1 1 Keefe, Bruyette & Woods 2012 Boston Bank Conference February 29, 2012 Exhibit 99.2 |

2 2 FORWARD-LOOKING FORWARD-LOOKING INFORMATION INFORMATION During the course of our remarks today, we will make During the course of our remarks today, we will make certain predictive statements regarding our plans and certain predictive statements regarding our plans and strategies and anticipated financial effects to assist you strategies and anticipated financial effects to assist you better in understanding our company. better in understanding our company. These forward looking statements about future results These forward looking statements about future results are subject to risks and uncertainties. are subject to risks and uncertainties. Refer to our periodic reports on file with the SEC and the Refer to our periodic reports on file with the SEC and the slides at the end of this presentation regarding forward- slides at the end of this presentation regarding forward- looking statements for further detail in this regard. looking statements for further detail in this regard. |

Today’s Presentation Today’s Presentation Who we are Who we are Where we have been-how we got here Where we have been-how we got here Where we are going Where we are going Summary financial results Summary financial results Questions Questions 3 3 |

|

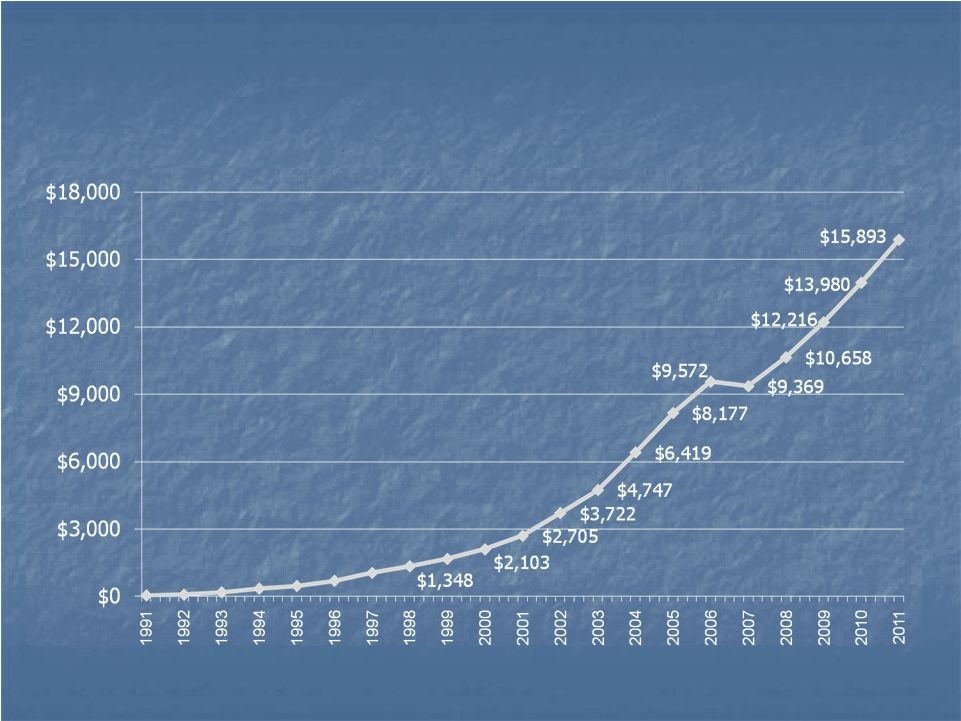

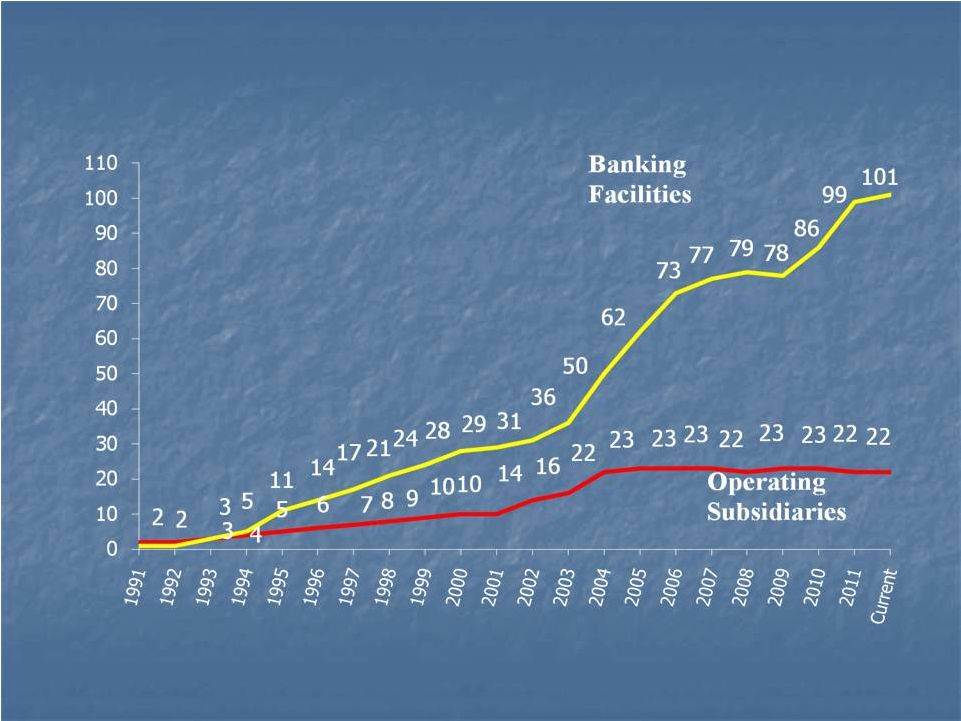

5 5 Who We Are Who We Are Nearly twenty year-old community focused banking organization Nearly twenty year-old community focused banking organization with approximately $16 billion in assets with approximately $16 billion in assets Fifteen community banks with strong ties to local residents and Fifteen community banks with strong ties to local residents and business leaders in the Chicago and Milwaukee metropolitan markets business leaders in the Chicago and Milwaukee metropolitan markets 9 de novo charters established since 1991 9 de novo charters established since 1991 15 15 bank bank acquisitions acquisitions since since the the 4 4 th qtr qtr 2003, 2003, including including 7 7 FDIC-assisted FDIC-assisted acquisitions in 2010-2012 (some were merged into existing charters) acquisitions in 2010-2012 (some were merged into existing charters) A small branch acquisition completed in October 2010 in Naperville, A small branch acquisition completed in October 2010 in Naperville, IL. Total deposits acquired were approximately $23 million IL. Total deposits acquired were approximately $23 million 101 existing banking locations 101 existing banking locations In our early years and by design, the vast majority of customers In our early years and by design, the vast majority of customers didn’t even know Wintrust existed -- didn’t even know Wintrust existed -- as you will see later, this is as you will see later, this is changing changing |

6 6 Who We Are - Who We Are - Company Overview Company Overview Community Banking Specialty Finance Wealth Management Fifteen community banks Chicago and Milwaukee metropolitan markets 101 locations Full product suite – home equity, home mortgage, consumer, real estate and commercial loans, safe deposit facilities, ATMs, & internet banking Wintrust Mortgage National mortgage production capabilities with focus on Chicago metropolitan area Two finance companies – premium finance and account receivables Loan production to optimize banks’ balance sheets First Insurance Funding P&C Life Insurance Tricom- Temporary help industry processing and financing Other niches (including housing associations, franchise lending, mortgage warehouse lending, indirect auto lending – to name a few) Wayne Hummer acquired in 2002, and 4 subsequent acquisitions $13+ bn in AUM Brokerage, asset management and trust capabilities Commercial Banking HAVE HAVE IT IT ALL ALL – Big Big Bank Resources, Bank Resources, Community Bank Community Bank Service Service Chicago and Chicago and Milwaukee Milwaukee downtown lending downtown lending offices offices All community All community banks banks Full Full product product suite suite – commercial loans, commercial loans, treasury treasury management, lock management, lock box services, box services, international international Focus Focus on on middle- market C&I C&I Added over 50 new Added over 50 new lenders since the lenders since the beginning of 2009. beginning of 2009. |

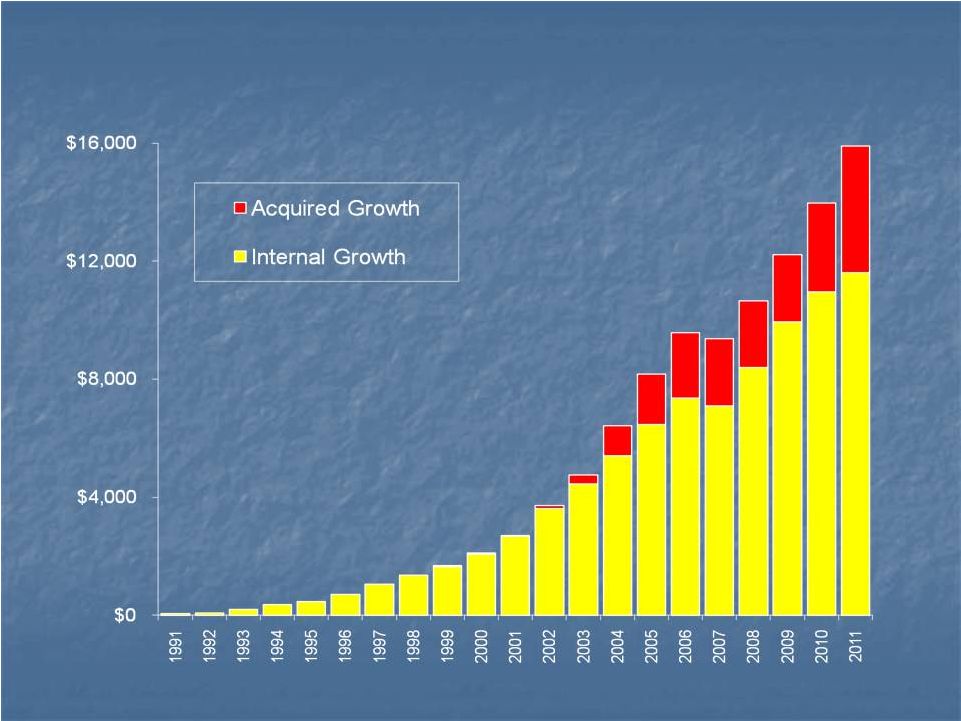

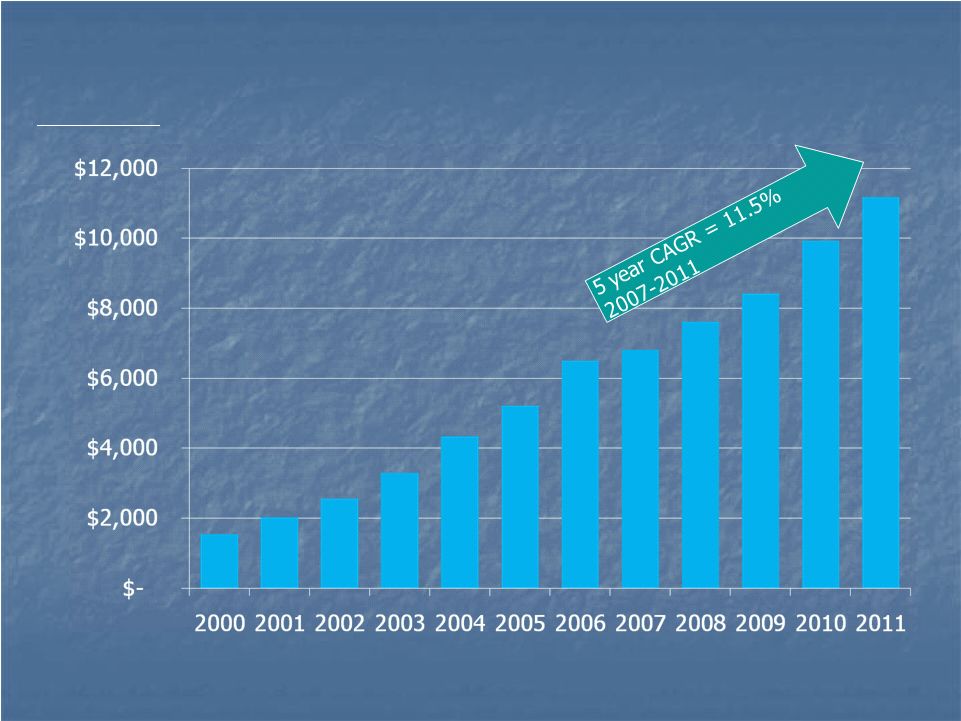

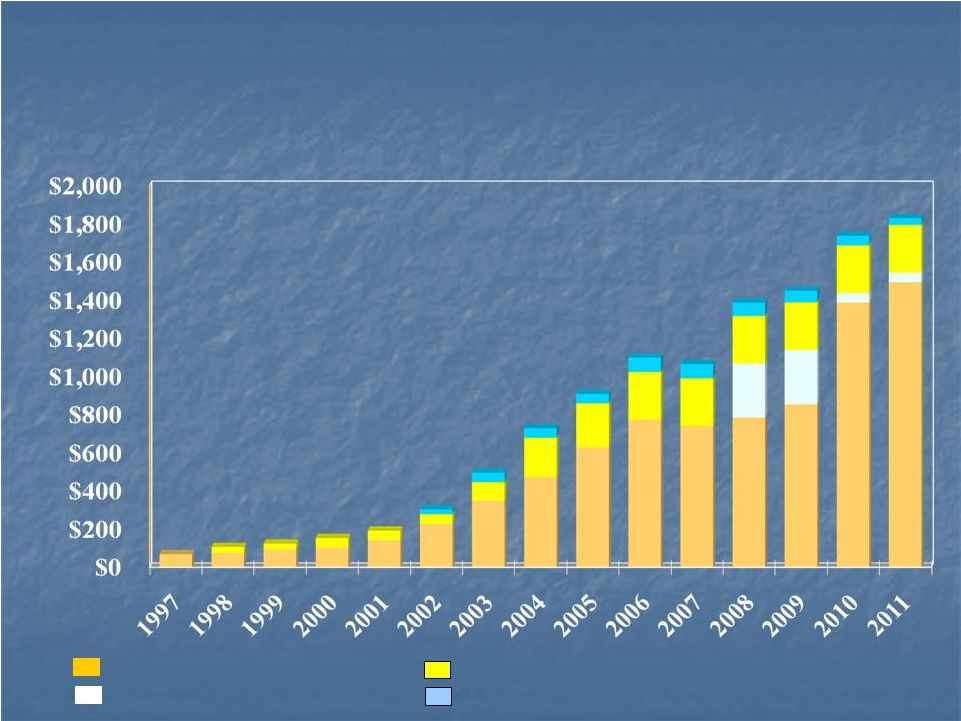

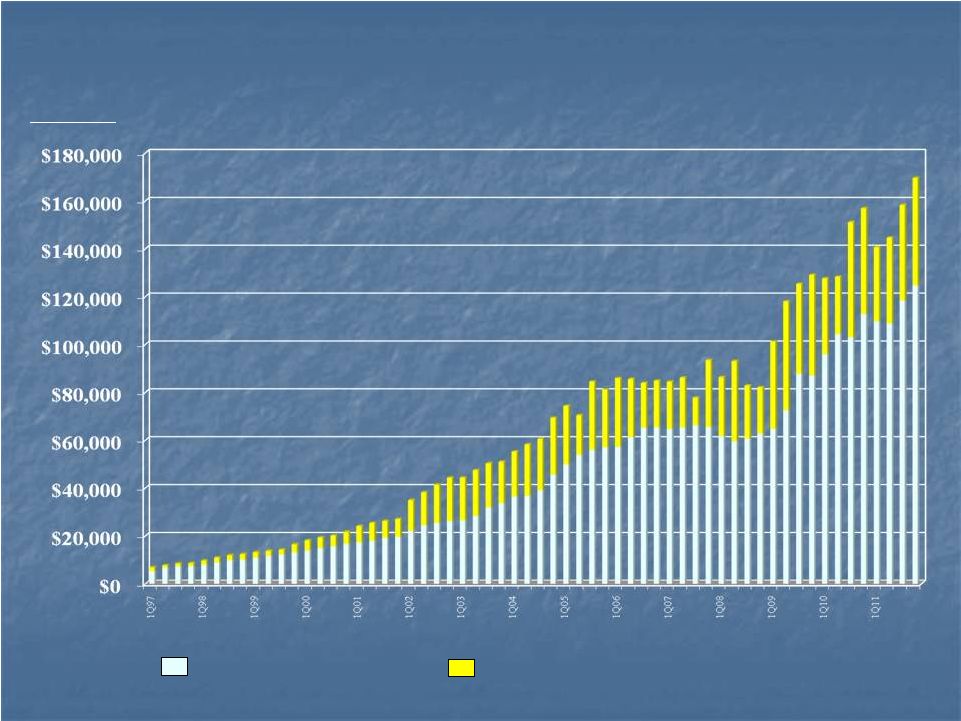

7 7 Asset Growth – Asset Growth – Internal / Acquired Internal / Acquired (in millions) (in millions) |

8 8 Banking Locations Banking Locations |

9 A Leading Chicago Bank Beginning of 2010 At December 31, 2011 Wintrust Banks: Recent Growth in Locations Wintrust Banks: Recent Growth in Locations |

10 10 Chicago and Milwaukee metropolitan markets Chicago and Milwaukee metropolitan markets Initially focused on high net worth areas. Have Initially focused on high net worth areas. Have since moved into broader market since moved into broader market Flexibility to continue to profitably penetrate Flexibility to continue to profitably penetrate broader market broader market Downtown Chicago focusing on corporate and Downtown Chicago focusing on corporate and commercial customers commercial customers Positioned as local alternatives to the “Big Banks” Positioned as local alternatives to the “Big Banks” We know our communities extremely well We know our communities extremely well Personalized service, creative marketing and Personalized service, creative marketing and employee involvement employee involvement Have taken advantage of big-bank consolidation Have taken advantage of big-bank consolidation and market dislocation to grow quickly and market dislocation to grow quickly Vigorously defend and grow market share Vigorously defend and grow market share Who We Are - Who We Are - Core Strategy Core Strategy Good Markets Consistent strategy for twenty years Community Focused Market Share Growth |

11 11 Funding Funding Assets Assets Who We Are - Who We Are - Operating Strategy Operating Strategy Loan-to-deposit ratio 85% - 90% Generate ~ two-thirds of loan volume from banks Remaining loan volume from niche businesses First Insurance Funding Tricom Other (including housing associations, franchise lending, mortgage warehouse lending, indirect auto -- to name a few) Consistent, conservative credit standards Manage risk through portfolio diversification and decentralized structure Minimal "nuisance fees", if at all Same or better products and delivery - differentiate with service Technology as the great equalizer Strong, diversified funding base Recent markets have proven the value of that approach Franchise is built on deposit funding 87% of total funding Substantially all deposits are customer generated Approximately 4% traditional brokered deposits Goal is to be top two in both deposit market share and household penetration in each banks’ local market area |

12 12 Deposit Market Share-Chicago MSA Deposit Market Share-Chicago MSA As of June 30, 2011 and 2010 As of June 30, 2011 and 2010 At June 30, 2011 At June 30, 2011 At June 30, 2010 At June 30, 2010 In-market Deposit In-market Deposit 2011 2011 Deposit Deposit Market Market Deposit Deposit Market Market Rank Rank Bank Holding Company Bank Holding Company Dollars Dollars Share % Share % Dollars Dollars Share % Share % 1. 1. JP Morgan Chase & Co. ** JP Morgan Chase & Co. ** $ 57.9 BB $ 57.9 BB 19.8% 19.8% $49.2 BB $49.2 BB 17.2% 17.2% 2. 2. Bank of Montreal ** Bank of Montreal ** $ 33.3 BB $ 33.3 BB 11.4 % 11.4 % $26.7 BB $26.7 BB 9.4% 9.4% 3. 3. Bank of America ** Bank of America ** $ 25.1 BB $ 25.1 BB 8.6% 8.6% $32.0 BB $32.0 BB 11.2% 11.2% 4. 4. Northern Trust Corporation Northern Trust Corporation $ 18.9 BB $ 18.9 BB 6.4 % 6.4 % $12.7 BB $12.7 BB 4.4% 4.4% 5. 5. PNC Financial Services Group** PNC Financial Services Group** $ 11.9 BB 4.1 % $ 11.9 BB 4.1 % $13.0 BB $13.0 BB 4.6% 4.6% 6. 6. Wintrust Financial Corp. Wintrust Financial Corp. $10.7 BB $10.7 BB 3.7 % 3.7 % $10.2 BB $10.2 BB 3.6% 3.6% 7. 7. Citigroup Inc. ** Citigroup Inc. ** $ 9.4 BB $ 9.4 BB 3.2 % 3.2 % $ 9.9 BB $ 9.9 BB 3.5% 3.5% 8. 8. PrivateBancorp, Inc. PrivateBancorp, Inc. $ 8.7 BB $ 8.7 BB 3.0 % 3.0 % $ 9.0 BB $ 9.0 BB 3.2% 3.2% A Leading Chicago bank Source: FDIC Website – Summary of Deposits as of June 30, 2011 and 2010 Market share data is for the Chicago Metropolitan Statistical Area ** - Corporate Headquarters is out-of-state |

How We Got Here How We Got Here 13 13 |

14 14 Consistent Strategy – Consistent Strategy – Changing Tactics Changing Tactics (1991-2005) (2010-11) (2008) (2009) (2006-07) Organic & Organic & Acquisition Growth Acquisition Growth 7 traditional bank 7 traditional bank acquisitions since 2003 acquisitions since 2003 9 de novo charters since 9 de novo charters since 1991 1991 “Rope - A – Dope” Slowed growth Maintained extremely conservative underwriting Reduced relative cost of funds Controlled expenses “Off the Ropes” Life insurance premium finance acquisition PMP acquisition (in late Dec ’08) Over 50 new lenders hired since Jan ‘09 Loans $800 mm in 2009 Deposits $1.5 bn in 2009 Organic & Acquisition Growth Take advantage of “dislocation” Consistent loan growth – approx. $1.8 billion since 2009 (excl. covered loans) 6 FDIC-assisted transactions Acquired 1 branch in Naperville, Acquired asset management firm with approx. $2.4 bn in AUM Acquired Elgin State Bank (unassisted) Raised capital-RETIRED TARP WINTRUST TACTICS CREDIT CYCLE Capital & TARP-CPP Focused on minimizing dilution to shareholders Q3’08 – raised $50 mm of convertible preferred Dec. ’08 - $250 mm TARP-CPP Healthy Restrained Recovery The Perfect Storm Stabilization Storm Clouds Gather Warning signs 1Q’06 Disadvantageous yield curve Loosened credit standards Credit spreads moved to unacceptable levels Compound Annual Growth Rates 1991-2005 2006-2007 2007-2008 2008-2009 2009-2010 2010-2011 Asset Growth 43.4% -2.1% 13.8% 14.6% 14.4% 13.7% |

15 15 Compound Annual Growth Rates Compound Annual Growth Rates Through 2005 Through 2005 (Years ended December 31, 2005) (Years ended December 31, 2005) 1 year 1 year 2 year 2 year 3 year 4 year 5 year 3 year 4 year 5 year • • Revenues Revenues 27.6% 27.6% 26.8 25.0% 31.8% 31.4% 26.8 25.0% 31.8% 31.4% • • Net Income Net Income 30.5 30.5 32.6 32.6 34.0 34.0 38.1 43.1 38.1 43.1 • • EPS (diluted) EPS (diluted) 17.5 17.5 17.9 17.9 19.8 19.8 21.3 27.1 21.3 27.1 • • Assets Assets 27.4 27.4 31.2 31.2 30.0 30.0 31.9 31.2 31.9 31.2 • • Loans Loans 19.9 19.9 25.7 25.7 26.8 26.8 26.8 27.5 26.8 27.5 • • Deposits Deposits 31.8 31.8 31.8 31.8 29.6 29.6 30.6 29.8 30.6 29.8 |

16 16 So How Did Wintrust Fare?? So How Did Wintrust Fare?? Remained profitable throughout the cycle. Remained profitable throughout the cycle. We have taken advantage of the many opportunities We have taken advantage of the many opportunities which are always present in adverse credit cycles which are always present in adverse credit cycles Dislocated people Dislocated people Dislocated assets Dislocated assets Dislocated banks Dislocated banks Key Financial Goals Key Financial Goals Increase pre-tax pre-provision adjusted earnings Increase pre-tax pre-provision adjusted earnings Move bad assets out Move bad assets out |

17 17 Taking Advantage of Dislocations Taking Advantage of Dislocations Dislocated People Dislocated People Dislocated Assets Dislocated Assets Dislocated Banks Dislocated Banks FIFC purchased a portfolio of domestic life insurance premium finance loans and certain related assets from indirect wholly-owned subsidiaries of AIG Aggregate balance of approximately $1.03 billion Purchase price of $746 million Resulting discount of $287 million Pre-tax bargain purchase price gain of $167 million First purchase: July 28, 2009 Smaller, second purchase: October 2, 2009 Set up downtown Chicago office to capture core commercial and industrial (C&I) business Added 50+ lenders since the beginning of 2009 added throughout the organization Adding talented staff in other areas to support our growth and to stay out in front on product delivery systems and regulatory changes. Since April 2010, acquired seven failed banks from the FDIC - they cover the majority of losses Very disciplined bids- $71 million in Bargain Purchase Gains (BPG) recorded in 2010/2011 Accretive to earnings Strategic as we moved into contiguous markets not served by us We intend to assimilate and then aggressively grow these acquisitions to be market leaders Acquired a branch with $23 million in deposits in Naperville, IL in 2010 Acquired a non-assisted bank with 3 branches in 3Q11 Acquired 3 bank facilities from the FDIC |

FDIC-Assisted Transactions FDIC-Assisted Transactions 18 18 Bank Date of Acquisition Number Of Branches Fair Value of Asset Acquired (in 000s) Fair Value of Loans Acquired (in 000s) Fair Value of Liabilities Acquired (in 000s) Bargain Purchase Gain Lincoln Park 4/23/2010 4 157,078 103,420 192,018 $4.2MM Wheatland 4/23/2010 1 343,870 175,277 415,560 $22.3 MM Ravenswood 8/6/2010 2 173,919 97,956 122,943 $6.8 MM Community First Bank 2/4/2011 1 50,891 27,332 49,779 $2.0 MM The Bank of Commerce 3/25/11 1 173,986 77,887 168,472 $8.6 MM First Chicago Bank 7/8/11 7 768,873 330,203 741,508 $27.4 MM Total through 2011 16 1,668,617 812,075 1,690,280 $71.3 MM Additionally, acquired Charter National Bank & Trust on February 10, 2012 in an FDIC-assisted transaction with two branches and approximately $90 million in assets and deposits. |

19 19 Consolidated Net Income Consolidated Net Income (before Preferred Dividends, in 000s) (before Preferred Dividends, in 000s) |

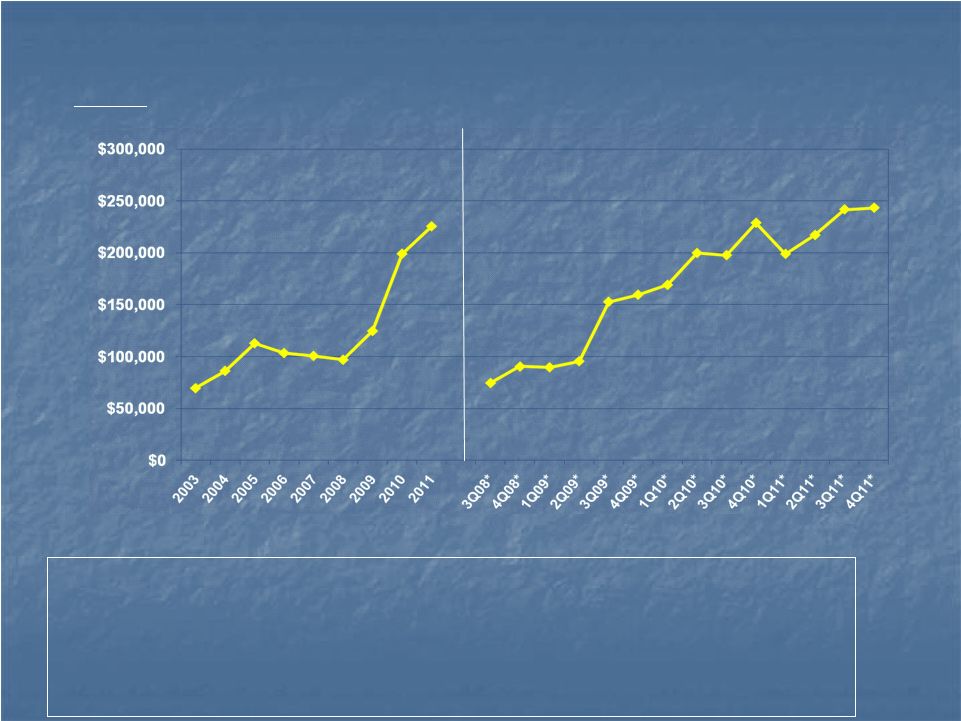

20 20 Annual “Pre-tax Adjusted Earnings” Annual “Pre-tax Adjusted Earnings” (in 000s) (* - Annualized) “Pre-tax Adjusted Earnings” are calculated by removing from reported Pre-tax earnings the following categories: Provision for Credit Losses; OREO Related Costs; Mortgage Recourse Obligations on Loans Previously Sold; Covered Loan Expense; Mortgage Servicing Rights Fair Value adjustments; Bargain Purchase Gains; Gains or Losses on from Investments in Limited Partnerships; Trading Gains or Losses; and Securities Gains or Losses. Further information regarding the calculation methodology is available in our news release filed on Form 8-K dated January 18, 2012 under the section titled “Supplemental Financial Measures/Ratios”. |

LOAN GROWTH LOAN GROWTH (excluding Loans Held for Sale) (excluding Loans Held for Sale) 21 21 (in millions) Loan pipelines remain good |

22 22 Non-Performing Asset Ratio Non-Performing Asset Ratio Wintrust vs. Peer Group Wintrust vs. Peer Group Peer Group Data is per the Federal Reserve’s Bank Holding Company Performance Report |

23 23 Net Charge-offs Ratio Net Charge-offs Ratio Wintrust vs. Peer Group Wintrust vs. Peer Group Peer Group Data is per the Federal Reserve’s Bank Holding Company Performance Report |

24 24 Capital Summary Capital Summary Enhance and maintain strong capital ratios 12/31/09 12/31/10 12/30/11 Tier 1 Risk-based capital 11.0% 12.5% 11.8% Total capital ratio 12.4% 13.8% 13.0% Leverage ratio 9.3% 10.1% 9.4% Tangible common equity ratio 4.7% 8.0% 7.5% Provide flexibility for growth Organic growth & lending opportunities Portfolio and business acquisitions 2010 Capital Activity March 2010 – Sale of Common Stock (+$210 mm) December 2010- Sale of Common Stock and TEUs (+$327 mm) Repaid TARP-CPP in December 2010 (-$250 mm) |

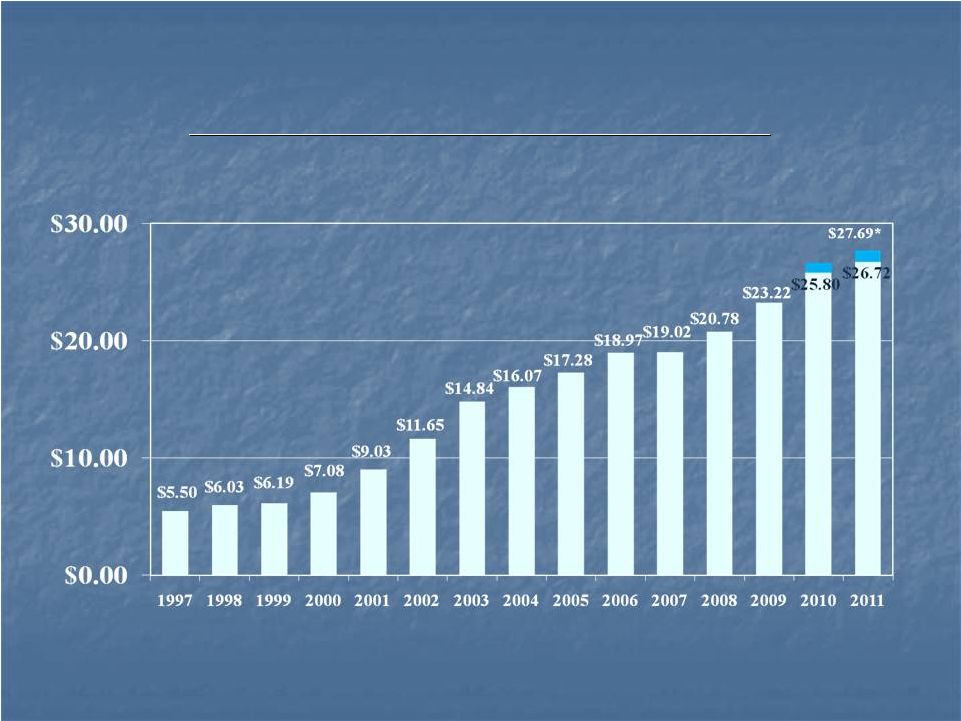

Financial Overview – Financial Overview – Wintrust Has Consistently Grown Wintrust Has Consistently Grown Tangible Book Value Per Share Through Cycles Tangible Book Value Per Share Through Cycles Tangible Common Book Value Per Share Tangible Common Book Value Per Share $26.66* * Proforma assuming tangible equity units convert at a maximum price of $37.50 |

26 26 Financial Overview – Financial Overview – Capital Components Capital Components (in millions) (in millions) - Common Shareholders Equity - Trust Preferred Securities - Subordinated Debt - Preferred Securities |

Wintrust Strategy for 2012 Wintrust Strategy for 2012 and Beyond and Beyond Back to the Future Back to the Future 27 27 |

28 28 Back to the Future Back to the Future Strategy for 2012 and Beyond Strategy for 2012 and Beyond This cycle isn’t over yet so we need to proceed cautiously in This cycle isn’t over yet so we need to proceed cautiously in all of our endeavors all of our endeavors Continue to increase core earnings Continue to increase core earnings Continue to expeditiously remove problem assets from the Continue to expeditiously remove problem assets from the balance sheet balance sheet Plan is to return to the growth mode experienced in the first Plan is to return to the growth mode experienced in the first 15 years of our existence with an overriding emphasis on 15 years of our existence with an overriding emphasis on achieving superior profitability achieving superior profitability Organic growth Organic growth New hires New hires Chicago office Chicago office Selective, opportunistic acquisitions in all areas of our business Selective, opportunistic acquisitions in all areas of our business Continue to locate “dislocations” Continue to locate “dislocations” in the market and take advantage in the market and take advantage of them of them Never take our eye off the major operating tenet that made Never take our eye off the major operating tenet that made us successful throughout the years-Service, Service, Service us successful throughout the years-Service, Service, Service |

Expected Pre-tax Adjusted Earnings Expected Pre-tax Adjusted Earnings Improvements Improvements “Pre-tax adjusted earnings” “Pre-tax adjusted earnings” annualized run rate annualized run rate $229 million run rate in the 4 $229 million run rate in the 4 th Quarter of 2010 Quarter of 2010 $243 million run rate in the 4 $243 million run rate in the 4 th Quarter of 2011 Quarter of 2011 Subject to market and other conditions, including interest Subject to market and other conditions, including interest Continued deposit re-pricing Continued deposit re-pricing Organic growth Organic growth Income from additional acquisitions Income from additional acquisitions 29 29 rate environments, liquidity positions and other factors rate environments, liquidity positions and other factors influencing growth, pre-tax, pre-provision adjusted influencing growth, pre-tax, pre-provision adjusted earnings could benefit from the following: earnings could benefit from the following: |

Organic Growth and Branding Organic Growth and Branding Organic Growth-going back to pre Rope-A-Dope model Organic Growth-going back to pre Rope-A-Dope model Expect each bank to grow $75 million per year Expect each bank to grow $75 million per year Expect each bank to open a branch every two years Expect each bank to open a branch every two years The Wintrust Brand The Wintrust Brand By design becoming more prevalent and recognized over the last two By design becoming more prevalent and recognized over the last two years years Wintrust Wintrust Wealth Wealth Management, Management, Wintrust Wintrust Mortgage Mortgage Co., Co., Wintrust Wintrust Commercial Commercial Banking Banking Recently began to offer full affiliate banking to all of our customers Recently began to offer full affiliate banking to all of our customers Each of our banks will take on the sub-brand of “A Wintrust Each of our banks will take on the sub-brand of “A Wintrust Community Bank” Community Bank” in order to take advantage of our network in order to take advantage of our network Will Will not not lose lose positioning positioning of of the the local local alternative alternative to to the the big big banks banks Rather, Rather, we we are are a a consortium consortium of of community community banks banks that that give give customers customers the the best best of of all worlds-community banks service with big bank products “Have it All” 30 30 |

31 31 Penetrate new markets with community banking model Penetrate new markets with community banking model Within 1½ Within 1½ hours of Wintrust headquarters hours of Wintrust headquarters Acquired entities with existing management that wish to continue Acquired entities with existing management that wish to continue to grow to grow Acquisitions in specialty finance and wealth management Acquisitions in specialty finance and wealth management Must complement existing franchise, be a strategic new business Must complement existing franchise, be a strategic new business line, or add/improve customer products and services line, or add/improve customer products and services Acquired Great Lakes Advisors in July 2011 Acquired Great Lakes Advisors in July 2011 Canadian premium finance business acquisition announce in Canadian premium finance business acquisition announce in February February 2012. 2012. Closing Closing expected expected by by early early 2 2 Quarter Quarter of of 2012 2012 Evaluating FDIC-assisted and unassisted bank deals Evaluating FDIC-assisted and unassisted bank deals Completed seven FDIC-assisted transactions since April 2010 Completed seven FDIC-assisted transactions since April 2010 Acquired a separate branch location in Naperville, IL in October Acquired a separate branch location in Naperville, IL in October 2010 through an unassisted transaction 2010 through an unassisted transaction Acquired a bank in Elgin, IL in Sept. 2011 (not FDIC-assisted) Acquired a bank in Elgin, IL in Sept. 2011 (not FDIC-assisted) Branch and trust operation acquisition is pending Branch and trust operation acquisition is pending Focus Focus on on earnings earnings accretion accretion and and improving improving franchise franchise value value Growth Strategy - Growth Strategy - Expansion Expansion nd |

Growth Strategy – Growth Strategy – Market Conditions Market Conditions Our opinion is that about half of the customers in the Our opinion is that about half of the customers in the market prefer a local community oriented bank while the market prefer a local community oriented bank while the other half prefer a large banking organization. other half prefer a large banking organization. We believe our structure (multiple charters with locally We believe our structure (multiple charters with locally engaged management and the resources of a larger engaged management and the resources of a larger institution) will allow us to take advantage of the existing institution) will allow us to take advantage of the existing market conditions. Specifically, we believe: market conditions. Specifically, we believe: Banks Banks under under $1 $1 billion billion in in assets assets will will find find it it hard hard to to operate operate and and grow due to: grow due to: Increased regulatory burden Increased regulatory burden Difficulty in competing for high quality assets Difficulty in competing for high quality assets Difficulty in accessing capital for growth Difficulty in accessing capital for growth We are a logical partner for these banks and a logical We are a logical partner for these banks and a logical bank bank for for their their customers customers to to HAVE HAVE IT IT ALL™ ALL™ with with Wintrust Wintrust 32 32 |

Why Invest in Wintrust? Why Invest in Wintrust? Managing well through the cycle-consistently profitable Managing well through the cycle-consistently profitable with strong core earnings growth with strong core earnings growth Asset quality position is manageable and better than Asset quality position is manageable and better than peer group and should allow us to be first out of this peer group and should allow us to be first out of this cycle cycle Strong capital position-NO TARP overhang Strong capital position-NO TARP overhang Enviable core deposit franchise in market area Enviable core deposit franchise in market area Differentiated, highly diversified and sustainable Differentiated, highly diversified and sustainable business model business model Well positioned to take advantage of industry Well positioned to take advantage of industry consolidation consolidation We believe our stock is underpriced relative to current We believe our stock is underpriced relative to current market metrics and relative positioning among local market metrics and relative positioning among local peers peers 33 33 |

34 34 |

Supplemental Financial Supplemental Financial Data Data |

36 36 Total Assets Total Assets (in millions) |

37 37 Historical Growth Historical Growth |

38 38 Asset Growth of Banks by Year Asset Growth of Banks by Year (in millions) |

39 39 Net Interest Margin Net Interest Margin (fully taxable equivalent) (fully taxable equivalent) |

40 40 - Net interest income - Non-interest income (in 000s) Revenue Growth by Quarter Revenue Growth by Quarter (excluding Bargain Purchase Gains recorded in 3Q09 through 4Q11) (excluding Bargain Purchase Gains recorded in 3Q09 through 4Q11) |

41 41 EPS Growth EPS Growth Annual Quarterly 4 th Quarter and full year 2010 amounts exclude $(0.33) and $(0.36) per diluted common share as a result of the deemed preferred stock dividend resulting from the repurchase of the TARP-CPP preferred stock. |

42 42 Net Overhead Ratio & Efficiency Ratio Net Overhead Ratio & Efficiency Ratio |

43 43 Diversified Loan Portfolio Diversified Loan Portfolio Composition as of December 31, 2011 - Composition as of December 31, 2011 - $11.2 Billion $11.2 Billion (excludes loans held for sale) (excludes loans held for sale) Commercial and Industrial Premium Finance – Life Insurance Res. R/E Home Equity Other Other Commercial Niches Commercial Real Estate Premium Finance – Commercial Covered Loans |

44 44 Ending Loan-to-Deposit/Secured Ending Loan-to-Deposit/Secured Borrowing Ratio* Borrowing Ratio* (excludes loans held for sale) (excludes loans held for sale) *Includes $600 million of secured borrowing related to the commercial premium finance loan securitization for which the related loans are recorded on the balance sheet beginning in 2010. |

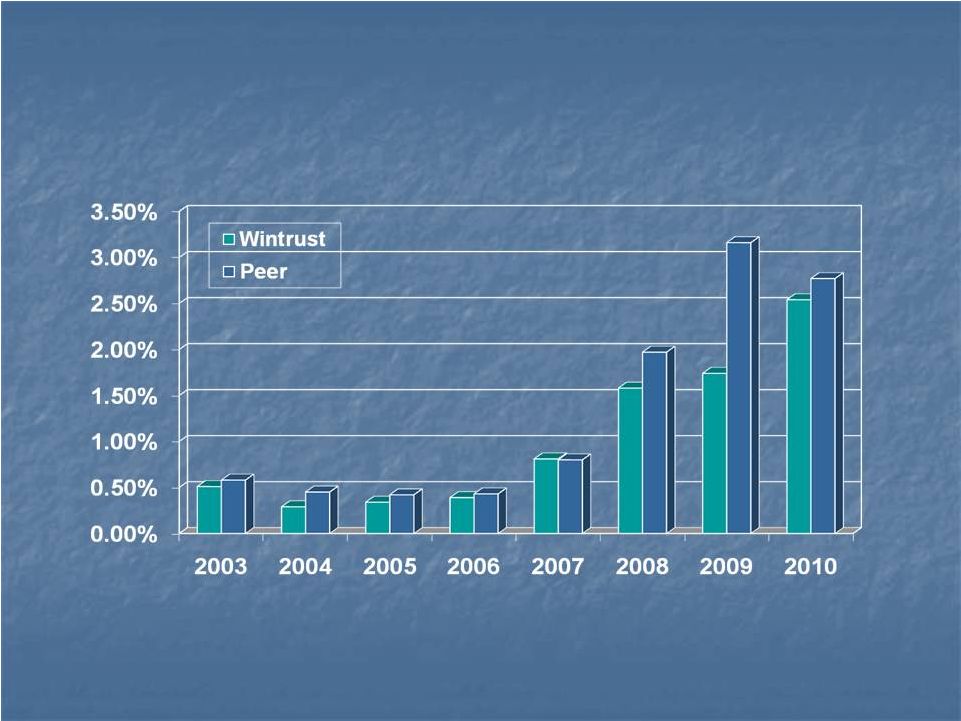

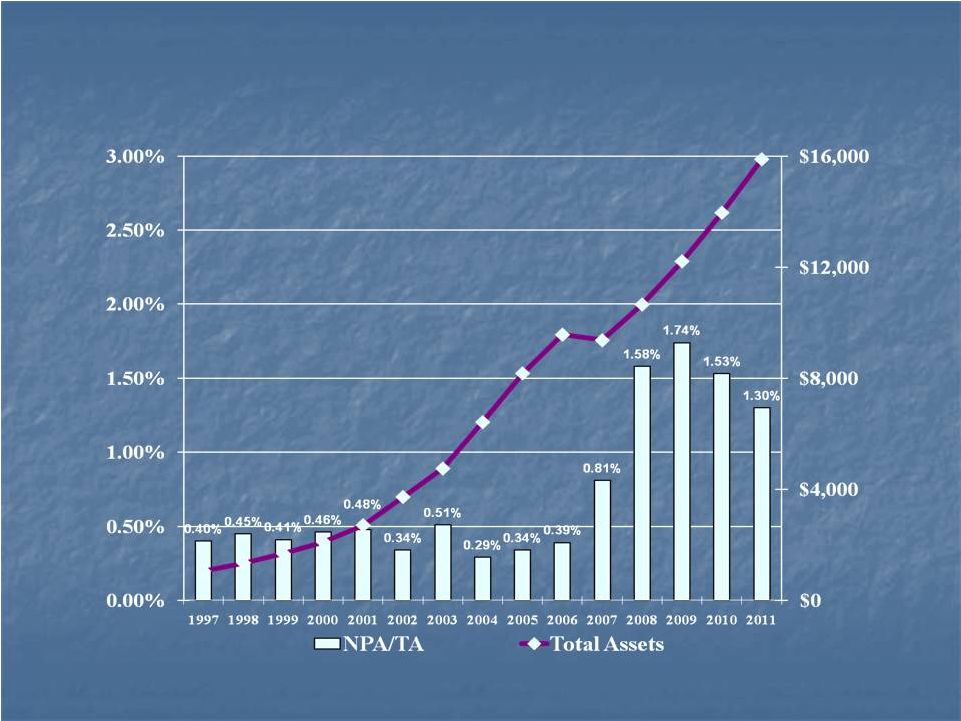

45 45 Non-Performing Assets to Total Assets Non-Performing Assets to Total Assets (NPAs include NPLs and OREO and exclude covered loans) (NPAs include NPLs and OREO and exclude covered loans) Assets in millions Peer Group-2003 = 0.58% Peer Group-2004 = 0.45% Peer Group-2005 = 0.42% Peer Group-2006 = 0.43% Peer Group-2007 = 0.80% Peer Group-2008 = 1.97% Peer Group-2009 = 3.16% Peer Group-2010 = 2.77% Peer Group Data is per the Federal Reserve’s Bank Holding Company Performance Report |

46 46 Net Charge-offs to Total Average Loans Net Charge-offs to Total Average Loans Loans In millions Peer Group-2003 = 0.33% Peer Group-2004 = 0.21% Peer Group-2005 = 0.18% Peer Group-2006 = 0.15% Peer Group-2007 = 0.27% Peer Group-2008 = 1.10% 0.31% Peer Group Data is per the Federal Reserve’s Bank Holding Company Performance Report Peer Group-2010 = 2.04% Peer Group-2009 = 2.33% |

FORWARD-LOOKING STATEMENTS FORWARD-LOOKING STATEMENTS This document contains forward-looking statements within the meaning of federal securities laws. Forward-looking information can be identified through the use of words such as “intend,” “plan,” “project,” “expect,” “anticipate,” “believe,” “estimate,” “contemplate,” “possible,” “point,” “will,” “may,” “should,” “would” and “could.” Forward-looking statements and information are not historical facts, are premised on many factors and assumptions, and represent only management’s expectations, estimates and projections regarding future events. Similarly, these statements are not guarantees of future performance and involve certain risks and uncertainties that are difficult to predict, which may include, but are not limited to, those listed below and the Risk Factors discussed under Item 1A of the Company’s 2010 Annual Report on Form 10-K and in any of the Company’s subsequent SEC filings. The Company intends such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995, and is including this statement for purposes of invoking these safe harbor provisions. Such forward-looking statements may be deemed to include, among other things, statements relating to the Company’s future financial performance, the performance of its loan portfolio, the expected amount of future credit reserves and charge-offs, delinquency trends, growth plans, regulatory developments, securities that the Company may offer from time to time, and management’s long-term performance goals, as well as statements relating to the anticipated effects on financial condition and results of operations from expected developments or events, the Company’s business and growth strategies, including future acquisitions of banks, specialty finance or wealth management businesses, internal growth and plans to form additional de novo banks or branch offices. Actual results could differ materially from those addressed in the forward-looking statements as a result of numerous factors, including the following: 47 47 |

48 48 FORWARD-LOOKING STATEMENTS (cont.) FORWARD-LOOKING STATEMENTS (cont.) • negative economic conditions that adversely affect the economy, housing prices, the job market and other factors that may affect the Company’s liquidity and the performance of its loan portfolios, particularly in the markets in which it operates; • the extent of defaults and losses on the Company’s loan portfolio, which may require further increases in its allowance for credit losses; • effects of the potential delay or failure of the U.S. federal government to pay its debts as they become due or make payments in the ordinary course; • estimates of fair value of certain of the Company’s assets and liabilities, which could change in value significantly from period to period; • changes in the level and volatility of interest rates, the capital markets and other market indices that may affect, among other things, the Company’s liquidity and the value of its assets and liabilities; • a decrease in the Company’s regulatory capital ratios, including as a result of further declines in the value of its loan portfolios, or otherwise; • legislative or regulatory changes, particularly changes in regulation of financial services companies and/or the products and services offered by financial services companies, including those resulting from the Dodd-Frank Act; • restrictions upon our ability to market our products to consumers and limitations on our ability to profitably operate our mortgage business resulting from the Dodd-Frank Act; • increased costs of compliance, heightened regulatory capital requirements and other risks associated with changes in regulation and the current regulatory environment, including the Dodd-Frank Act; • changes in capital requirements resulting from Basel II and III initiatives; • increases in the Company’s FDIC insurance premiums, or the collection of special assessments by the FDIC; • losses incurred in connection with repurchases and indemnification payments related to mortgages; |

49 49 FORWARD-LOOKING STATEMENTS (cont.) FORWARD-LOOKING STATEMENTS (cont.) • competitive pressures in the financial services business which may affect the pricing of the Company’s loan and deposit products as well as its services (including wealth management services); • delinquencies or fraud with respect to the Company’s premium finance business; • failure to identify and complete favorable acquisitions in the future or unexpected difficulties or developments related to the integration of recent or future acquisitions; • unexpected difficulties and losses related to FDIC-assisted acquisitions, including those resulting from our loss-sharing arrangements with the FDIC; • credit downgrades among commercial and life insurance providers that could negatively affect the value of collateral securing the Company’s premium finance loans; • any negative perception of the Company’s reputation or financial strength; • the loss of customers as a result of technological changes allowing consumers to complete their financial transactions without the use of a bank; • the ability of the Company to attract and retain senior management experienced in the banking and financial services industries; • the Company’s ability to comply with covenants under its securitization facility and credit facility; • unexpected difficulties or unanticipated developments related to the Company’s strategy of de novo bank formations and openings, which typically require over 13 months of operations before becoming profitable due to the impact of organizational and overhead expenses, the startup phase of generating deposits and the time lag typically involved in redeploying deposits into attractively priced loans and other higher yielding earning assets; • changes in accounting standards, rules and interpretations and the impact on the Company’s financial statements; • adverse effects on our operational systems resulting from failures, human error or tampering; • significant litigation involving the Company; and • the ability of the Company to receive dividends from its subsidiaries. |

50 50 FORWARD-LOOKING STATEMENTS (cont.) FORWARD-LOOKING STATEMENTS (cont.) Therefore, there can be no assurances that future actual results will correspond to these forward-looking statements. The reader is cautioned not to place undue reliance on any forward-looking statement made by or on behalf of Wintrust. Any such statement speaks only as of the date the statement was made or as of such date that may be referenced within the statement. The Company undertakes no obligation to release revisions to these forward-looking statements or reflect events or circumstances after the date of this press release. Persons are advised, however, to consult further disclosures management makes on related subjects in its reports filed with the Securities and Exchange Commission and in its press releases. |

51 51 Questions Questions |