firm.

While our audit firm, Yoganandh & Ram, is registered with the U.S. Public Company Accounting Oversight Board (the “PCAOB”), the SEC requires that the audits conducted by Yoganandh & Ram be reviewed by another PCAOB registered firm. If the review identifies changes to an audit, we will be required to amend our annual report as filed on Form 10-K incorporating the audited financial statements. During the year ended March 31, 2010, the PCAOB conducted an inspection of Yoganandh & Ram. One result of the inspection is an expected increase in our auditing expense.

Risks Associated with Doing Business in India and China.

Any downgrading of China’s or India’s debt rating by an international rating agency, or an increase in interest rates in China or India, could have a negative impact onadversely affect our ability to borrowgenerate or use Letters of Credit.

The iron ore business relies heavily on Letters of Credit. Ironman is attempting to establish a record of execution that can eventually lead to back-to-back Letters of Credit, which would greatly enhance our business and help us grow rapidly. Back-to-back Letters of Credit are used primarily in India.

A change in government policy, a downturn in the Indianglobal, Chinese or ChineseIndian economy or a natural disaster could adversely affect our business, financial condition, results of operations and future prospects.

Political, economic, social and other factors in China may adversely affect business.

Our results of operations, financial condition and prospects could be adversely affected by economic, political and legal developments in China. Since the late 1970s, the Chinese government has been reforming its economic system. These policies and measures may from time to time be modified or revised. While the Chinese economy has experienced significant growth in the past 20 years, growth has been uneven across different regions and among various economic sectors of China. Furthermore, while the Chinese government has implemented various measures to encourage economic development and guide the allocation of resources, some of these measures may also have a negative effect on us. For example, our financial condition and results of operations may be adversely affected by government control over capital investments or changes in tax regulations that are applicable to Ironman. The processing unit operated by Ironman is subject to central, provincial, local and municipal regulation and licensing in China. Compliance with such regulations and licensing can be expected to be a time-consuming, expensive process resulting in expenses which could adversely affect our margins.

Returns on investment in Chinese and Indian companies may be decreased by withholding and other taxes.

Our investment in China and India may incur tax risk unique to investment in China, India and in developing economies in general. Income that might otherwise not be subject to withholding of local income tax under normal international conventions may be subject to withholding of Chinese and/or Indian income tax. Under treaties with India and under local Indian income tax law, income is generally sourced in India and subject to Indian tax if paid from India. This is true whether or not the services or the earning of the income would normally be considered as being from sources outside India in other contexts. Additionally, proof of payment of withholding taxes may be required as part of the remittance procedure. Any withholding taxes paid by us on income from our investments in China and/or India may or may not be creditable on our income tax returns. We may also incur taxes in India on any profits that we may choose to distribute as dividends to our shareholders. We intend to avail ourselves of transfer pricing rules and minimize any Chinese and/or Indian withholding tax or local taxes. However, there is no assurance that the Chinese and/or the Indian tax authorities will always recognize such rules in its applications. We have created a foreign subsidiary in Mauritius, in order to limit the potential tax exposure in India.

Our industry depends on the stability of policies and the political situation in India and China and a change in policy could adversely affect our business.

The role of the Indian central and state governments for contracts. Their operations and financial results may be affected by changes in the government’s policy toward building infrastructure. In addition, the recent slowdown in the Indian economy on producers, consumers and regulators has caused a tightening of credit and a slowdown of companies bidding on government contracts. We foresee no immediate changes to government policy or market conditions that would adversely affect our ability to conduct business other than limited access to credit. Government support for infrastructure spending remains strong. The Wall Street Journal of May 31, 2010 reported that India plans to create an $11 billion fund t o finance new infrastructure projects. Additionally a recent Indian government Economic Survey projected rapid growth forremained significant over the next several years.

Terrorist attacks and other acts of violence or war within India or involving India and other countries could adversely affect the financial markets and our business.

Terrorist attacks and other acts of violence could have the direct effect of destroying our plants and property causing a loss and interruption of business. According to the CIA 20102011 World Factbook, religious and border disputes persist in India and remain pressing problems. For example, India has from time to time experienced civil unrest and hostilities with Pakistan and other neighboring countries. The longstanding dispute with Pakistan over the border Indian states of Jammu and Kashmir, a majority of whose populations are Muslim, remains unresolved. Fortunately, as the Council on Foreign Relations noted,While India and Pakistan have scheduled meetings in July with the hope of resumingresumed formal peace talks.

talks, there are no guarantees that these will be successful. In addition, the April 8, 2010 Economist reported India continues to struggle with insurgent attacks from Maoist-NaxaliteMaoist- Naxalite groups. If the Indian government is unable to control the violence and disruption associated with these insurgencies, then the result could be the destabilization of the economy, and, consequently, an adverse effect on our business.

Since early 2003, there have also been military hostilities and civil unrest in Afghanistan, in Iraq, and more recently in Pakistan and other Asian countries. These events could adversely affect the Indian economy, and, as a result, negatively impactaffect our business.

While we may have insurance to cover some of these risks and can file claims against the Indian contracting agencies, there can be no guarantee that we will be able to collect in a timely manner. Further, India has a fairly active insurgency and a fairly active communist following. Any serious uprising from these groups could delay our roadwork and disrupt our business. Terrorist attacks, insurgencies, or other threats of violence could slow down road building activity and the production of iron ore and rock aggregate, thereby adversely affecting our business.

Exchange controls that exist in India may limit our ability to utilize our cash flow effectively following a business combination.

We are subject to India’s rules and regulations on currency conversion. In India, the Foreign Exchange Management Act, FEMA, regulates the conversion of the Indian rupee into foreign currencies. However, as according to the Reserve Bank of India, comprehensive amendments have been made to FEMA to support the government’s policy for economic liberalization. Companies are now permitted to operate in India without any special restrictions, effectively placing them on a par with wholly-owned Indian companies. In addition, foreign exchange controls have been substantially relaxed. Notwithstanding these changes, the Indian foreign exchange market is not yet fully developed and we cannot assure that the Indian authorities will not revert back to regulating companies and imposing new restrictions on the convertibility o fof the Indian rupee. Any future restrictions on currency exchange may limit our ability to use our cash flow to fund operations outside of India.

Changes in the exchange rate of the Indian rupee may negatively impactinfluence our revenues and expenses.

Our operations are primarily located in India. We receive payment in Indian rupees for the construction work we do in India (ourand the sale of rock aggregate. Our contracts to supply iron ore to Chinese companies are paid in U.S. dollars).dollars. As the results of our operations are reported in U.S. dollars, to the extent that there is a decrease in the exchange rate of Indian rupees intorelative to U.S. dollars, such a decrease could have a material impact on our operating results or financial condition. This

Restrictions on the RMB may limit our ability to move funds out of China.

The Chinese currency, the renminbi (“RMB”), like the Indian rupee, is unlikely because,not a freely convertible currency, which could limit our ability to move money out of China freely. We would rely on the Chinese government’s foreign currency conversion policies, which may change from time to time. In China, the government has control over RMB reserves through, among other things, direct regulation of the conversion of RMB into other foreign currencies and restrictions on certain types of foreign imports. A change in the currency regulations, which lead to further restrictions, could negatively affect our ability to finance growth, or pay dividends, outside of China using the profits from China.

U.S.-listed companies with business operations in China have recently come under increased scrutiny, criticism and negative publicity.

Since 2010, a number of U.S. publicly-listed companies with substantial operations in China have been the subject of intense scrutiny, criticism and negative publicity by investors, financial commentators and regulatory agencies, such as the Wall Street Journal reportedSEC and the Justice Department resulting in mid-April, the rupee is expected to appreciate another 3% against the dollar by the enda loss of share value. Much of the year.scrutiny and negative publicity has centered around accounting weaknesses, inadequate corporate governance and, in some cases, allegations of fraud. As a result of such scrutiny and negative publicity, the stock prices of most U.S. publicly listed companies with operations in China have sharply decreased in recent months.