As filed with the Securities and Exchange Commission on March 5,16, 2004

Registration Statement No. 333-111338

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Pre-Effective

Amendment No. 23 to

FORM S-1

REGISTRATION STATEMENT

Under

The Securities Act of 1933

PERINI CORPORATION

(Exact Name of Registrant as Specified in its Charter)

| Massachusetts | 1542 | 04-1717070 | ||

(State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

73 Mt. Wayte Avenue

Framingham, MA 01701

(508) 628-2000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive office)

Robert Band

President and Chief Operating Officer

Perini Corporation

73 Mt. Wayte Avenue

Framingham, MA 01701

(508) 628-2000

(Name, address, including zip code and telephone number, including area code, of agent for service)

Copies to:

| Richard A. Soden, Esq. | Kris F. Heinzelman, Esq. | |

| Robert P. Whalen, Jr., Esq. | Cravath, Swaine & Moore LLP | |

| Goodwin Procter LLP | 825 Eighth Avenue | |

| Exchange Place | New York, New York 10019 | |

| Boston, Massachusetts 02109 | (212) 474-1000 | |

| (617) 570-1000 | Fax: (212) 474-3700 | |

| Fax: (617) 523-1231 |

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is used to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. ¨

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. The selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED ,MARCH 16, 2004

5,910,800 Shares

Common Stock

The shares of common stock are being sold by the selling stockholders. We will not receive any of the proceeds from the shares of common stock sold by the selling stockholders.

Our common stock is listed on the American Stock Exchange under the symbol “PCR.” The last reported sale price on March 2,12, 2004, was $13.70$16.47 per share.

The underwriters have an option to purchase a maximum of 886,620 additional shares to cover over-allotments of shares.

Investing in our common stock involves risks. See “Risk Factors” on page 7.

Price to Public | Underwriting Discounts and Commissions | Proceeds to Selling Stockholders | |||||||

Per Share | $ | $ | $ | ||||||

Total | $ | $ | $ | ||||||

Delivery of the shares of common stock will be made on or about , .2004.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Credit Suisse First Boston

D.A. Davidson & Co.

Morgan Joseph & Co. Inc.

The date of this prospectus is , .2004.

[Headings “Perini Building Company”, “Perini Civil Construction” and “Perini Management Services” with various pictures of completed construction sites.]

| Page | ||

| 1 | ||

| 7 | ||

| 16 | ||

| 17 | ||

| 17 | ||

| 17 | ||

| 18 | ||

| 19 | ||

MANAGEMENT’S DISCUSSIONAND ANALYSISOF FINANCIAL CONDITIONAND RESULTSOF OPERATIONS | 21 | |

| 53 | ||

| Page | ||

| 63 | ||

| 66 | ||

| 71 | ||

| 77 | ||

| 78 | ||

| 81 | ||

| 84 | ||

| 85 | ||

| 85 | ||

| 85 | ||

| F-1 | ||

You should rely only on the information contained in this document or to which we have referred you. We have not authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document.

The following summary contains information about our business and the offering of our common stock. It does not contain all of the information that you need to consider in making an investment decision. You should read this entire prospectus carefully, including the information under “Risk Factors” and our consolidated financial statements and the related notes included elsewhere in this prospectus. In this prospectus, unless the context requires otherwise, “Perini,” “we,” “us” and “our” refer to Perini Corporation, a Massachusetts corporation, and our subsidiaries, including the operations of businesses we acquired prior to the date of acquisition, and not to the underwriters.

Our Company

We are a leading construction services company, based on revenues, as ranked by Engineering News-Record, offering diversified general contracting, construction management and design-build services to private clients and public agencies throughout the world. We have provided construction services since 1894 and have established a strong reputation within our markets by executing large, complex projects on time and within budget while adhering to strict quality control measures. We offer general contracting, preconstruction planning and comprehensive project management services, including the planning and scheduling of the manpower, equipment, materials and subcontractors required for a project. We also offer self-performed construction services including earthwork,site work, concrete forming and placement and steel erection. During the nine monthsyear ended September 30,December 31, 2003, we performed work on over 100 construction projects for over 75 federal, state and local government agencies or authorities and private customers. Our headquarters are in Framingham, Massachusetts, and we have seven other principal offices throughout the United States. As of September 30,December 31, 2003, we employed approximately 3,4001,725 people. Our common stock is currently listed on the American Stock Exchange under the symbol “PCR.” We have applied for the listing of our common stock on the New York Stock Exchange. We expect our common stock to begin trading on the New York Stock Exchange in April 2004 under the symbol “PCR.”

Our business is now conducted through three primary segments: building, civil, and management services. Our building segment is comprised of Perini Building Company and James A. Cummings, Inc., or Cummings, and focuses on large, complex projects in the hospitality and gaming, sports and entertainment, educational, transportation and healthcare markets. Our civil segment is involved in public works construction primarily in the northeastern United States, including the repair, replacement and reconstruction of the United States public infrastructure such as highways, bridges and mass transit systems. Our management services segment provides diversified construction, design-build and maintenance services to the U.S. military and government agencies as well as power producers, surety companies and multi-national corporations.

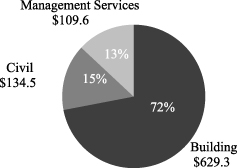

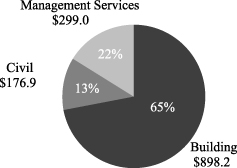

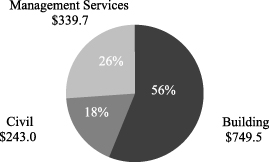

For the nine monthsyear ended September 30,December 31, 2003, our revenues were $873.4$1,374.1 million and income before income taxes was $15.0$30.9 million, which represents a 6.2%26.6% and 6.5%29.5% increase, respectively, over the same period in 2002. Our backlog was $1.33 billion$1,666.5 million as of September 30,December 31, 2003, an increase of 34.5%68.3% from $990 million at the end of 2002.

The following chart presents our revenues by segment for the nine monthsyear ended September 30,December 31, 2003 and our backlog by segment as of September 30,December 31, 2003 (in millions):

Revenue by Segment ( | Backlog by Segment (As of | |

|   |

Our Strengths

We believe our competitive position is augmented by the following principal competitive strengths:

| • | Market Leadership in Several High-Growth Building End Markets. Our significant experience, strong relationships, market leadership, design-build expertise and presence in certain key areas throughout the United States allow us to successfully compete for projects in certain end markets such as hospitality and gaming. |

| • | Extensive Experience in Complex Civil Construction. For over 100 years, we have provided specialized civil construction services, with an emphasis on large, complex projects in dense urban areas. |

| • | Responsiveness and Performance with Challenging Projects. Our clients often rely on us to respond rapidly to complete projects in challenging business or operating environments throughout the world. |

| • | Long-Term Relationships and Operating History with Clients. We maintain strong, long-term relationships with many of our clients. |

| • | Focus on Managing Contract and Project Risk. Our extensive experience and history in our markets provide us with an understanding of the risks associated with certain projects. |

| • | Experienced Management Team and Highly Skilled Workforce. Our senior management team and workforce bring significant industry work experience and specialized project expertise to our project execution capabilities. |

Our Strategy

We will seek to increase shareholder value by pursuing the following growth strategies:

| • | Leverage Leadership Position in Hospitality and Gaming Market. We intend to leverage our leadership position in this market by emphasizing our experience and our proven ability to complete challenging projects on accelerated schedules. |

| • | Extend Building Construction Expertise to Additional Markets. As we expand our market presence within particular project types or geographic areas, we will seek opportunities to cross-utilize our building construction expertise. |

| • | Pursue Expanding Federal Contracting Opportunities for Defense, Reconstruction and Security. We have well established relationships with U.S. government agencies that include, among others, the Departments of Defense and State. We will continue to pursue construction and support projects at various domestic and overseas locations such as military bases, military installations and U.S. embassies. |

| • | Seek Complex Civil Construction Projects in the Northeast. We intend to maintain and build upon our established position as a leading civil construction contractor in the northeastern United States. As one of a limited number of firms that has the ability to consistently pre-qualify for major projects, we will selectively focus on large, complex projects where our competitive advantages can be leveraged. |

| • | Focus on Margin Expansion Opportunities. We will actively seek to expand our profit margins by managing our business mix, targeting high value-added projects and continuously evaluating our corporate support and field operations cost structures. |

| • | Pursue Selected Strategic Acquisitions. We intend to supplement our internal growth and achieve strategic benefits by pursuing selected acquisitions. |

We are a Massachusetts corporation. Our principal office is located at 73 Mt. Wayte Avenue, Framingham, Massachusetts 01701 and our telephone number is (508) 628-2000.

Risk Factors

You should carefully consider the matters discussed in the “Risk Factors” section beginning on page 7 of this prospectus prior to deciding whether to invest in shares of our common stock. Some of the risks include:

The Offering

Common stock offered by the selling stockholders (1) | 5,910,800 shares | |

Common stock outstanding before and after this offering | ||

Dividend policy | We have not paid any cash dividends on our common stock since 1990 and currently do not expect to pay dividends or make any other distributions on such stock in the immediate future. | |

Use of proceeds | We will not receive any proceeds from the sale of common stock by the selling stockholders. | |

American Stock Exchange Symbol | PCR | |

| (1) | Assumes no exercise by the underwriters of their option to purchase up to 886,620 additional shares from the selling stockholders to cover over-allotments. |

All of the shares offered by this prospectus are being offered by the selling stockholders.

The number of shares of common stock outstanding before and after this offering is based on the number of shares outstanding as of December 15, 2003February 23, 2004 and excludes:

As of December 15, 2003February 23, 2004 the selling stockholders held approximately 52% of our outstanding common stock. After giving effect to this offering and assuming the full exercise of the underwriters’ option to purchase 886,620 additional shares, the selling stockholders will own approximately 22% of our outstanding common stock.

Unless otherwise indicated, the information in this prospectus assumes that the underwriters will not exercise the over-allotment option granted to them by the selling stockholders.

Our common stock is listed on the American Stock Exchange. We have applied for the listing of our common stock on the New York Stock Exchange. We expect our common stock to begin trading on the New York Stock Exchange in April 2004 under the symbol “PCR.”

Summary Consolidated Financial Data

The following summary consolidated financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Selected Historical Financial Data” and our consolidated financial statements and related notes included elsewhere in this prospectus. The summary consolidated financial data for the years ended December 31, 2003, 2002 2001 and 2000,2001, and as of December 31, 20022003 and 2001,2002, are derived from our audited consolidated financial statements included elsewhere in this prospectus. The summary consolidated financial data for the years ended December 31, 19992000 and 19981999 and as of December 31, 2001, 2000 1999 and 19981999 are derived from our audited financial statements not included in this prospectus. The summary consolidated condensed financial data for the nine months ended September 30, 2003 and 2002 and as of September 30, 2003 and 2002, are derived from our unaudited consolidated condensed financial statements included elsewhere in this prospectus. Backlog and new business awarded are not measures defined in generally accepted accounting principles and have not been derived from our consolidated financial statements. In the opinion of management the unaudited consolidated financial statements include all adjustments, consisting only of normal recurring adjustments, necessary to present fairly the information set forth therein. The historical results are not necessarily indicative of our future results of operations or financial performance and the results for the nine months ended September 30, 2003 should not be considered indicative of results expected for the full fiscal year.performance.

| Nine Months Ended September 30, | Year Ended December 31, | Year Ended December 31, | ||||||||||||||||||||||||||||||||||||||||||

| 2003 | 2002 | 2002 | 2001 | 2000 | 1999 | 1998 | 2003 | 2002 | 2001 | 2000 | 1999 | |||||||||||||||||||||||||||||||||

| (in thousands, except per share data) | (in thousands, except per share data) | |||||||||||||||||||||||||||||||||||||||||||

Statement of Operations Data: | ||||||||||||||||||||||||||||||||||||||||||||

Statement of Operations Data | ||||||||||||||||||||||||||||||||||||||||||||

CONTINUING OPERATIONS: | ||||||||||||||||||||||||||||||||||||||||||||

Revenues | $ | 873,451 | $ | 822,482 | $ | 1,085,041 | $ | 1,553,396 | $ | 1,105,660 | $ | 1,019,484 | $ | 1,011,322 | $1,374,103 | $ | 1,085,041 | $ | 1,553,396 | $ | 1,105,660 | $ | 1,019,484 | |||||||||||||||||||||

Cost of Operations | 829,590 | 784,744 | 1,026,391 | 1,495,834 | 1,053,328 | 969,015 | 957,651 | |||||||||||||||||||||||||||||||||||||

Cost Of Operations | 1,303,851 | 1,026,391 | 1,495,834 | 1,053,328 | 969,015 | |||||||||||||||||||||||||||||||||||||||

Gross Profit | 43,861 | 37,738 | 58,650 | 57,562 | 52,332 | 50,469 | 53,671 | 70,252 | 58,650 | 57,562 | 52,332 | 50,469 | ||||||||||||||||||||||||||||||||

G&A Expense | 27,709 | 22,132 | 32,770 | 28,061 | 24,977 | 26,635 | 27,397 | 39,762 | 32,770 | 28,061 | 24,977 | 26,635 | ||||||||||||||||||||||||||||||||

Income From Operations | 16,152 | 15,606 | 25,880 | 29,501 | 27,355 | 23,834 | 26,274 | |||||||||||||||||||||||||||||||||||||

Income From Construction Operations | 30,490 | 25,880 | 29,501 | 27,355 | 23,834 | |||||||||||||||||||||||||||||||||||||||

Other (Income) Expense, Net | 428 | 360 | 520 | 227 | (949 | ) | (72 | ) | 652 | (1,435) | 520 | 227 | (949 | ) | (72 | ) | ||||||||||||||||||||||||||||

Interest Expense | 701 | 1,146 | 1,485 | 2,006 | 3,966 | 7,128 | 8,473 | 1,003 | 1,485 | 2,006 | 3,966 | 7,128 | ||||||||||||||||||||||||||||||||

Income Before Income Taxes | 15,023 | 14,100 | 23,875 | 27,268 | 24,338 | 16,778 | 17,149 | 30,922 | 23,875 | 27,268 | 24,338 | 16,778 | ||||||||||||||||||||||||||||||||

Provision (Credit) for Income Taxes | (6,410 | ) | 551 | 801 | 850 | (43 | ) | 421 | 1,100 | |||||||||||||||||||||||||||||||||||

(Provision) Credit For Income Taxes | 13,096 | (801 | ) | (850 | ) | 43 | (421 | ) | ||||||||||||||||||||||||||||||||||||

Income From Continuing Operations | 21,433 | 13,549 | 23,074 | 26,418 | 24,381 | 16,357 | 16,049 | 44,018 | 23,074 | 26,418 | 24,381 | 16,357 | ||||||||||||||||||||||||||||||||

DISCONTINUED OPERATIONS: | ||||||||||||||||||||||||||||||||||||||||||||

Loss From Operations | — | — | — | — | — | (694 | ) | (4,397 | ) | |||||||||||||||||||||||||||||||||||

Loss on Disposal of Real Estate Business Segment | — | — | — | — | — | (99,311 | ) | — | ||||||||||||||||||||||||||||||||||||

Loss From Discontinued Operations | — | — | — | — | — | (100,005 | ) | (4,397 | ) | — | — | — | — | (100,005 | ) | |||||||||||||||||||||||||||||

Net Income (Loss) | $ | 21,433 | $ | 13,549 | $ | 23,074 | $ | 26,418 | $ | 24,381 | $ | (83,648 | ) | $ | 11,652 | $ | 44,018 | $ | 23,074 | $ | 26,418 | $ | 24,381 | $ | (83,648 | ) | ||||||||||||||||||

Income Available for Common Stockholders (1) | $ | 27,331 | $ | 11,955 | $ | 20,949 | $ | 24,293 | $ | 7,299 | $ | (89,917 | ) | $ | 5,743 | |||||||||||||||||||||||||||||

Income Available For Common Stockholders (1) | $ | 49,619 | $ | 20,949 | $ | 24,293 | $ | 7,299 | $ | (89,917 | ) | |||||||||||||||||||||||||||||||||

Per Share of Common Stock: | ||||||||||||||||||||||||||||||||||||||||||||

Per Share Of Common Stock: | ||||||||||||||||||||||||||||||||||||||||||||

Basic Earnings (Loss): | ||||||||||||||||||||||||||||||||||||||||||||

Income From Continuing Operations (2) | $ | 1.20 | $ | 0.53 | $ | 0.92 | $ | 1.07 | $ | 0.39 | $ | 1.80 | $ | 1.91 | ||||||||||||||||||||||||||||||

Income From Continuing Operations | $ | 2.18 | $ | 0.92 | $ | 1.07 | $ | 0.39 | $ | 1.80 | ||||||||||||||||||||||||||||||||||

Loss From Discontinued Operations | — | — | — | — | — | (0.12 | ) | (0.83 | ) | — | — | — | — | (17.84 | ) | |||||||||||||||||||||||||||||

Estimated Loss on Disposal | — | — | — | — | — | (17.72 | ) | — | ||||||||||||||||||||||||||||||||||||

Total | $ | 1.20 | $ | 0.53 | $ | 0.92 | $ | 1.07 | $ | 0.39 | $ | (16.04 | ) | $ | 1.08 | $ | 2.18 | $ | 0.92 | $ | 1.07 | $ | 0.39 | $ | (16.04 | ) | ||||||||||||||||||

Diluted Earnings (Loss): | ||||||||||||||||||||||||||||||||||||||||||||

Income From Continuing Operations (2) | $ | 1.17 | $ | 0.52 | $ | 0.91 | $ | 1.04 | $ | 0.39 | $ | 1.80 | $ | 1.91 | ||||||||||||||||||||||||||||||

Income From Continuing Operations | $ | 2.10 | $ | 0.91 | $ | 1.04 | $ | 0.39 | $ | 1.80 | ||||||||||||||||||||||||||||||||||

Loss From Discontinued Operations | — | — | — | — | — | (0.12 | ) | (0.83 | ) | — | — | — | — | (17.84 | ) | |||||||||||||||||||||||||||||

Estimated Loss on Disposal | — | — | — | — | — | (17.72 | ) | — | ||||||||||||||||||||||||||||||||||||

Total | $ | 1.17 | $ | 0.52 | $ | 0.91 | $ | 1.04 | $ | 0.39 | $ | (16.04 | ) | $ | 1.08 | $ | 2.10 | $ | 0.91 | $ | 1.04 | $ | 0.39 | $ | (16.04 | ) | ||||||||||||||||||

Weighted Average Common Shares Outstanding: | ||||||||||||||||||||||||||||||||||||||||||||

Basic | 22,726 | 22,664 | 22,664 | 22,623 | 18,521 | 5,606 | 5,318 | 22,763 | 22,664 | 22,623 | 18,521 | 5,606 | ||||||||||||||||||||||||||||||||

Diluted | 23,399 | 23,028 | 22,939 | 23,442 | 18,527 | 5,606 | 5,318 | 23,583 | 22,939 | 23,442 | 18,527 | 5,606 | ||||||||||||||||||||||||||||||||

| Nine Months Ended September 30, | Year Ended December 31, | Year Ended December 31, | ||||||||||||||||||||||||||||||||||||

| 2003 | 2002 | 2002 | 2001 | 2000 | 1999 | 1998 | 2003 | 2002 | 2001 | 2000 | 1999 | |||||||||||||||||||||||||||

| (in thousands, except per share data) | (in thousands, except per share data) | |||||||||||||||||||||||||||||||||||||

Balance Sheet Data (end of period): | ||||||||||||||||||||||||||||||||||||||

Total Assets | $ | 464,412 | $ | 395,326 | $ | 402,389 | $ | 501,241 | $ | 487,478 | $ | 385,767 | $ | 452,496 | $ | 565,443 | $ | 402,389 | $ | 501,241 | $ | 487,478 | $ | 385,767 | ||||||||||||||

Working Capital | 122,110 | 130,346 | 115,908 | 93,369 | 80,477 | 48,430 | 57,665 | 125,397 | 115,908 | 93,369 | 80,477 | 48,430 | ||||||||||||||||||||||||||

Long-term Debt, Less Current Maturities | 25,566 | 33,700 | 12,123 | 7,540 | 17,218 | 41,091 | 75,857 | 8,522 | 12,123 | 7,540 | 17,218 | 41,091 | ||||||||||||||||||||||||||

Stockholders’ Equity (Deficit) | 103,510 | 91,364 | 86,649 | 79,408 | 60,622 | (36,618 | ) | 50,558 | 120,560 | 86,649 | 79,408 | 60,622 | (36,618 | ) | ||||||||||||||||||||||||

Other Data: | ||||||||||||||||||||||||||||||||||||||

Depreciation and Amortization | $ | 2,524 | $ | 2,309 | $ | 3,202 | $ | 2,602 | $ | 2,191 | $ | 3,342 | $ | 3,059 | $ | 3,389 | $ | 3,202 | $ | 2,602 | $ | 2,191 | $ | 3,342 | ||||||||||||||

Capital Expenditures | 4,406 | 3,710 | 4,510 | 4,528 | 1,793 | 1,599 | 1,418 | 5,399 | 4,510 | 4,528 | 1,793 | 1,599 | ||||||||||||||||||||||||||

Backlog (end of period) | 1,332,148 | 1,124,818 | 990,175 | 1,213,535 | 1,788,731 | 1,658,077 | 1,232,256 | 1,666,464 | 990,175 | 1,213,535 | 1,788,731 | 1,658,077 | ||||||||||||||||||||||||||

New Business Awarded | 1,215,423 | 733,256 | 861,681 | 978,200 | 1,236,314 | 1,445,305 | 934,124 | 2,050,392 | 861,681 | 978,200 | 1,236,314 | 1,445,305 | ||||||||||||||||||||||||||

| (1) | Income available for common stockholders includes adjustments to net income for (a) accrued and unpaid dividends on our $21.25 Preferred Stock, or $2.125 Depositary Shares, (b) the reversal of previously accrued and unpaid dividends in the amount of approximately $7.3 million applicable to 440,627 of the $2.125 Depositary Shares purchased and retired by us on June 9, 2003, (c) dividends declared and paid on our Series B Preferred Stock until its exchange for shares of common stock on March 29, 2000 and (d) the $13.7 million assigned to the induced conversion of the Series B Preferred Stock into common stock on March 29, |

| (2) |

| A construction project is included in our backlog at such time as a contract is awarded or a firm letter of commitment is obtained and funding is in place. Backlog is not a measure defined in generally accepted accounting principles, or GAAP, and our backlog may not be comparable to the backlog of other companies. Management uses backlog to assist in forecasting future results. |

| New business awarded consists of the original contract price of projects added to our backlog in accordance with Note |

You should carefully consider the following risks and all other information contained in this prospectus before purchasing our common stock. If any of the following risks occur, our business, prospects, reputation, results of operations or financial condition could be harmed. In that case, the trading price of our common stock could decline, and you could lose all or part of your investment. This prospectus also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in the forward-looking statements as a result of specific factors, including the risks described below and elsewhere in this prospectus.

Risks Relating to Our Business

We are subject to significant legal proceedings, which, if determined adversely to us, could harm our reputation, preclude us from bidding on future projects and/or have a material adverse effect on us.

We are involved in various lawsuits, including the legal proceedings described under “Business—Legal Proceedings.” Some of these proceedings involve claims and judgments against us for significant amounts. For example, the litigation with the Los Angeles MTA has resulted in an award against the Tutor-Saliba-Perini joint venture (a joint venture in which we have a 40% interest), Tutor-Saliba and us, jointly and severally, for $63.0 million plus accrued interest. This award is currently being appealed by the joint venture. We do not believe that this or any other pending litigation will ultimately result in a final judgment against us that would materially adversely affect us. Litigation is, however, inherently uncertain and it is not possible to predict what the final outcome will be of any legal proceeding. A final judgment against us would require us to record the related liability and fund the payment of the judgment and, if such adverse judgment is significant, it could have a material adverse effect on us.

In addition, legal proceedings resulting in judgments or findings against us may harm our reputation and prospects for future contract awards. For example, we are defendants in a civil action brought by the San Francisco City Attorney on behalf of the City and County of San Francisco and the citizens of California, in which it is alleged, among other things, that we violated various bidding practices and minority contracting regulations and committed acts of fraud. If a final judgment is determined adversely to us, it may harm our reputation among other municipalities, which could preclude us from being qualified to bid on future municipal projects.

Our contracts require us to perform extra or change order work, which can result in disputes and adversely affect our working capital, profits and cash flows.

Our contracts generally require us to perform extra or change order work as directed by the client even if the client has not agreed in advance on the scope or price of the work to be performed. This process may result in disputes over whether the work performed is beyond the scope of the work included in the original project plans and specifications or, if the client agrees that the work performed qualifies as extra work, the price the client is willing to pay for the extra work. Even when the client agrees to pay for the extra work, we may be required to fund the cost of such work for a lengthy period of time until the change order is approved and funded by the client.

Also, these unapproved change orders, contract disputes or claims result in costs being incurred by us that cannot be billed currently and therefore, are reflected as “unbilled work” in our balance sheet. See Note 1(d) of Notes to Consolidated Financial Statements. To the extent actual recoveries with respect to unapproved change orders, contract disputes or claims are lower than our estimates, the amount of any shortfall will reduce our revenues and the amount of unbilled work recorded on our balance sheet, and could have a material adverse effect on our working capital, results of operations and cash flows. In addition, any delay caused by the extra work may adversely impact the timely scheduling of other project work and our ability to meet specified contract

milestone dates. For example, we are currently, along with our joint venture partners, pursuing a series of claims for additional contract time and compensation against the Massachusetts Highway Department for work performed by the joint venture on a portion of the Central Artery/Tunnel project in Boston, Massachusetts. During construction, the Massachusetts Highway Department ordered the joint venture to perform changes to the work and issued related direct cost changes with an estimated value, excluding time delay and inefficiency costs, in excess of $100 million. In addition, we encountered a number of unforeseen conditions during construction that greatly increased our cost of performance. See “Business—Legal Proceedings.”

Economic, political and other risks associated with our international operations involve risks not faced by our domestic competitors, which could adversely affect our revenue and earnings.

Approximately 10%18% of our revenuerevenues for the nine monthsyear ended September 30,December 31, 2003 waswere derived from our work on projects located outside of the United States. We expect non-U.S. projects to continue to contribute to our revenue and earnings for the foreseeable future. Our international operations expose us to risks inherent in doing business outside the United States, including:

Any of these factors could harm our international operations and, consequently, our business and consolidated operating results. Specifically, failure to successfully manage international growth could result in higher operating costs than anticipated or could delay or preclude altogether our ability to generate revenues in key international markets.

A decrease in U.S. government funding or change in government plans, particularly with respect to rebuilding Iraq and Afghanistan, as well as the risks associated with undertaking projects in these countries, could adversely affect the continuation of existing projects or the number of projects available to us in the future.

We recently performed design-build security upgrades at United States embassies and consulates throughout the world, and we are currently engaged in significant building and infrastructure re-construction activities in Iraq and Afghanistan. The United States federal government has recently approved a spending bill for the reconstruction and defense of Iraq and has allocated significant funds to the defense of United States interests around the world from the threat of terrorism. A decrease in government funding of these projects or a decision by the federal government to reduce or eliminate the use of outside contractors to perform this work would decrease the number of projects available to us and limit our ability to obtain new contracts in this area.

In addition, our projects in Iraq, Afghanistan and other areas of political and economic instability carry with them specific security and operational risks. Intentional or unintentional acts in those countries could result in damage to our construction sites or harm to our employees and could result in our decision to withdraw our operations from the area. Also, as a result of these acts, the federal government could decide to cancel or suspend our operations in these areas.

Increased regulation of the hospitality and gaming industry could reduce the number of future hospitality and gaming projects available, which, in turn, could adversely impact our future earnings.

The hospitality and gaming industry is regulated extensively by federal and state regulatory bodies, including state gaming commissions, the National Indian Gaming Commission and state and federal taxing and law enforcement agencies. From time to time, legislation is proposed in the legislatures of some of these jurisdictions that, if enacted, could adversely affect the tax, regulatory, operational or other aspects of the hospitality and gaming industry. Legislation of this type may be enacted in the future. The federal government has also previously considered a federal tax on casino revenues and may consider such a tax in the future. In addition, companies that operate in the hospitality and gaming industry are currently subject to significant state and local taxes and fees in addition to normal federal and state corporate income taxes, and such taxes and fees are subject to increase at any time. For example, a new tax law enacted in Nevada on July 22, 2003 increased the taxes applicable to Nevada gaming operations. Similar legislation or new hospitality and gaming regulations could deter future hospitality and gaming construction projects in jurisdictions in which we derive significant revenue. As a result, the enactment of such legislation or regulations could adversely impact our future earnings.

A decrease in government funding of infrastructure projects could reduce revenues within our civil construction business segment.

Our civil construction markets are dependent on the amount of infrastructure work funded by various governmental agencies which, in turn, depends on the condition of the existing infrastructure, the need for new or expanded infrastructure and federal, state or local government spending levels. A decrease in government funding of infrastructure projects could decrease the number of civil construction projects available and limit our ability to obtain new contracts, which could reduce revenues within our civil construction segment.

If we are unable to accurately estimate the overall risks, revenues or costs on a contract, we may achieve a lower than anticipated profit or incur a loss on the contract.

We generally enter into four principal types of contracts with our clients: fixed price contracts, cost plus award fee contracts, guaranteed maximum price contracts, and, to a lesser extent, construction management, or design-build, contracts. A significant portion of our revenues and backlog are derived from fixed price contracts. For example, approximately 25%18% of our revenues for the first nine months ofyear ended December 31, 2003 were derived from fixed price contracts. Fixed price contracts require us to perform the contract for a fixed price irrespective of our actual costs. As a result, we realize a profit on these contracts only if we successfully control our costs and avoid cost overruns. Cost plus award fee contracts provide for reimbursement of the costs required to complete a project, but generally have a lower base fee and an incentive fee based on cost and/or schedule performance. If our costs exceed the revenues available under such a contract or are not allowable under the provisions of the contract, we may not receive reimbursement for these costs. Guaranteed maximum price contracts provide for a cost plus fee arrangement up to a maximum agreed-upon price. These contracts also place the risk on us for cost overruns that exceed the guaranteed maximum price. Construction management and design-build contracts are those under which we agree to manage a project for the client for an agreed upon fee, which may be fixed or may vary based upon negotiated factors. Profitability on these types of contracts is driven by changes in the scope of work or design issues, which could cause cost overruns beyond our control and limit profits on these contracts.

Cost overruns, whether due to inefficiency, faulty estimates or other factors, result in lower profit or a loss on a project. A significant number of our contracts are based in part on cost estimates that are subject to a number of assumptions. If our estimates of the overall risks, revenues or costs prove inaccurate or circumstances change, then we may incur a lower profit or a loss on the contract.

The percentage-of-completion method of accounting for contract revenue may result in material adjustments, which could result in a charge against our earnings.

We recognize contract revenue using the percentage-of-completion method. Under this method, estimated contract revenue is recognized by applying the percentage of completion of the project for the period to the total

estimated revenue for the contract. Estimated contract losses are recognized in full when determined. Contract revenue and total cost estimates are reviewed and revised at a minimum on a quarterly basis as the work progresses and as change orders are approved, and adjustments based upon the percentage of completion are reflected in contract revenue in the period when these estimates are revised. To the extent that these adjustments result in an increase, a reduction or an elimination of previously reported contract profit, we recognize a credit or a charge against current earnings, which could be material.

We are subject to a number of risks as a government contractor, which could harm our reputation, result in fines or penalties against us and/or adversely impact our financial condition.

We are a major provider of services to government agencies and therefore are exposed to risks associated with government contracting. For example, we must comply with and are affected by laws and regulations relating to the formation, administration and performance of government contracts, such as the Federal Acquisition Regulation, the Cost Accounting Standards and Department of Defense security regulations. A violation of these laws or regulations could require us to pay fines and penalties, result in the termination of existing contracts or result in our being suspended from future government contracts. If a government agency determines that we or a subcontractor engaged in improper conduct, we may be subject to civil and criminal penalties and administrative sanctions, including termination of contracts, forfeiture of profits, suspension of payments, fines and suspension or prohibition from doing business with the government, any of which could impact our future earnings or harm our reputation.

Government clients generally can terminate or modify their contract with us at their convenience and some government contracts must be renewed annually. If a government client terminates or fails to renew a contract, our backlog may be reduced. If a government client terminates a contract due to our unsatisfactory performance, it could result in liability to us and harm our ability to compete for future contracts.

We have been, are and will be in the future, the subject of audits and cost reviews by contracting agencies, such as the United States Defense Contract Audit Agency, or the DCAA. These agencies review a contractor’s performance and may disallow costs if the agency determines that we accounted for such costs in a manner inconsistent with Cost Accounting Standards or other regulatory and contractual requirements. Therefore, a negative audit could result in a substantial adverse adjustment to our revenues and costs, harm our reputation and result in civil and criminal penalties.

Our participation in construction joint ventures exposes us to liability and/or reputational harm for failures of our partners.

We sometimes enter into joint venture arrangements with outside partners on a joint and several basis so that we can jointly bid on and execute a particular project and reduce our financial or operational risk with respect to such projects. Success on these joint projects depends in large part on whether our joint venture partners satisfy their contractual obligations. If a joint venture partner fails to perform or is financially unable to bear its portion of required capital contributions, we could be required to make additional investments and provide additional services in order to make up for our partner’s shortfall. Further, if we are unable to adequately address our partner’s performance issues, the client may terminate the project, which could result in legal liability to us, harm our reputation and reduce profit on a project.

Our pension plan is underfunded and we may be required to make significant future contributions to the plan.

Our defined benefit pension plan is a non-contributory pension plan covering substantially all of our employees. As of December 31, 2002,2003, our pension plan was underfunded by approximately $32.3$37.2 million. We are required to make cash contributions to our pension plan to the extent necessary to comply with minimum funding requirements imposed by employee benefit and tax laws. The amount of any such required contributions

is determined based on an annual actuarial valuation of the plan as performed by the plan’s actuaries. During 2002,2003, we contributed $2.4$3.0 million in cash to our defined benefit pension plan, of which $2.2 million was voluntary. Through September 30, 2003, we contributed $3.1 million to our defined benefit pension plan, of which $3.0 million was voluntary.plan. The amount of future contributions will depend upon asset returns, then-current discount rates and a number of other factors, and, as a result, the amount we may elect or be required to contribute to our pension plan in the future may increase significantly. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies—Defined Benefit Retirement Plan.”

The construction services industry is highly schedule driven, and our failure to meet schedule requirements of our contracts could adversely affect our reputation and/or expose us to financial liability.

Many of our contracts are subject to specific completion schedule requirements with liquidated damages charged to us in the event the construction schedules are not achieved. Failure to meet any such schedule requirements could cause us to suffer damage to our reputation within our industry and client base, as well as pay significant liquidated damages.

Procurement of new project awards is very competitive and our failure to compete effectively could reduce our market share and profits.

New project awards are often determined through either a competitive bid basis or a negotiated basis. Bids or negotiated contracts with public or private owners are generally awarded based upon price, but many times other factors, such as shorter project schedules or prior experience with the owner, result in the award of the contract. Within our industry, we compete with many national, regional and local construction firms. Some of these competitors have achieved greater market penetration than we have in the markets in which we compete, and some have greater financial and other resources than we do. As a result, we may need to accept lower contract margins or more fixed price or unit price contracts in order for us to compete against competitors that have the ability to accept awards at lower prices or have a pre-existing relationship with the owner. If we are unable to compete successfully in such markets, our relative market share and profits could be reduced.

Economic downturns could reduce the level of consumer spending within the hospitality and gaming industry, which could adversely affect demand for our services.

Consumer spending in the hospitality and gaming industry is discretionary and may decline during economic downturns, when consumers have less disposable income. Even an uncertain economic outlook may adversely affect consumer spending in hospitality and gaming operations, as consumers may spend less in anticipation of a potential economic downturn. Decreased spending in the hospitality and gaming market could deter new projects within the industry and the expansion or renovation of existing hospitality and gaming facilities, which could impact our revenues and earnings.

An inability to obtain bonding could limit the number of projects we are able to pursue.

As is customary in the construction business, we often are required to provide surety bonds to secure our performance under construction contracts. Our ability to obtain surety bonds primarily depends upon our capitalization, working capital, past performance, management expertise and certain external factors, including the overall capacity of the surety market. Surety companies consider such factors in relationship to the amount of our backlog and their underwriting standards, which may change from time to time. Since 2001, the surety industry has undergone significant changes with several companies withdrawing completely from the industry or significantly reducing their bonding commitment. In addition, certain re-insurers of surety risk have limited their participation in this market. Therefore, we may be unable to obtain surety bonds, which could adversely affect our results of operations and revenues.

Conflicts of interest may arise with respect to our Chairman and Chief Executive Officer.

Ronald N. Tutor, our chief executive officer and chairman of our Board of Directors, is the sole shareholder and chief executive officer of Tutor-Saliba Corporation, or Tutor-Saliba, a California corporation that beneficially

owns approximately 27% of our common stock. Mr. Tutor also devotes a substantial amount of time to the business activities of Tutor-Saliba. Tutor-Saliba is engaged in the construction industry, and, as described under “Certain Transactions,” we have participated in joint ventures with Tutor-Saliba and expect to continue to do so. Although our joint ventures with Tutor-Saliba are discussed with our Audit Committee, transactions we enter into with Tutor-Saliba could be influenced by Mr. Tutor. As in any joint venture, we could have disagreements with Tutor-Saliba over the operation of the joint ventures or the joint ventures could be involved in disputes with third parties, such as the litigation described under “Business—Legal Proceedings,” where we may or may not have an identity of interest with Tutor-Saliba. When such situations arise, we may feel constrained in aggressively pursuing all options available to us because of Mr. Tutor’s importance to us as our Chief Executive Officer and Chairman and a significant shareholder. If we face such a situation and elect to pursue options against Tutor-Saliba, it is possible that Mr. Tutor or we could terminate his management relationship with us, which could harm our reputation and impact our ability to procure future projects.

We could incur significant costs as a result of liability under environmental laws.

Our operations are subject to environmental laws and regulations governing among other things, the discharge of pollutants to air and water, the handling, storage and disposal of solid or hazardous materials or wastes and the remediation of contamination, sometimes associated with leaks or releases of hazardous substances. For example, we own, lease, or have used, in our construction, real estate and environmental remediation operations property upon which solid or hazardous wastes may have been disposed of or released. Any release of such materials or wastes by us or by third parties who operated on these properties may result in liability for investigation or remediation costs. In addition, violations of these environmental laws and regulations could subject us and our management to fines, civil and criminal penalties, cleanup costs and third party property damage or personal injury claims.

Various federal, state and local environmental laws and regulations may impose liability for the entire cost of investigation and clean-up of hazardous or toxic substances. These laws may impose liability without regard to ownership at the time of the contamination or whether or not we caused the presence of contaminants.

If we are unable to attract and retain key personnel, our reputation may be harmed and our future earnings may be negatively impacted.

Our business substantially depends on the continued service of key members of our management, particularly Ronald N. Tutor, Robert Band, Craig W. Shaw, Zohrab B. Marashlian and Michael E. Ciskey who, collectively, have an average of 29 years in the construction industry and 23 years with us. The loss of the services of any of our key senior management could have a material adverse effect on us. Our future success will also depend on our ability to attract and retain highly skilled personnel, such as engineering, project management and senior management professionals. Competition for these employees is intense, and we could experience difficulty from time to time in hiring and retaining the personnel necessary to support our business. If we do not succeed in retaining our current employees and attracting new high quality employees, our reputation may be harmed and our future earnings may be negatively impacted.

Work stoppages and other labor problems could adversely affect portions of our business, financial position, results of operations and cash flows.

We are a signatory to numerous local and regional collective bargaining agreements, both directly and through trade associations. Future agreements reached in collective bargaining could increase our operating expenses and reduce our profits as a result of increased wages and benefits. If the industry were unable to negotiate with any of the unions, it could result in strikes, work stoppages or increased operating costs as a result of higher than anticipated wages or benefits. If the unionized workers engage in a strike or other work stoppage, or other employees become unionized, we could experience a disruption of our operations and higher ongoing labor costs, which could adversely affect portions of our business, financial position, results of operations and cash flows.

We are subject to restrictive covenants under our credit facility that could limit our flexibility in managing the business.

Our credit facility imposes operating and financial restrictions on us. These restrictions include, among other things, limitations on our ability to:

In addition, our credit facility prohibits us from incurring any debt, other than debt incurred for financing our corporate headquarters, insurance premiums and construction equipment, from other sources without the consent of our lenders. The amount available to us under our credit facility at September 30,December 31, 2003 was $30.2$67.2 million.

Our credit facility contains financial covenants that require us to maintain specified working capital, tangible net worth and operating profit levels. Our credit facility also requires us to comply with a minimum interest coverage ratio. Our ability to borrow funds for any purpose will depend on our satisfying these tests. If we are unable to meet the terms of the financial covenants or fail to comply with any of the other restrictions contained in our credit facility, an event of default could occur. An event of default, if not waived by our lenders, could result in the acceleration of any outstanding indebtedness, causing such debt to become immediately due and payable. If such an acceleration occurs, we may not be able to repay such indebtedness on a timely basis. As our credit facility is secured by substantially all of our assets, acceleration of this debt could result in foreclosure of those assets. In the event of a foreclosure, we would be unable to conduct our business and may be forced to discontinue ongoing operations.

We may have difficulty raising needed capital in the future, which could limit our available working capital and our ability to make acquisitions or future investments.

We may require additional financing in order to make future investments, make acquisitions or provide needed additional working capital. Our ability to arrange such financing in the future will depend in part upon prevailing capital market conditions, as well as conditions in our business and our operating results; such factors may impact our efforts to arrange additional financing on terms satisfactory to us. We have pledged substantially all of our assets as collateral in connection with our credit facility. As a result, we may have difficulty obtaining additional financing in the future if such financing requires us to pledge our assets as collateral. Also, under our credit facility, we must obtain the consent of our lenders to incur any amount of additional debt from other sources. If additional financing is obtained by the issuance of additional shares of common stock, control of Perini may change and stockholders may suffer dilution. If adequate funds are not available, or are not available on acceptable terms, we may not be able to make future investments, take advantage of acquisition or other opportunities, or otherwise respond to competitive challenges.

Timing of the award and performance of new contracts could have an adverse effect on our operating results.

At any point in time, a substantial portion of our revenues is directly or indirectly derived from a limited number of large construction projects. It is generally very difficult to predict whether and when we will receive such awards as these contracts frequently involve a lengthy and complex bidding and selection process which is affected by a number of factors, such as market conditions, financing arrangements and governmental approvals. Because a significant portion of our revenue is generated from large projects, our results of operations and cash flows can fluctuate from quarter to quarter depending on the timing of our new contract awards.

In addition, timing of the revenues, earnings and cash flows from our projects can be delayed by a number of factors, including weather conditions, delays in receiving material and equipment from vendors and changes in the scope of work to be performed. Such delays, if they occur, could have an adverse effect on our operating results for a particular period.

We may not be able to fully realize the revenue value reported in our backlog.

As of September 30,December 31, 2003, our backlog was approximately $1.3 billion.$1,666.5 million. We include a construction project in our backlog at such time as a contract is awarded or a firm letter of commitment is obtained and funding is in place. The revenue projected in our backlog may not be realized or, if realized, may not result in profits. For example, if a project reflected in our backlog is terminated, suspended or reduced in scope, it would result in a reduction to our backlog which would reduce, potentially to a material extent, the revenue and profit we actually receive from contracts in backlog. If a client cancels a project, we may be reimbursed for certain costs but typically have no contractual right to the total revenues reflected in our backlog. Significant cancellations or delays of projects in our backlog could have a material adverse effect on our revenues and profits.

We have not paid dividends on our $21.25 Preferred Stock in several years and are currently in litigation with certain of our preferred stockholders.

Under the terms of our $21.25 Preferred Stock, the holders of shares of our $21.25 Preferred Stock are entitled to receive an annual cash dividend of $21.25 per share when and as declared by the Board of Directors out of funds legally available for such purposes. We have not paid dividends on our $21.25 Preferred Stock since 1995, though they have been fully accrued due to the “cumulative” feature of the $21.25 Preferred Stock. The holders of our $21.25 Preferred Stock have the right to elect two directors to our board in the event that dividends are in arrears for at least six quarters, and they have done so at each of our last six annual meetings of stockholders. We are currently in litigation with certain holders of our $21.25 Preferred Stock. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Dividends” and “Business—Legal Proceedings—$21.25 Preferred Shareholders Class Action Lawsuit.” If this litigation results in a final judgment against us, and such adverse judgment is significant, it could have a material adverse effect on our revenues and profits.

Our acquisition strategy involves a number of risks, which could adversely impact our future revenues and the revenues of the businesses that we acquire.

As a part of our growth strategy, we plan to pursue selective strategic acquisitions of businesses. This strategy involves risks, including diversion of management’s attention, potential loss of key employees of acquired businesses and difficulties in integrating operations and systems. We cannot be certain that we will be able to locate suitable acquisitions or consummate any such transactions on terms and conditions acceptable to us or that such transactions will be successful. An inability to successfully integrate acquired businesses into our operations could result in significant losses for us.

Risks Relating to Our Common Stock

This offering will result in a substantial amount of previously unregistered shares of our common stock being registered, which may depress the market price of our common stock.

As of December 15, 2003,February 23, 2004, the number of shares of our outstanding common stock freely tradeable on the American Stock Exchange and not owned by our officers, directors, or affiliates was approximately 5.55.4 million. The sale of the shares of common stock in this offering could depress the market price of our common stock.

Future sales of a substantial amount of our common stock may cause our stock price to decline.

Upon completing this offering, we will have approximately 22.923.0 million shares of common stock outstanding. Our principal stockholders, directors and executive officers will own approximately 11.5 million of

these shares. These stockholders will be free to sell those shares, subject to the limitations of Rule 144 or Rule 144(k) under the Securities Act of 1933, as amended (which are discussed under “Shares Eligible for Future Sale”), applicable restrictions on transfer contained in our shareholders agreement and, subject to certain exceptions, the 90-day lock-up agreements that these stockholders will enter into with the underwriters. See “Underwriting.” In addition, after giving effect to the sale of shares in this offering (excluding any exercise of the over-allotment option granted to the underwriters), the holders of approximately11.8 million of our shares (including warrants to purchase 420,000 shares of our common stock which are not subject to lock-up agreements) have the right to require us to register all or part of their shares under registration rights agreements. See “Description of Capital Stock—Registration Rights Agreements” for a more detailed discussion of the registration rights agreements. Registration of these restricted shares of common stock would permit their sale into the public market immediately. See “Shares Eligible for Future Sale.” We cannot predict when these stockholders may sell their shares or in what volumes. However, the market price of our common stock could decline significantly if these stockholders sell a large number of shares into the public market after this offering or if the market believes that these sales may occur.

We may also issue our common stock from time to time as consideration for future acquisitions and investments. In the event any such acquisition or investment is significant, the number of shares of our common stock that we may issue could in turn be significant. In addition, we may also grant registration rights covering those shares in connection with any such acquisitions and investments.

Limited trading volume of our common stock may contribute to its price volatility.

Our common stock is traded on the American Stock Exchange. For the fourth quarter of 2003, the average daily trading volume for our common stock as reported by the American Stock Exchange was approximately 22,400 shares. Even if we achieve a wider dissemination by means of the shares offered pursuant to this prospectus, we are uncertain as to whether a more active trading market in our common stock will develop. As a result, relatively small trades may have a significant impact on the price of our common stock.

Our stock price has been and may continue to be volatile and may result in substantial losses for investors.

The market price of our common stock has been, and is likely to continue to be, volatile. Since January 1, 2003, the market price for our common stock has been as high as $14.90$16.70 per share and as low as $3.62 per share. Additionally, the stock market in general has been highly volatile since 2000. This volatility in stock price often has been unrelated to our operating performance.

In addition, the trading price of our common stock could be subject to wide fluctuations in response to:

Fluctuations in our stock price as a result of any of the foregoing factors may result in substantial losses for investors.

Fluctuations in our quarterly revenues and operating results may lead to reduced prices for our stock.

Because our operating results are primarily generated from a limited number of significant active construction projects, operating results in any given fiscal quarter can vary depending on the timing of progress

achieved and changes in the estimated profitability of the projects being reported. Progress on projects in certain areas may also be delayed by weather conditions. Such delays, if they occur, may result in inconsistent quarterly operating results due to more or less progress than anticipated being achieved on certain projects, which may in turn lead to reduced prices for our stock.

Ownership of our common stock is concentrated among a few stockholders who could act in a way that favors their interests to the detriment of our interests and those of other stockholders.

Following this offering and assuming that all of the selling stockholders sell all of the shares of common stock being registered in this offering, the percentage of shares owned by our executive officers, directors and 5% stockholders would be reduced to 50.2%49.8%. These stockholders have the powerability to controlsignificantly influence the outcome of the election of most of our directors, and the approval of any action requiring majority approval of our common stockholders, including certain amendments to our charter. In addition, without the consent of these stockholders, we may not be able to enter into transactions that could be beneficial to us or our other stockholders.

Provisions of Massachusetts law and of our charter and bylaws may make a takeover of us more difficult, which could impede the ability of our stockholders to benefit from a change in control or to change our management and Board of Directors.

Provisions in our restated articles of organization and bylaws and in the Massachusetts corporate law may make it difficult and expensive for a third party to pursue a tender offer, change in control or takeover attempt which is opposed by our management and Board of Directors. Public stockholders who might desire to participate in such a transaction may not have an opportunity to do so. Our bylaws provide for a staggered Board of Directors which makes it difficult for stockholders to change the composition of the Board of Directors in any one year. Our Board of Directors has the authority to issue preferred stock with voting or other rights or preferences that could impede the success of any attempt to effect a change in control or takeover of Perini. Also, we have adopted a rights plan that limits the ability of any person to acquire more than 10% of our common stock, except in limited circumstances. These anti-takeover provisions could substantially impede the ability of public stockholders to benefit from a change in control or to change our management and Board of Directors. See “Description of Capital Stock.”

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

The statements contained in this prospectus, including under the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and other sections of this prospectus that are not purely historical are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, including without limitation, statements regarding Perini’s or our management’s expectations, hopes, beliefs, intentions or strategies regarding the future. These forward-looking statements are based on our current expectations and beliefs concerning future developments and their potential effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by such forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading “Risk Factors.” We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise except as may be required under applicable securities laws.

We will not receive any proceeds from the sale of shares by the selling stockholders or the additional shares to be sold by the selling stockholders if the underwriters exercise their over-allotment option.

We have not paid any cash dividends on our common stock since 1990. For the foreseeable future, we intend to retain any earnings in our business and we do not anticipate paying any cash dividends. In addition, under the terms of our preferred stock, we cannot pay dividends on our common stock until all accrued dividends on our preferred stock have been paid. Whether or not to declare any dividends will be at the discretion of our Board of Directors, considering then existing conditions, including our financial condition and results of operations, capital requirements, bonding prospects, contractual restrictions, business prospects and other factors that our Board of Directors considers relevant.

MARKET PRICE OF OUR COMMON STOCK

Our common stock is traded on the American Stock Exchange under the symbol “PCR.” The quarterly market high and low sales prices for our common stock for 2004 (through March 2,16, 2004), 2003, and 2002 are summarized below:

| High | Low | High | Low | |||||||

Year Ending December 31, 2002 | ||||||||||

First Quarter | 7.28 | 5.75 | $ | 7.28 | $ | 5.75 | ||||

Second Quarter | 6.40 | 3.40 | 6.40 | 3.40 | ||||||

Third Quarter | 4.58 | 3.50 | 4.58 | 3.50 | ||||||

Fourth Quarter | 4.44 | 3.00 | 4.44 | 3.00 | ||||||

Year Ending December 31, 2003 | ||||||||||

First Quarter | 4.70 | 3.62 | 4.70 | 3.62 | ||||||

Second Quarter | 9.05 | 3.80 | 9.05 | 3.80 | ||||||

Third Quarter | 8.99 | 6.26 | 8.99 | 6.26 | ||||||

Fourth Quarter | 10.10 | 6.95 | 10.10 | 6.95 | ||||||

Year ending December 31, 2004 | ||||||||||

First Quarter (through March 2, 2004) | 14.90 | 8.80 | ||||||||

First Quarter (through March 16, 2004) | 16.70 | 8.80 | ||||||||

On March 2,16, 2004, the closing sale price of our common stock as reported on the American Stock Exchange was $13.70$16.47 per share. At March 2,16, 2004, there were 1,0411,038 holders of record of our common stock, based on the stockholders list maintained by our transfer agent.

Our common stock is listed on the American Stock Exchange. We have applied for the listing of our common stock on the New York Stock Exchange. We expect our common stock to begin trading on the New York Stock Exchange in April 2004 under the symbol “PCR.”

The table below sets forth our consolidated short-term debt and capitalization as of September 30,December 31, 2003 (in thousands, except share data). We have not provided an adjusted capitalization table because we will not receive any of the proceeds from this offering. You should read the following information in conjunction with our consolidated financial statements and related notes and the information provided under the captions “Selected Historical Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” which are included elsewhere in this prospectus.

Short-term debt: | ||||||||

Notes payable to banks | $ | – | $ | – | ||||

Current maturities of long-term debt | 831 | 490 | ||||||

Total short-term debt | $ | 831 | $ | 490 | ||||

Long-term debt: | ||||||||

Mortgages on real estate | $ | 8,489 | $ | 8,426 | ||||

Revolving credit loans (1) | 17,000 | — | ||||||

Other indebtedness | 77 | 96 | ||||||

Total long-term debt | 25,566 | 8,522 | ||||||

Stockholders’ equity: | ||||||||

Preferred stock, $1.00 par value | ||||||||

Authorized - 1,000,000 shares | ||||||||

Designated, issued and outstanding – 55,927 shares, aggregate liquidation preference of $13,982 | 56 | 56 | ||||||

Series A junior participating preferred stock, $1.00 par value | ||||||||

Designated - 200,000 shares | ||||||||

Issued – none | – | – | ||||||

Stock purchase warrants | 2,233 | 2,233 | ||||||

Common stock, $1.00 par value | ||||||||

Authorized - 40,000,000 shares (2) | ||||||||

Issued – 22,903,064 shares (2) | 22,903 | |||||||

Issued – 22,946,064 shares (2) | 22,946 | |||||||

Paid-in surplus (2) | 91,137 | 90,296 | ||||||

Retained earnings | 7,719 | 30,007 | ||||||

Less - common stock in treasury, at cost - 60,529 shares (2) | (965 | ) | (965 | ) | ||||

Accumulated other comprehensive loss | (19,573 | ) | (24,013 | ) | ||||

Total stockholders’ equity | 103,510 | 120,560 | ||||||

Total capitalization | $ | 129,076 | $ | 129,082 | ||||

| (1) | The revolving credit facility provides for revolving loans up to a maximum of $50 million to June 20, 2005, at which time any amounts unpaid convert to a three-year term loan with equal quarterly principal payments. The weighted average interest rate at |

| (2) | As of |

SELECTED HISTORICAL CONSOLIDATED FINANCIAL DATA

The selected historical consolidated financial data shown below for the five-year period ended December 31, 20022003 has been derived from our consolidated financial statements audited by Deloitte & Touche LLP (three-year(four-year period ended December 31, 2002)2003) and by Arthur Andersen LLP (two-year(one-year period ended December 31, 1999), our current and former independent auditors, respectively.

The information for the nine months ended September 30, 2003 and 2002 has been derived from unaudited consolidated condensed financial statements and, in our opinion, includes all adjustments (consisting only of normal recurring adjustments) necessary to present fairly such financial information in accordance with generally accepted accounting principles applied on a consistent basis. Our results are generated from a limited number of significant active construction projects. Consequently, quarterly results can vary depending on the timing of progress and changes in the estimated profitability of the projects being reported. For the foregoing and other reasons, results for the nine months ended September 30, 2003 may not necessarily be indicative of results to be expected for the full year ended December 31, 2003. Backlog and new business awarded are not measures defined in generally accepted accounting principles and have not been derived from our consolidated financial statements. The selected historical consolidated financial data should be read in conjunction with our consolidated financial statements and related notes, “Capitalization” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” which are included elsewhere in this prospectus.

| Nine Months Ended September 30, | Year Ended December 31, | Year Ended December 31, | ||||||||||||||||||||||||||||||||||||||||||

| 2003 | 2002 | 2002 | 2001 | 2000 | 1999 | 1998 | 2003 | 2002 | 2001 | 2000 | 1999 | |||||||||||||||||||||||||||||||||

| (in thousands, except per share data) | (in thousands, except per share data) | |||||||||||||||||||||||||||||||||||||||||||

Statement of Operations Data: | ||||||||||||||||||||||||||||||||||||||||||||

CONTINUING OPERATIONS: | ||||||||||||||||||||||||||||||||||||||||||||

Revenues | $ | 873,451 | $ | 822,482 | $ | 1,085,041 | $ | 1,553,396 | $ | 1,105,660 | $ | 1,019,484 | $ | 1,011,322 | $1,374,103 | $ | 1,085,041 | $ | 1,553,396 | $ | 1,105,660 | $ | 1,019,484 | |||||||||||||||||||||

Cost of Operations | 829,590 | 784,744 | 1,026,391 | 1,495,834 | 1,053,328 | 969,015 | 957,651 | |||||||||||||||||||||||||||||||||||||

Cost Of Operations | 1,303,851 | 1,026,391 | 1,495,834 | 1,053,328 | 969,015 | |||||||||||||||||||||||||||||||||||||||

Gross Profit | 43,861 | 37,738 | 58,650 | 57,562 | 52,332 | 50,469 | 53,671 | 70,252 | 58,650 | 57,562 | 52,332 | 50,469 | ||||||||||||||||||||||||||||||||

G&A Expense | 27,709 | 22,132 | 32,770 | 28,061 | 24,977 | 26,635 | 27,397 | 39,762 | 32,770 | 28,061 | 24,977 | 26,635 | ||||||||||||||||||||||||||||||||

Income From Operations | 16,152 | 15,606 | 25,880 | 29,501 | 27,355 | 23,834 | 26,274 | |||||||||||||||||||||||||||||||||||||

Income From Construction Operations | 30,490 | 25,880 | 29,501 | 27,355 | 23,834 | |||||||||||||||||||||||||||||||||||||||

Other (Income) Expense, Net | 428 | 360 | 520 | 227 | (949 | ) | (72 | ) | 652 | (1,435) | 520 | 227 | (949 | ) | (72 | ) | ||||||||||||||||||||||||||||

Interest Expense | 701 | 1,146 | 1,485 | 2,006 | 3,966 | 7,128 | 8,473 | 1,003 | 1,485 | 2,006 | 3,966 | 7,128 | ||||||||||||||||||||||||||||||||

Income Before Income Taxes | 15,023 | 14,100 | 23,875 | 27,268 | 24,338 | 16,778 | 17,149 | 30,922 | 23,875 | 27,268 | 24,338 | 16,778 | ||||||||||||||||||||||||||||||||

Provision (Credit) for Income Taxes | (6,410 | ) | 551 | 801 | 850 | (43 | ) | 421 | 1,100 | |||||||||||||||||||||||||||||||||||

(Provision) Credit For Income Taxes | 13,096 | (801 | ) | (850 | ) | 43 | (421 | ) | ||||||||||||||||||||||||||||||||||||

Income From Continuing Operations | 21,433 | 13,549 | 23,074 | 26,418 | 24,381 | 16,357 | 16,049 | 44,018 | 23,074 | 26,418 | 24,381 | 16,357 | ||||||||||||||||||||||||||||||||

DISCONTINUED OPERATIONS: | ||||||||||||||||||||||||||||||||||||||||||||

Loss From Operations | – | – | – | – | – | (694 | ) | (4,397 | ) | |||||||||||||||||||||||||||||||||||

Loss on Disposal of Real Estate Business Segment | – | – | – | – | – | (99,311 | ) | – | ||||||||||||||||||||||||||||||||||||

Loss From Discontinued Operations | – | – | – | – | – | (100,005 | ) | (4,397 | ) | – | – | – | – | (100,005 | ) | |||||||||||||||||||||||||||||

Net Income (Loss) | $ | 21,433 | $ | 13,549 | $ | 23,074 | $ | 26,418 | $ | 24,381 | $ | (83,648 | ) | $ | 11,652 | $ | 44,018 | $ | 23,074 | $ | 26,418 | $ | 24,381 | $ | (83,648 | ) | ||||||||||||||||||

Income Available for Common Stockholders (1) | $ | 27,331 | $ | 11,955 | $ | 20,949 | $ | 24,293 | $ | 7,299 | $ | (89,917 | ) | $ | 5,743 | |||||||||||||||||||||||||||||

Income Available For Common Stockholders (1) | $ | 49,619 | $ | 20,949 | $ | 24,293 | $ | 7,299 | $ | (89,917 | ) | |||||||||||||||||||||||||||||||||

Per Share Of Common Stock: | ||||||||||||||||||||||||||||||||||||||||||||

Basic Earnings (Loss): | ||||||||||||||||||||||||||||||||||||||||||||

Income From Continuing Operations | $ | 2.18 | $ | 0.92 | $ | 1.07 | $ | 0.39 | $ | 1.80 | ||||||||||||||||||||||||||||||||||

Loss From Discontinued Operations | — | — | — | — | (17.84 | ) | ||||||||||||||||||||||||||||||||||||||

Total | $ | 2.18 | $ | 0.92 | $ | 1.07 | $ | 0.39 | $ | (16.04 | ) | |||||||||||||||||||||||||||||||||

Diluted Earnings (Loss): | ||||||||||||||||||||||||||||||||||||||||||||

Income From Continuing Operations | $ | 2.10 | $ | 0.91 | $ | 1.04 | $ | 0.39 | $ | 1.80 | ||||||||||||||||||||||||||||||||||

Loss From Discontinued Operations | — | — | — | — | (17.84 | ) | ||||||||||||||||||||||||||||||||||||||

Total | $ | 2.10 | $ | 0.91 | $ | 1.04 | $ | 0.39 | $ | (16.04 | ) | |||||||||||||||||||||||||||||||||

Weighted Average Common Shares Outstanding: | ||||||||||||||||||||||||||||||||||||||||||||

Basic | 22,763 | 22,664 | 22,623 | 18,521 | 5,606 | |||||||||||||||||||||||||||||||||||||||

Diluted | 23,583 | 22,939 | 23,442 | 18,527 | 5,606 | |||||||||||||||||||||||||||||||||||||||

Balance Sheet Data (end of period): | ||||||||||||||||||||||||||||||||||||||||||||

Total Assets | $ | 565,443 | $ | 402,389 | $ | 501,241 | $ | 487,478 | $ | 385,767 | ||||||||||||||||||||||||||||||||||

Working Capital | 125,397 | 115,908 | 93,369 | 80,477 | 48,430 | |||||||||||||||||||||||||||||||||||||||

Long-term Debt, Less Current Maturities | 8,522 | 12,123 | 7,540 | 17,218 | 41,091 | |||||||||||||||||||||||||||||||||||||||

Stockholders’ Equity (Deficit) | 120,560 | 86,649 | 79,408 | 60,622 | (36,618 | ) | ||||||||||||||||||||||||||||||||||||||