|X| ANNUAL REPORT UNDER SECTION 13 OR 15 (D) OF THE

SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2007

|_| TRANSITION REPORT PURSUANT TO SECTION 13 OF 15 (D) OF THE

SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM TO

COMMISSION FILE NUMBER: 000-26807

CYTOGENIX, INC.

(Exact name of registrant as specified in its charter)

Nevada 76-0484097

(State or other jurisdiction of incorporation) (I.R.S. Employer Identification or organization No.)

3100 WILCREST, SUITE 140, HOUSTON, TEXAS 77042

(Address of principal executive offices) (Zip Code)

Issuer’s telephone number, including area code: 713-789-0070

Securities registered under Section 12 (b) of the Exchange Act: NONE

Securities registered under Section 12 (g) of the Exchange Act:

COMMON STOCK WITH $.001 PAR VALUE

(Title of Class)

Indicate by check mark if the Registrant is a well known seasoned issuer as defined in Rule 405 of the securities Act. Yes |_| No |X| Indicate by check mark if Registrant is not required to file reports pursuant to Section 13 or Section 15 (d) of the Act. Yes |_| No |X|

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes |X| No |_|

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. |X|

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |_|

Accelerated Filer |X|

Non-accelerated filer || Smaller reporting company [ ]

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes |_| No |X|

The aggregate market value of the voting stock held by non-affiliates of the Registrant as of June 30, 2007 (the last business day of the Registrant’s most recently completed second fiscal quarter) was approximately $56,265,584. The number of outstanding shares of the Registrant’s Common Stock as of the close of business on March 17, 2008was 146,660,968.

DOCUMENTS INCORPORATED BY REFERENCE

Selected portions of the definitive Proxy Statement of CytoGenix, Inc., which will be filed with the Securities and Exchange Commission within 120 days after December 31, 2007, are incorporated by reference in Part III of this form 10-K.

2

CYTOGENIX, INC.

FORM 10-K INDEX

PART I

&nbs p; Page

Item 1.

Description of Business ……………………………………….................................................................................................................... 5

Submission of Matters to a Vote of Security Holders ……….........................................................................................................………. 26

PART II

Item 5.

Market for Common Equity and Related Stockholder Matters ……........................................................................................................… 27

Item 6.

Selected Financial Data ………………………………………….....................................................................................................…… 29

Item 7.

Management’s Discussion and Analysis of Financial Conditions and

Results of Operations ……………………………………….....................................................................................................………… 29

Item 7A.

Quantitative and Qualitative Disclosures about Market Risk …….........................................................................................................….. 37

Controls and Procedures …………………………………………....................................................................................................…... 60

Item 9B.

Other Information ………………………………………………….....................................................................................................…. 60

PART III

Item 10.

Directors and Executive Officers of the Registrant ……………........................................................................................................…….. 61

Security Ownership of Certain Beneficial Owners and Management

And Related Stockholder Matters …………………………….....................................................................................................……… 64

Item 13.

Certain Relationships and Related Transactions …….......................................................................................................……………….. 64

3

Item 14.

Principal Accountant Fees and Services …………….......................................................................................................………………. 64

PART IV

Item 15.

Exhibits, Financial Statement Schedules and Reports on Form 8-K…........................................................................................................ 64

CytoGenix, Inc. (“CytoGenix” or “the Company”) is a biopharmaceutical company whose primary focus is the development and commercialization of its proprietary technologies for identifying and silencing disease causing genes, expressing proteins for applications such as vaccines and isolating novel nucleic acid-based anti-microbial compounds. The Company’s three technologies include: i) gene silencing techniques (ssDNA) applicable to genes from pathogenic organisms or selected genes from a patient to prevent the expression of harmful proteins, thereby preventing or ameliorating disease; ii) a novel, cell free process to produce large quantities of DNA (synDNA™) for use in its own products and for sale to other biopharmaceutical or life science companies; and iii) a methodology to isolate and characterize novel DNA-based drugs (Oligogenix™) to which harmful bacteria have not developed immunity. The Company seeks to generate revenues and improve the health and well-being of humans, animals and plants by utilizing its technology to produce molecular therapies. In addition to development and commercialization of therapeutic compounds, the Company seeks to provide the service of custom DNA manufacturing as well as to sell and/or license its technology to other research facilities and companies seeking to research or regulate a specific gene function and to consumers of plasmid DNA.

The Company was formed in 1995 as a biomedical research and development company. The original name of the Company was Cryogenic Solutions, Inc., until the Company changed its name to CytoGenix, Inc. in January 2000. Equity funding has been the primary source of operational, research and commercialization working capital since the Company’s inception. The Company made a transition to research and development of its present technologies in 1998. Since then, the Company has dedicated itself to engineering DNA-based molecules for therapeutic and drug target identification purposes. The Company’s expertise in nucleic acid technology enables it to focus on the development of new types of nucleic acid-based therapeutics.

GENE EXPRESSION AND HUMAN DISEASE

Widely published scientific studies conducted over the last 20 years by leading universities, government research laboratories such as the National Institutes of Health and the National Cancer Institute, and private research laboratories, have established that most diseases are the result of malfunctioning genes in an organism’s genome, or the activities of genes expressed by pathogens such as viruses, bacteria or fungi. This genetic activity causes the production of harmful proteins that lead to the symptoms and destructive results of diseases. Examples of diseases caused by the production of such harmful proteins include cancer, herpes, sepsis (blood poisoning) and a host of others. To produce a protein, a cell first makes a positive copy (messenger RNA) of the DNA code containing the information necessary to produce the protein. This messenger RNA (mRNA) is called the “sense” molecule. This message-carrying molecule then moves to

5

another part of the cell where it participates in the assembly of the biochemical components to produce proteins.

In many instances it is possible to inhibit the production of these harmful proteins by introducing or producing small molecules of specific genetic material into the cells themselves. This genetic activity can be interrupted and controlled at three levels with the introduction of multiple copies of a specific sequence of single stranded DNA (“ssDNA”) into the cells at the level of the genomic DNA itself, interfering with the transcription of the messenger RNA (“mRNA”) or by directly binding to a protein to disable it.

CYTOGENIX GENE SILENCING TECHNOLOGY

CytoGenix owns patented intracellular expression system technology to produce desired sequence-specific, ssDNA molecules in individual cells for the purpose of triplex, antisense, catalytic DNA, and aptamer applications.

1.

Triplex: As mRNA is transcribed and the DNA strands are still separated, a single strand of complementary DNA is inserted into the gap forming a triple helix (triplex) structure, thus preventing the future production of mRNA from that segment.

2.

Antisense: Messenger RNA is intercepted en route by a complementary ssDNA sequence that it binds to and results in the destruction of the mRNA by enzymes within the cell, thus preventing the mRNA from producing the undesired protein.

3.

Catalytic DNA: Similar to antisense, an ssDNA sequence containing sequence regions binds to the mRNA, but also contains a unique sequence region that acts to cut and destroy the mRNA, thus preventing it from producing the undesired protein.

4.

Aptamer: The ssDNA binds to the protein itself in the cell and causes the undesired protein to become inactivated or dysfunctional.

The key to success with these genetic interventions is to insure that sufficient quantities of the ssDNA molecules ultimately are produced in targeted cells or induced from external sources. CytoGenix has invented a compound that functions as a tiny biological “factory” and after its introduction into the cell, actually produces many copies of specific ssDNA molecules in the cell. A major element of CytoGenix’s business is to refine this technology and apply it to the delivery of various patented DNA molecules for the development of effective therapeutic drugs.

DEVELOPMENTS TO DATE (RESEARCH AND DEVELOPMENT)

The ssDNA expression vector technology originated with the work of Dr. Charles Conrad, which he developed while at InGene, Inc. The original expression cassette technology is protected by issued United States Patent No. 6,054,299 entitled, “Methods and Compositions for Producing Single-stranded cloned DNA in eukaryotic cells.” In

6

1999, CytoGenix purchased the rights to Dr. Conrad’s patent as well as other proprietary information from InGene, and has since instituted a broad research and development program to advance single stranded DNA expression technology. Applications to protect

subsequent improvements and therapeutic applications of this technology have since been filed to expand the protection of this technology in both the US and foreign markets. As of December 31, 2007 CytoGenix holds a patent portfolio of approximately 13 granted and 2 allowances with approximately 55 additional foreign or US pending patent applications claiming methods and materials in connection with our platform technologies. This assertive approach for protection of the Company’s technology has enabled CytoGenix to expand and refine the development of therapeutics for human, animal and agricultural use. The Company currently holds thirteen granted patents covering the early ssDNA expression technology in US and foreign markets, and one US and one foreign allowance for our Herpes therapeutic.

These patents are important to the Company because they help form the basis of the technology needed for the production of the Company’s complementary technology and other products. The technology has been proven in numerous laboratory and animal experiments and has been widely published as set forth below. It has been reported in scientific literature, such as in Reuters Business Insight 2000 publication, Antisense Therapy: Technical Aspects and Commercial Opportunities by Prof. Dr. K.K. Jain, M.D. that other molecule delivery methods have failed to provide sufficient quantities to be therapeutically effective except in limited applications. Laboratory cell culture studies have demonstrated that the Company’s ssDNA expression vector can adequately deliver sequence specific DNA molecules in sufficient quantities in virtually all cell types, thereby overcoming many of the challenges previously experienced. As described under “CytoGenix Gene Silencing Technology” above, the Company’s technology is not limited to only antisense applications, but can target and enzymatically cleave target mRNA using DNA enzyme formulations. As described above, the technology can also be used to (i) generate triplex forming oligonucleotides that bind to specific sites in the genome itself to inhibit expression by the gene at that site, (ii) generate ssDNA that bind to specific, targeted proteins to neutralize them and (iii) competitively inhibit genetic expression/transcription of targeted genes. The Company has successfully extended the results achieved in cell cultures to cells in live animals.

The genomics field has vastly expanded the number of potential drug targets. The Company has utilized its ssDNA expression technology to develop a library screening technique for gene target identification and validation. The CytoGenix proprietary gene neutralization system is a powerful tool in confirming gene target function. The screening library technique enables efficient testing of multiple oligonucleotide sequences. When a sequence silences a targeted gene, the construct for introducing the identified sequence in cellular and animal experiments is readily produced. Use of the screening library has led to the discovery of sequences that have been useful in several of the Company’s products under development.

The Company has developed a novel screening library technique to identify oligonucleotides with specific activity against bacteria in a given culture. This technology platform is called Oligogenix™ and has been used to produce compounds with activity against bacteria using mimetic oligonucleotides as sequences to silence targeted bacterial genes. Targeted genes include those necessary for the bacteria’s

7

survival, reproduction and/or for the expression of various toxins. Animal studies using these compounds have demonstrated cytotoxic activity against bacterial species including echerichia coli, methicillin resistant and vancomycin resistant Staphylococcus aureus.

The Company has also developed a novel cell-free large scale DNA synthesis technique (synDNA™) for producing therapeutic DNA which bypasses the bacteria-based fermentation process. The cell-free synthesis of DNA has various advantages: CytoGenix’s DNA is virtually free of bacterial endotoxins, as well as bacterial DNA, RNA and proteins which must be removed from DNA manufactured using traditional fermentation process using live bacteria. CytoGenix’s process does not require the use of antibiotic markers and does not require genetic sequences comprising the usual backbone of plasmid DNA. Elimination of the plasmid backbone enables production of DNA constructs that are approximately 3 kilobase pairs smaller than the equivalent plasmid DNA. More importantly, the synDNA™ technology can produce therapeutic DNA’s more rapidly and with fewer complications than in the traditional fermentation methods.

Using its expanding technological base, the Company is seeking to develop drugs that address significant and unmet medical needs. The Company is conducting research and/or preclinical development with product candidates in the following areas: infectious disease (anti-virals and anti-bacterials), inflammation, cancer and vaccines.

PRODUCTS UNDER DEVELOPMENT:

INFECTIOUS DISEASE PROGRAM

ANTI-VIRAL: Our herpes therapeutic, SIMPLIVIR™, is an anti-herpes topical compound which will potentially address the needs of 70 million infected Americans. Today’s marginally effective products have revenues in excess of $1 billion. The most likely methods of use include prophylactic and neonatal applications. The Company’s proprietary plasmid DNA sequences are believed to turn-off the expression of the HSV ICP4 and ICP47 genes. Found in HSV-1, -2, Herpes Zoster, and other viruses in that family, the ICP4 gene is critical for the replication of the virus in the host cell. The ICP47 gene produces a protein that assists the virus in interfering with a host’s immune system in recognizing the virus and eliminating it. Pre-clinical, in vitro studies have shown a 100-fold reduction in HSV viral load in test cells containing the Company’s proprietary plasmid DNA coded with an ICP4 knockdown sequence. Mouse trials have been conducted and additional studies with cotton rats are planned. Pre-clinical toxicology, absorption, distribution, metabolism and excretion (ADME) studies are being designed and will enable the filing of an Investigational New Drug (IND) application with the Food & Drug Administration (FDA) in the near future.

ANTI-MICROBIALS: Using its proprietary technique (Oligogenix™), the Company has developed and tested compounds against methicillin and vancomycin resistant Staphylococcus aureaus (MRSA and VRSA). Additional studies to determine dosages and minimum inhibitory concentrations are planned. These anti-bacterial compounds also require ADME studies.

DNA VACCINES: Using the synDNA™ process, the Company is developing DNA vaccines for use in humans and animals.

8

HUMAN VACCINES:

DNA vaccines against both seasonal influenza as well as the highly pathogenic and potentially pandemic humanized avian influenza virus (H5N1) are being developed and tested in choice animal models (mice and ferrets). Together with ADME and toxicology studies, additional pre-clinical studies have been planned in order to analyze the immune response triggered as well as optimize the immunization regimen.

ANIMAL VACCINES:

Poultry: Utilizing the knowledge and experience gathered from the development of DNA vaccines against human influenza, studies on developing vaccines for use in poultry against avian flu are under development. Potential collaborators in both academic and industry settings are being approached.

Aquaculture: In other extramural collaborations, the Company is developing DNA vaccines for use in fish. Focus has been given to fish species of high economic impact such grouper, salmon and Cobia. The Company has identified target viral diseases and it is determining the optimal course of action to generate and test various DNA constructs.

Cattle: Finally, in collaboration with the United States Department of Agriculture, the Company is engaged in a project to develop a synDNA™ based vaccine against brucellosis, a zoonotic disease which is easily transmitted from animals to humans and is consequently of global importance. Tests using various DNA vaccines developed by the Company as well as various combinatory formulas have been completed in a laboratory animal model. Ongoing analysis of the data gathered should provide information as to the next course of action to be taken.

CANCER PROGRAM

The Company has sponsored research with scientists at Albert Einstein College of Medicine/Montefiore Medical Center for preclinical experiments using the Company’s ssDNA expression vector technology to silence a gene that has been shown to cause malignant transformation of tumor cells.

synDNA™ PROCESS

As briefly noted above, the Company has developed a novel method for producing large amounts of high quality therapeutic DNA (synDNA™) with reductions in residual contaminants compared to traditional fermentation methods. Specifically, the Company has identified and developed a method for in vitro DNA synthesis and amplification for the production of good manufacturing practice-grade (GMP) drug substances.

Cell-free amplification of DNA sequences has many important benefits beginning with the size and composition of the therapeutic compound. Under this system, there is no need for bacterial replication genes or selection markers such as antibiotic resistant genes found on most plasmid vectors. In most cases, this will reduce the size and weight of the therapeutic DNA by at least 3,000 base pairs or a molecular weight of approximately

9

2,000 kilo Daltons (kDa). The Dalton is a measure of molecular weight or mass. The total absence of bacteria and growth media assures that there is no need to employ mechanical or chemical purification methods to extract cell or animal proteins, RNA, genomic DNA and backbone molecules. This feature allows the designer more control of coding for non-specific and specific immune responses.

Robust biological activity

The Company’s experiments have shown that the biological response to this material (devoid of vector backbone) is similar to traditional plasmids. Experiments conducted in several animal models have shown that linear DNA prepared with the CytoGenix synDNA™ process triggers a robust biological response (immune or physiological, depending on the application) in treated groups similar to plasmid DNA -treated animals.

Low risk, competitive cost, universal accessibility and fast cycle time.

The entire process is bench-scale and requires little equipment, space or human intervention in comparison to bioprocess or bacterial fermentation manufacturing facilities. This process easily lends itself to liquid-handling automation, and a skilled technician can synthesize multi-gram quantities of this material within a few weeks, while working in a compact room-size facility. Unlike PCR, this process requires only basic laboratory equipment and is therefore accessible to many facilities around the world, especially field facilities in rural settings where access to specialized equipment is limited and often prohibitive.

Improved regulatory profile

The benefits of using this cell-free DNA manufacturing technology are significant from a regulatory agency review and compliance perspective. Product cGMP manufacturing procedures detailing methods for cell collection, processing and cell culture conditions are no longer necessary and therefore reduces the level of risk, amount of documentation, amount of required space, as well as QA/QC and compliance costs.

CytoGenix is carrying out a multi-pronged strategy to continue commercializing this technology. The following summarizes the Company’s activities and plans:

o

PROCESS OPTIMIZATION AND SCALE-UP: The Company is conducting continued experimentation to achieve yield optimization, efficiency and reduced costs. The process has progressed from manufacture of milligram quantities to producing gram quantities consistently. The Company has conducted animal studies comparing synDNA™ compounds with various plasmids to verify that the synDNA™ based compounds exert bioactivity equal to or greater than plasmids produced via traditional methods. These studies have analyzed various Company produced DNA vaccines and compounds for expressing specific proteins.

10

o

DEVELOP REAGENT SUPPLIERS AND SOURCING: The Company entered into an Agreement with General Electric Healthcare Bio-Science Corporation (“GEHBC”) to provide necessary enzymes and reagents for large-scale production of DNA using the synDNA™ process for therapeutic applications. GEHBC is the Company’s largest supplier of enzymes and reagents, however other sources are available for the Company’s research purposes.

o

BUSINESS DEVELOPMENT, the Company is currently evaluating options for industry partnership for continued development of the process including contract manufacturing.

The Company is currently supporting the following Sponsored Research Agreements (SRA):

1.

Dr. Cy Stein’s laboratory at Montefiore Medical Center is using CytoGenix’s proprietary gene silencing DNA technology against a gene found in melanoma cells that produces a protein known to counteract the effect of several chemotherapeutic agents in difficult to treat cancers. This project is completed and scientific papers summarizing study results are being prepared.

2.

Dr. Jeffrey Actor’s laboratory at University of Texas Health Science Center in Houston is conducting animal trials to determine efficacies of CytoGenix’s antimicrobial oligodeoxynucleotides (ODN) compounds.

3.

Dr. David Weiner’s laboratory at University of Pennsylvania has conducted animal trials to determine efficacies of CytoGenix’s synDNA™ vaccines against Smallpox and HIV. This project is completed and scientific papers summarizing study results are being prepared.

4.

Dr. Slobodan Paessler at the University of Texas Medical Branch at Galveston is conducting animal trials to test CytoGenix’s synDNA™ vaccine against avian flu (H5N1). Several challenge rounds have been conducted exposing vaccinated mice to lethal doses of the Vietnam strain of avian flu. A significant majority of vaccinated mice survived the exposure. All animals in the control groups died. These experiments are continuing with the use of ferrets as a second animal model. The collaboration with Dr. Paessler has been extended for development of DNA vaccines with veterinary applications.

COOPERATIVE AGREEMENTS

The Company is currently working under a cooperative research and development agreement (CRADA) with the United States Department of Agriculture to develop and test a DNA vaccine against brucellosis.

11

The Company is currently working under a CRADA with the United States Army Medical Research Institute for Infectious Diseases to develop and test DNA vaccines for strains of ebola and equine encephalitis.

The Company has entered into a collaborative Agreement with Taiwan Cobia, Inc., a Taiwanese aquaculture company, to develop DNA vaccines against fish viruses.

In addition to the industry and government agency relationships disclosed above, the Company is actively seeking out-licensing opportunities in the application of the Company’s core technologies in the following areas:

1. infectious diseases;

2. inflammation;

3. cancer; and

4. animal health.

There can be no assurance the Company will be able to enter into licensing arrangements and thereby generate licensing revenues.

PUBLICATIONS

The Company and its cooperating university scientists have published a number of scientific papers and presented at scientific meetings. These publications include:

1.

Kendirgi, F., Nadezda E. Yun, N.E, Linde, N.S., Zacks, M.A, Smith, J.N., Smith, J.K., McMicken, H., Chen, Y.*, & Paessler, S. Novel linear DNA vaccines induce protective immune responses against lethal infection with influenza virus type A/H5N1 (under review).

2.

Benimetskaya, L., Ayyanar, K. Kornblum, N., Castanotto, D., Rossi, J., Wu, S., Lai, J., Brown, B., Popova, N., Miller, P., McMicken, H., Chen, Y. & Stein, C. Bcl-2 protein in 518A2 melanoma cells in vivo and in vitro. Clinical Cancer Research, 12:4940-4948, 2006.

3.

Xing-Xin Tan & Yin Chen, Discovery of Novel Antibiotics By screening of an Oligodeoxynucleotide Expression Library, (invited review article, submitted) “New Research on Antisense Elements (Genetics).” Frank Columbus, Editor-in-Chief, Nova Science Publishers, Inc.

4.

Tan, X. & Chen, Y., A novel genomic approach identifies bacterial DNA-dependent RNA polymerase as the target of an antibacterial oligodeoxynucleotide, RBL-1 Biochemistry, 44:6708-6714, 2005.

5.

Tan, X., Actor, J.K., & Chen, Y., PNA antisense oligomer as a therapeutic strategy against bacterial infection: proof of principle using mouse peritonitis model, Antimicrobial Agent and Chemotherapy, 49: 3203-3207, 2005.

6.

Tan, X., & Chen, Y., Discovery of novel antibiotics using cell-based screening (Review), Current Drug Discovery, pp. 21-23, April, 2004.

7.

Tan, X., Knesha, R., Margolin, W. and Chen, Y., DNA enzyme generated by a novel single-stranded DNA expression vector inhibits expression of the essential bacterial cell division gene ftsZ, Biochemistry, 43:1111-1117, 2004.

12

8.

McMicken, H., Bates, P. and Chen, Y., Antiproliferative activity of G-quartet-containing oligonucleotides generated by a novel single-stranded DNA expression system, Cancer Gene Therapy, 10(12):867-869, 2003.

9.

Chen, Y. and McMicken, H., Intracellular production of DNA enzyme by a novel single-stranded DNA expression vector, Gene Therapy, 10:1776-1780, 2003.

10.

Chen, Y., Ji, Y. and Conrad, C., Expression of single-stranded DNA in mammalian cells, Biotechniques, 34:167-171, 2003.

Datta, H. and Glazer, P., Intracellular generation of single-stranded DNA for chromosomal triplex formation and induced recombination, Nucleic Acid Research, 29:5140-5147, 2001. A marvel of biochemical engineering means cells can produce DNA enzyme to attach cancer, New Scientist, January, 2001.

16.

Chen, Y., Ji, Y., Roxby, R. and Conrad, C., In vivo expression of single-stranded DNA in mammalian cells with DNA enzyme sequences targeted to c-raf, Antisense & Nucleic Acid Drug Development, 10:415-422, 2000.

BUSINESS STRATEGY

The goal and the focus of the Company are to leverage its proprietary technology to maximize shareholder value. The Company is developing anti-viral and anti-bacterial products based on its proprietary technologies including: topical compounds for herpes infections, DNA vaccines, and compounds against methicillin and vancomycin resistant bacteria. Upon initiation of clinical trials, the Company intends to seek license and distribution agreements with domestic and foreign pharmaceutical companies. To this end:

o

The Company will pursue partnerships with pharmaceutical or biotechnology companies to develop DNA expression-based therapeutics.

o

The Company will seek to maintain and expand its patent portfolio and proprietary technology. The Company aggressively pursues patent protection to maintain worldwide rights relating to the development, manufacture and sale of oligodeoxynucleotide mediated therapeutics and services and products related to the manufacture of synDNA™ and ssDNA.

o

The Company intends to leverage its oligonucleotide expertise through licensing, process development and pilot manufacturing. The Company believes that it has established one of the leading nucleic acid chemistry groups that can provide medicinal chemistry, process development and manufacturing to others in need of this expertise. The Company believes that

13

it will be able to capitalize on its continuing investment in oligonucleotide and nucleic acid technology by entering into licensing, process development and pilot manufacturing arrangements with collaborators to generate revenues, while retaining this capability for its own drug development.

o

The Company plans to expand its customer base of non-competitors for uses of synDNA™ as it advances the ability to amplify and purify diverse sequences. The sales will come from excess capacity above the material the Company needs for its own product development. The Company will seek strategic partners to expand the production and distribution of synDNA™ based products.

MARKETING STRATEGY

The Company plans to market initial products, when developed, and for which it will obtain regulatory approval, through marketing arrangements or other licensing arrangements with pharmaceutical companies. Implementation of this strategy will depend on many factors, including the market potential of any products the Company develops, and its financial resources. To market products that will serve a large, geographically diverse patient population, we expect to enter into licensing, distribution, or partnering agreements with pharmaceutical companies that have large, established sales organizations. The timing of the Company’s entry into marketing arrangements or other licensing arrangements with large pharmaceutical companies will depend on successful product development and regulatory approval within the regulatory framework established by the Federal Food, Drug and Cosmetics Act, as amended, and regulations promulgated there under. Although the implementation of initial aspects of the Company’s marketing strategy may be undertaken before this process is completed, the development and approval process typically is not completed in less than three to five years after the filing of an Investigational New Drug (“IND”) application and its marketing strategy therefore may not be implemented for several years. See “Drug Approval Process and Other Governmental Regulation” below.

INTELLECTUAL PROPERTY RIGHTS

The Company has developed or acquired a comprehensive body of intellectual rights. The proprietary nature of, and protection for, the Company’s technology, processes and know-how are important to its business. The Company plans to prosecute and aggressively defend its patents and proprietary technology. Our policy is to seek patent protection for technologies, inventions, and improvements that are considered important to the development of our business. The Company also depends upon trade secrets, know-how, and continuing technological innovation to develop and maintain its competitive position.

CytoGenix currently holds 13 granted and 2 allowances with approximately 55 additional foreign or US pending patent applications claiming methods and materials in connection with these platform technologies. The Company intends to protect its proprietary technology with additional filings as appropriate.

14

DRUG APPROVAL PROCESS AND OTHER GOVERNMENT REGULATION

The system of reviewing and approving drugs in the United States is considered the most rigorous in the world. Estimates of the upper range of costs to bring a single product from research through market approval and launch into commerce range from $800 million (Pharmaceutical Research and Manufacturers Association) to $1.7 billion in 2000 through 2002 (FDA), with the timing to do so typically ranging between 10 and 15 years. The Pharmaceutical Research and Manufacturers Association estimates that of every 5,000 medicines tested, on average, only five are tested in clinical trials, and only one of those is approved for human use. These estimates may vary depending on the nature of the drug and the mechanism by which it works.

DRUG DISCOVERY

The drug discovery process can take several years. Once a company locates a screening lead, or starting point for drug development, isolation and structural determination may begin. The development process results in numerous chemical modifications to the screening lead in an attempt to improve its drug properties. After a compound emerges from the above process, the next steps are to conduct further preliminary studies on the mechanism of action, further in vitro (test tube) screening against particular disease targets and, finally, some in vivo (animal) screening. If the compound passes these barriers, the toxic effects of the compound, if any, are analyzed by performing preliminary exploratory animal toxicology. If the results are positive, the compound emerges from the basic research mode and moves into the pre-clinical phase.

Preclinical Testing

During the pre-clinical testing stage, laboratory and animal studies are conducted to show biological activity of the compound against the targeted disease, and the compound is evaluated for safety, stability, biodistribution (where the drug goes in the body) and genomic integration (where the DNA is incorporated in any of the body’s cell’s genome).

Investigational New Drug Application

During the pre-clinical testing, an Investigational New Drug Application (“IND”) is filed with the FDA to seek permission to begin human testing of the drug. The IND becomes active if not rejected by the FDA within 30 days. The IND must indicate the results of previous experiments, how, where and by whom the studies were conducted, the chemical structure of the compound, the method by which it is believed to work in the human body, any toxic effects of the compound found in the animal studies and how the compound is manufactured. Progress reports detailing the results of the clinical trials must be submitted at least annually to the FDA.

Phase I Clinical Trials

After an IND becomes active, Phase I human clinical trials may begin. These tests, involving usually between 20 and 80 patients or healthy volunteers, typically take approximately one year to complete and cost between $300,000 and $500,000 per trial. The Phase I clinical studies also determine how a drug is absorbed, distributed,

15

metabolized and excreted by the body, and the duration of its action. Phase I trials are not normally conducted for anticancer product candidates. A Phase Ib study involves patients with the targeted disease cancer and is focused on safety.

Phase II Clinical Trials

In Phase II Clinical trials, controlled studies are conducted on approximately 100 to 300 volunteer patients with the targeted disease. The preliminary purpose of these tests is to evaluate the effectiveness of the drug on the volunteer patients as well as to determine if there are any side effects. These studies generally take approximately two years and cost between $500,000 and $4 million per trial. In addition, Phase I/ II clinical trials may be conducted to evaluate not only the efficacy of the drug on the patient population, but also its safety.

Phase III Clinical Trials

This phase typically lasts about three years, usually involves 1,000 to 3,000 patients and costs between $5 million and $50 million per trial. During the Phase III clinical trials, physicians monitor the patients to determine efficacy and to observe and report any reactions that may result from long-term use of the drug.

New Drug Application

After the completion of the requisite three phases of clinical trials, if the data indicate that the drug has an acceptable benefit to risk assessment and it is found to be safe and effective, a New Drug Application (“NDA”) is filed with the FDA. The requirements for submitting an NDA are defined by the FDA. These applications are comprehensive, including all information obtained throughout all clinical trials as well as all data pertaining to the manufacturing and testing of the product. In general, these filings can far exceed 100,000 pages. With the implementation of the Prescription Drug Users Fee Act (PDUFA), review fees are provided at the time of NDA filing. In 2007, each NDA with clinical data must be accompanied by an $896,200 review fee. If the NDA is assessed as unacceptable in the initial 30 day review, it is returned to the submitter, with 50% of the fee. The historical average review time for a New Molecular Entity (NME) has remained static at approximately 16 months, however, a new NME can be approved in as little as six months.

Marketing Approval

If the FDA approves the NDA, the drug becomes available for physicians to prescribe. Periodic reports must be submitted to the FDA, including descriptions of any adverse reactions reported. The FDA may request additional studies (Phase IV) to evaluate long-term effects.

Phase IV Clinical Trials and Post Marketing Studies

In addition to studies requested by the FDA after approval, these trials and studies are conducted to explore new indications. The purpose of these trials and studies and related

16

publications is to broaden the application and use of the drug and its acceptance in the medical community.

COMPETITION

The pharmaceutical and biotechnology industries are highly competitive. The Company faces competition from biotechnology and pharmaceutical companies using more traditional approaches to treating human diseases. The Company’s competitors may develop safer, more effective or less costly gene-based therapeutics. In addition, the Company faces and will continue to face competition from other companies for corporate collaborations with pharmaceutical and biotechnology companies, for establishing relationships with academic and research institutions and for licenses to proprietary technology, including intellectual property.

Many of the Company’s competitors and potential competitors have substantially greater product development capabilities and financial, scientific, manufacturing, managerial and human resources than the Company. There can be no assurance that research and development by others will not render the Company’s products, or the products developed by corporate partners using its licensed technologies obsolete, or non-competitive, or that any product the Company or its corporate partners develop will be preferred to any existing or newly developed technologies. In addition, there can be no assurance that the Company’s competitors will not develop safer, more effective or less costly cardiovascular therapies, gene delivery systems, gene therapeutics, non-gene therapies, or other therapies, achieve superior patent protection or obtain regulatory approval of product commercialization earlier than the Company, any of which could have a material adverse effect on its business, financial condition or results of operations.

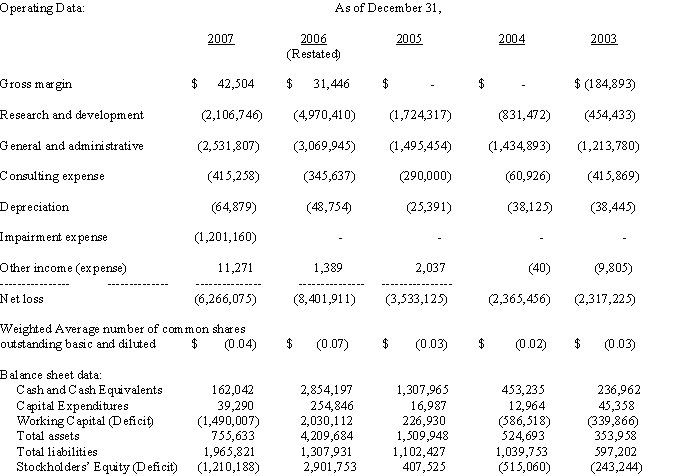

RESEARCH AND DEVELOPMENT

The Company expensed $2,106,746, $4,970,410, and $1,724,317 on research and development activities during the years ended December 31, 2007, 2006, and 2005, respectively. Research and development (R&D) expenses include related salaries and other share based compensation, contractor fees, materials, and utilities.

R&D expenses also consist of independent R&D costs and costs associated with collaborative development arrangements with other companies and research institutions. Research and development costs are expensed as incurred.

EMPLOYEES

As of December 31, 2007, the Company has 8 employees, 6 of whom hold advanced degrees. None of the Company’s employees are covered by collective bargaining agreements, and the Company considers relations with its employees to be good.

HOW YOU CAN FIND ADDITIONAL INFORMATION

The Company is a reporting company and files annual, quarterly and current reports, proxy statements and other information with the SEC. For further information with respect to the Company, you may read and copy its reports, proxy statements and other

17

information, at the SEC public reference rooms at 100 F. Street, N.E., Washington, D.C. 20549, as well as at the SEC’s regional offices at 500 West Madison Street, Suite 1400, Chicago, IL 60661 and at 233 Broadway, New York, NY 10279. You can request copies of these documents by writing to the SEC and paying a fee for the copying cost. Please call the SEC at 1-800-SEC-0330 for more information about the operation of the public reference rooms. The Company’s SEC filings are also available at the SEC’s web site at http://www.sec.gov. In addition, you can read and copy the Company’s SEC filings at the office of the National Association of Securities Dealers, Inc. at 1735 K Street, N.W., Washington, D.C. 2006.

Copies of CytoGenix’s Annual Reports on Form 10K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are all available on its website (www.cytogenix.com) or by sending a request for a paper copy to: CytoGenix, Inc. 3100 Wilcrest, Suite 140, Houston, TX 77042, attn. Investor Relations.

ITEM 1A.

RISK FACTORS

RISKS AFFECTING FUTURE OPERATING RESULTS

The Company does not provide forecasts of its future financial performance. While the Company is optimistic about its long-term prospects, the following factors should be considered in evaluating its outlook. If the possibilities described as risks below actually occur, the Company’s operating results and financial condition would likely suffer and the trading price of its common stock may fall, causing a loss of some or all of an investment in its common stock.

There is substantial doubt about CytoGenix’s ability to continue as a going concern.

CytoGenix has had negligible revenues since inception and only approximately $144,000 in the last two years. The Company has incurred losses totaling $37,726,040 from inception through December 31, 2007. Because of these conditions, CytoGenix will require additional working capital to develop business operations which it can in no way be assured of doing.

There are no assurances that CytoGenix will be able to achieve a level of revenue adequate to generate sufficient cash flow from operations or obtain additional financing necessary to support CytoGenix’s working capital requirements. To the extent that funds generated from any private placements, public offerings and/ or bank financing are insufficient, CytoGenix will have to raise additional working capital. No assurance can be given that additional financing will be available, or if available, will be on terms acceptable to CytoGenix. If adequate working capital is not available, CytoGenix may not increase its operations.

CytoGenix’s products are in the pre-clinical stage of development and may not be determined to be safe or effective.

18

The Company is in the pre-clinical stages of development with its biopharmaceutical products. The Company has devoted almost all of its time to research and development of its technology and products, protecting its proprietary rights and establishing strategic alliances. The Company’s proposed products are in the pre-clinical stages of development and will require significant further research, development, clinical testing and regulatory clearances. The proposed products are subject to development risks. These risks include the possibilities that any of the products could be found to be ineffective or toxic, or could fail to receive necessary regulatory clearances. The Company has not received any significant revenues from the sale of products, and the Company may not successfully develop marketable products that will increase sales and, given adequate margins, make it profitable. Competitors may develop superior or equivalent, but less expensive, products. The Company has incurred net losses since its inception, and the Company may not achieve or sustain profitability.

The Company incurred a net loss of $ 6.26 million in 2007, $8.40 million in 2006 and $3.53 million in 2005. As of December 31, 2007, total shareholder’s deficit was $1,210,188. Losses have resulted principally from expenses incurred in research and development of technology and products, and general and administrative expenses that the Company has incurred while building its business infrastructure. The Company expects to continue to incur significant operating losses in the future as it continues its research and development efforts and seeks to obtain regulatory approval of its products. The Company’s ability to achieve profitability depends on its ability to raise additional capital, complete development of its products, obtain regulatory approvals and market those products. It is uncertain when, if ever, the Company will become profitable.

If the Company fails to attract significant additional capital, the Company may be unable to continue to successfully develop its products.

Since the Company began operations, the Company has obtained operating funds primarily by selling common stock. Based on its current plans, the Company does not believe that current cash balances will be sufficient to meet its operating and capital needs throughout 2008. Furthermore, the actual amount of funds that will be needed will be determined by many factors, some of which are beyond the Company’s control. These factors include the success of its research and development efforts, the status of its pre-clinical and clinical testing, costs relating to securing regulatory approvals and the costs and timing of obtaining new patent rights, regulatory changes, competition and technological developments in the market. The Company may need funds sooner than currently anticipated.

If necessary, potential sources of additional funding could include strategic relationships, public or private sales of shares of common stock or debt or other arrangements. The Company may not obtain additional funding when the Company needs it on terms that will be acceptable to it or at all. If the Company raises funds by selling additional shares of common stock or securities convertible into common stock, the ownership interest of existing shareholders will be diluted. If the Company is unable to obtain financing when needed, its business and future prospects could be materially adversely affected.

If the Company fails to receive necessary regulatory approvals, the Company will be unable to commercialize its products. All of the Company’s products are subject to

19

extensive regulation by the United States Food and Drug Administration, or FDA, and by comparable agencies in other countries. The FDA and comparable agencies require new pharmaceutical products to undergo lengthy and detailed clinical testing procedures and other costly and time-consuming compliance procedures. The Company does not know when or if it will be able to submit its products for regulatory review. Even if the Company submits a new drug application, there may be delays in obtaining regulatory approvals, if the Company obtains them at all. Sales of the Company’s products outside the United States will also be subject to regulatory requirements governing clinical trials and product approval. These requirements vary from country to country and could delay introduction of products in those countries. The Company cannot provide assurance that any of its products will receive marketing approval from the FDA or comparable foreign agencies.

The Company may fail to compete effectively, particularly against larger, more established pharmaceutical companies, causing its business to suffer.

The biotechnology industry is highly competitive. The Company competes with companies in the United States and abroad that are engaged in the development of similar pharmaceutical technologies and products. They include: biotechnology, pharmaceutical, chemical and other companies; academic and scientific institutions; governmental agencies, and public and private research organizations.

Many of these companies and many other competitors have significantly greater financial and technical resources as well as superior production and marketing capabilities than the Company does. The biopharmaceutical industry is characterized by extensive research and development and rapid technological progress. Competitors may successfully develop and market superior or less expensive products which render the Company’s products less valuable or unmarketable.

The Company has limited operating experience.

The Company has engaged solely in the development of biopharmaceutical technology. Although some members of the Company’s management team have experience in biotechnology operations, the Company has limited experience in manufacturing or selling biopharmaceutical products. The Company also has only limited experience in negotiating and maintaining strategic relationships, and in conducting clinical trials and other later-stage phases of the regulatory approval process. The Company may not successfully engage in some or all of these activities.

The Company has limited manufacturing capability.

While the Company believes that it can produce materials for clinical trials and produce products for human use at its synDNA™ production suite, the Company may need to expand its commercial manufacturing capabilities for products in the future if the Company elects not to or cannot successfully partner with others to manufacture its products. This expansion may occur in stages, each of which would require regulatory approval, and product demand could at times exceed supply capacity. The Company has not obtained regulatory approvals for any production facilities for its products, nor can the Company assure investors that it will be able to do so.

20

If the Company loses key personnel or is unable to attract and retain additional, highly skilled personnel required for its activities, its business will suffer.

Competition for qualified personnel in the biopharmaceutical industry is intense, and the Company’s success will depend on its ability to attract and retain highly skilled personnel. The Company is not aware of any key personnel who plan to retire or otherwise leave the Company in the near future other than Malcolm Skolnick who has expressed his desire to retire after the Company identifies a new Chief Executive Officer.

Asserting, defending and maintaining the Company’s intellectual property rights could be difficult and costly, and failure to do so will harm its ability to compete.

The Company’s success will depend on existing patents and licenses, and its ability to obtain additional patents in the future. The purpose of our patent portfolio of approximately 70 domestic and foreign patents and patent applications is to protect the Company’s technologies.

The Company cannot assure investors that its pending patent applications will result in patents being issued in the United States or foreign countries. In addition, the patents which have been or will be issued may not afford meaningful protection for its technology and products. Competitors may develop products similar to the Company’s which do not conflict with its patents. Others may challenge the Company’s patents and, as a result, the patents could be narrowed or invalidated. The patent position of biotechnology firms generally is highly uncertain, involves complex legal and factual questions, and has recently been the subject of much litigation. No consistent policy has emerged from the United States Patent and Trademark Office (USPTO), or the courts regarding the breadth of claims allowed, or the degree of protection afforded under biotechnology patents. In addition, there is a substantial backlog of biotechnology patent applications at the USPTO and the approval or rejection of patents may take several years.

CytoGenix’s success will also depend partly on its ability to operate without infringing upon the proprietary rights of others, as well as its ability to prevent others from infringing on its proprietary rights. The Company may be required at times to take legal action to protect its proprietary rights and, despite its best efforts, the Company may be sued for infringing on the patent rights of others. The Company has not received any communications or other indications from owners of related patents or others that such persons believe the Company’s products or technology may infringe their patents. Patent litigation is costly and, even if the Company prevails, the cost of such litigation could adversely affect its financial condition. If the Company does not prevail, in addition to any damages the Company might have to pay, the Company could be required to stop the infringing activity or obtain a license. Any required license may not be available to the Company on acceptable terms, or at all. If the Company fails to obtain a license, its business might be materially adversely affected.

To help protect its proprietary rights in unpatented trade secrets, the Company requires its employees, consultants and advisors to execute confidentiality agreements. However, such agreements may not provide the Company with adequate protection if confidential information is used or disclosed improperly. In

21

addition, in some situations, these agreements may conflict with, or be subject to, the rights of third parties with whom the Company’s employees, consultants or advisors have prior employment or consulting relationships. Furthermore, others may independently develop substantially equivalent proprietary information and techniques, or otherwise gain access to the Company’s trade secrets.

If CytoGenix’s strategic relationships are unsuccessful, its business could be harmed.

The Company’s strategic relationships with its collaborators and partners are important to its success. The development, improvement and marketing of many of its key therapeutic products are or will be dependent, in part, on the efforts of the Company’s strategic partners. For example, under the GE Healthcare relationship, the Company may fail to achieve product development milestones; GE Healthcare may fail to perform its obligations under the agreement, such as failing to produce an adequate supply of sufficient quality raw materials to produce synDNA™; and the agreement with GE Healthcare may be subject to termination in the event of a breach. The Company may not be commercially successful in its effort to produce and/or sell synDNA™. The transactions contemplated by its agreements with strategic partners, including equity purchases and cash payments, are subject to numerous risks and conditions. The occurrence of any of these events could severely harm CytoGenix’s business.

The Company’s near-term strategy is to develop its own products as well as co-develop products with strategic partners, or to license the marketing rights for its products to pharmaceutical partners after the Company completes one or more Phase II clinical trials. In this manner, the extensive costs associated with late-stage clinical development and marketing will be shared with, or will be the responsibility of, the Company’s strategic partners.

To fully realize the potential of its products, including development, production and marketing, the Company may need to establish other strategic relationships.

The Company has limited sales capability and may not be able to successfully commercialize its products.

The Company has been engaged solely in the development of biopharmaceutical technology. Although some of its management have experience in biotechnology company operations, the Company has limited experience in manufacturing or selling pharmaceutical products. The Company also has only limited experience in negotiating and maintaining strategic relationships, and in conducting clinical trials and other later-stage phases of the regulatory approval process. To the extent the Company relies on strategic partners to fully commercialize its products, the Company will be dependent on their efforts. The Company may not successfully engage in any of these activities.

The Company may be subject to product liability lawsuits and its insurance may not be adequate to cover damages.

22

The Company believes it carries adequate insurance for the product development research it currently conducts. In the future, when the Company has products available for commercial sale and use, the use of its products will expose it to the risk of product liability claims. Although the Company intends to obtain product liability insurance coverage, product liability insurance may not continue to be available to it on acceptable terms and its coverage may not be sufficient to cover all claims. A product liability claim, even one without merit or for which the Company has substantial coverage, could result in significant legal defense costs, thereby increasing expenses, lowering earnings and, depending on revenues, potentially resulting in additional losses.

Continuing efforts of government and third party payers to contain or reduce the costs of health care may adversely affect the Company’s revenues and future profitability.

In addition to obtaining regulatory approval, the successful commercialization of its products will depend on the Company’s ability to obtain reimbursement for the cost of the product and treatment. Government authorities, private health insurers and other organizations, such as health maintenance organizations are increasingly challenging the prices charged for medical products and services. Also, the trend toward managed health care in the United States, the growth of healthcare organizations such as HMOs, and legislative proposals to reform healthcare and government insurance programs could significantly influence the purchase of healthcare services and products, resulting in lower prices and reducing demand for products. The cost containment measures that healthcare providers are instituting and any healthcare reform could affect the Company’s ability to sell its products and may have a material adverse effect on operations. Reimbursement in the United States or foreign countries may not be available for any of the Company’s products, any reimbursement granted may be reduced or discontinued, and limits on reimbursement available from third-party payers may reduce the demand for, or the price of, its products. The lack or inadequacy of third-party reimbursements for its products could have a material adverse effect on the Company’s operations. Additional legislation or regulation relating to the healthcare industry or third-party coverage and reimbursement may be enacted in the future that adversely affects the Company’s products and its business.

If the Company fails to establish strategic relationships with larger pharmaceutical partners, its business may suffer.

The Company does not intend to conduct late-stage (Phase III) human clinical trials on its own. The Company anticipates entering into relationships with larger pharmaceutical companies to conduct later trials and to market its products. The Company also plans to continue to use contract manufacturing for late stage clinical and commercial quantities of its products. The Company may be unable to enter into corporate partnerships which could impede its ability to bring its products to market. Any such corporate partnerships, if entered into, may not be on favorable terms and may not result in the successful development or marketing of the Company’s products. If the Company is unsuccessful in establishing advantageous clinical testing, manufacturing and marketing relationships, it is not likely to generate significant revenues and become profitable.

23

RISKS RELATED TO SHARE OWNERSHIP

CytoGenix’s right to issue preferred stock and/or its classified Board of Directors may delay a takeover attempt and prevent or frustrate any attempt to replace or remove the then current management of the Company by shareholders.

Authorized capital consists of 300,000,000 shares of common stock and 50,000,000 shares of preferred stock. The Company’s board of directors, without any further vote by the shareholders, has the authority to issue preferred shares and to determine the price, preference, rights and restrictions, including voting and dividend rights, of these shares. The rights of the holders of shares of common stock may be affected by the rights of holders of any preferred shares that the board of directors may issue in the future. For example, the board of directors may allow the issuance of preferred shares with more voting rights, higher dividend payments or more favorable rights upon dissolution, than the shares of common stock or special rights to elect directors.

The Company has a “classified” board of directors, which means that only one-third of its directors are eligible for election each year. Therefore, if shareholders wish to change the composition of the Board of Directors, it could take at least two years to remove a majority of the existing directors or three years to change all directors. Having a classified board of directors may, in some cases, delay mergers, tender offers or other possible transactions which may be favored by some or a majority of the Company’s shareholders and may delay or frustrate action by shareholders to change the then current Board of Directors and management.

CytoGenix’s stock price is volatile and may fluctuate due to factors beyond its control.

Historically, the market price of the Company’s stock has been highly volatile as reflected in the table in Part II, Item 5 of this report. The following types of announcements could have a significant impact on the price of the Company’s common stock: positive or negative results of testing and clinical trials by the Company or its competitors; delays in entering into corporate partnerships; technological innovations or commercial product introductions by the Company or its competitors; changes in government regulations; developments concerning proprietary rights, including patents and litigation matters; public concern relating to the commercial value or safety of any of the Company’s products; financing or other corporate transactions; or general stock market conditions.

Further, the stock market experiences significant price and volume fluctuations. These fluctuations have particularly affected the market prices of equity securities of many biopharmaceutical companies that are not yet profitable. Often, the effect on the price of such securities is unrelated or disproportionate to the operating performance of such companies. These broad market fluctuations may adversely affect the ability of a shareholder to dispose of his or her shares at a price equal to or above the price at which the shares were purchased.

The significant number of the Company’s shares of Common Stock eligible for future sale may cause the price of its common stock to fall.

24

The Company has 146,309,719 shares of common stock outstanding as of December 31, 2007 and substantially all are eligible for sale under Rule 144 or are otherwise freely tradable.

CytoGenix’s employees have been granted options to buy a total of 24,286,000 shares of common stock as of December 31, 2007. The options granted have exercise prices between $.185 and $1.01 per share. The shares of common stock granted in the options under the stock option plan have not been registered as of December 31, 2007.

The Company may issue options to purchase up to an additional 11,714,000 shares of common stock as of December 31, 2007 under its stock option plans.

Sales of substantial amounts of shares into the public market could lower the market price of the common stock.

The Company does not expect to pay dividends in the foreseeable future.

The Company has never paid dividends on its shares of common stock and does not intend to pay dividends in the foreseeable future. Therefore, an investment should only be made with the expectation of realizing a return through capital appreciation. An investment should not be made with the expectation of dividend income.

ITEM 1B.

UNRESOLVED STAFF COMMENTS

On August 9, 2007, the Company received a letter from the SEC with comments regarding it filings on Form 10-K for the fiscal year ended December 31, 2006 and on its Form 10-Qs for the fiscal quarters ending March 31, 2007, June 30, 2007 and September 31, 2007. The Company responded to the letter and entered into discussions with the staff regarding its filings and subsequently restated its filings for the indicated periods. The Company believes there are no unresolved staff comments but the staff may provide further comments regarding its 10-K/A and 10-Q/As.

ITEM 2.

DESCRIPTION OF PROPERTY

The Company’s corporate executive offices are located at 3100 Wilcrest, Suite 140, Houston, Texas 77042. The Company has occupied approximately 6000 square feet of executive office and laboratory space since December 2003. The facility is in reasonable condition and is adequate for the Company’s current operations. Rent on the facility averages to be $5,701 per month with a lease term ending September 2009. The Company believes it’s current and contracted for facilities are suitable and adequate for its present and immediately foreseeable future operational requirements.

ITEM 3.

LEGAL PROCEEDINGS

WILLIAM B. WALDROFF AND APPLIED VETERINARY GENOMICS, INC. V. CYTOGENIX, INC.

25

Waldroff and Applied Veterinary Genomics, Inc. - Litigation initiated in March 2004 over the validity of license agreements between CytoGenix (licensor) and William Waldroff (licensee) for use of CytoGenix ssDNA expression technology in shrimp and horse therapeutic applications. AVGI, as sublicensee, was a third party in this action. A jury trial held in February 2005 resulted in entry of a judgment against CytoGenix requiring performance on the contracts and payment of attorney fees. CytoGenix subsequently appealed this decision and in December 2006 the 1st Court of Appeals reversed the trial court's judgment, finding no need for CytoGenix to perform on the contracts and no need for either party to pay the opposing party's attorney fees. Waldroff and Applied Veterinary Genomics filed a motion for a rehearing and CytoGenix filed a timely response to that motion.On March 3, 2007, the Court of Appeals denied Waldroff/AVGI’s Motion forRehearing. Waldroff filed a petition for review by the Supreme Court of Texas which was denied. The Supreme Court directed the Court of appeals to issue a Mandate to finalize the action. The Mandate was issued and the Company recovered its appeal bond and the matter was finalized.

DEFAMATORY ACTIONS

The Company has actively pursued legal action against various parties involved in the posting of defamatory comments about the Company and several of its officers on public investor chat-room websites. A settlement was reached with a poster who published an apology on Investor’s Hub (www.investorshub.com) in March 2007.

EMPLOYMENT ACTIONS

In November of 2006, the former Chief Financial Officer (CFO), Lawrence Wunderlich, and the former Chief Operations Officer (COO), Frank Vazquez, resigned from the Company. The Company and former officers are currently pursuing arbitration to resolve claims by Messrs Vazquez and Wunderlich and counterclaims by the Company. In conjunction with the former officers’ resignations, the former CFO filed a SOX Whistleblower Complaint with the Department of Labor in January of 2007. The action is against the Company and the Chief Executive Officer, Malcolm Skolnick. The SEC has requested information from the Company addressing the allegations and the Company has responded in compliance with that request. The Company’s Board of Directors instituted a special committee of independent directors who appointed an independent, outside counsel to conduct an independent investigation. The investigation was completed and the investigator’s report found that the allegations made in the SOX complaint had no merit. This matter is set for arbitration in May 2008. Depositions have been taken of the parties and Management intends to vigorously defend its position.

ITEM 4.

SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

There were no matters submitted to a vote of securities holders during the fourth quarter of our fiscal year ended December 31, 2007.

26

PART II

ITEM 5.

MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

Authorized capital stock consists of 300,000,000 shares of common stock, par value $0.001 per share, and 50,000,000 shares of preferred stock, par value $0.001 per share. There were 146,660,968 shares of common stock and no shares of preferred stock outstanding as of March 31, 2008. The Company’s common stock is traded on the NASDAQ, OTC Bulletin Board under the ticker symbol CYGX.OB.

The high and low bid prices for the Company’s common stock for each quarter within the last two fiscal years, as quoted by the OTC Bulletin Board, were as follows. The quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not represent actual transactions.

Fiscal Year Ending December 31, 2005

High

Low

Quarter 1

$0.95

$0.43

Quarter 2

$0.79

$0.46

Quarter 3

$0.67

$0.34

Quarter 4

$1.15

$0.44

Fiscal Year Ending December 31, 2006

Quarter 1

$1.54

$0.73

Quarter 2

$1.54

$0.85

Quarter 3

$1.09

$0.67

Quarter 4

$0.88

$0.56

Fiscal Year Ending December 31, 2007

Quarter 1

$0.66

$0.37

Quarter 2

$0.56

$0.30

Quarter 3

$0.40

$0.23

Quarter 4

$0.35

$0.11

Quarter 1 to March 17, 2008

$0.16

$0.06

STOCKHOLDERS

As of March 31, 2008 there were approximately 649 shareholders of record of Common Stock, one of which is Cede & Co., a nominee for Depository Trust Company (or DTC). All of the shares of Common Stock held by brokerage firms, banks, and other financial institutions as nominees for beneficial owners are deposited into participant accounts at DTC, and are considered to be held of record by Cede & Co. as one shareholder. The Company has not paid any dividends on its Common Stock and the Board does not intend to declare any dividends in the foreseeable future.

27

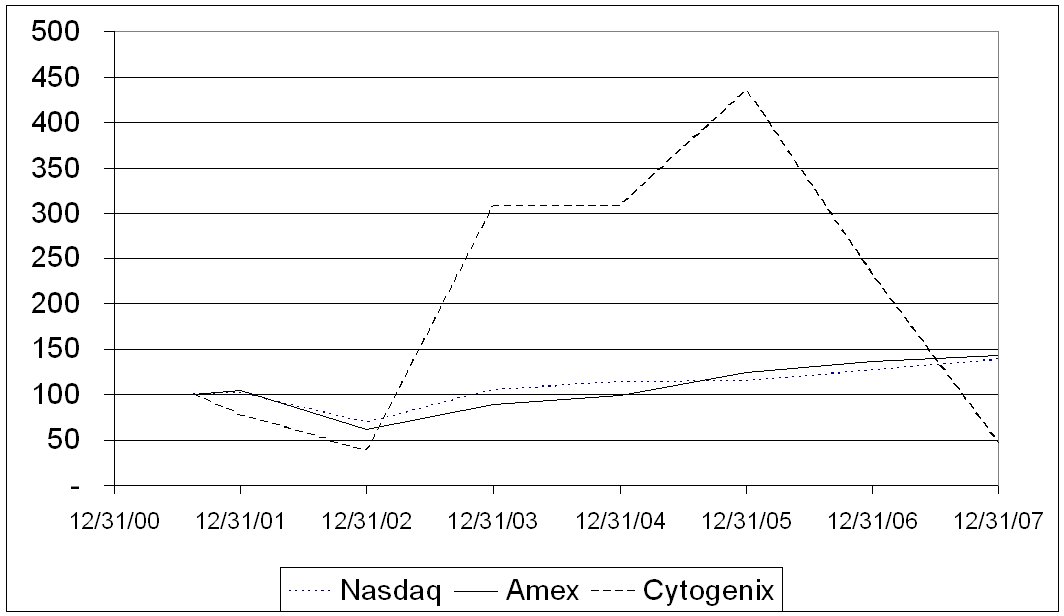

PERFORMANCE GRAPH

The Company’s common stock began trading on the OTC Bulletin Board in August 2001. The following graph depicts the Company’s total return to stockholders from August 2001 through December 31, 2007, relative to the performance of the Amex Biotech Index and NASDAQ Composite Index. All of the cumulative total returns are computed assuming the value of the investment in Common Stock and each indexed as $100.00 on August 16, 2001 and the reinvestment of dividend at the frequency with which dividends were paid during applicable years.

Base

INDEXED RETURNS

Period

Years Ending

Company/Index

24-Aug-01

31-Dec-01

31-Dec-02

31-Dec-03

31-Dec-04

31-Dec-05

31-Dec-06

31-Dec-07

CYTOGENIX, INC………………….

100

77

39

308

308

435

231

46

AMEX BIOTECH INDEX…………

100

106

61

89

99

124

137

143

NASDAQ COMPOSITE INDEX……

100

102

70

105

113

115

126

138

CHANGES IN SECURITIES

All of the Company’s securities sold during 2007 have been either previously reported on its Form 10-Qs and Form 8-Ks filed with the Securities and Exchange Commission.

On November 30, 2007, the Company completed a private placement of 4,441,000 shares (4,389,750 shares issued as of December 31, 2007, 101,250 issued subsequent to December 31, 2007) of restricted common stock at $0.16 per share for gross proceeds of $718,560. The difference between the selling price and the market value on the date the shares were sold was approximately $0.09 per share ($399,690). In 2007 the Company issued 1,256,008 shares for services; approximately 333,336 were issued each to TMS Investments, Inc., Harris Forbes, Inc., and Chasseur Corporation; approximately 156,000 were issued to

28

directors; and approximately 100,000 shares were issued to Fusion Capital Fund II, LLC. In 2007 and in 2006, there were no shares issued for debt.

ITEM 6. SELECTED FINANCIAL DATA

The following selected financial data should be read in conjunction with Item 7. “Management’s Discussion and Analysis or Plan of Operation” and Item 8. “Financial Statements.”

ITEM 7.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONS AND RESULTS OF OPERATIONS

FORWARD-LOOKING INFORMATION

This report contains forward-looking statements regarding the Company’s plans, expectations, estimates and beliefs. Actual results could differ materially from those discussed in, or implied by, these forward-looking statements. Forward-looking statements are identified by words such as “believe,” “anticipate,” “expect,” “intend,” “plan,” “will,” “may,” and other similar expressions. In addition, any statements that refer to expectations, projections or other characterizations of future events or circumstances are forward-looking statements. The Company has based these forward-looking statements largely on its expectations. Forward-looking statements in this report include, but are not necessarily limited to, those relating to the Company’s:

o

intention to introduce new products,

o

receipt of any required FDA or other regulatory approval for its products,

o

expectations about the markets for its products,

o

acceptance of its products, when introduced, in the marketplace,

o

future capital needs, and

o

success of its patent applications.

Forward-looking statements are subject to risks and uncertainties, certain of which are beyond the Company’s control. Actual results could differ materially from those anticipated as a result of the factors described in the “Risk Factors” and detailed in the Company’s other Securities and Exchange Commission filings, including among others:

o

the effect of regulation by the FDA and other governmental agencies,

o

delays in obtaining, or its inability to obtain, approval by the FDA or other regulatory authorities for its products,

o

research and development efforts, including delays in developing, or the failure to develop, its products,

o

the development of competing or more effective products by other parties,

o

the results of pre-clinical and clinical testing,

o

uncertainty of market of acceptance of its products,

29

o

problems that it may face in manufacturing, marketing, and distributing its products,

o

inability to raise additional capital when needed,

o

delays in the issuance of, or the failure to obtain, patents for certain of its products and technologies, and

o

problems with important suppliers and business partners.