As filed with the Securities and Exchange Commission on FebruaryApril 11, 2005

Registration No. 333-121407

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 13

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

LAZARD LTD

(Exact name of Registrant as specified in its charter)

| Bermuda | 6199 | 98-0437848 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

Clarendon House

2 Church Street

Hamilton HM 11, Bermuda

(441) 295-1422

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Scott D. Hoffman, Esq.

Lazard Ltd

30 Rockefeller Plaza

New York, New York 10020

(212) 632-6000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Adam D. Chinn, Esq. Craig M. Wasserman, Esq. Gavin D. Solotar, Esq. Wachtell, Lipton, Rosen & Katz 51 West 52nd Street New York, New York 10019 (212) 403-1000 | Kris F. Heinzelman, Esq. Erik R. Tavzel, Esq. Cravath, Swaine & Moore LLP Worldwide Plaza 825 Eighth Avenue New York, New York 10019 (212) 474-1000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, please check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434 under the Securities Act, please check the following box. ¨

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to Be Registered | Proposed Maximum Offering Price (1) | Amount of Registration Fee (2) | Proposed Maximum Offering Price (1) | Amount of Registration Fee (2) | ||||||||

Class A common stock, par value $0.01 per share | $ | 850,000,000 | $ | 100,045 | $ | 945,925,182 | $ | 111,335 | ||||

| (1) | Estimated solely for purposes of calculating the amount of the registration fee in accordance with Rule |

| (2) |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to such Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion. DatedFebruaryDatedApril 11, 2005.

30,464,579 Shares

Class A Common Stock

This is an initial public offering of shares of Class A common stock, which we refer to as common stock, of Lazard Ltd, or “Lazard”.“Lazard.” All of the shares of common stock are being sold by Lazard.

Prior to this offering, there has been no public market for the common stock. It is currently estimated that the initial public offering price per share will be between $$25.00 and $ .$27.00. Lazard intends to applyhas applied for listing of the common stock on the New York Stock Exchange under the symbol “LAZ”.

In addition to offering these shares of common stock, Lazard concurrently is offering pursuant to a separate prospectus $250 million of equity security units, plus up to an additional $37.5 million of equity security units if the underwriters for that offering exercise their option to purchase additional equity security units. Lazard LLC also is offering $650 million in principal amount of senior, unsecured notes concurrently in a private placement. The completion of this offering of common stock is subject to the completion of the offering of equity security units and the private placement of the Lazard LLC senior notes and also is subject to satisfaction of the conditions to the separation described in this prospectus. Lazard also intends to sell $150 million of equity security units and $50 million of our common stock to a third party in a private placement upon closing of this offering.

See “Risk Factors” beginning on page2127 to read about important factors you should consider before buying shares of the common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||

Initial public offering price | $ | $ | ||||

Underwriting discount | $ | $ | ||||

Proceeds, before expenses, to Lazard | $ | $ | ||||

To the extent that the underwriters sell more than 30,464,579 shares of common stock, the underwriters have the option to purchase up to an additional 4,569,687 shares of common stock from Lazard at the initial public offering price less the underwriting discount.

The underwriters expect to deliver the shares against payment in New York, New York on , 2005.

Goldman, Sachs & Co.

Citigroup

Lazard

Merrill Lynch & Co.

Morgan Stanley

| Credit Suisse First Boston | JPMorgan | |

Prospectus dated , 2005.

Our Core Values

Integrity. We take great pride in the tradition of integrity that we have developed over 156 years.

Independence. We are dedicated to offering our clients independent, trusted and unbiased advice. We limit our participation in conflicting business activities.

| Ÿ | Established 1848 |

Excellence. We endeavor to deliver service of exceptional quality to our clients, custom-tailored to their unique needs.

| Ÿ | Presence in 27 cities in 15 countries |

Intellectual Capital. Our people are our product, and intellectual capital is our principal asset. We therefore focus on attracting, training and retaining the best talent.

Clients. We take a client-centric perspective, attuned to their local needs. We emphasize a long-term approach to client relationships.

Heritage. Our heritage is distinctively Euro-American with deep, long-standing roots through local offices in our key markets. We link these offices together through a global network of industry expertise for the benefit of our clients.

Culture. Ours is an entrepreneurial culture that celebrates the individual while emphasizing teamwork. We strive to innovate and adapt as our markets change.

Ownership. Our managing directors are among our largest owners. We manage our business with an owner’s orientation focused on long-term stockholder returns.

Citizenship. We are deeply aware of the importance of our conduct to our employees, business partners, clients, regulators, investors and the public at large. Above all, we must earn and maintain their trust in all our daily endeavors.

Our Business

| Ÿ | Executive offices in Paris, London, Milan and New York |

Financial Advisory | Asset Management | |

Ÿ 2004 Net Ÿ | Ÿ 2004 Net Ÿ 35 managing directors | |

2004 Net Revenue

| Assets Under Management $ | |

| ||

INTRODUCTORY NOTEPROSPECTUS SUMMARY

This is a public offering of Class A common stock of Lazard Ltd, which will be the holding company for the public’s common equity interests in our company. Unless the context otherwise requires, the terms:

| Ÿ | “Lazard,” “we,” “us” and “our” refer to Lazard Ltd, a newly-formed company incorporated under the laws of Bermuda, and its subsidiaries, including Lazard Group (as defined below) and the businesses, subsidiaries, assets and liabilities that Lazard Group will retain after the completion of the transactions described in this prospectus, and |

| Ÿ | “Lazard Group” refers to Lazard LLC, a Delaware limited liability company that is the current holding company for our businesses, which will be renamed Lazard Group LLC in connection with this offering and in which Lazard Ltd will acquire a controlling interest upon completion of this offering. |

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. The distribution of this prospectus and sale of these securities in certain jurisdictions may be restricted by law. Persons in possession of this prospectus are required to inform themselves about and observe any such restrictions. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate as of the date on the front cover of this prospectus only. Our business, financial condition, results of operations and prospects may have changed since that date.

This is a public offering of Class A common stock of Lazard Ltd, which will be the holding company for the public’s common equity interests in Lazard LLC, which we refer to in this prospectus as “Lazard Group.”

Unless the context otherwise requires, the terms:

The Bermuda Monetary Authority has classified us as a non-resident of Bermuda for exchange control purposes. Accordingly, the Bermuda Monetary Authority does not restrict our ability to engage in transactions in currencies other than Bermuda dollars, to transfer funds in and out of Bermuda or to

i

pay dividends to non-Bermuda residents who are stockholders, other than in Bermuda dollars. We have received consent under the Exchange Control Act 1972 from the Bermuda Monetary Authority for the issue and transfer of the common stock to and between non-residents of Bermuda for exchange control purposes, provided that our shares remain listed on an appointed stock exchange, which includes the New York Stock Exchange, or the “NYSE.” This prospectus will be filed with the Registrar of Companies in Bermuda in accordance with Bermuda law. In granting such consent and in accepting this prospectus for filing, neither the Bermuda Monetary Authority nor the Registrar of Companies in Bermuda accepts any responsibility for our financial soundness or the correctness of any of the statements made or opinions expressed in this prospectus.

We report our financial statements in U.S. dollars and prepare our financial statements, including all of the financial statements included in this prospectus, in conformity with accounting principles generally accepted in the U.S., or “U.S. GAAP.” We have adopted a fiscal year end of December 31. In this prospectus, except where otherwise indicated, references to “$” or “dollars” are to the lawful currency of the U.S.

The Lazard logo and the other trademarks, trade names and service marks of Lazard mentioned in this prospectus, including Lazard®, are the property of, and are used with the permission of, Lazard Group and its subsidiaries.

ii

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider before investing in our Class A common stock, which we refer to in this prospectus as our common“common stock.” You should read this entire prospectus carefully, especially the risks of investing in our common stock discussed under “Risk Factors.”

Lazard

We are a preeminent international financial advisory and asset management firm that has long specialized in crafting solutions to the complex financial and strategic challenges of our clients. We serve a diverse set of clients around the world, including corporations, partnerships, institutions, governments and high-net worth individuals. We believe that what sets us apart is our dedication to:

| Ÿ | competing on the basis of our intellectual (rather than financial) capital, which is personified by our team of highly skilled professionals, |

| Ÿ | demanding excellence and superior quality in all that we do, |

| Ÿ | cultivating long-term, senior-level relationships with clients, through deep roots in local markets, |

| Ÿ | linking together our local offices through a global network of industry expertise, |

| Ÿ | remaining focused on our chosen lines of business to provide the highest degree of expertise and continuous innovation, |

| Ÿ | emphasizing our tradition of integrity in all our dealings, and |

| Ÿ | offering independent, trusted and unbiased advice. |

Lazard was founded in 1848, expanded shortly thereafter to provision the needs of the California gold rush, and eventually evolved its business exclusively into financial services. Having recently united the historical New York, Paris and London “Houses” of Lazard under Lazard Group, we operate

today from 27 cities in key business and financial centers across 15 countries in Europe, North America, Asia and Australia. We believe that the mix of our activities across business segments, geographic regions, industries and investment strategies helps to diversify and stabilize our revenue stream.

Our Strategic Positioning

We focus primarily on two business segments, Financial Advisory (including our Mergers and Acquisitions and Financial Restructuring practices) and Asset Management. Since January 2002, when new senior management joined our firm, we have made significant reinvestments in the intellectual capital of our business to strengthen ourselves for future growth and profitability. As a result of our strategic initiatives, we believe that we are now positioned such that:

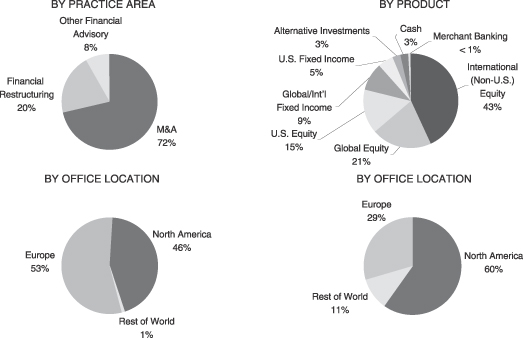

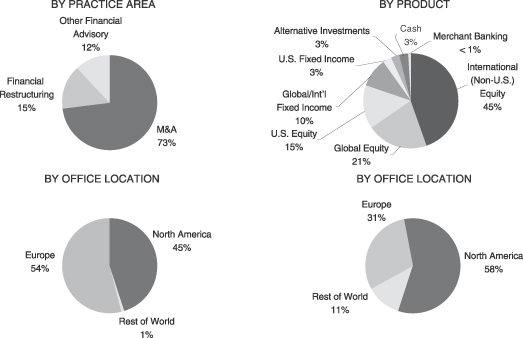

| Ÿ | Our Mergers and Acquisitions practice is poised to capitalize on any future growth in the mergers and acquisitions market. This practice comprised |

Our Financial Restructuring practice, which comprised 7%9% of our net revenue from continuing operations for the nine monthsyear ended September 30,December 31, 2004, provides countercyclicalcounter-cyclical balance to

1

our Mergers and Acquisitions practice. Following the recent economic recovery, and consistent with our expectation, this practice has experienced a substantial61% cyclical decline in revenue over the last year. During the first quarter of 2005, net revenue in our Financial Restructuring practice increased 36% in comparison to the first quarter of 2004. Revenue in a particular quarter may not be indicative, however, of future results. With our leading position in this practice area, we believe that we are positioned to benefit from any resurgence in corporate credit defaults and financial distress.

| Ÿ | Our Asset Management business, which comprised |

We believe that our increase in business activity since September 30, 2004 reflects both the results of our recent strategic initiatives as well as improved market conditions generally. For a further discussion of our performance since September 30, 2004, see “—Recent Developments” below. Despite these results, we face a number of competitive challenges and potential risks. See “Risk Factors” for a discussion of the factors you should consider before buying shares of our common stock.

Our Business Model

We have a focused business model. We generate Financial Advisory revenue primarily from fees earned upon the closing of mergers and acquisitions, restructurings and other engagements on which we have provided advisory services. We generate Asset Management revenue primarily from investment advisory fees calculated as a percentage of the assets under our management, or “AUM.” Employment costs are our largest expense, a significant portion of which is paid in the form of discretionary bonuses. Our policy will be to set our total compensation and benefits expense, including amounts payable to our managing directors, at a level not to exceed 57.5% of our operating revenue, such that after considering other operating costs, we may realize our operating profit margin goal. For more information on our compensation and benefits expenses, see “Unaudited Pro Forma Financial

Information” and “Risk Factors—Risks Related to the Separation—Our financial performance depends on our ability to achieve our target compensation expense.expense level, and the failure to achieve this target level may materially adversely affect our results of operations and financial position.”

Financial Advisory

Our Financial Advisory business provides advice in connection with a wide range of strategic and financial matters that are typically of great importance to our clients. Our goal is to continue to grow our business by fostering long-term, senior-level relationships with existing and new clients as their independent advisor on strategic transactions such as mergers, acquisitions, restructurings and other financial matters. Our Mergers and Acquisitions services include general strategic advice and transaction-specific advice regarding domestic and cross-border mergers and acquisitions, divestitures, privatizations, special committee assignments, takeover defenses, strategic partnerships, joint ventures and specialized real estate advisory services. We provide advice to managements and boards of directors, business owners, governments, institutions, investors and other interested parties on a worldwide basis. Our dedicated industry specialty groups include: consumer, financial institutions, financial sponsors, healthcare and life sciences, industrial, power and energy, real estate and technology, media and telecommunications. We also currently provide various corporate finance services, such as fund-raising for alternative investment firms and public and private financings.

2

Our Financial Restructuring practice, which specializes in helping companies in financial distress, is an important strategic component of our Financial Advisory business. We believe we are the leading financial restructuring advisory firm in the world, having advised on most of the largest and highest profile corporate restructurings over the last several years. We believe that we have been able to secure our leading position in this practice area through a combination of our restructuring and industry-related expertise and our independent position. This practice complements our Mergers and Acquisitions practice because it is generally more active when our Mergers and Acquisitions practice is less active. In addition, our Financial Restructuring practice often generates follow-on relationships and assignments that survive the completion of restructuring-related engagements.

In 2003,2004, Financial Advisory net revenue totaled $691$655 million, accounting for 66%60% of our net revenue from continuing operations, and was earned from a diverse group of 370435 clients. FiftyFifty-four percent of Financial Advisorythis net revenue was generated in Europe, 49%45% in North America and 1% in the rest of the world in the same year.world.

Since January 2002, when new senior management joined our firm, our focus in our Financial Advisory business has been on:

| Ÿ | making a significant reinvestment in our intellectual capital with the addition of many senior professionals who we believe have strong client relationships and industry expertise. We have recruited or promoted 68 new managing directors from January 2002 through |

| Ÿ | increasing our contacts with existing clients to further enhance our long-term relationships and our efforts in developing new client relationships, |

| Ÿ | expanding the breadth and depth of our industry expertise and adding new practice areas, |

| Ÿ | coordinating our industry specialty groups on a global basis, and |

| Ÿ | broadening our global presence by adding six new regional offices and entering into strategic alliances in new geographies. |

As a result, our Financial Advisory practice today consists of an experienced group of advisors with specialties across a wide range of industries and practice areas, operating, we believe, with increased quality and frequency of client contact. We made these investments during a period of financial market weakness, when many of our competitors were reducing senior staffing, to position us to capitalize more fully on any financial services industry recovery. We believe that it generally takes a new managing director from one to two years from the date of hiring to produce revenue at his or her full capacity. As a result, we believe that many of our new managing directors have not yet reached their full revenue generating potential.

In addition to the recent expansion of our Financial Advisory team, we believe that the following external market factors may enable our Financial Advisory practice to benefit from future growth in the global mergers and acquisitions advisory business:

| Ÿ | increasing demand for independent, unbiased financial advice, and |

| Ÿ | a potential increase in cross-border mergers and acquisitions and large capitalization mergers and acquisitions, two of our areas of historical specialization, which have experienced greater than average declines in recent years. |

3

Asset Management

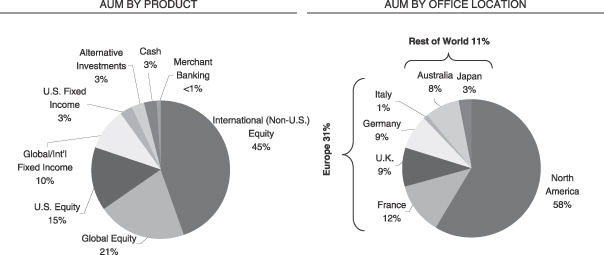

Our Asset Management business provides investment management and advisory services to institutional clients, financial intermediaries, private clients and investment vehicles around the world. Our goal in our Asset Management business is to produce superior risk-adjusted investment returns and provide investment solutions customized for our clients. As of September 30,December 31, 2004, total AUM was $78.5$86.4 billion, of which approximately 80% was managed on behalf of institutional clients, including corporations, labor unions, public pension funds, insurance companies and banks, and through sub-advisory relationships, mutual fund sponsors, broker-dealers and registered advisors. As of the same date, approximately 20% of our AUM was managed on behalf of individual client relationships, which are principally with family offices and high-net worth individuals.

Many of our equity investment strategies share an investment philosophy that centers on fundamental security selection with a focus on the trade-off between a company’s valuation and its financial productivity. As of September 30,December 31, 2004, 79%81% of our AUM was invested in equities, 15%13% in fixed income, 3% in alternative investments, 3% in cash and less than 1% in merchant banking funds. As of the same date, approximately 54%56% of our AUM was invested in international (i.e., non-U.S.) investment strategies, 25%23% was invested in global investment strategies and 21% was invested in U.S. investment strategies.

We operate our Asset Management business through two principal subsidiaries, Lazard Asset Management LLC, or “LAM,” in New York, San Francisco, London, Milan, Frankfurt, Hamburg, Tokyo, Sydney and Seoul (aggregating $69.3$76.5 billion in total AUM as of September 30,December 31, 2004), and Lazard Frères Gestion, or “LFG,” in Paris (aggregating $8.8$9.4 billion in total AUM as of September 30,December 31, 2004). These operations provide our business with a global presence and a local identity. We also manage $0.5 billion of merchant banking funds.

In 2003,2004, Asset Management net revenue was $350$417 million, accounting for 33%38% of our net revenue from continuing operations. Sixty-threeFifty-nine percent of Asset Managementthis net revenue was generated in North America, 30%33% in Europe and 7%8% in the rest of the world.

Our strategic plan in our Asset Management business is to focus on delivering superior investment performance and client service and broadening our product offerings and distribution in selected areas in order to continue to drive business results. In March 2004, we undertook a senior management transition at LAM to put in place the next generation of leadership and to better position the business to execute our strategic plan. Over the past several years, in an effort to improve LAM’s operations and expand our business, we have:

| Ÿ | focused on enhancing our investment performance, |

| Ÿ | improved our investment management platform by hiring ten senior equity analysts and filling the newly established position of Head of Risk Management, |

| Ÿ | strengthened our marketing capabilities by establishing a global consultant relations effort aimed at improving our relations with the independent consultants who advise many of our clients on the selection of investment managers, |

| Ÿ | expanded our product platform by “lifting-out” experienced portfolio managers to establish new products in the hedge fund area and in thematic investing, and |

| Ÿ | launched new products such as “Lazard European Explorer,” a European long/short strategy, and “Lazard Global Total Return and Income Fund, Inc.,” a closed-end fund. |

We believe that LAM has long maintained an outstanding team of portfolio managers and global research analysts. We intend to maintain and supplement our intellectual capital to achieve our goals. We also believe that LAM’s specific investment strategies, global reach, unique brand identity and

4

access to multiple distribution channels will allow it to leverage into new investment products, strategies and geographic locations. In addition, we plan to expand our participation in merchant banking activities through investments in new and successor funds.

Competitive Advantages

We attribute our success and distinctiveness to a combination of long-standing advantages from which we and our predecessor partnerships have benefited, including:

| Ÿ | Experienced People. Our professionals concentrate on solving complex financial problems and executing specialized investment strategies. We strive to maintain and enhance our base of highly talented professionals and pride ourselves on being able to offer clients more senior-level attention than may be available from many of our competitors. |

| Ÿ | Independence. We are an independent firm, free of many of the conflicts that can arise at larger financial institutions as a result of their varied sales, trading, underwriting, research and lending activities. We believe that recent instances of perceived or actual conflicts of interest, and a desire to avoid any potential future conflicts, have increased the demand by managements and boards of directors for trusted, unbiased advice from professionals whose main product is advice. |

| Ÿ | Reputation. Our firm has a brand name with over 150 years of history. We are focused on providing world-class professional advice in complex strategic and financial assignments, utilizing both our global capabilities and deeply rooted, local know-how. |

| Ÿ | Focus. We are focused on two primary businesses—Financial Advisory and Asset Management—rather than on a broad range of financial services. We believe this focus has helped, and will continue to help, us attract clients and recruit professionals who want to work in a firm where these activities are the central focus. |

| Ÿ | Global Presence with Local Relationships. We believe that linking our talented indigenous professionals, deep local roots and industry expertise across offices enables us to be a global firm while maintaining a local identity. We believe this approach enables us to build close, local relationships with our clients and to develop insight into both local and international commercial, economic and political issues affecting their businesses. We do not regard any single jurisdiction as our home country. |

| Ÿ | Balance. Our Financial Advisory business includes both our Mergers and Acquisitions practice and our Financial Restructuring practice, which historically have been |

| Ÿ | Strong Culture. We believe that our people are united by a desire to be a part of an independent firm in which their activities are at the core and by a commitment to excellence and integrity in their activities. This is reinforced by the significant economic stake our managing directors have in our success. In our opinion, the strength of our many long-term client relationships is a testament to our distinctive culture and approach to providing superior advice to our clients. |

Notwithstanding these competitive strengths, weSelected Risk Factors

We face a number of competitive challenges and potential risks. See “Risk Factors” for a discussion of the factors you should consider before buying sharesour securities. Some of our common stock.the more significant challenges and risks include the following:

| Ÿ | Retention of our Managing Directors and other Key Professionals. Our business depends upon our retention and recruitment of talented people, and we face competitive pressures for retaining and recruiting top talent. Because of these competitive pressures and our goal of achieving our target ratio of compensation expense-to-operating revenue, we may not be able to retain our managing directors or recruit new managing directors. |

5

| Ÿ | Our Results Will Fluctuate. The level and source of our revenue fluctuates from period to period. In particular, despite the improvement in our Mergers and Acquisitions and Asset Management net revenue during 2004 and the first quarter of 2005, these businesses remain subject to cyclical economic and market influences. The cyclical downturn in the financial services industry between 2000 and 2003, the year prior to the recent recovery, in combination with our having undertaken to invest significantly in the intellectual capital of our business commencing in 2002, resulted in substantial declines in our net revenue and net income allocable to members from 2000 to 2004. |

| Ÿ | Dependence on Market Conditions.As a financial services firm, our businesses are materially affected by conditions in the global financial markets and economic conditions throughout the world. The performance of our Financial Advisory business depends, in part, upon the level of merger and acquisition activity and the rate of financial restructurings. The performance of our Asset Management business, including both management and incentive fees that we earn, depend, in part, upon the performance of securities markets generally. As a result, market and economic conditions significantly affect our performance. |

| Ÿ | Retention of Asset Management Clients. In addition to being dependent upon general market conditions, our Asset Management business also is dependent upon performance relative to our competitors. If our AUM underperform relative to our competitors, our clients may withdraw funds from our Asset Management business, which would decrease the amount of AUM upon which we earn management fees. |

| Ÿ | Competition from Other Financial Institutions. The financial services industry is intensely competitive. Many of our competitors have the ability to offer a wide range of products, from loans, deposit-taking and insurance to brokerage, asset management and investment banking services. These competitors have the ability to support their investment banking services, including financial advisory services, with commercial banking, insurance and other financial services revenue. Such cross-subsidization could result in pricing pressure in our businesses. |

| Ÿ | Industry Litigation and Regulation.The financial services industry faces substantial litigation and regulatory risks, and we may face legal liability and damage to our professional reputation if our services are not regarded as satisfactory or do not meet regulatory requirements. |

Our Initial Public Offering

We decided to become a public company in order to:

| Ÿ | incentivize our key employees, who also will be our primary owners, to grow the profitability of our business and enhance our ability to retain and recruit talented professionals, |

| Ÿ | better align the interests of all of our owners by using the net proceeds from this offering, and the net proceeds from the additional financing transactions, primarily to redeem membership interests in our firm held by the historical partners, and |

| Ÿ | provide us with publicly traded securities, which we could use to finance strategic acquisitions in the future. |

This offering is a public offering of Class A common stock of Lazard Ltd, which will be the holding company for the public’s common equity interests in Lazard Group. Lazard Group holds our Financial Advisory and Asset Management businesses.

This offering is one of a series of concurrent securities offerings that Lazard Ltd, and Lazard Group and one or more of their subsidiaries intend to complete, which other offerings we refer to in this prospectus as the “additional financing transactions.”

The additional financing transactions consist of an offering, by means of a separate prospectus, of equity security units, which we refer to in this prospectus as the “ESU offering,” a private placement of senior unsecured notes of Lazard Group, by means of a separate offering memorandum, which we refer to in this prospectus as the “debt offering,” and an investment agreement with IXIS—Corporate & Investment Bank, which we refer to in this prospectus as the “IXIS investment agreement.” This prospectus shall not be deemed to be an offer to sell or a solicitation of an offer to buy any securities offered in the ESU offering or the debt offering or any securities to be acquired pursuant to the IXIS investment agreement. See “Description of Capital Stock—IXIS Investment in Our Common Stock,” “Description of Indebtedness—IXIS Investment in Exchangeable Debt Securities” and “Description of Indebtedness—Lazard Group Senior Notes.”

Our History

Our origins date back to 1848 when our founders, the Lazard brothers, formed Lazard Frères & Co. as a dry goods business in New Orleans, Louisiana, with a combined contribution of $9,000. Shortly thereafter, the Lazard brothers moved to the gold rush town of San Francisco, California, where

they opened a business selling imported goods and exporting gold bullion. The business progressively became involved in financial transactions, first with its retail clients and then increasingly with commercial clients. Over time, the business expanded into the banking and foreign exchange businesses.

Seeking to expand operations to Europe, the Lazard brothers opened offices in Paris and London in 1858 and 1870, respectively. By 1876, Lazard’s businesses had become solely focused on providing financial services. In 1880, Alexander Weill, the founding brothers’ cousin, assumed control of Lazard.

Through the early and mid-twentieth century, the three Lazard Houses in London, Paris and New York continued to grow their respective operations independently of each other, with the New York House coming under the leadership of André Meyer in 1944. Under Mr. Meyer and continuing with Felix Rohatyn, the New York House further developed its reputation as a preeminent mergers and acquisitions advisory firm. Michel David-Weill, a descendant of the founding families, joined Lazard Frères et Cie. in Paris in 1956, ascended to a leadership role within the French operations and later moved to the New York House, where he became senior partner in 1977.

Lazard has conducted an asset management business in Paris since 1969, establishing a separate subsidiary, LFG, for those operations in 1995. In 1970, the New York House entered the institutional asset management business by establishing LAM to complement its financial advisory business.

Throughout the twentieth century, Lazard’s Paris and New York Houses were owned by the Houses’ individual partners and by relations of their founders. For much of that period, the London House was majority-owned by Pearson plc, until the sale in 2000 by Pearson of its interests to a predecessor of Eurazeo S.A.

The unification of the Houses of Lazard under a single global firm was completed as of January 3, 2000, with their merger to form Lazard LLC. We believe that this combination has enabled us to offer our clients the benefits of a more unified global firm while preserving the advantages of our century-old, local

6

roots. Bruce Wasserstein joined Lazard in early 2002 as Head of Lazard. Under Mr. Wasserstein’s direction, Lazard has pursued a strategy of growing its Financial Advisory and Asset Management businesses by attracting senior investment bankers and investment advisory professionals to our firm.

Lazard’s history as a preeminent financial advisor has contributed to its ability to secure key advisory roles in some of the most important, complex and recognizable mergers and acquisitions of the last 75 years. Since 1999, we have advised on nearly 1,000 completed mergers and acquisitions, having a cumulative value in excess of $1 trillion. During this period, we have participated in many prominent transactions, advising:

| Ÿ | MCI, Inc. in evaluating its strategic alternatives, including its announced agreement to engage in a merger, |

| Ÿ | Nextel Communications in its pending merger-of-equals with Sprint Corporation (to create a company with a combined equity market value of approximately $70 |

| Ÿ | Telecom Italia Mobile in its pending€21 billion sale of the remaining public interests to Telecom Italia (integrating Italy’s largest phone carrier and leading mobile operator), |

| Ÿ | Mitsubishi Tokyo Financial Group in its |

| Ÿ | Hollinger International Inc. in its £730 million sale of the Telegraph Group Limited to Press Holdings International (owned by the Barclay brothers) in 2004 (the largest single title newspaper transaction as of the date of this prospectus), |

| Ÿ | Fisher Scientific International Inc. in its $3.7 billion acquisition of Apogent Technologies Inc. in 2004 (creating a leading life sciences business), |

| Ÿ | Bank One Corporation in its $59 billion sale to JPMorgan Chase & Co. in 2004 (creating the second largest bank in the U.S. as of the date of this prospectus), |

| Ÿ | Canary Wharf Group PLC in its £5 billion sale of a majority interest to an investment consortium in 2004 (the largest ever public-to-private transaction for a listed real estate company as of the date of this prospectus), |

| Ÿ | Alcan Inc. in its $7 billion acquisition of Pechiney in 2004 (creating the world’s largest aluminum company based on revenue as of the date of this prospectus), |

| Ÿ | Telecom Italia in its€25 billion sale of minority stockholder interests to Olivetti in 2003 (simplifying the ownership structure of one of Europe’s largest telecommunications firms), |

| Ÿ | Caisse des Dépôts et Consignations in its€16 billion partnership with Group Caisse d’Epargne in 2003 (completing the restructuring of the French public finance sector and creating a major universal bank), and |

| Ÿ | Pfizer Inc. in its $89 billion acquisition of Warner-Lambert Company in 2000 (the largest unsolicited acquisition at the time) and in its $61 billion acquisition of Pharmacia (the largest announced acquisition in 2002). |

In recent years, we have been an advisor in most of the largest and highest profile corporate restructurings around the world. Since 1999, we have advised on over 100 in and out-of-court restructurings comprising in excess of $300 billion of debt restructured. Our restructuring assignments have included, in the U.S., WorldCom Inc. ($38 billion of debt) and Reliant Resources ($9 billion of debt), in Italy, Parmalat ($27 billion of debt), in the U.K., Marconi Corporation plc ($8 billion of debt),in France and the U.K., Eurotunnel plc ($12 billion of debt) and in Korea, Daewoo ($50 billion of debt).

7

We were incorporated in Bermuda on October 25, 2004. Our registered office in Bermuda is located at Clarendon House, 2 Church Street, Hamilton HM 11, Bermuda, with a general telephone number of (441) 295-1422. Our principal executive offices are located in the U.S. at 30 Rockefeller Plaza, New York, New York 10020, with a general telephone number of (212) 632-6000, in France at 121 Boulevard Haussmann, 75382 Paris Cedex 08, with a general telephone number of 33-1-44-13-01-11, in the U.K. at 50 Stratton Street, London W1J 8LL, with a general telephone number of 44-207-187-2000 and in Italy at via Dell’Orso 2, 20121 Milan, with a general telephone number of 39-02-723121. In total, we maintain offices in 27 cities worldwide. We maintain an Internet site atwww.lazard.com.Our website and the information contained on that site, or connected to that site, are not incorporated into this prospectus.prospectus, and you should not rely on any such information in making your decision whether to purchase our securities.

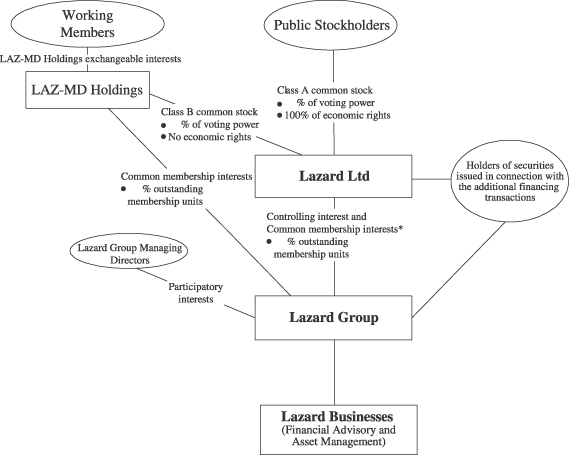

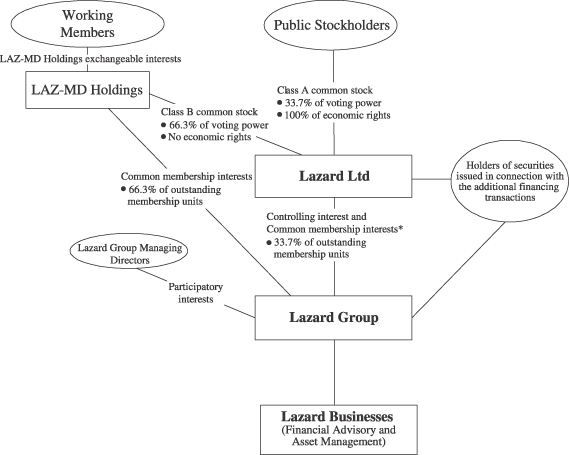

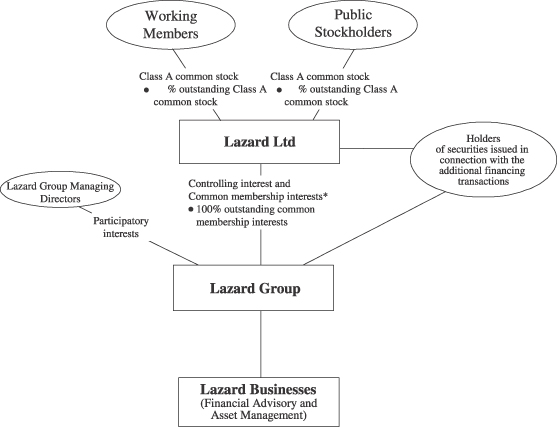

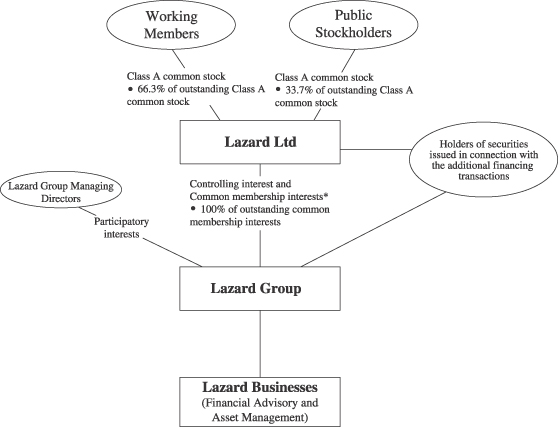

Lazard’s Organizational Structure

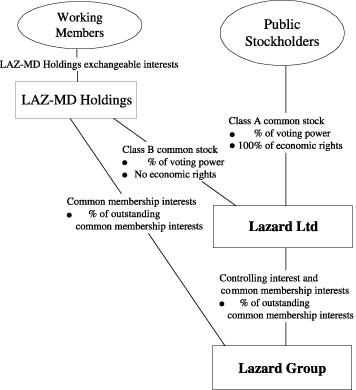

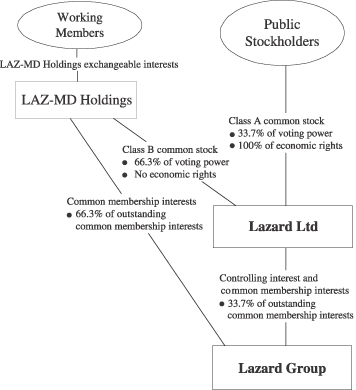

Lazard Ltd is a Bermuda holding company. After completion of this offering, Lazard Ltd will have no material assets other than ownership of approximately %approximately33.7% of the common membership interests of Lazard Group, the Delaware limited liability company that holds our business. The remaining %remaining66.3% of Lazard Group’s common membership interests will be held by LAZ-MD Holdings, a holding company that will be owned by current and former managing directors of Lazard Group. The Lazard Group common membership interests held by LAZ-MD Holdings will be effectively exchangeable over time on a one-for-one basis for shares of our common stock, as described in “The Separation and Recapitalization Transactions and the Lazard Organizational Structure.”

Lazard Ltd will hold a controlling interest in, and consolidate the financial statements of, Lazard Group. LAZ-MD Holdings’ ownership interests in Lazard Group will be accounted for as a minority interest in our consolidated financial results after this offering.

Lazard Group distributions will be allocated to holders of Lazard Group common membership interests on a pro rata basis. As we will hold approximately %approximately33.7% of the outstanding Lazard Group common membership interests immediately after this offering, we will receive approximately %approximately33.7% of the aggregate distributions in respect of the Lazard Group common membership interests.

WeOur stockholders will experience significant dilution upon the completion of this offering since we will use the net proceeds of this offering and the additional financing transactions primarily to recapitalize Lazard Group, which transaction we refer to in this prospectus as the “recapitalization.” As part of the recapitalization, Lazard Group will use the proceeds from this offering and the additional financing transactions primarily to redeem outstanding membership interests of its historical partners. See “Dilution” and “Use of Proceeds.”

Prior to completing the recapitalization, Lazard Group will transfer its capital markets business, which is comprisedconsists of equity, fixed income and convertibles sales and trading, broking, research and underwriting services, its merchant banking fund management activities other than its existing merchant banking business in France and specified non-operating assets and liabilities, to LFCM Holdings. We refer to these businesses, assets and liabilities as the “separated businesses” and these transfers collectively as the “separation.” For a more detailed description of the separation and the separated businesses, see “The Separation and Recapitalization Transactions and the Lazard Organizational Structure,” “Certain Relationships and Related Transactions—RelationshipsRelationship with LAZ-MD Holdings and LFCM Holdings—Master Separation Agreement” and “Risk Factors—Risks Related to the Separation.”

Except as otherwise expressly noted, this prospectus describes Lazard Group’s business as if the separation were complete for all purposes and for all periods described. The historical consolidated financial data of Lazard Group included in this prospectus, however, reflect the historical results of operations and financial position of Lazard Group, including the separated businesses. In addition to

8

other adjustments, the pro forma financial data included in this prospectus reflect financial data for Lazard Group and Lazard Ltd giving effect to the separation, as well as other adjustments made as a result of this offering and the additional financing transactions.

Each share of our common stock will entitle its holder to one vote per share. The share of our Class B common stock is intended to allow our managing directors to individually vote in proportion to their indirect economic interests in us. This will be effected by LAZ-MD Holdings, which holds our Class B common stock, entering into a stockholders’ agreement with its members pursuant to which

the members individually will be entitled to direct LAZ-MD Holdings how to vote their proportionate interest in our Class B common stock on an as-if-exchanged basis. This means that if a member held a LAZ-MD Holdings exchangeable interest that was effectively exchangeable for 1,000 shares of our common stock, that member would be entitled to direct LAZ-MD Holdings how to vote 1,000 votes represented by our Class B common stock. Our Class B common stock will be entitled, on all matters submitted to a vote of the stockholders of Lazard Ltd, to the number of votes equal to the number of shares of our common stock that would be issuable if all of the then outstanding Lazard Group common membership interests issued to LAZ-MD Holdings were exchanged for shares of our common stock. We refer to this stockholders’ agreement as the “LAZ-MD Holdings Stockholders’ Agreement.stockholders’ agreement.” Immediately after this offering, our Class B common stock will have %66.3% of the voting power of our company, which percentage will decrease proportionately as Lazard Group common membership interests are exchanged for shares of our common stock. In order to seek to avoid the possibility that LAZ-MD Holdings would be deemed to be an “investment company” for purposes of the U.S. Investment Company Act of 1940, as amended, or the “Investment Company Act,” the voting power of our outstanding Class B common stock will, however, represent no less than 50.1% of the voting power of our company until December 31, 2007. In addition, the board of directors of LAZ-MD Holdings will have the ability to vote the entire voting interest represented by our Class B common stock in its discretion if the LAZ-MD Holdings board of directors determines that it is in the best interests of LAZ-MD Holdings.

Our public stockholders, including IXIS and working members who hold historical partner interests and who have elected to exchange those interests for shares of our common stock, initially will hold allallof the outstanding shares of our common stock, representing approximately %approximately33.7% of the voting power in our companyLazard Ltd and 100% of ourLazard Ltd’s capital stock on an economic basis. The Class B common stock will not have any economic rights.

9rights in Lazard Ltd. As noted above, Lazard Ltd will hold approximately 33.7% of the Lazard Group common membership interests immediately after this offering, entitling our company to an equivalent percentage of any distributions made by Lazard Group in respect of its common membership interests. The remaining approximately 66.3% of Lazard Group common membership interests outstanding immediately after this offering will be held by LAZ-MD Holdings, entitling LAZ-MD Holdings to an equivalent percentage of any distributions made by Lazard Group in respect of its common membership interests.

The graphic below illustrates our expected pro forma ownership structure immediately following completion of this offering, assuming no exercise of the underwriters’ over-allotment option. The graphic below does not display all of the subsidiaries of Lazard Ltd, Lazard Group and LAZ-MD Holdings (including those through which Lazard Ltd holds its interests in Lazard Group), all of the minority interests in Lazard Group (including the participatory interests to be granted to managing directors) or other securities we expect to issue or grant in connection with the additional financing transactions. The “Public Stockholders” caption on the graphic below includes shares of common stock that will be issued to IXIS pursuant to the IXIS investment agreement and to working members who hold historical partner interests and who have elected to exchange those interests for shares of our common stock. For a more detailed graphic, we refer you to “The Separation and Recapitalization Transactions and the Lazard Organizational Structure” and, for a further discussion of minority interests, to “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Financial Measures and Indicators—Minority Interest.”

The working members will receive, in exchange for their interests in Lazard Group, membership interests in LAZ-MD Holdings, including LAZ-MD Holdings exchangeable interests, in connection with the separation and recapitalization transactions. These LAZ-MD Holdings exchangeable interests are effectively exchangeable for shares of our common stock on the eighth anniversary of this offering. In addition, the LAZ-MD Holdings exchangeable interests held by our working members who continue to provide services to us or LFCM Holdings will, subject to certain conditions, generally be effectively exchangeable for shares of our common stock in equal increments on and after each of the third, fourth and fifth anniversaries of this offering. LAZ-MD Holdings and certain subsidiaries of Lazard Ltd (which will effect the exchanges), with the consent of the Lazard Ltd board of directors, also have the right to cause the holders of LAZ-MD Holdings exchangeable interests to exchange all such remaining

interests during the 30-day period following the ninth anniversary of this offering.offering and under certain other circumstances. Upon full exchange of the LAZ-MD Holdings exchangeable interests for shares of our common stock, the Class B common stock would cease to be outstanding, and all of the Lazard Group common membership interests formerly owned by LAZ-MD Holdings would be owned indirectly by Lazard Ltd. Pursuant to a master separation

10

agreement that we will enter into with Lazard Group, LAZ-MD Holdings and LFCM Holdings, a stockholders’ committee will be formed and will have the ability to accelerate the exchangeability of these LAZ-MD Holdings exchangeable interests, with the prior approval of our board of directors. See “Certain Relationships and Related Transactions—Relationship with LAZ-MD Holdings and LFCM Holdings—Master Separation Agreement—LAZ-MD Holdings Exchangeable Interests.”

In connection with the separation and recapitalization transactions, our managing directors who are managing directors of LAM will retain their equity interests and phantom equity rights in LAM, which we refer to in this prospectus as “LAM equity units,” and, accordingly, will not hold any membership interests in LAZ-MD Holdings. For a discussion of the LAM equity units, see “Management’s Discussion and Analysis of Financial Condition and Results of Operation—Key Financial Measures and Indicators—Minority Interest.”

We anticipate that Lazard Ltd will be structured as a partnership for U.S. federal income tax purposes, though Lazard Ltd will be organized as a company under Bermuda law. We intend to operate our business in a manner that does not result in the allocation of any income or deductible expenses to our stockholders, other than amounts that we distribute to our stockholders.

We intend to undertake several transactions concurrently with this offering, including the additional financing transactions, in order to establish this organizational structure and effect the recapitalization of Lazard Group. For more information about these transactions, see “The Separation and Recapitalization Transactions and the Lazard Organizational Structure.” Under the terms of the master separation agreement that we intend to enter into regarding the separation, we may withdraw the proposed transactions, including this offering, without liability at any time prior to the time that this offering is effected. See “Certain Relationships and Related Transactions—Relationship with LAZ-MD Holdings and LFCM Holdings—Master Separation Agreement” and “Risk Factors—Risks Related to the Separation.”

Material U.S. Federal Income Tax and Bermuda Tax Considerations

Lazard Ltd is not subject to any Bermuda income or profits tax, withholding tax, capital gains tax, capital transfer tax, estate duty or inheritance tax. In addition, under current Bermuda law, there is no Bermuda income or profits tax, withholding tax, capital gains tax, capital transfer tax, estate duty or inheritance tax payable by our stockholders in respect of our common stock.

We intend to operate our business so that, with respect to our common shares, each shareholderstockholder will generally be required to report on its U.S. federal income tax return only the amount of cash actually distributed to such shareholder.stockholder. Lazard Ltd, ourthe parent holding company, has made an election to be treated as a partnership for U.S. federal income tax purposes. As a result, each stockholder will be required to report on its income tax return its allocable share of Lazard Ltd’s income, gains, losses and deductions.

Because Lazard Ltd is a partnership for U.S. federal income tax purposes, Lazard Ltd itself will not pay any U.S. federal income tax, although Lazard Ltd’s U.S. subsidiaries generally will be subject to U.S. federal income tax on a net income basis on their share of the income of Lazard Group and its subsidiaries, and Lazard Ltd’s non-U.S. subsidiaries generally will be subject to U.S. federal income tax on a net income basis on the income of Lazard Group and its subsidiaries that is “effectively connected” with their conduct of a trade or business in the United States.U.S.

For additional information concerning the material tax consequences of investing in our common shares, see “Material U.S. Federal Income Tax and Bermuda Tax Considerations.”

11

Relationship with LAZ-MD Holdings and LFCM Holdings

In addition to LAZ-MD Holdings’ equity and voting interests in Lazard Ltd and Lazard Group as described above in “—Lazard’s Organizational Structure,” we will have ongoing relationships with LAZ-MD Holdings and LFCM Holdings and its subsidiaries after the separation and this offering, including several agreements with LAZ-MD Holdings and LFCM Holdings that are intended to define and regulate Lazard’s ongoing relationship with LAZ-MD Holdings and LFCM Holdings after the separation and this offering. For a further discussion, see “Certain Relationships and Related Transactions—Relationship with LAZ-MD Holdings and LFCM Holdings.”

Bermuda Law

The Companies Act 1981 of Bermuda, as amended, which we refer to in this prospectus as the “Companies Act,” which applies to Lazard Ltd, differs in certain material respects from laws generally applicable to U.S. corporations and their stockholders. These differences include:

| Ÿ | Voting rights of stockholders. Under Bermuda law, voting rights of stockholders are regulated by the company’s bye-laws and, in certain circumstances, the Companies Act. While we have generally sought to provide for voting rights that are similar to those of a Delaware corporation, our bye-laws and Bermuda law contain selected provisions that differ from what would require a stockholder vote in a Delaware corporation. For example, at any annual or general meeting of our stockholders, two or more persons present in person and generally representing greater than 50% of the votes are required to form a quorum for the transaction of business. Generally, except as otherwise provided in the bye-laws, any action or resolution requiring approval of the stockholders may be passed by a simple majority of votes cast. Delaware law provides that a majority of the shares entitled to vote constitutes a quorum at a meeting of stockholders. For a Delaware corporation, in matters other than the election of directors, with the exception of special voting requirements related to extraordinary transactions, the affirmative vote of the majority is required for stockholder action, and the affirmative vote of a plurality is required for the election of directors. |

In Bermuda, mergers and amalgamations (other than between certain affiliated companies) generally require the approval of a company’s board of directors and, unless the company’s bye-laws provide otherwise, the approval of 75% of the stockholders. Our bye-laws provide that a merger or an amalgamation (other than with a wholly owned subsidiary) approved by our board of directors must be approved by a majority of the combined voting power of all of the shares voting together as a single class. In Delaware, with certain exceptions, a merger, consolidation or sale of all or substantially all the assets of a corporation must be approved by the board of directors and a majority of the outstanding shares entitled to vote thereon.

| Ÿ | The ability of a company to pay dividends. Under the Companies Act, we may declare or pay a dividend or make a distribution out of distributable reserves only if we have reasonable grounds for believing that we are, or would after the payment be, able to pay our liabilities as they become due and if the realizable value of our assets would thereby not be less than the aggregate of our liabilities and issued share capital and share premium accounts. A Delaware company, subject to any restrictions contained in the company’s certificate of incorporation, may pay dividends out of surplus or, if there is no surplus, out of net profits for the fiscal year in which the dividend is declared and for the preceding fiscal year, but the company may not pay dividends out of net profits if, after the payment of the dividend, capital is less than the capital represented by the outstanding stock of all classes having a preference upon the distribution of assets. |

| Ÿ | Stockholders’ ability to call meetings. Bermuda law provides that a special general meeting must be called upon the request of stockholders holding not less than 10% of the paid-up share capital of the company carrying the right to vote. Delaware law permits the certificate of incorporation of a Delaware corporation to bar stockholder ability to call a special meeting. |

| Ÿ | Access to books and records by the |

| Ÿ |

| Ÿ |

The Bermuda Monetary Authority has classified us as a non-resident of Bermuda for exchange control purposes. Accordingly, the Bermuda Monetary Authority does not restrict our ability to engage in transactions in currencies other than Bermuda dollars, to transfer funds in and out of Bermuda or to pay dividends to non-Bermuda residents who are stockholders, other than in Bermuda dollars. We have received consent under the Exchange Control Act 1972 from the Bermuda Monetary Authority for the issue and transfer of the common stock to and between non-residents of Bermuda for exchange control purposes, provided that our shares remain listed on an appointed stock exchange, which includes the New York Stock Exchange, or the “NYSE.” This prospectus will be filed with the Registrar of Companies in Bermuda in accordance with Bermuda law. In granting such consent and in accepting this prospectus for filing, neither the Bermuda Monetary Authority nor the Registrar of Companies in Bermuda accepts any responsibility for our financial soundness or the correctness of any of the statements made or opinions expressed in this prospectus.

For more information on the rights under the Companies Act, including where relevant, information on Lazard Ltd’s bye-laws, and a comparison to Delaware corporate law, see “Description of Capital Stock—Delaware Law” and “Certain Relationships and Related Transactions—Certain Relationships with Our Directors, Executive Officers and Employees—Director and Officer Indemnification.”

12

The Offering

Common stock offered by Lazard Ltd(a) | 30,464,579 shares |

Capital stock to be outstanding immediately following this offering:

Class A common stock(b) | 33,653,846 shares |

Class B common stock | 1 share |

Lazard Group common membership interests to be outstanding immediately after the offering:

Owned by Lazard Ltd | 33,653,846 interests |

Owned by LAZ-MD Holdings(c) | 66,346,154 interests |

Total | 100,000,000 interests |

Additional Financing Transactions | Concurrently with this offering, Lazard Ltd, Lazard Group or one or more of their subsidiaries intend to sell additional securities in the ESU offering, the debt offering and pursuant to the IXIS investment agreement to raise estimated net proceeds |

|

|

| (a) | Excludes all of |

| (b) | Includes |

| (c) | The Lazard Group common membership interests held by LAZ-MD Holdings will be effectively exchangeable over time, on a one-for-one basis, for shares of our common stock, as described in “The Separation and Recapitalization Transactions and the Lazard Organizational Structure.” In connection with this offering, the number of Lazard Group common membership interests owned by LAZ-MD Holdings will be set to equal the difference between (1) 100,000,000 and (2) the number of Lazard Group common membership interests owned by Lazard Ltd (which will equal the number of shares of Lazard Ltd common stock outstanding following this offering) before giving effect to the possible exercise of the underwriters’ over-allotment option, the exercise of which would have no additional effect on the number of Lazard Group common membership interests to be owned by LAZ-MD Holdings. |

IXIS Investment Agreement | Under the IXIS investment agreement, IXIS—Corporate & Investment Bank, which we refer to in this prospectus as “IXIS” and which is a subsidiary of Caisse Nationale des Caisses d’Epargne, has agreed to purchase an aggregate of $200 million of our securities concurrently with this offering, $150 million of which will be debt securities of a financing subsidiary that will be effectively exchangeable into shares of our common stock, which we refer to in this prospectus as the “IXIS ESU placement,” and $50 million of which will be shares of our common stock. The exchangeable securities issued in connection with the IXIS ESU placement will be the same as the equity security units issued in the ESU offering. The price per security to be paid by IXIS will be equal, in the case of shares of our common stock, to the price per share in this offering and, in the case of equity security units, the price per unit in the ESU Offering. See “Description of Capital Stock—IXIS Investment in Our Common Stock” and “Description of Indebtedness—IXIS Investment in Exchangeable Debt Securities.” |

ESU Offering | Concurrently with this offering, we will offer, by means of a separate prospectus, equity security units for an aggregate offering amount of $250 million, plus an additional $37.5 million if the underwriters’ option to purchase additional equity security units is exercised in full. Each unit will consist of (a) a contract which will obligate holders to purchase, and Lazard Ltd to sell, on , 2008, a number of newly issued shares of our common stock equal to a settlement rate based on the trading price of our common stock during a period preceding that date and (b) a 1/40, or 2.5%, ownership interest in a senior note of Lazard Group Finance LLC, which we refer to in this prospectus as “Lazard Group Finance,” with a principal amount of $1,000. |

13

We will make quarterly contract adjustment payments on the purchase contracts, subject to our right to defer these payments. In general, during any period in which we defer contract adjustment payments, we cannot declare or pay dividends on, make distributions with respect to, or redeem, purchase or acquire, or make a liquidation payment with respect to, any of our capital stock. |

The senior notes of Lazard Group Finance will be senior obligations of Lazard Group Finance. The notes will mature on , 2035, or on such earlier date as we may elect in connection with the remarketing. In no event, however, will we reset the maturity date to be prior to , 2010. Lazard Group Finance will use the net proceeds from the ESU offering to purchase the senior notes from Lazard Group. The Lazard Group notes will be pledged to secure the obligations of Lazard Group Finance under the senior notes. The ability of Lazard Group |

Finance to pay its obligations under the senior notes depends on its ability to obtain interest and principal payments on the Lazard Group notes. |

Upon a remarketing of the senior notes, in which the applicable interest rate, payment dates and maturity date on the notes will be reset and the notes remarketed, the interest rate, payment dates and maturity date on the Lazard Group notes also will be reset on the same terms such that the interest rate, payment dates and maturity date on the Lazard Group notes are the same as those for the senior notes. See “Description of the Equity Security Units.” |

Debt Offering | Concurrently with this offering, we are privately placing senior notes to be issued by Lazard Group, which we refer to in this prospectus as the “Lazard Group senior notes,” for an aggregate offering amount of $650 million. The Lazard Group senior notes are being offered only to qualified institutional buyers in an offering exempt from the registration requirements of the Securities Act. See “Description of Indebtedness—Lazard Group Senior Notes.” |

Use of Proceeds | We will use the net proceeds from this offering, as well as the net proceeds from the additional financing transactions, primarily to redeem membership interests held by the historical partners, through the transactions described below. |

By Lazard Ltd | Based upon an initial public offering price of |

By Lazard Group | Lazard Group will use the net proceeds from the sale of the common membership interests to Lazard Ltd, along with the net proceeds of the additional financing transactions, primarily to redeem all of the classes of membership interests held by the historical partners for an aggregate redemption price of approximately $1.6 billion. In addition, |

the terms of the retention agreements with our managing directors and the managing directors of LFCM Holdings and for general corporate purposes. |

Voting Rights | Each share of our common stock will entitle its holder to one vote per share. The share of our Class B common stock is intended to allow our managing directors to individually vote in proportion to their indirect economic interests in us. Pursuant to the LAZ-MD Holdings stockholders’ agreement, the members of LAZ-MD Holdings will individually be entitled to direct LAZ-MD Holdings how to vote their proportionate interest in our Class B common stock on an as-if-exchanged basis. The single share of Class B common stock held by LAZ-MD Holdings will be entitled to 66,346,154 votes (representing approximately |

14

interests issued to LAZ-MD Holdings were exchanged for shares of our common stock on the applicable record date. The voting power of the Class B share will decrease proportionately as Lazard Group common membership interests are exchanged for shares of our common stock. In order to seek to avoid the possibility that LAZ-MD Holdings would be deemed to be an “investment company” for purposes of the Investment Company Act, the voting power of our outstanding Class B common stock will, however, represent no less than 50.1% of the voting power of our company until December 31, 2007. See “The Separation and Recapitalization Transactions and the Lazard Organizational Structure” and “Description of Capital Stock.” For a description of the LAZ-MD Holdings stockholders’ agreement addressing how LAZ-MD Holdings will vote its share of Class B common stock, see “Certain Relationships and Related Transactions—LAZ-MD Holdings Stockholders’ Agreement.” |

Economic Rights | Pursuant to our bye-laws, each share of our common stock is entitled to equal economic rights. However, the Class B common stock will have no rights to dividends or any liquidation preference. |

Dividend Policy | We currently intend to declare quarterly dividends on all outstanding shares of our common stock and expect our initial quarterly dividend to be approximately |

The declaration of this and any other dividends and, if declared, the amount of any such dividend, will be subject to our actual future earnings, cash flow and capital requirements, the amount of distributions to us from Lazard Group and the discretion of our board of directors. For a discussion of the factors that will affect the determination by our board of directors to declare dividends, see “Dividend Policy.” |

Risk Factors | For a discussion of factors you should consider before buying shares of common stock, see “Risk Factors.” |

Proposed NYSE Symbol | LAZ |

15

Summary Consolidated Financial Data

The following table sets forth the historical summary consolidated income statement data for Lazard Group, including the separated businesses, for all periods presented. The table also presents certain pro forma consolidated financial data for Lazard LtdGroup and Lazard Group on a consolidated basis.Ltd.

The historical financial statements do not reflect what our results of operations and financial position would have been had we been a stand-alone, public company for the periods presented. Specifically, our historical results of operations do not give effect to the matters set forth below.

| Ÿ | The separation, which is described in more detail in “The Separation and Recapitalization Transactions and the Lazard Organizational Structure” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” |

| Ÿ | Payment for services rendered by Lazard Group’s managing directors, which, as a result of Lazard Group operating as a limited liability company, historically has been accounted for as distributions from members’ capital, or in some cases as minority interest, rather than as employee compensation and benefits expense. As a result, Lazard Group’s operating income historically has not reflected payments for services rendered by its managing directors. After this offering, we will include all payments for services rendered by our managing directors to us in employee compensation and benefits expense. |

| Ÿ | U.S. corporate federal income taxes, since Lazard Group has operated in the U.S. as a limited liability company that was treated as a partnership for U.S. federal income tax purposes. As a result, Lazard Group’s income has not been subject to U.S. federal income taxes. Taxes related to income earned by partnerships represent obligations of the individual partners. Outside the U.S., Lazard Group historically has operated principally through subsidiary corporations and has been subject to local income taxes. Income taxes shown on Lazard Group’s historical consolidated statements of income are attributable to taxes incurred in non-U.S. entities and to the New York City Unincorporated Business Tax, or “UBT,” attributable to Lazard Group’s operations apportioned to New York City. |

| Ÿ | Minority interest expense reflecting LAZ-MD Holdings’ ownership of |

| Ÿ | The use of proceeds from this offering and the additional financing transactions. |

| Ÿ | The net incremental expense related to the additional financing transactions. |

The unaudited pro forma data set forth below are derived from the unaudited pro forma condensed financial statements included elsewhere in this prospectus. The data reflect the separation and recapitalization transactions and the completion of this offering and the additional financing transactions as if they had occurred as of January 1, 2003,2004, and are included for informational purposes only and do not purport to represent what our results of operations would actually have been had we operated as a separate, independent company during the periodsperiod presented, nor dodoes the pro forma data give effect to any events other than those discussed above and in the related notes. As a result, the pro forma operating results are not necessarily indicative of the operating results for any future period. See “Unaudited Pro Forma Financial Information” included elsewhere in this prospectus.

The historical consolidated statementstatements of income data for the years ended December 31, 2000, 2001, 2002, 2003 and 20032004 have been derived from Lazard Group’s consolidated financial statements audited by Deloitte & Touche LLP, an independent registered public accounting firm. The audited

16

consolidated financial statements for the years ended December 31, 2001, 2002, 2003 and 20032004 are included elsewhere in this prospectus. The audited consolidated financial statements for the yearyears ended December 31, 2000 and 2001 are not included in this prospectus. The historical combined statement of income data for the year ended December 31, 1999 has been derived from Lazard Group’s unaudited combined financial statements, which are not included in this prospectus. The historical consolidated statement of income data for the nine months ended September 30, 2003 and 2004 have been derived from Lazard Group’s unaudited consolidated financial statements, which are included elsewhere in this prospectus. The September 30, 2003 and 2004 as well as the December 31, 1999 financial statements have been prepared on a basis consistent with our audited consolidated financial statements and reflect all adjustments, consisting of normal recurring adjustments, which are, in the opinion of management, necessary for a fair presentation of the financial position and results of operations for the periods presented. Historical results are not necessarily indicative of results for any future period and interim results are not necessarily indicative of results for any future interim period.

The summary consolidated financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Unaudited Pro Forma Financial Information” and Lazard Group’s historical consolidated financial statements and related notes included elsewhere in this prospectus. See also “The Separation and Recapitalization Transactions and the Lazard Organizational Structure.”

17

Summary Consolidated Financial Data

| For the Year Ended December 31, | For the Nine September 30, | ||||||||||||||||||||||||

| 1999(a) | 2000 | 2001 | 2002 | 2003 | 2003 | 2004 | |||||||||||||||||||

| ($ in thousands, except as otherwise noted and except for per share data) | |||||||||||||||||||||||||

Lazard Group—Historical Consolidated Statement of Income Data | |||||||||||||||||||||||||

Net Revenue: | |||||||||||||||||||||||||

Financial Advisory (b) | $ | 662,555 | $ | 766,856 | $ | 551,356 | $ | 532,896 | $ | 690,967 | $ | 480,162 | $ | 406,126 | |||||||||||

Asset Management (c) | 385,529 | 457,124 | 410,237 | 454,683 | 350,348 | 225,361 | 289,956 | ||||||||||||||||||

Corporate (d) | 71,352 | 34,432 | (14,392 | ) | (4,768 | ) | 6,500 | (6,073 | ) | 4,734 | |||||||||||||||

Capital Markets and Other | 365,985 | 294,388 | 224,854 | 183,468 | 135,569 | 106,619 | 134,112 | ||||||||||||||||||

Net Revenue (e) | 1,485,421 | 1,552,800 | 1,172,055 | 1,166,279 | 1,183,384 | 806,069 | 834,928 | ||||||||||||||||||

Employee Compensation and Benefits | 474,503 | 570,064 | 524,417 | 469,037 | 481,212 | 351,392 | 401,901 | ||||||||||||||||||

Other Operating Expenses | 265,532 | 306,339 | 288,676 | 321,197 | 312,818 | 201,305 | 237,461 | ||||||||||||||||||

Operating Income | 745,386 | 676,397 | 358,962 | 376,045 | 389,354 | 253,372 | 195,566 | ||||||||||||||||||

Income Allocable to Members Before Extraordinary Item | 676,898 | 558,708 | 305,777 | 297,447 | 250,383 | 171,924 | 128,809 | ||||||||||||||||||

Net Income Allocable to Members | 676,898 | 558,708 | 305,777 | 297,447 | 250,383 | 171,924 | 134,316 | (f) | |||||||||||||||||

Lazard Group—Pro Forma Consolidated Statement of Income Data | |||||||||||||||||||||||||

Net Revenue: | |||||||||||||||||||||||||

Financial Advisory (b) | $ | 690,967 | $ | 480,162 | $ | 406,126 | |||||||||||||||||||

Asset Management (c) | 350,348 | 225,361 | 289,956 | ||||||||||||||||||||||

Corporate | |||||||||||||||||||||||||

Net Revenue (g) | |||||||||||||||||||||||||

Operating Income (h) | |||||||||||||||||||||||||

Net Income (i) | |||||||||||||||||||||||||

Lazard Ltd Consolidated—Pro Forma Consolidated Statement of Income Data | |||||||||||||||||||||||||

Net Revenue: | |||||||||||||||||||||||||

Financial Advisory (b) | $ | 690,967 | $ | 480,162 | $ | 406,126 | |||||||||||||||||||

Asset Management (c) | 350,348 | 225,361 | 289,956 | ||||||||||||||||||||||

Corporate | |||||||||||||||||||||||||

Net Revenue (g) | |||||||||||||||||||||||||

Operating Income (h) | |||||||||||||||||||||||||

Net Income (Before LAZ-MD Holdings’ Minority Interest) (j) | |||||||||||||||||||||||||

Net Income (After LAZ-MD Holdings’ Minority Interest) (k) | |||||||||||||||||||||||||

Pro Forma Diluted Net Income Per Share, as Adjusted for this Offering (l) | |||||||||||||||||||||||||

Pro Forma Diluted Weighted Average Common Shares, as Adjusted for this Offering (l) | |||||||||||||||||||||||||

Other Lazard Group Historical Data | |||||||||||||||||||||||||