EXHIBIT 99.3

Cameco Corporation

2011 Management’s Discussion and Analysis

February 9, 2012

Management’s discussion and analysis

February 9, 2012

2011 Highlights | 4 | |||

The nuclear fuel cycle | 7 | |||

About Cameco | 8 | |||

The nuclear industry today | 11 | |||

The long-term view | 14 | |||

Our strategy | 17 | |||

Financial results | 32 | |||

Our operations and development projects | 61 | |||

Mineral reserves and resources | 96 | |||

Additional information | 101 | |||

Throughout this document, the termswe, us, our andCameco mean Cameco Corporation and its subsidiaries.

Management’s discussion and analysis

This management’s discussion and analysis (MD&A) includes information that will help you understand management’s perspective of our audited consolidated financial statements (financial statements) and notes for the year ended December 31, 2011. This information is based on what we knew on February 8, 2012.

We encourage you to read our financial statements and notes as you review this MD&A. You can find more information about Cameco, including our financial statements and our most recent annual information form, on our website at cameco.com, on SEDAR at sedar.com or on EDGAR at sec.gov. You should also read our annual information form before making an investment decision about our securities.

On January 1, 2011, we adopted International Financial Reporting Standards (IFRS), which have become the generally accepted accounting principles required to be used by most Canadian publicly accountable enterprises. Our financial statements and notes for the year ended December 31, 2011 have been prepared using IFRS. Amounts relating to the year ended December 31, 2010 in this MD&A and our financial statements have been revised to reflect our adoption of IFRS. Amounts for periods prior to January 1, 2010 are presented in accordance with Canadian Generally Accepted Accounting Principles (Canadian GAAP) in effect prior to January 1, 2011. When we refer to Canadian GAAP in this MD&A, we mean Canadian GAAP as in effect before adoption of IFRS.

Presentation and terminology used in our financial statements and this MD&A differ from that used in previous years. Details of the more significant accounting differences can be found in note 3 to our financial statements.

Unless we have specified otherwise, all dollar amounts are in Canadian dollars.

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 1

Caution about forward-looking information

Our MD&A includes statements and information about our expectations for the future. When we discuss our strategy, plans, future financial and operating performance, or other things that have not yet taken place, we are making statements considered to beforward-looking information orforward-looking statements under Canadian and United States securities laws. We refer to them in this MD&A asforward-looking information.

Key things to understand about the forward-looking information in this MD&A:

| • | It typically includes words and phrases about the future, such as: believe, estimate, anticipate, expect, plan, intend, predict, goal, target, project, potential, strategy and outlook (see examples below). |

| • | It represents our current views, and can change significantly. |

| • | It is based on a number ofmaterial assumptions,including those we have listed on page 3, which may prove to be incorrect. |

| • | Actual results and events may be significantly different from what we currently expect, due to the risks associated with our business. We list a number of thesematerial riskson page 3. We recommend you also review our annual information form, which includes a discussion of other material risks that could cause actual results to differ significantly from our current expectations. |

| • | Forward-looking information is designed to help you understand management’s current views of our near and longer term prospects, and may not be appropriate for other purposes. We will not necessarily update this information unless we are required to by securities laws. |

Examples of forward-looking information in this MD&A

| • | our expectations about 2012 and future global uranium supply, consumption, demand and number of operable reactors, including the discussion on the expected impact resulting from the March 2011 nuclear incident in Japan |

| • | our expectations for spot prices in 2012 |

| • | our strategy for increasing annual production to 40 million pounds by 2018 and our expectation that existing cash balances and operating cash flows will meet anticipated capital requirements without the need for any significant additional financing to reach this goal |

| • | our expectations regarding uranium demand in the near term |

| • | our 2012 objectives |

| • | the outlook for each of our operating segments for 2012, and our consolidated outlook for the year |

| • | our expectation that we will invest significantly in expanding production at our existing mines and advancing projects as we pursue our growth strategy |

| • | our expectation that cash balances will decline as we use the funds in our business and pursue our growth plans |

| • | our expectations for 2012, 2013 and 2014 capital expenditures |

| • | our expectation that our operating and investment activities in 2012 will not be constrained by the financial covenants in our unsecured revolving credit facility |

| • | our uranium price sensitivity analysis |

| • | forecast production at our uranium operations from 2012 to 2016 |

| • | the likely terms and volumes to be covered by long-term delivery contracts that we enter into in 2012 and in future years |

| • | future production at our fuel services operations |

| • | future royalty and tax payments and rates |

| • | our future plans for each of our uranium operating properties, development projects and projects under evaluation, and fuel services operating sites |

| • | our expectations regarding Cigar Lake |

| • | our mineral reserve and resource estimates |

2 CAMECOCORPORATION

Material risks

| • | actual sales volumes or market prices for any of our products or services are lower than we expect for any reason, including changes in market prices or loss of market share to a competitor |

| • | we are adversely affected by changes in foreign currency exchange rates, interest rates or tax rates |

| • | our production costs are higher than planned, or necessary supplies are not available, or not available on commercially reasonable terms |

| • | our estimates of production, purchases, costs, decommissioning or reclamation expenses, or our tax expense estimates, prove to be inaccurate |

| • | we are unable to enforce our legal rights under our existing agreements, permits or licences, or are subject to litigation or arbitration that has an adverse outcome |

| • | there are defects in, or challenges to, title to our properties |

| • | our mineral reserve and resource estimates are not reliable, or we face unexpected or challenging geological, hydrological or mining conditions |

| • | we are affected by environmental, safety and regulatory risks, including increased regulatory burdens or delays |

| • | we cannot obtain or maintain necessary permits or approvals from government authorities |

| • | we are affected by political risks in a developing country where we operate |

| • | we are affected by terrorism, sabotage, blockades, civil unrest, accident or a deterioration in political support for, or demand for, nuclear energy |

| • | we are impacted by changes in the regulation or public perception of the safety of nuclear power plants, which adversely affect the construction of new plants, the relicensing of existing plants and the demand for uranium |

| • | there are changes to government regulations or policies that adversely affect us, including tax and trade laws and policies |

| • | our uranium and conversion suppliers fail to fulfil delivery commitments |

| • | our Cigar Lake development, mining or production plans are delayed or do not succeed, including as a result of any difficulties encountered with the jet boring mining method or our inability to acquire any of the required jet boring equipment |

| • | we are affected by natural phenomena, including inclement weather, fire, flood and earthquakes |

| • | our operations are disrupted due to problems with our own or our customers’ facilities, the unavailability of reagents, equipment, operating parts and supplies critical to production, equipment failure, lack of tailings capacity, labour shortages, labour relations issues, strikes or lockouts, underground floods, cave ins, ground movements, tailings dam failures, transportation disruptions or accidents, or other development and operating risks |

Material assumptions

| • | our expectations regarding sales and purchase volumes and prices for uranium, fuel services and electricity |

| • | our expectations regarding the demand for uranium, the construction of new nuclear power plants and the relicensing of existing nuclear power plants not being adversely affected by changes in regulation or in the public perception of the safety of nuclear power plants |

| • | our expected production level and production costs |

| • | our expectations regarding spot prices and realized prices for uranium, and other factors discussed on page 48,Price sensitivity analysis: uranium |

| • | our expectations regarding tax rates, foreign currency exchange rates and interest rates |

| • | our decommissioning and reclamation expenses |

| • | our mineral reserve and resource estimates, and the assumptions upon which they are based, are reliable |

| • | the geological, hydrological and other conditions at our mines |

| • | our Cigar Lake development, mining and production plans succeed, including the success of the jet boring mining method at Cigar Lake and that we will be able to obtain the additional jet boring system units we require on schedule |

| • | our ability to continue to supply our products and services in the expected quantities and at the expected times |

| • | our ability to comply with current and future environmental, safety and other regulatory requirements, and to obtain and maintain required regulatory approvals |

| • | our operations are not significantly disrupted as a result of political instability, nationalization, terrorism, sabotage, blockades, civil unrest, breakdown, natural disasters, governmental or political actions, litigation or arbitration proceedings, the unavailability of reagents, equipment, operating parts and supplies critical to production, labour shortages, labour relations issues, strikes or lockouts, underground floods, cave ins, ground movements, tailings dam failure, lack of tailings capacity, transportation disruptions or accidents or other development or operating risks |

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 3

2011 Highlights

After a year of global economic, political and environmental challenges, we reassessed our corporate growth strategy and found it to be as relevant today as it was in 2008 when we set our Double U course. We remain confident in the long-term fundamentals of the nuclear industry. World demand for safe, clean, reliable and affordable energy continues to grow and the need for nuclear energy as part of the world’s energy mix remains compelling.

We are preparing our assets to ensure we can be among the first to respond when the market signals new production is needed and to maintain our position as one of the world’s largest uranium producers.

We demonstrated our financial strength again this year and we continued to make good progress on our pipeline of projects in development and under evaluation, hitting some key milestones along the way.

Strong financial performance

Our financial results were better than expected and we achieved a number of performance records for the year and during the fourth quarter, including:

| • | annual revenue of $2.4 billion and quarterly revenue of $977 million from our nuclear business |

| • | annual gross profit of $776 million and quarterly gross profit of $353 million from our nuclear business |

| • | annual revenue of $1.6 billion and quarterly revenue of $731 million from our uranium segment |

| • | annual average realized price of $49.18 per pound ($49.17 US per pound) in our uranium segment |

Net earnings attributable to our shareholders (net earnings) in 2011 were $450 million. In 2010, net earnings were higher by $66 million, mainly due to higher earnings in both our electricity and fuel services segments.

Highlights December 31 ($ millions except where indicated) | 2011 | 2010 | change | |||||||||||||

Revenue | 2,384 | 2,124 | 12 | % | ||||||||||||

Gross profit | 776 | 771 | 1 | % | ||||||||||||

Net earnings | 450 | 516 | (13 | )% | ||||||||||||

$ per common share (diluted) | 1.14 | 1.31 | (13 | )% | ||||||||||||

Adjusted net earnings (non-IFRS, see page 33 & 34) | 509 | 497 | 2 | % | ||||||||||||

$ per common share (adjusted and diluted) | 1.29 | 1.26 | 2 | % | ||||||||||||

Cash provided by operations (after working capital changes) | 732 | 521 | 40 | % | ||||||||||||

Average realized prices | Uranium | $US/lb $Cdn/lb |

| 49.17 49.18 |

|

| 43.63 45.81 |

|

| 13 7 | % % | |||||

| Fuel services | $Cdn/kgU | 16.71 | 16.86 | (1 | )% | |||||||||||

| Electricity | $Cdn/MWh | 54 | 58 | (7 | )% | |||||||||||

Shares and stock options outstanding

At February 9, 2012, we had:

| • | 394,767,078 common shares and one Class B share outstanding |

| • | 8,442,385 stock options outstanding, with exercise prices ranging from $10.51 to $46.88 |

Dividend policy

Our board of directors has established a policy of paying a quarterly dividend of $0.10 ($0.40 per year) per common share. This policy will be reviewed from time to time based on our cash flow, earnings, financial position, strategy and other relevant factors.

4 CAMECOCORPORATION

Excellent progress in our uranium segment this year

In our uranium segment this year, production was 3% higher than the guidance we provided in our 2011 third quarter MD&A. We had a number of successes at our mining operations, development projects and projects under evaluation. Key highlights:

| • | realized benefits of production flexibility provisions in our McArthur River/Key Lake licences, matching our 2010 production record and exceeding our production target by 5% |

| • | realized benefits of improved efficiency and reliability of equipment at Key Lake |

| • | completed construction of the acid, steam and oxygen plants at Key Lake |

| • | signed a memorandum of agreement (MOA) to increase production at Inkai from 3.9 million pounds (100% basis) to 5.2 million pounds (100% basis). SeeUranium – operating properties – Inkaion page 79 for more information. |

| • | signed an agreement to process all Cigar Lake ore at the McClean Lake mill, which is expected to result in a significant reduction in the operating cost of the project. SeeUranium – development project – Cigar Lakeon page 83 for more information. |

| • | completed remediation of the underground and sinking of shaft 2 to the 480 metre level at Cigar Lake |

| • | received regulatory approval for our Cigar Lake mine plan and to begin work on our project to allow the release of treated water directly to Seru Bay |

| • | completed a memorandum of understanding (MOU) for a mine development agreement with the Martu (the local indigenous people) at our Kintyre project |

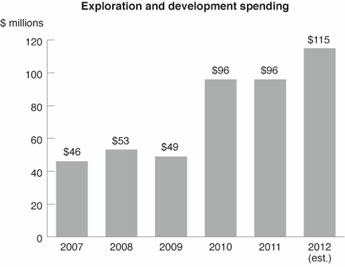

We continued to advance our exploration activities, spending $10 million on five brownfield exploration projects, and $38 million for resource delineation at Kintyre and Cigar Lake. We spent about $48 million on regional exploration programs, mostly in Saskatchewan, followed by Australia, northern Canada, Asia and South America.

Updates on our other segments

In our fuel services segment, we decreased production due to unfavourable market conditions for UF6.

In our electricity segment, Bruce Power Limited Partnership (BPLP) generated 24.9 terawatt hours (TWh) of electricity, at a capacity factor of 87%. Our share of earnings before taxes was $92 million.

Our investment in Global Laser Enrichment (GLE) continues to progress. GLE is continuing its testing activities and engineering design work for a commercial facility. The US Nuclear Regulatory Commission is assessing GLE’s application for a commercial facility construction and operating licence.

Highlights | 2011 | 2010 | change | |||||||||||

Uranium | Production volume (million lbs) | 22.4 | 22.8 | (2 | )% | |||||||||

| Sales volume (million lbs) | 32.9 | 29.6 | 11 | % | ||||||||||

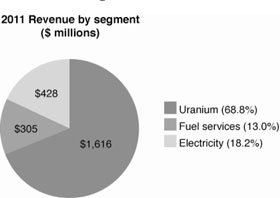

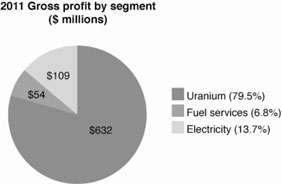

| Revenue ($ millions) | 1,616 | 1,358 | 19 | % | ||||||||||

| Gross profit ($ millions) | 632 | 532 | 19 | % | ||||||||||

Fuel services | Production volume (million kgU) | 14.7 | 15.4 | (5 | )% | |||||||||

| Sales volume (million kgU) | 18.3 | 17.0 | 8 | % | ||||||||||

| Revenue ($ millions) | 305 | 287 | 6 | % | ||||||||||

| Gross profit ($ millions) | 54 | 65 | (17 | )% | ||||||||||

Electricity | Output (100%) (TWh) | 24.9 | 25.9 | (4 | )% | |||||||||

| Revenue (100%) | 1,354 | 1,509 | (10 | )% | ||||||||||

| Our share of earnings before taxes ($ millions) | 92 | 172 | (47 | )% | ||||||||||

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 5

Key market facts

Demand for electricity is expected to nearly double from 2009 to 2035, driven mainly by growth in the developing world as it seeks to diversify sources of energy and provide security of supply.

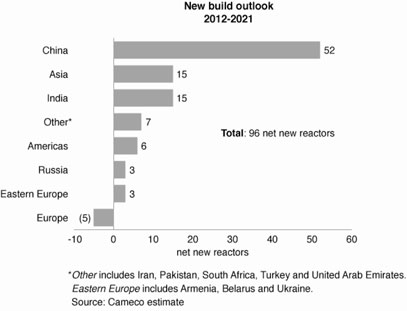

| • | At the start of 2012, there were 431 operable commercial nuclear power reactors in 31 countries, providing about 13% of the world’s electricity. |

| • | At the start of 2012, there were 63 reactors under construction, and by 2021 we expect 96 new reactors (net) to come on line. |

| • | Most of this new build is being driven by rapidly developing countries like China and India, which have severe energy deficits and want clean sources of electricity to improve their environment and sustain economic growth. |

| • | Over the next decade, we expect demand for uranium to grow by an average of 3% per year. |

| • | To meet global demand over the next 10 years, we expect 65% of uranium supply will come from mines that are currently in operation, 15% from finite sources of secondary supply (mainly Russian highly enriched uranium (HEU), government inventories and limited recycling), and 20% will have to come from new sources of supply. |

| • | With uranium assets on three continents, including high-grade reserves and low-cost mining operations in Canada, and investments that cover the nuclear fuel cycle—we are ideally positioned to benefit from the world's growing need for clean, reliable energy. |

6 CAMECOCORPORATION

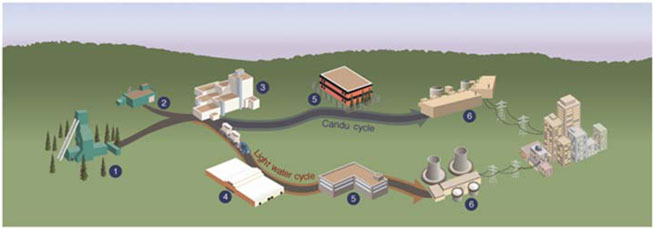

The nuclear fuel cycle

| 1 | Mining |

There are three common ways to mine uranium, depending on the depth of the orebody and the deposit’s geological characteristics:

| • | Open pit mining is used if the ore is near the surface. The ore is usually mined using drilling and blasting. |

| • | Underground mining is used if the ore is too deep to make open pit mining economical. Tunnels and shafts provide access to the ore. |

| • | In situ recovery (ISR) does not require large scale excavation. Instead, holes are drilled into the ore and a solution is used to dissolve the uranium. The solution is pumped to the surface where the uranium is recovered. |

| 1 | Milling |

Ore from open pit and underground mines is processed to extract the uranium and package it as a powder typically referred to asuranium concentrates (U3O8) oryellowcake. The leftover processed rock and other solid waste (tailings) is placed in an engineered tailings facility.

| 2 | Refining |

Refining removes the impurities from the uranium concentrate and changes its chemical form touranium trioxide (UO3).

| 3 | Conversion |

For light water reactors, the UO3 is converted touranium hexafluoride (UF6) gas to prepare it for enrichment. For heavy water reactors like the Candu reactor, the UO3 is converted into powdereduranium dioxide (UO2).

| 4 | Enrichment |

Uranium is made up of two main isotopes: U-238 and U-235. Only U-235 atoms, which make up 0.7% of natural uranium, are involved in the nuclear reaction (fission). Most of the world’s commercial nuclear reactors require uranium that has an enriched level of U-235 atoms.

The enrichment process increases the concentration of U-235 to between 3% and 5% by separating U-235 atoms from the U-238. Enriched UF6 gas is then converted to powdered UO2.

| 5 | Fuel manufacturing |

Natural or enriched UO2 is pressed into pellets, which are baked at a high temperature. These are packed into zircaloy or stainless steel tubes, sealed and then assembled into fuel bundles.

| 6 | Generation |

Nuclear reactors are used to generate electricity.

U-235 atoms in the reactor fuel fission, creating heat that generates steam to drive turbines. The fuel bundles in the reactor need to be replaced as the U-235 atoms are depleted, typically after one or two years depending upon the reactor type. The used–orspent–fuel is stored or reprocessed.

Spent fuel management

The majority of spent fuel is safely stored at the reactor site. A small amount of spent fuel is reprocessed. The reprocessed fuel is used in some European and Japanese reactors.

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 7

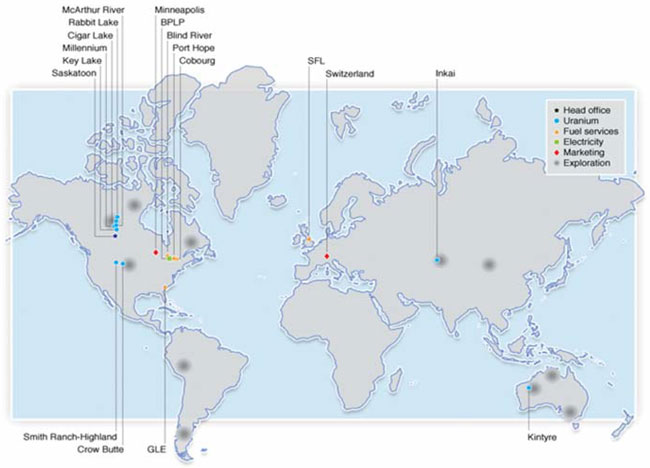

About Cameco

Our head office is in Saskatoon, Saskatchewan. We are one of the world’s largest uranium producers, with uranium assets on three continents. Nuclear energy plants around the world use our uranium products to generate one of the cleanest sources of electricity available today. Our operations and investments span the nuclear fuel cycle, from exploration to electricity generation.

Management update

On July 1, 2011, Tim Gitzel assumed the role of president and chief executive officer (CEO), succeeding Jerry Grandey, who retired after more than eight years as CEO and 18 years with Cameco. Tim has developed extensive experience in Canadian and international uranium mining activities during his 18 years in senior management positions, and his transition to CEO was well planned and seamlessly executed. Tim joined the company in 2007 as senior vice-president and chief operating officer and was promoted to president in May of 2010. Before joining Cameco, he was executive vice-president, mining business unit for AREVA, based in Paris, France, with responsibility for uranium, gold, exploration and decommissioning operations in 11 countries around the world.

On July 15, 2011, Grant Isaac, previously senior vice-president, corporate services, became senior vice-president and chief financial officer (CFO), succeeding Kim Goheen who retired after 14 years with Cameco.

Alice Wong, previously vice-president, safety, health, environment, quality and regulatory relations, was appointed senior vice-president, corporate services.

Under Tim’s direction, the management team remains committed to the strategy, vision and values that have helped us become a global leader in the nuclear industry.

Strengths

We are a pure-play nuclear investment with a proven track record and the strengths to take advantage of the world’s rising demand for safe, clean and reliable energy. Our core strengths make us unique:

| • | a large portfolio of low-cost mining operations and geographically diverse uranium assets |

| • | controlling interests in the world’s largest high-grade uranium reserves |

| • | extensive mineral reserves and resources located near our existing infrastructure |

| • | excellent growth potential from existing assets, combined with an advanced global exploration program |

| • | multiple sources of conversion and the ability to adjust production in response to changing market signals |

| • | a worldwide marketing presence and a strong, creditworthy customer base |

| • | an extensive portfolio of long-term sales contracts supported by long-life assets |

| • | innovative technology and experience operating in technically challenging environments |

| • | a leader in corporate social responsibility—building long-term, trusting relationships with communities impacted by our operations |

| • | an enterprise-wide risk management system tied directly to our strategy and objectives |

| • | balanced financial management focused on adding value for our shareholders while positioning us for growth |

| • | among the first to build relationships in emerging markets |

With our extraordinary assets, contract portfolio, employee expertise, comprehensive industry knowledge and financial strength, we are confident in our ability to continue to grow and increase shareholder value.

8 CAMECOCORPORATION

Business segments

|  |

Uranium

We are one of the world’s largest uranium producers, and in 2011 accounted for about 16% of the world’s production. We have controlling ownership of the world’s largest high-grade reserves, with ore grades up to 100 times the world average, and low-cost operations.

Product

| • | uranium concentrates (U3O8) |

Mineral reserves and resources

Mineral reserves

| • | approximately 435 million pounds proven and probable |

Mineral resources

| • | approximately 254 million pounds measured and indicated and 318 million pounds inferred |

Global exploration

| • | focused on four continents |

| • | approximately 5 million hectares of land |

Operating properties

| • | McArthur River and Key Lake, Saskatchewan |

| • | Rabbit Lake, Saskatchewan |

| • | Smith Ranch-Highland, Wyoming |

| • | Crow Butte, Nebraska |

| • | Inkai, Kazakhstan |

Development project

| • | Cigar Lake, Saskatchewan |

Projects under evaluation

| • | Inkai blocks 1 and 2 production increase, Kazakhstan |

| • | Inkai block 3, Kazakhstan |

| • | McArthur River extension, Saskatchewan |

| • | Kintyre, Australia |

| • | Millennium, Saskatchewan |

Fuel services

We are an integrated uranium fuel supplier, offering refining, conversion and fuel manufacturing services.

Products

| • | uranium trioxide (UO3) |

| • | uranium hexafluoride (UF6) (control about 25% of world conversion capacity) |

| • | uranium dioxide (UO2) (the world’s only commercial supplier of natural UO2) |

| • | fuel bundles, reactor components and monitoring equipment used by Candu reactors |

Operations

| • | Blind River refinery, Ontario |

(refines uranium concentrates to UO3) |

| • | Port Hope conversion facility, Ontario |

(converts UO3 to UF6 or UO2) |

| • | Cameco Fuel Manufacturing Inc., Ontario |

| (manufactures fuel bundles and reactor components) |

| • | a toll conversion agreement with Springfields Fuels Ltd. |

(SFL), Lancashire, United Kingdom (UK) (to convert UO3 to UF6– expires in 2016) |

We also have a 24% interest in Global Laser Enrichment (GLE) in North Carolina, with General Electric (51%) and Hitachi Ltd. (25%). GLE is testing a third-generation technology that, if successful, will use lasers to commercially enrich uranium.

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 9

Electricity

We generate clean electricity through our 31.6% interest in the Bruce Power Limited Partnership (BPLP), which operates four nuclear reactors at the Bruce B generating station in southern Ontario.

Capacity

| • | 3,260 megawatts (MW) (100% basis) (about 18% of Ontario’s electricity) |

We also have agreements to manage the procurement of fuel and fuel services for BPLP, including:

| • | uranium concentrates |

| • | conversion services |

| • | fuel fabrication services |

Global presence

10 CAMECOCORPORATION

The nuclear energy industry today

The nuclear energy industry addressed significant challenges in 2011 related to events at the Fukushima-Daiichi nuclear power plant in Japan. As a result, the outlook for the industry remains uncertain for the near to medium term. In the long term, however, we continue to see a very strong and promising growth profile for the nuclear industry.

On March 11, an earthquake and tsunami in Japan caused cooling systems at the Fukushima-Daiichi nuclear power station to fail, and radioactive materials were released. This reduced public confidence in nuclear power in some countries, most notably Germany, which represents 5% of world nuclear generating capacity. It decided to revert to its previous phase-out policy, shutting down eight of its reactors, and plans to shut down the remaining nine reactors by 2022.

It remains unclear what level of nuclear power Japan itself—which represents 12% of global nuclear generating capacity—will depend on in the future. As of February 8, 2012, Japan had three reactors operating. These three reactors are scheduled to enter regular maintenance shutdowns between late February and the end of April, at which time we expect all of Japan’s nuclear reactors will be offline. Many are unaffected by the events in March 2011 but are offline for both planned and unplanned maintenance outages, and diminished public support has prevented utilities from gaining the regulatory and political approvals necessary to restart them. The Japanese government has ordered stress tests to be conducted on all reactors before allowing them to restart, and is implementing reforms to its existing nuclear regulatory framework and energy policy. Stress tests are progressing, but the government has not made any final decisions about restarting the reactors. Local government approval will also likely be required to allow reactors to restart.

The current operating status of reactors in Germany and Japan has caused concern that, in the near to medium term, additional volumes could be introduced to the market from deferrals and/or cancellations of deliveries under sales contracts. This has caused market participants to be discretionary in their purchases. We believe that utilities will continue to work with producers to manage these materials and minimize the impact on the market.

Cameco well positioned

During this period of uncertainty, we are in the enviable position of being heavily committed under long-term sales contracts through 2016. As well, we have commitments to supply a total of about 290 million pounds of uranium under all of our long-term contracts, many of which extend beyond 2016. Therefore, we expect to have a solid revenue stream for years to come, even in the event of declining uranium market prices.

Industry taking action

At the same time, the industry has taken action. Countries with nuclear programs are reviewing regulatory standards, assessing the safety of existing facilities and the design of reactors under construction or in the planning stage. Third party organizations such as the International Atomic Energy Association, Nuclear Energy Institute, World Association of Nuclear Operators, Institute of Nuclear Power Operators, and the World Nuclear Association are lending their support and technical expertise to governments and operators, and providing an accurate source of information for the public.

Preliminary safety reviews are now complete and lessons are being applied that we expect will make the industry even safer. Most countries with nuclear generation capacity have reconfirmed their commitment to the technology and to the future of nuclear energy.

Long-term outlook is positive

Electricity is essential to maintaining and improving the standard of living for people around the world. Demand for safe, clean, reliable, affordable energy continues to grow and the need for nuclear as part of the world’s energy mix remains compelling. We expect demand for uranium to grow, and along with it the need for new supply to meet future customer requirements. You can read more about our outlook on future supply and demand inThe long-term viewon page 14.

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 11

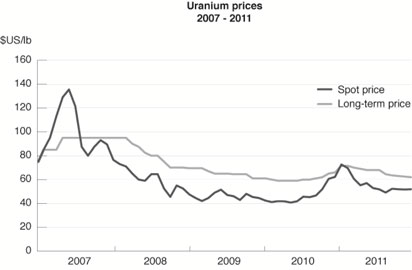

Industry prices

Since March, the spot price has declined from $70 (US) per pound to the low $50 (US) per pound range. Utilities continue to be well covered under existing contracts. Given the current uncertainties in the market, we expect utilities and other market participants will continue to be cautiously opportunistic in their buying. We expect uranium demand in the near to medium term to remain somewhat discretionary, and so we expect prices to be relatively stable in 2012.

| 2011 | 2010 | change | ||||||||||

Uranium($US/lb) 1 | ||||||||||||

Average spot market price | 56.36 | 46.83 | 20 | % | ||||||||

Average long-term price | 66.79 | 60.92 | 10 | % | ||||||||

Fuel services ($US/kgU UF6)1 | ||||||||||||

Average spot market price | ||||||||||||

• North America | 10.61 | 9.11 | 16 | % | ||||||||

• Europe | 10.61 | 9.83 | 8 | % | ||||||||

Average long-term price | ||||||||||||

• North America | 16.09 | 12.21 | 32 | % | ||||||||

• Europe | 16.42 | 13.27 | 24 | % | ||||||||

Note: the industry does not publish UO2prices. | ||||||||||||

Electricity ($/MWh) | ||||||||||||

Average Ontario electricity spot price | 30 | 36 | (17 | )% | ||||||||

| 1 | Average of prices reported by TradeTech and Ux Consulting (Ux) |

12 CAMECOCORPORATION

World consumption and production

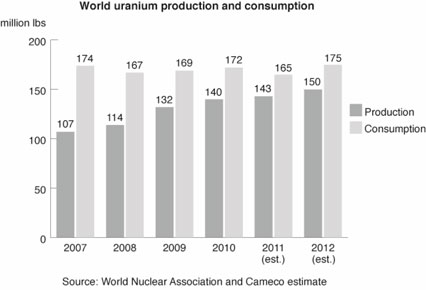

While the events of 2011 reduced our estimate of global consumption in 2011 to 165 million pounds, which is about 15% lower than our original estimate of 195 million pounds, the industry also faced a number of production challenges this year. We estimate 2011 global production was 143 million pounds, about 5% below our original estimate of 150 million pounds.

We expect global uranium consumption to increase to about 175 million pounds in 2012, and global production to be approximately 150 million pounds. Secondary supplies should continue to bridge the gap.

By 2021, we expect world uranium consumption to be about 230 million pounds per year, an average annual growth rate of about 3%.

World consumption for UF6 and natural UO2 conversion services decreased 3% in 2011. After the events in Japan, a number of reactors were taken offline (primarily in Germany and Japan) and a number of new reactor startups were delayed as increased safety checks were required. We expect world consumption to increase by about 6% in 2012 as delayed new reactors come online.

Contract volumes

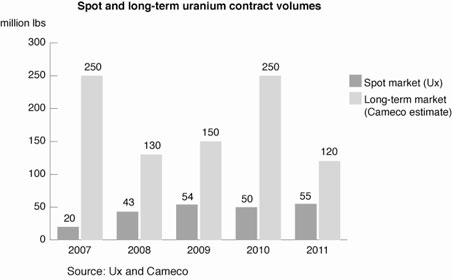

The Ux estimate for global spot market sales in 2011 is about 55 million pounds, 2% above the previous record high of 54 million pounds in 2009. Utilities were responsible for 34% of the purchases. Traders and financial players were the primary participants, taking advantage of the lower spot prices to make opportunistic purchases.

At the start of 2011, we expected long-term contracting volumes for the year to be between 150 million and 200 million pounds, but they ended the year at about 120 million pounds. We believe the decrease is likely related to utilities’ reluctance to contract during this period of market and price uncertainty. We estimate long-term contracting volumes in 2012 will be between 80 and 100 million pounds, depending on supply, market expectations and market prices.

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 13

The long-term view

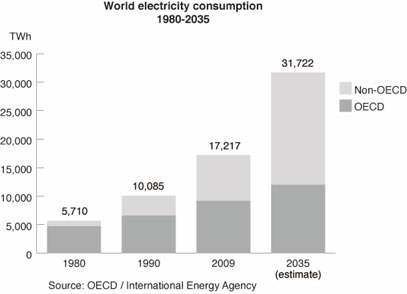

We remain confident in the long-term fundamentals of the nuclear industry, despite the near- to medium-term uncertainty. World population and industrial development continue to grow, and the World Energy Outlook for 2011 predicts a near doubling of electricity consumption between 2009 and 2035. Most of this energy will be used by developing (non-OECD) countries as their populations and standards of living increase.

New reactor outlook

Within this context, most countries are pursuing a diversified approach to energy growth, with an emphasis on energy security and clean energy. Nuclear power can generate baseload electricity with no toxic air pollutants, carbon dioxide (CO2) or other greenhouse gas emissions. It has the capacity to produce enough electricity on a global scale to meet the world’s growing needs, and while it is not the only solution, it is an affordable and sustainable source of safe, clean and reliable energy. As a result, we expect nuclear energy to remain an important part of the energy mix.

This is evident in the growth in reactor construction we expect over the next 10 years. There are 431 reactors operable today. We expect the start up of 96 net new reactors by 2021, increasing the total number of operable reactors to 527.

This is a rate of growth in new reactor construction not seen since the 1970s.

14 CAMECOCORPORATION

Today there are 63 reactors under construction around the world. China continues to lead the growth, with 26 reactors under construction and dozens more planned. India, Russia and South Korea also continue to expand their nuclear generating capacity.

In the UK, government commitment to nuclear energy is strong, driven by concerns about energy security and the need to limit CO2 emissions. The US continues to make progress toward new nuclear development with six units planned, four of which we expect will receive construction licences this year, and one of which is already under construction.

We have long-term supply contracts in many of these countries, including the US and China.

Other previously non-nuclear countries are either moving ahead with their reactor construction programs or considering adding nuclear to their energy programs in the future. For example, the United Arab Emirates is proceeding with its plans to have 5.6 gigawatts of nuclear capacity in place by 2020 and is beginning the process to secure fuel for those reactors. In Saudi Arabia, where power demand has been increasing by 7% to 8% annually, plans to build 16 reactors by 2030 have been announced. Vietnam, Poland, Lithuania, Turkey, Jordan, Egypt and Belarus are also moving forward with plans to proceed with nuclear power development.

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 15

Demand for uranium is growing

Not surprisingly, as the number of reactors grows, so too does the demand for uranium.

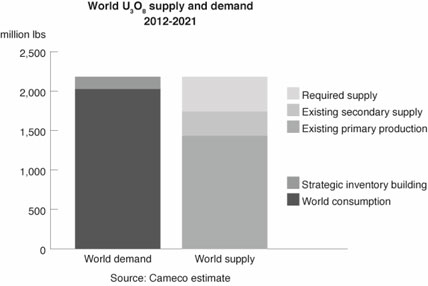

We expect world demand of approximately 2.2 billion pounds over the next 10 years, which includes both world consumption and strategic inventory building. Although our previous forecast has decreased by about 7% due to the events in 2011, it is still significant growth. By 2021, we expect world uranium demand to be about 250 million pounds per year, an average annual growth rate of about 3%.

Supply is expected to tighten

While the impact of the March events in Japan on demand was more immediately apparent, the drop in uranium prices and ongoing global economic turmoil are beginning to have an impact on the outlook for supply.

Disruptions in mine production, difficulty raising funds for new mining projects, project delays, the announced cancellations of new mines or mine expansions, and the end of the Russian highly enriched uranium (HEU) commercial agreement, all point to tightening supply.

We expect 65% of global uranium supply over the next 10 years to come from existingprimary production—mines that are currently in commercial operation—while we expect 15% to come from existingsecondary supply sources. However, most secondary sources are finite and will not meet long-term needs. Currently, one of the largest sources of secondary supply is uranium derived from the Russian HEU commercial agreement. We expect all deliveries from this source to be made by the end of 2013, leaving a gap of about 24 million pounds per year. SeeManaging our supply and costsstarting on page 23 for more information about the Russian HEU commercial agreement.

The result is that we expect 20% of supply will need to come fromnew sources at a time when new projects are being delayed or cancelled because of current market conditions.In addition, there are barriers to entry, and the lead time for new uranium production can be as long as 10 years or more, depending on the deposit type and location.

Cameco is well positioned

Given our extensive base of mineral reserves and resources, diversified sources of supply and global exploration program, we are well positioned to meet the growing demand for uranium.

16 CAMECOCORPORATION

Our strategy

Our strategy is to increase annual uranium production to 40 million pounds by 2018 and to invest in opportunities across the nuclear fuel cycle that we expect will complement and enhance our business.

Growth

Our growth strategy continues to focus on our uranium segment. Over the next 10 years, we expect 96 net new reactors to be built. Deliveries under the Russian HEU commercial agreement will end in 2013, and the industry will need new production. Lead-times in our industry are long, so we are preparing our assets today to make sure we can respond quickly to changing market conditions with a continued focus on profitability.

In addition, we have an active exploration program and a disciplined acquisition strategy, which we expect will provide us with opportunities to create synergies and grow.

Exploration

Our program is directed at replacing mineral reserves as they are depleted by our production, and ensuring our growth beyond 2018. We have maintained an active exploration program even during periods of weak uranium prices, which has helped us secure land with exploration and development prospects that are among the best in the world. Many of these prospects are located close to our existing operations where we have established infrastructure and capacity to expand.

Our exploration efforts have increased uranium mineral reserves and resources at our operations. We have direct interests in almost 75 active exploration projects in eight countries, over 110 experienced professionals searching for the next generation of deposits, and ownership interests in approximately 5 million hectares (12.5 million acres) of land mainly in Canada, Australia, Kazakhstan, the US, Mongolia and Peru. In northern Saskatchewan alone, we have direct interests in 1.4 million hectares (3.5 million acres) of land covering many of the most prospective exploration areas of the Athabasca Basin. Many of our projects are advanced through joint ventures with both junior and major uranium companies.

For properties that meet our investment criteria, we will partner with other companies through strategic alliances, equity holdings and traditional joint venture arrangements. Our leadership position and industry expertise in both exploration and corporate social responsibility make us a partner of choice.

Acquisition

We have a dedicated team looking for acquisition opportunities that we expect will further add to our production, support our sales activities, and complement and enhance our business in the nuclear industry. We will invest when an opportunity is available at the right time and the right price.

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 17

Uranium: growing production

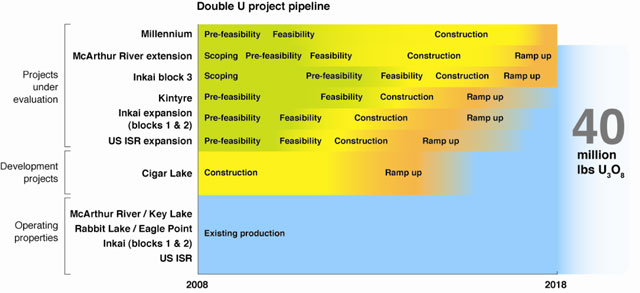

We have a strategy and process in place to increase our annual production to 40 million pounds by 2018, which we expect to come from three sources:

| • | operating properties |

| • | development projects |

| • | projects under evaluation |

We expect about half of the total 2018 annual production will come from mines that are already operating, while the other half is expected to come from projects that are in development or under evaluation.

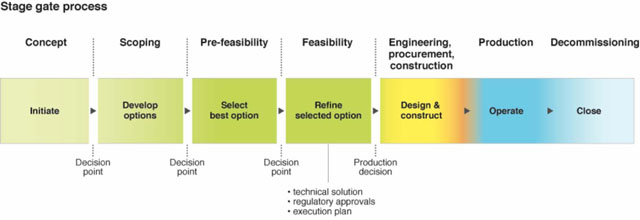

We advance each project through a stage gate process that includes several defined decision points in the assessment and development stages. At each point, we re-evaluate the project based on current economic, competitive, social, legal, political and environmental considerations. If it continues to meet our criteria, we proceed to the next stage. This process allows us to build a pipeline of projects ready for a production decision.

The chart below shows the mix of projects we had when we started our Double U strategy in 2008 and how we expect each of these sources to progress towards achieving our 2018 production goal.

Many of these projects are in the early stage. Depending on the results of our evaluation activities or changing market signals, the mix of projects to reach our 2018 goal may change.

18 CAMECOCORPORATION

To meet our goal, we estimate our capital costs for the development projects and projects under evaluation in the chart will be between $200 and $400 million per year in growth capital for the next three years. SeeCapital spending starting on page 42.

This is a preliminary estimate that we expect to fund using existing cash balances and operating cash flows. Many of these are early stage projects, however, and the mix of projects and their underlying capital estimates could change significantly.

In 2008 Cameco launched a strategy to double our annual uranium production to 40 million pounds by 2018 (Double U).

We have been working toward that goal by focusing on our existing portfolio, monitoring the market and putting resources into the projects that make the most sense. We just completed year four of our 10-year strategy, and we are on track.

Operating properties

Our current sources of production are McArthur River/Key Lake, Rabbit Lake, Smith Ranch-Highland, Crow Butte and Inkai.

We plan to maintain production at these operations, and to expand production where we can by developing new mining zones. We are upgrading the mills at Key Lake and Rabbit Lake to support our plans for production growth.

Inkai blocks 1 and 2, in Kazakhstan, have the potential to significantly increase production. Based on current mineral reserves, we expect Rabbit Lake to produce until 2017, although work is ongoing to extend its mine life even further.

Development project

Cigar Lake is our project in development. It is a superior, world-class deposit that we expect to generate 9 million pounds of uranium per year (our share) after we finish construction and ramp up to full production. We are targeting first commissioning in ore in mid-2013, with the first pounds to be packaged at the McClean Lake mill in the fourth quarter of 2013.

Projects under evaluation

We are evaluating several potential sources of production, including expanding McArthur River, increasing production at Inkai blocks 1 and 2, advancing Inkai block 3, increasing production in the US, and advancing Kintyre and Millennium.

| • | The McArthur River extension is expected to expand our existing mining area, which is part of the most prolific high-grade uranium system in the world. |

| • | Under an MOU with our Inkai partner, National Atomic Company KazAtomProm Joint Stock Company (Kazatomprom), we are in discussions to increase annual production from blocks 1 and 2 to 10.4 million pounds (100% basis). |

| • | Inkai block 3, in Kazakhstan, has the potential to become a significant source of production. |

| • | We are the largest producer in the US and are planning to almost double annual production. |

| • | Our 70% interest in Kintyre, in Australia, adds potential to diversify our production by geography and deposit type. |

| • | Millennium is a uranium deposit in northern Saskatchewan that we expect will take advantage of our excess milling capacity. |

We expect to spend between $20 million and $25 million per year on average for the next three years to assess the feasibility of projects under evaluation. These amounts will be expensed as incurred.

You can read more about each of these projects inOur operations and development projects on page 61.

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 19

Fuel services: capturing synergies

We control about 25% of world UF6 conversion capacity and are the only commercial supplier of natural UO2. Our focus is on cost-competitiveness and operational efficiency.

Our fuel services segment is strategically important because it helps support the growth of the uranium segment. Offering a range of products and services to customers helps us broaden our business relationships and expand our uranium market share.

We also continue to explore innovative areas like laser enrichment technology to broaden our fuel cycle participation and help us serve our customers more effectively.

Today, uranium enrichment is the second largest value component, after uranium, in a typical light water reactor fuel bundle. The enrichment market has the same customer base as the uranium market, and most of the world’s commercial nuclear reactors need enriched uranium.

Uranium and enrichment can be substituted for each other to some extent to produce a given amount of enriched uranium product. For example, when uranium is relatively more expensive than enrichment, it is more cost effective to reduce the amount of uranium feedstock and use more enrichment capacity. When enrichment is relatively more expensive, it makes sense to use more uranium and less enrichment to produce the same amount of enriched uranium product.

Enrichment has the potential to be a significant growth area for us, and offers operational synergies that could significantly enhance profit margins for both our uranium business and future enrichment operations. As one of the largest uranium suppliers in the world, our investment in this segment of the fuel cycle would help us capture additional value.

Electricity: capturing added value

Our investment in BPLP has been an excellent source of cash flow. Our focus is on maintaining steady cash flow and building synergies with our other segments. BPLP is considering extending the operating life of the four Bruce B units and we will have an opportunity to invest if BPLP decides to proceed. We would base this investment decision on the underlying value proposition and the strategic fit with our other growth objectives.

20 CAMECOCORPORATION

This discussion of our strategy and our process to increase our annual uranium production by 2018 is all forward-looking information. It is based on the assumptions and subject to the material risks discussed on page 3, and specifically on the assumptions and risks listed here.

Assumptions

Our statements about increasing annual production by 2018 to 40 million pounds reflect our current production target for 2018. Although we are confident in our efforts to reach that target, we cannot guarantee that we will. We have made assumptions about 2018 production levels at each of our existing operating mines. We have also made assumptions about the development of mines that are not operating yet and their 2018 production levels. We believe these assumptions are reasonable, individually and together, but if an assumption about one or more mines proves to be incorrect, we will not reach our 2018 target production level unless the shortfall can be made up by additional production at another mine.

Material risks that could prevent us from reaching our target

| • | we cannot locate additional mineral reserves and identify appropriate methods of mining to maintain and increase production levels at McArthur River |

| • | we cannot locate additional mineral reserves to extend Rabbit Lake’s mine life to maintain production |

| • | our partner or the Kazakh government does not support an increase in production to the expected level at Inkai, blocks 1 and 2, or we do not reach the full production level as quickly as we expect |

| • | we cannot bring block 3 into production at Inkai if the feasibility study is not favourable or we cannot secure partner or government approval |

| • | development at Cigar Lake is not completed on schedule, or we do not reach the full production level as quickly as we expect |

| • | development of Kintyre is delayed due to political, regulatory or indigenous people issues |

| • | we cannot obtain a favourable feasibility study for Kintyre or the Millennium project, or we cannot reach agreement with our project partners to move ahead with production at Kintyre or Millennium |

| • | the Key Lake mill does not have enough capacity to handle anticipated production increases, and we are not able to expand its capacity or to identify alternative milling arrangements |

| • | the projects under evaluation do not proceed or, if they do, are not completed on schedule or do not reach full production levels as quickly as we expect |

| • | uranium prices and development and operating costs make it uneconomical to develop projects under consideration |

| • | we cannot obtain or maintain necessary permits or approvals from government authorities |

| • | disruption in production or development due to natural phenomena, labour disputes, political risks, blockades or other acts of social or political activism, lack of tailings capacity, or other development and operation risks |

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 21

Building on our strengths

World-class assets

We have extensive mineral reserves and resources, a large portfolio of low-cost mining operations, and geographically diverse uranium assets with controlling interests in the world’s largest high-grade uranium reserves.

Employee expertise

Our company is filled with talented and creative people who are committed to achieving our strategy in a manner consistent with our corporate values of protecting people and the environment, excellence and integrity.

Strong customer relationships

We have large, creditworthy customers that continue to need uranium, even during weak economic conditions, and we expect the uranium contract portfolio we have built to provide a solid revenue stream for years to come.

Uranium price leverage

Our plans to increase our production of uranium, combined with our contracting strategy, are designed to give us leverage when uranium prices go up, and to protect us when prices decline.

Financial strength

We are in a strong financial position to proceed with our growth plans. We are working to ensure our capital structure is appropriate and adds value for our shareholders.

Disciplined portfolio management

We have a disciplined portfolio management process that incorporates all capital projects into a single capital plan and uses a stage gate decision process (see page 18). This ensures our capital projects are aligned with our strategic objectives, and that business benefits are measurable and attainable.

Focused risk management

We have a formal enterprise-wide risk management process that we apply consistently and systematically across our organization. Risk management is a core element of our strategy and our objectives, and we use it to continuously improve our organization. It will underpin decisions we make as we move ahead with our growth strategy.

Innovation

We are always looking for ways to improve processes, to increase safety and environmental performance, and reduce costs. We are currently working on projects in all aspects of operations, including upgrading the Key Lake and Rabbit Lake mills.

Reputation

We believe strongly in our values and apply them consistently in our operations and business dealings. We are recognized as a reliable supplier and business partner, strong community supporter and employer of choice.

22 CAMECOCORPORATION

Managing our growth

Our ability to grow is a function of our people, processes, assets and reputation, and the ability to enhance and leverage these strengths to add value and build competitive advantage.

We use four categories to define what we are committed to deliver, and how we will measure our results:

| • | outstanding financial performance |

| • | a safe, healthy and rewarding workplace |

| • | a clean environment |

| • | supportive communities |

We introduced these measures of success to proactively address the financial, social and environmental aspects of our business. We believe that each is integral to our overall success and that, together, they will ensure our long-term sustainability.

Focus on long-term sustainability

Companies are under growing scrutiny for the way they conduct their businesses, and there has been a significant increase in stakeholder expectations for environmentally and socially responsible business practices.

Rather than viewing sustainable development as an ‘add-on’ to traditional business activity, we see it as integral to the way we do business, and have made it a strategic priority, integrating it into our objectives and compensation policies.

You can find out more in our sustainable development report and annual information form, which are on our website (cameco.com).

Outstanding financial performance

The mining industry is becoming increasingly competitive, particularly in two of the jurisdictions where we operate, northern Saskatchewan in Canada and Western Australia. Our financial results depend heavily on our sales and production volumes, on the cost of supply, and on the prices we realize in our uranium and fuel services segments.

Managing our supply and costs

We sell more uranium than we produce every year. We meet our delivery commitments using uranium we obtain:

| • | from our own production |

| • | through long-term purchase agreements and on the spot market |

| • | from our existing inventory—we target inventories of about six months of forward sales of uranium concentrates and UF6 |

Like all mining companies, our uranium segment is affected by the rising cost of inputs like labour and fuel. In 2011, labour, production supplies and contracted services made up 88% of the production costs at our uranium mines. Labour (34%) was the largest component. Production supplies (27%) included fuels, reagents and other items. Contracted services (27%) included mining and maintenance contractors, air charters, security and ground freight.

Operating costs in our fuel services segment are mainly fixed. In 2011, labour accounted for about 49% of the total. The largest variable operating cost is for energy (natural gas and electricity), followed by zirconium and anhydrous hydrogen fluoride.

To help us operate efficiently and cost-effectively as we grow, we manage operating costs and improve plant reliability by prudently investing in production infrastructure, new technology and business process improvements.

Our costs are also affected by the purchases of uranium and conversion services we make under long-term contracts and on the spot market.

Our long-term purchase contracts are at fixed prices that are lower than the current published spot and long-term prices. Our most significant long-term purchase contract is the Russian HEU commercial agreement, which ends in 2013. We expect to purchase about 17 million pounds, our remaining volumes, under this agreement to the end of 2013. The purchase price escalates with inflation and was agreed to in 2001 when uranium prices were much lower than today. In 2008, pricing on approximately 6 million pounds of the remaining volumes available to us in 2012 and

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 23

2013 was renegotiated. Using a $60 (US) per pound uranium spot price, the average price increase from 2012 to 2013 on these 6 million pounds is expected to be about $18 (US) per pound (including an adjustment for inflation).

After the Russian HEU commercial agreement ends in 2013, we expect to maintain our sales volumes using a combination of sources including:

| • | increased production from various supply sources (including the rampup of Cigar Lake) |

| • | normal-course purchases of uranium under existing and/or new arrangements |

| • | discretionary use of inventories |

We expect our purchases will result in profitable sales; however, the cost of purchased material is likely to be higher than our other sources of supply.

In addition, we will make spot purchases to take advantage of opportunities to place material into higher priced contracts. We make spot purchases prudently, looking at the spot price and other factors relating to our business to decide whether a spot purchase is appropriate. This activity gives us insight into the underlying market fundamentals and is a source of profit.

Managing contracts

We sell uranium and fuel services directly to nuclear utilities around the world, as uranium concentrates, UO2, UF6, conversion services or fuel fabrication.

Uranium is not traded in meaningful quantities on a commodity exchange. Utilities buy the majority of their uranium and fuel services products under long-term contracts with suppliers, and meet the rest of their needs on the spot market.

Our extensive portfolio of long-term sales contracts—and the long-term, trusting relationships we have with our customers—are core strengths for us.

Because we deliver large volumes of uranium every year, our net earnings and operating cash flows are affected by changes in the uranium price. Our contracting strategy is to secure a solid base of earnings and cash flow by maintaining a balanced contract portfolio that maximizes our realized price. Market prices are influenced by the fundamentals of supply and demand, geopolitical events, disruptions in planned supply and other market factors. Contract terms usually reflect market conditions at the time the contract is accepted, with deliveries beginning several years in the future.

Our current uranium contracting strategy is to sign contracts with terms of 10 years or more that include mechanisms to protect us when market prices decline, and allow us to benefit when market prices go up. Our portfolio includes a mix of fixed-price and market-related contracts, which we target at a 40:60 ratio. Fixed-price contracts are typically based on the industry long-term price indicator at the time the contract is accepted, adjusted for inflation to the time of delivery. Market-related contracts may be based on either the spot price or the long-term price as quoted at the time of delivery, and often include floor prices adjusted for inflation and some include ceiling prices also adjusted for inflation.

This is a balanced approach that reduces the volatility of our future earnings and cash flow, and that we believe delivers the best value to shareholders over the long term. It is also consistent with the contracting strategy of our customers. This strategy has allowed us to add increasingly favourable contracts to our portfolio that will enable us to benefit from any increases in market prices in the future.

The majority of our contracts include a supply interruption clause that gives us the right to reduce, on a pro rata basis, defer or cancel deliveries if there is a shortfall in planned production or in deliveries under the Russian HEU commercial agreement.

We are heavily committed under long-term uranium contracts through 2016, so we are being selective when considering new commitments.

The majority of our fuel services contracts are at a fixed price per kgU, adjusted for inflation, and reflect the market at the time the contract is accepted.

24 CAMECOCORPORATION

A safe, healthy and rewarding workplace

We strive to foster a safe, healthy and rewarding workplace at all of our facilities, and measure progress against key indicators, such as conventional and radiation safety statistics, employee sentiment toward the company and employment creation.

To achieve our growth objectives, we continue to build an engaged, qualified and diverse organization capable of leading and implementing our strategies. Our challenge is to retain our current workforce and compete for the limited number of qualified people available, both to replace retiring employees and to support our growth. Our long-term people strategy includes identifying critical workforce segments and planning our workforce to meet this challenge.

Our approach is working. We were recognized in a number of ways for our employee programs in 2011: the Financial Post named Cameco one of the Top 10 Best Companies to Work For in Canada; Mediacorp named us one of Canada’s Top 100 Employers; and The Globe and Mail named us one of Canada’s Top Diversity Employers. You can find out more about our awards on cameco.com.

A clean environment

We are committed to operating our business with respect and care for the local and global environment. We strive to be a leader in environmental practices and performance by complying with and moving beyond legal and other requirements.

We are committed to integrating environmental leadership into everything we do. In 2005, we launched a formal environmental leadership initiative, and set objectives and performance indicators to measure our progress in protecting the air, water and land near our operations, and in reducing the amount of waste we generate and energy we use.

Reducing our impact

We have been working to reduce the impact we have on the environment. This includes monitoring and reducing our effect on air, water and land, reducing the greenhouse gases we produce and the amount of energy we consume, and managing the effects of waste.

We are investing in management systems and safety initiatives to achieve operational excellence, and this continues to improve our safety and environmental performance and operating efficiency.

We have developed new water treatment technologies that have improved the quality of the water released from our Saskatchewan uranium milling operations, and are working on other projects to reduce waste, improve the reclamation process and manage waste rock more effectively.

We have also completed an energy assessment at each of our North American operations, and developed management plans for reducing our energy intensity and greenhouse gas emissions.

We are maximizing the lifespan of our operating sites to limit the environmental impact of operations, and revitalizing the Key Lake mill (in operation for 29 years) and Rabbit Lake mill (in operation for 37 years).

Like other large industrial organizations, we use chemicals in our operations that could be hazardous to our health and the environment if they are not handled correctly. We train our employees in the proper use of hazardous substances and in emergency response techniques.

We work with communities who are affected by our activities to tell them what we are doing and to receive feedback and further input to build and sustain their trust. For example, in Saskatchewan, we participate in the Athabasca Working Group and Northern Saskatchewan Environmental Quality Committee. In Ontario, we liaise with our communities by regularly holding educational and environment-focused activities.

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 25

Supportive communities

To maintain public support for our operations (our social licence to operate) and our global reputation, we need the respect and support of communities, indigenous people, governments and regulators affected by our operations.

We build and sustain the trust of local communities by being a leader in corporate social responsibility (CSR). Through our CSR initiatives, we educate, engage, employ and invest in the people in the regions where we operate.

For example, in northern Saskatchewan in 2011:

| • | just over 50% of the employees at our northern mines were local residents (more than 760 residents) and were paid over $43 million in wages |

| • | approximately $390 million was paid to northern businesses, who provided 74% of services to our northern minesites. This is the most that we have ever procured from northern vendors in one year. |

| • | we made nearly 90 community visits in northern Saskatchewan to discuss potential projects at our northern operations and to provide career information to high school students and community members |

| • | we donated over $1.3 million to northern and aboriginal initiatives for youth, health and wellness, education and literacy, and culture and recreation |

| • | we provided $100,000 in scholarships to post-secondary students |

Our operations are closely regulated to give the public comfort that we are operating in a safe and environmentally responsible way. Regulators approve the construction, startup, continued operation and any significant changes to our operations. Our operations are also subject to laws and regulations related to safety and the environment, including the management of hazardous wastes and materials.

Our objectives are consistent with those of our regulators—to keep people safe and to protect the environment. We pursue these goals through open and co-operative relationships with all of our regulators. We work to earn their trust and that of other stakeholders by continually striving to protect people and the environment.

26 CAMECOCORPORATION

Measuring our results

We set corporate, business unit and departmental objectives every year under our four measures of success, and these become the foundation for a portion of annual employee compensation.

2011 objectives | Results | 2012 objectives This is forward-looking information. See page 2 for more information. | ||

Outstanding financial performance | ||||

Production

• Produce 21.9 million pounds of U3O8 and between 15 million and 16 million kgU from fuel services. | Achieved

• Our share of U3O8 production was 22.4 million pounds, or 102% of plan, and we produced 14.7 million kgU at fuel services, or 98% of plan.

Exceeded

• Exceeded our production target of 18.7 million lbs U3O8 (100% basis) by 7% at McArthur River/Key Lake through technological advancements and identification of mining opportunities that allowed us to take advantage of production flexibility provisions in our operating licences. | Production

• Achieve budgeted production from our uranium and fuel services segments.

McArthur River

• Implement productivity improvements to maintain planned production during mining zone transitions. | ||

Financial measures

Corporate performance

• Achieve budgeted net earnings and cash flow from operations (before working capital changes). | Exceeded

• Adjusted net earnings1 were $509 million, 32% higher than budget. Cash flow from operations (before working capital changes)1 was $850 million, 41% higher than budget. | Financial measures

Corporate performance • Achieve budgeted adjusted net earnings and cash flow from operations (before working capital changes). | ||

Costs

• Strive for unit costs below budget. | Achieved

• Actual unit operating costs for uranium were 1% better than budgeted costs of $19.19 per lb U3O8 produced and exceeded budgeted unit production costs for fuel services of $15.65 per kgU sold, by 3%. The results were weighted 70/30, reflecting the portion each segment makes up of our business. Our minimum target was to achieve budgeted unit costs on a consolidated basis. Target was achieved in the face of cost escalation fueled by increased resource development activity where we operate. | Costs

• Achieve budgeted unit costs. | ||

| 1 | We use adjusted net earnings and cash flow from operations (before working capital changes) as a more meaningful way to compare our financial performance from period to period. These are not standard measures, and not a substitute for financial information prepared in accordance with IFRS. Other companies may calculate these measures differently. SeeAdjusted net earnings (non-IFRS/GAAP measure)and note 26 to our audited 2011 financial statements for more information. |

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 27

2011 objectives | Results | 2012 objectives | ||

Outstanding financial performance | ||||

Growth

Cigar Lake

• Advance the project towards mid-2013 startup by completing remediation of all underground workings and advancing shaft 2 sinking.

Inkai

• Advance block 3 mineral resource delineation and the engineering design of a test leach facility. Advance construction of site infrastructure. | Achieved

• Completed remediation of all underground workings and completed sinking of shaft 2 to the 480 metre level. Cigar Lake is a challenging deposit to mine. Completion of these critical milestones required careful planning and deliberate execution.

Partially achieved

• Advanced block 3 mineral resource delineation, completed engineering for a test leach facility and began infrastructure development. We need regulatory approval of the detailed delineation and test leach work programs. The approval process has been challenging because of the complex and developing regulatory environment.

Partially achieved | Growth

• Meet regulatory project milestones and stage gate assessments on projects that support our Double U strategy.

Cigar Lake

• Advance the project towards startup in 2013 by successfully completing critical activities planned for 2012.

Inkai

• Advance block 3 mineral resource delineation drilling and complete the test leach facility.

• Receive approval to increase annual production from blocks 1 and 2 to design capacity of 5.2 million pounds per annum (100% basis). Continue to advance our longer-term objective of receiving approval to double annual production from blocks 1 and 2, extend the lease terms and secure block 3 mining rights. | ||

• Receive approval to increase annual production from blocks 1 and 2 to design capacity of 5.2 million pounds per annum (100% basis). Pursue our longer-term objective of receiving approval to double annual production from blocks 1 and 2 by advancing the conversion joint venture project with Kazatomprom. | • Signed memorandum of agreement with our partner to increase annual production from blocks 1 and 2 to 5.2 million pounds per year (100% basis). Government approval is pending in this complex and developing regulatory environment. To pursue our longer-term objective to double annual production, we continued to explore with Kazatomprom the feasibility of building a uranium conversion facility and other potential collaborations in uranium conversion. | |||

28 CAMECOCORPORATION

2011 objectives | Results | 2012 objectives | ||

Outstanding financial performance | ||||

Growth (continued)

Kintyre

• Continue to advance project evaluation to allow a production decision as soon as possible. | Partially achieved

• Significantly advanced a prefeasibility study and an environmental review and management program in a remote area that is often subject to extreme weather conditions. To support our prefeasibility study, we expanded the scope of our drilling program and delayed these activities to 2012. Gained support in principle from the Martu, the local indigenous people, for development of the project. | Growth (continued)

Kintyre

• Continue to advance project evaluation in 2012 and decide if we will proceed to feasibility.

Exploration and innovation

• Replace mineral reserves and resources at the rate of annual U3O8 production based on a three-year rolling average. | ||

Millennium

• Continue to advance the Millennium project toward a project decision. | Achieved

• Continued to work on the environmental assessment and carried out additional studies and design work. Our 2011 drill program resulted in an increase in inferred resources. As a project under evaluation, it must pass a number of decision points before the project decision is made. | |||

Exploration and innovation

• Replace mineral reserves and resources at the rate of annual U3O8 production based on a three-year rolling average. | Achieved

• Over the last three years, mineral reserves decreased by 60 million pounds compared to production of 66 million pounds, measured and indicated resources increased by 126 million pounds and inferred resources decreased by 18 million pounds. On average, production was replaced and exceeded by 16 million pounds per year in each of the last three years (2009 to 2011). Replacing our reserves and resources is fundamental to our long-term success.

Achieved | |||

• Support production growth and improved operating efficiencies through targeted research, development and technological innovation. | • Advanced numerous ongoing research projects and selected four of these to fast track that are aimed at improving our environmental performance and process efficiencies at our operations. Innovation is critical to achieving continuous improvement in these areas even though it is complex and its outcome is uncertain. | |||

2011 MANAGEMENT’SDISCUSSIONANDANALYSIS 29

2011 objectives | Results | 2012 objectives | ||

Outstanding financial performance | ||||

Growth (continued)

McArthur River extension

• Advance the underground exploration drifts to the north of current mining areas and initiate a feasibility study. | Achieved

• �� Advanced the underground exploration drifts based on our updated mine plan and began feasibility work. Upgraded resources from inferred to indicated based on surface drilling. Achieved these results while managing the operational risks associated with the location and grade of the orebody. | Growth (continued) | ||

Management

• Sustain and grow production in accordance with our strategy to double annual uranium production by 2018 by advancing pipeline uranium projects through the stage gate process. | Achieved

• Successfully implemented the stage gate process and incorporated all of our global development projects into the process. This is a complex scheduling process involving cross-functional teams, communication across different disciplines and several large capital projects in different geographic locations competing for internal resources. | Management

• Deliver capital projects planned for completion in 2012 within budget and on schedule. | ||