As filed with the Securities and Exchange Commission on July 11, 2016.May 8, 2017.

Registration No. 333-212093333-217415

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 12

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

TPI Composites, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 3511 | 20-1590775 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

TPI Composites, Inc.

8501 N. Scottsdale Rd.

Gainey Center II, Suite 100

Scottsdale, AZ 85253

(480) 305-8910

(Address, including zip code, and telephone number,

including area code, of registrant’s principal executive offices)

Steven C. Lockard

Chief Executive Officer

TPI Composites, Inc.

8501 N. Scottsdale Rd.

Gainey Center II, Suite 100

Scottsdale, AZ 85253

(480) 305-8910

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

H. David Henken, Esq. Bradley C. Weber, Esq.

Goodwin Procter LLP

Boston, MA (617) 570-1000 | William E. Siwek Chief Financial Officer Steven Fishbach, Esq. General Counsel TPI Composites, Inc. 8501 N. Scottsdale Rd. Gainey Center II, Suite 100 Scottsdale, AZ 85253 (480) 305-8910 | Sandra L. Flow, Esq. Cleary Gottlieb Steen & Hamilton LLP One Liberty Plaza New York, NY 10006 (212) 225-2000 |

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier registration statement for the same offering. ¨☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier registration statement for the same offering. ¨☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”filer,” “smaller reporting company” and “smaller reporting“emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | Accelerated filer | Non-accelerated filer | Smaller reporting company | |||

| Emerging growth company ☒ | ||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☒

CALCULATION OF REGISTRATION FEE

| ||||||||

Title of Each Class of Securities to be Registered | Amount to be Registered(1) | Proposed Maximum | Proposed Maximum Aggregate Offering Price(2) | Amount of Registration Fee(3) | ||||

Common Stock, par value $0.01 | 8,337,500 | $17.00 | $141,737,500 | $14,272.97 | ||||

| ||||||||

| ||||||||

| ||||||||

Title of Each Class of Securities To Be Registered | Amount to be Registered(1) | Proposed Maximum Price Per Share(2) | Proposed Maximum Offering Price(2) | Amount of Registration Fee(3) | ||||

Common Stock, $0.01 par value per share | 5,175,000 | $19.46 | $100,705,500 | $11,671.77 | ||||

| ||||||||

| ||||||||

| (1) | Includes |

| (2) | Estimated solely for the purpose of |

| (3) | The |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securitiesThe selling stockholders may not be soldsell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seekthese securities and the selling stockholders are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated July 11, 2016May 8, 2017

PRELIMINARY PROSPECTUS

7,250,0004,500,000 Shares

Common Stock

This is the initial public offeringThe selling stockholders identified in this prospectus, which include certain of TPI Composites, Inc. Weour executive officers, are selling 7,250,000 shares of our common stock.

stock in this offering. We expectwill not receive any proceeds from the public offering pricesale of shares to be between $15.00 and $17.00 per share. Currently, no public market exists foroffered by the shares. After pricing of the offering, we expect that the shares will tradeselling stockholders.

Our common stock is listed on The NASDAQ Global Market under the symbol “TPIC”.“TPIC.” On May 5, 2017, the last reported sale price of our common stock on The NASDAQ Global Market was $17.97 per share.

We are an “emerging growth company” under federal securities laws and, as such, will beare subject to reduced public company disclosure standards. See “Prospectus Summary—Implications of Being an Emerging Growth Company.”

Investing in our common stock involves risks that are described in the “Risk Factors” section beginning on page 2118 of this prospectus.

Per Share | Total | |||||||

Public offering price | ||||||||

Underwriting discount(1) | ||||||||

Proceeds, before expenses, to | ||||||||

| (1) | See “Underwriting” beginning on page |

The underwriters may also exercise their option to purchase up to an additional 1,087,500675,000 shares from usthe selling stockholders at the public offering price, less the underwriting discount, for 30 days after the date of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares will be ready for delivery on or about , 2016.2017.

| J.P. Morgan | Morgan Stanley |

Cowen and Company | Raymond James | Canaccord Genuity | ||||

The date of this prospectus is , 2016.2017.

Page | ||||

| 1 | ||||

| 50 | ||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||||

| 91 | ||||

Certain Material U.S. Federal Income and Estate Tax Considerations to Non-U.S. Holders | ||||

| F-1 | ||||

We, the selling stockholders and the underwriters have not authorized anyone to provide any information other than that contained in this prospectus or any free writing prospectus prepared by us or on our behalf. We, the selling stockholders and the underwriters are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. The information contained in this prospectus is accurate only as of the date on the front cover of this prospectus regardless of the time of delivery of this prospectus or of any sale of our common stock.

INDUSTRY AND MARKET DATA

This prospectus contains statistical data, estimates and forecasts that are based on independent industry publications, such as those published by the American Wind Energy Association or AWEA,(AWEA), Bloomberg New Energy Finance or BNEF,(BNEF), International Energy Agency or IEA,(IEA), MAKE Consulting or MAKE,(MAKE), Energy Information Administration or EIA,(EIA), Lazard Ltd or Lazard,(Lazard), the International Renewable Energy Agency (IRENA), Wind Energy Foundation (WEF), Global Wind Energy Council (GWEC), or other publicly available information, as well as other information based on our internal sources. Although we believe that the third-party sources referred to in this prospectus are reliable, neither we nor the underwriters have independently verified the information provided by these third parties. While we are not aware of any misstatements regarding any third-party information presented in this prospectus, their estimates, in particular as they relate to projections, involve numerous assumptions, are subject to risks and uncertainties, and are subject to change based on various factors, including those discussed under the section titled “Risk Factors” and elsewhere in this prospectus.

i

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our common stock, you should carefully read this entire prospectus, including our consolidated financial statements and the related notes included elsewhere in this prospectus. You should consider, among other things, the matters described in “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in each case included elsewhere in this prospectus. Unless the context otherwise requires, we use the terms “TPI Composites,” “TPI,” “we,” “us” and “our” in this prospectus to refer to TPI Composites, Inc. and its consolidated subsidiaries.

TPI Composites, Inc.

Company Overview

We are the largest U.S.-based independent manufacturer of composite wind blades. We enable many of the industry’s leading wind turbine original equipment manufacturers or OEMs,(OEMs), who have historically relied on in-house production, to outsource the manufacturing of some of their wind blades through our global footprint of advanced manufacturing facilities strategically located to serve large and growing wind markets in a cost-effective manner. Given the importance of wind energy capture, turbine reliability and cost to power producers, the size, quality and performance of wind blades have become highly strategic to our OEM customers. As a result, we have become a key supplier to our OEM customers in the manufacture of wind blades and related precision molding and assembly systems. We have entered into long-term supply agreements pursuant to which we dedicate capacity at our facilities to our customers in exchange for their commitment to purchase minimum annual volumes of wind blade sets, which consist of three wind blades. As of March 31, 2016,April 28, 2017, our long-term supply agreements provide for estimated minimum aggregate volume commitments from our customers of $1.5approximately $2.7 billion and encourage our customers to purchase additional volume up to, in the aggregate, an estimated total contract value of over $3.0approximately $4.2 billion through the end of 2021.2023. This collaborative dedicated supplier model provides us with contracted volumes that generate significant revenue visibility, drive capital efficiency and allow us to produce wind blades at a lower total delivered cost, while ensuring critical dedicated capacity for our customers.

Our OEM customers include General Electric International, Inc. and its affiliates (GE Wind), Vestas Wind Systems A/S (Vestas), Gamesa Wind US LLC (Gamesa)(or Gamesa, which, on April 3, 2017, was merged along with its parent company, Gamesa Corporatión Tecnológica, with Siemens Wind Power) and Nordex SE (or Nordex, which, in April 2016, acquired Acciona Windpower, S.A., or Acciona, (Acciona) for whom we also manufacture wind blades). Prior to 2013, we had one OEM customer that, according to data from MAKE, represented approximately 10% of the global wind energy market based on megawatts or MWs,(MWs) of energy capacity installed. Although we do not supply all of their wind blade volume, according to data from MAKE our OEM customers collectively accounted for approximately 32%42% of the global onshore wind energy market and approximately 56%63% of that market excluding China over the three years ended December 31, 2015,2016, based on MWs of energy capacity installed. The wind power generation industry is experiencing significant growth in countries belonging to the Organization for Economic Cooperation and Development or OECD,(OECD) as well as in emerging growth markets. To meet this growth in demand reliably in a capital-efficient and cost-effective manner, many OEMs are shifting from manufacturing wind blades themselves to the outsourced manufacture of their wind blades. Our collaborative approach, advanced composite technology and global manufacturing footprint have allowed us to capitalize on this trend by replacing or augmenting the in-house capabilities of our customers and efficiently delivering wind blades when and where required. Our facilities in the United States, China, Mexico and Turkey create a geographically-diverse, global production platform to meet our customers’ needs in key large and growing wind markets. We intend to continue expanding in certain existing markets and in new locations that

represent growth opportunities for the wind energy market and our customers. We believe our geographic and customer diversification, together with our long-term

agreements, allow us to take advantage of growth trends and help to insulate us from potential short-term fluctuations or legislative changes in any one market.

Our wind blade and precision molding and assembly systems manufacturing businesses accounted for over 99%, over 99%, 99%, and 97% of our total net sales in the three months ended March 31, 2016 and in the years ended December 31, 2015, 2014 and 2013, respectively. We also leverage our advanced composite technology and the expertise gained from our history of innovation to supply high strength, lightweight and durable composite solutions for the transportation market.

Global Wind Energy Market

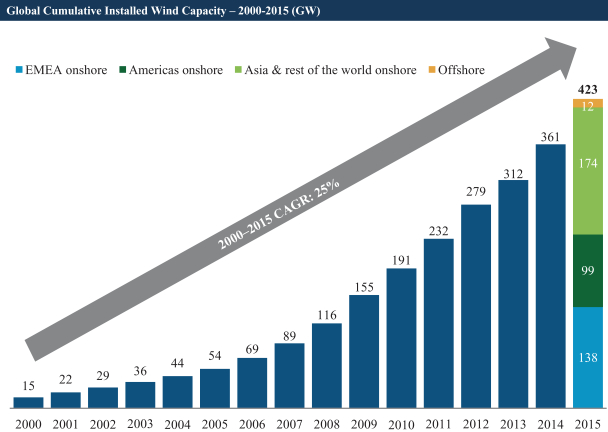

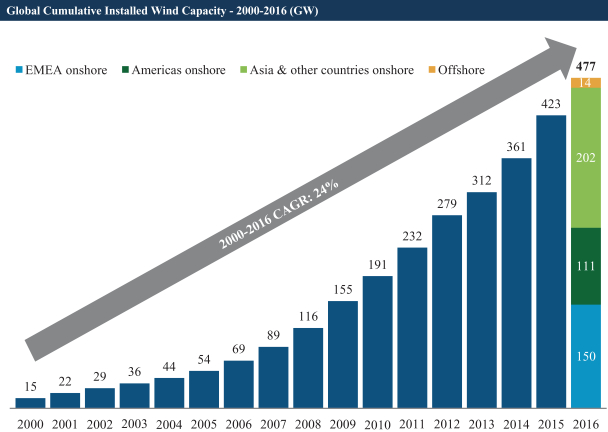

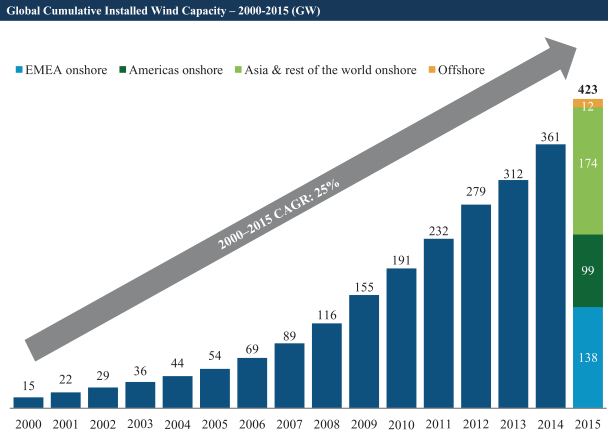

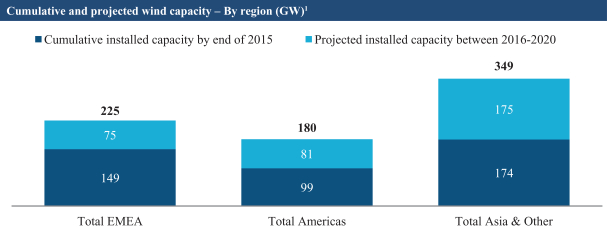

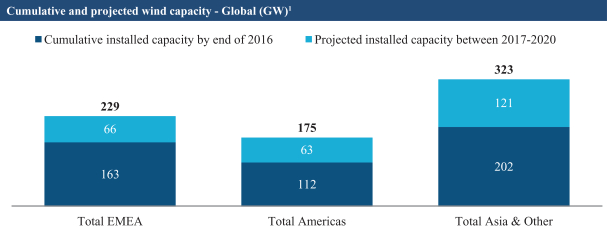

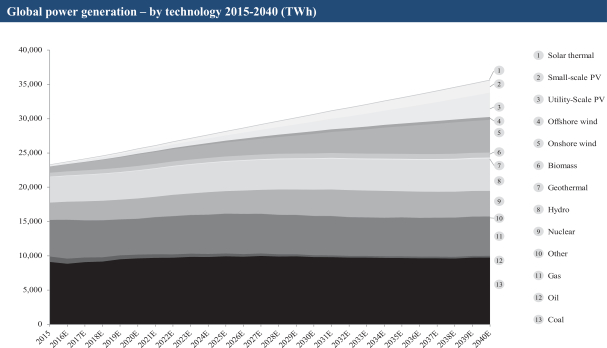

The wind power generation industry has grown rapidly and expanded worldwide in recent years to meet high global demand for clean electricity. According to BNEF, from 2000 to 2015,2016, the cumulative global power generating capacity in gigawatts or GWs,(GWs) grew at an average annual rate of 25%24%. Cumulative installed capacity is led by China (approximately 139162 GWs), the United States (approximately 7482 GWs) and Germany (approximately 4550 GWs). In addition, from 2008 to 2015,2016, the cumulative global power generating capacity of wind turbine installations in GWs increased by more than three and a halffour times. WindAccording to GWEC, wind energy is now used in over 8090 countries, 2429 of which have more than 1 GW installed. The rapid growth in the wind power generation industry has been driven by population growth and the associated increase in electricity demand, widespread emphasis on expanded use of renewable energy, the increasing effectiveness and cost-competitiveness of wind energy and accelerated urbanization in developing countries, among other factors. We believe that recent U.S. and global policy initiatives aimed at reducing fossil fuel consumption through the expansion of renewable energy, coupled with corporate commitments to cost-effective environmentally and socially responsible electricity consumption, will drive additional growth. In 2015,2016, U.S. corporate, non-profit and government entities procured an aggregate of 2.41.6 GWs of wind capacity via power purchase agreements, which represents an increaserepresented 39% of 12 times since 2008,the total capacity contracted in 2016 according to BNEF.AWEA. The Paris Agreement achieved at the 21st Conference of Parties or COP21,(COP21) of the United Nations Framework Convention on Climate Change the U.S. Environmental Protection Agency’s, or EPA’s, Clean Power Plan and the long-term extension of the Production Tax Credit for Renewable Energy or PTC,(PTC) are all recent examples of policies that promote the growth of renewable energy. Overall, renewable technologies, including hydroelectric, are projected to increase their share of global electricity generation from 24% in 2015 to 45% by 2040 according to BNEF. Additionally, according to BNEF, onshore wind is expected to experience the largest increase in global market share over the same period, growing from 4% to 13% of the market.

Source: Bloomberg New Energy Finance. Regional onshore and worldwide offshore figures presented for 20152016 only.

In 2015,2016, the wind industry added approximately 6254 GWs of generation capacity. According to BNEF, market diversification increased as a result of demand from newer markets in Asia, Latin America and non-EU Europe, which collectively represented 45.2%approximately 47% of capacity in 2015,2016, as compared to 42.7%approximately 45% in 2014.2015. Although Europe and the United States led early wind development, since 2010, the majority of wind turbines have been installed in non-OECD countries, particularly in Asia and Latin America, where wind generation capacity is growing. For example, cumulative wind generation capacity from 2013 to 20152016 grew by 75.0%approximately 105% to 2.83.3 GWs in Mexico and by 64.1%approximately 115% to 4.55.9 GWs in Turkey, underpinned by strong wind resources, high electricity prices, robust energy demand and key regulatory policies tailored to incentivize usage, among other factors.

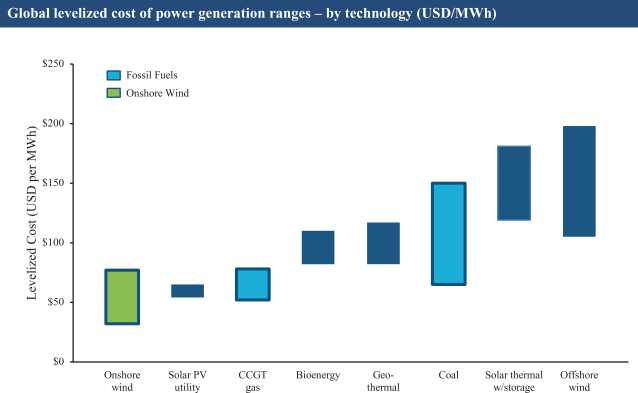

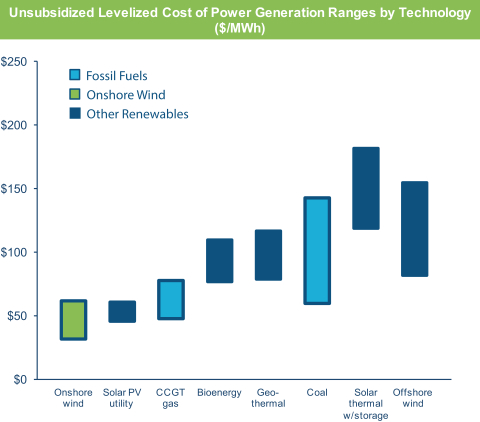

Onshore wind LCOE—which reflects the levelized cost of energy per megawatt hour of a generation project over its lifetime—is already on par with new combined cycle gas turbines and substantially below solar photovoltaic, according to Lazard. The advancement of wind turbine technology, including larger rotor diameters and higher hub heights, has increased energy capture, thus reducing LCOE for onshore wind. For a further discussion of LCOE, see “Our Industry—Global Wind Energy Market.” The proliferation of cost-effective wind generation enhances energy resource diversity and mitigates the price volatility associated with fossil fuels, thereby helping to stabilize overall electricity costs in the long term. Wind energy projects do not require any fuel, such as natural gas or coal, during operation, and we believe that they are generally constructed within a substantially shorter period of time relative to conventional generation resources. According to Lazard, the cost of onshore wind has declined by over 61%66% in the last sixseven years. Costs are expected to continue to decline an

additional 15%26% by 20212025 according to MAKEIRENA1, due to progress in reducing the costs of wind turbines, improving capacity factors and lower operating and maintenance costs.

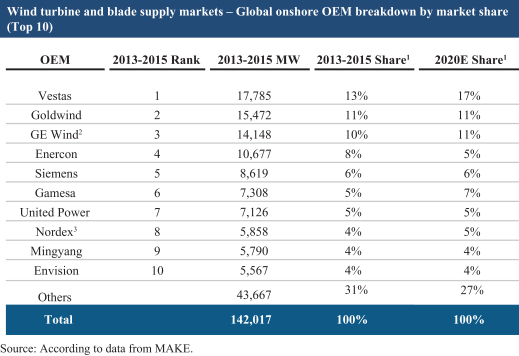

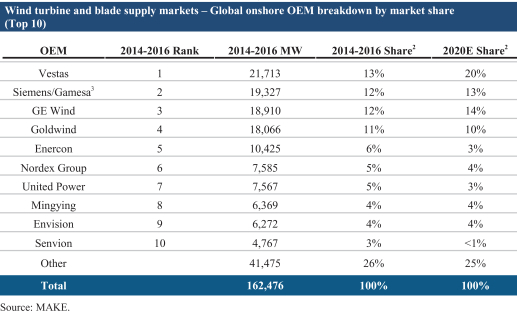

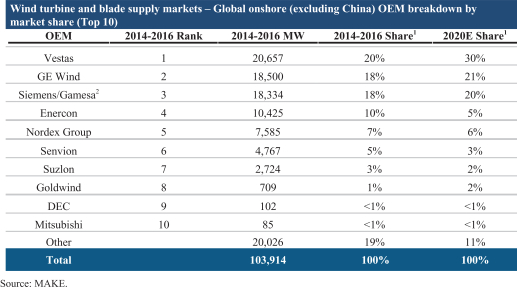

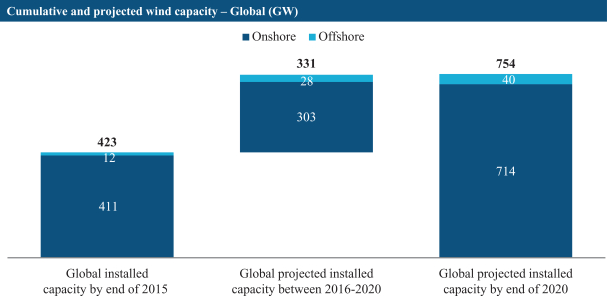

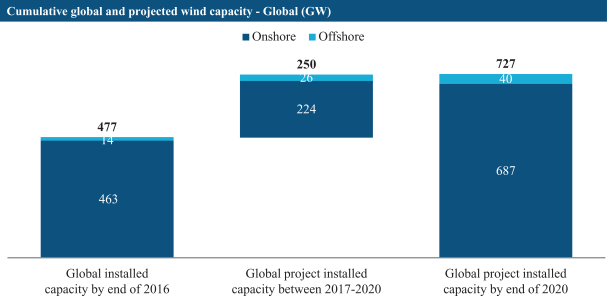

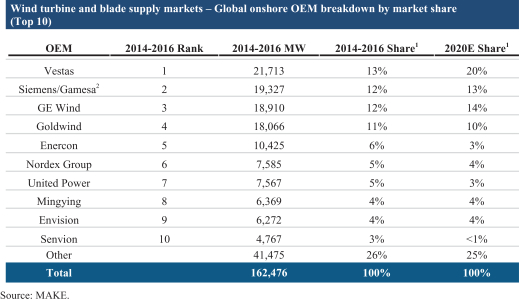

The wind turbine industry, which constitutes our direct customer base, is concentrated among a fewlimited number of established players, with the top ten OEMs accounting for approximately 69%74% of the total global onshore market for the three years ended December 31, 20152016 based on MWs installed, according to data from MAKE. We believe MWs installed is the most widely followed measure of market share in the wind turbine industry and also reflects the OEMs’ demand for wind blades. We currently have long-term supply agreements with four of these top ten OEMs and are developing new relationships with additional OEMs to grow our business. In addition, we expect growth in the industry itself – by the end of 2020, cumulative global installed wind capacity is projected to be over 750727 GWs, with China accounting for approximately 35% of this capacity, according to BNEF. This represents a five-year compounded annual growth rate of approximately 12% for the global wind market including China, and a similar growth rate of approximately 11% for the global wind market excluding China.

1

| 1 | © 2016 IRENA,The Power to Change: Solar and Wind Cost Potential to 2025. |

| 2 | Figures are rounded to nearest whole percent. |

| Figures for |

Historically, many wind turbine OEMs manufactured their own wind blades in-house to ensure a high level of quality and dedicated capacity, reflecting the importance of the wind blade supply to turbine production, concerns over protecting their proprietary wind blade designs and the scarcity of independent wind blade suppliers with sufficient manufacturing expertise and capacity. During 2007 and 2008, the U.S. and China markets grew at a rapid pace, which created additional demand in the wind turbine manufacturing supply chain. To balance supply and demand, many leading wind turbine OEMs established a production footprint inhigh-growth regions.

The current globalization of the wind industry presents a new set of challenges and opportunities for wind turbine OEMs. As opposed to establishing a manufacturing presence in each new core growth market, wind turbine OEMs are now focusing on supply chain efficiencies and their core competencies in the design, marketing and sale of wind turbines. In doing so, many wind turbine OEMs are increasingly outsourcing the production of key components, such as wind blades, to select manufacturers to remain competitive, address growth markets and manage global talent constraints. Despite this ongoing trend of outsourcing of wind blade production by wind turbine OEMs, General Electric Company (GE), the parent company of GE Wind, completed its acquisition of LM Wind Power (LM), our largest competitor. We expect that GE Wind will utilize LM for a substantial percentage of its wind blade production in the future.

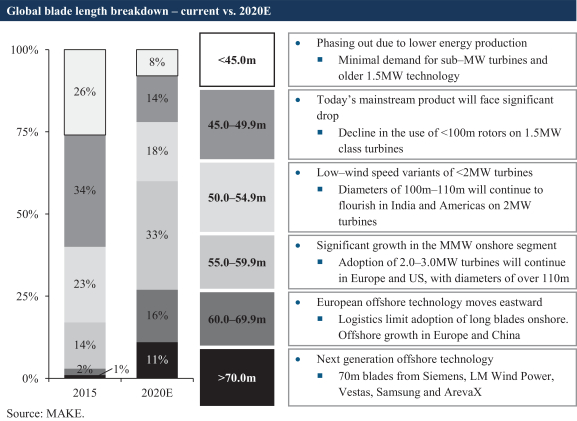

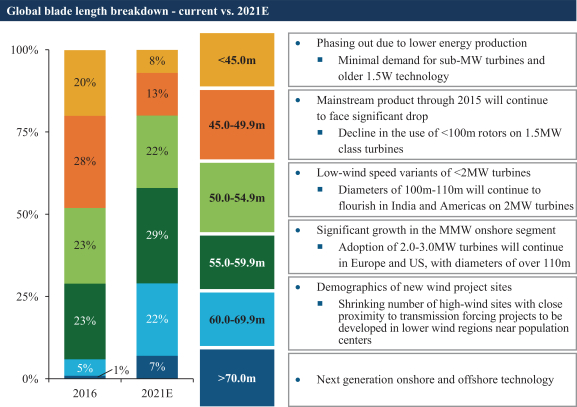

This outsourcing approach enables wind turbine OEMs to lower their capital costs and shift the production components to manufacturers that possess highly specialized expertise in advanced composite, production and process technology. From a product perspective, wind turbine OEMs have adopted a variety of strategies, including the introduction of new turbine models with improved technology, warranty terms, more stringent performance guarantees, and tailor-made turbines for specific countries or regions. During the past three years, all of the top ten wind turbine suppliers in the world have introduced wind turbines with longer wind blade lengths and taller towers designed to capture more energy at the lower end of the wind speed scale. We believe that installation of wind turbines in regions with lower wind speeds is encouraged due to proximity to energy

| 1 | Figures are rounded to nearest whole percent. |

| 2 | Figures for |

proximity to energy demand centers, thereby reducing the amount of transmission infrastructure required. We expect this trend of expansion to regions not traditionally classified as high wind resource regions to continue, which we believe will help us continue to expand our global footprint.

According to BNEF, the total wind blade industry generated $11.9 billion in revenues in 2014 and is projected to grow to $19.7 billion by 2040. We believe our addressable market will continue to expand, as outsourced wind blade manufacturing is expected to rise from 52% in 2013 to 59% in 2017, according to data from MAKE. As the wind energy market continues to expand globally and wind turbine OEMs continue to shift towards increased outsourcing of wind blade manufacturing, we believe we are well-positioned to continue the expansion of our global footprint.

Competitive Strengths

Our long-term success will be driven by our competitive strengths. The key elements of our competitive strengths are as follows:

| • | Wind industry leader with cost-effective, global footprint. We are the largest U.S.-based independent manufacturer of composite wind blades and have developed a global footprint to serve the growing wind energy market worldwide. We currently have |

| • | Positioned to capitalize on significant growth trends in the wind energy market. We believe that our reputation as a reliable, global wind blade manufacturer and our focus on developing replicable and scalable manufacturing facilities and processes positions us to continue to capture opportunities in large and growing wind energy markets. Our ability to capitalize on recent growth trends in the wind energy market and OEM outsourcing has allowed us to grow our revenue |

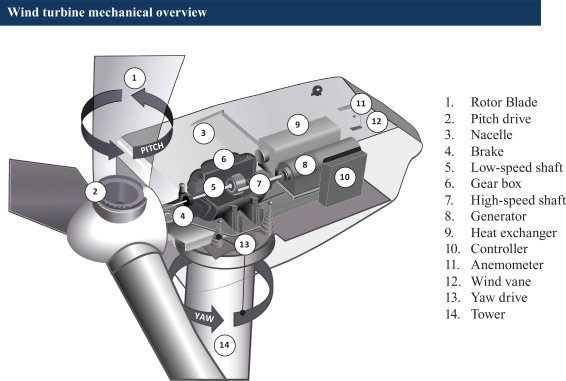

| • | Advanced composite technology and production expertise.Our significant expertise in advanced composite technology and production enables us to manufacture lightweight and durable wind blades with near-aerospace grade precision at an industrial cost. We have developed and usehigh-performance composite materials, precision molding and assembly systems, including modular tooling techniques, and advanced process technology, as well as sophisticated measurement, inspection, testing and quality assurance tools, which, as of March 31, 2017, have allowed us to produce |

innovation and a collaborative “design for manufacturability” approach, we continue to address increasing physical |

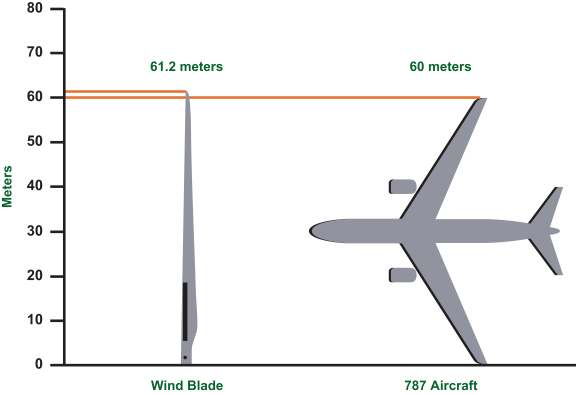

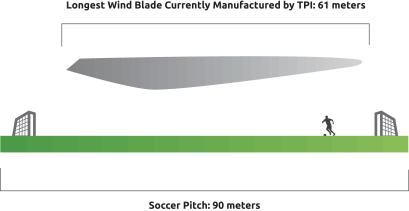

dimensions and the need for rapid model changes, demanding technical specifications and strict quality control requirements for wind blades, which today are generally 50 to 60 meters or more in length. We also invest in ongoing simplification and selective automation of production processes for increased efficiency and precision. We have partnered with the U.S. Department of Energy, government laboratories, universities and our customers to innovate through cost sharing Advanced Manufacturing Innovation |

| • | Collaborative dedicated supplier model. Our deeply collaborative dedicated supplier model engenders stable, long-term relationships with customers, driving capital efficiency and helping to insulate us from potential short-term fluctuations or legislative changes in any one market. Our collaborative approach to manufacturing wind blades to meet our customers’ unique specifications, coupled with their investment in model-specific tooling in our facilities, promotes significant customer loyalty and creates higher switching costs. Our focused factory model, in which we contractually dedicate production lines to a specific customer in exchange for their commitment to purchase minimum annual volumes, also serves to protect the confidentiality of our customers’ proprietary wind blade and turbine designs. Our ability to manufacture the model-specific tooling for our customers further strengthens our role as a “one stop shop” for our customers, provides an efficient solution to their wind blade supply needs and allows us to produce high-quality wind blades at a lower total delivered cost. We work to continue to drive down the cost of materials and production through innovation and global sourcing, the benefit of which we share with our customers contractually in a manner that reduces LCOE for the customer and improves our margins, further strengthening our deep customer relationships. We manufacture wind blades for four of the largest global wind turbine suppliers: GE Wind, Vestas, Gamesa and |

| • | Long-term supply agreements provide significant revenue visibility.In our collaborative dedicated supplier model, we enter into long-term supply agreements that provide significant incentives for our customers to maximize the volume of wind blades purchased, through increased pricing at lower volumes that contribute to profitability at minimum volume levels. As of |

short-term fluctuations or legislative changes in any one market due in part to the annual minimum purchase commitments of our customers contained in those agreements. These annual minimum purchase commitments generally require our customers to |

purchase a negotiated percentage of the manufacturing capacity that we have agreed to dedicate to them. Generally, this percentage begins at 100% and declines after the first few years pursuant to the terms of the supply agreement, but generally remains above 50%. It is our experience that our customers will generally order wind blades from us in a volume that exceeds |

| • | Compelling |

| • | Experienced management team with a strong track record of delivering growth. Our senior management team has significant experience managing high growth, international operations. Over the course of the past decade, the team has successfully positioned us as the largest independent U.S.-based manufacturer of wind blades and has developed and deepened customer relationships with leading OEMs in the global wind energy market. At the same time, our team has built a global manufacturing network with |

Business Strategy

Our long-term success will also be driven by our competitive strengths and business strategy. The key elements of our business strategy are as follows:

| • | Grow our existing relationships and develop new relationships with leading industry OEMs.We plan to continue growing and expanding our relationships with existing customers who, according to data from MAKE, represented approximately |

Wind and entered into a new supply agreement with |

existing Turkey supply agreement with Nordex and |

| • | Expand our footprint in large and growing wind markets, capitalize on the continuing outsourcing trend and evaluate strategic acquisitions.As the wind energy market continues to expand globally and many wind turbine OEMs continue to shift towards increased outsourcing of wind blade manufacturing, we believe we are well-positioned to continue the expansion of our global footprint. We utilize our strengths in composites technology and manufacturing, combined with our collaborative dedicated supplier model to provide our customers with an efficient solution for their expansion in large and growing wind markets. Our quality, reliability and total delivered cost reduce sourcing risk for our customers. In addition, our demonstrated ability to expand into new markets and the strength of our manufacturing capabilities afford us the optionality either to build new factories or grow through strategic acquisitions. |

| • | Focus on continuing innovation.We have a history of innovation in advanced composite technologies and production techniques and use several proprietary technologies related to wind blade manufacturing. With this culture of innovation and a collaborative “design for manufacturability” approach, we continue to address increasing physical dimensions, demanding technical specifications and strict quality control requirements for our customers’ most advanced wind blades. We also invest in ongoing simplification and selective automation of production processes for increased efficiency and precision. In addition, we plan to leverage our history of composite industry-first innovations to grow our business in the transportation market, in which we believe there is a demand for high precision, structural composites manufacturing. |

| • | Continue to drive down costs of wind |

Recent Developments

Set forth below are selected preliminary estimated unaudited financial results as of and for the three months ended June 30, 2016. These financial results are unaudited and shouldIn April 2017, we entered into a multiyear supply agreement with Vestas to supply wind blades from two manufacturing lines at a new manufacturing facility that will be considered preliminary and subjectconstructed in Matamoros, Mexico. We also granted Vestas an option to change. We have provided ranges, rather than specific amounts, for the preliminary results described below as our final results remain subjectadd additional manufacturing lines to the completionscope of our closing procedures, final adjustments, developmentsthe supply agreement. We expect that may arise between nowthe manufacturing facility will open for production in the first half of 2018 and that the time the financial results are finalized,wind blades produced at this manufacturing facility will primarily serve wind markets in Mexico, Central America and management’s andSouth America.

the audit committee’s final reviews. Accordingly, you should not place undue reliance on this preliminary data, which may differ materially from our final results. Please see “Risk Factors,” “Special Note Regarding Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for a discussion of certain factors that could result in differences between the preliminary financial data reported below and the final results. These preliminary estimates should not be viewed as a substitute for our full unaudited condensed consolidated financial statements prepared in accordance with accounting principles generally accepted in the United States. In addition, they are not necessarily indicative of the results to be achieved in any future period.

These estimates have been prepared by and are the responsibility of management. Our independent registered public accounting firm has not audited, compiled, performed any procedures on or reviewed the preliminary financial data, and accordingly does not express an opinion or any other form of assurance with respect to the preliminary financial data.

The following are the selected preliminary estimated unaudited financial results as of and for the three months ended June 30, 2016, as well as a comparison to our unaudited financial results as of and for the three months ended June 30, 2015:

| Three months ended June 30, 2015 | Three months ended June 30, 2016 | |||||||||||||

| Actual | Low End of Range | High End of Range | ||||||||||||

| (in thousands) | ||||||||||||||

Other Financial Information: | ||||||||||||||

Net sales | $ | 149,739 | $ | 193,500 | to | $ | 194,500 | |||||||

Total billings(1) | $ | 139,601 | $ | 195,000 | to | $ | 196,600 | |||||||

Gross profit | $ | 12,150 | $ | 22,000 | to | $ | 23,000 | |||||||

Net income | $ | 4,090 | $ | 11,000 | to | $ | 12,000 | |||||||

EBITDA(1) | $ | 11,868 | $ | 19,900 | to | $ | 21,250 | |||||||

Adjusted EBITDA(1) | $ | 12,301 | $ | 19,900 | to | $ | 21,350 | |||||||

| Three months ended June 30, | ||||||||||||||

| 2015 | 2016 | |||||||||||||

Other Operating Information: | ||||||||||||||

Sets(2) | 346 | 551 | ||||||||||||

Estimated megawatts(3) | 772 | 1,252 | ||||||||||||

Total manufacturing line capacity(4) | 30 | 32 | ||||||||||||

Dedicated manufacturing lines(5) | 29 | 38 | ||||||||||||

Manufacturing lines in startup(6) | 7 | 0 | ||||||||||||

Manufacturing lines in transition(7) | 10 | 3 | ||||||||||||

For the three months ended June 30, 2016, we expect to report net sales of between $193.5 million and $194.5 million and total billings of between $195.0 million and $196.6 million. This compares to net sales and total billings of $149.7 million and $139.6 million, respectively, for the three months ended June 30, 2015. The increase is primarily due to an increase in wind blade sets produced across all of our plants.

We expect to report net income of between $11.0 million and $12.0 million for the three months ended June 30, 2016, as compared to net income of $4.1 million for the three months ended June 30, 2015. The increase is due to the increased net sales above as well as improved operating efficiency.

For the three months ended June 30, 2016, we expect to report EBITDA of between $19.9 million and $21.3 million and adjusted EBITDA of between $19.9 million and $21.4 million. This compares to EBITDA of $11.9 million and adjusted EBITDA of $12.3 million for the three months ended June 30, 2015. The increase is due to the factors described above.

We expect to report cash and cash equivalents as of June 30, 2016 of approximately $31.3 million and an aggregate principal amount of total indebtedness as of June 30, 2016 of approximately $124.0 million. During the three months ended June 30, 2016, we repaid approximately $7.2 million of outstanding long-term indebtedness.

The following table presents reconciliations of estimated total billings to our preliminary estimated low end and high end ranges for our estimated net sales as well as estimated EBITDA and adjusted EBITDA to our preliminary estimated low end and high end ranges for our estimated net income, each for the three months ended June 30, 2016. See Management’s Discussion and Analysis of Financial Condition and Results of Operations” for a reconciliation of total billings to net sales and EBITDA and adjusted EBITDA to net income for the prior periods.

| Three months ended June 30, 2015 | Three months ended June 30, 2016 | |||||||||||||||

| Actual | Low End of Range | High End of Range | ||||||||||||||

(in thousands) | ||||||||||||||||

Net sales | $ | 149,739 | $ | 193,500 | to | $ | 194,500 | |||||||||

|

|

|

|

|

| |||||||||||

Change in deferred revenue: | ||||||||||||||||

Blade-related deferred revenue at beginning of period | (76,534 | ) | (65,000 | ) | to | (65,000 | ) | |||||||||

Blade-related deferred revenue at end of period | 68,226 | 66,000 | to | 66,100 | ||||||||||||

Foreign exchange impact(1) | (1,830 | ) | 500 | to | 1,000 | |||||||||||

|

|

|

|

|

| |||||||||||

Change in deferred revenue | (10,138 | ) | 1,500 | to | 2,100 | |||||||||||

|

|

|

|

|

| |||||||||||

Total billings | $ | 139,601 | $ | 195,000 | to | $ | 196,600 | |||||||||

|

|

|

|

|

| |||||||||||

Net income | $ | 4,090 | $ | 11,000 | to | $ | 12,000 | |||||||||

Adjustments: | ||||||||||||||||

Depreciation and amortization | 2,910 | 3,100 | to | 3,200 | ||||||||||||

Interest expense (net of interest income) | 3,644 | 4,100 | to | 4,150 | ||||||||||||

Income tax provision | 1,224 | 1,700 | to | 1,900 | ||||||||||||

|

|

|

|

|

| |||||||||||

EBITDA | 11,868 | 19,900 | to | 21,250 | ||||||||||||

Realized loss on foreign currency remeasurement | 433 | — | to | 100 | ||||||||||||

|

|

|

|

|

| |||||||||||

Adjusted EBITDA | $ | 12,301 | $ | 19,900 | to | $ | 21,350 | |||||||||

|

|

|

|

|

| |||||||||||

Risks Related to Our Business

Our business is subject to many risks and uncertainties of which you should be aware before you decide to invest in our common stock. These risks are discussed more fully under “Risk Factors” in this prospectus. Some of these risks include, but are not limited to, the following:

We have experienced and could in the future experience quality or operational issues in connection with plant construction or expansion, wind blade model transition and wind blade manufacturing,

which could result in losses and cause delays in our ability to complete our projects and may therefore materially harm our business, financial condition and results of operations.

|

Implications of Being an Emerging Growth Company

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 or the(the JOBS Act.Act). As an emerging growth company, we may take advantage of specified reduced disclosure and other requirements that are otherwise applicable generally to public companies. These provisions include:

We may take advantage of these exemptions for up to five years or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company on the date that is the earliest of (i) the last day of the fiscal year in which we have total annual gross revenues of $1.0$1.07 billion or more; (ii) the last day of our fiscal year following the fifth anniversary of the date of the completion of this offering;our initial public offering (IPO); (iii) the date on which we have issued more than $1.0 billion in nonconvertible debt during the previous three years; or (iv) the date on which we are deemed to be a large accelerated filer under the rules of the Securities and Exchange Commission or the SEC.(SEC). We may choose to take advantage of some but not all of these exemptions. We have taken advantage of reduced reporting requirements in this prospectus. Accordingly, the information contained herein may be different from the information you receive from other public companies in which you hold stock. We have irrevocably elected to “opt out” of the exemption for the delayed adoption of certain accounting standards and, therefore, will be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies.

Company and Other Information

We were founded in 1968 and have been providing composite wind blades for 15 years.since 2001. Our knowledge and experience of composite materials and manufacturing originates with our predecessor company, Tillotson Pearson Inc., a leading manufacturer of high-performance sail and powerboats along with a wide range of composite structures used in other industrial applications. Following the separation from our boat building business in 2004, we reorganized in Delaware as LCSI Holding, Inc. Weand then changed our corporate name to TPI Composites, Inc. in 2008. Today, we are headquartered in Scottsdale, Arizona, and we have expanded our global footprint to include domestic facilities in Newton, Iowa; Fall River, Massachusetts; Warren, Rhode Island; and Santa Teresa, New Mexico and international facilities in Dafeng, China; Taicang Port, China; Taicang City, China; Juarez,Juárez, Mexico; and Izmir, Turkey. Together, as of June 30, 2016,March 31, 2017, we have approximately 3.5 million square feet of manufacturing space and over 6,000nearly 8,000 employees, including materials and process engineers, manufacturing process engineers, quality assurance personnel and production workers.

Our wind blade and precision molding and assembly systems manufacturing businesses accounted for over 99% of our total net sales for the three months ended March 31, 2017 and for each of the years ended December 31, 2016, 2015 and 2014. We also leverage our advanced composite technology and history of innovation to supply high strength, lightweight and durable composite products to the transportation market. For a further discussion regarding our wind blade and precision molding and assembly system businesses, refer to the discussion in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations” included elsewhere in this prospectus.

In July 2016, we completed an initial public offering of 7,187,500 shares of our common stock at a price of $11.00 per share, which included 937,500 shares issued pursuant to the underwriters’ exercise of their option to purchase additional shares. Certain of our existing shareholders, a non-employee director and executive officers purchased an aggregate of 1,250,000 shares of common stock in the IPO included in the total issuance above. The net proceeds from the IPO were $67.2 million after deducting underwriting discounts and offering expenses. Immediately prior to the closing of the IPO, all shares of the then-outstanding redeemable preferred shares converted into an aggregate of 21,110,204 shares of common stock and the redeemable preferred share

warrants converted on a net issuance basis into 120,923 shares of common stock. In addition, concurrent with the closing of the IPO, certain subordinated convertible promissory notes in the aggregate principal and interest amount of $11.9 million were converted into 1,079,749 shares of common stock at the public offering price of $11.00 per share.

Prior to the IPO, in July 2016 we amended our amended and restated certificate of incorporation to effect a 360-for-1 forward stock split of our common stock. As a result of the stock split, we have adjusted the share amounts authorized and issuable under our share-based compensation plans. All share and per share common stock information (including those related to our share-based compensation plans) referenced throughout the consolidated financial statements and notes thereto have been retroactively adjusted to reflect this stock split. The stock split did not cause an adjustment to the par value of the authorized shares of common stock.

Our principal executive offices are located at 8501 North Scottsdale Road, Gainey Center II, Suite 100, Scottsdale, Arizona 85253 and our telephone number is (480) 305-8910. Our website address iswww.tpicomposites.com. The information contained on our website or that can be accessed through our website is not part of this prospectus, and investors should not rely on any such information in deciding whether to purchase our common stock.

This prospectus contains references to our trademarks. This prospectus contains additional trade names, trademarks and service marks of other companies. Those other trade names, trademarks and service marks are the property of their respective owners. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, these other companies. Solely for convenience, the trademarks and trade names in this prospectus are referred to without the® and ™ symbols, but such references should not be construed as any indicator that their respective owners will not assert, to the fullest extent under applicable law, their rights thereto.

THE OFFERING

Common stock offered by |

Common stock to be outstanding immediately after this offering |

Option to purchase additional shares from |

Use of proceeds |

| offering. We |

Concentration of Ownership | Upon the completion of this offering, our executive officers and directors and stockholders holding more than 5% of our capital stock, and their affiliates, will beneficially own, in the aggregate, approximately |

Dividend Policy | We currently intend to retain earnings, if any, to finance the development and growth of our business and do not anticipate paying cash dividends on the common stock in the future. |

|

Risk factors | You should read “Risk Factors” beginning on page |

The number of shares of common stock to be outstanding after this offering is based on 25,531,26333,736,863 shares of common stock outstanding as of March 31, 20162017 and excludes:

Except as otherwise indicated, all information in this prospectus:

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

We have derived the summary consolidated statements of operations data for the three months ended March 31, 20162017 and 20152016 and the consolidated balance sheet data as of March 31, 20162017 from our unaudited interim condensed consolidated financial statements included elsewhere in this prospectus. The unaudited interim condensed consolidated financial statements were prepared on a basis consistent with our audited financial statements and include, in the opinion of management, all adjustments, consisting only of a normal recurring nature, that are necessary for a fair presentation of the financial information set forth in those statements. We have derived the summary consolidated statements of operations data for the years ended December 31, 2016, 2015 and 2014 and 2013the summary consolidated balance sheet data as of December 31, 2016 from our audited consolidated financial statements included elsewhere in this prospectus. Our historical results are not necessarily indicative of the results that may be expected in the future and the results in the three months ended March 31, 2016 are not necessarily indicative of the results that may be expected for the full year or any other period.future. The following summary consolidated financial and other data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus.

Three Months Ended | Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||

Three Months Ended | Year Ended December 31, | 2017 | 2016 | 2016 | 2015 | 2014 | ||||||||||||||||||||||||||||||||||

2016 | 2015 | 2015 | 2014 | 2013 | (unaudited) | |||||||||||||||||||||||||||||||||||

| (in thousands, except per share data) | (in thousands, except per share data) | |||||||||||||||||||||||||||||||||||||||

Consolidated Statements of Operations Data: | ||||||||||||||||||||||||||||||||||||||||

Net sales | $ | 176,110 | $ | 95,589 | $ | 585,852 | $ | 320,747 | $ | 215,054 | $ | 191,602 | $ | 176,110 | $ | 754,877 | $ | 585,852 | $ | 320,747 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Cost of sales | 159,866 | 90,884 | 528,247 | 289,528 | 200,182 | 167,423 | 159,866 | 659,745 | 528,247 | 289,528 | ||||||||||||||||||||||||||||||

Startup and transition costs | 3,306 | 4,154 | 15,860 | 16,567 | 6,607 | 6,159 | 3,306 | 18,127 | 15,860 | 16,567 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Total cost of goods sold | 163,172 | 95,038 | 544,107 | 306,095 | 206,789 | 173,582 | 163,172 | 677,872 | 544,107 | 306,095 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Gross profit | 12,938 | 551 | 41,745 | 14,652 | 8,265 | 18,020 | 12,938 | 77,005 | 41,745 | 14,652 | ||||||||||||||||||||||||||||||

General and administrative expenses | 4,749 | 3,208 | 14,126 | 9,175 | 7,566 | 8,306 | 4,749 | 33,892 | 14,126 | 9,175 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Income (loss) from operations | 8,189 | (2,657 | ) | 27,619 | 5,477 | 699 | ||||||||||||||||||||||||||||||||||

Income from operations | 9,714 | 8,189 | 43,113 | 27,619 | 5,477 | |||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Other income (expense): | ||||||||||||||||||||||||||||||||||||||||

Interest income | 21 | 59 | 161 | 186 | 155 | 19 | 21 | 344 | 161 | 186 | ||||||||||||||||||||||||||||||

Interest expense | (3,912 | ) | (3,551 | ) | (14,565 | ) | (7,236 | ) | (3,474 | ) | (3,026 | ) | (3,912 | ) | (17,614 | ) | (14,565 | ) | (7,236 | ) | ||||||||||||||||||||

Loss on extinguishment of debt | — | — | — | (2,946 | ) | — | — | — | (4,487 | ) | — | (2,946 | ) | |||||||||||||||||||||||||||

Realized gain (loss) on foreign currency remeasurement | (439 | ) | 163 | (1,802 | ) | (1,743 | ) | (1,892 | ) | |||||||||||||||||||||||||||||||

Realized loss on foreign currency remeasurement | (1,381 | ) | (439 | ) | (757 | ) | (1,802 | ) | (1,743 | ) | ||||||||||||||||||||||||||||||

Miscellaneous income | 190 | 129 | 246 | 539 | 140 | 320 | 190 | 238 | 246 | 539 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Total other expense | (4,140 | ) | (3,200 | ) | (15,960 | ) | (11,200 | ) | (5,071 | ) | (4,068 | ) | (4,140 | ) | (22,276 | ) | (15,960 | ) | (11,200 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Income (loss) before income taxes | 4,049 | (5,857 | ) | 11,659 | (5,723 | ) | (4,372 | ) | 5,646 | 4,049 | 20,837 | 11,659 | (5,723 | ) | ||||||||||||||||||||||||||

Income tax benefit (provision) | (2,303 | ) | 120 | (3,977 | ) | (925 | ) | 3,346 | ||||||||||||||||||||||||||||||||

|

|

|

|

| ||||||||||||||||||||||||||||||||||||

Net income (loss) before noncontrolling interest | 1,746 | (5,737 | ) | 7,682 | (6,648 | ) | (1,026 | ) | ||||||||||||||||||||||||||||||||

Net loss attributable to noncontrolling interest(1) | — | — | — | — | 2,305 | |||||||||||||||||||||||||||||||||||

Income tax provision | (2,101 | ) | (2,303 | ) | (6,995 | ) | (3,977 | ) | (925 | ) | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Net income (loss) | 1,746 | (5,737 | ) | 7,682 | (6,648 | ) | 1,279 | 3,545 | 1,746 | 13,842 | 7,682 | (6,648 | ) | |||||||||||||||||||||||||||

Net income attributable to preferred shareholders(2) | 2,437 | 2,356 | 9,423 | 13,930 | 14,149 | |||||||||||||||||||||||||||||||||||

Net income attributable to preferred shareholders(1) | — | 2,437 | 5,471 | 9,423 | 13,930 | |||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Net loss attributable to common shareholders | $ | (691 | ) | $ | (8,093 | ) | $ | (1,741 | ) | $ | (20,578 | ) | $ | (12,870 | ) | |||||||||||||||||||||||||

Net income (loss) attributable to common shareholders | $ | 3,545 | $ | (691 | ) | $ | 8,371 | $ | (1,741 | ) | $ | (20,578 | ) | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Weighted-average common shares outstanding, basic and diluted(3) | 4,238 | 4,238 | 4,238 | 4,238 | 4,238 | |||||||||||||||||||||||||||||||||||

|

|

|

|

| ||||||||||||||||||||||||||||||||||||

Net loss per common share, basic and diluted(3) | $ | (0.16 | ) | $ | (1.91 | ) | $ | (0.41 | ) | $ | (4.86 | ) | $ | (3.04 | ) | |||||||||||||||||||||||||

|

|

|

|

| ||||||||||||||||||||||||||||||||||||

Pro forma net income attributable to common shareholders | $ | 1,746 | $ | 7,682 | ||||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||||||

Pro forma weighted-average common shares outstanding (unaudited) | ||||||||||||||||||||||||||||||||||||||||

Basic(3) | 25,531 | 25,531 | ||||||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||||||

Diluted(3) | 25,553 | 25,553 | ||||||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||||||

Pro forma net income per common share (unaudited) | ||||||||||||||||||||||||||||||||||||||||

Weighted-average common shares outstanding: | ||||||||||||||||||||||||||||||||||||||||

Basic(2) | 33,737 | 4,238 | 17,530 | 4,238 | 4,238 | |||||||||||||||||||||||||||||||||||

Diluted(2) | 33,827 | 4,238 | 17,616 | 4,238 | 4,238 | |||||||||||||||||||||||||||||||||||

Net income (loss) per common share: | ||||||||||||||||||||||||||||||||||||||||

Basic | $ | 0.07 | $ | 0.30 | $ | 0.11 | $ | (0.16 | ) | $ | 0.48 | $ | (0.41 | ) | $ | (4.86 | ) | |||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||||||

Diluted | $ | 0.07 | $ | 0.30 | $ | 0.10 | $ | (0.16 | ) | $ | 0.48 | $ | (0.41 | ) | $ | (4.86 | ) | |||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||||||

Three Months Ended | Year Ended December 31, | |||||||||||||||||||

2016 | 2015 | 2015 | 2014 | 2013 | ||||||||||||||||

| (in thousands, except other operating information) | ||||||||||||||||||||

Other Financial Information: | ||||||||||||||||||||

Total billings(4) | $ | 174,538 | $ | 117,090 | $ | 600,107 | $ | 362,749 | $ | 221,057 | ||||||||||

EBITDA(4) | $ | 10,951 | $ | 36 | $ | 37,479 | $ | 8,768 | $ | 6,502 | ||||||||||

Adjusted EBITDA(4) | $ | 11,390 | $ | (127 | ) | $ | 39,281 | $ | 13,457 | $ | 8,430 | |||||||||

Capital expenditures | $ | 10,888 | $ | 10,605 | $ | 26,361 | $ | 18,924 | $ | 7,065 | ||||||||||

Total debt, net of debt issuance costs and discount | $ | 131,163 | $ | 115,287 | $ | 129,346 | $ | 120,849 | $ | 36,562 | ||||||||||

Net debt(4) | $ | 101,392 | $ | 98,070 | $ | 90,667 | $ | 87,547 | $ | 26,590 | ||||||||||

Other Operating Information: | ||||||||||||||||||||

Sets(5) | 486 | 303 | | 1,609 | | 966 | 648 | |||||||||||||

Estimated megawatts(6) | 1,113 | 645 | 3,595 | 2,029 | 1,173 | |||||||||||||||

Total manufacturing line capacity(7) | 32 | 30 | 32 | 30 | 16 | |||||||||||||||

Dedicated manufacturing lines(8) | 38 | 29 | 34 | 29 | 16 | |||||||||||||||

Manufacturing lines in startup(9) | 0 | 8 | 10 | 9 | 2 | |||||||||||||||

Manufacturing lines in transition(10) | 3 | 4 | 11 | 8 | 2 | |||||||||||||||

Three Months Ended | Year Ended December 31, | |||||||||||||||||||

2017 | 2016 | 2016 | 2015 | 2014 | ||||||||||||||||

| (unaudited) | ||||||||||||||||||||

| (in thousands, except other operating information) | ||||||||||||||||||||

Other Financial Information: | ||||||||||||||||||||

Total billings(3) | $ | 211,360 | $ | 174,538 | $ | 764,424 | $ | 600,107 | $ | 362,749 | ||||||||||

EBITDA(3) | $ | 12,482 | $ | 10,951 | $ | 55,491 | $ | 37,479 | $ | 11,714 | ||||||||||

Adjusted EBITDA(3) | $ | 15,570 | $ | 11,390 | $ | 66,150 | $ | 39,281 | $ | 13,457 | ||||||||||

Capital expenditures | $ | 16,922 | $ | 10,888 | $ | 30,507 | $ | 26,361 | $ | 18,924 | ||||||||||

Total debt, net of debt issuance costs and discount | $ | 120,489 | $ | 131,163 | $ | 123,155 | $ | 129,346 | $ | 120,849 | ||||||||||

Net debt(3) | $ | 7,095 | $ | 101,392 | $ | 6,379 | $ | 90,667 | $ | 87,547 | ||||||||||

Other Operating Information: | ||||||||||||||||||||

Sets(4) | 636 | 486 | 2,154 | 1,609 | 966 | |||||||||||||||

Estimated megawatts(5) | 1,460 | 1,113 | 4,920 | 3,595 | 2,029 | |||||||||||||||

Dedicated manufacturing lines(6) | 44 | 38 | 44 | 34 | 29 | |||||||||||||||

Total manufacturing lines installed(7) | 39 | 32 | 33 | 30 | 22 | |||||||||||||||

Manufacturing lines in startup(8) | 9 | — | 3 | 10 | 9 | |||||||||||||||

Manufacturing lines in transition(9) | — | 3 | 3 | 11 | 8 | |||||||||||||||

| (1) |

| Represents the annual accrual of dividends on our convertible and senior redeemable preferred shares, the accretion to redemption amounts on our convertible preferred shares and warrant fair value adjustments. Immediately prior to the closing of the IPO, all preferred shares were converted into shares of our common stock and as a result, the accrual of dividends ceased. |

| For the |

| See “Non-GAAP Financial Measures” below for more information. |

| Number of wind blade sets (which consist of three wind blades) invoiced |

| Estimated megawatts of energy capacity to be generated by wind blade sets invoiced in the period. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Metrics Used By Management to Measure Performance” for more information. |

| Number of manufacturing lines |

| Number of manufacturing lines installed and either in |

| Number of manufacturing lines in a startup phase during the pre-production and production ramp-up periods. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Metrics Used By Management to Measure Performance” for more information. |

| (9) | Number of manufacturing lines that were being transitioned to a new wind blade model during the period. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Metrics Used By Management to Measure Performance” for more information. |

As of | ||||||||||||

Actual | Pro Forma(1) | Pro Forma As Adjusted(2)(3) | ||||||||||

| (in thousands) | ||||||||||||

Consolidated Balance Sheet Data | ||||||||||||

Cash and cash equivalents | $ | 35,842 | $ | 35,842 | $ | 125,222 | ||||||

Total assets | 358,462 | 358,462 | 447,842 | |||||||||

Total debt, net of debt issuance costs and discount | 131,163 | 131,163 | 123,188 | |||||||||

Total liabilities | 348,640 | 348,640 | 337,165 | |||||||||

Total convertible and senior redeemable preferred shares and warrants | 201,282 | — | — | |||||||||

Total shareholders’ equity (deficit) | (191,460 | ) | 9,822 | 110,677 | ||||||||

| March 31, 2017 | ||||

(unaudited) | ||||

| (in thousands) | ||||

Consolidated Balance Sheet Data | ||||

Cash and cash equivalents | $ | 115,541 | ||

Total assets | 477,941 | |||

Total debt, net of debt issuance costs and discount | 120,489 | |||

Total liabilities | 365,875 | |||

Total shareholders’ equity | 112,066 | |||

Non-GAAP Financial Measures

In addition to providing results that are determined in accordance with GAAP, we have provided certain financial measures that are not in accordance with GAAP. Total billings, EBITDA, adjusted EBITDA and net debt are non-GAAP financial measures. We define total billings as the total amounts we have invoiced our customers for products and services for which we are entitled to payment under the terms of our long-term supply agreements or other contractual agreements. Under GAAP, we do not recognize revenue on our wind blade sales until the wind bladesthey have been delivered to our customers. In many cases, customers request us to store their wind blades for a

period of time after we have invoiced them. The revenues associated with these transactions are deferred and recognized upon delivery but we are contractually entitled to payment for those wind blades and, accordingly, invoice them when the blades are placed in storage.

We define EBITDA as net income (loss) attributable to the Company plus interest expense (net(including losses on the extinguishment of debt and net of interest income), income taxes and depreciation and amortization.

We define adjusted EBITDA as EBITDA plus any share-based compensation expense, plus or minus any realized gains or losses from foreign currency remeasurement plus any loss on extinguishment of debt. EBITDA and adjusted EBITDA are calculated differently from EBITDA as used in our Credit Facility (as defined below).remeasurement.

We define net debt as the total principal amount of debt outstanding less unrestricted cash and cash equivalents. The total principal amount of debt outstanding is comprised of the long-term debt and current maturities of long-term debt as presented in our consolidated balance sheets adjusting for any debt issuance costs and discount.

Our use of total billings, EBITDA, adjusted EBITDA and net debt have limitations, and you should not consider total billings, EBITDA, adjusted EBITDA or net debt in isolation from or as a substitute for measures such as net sales, net income (loss) or total debt, net of debt issuance costs and discount reported under GAAP. See the “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Metrics Used by Management to Measure Performance” for the related reconciliations of total billings, EBITDA, adjusted EBITDA and net debt.

An investment in our common stock involves a high degree of risk. You should consider carefully the following risks and other information contained in this prospectus, including our consolidated financial statements and related notes, before you decide whether to buy our common stock. If any of the events contemplated by the following discussion of risks should occur, our business, results of operations, financial condition and growth prospects could suffer significantly. As a result, the market price of our common stock could decline, and you may lose all or part of the money you paid to buy our common stock. The risks below are not the only ones we face. Additional risks that we currently do not know about or that we currently believe to be immaterial may also impair our business. Certain statements below are forward-looking statements. See “Special Note Regarding Forward-Looking Statements” in this prospectus.

Risks Related to Our Wind Blade Business

GE’s acquisition of LM Wind Power, our largest competitor, may materially harm our business, financial condition and results of operations and may cause the price of our common stock to decline.

In April 2017, GE completed its acquisition of LM Wind Power, our largest competitor. We currently have entered into five supply agreements with GE Wind providing for the supply of wind blades from our Iowa facility; two Juárez, Mexico facilities; our original Turkey facility; and our Taicang Port, China facility. In October 2016, we entered into (i) an amended and restated supply agreement for the continued supply of wind blades from our Iowa facility through December 31, 2020, (ii) an amendment to our existing supply agreement for the continued supply of wind blades from our original Juárez, Mexico facility through December 31, 2020 and (iii) a new supply agreement with GE Wind for the supply of incremental wind blades from our second manufacturing facility in Juárez, Mexico through December 31, 2020. Although we recently extended and expanded certain of our supply agreements, GE Wind may decide to utilize LM for more of its wind blade production as a result of the acquisition of LM. As such, GE Wind may not continue to purchase wind blades from us at similar volumes or on as favorable terms in the future. In addition, our current supply agreements with GE Wind for the supply of wind blades from our Turkey and Taicang, China facilities expire on December 31, 2017. In March 2017, the Company announced that it does not intend to renew the Turkey supply agreement with GE Wind, and GE Wind or the Company may elect not to renew the China supply agreement. GE Wind also may elect to terminate our Iowa supply agreement at the end of 2018 or 2019 by providing us with 12 months’ advance notice and paying us a specified termination fee. GE Wind may also elect to terminate our two Mexico supply agreements with 15 days’ notice and pay us a termination fee. If GE Wind elects to utilize LM for more of its wind blade production, reduce the volumes of wind blades it purchases from us or terminates any of our supply agreements, it may materially harm our business, financial condition and results of operations.

In addition, GE Ventures Limited (GE Ventures), a GE affiliated company, owns 8.4% of our outstanding common stock as of March 31, 2017. GE Ventures’ lock-up agreement with our IPO underwriters expired on January 17, 2017 and as a result of GE’s recent acquisition of LM, GE Ventures may be more inclined to sell all or a portion of its shares of our common stock. If GE Ventures sells all or a portion of its holdings of our common stock pursuant to Rule 144 or otherwise, it may cause the price of our common stock to decline.

The results of the 2016 United States presidential and congressional elections has created regulatory uncertainty for our business and the wind energy sector and may materially harm our business, financial condition and results of operations.

U.S. President Trump, certain members of the U.S. Congress, and key U.S. administrative officials and policy makers have suggested renegotiation of The North American Free Trade Agreement and the implementation of tariffs, duties, border taxes or other similar assessments that could impact the level of trade between the U.S. and Mexico. President Trump also has publicly stated that he may seek to impose tariffs, duties,

border taxes or other similar assessments on products imported from China. A substantial amount of the wind blades that we manufacture in our Mexico and China facilities are imported into the United States. If any such tariffs, duties, border taxes or other assessments are imposed on our wind blades that are imported into the United States, it would increase the total cost of our wind blades and may decrease demand for our wind blades. In addition, we may not be able to fully pass on the added cost of such tariffs, taxes, duties or assessments to our customers and may materially harm our business, financial condition and results of operations.

President Trump also has made comments during his presidency and the presidential campaign suggesting that he is not supportive of various clean energy programs and initiatives designed to curtail global warming. In March 2017, President Trump signed an executive order that requires, among other things, that the EPA withdraw the Clean Power Plan and draft new regulations to replace it. It remains unclear what impact, if any, this executive order will have on the demand for wind energy domestically and internationally. In addition, it remains unclear what specifically President Trump would or would not do with respect to these programs and initiatives, and what support he would have for any potential changes to such legislative programs and initiatives in the Unites States Congress, even though both the House of Representatives and Senate are controlled by the Republican Party. If President Trump and/or the United States Congress take action or publicly speak out about the need to eliminate, modify or further reduce the PTC, the Clean Power Plan or other legislation, regulations and incentives supporting wind energy, such actions may result in a decrease in demand for wind energy in the United States and other geographical markets and may materially harm our business, financial condition and results of operations.

A significant portion of our business is derived from a small number of customers, and one wind blade customer in particular, therefore any loss of or reduction in purchase orders, failure of these customers to fulfill their obligations or our failure to secure long-term supply agreement renewals from these customers would materially harm our business.

Substantially all of our revenues are derived from four wind blade customers. One customer, GE Wind, accounted for 54.6%44.3%, 50.3%, 53.3%, and 73.2% and 91.2% of our total net sales for the three months ended March 31, 20162017 and for the years ended December 31, 2016, 2015 2014 and 2013,2014, respectively. In addition, three customers, Vestas, Nordex and Gamesa accounted for 17.0%23.2%, 11.1%17.5% and 10.3%13.7% of our net sales for the three months ended March 31, 2016,2017, respectively, and three customers, Nordex, Acciona (which was acquired by Nordex in April 2016)20.1%, 17.5% and Gamesa accounted for 15.7%, 10.8% and 10.3% of our net sales for the year ended December 31, 2016, respectively. During the year ended December 31, 2015, two customers, Nordex and Gamesa, accounted for 26.5% and 10.3% of our net sales, respectively. Accordingly, we are substantially dependent on continued business from our current wind blade customers, and GE Wind in particular. GE Wind and other customers may not continue to purchase wind blades from us at similar volumes or on as favorable terms in the future. For example, GESee “GE’s acquisition of LM Wind has inPower, our largest competitor, may materially harm our business, financial condition and results of operations and may cause the past informed usprice of their intentionour common stock to terminate a supply agreement. However, in that case, the agreement was not terminated but was instead renegotiated.decline.” If GE Wind or one or more of our other wind blade customers were to reduce or delay wind blade orders, fail to pay amounts due or satisfactorily perform their respective contractual obligations with us or otherwise terminate or fail to renew their long-term supply agreements with us, our business, financial condition and results of operations could be materially harmed.

Defects in materials and workmanship or wind blade failures could harm our reputation, expose us to product warranty or other liability claims, decrease demand for our wind blades, or materially harm existing or prospective customer relationships.

Defects in our wind blades, whether caused by a design, engineering, materials, manufacturing or component failure or deficiencies in our manufacturing processes, are unpredictable and an inherent risk in manufacturing technically advanced products. We have, in the past, experienced wind blade testing failures and defects at some of our facilities during the startup manufacturing phase of new products, and we may experience failures or defects in the future. For instance, customer qualification of our Iowa facility was delayed due to some wind blade testing failures in 2010, resulting in corresponding delays in our wind blade production at that facility. We have also experienced wind blade failures in the field. For example, in April 2015, a wind blade we manufactured failed in Finland. Any such customer qualification and wind blade testing failures or other product defects in the future could materially harm our existing and prospective customer relationships. Specifically, negative publicity about the quality of our wind

blades or defects in the wind blades supplied to our customers could result in a reduction in wind blade orders, increased warranty claims, product liability claims and other damages or termination of our long-term supply agreements or business relationships with current or new customers. In addition, we have recently started wind blade production at new facilities in Turkey and Mexico which may expose us to greater risk of warranty claims as these facilities ramp up to serial production levels.

We may determine that resolving potential warranty claims through a negotiated settlement may be in the best interest of the business and long-term customer relationships. For example, in June 2016, we entered into

a settlement agreement and release with one of our customers, Nordex relating to the April 2015 wind blade failure referenced above.failure. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Other Contingencies” for more information. Wind blades may also fail due to lightning strikes andor other extreme weather, which could also result in negative publicity regarding our wind blades and wind energy in general. In addition, product defects may require costly repairs or replacement components, a change in our manufacturing processes or recall of previously manufactured wind blades, which could result in significant expense and materially harm our existing or prospective customer relationships. Further, defects or product liability claims, with or without merit, may result in negative publicity that could harm our future sales and our reputation in the industry. Any of the foregoing could materially harm our business, operating results and financial condition.

We have experienced, and could in the future experience, quality or operational issues in connection with plant construction or expansion, wind blade model transitions and wind blade manufacturing, which could result in losses and cause delays in our ability to complete our projects and may therefore materially harm our business, financial condition and results of operations.

We dedicate most of the capacity of our current wind blade manufacturing facilities to existing customers and, as a result, we may need to build additional manufacturing capacity or facilities to serve the needs of new customers or expanded needs of existing customers. We haverecently entered into lease agreements with third parties to lease new manufacturing facilities in Mexico and Turkey, and we expect to commencecommenced operations at these new facilities in the second halfthird quarter of 2016. We have also entered into a new lease with a third party for a third manufacturing facility in Juárez, Mexico, and we expect to commencecommenced operations at this facility in the first half ofJanuary 2017. The construction of new plants and the expansion of existing plants involves significant time, cost and other risks. We expect our plants to generate losses in their first 12 to 24 months of operations related to production startup expenses.costs. Additionally, numerous factors can contribute, and have in the past contributed, to delays or difficulties in the startup of, or the adoption of our manufacturing lines to produce larger wind blade models, which we refer to as model transitions, in our manufacturing facilities, including permitting, construction or renovation delays, the engineering and fabrication of specialized equipment, the modification of our general production know-how and customer-specific manufacturing processes to address the specific wind blades to be tested and built, changing and evolving customer specifications and expectations and the hiring and training of plant personnel. If our production or the delivery by any third-party suppliers of any custom equipment is delayed, the construction or renovation of the facility, or the addition of the production line would be delayed. Any delays or difficulties in plant startup or expansion may result in cost overruns, production delays, contractual penalties, loss of revenues and impairment of customer relationships, which could materially harm our business, financial condition and results of operations.

Our long-term supply agreements with our customers are subject to termination on short notice and our failure to perform our obligations under these agreements or the termination of agreements would materially harm our business.

Our current long-term supply agreements expire between the end of 2017 and the end of 2021.2023. Some of our long-term supply agreements contain provisions that allow for the termination of those agreements upon the customer providing us with 92 to 365 days’ advance written notice or, in one instance,two instances, upon no advance notice, or upon a material breach that goes uncured for up to 15 to 30 days. Additionally, our long-term supply agreements contain provisions allowing our customers to terminate these agreements upon our failure to deliver

the contracted wind blade volumes or our failure to meet certain mutually agreed upon cost reductions. Our customers may not continue to maintain long-term supply agreements with us in the future. If one or more of our customers terminate or fail to renew their long-term supply agreements with us, it would materially harm our business, financial condition and results of operations.