| (a) | For purposes of calculating the pro forma net income per Class A share, the number of Class A shares of Silvercrest outstanding are calculated as follows: | | | Incremental shares of Class A common stock (1) | | | Shares of Class A common stock outstanding immediately after this offering | | | | | | Total pro forma Class A shares of Silvercrest for purposes of calculating pro forma net income per Class A share the number of Class A shares of Silvercrest outstanding are calculated as follows: |

| | | Pro forma Class A shares of Silvercrest

| | | | | |

| (1) | Represents incremental Class A shares whose proceeds are assumed to fund the cash distribution to our existing principals as such distribution exceeds current year pro forma earnings. |

| | | | | Distribution prior to offering | | | $ | | Pro forma net income attributable to Silvercrest | | $ | | | | | | | | Distribution in excess of pro forma net income attributable to Silvercrest | | $ | | | Initial public offering price per share | | $ | | | | | | | | Incremental shares of Class A common stock | | | | | Shares of Class A common stock outstanding immediately after this offering | | | | | | | | | | Total pro forma Class A shares of Silvercrest for purposes of calculating pro forma net income per Class A share | | | | | | | | | |

The pro forma basic and diluted net income per Class A share is calculated as follows (Dollars in thousands, except per share data): | | | | | | | | | | | | Basic | | | Diluted | | Pro forma net income attributable to Silvercrest(1)Silvercrest (2) | | $ | | | | $ | | | Weighted average common shares outstanding | | | | | | | | | | | | | | | | | | Pro forma net income per Class A share | | $ | | | | $ | | | | | | | | | | | |

(1)(2) | Our shares of Class B common stock do not share in our earnings and are therefore not included in the weighted average shares outstanding or net income per share. Furthermore, no pro forma effect was given to the future potential exchanges of the Class B units of Silvercrest L.P. held by our principals that will be outstanding immediately after the consummation of the reorganization and the offering for a corresponding number of shares of our Class A common stock because the issuance of shares of Class A common stock upon these exchanges would not be dilutive. |

Employee bonuses and related payroll taxes of $ are expected to be paid in conjunction with the completion of this offering but have not been reflected in the unaudited pro forma statement of operations given the non-recurring nature of these payments. MANAGEMENT’S DISCUSSION AND ANALYSIS OF OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

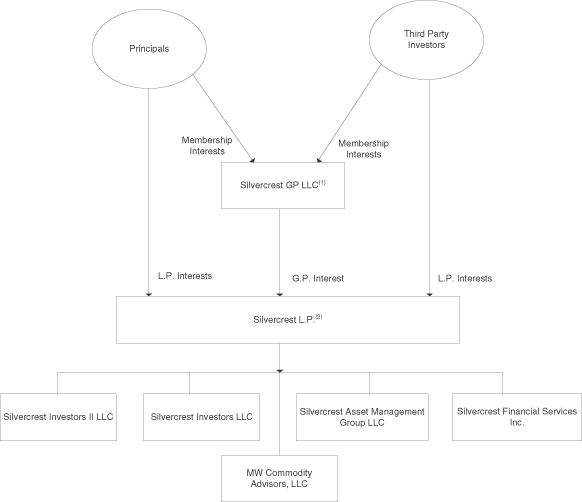

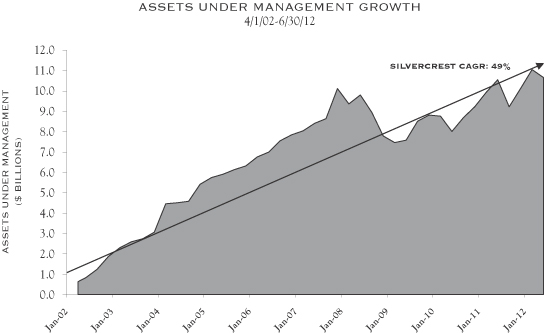

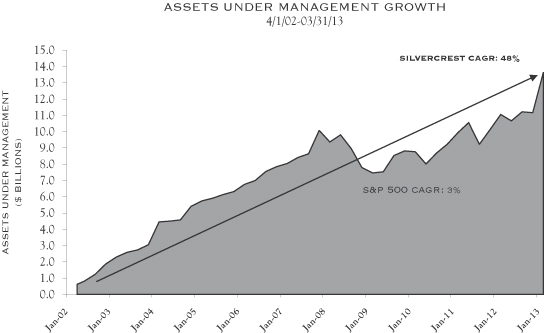

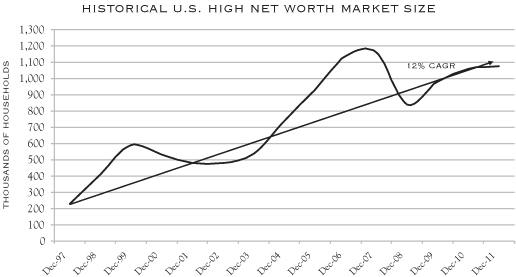

You should read this discussion and analysis of our financial condition and results of operation in conjunction with our “Selected Historical Consolidated Financial Data” and our historical financial statements and related notes included elsewhere in this prospectus. The information in this section contains forward-looking statements (see “Special Note Regarding Forward-Looking Statements”). Our actual results may differ significantly from the results suggested by these forward-looking statements and from our historical results. Some factors that may cause our results to differ are described in the “Risk Factors” section of this prospectus. The historical financial data discussed below reflect the historical results of operations and financial condition of Silvercrest L.P. and its subsidiaries and do not give effect to our reorganization. See “Reorganization“The Reorganization and Our Holding Company Structure” and “Unaudited Pro Forma Consolidated Financial Information,” included elsewhere in this prospectus, for a description of our reorganization and its effect on our historical results of operations. Overview We are a premier, full-service wealth management firm focused on providing financial advisory and related family office services to ultra-high net worth individuals and endowments, foundations and other institutional investors. In addition to a wide range of investment capabilities, we offer a full suite of complementary and customized family office services for families seeking a comprehensive oversight of their financial affairs. During the sixthree months ended June 30,March 31, 2013, our assets under management grew 21.4% from $11.2 billion to $13.6 billion. During the year ended December 31, 2012, our assets under management grew 5.9%10.9%, from $10.1 billion to $10.7 billion. During the twelve months ended December 31, 2011, our assets under management grew 9.8%, from $9.2 billion to $10.1$11.2 billion. As part of the reorganization of our company occurring in connection with this offering, Silvercrest will become the general partner of Silvercrest, L.P, our operating company. In addition, the partnership units of all continuing partners of Silvercrest L.P. will be reclassified as Class B units that have equal economic rights to our shares of Class A common stock. After giving effect to the reorganization described above, we will hold approximately % of the partnership interests in Silvercrest L.P. (or approximately % if the underwriters exercise in full their option to purchase additional shares). The partners in Silvercrest L.P. following this offering, consisting of 37 of our current employees and two non-employee partners, will collectively hold the remaining approximately % of the partnership interests in Silvercrest L.P. (or approximately % if the underwriters in full exercise their over-allotment option)option to purchase additional shares). In addition, Silvercrest L.P. has issued deferred equity units exercisable for Class B units which entitle the holderholders thereof to receive distributions from Silvercrest L.P. to the same extent as if the underlying Class B units were outstanding. Net profits and net losses of Silvercrest L.P. will be allocated, and distributions from Silvercrest L.P. will be made, to its current partners pro rata in accordance with their respective partnership units (and assuming the Class B units underlying all deferred equity units are outstanding). For more information on our reorganization, see “The Reorganization and Our Holding Company Structure.” The historical results of operations discussed in this Management’s Discussion and Analysis of Financial Condition and Results of Operations are those of Silvercrest L.P. and its subsidiaries. After the completion of the reorganization, as the general partner of Silvercrest L.P., we will control its business and affairs and, therefore, consolidate its financial results with ours. In light of our employees’ collective % partnership interest in Silvercrest L.P. immediately after the reorganization and this offering (or approximately % if the underwriters exercise in full their option to purchase additional shares), we will reflect the interests of these employees as a non-controlling interest in our consolidated financial statements. As a result, our net income, after amounts attributable to non-controlling interests, will represent % of Silvercrest L.P.’s net income (or approximately % if the underwriters exercise in full their option to purchase additional shares), and similarly, outstanding shares of our Class A common stock will represent % of the outstanding partnership units of Silvercrest L.P. (or approximately % if the underwriters exercise in full their over-allotment option)option to purchase additional shares). For more information on the pro forma impact of our reorganization, see “Unaudited Pro Forma Consolidated Financial Information.” Key Performance Indicators When we review our performance, we focus on the indicators described below: | | | | For the year ended December 31, | | | For the six months ended

June 30, | | | For the Years Ended December 31, | | For the Three Months Ended

March 31, | | (in thousands except as indicated) | | 2011 | | | 2010 | | | 2009 | | | 2012 | | | 2011 | | | 2012 | | 2011 | | 2010 | | 2013 | | 2012 | | Revenue | | $ | 42,787 | | | $ | 36,831 | | | $ | 32,534 | | | $ | 24,787 | | | $ | 20,779 | | | $ | 51,690 | | | $ | 42,787 | | | $ | 36,831 | | | $ | 13,685 | | | $ | 11,880 | | Income before other income (expense) | | $ | 14,446 | | | $ | 10,844 | | | $ | 2,207 | | | $ | 9,979 | | | $ | 7,881 | | | Income before other income (expense), net | | | $ | 18,902 | | | $ | 14,446 | | | $ | 10,844 | | | $ | 5,774 | | | $ | 4,546 | | Net income | | $ | 14,609 | | | $ | 10,942 | | | $ | 8,086 | | | $ | 9,404 | | | $ | 7,544 | | | $ | 19,720 | | | $ | 14,609 | | | $ | 10,942 | | | $ | 5,464 | | | $ | 4,289 | | Adjusted EBITDA (1) | | $ | 10,839 | | | $ | 9,068 | | | $ | 6,449 | | | $ | 6,776 | | | $ | 5,580 | | | $ | 14,702 | | | $ | 10,839 | | | $ | 9,068 | | | $ | 4,137 | | | $ | 3,447 | | Adjusted EBITDA margin (2) | | | 25.3% | | | | 24.6% | | | | 19.8% | | | | 27.3% | | | | 26.9% | | | | 28.4 | % | | | 25.3 | % | | | 24.6 | % | | | 30.2 | % | | | 29.0 | % | Assets under management at period end (in billions) | | $ | 10.1 | | | $ | 9.2 | | | $ | 8.8 | | | $ | 10.7 | | | $ | 10.6 | | | Average assets under management (in billions) (3) | | $ | 9.7 | | | $ | 9.0 | | | $ | 8.3 | | | $ | 10.4 | | | $ | 9.9 | | | Assets under management at period end (billions) | | | $ | 11.2 | | | $ | 10.1 | | | $ | 9.2 | | | $ | 13.6 | | | $ | 11.1 | | Average assets under management (billions) (3) | | | $ | 10.7 | | | $ | 9.7 | | | $ | 9.0 | | | $ | 12.4 | | | $ | 10.6 | |

| (1) | EBITDA represents net income before income tax expense, interest income, interest expense, depreciation and amortization. We define Adjusted EBITDA as EBITDA without giving effect to professional fees associated with acquisitions or financing transactions, losses on forgiveness of notes receivable from our principals, gains on extinguishment of debt or other obligations related to acquisitions, impairment charges and losses on disposals or abandonment of assets and leaseholds, client reimbursements and fund redemption costs, severance and other similar expenses, but including partner incentive allocations as an expense. See “Selected Historical Consolidated Financial Data” for a further explanation of Adjusted EBITDA and its reconciliation to net income on a basis consistent with GAAP. |

| (2) | Adjusted EBITDA margin is calculated by dividing Adjusted EBITDA by total revenue. |

| (3) | We have computed average assets under management by averaging assets under management at the beginning of the applicable period and assets under management at the end of the applicable period. |

Revenue We generate revenue from management and advisory fees, performance fees, and family office services fees. Our management and advisory fees are generated by managing assets on behalf of separate accounts and acting as investment adviser for various investment funds. Our performance fees relate to assets managed in external investment strategies in which we have a revenue sharing arrangement and in funds in which we have no partnership interest. Our management and advisory fees and family office services fees income is recognized through the course of the period in which these services are provided. Income from performance fees is recorded at the conclusion of the contractual performance period when all contingencies are resolved. In certain arrangements, we are only entitled to receive performance fees and allocations when the return on assets under management exceeds certain benchmark returns or other performance targets. The discretionary investment management agreements for our separately managed accounts do not have a specified term. Rather, each agreement may be terminated by either party at any time upon written notice of termination to the other party. The investment management agreements for our private funds are generally in effect from year to year, and may be terminated at the end of any year (or, in certain cases, on the anniversary of execution of the agreement) (i) by us upon 30 or 90 days’ prior written notice and (ii) after receiving the affirmative vote of a specified percentage of the investors in the private fund that are not affiliated with us, by the private fund on 60 or 90 days’ prior written notice. The investment management agreements for our private funds may also generally be terminated effective immediately by either party where the non-terminating party (i) commits a material breach of the terms subject, in certain cases, to a cure period, (ii) is found to have committed fraud, gross negligence or willful misconduct or (iii) terminates, become bankrupt, becomes insolvent or dissolves. Each of our investment management agreements contains customary indemnification obligations from us to our clients. The tables below set forth the amount of assets under management, the percentage of management and advisory fees revenues, the amount of revenue recognized, and the average assets under management for discretionary managed accounts and for private funds for each period presented. Discretionary Managed Accounts | | | | | | | | | | | | | | | | | | | | | | | | As of and for the

Year Ended

December 31, | | | As of and for the

Six Months

Ended

June 30, | | | (In billions) | | 2011 | | | 2010 | | | 2009 | | | 2012 | | | 2011 | | AUM concentrated in Discretionary Managed Accounts ($) | | $ | 6.2 | | | $ | 5.7 | | | $ | 5.3 | | | $ | 6.7 | | | $ | 6.4 | | Average AUM For Discretionary Managed Accounts | | $ | 6.0 | | | $ | 5.5 | | | $ | 5.0 | | | $ | 6.5 | | | $ | 6.1 | | Discretionary Managed Accounts Revenue ($) (in millions) | | $ | 32.5 | | | $ | 27.5 | | | $ | 24.0 | | | $ | 18.1 | | | $ | 16.1 | | Percentage of management and advisory fees revenue (%) | | | 86 | % | | | 85 | % | | | 82 | % | | | 81 | % | | | 87 | % | Private Funds | | | | | | | | | | | | | | | | | | | | | | | | As of and for the

Year Ended

December 31, | | | As of and for the

Six Months

Ended

June 30, | | | (In billions) | | 2011 | | | 2010 | | | 2009 | | | 2012 | | | 2011 | | AUM concentrated in Private Funds ($) | | $ | 0.8 | | | $ | 0.7 | | | $ | 0.8 | | | $ | 0.9 | | | $ | 0.7 | | Average AUM for Private Funds | | $ | 0.8 | | | $ | 0.8 | | | $ | 1.1 | | | $ | 0.9 | | | $ | 0.7 | | Private Funds Revenue ($) (in millions) | | $ | 5.4 | | | $ | 4.9 | | | $ | 5.3 | | | $ | 4.2 | | | $ | 2.4 | | Percentage of management and advisory fees revenue (%) | | | 14 | % | | | 15 | % | | | 18 | % | | | 19 | % | | | 13 | % |

| | | | | | | | | | | | | | | | | | | | | | | | As of and for the Years Ended December 31, | | | As of and for the Three

Months Ended March 31, | | (in billions) | | 2012 | | | 2011 | | | 2010 | | | 2013 | | | 2012 | | AUM concentrated in Discretionary Managed Accounts ($) | | $ | 7.1 | | | $ | 6.2 | | | $ | 5.7 | | | $ | 7.8 | | | $ | 6.9 | | Average AUM For Discretionary Managed Accounts | | $ | 6.7 | | | $ | 6.0 | | | $ | 5.5 | | | $ | 7.5 | | | $ | 6.6 | | Discretionary Managed Accounts Revenue ($) (in millions) | | $ | 37.6 | | | $ | 32.5 | | | $ | 27.5 | | | $ | 10.3 | | | $ | 8.7 | | Percentage of management and advisory fees revenue (%) | | | 82% | | | | 86% | | | | 85% | | | | 83% | | | | 81% | |

Private Funds | | | | | | | | | | | | | | | | | | | | | | | | As of and for the Years Ended December 31, | | | As of and for the Three

Months Ended March 31, | | (in billions) | | 2012 | | | 2011 | | | 2010 | | | 2013 | | | 2012 | | AUM concentrated in Private Funds ($) | | $ | 0.9 | | | $ | 0.8 | | | $ | 0.7 | | | $ | 0.9 | | | $ | 0.9 | | Average AUM For Private Funds | | $ | 0.9 | | | $ | 0.8 | | | $ | 0.8 | | | $ | 0.9 | | | $ | 0.9 | | Private Funds Revenue ($) (in millions) | | $ | 8.5 | | | $ | 5.4 | | | $ | 4.9 | | | $ | 2.2 | | | $ | 2.0 | | Percentage of management and advisory fees revenue (%) | | | 18% | | | | 14% | | | | 15% | | | | 17% | | | | 19% | |

Our advisory fees are primarily driven by the level of our assets under management. Our assets under management increase or decrease based on the net inflows or outflows of funds into our various investment strategies and the investment performance of our clients’ accounts. In order to increase our assets under management and expand our business, we must develop and market investment strategies that suit the investment needs of our target clients and provide attractive returns over the long term. Our ability to continue to attract clients will depend on a variety of factors including, among others: our ability to educate our target clients about our classic value investment strategies and provide them with exceptional client service; the relative investment performance of our investment strategies, as compared to competing products and market indices; competitive conditions in the investment management and broader financial services sectors; investor sentiment and confidence; and our decision to close strategies when we deem it to be in the best interests of our clients. The majority of advisory fees that we earn on separately-managed accounts are based on the value of assets under management on the last day of each calendar quarter. Most of our advisory fees are billed quarterly in advance on the first day of each calendar quarter. Our basic annual fee schedule for management of clients’ assets in separately managed accounts is: (i) for managed equity or balanced portfolios, 1% of the first $10 $10 million and 0.60% on the balance, (ii) for managed fixed income only portfolios, 0.40% on the first $10 million and 0.30% on the balance and (iii) for the municipal value strategy, 0.65%. Our fee for monitoring non-discretionary assets can range from 0.05% to 0.01%, but can also be incorporated into an agreed-upon fixed family office service fee. The majority of our client relationships pay a blended fee rate since they are invested in multiple strategies. Management fees earned on investment funds that we advise are calculated primarily based on the net assets of the funds. Some funds calculate investment fees based on the net assets of the funds as of the last business day of each calendar quarter, whereas other funds calculate investment fees based on the value of net assets on the first business day of the month. Depending on the investment fund, fees are paid either quarterly in advance or quarterly in arrears. For our private funds, the fees range from 0.25% to 1.5% annually. Certain management fees earned on investment funds for which we perform risk management and due diligence services are based on flat fee agreements customized for each engagement. Average management fee is calculated by dividing our actual revenue earned over a period by our average assets under management during the same period (which is calculated by averaging quarter-end assets under management for the applicable period). Our average management fee was 0.43%0.44% and 0.37%0.40% for the sixthree months ended June 30,March 31, 2013 and 2012, and 2011, respectively, and 0.39%was 0.43%, 0.36%0.39% and 0.35%0.36% for the years ended December 31, 2012, 2011 2010 and 2009,2010, respectively. Increases in our total average management fee rates are primarily the result of a change in the mix and increased concentration of our assets under management and increased concentration in our equities strategies whose fee rates are higher than those of other investment strategies. Advisory fees are also adjusted for any cash flows into or out of a portfolio, where the cash flow represents greater than 10% of the value of the portfolio. Silvercrest L.P. has authority to take fees directly from external custodian accounts of its separately managed accounts. Our advisory fees may fluctuate based on a number of factors, including the following: changes in assets under management due to appreciation or depreciation of our investment portfolios, and the levels of the contribution and withdrawal of assets by new and existing clients; allocation of assets under management among our investment strategies, which have different fee schedules; allocation of assets under management between separately managed accounts and advised funds, for which we generally earn lower overall advisory fees; and the level of our performance with respect to accounts and funds on which we are paid incentive fees. Our family office services capabilities enable us to provide comprehensive and integrated services to our clients. Our dedicated group of tax and financial planning professionals provide financial planning, tax planning and preparation, partnership accounting and fund administration and consolidated wealth reporting among other services. Family office services income fluctuates based on both the number of clients for whom we perform these services and the level of agreed-upon fees, most of which are flat fees. Therefore, non-discretionary assets under management, which are associated with family office services, do not typically serve as the basis for the amount of family office services revenue that is recognized. We have experienced a steady increase in family office services fees over the past few years as more of our separately managed accounts relationships have taken advantage of these services. We have also been successful in attracting new clients who have engaged us primarily for our family office services. Expenses Our expenses consist primarily of compensation and benefits expenses, as well as general and administrative expense including rent, professional services fees, data-related costs and sub-advisory fees. These expenses may fluctuate due to a number of factors, including the following: variations in the level of total compensation expense due to, among other things, bonuses, awards of equity to our employees and partners of Silvercrest L.P., changes in our employee count and mix, and competitive factors; and the level of management fees from funds that utilize sub-advisors will affect the amount of sub-advisory fees. We expect our professional services fees to increase after this offering as a result of being a public company. Compensation and Benefits Expense Our largest expense is compensation and benefits, which includes the salaries, bonuses, equity-based compensation and related benefits and payroll costs attributable to our principals and employees. Our compensation methodology is intended to meet the following objectives: (i) support our overall business strategy; (ii) attract, retain and motivate top-tier professionals within the investment management industry; and (iii) align our partner’employees’ interests with those of our equity owners. We have experienced, and expect to continue to experience, a general rise in compensation and benefits expense commensurate with growth in headcount and with the need to maintain competitive compensation levels. Upon the completion of the reorganization and this offering, we will account for partner incentive payments as an expense in our statement of operations and have reflected the related adjustments in our pro forma financial statements. Accordingly, this will have the effect of increasing compensation expense relative to the amounts that have been recorded historically in our financial statements. See “Unaudited Pro Forma Consolidated Financial Information.” The components of our compensation expenses for the three months ended March 31, 2013 and 2012 and three years ended December 31, 2011 and the six months ended June 30, 2012 and 2011 are as follows: | | | | For the Year Ended December 31, | | | For the Six Months Ended

June 30, | | | For the Year Ended December 31, | | | For the Three Months Ended

March 31, | | (in thousands) | | 2011 | | | 2010 | | | 2009 | | | 2012 | | | 2011 | | | 2012 | | | 2011 | | | 2010 | | | 2013 | | | 2012 | | Cash compensation and benefits | | $ | 16,495 | | | $ | 15,936 | | | $ | 15,630 | | | $ | 8,777 | | | $ | 7,973 | | | $ | 17,726 | | | $ | 16,495 | | | $ | 15,936 | | | $ | 4,574 | | | $ | 4,331 | | Distributions on liability awards (1) | | | 20 | | | | 9 | | | | — | | | | 17 | | | | 5 | | | | 28 | | | | 20 | | | | 9 | | | | 7 | | | | 6 | | Non-cash equity-based compensation expense | | | 977 | | | | 583 | | | | — | | | | 806 | | | | 496 | | | | 1,354 | | | | 977 | | | | 583 | | | | 620 | | | | 431 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | Total compensation expense | | $ | 17,492 | | | $ | 16,528 | | | $ | 15,630 | | | $ | 9,600 | | | $ | 8,474 | | | $ | 19,108 | | | $ | 17,492 | | | $ | 16,528 | | | $ | 5,201 | | | $ | 4,768 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | Cash distributions on the portion of unvested deferred equity units that are subject to forfeiture are expensed when paid. Unvested deferred equity units are classified as liability awards. |

On February 29, 2012, February 28, 2011 and February 24, 2010, Silvercrest L.P. and Silvercrest GP LLC, our predecessor, granted equity-based compensation awards to certain of their principals based on the fair value of the equity interests of Silvercrest L.P. and Silvercrest GP LLC. Each grant includes a deferred equity unit and performance unit, subject to forfeiture and acceleration of vesting. Each 100 deferred equity units represent the unsecured right to receive one unit of Silvercrest GP LLC and 99 units of Silvercrest L.P., subject to vesting over a four-year period beginning on the first-yearfirst anniversary of the date of grant. Each deferred equity unit, whether vested or unvested, entitles the holder to receive distributions from Silvercrest L.P. and Silvercrest GP LLC as if such holder held such unit. Upon each vesting date, a holder may receive the number of units vested or the equivalent cash value and units, but in no event may the holder receive more than 50% of the aggregate value in cash. To the extent that holders elect to receive up to 50% of the aggregate value in cash, we could have less cash to utilize. We have accounted for the distributions on the portion of the deferred equity units that are subject to forfeiture as compensation expense. Equity-based compensation expense will be recognized on the February 29, 2012, February 28, 2011 and February 24, 2010 deferred equity unit and performance unit awards through February 29, 2016, February 28, 2015 and February 24, 2014, respectively. Each performance unit represents the right to receive one unit of Silvercrest L.P. and one unit of Silvercrest GP LLC for each two units of Silvercrest L.P. and Silvercrest GP LLC, respectively, issued upon vesting of the deferred equity units awarded to the employee, in each case subject to the achievement of defined performance goals. Although performance units will only vest upon the achievement of the performance goals, they are expensed over the same vesting period as the deferred equity units thatwith which they are associated with because there is an explicit service period. For more information on the terms of the deferred equity units and performance units, see “Compensation Discussion and Analysis—Deferred Equity Units and Performance Units.” General and Administrative Expenses General and administrative expenses include occupancy-related costs, professional and outside services fees, office expenses, depreciation and amortization, sub-advisory fees and the costs associated with operating and maintaining our research, trading and portfolio accounting systems. Our costs associated with operating and maintaining our research, trading and portfolio accounting systems and professional services expenses generally increase or decrease in relative proportion to the number of employees retained by us and the overall size and scale of our business operations. Sub-advisory fees will fluctuate based on the level of management fees from funds that utilize sub-advisors. Following this offering, we expect that we will incur additional expenses as a result of becoming a public company for, among other things, directors and officers insurance, director fees, SEC reporting and compliance, including Sarbanes-Oxley compliance, transfer agent fees, professional fees and other similar expenses. These additional expenses will reduce our net income. Other Income Other income is derived primarily from investment income arising from our investments in various private investment funds that were established as part of our investment strategies. We expect the investment components of other income, in the aggregate, to fluctuate based on market conditions and the success of our investment strategies. Performance fees earned from those investment funds in which we have a partnership interest have been earned over the past few years as a result of the achievement of various high water marks depending on the investment fund. These performance fees are recorded based on the equity method of accounting. The majority of our performance fees over the past few years have been earned from our fixed income-related funds. Minority and Non-Controlling Interests After our reorganization, we will be the general partner of Silvercrest L.P. and will control its business and affairs and, therefore, consolidate its financial results with ours. In light of our employees’ expected % interest in Silvercrest L.P. (or % if the underwriters exercise in full their option to purchase additional shares) immediately after the consummation of the reorganization and this offering, we will reflect their partnership interests as a non-controlling interestinterests in our consolidated financial statements. As a result, immediately after the consummation of this offering, our net income, after income attributable to non-controlling interests, will represent % of Silvercrest L.P.’s net income (or % if the underwriters exercise in full their option to purchase additional shares), and similarly, outstanding shares of our Class A common stock will represent % of the outstanding partnership units of Silvercrest L.P. (or % if the underwriters exercise in full their option to purchase additional shares). Provision for Income Tax While Silvercrest L.P. has historically not been subject to U.S. federal and certain state income taxes, it has been subject to the New York City Unincorporated Business Tax. As a result of our reorganization, we will become subject to taxes applicable to C-corporations. We expect our effective tax rate, and the absolute dollar amount of our tax expense, to increase as a result of this reorganization offset by the benefits of the tax receivable agreement. For more information on the pro forma income taxes applicable to us under C-corporation status, see “The Reorganization and Our Holding Company Structure” and “Unaudited Pro Forma Consolidated Financial Information.” Significant TransactionsAcquisition

Milbank

On November 1, 2011,March 28, 2013, we acquired substantially all of thecertain assets of Milbank Winthrop & Co., Inc., or Milbank,Ten-Sixty. Ten-Sixty is a registered investment adviser that managedadvises on approximately $500 million$1.9 billion of assets primarily on behalf of ultra-high net worth families. Theinstitutional clients. This strategic acquisition expands our hedge fund due diligence capabilities and continues the growth of Milbank, a long-standing and highly regarded investment boutique, strengthens Silvercrest L.P.’s presence in the New York market and adds investment managers that have significant experience and knowledge of the industry. Under the terms of the asset purchase agreement, the purchase price for the assets of Milbank consisted of a cash consideration of $3.4 million (net of cash acquired of $0.8 million), interests in Silvercrest L.P. and Silvercrest GP LLC with a fair value of $3.1 million, and a promissory note issued by Silvercrest Asset Management Group LLC to Milbank for $3.2 million. As part of the asset purchase agreement, we are obligated to make future earnout payments to Milbank should specific financial and performance targets be achieved by the Milbankour institutional business. We determined that the acquisition-date fair value of the contingent consideration was $1.7 million based on the likelihood that the financial and performance targets included in the asset purchase agreement will be achieved. Under the terms of the asset purchase agreement, Milbank is entitledwe paid cash consideration at closing of $2.5 million and issued a promissory note to receive six earnout paymentsTen-Sixty for the following periods: November 1, 2011 through December 31, 2011, full calendar years 2012, 2013, 2014 and 2015, and January 1, 2016 through October 31, 2016. Each earnout payment is equal$1.5 million subject to 20% of EBITDA generated by the Milbank business (as defined in the asset purchase agreement) during the relevant earnout period.adjustment. The aggregate principal amount of the earnout payment will vary dependingpromissory note is payable in two initial installments of $0.2 million each on the level of EBITDA that is generated in each respective earnout period. Milbank revenueApril 30, 2013 and operating expenses for the two months ended December 31, 2011 were $0.92013 and then quarterly installments from June 30, 2014 through March 31, 2017 of $0.1 million and $0.4 million, respectively.

LongChamp

In 2009, we entered into a settlement agreement witheach. The principal amount outstanding under this note bears interest at the former ownersrate of The LongChamp Group, Inc., or LGI, to close the business of LGI, a hedge fund advisory business, which was acquired by Silvercrest L.P. in 2007, and terminate all agreements between them and our company. The termination of these agreements coupled with declining economic conditions resulted in various client redemptions. LGI was ultimately wound down in 2009. For further explanation of the closing of the LGI business, see Note 10 to the audited consolidated financial statements of Silvercrest L.P. included elsewhere in this prospectus.five percent per annum.

Operating Results Revenue Our revenues for the sixthree months ended June 30,March 31, 2013 and 2012 and 2011 and the years ended December 31, 2012, 2011 2010 and 20092010 are set forth below: | | | | | | | | | | | For the Three Months Ended March 31, | | | (in thousands) | | For the Six Months Ended June 30, | | | 2013 | | | 2012 | | | 2013 vs. 2012 ($) | | | 2013 vs. 2012 (%) | | | | | 2012 | | | 2011 | | | 2012 vs. 2011 ($) | | 2012 vs. 2011 (%) | | | Management and advisory fees | | $ | 22,327 | | | $ | 18,539 | | | $ | 3,788 | | | | 20.4 | % | | $ | 12,457 | | | $ | 10,682 | | | $ | 1,775 | | | | 16.6 | % | Performance fees and allocations | | | 16 | | | | 31 | | | | (15 | ) | | | -48.4 | % | | | 3 | | | | — | | | | 3 | | | | Family office services | | | 2,444 | | | | 2,209 | | | | 235 | | | | 10.6 | % | | | 1,225 | | | | 1,198 | | | | 27 | | | | 2.3 | % | | | | | | | | | | | | | | | | | | | | | | | | Total revenue | | $ | 24,787 | | | $ | 20,779 | | | $ | 4,008 | | | | 19.3 | % | | $ | 13,685 | | | $ | 11,880 | | | $ | 1,805 | | | | 15.2 | % | | | | | | | | | | | | | | | | | | | | | | | |

| | | | For the Year Ended December 31, | | | For the Years Ended December 31, | | | | | 2011 | | | 2010 | | | 2011 vs. 2010 ($) | | 2011 vs. 2010 (%) | | | (in thousands) | | | 2012 | | | 2011 | | | 2012 vs. 2011 ($) | | | 2012 vs. 2011 (%) | | Management and advisory fees | | $ | 37,869 | | | $ | 32,442 | | | $ | 5,427 | | | | 16.7 | % | | $ | 46,069 | | | $ | 37,869 | | | $ | 8,200 | | | | 21.7 | % | Performance fees and allocations | | | 85 | | | | 548 | | | | (463 | ) | | | -84.5 | % | | | 714 | | | | 85 | | | | 629 | | | | 740.0 | % | Family office services | | | 4,833 | | | | 3,841 | | | | 992 | | | | 25.8 | % | | | 4,907 | | | | 4,833 | | | | 74 | | | | 1.5 | % | | | | | | | | | | | | | | | | | | | | | | | | Total revenue | | $ | 42,787 | | | $ | 36,831 | | | $ | 5,956 | | | | 16.2 | % | | $ | 51,690 | | | $ | 42,787 | | | $ | 8,903 | | | | 20.8 | % | | | | | | | | | | | | | | | | | | | | | | | | | | | | For the Year Ended December 31, | | | | | | 2010 | | | 2009 | | | 2010 vs. 2009 ($) | | 2010 vs. 2009 (%) | | | Management and advisory fees | | $ | 32,442 | | | $ | 29,341 | | | $ | 3,101 | | | | 10.6 | % | | Performance fees and allocations | | | 548 | | | | 96 | | | | 452 | | | | 470.8 | % | | Family office services | | | 3,841 | | | | 3,097 | | | | 744 | | | | 24.0 | % | | | | | | | | | | | | | | | Total revenue | | $ | 36,831 | | | $ | 32,534 | | | $ | 4,297 | | | | 13.2 | % | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | For the Years Ended December 31, | | (in thousands) | | 2011 | | | 2010 | | | 2011 vs. 2010 ($) | | | 2011 vs. 2010 (%) | | Management and advisory fees | | $ | 37,869 | | | $ | 32,442 | | | $ | 5,427 | | | | 16.7 | % | Performance fees and allocations | | | 85 | | | | 548 | | | | (463 | ) | | | -84.5 | % | Family office services | | | 4,833 | | | | 3,841 | | | | 992 | | | | 25.8 | % | | | | | | | | | | | | | | | | | | Total revenue | | $ | 42,787 | | | $ | 36,831 | | | $ | 5,956 | | | | 16.2 | % | | | | | | | | | | | | | | | | | |

The growth in our assets under management during the sixthree months ended June 30, 2011March 31, 2013 and 2012 and from December 31, 2009January 1, 2010 to December 31, 2011 and2012 is described below: | | | | | | | | | Assets Under Management | | | (in billions) | | Assets Under Management | | | Discretionary | | Non-

Discretionary | | Total | | As of December 31, 2011 | | | $ | 7.0 | | | $ | 3.1 | | | $ | 10.1 | | Gross client additions | | | | 1.6 | | | | 0.1 | | | | 1.7 | | Gross client withdrawals | | | | (1.3 | ) | | | (0.1 | ) | | | (1.4 | ) | Market appreciation | | | | 0.4 | | | | 0.3 | | | | 0.6 | | | | | Discretionary | | Non-Discretionary | | Total | | | | | | | | | | | As of December 31, 2010 | | $ | 6.3 | | | $ | 2.9 | | | $ | 9.2 | | | As of March 31, 2012 | | | $ | 7.7 | | | $ | 3.4 | | | $ | 11.1 | (2) | | | | | | | | | | | | As of December 31, 2012 | | | $ | 8.0 | | | $ | 3.1 | | | $ | 11.2 | | Gross client additions | | | | 1.6 | | | | 2.0 | | | | 3.6 | | Gross client withdrawals | | | | (1.5 | ) | | | (0.2 | ) | | | (1.7 | ) | Market appreciation | | | | 0.5 | | | | 0.1 | | | | 0.6 | | | | | | | | | | | | | As of March 31, 2013 | | | $ | 8.6 | | | $ | 5.0 | | | $ | 13.6 | (2) | | | | | | | | | | | | As of January 1, 2010 | | | $ | 6.1 | | | $ | 2.7 | | | $ | 8.8 | | Gross client inflows | | | 1.5 | | | | 1.0 | | | | 2.5 | | | | 1.5 | | | | 1.0 | | | | 2.5 | | Gross clientoutflows | | | (1.1 | ) | | | (0.7 | ) | | | (1.8 | ) | | | (1.7 | ) | | | (0.8 | ) | | | (2.5 | ) | Market appreciation (1) | | | 0.4 | | | | 0.3 | | | | 0.7 | | | | | | | | | | | | | | As of June 30, 2011 | | $ | 7.1 | | | $ | 3.5 | | | $ | 10.6 | | | | | | | | | | | | | | As of December 31, 2011 | | $ | 7.0 | | | $ | 3.1 | | | $ | 10.1 | | | Gross client inflows | | | 3.0 | | | | 0.3 | | | | 3.3 | | | Gross clientoutflows | | | (2.7 | ) | | | (0.3 | ) | | | (3.0 | ) | | Market appreciation (1) | | | 0.3 | | | | — | | | | 0.3 | | | | | | | | | | | | | | As of June 30, 2012 | | $ | 7.6 | | | $ | 3.1 | | | $ | 10.7 | | | | | | | | | | | | | | As of January 1, 2009 | | $ | 6.0 | | | $ | 1.8 | | | $ | 7.8 | | | Gross client inflows | | | 1.4 | | | | 0.5 | | | | 1.9 | | | Gross client outflows | | | (2.5 | ) | | | (0.7 | ) | | | (3.2 | ) | | Market appreciation (1) | | | 1.2 | | | | 1.1 | | | | 2.3 | | | | | | | | | | | | | | As of December 31, 2009 | | $ | 6.1 | | | $ | 2.7 | | | $ | 8.8 | | | Gross client inflows | | | 1.5 | | | | 1.0 | | | | 2.5 | | | Gross clientoutflows | | | (1.7 | ) | | | (0.8 | ) | | | (2.5 | ) | | Market appreciation (depreciation) (1) | | | 0.5 | | | | (0.1 | ) | | | 0.4 | | | Market appreciation (depreciation) (1) | | | | 0.5 | | | | (0.1 | ) | | | 0.4 | | | | | | | | | | | | | | | | | | | | | As of December 31, 2010 | | $ | 6.4 | | | $ | 2.8 | | | $ | 9.2 | | | | 6.3 | | | | 2.9 | | | | 9.2 | | Gross client inflows | | | 3.6 | | | | 1.5 | | | | 5.1 | | | | 3.8 | | | | 1.5 | | | | 5.3 | | Gross clientoutflows | | | (3.1 | ) | | | (1.1 | ) | | | (4.2 | ) | | | (3.1 | ) | | | (1.2 | ) | | | (4.3 | ) | Market appreciation (depreciation) (1) | | | 0.1 | | | | (0.1 | ) | | | — | | | | 0.1 | | | | (0.1 | ) | | | — | | | | | | | | | | | | | | | | | | | | | As of December 31, 2011 | | $ | 7.0 | | | $ | 3.1 | | | $ | 10.1 | (2) | | | 7.0 | | | | 3.1 | | | | 10.1 | | Gross client inflows | | | | 6.7 | | | | 0.6 | | | | 7.3 | | Gross client outflows | | | | (6.3 | ) | | | (0.6 | ) | | | (6.9 | ) | Market appreciation (1) | | | | 0.5 | | | | 0.1 | | | | 0.6 | | | | | | | | | | | | | | | | | | | | | As of December 31, 2012 | | | $ | 8.0 | | | $ | 3.1 | | | $ | 11.2 | (2) | | | | | | | | | | | |

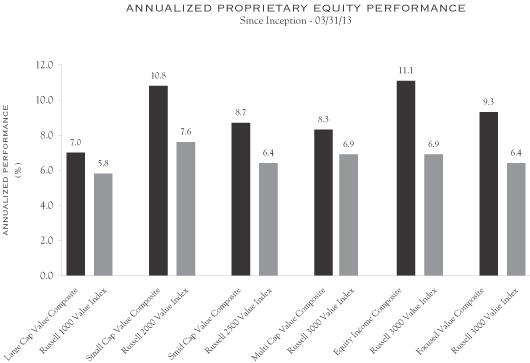

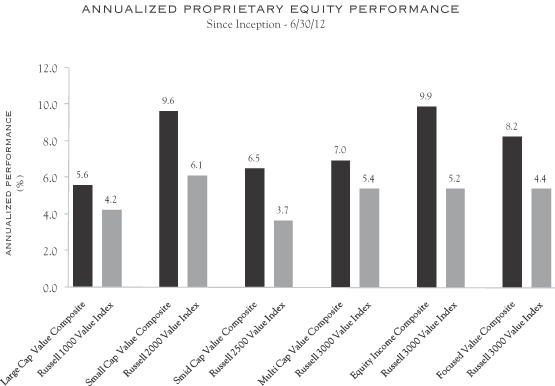

| (1) | For additional investment strategy performance information disclosed elsewhere in this prospectus, please see the “Business” section. |

| (2) | Less than 5% of assets under management generate performance fees. |

SixThree Months Ended June 30,March 31, 2013 versus Three Months Ended March 31, 2012

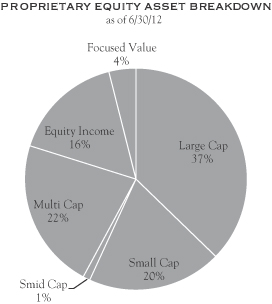

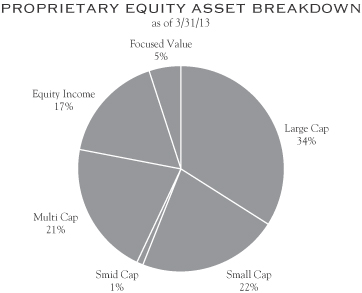

Our total revenue increased by $1.8 million, or 15.2%, to $13.7 million for the three months ended March 31, 2013, from $11.9 million for the three months ended March 31, 2012. This increase was driven primarily by growth in our management and advisory fees as a result of increased assets under management. Assets under management increased by $2.4 billion, or 21.4%, to $13.6 billion at March 31, 2013 from $11.2 billion at December 31, 2012. Contributing to the growth in assets under management was $1.9 billion of assets under management related to the Ten-Sixty acquisition, $1.6 billion of client inflows and $0.6 billion in market appreciation, partially offset by client outflows of $1.7 billion. Our market appreciation during the three months ended March 31, 2013 constituted a 5.4% rate of increase in our total assets under management compared to the year ended December 31, 2012. Our growth in assets under management for the three months ended March 31, 2013 was attributable to an increase of $0.6 billion and $1.9 billion in discretionary and non-discretionary assets under management, respectively, primarily related to the Ten-Sixty acquisition, The growth in our discretionary assets under management was primarily driven by an increase in separately managed accounts. An increase in the concentration of equity securities, which are included in discretionary assets under management and whose fee rates are higher than those of other investments, was the primary driver of increased management and advisory fees revenue for the three months ended March 31, 2013 compared to the prior year. Sub-advised fund management revenue remained flat for the three months ended March 31, 2013 compared to the same period in the prior year. Proprietary fund management revenue increased by $0.2 million to $1.9 million for the three months ended March 31, 2013 from $1.7 million for the same period in the prior year. This increase in proprietary fund management revenue was primarily attributable to market appreciation. With respect to our discretionary assets under management, equity assets experienced growth of 11.7% during the three months ended March 31, 2013 while fixed income assets experienced growth of 1.9% during the same period. Most of our growth came from our small cap value, equity income and large cap value strategies with composite returns of 12.7%, 11.8% and 12.2%, respectively. As of March 31, 2013, the composition of our assets under management was 63% in discretionary assets, which includes both separately managed accounts and proprietary and sub-advised funds, and 37% in non-discretionary assets which represent assets on which we provide portfolio reporting but do not have investment discretion. Year Ended December 31, 2012 versus Six MonthsYear Ended June 30,December 31, 2011 Our total revenue increased by $4.0$8.9 million, or 19.3%20.8%, to $24.8$51.7 million for the six monthsyear ended June 30,December 31, 2012, from $20.8$42.8 million for the six monthsyear ended June 30,December 31, 2011. This increase was driven primarily by growth in our management and advisory fees as a result of increased assets under management. Assets under management increased by $0.6$1.1 billion, or 5.9%10.9%, to $10.7$11.2 billion at June 30,December 31, 2012 from $10.1 billion at December 31, 2011. Contributing to the growth in assets under management was $3.3$7.3 billion of client inflows and $0.3$0.7 billion in market appreciation, partially offset by client outflows of $3.0$6.9 billion. Our market appreciation during the six monthsyear ended June 30,December 31, 2012 constituted a 3.0%6.9% rate of increase in our total assets under management compared to the year ended December 31, 2011. Our growth in assets under management for the six monthsyear ended June 30,December 31, 2012 was primarily attributable to an increase of $0.6$0.9 billion in separately managed accounts, which are included in discretionary assets under management. An increase in the concentration of equity securities, which are included in discretionary assets under management and whose fee rates are higher than those of other investments, was the primary driver of increased management and advisory fees revenue for the six monthsyear ended June 30,December 31, 2012 compared to the same period in the prior year. Sub-advised fund management revenue decreased by $0.3$0.4 million to $0.6$1.2 million for the six monthsyear ended June 30,December 31, 2012 from $0.9$1.6 million for the same period in the prior year. While sub-advised fund assets under management remained flat as of June 30,December 31, 2012 as compared to December 31, 2011, client redemptions primarily contributed to the decrease in sub-advised fund management revenue. Proprietary fund management revenue increased by $2.1$3.5 million to $3.7$7.3 million for the six monthsyear ended June 30,December 31, 2012 from $1.6$3.8 million for the same period in the prior year. This increase in proprietary fund management revenue was attributable to a $0.4 billion increase in proprietary fund assets under management from $0.4 billion asthe acquisition of June 30, 2011 to $0.8 billion as of June 30, 2012 primarily as a result of the addition of $0.3 billion of Milbank fund assets under management in November 2011. With respect to our discretionary assets under management, equity and fixed income assets experienced growth of 23.7% and 3.6%, respectively, for30.5% during the six monthsyear ended June 30, 2012.December 31, 2012 while fixed income assets were flat during the same period. Most of our growth came from our equity incomeSMID cap, multi cap and small cap value strategies with composite returns of 8.0%16.7%, 16.5% and 7.7%16.0%, respectively. As of June 30,December 31, 2012, the composition of our assets under management was 71%72% in discretionary assets, which includes both separately managed accounts and proprietary and sub-advised funds, and 29%28% in non-discretionary assets which represent assets on which we provide portfolio reporting but do not have investment discretion. Assets under managementPerformance fee revenue increased by $1.4 billion, or 15.2%,$629 thousand to $10.6 billion at June 30, 2011 from $9.2 billion at December 31, 2010. Contributing to the growth in assets under management was $2.5 billion of client inflows and $0.7 billion in market appreciation partially offset by client outflows at $1.8 billion. Our market appreciation during the six months ended June 30, 2011 constituted a 7.6% rate of increase in our total assets under management compared to$714 thousand for the year ended December 31, 2010. Our growth in assets under management2012 from $85 thousand for the six monthsyear ended June 30, 2011 wasDecember 31, 2011. These performance fees are primarily related to external investment strategies in which we have a revenue sharing arrangement. The increase in performance fee revenue is directly attributable to an increasehigher returns achieved at our external investment strategies. The balance of $0.8 billion in separately managed accounts, whichour performance fees are earned from proprietary funds and are included in discretionary assets under management, and $0.6 billionequity income from investments, which is discussed below in non-discretionary assets. An increase in“—Other Income (Expense).”

Family office services income increased by $0.1 million or 1.5%, from $4.8 million for the concentration of equity securities, which are included in discretionary assets under management and whose fee rates are higher than those of other investments, wasyear ended December 31, 2011 to $4.9 million for the primary driveryear ended December 31, 2012, primarily as a result of increased discretionary assets under managementfees from December 31, 2010 to June 30, 2011. Proprietary fund assets under management asexisting clients because of June 30, 2011 remained flat as compared to December 31, 2010. With respect to our discretionary assets under management, equities experienced growthincreased rates in certain cases and a greater amount of 17.6% while fixed income assets remained flat for the six months ended June 30, 2011. Most of our growth came from our equity income, large cap value, multi cap value, and small cap value portfolios with composite returns of 8.0%, 7.3%, 9.1%, and 8.2%, respectively. The increaseservices provided in non-discretionary assets was primarily driven by a new family office relationship entered into during the six months ended June 30, 2011. As of June 30, 2011, the composition of our assets under management was 67% in discretionary assets, which includes both separately managed accounts and proprietary and sub-advised funds, and 33% in non-discretionary assets which represent assets on which we provide portfolio reporting but do not have investment discretion.other cases. Year Ended December 31, 2011 versus Year Ended December 31, 2010 Our total revenue increased by $6.0 million, or 16.2%, to $42.8 million for the year ended December 31, 2011, from $36.8 million for the year ended December 31, 2010. This increase was driven primarily by growth in our management and advisory fees as a result of increased assets under management. Assets under management increased by $0.9 billion, or 9.8%, to $10.1 billion at December 31, 2011 from $9.2 billion at December 31, 2010. Contributing to the growth in assets under management was $5.1 billion of net client inflows partially offset by $4.2 billion of client outflows. Our growth in assets under management in 2011 was primarily attributable to an increase of $0.5 billion in separately managed accounts and $0.2 billion in proprietary and sub-advised funds, which are included in discretionary assets under management. An increase in the concentration of equity securities, which are included in discretionary assets under management and whose fee rates are higher than those of other investments, was the primary driver of increased management and advisory fees revenue for the year ended December 31, 2011 compared to the year ended December 31, 2010. Sub-advised fund management revenue increased by $0.2 million to $1.6 million for the year ended December 31, 2011 from $1.4 million for the year ended December 31, 2010 while sub-advised fund assets under management remained flat. Proprietary fund management revenue increased by $0.3 million to $3.8 million for the year ended December 31, 2011 from $3.5 million for the year ended December 31, 2010. This increase in proprietary fund management revenue was attributable to a $0.2 billion increase in proprietary fund assets under management from $0.5 billion as of December 31, 2010 to $0.7 billion as of December 31, 2011. This increase was primarily the result of the addition of $0.3 billion of Milbank fund assets under management in November 2011, partially offset by $0.1 billion of client fund redemptions. With respect to our discretionary assets under management, equities experienced growth of 9.4% while fixed income assets declined 3.0% for the year ended December 31, 2011. Most of our growth came from our equity income, multi cap value and small cap value strategies with composite returns of 4.4%, 0.5%, and 1.5%, respectively. As of December 31, 2011, the composition of our assets under management was 70% in discretionary assets, which includes both separately managed accounts and proprietary and sub-advised funds, and 30% in non-discretionary assets, which represent assets on which we provide portfolio reporting but do not have investment discretion. Performance fee revenue decreased by $463 thousand to $85 thousand for the year ended December 31, 2011 from $548 thousand for the year ended December 31, 2010. These performance fees are primarily related to external investment strategies in which we have a revenue sharing arrangement. The decrease in performance fee revenue is directly attributable to lower returns achieved at our external investment strategies. The balance of our performance fees are earned from proprietary funds and are included in equity income from investments, which is discussed below in “—Other Income (Expense)., Net.” Family office services income increased by $1.0 million or 25.8%, from $3.8 million for the year ended December 31, 2010 to $4.8 million for the year ended December 31, 2011, primarily as a result of the addition of significant family relationships in 2011 and increased fees from existing clients because of increased rates in certain cases and a greater amount of services provided in other cases. Year Ended December 31, 2010 versus Year Ended December 31, 2009

Our total revenue increased by $4.3 million, or 13.2%, to $36.8 million for the year ended December 31, 2010, from $32.5 million for the year ended December 31, 2009. This increase was driven primarily by growth in our management and advisory fees as a result of increased assets under management.

Assets under management increased by $0.4 billion, or 4.5%, to $9.2 billion at December 31, 2010 from $8.8 billion at December 31, 2009. Contributing to the growth in assets under management was $0.4 billion in market appreciation. Our market appreciation during the year ended December 31, 2010 constituted a 4.5% rate of increase in our total assets under management compared to the year ended December 31, 2009. Our growth in assets under management in 2010 was attributable to an increase of $0.3 billion in discretionary separately managed accounts, and $0.2 billion in non-discretionary assets. An increase in the concentration of equity securities, which are included in discretionary assets under management and whose fee rates are higher than those of other investments, was the primary driver of increased management and advisory fees revenue for the year ended December 31, 2010 compared to the year ended December 31, 2009. Sub-advised fund management revenue decreased by $1.0 million to $1.4 million for the year ended December 31, 2010 from $2.4 million for the year ended December 31, 2009. With respect to our discretionary assets under management, equities experienced growth of 13.0% while fixed income assets declined 6.3% for the year ended December 31, 2010. Most of our growth came from our equity income, large cap value, multi cap value and small cap value strategies with composite returns of 17.5%, 15.4%, 19.4%, and 25.7%, respectively. The closing of our LongChamp business contributed to this decrease in sub-advised fund management revenue. Proprietary fund management revenue increased by $0.5 million to $3.5 million for the year ended December 31, 2010 from $3.0 million for the year ended December 31, 2009. As of December 31, 2010, the composition of our assets under management was 69% in discretionary assets, which includes both separately managed accounts and proprietary and sub-advised funds, and 31% in non-discretionary assets, which represent assets on which we provide portfolio reporting but do not have investment discretion.

Assets under management increased by $1.0 billion, or 12.8%, to $8.8 billion at December 31, 2009 from $7.8 billion at December 31, 2008. Contributing to the growth in assets under management was $1.9 billion of

client inflows and $2.3 billion in market appreciation, partially offset by $3.2 billion of client outflows. Our market appreciation during the year ended December 31, 2009 constituted a 29.5% rate of increase in our total assets under management compared to the year ended December 31, 2008. Our growth in assets under management in 2009 was attributable to an increase of $0.2 billion in separately managed accounts, which are included in discretionary assets under management, and $0.9 billion in non-discretionary assets. An increase in the concentration of equity securities, which are included in discretionary assets under management, was the primary driver of increased management and advisory fees revenue for the year ended December 31, 2009 compared to the year ended December 31, 2008. Sub-advised fund management revenue decreased by $5.7 million to $2.4 million for the year ended December 31, 2009 from $8.1 million for the year ended December 31, 2008. This decrease in sub-advised fund management revenue was the result of a decrease in sub-advised fund assets under management from $0.5 billion as of December 31, 2008 to $0.3 billion as of December 31, 2009 because of the closing of our LongChamp business and other client fund redemptions. Proprietary fund management revenue decreased by $1.1 million to $3.0 million for the year ended December 31, 2009 from $4.1 million for the year ended December 31, 2008 primarily as a result of lower revenue from our fixed income funds. With respect to our discretionary assets under management, equity and fixed income assets experienced growth of 34.9% and 43.3%, respectively, for the year ended December 31, 2009. Most of our growth came from our large cap value, multi cap value, and small cap value strategies with composite returns of 29.6%, 30.5%, and 24.7%, respectively. Most of our fixed income asset growth came from our separately managed accounts with composite returns for our taxable high yield and core fixed income strategies of 36.5% and 3.0%, respectively. As of December 31, 2009, the composition of our assets under management was 69% in discretionary assets, which includes both separately managed accounts and proprietary and sub-advised funds, and 31% in non-discretionary assets, which represent assets on which we provide portfolio reporting but do not have investment discretion.

Performance fee revenue increased by $452 thousand to $548 thousand for the year ended December 31, 2010 from $96 thousand for the year ended December 31, 2009. These performance fees are primarily related to external investment strategies in which we have a revenue sharing arrangement. The increase in performance fee revenue is directly attributable to higher returns achieved at our external investment strategies. The balance of our performance fees are included in equity income from investments which is discussed below in “—Other Income (Expense).”

Family office services income increased by $0.7 million, or 24.0%, from $3.1 million for the year ended December 31, 2009 to $3.8 million for the year ended December 31, 2010, primarily as a result of increases to fee rates for existing clients.

Expenses Our expenses for the sixthree months ended June 30,March 31, 2013 and 2012 and 2011 and the years ended December 31, 2012, 2011 2010 and 20092010 are set forth below: | | | | | | | | | | | For the Three Months Ended March 31, | | | (in thousands) | | For the Six Months Ended June 30, | | | 2013 | | | 2012 | | | 2013 vs. 2012 ($) | | | 2013 vs. 2012 (%) | | | | | 2012 | | | 2011 | | | 2012 vs. 2011 ($) | | | 2012 vs. 2011 (%) | | | Compensation and benefits | | $ | 9,600 | | | $ | 8,474 | | | $ | 1,126 | | | | 13.3 | % | | $ | 5,201 | | | $ | 4,768 | | | $ | 433 | | | | 9.1 | % | General and administrative | | | 5,208 | | | | 4,424 | | | | 784 | | | | 17.7 | % | | General, administrative and other | | | | 2,710 | | | | 2,566 | | | | 144 | | | | 5.6 | % | | | | | | | | | | | | | | | | | | | | | | | | Total expenses | | $ | 14,808 | | | $ | 12,898 | | | $ | 1,910 | | | | 14.8 | % | | $ | 7,911 | | | $ | 7,334 | | | $ | 577 | | | | 7.9 | % | | | | | | | | | | | | | | | | | | | | | | | | | | | | For the Year Ended December 31, | | | | | | 2011 | | | 2010 | | | 2011 vs. 2010 ($) | | | 2011 vs. 2010 (%) | | | Compensation and benefits | | $ | 17,492 | | | $ | 16,528 | | | $ | 964 | | | | 5.8 | % | | General and administrative | | | 10,849 | | | | 9,459 | | | | 1,390 | | | | 14.7 | % | | | | | | | | | | | | | | | Total expenses | | $ | 28,341 | | | $ | 25,987 | | | $ | 2,354 | | | | 9.1 | % | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | For the Years Ended December 31, | | (in thousands) | | 2012 | | | 2011 | | | 2012 vs. 2011 ($) | | | 2012 vs. 2011 (%) | | Compensation and benefits | | $ | 19,108 | | | $ | 17,492 | | | $ | 1,616 | | | | 9.2 | % | General, administrative and other | | | 13,680 | | | | 10,849 | | | | 2,831 | | | | 26.1 | % | | | | | | | | | | | | | | | | | | Total expenses | | $ | 32,788 | | | $ | 28,341 | | | $ | 4,447 | | | | 15.7 | % | | | | | | | | | | | | | | | | | |

| | | | For the Year Ended December 31, | | | For the Years Ended December 31, | | | | | 2010 | | | 2009 | | | 2010 vs. 2009 ($) | | 2010 vs. 2009 (%) | | | (in thousands) | | | 2011 | | | 2010 | | | 2011 vs. 2010 ($) | | | 2011 vs. 2010 (%) | | Compensation and benefits | | $ | 16,528 | | | $ | 15,630 | | | $ | 898 | | | | 5.7 | % | | $ | 17,492 | | | $ | 16,528 | | | $ | 964 | | | | 5.8 | % | General and administrative | | | 9,459 | | | | 13,006 | | | | (3,547 | ) | | | -27.3 | % | | | 10,849 | | | | 9,459 | | | | 1,390 | | | | 14.7 | % | Impairment charges | | | — | | | | 1,691 | | | | (1,691 | ) | | | -100 | % | | | | | | | | | | | | | | | | | | | | | | | | | Total expenses | | $ | 25,987 | | | $ | 30,327 | | | $ | (4,340 | ) | | | -14.3 | % | | $ | 28,341 | | | $ | 25,987 | | | $ | 2,354 | | | | 9.1 | % | | | | | | | | | | | | | | | | | | | | | | | |

Our expenses are driven primarily by our compensation costs. The table included in “—Expenses—Compensation and Benefits Expense” describes the components of our compensation expense for the sixthree months ended June 30,March 31, 2013 and 2012 and 2011 andfor the three years ended December 31, 2011.2012. Other expenses, such as rent, professional service fees, data-related costs, and sub-advisory fees incurred are included in our general and administrative expenses. SixThree Months Ended June 30,March 31, 2013 versus Three Months Ended March 31, 2012

Total expenses increased by $0.6 million, or 7.9%, to $7.9 million for the three months ended March 31, 2013 from $7.3 million for the three months ended March 31, 2012. This increase was primarily attributable to increases in compensation and benefits expense and general and administrative expenses of $0.4 million and $0.2 million, respectively. Compensation and benefits expense increased by $0.4 million, or 9.1%, to $5.2 million for the three months ended March 31, 2013 from $4.8 million for the three months ended March 31, 2012. The increase was primarily attributable to an increase in salaries of $0.2 million as a result of both merit increases and increased headcount, and increased equity-based compensation expense of $0.2 million primarily due to an increase in the fair value of the deferred equity units. General and administrative expenses increased by $0.1 million, or 5.6%, to $2.7 million for the three months ended March 31, 2013 from $2.6 million for the three months ended March 31, 2012. This increase was primarily due to an increase in professional fees of $64 thousand for legal fees related to the Ten-Sixty acquisition, higher operating escalation charges of $20 thousand at our corporate headquarters, and increased sub-advisory fees of $34 thousand related to increased services received in addition to increased fund management revenue. Year Ended December 31, 2012 versus Six MonthsYear Ended June 30,December 31, 2011 Total expenses increased by $1.9$4.5 million, or 14.8%15.7%, to $14.8$32.8 million for the six monthsyear ended June 30,December 31, 2012 from $12.9$28.3 million for the six monthsyear ended June 30,December 31, 2011. This increase was primarily attributable to increases in compensation and benefits expense and general and administrative expenses of $1.1$1.6 million and $0.8$2.8 million, respectively. Compensation and benefits expense increased by $1.1$1.6 million, or 13.3%9.2%, to $9.6$19.1 million for the six monthsyear ended June 30,December 31, 2012 from $8.5$17.5 million for the six monthsyear ended June 30,December 31, 2011. The increase was primarily attributable to an increase in salaries of $0.6$0.9 million as a result of both merit increases and increased headcount primarily as a result of the Milbank acquisition, increased incentive compensation expense of $0.1$0.3 million, and increased equity-based compensation expense of $0.3 million due to the grant of additional deferred equity units to employees and an increase in the fair value of the deferred equity units. General and administrative expenses increased by $0.8$2.8 million, or 17.7%26.1%, to $5.2$13.7 million for the six monthsyear ended June 30,December 31, 2012 from $4.4$10.9 million for the six monthsyear ended June 30,December 31, 2011. This increase was primarily due to an increase in professional fees of $2.3 million for services rendered in connection with a planned initial public offering that was withdrawn in November 2012 and acquisition transactions and depreciation and amortization expense of $0.3$0.4 million dueprimarily related to amortization of intangible assets related to Milbank, a $0.2 million increase in costs related to the development of our portfolio management system and investment research and pricing subscriptions, a $0.1 million increase in rent as a resultpart of the Milbank acquisition and the non-renewal of one of our sub-leases, and a $0.6 million increase in professional fees including acquisition transactions. transaction. On May 1, 2012, we reoccupied space at our headquarters that we had previously abandoned in 2009. As a result, we recorded a reversal of a lease abandonmentthis released the remaining abandonment-related liability of $0.7 million. This reversal was partially offset by increased operating cost escalations of $0.2 million which reduced occupancy expense for the six months ended June 30, 2012.and lower sub-tenant rent of $0.2 million. Year Ended December 31, 2011 versus Year Ended December 31, 2010 Total expenses increased by $2.4 million, or 9.1%, to $28.3 million for the year ended December 31, 2011 from $26.0 million for the year ended December 31, 2010. This increase was primarily attributable to increases in compensation and benefits expense and general and administrative expenses of $1.0 million and $1.4 million, respectively. Compensation and benefits expense increased by $1.0 million, or 5.8%, to $17.5 million for the year ended December 31, 2011 from $16.5 million for the year ended December 31, 2010. The increase was primarily attributable to an increase in equity-based compensation expense of $0.5 million due to the grant of deferred equity units to employees, increased salaries of $0.8 million as a result of both merit increases and increased headcount, and increased benefits and payroll taxes expense of $0.1 million, partially offset by lower employee bonus expense of $0.4 million. General and administrative expenses increased by $1.4 million, or 14.7%, to $10.8 million for the year ended December 31, 2011 from $9.4 million for the year ended December 31, 2010. This increase was primarily due to an increase in professional fees of $0.8 million for services rendered in connection with this offering and acquisition transactions, $0.7 million in reimbursements to clients and a $0.2 million increase in costs related to the development of our portfolio management system and investment research and pricing subscriptions, offset by decreased occupancy costs of $0.3 million due to increased sub-tenant rent. Other Income (Expense), Net | | | | | | | | | | | | | | | | | | | | For the Three Months Ended March 31, | | (in thousands) | | 2013 | | | 2012 | | | 2013 vs. 2012 ($) | | | 2013 vs. 2012 (%) | | Other income (expense), net | | $ | 29 | | | $ | 32 | | | $ | (3 | ) | | | -9.4 | % | Interest income | | | 27 | | | | 45 | | | | (18 | ) | | | -40.0 | % | Interest expense | | | (37 | ) | | | (64 | ) | | | 27 | | | | -42.2 | % | | | | | | | | | | | | | | | | | | Total other income (expense), net | | $ | 19 | | | $ | 13 | | | $ | 6 | | | | 46.2 | % | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | For the Years Ended December 31, | | (in thousands) | | 2012 | | | 2011 | | | 2012 vs. 2011 ($) | | | 2012 vs. 2011 (%) | | Loss on forgiveness of notes receivable | | $ | — | | | $ | (34 | ) | | $ | 34 | | | | -100.0 | % | Other | | | 123 | | | | (210 | ) | | | 333 | | | | -41.4 | % | Interest income | | | 145 | | | | 187 | | | | (42 | ) | | | -22.5 | % | Interest expense | | | (304 | ) | | | (164 | ) | | | (140 | ) | | | 85.4 | % | Equity income from investments | | | 1,911 | | | | 950 | | | | 961 | | | | -158.6 | % | | | | | | | | | | | | | | | | | | Total other income (expense), net | | $ | 1,875 | | | $ | 729 | | | $ | 1,146 | | | | 157.2 | % | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | For the Years Ended December 31, | | (in thousands) | | 2011 | | | 2010 | | | 2011 vs. 2010 ($) | | | 2011 vs. 2010 (%) | | Loss on forgiveness of notes receivable | | $ | (34 | ) | | $ | (508 | ) | | $ | 474 | | | | -93.3 | % | Other | | | (210 | ) | | | 32 | | | | (242 | ) | | | -756.3 | % | Interest income | | | 187 | | | | 231 | | | | (44 | ) | | | -19.0 | % | Interest expense | | | (164 | ) | | | (241 | ) | | | 77 | | | | -32.0 | % | Equity income from investments | | | 950 | | | | 1,241 | | | | (291 | ) | | | -23.4 | % | | | | | | | | | | | | | | | | | | Total other income (expense), net | | $ | 729 | | | $ | 755 | | | $ | (26 | ) | | | -3.4 | % | | | | | | | | | | | | | | | | | |

Three Months Ended March 31, 2013 versus Three Months Ended March 31, 2012 Other income (expense), net increased by $6 thousand to $19 thousand of other income for the three months ended March 31, 2013 from $13 thousand of other income for the three months ended March 31, 2012. Year Ended December 31, 20102012 versus Year Ended December 31, 20092011 Total expenses decreasedOther income (expense), net increased by $4.3$1.1 million or 14.3%, to $26.0$1.9 million for the year ended December 31, 20102012 from $30.3$0.7 million for the year ended December 31, 2009. This was primarily2011. The increase in other income (expense), net is attributable to decreasesa $1.0 million increase in general and administrative expenses and impairment charges of $3.5 million and $1.7 million, respectively,equity income from investments resulting from performance fee allocations partially offset by a $0.9 million increase in compensation and benefits expense.

Compensation and benefits expense increased by $0.9 million, or 5.7%, to $16.5 million for the year ended December 31, 2010 from $15.6 million for the year ended December 31, 2009. The increase was primarily attributable to a $0.6 million increase in equity-based compensation expense, increased employee bonusnet interest expense of $0.1$0.2 million a $0.1 million increase in salaries, and $0.1 million of severance charges related to the termination of two employees.

General and administrative expenses decreased by $3.5 million, or 27.3%, to $9.5 million for the year ended December 31, 2010 from $13.0 million for the year ended December 31, 2009. This $3.5 million decrease was primarily attributable to a one-time $1.2 million lease abandonment charge in 2009 for space at our corporate headquarters, and a $2.3 million decrease in LGI operating expenses as a result of the wind-down of our LGI business in 2009.

Impairment charges decreased by $1.7 million from the year ended December 31, 2009 to the year ended December 31, 2010 as a result of a $1.2 million leasehold improvements impairment charge in 2009 related to the abandonment of a portion of the leased space at our corporate headquarters. Also, a $0.5 million charge was taken in 2009 to write-off goodwill and assets related to the LGI business closure.

Other Income (Expense)

| | | | | | | | | | | | | | | | | | (in thousands) | | For the Six Months Ended June 30, | | | | | 2012 | | | 2011 | | | 2012 vs. 2011 ($) | | | 2012 vs. 2011 (%) | | Other income (expense) | | $ | 61 | | | $ | (176 | ) | | $ | 237 | | | | -134.7 | % | Interest income | | | 86 | | | | 92 | | | | (6 | ) | | | -6.5 | % | Interest expense | | | (206 | ) | | | (75 | ) | | | (131 | ) | | | 174.7 | % | | | | | | | | | | | | | | | | | | Total other income (expense) | | $ | (59 | ) | | $ | (159 | ) | | $ | 100 | | | | -62.9 | % | | | | | | | | | | | | | | | | | | | | | | | For the Year Ended December 31, | | | | | 2011 | | | 2010 | | | 2011 vs. 2010 ($) | | | 2011 vs. 2010 (%) | | Loss on forgiveness of notes receivable | | $ | (34 | ) | | $ | (508 | ) | | $ | 474 | | | | -93.3 | % | Interest income | | | 187 | | | | 231 | | | | (44 | ) | | | -19.0 | % | Interest expense | | | (164 | ) | | | (241 | ) | | | 77 | | | | -32.0 | % | Equity income from investments | | | 950 | | | | 1,241 | | | | (291 | ) | | | -23.4 | % | Other | | | (210 | ) | | | 32 | | | | (242 | ) | | | -756.3 | % | | | | | | | | | | | | | | | | | | Total other income (expense) | | $ | 729 | | | $ | 755 | | | $ | (26 | ) | | | -3.4 | % | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | (in thousands) | | For the Year Ended December 31, | | | | | 2010 | | | 2009 | | | 2010 vs. 2009 ($) | | | 2010 vs. 2009 (%) | | Gain on extinguishment of debt | | $ | — | | | $ | 3,934 | | | $ | (3,934 | ) | | | -100.0 | % | Gain on settlement with former LGI shareholders | | | — | | | | 1,470 | | | | (1,470 | ) | | | -100.0 | % | Loss on forgiveness of notes receivable | | | (508 | ) | | | — | | | | (508 | ) | | | — | | Interest income | | | 231 | | | | 213 | | | | 18 | | | | 8.5 | % | Interest expense | | | (241 | ) | | | (467 | ) | | | 226 | | | | -48.4 | % | Equity income from investments | | | 1,241 | | | | 274 | | | | 967 | | | | 352.9 | % | Other | | | 32 | | | | 134 | | | | (102 | ) | | | -76.1 | % | | | | | | | | | | | | | | | | | | Total other income (expense) | | $ | 755 | | | $ | 5,558 | | | $ | (4,803 | ) | | | -86.4 | % | | | | | | | | | | | | | | | | | |

Six Months Ended June 30, 2012 versus Six Months Ended June 30, 2011

Other income (expense) decreased by $100 thousand to ($59) thousand for the six months ended June 30, 2012 from ($159) thousand for the six months ended June 30, 2011. The decrease in other income (expense) is attributable to $0.2 million loss on a sub-lease charge related to a new sub-tenant on our leased space in January 2011. Interest expense increased by $131 thousand to $206 thousand for the six months ended June 30, 2012 from $75 thousand for the six months ended June 30, 2011, primarily due to a write off prepaid interest expense of $86 thousand related to the reversal of thea lease abandonment liability in addition to an increase in notes payable issued in connection with the acquisition of Milbank.

Year Ended December 31, 2011 versus Year Ended December 31, 2010 Other income (expense), net decreased by $26 thousand, or 3.4%, to $0.7 million for the year ended December 31, 2011 from $0.8 million for the year ended December 31, 2010. In 2011 and 2010, we recorded losses on the forgiveness of notes receivable of $34 thousand and $508 thousand, respectively, in connection with the termination of principalsemployee-partners and the related termination of existing notes in exchange for the repurchase of units of Silvercrest L.P. and Silvercrest GP LLC. Interest income decreased by $44 thousand or 19.0% to $187 thousand for the year ended December 31, 2011 from $231 thousand for the year ended December 31, 2010. Interest expense decreased by $77 thousand or 32.0% to $164 thousand for the year ended December 31, 2011 from $241 thousand for the year ended December 31, 2010. Equity income from investments decreased by $0.3 million primarily as a result of decreased performance fee allocations from some of our funds. Other income (expense) decreased by $0.2 million as a result of a $0.1 million loss on sub-lease charge related to a new sub-tenant on our leased space in January 2011 and $0.1 million of unrealized and realized losses related to an investment in marketable securities. Provision for Income Taxes Three Months Ended March 31, 2013 versus Three Months Ended March 31, 2012 The provision for income taxes was $0.3 million for the three months ended March 31, 2013 and 2012. Our provision for income taxes as a percentage of income before provision for income taxes for the three months ended March 31, 2013 and 2012 was 5.7% and 5.9%, respectively. Year Ended December 31, 20102012 versus Year Ended December 31, 2009 Other income (expense) decreased by $4.8 million, or 86.4%, to $0.8 million for the year ended December 31, 2010 from $5.6 million for the year ended December 31, 2009. This decrease was primarily attributable to a $3.9 million gain on extinguishment of debt related to the closing of the LGI business and a $1.5 million gain on settlement with the former owners of the LGI business in 2009. In 2010, we forgave $0.5 million of notes receivable in connection with the termination of a partner. This note was originally issued for the purchase of units in Silvercrest L.P. and Silvercrest GP LLC by a terminated partner at the time he joined our company. Upon termination of the partner, the note was cancelled and we redeemed and cancelled the underlying equity. Interest income increased by $18 thousand or 8.5% to $231 thousand for the year ended December 31, 2010 from $213 thousand for the year ended December 31, 2009. Interest expense decreased by $0.3 million, or 48.4%, to $0.2 million for the year ended December 31, 2010 from $0.5 million for the year ended December 31, 2009 due to a decrease in interest expense from notes issued to principals and as consideration in connection with prior acquisitions. Interest expense decreased as a result of the repayment and scheduled principal payments on notes issued to partners, scheduled principal payments on a note, and the forgiveness of a note in conjunction with the closing of the LGI business. Equity income from investments increased by $1.0 million primarily as a result of increased performance fee allocations from some of our funds.

Provision for Income Taxes

Six Months Ended June 30, 2012 versus Six Months Ended June 30, 2011