(Name, address, including zip code, and telephone number, including area code, of Agentagent for Service)service)

With a copy to:

David P. Hooper, Esq. Barnes & Thornburg LLP 11 S. Meridian Street Indianapolis, Indiana 46204 (317) 236-1313 |

Approximate date of commencement of proposed sale to the public:

From time to time or at one time after the effective date of this registration statementRegistration Statement, as the registrant shall determine.

If the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans, please check the following box.box: o☐

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, other than securities offered only in connection with dividend or interest reinvestment plans, check the following box.box: x☒

If this Form is filed to register additional securities offor an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o☐

If this Form is a post‑effectivepost-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o☐

If this Form is a registration statement pursuant to General Instruction I.D. or a post-effective amendment thereto that shall become effective upon filing with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box. o☐

If this Form is a post‑effectivepost-effective amendment to a registration statement filed pursuant to General Instruction I.D. filed to register additional securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following box. o☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See definitionthe definitions of “large accelerated filer”,filer,” “accelerated filer”filer,” “smaller reporting company” and “smaller reporting“emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ☐ | Accelerated filer | ☒ | |

Non-accelerated filer | ☐ | Smaller reporting company | ☒ | |

Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of Registration Feethe Securities Act. ☐

CALCULATION OF REGISTRATION FEE

Title of each class of securities to be registered |

| Amount to be registered(1) |

| Proposed maximum offering price per unit |

| Proposed maximum aggregate offering price(2) |

| Amount of registration fee(2) |

Beneficial unit certificates representing assigned limited partnership interests |

| – |

| – |

| $225,000,000 |

| $20,576 |

| Title of each class of securities to be registered | Proposed maximum aggregate offering price(1) | Amount of registration fee(2), (3) |

| Shares representing assigned limited partnership interests | $225,000,000 | $30,690 |

(1) | There are being registered hereunder such presently indeterminate number of |

(2) | The proposed maximum aggregate offering price has been estimated solely to calculate the registration fee |

THE REGISTRANT HEREBY AMENDS THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL THE REGISTRANT SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(a) of the Securities Act ofOF THE SECURITIES ACT OF 1933 or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said SectionOR UNTIL THE REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE COMMISSION, ACTING PURSUANT TO SAID SECTION 8(a), may determine.

THE INFORMATION IN THIS PROSPECTUS IS NOT COMPLETE AND MAY BE CHANGED. WE MAY NOT ISSUESELL THESE SECURITIES UNTIL THE REGISTRATION STATEMENT FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ISBECOMES EFFECTIVE. THIS PROSPECTUS IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT SOLICITING AN OFFER TO BUY THESE SECURITIES IN ANY STATE OR JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

Subject to completion, dated November 26, 2019

PROSPECTUS

$225,000,000

Beneficial Unit Certificates Representing Assigned Limited Partnership Interests

We may use this prospectus to offer, sharesfrom time to time, in one or more offerings, beneficial unit certificates representing assigned limited partnership interests (“BUCs”) in America First Tax ExemptMultifamily Investors, L.P. We may offer these shares from time to time.The aggregate initial offering price of all BUCs sold by us under this prospectus will not exceed $225,000,000. We will provide the specific terms of each issuance of these securities in supplements to this prospectus. You should read this prospectus and any supplement carefully before you decide to invest in our shares.

Our sharesBUCs are quotedtraded on the NASDAQ Global Select Market under the symbol “ATAX.” The last reported sale price of our BUCs on November 25, 2019 was $7.32 per BUC. Our principal executive offices are located at 1004 Farnam Street, Suite 400, Omaha, Nebraska, 68102. Our telephone number is (402) 444-1630.

We may offer and sell these securities to or through one or more underwriters, dealers, and agents, or directly to purchasers, on a continuous or delayed basis, and in amounts, at prices, and at terms to be determined by market conditions and other factors at the time of the offering. This prospectus describes the general terms of the securities and the general manner in which we will offer the securities. Each time we offer to sell securities we will provide a prospectus supplement that will contain specific information about those securities and the terms of that offering. The prospectus supplement also may add, update, or change information contained in this prospectus. If agents or any dealers or underwriters are involved in the sale of the securities, the applicable prospectus supplement will set forth the names of the agents, dealers, or underwriters and any applicable commissions or discounts. Net proceeds from the sale of securities will be set forth in the applicable prospectus supplement. For general information about the distribution of securities offered, please see “Plan of Distribution” in this prospectus.

This prospectus may be used to offer and sell securities only if accompanied by a prospectus supplement. You should read this prospectus and any prospectus supplement carefully before you invest. You should also read the documents we refer to in the “Where You Can Find More Information” section of this prospectus for information on us and our financial statements.

Investing in our sharessecurities involves a high degree of risk. Limited partnerships are inherently different from corporations. You should carefully consider the information under the heading “RISK FACTORS”“Risk Factors” beginning on page 97 of this prospectus, before buying our shares.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is _______, 2013

Page No. | |

1 | |

2 | |

3 | |

7 | |

8 | |

8 | |

18 | |

18 | |

32 | |

34 | |

35 | |

35 | |

35 | |

35 |

You should rely only on the information incorporated by reference or provided in this prospectus or any prospectus supplement or any “free writing prospectus” we may authorize to be delivered to you. We have not authorized anyone else to provide you with different information or to make additional representations. We are not making or soliciting an offer of any securities other than the securities described in this prospectus and any prospectus supplement. We are not making or soliciting an offer of these securities in any state or jurisdiction where an offer is not permitted or in any circumstances in which such offer or solicitation is unlawful. You should not assume that the information contained or incorporated by reference in this prospectus andor any related prospectus supplement. supplement is accurate as of any date other than the date on the front cover of each of those documents.

We have not authorized anyone to provide you with information or to make any representation that differs from the information in this prospectus and any related prospectus supplement. If anyone provides you with different or inconsistent information, you should not rely on it. You should not assumefurther note that the information containedrepresentations, warranties, and covenants made by us in this prospectus, any related prospectus supplement and the documentsagreement that is filed as an exhibit to any document that is incorporated by reference herein is correct on any date after their respective dates even though this prospectus and any related prospectus supplement are delivered or shares are sold pursuant to this prospectus and a related prospectus supplement at a later date. Our business, financial condition, results of operations or prospects may have changed since those dates. To the extent the information contained in this prospectus or the documents incorporated by reference herein differs or varies from the information contained in any prospectus supplement deliveredwere made solely for the benefit of the parties to you,such agreement and the informationthird-party beneficiaries named therein, if any, including, in some cases, for the purpose of allocating risk among the parties to such prospectus supplement will supersedeagreements, and should not be deemed to be a representation, warranty, or covenant to you. Moreover, such information.representations, warranties, or covenants were accurate only as of the date when made. Accordingly, such representations, warranties, and covenants should not be relied on as accurately representing the current state of our affairs.

i

This prospectus is part of a “shelf” registration statement on Form S-3 that we filed with the Securities and Exchange Commission, (or “SEC”) using a “shelf”or SEC. Under the shelf registration process. Under this process, we may, offer andfrom time to time, sell shares representing assigned limited partnership interestsup to $225,000,000 in our companytotal aggregate offering price of BUCs, as described in this prospectus, in one or more offerings for total proceeds of up to $225,000,000. offerings.

This prospectus provides you with a general description of our businessus and the shares that we may offer.securities offered under this prospectus. Each time we offer to sell any shares,securities under this prospectus, we will provide a prospectus supplement to this prospectus that will contain specific information about the terms of that offering.offering and the securities being offered. The prospectus supplement also may also add to, update, or change the information contained in this prospectus. ItIf there is important for you to considerany inconsistency between the information contained in this prospectus and any information incorporated by reference in this prospectus, on the one hand, and the information contained in any applicable prospectus supplement together withor incorporated by reference therein, on the other hand, you should rely on the information in the applicable prospectus supplement or incorporated by reference in the prospectus supplement. You should read carefully this prospectus, any prospectus supplement, and the additional information described below under the heading “WHERE YOU CAN FIND MORE INFORMATION.“Where You Can Find More Information.”

Wherever references are made in this prospectus to information that will be included in a prospectus supplement, to the extent permitted by applicable law, rules, or regulations, we may instead include such information or add, update, or change the information contained in this prospectus by means of a post-effective amendment to the registration statement, of which this prospectus is a part, through filings we make with the SEC that are incorporated by reference into this prospectus or by any other method as may then be permitted under applicable law, rules, or regulations.

Statements made in this prospectus, in any prospectus supplement or in any document incorporated by reference in this prospectus or any prospectus supplement as to the contents of any contract or other document are not necessarily complete. In each instance we refer you to the copy of the contract or other document filed as an exhibit to the registration statement of which this prospectus is a part, or as an exhibit to the documents incorporated by reference. You may obtain copies of those documents as described in this prospectus under “Where You Can Find More Information.”

Neither the delivery of this prospectus nor any sale made hereunder implies that there has been no change in our affairs or that the information in this prospectus is correct as of any date after the date of this prospectus. You should not assume that the information in this prospectus, including any information incorporated in this prospectus by reference, an accompanying prospectus supplement, or any “free writing prospectus” we may authorize to be delivered to you, is accurate as of any date other than the date on the front cover of each of those documents. Our business, financial condition, results of operations, and prospects may have changed since that date.

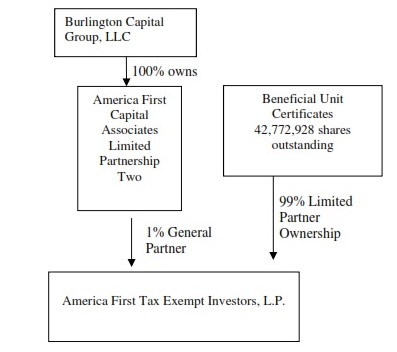

Throughout this prospectus, when we use the terms “we,” “us,” or the “Partnership,” we are referring to America First Multifamily Investors, L.P. References in this prospectus to our “General Partner” refer to America First Capital Associates Limited Partnership Two, whose general partner is Greystone AF Manager, LLC (“Greystone”). In addition, references in this prospectus to “Units” refer collectively to our BUCs and Series A Preferred Units, and references to our “Unitholders” refer collectively to the holders of our BUCs and Series A Preferred Units.

This prospectus contains or incorporates by reference certain forward-looking statements. All statements other than statements of historical facts contained in this prospectus, including statements regarding our future results of operations and financial position, business strategy, and plans and objectives of management for future operations, are forward-looking statements. When used, statements which are not historical in nature, including those containing words such as “anticipate,” “estimate,” “should,” “expect,” “believe,” “intend,” and similar expressions, are intended to identify forward-looking statements. We have based forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition, and results of operations. This prospectus also contains estimates and other statistical data made by independent parties and by us relating to market size and growth and other industry data. This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. We have not independently verified the statistical and other industry data generated by independent parties andwhich are contained in this prospectus and, accordingly, we cannot guarantee their accuracy or completeness. In addition, projections, assumptions and estimates of our future performance and the future performance of the industries in which we operate are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described under the headings “RISK FACTORS” beginning on page 9 of this prospectus and page 10 of our Annual Report on Form 10-K for the fiscal year ended December 31, 2012.

These forward-looking statements are subject, but not limited, to various risks and uncertainties, including but not limited to those relating to:

current maturities of our financing arrangements and our ability to renew or refinance such financing arrangements;

defaults on the mortgage loans securing our mortgage revenue bonds;

the competitive environment in which we operate; | |

risks associated with investing in multifamily and student residential properties and commercial properties, including changes in business conditions and the general economy;

changes in interest rates;

our ability to use borrowings or obtain capital to finance our assets;

local, regional, national, and international economic and credit market conditions;

recapture of previously issued Low Income Housing Tax Credits (“LIHTCs”) in accordance with Section 42 of the Internal Revenue Code;

changes in the United States Department of Housing and Urban Development’s (“HUD’s”) Capital Fund Program;

geographic concentration within the mortgage revenue bond portfolio held by the Partnership;

appropriations risk related to the funding of federal housing programs, including HUD Section 8; and

changes in the U.S. corporate tax code and other government regulations affecting our business.

Other risks, uncertainties, and factors, including those discussed in any supplement to this prospectus or in the reports that we file from time to time with the Securities and Exchange Commission (such as our Forms 10-K and 10-Q) could cause our actual results to differ materially from those projected in any forward-looking statements we make. We are not obligated to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise.

ABOUT AMERICA FIRST MULTIFAMILY INVESTORS, L.P.

Our Business

America First Tax Exempt Investors, L.P. The “Company” is the consolidation of the Partnership and its VIEs segment (as defined below).

We have been in operation since 1998 and as of June 30, 2013, owned 31 federally tax-exempt mortgage revenue bondsown 76 MRBs with an aggregate outstanding principal amount of approximately $229 million. These bonds$681.4 million as of September 30, 2019. The majority of these MRBs were issued by various state and local housing authorities in order to provide construction and/or permanent financing of 20 multifamily residential apartmentsfor 66 Residential Properties containing a total of 3,88010,871 rental units located in 13 states in the states of Florida, Illinois, Iowa, Kansas, Kentucky, Minnesota, North Carolina, Ohio, South Carolina, Tennessee, and Texas. In each caseUnited States. Each MRB for the Partnership owns, either directly or indirectly, 100% of the bonds issued for these properties. Each bondResidential Properties is secured by a mortgage or deed of trusttrust. One MRB is secured by a mortgage on the financed apartment property.ground, facilities, and equipment of a commercial ancillary health care facility in Tennessee. Each of the bondsMRBs provides for "base" interest payable at a fixed rate on a periodic basis. Additionally, five of the bonds also provide for the payment of contingent interest determined by the net cash flow and net capital appreciation of the underlying real estate properties. As a result, these mortgage revenue bonds provide the Partnership with the potential to participate in future increases in the cash flow generated by the financed properties, either through operations or from their ultimate sale. Of the 31 bonds owned, 12 are owned

We directly by the Partnership,own 13 MRBs, while seven MRBs are owned by ATAX TEBS I, LLC,LLC; 12 MRBs are owned by ATAX TEBS II, LLC; seven MRBs are owned by ATAX TEBS III, LLC; and 25 MRBs are owned by ATAX TEBS IV, LLC. Each of these entities is a special purpose entity owned and controlled by the Partnership created to facilitate a Tax Exempt Bond Securitization (“TEBS”) FinancingFinancings with Federal Home Loan Mortgage Corporation also known as "Freddie Mac"Freddie Mac. One MRB is securitized and sixheld by Deutsche Bank AG (“Deutsche Bank”) in a Term Tender Option Bond (“Term TOB”) facility. Five MRBs are securitized and held by Deutsche Bank ("DB"in Term A/B Trust financing facilities. One MRB is securitized and held by Morgan Stanley Bank, N.A. (“Morgan Stanley”) in a Term TOB facility. Five MRBs are securitized and held by Mizuho Capital Markets, LLC (“Mizuho”) in Tender Option Bond ("TOB Trust"(“TOB”) Trust financing facilities.

The ability of the properties collateralizingResidential Properties and the commercial property that collateralize our tax-exempt mortgage revenue bondsMRBs to make payments of base and contingent interest is a function of the net operating incomecash flow generated by these properties. Net operating incomecash flow from a multifamily or student residential property depends on the rental and occupancy rates of the property and the level of operating expenses. Occupancy rates and rents are directly affected by the supply of, and demand for, apartments in the market areas in which a property is located. This, in turn, is affected by several factors such as the requirement that a certain percentage of the rental units be set aside for tenants who qualify as persons of low to moderate income, local or national economic conditions, and the amount of new apartment construction and interest rates on single-family mortgage loans. Net cash flow from the commercial property depends on the number of cancer patients which utilize the cancer therapy center and the ability to hire and retain key employees to provide the related cancer treatment. In addition, factors such as government regulation, inflation, real estate and other taxes, labor problems, and natural disasters can affect the economic operations of the properties which collateralize the MRBs. The return we realize from our investments in MRBs depends upon the economic performance of the Residential Properties and the commercial property which collateralize these MRBs. We may be in competition with other residential rental properties and commercial properties located in the same geographic areas as the properties financed with our MRBs.

We may also make taxable property loans to Residential Properties which are financed by MRBs held by us. We do this to provide financing for capital improvements at these properties or to otherwise support property operations when we determine it is in our best long-term interest. We may also invest in other types of securities that may or may not be secured by real estate to the extent allowed by the Partnership Agreement. We also rely on

an exemption from registration under the Investment Company Act of 1940, which has certain restrictions on the types and amounts of securities owned by the Partnership.

Under the Partnership Agreement, any tax-exempt investments, other than MRBs, that are not secured by a direct or indirect interest in a property must be rated in one of the four highest rating categories by at least one nationally recognized securities rating agency. The Partnership’s acquisition of any tax-exempt investment or other investment may not cause the aggregate book value of such investments to exceed 25% of our assets at the time of acquisition. As of September 30, 2019, the Partnership owned three Public Housing Capital Fund Trusts Certificates (“PHC Certificates”). The PHC Certificates had an aggregate outstanding principal amount of approximately $44.9 million as of September 30, 2019. The PHC Certificates represent beneficial interests in three trusts (“PHC Trusts”). The PHC Certificates consist of custodial receipts evidencing loans made to numerous public housing authorities. Principal and interest on these loans are payable by the respective public housing authorities out of annual appropriations to the public housing authorities by HUD under HUD’s Capital Fund Program established under the Quality Housing and Work Responsibility Act of 1998 (the “Capital Fund Program”). The PHC Trusts have a first lien on these annual Capital Fund Program payments to secure the public housing authorities’ respective obligations to pay principal and interest on their loans. The PHC Certificates are securitized into three separate TOB Trust financing facilities with Mizuho.

As of September 30, 2019, we owned membership interests in nine unconsolidated entities (“Vantage Properties”). Our investments in the Vantage Properties are used to construct multifamily real estate properties. We do not have controlling interests in the Vantage Properties and account for the membership interests under the equity method of accounting. We earn a return on our membership interests accruing immediately on our contributed capital, which is guaranteed, up to a specified amount, through the second anniversary of construction completion by an unrelated third party. The limited membership interests entitle us to shares of certain cash flows generated by the Vantage Properties from operations and upon the occurrence of certain capital transactions, such as a refinancing or sale.

We may acquire ownership interests in multifamily and student apartment properties (“MF Properties”). As of September 30, 2019, we owned two MF Properties containing 859 rental units located in Nebraska and California. In addition, we may acquire real estate securing our MRBs through foreclosure in the event of a default. Net cash flow of our MF Properties depends on the rental and occupancy rates of the property and the level of operating expenses. Occupancy rates and rents are directly affected by the supply of, and demand for, apartments in the market areas in which a property is located. This, in turn, is affected by several factors such as local or national economic conditions, and the amount of new apartment construction and interest rates on single-family mortgage loans. In addition, factors such asloans, government regulation, inflation, real estate and other taxes, labor problems, and natural disasters can affect the economic operations of a property. Because the return to the Partnership from its investments in tax-exempt mortgage revenue bonds depends upon the economic performance of the multifamily residential properties which collateralize these bonds, the Partnership may be considered to be in competition with other multifamily rental properties located in the same geographic areas as the properties financed with its tax-exempt bonds.

Business Objectives and Strategy

Our business objectives are to (i) preserveacquiring, holding, selling, and protect our capital and (ii) provide regular and increasing cash distributions to our shareholders which are substantially exempt from federal income tax. We have sought to meet these objectives by primarily investing inotherwise dealing with a portfolio of tax-exempt mortgage revenue bonds that wereMRBs which have been issued to finance,provide construction and/or permanent financing for affordable multifamily, student housing, and are secured by first mortgages on, multifamily apartment properties, including student housing. Certain of these bonds may be structured to provide a potential for an enhanced federally tax-exempt yield through the payment of contingent interest, which is payable out of net cash flow from operations and net capital appreciation of the financed apartmentcommercial properties. For the years ended December 31, 2012, 2011, and 2010, the Partnership reported on its federal income tax return tax-exempt interest income as a percentage of total income of approximately 90%, 94%, and 89%. A shareholder’s tax form K-1 reported a similar percentage of tax-exempt income compared to total income assuming the shareholder owned the shares during the full calendar year.

We are pursuing a business strategy of acquiring additional MRBs and other investments, as permitted by the Partnership Agreement, on a leveraged basis to (i) increase the amount of interest available for distribution to our Unitholders; and (ii) reduce risk through interest rate hedging. We may finance the acquisition of additional tax-exempt mortgage revenue bondsMRBs and other investments through the reinvestment of cash flow,flows, the issuance of additional shares,BUCs or Series A Preferred Units, lines of credit, or securitization financing using our existing portfolio of tax-exempt mortgage revenue bonds.MRBs and other investments. Our current operating policy is to use securitizations or other forms of leverage to maintain a level of debt financing between 40% and 60%which will not exceed 75% of the total par value of our mortgage bond portfolio. At June 30, 2013,Partnership assets. The Partnership assets are defined as the leverage on the portfolio of the tax-exempt mortgage revenue bonds was approximately 60% of the par value of the portfolio.

In connection with our growth strategy, we are also assessingWe continually assess opportunities to reposition our existing portfolio of tax-exempt mortgage revenue bonds.MRBs. The principal objective of this repositioning initiativeassessment is to improve the quality and performance of our revenue bondMRB portfolio and, ultimately, increase the amount of cash available for distribution to our shareholders.Unitholders. In some cases, we may elect to redeem selected tax-exempt bonds that are secured by multifamily propertiesMRBs that have experienced significant appreciation. Through the selective redemption of the bonds,MRBs, a sale or refinancing of the underlying property will be required which, if sufficient sale or refinancing proceeds exist, may entitle the Partnership to receive payment of contingent interest on its bond investment.required. In other cases, we may elect to sell bondsMRBs on properties that are in stagnant or declining markets. The proceeds received from these transactions would be redeployed into other tax‑exempt investments consistent with our investment objectives.

We may also be able to use a higher-quality investment portfolio to obtain higher leverage to be used to acquire additional investments.

1. | Private activity bonds issued under Section 142(d) of the Internal Revenue |

2. | Bonds issued under Section 145 of the |

3. | Essential function bonds issued by a public instrumentality to finance |

4. | Existing “80/20 bonds” that were issued under Section 103(b)(4)(A) of the Internal Revenue Code of 1954. |

Each of these bond structures permits the issuance of tax-exempt bondsMRBs to finance the construction or acquisition and rehabilitation of affordable rental housing.housing or other not-for-profit commercial property. Under applicable Treasury Regulations, any affordable apartmentmultifamily residential project financed with MRBs that are purportedly tax-exempt bonds must set aside a percentage of its total rental units for occupancy by tenants whose incomes do not exceed stated percentages of the median income in the local area. In each case, the balance of the rental units in the apartmentmultifamily residential project may be rented at market rates.rates (unless otherwise restricted by local housing authorities). With respect to private activity bonds issued under Section 142(d) of the Internal Revenue Code, the owner of the apartmentmultifamily residential project may elect, at the time the bondsMRBs are issued, whether to set aside a minimum of 20% of the units for tenants making less than 50% of area median income (as adjusted for household size) or 40% of the units for tenants making less than 60% of the area median income (as adjusted for household size). Multifamily housing bondsThe MRBs that were secured by Residential Properties issued prior to the Tax Reform Act of 1986 (so called “80/20” bonds) require that 20% of the rental units be set aside for tenants whose income does not exceed 80% of the area median income, without adjustment for household size.

We expect that many of the private activity housing bondsMRBs that we evaluate for acquisition will be issued in conjunction with the syndication of LIHTCs by the owner of the financed apartmentmultifamily residential project. Additionally, to facilitate our investment strategy of acquiring additional tax-exempt mortgage bonds secured by MF Properties,MRBs, we may acquire ownership positions in the MF Properties. WeIn many cases, we expect to acquire tax-exempt mortgage revenue bondsMRBs on these MF Properties in many cases at the time of a restructuring of the MF PropertyProperty’s ownership. Such restructuring may involve the syndication of LIHTCs in conjunction with a property rehabilitation.

Additionally, we are continuing to pursue a business strategy of making equity investments in market-rate multifamily residential properties through non-controlling membership interests in unconsolidated entities. Our investments in unconsolidated entities are used to construct market-rate, multifamily real estate properties.

Investment Types

Residential Properties and the tax-exempt mortgage revenue bonds. commercial property whichcollateralize the MRBs. Net operating incomecash flow from a multifamily residential property depends on the rental and occupancy rates of the property and the level of operating expenses. The estimated fair valuesNet cash flow from the commercial property depends on the number of cancer patients that utilize the tax-exempt mortgage revenue bonds represent approximately 46% ofcancer therapy center and the total assets ofability to hire and retain key employees to provide the Partnership at June 30, 2013. The Partnership’s total assets exclude the VIE segment for purposes of this calculation.related cancer treatment.

Other Tax-Exempt Securities.

PHC Certificates")

Other Investments. We also have a reportable segment consisting of the PHC Certificates represent approximately 13%our ownership of the total assets of the Partnership at June 30, 2013. The Partnership’s total assets exclude the VIE segment for purposes of this calculation.

Property Loans.

MF PropertiesInterests in Real Property. While the Partnership generally does not seek to. We may acquire equitycontrolling interests in real property as long-termmultifamily, student or permanent investments, it may acquire real estate securing its revenue bonds or taxable mortgage loans through foreclosure insenior citizen residential properties. We plan to operate the event of a default. In addition, as part of its growth strategy, the Partnership may acquire direct or indirect interests in MF Properties on a temporary basis in order to position itselfourselves for a future investment in tax-exempt mortgage revenue bondsMRBs issued to finance the acquisition and/or substantial rehabilitation of such apartment complexesthe property by a new owner. A new owner would typically seek to obtain low income housing tax credits ("LIHTCs") in connection with the issuance of the new tax-exempt bonds, but if LIHTCs had previously been issued for the property, such a restructuring could not occuror until the expiration of a 15-year compliance period for the initial LIHTCs. The Partnership may acquire an interest in MF Properties prior to the end of the LIHTC compliance period. After the LIHTC compliance period, the Partnership would expectopportunity arises to sell its interest in such MF Propertythe properties at what we believe is their optimal fair value.

Investment Opportunities and Business Challenges

There continues to a new owner which could syndicate new LIHTCs and seek tax-exempt bond financing on the MF Property which the Partnership could acquire. Such restructurings will generally be expected to occur within 36 months of the acquisition by the Partnership of an interest in an MF Property. The Partnership will not acquire LIHTCs in connection with these transactions. The net real estate assets represent approximately 17% of the total assets of the Partnership at June 30, 2013. The Partnership’s total assets exclude the VIE segment for purposes of this calculation.

The National Councildemand for affordable housing by qualified potential residents whose income does not exceed 50-60% of State Housing Agencies Fact Sheetthe area median income continues to increase. Government programs that provide direct rental support to residents has not kept up with the demand, therefore programs that support private sector development and HUDsupport for affordable housing through MRBs, tax credits, and grant funding to developers have captured some key scale metrics and opportunities of this market:

In addition to tax-exempt revenue bonds,MRBs, the federal government promotes affordable housing through the use ofusing LIHTCs for affordable multifamily rental housing. The syndication and sale of LIHTCs along with tax-exempt bondMRB financing is attractive to developers of affordable housing because it helps them raise equity and debt financing for their projects. Under this program, developers that receive an allocation of private activity bonds will also receive an allocation of federal LIHTCs as a method to encourage the development of affordable multifamily housing. The Partnership doesWe do not invest in LIHTCs but isare attracted to tax-exempt mortgage revenue bondsMRBs that are issued in association with federal LIHTC syndications because in order to be eligible for federal LIHTCs a property must either be newly constructed or substantially rehabilitated and therefore, may be less likely to become functionally obsolete in the near term than an older property. There are various requirements in order to be eligible for federal LIHTCs, including rent and tenant income restrictions. In general, the property owner must elect to set aside either 40% or more of the property’s residential units for occupancy by individualshouseholds whose income is 60% or less (adjusted for family size) of the area median gross income or 20% or more of the property’s residential units for occupancy by individualshouseholds whose income is 50% or less (adjusted for family

size) of the area median gross income. These units remain subject to these set aside requirements for a minimum of 30 years.

The inability to access debt financing may result in adverse effects on our financial condition and results of operations. There can be no assurance that we will be able to finance additional acquisitions of tax-exempt mortgage revenue bondsMRBs or other investments through

Since 2016, we have identified, and owned, membership interests in eleven Vantage Properties. These investments in the form of lower occupancy. While some properties have been negatively effected, the overall economic occupancy (which is adjusted to reflect rental concessions, delinquent rents and non-revenue units such as model units and employee units) of the apartment properties that the Partnership has financed with tax-exempt mortgage revenue bonds was approximately at 86% during 2012 as compared to 85% during 2011. Overall economic occupancy of the MF Properties has remained the same at approximately 76% during 2012 and 2011. Based on the growth statistics in the market, we expect to see continued improvement in property operations and profitability in 2013 and 2014 and we believe that rental rate and occupancy trends will continue to be positive.

General Information

The Partnership was formed on April 2, 1998 under the Delaware Revised Uniform Limited Partnership Act.Act (the “Delaware LP Act”). The operations of the Partnership are conducted pursuant to the terms and conditions of itsthe Partnership Agreement. See “TERMS OF THE PARTNERSHIP AGREEMENT.“The Partnership Agreement”

Our general partner is America First Capital Associates Limited Partnership 2Two (the “General Partner”), whose general partner is Greystone. Greystone is an affiliate of Greystone & Co., Inc., which, together with its affiliated companies, is a subsidiary of The Burlington Capital Group L.L.C. (“Burlington”). Since 1984, Burlington (which was known as America First Companies L.L.C. until 2005) has specialized in the management of investment funds, many of which were formed to acquire real estate investments such as tax-exempt mortgage revenue bonds, mortgage securitieslending, investment, and multifamily real estate properties. Our sole limited partner is America First Fiduciary Corporation Number Five, a Nebraska corporation. Our shares, which are referred to as “beneficial unit certificates” or “BUCs” in the Partnership Agreement, represent assignments by the sole limited partner of its rights and obligationsadvisory company with an established reputation as a limited partner.

We are a partnership for federal income tax purposes. This means that we do not pay federal income taxes on our income. Instead, all of our profits and losses are allocated to our partners, including the holders of shares,BUCs, under the terms of our Partnership Agreement. See “U.S. Federal Income Tax Considerations” beginning on page 18. In addition, a majority of our income consists of tax‑exemptwhat we believe and expect to be tax-exempt interest income. See “U.S. FEDERAL INCOME TAX CONSIDERATIONS.”

Our principal executive office isoffices are located at 1004 Farnam Street, Suite 400, Omaha, Nebraska 68102, and our telephone number is (402) 444-1630. We maintain a website at www.ataxfund.com,, where certain information about the Partnership is available. The information found on, or accessible through, our website is not incorporated into, and does not form a part of, this prospectus, any accompanying prospectus supplement or any other report or document we file with or furnish to the SEC.

Our initial limited partner, which has the General Partner, which is managed by its general partner, Burlington. The persons acting as the Board of Managers and executive officers of Burlington act as the directors and executive officersobligation to perform certain actions on behalf of the Partnership. Certain services are provided to the Partnership by other employees of Burlington and the Partnership reimburses Burlington for its allocated share of these salaries and benefits. The Partnership is not charged, and does not reimburse Burlington, for the services performed by executive officers of Burlington. As a result, the Partnership does not pay compensation of any nature to the persons who effectively act as its executive officers. Accordingly, the Partnership does not provide tabular disclosures regarding executive compensation, compensation discussion and analysis, a compensation committee report or information regarding compensation committee interlocks in the reports it files with the SEC.

For additional information about our business, properties, and financial condition, please refer to the documents cited in an amount equal to 0.45% per annum“Where You Can Find More Information.”

An investment in our securities involves risks. Additionally, limited partner interests are inherently different from the capital stock of a corporation, although many of the principal amount of the revenue bonds, other tax-exempt investments and taxable mortgage loans held by the Partnership. Six of the tax-exempt revenue bonds held by the Partnership provide for the payment of this administrative feebusiness risks to the General Partner by the owner of the financed property. When the administrative fee is payablewhich we are subject are similar to those that would be faced by a property owner, it is subordinated to the payment of all base interest to the Partnership on the tax-exempt revenue bond secured by that property. The Partnership Agreement provides that the administrative fee will be paid directly by the Partnership with respect to any investments for which the administrative fee is not payable by the property owner or a third party. In addition, the Partnership Agreement provides that the Partnership will pay the administrative fee to the General Partner with respect to any foreclosed mortgage bonds.

securities. If any of thethese risks discussed in this prospectus or such prospectus supplement actuallywere to occur, our business, financial condition, andor results of operations could be materially adversely affected. If this were to occur, the amount of cash distributions we pay on the shares may be reduced,In that case, the trading price of the sharesour BUCs could decline and you maycould lose all or part of your investment.

Unless we inform you otherwise in a supplement to this prospectus, we intend to use the net proceeds to us from the sale of any particular offering of securities covered by this offering primarilyprospectus to acquire additional tax-exempt mortgage revenue bonds secured by multifamily apartment propertiesMRBs and other investments meeting our investment criteria. Any remaining net proceeds will be used for general business purposes, including reduction in our indebtedness.

General

The rights and obligations of shareholdersUnitholders and the General Partner are set forth in the Partnership Agreement. The following is a summary of the material provisions of the Partnership Agreement. This summary does not purport to be complete and is subject to, and qualified in its entirety by, the terms of the Partnership Agreement, which is incorporated by reference into the registration statement of which this prospectus.

Organization and Duration

The Partnership was organized in 1998 and has a perpetual existence.

Purpose

The purpose of the Partnership under the Partnership Agreement is to engage directly in, or enter into or form, hold, and dispose of any corporation, partnership, joint venture, limited liability company, or other arrangement to engage indirectly in, any business activity that is approved by the General Partner and that lawfully may be conducted by a limited partnership organized under the Delaware LP Act, and do anything necessary or appropriate to the foregoing. In this regard, the purpose of the Partnership includes, without limitation, the acquisition, holding, selling, and otherwise dealing with MRBs and other instruments backed by multifamily residential properties, and other investments as determined by the General Partner.

Management

Management by General Partner

Under the terms of the Partnership Agreement, the General Partner has full, complete, and exclusive authority to manage and control the business affairs of the Partnership. Such authority specifically includes, but is not limited to, the power to (i) acquire, hold, refund, reissue, remarket, securitize, transfer, foreclose upon, sell or otherwise deal with the investments of the Partnership, (ii) issue additional shares,Units and other Partnership securities, borrow money, and issue evidences of indebtedness, and (iii) apply the proceeds from the sale or the issuance of additional sharesUnits or other Partnership securities to the acquisition of additional revenue bondsMRBs (and associated taxable mortgages) and other types of investments meeting the Partnership’s investment criteria.criteria, (iv) issue options, warrants, rights, and other equity instruments relating to Units under employee benefit plans and executive compensation plans maintained or sponsored by the Partnership and its affiliates, (v) issue Partnership securities in one or more classes or series with such designations, preferences, rights, powers, and duties, which may be senior to existing classes and series of Partnership securities, including BUCs, and (vi) engage in spin-offs and other similar transactions, and otherwise transfer or dispose of Partnership assets pursuant to such transactions. The Partnership Agreement provides that the General Partner and its affiliates may and shall have the right to provide goods and

services to the Partnership subject to certain conditions. The Partnership Agreement also imposes certain limitations on the authority of the General Partner, including restrictions on the ability of the General Partner to dissolve the Partnership without the consent of a majority in interest of the shareholders.

Other than certain limited voting rights discussed under “VOTING RIGHTS,“Voting Rights of Unitholders,” the shareholdersBUC holders do not have any authority to transact business for, or participate in the management of, the Partnership. The only recourse available to shareholdersBUC holders in the event that the General Partner takes actions with respect to the business of the Partnership with which shareholdersBUC holders do not agree is to vote to remove the General Partner and admit a substitute general partner. See “Removal“Withdrawal or WithdrawalRemoval of the General Partner”Partner” below.

Change of Management Provisions

The Partnership Agreement contains provisions that are intended to discourage any person or group from attempting to remove the General Partner or otherwise changing the Partnership’s management, and thereby achieve a takeover of the Partnership, without first negotiating such acquisition with the Board of Managers of Greystone. In this regard, the Partnership Agreement provides that if any person or group (other than the General Partner and its affiliates) acquires beneficial ownership of 20% or more of any class of Partnership securities (including BUCs), that person or group loses voting rights with respect to all of his, her, or its securities and such securities will not be considered “outstanding” for voting or notice purposes, except as required by law. This loss of voting rights will not apply to any person or group that acquires the securities from the General Partner or its affiliates and any transferees of that person or group approved by the General Partner, or to any person or group who acquires the securities with the prior approval of the Board of Managers of Greystone.

In addition, the Partnership Agreement provides that, under circumstances where the General Partner withdraws without violating the Partnership Agreement or is removed by the BUC holders without cause, the departing General Partner will have the option to require the successor general partner to purchase the general partner interest of the departing General Partner and its general partner distribution rights for their fair market value. See “Withdrawal or Removal of the General Partner” below.

Issuance of Partnership Securities

General

As of the date of this prospectus, other than the interest of the General Partner in the Partnership, our only outstanding Partnership securities are the BUCs and the Series A Preferred Units representing limited partnership interests in the Partnership. The Partnership Agreement provides that the General Partner may cause the Partnership to issue additional Units from time to time on such terms and conditions as it shall determine. In addition, subject to certain approval rights of the holders of Series A Preferred Units for issuances adversely affecting the Series A Preferred Units, the Partnership Agreement authorizes the General Partner to issue additional limited partnership interests and other Partnership securities in one or more classes or series with such designations, preferences, rights, powers, and duties, which may be senior to existing classes and series of Partnership securities, including BUCs, as determined by the General Partner without the approval of Unitholders.

It is possible that we will fund acquisitions of our investments and other business operations through the issuance of additional BUCs, Series A Preferred Units, or other equity securities. The holders of Units do not have a preemptive right to acquire additional BUCs, Series A Preferred Units, or other Partnership securities. All limited partnership interests issued pursuant to and in accordance with the Partnership Agreement are considered fully paid and non-assessable limited partnership interests in the Partnership.

Series A Preferred Units

Holders of the Series A Preferred Units are entitled to receive, when, as, and if declared by the General Partner out of funds legally available for the payment of distributions, non-cumulative cash distributions at the rate of 3.00% per annum of the $10.00 per unit purchase price of the Series A Preferred Units, payable quarterly. In the event of any liquidation, dissolution, or winding up of the Partnership, the holders of the Series A Preferred Units

are entitled to a liquidation preference in connection with their investments in an amount equal to $10.00 per Series A Preferred Unit, plus an amount equal to all distributions declared and unpaid thereon to the date of final distribution.

With respect to anticipated quarterly distributions and rights upon liquidation, dissolution, or the winding-up of the Partnership’s affairs, the Series A Preferred Units rank senior to the BUCs and to any other class or series of Partnership interests or securities expressly designated as ranking junior to the Series A Preferred Units, and junior to any other class or series of Partnership interests or securities expressly designated as ranking senior to the Series A Preferred Units. The Series A Preferred Units have no stated maturity, are not subject to any sinking fund requirements, and will remain outstanding indefinitely unless repurchased or redeemed by the Partnership. Upon the sixth anniversary of the closing of the sale of Series A Preferred Units to a holder thereof, and upon each anniversary thereafter, each holder of Series A Preferred Units will have the right to redeem, in whole or in part, the Series A Preferred Units held by such holder at a per unit redemption price equal to $10.00 per unit plus an amount equal to all declared and unpaid distributions. Holders of Series A Preferred Units have no voting rights except for limited voting rights relating to issuances of Partnership securities adversely affecting the Series A Preferred Units.

Cash Distributions

General

The Partnership Agreement provides that all Net Interest Income generated by the Partnership that is not contingent interest will be distributed 99% to shareholdersthe limited partners and BUC holders as a class and 1% to the General Partner. During the years ended December 31, 20122018 and 2011,2017, the General Partner received total distributions of Net Interest Income of approximately $180,000$166,000 and $155,000,$194,000, respectively. In addition, the Partnership Agreement provides that the General Partner is entitled to 25% of Net Interest Income representing contingent interest up to a maximum amount equal to 0.9% per annum of the principal amount of all mortgage bonds held by the Partnership, as the case may be. During the year ended December 31, 2011, the General Partner received total distributions of Net Interest Income representing contingent interest of approximately $310,000. The General Partner did not receive any distributions of Net Interest Income representing contingent interest in 2012.

Interest Income of the Partnership includes all cash receipts, except for (i) capital contributions, (ii) Residual Proceeds (defined below), or (iii) the proceeds of any loan or the refinancing of any loan. “Net Interest Income” of the Partnership means all Interest Income plus any amount released from the PartnershipPartnership’s reserves for distribution, less expenses and debt service payments and any amount deposited in reserve or used or held for the acquisition of additional investments.

The Partnership Agreement provides that Net Residual Proceeds (whether representing a return of principal or contingent interest) will be distributed 100% to the shareholders,limited partners and BUC holders as a class, except that 25% of Net Residual Proceeds representing contingent interest will be distributed to the General Partner until it receives a maximum amount per annum (when combined with all distributions to it of Net Interest Income representing contingent interest during the year) equal to 0.9% of the principal amount of the Partnership’sPartnership’s mortgage bonds. Under the terms of the Partnership Agreement, “Residual Proceeds”“Residual Proceeds” means all amounts received by the Partnership upon the sale of any asset or from the repayment of principal of any bond. “Net“Net Residual Proceeds”Proceeds” means, with respect to any distribution period, all Residual Proceeds received by the Partnership during such distribution period, plus any amounts released from reserves for distribution, less all expenses that are directly

The General Partner received total distributions of Net Interest Income representing contingent interest and Net Residual Proceeds of approximately $2.1 million and $2.0 million during each of the years ended December 31, 20122018 and 2011, distributions2017, respectively.

With respect to the cash available for distribution to the limited partners, and subject to the preferential rights of Net Residual Proceeds were madethe holders of any class or series of our Partnership securities ranking senior to the Series A Preferred Units

with respect to distribution rights, holders of Series A Preferred Units are entitled to receive, when, as, and if declared by the Partnership to the General Partner totaling approximately $658,000 and $169,000, respectively.

Distributions Upon Liquidation

Upon the dissolution of the Partnership, the proceeds from the liquidation of its assets will be first applied to the payment of the obligations and liabilities of the Partnership and the establishment of any reservereserves therefor as the General Partner determines to be necessary, and then distributed to the partners (including both the General Partner and the shareholderslimited partners) and Unitholders in proportion to, and to the extent of, their respective capital account balances, and then in the same manner as Net Residual Proceeds.

Timing of Cash Distributions

The Partnership currently makes quarterly cash distributions to shareholders.BUC holders. However, the Partnership Agreement allows the General Partner to elect to make cash distributions on a more or less frequent basis provided that distributions are made at least semiannually. Regardless of the distribution period selected by the General Partner, cash distributions to BUC holders must be made within 60 days of the end of each such period.

Allocation of Income and Losses

Income and losses from operations will be allocated 99% to the shareholderslimited partners and BUC holders as a class and 1% to the General Partner. Income arising from a sale of or liquidation of the Partnership’s assets will be first allocated to the General Partner in an amount equal to the Net Residual Proceeds or liquidation proceeds distributed to the General Partner from such transaction, and the balance will be distributedallocated to the shareholders.limited partners and Unitholders as a class. Losses from a sale of a property or from a liquidation of the Partnership will be allocated among the General Partner and the shareholderspartners in the same manner as the Net Residual Proceeds or liquidation proceeds from such transaction are distributed.

Determination of Allocations to Unitholders

Income and losses will be allocated on a monthly basis to the shareholdersUnitholders of record as of the last day of a month. If a shareholderUnitholder is recognized as the record holder of sharesUnits on such date, such shareholderUnitholder will be allocated all income and losses for such month.

Cash distributions will be made to the shareholdersBUC holders of record as of the last day of each distribution period. If the Partnership recognizes a transfer prior to the end of a distribution period, the transferee will be deemed to be the holder for the entire distribution period and will receive the entire cash distribution for such period. Accordingly, if the General Partner selects a quarterly or semiannual distribution period, the transferor of sharesBUCs during such a distribution period may be recognized as the record holder of the sharesBUCs at the end of one or more months during such period and be allocated income or losses for such months but not be recognized as the record holder of the sharesBUCs at the end of the period and, therefore, not be entitled to a cash distribution for such period.

Distributions to the holders of Series A Preferred Units are made quarterly in arrears on the 15th day of the first month of each calendar quarter.

The General Partner retains the right to change the method by which income and losses of the Partnership will be allocated between buyers and sellers of sharesUnits during a distribution period based on consultation with tax counsel and accountants. However, no change may be made in the method of allocation of income or losses without written notice to the shareholdersUnitholders at least 10 days prior to the proposed effectiveness of such change unless otherwise required by law.

Payments to the General Partner

Fees

In addition to its share of Net Interest Income and Net Residual Proceeds and reimbursement for expenses, the General Partner will beis entitled to an administrative fee in an amount equal to 0.45% per annum of the principal amount of the revenue bonds,MRBs, other tax-exempt investments, and taxable mortgage loans held by the Partnership. In general, the

Reimbursement of Expenses

In addition to the allocation of profits, lossescash distributions and cash distributionsfee payments to the General Partner described above, the Partnership will reimburse the General Partner or its affiliates on a monthly basis for the actual out‑of‑pocketout-of-pocket costs of direct telephone and travel expenses incurred in connection with the business of the Partnership, direct out‑of‑pocketout-of-pocket fees, expenses, and charges paid to third parties for rendering legal, auditing, accounting, bookkeeping, computer, printing, and public relations services, expenses of preparing and distributing reports to shareholders,limited partners and BUC holders, an allocable portion of the salaries and fringe benefits of non-officer employees of Burlington,the general partner of the General Partner, insurance premiums (including premiums for liability insurance that will cover the Partnership and the General Partner and Burlington)Partner), the cost of compliance with all state and federal regulatory requirements and NASDAQ listing fees and charges, and other payments to third parties for services rendered to the Partnership. The General Partner will also be reimbursed for any expenses it incurs acting as the partnership representative (or tax matters partnerpartner) for tax purposes for the Partnership. The Partnership will not reimburse the General Partner or its affiliates for the travel expenses of the president of Burlingtonthe general partner of the General Partner or for any items of general overhead. The Partnership will not reimburse the General Partner or Burlingtonits general partner for any salaries or fringe benefits of any of the executive officers of Burlington. The Partnership’s independent accountants are required to verify that any reimbursements received bythe general partner of the General Partner from the Partnership were for expenses incurred by the General Partner or its affiliates in connection with the conduct of the business and affairs of the Partnership or the acquisition and management of its assets and were otherwise permissible reimbursements under the terms of the Partnership Agreement.Partner. The annual report to shareholdersUnitholders is required to itemize the amounts reimbursed to the General Partner and its affiliates.

Payments for Goods and Services

The Partnership Agreement provides that the General Partner and its affiliates may provide goods and services to the Partnership. The provision of any goods and services by the General Partner or its affiliates to the Partnership must be part of their ordinary and ongoing business in which it or they have previously engaged, independent of the activities of the Partnership, and such goods and services shall be reasonable for and necessary to the Partnership, shall actually be furnished to the Partnership, and shall be provided at the lower of the actual cost of such goods or services or the competitive price charged for such goods or services for comparable goods and services by independent parties in the same geographic location. All goods and services provided by the General Partner or any affiliates must be rendered pursuant to the terms of the Partnership Agreement or a written contract containing a clause allowing termination without penalty on 60 days’ notice to the General Partner by the vote of the majority in interest of the shareholders. PaymentBUC holders. Any payment made to the General Partner or any affiliate for goods and

services must be fully disclosed to shareholders. all limited partners and BUC holders. The General Partner does not currently provide goods and services to the Partnership other than its services as General Partner. If the Partnership acquires ownership of any property through foreclosure of a revenue bond, an affiliate ofMRB, the General Partner or an affiliate may provide property management services for such property and, in such case, the Partnership will pay such party its fees for such services. Under the Partnership Agreement, such property management fees may not exceed the lesser of (i) the fees charged by unaffiliated property managers in the same geographic area, or (ii) 5% of the gross revenues of the managed property.

Liability of Partners and Shareholders

Under the Delaware Revised Uniform Limited PartnershipLP Act (the “Delaware LP Act”)and the terms of the Partnership Agreement, the General Partner will be liable to third parties for all general obligations of the Partnership to the extent not paid by the Partnership. However, the Partnership Agreement provides that the General Partner has no liability to the Partnership for any act or omission reasonably believed to be within the scope of authority conferred by the Partnership Agreement and in the best interest of the Partnership. The Partnership providedAgreement also provides that, except as otherwise expressly set forth in the course of conduct giving risePartnership Agreement, the General Partner does not owe any fiduciary duties to the threatened, pending or completed claim, action or suit did not constitute fraud, bad faith, negligence, misconduct or a breach of its fiduciary obligations to the shareholders.limited partners and BUC holders. Therefore, shareholdersUnitholders may have a more limited right of action against the General Partner than they would have absent those limitations in the Partnership Agreement. The Partnership Agreement also provides for indemnification of the General Partner and its affiliates by the Partnership for certain liabilities that the General Partner and its affiliates may incur under the Securities Act of 1933, as amended, and in dealingsconnection with the Partnership and third parties on behalfbusiness of the Partnership.Partnership; provided that no indemnification will be available to the General Partner and/or its affiliates if there has been a final judgment entered by a court determining that the General Partner’s and/or affiliate’s conduct for which indemnification is requested constitutes fraud, bad faith, gross negligence, or willful misconduct. To the extent that the provisions of the Partnership Agreement include indemnification for liabilities arising under the Securities Act of 1933, as amended, such provisions are, in the opinion of the SEC, against public policy and, therefore, unenforceable.

No shareholderUnitholder will be personally liable for the debts, liabilities, contracts, or any other obligations of the Partnership unless, in addition to the exercise of his or her rights and powers as a shareholder,Unitholder, he or she takes part in the control of the business of the Partnership. It should be noted, however, that the Delaware LP Act prohibits a limited partnership from making a distribution that causes the liabilities of the limited partnership to exceed the fair value of its assets. Any limited partner who receives a distribution knowing that the distribution was made in violation of this provision of the Delaware LP Act is liable to the limited partnership for the amount of the distribution. This provision of the Delaware LP Act probablylikely applies to shareholders as well as to the sole limited partner of the Partnership.Unitholders. In any event, the Partnership Agreement provides that to the extent our soleinitial limited partner is required to return any distributions or repay any amount by law or pursuant to the Partnership Agreement, each shareholderBUC holder who has received any portion of such distributions is required to repay his or her proportionate share of such distribution to our soleinitial limited partner immediately upon notice by the soleinitial limited partner to such shareholder.BUC holder. Furthermore, the Partnership Agreement allows the General Partner to withhold future distributions to shareholdersBUC holders until the amount so withheld equals the amount required to be returned by the soleinitial limited partner. Because sharesBUCs are transferable, it is possible that distributions may be withheld from a shareholderBUC holder who did not receive the distribution required to be returned.

Voting Rights

The Partnership Agreement provides that the soleinitial limited partner will vote its limited partnership interests as directed by the shareholders.BUC holders. Accordingly, except as described below regarding a person or group owning 20% or more of any class of Partnership securities then outstanding, the shareholders,BUC holders, by vote of a majority in interest thereof,of the outstanding BUCs, may:

(i) | amend the Partnership Agreement (provided that the concurrence of the General Partner is required for any amendment that modifies the compensation or distributions to which the General Partner is entitled or that affects the duties of the General Partner); |

(ii) | approve or disapprove the |

(iv) | elect a successor general partner; and |

(v) | terminate an |

In addition, subject to the provisions of the Partnership Agreement regarding removal of the General Partner (described below), the BUC holders holding at least 662/3% of the outstanding BUCs may remove the General Partner.

Each limited partner and BUC holder that has voting rights under the Partnership Agreement is entitled to cast one vote for each unit of limited partnership interest such person owns. However, if any person or group (other than the General Partner and its affiliates) acquires beneficial ownership of 20% or more of any class of Partnership securities (including BUCs), that person or group loses voting rights with respect to all of his, her, or its securities and such securities will not be considered “outstanding” for voting or notice purposes, except as required by law. This loss of voting rights will not apply to any person or group that acquires the Partnership securities from the General Partner or its affiliates and any transferees of that person or group approved by the General Partner, or to any person or group who acquires the securities with the prior approval of the board of managers of the general partner of the General Partner.

The holders of Series A Preferred Units have no voting rights under the Partnership Agreement, except with respect to any amendment to the Partnership Agreement that would have a material adverse effect on the existing terms of the Series A Preferred Units, and with respect to the creation or issuance of any Partnership securities that are senior to the Series A Preferred Units. Other than as set forth above, the holders of Series A Preferred Units have no voting rights under the Partnership Agreement on any matter that may come before the BUC holders for a vote. The approval of any of the matters for which the Series A Preferred Units have voting rights requires the affirmative vote or consent of the holders of a majority of the outstanding Series A Preferred Units. For any matter described in this paragraph for which the Series A Preferred Unit holders are entitled to vote, such holders are entitled to one vote for each Series A Preferred Unit held.

The General Partner may at any time call a meeting of the shareholders,limited partners and BUC holders, call for a vote without a meeting of the shareholderslimited partners and BUC holders, or otherwise solicit the consent of the shareholderslimited partners and BUC holders, and is required to call such a meeting or vote or solicit consents following receipt of a written request therefor signed by 10% or more in interest of the shareholders.outstanding limited partnership interests. The Partnership does not intend to hold annual or other periodic meetings of shareholders. Although the Partnership Agreement permits the consentany of the shareholders to be given after the act is done with respect to which the consent is solicited, the General Partner does not intend to act without the prior consent of the shareholders, in such cases where consent of the shareholders is required, except in extraordinary circumstances where inaction may have a material adverse effect on the interest of the shareholders.

Reports

Within 120 days after the end of the fiscal year, the General Partner will distribute a report to shareholdersUnitholders that shall include (i) financial statements of the Partnership for such year that have been audited by the Partnership’s independent public accountant, (ii) a report of the activities of the Partnership during such year, and (iii) a statement (which need not be audited) showing distributions of Net Interest Income and Net Residual Proceeds. The annual report will also include a detailed statement of the amounts of fees and expense reimbursements paid to the General Partner and its affiliates by the Partnership during the fiscal year.

Within 60 days after the end of the first three quarters of each fiscal year, the General Partner will distribute a report that shall include (i) unaudited financial statements of the Partnership for such quarter, (ii) a report of the activities of the Partnership during such quarter, and (iii) a statement showing distributions of Net Interest Income and Net Residual Proceeds during such quarter.

The Partnership will also provide shareholdersUnitholders with a report on Form K‑1K-1 or other information required for federal and state income tax purposes within 75 days of the end of each year.

The General Partner may not withdraw voluntarily from the Partnership or sell, transfer, or assign all or any portion of its interest in the Partnership unless a substitute general partner has been admitted in accordance with the terms of the Partnership Agreement. With the consent of a majority in interest of the shareholders,BUC holders, the General Partner may at any time designate one or more persons as additional general partners, provided that the interests of the shareholderslimited partners and BUC holders in the Partnership are not reduced thereby. The designation must meet the conditions set out in the Partnership Agreement and comply with the provisions of the Delaware LP Act with respect to admission of an additional general partner. In addition to the requirement that the admission of a person as successor or additional general partner have the consent of the majority in interest of the shareholders,BUC holders, the Partnership Agreement requires, among other things, that (i) such person agree to and execute the Partnership Agreement, and (ii) counsel for the Partnership or shareholders renderthe General Partner (or any of the General Partner’s affiliates) renders an opinion that such person’s admission would not result in the loss of limited liability of any limited partner or BUC holder or cause the Partnership or any of its affiliates to be taxed as a corporation or other entity under U.S. federal tax law.

With respect to the removal of the General Partner, the Partnership Agreement provides that the General Partner may not be removed unless that removal is approved by a vote of the holders of not less than 662/3% of the outstanding BUCs, including BUCs held by the General Partner and its affiliates, voting together as a single class, and the Partnership receives an opinion of counsel regarding limited liability and tax matters. Any removal of the General Partner also will be subject to the approval of a successor general partner by the vote of a majority in accordance withinterest of the Delaware LP Act.

In addition, the Partnership Agreement provides that, under circumstances where the General Partner withdraws without violating the Partnership Agreement or is removed by the BUC holders without cause, the departing General Partner will have the option to require the successor general partner to purchase the general partner interest of the departing General Partner and its general partner distribution rights for their fair market value. This fair market value will be determined by agreement between the departing General Partner and the successor general partner. If no such agreement is reached, an independent investment banking firm or other independent expert selected by the departing General Partner and successor general partner will determine the fair market value. If the departing General Partner and successor general partner cannot agree upon an expert, then an expert chosen by agreement of the experts selected by each of them will determine the fair market value. If the option described above is not exercised, the departing General Partner’s interest and general partner distribution rights will automatically convert into BUCs equal to the fair market value of those interests as determined by an investment banking firm or other independent expert selected in the manner described above.