As filed with the Securities and Exchange Commission on July 19,August 7, 2013

Registration No. 333-189575333-189576

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 13

TO

FORMS-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

HEXION U.S. FINANCE CORP.

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | 2821 (Primary Standard Industrial Classification Code Number) | 20-1362484 (I.R.S. Employer Identification No.) |

180 East Broad Street

Columbus, Ohio 43215

(614) 225-4000

HEXION NOVA SCOTIA FINANCE, ULC

(Exact name of registrant as specified in its charter)

| Nova Scotia, Canada | 2821 | None | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

180 East Broad Street

Columbus, Ohio 43215

(614) 225-4000

GUARANTORS LISTED ON SCHEDULE A HERETO

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Douglas A. Johns, Esq.

Hexion U.S. Finance Corp.

180 East Broad Street

Columbus, Ohio 43215

(614) 225-4000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

David S. Huntington, Esq.

Paul, Weiss, Rifkind, Wharton & Garrison LLP

1285 Avenue of the Americas

New York, New York 10019-6064

(212) 373-3000

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement becomes effective.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is apost-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||||||

| Non-accelerated filer | x | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ¨

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) ¨

The Registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

SCHEDULE A

Guarantor | State or Other Jurisdiction of Incorporation or Organization | Address of Registrants’ Principal Executive Offices | I.R.S. Employer Identification Number | |||

Momentive Specialty Chemicals Inc. | New Jersey | 180 East Broad Street Columbus, Ohio 43215 (614) 225-4000 | 13-0511250 | |||

Momentive Specialty Chemicals Investments Inc. | Delaware | 180 East Broad Street Columbus, Ohio 43215 (614) 225-4000 | 51-0370359 | |||

Borden Chemical Foundry, LLC | Delaware | 180 East Broad Street Columbus, Ohio 43215 (614) 225-4000 | 31-1766429 | |||

HSC Capital Corporation | Delaware | 180 East Broad Street Columbus, Ohio 43215 (614) 225-4000 | 76-0660306 | |||

Lawter International Inc. | Delaware | 180 East Broad Street Columbus, Ohio 43215 (614) 225-4000 | 36-1370818 | |||

Momentive International Inc. | Delaware | 180 East Broad Street Columbus, Ohio 43215 (614) 225-4000 | 20-2833048 | |||

Oilfield Technology Group, Inc. | Delaware | 15115 Park Row, Ste. 160 Houston, TX 77984 (218) 646-2800 | 20-2873694 | |||

Momentive CI Holding Company (China) LLC | Delaware | 180 East Broad Street Columbus, Ohio 43215 (614) 225-4000 | 20-3907441 | |||

NL Coop Holdings LLC | Delaware | 180 East Broad Street Columbus, Ohio 43215 (614) 225-4000 | 27-2090696 | |||

The primary standard industrial classification code number of each of the additional registrants is 3089.

EXPLANATORY NOTE

This Amendment No. 3 to the Registration Statement on Form S-4 (File No. 333-189576) of Hexion U.S. Finance Corp. and Hexion Nova Scotia Finance, ULC is being filed solely for the purpose of filing an exhibit as indicated in Part II of this Amendment No. 3. This Amendment No. 3 does not modify any provision of the proxy statement/prospectus that forms a part of the Registration Statement. Accordingly, a preliminary prospectus has been omitted.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 19,AUGUST 7, 2013

PROSPECTUS

Hexion U.S. Finance Corp.

Hexion Nova Scotia Finance, ULC

Exchange Offer for $1,100,000,000$200,000,000

6.625% First-Priority8.875% Senior Secured Notes due 20202018 and Related Guarantees

The Notes and the Guarantees

We are offering to exchange $1,100,000,000$200,000,000 of our outstanding 6.625% First-Priority8.875% Senior Secured Notes due 20202018 and certain related guarantees, which were issued on January 31,14, 2013 and which we refer to collectively as the “initial notes,” for a like aggregate amount of our registered 6.625% First-Priority8.875% Senior Secured Notes due 20202018 and certain related guarantees, which we refer to collectively as the “exchange notes.” The exchange notes will be issued under an indenture dated as of March 14, 2012.January 29, 2010. We refer to the initial notes and the exchange notes collectively as the “notes.”

The exchange notes will mature on April 15, 2020.February 1, 2018. We will pay interest on the exchange notes semi-annually on April 15February 1 and October 15August 1 of each year, commencing on April 15,February 1, 2013, at a rate of 6.625%8.875% per annum, to holders of record on the April 1January 15 or October 1July 15 immediately preceding the interest payment date.

The exchange notes will beare senior obligations of the Issuers, are guaranteed on aas senior secured basis by our parent,obligations of Momentive Specialty Chemicals Inc., and certain of its existingour domestic subsidiaries, that guarantee its obligations under its ABL Facility.

The exchange notes and the related guarantees will beare secured by first-priority liens, on the Notes Priority Collateral (which generally includes most of our and our domestic subsidiaries’ assets other than the ABL Priority Collateral) and by second-priority liens on the ABL Priority Collateral (which generally includes most of our and our domestic subsidiaries’ inventory and accounts receivable and related assets), in each case subject to certain exceptions and permitted liens, as described herein. The exchange notes will rank equally with allon certain of our and the guarantors’ existing and future senior indebtedness.domestic assets. In the event of enforcement of the security securing the notes, the proceeds thereof will first be applied to repay our obligations under our asset-based revolving loan facility, our first lien notes and any other first-priority lien obligations, prior to the repayment of obligations under the notes, but such proceeds will be applied to repay the notes before being applied to repay our existing second lien notes.

Terms of the Exchange Offer

It will expire at 5:00 p.m., New York City time, on , 2013, unless we extend it.

If all the conditions to this exchange offer are satisfied, we will exchange all of our initial notes that are validly tendered and not withdrawn for the exchange notes.

You may withdraw your tender of initial notes at any time before the expiration of this exchange offer.

The exchange notes that we will issue you in exchange for your initial notes will be substantially identical to your initial notes except that, unlike your initial notes, the exchange notes will have no transfer restrictions or registration rights.

The exchange notes that we will issue you in exchange for your initial notes are new securities with no established market for trading.

Before participating in this exchange offer, please refer to the section in this prospectus entitled

“Risk Factors” commencing on page 21.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

We have not applied, and do not intend to apply, for listing the notes on any national securities exchange or automated quotation system.

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of those exchange notes. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act of 1933, as amended (the “Securities Act”). This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for initial notes where those initial notes were acquired by that broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 180 days after the expiration date, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See “Plan of Distribution.”

The date of this prospectus is , 2013.

| Page | ||||

| ii | ||||

| 1 | ||||

| 21 | ||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||||

Security Ownership of Certain Beneficial Owners and Management | ||||

| Service of Process and Enforceability of Civil Liabilities | 225 | |||

| 226 | ||||

| F-1 | ||||

i

We have not authorized anyone to give you any information or to make any representations about us or the transactions we discuss in this prospectus other than those contained in this prospectus. If you are given any information or representations about these matters that is not discussed in this prospectus, you must not rely on that information. This prospectus is not an offer to sell or a solicitation of an offer to buy securities anywhere or to anyone where or to whom we are not permitted to offer or sell securities under applicable law. The delivery of this prospectus does not, under any circumstances, mean that there has not been a change in our affairs since the date of this prospectus. Subject to our obligation to amend or supplement this prospectus as required by law and the rules of the Securities and Exchange Commission (the “SEC”), the information contained in this prospectus is correct only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of these securities.

The notes may not be offered or sold in or into the United Kingdom by means of any document except in circumstances that do not constitute an offer to the public within the meaning of the Public Offers of Securities Regulations 1995. All applicable provisions of the Financial Services and Markets Act 2000 must be complied with in respect of anything done in relation to the notes in, from or otherwise involving or having an effect in the United Kingdom.

The notes have not been and will not be qualified under the securities laws of any province or territory of Canada. The notes are not being offered or sold, directly or indirectly, in Canada or to or for the account of any resident of Canada in contravention of the securities laws of any province or territory thereof.

Until , 2013 (90 days after the date of this prospectus), all dealers effecting transactions in the exchange notes, whether or not participating in the exchange offer, may be required to deliver a prospectus. This is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

MARKET AND INDUSTRY DATA AND FORECASTS

This prospectus includes industry data that we obtained from periodic industry publications and internal company surveys. This prospectus includes market share and industry data that we prepared primarily based on management’s knowledge of the industry and industry data. Unless otherwise noted, statements as to our market share and market position relative to our competitors are approximated and based on management estimates using the above-mentioned latest-available third-party data and our internal analysis and estimates. We determined our market share and market positions utilizing periodic industry publications. If we were unable to obtain relevant periodic industry publications, we based our estimates on our knowledge of the size of our markets, our sales in each of these markets and publicly available information regarding our competitors, as well as internal estimates of competitors’ sales based on discussion with our sales force and other industry participants.

While we believe our internal estimates with respect to our industry are reliable, our estimates have not been verified by any independent sources. While we are not aware of any misstatements regarding any industry data presented in this prospectus, our estimates, in particular as they relate to market share and our general expectations, involve risks and uncertainties and are subject to change based on various factors, including those discussed under sections entitled “Risk Factors” and “Cautionary Statement Concerning Forward-Looking Statements.”

ii

This summary highlights information about Momentive Specialty Chemicals Inc. and the notes contained elsewhere in this prospectus. This summary is not complete and may not contain all the information that may be important to you. You should carefully read the entire prospectus before making an investment decision, especially the information presented under the heading “Risk Factors.” In this prospectus, except as otherwise indicated herein, or as the context may otherwise require, (i) all references to “MSC,” the “Company,” “we,” “us” and “our” refer to Momentive Specialty Chemicals Inc. and its subsidiaries and (ii) all references to “Issuer”“Issuers” refer to Hexion U.S. Finance Corp., and Hexion Nova Scotia Finance, ULC, the issuerissuers of the notes, and itstheir successors, which is aare wholly owned subsidiarysubsidiaries of Momentive Specialty Chemicals Inc.

Our Company

Momentive Specialty Chemicals Inc., a New Jersey corporation, is the world’s largest producer of thermosetting resins, or thermosets, and a leading producer of adhesive and structural resins and coatings. Thermosets are a critical ingredient for virtually all paints, coatings, glues and other adhesives produced for consumer or industrial uses. We provide a broad array of thermosets and associated technologies and have significant market positions in each of the key markets that we serve. Our products are used in thousands of applications and are sold into diverse markets, such as forest products, architectural and industrial paints, packaging, consumer products and automotive coatings, as well as higher growth markets, such as composites and electrical laminates. Major industry sectors that we serve include industrial/marine, construction, consumer/durable goods, automotive, wind energy, aviation, electronics, architectural, civil engineering, repair/remodeling, graphic arts and oil and gas field support. Key drivers for our business include general economic and industrial conditions, including housing starts, auto build rates and active gas drilling rigs.

As of March 31, 2013, we had 62 active production sites around the world. Through our worldwide network of strategically located production facilities, we serve more than 5,700 customers in approximately 100 countries. Our position in certain additives, complementary materials and services further enables us to leverage our core thermoset technologies and provide our customers with a broad range of product solutions. As a result of our focus on innovation and a high level of technical service, we have cultivated long-standing customer relationships. Our global customers include leading companies in their respective industries, such as 3M, Ashland Chemical, BASF, Bayer, DuPont, GE, Halliburton, Honeywell, Louisiana Pacific, Owens Corning, PPG Industries, Sumitomo, Valspar and Weyerhaeuser.

Momentive Combination

In October 2010, our parent, Momentive Specialty Chemicals Holdings LLC (formerly known as Hexion LLC) (“MSC Holdings”) and Momentive Performance Materials Holdings Inc. (“MPM Holdings”), the parent company of Momentive Performance Materials Inc. (“MPM”), became subsidiaries of a newly formed holding company, Momentive Performance Materials Holdings LLC (“Momentive Holdings”). We refer to this transaction as the “Momentive Combination.”

At the time of the Momentive Combination, Hexion LLC changed its name to Momentive Specialty Chemicals Holdings LLC and Hexion Specialty Chemicals, Inc. changed its name to Momentive Specialty Chemicals Inc. As a result of the Momentive Combination, Momentive Holdings became the ultimate parent entity of MPM and MSC. Momentive Holdings is controlled by investment funds (the “Apollo Funds”) managed by affiliates of Apollo Management Holdings, L.P. (together with Apollo Global Management, LLC and its subsidiaries, “Apollo”). Apollo may also be referred to as the Company’s owner.

The notes are not issued or guaranteed by Momentive Holdings, MPM Holdings, MPM or any of MPM’s subsidiaries, and are also not secured by any assets of such entities. None of Momentive Holdings, MPM Holdings, MPM or any of MPM’s subsidiaries is obligated with respect to any of our indebtedness or other liabilities.

Our Business

We are a large participant in the specialty chemicals industry, and a leading producer of adhesive and structural resins and coatings. Thermosets are a critical ingredient for virtually all paints, coatings, glues and other adhesives produced for consumer or industrial uses. We provide a broad array of thermosets and associated technologies and have significant market positions in all of the key markets that we serve.

Our products are used in thousands of applications and are sold into diverse markets, such as forest products, architectural and industrial paints, packaging, consumer products and automotive coatings, as well as higher growth markets, such as composites, UV cured coatings and electrical composites. Major industry sectors that we serve include industrial/marine, construction, consumer/durable goods, automotive, wind energy, aviation, electronics, architectural, civil engineering, repair/remodeling, graphic arts and oil and gas field support. Key drivers for our business include general economic and industrial conditions, including housing starts, auto build rates and active gas drilling rigs. In addition, due to the nature of our products and the markets we serve, competitor capacity constraints and the availability of similar products in the market may impact our results. As is true for many industries, our financial results are impacted by the effect on our customers of economic upturns or downturns, as well as by the impact on our own costs to produce, sell and deliver our products. Our customers use most of our products in their production processes. As a result, factors that impact their industries can and have significantly affected our results.

The table below illustrates our net sales to external customers for the year ended December 31, 2012 as well as the major product lines, major industry sectors served, major end-use markets and key differentiating characteristics relative to our products.

Epoxy, Phenolic and Coating Resins | Forest Products Resins | |||||||||

2012 Net Sales | $3.0 billion | $1.7 billion | ||||||||

Major Products | • • • • • • • | Epoxy specialty resins Epoxy resins and intermediates Phenolic specialty resins Versatic acids and derivatives Phenolic encapsulated substrates Polyester resins Acrylic resins | • | Formaldehyde based resins and formaldehyde | ||||||

Major Industries Served | • • • • • • • • • • • | Wind Energy Oil and gas field drilling and development Transportation and industrial Construction Electrical equipment and appliances Electronic products Marine and recreational (boats, RVs) Chemical manufacturing Home building and maintenance Consumer durable and non-durable products General manufacturing | • • • • | Home building and maintenance Home repair and remodeling Furniture Agriculture | ||||||

Epoxy, Phenolic and Coating Resins | Forest Products Resins | |||||||||

| Core End-Use Markets | • • • • • • • • | Oil and gas field proppants Wind energy Auto coatings and friction materials Marine and industrial coatings Electronics Commercial and residential construction Engineered materials Decorative paints | • • • • | Commercial and residential construction Plywood, particleboard, medium-density fiberboard (“MDF”), oriented strand board (“OSB”) Furniture Agrochemical | ||||||

Key Product Characteristics | • • • | Strength and adhesion Durability Resistance (water, UV, corrosion, temperature) | • • • | Strength and adhesion Durability Moisture resistance | ||||||

The discussion that follows is based on our organizational structure and reportable segments in 2013.

Epoxy, Phenolic and Coating Resins

We believe that we are a leading global supplier of epoxy, phenolic and coating resins which are used in a variety of industrial and consumer applications to increase strength, adhesion and provide durability. These products are used in numerous end-markets including: oil and gas, wind energy, electronics, protective coatings, engineered materials, automotive, decorative paints, specialty coatings and residential, commercial and industrial construction.

Epoxy resins are the fundamental component of many types of materials and are used either as replacements for traditional materials such as metal, or in applications where traditional materials do not meet demanding engineering applications. Phenolic resins are used in applications that require extreme heat resistance and strength, such as after-market automotive and OEM truck brake pads, aircraft components and electrical laminates. Additionally, epoxy-based surface coatings are among the most widely used industrial coatings due to their structural stability and broad application functionality combined with overall economic efficiency. The demand for epoxy, phenolic and coating resins is driven by both economic growth generally and technological innovation, including environmentally friendly and energy efficient applications.

Supporting the growth in our business, we operate two of the three largest epoxy resins manufacturing facilities in the world, including the world’s only continuous-flow manufacturing process facility. We believe our global scope and our ability to internally produce key raw materials gives us a significant competitive advantage versus our non-integrated competitors. For example, we produce and internally consume the majority of our bisphenol-A, or BPA, and virtually all of our epichlorohydrin, or ECH, the key base chemicals in the downstream manufacturing of base epoxy resins and epoxy specialty resins.

Forest Products Resins

We are a leading global supplier of formaldehyde-based resins used in a variety of industrial and consumer applications. These products are used in numerous end-markets including: residential, commercial and industrial construction, furniture and agriculture. The demand for forest products resins is driven by general economic growth and environmental sustainability and we benefit from a manufacturing footprint that is strategically located in close proximity to our customers. Demand for our formaldehyde-based resins is also primarily driven by the residential housing market globally and in particular North America.

We are the leading producer of formaldehyde-based resins used in a wide range of applications for the North American forest products industry and also hold significant positions in Europe, Latin America, Australia and New Zealand. We are also the world’s largest producer of formaldehyde, a key raw material used to manufacture thousands of products and we internally consume the majority of our formaldehyde production. We believe this strategic back-end integration gives us significant incremental economic value.

Growth and Strategy

We believe that we have opportunities for growth through the following strategies:

Expand Our Global Reach in Faster Growing Regions. We intend to continue to grow internationally by expanding our product sales to our customers around the world. Specifically, we are focused on growing our business in markets in the high growth regions of Asia-Pacific, Latin America, India, Eastern Europe and the Middle East, where the usage of our products is increasing. We are currently expecting new capacity in China to come online in the second half of 2013, which will better enable us to serve our middle-market customers in the region. Furthermore, by consolidating sales and distribution infrastructures via the Momentive Combination, we expect to accelerate the penetration of our high-end, value-added products into new markets, thus further leveraging our research and application efforts and existing global footprint.

Develop and Market New Products. We will continue to expand our product offerings through research and development initiatives and research partnership formations with third parties. Through these innovation initiatives we will continue to create new generations of products and services which will drive revenue and earnings growth. Approximately 25%, 25% and 21% of our 2012, 2011 and 2010 net sales, respectively, were from products developed in the last five years. In 2012, 2011 and 2010 we invested $69 million, $70 million and $66 million, respectively, in research and development.

Increase Shift to High-Margin Specialty Products. We continue to proactively manage our product portfolio with a focus on specialty, high-margin applications and the reduction of our exposure to lower-margin products. As a result of this capital allocation strategy and strong end market growth underlying these specialty segments including wind energy and oil field applications, they will continue to be a larger part of our broader portfolio. Consequently, we have witnessed a strong organic improvement in our profitability profile as a trend over the last several years which we believe will continue.

Continue Portfolio Optimization and Pursue Targeted Add-On Acquisitions and Joint Ventures. The specialty chemicals and materials market is comprised of numerous small and mid-sized specialty companies focused on niche markets, as well as smaller divisions of large chemical conglomerates. As a large manufacturer of specialty chemicals and materials with leadership in the production of thermosets, we have a significant advantage in pursuing add-on acquisitions and joint ventures in areas that allow us to build upon our core strengths, expand our product, technology and geographic portfolio and better serve our customers. We believe we may have the opportunity to consummate acquisitions at relatively attractive valuations due to the scalability of our existing global operations and deal-related synergies. In addition, we have and will continue to monitor the strategic landscape for opportunistic divestments consistent with our broader specialty strategy. For example, we recently completed a joint venture effort to construct a versatics manufacturing facility in China, which began operations in the second quarter of 2012, and also recently announced a joint venture to construct a phenolic specialty resins manufacturing facility in China, which is expected to be operational by the end of 2013. In January 2013, we announced the acquisition of a 50% interest in a forest products joint venture in western Australia, which will provide formaldehyde, urea formaldehyde resins and other products to industrial customers in the region.

Capitalize on the Momentive Combination to Grow Revenues and Realize Operational Efficiencies. We believe the Momentive Combination will present opportunities to increase our revenues by leveraging each of our and MPM’s respective global manufacturing footprints and technology platforms. For example, we anticipate being able to accelerate the penetration of our products into Asia. Further, we anticipate the Momentive Combination will provide opportunities to streamline our business and reduce our cost structure, and are currently targeting $65 million in annual cost savings related to the Momentive Combination. We anticipate these savings to come from logistics optimization, reductions in corporate expenses and reductions in the costs of raw materials and other inputs. Through March 31, 2013, we realized $60 million of these savings on a run-rate basis, and anticipate fully realizing the remaining anticipated savings over the next 12 months.

Generate Free Cash Flow and Deleverage. We expect to generate strong free cash flow over the long-term due to our size, cost structure and reasonable ongoing capital expenditure requirements. Furthermore, we have demonstrated expertise in efficiently managing our working capital. Our strategy of generating significant free cash flow and deleveraging is complemented by our long-dated capital structure with no significant short-term maturities and strong liquidity position. This financial flexibility allows us to prudently balance deleveraging with our focus on growth and innovation.

Risk Factors

Despite our competitive strengths discussed above, investing in the Notes involves a number of risks, including:

As of March 31, 2013, we have approximately $3.8 billion of consolidated outstanding indebtedness, including payments due within the next twelve months and short-term borrowings. In addition, we had $301 million of borrowings available under our ABL Facility. Our substantial debt could adversely affect our operations and prevent us from satisfying our obligations under our debt obligations. In 2013, our cash interest expense is projected to be approximately $297 million based on consolidated indebtedness and interest rates at March 31, 2013, of which $290 million represents cash interest expense on fixed-rate obligations, including variable rate debt subject to interest rate swap agreements;

If global economic conditions remain weak or further deteriorate, it will negatively impact our business operations, results of operations and financial condition;

We may be unable to achieve the cost savings or synergies that we expect to achieve from our strategic initiatives, including the Momentive Combination, which would adversely affect our profitability and financial condition;

Fluctuations in direct or indirect raw material costs could have an adverse impact on our business; and

We depend on certain of our key executives and our ability to attract and retain qualified employees.

For discussion of the significant risks associated with our business, our industry and investing in the notes, you should read the section entitled “Risk Factors.”

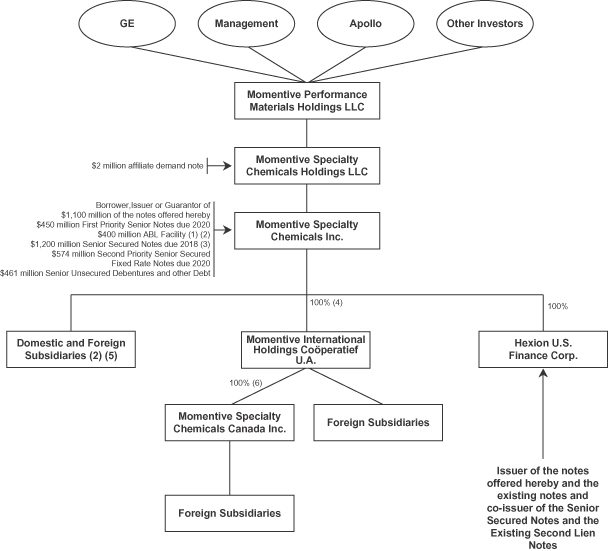

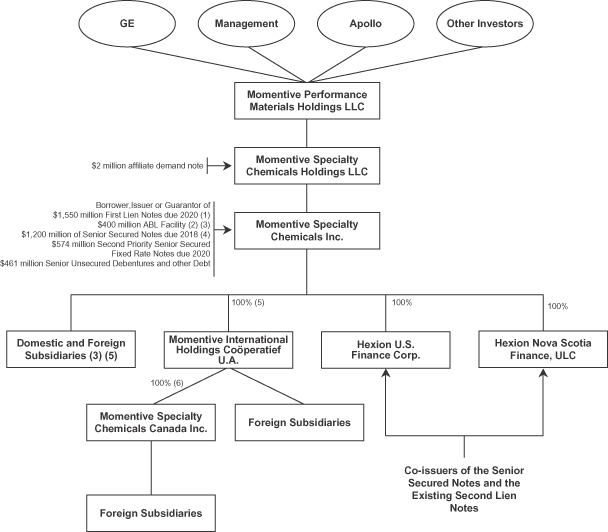

Organizational Structure

Hexion U.S. Finance Corp. is aand Hexion Nova Scotia Finance, ULC are direct wholly-owned subsidiarysubsidiaries of MSC. No separate financial information has been provided in this prospectus for Hexion U.S. Finance Corp. or Hexion Nova Scotia Finance, ULC because (1) Hexion U.S. Finance Corp. hasand Hexion Nova Scotia Finance, ULC have no independent operations other than acting as a finance companyfinancing companies of MSC, (2) Hexion U.S. Finance Corp. hasand Hexion Nova Scotia Finance, ULC have no material assets, and (3) MSC and certain of its domestic subsidiaries guarantee the notes. The indenture governing the notes restricts the IssuerIssuers from conducting any business operations other than those in connection with the issuance of the notes and other similar debt securities.

The following chart summarizes our corporate structure on March 31, 2013:

| (1) | As used in this prospectus, the “First Lien Notes” refer to the 6.625% First-Priority Senior Secured Notes due 2020. The First Lien Notes are secured by senior liens on the collateral. Includes $1,100 million of First Lien Notes issued pursuant to First Lien Notes Offering. |

| (2) | As used in this prospectus, the “ABL Facility” refers to the $400 million asset-based revolving loan facility that we entered into in March 2013 that replaced our prior senior secured credit facilities. Total availability of $400 million, subject to borrowing base availability, of which $301 million was available for borrowings as of March 31, 2013, reflecting a borrowing base after reserves of $348 million and $47 million of outstanding letters of credit. The ABL Facility covenants includes a fixed charge coverage ratio of 1.0 to 1.0 |

| that will only apply if our availability is less than the greater of (a) 12.5% of the lesser of the borrowing base and the total ABL Facility commitments at such time and (b) $40 million. |

| Certain of our non-U.S. subsidiaries are borrowers, or provide guarantees, under the ABL Facility but do not guarantee the notes. |

| The Senior Secured Notes are secured by junior liens on the collateral. Includes $200 million of Senior Secured Notes issued pursuant to the MSC Holdings |

| Direct and indirect ownership. |

| (6) | Indirect |

Additional Information

MSC is a New Jersey corporation, with predecessors dating back to 1899. Our principal executive offices are located at 180 East Broad Street, Columbus, Ohio 43215. Our telephone number is (614) 225-4000. We maintain a website atwww.momentive.com where general information about our business is available. The internet address is provided for informational purposes only and is not intended to be a hyperlink. The information contained on our website is not a part of this prospectus.

Our Equity Sponsor

Apollo Global Management, LLC is a leading global alternative asset manager with offices in New York, Los Angeles, Houston, London, Frankfurt, Luxembourg, Singapore, Hong Kong and Mumbai. As of December 31, 2012, Apollo Global Management, LLC had assets under management of approximately $113.4 billion invested in its private equity, capital markets and real estate businesses.

MSC Holdings Exchange

On January 14, 2013, we and our parent company, Momentive Specialty Chemicals Holdings LLC (“MSC Holdings”), entered into an agreement with the lenders under MSC Holdings’ credit agreement (the “Holdings Lenders”) to exchange all outstanding term loans under such credit agreement (the “Holdings Loans”) for $200 million aggregate principal amount of new 8.875% Senior Secured Notes due 2018 (“Notes”). We refer to this exchange transaction, which closed on January 14, 2013, as the “MSC Holdings Exchange.” We refer to the $1.0 billion aggregate principal amount of 8.875% Senior Secured Notes due 2018, which were issued on January 29, 2010, as the “Existing Senior Secured Notes,” and together with the “Notes,” the “Senior Secured Notes”. As a result of the MSC Holdings Exchange, all outstanding Holdings Loans have been satisfied in full. In connection with the MSC Holdings Exchange, we agreed to assist Credit Suisse Securities (USA) LLC (“Credit Suisse”), which acquired Notes in the MSC Holdings Exchange, in selling its Notes under certain circumstances.

Summary of the Exchange Offer

In connection with the closing of the offering of the initial notes, we entered into a registration rights agreement (as more fully described below) with the initial purchasers of the initial notes. You are entitled to exchange in the exchange offer your initial notes for exchange notes which are identical in all material respects to the initial notes except that:

the exchange notes have been registered under the Securities Act and will be freely tradable by persons who are not affiliated with us;

the exchange notes are not entitled to the registration rights applicable to the initial notes under the registration rights agreement; and

our obligation to pay additional interest on the initial notes due to the failure to consummate the exchange offer by a prior date does not apply to the exchange notes.

Exchange Offer | We are offering to exchange up to |

Expiration Date | This exchange offer will expire at 5:00 p.m., New York City time, on , 2013, unless we decide to extend it. |

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions, some of which we may waive, that include the following conditions: |

there is no change in the laws and regulations which would impair our ability to proceed with this exchange offer;

there is no change in the current interpretation of the staff of the SEC permitting resales of the exchange notes;

there is no stop order issued by the SEC which would suspend the effectiveness of the registration statement which includes this prospectus or the qualification of the exchange notes under the Trust Indenture Act of 1939;

there is no litigation or threatened litigation which would impair our ability to proceed with this exchange offer; and

we obtain all the governmental approvals we deem necessary to complete this exchange offer.

| Please refer to the section in this prospectus entitled “The Exchange Offer—Conditions to the Exchange Offer.” |

Procedures for Tendering Initial Notes | To participate in this exchange offer, you must complete, sign and date the letter of transmittal or its facsimile and transmit it, together with your initial notes to be exchanged and all other documents |

required by the letter of transmittal, to Wilmington Trust, National Association, as exchange agent, at its address indicated under “The Exchange Offer—Exchange Agent.” In the alternative, you can tender your initial notes by book-entry delivery following the procedures described in this prospectus. For more information on tendering your notes, please refer to the section in this prospectus entitled “The Exchange Offer—Procedures for Tendering Initial Notes.” |

Special Procedures for Beneficial Owners | If you are a beneficial owner of initial notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee and you wish to tender your initial notes in the exchange offer, you should contact the registered holder promptly and instruct that person to tender on your behalf. |

Guaranteed Delivery Procedures | If you wish to tender your initial notes and you cannot get the required documents to the exchange agent on time, you may tender your notes by using the guaranteed delivery procedures described under the section of this prospectus entitled “The Exchange Offer—Procedures for Tendering Initial Notes—Guaranteed Delivery Procedure.” |

Withdrawal Rights | You may withdraw the tender of your initial notes at any time before 5:00 p.m., New York City time, on the expiration date of the exchange offer. To withdraw, you must send a written or facsimile transmission notice of withdrawal to the exchange agent at its address indicated under “The Exchange Offer—Exchange Agent” before 5:00 p.m., New York City time, on the expiration date of the exchange offer. |

Acceptance of Initial Notes and Delivery of Exchange Notes | If all the conditions to the completion of this exchange offer are satisfied, we will accept any and all initial notes that are properly tendered in this exchange offer on or before 5:00 p.m., New York City time, on the expiration date. We will return any initial note that we do not accept for exchange to you without expense promptly after the expiration date. We will deliver the exchange notes to you promptly after the expiration date and acceptance of your initial notes for exchange. Please refer to the section in this prospectus entitled “The Exchange Offer—Acceptance of Initial Notes for Exchange; Delivery of Exchange Notes.” |

Federal Income Tax Considerations Relating to the Exchange Offer | Exchanging your initial notes for exchange notes will not be a taxable event to you for U.S. federal income tax purposes. Please refer to the section of this prospectus entitled “Federal Income Tax Considerations.” |

Exchange Agent | Wilmington Trust, National Association is serving as exchange agent in the exchange offer. |

Fees and Expenses | We will pay all expenses related to this exchange offer. Please refer to the section of this prospectus entitled “The Exchange Offer—Fees and Expenses.” |

Use of Proceeds | We will not receive any proceeds from the issuance of the exchange notes. We are making this exchange offer solely to satisfy certain of our obligations under our registration rights agreement entered into in connection with the offering of the initial notes. |

Consequences to Holders Who Do Not Participate in the Exchange Offer | If you do not participate in this exchange offer: |

except as set forth in the next paragraph, you will not necessarily be able to require us to register your initial notes under the Securities Act;

you will not be able to resell, offer to resell or otherwise transfer your initial notes unless they are registered under the Securities Act or unless you resell, offer to resell or otherwise transfer them under an exemption from the registration requirements of, or in a transaction not subject to, the Securities Act; and

the trading market for your initial notes will become more limited to the extent other holders of initial notes participate in the exchange offer.

| You will not be able to require us to register your initial notes under the Securities Act unless: |

an initial purchaser requests us to register initial notes that are not eligible to be exchanged for exchange notes in the exchange offer;

you are not eligible to participate in the exchange offer;

you may not resell the exchange notes you acquire in the exchange offer to the public without delivering a prospectus and the prospectus contained in the exchange offer registration statement is not appropriate or available for such resales by you; or

you are a broker-dealer and hold initial notes that are part of an unsold allotment from the original sale of the initial notes.

| In these cases, the registration rights agreement requires us to file a registration statement for a continuous offering in accordance with Rule 415 under the Securities Act for the benefit of the holders of the initial notes described in this paragraph. We do not currently anticipate that we will register under the Securities Act any notes that remain outstanding after completion of the exchange offer. |

| Please refer to the section of this prospectus entitled “The Exchange Offer—Your Failure to Participate in the Exchange Offer Will Have Adverse Consequences.” |

Resales | It may be possible for you to resell the notes issued in the exchange offer without compliance with the registration and prospectus delivery provisions of the Securities Act, subject to the conditions described under “—Obligations of Broker-Dealers” below. |

| To tender your initial notes in this exchange offer and resell the exchange notes without compliance with the registration and prospectus delivery requirements of the Securities Act, you must make the following representations: |

you are authorized to tender the initial notes and to acquire exchange notes, and that we will acquire good and unencumbered title thereto;

the exchange notes acquired by you are being acquired in the ordinary course of business;

you have no arrangement or understanding with any person to participate in a distribution of the exchange notes and are not participating in, and do not intend to participate in, the distribution of such exchange notes;

you are not an “affiliate,” as defined in Rule 405 under the Securities Act, of ours, or you will comply with the registration and prospectus delivery requirements of the Securities Act to the extent applicable;

if you are not a broker-dealer, you are not engaging in, and do not intend to engage in, a distribution of exchange notes; and

if you are a broker-dealer, initial notes to be exchanged were acquired by you as a result of market-making or other trading activities and you will deliver a prospectus in connection with any resale, offer to resell or other transfer of such exchange notes.

| Please refer to the sections of this prospectus entitled “The Exchange Offer—Procedures for Tendering Initial Notes—Proper Execution and Delivery of Letters of Transmittal,” “Risk Factors—Risks Related to the Exchange Offer—Some persons who participate in the exchange offer must deliver a prospectus in connection with resales of the exchange notes” and “Plan of Distribution.” |

Obligations of Broker-Dealers | If you are a broker-dealer (1) that receives exchange notes, you must acknowledge that you will deliver a prospectus in connection with any resales of the exchange notes, (2) who acquired the initial notes as a result of market making or other trading activities, you may use the exchange offer prospectus as supplemented or amended, in connection with resales of the exchange notes, or (3) who acquired the initial notes directly from the issuers in the initial offering and not as a result of market making and trading activities, you must, in the absence of an exemption, comply with the registration and prospectus delivery requirements of the Securities Act in connection with resales of the exchange notes. |

Summary of Terms of the Exchange Notes

| Hexion U.S. Finance Corp. and Hexion Nova Scotia Finance, ULC. |

Notes Offered | $ |

Maturity Date | The notes will mature on |

Interest |

Guarantees | The notes are guaranteed, jointly and severally, irrevocably and unconditionally, on a senior secured basis, by MSC and certain of its existing domestic subsidiaries that guarantee its obligations under its ABL Facility and MSC’s future domestic subsidiaries that guarantee any debt of MSC, the |

Ranking | The notes and the guarantees are our senior secured obligations. The notes and the guarantees rank: |

senior in priority as to collateral with respect to our and our guarantors’ indebtedness under the ABL Facility, to the extent of the value of the Notes Priority Collateral;

effectively junior in priority as to collateral with respect to our and our guarantors’ indebtednessobligations under theour ABL Facility, the First Lien Notes and any other future obligations secured by a first-priority lien on the collateral (subject to the extentcertain exceptions as described in “Description of the value ofNotes—Security for the ABL Priority Collateral;Notes”);

| • | pari passu in |

senior in priority as to collateral with respect to our and our guarantors’ existing and future obligations under our second-priority senior secured notes and any other future obligations secured by a junior-prioritysecond-priority lien on the collateral, including our other secured notes;collateral; and

senior in right of payment to all of our and our guarantors’ existing and future subordinated indebtedness; andindebtedness.

effectively junior in right of payment to all existing and future indebtedness and other liabilities of any subsidiary that does not guarantee the

| The notes are also effectively junior to the liabilities of our non-guarantor subsidiaries, including our foreign subsidiaries. |

| At March 31, 2013: |

MSC and its subsidiaries had approximately $3.8 billion aggregate principal amount of total indebtedness outstanding, (including the notes and the guarantees), including payments due within the next twelve months and short-term borrowings.$1.2 billion of Senior Secured Notes. In addition, as of such date we had $301 million of borrowings availableavailability under the ABL Facility (subject to borrowing base availability) and $1.55 billion of First Lien Notes, constituting first-priority lien obligations senior to the notes, and $574 million aggregate principal amount of secured indebtedness outstanding constituting junior-priority lien obligations, consisting of our ABL Facility;existing second lien notes and the guarantees thereof; and

MSC’s subsidiaries that are not guarantors with respect to the notes had total indebtedness of approximately $130 million (excludingand total liabilities of $808 million (in each case excluding intercompany liabilities of subsidiaries that are not such obligors).

Collateral | The notes and the guarantees are secured by |

substantially all of MSC’s and each subsidiary guarantor’s tangible and intangible assets (including, but not limited to, accounts receivable, inventory, general intangibles and proceeds of the foregoing), except for those assets excluded as collateral under our ABL Facility; and

all of MSC’s and each subsidiary guarantor’s capital stock of certain direct subsidiaries other than the capital stock which is prohibited from being pledged pursuant to the indentures governing our other outstanding debentures, provided that no more than 65% of the capital stock of first-tier foreign subsidiaries (through which substantially all of our foreign operations are conducted) is required to be pledged, subject to certain exceptions as described below if any such pledge would require that separate financial statements with respect to any such pledged entity (other than Momentive International Holdings Coöperatief U.A., “Momentive Coop,” which is the indirect owner of Momentive Specialty Chemicals Canada, Inc. (“Momentive Canada”)) be provided pursuant to Rule 3-16 of Regulation S-X in connection with the filing of a registration statement related to the notes or any other filing we are required to make with the SEC. See “Description of the Notes—Security for the Notes—Limitations on Stock Collateral.”

Notwithstanding the foregoing, the initial collateral securing the notes does not include (A) any real estate or Principal Property (as such term is defined in the |

in the collateral, |

| See “Risk Factors—Risks Related to an Investment in the |

| The book value of the assets of MSC, and the assets of the domestic subsidiary guarantors, which are included in the collateral, was approximately $2,922 million as of March 31, 2013. |

| Certain of our first-tier foreign subsidiaries, from time to time, could have a value in excess of 20% of the principal amount of the notes, and pledges of the capital stock of such entities would require that separate financial statements pursuant to Rule 3-16 of Regulation S-X be provided in connection with the filing of a registration statement related to the notes or any other filing we are required to make with the SEC. However, pursuant to collateral cut-back provisions in the indenture governing the notes, our pledge of such stock as collateral for the notes |

| The obligations under our ABL Facility also benefit from a security interest in certain assets of certain of our foreign subsidiaries that are borrowers or loan parties thereto. The notes do not have the benefit of a security interest in such foreign assets. The pledge of the stock of certain of our foreign subsidiaries as collateral for the obligations under our ABL Facility also is not subject to any collateral cut back provisions of the type that are applicable to the collateral for the notes. |

The priority of the collateral liens securing the notes is junior to the collateral liens on our and the guarantors’ assets securing the ABL Facility and other obligations secured by first-priority liens as described under “Description of the Notes—Security for the Notes.” The value of collateral securing the notes at any time will depend on market and other economic conditions, including the availability of suitable buyers for the collateral. The liens on the collateral may be released without the consent of the holders of notes if collateral is disposed of in a transaction that complies with the applicable indenture, security documents and intercreditor agreement and otherwise as provided in the indenture and the intercreditor |

agreement. In the event of a liquidation of the collateral, the proceeds may not be sufficient to satisfy the obligations under the notes and any other indebtedness secured on a senior orpari passu basis thereto. See “Risk Factors—Risks Related to an Investment in the Notes—It may be difficult to realize the value of the collateral securing the notes.” |

Intercreditor Agreements | The notes are subject to the terms of an intercreditor agreement pursuant to which the liens securing the notes are junior in priority and subordinated to the liens that secure obligations under the ABL |

| The trustee |

Optional Redemption | We may redeem some or all of the notes before |

|

Change of Control | If we experience a change of control (as defined in the indenture governing the notes), we will be required to make an offer to repurchase the notes at a price equal to 101% of their principal amount, plus accrued and unpaid interest, if any, to the date of repurchase. See “Description of the Notes—Change of Control.” |

|

Certain Covenants | The |

incur or guarantee additional indebtedness or issue preferred stock;

grant liens on assets;

pay dividends or make distributions to our stockholders;

repurchase or redeem capital stock or subordinated indebtedness;

make investments or acquisitions;

enter into sale/leaseback transactions;

incur restrictions on the ability of our subsidiaries to pay dividends or to make other payments to us;

enter into transactions with our affiliates;

merge or consolidate with other companies or transfer all or substantially all of our assets; and

transfer or sell assets.

| These covenants are subject to a number of important limitations and exceptions as described under “Description of the Notes—Certain Covenants.” |

Absence of a Public | The |

Use of Proceeds | We will not receive any proceeds from the issuance of the exchange |

|

Risk Factors | See “Risk Factors” and the other information in this prospectus for a discussion of the factors you should carefully consider before deciding to invest in the notes. |

MOMENTIVE SPECIALTY CHEMICALS INC.

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL DATA

The following table presents MSC’s summary historical financial information for the periods presented. The summary historical financial information for each of the years ended December 31, 2012, 2011 and 2010 has been derived from MSC’s audited Consolidated Financial Statements and related notes and other financial information contained elsewhere in this prospectus. The summary historical financial data for the three months ended March 31, 2013 and 2012 have been derived from MSC’s unaudited Condensed Consolidated Financial Statements and related notes and other information contained elsewhere in this prospectus. In the opinion of management, all adjustments consisting of normal, recurring adjustments considered necessary for a fair statement have been included. Results for the interim periods are not necessarily indicative of results for the entire year.

You should read this data in conjunction with “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and all the financial statements and the related notes included elsewhere in this prospectus.

| As of and for the Year Ended December 31, | As of and for the Three Months Ended March 31, | |||||||||||||||||||

(in millions) | 2012 | 2011 | 2010 | 2013 | 2012 | |||||||||||||||

Statement of Operations | ||||||||||||||||||||

Net sales | $ | 4,756 | $ | 5,207 | $ | 4,597 | $ | 1,192 | $ | 1,236 | ||||||||||

Cost of sales | 4,160 | 4,473 | 3,866 | 1,049 | 1,064 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Gross profit | 596 | 734 | 731 | 143 | 172 | |||||||||||||||

Selling, general & administrative expense | 322 | 335 | 332 | 92 | 85 | |||||||||||||||

Terminated merger and settlement income, net (1) | — | — | (171 | ) | — | — | ||||||||||||||

Asset impairments | 23 | 32 | — | — | 23 | |||||||||||||||

Business realignment costs | 35 | 15 | 20 | 9 | 15 | |||||||||||||||

Other operating expense (income), net | 14 | (16 | ) | 4 | (3 | ) | 5 | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operating income | 202 | 368 | 546 | 45 | 44 | |||||||||||||||

Interest expense, net | 263 | 262 | 276 | 74 | �� | 65 | ||||||||||||||

Loss on extinguishment of debt | — | — | 30 | 6 | — | |||||||||||||||

Other non-operating (income) expense, net | (1 | ) | 3 | (4 | ) | 5 | 2 | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

(Loss) income from continuing operations before income tax, earnings from unconsolidated entities | (60 | ) | 103 | 244 | (40 | ) | (23 | ) | ||||||||||||

Income tax (benefit) expense | (365 | ) | 3 | 35 | (32 | ) | (2 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Income (loss) from continuing operations before earnings from unconsolidated entities | 305 | 100 | 209 | (8 | ) | (21 | ) | |||||||||||||

Earnings from unconsolidated entities, net of taxes | 19 | 16 | 8 | 4 | 5 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) from continuing operations | 324 | 116 | 217 | (4 | ) | (16 | ) | |||||||||||||

Net income (loss) from discontinued operations, net of taxes (2) | — | 2 | (3 | ) | — | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) | $ | 324 | $ | 118 | $ | 214 | $ | (4 | ) | $ | (16 | ) | ||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Dividends declared per common share | $ | 0.04 | $ | 0.02 | $ | — | $ | — | $ | — | ||||||||||

Cash Flow Data | ||||||||||||||||||||

Cash flows provided by (used in) operating activities | $ | 177 | $ | 171 | $ | 51 | $ | (33 | ) | $ | 18 | |||||||||

Cash flows (used in) provided by investing activities | (138 | ) | 33 | (105 | ) | (27 | ) | (28 | ) | |||||||||||

Cash flows (used in) provided by financing activities | (59 | ) | 57 | 97 | 58 | (22 | ) | |||||||||||||

| As of and for the Year Ended December 31, | As of and for the Three Months Ended March 31, | |||||||||||||||||||

(in millions) | 2012 | 2011 | 2010 | 2013 | 2012 | |||||||||||||||

Other Financial Data | ||||||||||||||||||||

Cash and equivalents | $ | 419 | $ | 419 | $ | 166 | $ | 400 | ||||||||||||

Short-term investments | 5 | 7 | 6 | 6 | ||||||||||||||||

Working capital (3) | 669 | 682 | 551 | 705 | ||||||||||||||||

Total assets | 3,325 | 3,096 | 3,118 | 3,510 | ||||||||||||||||

Total long-term debt | 3,419 | 3,420 | 3,588 | 3,727 | ||||||||||||||||

Total net debt (4) | 3,071 | 3,113 | 3,500 | 3,382 | ||||||||||||||||

Total liabilities | 4,642 | 4,861 | 5,137 | 5,052 | ||||||||||||||||

Total deficit | (1,317 | ) | (1,765 | ) | (2,019 | ) | (1,542 | ) | ||||||||||||

EBITDA (5) | 375 | 550 | 719 | 82 | 85 | |||||||||||||||

Transaction and terminated merger and settlement income, net, asset impairments, non-cash charges and integration costs included in EBITDA (6) | 66 | 60 | (163 | ) | 14 | 46 | ||||||||||||||

Unusual items included in EBITDA (7) | 49 | 25 | 51 | 9 | 15 | |||||||||||||||

Twelve months ended March 31, 2013 Adjusted | 480 | |||||||||||||||||||

| (1) | Terminated merger and settlement income, net for the year ended December 31, 2010 includes the non-cash push-down of insurance recoveries by the Company’s owner related to the settlement payment made by the Company’s owner that had been treated as an expense of the Company for the year ended December 31, 2008 associated with the terminated merger with Huntsman Corporation, as well as reductions on certain of the Company’s merger related service provider liabilities. |

| (2) | Net income (loss) from discontinued operations reflects the results of our global inks and adhesive resins business (the “IAR Business”) and our North American coatings and composite resins business (the “CCR Business”). |

| (3) | Working capital is defined as current assets less current liabilities. As of December 31, 2010, the assets and liabilities of the IAR Business and CCR Business totaling $184 million have been classified as current. |

| (4) | Net debt is defined as long-term debt plus short-term debt less cash and cash equivalents and short-term investments. |

| (5) | EBITDA is defined as Net income (loss) (excluding loss (gain) on extinguishment of debt) before interest, income taxes and depreciation and amortization. We have presented EBITDA because we believe that EBITDA is useful to investors since it is frequently used by securities analysts, investors and other interested parties to evaluate companies in our industry. EBITDA is not a recognized term under U.S. Generally Accepted Accounting Principles (“GAAP”), should not be viewed in isolation and does not purport to be an alternative to Net income as an indicator of operating performance or cash flows from operating activities as a measure of liquidity. There are material limitations associated with making the adjustments to our earnings to calculate EBITDA and using this non-GAAP financial measure as compared to the most directly comparable U.S. GAAP financial measures. For instance, EBITDA does not include: |

interest expense, and because we have borrowed money in order to finance our operations, interest expense is a necessary element of our costs and ability to generate revenue;

depreciation and amortization expense, and because we use capital assets, depreciation and amortization expense is a necessary element of our costs and ability to generate revenue; and

tax expense, and because the payment of taxes is part of our operations, tax expense is a necessary element of our costs and ability to operate.

Additionally, EBITDA is not intended to be a measure of free cash flow for management’s discretionary use, as it does not consider certain cash requirements such as capital expenditures, contractual commitments, interest payments, tax payments and debt service requirements. Because not all companies use identical calculations, this presentation of EBITDA may not be comparable to other similarly titled measures for other companies. Also the amounts shown for EBITDA as presented herein differ from the amounts calculated under the definition of Adjusted EBITDA used in our debt instruments, which further adjust for certain cash and non-cash charges and is used to determine compliance with financial covenants and our ability to engage in certain activities such as incurring additional debt and making acquisitions.

See below for a reconciliation of Net income (loss) to EBITDA.

| Year Ended December 31, | Three Months Ended March 31, | Year Ended December 31, | Three Months Ended March 31, | |||||||||||||||||||||||||||||||||||||

(in millions) | 2012 | 2011 | 2010 | 2013 | 2012 | 2012 | 2011 | 2010 | 2013 | 2012 | ||||||||||||||||||||||||||||||

Reconciliation of Net Income (Loss) to EBITDA | ||||||||||||||||||||||||||||||||||||||||

Net income (loss) | $ | 324 | $ | 118 | $ | 214 | $ | (4 | ) | $ | (16 | ) | $ | 324 | $ | 118 | $ | 214 | $ | (4 | ) | $ | (16 | ) | ||||||||||||||||

Income tax (benefit) expense | (365 | ) | 3 | 35 | (32 | ) | (2 | ) | (365 | ) | 3 | 35 | (32 | ) | (2 | ) | ||||||||||||||||||||||||

Loss on extinguishment of debt | — | — | 30 | 6 | — | — | — | 30 | 6 | — | ||||||||||||||||||||||||||||||

Interest expense, net | 263 | 262 | 276 | 74 | 65 | 263 | 262 | 276 | 74 | 65 | ||||||||||||||||||||||||||||||

Depreciation and amortization | 153 | 167 | 164 | 38 | 38 | 153 | 167 | 164 | 38 | 38 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

EBITDA | $ | 375 | $ | 550 | $ | 719 | $ | 82 | $ | 85 | $ | 375 | $ | 550 | $ | 719 | $ | 82 | $ | 85 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

| (6) | Amounts for the years ended December 31, 2012, 2011 and 2010 and the three months ended March 31, 2013 and 2012 consist of the following items: |

| Year Ended December 31, | Three Months Ended March 31, | |||||||||||||||||||

(in millions) | 2012 | 2011 | 2010 | 2013 | 2012 | |||||||||||||||

Terminated merger and settlement income, net | $ | — | $ | — | $ | (171 | ) | $ | — | $ | — | |||||||||

Integration costs | 12 | 19 | — | 3 | 5 | |||||||||||||||

Asset impairments | 23 | 32 | — | — | 23 | |||||||||||||||

Non-cash items (a) | 31 | 9 | 8 | 11 | 18 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total | $ | 66 | $ | 60 | $ | (163 | ) | $ | 14 | $ | 46 | |||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| (7) | Amounts for the years ended December 31, 2012, 2011 and 2010 and the three months ended March 31, 2013 and 2012 consist of the following items: |

| Year Ended December 31, | Three Months Ended March 31, | |||||||||||||||||||

(in millions) | 2012 | 2011 | 2010 | 2013 | 2012 | |||||||||||||||

Business realignment costs (b) | $ | 35 | $ | 15 | $ | 20 | $ | 9 | $ | 15 | ||||||||||

Net (income) loss from discontinued operations (c) | — | (2 | ) | 3 | — | — | ||||||||||||||

Other (d) | 14 | 12 | 28 | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total | $ | 49 | $ | 25 | $ | 51 | $ | 9 | $ | 15 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| (a) | Primarily includes stock-based compensation expense, accelerated depreciation and unrealized derivative and foreign exchange gains and losses. |

| (b) | Represents plant rationalization and headcount reduction expenses related to productivity programs and other costs associated with business realignments. |

| (c) | Represents the results of the IAR Business and CCR Business. |

| (d) | Primarily includes business optimization expenses, management fees, retention program costs and certain intercompany or non-operational realized foreign currency activity. |

| (8) | See “Covenant Compliance” for our reasons for presenting LTM Adjusted EBITDA, a reconciliation of Net Loss to LTM Adjusted EBITDA and qualifications as to the use of LTM Adjusted EBITDA, which is not a recognized term under U.S. GAAP. |

Ratio of Earnings to Fixed Charges

| Three Months Ended March 31, 2013 | Year Ended December 31, | |||||||||||||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||||||||||||

Ratio of earnings to fixed charges and preferred stock dividends (1) | — | — | 1.37 | 1.84 | 1.57 | — | ||||||||||||||||||||||||

| (1) | Due to the net losses in the three months ended March 31, 2013 and the years ended December 31, 2012 and 2008, the ratio of earnings to fixed charges and preferred stock dividends was less than 1. Our earnings were insufficient to cover fixed charges and preferred stock dividend requirements by $40 million, $60 million and $1,171 million for the three months ended March 31, 2013 and the years ended December 31, 2012 and 2008, respectively. |

Investing in the exchange notes in this exchange offer involves a high degree of risk. You should carefully consider the risks described below in addition to the other information set forth in this prospectus before participating in the exchange offer. Any of the following risks could materially adversely affect our business, financial condition or results of operations and prospects, which in turn could adversely affect our ability to make payments with respect to the notes. In such case, you may lose all or part of your original investment.

Risks Related to an Investment in the Notes

The notes are effectively subordinated to all liabilities of our non-guarantor subsidiaries and structurally subordinated to claims of creditors of all of our foreign subsidiaries.

The notes are structurally subordinated to indebtedness and other liabilities of MSC’s subsidiaries that are not the IssuerIssuers or guarantors of the notes. As of March 31, 2013, MSC’s subsidiaries that are not the IssuerIssuers or guarantors had total indebtedness of approximately $130 million and total liabilities of $808 million (in each case, excluding intercompany liabilities of such non-guarantor subsidiaries). In the event of a bankruptcy, liquidation or reorganization of any of our non-guarantor subsidiaries, these non-guarantor subsidiaries will pay the holders of their debts, holders of preferred equity interests and their trade creditors before they will be able to distribute any of their assets to MSC or the Issuer.Issuers.

The notes are not guaranteed by any of MSC’s non-U.S. subsidiaries. MSC’s non-U.S. subsidiaries are separate and distinct legal entities and have no obligation, contingent or otherwise, to pay any amounts due pursuant to the notes, or to make any funds available therefor, whether by dividends, loans, distributions or other payments. Any right that MSC or the subsidiary guarantors have to receive any assets of any of the foreign subsidiaries upon the liquidation or reorganization of those subsidiaries, and the consequent rights of holders of notes to realize proceeds from the sale of any of those subsidiaries’ assets, will be effectively subordinated to the claims of those subsidiaries’ creditors, including trade creditors and holders of preferred equity interests of those subsidiaries.

Additional indebtedness is secured by the collateral securing the notes, and the notes will be secured only to the extent of the value of the assets that have been granted as security for the notes and the guarantees, which may not be sufficient to satisfy our obligations under the notes.

Indebtedness under our First Lien Notes and our ABL Facility, the interest rate protection and other hedging agreements, cash management agreements and the overdraft facility pursuantpermitted thereunder (referred(collectively referred to herein as the “ABL“First-Priority Lien Obligations”), are secured by first-priority liens on the ABL Priority Collateralsubstantially all tangible and otherintangible assets of MSC and its subsidiaries and junior liens on the Notes Priority Collateral.each subsidiary guarantor, except for certain excluded collateral (such as our Principal Properties). The notes are secured by a lien on only a portion of the assets that secure the other indebtedness permitted to be securedpari passuwith the notes (referred to herein as other “First-PriorityFirst-Priority Lien Obligations”) and the ABL Obligations and there may not be sufficient collateral to pay all or any of the notes. In the event of a bankruptcy, liquidation, dissolution, reorganization or similar proceeding against us or any future domestic subsidiary, the assets that are pledged as shared collateral securing the other First-Priority Lien Obligations and the notes must be used first to pay the other First-Priority Lien Obligations andin full before making any payments on the notes. Accordingly, the notes ratably, as set forth inwill be effectively subordinated to these obligations to the first lien intercreditor agreement.extent of the collateral securing such obligations. We may incur additional First-Priority Lien Obligations and ABL Obligations in the future.

As of March 31, 2013, we had $3.8 billion of outstanding indebtedness, including the notes and guarantees and including $450 million$1.2 billion of other First-Priority Lien Obligations constituting the existing notes.Senior Secured Notes. As of March 31, 2013, borrowings of $301 million were available under our ABL Facility. In addition to other First-Priority Lien Obligations, the indenture governing the notes allows a significant amount of other indebtedness and other obligations to be secured by a lien on the collateral securing the notes on an equal and ratable basis, provided that, in

each case, such indebtedness or other

obligation could be incurred under the debt and lien incurrence covenants contained in the indenture governing the notes. Any additional obligations secured by an equal priority lien on the collateral securing the notes will adversely affect the relative position of the holders of the notes with respect to the collateral securing the notes.

Many of our assets, such as certain assets owned by our foreign subsidiaries, are not part of the collateral securing the notes, but do secure some other First-Priority Lien Obligations and secure the ABL Facility. In addition, our foreign subsidiaries will be permitted to incur substantial indebtedness in compliance with the covenants under our ABL Facility, the indenture governing the First Lien Notes, the indentures governing the junior-priority secured notes, the indenture governing the notes and the agreements governing our other indebtedness, most of which is permitted to be other First-Priority Lien Obligations. We are also permitted to transfer assets from guarantors to non-guarantor subsidiaries, including non-U.S. subsidiaries in compliance with the covenants under the indenture. Upon such a transfer, those assets will be released automatically from the lien securing the notes. With respect to those assets that are not part of the collateral securing the notes but which secure other obligations, the notes will be effectively junior to these obligations to the extent of the value of such assets. There is no requirement that the holders of the other First-Priority Lien Obligations or ABL Obligations first look to these excluded assets before foreclosing, selling or otherwise acting upon the collateral shared with the notes.

No appraisals of any collateral have been prepared in connection with the offering of the notes. The value of the collateral at any time will depend on market and other economic conditions, including the availability of suitable buyers for the collateral. By their nature, some or all of the pledged assets may be illiquid and may have no readily ascertainable market value. The value of the assets pledged as collateral for the notes could be impaired in the future as a result of changing economic conditions, our failure to implement our business strategy, competition and other future events or trends. In the event of a foreclosure, liquidation, bankruptcy or similar proceeding, no assurance can be given that the proceeds from any sale or liquidation of the collateral will be sufficient to pay our obligations under the notes, in full or at all, while also payingafter first satisfying our obligations in full under the Other First-Priority Lien Obligations in accordance with the first lien intercreditor agreement.

In the event of a bankruptcy, liquidation, dissolution, reorganization or similar proceeding against us orand any future guarantor, all proceeds from ABL Priority Collateral will be applied first to repay theother obligations in respect of the ABL Facility and, second, to repay the obligations in respect of the notes and other First Priority Lien Obligations that are secured by a Lien that ispari passu withpriority lien on the notes, and proceeds from Notes Priority Collateral will be applied first to repay the obligations in respect of the notes and other First Priority Lien Obligations that are secured by a Lien that ispari passu with the notes and, second, to repay the obligations in respect of the ABL Facility. No assurance can be given that the proceeds from any sale or liquidation of the collateral will be sufficient to pay our obligations under the notes, in full or at all, while also paying obligations under the ABL Facility and other First Priority Lien Obligations that are secured by a Lien that ispari passu with the notes.collateral.

Accordingly, there may not be sufficient collateral to pay all or any of the amounts due on the notes. Any claim for the difference between the amount, if any, realized by holders of the notes from the sale of the collateral securing the notes and the obligations under the notes will rank equally in right of payment with all of our other unsecured unsubordinated indebtedness and other obligations, including trade payables.