| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-172143-08 | ||

| November 27, 2012 | |||||

| FREE WRITING PROSPECTUS | |||||

| COLLATERAL TERM SHEET | |||||

| COMM 2012-CCRE5 | |||||

| Deutsche Mortgage & Asset Receiving Corporation | |||||

| Depositor | |||||

German American Capital Corporation Cantor Commercial Real Estate Lending, L.P. | |||||

| KeyBank National Association | |||||

| Sponsors and Mortgage Loan Sellers | |||||

Deutsche Bank Securities | Cantor Fitzgerald & Co. | ||||

| Joint Bookrunning Managers and Co-Lead Managers | |||||

| KeyBanc Capital Markets | CastleOak Securities, L.P. | ||||

| Co-Managers | |||||

| The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the Securities and Exchange Commission website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by emailing: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us. | |||||

| This free writing prospectus does not contain all information that is required to be included in the prospectus and the prospectus supplement. | |||||

STATEMENT REGARDING ASSUMPTIONS AS TO

SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

This material is for your information, and none of Deutsche Bank Securities Inc., Cantor Fitzgerald & Co. Inc., KeyBanc Capital Markets Inc. and CastleOak Securities, L.P. (the “Underwriters”) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

Neither this document nor anything contained herein shall form the basis for any contract or commitment whatsoever. The information contained herein is preliminary as of the date hereof. These materials are subject to change, completion or amendment from time to time. The information contained herein will be superseded by similar information delivered to you as part of the offering document relating to the Commercial Mortgage Pass-Through Certificates, Series COMM 2012-CCRE5 (the “Offering Document”). The Information supersedes any such information previously delivered. The Information should be reviewed only in conjunction with the entire Offering Document. All of the information contained herein is subject to the same limitations and qualifications contained in the Offering Document. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described elsewhere in the Offering Document. The information contained herein will be more fully described elsewhere in the Offering Document. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Offering Document its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this free writing prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Underwriters or any of their respective affiliates makes any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities.

This document contains forward-looking statements. Those statements are subject to certain risks and uncertainties that could cause the success of collections and the actual cash flow generated to differ materially from the information set forth herein. While such information reflects projections prepared in good faith based upon methods and data that are believed to be reasonable and accurate as of the dates thereof, the issuer undertakes no obligation to revise these forward-looking statements to reflect subsequent events or circumstances. Individuals should not place undue reliance on forward-looking statements and are advised to make their own independent analysis and determination with respect to the forecasted periods, which reflect the issuer’s view only as of the date hereof.

IRS CIRCULAR 230 NOTICE: THIS TERM SHEET IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, FOR THE PURPOSE OF AVOIDING U.S. FEDERAL, STATE OR LOCAL TAX PENALTIES. THIS TERM SHEET IS WRITTEN AND PROVIDED IN CONNECTION WITH THE PROMOTION OR MARKETING BY THE DEPOSITOR AND THE UNDERWRITERS OF THE TRANSACTION OR MATTERS ADDRESSED HEREIN. INVESTORS SHOULD SEEK ADVICE BASED ON THEIR PARTICULAR CIRCUMSTANCES FROM AN INDEPENDENT TAX ADVISOR.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS |

Any legends, disclaimers or other notices that may appear at the bottom of the email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation being made that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

7979 Pittsford-Victor Road and 7550 Commons Boulevard Victor, NY 14564 | Collateral Asset Summary Eastview Mall and Commons | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $90,000,000 57.1% 2.17x 10.3% |

| Mortgage Loan Information | Property Information | ||||||

| Loan Seller: | GACC | Single Asset / Portfolio: | Single Asset | ||||

| Loan Purpose: | Refinance | Property Type: | Super Regional Mall | ||||

| Sponsor: | Rochester Malls, LLC | Collateral(4): | Fee Simple/Leasehold | ||||

| Borrower: | Eastview Mall, LLC | Location: | Victor, NY | ||||

| Original Balance: | $90,000,000 | Year Built / Renovated: | 1971, 1998 / 1995, 2003 | ||||

| Cut-off Date Balance: | $90,000,000 | Total Sq. Ft.: | 1,729,853 | ||||

| % by Initial UPB: | -.-% | Total Collateral Sq. Ft.(5): | 811,671 | ||||

| Interest Rate: | 4.6250% | Property Management: | Wilmorite Management Group, LLC | ||||

| Payment Date: | 6th of each month | Underwritten NOI: | $21,535,429 | ||||

| First Payment Date: | October 6, 2012 | Underwritten NCF: | $21,352,529 | ||||

| Maturity Date: | September 6, 2022 | Appraised Value(6): | $368,000,000 | ||||

| Amortization: | Interest Only | Appraisal Date: | July 7, 2012 | ||||

Additional Debt(1): | $120,000,000 Pari Passu Debt | ||||||

| Call Protection: | L(27), D(89), O(4) | Historical NOI | |||||

| Lockbox / Cash Management: | Hard / In Place | TTM NOI: | $19,590,952 (T-12 May 31, 2012) | ||||

| 2011 NOI: | $18,838,827 (December 31, 2011) | ||||||

Reserves(2) | 2010 NOI: | $19,006,318 (December 31, 2010) | |||||

| Initial | Monthly | 2009 NOI: | $17,962,929 (December 31, 2009) | ||||

| Taxes: | $1,154,679 | $131,255 | |||||

| Insurance: | $0 | Springing | Historical Occupancy(7) | ||||

| CapEx & TI/LC: | $0 | Springing | Current Occupancy(8)(9): | 93.9% (June 26, 2012) | |||

| PIF/CapEx Funds: | $8,000,000 | $0 | 2011 Occupancy: | 94.3% (December 31, 2011) | |||

| Von Maur Expenditure: | $4,000,000 | $0 | 2010 Occupancy: | 94.6% (December 31, 2010) | |||

| 2009 Occupancy: | 93.4% (December 31, 2009) | ||||||

Financial Information(3) | 2008 Occupancy: | 92.7% (December 31, 2008) | |||||

| Cut-off Date Balance / Sq. Ft.: | $259 | 2007 Occupancy: | 96.4% (December 31, 2007) | ||||

| Balloon Balance / Sq. Ft.: | $259 | (1) The Original Balance of $90.0 million represents the Note A-2 of a $210.0 million whole loan evidenced by two pari passu notes. The pari passu companion loan is comprised of Note A-1, with an original principal amount of $120.0 million, which was included in the COMM 2012-CCRE4 securitization. (2) See “Initial Reserves” and “Ongoing Reserves” herein. (3) DSCR, LTV, Debt Yield and Balance / Sq. Ft. calculations are based on the aggregate Cut-off Date Balance of $210,000,000. (4) A portion of the Eastview Mall and Commons Property is under a ground lease with the Town of Victor in connection with a tax incremental financing agreement. The agreement is scheduled to expire in 2014, at which time the city of Victor will convey the portion back to the borrower. See “TIF Financing” herein. (5) Total Collateral Sq. Ft. excludes JCPenney, Lord & Taylor, Macy’s, Sears, Von Maur, Target and Home Depot, which are not part of the collateral. The Von Maur space, consisting of 140,000 sq. ft., is currently under construction and is expected to open in fall 2013. (6) The Appraised Value of $368.0 million includes an allocation of $11.0 million to the Eastview Commons portion of the Eastview Mall and Commons Property. (7) Historical Occupancy is based on Total Collateral Sq. Ft. (8) Current Occupancy excludes a 6,925 sq. ft. portion of The Gap/Gap Kids, which is expected to be vacated in January 2013. (9) Based on Total Sq. Ft. of 1,729,853, Current Occupancy is 97.1% as of June 26, 2012. | |||||

| Cut-off Date LTV: | 57.1% | ||||||

| Balloon LTV: | 57.1% | ||||||

| Underwritten NOI DSCR: | 2.19x | ||||||

| Underwritten NCF DSCR: | 2.17x | ||||||

| Underwritten NOI Debt Yield: | 10.3% | ||||||

| Underwritten NCF Debt Yield: | 10.2% | ||||||

| | |||||||

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

1

7979 Pittsford-Victor Road and 7550 Commons Boulevard Victor, NY 14564 | Collateral Asset Summary Eastview Mall and Commons | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $90,000,000 57.1% 2.17x 10.3% |

| Eastview Mall Anchor and Major Tenant Summary | |||||||||||||

| Tenant Mix | Ratings (Fitch/Moody’s/S&P)(1) | Total Sq. Ft. | % of Total Collateral GLA | Lease Expiration | Total Sales (000s)(2) | Sales PSF(2) | Occupancy Cost(2) | ||||||

| Non-Collateral Anchor Tenants | |||||||||||||

| Macy’s | BBB/Baa3/BBB | 168,900 | NAP | NAP | $32,000 | $189 | NAP | ||||||

| JCPenney | B+/NR/BB+ | 141,992 | NAP | NAP | $23,000 | $162 | NAP | ||||||

Von Maur(3) | NR/NR/NR | 140,000 | NAP | NAP | NAP | NAP | NAP | ||||||

| Sears | CCC/B3/CCC+ | 123,000 | NAP | NAP | $25,000 | $203 | NAP | ||||||

| Lord & Taylor | NR/NR/NR | 88,787 | NAP | NAP | $18,000 | $203 | NAP | ||||||

| Total Non-Collateral Anchors | 662,679 | $98,000 | $187 | ||||||||||

| Collateral Anchors | |||||||||||||

| Regal Cinemas | B-/B3/B+ | 76,230 | 10.5% | 2/28/2026 | $4,425 | $340,355(4) | 19.7% | ||||||

Major Tenants (>10,000 sq. ft.) | |||||||||||||

Forever 21(5) | NR/NR/NR | 45,778 | 6.3% | 8/31/2021 | NAP | NAP | NAP | ||||||

| H&M | NR/NR/NR | 18,690 | 2.6% | 1/31/2013 | $3,288 | $176 | 27.5% | ||||||

| Pottery Barn | NR/NR/NR | 12,769 | 1.8% | 1/31/2016 | $3,900 | $305 | 10.0% | ||||||

The Gap/Gap Kids(6) | BBB-/Baa3/BB+ | 12,125 | 1.7% | 12/31/2022 | $4,140 | $217 | 19.0% | ||||||

| Eckerd | CCC/Caa2/B- | 11,033 | 1.5% | 1/31/2015 | NAP | NAP | NAP | ||||||

| Victoria’s Secret | BB+/Ba1/BB+ | 10,782 | 1.5% | 1/31/2018 | $7,151 | $663 | 7.6% | ||||||

Anthropologie(7) | NR/NR/NR | 10,500 | 1.4% | 1/31/2020 | $3,308 | $315 | NAP | ||||||

| Subtotal Major Tenants | 121,677 | 16.8% | $21,788 | $303 | 14.2% | ||||||||

| In-line Tenants (<10,000 sq. ft.) | 315,564 | 43.5% | $110,105 | $420 | 13.1% | ||||||||

| Apple | NR/NR/NR | 3,614 | 0.5% | 1/31/2016 | $31,114 | $8,609 | 0.6% | ||||||

| Total In-line Tenants | 319,178 | 44.0% | $141,219 | $531 | 10.3% | ||||||||

| Outparcel | 145,076 | 20.0% | $20,413 | $250 | 8.5% | ||||||||

| Restaurant / Food Court | 16,884 | 2.3% | $5,763 | $456 | 18.0% | ||||||||

| Kiosk | 1,109 | 0.2% | $1,443 | $2,797 | 8.8% | ||||||||

| Storage | 4,565 | 0.6% | NAP | NAP | NAP | ||||||||

| Total Occupied Collateral | 684,719 | 94.4% | |||||||||||

| Vacant | 40,584 | 5.6% | |||||||||||

| Total Collateral Sq. Ft. | 725,303 | 100.0% | |||||||||||

| (1) | Certain ratings may be those of the parent company whether or not the parent company guarantees the lease. |

| (2) | Total Sales (000s), Sales PSF and Occupancy Cost are based on T-12 May 2012 sales provided by the borrower and only include tenants reporting a full 12 months of sales. Sales figures for Macy’s, JCPenney, Sears and Lord & Taylor are based upon management estimates provided to the borrower. |

| (3) | The Von Maur store is a former Bon Ton store and is currently under construction. The space is expected to be completed in fall 2013. A $4.0 million reserve was established at closing in connection with the Von Maur space. |

| (4) | Sales PSF for Regal Cinemas are reflected as sales per screen based on thirteen screens. |

| (5) | Forever 21 has the right to terminate its lease with at least three months notice and a fee equal to 50% of the unamortized portion of the tenant allowance, if gross sales during its 7th lease year (2017-2018) are less than $8,000,000. |

| (6) | The Gap/Gap Kids occupies 19,050 sq. ft., but will be downsizing to approximately 12,125 sq. ft. in January 2013. Sales PSF for The Gap/Gap Kids is based on 19,050 sq. ft. The Gap/Gap Kids has been underwritten based on 12,125 sq. ft. |

| (7) | Anthropologie pays percentage rent in lieu of base rent equal to 6.0% of annual sales. In addition, Anthropologie has the right to terminate its lease, with at least three months notice, if its annual gross sales during any calendar year from 2011-2013 are less than $4,250,000. |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

2

7979 Pittsford-Victor Road and 7550 Commons Boulevard Victor, NY 14564 | Collateral Asset Summary Eastview Mall and Commons | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $90,000,000 57.1% 2.17x 10.3% |

| Eastview Commons Anchor and Major Tenant Summary | ||||||||

Ratings (Fitch/Moody’s/S&P)(1) | Net Rentable Area (Sq. Ft.) | % of Net Rentable Area | % of Total U/W Base Rent | Lease Expiration | Total Sales (000s) | Sales PSF | Occupancy Cost | |

| Non-Collateral Anchors | ||||||||

| Target | A-/A2/A+ | 132,003 | NAP | NAP | NAP | NAP | NAP | NAP |

| Home Depot | A-/A3/A- | 123,500 | NAP | NAP | NAP | NAP | NAP | NAP |

| Total Non-Collateral Anchors | 255,503 | |||||||

| Major Tenants | ||||||||

| Best Buy | BB+/Baa2/BB+ | 34,996 | 40.5% | 23.7% | 1/31/2021 | NAP | NAP | NAP |

| Staples | BBB/Baa2/BBB | 24,100 | 27.9% | 42.8% | 2/28/2015 | NAP | NAP | NAP |

| Old Navy | BBB-/Baa3/BB+ | 18,172 | 21.0% | 33.4% | 1/31/2019 | NAP | NAP | NAP |

| Total Major Tenants | 77,268 | 89.5% | 100.0% | |||||

| Vacant | 9,100 | 10.5% | ||||||

| Total Collateral Sq. Ft. | 86,368 | 100.0% | ||||||

| (1) | Certain ratings are those of the parent company, regardless of whether the parent company guarantees the lease. |

Lease Rollover Schedule(1) | ||||||||||||||||

| Year | # of Leases Expiring | Total Expiring Sq. Ft. | % of Total Sq. Ft. Expiring | Cumulative Sq. Ft. Expiring | Cumulative % of Sq. Ft. Expiring | Annual U/W Base Rent Per Sq. Ft. | % U/W Base Rent Rolling | Cumulative % of U/W Base Rent | ||||||||

| MTM | 0 | 0 | 0.0% | 0 | 0.0% | $0.00 | 0.0% | 0.0% | ||||||||

| 2012 | 8 | 7,148 | 0.9% | 7,148 | 0.9% | $42.08 | 1.8% | 1.8% | ||||||||

| 2013 | 16 | 58,400 | 7.2% | 65,548 | 8.1% | $33.79 | 11.6% | 13.4% | ||||||||

| 2014 | 13 | 49,591 | 6.1% | 115,139 | 14.2% | $21.20 | 6.2% | 19.6% | ||||||||

| 2015 | 22 | 99,305 | 12.2% | 214,444 | 26.4% | $23.94 | 14.0% | 33.6% | ||||||||

| 2016 | 33 | 95,300 | 11.7% | 309,744 | 38.2% | $32.08 | 18.0% | 51.7% | ||||||||

| 2017 | 10 | 26,830 | 3.3% | 336,574 | 41.5% | $35.52 | 5.6% | 57.3% | ||||||||

| 2018 | 21 | 118,351 | 14.6% | 454,925 | 56.0% | $19.55 | 13.7% | 71.0% | ||||||||

| 2019 | 5 | 27,680 | 3.4% | 482,605 | 59.5% | $24.76 | 4.0% | 75.0% | ||||||||

| 2020 | 9 | 57,780 | 7.1% | 540,385 | 66.6% | $15.38 | 5.2% | 80.2% | ||||||||

| 2021 | 9 | 95,046 | 11.7% | 635,431 | 78.3% | $10.62 | 6.0% | 86.2% | ||||||||

| 2022 | 10 | 47,418 | 5.8% | 682,849 | 84.1% | $35.21 | 9.8% | 96.0% | ||||||||

| Thereafter | 2 | 79,138 | 9.8% | 761,987 | 93.9% | $8.49 | 4.0% | 100.0% | ||||||||

Vacant(2) | NAP | 49,684 | 6.1% | 811,671 | 100.0% | NAP | NAP | |||||||||

| Total / Wtd. Avg. | 158 | 811,671 | 100.0% | $22.25 | 100.00% | |||||||||||

| (1) | Certain tenants have lease termination options related to co-tenancy provisions and sales thresholds that may become exercisable prior to the originally stated expiration date of the tenant lease and that are not considered in the lease rollover schedule. |

| (2) | Vacant space includes 6,925 sq. ft. that are occupied by Gap/Gap Kids but will become vacant in January 2013 when Gap/Gap Kids downsizes its space. |

The Loan. The Eastview Mall and Commons loan (the “Eastview Mall and Commons Loan”) is a fixed rate loan secured by the borrower’s fee simple and leasehold interests in an 811,671 sq. ft. portion of a super regional mall and power center located at 7979 Pittsford-Victor Road and 7550 Commons Boulevard in Victor, New York (the “Eastview Mall and Commons Property”). The Eastview Mall and Commons Loan is comprised of the A-2 Note portion of a $210.0 million whole loan (the “Eastview Mall and Commons Loan Combination”) that is evidenced by two pari passu notes. Only the A-2 Note, with an original principal balance of $90.0 million, will be included in the COMM 2012-CCRE5 trust. The A-1 Note, with an original principal balance of $120.0 million, was included in the COMM 2012-CCRE4 securitization. The Eastview Mall and Commons Loan has a 10-year term with interest only payments.

The Eastview Mall and Commons Loan accrues interest at a fixed rate equal to 4.6250% per annum and has a cut-off date balance of $90.0 million. The whole loan proceeds were used to, among other things, retire existing debt of approximately $140.8 million, which includes approximately $95.2 million in defeasance costs, and to give the borrower a return of equity of approximately $54.8 million. Based on the appraised value of $368.0 million as of July 7, 2012, the cut-off date LTV of the Eastview Mall and Commons Loan

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

3

7979 Pittsford-Victor Road and 7550 Commons Boulevard Victor, NY 14564 | Collateral Asset Summary Eastview Mall and Commons | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $90,000,000 57.1% 2.17x 10.3% |

Combination is 57.1% and the remaining implied equity is $158.0 million. Prior to the securitization of the $120.0 million pari passu A-1 Note in the COMM 2012-CCRE4 transaction, the most recent prior financing of the Eastview Mall and Commons Property was included in the MSC 2004-HQ4 transaction.

The relationship between the holders of the A-1 Note and the A-2 Note will be governed by an intercreditor agreement to be described under “Description of the Mortgage Pool ― Loan Combinations ― The Eastview Mall and Commons Loan Combination” in the free writing prospectus.

| Sources and Uses | ||||||

| Sources | Proceeds | % of Total | Uses | Proceeds | % of Total | |

| Loan Amount | $210,000,000 | 100.0% | Loan Payoff | $140,798,951 | 67.0% | |

| Reserves | $13,154,679 | 6.3% | ||||

| Closing Costs | $1,278,775 | 0.6% | ||||

| Return of Equity | $54,767,595 | 26.1% | ||||

| Total Sources | $210,000,000 | 100.0% | Total Uses | $210,000,000 | 100.0% | |

The Borrower / Sponsor. The borrower, Eastview Mall, LLC, is a single purpose Delaware limited liability company structured to be bankruptcy-remote, with two independent directors in its organizational structure. The sponsor of the borrower and the nonrecourse carve-out guarantor is Rochester Malls, LLC, a wholly owned subsidiary of Wilmorite, a commercial real estate development and management company.

Founded in the 1940s, Wilmorite has over six decades of experience as a builder, construction manager, and real estate developer in projects involving shopping centers, academic facilities, first-class hotels and resorts. Originally a residential construction firm, Wilmorite moved into commercial construction in the 1950s, redeveloping modern high-rise offices, housing, hotels, and shopping centers. In 1967, Wilmorite acquired Greece Towne Mall, the first enclosed suburban shopping mall in upstate New York and through the 1970s and 1980s, Wilmorite opened eight major shopping malls in the eastern United States. Wilmorite remains a leading real estate management company, developer, builder and construction manager.

As of December 31, 2011, Rochester Malls, LLC had total assets, net of minority interests, of $293.1 million, of which $236.5 million relates to shopping malls.

The Property. Eastview Mall and Commons Property consists of a one-story, super regional mall and power center located in Victor, New York, built in 1971 and 1998, and renovated in 1995 and 2003. The Eastview Mall and Commons Property collateral totals 811,671 sq. ft., with 725,303 sq. ft. in the portion known as Eastview Mall and 86,368 sq. ft. in the portion known as Eastview Commons. The collateral does not include 918,182 sq. ft. leased to seven non-collateral anchor tenants, for a total mall area of 1,729,853 sq. ft. The Eastview Mall and Commons Property is 93.9% leased to approximately 150 tenants as of June 26, 2012 and has maintained an average occupancy of 94.1% since 2009. Including the non-collateral anchor tenants, the total mall area is 97.1% leased.

Eastview Mall consists of 1,387,982 total square feet, of which 725,303 sq. ft. is collateral for the Eastview Mall and Commons Loan. Eastview Mall was originally built in 1971 by the sponsor and subsequently underwent two significant renovations in 1995 and 2003, with a planned third expansion underway. In 1995, approximately 525,000 square feet were added to what was then a 750,000 square foot mall, along with other renovations to the existing space, for a total cost of approximately $25.0 million ($48 PSF). In 2003, the sponsor added approximately 57,854 sq. ft. consisting of four new inline stores and three exterior restaurants, at an approximate cost of $21.0 million ($363 PSF). The third renovation consists of the construction of the new Von Maur store, which is expected to open in the fall of 2013, at the recently demolished former Bon Ton space. The mall is anchored by Regal Cinemas, JCPenney, Lord & Taylor, Macy’s and Sears. Regal Cinemas is the only anchor tenant that is collateral for the Eastview Mall and Commons Loan. Macy’s and Sears own their own improvements, and JCPenney and Lord & Taylor are expected to purchase their own improvements in 2014 when the TIF Bonds (see “TIF Financing” herein) are paid. Von Maur will also own its own improvements and will not serve as collateral for the Eastview Mall and Commons Loan. The Eastview Mall collateral is 94.4% leased as of June 26, 2012 (97.1% leased including non-collateral anchor tenants).

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

4

7979 Pittsford-Victor Road and 7550 Commons Boulevard Victor, NY 14564 | Collateral Asset Summary Eastview Mall and Commons | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $90,000,000 57.1% 2.17x 10.3% |

Eastview Commons consists of 341,871 total sq. ft., of which 86,368 sq. ft. is collateral for the Eastview Mall and Commons Loan. Eastview Commons was built in 1998. Eastview Commons is anchored by Target and Home Depot, neither of which is collateral for the Eastview Mall and Commons Loan. The collateral space includes Staples, Old Navy and Best Buy, with one 9,100 sq. ft. vacant space. Eastview Commons is 89.5% leased as of June 26, 2012 (97.3% leased including non-collateral anchor tenants).

Eastview Mall and Commons Historical Sales PSF(1) | ||||||||||||

| 2009 | 2010 | 2011(2) | T-12 May 2012 | T-12 May 2012 Occupancy Cost | 2011 National Avg. | |||||||

| Macy’s | NAP | NAP | $189 | NAP | NAP | $154 | ||||||

| JCPenney | NAP | NAP | $162 | NAP | NAP | $145 | ||||||

| Sears | NAP | NAP | $203 | NAP | NAP | $148 | ||||||

| Lord and Taylor | NAP | NAP | $203 | NAP | NAP | NAP | ||||||

Regal Cinemas(3) | NAP | $301,987 | $310,378 | $340,355 | 19.7% | NAP | ||||||

| Major Tenants (>10,000 sq. ft.) | $150 | $214 | $294 | $303 | 14.2% | |||||||

| In-line Tenants (<10,000 sq. ft.) | $397 | $407 | $408 | $420 | 13.1% | |||||||

Apple(4) | $5,165 | $7,111 | $8,133 | $8,609 | 0.6% | $5,647 | ||||||

| Total In-line Tenants | $470 | $496 | $507 | $531 | 10.3% | |||||||

| (1) | Historical Sales PSF is based on historical statements provided by the sponsor. |

| (2) | 2011 Sales PSF figures for Macy’s, JCPenney, Sears and Lord & Taylor are based upon management estimates provided to the sponsor. |

| (3) | Regal Cinemas’ sales are reflected as sales per screen based on thirteen screens. |

| (4) | The Apple store at the Eastview Mall and Commons Property is the only Apple retail store in an approximate 75 mile radius. |

TIF Financing. In connection with the 1995 expansion and renovation of the Eastview Mall and Commons Property, Great Eastern Mall L.P. (“GEM”), the direct parent of the borrower, entered into a financing arrangement with the Town of Victor, pursuant to which the Town of Victor agreed to issue tax incremental funding bonds (“TIF Bonds”) and exempt a portion of the property (“TIF Property”) from the payment of taxes and assessments. In connection therewith, GEM deeded the TIF Property to the Town of Victor and the Town of Victor leased the TIF Property back to GEM. The TIF Bonds will mature in 2014 and upon payment in full, the ground lease will terminate and in connection therewith Town of Victor will convey fee ownership of the TIF Property (less the JCPenney and Lord & Taylor sites) to the borrower and fee ownership of the JCPenney and Lord & Taylor sites to each tenant, respectively (and Borrower shall have no further interest in such sites). The borrower has deposited $1,782,727 into a TIF payment fund reserve at M&T Bank (not collateral for the Eastview Mall and Commons Loan), which is the amount needed from the borrower for the two remaining payments on the TIF Bonds (JCPenney and Lord & Taylor are responsible for their pro rata payments). In addition, the borrower deposited $8.0 million into a PIF/CapEx reserve at closing. If either of JCPenney or Lord & Taylor fails to pay their pro rata share of the outstanding payments due under the TIF Bond (approximately $289,485 for JCPenney and approximately $208,000 for Lord & Taylor), the borrower is required to make such payments on behalf of JCPenney and/or Lord & Taylor. If the borrower fails to do so, the lender has the right, but not the obligation, to make such payments on the borrower’s behalf by withdrawing funds from the PIF/CapEx Account and the borrower is required to deposit funds equal to such amount within five days of lender’s withdrawal. Losses incurred as a result of the borrower’s failure to make such payments with respect to the TIF Bonds, are recourse to the sponsor.

IDA PILOT. In connection with the 2003 renovation of the Eastview Mall and Commons Property, the Ontario County Industrial Development Agency (the “IDA”) entered into a payment in-lieu-of taxes (“PILOT”) agreement with the borrower through December 31, 2041, which sets forth a schedule of payments the borrower must make to the various taxing authorities. The total tax expense being passed along to the tenants at the Eastview Mall and Commons Property is approximately $4.8 million; however, the amount paid to the taxing authorities is approximately $2.1 million. The remaining approximate $2.7 million is swept two times a year into the deposit account controlled by lender and, provided no trigger event is occurring, will be disbursed to the borrower to be used to reimburse the sponsor for capital expenditures and related financing costs at the Eastview Mall and Commons Property. The sponsor agreed to spend approximately $30.575 million in capital expenditures and related costs for the Eastview Mall and Commons Property and spent such amount by obtaining a $30.0 million loan from M&T Bank, which loan was repaid with proceeds from the Eastview Mall and Commons Loan. In connection with the PILOT, the IDA put a subordinate mortgage on the Eastview Mall and Commons Property (which mortgage secures the scheduled PILOT payments Borrower is obligated to make to the IDA). Pursuant to an Intercreditor Agreement between Lender and the IDA, the IDA mortgage is subordinate to the senior mortgage and the Lender is afforded certain notice and cure rights under the various documents entered into by Borrower and the IDA in connection with the PILOT Agreement.

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

5

7979 Pittsford-Victor Road and 7550 Commons Boulevard Victor, NY 14564 | Collateral Asset Summary Eastview Mall and Commons | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $90,000,000 57.1% 2.17x 10.3% |

Environmental Matters. The Phase I environmental report dated July 16, 2012 recommended no further action at the Eastview Mall and Commons Property, other than the continued implementation of the asbestos operation and maintenance plan.

The Market. The Eastview Mall and Commons Property is located in Victor, New York, within the Rochester metropolitan statistical area (“Rochester MSA”), approximately 14 miles southeast of downtown Rochester. Rochester has a population of approximately 1.1 million people and is home to several international businesses. Education and health services represent the largest sectors in the Rochester MSA, representing 21.3% of the area employment. The Rochester MSA supports approximately 16 colleges and universities, with the University of Rochester being the largest employer in the area. The unemployment rate as of March 2012 was 8.0%. Rochester has traditionally had a low unemployment rate, with an average of 5.8% between 2001 and 2011, lower than the national average of 6.4% over the same period.

The town of Victor is part of the Finger Lakes region and benefits from its proximity to tourism and vacation destinations. The trade area for the Eastview Mall and Commons Property spans an area encompassing approximately ten to fifteen miles around the center. The appraiser determined the 2011 population within a three-mile radius to be 15,386, with an average household income of $125,869. As of Q2 2012, the Rochester retail market consists of 5,085 properties with approximately 63.2 million square feet of inventory, with an overall vacancy rate of 6.3%. The five mall properties in the market total approximately 5.7 million square feet with an average vacancy of 6.2%.

The Eastview Mall and Commons Property has two primary competitors, Marketplace Mall and Mall at Greece Ridge, both of which are owned by the sponsor.

Competitive Set(1) | |||||

| Name | Eastview Mall and Commons Property | Marketplace Mall | Mall at Greece Ridge | Walden Galleria | Carousel Center / Destiny USA |

| Distance from Subject | NAP | 12.5 miles | 23.0 miles | 78.0 miles | 73.0 miles |

| Property Type | Super Regional Mall | Super Regional Mall | Super Regional Mall | Super Regional Mall | Super Regional Mall |

| Owner | Wilmorite | Wilmorite | Wilmorite | Pyramid Companies | Pyramid Companies |

| Year Built / Renovated | 1971, 1998 / 1995, 2003 | 1982 / 1993 | 1967, 1971 / 1994 | 1989 / 2008 | 1990 / 2000 |

Sales PSF (in-line)(2) | $420 | $385 | $380 | $550 | $500 |

Total Occupancy(3) | 97.1% | 88.0% | 85.0% | 85.0% | 77.0% |

| Size (Sq. Ft.) | 1,729,853 | 946,000 | 1,543,921 | 1,620,000 | 2,366,741 |

| Anchors / Major Tenants | Macy’s; JCPenney; Sears; Lord & Taylor; Von Maur (future) | Dick’s Sporting Goods; JCPenney; Macy’s; Sears; Bon-Ton | JCPenney; Macy’s; Sears; Burlington Coat Factory; Regal Cinemas | Dick’s Sporting Goods; JCPenney; Lord & Taylor; Macy’s; Sears; Regal Cinemas | JCPenney; Lord & Taylor; Macy’s; Bon Ton; Regal Cinemas |

| (1) | Source: Appraisal |

| (2) | Sales PSF for the Eastview Mall and Commons Property excludes Apple. Including Apple, Sales PSF would be $531 PSF. |

| (3) | Total Occupancy for the Eastview Mall and Commons Property is based on Total Sq. Ft. of 1,729,853. |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

6

7979 Pittsford-Victor Road and 7550 Commons Boulevard Victor, NY 14564 | Collateral Asset Summary Eastview Mall and Commons | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $90,000,000 57.1% 2.17x 10.3% |

Cash Flow Analysis.

| Cash Flow Analysis | ||||||

| 2009 | 2010 | 2011 | T-12 5/31/2012 | U/W | U/W PSF | |

Base Rent(1) | $15,961,743 | $16,487,430 | $16,331,918 | $16,592,254 | $17,336,929 | $21.36 |

| Value of Vacant Space | 0 | 0 | 0 | 0 | 1,611,369 | 1.99 |

| Gross Potential Rent | $15,961,743 | $16,487,430 | $16,331,918 | $16,592,254 | $18,948,298 | $23.34 |

| Total Recoveries | 9,631,140 | 10,371,822 | 10,627,765 | 11,710,968 | 13,453,140 | 16.57 |

| Total Other Income | 955,538 | 1,267,181 | 1,435,112 | 1,369,665 | 1,635,054 | 2.01 |

| Less: Mark to Market | 0 | 0 | 0 | 0 | (245,640) | (0.30) |

Less: Vacancy(2) | 0 | 0 | 0 | 0 | (1,611,369) | (1.99) |

| Effective Gross Income | $26,548,421 | $28,126,433 | $28,394,795 | $29,672,887 | $32,179,483 | $39.65 |

| Total Operating Expenses | 8,585,492 | 9,120,115 | 9,555,968 | 10,081,935 | 10,644,054 | 13.11 |

| Net Operating Income | $17,962,929 | $19,006,318 | $18,838,827 | $19,590,952 | $21,535,429 | $26.53 |

| TI/LC | 113,362 | 82,064 | 88,258 | 87,615 | 739,399 | 0.91 |

| Capital Expenditures | 0 | 0 | 0 | 0 | 243,501 | 0.30 |

Upfront TI/LC Reserve Credit(3) | 0 | 0 | 0 | 0 | (800,000) | (0.99) |

| Net Cash Flow | $17,849,567 | $18,924,254 | $18,750,569 | $19,444,490 | $21,352,529 | $26.31 |

Average Annual Rent PSF(4) | $21.05 | $21.47 | $21.34 | |||

| (1) | U/W Base Rent includes $385,107 in contractual step rent through August 2013. |

| (2) | U/W Vacancy represents 4.7% of gross income. |

| (3) | The Upfront TI/LC Reserve Credit is based on the $8.0 million upfront PIF/CapEx reserve. |

| (4) | Historical Average Annual Rent PSF is based on historical operating statements and occupancy rates provided by the Eastview Mall and Commons borrower and exclude non-collateral anchors. |

Property Management. The Eastview Mall and Commons Property is managed by Wilmorite Management Group, LLC, a borrower affiliate.

Lockbox / Cash Management. The Eastview Mall and Commons Loan is structured with a hard lockbox and in place cash management. Tenants were instructed to deposit all rents and other payments directly into the lockbox account controlled by the lender. All funds in the lockbox account are required to be swept daily to a cash management account under the control of the lender and disbursed in accordance with the Eastview Mall and Commons Loan documents.

Additionally, all excess cash will be swept into a lender controlled account upon an event of default or if the DSCR for the trailing 12-month period is less than 1.20x on the last day of the calendar quarter until the DSCR is 1.25x or greater for two consecutive calendar quarters.

Initial Reserves. At closing, the borrower deposited (i) $1,154,679 into a tax reserve account, (ii) $8,000,000 into a PIF/CapEx reserve to be used for approved expenses under the PILOT agreement, and (iii) $4,000,000 into the Von Maur expenditure reserve.

Ongoing Reserves. On a monthly basis, the borrower is required to deposit reserves of (i) 1/12 of the estimated annual real estate taxes, which currently equates to $131,255 into a tax reserve account. The borrower will be required to deposit 1/12 of the annual insurance premiums into the insurance reserve if an acceptable blanket insurance policy is no longer in place. If the amount on deposit in the PIF/CapEx account falls below $1,000,000, the borrower is required to make monthly deposits of $81,908, subject to a cap of $1,200,000 (collectively in the PIF/CapEx reserve and the CapEx & TI/LC reserve), into a CapEx & TI/LC reserve to be used for approved capital expenditures and leasing commissions.

Current Mezzanine or Subordinate Indebtedness. None.

Future Mezzanine or Subordinate Indebtedness Permitted. None.

Partial Release. None. See “TIF Financing” section above regarding the conveyance of the JCPenney and Lord & Taylor parcels.

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

7

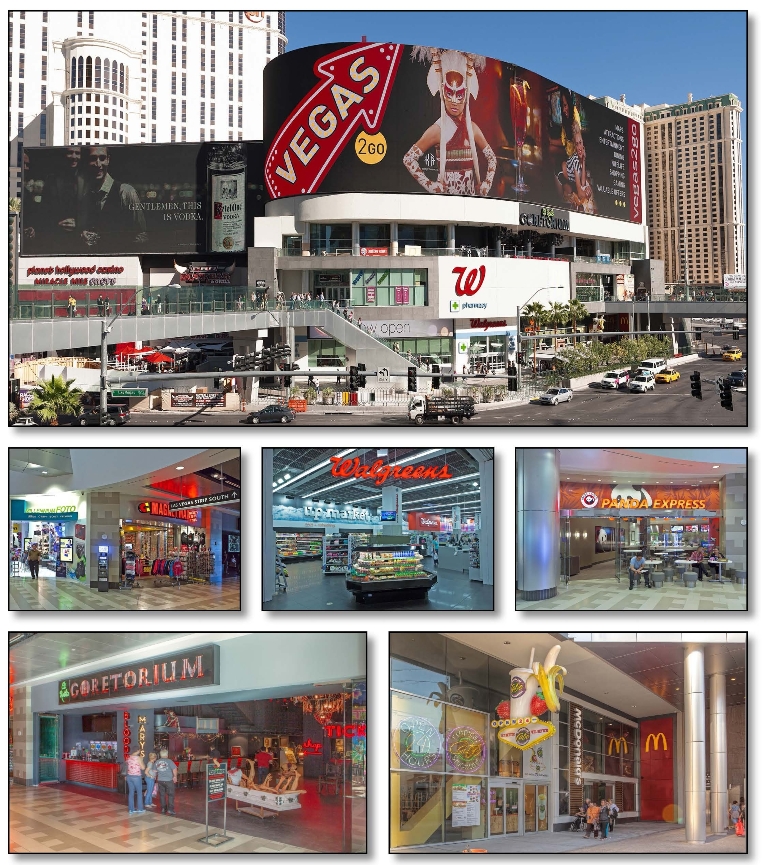

3717 Las Vegas Boulevard South Las Vegas, NV 89109 | Collateral Asset Summary Harmon Corner | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $74,895,512 61.8% 1.63x 9.7% |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

8

3717 Las Vegas Boulevard South Las Vegas, NV 89109 | Collateral Asset Summary Harmon Corner | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $74,895,512 61.8% 1.63x 9.7% |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

9

3717 Las Vegas Boulevard South Las Vegas, NV 89109 | Collateral Asset Summary Harmon Corner | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $74,895,512 61.8% 1.63x 9.7% |

| Mortgage Loan Information | Property Information | ||||||

| Loan Seller: | CCRE | Single Asset / Portfolio: | Single Asset | ||||

| Loan Purpose: | Refinance | Property Type: | Anchored Retail | ||||

| Sponsor: | Brett Torino; Paul Kanavos; | Collateral: | Fee Simple | ||||

| Steven J. Johnson | Location: | Las Vegas, NV | |||||

| Borrower: | BPS Harmon, LLC | Year Built / Renovated: | 2012 / NAP | ||||

Original Balance(1): | $75,000,000 | Total Sq. Ft.: | 66,833 | ||||

Cut-off Date Balance(1): | $74,895,512 | Property Management: | BPS Management Services, LLC | ||||

| % by Initial UPB: | -.-% | Underwritten NOI: | $10,648,994 | ||||

| Interest Rate: | 4.1880% | Underwritten NCF: | $10,535,627 | ||||

| Payment Date: | 6th of each month | Appraised Value(4): | $177,700,000 | ||||

| First Payment Date: | December 6, 2012 | Appraisal Date(4): | January 1, 2013 | ||||

| Maturity Date: | November 6, 2022 | ||||||

| Amortization: | 360 months | Historical NOI(6) | |||||

Additional Debt(1): | $34,951,239 Pari Passu Debt | YTD NOI: | $3,037,722 (August 31, 2012) | ||||

| Call Protection: | L(25), D(89), O(6) | ||||||

| Lockbox / Cash Management: | Hard / In Place | Historical Occupancy | |||||

Current Occupancy(7): | 100.0% (November 15, 2012) | ||||||

Reserves(2) | (1) The Original Balance of $75.0 million and Cut-off Date Balance of $74.9 million represent the Note A-1 of a $110.0 million whole loan evidenced by two pari passu notes. The pari passu companion loan is the Note A-2 in the original principal amount of $35.0 million. (2) See “Initial Reserves” and “Ongoing Reserves” herein. (3) The TI/LC Reserve was collected to fund all outstanding tenant improvement allowances and leasing commissions owed in connection with recent leases. The Free Rent Reserve was collected to cover any free rent periods between the first payment date of the loan and the hard rent commencement dates for all tenants. The latest hard rent commencement date is March 22, 2013. (4) Cut-off Date LTV, Balloon LTV and Appraised Value are based on the market value as of January 1, 2013. The appraised value as of August 6, 2012 is $173,500,000, which is $4.2 million less than the market value as of January 1, 2013. The market value as of January 1, 2013 assumes that all tenant improvement allowances and leasing commissions have been paid and that all free rent periods have expired. Lender reserved approximately $4.9 million to fund all such outstanding tenant improvement allowances and leasing commissions as well as to cover free rent periods. (5) DSCR, LTV, Debt Yield and Balance / Sq. Ft. calculations are based on the aggregate Cut-off Date Balance of $109.8 million. (6) The Harmon Corner Property was completed in 2012 with the first tenants taking occupancy in early 2012. Historical NOI is based on the year-to-date financials as of August 31, 2012 and represents only partial year financials during the lease up period of the Harmon Corner Property. See “Cash Flow Analysis” herein for additional detail. (7) All tenants have accepted possession of their spaces and delivered clean estoppels. No tenants have termination options tied to the delivery of space or other landlord obligations. Current Occupancy includes tenants that have not yet opened for business. As of November 15, 2012, 16 out of 19 tenants were open for business. According to the borrower, two of the final tenants are scheduled to open by year-end 2012 with the last tenant to open in March 2013. | ||||||

| Initial | Monthly | ||||||

| Taxes: | $42,000 | $21,000 | |||||

| Insurance: | $73,813 | $6,710 | |||||

| Replacement: | $0 | $1,114 | |||||

TI/LC(3)(4): | $4,165,103 | $8,333 | |||||

Free Rent(3)(4): | $731,208 | $0 | |||||

Financial Information(5) | |||||||

| Cut-off Date Balance / Sq. Ft.: | $1,121 | ||||||

| Balloon Balance / Sq. Ft.: | $897 | ||||||

Cut-off Date LTV(4): | 61.8% | ||||||

Balloon LTV(4): | 49.5% | ||||||

| Underwritten NOI DSCR: | 1.65x | ||||||

| Underwritten NCF DSCR: | 1.63x | ||||||

| Underwritten NOI Debt Yield: | 9.7% | ||||||

| Underwritten NCF Debt Yield: | 9.6% | ||||||

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

10

3717 Las Vegas Boulevard South Las Vegas, NV 89109 | Collateral Asset Summary Harmon Corner | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $74,895,512 61.8% 1.63x 9.7% |

| Tenant Summary | |||||||

Tenant | Ratings (Fitch/Moody’s/S&P) | Net Rentable Area (Sq. Ft.) | % of Net Rentable Area | U/W Base Rent PSF | % of Total U/W Base Rent | Lease Expiration | |

| Eli Roth’s Goretorium (“Goretorium”) | NR/NR/NR | 14,799 | 22.1% | $120.29 | 15.2% | 9/30/2022 | |

| Bubba Gump Shrimp Co. | NR/NR/NR | 12,782 | 19.1% | $93.81 | 10.2% | 11/30/2022(1) | |

| Twin Peaks | NR/NR/NR | 11,834 | 17.7% | $136.14 | 13.7% | 12/31/2022(2) | |

| McDonald’s | A/A2/A(3) | 6,217 | 9.3% | $148.79 | 7.9% | 4/30/2022 | |

| Walgreens | NR/Baa1/BBB(3) | 4,033(4) | 6.0% | $119.02 | 4.1% | 2/28/2042(5) | |

| DLV Kiosk Group | NR/NR/NR | NAP(6) | 0.0% | $143,250(6) | 9.8% | 6/30/2017 | |

| Total Major Tenants | 49,665 | 74.3% | $143.79(7) | 60.9% | |||

| Remaining Tenants | 17,168 | 25.7% | $267.26 | 39.1% | |||

| Total Occupied Collateral | 66,833 | 100.0% | $175.50(7) | 100.0% | |||

| Vacant | 0 | 0.0% | |||||

| Total | 66,833 | 100.0% | |||||

| (1) | The Bubba Gump Shrimp Co. lease includes a termination option, which may become effective no earlier than November 30, 2015 and is subject to a lease termination payment. |

| (2) | The Twin Peaks lease includes a termination option, which may become effective no earlier than June 30, 2018 and is subject to a lease termination payment. |

| (3) | Certain ratings may be those of the parent company whether or not the parent company guarantees the lease. |

| (4) | The 4,033 sq. ft. Walgreens space is the second floor portion of a larger 23,908 sq. ft. two-floor store, which includes 19,875 sq. ft. of ground floor space that is not collateral for the Harmon Corner Loan. |

| (5) | The Walgreens lease expires February 28, 2111 with an initial termination option effective February 28, 2042. The ground floor lease is coterminous with the second floor lease. |

| (6) | DLV Kiosk Group has eight kiosk spaces within the Harmon Corner Property and does not have any net rentable area assigned to it as it occupies space within common areas. DLV Kiosk Group U/W Base Rent PSF is based on the average U/W Base Rent per kiosk space (eight spaces). |

| (7) | U/W Base Rent PSF totals include $1,146,000 of U/W Base Rent attributed to the DLV Kiosk Group space, which does not have any net rentable area assigned to it. |

Lease Rollover Schedule(1) | ||||||||

| Year | # of Leases Expiring | Total Expiring Sq. Ft. | % of Total Sq. Ft. Expiring | Cumulative Sq. Ft. Expiring | Cumulative % of Sq. Ft. Expiring | Annual U/W Base Rent Per Sq. Ft. | % U/W Base Rent Rolling | Cumulative % of U/W Base Rent |

| MTM | 0 | 0 | 0.0% | 0 | 0.0% | $0.00 | 0.0% | 0.0% |

| 2012 | 0 | 0 | 0.0% | 0 | 0.0% | $0.00 | 0.0% | 0.0% |

| 2013 | 0 | 0 | 0.0% | 0 | 0.0% | $0.00 | 0.0% | 0.0% |

| 2014 | 0 | 0 | 0.0% | 0 | 0.0% | $0.00 | 0.0% | 0.0% |

| 2015 | 0 | 0 | 0.0% | 0 | 0.0% | $0.00 | 0.0% | 0.0% |

| 2016 | 0 | 0 | 0.0% | 0 | 0.0% | $0.00 | 0.0% | 0.0% |

2017(2) | 2 | 288 | 0.4% | 288 | 0.4% | $4,847.22(2) | 11.9% | 11.9% |

| 2018 | 0 | 0 | 0.0% | 288 | 0.4% | $0.00 | 0.0% | 11.9% |

| 2019 | 0 | 0 | 0.0% | 288 | 0.4% | $0.00 | 0.0% | 11.9% |

| 2020 | 0 | 0 | 0.0% | 288 | 0.4% | $0.00 | 0.0% | 11.9% |

| 2021 | 1 | 1,402 | 2.1% | 1,690 | 2.5% | $216.69 | 2.6% | 14.5% |

| 2022 | 15 | 61,110 | 91.4% | 62,800 | 94.0% | $156.27 | 81.4% | 95.9% |

| Thereafter | 1 | 4,033 | 6.0% | 66,833 | 100.0% | $119.02 | 4.1% | 100.0% |

| Vacant | NAP | 0 | 0.0% | 66,833 | 100.0% | NAP | NAP | |

| Total / Wtd. Avg. | 19 | 66,833 | 100.0% | $175.50 | 100.0% | |||

| (1) | Certain tenants have lease termination options that may become exercisable prior to the originally stated expiration date of the tenant lease and that are not considered in the lease rollover schedule. |

| (2) | 2017 expiring tenants include one tenant for 288 sq. ft. and DLV Kiosk Group, which does not have any net rentable area assigned to it as it occupies space within common areas of the Harmon Corner Property. DLV Kiosk Group has total U/W Base Rent of $1,146,000. |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

11

3717 Las Vegas Boulevard South Las Vegas, NV 89109 | Collateral Asset Summary Harmon Corner | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $74,895,512 61.8% 1.63x 9.7% |

The Loan. The Harmon Corner loan (the “Harmon Corner Loan”) is a fixed rate loan secured by the borrower’s fee simple interest in a 66,833 square foot Class A, anchored retail center located at 3717 Las Vegas Boulevard South (the “Las Vegas Strip”) in Las Vegas, Nevada (the “Harmon Corner Property”) with an original principal balance of $75.0 million. The Harmon Corner Loan of $75.0 million represents the controlling Note A-1 of a $110.0 million whole loan (the “Harmon Corner Loan Combination”) evidenced by two pari passu notes. Only the $75.0 million controlling Note A-1 will be included in the COMM 2012-CCRE5 trust. The Note A-2, with an original principal balance of $35.0 million, is held by CCRE and is expected to be included in a future securitization. The Harmon Corner Loan Combination has a 10-year term and amortizes on a 30-year schedule. The Harmon Corner Loan accrues interest at a fixed rate equal to 4.1880% and has a cut-off date balance of approximately $74.9 million. Loan proceeds were used to retire existing debt provided by W.P. Carey, Inc. of approximately $47.6 million and return equity to the borrower of approximately $56.1 million. Based on the appraised value of $177.7 million as of January 1, 2013, the cut-off date LTV is 61.8% and the remaining implied equity is $67.9 million. The most recent prior financing of the Harmon Corner Property was not included in a securitization.

| Sources and Uses | ||||||

| Sources | Proceeds | % of Total | Uses | Proceeds | % of Total | |

| Loan Combination Amount | $110,000,000 | 100.0% | Loan Payoff | $47,638,683 | 43.3% | |

| Reserves | $5,012,124 | 4.6% | ||||

| Closing Costs | $1,230,029 | 1.1% | ||||

| Return of Equity | $56,119,163 | 51.0% | ||||

| Total Sources | $110,000,000 | 100.0% | Total Uses | $110,000,000 | 100.0% | |

The Borrower / Sponsor. The borrower, BPS Harmon, LLC, is a single purpose Delaware limited liability company structured to be bankruptcy-remote, with two independent directors in its organizational structure. The sponsors of the borrower and the nonrecourse carve-out guarantors, jointly and severally, are Brett Torino, Paul Kanavos and Steven J. Johnson (the “Harmon Corner Sponsors”). W.P. Carey, Inc. (“W.P. Carey”) holds a 15% equity interest in the borrower.

Brett Torino serves as the CEO and president of Torino Companies. Mr. Torino has approximately 30 years of real estate experience and has led the development, construction and sale of commercial, residential and resort properties in California, Colorado, Nevada and Arizona. For the last 20 years, Mr. Torino has focused primarily on properties located in Las Vegas with significant experience on the Las Vegas Strip.

Paul Kanavos founded Flag Luxury Properties, LLC in 1996 and serves as its CEO. Mr. Kanavos has developed Ritz-Carlton Hotels in South Beach, Coconut Grove and Jupiter as well as the St. Regis Resort Temenos Anguilla.

Steven J. Johnson is the principal of SJJ Development, LLC. Within the past 35 years, Mr. Johnson has developed in excess of 6.0 million sq. ft. of neighborhood shopping centers. Mr. Johnson has developed approximately 130 Walgreens locations throughout Arizona, New Mexico, Texas and Nevada including 27 in Las Vegas.

W.P. Carey Inc. is a publicly traded REIT (NYSE: WPC) that provides long-term sale-leaseback and build-to-suit financing for companies worldwide and manages an investment portfolio of approximately $12.7 billion as of October 2012. W.P. Carey is the largest owner/manager of net lease assets in the world. As of October 2012, the company had a market capitalization of approximately $5.0 billion and portfolio of assets consisting of 429 properties totaling 39.1 million sq. ft. with a 97.6% occupancy rate and average lease term of 8.9 years.

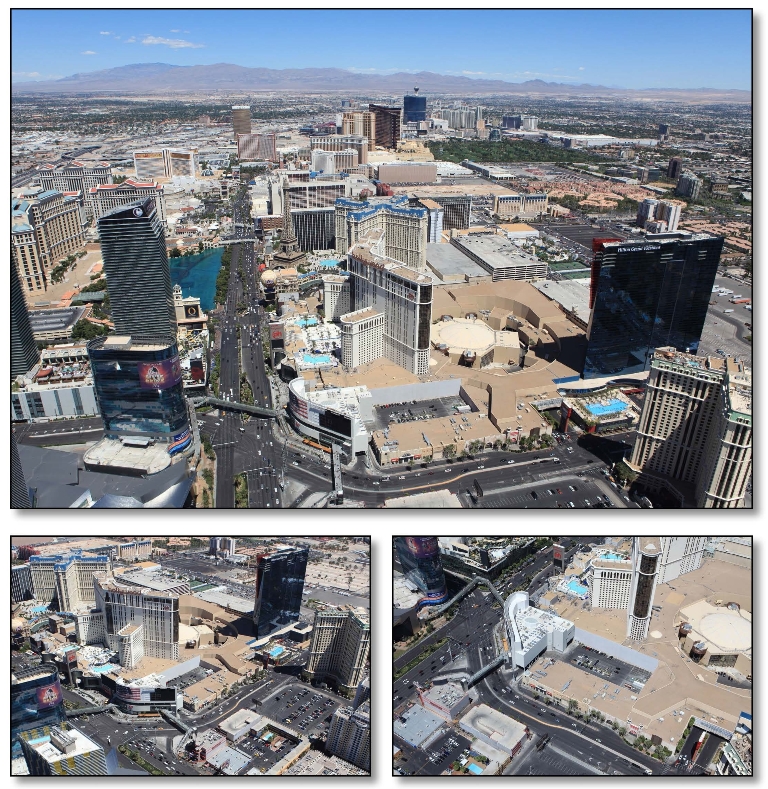

The Property. The Harmon Corner Property is located on the east side of the Las Vegas Strip at the intersection of Harmon Avenue in Las Vegas, Nevada, adjacent to Miracle Mile Shops at Planet Hollywood and directly across the Las Vegas Strip from CityCenter and the Cosmopolitan Hotel. Constructed in 2012, the Harmon Corner Property consists of a 100.0% leased, three-story building totaling 66,833 sq. ft. with 19 tenants including Walgreens, Goretorium, Twin Peaks, Bubba Gump Shrimp Co. and McDonald’s.

The Harmon Corner Property is part of a larger development consisting of a 110,000 sq. ft. retail structure with a three-story LED billboard sign attached and an adjacent 156 space outdoor parking lot. The 19,875 sq. ft. ground floor portion of the Walgreens, the LED billboard sign and the parking lot are all excluded from the collateral for the Harmon Corner Loan. The total costs to build the entire development were approximately $95.0 million, with approximately $79.4 million attributed to the collateral.

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-172143) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

12

3717 Las Vegas Boulevard South Las Vegas, NV 89109 | Collateral Asset Summary Harmon Corner | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $74,895,512 61.8% 1.63x 9.7% |

Pedestrian bridges above Harmon Avenue and the Las Vegas Strip connect directly to the second floor of the Harmon Corner Property and generate a significant amount of daily foot traffic, estimated to be approximately 74,000 pedestrians per day. The Harmon Corner Sponsors developed the bridge over Harmon Avenue, providing uninterrupted foot traffic along the east side of the Las Vegas Strip directly through the second floor of the Harmon Corner Property. In addition, the Harmon Corner Sponsors connected an already existing bridge over the Las Vegas Strip directly into the second floor of the Harmon Corner Property.

The Harmon Corner Property is anchored by a two-story, 23,908 sq. ft. Walgreens, of which the 4,033 sq. ft. second floor portion of the store is collateral for the Harmon Corner Loan. Walgreens is required to report sales on an annual basis and has not yet reported sales; however, the Harmon Corner Sponsors indicated that this Walgreens is achieving estimated sales of approximately $2.9 million per month (representing $34.8 million annually or $1,456 PSF). In addition, six in-line tenants that are open for business have reported sales for at least six months. Excluding the first partial month for each of these tenants, average annualized sales PSF are approximately $1,200 PSF (summarized below):

| Historical Sales PSF | ||||

| Sq. Ft. | Total Annualized Sales | $PSF | Period | |

| Panda Express | 1,402 | $2,088,394 | $1,490 | T8 9/30/2012 |

| Maui Magnets | 1,400 | $1,943,581 | $1,388 | T9 10/31/2012 |

| Beauty One | 980 | $1,226,998 | $1,252 | T5 10/31/2012 |

| Viva Vegas | 1,421 | $1,758,413 | $1,237 | T9 10/31/2012 |

| Afterhours | 1,529 | $1,795,037 | $1,174 | T8 10/31/2012 |

| Rockin’ Taco | 3,018 | $2,804,668 | $929 | T5 10/31/2012 |

| Total / Wtd. Avg. | 9,750 | $11,617,090 | $1,191 | NAP |

The three largest tenants included in the collateral for the Harmon Corner Loan are Goretorium, Bubba Gump Shrimp Co. and Twin Peaks. All three of these tenants have space on both the second and third floors of the Harmon Corner Property. The second floor spaces for each of these tenants are located adjacent to the pedestrian bridge entrances and the third floor spaces all have outdoor terraces facing the Las Vegas Strip. Goretorium opened for business on October 1, 2012 with Twin Peaks and Bubba Gump Shrimp Co. in the process of completing their build-outs. Bubba Gump Shrimp Co. and Twin Peaks are expected to open for business in December 2012 and March 2013, respectively. Descriptions for these tenants are provided in the “Major Tenants” section herein.

Environmental Matters. The Phase I environmental report dated August 14, 2012 recommended no further action at the Harmon Corner Property.

Major Tenants.

Walgreens (4,033 sq. ft., 6.0% of NRA, 4.1% of U/W Base Rent)

Walgreens (NYSE: WAG) (NR/Baa1/BBB by Fitch/Moody’s/S&P) is the largest drug retailing chain in the US with more than 8,300 locations and approximately 240,000 employees as of August 31, 2012. Walgreens reported fiscal 2012 net sales of $71.6 billion and net earnings of $2.1 billion. Walgreens had a market capitalization as of November 19, 2012 of approximately $30.8 billion. Walgreens also occupies an additional 19,875 sq. ft. of space in the development, which is not part of the collateral for the Harmon Corner Loan, making the total store size equal to 23,908 sq. ft.

Eli Roth’s Goretorium (14,799 sq. ft., 22.1% of NRA, 15.2% of U/W Base Rent)

Eli Roth’s Goretorium (“Goretorium”) is a live, self-guided horror experience created by Eli Roth, an American film director, producer, writer and actor. Goretorium consists of more than 20 rooms with different displays and ends with a drinks lounge featuring outdoor space overlooking the Las Vegas Strip. Goretorium opened October 1, 2012. According to the Harmon Corner Sponsors, Goretorium has invested approximately $8 million ($541 PSF) to build out its space. Goretorium has a lease expiration date of September 30, 2022 and two five-year renewal options.

Bubba Gump Shrimp Co. (12,782 sq. ft., 19.1% of NRA, 10.2% of U/W Base Rent)

Bubba Gump Shrimp Co. is an international seafood restaurant chain which provides a casual dining environment. The first Bubba Gump Shrimp Co. restaurant and market opened in 1996 in Monterey, CA and has since grown to 36 locations worldwide including Times Square New York, Universal CityWalk Orlando, Victoria’s Peak Hong Kong, Santa Monica Pier, and Pier 39 in San Francisco. Bubba Gump Shrimp Co. is owned by Landry’s, Inc., which purchased Bubba Gump Shrimp Co. in 2010. Landry’s, Inc. is the owner