As filed with the Securities and Exchange Commission on July 10, 2017

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION ON JULY 30, 1996

REGISTRATION NO. 333-06693

- -------------------------------------------------------------------------------

- -------------------------------------------------------------------------------

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON,

Washington, D.C. 20549

----------------

AMENDMENT NO. 1

TO

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

----------------

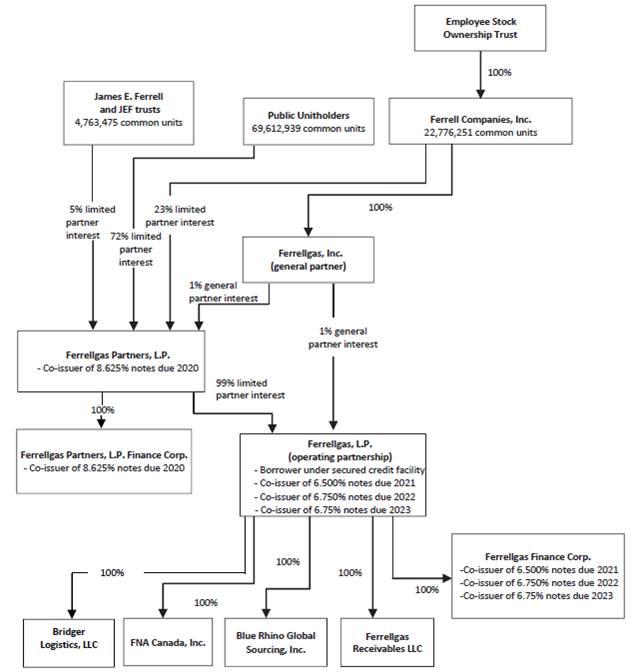

FERRELLGAS PARTNERS, L.P.

FERRELLGAS PARTNERS FINANCE CORP.

FERRELLGAS, L.P.

(EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER)

DELAWARE 5984 43-1698480

(STATE OR OTHER (PRIMARY STANDARD 43-1742520

JURISDICTION INDUSTRIAL 43-1698481

OF INCORPORATION OR CLASSIFICATION CODE (I.R.S. EMPLOYER

ORGANIZATION) NUMBER) IDENTIFICATION NO.)

----------------

ONE LIBERTY PLAZA

LIBERTY, MISSOURI 64068

(816) 792-1600

(ADDRESS, INCLUDING ZIP CODE, AND TELEPHONE NUMBER, INCLUDING AREA CODE, OF

REGISTRANT'S PRINCIPAL EXECUTIVE OFFICES)

----------------

DANLEY K. SHELDON

SENIOR VICE PRESIDENT

FERRELLGAS, INC.

ONE LIBERTY PLAZA

LIBERTY, MISSOURI 64068

(816) 792-1600

(NAME, ADDRESS, INCLUDING ZIP CODE, AND TELEPHONE NUMBER, INCLUDING AREA CODE,

OF AGENT FOR SERVICE)

----------------

(Exact name of registrants as specified in their charters)

Delaware | 5900 | 43-1698480 | ||

Delaware | 5900 | 43-1742520 | ||

(State or other jurisdictions of | (Primary Standard Industrial | (I.R.S. Employer |

7500 College Boulevard, Suite 1000, Overland Park, Kansas 66210

(913) 661-1500

(Address, including zip code, and telephone number, including area code, of the registrants’ principal executive offices)

Alan C. Heitmann

Executive Vice President; Chief Financial Officer; Treasurer

Ferrellgas, Inc.

7500 College Boulevard, Suite 1000, Overland Park, Kansas 66210

(913) 661-1500

(Name, address, including zip code, and telephone number, including area code, of the registrants’ agent for service)

Copies to:

KENDRICK T. WALLACE, ESQ

BRYAN CAVE

Charles H. Still, Jr.

Bracewell LLP

1200 MAIN STREET, SUITE 3500

KANSAS CITY, MISSOURI 64105

(816) 374-3200

----------------

APPROXIMATE DATE OF COMMENCEMENT OF PROPOSED SALE TO THE PUBLIC:

711 Louisiana Street, Suite 2300

Houston, Texas 77002

Telephone: (713) 221-3309

Approximate date of commencement of proposed sale of the securities to the public:

As soon as practicable afterfollowing the effective dateeffectiveness of this Registration Statement.

registration statement.

If any of the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. [_]

o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrants are a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Ferrellgas Partners, L.P.

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

Ferrellgas Partners Finance Corp.

Large accelerated filer o | Accelerated filer o | Non-accelerated filer x | Smaller reporting company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. o

CALCULATION OF REGISTRATION FEE

|

|

|

|

|

|

|

|

|

|

Title of each class of securities |

| Amount to be |

| Proposed maximum |

| Proposed maximum aggregate |

| Amount of |

|

85/8% Senior Notes due 2020 |

| $175,000,000 |

| 100% |

| $175,000,000 |

| $20,282.50 |

|

(1)Calculated pursuant to Rule 457(f) under the Securities Act of 1933, as amended.

THE REGISTRANTREGISTRANTS HEREBY AMENDSAMEND THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL THE REGISTRANTS SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(A)8(a) OF THE SECURITIES ACT OF 1933, AS AMENDED, OR UNTIL THETHIS REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE SECURITIES AND EXCHANGE COMMISSION, ACTING PURSUANT TO SAIDSUCH SECTION 8(A)8(a), MAY DETERMINE.

- -------------------------------------------------------------------------------

- -------------------------------------------------------------------------------

FERRELLGAS PARTNERS, L.P.

FERRELLGAS PARTNERS FINANCE CORP.

FERRELLGAS, L.P.

CROSS REFERENCE SHEET

PURSUANT TO ITEM 404(A) AND ITEM 501(B) OF REGULATION S-K SHOWING LOCATION IN

PROSPECTUS OF THE INFORMATION REQUIRED BY PART I OF FORM S-4

FORM S-4 ITEM NUMBER LOCATION IN PROSPECTUS

-------------------- ----------------------

1. Forepart of Registration

Statement and Outside Front

Cover Page of Prospectus... Outside Front Cover Page; Inside Front

Cover Page

2. Inside Front and Outside

Back Cover Pages of

Prospectus................. Inside Front Cover Page; Outside Back Cover

Page

3. Risk Factors, Ratio of Earn-

ings to Fixed Charges and

Other Information.......... Prospectus Summary; Risk Factors; Selected

Historical Consolidated Financial Data

4. Terms of the Transaction....

Prospectus Summary; The Exchange Offer;

Description of Exchange Notes; Certain

Federal Income Tax Considerations; Plan of

Distribution

5. Pro Forma Financial Informa-

tion....................... Prospectus Summary; The Skelgas and

Superior Acquisitions; Unaudited Pro Forma

Combined Financial Statements

6. Material Contracts with the

Company Being

Acquired................... Not Applicable

7. Additional Information Re-

quired for Reoffering by

Persons and Parties Deemed

to be Underwriters......... Not Applicable

8. Interests of Named Experts

and Counsel................ Not Applicable

9. Disclosure of Commission Po-

sition on Indemnification

for Securities Act

Liabilities................ Not Applicable

10. Information with Respect to

S-3 Registrants............ Not Applicable

11. Incorporation of Certain In-

formation by Reference..... Not Applicable

12. Information with Respect to

S-2 or S-3 Registrants..... Prospectus Summary; The Skelgas and

Superior Acquisitions; Capitalization;

Selected Historical Combined Financial

Data; Management's Discussion and Analysis

of Financial Condition and Results of

Operations; Business; Management; Certain

Related Transactions; Description of

Existing Indebtedness; Description of

Exchange Notes; Financial Statements

13. Incorporation of Certain In-

formation by Reference..... Information Incorporated By Reference

14. Information with Respect to

Registrants Other Than S-3

or S-2 Registrants......... Not Applicable

15. Information with Respect to

S-3 Companies.............. Not Applicable

FORM S-4 ITEM NUMBER LOCATION IN PROSPECTUS

-------------------- ----------------------

16. Information with Respect to S-2

or S-3 Companies............... Not Applicable

17. Information with Respect to Com-

panies Other Than S-2 or S-3

Companies...................... Not Applicable

18. Information if Proxies, Consents

or Authorizations are to be

Solicited...................... Not Applicable

19. Information if Proxies, Consents

or Authorizations are Not to be

Solicited or in an Exchange

Offer.......................... The Exchange Offer; Management; Principal

Unitholders

++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

+INFORMATION CONTAINED HEREIN IS SUBJECT TO COMPLETION OR AMENDMENT. A +

+REGISTRATION STATEMENT RELATING TO THESE SECURITIES HAS BEEN FILED WITH THE +

+SECURITIES AND EXCHANGE COMMISSION. THESE SECURITIES MAY NOT BE SOLD NOR MAY +

+OFFERS TO BUY BE ACCEPTED PRIOR TO THE TIME THE REGISTRATION STATEMENT +

+BECOMES EFFECTIVE. THIS PROSPECTUS SHALL NOT CONSTITUTE AN OFFER TO SELL OR +

+THE SOLICITATION OF AN OFFER TO BUY NOR SHALL THERE BE ANY SALE OF THESE +

+SECURITIES IN ANY STATE IN WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE +

+UNLAWFUL PRIOR TO REGISTRATION OR QUALIFICATION UNDER THE SECURITIES LAWS OF +

+ANY SUCH STATE. +

++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

PROSPECTUS

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 30, 1996

[LOGO OF FERRELGAS

OFFER TO EXCHANGE APPEARS HERE]

ALL OUTSTANDING

9 3/8% SERIES A SENIOR SECURED NOTES DUE 2006

FOR

9 3/8% SERIES B SENIOR SECURED NOTES DUE 2006

OF

FERRELLGAS PARTNERS, L.P.

FERRELLGAS PARTNERS FINANCE CORP.

-----------

THE EXCHANGE OFFER

WILL EXPIRE AT 5:00 P.M, NEW YORK CITY TIME

ON , 1996 UNLESS EXTENDED

-----------

10, 2017

PRELIMINARY PROSPECTUS

![]()

Ferrellgas Partners, L.P., a Delaware limited partnership (the

"Partnership"), and

Ferrellgas Partners Finance Corp., a Delaware corporation

and wholly owned subsidiary

OFFER TO EXCHANGE

$175,000,000 of the Partnership ("Finance Corp." and, together

with the Partnership, the "Issuers") hereby offer (the "Exchange Offer"), upon

the terms and subject to the conditions set forth in this Prospectus and the

accompanying Letter of Transmittal (the "Letter of Transmittal"), to exchange

$1,000 principal amount of their 9 3/8% Series B85/8% Senior Secured Notes due 2006

(the "Exchange Notes") for each $1,000 principal amount2020

that have been registered under the Securities Act of their1933

for

$175,000,000 of outstanding 9

3/8% Series A85/8% Senior Secured Notes due 2006 (the "Private Notes") which2020

that have not been registered under the Securities Act of 1933 as amended (the

"Securities Act"). Private Notes

THE EXCHANGE OFFER WILL EXPIRE AT 5:00 PM, NEW YORK

CITY TIME, ON , 2017, UNLESS WE EXTEND THE OFFER

· We are offering, on the terms and conditions set forth in this prospectus and the accompanying letter of transmittal, to exchange $175,000,000 aggregate principal amount of $160,000,000 wereour registered 85/8% Senior Notes due 2020, which we refer to as the exchange notes, for all $175,000,000 outstanding aggregate principal amount of our unregistered 85/8% Senior Notes due 2020 originally issued on April 26, 1996 and are outstanding as of the date

hereof. The form and terms of the Exchange Notes are the sameJanuary 30, 2017, which we refer to as the form and

terms of the Private Notes except that (i) the exchange will have been

registered under the Securities Act, and, therefore, the Exchange Notes will

not bear legends restricting the transfer thereof, (ii) holders of the Exchange

Notes will not be entitled to certain rights of holders of the Private Notes

under the Registration Rights Agreement (as hereinafter defined), which rights

will terminate upon the consummation of the Exchange Offer, and (iii) if the

Exchange Offer is not completed by January 14, 1997, certain Liquidated Damages

(as hereinafter defined) will be payable in respect of the Private Notes. The

Exchange Notes will evidence the same indebtedness and be secured by the same

collateral as the Private Notes (which they replace) and will be issued under

and entitled to the benefits of, the indenture dated as of April 26, 1996

governing the Private Notes and the Exchange Notes (the "Indenture"). The

Private Notes and the Exchange Notes are sometimes referred to herein

collectively as the "Senior Notes." See "The Exchange Offer" and "Description

of Exchange Notes."

The Exchange Notes will bear interest from and including the date of issuance

at the same rate and on the same terms as the Private Notes. Holders whose

Private Notes are accepted for exchange will receive accrued interest thereon

from the most recent date to which interest has been paid to, but not

including, the date of issuance of the Exchange Notes, such interest to be

payable with the first interest payment on the Exchange Notes. Interest on the

Private Notes accepted for exchange will cease to accrue upon issuance of the

Exchange Notes.

(continued on next page)

-----------

SEE "RISK FACTORS" FOR A DISCUSSION OF CERTAIN FACTORS WHICH HOLDERS OF

PRIVATE NOTES SHOULD CONSIDER IN CONNECTION WITH THE EXCHANGE OFFER AND AN

INVESTMENT IN THE EXCHANGE NOTES.

-----------

THESE SECURITIES HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE SECURITIES AND

EXCHANGE COMMISSION OR ANY STATE SECURITIES COMMISSION NOR HAS THE

SECURITIES AND EXCHANGE COMMISSION OR ANY STATE SECURITIES COMMISSION

PASSED UPON THE ACCURACY OR ADEQUACY OF THIS PROSPECTUS. ANY

REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

-----------

THE DATE OF THIS PROSPECTUS IS , 1996

The Exchange Notes will be senior secured joint and several obligations of

the Issuers and will rank senior in right of payment to all future

subordinated Indebtedness (as hereinafter defined) of the Issuers and pari

passu in right of payment with other existing and future obligations of the

Issuers. The Exchange Notes will be effectively subordinated to all existing

Indebtedness and all future senior Indebtedness and, until the Subsidiary

Guarantee Effectiveness Date (as hereinafter defined), other liabilities and

commitments of the Partnership's subsidiaries. As of April 30, 1996, after

giving pro forma effect to the transactions described herein, the total

Indebtedness, liabilities and commitments (including trade payables and other

accrued liabilities) of the Partnership's subsidiaries were approximately

$359.8 million.

The Issuersunregistered notes.

· We will accept for exchange any and all Private Notesoutstanding unregistered notes that are validly tendered and not validly withdrawn prior to 5:00 p.m., New York City time,

on , 1996, unless such date is extended by the Issuers in their sole

discretion (as so extended, such date and time are referred to herein asexpiration of the "Expiration Date"). Tendersexchange offer.

· You may withdraw tenders of Private Notes may be withdrawnunregistered notes at any time prior to the Expiration Date. Private Notes mayexpiration of the exchange offer.

· The terms of the exchange notes will be tendered onlyidentical in integral multiplesall material respects to those of $1,000.the outstanding unregistered notes, except that the transfer restrictions, registration rights or provisions for additional interest applicable to the unregistered notes do not apply to the exchange notes.

· The Exchange Offer is subjectexchange of unregistered notes for exchange notes pursuant to certain customary conditions. See

"The Exchange Offer--Conditions."

Except as described herein in the event of a Change of Control (as

hereinafter defined) or an Asset Sale (as hereinafter defined), the Issuersexchange offer will not be required to make any mandatory redemption or sinking fund paymenta taxable exchange for U.S. federal income tax purposes. Because the unregistered notes were issued with respect tooriginal issue discount (“OID”) for U.S. federal income tax purposes, the Exchange Notes prior to maturity. The Exchange Notesexchange notes will be redeemable attreated as having been issued with OID.

· We will not receive any cash proceeds from the option ofexchange offer.

· There is no established trading market for the Issuers, in whole or in part, at any time

on or after June 15, 2001 at the redemption prices set forth herein plus

accrued and unpaid interest and Liquidated Damages, if any, to the date of

redemption. In the event of a Change of Control, holders of the Exchange Notes

will have the right to require the Issuers to purchase their Exchange Notes,

in whole or in part, at a purchase price equal to 101% of the aggregate

principal amount thereof, plus accrued and unpaid interest and Liquidated

Damages, if any, to the date of purchase.

Based on an interpretation by the staff of the Securities and Exchange

Commission (the "Commission") set forth in no-action letters issued to third

parties with respect to similar transactions, the Issuers believe that the

Exchange Notes issued pursuant to the Exchange Offer in exchange for Private

Notes may be offered for resale, resold and otherwise transferred by a holder

thereof without compliance with the registration and prospectus delivery

requirements of the Securities Act; provided that (i) the holder is not an

"affiliate" of the Issuers within the meaning of Rule 405 under the Securities

Act, (ii) the holder is acquiring the Exchange Notes in its ordinary course of

business, and (iii) the holder is not engaged in, and doesnotes. We do not intend to engage in, and has no arrangement or understanding with any person to

participate in, the distributionapply for listing of the Exchange Notes. Holdersexchange notes on any securities exchange or quotation of Private

Notes wishing to accept the Exchange Offer must represent to the Issuers, as

required by the Registration Rights Agreement, that such conditions have been

met.

exchange notes on any quotation system.

Each broker-dealer that receives Exchange Notesexchange notes for its own account inpursuant to the exchange for Private Notes, where such Private Notes were acquired by such

broker-dealer as a result of market-making activities or other trading

activities,offer must acknowledge that it will deliver a prospectus meeting the requirements of the Securities Act of 1933, as amended (the “Securities Act”), in connection with any resale of such Exchange Notes.exchange notes. The Letterletter of Transmittaltransmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an "underwriter"“underwriter” within the meaning of the Securities Act. This Prospectus,prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with anyresales of exchange notes received in exchange for unregistered notes where such resale. The Issuersunregistered notes were acquired by such broker-dealer as a result of market-making or other trading activities. Please note that this prospectus may not meet the requirements of the SEC for a resale prospectus for all purposes and may require additional information. See “The Exchange Offer—Resales of Exchanges Notes.” We have agreed that, theyfor a period ending on the earlier of 180 days after the date of this prospectus and the date on which a broker-dealer is no longer required to deliver a prospectus, we will make this Prospectus (as it may

be amended or supplemented)prospectus available to any broker-dealer for use in connection with any such resaleresale. See “Plan of Distribution.”

See “Risk Factors” beginning on page 20 of this prospectus for a perioddiscussion of 180 days fromrisks you should consider before determining whether to tender your unregistered notes in the date on

whichexchange offer.

Neither the Registration StatementSEC nor any state securities commission has approved or disapproved of whichthese securities or determined if this Prospectusprospectus is truthful or complete. Any representation to the contrary is a partcriminal offense.

The date of this prospectus is declared effective by the Commission. See "Plan, 2017.

YOU SHOULD CAREFULLY READ THIS PROSPECTUS AND THE EXCHANGEDOCUMENTS WE HAVE INCORPORATED BY REFERENCE AS DESCRIBED UNDER THE SECTION ENTITLED “INCORPORATION OF DOCUMENTS BY REFERENCE.” WE ARE NOT MAKING AN OFFER IS NOT BEING MADE TO, NOR WILL THE ISSUERS ACCEPT

SURRENDERS FOR EXCHANGE FROM, HOLDERS OF PRIVATE NOTESTHESE SECURITIES IN ANY JURISDICTION WHERE SUCH OFFER OR SALE IS NOT PERMITTED.

You should rely only on the information contained in this prospectus and the documents we have incorporated by reference. We have not authorized anyone to provide you with different information. You should not assume that the information provided by this prospectus or the documents we have incorporated by reference is accurate as of any date other than the date of the respective document.

THIS PROSPECTUS INCORPORATES IMPORTANT BUSINESS AND FINANCIAL INFORMATION ABOUT US THAT HAS NOT BEEN INCLUDED IN WHICHOR DELIVERED WITH THIS PROSPECTUS. WE WILL PROVIDE WITHOUT CHARGE TO EACH PERSON TO WHOM THIS PROSPECTUS IS DELIVERED, UPON WRITTEN OR ORAL REQUEST, A COPY OF ANY SUCH INFORMATION. REQUESTS FOR SUCH COPIES SHOULD BE DIRECTED TO: FERRELLGAS, INC., INVESTOR RELATIONS, 7500 COLLEGE BOULEVARD, SUITE 1000, OVERLAND PARK, KANSAS 66210; TELEPHONE NUMBER: 913-661-1500. TO OBTAIN TIMELY DELIVERY, YOU MUST REQUEST THIS INFORMATION NO LATER THAN FIVE BUSINESS DAYS BEFORE THE EXPIRATION DATE OF THE EXCHANGE OFFER OR THE ACCEPTANCE THEREOF WOULD NOT BE IN COMPLIANCE

WITH THE SECURITIES OR BLUE SKY LAWS OF SUCH JURISDICTION.

The Exchange Notes will be available initially onlyOFFER.

This prospectus and the documents we have incorporated by reference in book-entry form. The

Issuers expectthis prospectus include forward-looking statements. These forward-looking statements are identified as any statement that the Exchange Notes issued pursuantdoes not relate strictly to the Exchange Offer

will be issued in the form of one fully registered global note that will be

deposited with,historical or on behalf of, the Depository Trust Company ("DTC"current facts. These statements often use words such as “anticipate,” “believe,” “intend,” “plan,” “projection,” “forecast,” “strategy,” “position,” “continue,” “estimate,” “expect,” “may,” “will,” or the "Depositary") and registered in its name or in the namenegative of Cede & Co., as its

nominee. Beneficial interests in the global note representing the Exchange

Notes will be shown on, and transfers thereof will be effected only through,

records maintained by the Depositary and its participants. After the initial

issuance of such global note, Exchange Notes in certificated form will be

issued in exchange for the global note only in accordance with thethose terms and

conditions set forth in the Indenture. See "Description of Exchange Notes--

Book Entry, Delivery and Form."

AVAILABLE INFORMATION

The Issuers have filed with the Commission, under the Securities Act, a

Registration Statement on Form S-4 (together with all amendments thereto, the

"Registration Statement") with respect to the Exchange Offer. This Prospectus

does not contain all information set forth in the Registration Statement and

the exhibits thereto, to which reference is hereby made. Statements made in

this Prospectus as to the contents of any contract, agreement or other document are not necessarily complete. With respect to each such contract,

agreementvariations of them or other document titled as an exhibit to the Registration

Statement, reference is hereby made to such exhibit for a more complete

description of the matter involved, and each such statement shall be deemed

qualified in its entirety by such reference.

The Registration Statement (and the exhibits and schedules thereto), as well

as the periodic reports and other information filed by the Issuers with the

Commission,comparable terminology. These statements often discuss plans, strategies, events or developments that we expect or anticipate will or may be inspected and copied at the public reference facilities

maintained by the Commission at Room 1024, 450 Fifth Street, N.W. Washington,

D.C. 20549, and at the Commission's Regional Offices at Suite 1300, Seven

World Trade Center, New York, New York 10048 and Northwest Atrium, 500 West

Madison Street, Suite 1400, Chicago, Illinois 60601-2511. Copies of such

material also can be obtained from the Public Reference Section of the

Commission, Washington D.C. 20549 at prescribed rates. The Commission

maintains a web site (http://www.sec.gov.) that contains reports, proxy and

information statements and other information filed electronically by the

Partnership with the Commission through its Electronic Data Gathering,

Analysis and Retrieval (EDGAR) System. In addition, the Partnership's common

units are listed on the New York Stock Exchange (the "NYSE") and material

filed by the Partnership can be inspected at the offices of the NYSE, 20 Broad

Street, New York, New York 10005.

The Partnership is subject to the informational requirements of the

Securities Exchange Act of 1934, as amended (the "Exchange Act"), and Finance

Corp. will become subject to such requirements as a result of the Exchange

Offer, and in accordance therewith the Partnership and Finance Corp. are (or

will be) required to file periodic reports and other information with the

Commission. In the event the Issuers are not required to be subject to the

reporting requirements of the Exchange Actoccur in the future and are based upon the Issuersbeliefs and assumptions of our management and on the information currently available to them. In particular, statements, express or implied, concerning our future operating results or our ability to generate sales, income or cash flow are forward-looking statements.

Forward-looking statements are not guarantees of performance. You should not put undue reliance on any forward-looking statement. All forward-looking statements are subject to risks, uncertainties and assumptions that could cause our actual results to differ materially from those expressed in or implied by these forward-looking statements. Many of the factors that will affect our future results are beyond our ability to control or predict.

Some of our forward-looking statements include the following:

· that we will continue to have sufficient funds to meet our obligations, including any obligations under the unregistered notes and the exchange notes;

· that we will continue to meet all of the quarterly financial tests required by the agreements governing our indebtedness;

· that we will continue to have sufficient access to capital markets at yields acceptable to us to support our expected growth expenditures and refinancing of debt maturities;

· that we intend to or will be requiredsuccessful in reducing our debt and cash deficiencies;

· that our future maintenance capital expenditures and working capital needs will be provided by a combination of cash generated from future operations, existing cash balances, borrowings under our secured credit facility or our accounts receivable securitization facility; and

·the Indenture to file withdiscussion of future effects of certain factors as described under “Summary—Recent Developments—Factors Affecting the Commission the information,

documentsNine Months Ended April 30, 2017.”

For a more detailed description of these particular forward-looking statements and for other reports specifiedfactors that may affect any forward-looking statements, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Sections 13 and 15(d) of the Exchange

Act.

3

INFORMATION INCORPORATED BY REFERENCE

The following documents filed by the Partnership and the Operating

Partnership with the Commission are incorporated herein by reference:

(i) Theour Annual ReportsReport on Form 10-K offor the Partnership and the Operating

Partnership for thefiscal year ended July 31, 1995;

(ii) The2016 and our Quarterly Reports on Form 10-Q of the Partnership and the

Operating Partnership for the quartersquarterly periods ended October 31, 1995,2016, January 31, 19962017 and April 30, 1996;

(iii) The Current2017, which are incorporated by reference in this prospectus. See “Incorporation of Documents by Reference.”

When considering any forward-looking statement, you should also keep in mind the risk factors described under the section entitled “Risk Factors” in this prospectus, our Annual Report on Form 8-K/A dated November 10, 1994 (filed

August 16, 1995),10-K for the fiscal year ended July 31, 2016 and our Quarterly Reports on Form 10-Q for the quarterly periods ended October 31, 2016, January 31, 2017 and April 30, 2017. Any of these risks could cause our actual results to differ materially from those expressed in or implied by forward-looking statements and could impair our business, financial condition or results of operation. Any such impairment may affect our ability to make distributions or pay interest on the principal of any of our debt securities, including the unregistered notes and the exchange notes. In addition, the trading price, if any, of our securities could decline as a result of any such impairment.

Except for our ongoing obligations to disclose material information as required by federal securities laws, we undertake no obligation to update any forward-looking statements or risk factors after the date of this prospectus.

This summary may not contain all of the Partnershipinformation that may be important to you. You should read this summary together with this entire prospectus and the Operating Partnership,

furnishinginformation we have incorporated by reference to understand fully the unaudited pro forma consolidated financial statementsterms of the exchange notes being offered hereunder, as well as the tax and other considerations that are important to you in making your investment decision. You should pay special attention to the risk factors described under “Risk Factors” in this prospectus, our Annual Report on Form 10-K for the fiscal year ended July 31, 2016 and our Quarterly Reports on Form 10-Q for the quarterly periods ended October 31, 2016, January 31, 2017 and April 30, 2017 to determine whether an investment in the exchange notes is appropriate for you. See “Where You Can Find More Information” in this prospectus.

For purposes of this prospectus, unless otherwise noted or the context otherwise requires:

·“we,” “us,” “our,” “ours” and “our company” refer to Ferrellgas Partners, L.P. and Vision Energy Resources, Inc.;

(iv) The Current Report on Form 8-K dated March 27, 1996 of the

Partnership and the Operating Partnership, reporting the signing of a

letter of intent to acquire Skelgas;

(v) The Current Report on Form 8-K dated April 6, 1996 of the Partnership

and the Operating Partnership, reporting a private placement of debt

securities to qualified institutional investors under Rule 144A;

(vi) The Current Report on Form 8-K dated May 6, 1996 of the Partnership

and the Operating Partnership, reporting the acquisition by the Operating

Partnership of the propane business of Skelgas Propane, Inc.

(vii) The Current Report on Form 8-K/A dated May 6, 1996 (filed July 12,

1996), of the Partnership and the Operating Partnership, furnishing the

audited financial statements of Skelgas Propane, Inc. and the unaudited pro

formatogether with its consolidated financial statements ofsubsidiaries, including Ferrellgas Partners L.P.Finance Corp. and Skelgas Propane, Inc.

All documents filed by the Partnership and the Operating Partnership with

the Commission pursuant to Sections 13(a)Ferrellgas, L.P., 13(c), 14 or 15(d) of the Exchange

Act subsequent to the date hereof and prior to the termination of the Exchange

Offer shall be deemed to be incorporated by reference into this Prospectus and

to be a part hereof from the date of filing of such documents. Any statement

contained in a document incorporated or deemed to be incorporated herein by

reference shall be deemed to be modified or superseded for purposes of this

Prospectus to the extent that a statement contained herein or in any other

subsequently filed document which also is or is deemed to be incorporated

herein by reference, which statement so modified or superseded shall not be

deemed, except as so modified or superseded, to constitute a part of this

Prospectus.

This Prospectus incorporates documents by reference which are not presented

herein or delivered herewith. Copies of these documents (excluding exhibits

unless such exhibits are specifically incorporated by reference into the

information incorporated herein) will be provided by first class mail without

charge to each person to whom this Prospectus is delivered, upon written or

oral request, to Theresa Schekirke, its operating partnership;

· “Ferrellgas Inc., One Liberty Plaza,

Liberty, Missouri 64068 (telephone number: (816) 792-6263).

4

PROSPECTUS SUMMARY

The following summary is qualified in its entirety by, and should be read in

conjunction with, the more detailed information and financial data, including

the Financial Statements and Unaudited Pro Forma Combined Financial Statements

and notes thereto, appearing elsewhere in this Prospectus. As used in this

Prospectus, the term "Partnership"Partners” refers to Ferrellgas Partners, L.P.;

·“operating partnership” refers to Ferrellgas, L.P., together with its consolidated subsidiaries; and

where

·“general partner” refers to Ferrellgas, Inc., as general partner of Ferrellgas Partners and the context requires, its subsidiaryoperating partnership.

Our Company

Ferrellgas Partners is a Delaware limited partnership and corporations. The

Partnership's fiscal year ends on July 31. References to a particular fiscal

year of the Partnership are to the twelve-month period ended on July 31 of the

year indicated.

THE PARTNERSHIP

The Partnership isprimarily engaged in the sale,retail distribution marketing and trading of propane and other natural gas liquids. The Partnership believes it isrelated equipment sales and midstream operations, including crude oil logistics. We serve propane customers in all 50 states, the second largest retail marketerDistrict of Columbia and Puerto Rico and provide midstream services to major energy companies in the United States.

Our Business

Propane Operations and Related Equipment Sales

We are a leading distributor of propane and related equipment and supplies to customers in the United States based on gallons

sold, serving more than 800,000as measured by the volume of our retail sales in fiscal 2016 and a leading national provider of propane by portable tank exchange.

We serve residential, industrial/commercial, portable tank exchange, agricultural, wholesale and agriculturalother customers in 45all 50 states, and the District of Columbia through

approximately 487 retail outlets and 251 satellite locations in 38 states (some

outlets serve interstate markets). The Partnership's largest marketPuerto Rico. Our operations primarily include the distribution and sale of propane and related equipment and supplies with concentrations are in the Midwest, Great LakesSoutheast, Southwest and SoutheastNorthwest regions of the United States. Ferrellgas, Inc. ("Ferrellgas", "Predecessor" or the "General

Partner"), a wholly owned subsidiary of Ferrell Companies, Inc. ("Ferrell"),

serves as General Partner of the Partnership. The Partnership acquired theSales from propane business and assets of Ferrellgas in July 1994.

Retail propane sales volumes were approximately 645 million gallons during

the pro forma nine months ended April 30, 1996, and 671 million gallons during

the pro forma twelve months ended July 31, 1995. Net earnings for the same

respective periods were $49.6 million and $21.8 million. See "Unaudited Pro

Forma Combined Financial Statements."

BUSINESS STRATEGY

The Partnership's business strategy is to continue its historical focus on

residential and commercial retail propane operations and to continue to expand

its operations and increase its market share both through the acquisition of

local and regional propane distributors and through internal growth by

increased competitiveness and the opening of new locations. Acquisitions will

be an important element of growth for the Partnership, as the overall demand

for propane is expected to remain relatively constant for the foreseeable

future, with year-to-year industry volumes being affected primarily by weather

patterns. The General Partner believes theredistribution are numerous potential acquisition

candidates because the propane industry is highly fragmented, with over 5,000

retailers and with the ten largest retailers comprising 33% of industry sales.

The Partnership's retail operations accounted for approximately 8% of the

retailgenerated principally from transporting propane purchased in the United States in 1995, as measured by gallons

sold.

Historically, the Partnership and Ferrellgas have been successful in

acquiring independent propane retailers and integrating them into their

existing operations at what they believefrom third parties to be attractive returns. Since 1986,

and as of May 1, 1996, the Partnership and Ferrellgas have acquired a total of

95 smaller propane businesses. Except for the acquisition of Vision Energy

Resources, Inc. ("Vision") in November of 1995 and the acquisition of Skelgas

Propane, Inc. (discussed below), none of the acquisitions were individually

material. For the nine months ended April 30, 1996 and the five fiscal years in

the period ended July 31, 1995, the Partnership and the Predecessor invested

approximately $27.7 million, $70.1 million, $3.4 million, $0.9 million, $10.1

million and $25.3 million, respectively, to acquire propane businesses with

annual retail propane sales volumes of approximately 15.1 million, 70.0

million, 2.5 million, 0.7 million, 8.6 million and 18.0 million gallons,

respectively, at the time of acquisition.

The Partnership intends to concentrate its acquisition activities in

geographical areas in close proximity to the Partnership's existing operations

and to acquire propane retailers that can be efficiently combined with such

existing operations to provide an attractive return on investment after taking

into account the efficiencies which

5

may result from such combination. However, the Partnership will also pursue

acquisitions which broaden its geographic coverage. The Partnership's goal in

any acquisition will be to improve the operations and profitability of these

smaller companies by integrating them into the Partnership's established supply

network. The General Partner regularly evaluates a number of propane distribution companies which may be candidateslocations and then to tanks on customers’ premises or to portable propane tanks delivered to nationwide and local retailers. Sales from portable tank exchanges, nationally branded under the name Blue Rhino, are generated through a network of independent and partnership-owned distribution outlets. Our market areas for acquisition. The General

Partner believes that there are numerous local retail propane distribution

companies that are possible candidates for acquisition by the Partnership and

that the Partnership's geographic diversity of operations helps to create many

attractive acquisition opportunities. The Partnership intends to fund

acquisitions through internal cash flow, external borrowings or the issuance of

additional common units of the Partnership representing limited partner

interests (the "Common Units"). The Partnership's ability to accomplish these

goals will be subject to the continued availability of acquisition candidates

at prices attractive to the Partnership. There is no assurance the Partnership

will be successful in increasing the level of acquisitions or that any

acquisitions that are made will prove beneficial to the Partnership.

In addition to growth through acquisitions, the General Partner believes that

the Partnership may also achieve growth within its existing propane operations.

Historically, the Partnership and Ferrellgas have experienced modest internal

growth in their customer base. As a result of its experience in responding to

competition and in implementing more efficient operating standards, the General

Partner believes that it has positioned the Partnership to be more successful

in direct competition for customers. The Partnership currently has marketing

programs underway which focus specific resources toward this effort.

SKELGAS ACQUISITION

On April 30, 1996, Ferrellgas acquired (the "Skelgas Acquisition") all of the

outstanding capital stock of Skelgas Propane, Inc. ("Skelgas") from Superior

Propane, Inc., a Canadian corporation ("Seller").

Through its operating subsidiaries, Skelgas sells propane and related

appliances to industrial, commercial,our residential and agricultural customers in

11 states located in the north central region of the United States. During the

year ended December 31, 1995, Skelgas sold approximately 96 million gallons of

propane, generating revenues of $75.2 million and a net loss of $(53.9) million

(which includes a $47.6 million writedown of goodwill).

Ferrellgas paid $89.3 million in cashare generally rural while our market areas for the stock of Skelgas. In addition,

Ferrellgas will pay $1.2 million for a noncompete agreement with the Seller,

payable in three equal annual installments of $400,000 commencing on the

closing date. The purchase price will be adjusted upward or downward based on a

final determination of working capital balances acquired.

Ferrellgas financed the Skelgas Acquisition with the proceeds of a short term

acquisition loan. As of May 1, 1996, Skelgas and its operating subsidiaries

were merged into Ferrellgas and all of the assets acquired by Ferrellgas in

connection with such mergers (the "Skelgas Assets") were then contributed by

Ferrellgas to the Operating Partnership as a capital contribution. In

connection with this transaction, the Operating Partnership assumed the

obligation to repay the short term acquisition loan and issued a limited

partner interest in the Operating Partnership to Ferrellgas. Following the

contribution of the Skelgas Assets to the Operating Partnership, Ferrellgas

contributed the limited partner interest in the Operating Partnership to the

Partnership in exchange for Common Units of the Partnership with a value of

approximately $925,000, which represents consideration for certain tax

liabilities retained by Ferrellgas. The Operating Partnership utilized the

Credit Facility (as hereinafter defined) (see "Use of Proceeds") to discharge

its assumed obligations under the short term acquisition loan.

SUPERIOR ACQUISITION

On April 19, 1996, Ferrellgas acquired all of the outstanding capital stock

of Superior Propane, Inc., a California corporation ("Superior"), which is not

affiliated with the Seller in the Skelgas Acquisition, from Milton Heath and

Maskey Heath (collectively the "Heaths").

6

Superior sells propane and related appliances to industrial, our industrial/commercial and residentialportable tank exchange customers in 11 counties in California and one county in Nevada. In

the fiscal year ending July 31, 1995, Superior sold approximately 11.5 million

gallons of propane from its seven locations, generating revenues of $12.7

million.

Ferrellgas paid $18.9 million for the stock of Superior, $15.5 million of

which was paid in cash at closing and $3.4 million of which was paid at closing

in the form of 6% promissory notes having a term of five years. In addition,

Ferrellgas will pay a total of $1.0 million for noncompete agreements with the

Heaths, payable in installments over five years.

The purchase price was based on the assumption that the current assets of

Superior at closing were equal to or greater than the amount of Superior's

total liabilities on the closing date. The purchase price will be adjusted

upward or downward to the extent the current assets of Superior on the closing

date are subsequently determined to be more or less than the total liabilities

of Superior on the closing date.

Immediately following the acquisition, Superior was merged into Ferrellgas

and all of the assets acquired by Ferrellgas in connection with such merger

were transferred to the Operating Partnership in a series of transactions

structured in a manner similar to that involved in transferring the Skelgas

Assets to the Operating Partnership. The Partnership delivered to Ferrellgas

Common Units of the Partnership with a value of approximately $700,000, which

represents consideration for certain tax liabilities retained by Ferrellgas.

GENERAL

Propane, a by-product of natural gas processing and petroleum refining, is a

clean-burning energy source recognized for its transportability and ease of use

relative to alternative forms of stand alone energy sources. generally urban.

In the residential and industrial/commercial markets, propane is primarily used for space heating, water heating, cooking and cooking.other propane fueled appliances. In the portable tank exchange market, propane is used primarily for outdoor cooking using gas grills. In the agricultural market, propane is primarily used for crop drying, space heating, irrigation and weed control. In addition, propane is used for certaina variety of industrial applications, including use as an engine fuel which is burned in the internal combustion engines that powerof vehicles and forklifts and as a heating or energy source in manufacturing and drying processes. Consumption

A substantial majority of our gross margin from propane and other gas liquids sales is derived from the distribution and sale of propane as a heating fuel peaks sharply in winter

months.

Theand related risk management activities. Our gross margin from the retail distribution of propane business ofis primarily based on the Partnership consists principally of

transportingcents-per-gallon difference between the sales price we charge our customers and our costs to purchase and deliver propane to its retailour propane distribution outlets and thenlocations.

The distribution of propane to tanks

located on its customers' premises byresidential customers generally involves large numbers of small volume deliveries. Our retail deliveries averaging approximately 200 gallons each. The market areasof propane are generally rural

but also include suburban areas where natural gas service is not available. The

Partnership sells propane primarily to four specific markets: residential,

industrial/commercial, agricultural and other (principally to other propane

retailers and as an engine fuel). During the pro forma nine months ended April

30, 1996, sales to residential customers accounted for 60% of the Partnership's

retail gross profits, sales to industrial/commercial customers accounted for

26% of the Partnership's retail gross profits and sales to other customers

accounted for 14% of the Partnership's retail gross profits. Residential sales

generally have a greater profit margin and a more stable customer base and tend

to be less sensitive to price changes than the other markets served by the

Partnership. No single customer of the Partnership accounts for 10% or more of

the Partnership's consolidated revenues.

Profits in the retail propane industry are primarily based on margins, the

cents-per-gallon difference between the purchase price and the sales price of

propane. The Partnership generally purchases propane in the contract and spot

markets, primarilytypically transported from natural gas processing plants and major oil companies,

on a short-term basis. Therefore, its supply costs generally fluctuate with

market price fluctuations. Should wholesale propane prices decline in the

future, the General Partner believes the Partnership's margins on itsour retail propane distribution business should increaselocations to our customers by our fleet of bulk delivery trucks, which are generally fitted with tanks ranging in the short-term because retailsize from 2,600 to 3,500 gallons. Propane storage tanks located on our customers’ premises are then filled from these bulk delivery trucks. We also deliver propane to our industrial/ commercial and portable tank exchange customers using our fleet of portable tank and portable tank exchange delivery trucks, truck tractors and portable tank exchange delivery trailers.

Our residential customers and portable tank exchange customers typically provide us a greater cents-per-gallon margin than our industrial/commercial, agricultural, wholesale and other customers. We track “Propane sales volumes,” “Revenues—Propane and other gas liquids sales” and “Gross Margin— Propane and other gas liquids sales” by customer; however, we are not able to specifically allocate operating and other costs by customer in a manner that would determine their specific profitability with a high degree of accuracy. The wholesale propane price per gallon is subject to various market conditions, including inflation, and may fluctuate based on changes in demand, supply and other energy commodity prices, primarily crude oil and natural gas, as propane prices tend to change less rapidly than wholesale prices. Should wholesale

propane prices increase, for similar reasons retail margins and profitability

would likely be reduced at least forcorrelate with the short-term until retail prices can be

increased.

7

Retail propanefluctuations of these underlying commodities.

As of July 31, 2016, approximately 51% of our residential customers typically leaserent their stationary storage tanks from their propane distributors. Approximately 70% of the Partnership's customers

lease their tank from the Partnership. The leaseus. Our rental terms and in most states,

certainthe fire safety regulations restrict the refilling of a leased tank solelyin some states require rented bulk tanks to be filled only by the propane supplier that ownsowning the tank. The cost and inconvenience of switching bulk tanks minimizeshelps minimize a customer'scustomer’s tendency to switch among suppliers of propane on the basis of minor variations in price.

price, helping us minimize customer loss.

In addition, we lease tanks to some of our independent distributors involved with our delivery of propane for portable tank exchanges. Our owned and independent distributors provide portable tank exchange customers with a national delivery presence that is generally not available from most of our competitors.

In our past three fiscal years, our total annual propane sales volumes in gallons were:

Fiscal year ended | Propane Sales | ||

July 31, 2016 | 779 | ||

July 31, 2015 | 879 | ||

July 31, 2014 | 947 |

We utilize marketing programs targeting both new and existing customers by emphasizing:

· our efficiency in delivering propane to customers;

· our employee training and safety programs;

· our enhanced customer service, facilitated by our technology platform and our 24 hours a day, seven days a week emergency retail customer call support capabilities; and

· our national distributor network for our commercial and portable tank exchange customers.

Some of our propane distribution locations also conduct the retail sale of propane appliances and related parts and fittings, as well as other retail propane related services and consumer products. We also sell gas grills, grilling tools and accessories, patio heaters, fireplace and garden accessories, mosquito traps and other outdoor products through Blue Rhino Global Sourcing, Inc.

Our other activities in our propane and related equipment and supplies sales segment include the following:

· the sale of refined fuels, and

· common carrier services.

Effect of Weather and Seasonality

Weather conditions have a significant impact on demand for propane for heating purposes during the months of November through March (the “winter heating season”). Accordingly, the volume of propane used by our customers

for this purpose is directly affected by the severity of the winter weather in the regions we serve and can vary substantially from year to year. In any given region, sustained warmer-than-normal temperatures in the winter heating season will tend to result in reduced propane usage, while sustained colder-than-normal temperatures in the winter heating season will tend to result in greater usage. Although there is a strong correlation between weather and customer usage, general economic conditions in the United States and the wholesale price of propane can also significantly impact this correlation. Additionally, there is a natural time lag between the onset of cold weather and increased sales to customers. If the United States were to experience a cooling trend we could expect nationwide demand for propane to increase which could lead to greater sales, income and liquidity availability. Conversely, if the United States were to experience a warming trend, we could expect nationwide demand for propane to decrease which could lead to a reduction in our sales, income and liquidity availability.

The retail market for propane is seasonal because it is usedof increased demand during the winter heating season primarily for the purpose of providing heating in residential and commercial buildings. Consequently, sales and operating profits are concentrated in theour second and third fiscal quarters, (November through April). Whilewhich are during the winter heating season. However, our propane by portable tank exchange business experiences higher volumes in the spring and summer, which include the majority of the grilling season. These volumes add to our operating profits during our first and fourth fiscal quarters due to those counter-seasonal business activities. These sales also provide us the ability to better utilize our seasonal resources at our propane distribution business is seasonal

in nature and historically sensitive to variations in weather, management

believes that the geographical diversity of the Partnership's areaslocations. Other factors affecting our results of operations include competitive conditions, volatility in energy commodity prices, demand for propane, timing of acquisitions and general economic conditions in the United States.

We use information on temperatures to understand how our results of operations are affected by temperatures that are warmer or colder than normal. We use the definition of “normal” temperatures based on information published by the National Oceanic and Atmospheric Administration. Based on this information we calculate a ratio of actual heating degree days to normal heating degree days. Heating degree days are a general indicator of weather impacting propane usage.

We believe that our broad geographic distribution helps to minimize the Partnership'sus reduce exposure to regional weather orand economic patterns. Furthermore, long-term historicDuring times of colder-than-normal winter weather, datawe have been able to take advantage of our large, efficient distribution network to avoid supply disruptions, thereby providing us a competitive advantage in the markets we serve.

Risk Management Activities—Commodity Price Risk

We employ risk management activities that attempt to mitigate price risks related to the purchase, storage, transport and sale of propane generally in the contract and spot markets from the

National Climatic Data Center indicate that average annual temperatures have

remained relatively constant over the last 30 years, with fluctuations

occurringmajor domestic energy companies on a year-to-year basis only.

Propane competesshort-term basis. We attempt to mitigate these price risks through the use of financial derivative instruments and forward propane purchase and sales contracts. We enter into propane sales commitments with a portion of our customers that provide for a contracted price agreement for a specified period of time. These commitments can expose us to product price risk if not immediately hedged with an offsetting propane purchase commitment.

Our risk management strategy involves taking positions in the forward or financial markets that are equal and opposite to our positions in the physical products market in order to minimize the risk of financial loss from an adverse price change. This risk management strategy is successful when our gains or losses in the physical product markets are offset by our losses or gains in the forward or financial markets. Our propane related financial derivatives are designated as cash flow hedges.

Our risk management activities may include the use of financial derivative instruments including, but not limited to, swaps, options, and futures to seek protection from adverse price movements and to minimize potential losses. We enter into these financial derivative instruments directly with third parties in the over-the-counter market and with brokers who are clearing members with the New York Mercantile Exchange. We also enter into forward propane purchase and sales contracts with counterparties. These forward contracts qualify for the normal purchase normal sales exception within GAAP and are therefore not recorded on our financial statements until settled.

Through our supply procurement activities, we purchase propane primarily with natural gas, electricityfrom energy companies. Supplies of propane from these sources have traditionally been readily available, although no assurance can be given that they will be readily available in the future. We may purchase and fuel oil as an

energy source, principally onstore inventories of propane to avoid delivery interruptions during the basisperiods of price, availability and

profitability. Propane serves as an alternative to natural gas in rural and

suburban areas where natural gas is unavailable or portability of product is

required. Propane is generally more expensive than natural gas on an equivalent

British thermal unit ("BTU") basis in locations served by natural gas, although

propane is often sold in such areas as a standby fuel for use during peak

demand periods and during interruption in natural gas service. Propane is

generally less expensive to use than electricity for space heating, water

heating and cooking and competes effectively with electricity in those parts of

the country where propane is cheaper than electricity on an equivalent BTU

basis. Although propane is similar to fuel oil in application, marketincreased demand and price, propane and fuel oil have generally developed their own distinct

geographic markets, lessening competition between such fuels.

The Partnership is also engaged in the tradingto take advantage of propane and other natural

gas liquids, chemical feedstocks marketing and wholesale propane marketing. In

the pro forma nine months ended April 30, 1996 and the pro forma twelve months

ended July 31, 1995, the Partnership's annual wholesale and trading sales

volume was approximately 1.4 billion gallons and 1.6 billion gallons,

respectively,favorable commodity prices. As a result of propane and other natural gas liquids, of which 46% and 60%,

respectively, were propane. Because the Partnership possesses a large

distribution system, underground storage capacity and theour ability to buy large volumes of propane the General Partner believes that the Partnership isand utilize our national distribution system, we believe we are in a position to achieve product cost savings and avoid shortages during periods of tight supply to an extent not generally available to other retail propane distributors. PARTNERSHIP STRUCTURE AND MANAGEMENT

The managementDuring fiscal 2016, seven suppliers accounted for approximately

73% of our total propane purchases. Because there are numerous alternative suppliers available, we do not believe it is reasonably possible that this supplier concentration could cause a near-term severe impact on our ability to procure propane, though propane prices could be affected; however, if supplies were interrupted or difficulties in obtaining alternative transportation were to arise, the cost of procuring replacement supplies may materially increase. These transactions are accounted for at cost in ‘‘Cost of product sold—propane and employeesother gas liquids sales’’ in our consolidated statement of Ferrellgas manageearnings.

A portion of our propane inventory is purchased under supply contracts that typically have a one-year term and operate the propane

business and assets of the Partnership as officers and employees of the General

Partner.a price that fluctuates based on spot market prices. In order to simplifylimit overall price risk, we will enter into fixed price over-the-counter propane forward and/or swap contracts that generally have terms of less than 36 months. We may also use options to hedge a portion of our forecasted purchases, which generally do not exceed 36 months in the Partnership'sfuture.

We also incur risks related to the price and availability of propane during periods of much colder-than-normal weather, temporary supply shortages concentrated in certain geographic regions and commodity price distortions between geographic regions. We attempt to mitigate these risks through our transportation activities by utilizing our transport truck and railroad tank car fleet to distribute propane between supply or storage locations and propane distribution locations. The propane we sell to our customers is generally transported from gas processing plants and refineries, pipeline terminals and storage facilities to propane distribution locations or storage facilities by our leased railroad tank cars, our owned or leased highway transport trucks, common carrier, or owner-operated transport trucks.

Risk Management Activities—Transportation Fuel Price Risk

We employ risk management activities that attempt to mitigate price risks related to the purchase of gasoline and diesel fuel for use in the transport of propane from supply or storage locations and from retail fueling stations. We attempt to mitigate these price risks through the use of financial derivative instruments.

Our risk management strategy involves taking positions in the financial markets that are not more than the forecasted purchases of fuel for our internal use in both the supply and retail propane delivery fleet in order to minimize the risk of decreased earnings from an adverse price change. This risk management strategy locks in our purchase price and is successful when our gains or losses in the physical product markets are offset by our losses or gains in the financial markets. Our transport fuel financial derivatives are not designated as cash flow hedges.

Midstream Operations

Our midstream operations include crude oil logistics, which we operate under the Bridger Logistics tradename (“Bridger”) and water solutions operations (“Bridger Environmental”). Bridger primarily provides domestic crude oil transportation and logistics services with an integrated portfolio of midstream assets connecting crude oil production in prolific basins in the U.S. to downstream markets. Bridger’s truck, pipeline terminal, pipeline, rail and maritime assets form a comprehensive, fee-for-service business model, and substantially all of its cash flow is generated from fee-based commercial agreements.

Bridger’s fee-based business model generates income by providing crude oil transportation and logistics services on behalf of producers and end-users of crude oil with end markets across North America including a presence in all major domestic crude oil basins. The first link in Bridger’s integrated value chain is its truck transportation operations. Bridger charges producers and first purchasers of crude oil fees per barrel to transport crude from the wellhead to takeaway outlets, which provide connectivity to end markets and generate additional fee-for-service income. Bridger also owns or controls a number of assets connecting trucked crude volumes to downstream takeaway infrastructure, including pipeline injection terminals, crude storage, rail loading and unloading facilities, new build railcars, maritime assets and pipelines.

Bridger also engages in the marketing of physical crude oil in the major production basins of the United States. Bridger purchases this crude oil from producers and transports it using a mix of its truck transportation and rail assets as well as terminal and pipeline contracts to the sale point with its customers.

Bridger’s customers include crude oil producers, refiners and marketers. Generally, Bridger seeks to enter into long-term contracts to provide logistics services; however, contracts for the transportation of crude oil by truck tend to be terminable on 30 days’ notice.

Bridger Environmental generates revenues from treatment and disposal of salt water generated from crude oil production operations at its salt water disposal wells and from the sale of recovered crude oil from the skimming oil process.

Risk Management Activities—Crude Oil Price Risk

Our risk management activities attempt to mitigate price risks related to our crude oil line fill and inventory. We may use financial and commodity based derivative contracts to manage the risks produced by changes in the price of crude oil or to capture market opportunities.

Our risk management strategy involves taking positions in the financial markets that are equal and opposite to the forecasted crude oil line fill and inventory volume in order to minimize the risk of inventory price change. This risk management strategy locks in our sales price and is successful when our gains or losses on line fill or inventory are offset by our losses or gains in the financial markets. Our crude oil financial derivatives are not designated as cash flow hedges.

Business Strategy

Propane Operations and Related Equipment Sales

Our business strategy for our propane and related equipment sales business is to:

· Expand our operations through internal growth, as accretive opportunities become available;

· Capitalize on our national presence and economies of scale; and

· Maximize operating efficiencies through utilization of our technology platform.

Expand our operations through internal growth, as accretive opportunities become available

Our goal is to improve the operations and profitability of our propane and related equipment sales segment by integrating best practices and leveraging our established national organization and technology platforms to help reduce costs and enhance customer service. We believe that our enhanced operational synergies, improved customer service and ability to better track the financial performance of operations provide us a distinct competitive advantage and better analysis as we consider future opportunities.

We believe that we are positioned to successfully compete for growth opportunities within and outside of our existing operating regions. Our efforts will focus on adding density to our existing customer base, providing propane and complementary services to national accounts and providing other product offerings to existing customer relationships. This continued expansion will give us new growth opportunities by leveraging the capabilities of our operating platforms.

Capitalize on our national presence and economies of scale

We believe our national presence of 855 propane distribution locations in the United States as of July 31, 2016 gives us advantages over our smaller competitors. These advantages include economies of scale in areas such as:

· product procurement;

· transportation;

· fleet purchases;

· propane customer administration; and

· general administration.

We believe that our national presence allows us to be one of the few propane distributors that can competitively serve industrial/commercial and portable tank exchange customers on a nationwide basis, including the ability to serve such propane customers through leading home-improvement centers, mass merchants and hardware, grocery and convenience stores. In addition, we believe that our national presence provides us opportunities to make

acquisitions of other propane distribution companies whose operations overlap with ours, providing economies of scale and significant cost savings in these markets.

We also believe that investments in technology similar to ours require both a large scale and a national presence, in order to generate sustainable operational savings to produce a sufficient return on investment. For these reasons, we believe our national presence and economies of scale provide us with an on-going competitive advantage.

Maximize operating efficiencies through utilization of our technology platform

We believe our significant investments in technology give us a competitive advantage to operate more efficiently and effectively at a lower cost compared to most of our competitors. We do not believe that many of our competitors will be able to justify similar investments in the near term. Our technology advantage has resulted from significant investments made in our retail propane distribution operating platform together with our state-of-the-art tank exchange operating platform.

Our technology platform allows us to efficiently route and schedule our customer deliveries, customer administration and operational workflow for the retail sale and delivery of bulk propane. Our service centers are staffed to provide oversight and management to multiple distribution locations, referred to as service units. We operate a retail distribution network, including portable tank exchange operations, using a structure of 56 service centers and 855 service units as of July 31, 2016. The service unit locations utilize hand-held computers and cellular or satellite technology to communicate with management personnel who are typically located at the associated service center. We believe this structure and our technology platform allow us to more efficiently route and schedule customer deliveries and significantly reduce the need for daily on-site management.

The efficiencies gained from operating our technology platform allow us to consolidate our management teams at fewer locations, quickly adjust the sales prices to our customers and manage our personnel and vehicle costs more effectively to meet customer demand.

Our customer support capabilities allow us to accept emergency customer calls 24 hours a day, seven days a week. These combined capabilities provide us cost savings while improving customer service by reducing customer inconvenience associated with multiple, unnecessary deliveries.

Midstream Operations

Our current business strategy for our midstream operations is to maximize profitability utilizing existing assets. The continued, sustained decline in the price of crude oil has had a negative impact on domestic crude oil production, and as a result, has had a trending negative impact on the volumes of crude oil that we transport. We are evaluating all phases of our business in light of these challenges with the goal of operating more efficiently.

We are evaluating alternatives to maximize profitability relative to rail car assets previously committed to a recently terminated transportation and logistics agreement and Bridger’s largest customer and our trucking fleet which is currently operating under capacity. We believe this business strategy supports our overall current company strategy of reducing debt and improving our leverage ratio. See “—Recent Developments.”

Recent Developments

Termination of Bridger Agreement with Jamex

In connection with the closing of our acquisition of Bridger in June 2015, Bridger entered into a ten-year transportation and logistics agreement (the “Jamex TLA”) with Jamex Marketing, LLC (“Jamex”) pursuant to which Jamex would be responsible for certain payments to Bridger and also for sourcing crude oil volumes for Bridger’s largest customer.

As a result of concerns regarding the collectability of amounts owed to Bridger from Jamex under the Jamex TLA and certain other matters between Bridger and Jamex, Bridger, on September 1, 2016, Jamex, Ferrellgas Partners and certain other affiliated parties entered into a group of agreements that terminated the Jamex TLA, facilitated Ferrellgas Partners purchasing certain Ferrellgas Partners common units from Jamex, and established payment terms for certain amounts owed by Jamex to Bridger under the Jamex TLA. Consequently, we do not anticipate any material contribution to revenue or EBITDA from Jamex or Bridger’s former largest customer in the future.

On September 1, 2016, we entered into a Termination, Settlement and Release Agreement (the “Jamex Termination Agreement”) with Jamex, certain of Jamex’s affiliates, and James Ballengee (the owner of Jamex) pursuant to which:

(1) Jamex agreed to execute and deliver a secured promissory note in favor of Bridger in original principal amount of $49.5 million (the “Jamex Secured Promissory Note”) in satisfaction of all obligations owed to Bridger under the Jamex TLA;

(2) Mr. Ballengee and Bacchus Capital Trading, LLC, an entity controlled by Mr. Ballengee (“Bacchus”), executed and delivered a joint guarantee of the Jamex Secured Promissory Note obligations up to a maximum aggregate amount of $20.0 million;

(3) The operating partnership agreed to provide Jamex with a $5.0 million revolving secured working capital facility evidenced by a revolving promissory note (the “Jamex Revolving Promissory Note” and, together with the Jamex Secured Promissory Note, the “Jamex Notes”);

(4) The other Jamex entities agreed to execute and deliver a security agreement and a full guarantee of the obligations under the lawsJamex Notes;

(5) We paid approximately $16.9 million to Jamex and in return received 0.9 million of several

jurisdictionsFerrellgas Partners’ common units, which were cancelled upon receipt, and approximately 23,000 barrels of crude oil;

(6) The parties agreed to terminate the Jamex TLA and certain other commercial agreements and arrangements between them, and release any claims between or among them that may exist (other than those arising under the Jamex Termination Agreement or the other agreements entered into in connection with the Jamex Termination Agreement); and

(7) We waived the remaining lockup provision applicable to Jamex under the Registration Rights Agreement dated June 24, 2015 to which Jamex is party.

The Jamex Secured Promissory Note originally had an annual interest rate of 7%, which decreased to 2.8% as a result of Ferrellgas Partners’ reducing its quarterly distribution rate to $0.10, and contemplates quarterly amortizing principal payments, together with payments of accrued interest. The first quarterly interest payment of approximately $0.9 million was received in December 2016 and the first quarterly principal payment of approximately $2.5 million was received in March 2017. The maturity date of the Jamex Secured Promissory Note is December 17, 2021, and Jamex may prepay the Secured Promissory Note in whole or in part at any time.