UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07655

Driehaus Mutual Funds

(Exact name of registrant as specified in charter)

25 East Erie Street

Chicago, IL 60611

(Address of principal executive offices) (Zip code)

Janet L. McWilliams

Driehaus Capital Management LLC

25 East Erie Street

Chicago, IL 60611

(Name and address of agent for service)

Registrant’s telephone number, including area code: 312-587-3800

Date of fiscal year end: December 31

Date of reporting period: December 31, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Reports to Shareholders are attached herewith.

Driehaus Mutual Funds

Trustees & Officers

Richard H. Driehaus

Trustee

A.R. Umans

Chairman of the Board

Theodore J. Beck

Trustee

Francis J. Harmon

Trustee

Dawn M. Vroegop

Trustee

Daniel F. Zemanek

Trustee

Robert H. Gordon

President

Michelle L. Cahoon

Vice President & Treasurer

Janet L. McWilliams

Assistant Vice President

Michael Shoemaker

Chief Compliance Officer &

Assistant Vice President

Diane J. Drake

Secretary

Michael P. Kailus

Assistant Secretary

William H. Wallace, III

Assistant Secretary

Investment Adviser

Driehaus Capital Management LLC

25 East Erie Street

Chicago, IL 60611

Distributor

Driehaus Securities LLC

25 East Erie Street

Chicago, IL 60611

Administrator

BNY Mellon Investment Servicing (US) Inc.

4400 Computer Drive

Westborough, MA 01581

Transfer Agent

BNY Mellon Investment Servicing (US) Inc.

4400 Computer Drive

Westborough, MA 01581

Custodian

The Northern Trust Company

50 South LaSalle Street

Chicago, IL 60603

Annual Report to Shareholders

December 31, 2012

Driehaus International Discovery Fund

Driehaus Emerging Markets Growth Fund

Driehaus Emerging Markets Small Cap Growth Fund

Driehaus International Small Cap Growth Fund

Driehaus Global Growth Fund

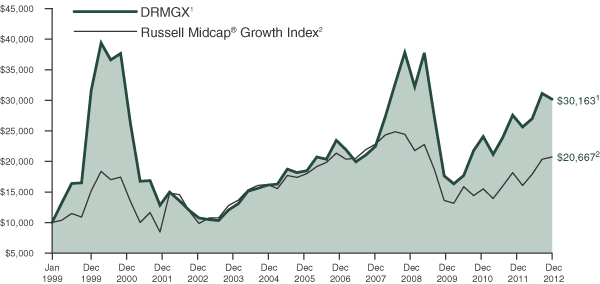

Driehaus Mid Cap Growth Fund

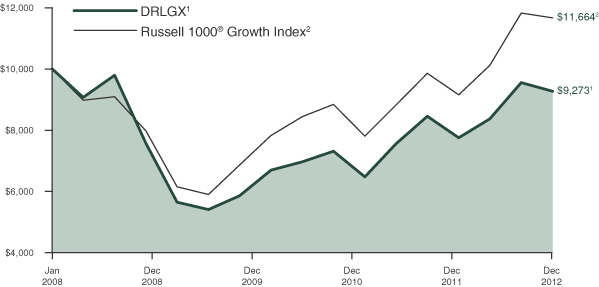

Driehaus Large Cap Growth Fund

Distributed by:

Driehaus Securities LLC

This report has been prepared for the shareholders of the Funds and is not an offering to sell or buy any Fund securities. Such offering is only made by the Funds' prospectus.

Investment Philosophy:

The Adviser seeks to achieve superior investment returns primarily by investing in global companies that are currently demonstrating rapid growth in their sales and earnings and which, in its judgement, have the ability to continue or accelerate their growth rates in the future. The Adviser manages the portfolios actively (above average turnover) to ensure that the Funds are fully invested, under appropriate market conditions, in companies that meet these criteria. Investors should note that investments in overseas markets can pose more risks than U.S. investments, and the international Funds’ share prices are expected to be more volatile than those of the U.S.-only Funds. In addition, the Funds’ returns will fluctuate with changes in stock market conditions, currency values, interest rates, government regulations, and economic and political conditions in countries in which the Funds invest. These risks are generally greater when investing in emerging markets.

Annual Report to Shareholders December 31, 2012

Driehaus International Discovery Fund

Driehaus Emerging Markets Growth Fund

Driehaus Emerging Markets Small Cap Growth Fund

Driehaus International Small Cap Growth Fund

Driehaus Global Growth Fund

Driehaus Mid Cap Growth Fund

Driehaus Large Cap Growth Fund

Portfolio Managers’ Letter, Performance Overview and Schedule of Investments: | ||||

| 1 | ||||

| 8 | ||||

| 15 | ||||

| 22 | ||||

| 28 | ||||

| 34 | ||||

| 39 | ||||

| 44 | ||||

| 46 | ||||

| 48 | ||||

| 51 | ||||

| 58 | ||||

| 70 | ||||

| 71 | ||||

| 73 | ||||

| 74 | ||||

| 76 | ||||

Board Considerations in Connection with the Annual Review of the Investment Advisory Agreement | 78 | |||

Driehaus International Discovery Fund — Portfolio Managers’ Letter

Dear Fellow Shareholders,

The Driehaus International Discovery Fund (“Fund”) returned 14.75% for the year ended December 31, 2012. This return was below the performance of the Morgan Stanley Capital International (“MSCI”) All Country World ex USA Growth Index (“Benchmark”) (which returned 17.07% for the year) and below the performance of the MSCI All Country World ex USA Index (which returned 17.39%), which is another index for the Fund.

Assisted by currency gains, the European indices saw strong gains for 2012, as did many equity markets in emerging Asia. From a sector perspective, financial stocks were favored while defensive sectors, such as utilities and consumer staples, were laggards after years of stronger relative performance. Energy also was a weak sector globally, as oil prices ended the year close to their starting point despite a volatile ride in between. As the year closed, an appreciating euro aided returns within the euro zone’s more defensive markets as well as its more speculative markets. Greek equities were the big winner thanks to further European largesse, posting strong returns for 2012. While countries with higher beta to the European crisis were rewarded, investors also continued to favor German stocks, helping it to also be one of the top developed markets for the year. Elsewhere, the Nikkei seemed to garner much attention due to the unusual nature of the yen’s descent.

Certain areas detracted from Fund performance during the year. Two sectors where stock selection negatively affected the performance of the Fund relative to the Benchmark were the health care and energy sectors. Additionally, holdings in China, Brazil and Australia detracted from Fund performance versus the Benchmark.

Stock selection within health care detracted from returns, including Korea-based holding Seegene, Inc. (Ticker: 096530 KS), which was a significant detractor for the year. Seegene specializes in molecular diagnostics and develops technology and products that diagnose disease from the genetic level. Seegene’s molecular diagnosis technology and products allow patients to benefit from cost effective and personalized diagnosis tools and allow doctors to offer accurate and effective treatment to patients. Seegene’s share price fell steeply mid-year due in part to a perceived delay in an expected global distribution deal.

Within China, Baidu, Inc. SP ADR (Ticker: BIDU) was a significant detractor from performance for 2012. Baidu is a Chinese-language Internet search provider. The company offers a Chinese-language search platform that enables users to find relevant information online, including Web pages, news, images, documents and multimedia files, through links provided on its websites. Baidu’s share price declined during the year due to the combination of lost market share to recently-launched competitor Qihoo 360 Technology (which continues to expand its vertical search engine platforms) and reduced advertising revenue due to macroeconomic uncertainty.

Over the course of 2012, key contributors to performance versus the Benchmark were the Fund’s holdings in the consumer discretionary and consumer staples sectors. In addition, stock selection in the United Kingdom, France and Canada positively contributed to the performance of the Fund.

Within the consumer discretionary sector, Sands China, Ltd. (Ticker: 1928 HK) was a significant contributor to performance for 2012. Sands China is a leading developer, owner and operator of multi-use integrated resorts in Macao, China. Sands China is a subsidiary of the Las Vegas Sands Corporation. Sands China’s stock stumbled during the second quarter but recovered during the summer and saw a strong second half of 2012. Sands China remains an earnings leader among gaming companies in Macao and continues to expand its market share.

Canadian-headquartered Catamaran Corp. (Ticker: CTRX) was the holding that contributed the most to the Fund’s return versus its Benchmark in 2012. Catamaran is a provider of pharmacy benefit management (PBM) services and health care information technology solutions to the health care benefit management industry. The company’s product offerings and solutions combine a range of applications and PBM services designed to assist its customers in reducing the cost and managing the complexity of their prescription drug programs. Catamaran merged with Catalyst Health Solutions during the year. The increased scale has left the company well positioned to expand its market share and it continues to acquire middle-market PBMs. Additionally, the company’s new business pipeline remains robust.

1

Looking ahead, each of the last few years has seen periods of extreme concern regarding the state of the world, and equivalently exuberant market responses when those concerns ultimately fade. These worries usually have been driven by risks in Europe, though increasingly those ‘risk-off’ events are occurring at the hands of U.S. policymakers. However, we believe that the ability of the global economy to withstand shocks, from the perspectives of economic strength and financial liquidity, is better than it has been in recent years. As such, we would not anticipate the global markets getting as near the cliff’s edge as they have in each of the past few years.

Recent improving global economic data is something we have been watching quite closely. We believe in the economic growth suggested by the data, but remain cautious. We remember this narrative from the past few years where expectations ramp up at the start of the year only to be revised downward as the year progresses. We continue to believe that we reside in a low-growth world and that investors must be nimble to manage the volatility that accompanies such environments.

Globally, we are seeing many new opportunities in non-U.S. markets that did not look possible at this time last year. Financial conditions in Europe have meaningfully eased and the emerging markets outlook has improved thanks to low inflation, lower cost of capital, and inflecting growth trajectories. We remain optimistic but expect periods of volatility as government actions help and hurt economies in the year ahead.

As always, we remain committed to uncovering attractive growth equity investment opportunities that we believe will adequately compensate our clients for the risk taken with their capital. Thank you for your continued confidence in our management capabilities and your interest in the Driehaus International Discovery Fund.

Sincerely,

|  | |

| Daniel M. Rea | Sebastien Pigeon | |

| Portfolio Manager | Assistant Portfolio Manager |

Performance is historical and does not represent future results.

Please see the following performance overview page for index descriptions.

2

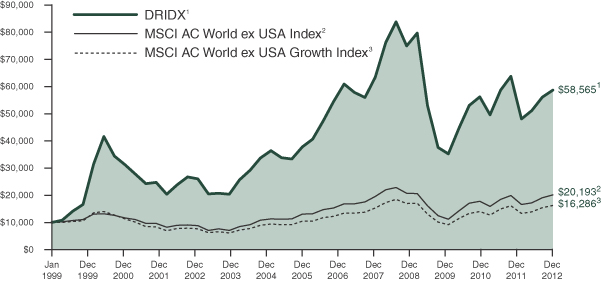

Driehaus International Discovery Fund

Performance Overview (unaudited)

The performance summarized below is historical and does not represent future results. Investment returns and principal value vary, and you may have a gain or loss when you sell shares. Performance data presented measures the change in the value of an investment in the Fund, assuming reinvestment of all dividends and capital gains. Average annual total return reflects annualized change.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The graph compares the results of a $10,000 investment in the Fund since December 31, 1998 (the date of the Fund’s inception), with all dividends and capital gains reinvested, with the indicated indices (and dividends reinvested) for the same period.

| Average Annual Total Returns as of 12/31/12 | 1 Year | 3 Years | 5 Years | 10 Years | Since Inception (12/31/98 - 12/31/12) | |||||||||||||||

Driehaus International Discovery Fund (DRIDX)1 | 14.75% | 1.43% | –6.89% | 10.93% | 13.46% | |||||||||||||||

MSCI AC World ex USA Index2 | 17.39% | 4.32% | –2.44% | 10.21% | 5.14% | |||||||||||||||

MSCI AC World ex USA Growth Index3 | 17.07% | 4.97% | –2.55% | 9.36% | 3.54% | |||||||||||||||

| 1 | The returns for the periods prior to July 1, 2003, reflect fee waivers and/or reimbursements without which performance would have been lower. |

| 2 | The Morgan Stanley Capital International All Country World ex USA Index (MSCI AC World ex USA Index) is a market capitalization-weighted index designed to measure equity market performance in 44 global developed and emerging markets, excluding the U.S. Data is in U.S. dollars. Source: Morgan Stanley Capital International Inc. |

| 3 | The Morgan Stanley Capital International All Country World ex USA Growth Index (MSCI AC World ex USA Growth Index) is a subset of the MSCI AC World ex USA Index and is composed only of the MSCI AC World ex USA Index stocks which are categorized as growth stocks. Data is in U.S. dollars. Source: Morgan Stanley Capital International Inc. |

3

Driehaus International Discovery Fund

Schedule of Investments

December 31, 2012

Number of Shares | Market Value (Note A) | |||||||

| EQUITY SECURITIES — 96.8% | ||||||||

| EUROPE — 51.2% | ||||||||

United Kingdom — 9.9% |

| |||||||

African Minerals, Ltd.** | 323,820 | $ | 1,718,201 | |||||

Antofagasta PLC | 100,450 | 2,201,368 | ||||||

ARM Holdings PLC | 94,892 | 1,198,373 | ||||||

ASOS PLC** | 56,590 | 2,496,096 | ||||||

Fenner PLC | 157,200 | 1,024,412 | ||||||

GlaxoSmithKline PLC | 75,120 | 1,635,544 | ||||||

Rio Tinto PLC — SP ADR | 28,130 | 1,634,072 | ||||||

Rolls-Royce Holdings PLC — C** | 5,770,680 | 9,374 | ||||||

Rotork PLC | 28,480 | 1,188,860 | ||||||

Telecity Group PLC | 295,574 | 3,817,188 | ||||||

The Weir Group PLC | 114,400 | 3,537,622 | ||||||

|

| |||||||

| 20,461,110 | ||||||||

|

| |||||||

France — 6.4% |

| |||||||

Ingenico SA | 49,240 | 2,801,244 | ||||||

Safran SA | 107,670 | 4,662,885 | ||||||

Societe BIC SA | 28,852 | 3,458,440 | ||||||

Technip SA | 20,235 | 2,339,906 | ||||||

|

| |||||||

| 13,262,475 | ||||||||

|

| |||||||

Denmark — 6.3% |

| |||||||

Christian Hansen Holding AS | 78,440 | 2,554,543 | ||||||

Coloplast AS — B | 26,640 | 1,306,430 | ||||||

Danske Bank AS** | 175,903 | 2,987,567 | ||||||

GN Store Nord AS | 177,189 | 2,575,086 | ||||||

Novo Nordisk AS — B | 21,502 | 3,501,314 | ||||||

|

| |||||||

| 12,924,940 | ||||||||

|

| |||||||

Switzerland — 5.3% |

| |||||||

Cie Financiere Richemont SA — A | 26,830 | 2,106,036 | ||||||

Dufry AG** | 12,703 | 1,679,743 | ||||||

Partners Group Holding AG | 9,857 | 2,278,737 | ||||||

Syngenta AG | 6,231 | 2,517,239 | ||||||

Temenos Group AG** | 74,979 | 1,311,610 | ||||||

Xstrata PLC | 59,790 | 1,043,688 | ||||||

|

| |||||||

| 10,937,053 | ||||||||

|

| |||||||

Netherlands — 4.6% |

| |||||||

ASML Holding NV | 18,980 | 1,217,263 | ||||||

Core Laboratories NV | 19,808 | 2,165,212 | ||||||

Koninklijke Vopak NV | 42,369 | 2,994,980 | ||||||

Sensata Technologies Holding NV** | 95,219 | 3,092,713 | ||||||

|

| |||||||

| 9,470,168 | ||||||||

|

| |||||||

Italy — 3.8% |

| |||||||

Lottomatica Group SpA | 49,280 | 1,125,987 | ||||||

Pirelli & C. SpA | 243,869 | 2,809,799 | ||||||

Saipem SpA | 45,184 | 1,760,062 | ||||||

Salvatore Ferragamo Italia SpA | 100,372 | 2,222,028 | ||||||

|

| |||||||

| 7,917,876 | ||||||||

|

| |||||||

Number of Shares | Market Value (Note A) | |||||||

Ireland — 3.8% |

| |||||||

Covidien PLC | 38,416 | $ | 2,218,140 | |||||

Elan Corp. PLC — SP ADR** | 136,186 | 1,390,459 | ||||||

Experian PLC | 133,620 | 2,153,555 | ||||||

Jazz Pharmaceuticals PLC** | 39,409 | 2,096,559 | ||||||

|

| |||||||

| 7,858,713 | ||||||||

|

| |||||||

Germany — 3.2% |

| |||||||

Aareal Bank AG** | 41,861 | 876,621 | ||||||

Adidas AG | 22,974 | 2,050,423 | ||||||

Bayerische Motoren Werke AG | 13,013 | 1,266,315 | ||||||

Infineon Technologies AG | 310,899 | 2,532,736 | ||||||

|

| |||||||

| 6,726,095 | ||||||||

|

| |||||||

Norway — 2.8% |

| |||||||

Gjensidige Forsikring ASA | 142,276 | 2,044,586 | ||||||

Seadrill, Ltd. | 27,580 | 1,016,100 | ||||||

Telenor ASA | 131,500 | 2,677,581 | ||||||

|

| |||||||

| 5,738,267 | ||||||||

|

| |||||||

Russia — 2.6% |

| |||||||

Magnit — SP GDR | 63,670 | 2,588,553 | ||||||

Sberbank RF — SP ADR | 219,187 | 2,747,967 | ||||||

|

| |||||||

| 5,336,520 | ||||||||

|

| |||||||

Portugal — 1.2% |

| |||||||

Jeronimo Martins SGPS SA | 126,981 | 2,455,369 | ||||||

|

| |||||||

Spain — 0.8% |

| |||||||

Viscofan SA | 29,624 | 1,677,985 | ||||||

|

| |||||||

Sweden — 0.5% |

| |||||||

Elekta AB — B | 66,210 | 1,032,376 | ||||||

|

| |||||||

Total EUROPE | 105,798,947 | |||||||

|

| |||||||

| FAR EAST — 24.6% | ||||||||

China — 8.2% |

| |||||||

AIA Group, Ltd. | 769,356 | 3,051,524 | ||||||

Baidu, Inc. — SP ADR** | 25,213 | 2,528,612 | ||||||

Golden Eagle Retail Group, Ltd. | 771,660 | 1,921,924 | ||||||

Michael Kors Holdings, Ltd.** | 41,370 | 2,111,111 | ||||||

New Oriental Education & Technology Group, Inc. — SP ADR | 66,980 | 1,301,421 | ||||||

Sands China, Ltd. | 777,562 | 3,476,219 | ||||||

Want Want China Holdings, Ltd. | 1,746,397 | 2,447,411 | ||||||

|

| |||||||

| 16,838,222 | ||||||||

|

| |||||||

Japan — 6.8% |

| |||||||

Astellas Pharma, Inc. | 59,096 | 2,657,050 | ||||||

FANUC Corp. | 12,507 | 2,326,922 | ||||||

M3, Inc. | 2,066 | 3,297,496 | ||||||

MonotaRO Co., Ltd. | 74,459 | 2,398,931 | ||||||

Shionogi & Co., Ltd. | 60,238 | 1,003,796 | ||||||

Notes to Financial Statements are an integral part of this Schedule.

4

Driehaus International Discovery Fund

Schedule of Investments

December 31, 2012

Number of Shares | Market Value (Note A) | |||||||

Ship Healthcare Holdings, Inc. | 11,504 | $ | 305,756 | |||||

Sugi Holdings Co., Ltd. | 56,444 | 1,991,310 | ||||||

|

| |||||||

| 13,981,261 | ||||||||

|

| |||||||

Australia — 4.1% |

| |||||||

Aurizon Holdings, Ltd. | 538,070 | 2,115,908 | ||||||

Aurora Oil & Gas, Ltd.** | 419,529 | 1,613,075 | ||||||

BHP Billiton, Ltd. — SP ADR | 46,108 | 3,616,711 | ||||||

Telstra Corp., Ltd. | 262,520 | 1,196,237 | ||||||

|

| |||||||

| 8,541,931 | ||||||||

|

| |||||||

South Korea — 2.1% |

| |||||||

Samsung Electronics Co., Ltd. | 2,977 | 4,277,353 | ||||||

|

| |||||||

Philippines — 1.0% |

| |||||||

SM Investments Corp. | 99,780 | 2,153,003 | ||||||

|

| |||||||

India — 0.9% |

| |||||||

Tata Motors, Ltd. — SP ADR | 67,690 | 1,944,057 | ||||||

|

| |||||||

Indonesia — 0.7% |

| |||||||

PT Bank Central Asia Tbk | 1,488,761 | 1,410,582 | ||||||

|

| |||||||

Thailand — 0.5% |

| |||||||

CP All PCL — NVDR | 680,980 | 1,023,977 | ||||||

|

| |||||||

Cambodia — 0.3% |

| |||||||

NagaCorp, Ltd. | 1,020,875 | 623,700 | ||||||

|

| |||||||

Total FAR EAST | 50,794,086 | |||||||

|

| |||||||

| NORTH AMERICA — 9.8% | ||||||||

Canada — 7.4% |

| |||||||

B2Gold Corp.** | 475,510 | 1,701,835 | ||||||

Finning International, Inc. | 104,022 | 2,569,439 | ||||||

Imax Corp.** | 47,440 | 1,066,451 | ||||||

Intact Financial Corp. | 13,931 | 907,119 | ||||||

Lululemon Athletica, Inc.** | 14,570 | 1,110,671 | ||||||

New Gold, Inc.** | 144,399 | 1,598,304 | ||||||

Pacific Rubiales Energy Corp. | 59,673 | 1,386,391 | ||||||

Suncor Energy, Inc. | 82,420 | 2,710,323 | ||||||

Trilogy Energy Corp. | 71,107 | 2,080,954 | ||||||

|

| |||||||

| 15,131,487 | ||||||||

|

| |||||||

United States — 1.4% |

| |||||||

Catamaran Corp.** | 62,118 | 2,926,379 | ||||||

|

| |||||||

Mexico — 1.0% |

| |||||||

Fibra Uno Administracion SA de CV — REIT | 694,680 | 2,095,922 | ||||||

|

| |||||||

Total NORTH AMERICA | 20,153,788 | |||||||

|

| |||||||

| SOUTH AMERICA — 9.5% | ||||||||

Brazil — 6.5% |

| |||||||

Anhanguera Educacional Participacoes SA | 178,310 | 3,010,587 | ||||||

BR Malls Participacoes SA | 155,360 | 2,050,221 | ||||||

Number of Shares | Market Value (Note A) | |||||||

Brazil Pharma SA | 170,712 | $ | 1,200,612 | |||||

Gerdau SA — SP ADR | 153,420 | 1,379,246 | ||||||

Multiplus SA | 53,100 | 1,237,574 | ||||||

OdontoPrev SA | 265,750 | 1,392,673 | ||||||

Qualicorp SA** | 305,655 | 3,166,272 | ||||||

|

| |||||||

| 13,437,185 | ||||||||

|

| |||||||

Chile — 1.9% |

| |||||||

SACI Falabella | 200,854 | 2,068,912 | ||||||

Sociedad Quimica y Minera de Chile SA — SP ADR | 30,410 | 1,752,832 | ||||||

|

| |||||||

| 3,821,744 | ||||||||

|

| |||||||

Peru — 1.1% |

| |||||||

Credicorp, Ltd. | 15,780 | 2,312,717 | ||||||

|

| |||||||

Total SOUTH AMERICA | 19,571,646 | |||||||

|

| |||||||

| MIDDLE EAST — 1.7% | ||||||||

Israel — 1.7% |

| |||||||

Mellanox Technologies, Ltd.** | 26,540 | 1,575,945 | ||||||

Teva Pharmaceutical Industries, Ltd. — SP ADR | 49,730 | 1,856,918 | ||||||

|

| |||||||

| 3,432,863 | ||||||||

|

| |||||||

Total MIDDLE EAST | 3,432,863 | |||||||

|

| |||||||

Total EQUITY SECURITIES | 199,751,330 | |||||||

|

| |||||||

| ||||||||

TOTAL INVESTMENTS | 96.8 | % | $ | 199,751,330 | ||||

Other Assets In Excess Of Liabilities | 3.2 | % | 6,641,981 | |||||

|

|

|

| |||||

| Net Assets | 100.0 | % | $ | 206,393,311 | ||||

| ||||||||

The federal income tax basis and unrealized appreciation (depreciation) for all investments is as follows:

| Basis: | $ | 172,278,532 | ||

|

| |||

| Gross Appreciation | $ | 30,128,015 | ||

| Gross Depreciation | (2,655,217 | ) | ||

|

| |||

Net Appreciation | $ | 27,472,798 | ||

|

|

| ** | Non-income producing security |

NVDR — Non-Voting Depository Receipt

REIT — Real Estate Investment Trust

SP ADR — Sponsored American Depository Receipt

SP GDR — Sponsored Global Depository Receipt

Notes to Financial Statements are an integral part of this Schedule.

5

Driehaus International Discovery Fund

Schedule of Investments

December 31, 2012

Regional Weightings*

Western Europe | 48.6% | |||

Asia/Far East Ex-Japan | 17.8% | |||

North America | 9.8% | |||

South America | 9.5% | |||

Japan | 6.8% | |||

Eastern Europe | 2.6% | |||

Middle East | 1.7% |

Top Ten Holdings*

Safran SA | 2.3% | |||

Samsung Electronics Co., Ltd. | 2.1% | |||

Telecity Group PLC | 1.8% | |||

BHP Billton, Ltd. — SP ADR | 1.8% | |||

The Weir Group PLC | 1.7% | |||

Novo Nordisk AS — B | 1.7% | |||

Sands China, Ltd. | 1.7% | |||

Societe BIC SA | 1.7% | |||

M3, Inc. | 1.6% | |||

Qualicorp SA | 1.5% |

| * | All percentages are stated as a percent of net assets at December 31, 2012. |

Notes to Financial Statements are an integral part of this Schedule.

6

Driehaus International Discovery Fund

Schedule of Investments

December 31, 2012

Industry | Percent of Net Assets | |||

Aerospace & Defense | 2.3% | |||

Auto Components | 1.4% | |||

Automobiles | 1.6% | |||

Biotechnology | 0.7% | |||

Capital Markets | 1.1% | |||

Chemicals | 3.3% | |||

Commercial Banks | 4.6% | |||

Commercial Services & Supplies | 2.3% | |||

Diversified Consumer Services | 2.1% | |||

Diversified Telecommunications | 1.9% | |||

Electrical Equipment | 1.5% | |||

Electronic Equipment, Instruments & Components | 1.4% | |||

Energy Equipment & Services | 3.5% | |||

Food & Staples Retailing | 4.5% | |||

Food Products | 2.0% | |||

Health Care Equipment & Supplies | 3.5% | |||

Health Care Providers & Services | 3.8% | |||

Health Care Technology | 1.6% | |||

Hotels, Restaurants & Leisure | 2.5% | |||

Industrial Conglomerates | 1.0% | |||

Insurance | 2.9% | |||

Industry | Percent of Net Assets | |||

Internet & Catalog Retail | 1.2% | |||

Internet Software & Services | 3.1% | |||

Machinery | 3.9% | |||

Media | 0.5% | |||

Metals & Mining | 7.2% | |||

Multiline Retail | 1.9% | |||

Oil, Gas & Consumable Fuels | 3.8% | |||

Pharmaceuticals | 6.2% | |||

Professional Services | 1.0% | |||

Real Estate Investment Trust | 1.0% | |||

Real Estate Management & Development | 1.0% | |||

Road & Rail | 1.0% | |||

Semiconductors & Semiconductor Equipment | 5.2% | |||

Software | 0.6% | |||

Specialty Retail | 0.8% | |||

Textiles, Apparel & Luxury Goods | 4.7% | |||

Thrifts & Mortgage Finance | 0.4% | |||

Trading Companies & Distributors | 2.4% | |||

Transportation Infrastructure | 1.4% | |||

Other Assets in Excess of Liabilities | 3.2% | |||

|

| |||

TOTAL | 100.0% | |||

|

| |||

Notes to Financial Statements are an integral part of this Schedule.

7

Driehaus Emerging Markets Growth Fund — Portfolio Managers’ Letter

Dear Fellow Shareholders,

The Driehaus Emerging Markets Growth Fund (“Fund”) returned 19.51% for the year ended December 31, 2012. This return was above the performance of the Morgan Stanley Capital International (“MSCI”) Emerging Markets Index (“Benchmark”) (which returned 18.63% for the year) and below the MSCI Emerging Markets Growth Index (which returned 20.86% for the year).

The Fund now uses the MSCI Emerging Markets Index as its Benchmark. The MSCI Emerging Markets Growth Index, which was previously used as the Fund’s primary benchmark, will be used as a secondary performance benchmark. The broad-based MSCI Emerging Markets Index is a more accurate representative of the Fund’s investment universe.

The strong returns within emerging markets during 2012 were fuelled by the significant increase in global liquidity by developed market central banks, which benefited most financial assets. Also, as emerging markets growth slowed due to the economic slowdown in Europe and China, a disinflationary tailwind swept across developing economies. This allowed many emerging market central banks to aggressively ease monetary policy and continue to stimulate their economies. This presented an attractive investment environment and emerging markets equities rallied strongly in the second half of 2012. As the year came to a close, there were signs that the Chinese economy was improving. Stimulus implemented at the start of the second quarter began to show up in the economic data. The quarter also brought new leadership in Beijing and optimism that the new leaders would usher in a more proactive reform agenda. Elsewhere in emerging markets, other large economies, such as Brazil, India and South Korea, were showing signs that the worst of the growth slowdown of 2012 had passed.

Over the course of 2012, key contributors to performance versus the Benchmark were the Fund’s holdings in the consumer discretionary and materials sectors. In addition, stock selection in Brazil and Mexico contributed positively to the performance of the Fund.

Consumer discretionary holding NagaCorp, Ltd. (Ticker: 3918 HK) was the most significant contributor to the Fund’s return for 2012 relative to the Benchmark. NagaCorp, Ltd. owns, manages and operates the largest integrated gaming and entertainment hotel complex in Cambodia, NagaWorld. During the past several years NagaWorld has seen strong earnings growth, which has coincided with the steady rise in tourism in Cambodia. The hotel complex is currently going through various upgrades that that should contribute to its near-term earnings growth. Additionally, the company is scheduled to open its Naga2 property by the end of 2015.

Within Brazil, Kroton Educacional SA (Ticker: KROT3 BZ) was a holding that significantly contributed to relative returns for the year. Kroton Educacional SA is active in the private education sector. The company manages preschool, elementary, secondary and college preparatory schools, as well as higher, professional and post-graduation education, free courses and other related educational activities. In addition, it is involved in the wholesale, retail, distribution, import and export of textbooks. Kroton is well-positioned to benefit from government efforts to establish a strong student financing platform. The Brazilian government is actively seeking to drive increased levels of post-secondary education to build a higher skilled workforce. With a new government financing program in place, we believe post-secondary education demand should noticeably strengthen as income potential can increase significantly with the attainment of a post-secondary degree.

Certain areas detracted from Fund performance during the year. Two sectors that negatively affected performance of the Fund versus the Benchmark were information technology and health care. Additionally, holdings in South Korea and China detracted from Fund performance versus the Benchmark.

Within information technology, China-based Baidu, Inc. SP ADR (Ticker: BIDU) was a significant detractor from performance for 2012. Baidu is a Chinese-language Internet search provider. The company offers a Chinese-language search platform that enables users to find relevant information online, including Web pages, news, images, documents and multimedia files, through links provided on its websites. Baidu’s share price declined during the year due to the combination of lost market share to recently launched competitor Qihu (which continues to expand its vertical search engine platforms) and reduced advertising revenue due to macroeconomic uncertainty.

8

Within South Korea, health care holding Seegene, Inc. (Ticker: 096530 KS) was the most significant detractor for the year. Seegene specializes in molecular diagnostics and develops technology and products that diagnose disease at the genetic level. Seegene’s molecular diagnosis technology and products allow patients to benefit from cost effective and personalized diagnosis tools and allow doctors to offer accurate and effective treatment to patients. Seegene’s share price fell steeply mid-year due in part to a perceived delay in an expected global distribution deal.

Looking ahead, each of the last few years has seen periods of extreme concern regarding the state of the world, and equivalently exuberant market responses when those concerns ultimately fade. These worries usually have been driven by risks in Europe, though increasingly those ‘risk-off’ events are occurring at the hands of U.S. policymakers. However, we believe that the ability of the global economy to withstand shocks, from the perspectives of economic strength and financial liquidity, is better than it has been in the recent years. As such, we would not anticipate the global markets getting as near the cliff’s edge as they have in each of the past few years.

Recent improving global economic data is something we have been watching quite closely. We believe in the economic growth suggested by the data but remain cautious. We remember this narrative from the past few years where expectations ramp up at the start of the year only to be revised downward as the year progresses. We continue to believe that we reside in a low-growth world and that investors must be nimble to manage the volatility that accompanies such environments.

Globally, we are seeing many new opportunities in non-U.S. markets that did not look possible at this time last year. Financial conditions in Europe have meaningfully eased and the emerging markets outlook has improved thanks to low inflation, lower cost of capital, and inflecting growth trajectories. We remain optimistic but expect periods of volatility as government actions help and hurt economies in the year ahead.

We at Driehaus Capital Management LLC thank you for your interest in the Driehaus Emerging Markets Growth Fund and would like to express our gratitude to you as shareholders for your confidence in our management capabilities.

Sincerely,

|  | |

| Howard Schwab | Chad Cleaver | |

| Lead Portfolio Manager | Co-Portfolio Manager |

Performance is historical and does not represent future results.

Please see the following performance overview page for index descriptions.

9

Driehaus Emerging Markets Growth Fund

Performance Overview (unaudited)

The performance summarized below is historical and does not represent future results. Investment returns and principal value vary, and you may have a gain or loss when you sell shares. Performance data presented measures the change in the value of an investment in the Fund, assuming reinvestment of all dividends and capital gains. Average annual total return reflects annualized change.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The graph compares the results of a $10,000 investment in the Fund since December 31, 1997 (the date of the Fund’s inception), with all dividends and capital gains reinvested, with the indicated indices (and dividends reinvested) for the same period.

| Average Annual Total Returns as of 12/31/12 | 1 Year | 3 Years | 5 Years | 10 Years | Since Inception (12/31/97 - 12/31/12) | |||||||||||||||

Driehaus Emerging Markets Growth Fund (DREGX)1 | 19.51% | 7.86% | –0.56% | 18.76% | 14.17% | |||||||||||||||

MSCI Emerging Markets Index2 | 18.63% | 4.98% | –0.61% | 16.89% | 9.24% | |||||||||||||||

MSCI Emerging Markets Growth Index3 | 20.86% | 5.50% | –1.71% | 15.11% | 8.22% | |||||||||||||||

| 1 | The returns for the periods prior to July 1, 2003, reflect fee waivers and/or reimbursements without which performance would have been lower. |

| 2 | The Morgan Stanley Capital International Emerging Markets Index (MSCI Emerging Markets Index) is a market capitalization-weighted index designed to measure equity market performance in 21 global emerging markets. Data is in U.S. dollars. Source: Morgan Stanley Capital International Inc. |

| 3 | The Morgan Stanley Capital International Emerging Markets Growth Index (MSCI Emerging Markets Growth Index) is a subset of the MSCI Emerging Markets Index and includes only the MSCI Emerging Markets Index stocks which are categorized as growth stocks. Data is in U.S. dollars. Source: Morgan Stanley Capital International Inc. |

10

Driehaus Emerging Markets Growth Fund

Schedule of Investments

December 31, 2012

| Number of Shares | Market Value (Note A) | |||||||

| EQUITY SECURITIES — 92.5% | ||||||||

| FAR EAST — 50.1% | ||||||||

China — 16.8% |

| |||||||

AIA Group, Ltd. | 2,835,910 | $ | 11,248,170 | |||||

Belle International Holdings, Ltd. | 3,002,000 | 6,639,149 | ||||||

China Life Insurance Co., Ltd. — H | 2,801,077 | 9,277,342 | ||||||

China State Construction International Holdings, Ltd. | 6,178,270 | 7,541,588 | ||||||

CIMC Enric Holdings, Ltd. | 13,386,583 | 12,122,862 | ||||||

CNOOC, Ltd. | 4,454,000 | 9,812,220 | ||||||

ENN Energy Holdings, Ltd. | 2,158,000 | 9,456,116 | ||||||

Geely Automobile Holdings, Ltd. | 15,645,344 | 7,560,463 | ||||||

Haier Electronics Group Co., Ltd.** | 11,910,886 | 17,666,210 | ||||||

Industrial & Commercial Bank of China, Ltd. — H | 20,062,000 | 14,480,287 | ||||||

Kunlun Energy Co., Ltd. | 4,648,000 | 9,827,459 | ||||||

Lenovo Group, Ltd. | 11,316,000 | 10,434,031 | ||||||

Sino-Ocean Land Holdings, Ltd. | 3,973,774 | 3,022,136 | ||||||

Sunac China Holdings, Ltd. | 9,598,000 | 7,510,613 | ||||||

Tencent Holdings, Ltd. | 622,400 | 20,412,670 | ||||||

Want Want China Holdings, Ltd. | 3,076,580 | 4,311,537 | ||||||

Zoomlion Heavy Industry Science and Technology Co., Ltd. — H | 3,219,000 | 4,847,117 | ||||||

|

| |||||||

| 166,169,970 | ||||||||

|

| |||||||

South Korea — 9.1% |

| |||||||

Hyundai Glovis Co., Ltd. | 58,847 | 12,248,410 | ||||||

Kolao Holdings | 243,063 | 4,196,097 | ||||||

Samsung Electro-Mechanics Co., Ltd. | 63,930 | 5,976,226 | ||||||

Samsung Electronics Co., Ltd. | 39,240 | 56,380,026 | ||||||

SK Innovation Co., Ltd. | 68,375 | 11,313,577 | ||||||

|

| |||||||

| 90,114,336 | ||||||||

|

| |||||||

India — 5.7% |

| |||||||

Axis Bank, Ltd. | 329,702 | 8,284,079 | ||||||

HCL Technologies, Ltd. | 638,777 | 7,256,478 | ||||||

HDFC Bank, Ltd. | 364,986 | 4,550,252 | ||||||

IDFC, Ltd. | 5,674,746 | 17,998,615 | ||||||

Maruti Suzuki India, Ltd. | 249,918 | 6,848,234 | ||||||

Sun Pharmaceutical Industries, Ltd. | 280,592 | 3,795,360 | ||||||

Yes Bank, Ltd. | 896,217 | 7,633,049 | ||||||

|

| |||||||

| 56,366,067 | ||||||||

|

| |||||||

| Number of Shares | Market Value (Note A) | |||||||

Taiwan — 4.3% |

| |||||||

Asustek Computer, Inc. | 458,000 | $ | 5,186,566 | |||||

Far EasTone Telecommunications Co., Ltd. | 2,586,000 | 6,603,037 | ||||||

MediaTek, Inc. | 529,000 | 5,917,966 | ||||||

Taiwan Semiconductor Manufacturing Co., Ltd. — SP ADR | 1,413,681 | 24,258,766 | ||||||

|

| |||||||

| 41,966,335 | ||||||||

|

| |||||||

Philippines — 3.5% |

| |||||||

Ayala Land, Inc. | 6,085,100 | 3,933,236 | ||||||

Bank of Philippine Islands | 4,417,804 | 10,248,529 | ||||||

International Container Terminal Services, Inc. | 3,039,461 | 5,491,058 | ||||||

SM Investments Corp. | 438,700 | 9,466,052 | ||||||

SM Prime Holdings, Inc. | 12,877,200 | 5,190,733 | ||||||

|

| |||||||

| 34,329,608 | ||||||||

|

| |||||||

Singapore — 2.9% |

| |||||||

Lippo Malls Indonesia Retail Trust — REIT | 22,142,888 | 8,919,620 | ||||||

Yoma Strategic Holdings, Ltd. | 33,774,152 | 19,936,468 | ||||||

|

| |||||||

| 28,856,088 | ||||||||

|

| |||||||

Malaysia — 2.3% |

| |||||||

Axiata Group BHD | 6,079,900 | 13,150,456 | ||||||

Public Bank BHD | 1,872,234 | 9,989,693 | ||||||

|

| |||||||

| 23,140,149 | ||||||||

|

| |||||||

Thailand — 1.9% |

| |||||||

CP All PCL — NVDR | 3,850,512 | 5,789,946 | ||||||

Land & Houses PCL — NVDR | 27,658,000 | 8,869,692 | ||||||

Siam Commercial Bank PCL — NVDR | 686,064 | 4,094,167 | ||||||

|

| |||||||

| 18,753,805 | ||||||||

|

| |||||||

Cambodia — 1.9% |

| |||||||

NagaCorp, Ltd. | 30,464,696 | 18,612,289 | ||||||

|

| |||||||

Indonesia — 1.7% |

| |||||||

PT Bank Mandiri Persero Tbk | 5,022,500 | 4,242,576 | ||||||

PT Semen Indonesia Persero Tbk | 2,679,947 | 4,426,791 | ||||||

PT Telekomunikasi Indonesia Persero Tbk | 4,183,592 | 3,943,150 | ||||||

PT Tower Bersama Infrastructure Tbk** | 7,731,445 | 4,576,557 | ||||||

|

| |||||||

| 17,189,074 | ||||||||

|

| |||||||

Total FAR EAST | 495,497,721 | |||||||

|

| |||||||

Notes to Financial Statements are an integral part of this Schedule.

11

Driehaus Emerging Markets Growth Fund

Schedule of Investments

December 31, 2012

| Number of Shares | Market Value (Note A) | |||||||

| SOUTH AMERICA — 15.5% | ||||||||

Brazil — 13.0% |

| |||||||

Anhanguera Educacional Participacoes SA | 605,700 | $ | 10,226,642 | |||||

Arezzo Industria e Comercio SA | 79,295 | 1,531,681 | ||||||

Banco Bradesco SA — Pref. | 391,201 | 6,719,677 | ||||||

BR Malls Participacoes SA | 642,578 | 8,479,833 | ||||||

Brazil Pharma SA | 841,202 | 5,916,146 | ||||||

Cia. de Bebidas das Americas — Pref. | 272,800 | 11,402,307 | ||||||

Even Construtora e Incorporadora SA | 1,407,875 | 6,463,504 | ||||||

Itau Unibanco Holding SA — PREF ADR | 678,823 | 11,173,427 | ||||||

Kroton Educacional SA** | 735,119 | 16,605,252 | ||||||

Mills Estruturas e Servicos de Engenharia SA | 465,228 | 7,725,398 | ||||||

Qualicorp SA** | 1,027,613 | 10,645,017 | ||||||

Randon Participacoes SA — Pref. | 486,570 | 3,015,665 | ||||||

Vale SA — Pref. | 1,424,872 | 28,441,767 | ||||||

|

| |||||||

| 128,346,316 | ||||||||

|

| |||||||

Peru — 1.4% |

| |||||||

Credicorp, Ltd. | 97,327 | 14,264,245 | ||||||

|

| |||||||

Chile — 0.7% |

| |||||||

SACI Falabella | 729,495 | 7,514,218 | ||||||

|

| |||||||

Colombia — 0.4% |

| |||||||

Almacenes Exito SA | 189,575 | 3,808,666 | ||||||

|

| |||||||

Total SOUTH AMERICA | 153,933,445 | |||||||

|

| |||||||

| EUROPE — 11.7% | ||||||||

Russia — 6.8% |

| |||||||

Eurasia Drilling Co., Ltd. —GDR | 496,363 | 17,989,114 | ||||||

Magnit — SP GDR | 593,532 | 24,130,500 | ||||||

Rosneft OAO — GDR | 1,337,622 | 12,120,533 | ||||||

Sberbank RF — SP ADR | 1,030,699 | 12,921,965 | ||||||

|

| |||||||

| 67,162,112 | ||||||||

|

| |||||||

Turkey — 2.5% |

| |||||||

Aselsan Elektronik Sanayi Ve Ticaret AS | 1,041,740 | 4,951,851 | ||||||

Tofas Turk Otomobil Fabrikasi AS | 454,873 | 2,677,702 | ||||||

Trakya Cam Sanayii AS** | 1,741,978 | 2,382,506 | ||||||

Turkiye Garanti Bankasi AS | 942,944 | 4,921,630 | ||||||

Turkiye Halk Bankasi AS | 992,534 | 9,784,055 | ||||||

|

| |||||||

| 24,717,744 | ||||||||

|

| |||||||

Netherlands — 1.4% |

| |||||||

LyondellBasell Industries NV | 243,212 | 13,884,973 | ||||||

|

| |||||||

| Number of Shares | Market Value (Note A) | |||||||

Poland — 0.5% |

| |||||||

Eurocash SA | 380,689 | $ | 5,374,896 | |||||

|

| |||||||

United Kingdom — 0.5% |

| |||||||

Old Mutual PLC | 1,618,348 | 4,704,185 | ||||||

|

| |||||||

Total EUROPE | 115,843,910 | |||||||

|

| |||||||

| NORTH AMERICA — 7.1% | ||||||||

Mexico — 7.1% |

| |||||||

Bolsa Mexicana de Valores SAB de CV | 1,953,005 | 4,925,459 | ||||||

El Puerto de Liverpool SAB de CV | 746,468 | 7,898,194 | ||||||

Fibra Uno Administracion SA de CV — REIT | 5,958,468 | 17,977,322 | ||||||

Fomento Economico Mexicano SAB de CV — SP ADR | 48,642 | 4,898,249 | ||||||

Grupo Financiero Banorte SAB de CV — O | 2,435,078 | 15,724,218 | ||||||

Kimberly-Clark de Mexico SAB de CV — A | 2,670,631 | 6,859,267 | ||||||

Mexichem SAB de CV | 2,096,254 | 11,645,405 | ||||||

|

| |||||||

| 69,928,114 | ||||||||

|

| |||||||

Total NORTH AMERICA | 69,928,114 | |||||||

|

| |||||||

| AFRICA — 5.2% | ||||||||

South Africa — 3.6% |

| |||||||

Barloworld, Ltd. | 17,164 | 178,006 | ||||||

FirstRand, Ltd. | 1,379,277 | 5,075,406 | ||||||

Impala Platinum Holdings, Ltd. | 264,968 | 5,299,130 | ||||||

Life Healthcare Group Holdings, Ltd. | 1,374,232 | 5,522,722 | ||||||

Mr. Price Group, Ltd. | 563,812 | 9,344,145 | ||||||

MTN Group, Ltd. | 484,489 | 10,197,875 | ||||||

|

| |||||||

| 35,617,284 | ||||||||

|

| |||||||

Nigeria — 1.6% |

| |||||||

Zenith Bank PLC | 125,462,191 | 15,659,674 | ||||||

|

| |||||||

Total AFRICA | 51,276,958 | |||||||

|

| |||||||

| MIDDLE EAST — 2.9% | ||||||||

Qatar — 1.2% |

| |||||||

Industries Qatar QSC | 268,641 | 11,485,565 | ||||||

|

| |||||||

United Arab Emirates — 1.1% |

| |||||||

Emaar Properties PJSC | 11,023,747 | 11,388,917 | ||||||

|

| |||||||

Pakistan — 0.6% |

| |||||||

Engro Foods, Ltd.** | 5,749,243 | 5,804,544 | ||||||

|

| |||||||

Total MIDDLE EAST | 28,679,026 | |||||||

|

| |||||||

Total EQUITY SECURITIES (Cost $769,883,793) | 915,159,174 | |||||||

|

| |||||||

Notes to Financial Statements are an integral part of this Schedule.

12

Driehaus Emerging Markets Growth Fund

Schedule of Investments

December 31, 2012

| Number of Shares | Market Value (Note A) | |||||||

| EQUITY CERTIFICATES — 1.0% | ||||||||

| MIDDLE EAST — 1.0% | ||||||||

Saudi Arabia — 1.0% |

| |||||||

Etihad Etisalat Co.† | 475,416 | $ | 9,634,584 | |||||

|

| |||||||

Total MIDDLE EAST | 9,634,584 | |||||||

|

| |||||||

Total EQUITY CERTIFICATES (Cost $8,851,698) | 9,634,584 | |||||||

|

| |||||||

| ||||||||

| EXCHANGE-TRADED FUNDS — 0.5% | ||||||||

| NORTH AMERICA — 0.5% | ||||||||

United States — 0.5% |

| |||||||

Energy Select Sector SPDR Fund | 71,997 | 5,143,466 | ||||||

|

| |||||||

Total NORTH AMERICA | 5,143,466 | |||||||

|

| |||||||

Total EXCHANGE-TRADED FUNDS | 5,143,466 | |||||||

|

| |||||||

| ||||||||

TOTAL INVESTMENTS | 94.0 | % | $ | 929,937,224 | ||||

Other Assets In Excess Of Liabilities | 6.0 | % | 59,320,786 | |||||

|

|

|

| |||||

| Net Assets | 100.0 | % | $ | 989,258,010 | ||||

| ||||||||

The federal income tax basis and unrealized appreciation (depreciation) for all investments is as follows:

| Basis: | $ | 788,366,456 | ||

|

| |||

| Gross Appreciation | $ | 146,752,637 | ||

| Gross Depreciation | (5,181,869 | ) | ||

|

| |||

Net Appreciation | $ | 141,570,768 | ||

|

|

| ** | Non-income producing security |

| † | Restricted security — Investments in securities not registered under the Securities Act of 1933, excluding 144A securities. At December 31, 2012, the value of these restricted securities amounted to $9,634,584 or 1.0% of net assets. |

Additional information on each restricted security is as follows (see Note A in Notes to Financial Statements):

Security | Counter- party | Acquisition Date(s) | Acquisition Cost | |||||||||

Etihad Etisalat Co. | MSCO | | 08/27/12 to 10/10/12 | | $ | 8,851,698 | ||||||

GDR — Global Depository Receipt

MSCO — Morgan Stanley & Co., Inc.

NVDR — Non-Voting Depository Receipt

PREF ADR — Preferred American Depository Receipt

REIT — Real Estate Investment Trust

SP ADR — Sponsored American Depository Receipt

SP GDR — Sponsored Global Depository Receipt

Regional Weightings*

Asia/Far East Ex-Japan | 50.1% | |||

South America | 15.5% | |||

Eastern Europe | 9.8% | |||

North America | 7.6% | |||

Africa | 5.2% | |||

Middle East | 3.9% | |||

Western Europe | 1.9% |

Top Ten Holdings*

Samsung Electronics Co., Ltd. | 5.7% | |||

Vale SA — Pref. | 2.9% | |||

Taiwan Semiconductor Manufacturing Co., Ltd. — SP ADR | 2.5% | |||

Magnit — SP GDR | 2.4% | |||

Tencent Holdings, Ltd. | 2.1% | |||

Yoma Strategic Holdings, Ltd. | 2.0% | |||

NagaCorp, Ltd. | 1.9% | |||

IDFC, Ltd. | 1.8% | |||

Eurasia Drilling Co., Ltd. — GDR | 1.8% | |||

Fibra Uno Administracion SA de CV — REIT | 1.8% |

| * | All percentages are stated as a percent of net assets at December 31, 2012. |

Notes to Financial Statements are an integral part of this Schedule.

13

Driehaus Emerging Markets Growth Fund

Schedule of Investments

December 31, 2012

Industry | Percent of Net Assets | |||

Aerospace & Defense | 0.5% | |||

Air Freight & Logistics | 1.2% | |||

Automobiles | 2.2% | |||

Beverages | 1.6% | |||

Buliding Products | 0.2% | |||

Chemicals | 2.6% | |||

Commercial Banks | 15.6% | |||

Computers & Peripherals | 1.6% | |||

Construction & Engineering | 2.8% | |||

Construction Materials | 0.4% | |||

Diversified Consumer Services | 2.7% | |||

Diversified Financial Services | 2.8% | |||

Diversified Telecommunications | 0.4% | |||

Electronic Equipment, Instruments & Components | 0.6% | |||

Energy Equipment & Services | 1.8% | |||

Food & Staples Retailing | 4.6% | |||

Food Products | 1.0% | |||

Gas Utilities | 1.0% | |||

Health Care Providers & Services | 1.6% | |||

Hotels, Restaurants & Leisure | 1.9% | |||

Household Durables | 2.4% | |||

Industry | Percent of Net Assets | |||

Household Products | 0.7% | |||

Industrial Conglomerates | 2.1% | |||

Insurance | 2.6% | |||

Internet Software & Services | 2.1% | |||

IT Services | 0.7% | |||

Machinery | 2.0% | |||

Metals & Mining | 3.4% | |||

Multiline Retail | 1.6% | |||

Oil, Gas & Consumable Fuels | 4.4% | |||

Other | 0.5% | |||

Pharmaceuticals | 0.4% | |||

Real Estate Investment Trust | 2.7% | |||

Real Estate Management & Development | 4.9% | |||

Semiconductors & Semiconductor Equipment | 8.7% | |||

Specialty Retail | 1.6% | |||

Textiles, Apparel & Luxury Goods | 0.2% | |||

Trading Companies & Distributors | 0.8% | |||

Transportation Infrastructure | 0.6% | |||

Wireless Telecommunication Services | 4.5% | |||

Other Assets in Excess of Liabilities | 6.0% | |||

|

| |||

TOTAL | 100.0% | |||

|

| |||

Notes to Financial Statements are an integral part of this Schedule.

14

Driehaus Emerging Markets Small Cap Growth Fund — Portfolio Managers’ Letter

Dear Fellow Shareholders,

The Driehaus Emerging Markets Small Cap Growth Fund (“Fund”) returned 28.83% for the year ended December 31, 2012.1 This return was above the performance of the Morgan Stanley Capital International (“MSCI”) Emerging Markets Small Cap Index (“Benchmark”) (which returned 22.60% for the same period) and above the performance of the MSCI Emerging Markets Index (which returned 18.63% for the same period), which is the Fund’s secondary benchmark index.

The strong returns within emerging markets during 2012 were fuelled by the significant increase in global liquidity by developed market central banks, which benefited most financial assets. Also, as emerging markets growth slowed due to the economic slowdown in Europe and China, a disinflationary tailwind swept across developing economies. This allowed many emerging market central banks to aggressively ease monetary policy and continue to stimulate their economies. This presented an attractive investment environment and emerging markets equities rallied strongly in the second half of 2012. As the year came to a close, there were signs that the Chinese economy was improving. Stimulus implemented at the start of the second quarter began to show up in the economic data. The quarter also brought new leadership in Beijing and optimism that the new leaders would usher in a more proactive reform agenda. Elsewhere in emerging markets, other large economies, such as Brazil, India and South Korea, were showing signs that the worst of the growth slowdown of 2012 had passed.

For 2012, key contributors to performance versus the Benchmark were the Fund’s holdings in the consumer staples and consumer discretionary sectors. In addition, stock selection in South Korea, Indonesia and Malaysia contributed to the Fund’s outperformance.

Consumer discretionary holding NagaCorp, Ltd. (Ticker: 3918 HK) was the most significant contributor to return for 2012. NagaCorp, Ltd. owns, manages and operates the largest integrated gaming and entertainment hotel complex in Cambodia, NagaWorld. During the past several years NagaWorld has seen strong earnings growth, which has coincided with the steady rise in tourism in Cambodia. The hotel complex is currently going through various upgrades that should contribute to its near-term earnings growth. Additionally, the company is scheduled to open its Naga2 property by the end of 2015.

Within South Korea, consumer staples company Cosmax, Inc. (Ticker: 044820 KS) was a significant contributor to the Fund’s return for 2012. Cosmax develops skincare, makeup, hair care, and health care products. The market for domestic brands in South Korea continued to expand during the year, benefiting domestic manufacturers such as Cosmax. Within China, Cosmax sales also grew at a strong pace. Earnings are likely to remain strong due to capacity increases from overseas operations and strong growth within its domestic market.

Certain areas detracted from Fund performance during the year. Two sectors that negatively affected performance of the Fund versus the Benchmark were health care and materials. Additionally, holdings in Canada (companies with significant exposure to emerging markets), the United Kingdom and Hong Kong detracted from Fund performance versus the Benchmark.

Within health care, South Korean holding Seegene, Inc. (Ticker: 096530 KS) was the most significant detractor for the year. Seegene specializes in molecular diagnostics and develops technology and products that diagnose disease at the genetic level. Seegene’s molecular diagnosis technology and products allow patients to benefit from cost effective and personalized diagnosis tools and allow doctors to offer accurate and effective treatment to patients. Seegene’s share price fell steeply mid-year due in part to a perceived delay in an expected global distribution deal.

Within the United Kingdom, energy holding Chariot Oil & Gas Ltd. (Ticker: CHAR LN) was the most significant detractor. Chariot Oil & Gas Ltd. is an independent oil and gas exploration company focused on offshore West Africa with a portfolio of assets located in the underexplored regions of Namibia, Mauritania and Morocco. Chariot’s exploration efforts during 2012 were less successful than investors had hoped and costs increased significantly during the year.

We utilized option strategies in the Fund primarily to hedge a portion of the Fund’s portfolio, dampen volatility, and manage downside risk. These strategies primarily consisted of puts and put spreads on exchange-traded funds (ETFs). As the market posted strong returns during 2012, the options detracted from

15

performance. However, the options did help lessen volatility and manage downside risk, which are key considerations in the management of the Fund.

Looking ahead, each of the last few years has seen periods of extreme concern regarding the state of the world, and equivalently exuberant market responses when those concerns ultimately fade. These worries usually have been driven by risks in Europe, though increasingly those ‘risk-off’ events are occurring at the hands of U.S. policymakers. However, we believe that the ability of the global economy to withstand shocks, from the perspectives of economic strength and financial liquidity, is better than it has been in the recent years. As such, we would not anticipate the global markets getting as near the cliff’s edge as they have in each of the past few years.

Recent improving global economic data is something we have been watching quite closely. We believe in the economic growth suggested by the data, but remain cautious. We remember this narrative from the past few years where expectations ramp up at the start of the year only to be revised downward as the year progresses. We continue to believe that we reside in a low-growth world and that investors must be nimble to manage the volatility that accompanies such environments.

Globally, we are seeing many new opportunities in non-U.S. markets that did not look possible at this time last year. Financial conditions in Europe have meaningfully eased and the emerging markets outlook has improved thanks to low inflation, lower cost of capital, and inflecting growth trajectories. We remain optimistic but expect periods of volatility as government actions help and hurt economies in the year ahead.

We at Driehaus Capital Management LLC thank you for your interest in the Driehaus Emerging Markets Small Cap Growth Fund and would like to express our gratitude to you as shareholders for your confidence in our management capabilities.

Sincerely,

| | |

| Chad Cleaver | Howard Schwab | |

| Lead Portfolio Manager | Co-Portfolio Manager |

| 1 | During this period, the Fund’s returns reflect fee waivers and/or reimbursements without which performance would have been lower. |

Performance is historical and does not represent future results.

Please see the following performance overview page for index descriptions.

16

Driehaus Emerging Markets Small Cap Growth Fund

Performance Overview (unaudited)

The performance summarized below is historical and does not represent future results. Investment returns and principal value vary, and you may have a gain or loss when you sell shares. Performance data presented measures the change in the value of an investment in the Fund, assuming reinvestment of all dividends and capital gains. Average annual total return reflects annualized change.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The graph compares the results of a $10,000 investment in the Fund since December 1, 2008 (the date of the Predecessor Limited Partnership’s inception), with all dividends and capital gains reinvested, with the indicated indices (and dividends reinvested) for the same period.

| Fund Only | Including Predecessor Limited Partnership | |||||||||||||||

| Average Annual Total Returns as of 12/31/12 | 1 Year | Since Inception (08/22/11 - 12/31/12) | 3 Years | Since Inception (12/01/08 - 12/31/12) | ||||||||||||

Driehaus Emerging Markets Small Cap Growth | 28.83% | 9.75% | 11.66% | 23.10% | ||||||||||||

MSCI Emerging Markets Small Cap Index2 | 22.60% | 4.17% | 4.51% | 28.20% | ||||||||||||

MSCI Emerging Markets Index3 | 18.63% | 9.27% | 4.98% | 21.72% | ||||||||||||

| 1 | The Driehaus Emerging Markets Small Cap Growth Fund (the “Fund”) performance shown above includes the performance of the Driehaus Emerging Markets Small Cap Growth Fund, L.P. (the “Predecessor Limited Partnership”), the Fund’s predecessor, for the periods before the Fund’s registration statement became effective. The Predecessor Limited Partnership, which was established on December 1, 2008, was managed with substantially the same investment objective, policies and philosophies as are followed by the Fund. The Fund succeeded to the Predecessor Limited Partnership’s assets on August 22, 2011. The Predecessor Limited Partnership was not registered under the Investment Company Act of 1940, as amended (“1940 Act”), and thus was not subject to certain investment and operational restrictions that are imposed by the 1940 Act. If the Predecessor Limited Partnership had been registered under the 1940 Act, its performance may have been adversely affected. The Predecessor Limited Partnership’s performance has been restated to reflect estimated expenses of the Fund. The returns for the periods reflect fee waivers and/or reimbursements without which performance would have been lower. |

| 2 | The Morgan Stanley Capital International Emerging Markets Small Cap Index (MSCI Emerging Markets Small Cap Index) is a market capitalization-weighted index designed to measure equity market performance of small cap stocks in 21 global emerging markets. Data is in U.S. dollars. Source: Morgan Stanley Capital International Inc. |

| 3 | The Morgan Stanley Capital International Emerging Markets Index (MSCI Emerging Markets Index) is a market capitalization weighted index designed to measure equity market performance in 21 global emerging markets. Data is in U.S. dollars. Source: Morgan Stanley Capital International Inc. |

17

Driehaus Emerging Markets Small Cap Growth Fund

Schedule of Investments

December 31, 2012

| Number of Shares | Market Value (Note A) | |||||||

| EQUITY SECURITIES — 81.3% | ||||||||

| FAR EAST — 51.2% | ||||||||

China — 13.8% |

| |||||||

China Medical System Holdings, Ltd. | 1,515,000 | $ | 1,182,514 | |||||

CIMC Enric Holdings, Ltd. | 1,280,000 | 1,159,165 | ||||||

Geely Automobile Holdings, Ltd. | 2,457,839 | 1,187,727 | ||||||

GOME Electrical Appliances Holding, Ltd.** | 6,134,000 | 742,209 | ||||||

Haier Electronics Group Co., Ltd.** | 1,464,853 | 2,172,668 | ||||||

Hilong Holding, Ltd. | 3,267,000 | 1,161,956 | ||||||

Honghua Group, Ltd. | 3,153,000 | 1,406,299 | ||||||

Ju Teng International Holdings, Ltd. | 1,308,000 | 630,328 | ||||||

Sunac China Holdings, Ltd. | 1,062,000 | 831,035 | ||||||

Trinity, Ltd. | 1,082,000 | 716,319 | ||||||

|

| |||||||

| 11,190,220 | ||||||||

|

| |||||||

Indonesia — 6.2% |

| |||||||

PT Ace Hardware Indonesia Tbk | 10,102,000 | 864,069 | ||||||

PT Bekasi Fajar Industrial Estate Tbk** | 6,551,000 | 463,921 | ||||||

PT Jasa Marga Persero Tbk | 798,000 | 452,047 | ||||||

PT Summarecon Agung Tbk | 3,624,000 | 717,024 | ||||||

PT Surya Esa Perkasa Tbk** | 1,422,000 | 458,968 | ||||||

PT Tempo Scan Pacific Tbk | 870,000 | 336,905 | ||||||

PT Tower Bersama Infrastructure Tbk** | 2,902,000 | 1,717,812 | ||||||

|

| |||||||

| 5,010,746 | ||||||||

|

| |||||||

Philippines — 6.2% |

| |||||||

Bloomberry Resorts Corp.** | 2,001,613 | 643,441 | ||||||

Megaworld Corp. | 8,305,000 | 562,162 | ||||||

Metro Pacific Investments Corp. | 7,521,000 | 818,415 | ||||||

Philippine Seven Corp. | 173,610 | 391,209 | ||||||

Robinsons Land Corp. | 1,455,800 | 737,035 | ||||||

Security Bank Corp. | 126,784 | 482,840 | ||||||

Universal Robina Corp. | 186,690 | 381,450 | ||||||

Vista Land & Lifescapes, Inc. | 8,263,000 | 980,310 | ||||||

|

| |||||||

| 4,996,862 | ||||||||

|

| |||||||

Thailand — 4.9% |

| |||||||

Beauty Community PCL — NVDR** | 1,215,900 | 635,973 | ||||||

Home Products Center PCL — NVDR | 1,858,380 | 772,688 | ||||||

Land & Houses PCL — NVDR | 4,805,300 | 1,541,020 | ||||||

| Number of Shares | Market Value (Note A) | |||||||

Malee Sampran Factory PCL — NVDR | 172,700 | $ | 641,534 | |||||

Siam Makro PCL — NVDR | 26,461 | 387,010 | ||||||

|

| |||||||

| 3,978,225 | ||||||||

|

| |||||||

Malaysia — 4.6% |

| |||||||

Dialog Group BHD | 854,700 | 674,536 | ||||||

Guinness Anchor BHD | 112,600 | 611,236 | ||||||

Oldtown BHD | 3,307,800 | 2,464,805 | ||||||

|

| |||||||

| 3,750,577 | ||||||||

|

| |||||||

South Korea — 4.2% |

| |||||||

Cosmax, Inc. | 14,670 | 595,559 | ||||||

Kolao Holdings | 164,533 | 2,840,401 | ||||||

|

| |||||||

| 3,435,960 | ||||||||

|

| |||||||

Singapore — 3.9% |

| |||||||

First REIT | 852,000 | 742,123 | ||||||

Lippo Malls Indonesia Retail Trust — REIT | 1,860,000 | 749,247 | ||||||

Parkson Retail Asia, Ltd. | 80,000 | 86,544 | ||||||

Yoma Strategic Holdings, Ltd. | 2,719,000 | 1,604,992 | ||||||

|

| |||||||

| 3,182,906 | ||||||||

|

| |||||||

Cambodia — 3.9% |

| |||||||

NagaCorp, Ltd. | 5,166,098 | 3,156,208 | ||||||

|

| |||||||

Taiwan — 2.5% |

| |||||||

Chailease Holding Co., Ltd. | 241,000 | 556,144 | ||||||

Hiwin Technologies Corp. | 102,150 | 755,009 | ||||||

St. Shine Optical Co., Ltd. | 45,000 | 688,258 | ||||||

|

| |||||||

| 1,999,411 | ||||||||

|

| |||||||

Sri Lanka — 1.0% |

| |||||||

John Keells Holdings PLC | 444,250 | 769,821 | ||||||

|

| |||||||

Total FAR EAST | 41,470,936 | |||||||

|

| |||||||

| SOUTH AMERICA — 9.9% | ||||||||

Brazil — 8.6% |

| |||||||

Arezzo Industria e Comercio SA | 47,374 | 915,088 | ||||||

BR Properties SA | 64,573 | 804,206 | ||||||

Iguatemi Empresa de Shopping Centers SA | 54,200 | 721,078 | ||||||

Kroton Educacional SA** | 47,200 | 1,066,178 | ||||||

Marcopolo SA — Pref. | 96,900 | 610,505 | ||||||

Mills Estruturas e Servicos de Engenharia SA | 49,100 | 815,336 | ||||||

OdontoPrev SA | 99,000 | 518,813 | ||||||

Qualicorp SA** | 59,846 | 619,943 | ||||||

Randon Participacoes SA — Pref. | 151,988 | 941,992 | ||||||

|

| |||||||

| 7,013,139 | ||||||||

|

| |||||||

Notes to Financial Statements are an integral part of this Schedule.

18

Driehaus Emerging Markets Small Cap Growth Fund

Schedule of Investments

December 31, 2012

| Number of Shares | Market Value (Note A) | |||||||

Peru — 1.3% |

| |||||||

Alicorp SA | 102,348 | $ | 332,806 | |||||

Intercorp Financial Services Inc. | 20,209 | 723,482 | ||||||

|

| |||||||

| 1,056,288 | ||||||||

|

| |||||||

Total SOUTH AMERICA | 8,069,427 | |||||||

|

| |||||||

| AFRICA — 7.8% | ||||||||

Nigeria — 5.4% |

| |||||||

Guaranty Trust Bank PLC | 9,796,926 | 1,443,031 | ||||||

Guinness Nigeria PLC | 534,757 | 941,775 | ||||||

Unilever Nigeria PLC | 1,232,564 | 367,924 | ||||||

Zenith Bank PLC | 13,038,278 | 1,627,384 | ||||||

|

| |||||||

| 4,380,114 | ||||||||

|

| |||||||

South Africa — 2.0% |

| |||||||

Life Healthcare Group Holdings, Ltd. | 201,186 | 808,520 | ||||||

The Spar Group, Ltd. | 50,536 | 788,852 | ||||||

|

| |||||||

| 1,597,372 | ||||||||

|

| |||||||

Kenya — 0.4% |

| |||||||

Safaricom, Ltd. | 5,575,500 | 327,399 | ||||||

|

| |||||||

Total AFRICA | 6,304,885 | |||||||

|

| |||||||

| NORTH AMERICA — 5.0% | ||||||||

Mexico — 4.6% |

| |||||||

Alsea SAB de CV** | 181,600 | 362,040 | ||||||

Banregio Grupo Financiero SAB de CV | 192,943 | 879,164 | ||||||

Bolsa Mexicana de Valores SAB de CV | 374,376 | 944,173 | ||||||

Fibra Uno Administracion SA de CV — REIT | 522,100 | 1,575,230 | ||||||

|

| |||||||

| 3,760,607 | ||||||||

|

| |||||||

Canada — 0.4% |

| |||||||

Africa Oil Corp.** | 44,412 | 315,407 | ||||||

|

| |||||||

Total NORTH AMERICA | 4,076,014 | |||||||

|

| |||||||

| EUROPE — 4.2% | ||||||||

Turkey — 2.1% |

| |||||||

Koza Altin Isletmeleri AS | 15,256 | 369,079 | ||||||

Tofas Turk Otomobil Fabrikasi AS | 91,439 | 538,274 | ||||||

Trakya Cam Sanayii AS** | 560,988 | 767,264 | ||||||

|

| |||||||

| 1,674,617 | ||||||||

|

| |||||||

United Kingdom — 1.3% |

| |||||||

Ophir Energy PLC** | 129,063 | 1,066,564 | ||||||

|

| |||||||

Kazakhstan — 0.8% |

| |||||||

Halyk Savings Bank of Kazakhstan — GDR** | 79,945 | 655,549 | ||||||

|

| |||||||

Total EUROPE | 3,396,730 | |||||||

|

| |||||||

| Number of Shares | Market Value (Note A) | |||||||

| MIDDLE EAST — 3.2% | ||||||||

Pakistan — 1.8% |

| |||||||

Engro Foods, Ltd.** | 909,797 | $ | 918,548 | |||||

Fatima Fertilizer Co., Ltd. | 1,864,817 | 506,467 | ||||||

|

| |||||||

| 1,425,015 | ||||||||

|

| |||||||

Egypt — 1.4% |

| |||||||

Commercial International Bank Egypt SAE | 95,912 | 521,333 | ||||||

Juhayna Food Industries | 508,882 | 615,299 | ||||||

|

| |||||||

| 1,136,632 | ||||||||

|

| |||||||

Total MIDDLE EAST | 2,561,647 | |||||||

|

| |||||||

Total EQUITY SECURITIES (Cost $52,776,606) | 65,879,639 | |||||||

|

| |||||||

| ||||||||

| EQUITY CERTIFICATES— 8.7% | ||||||||

| FAR EAST — 6.8% | ||||||||

India — 6.8% |

| |||||||

Colgate-Palmolive, Ltd.† | 43,001 | 1,229,912 | ||||||

Federal Bank, Ltd.† | 116,215 | 1,141,575 | ||||||

Jaiprakash Associates, Ltd.† | 593,755 | 1,050,098 | ||||||

Kaveri Seed Co., Ltd.† | 28,723 | 674,118 | ||||||

Page Industries, Ltd.† | 8,242 | 515,121 | ||||||

Yes Bank, Ltd.†** | 107,667 | 911,898 | ||||||

|

| |||||||

| 5,522,722 | ||||||||

|

| |||||||

Total FAR EAST | 5,522,722 | |||||||

|

| |||||||

| MIDDLE EAST — 1.9% | ||||||||

Saudi Arabia — 1.9% |

| |||||||

Fawaz Abdulaziz Alhokair & Co.† | 28,608 | 793,353 | ||||||

Herfy Food Services Co.† | 25,992 | 727,737 | ||||||

|

| |||||||

| 1,521,090 | ||||||||

|

| |||||||

Total MIDDLE EAST | 1,521,090 | |||||||

|

| |||||||

Total EQUITY CERTIFICATES (Cost $6,278,516) | 7,043,812 | |||||||

|

| |||||||

| ||||||||

| EXCHANGE-TRADED FUNDS —2.2% | ||||||||

| FAR EAST — 1.2% | ||||||||

China — 1.2% |

| |||||||

iShares A50 China Index | 674,600 | 969,577 | ||||||

|

| |||||||

Total FAR EAST | 969,577 | |||||||

|

| |||||||

| NORTH AMERICA — 1.0% | ||||||||

United States — 1.0% |

| |||||||

Market Vectors Junior Gold Miners | 43,713 | 865,517 | ||||||

|

| |||||||

Total NORTH AMERICA | 865,517 | |||||||

|

| |||||||

Total EXCHANGE-TRADED FUNDS | 1,835,094 | |||||||

|

| |||||||

Notes to Financial Statements are an integral part of this Schedule.

19

Driehaus Emerging Markets Small Cap Growth Fund

Schedule of Investments

December 31, 2012

| Number of Shares | Market Value (Note A) | |||||||

| PURCHASED CALL OPTIONS — 0.2% | ||||||||

iShares MSCI Taiwan Index Fund, Exercise Price: $13.00, Expiration Date January, 2013** | 1,000 | $ | 55,000 | |||||

SPDR Gold Trust, Exercise Price: $164.00, Expiration Date March, 2013** | 250 | 81,000 | ||||||

|

| |||||||

Total PURCHASED CALL OPTIONS (Premiums paid $157,803) | 136,000 | |||||||

|

| |||||||

| ||||||||

| PURCHASED PUT OPTIONS — 0.3% | ||||||||

iShares MSCI Emerging Markets Index Fund, Exercise Price: $43.00, Expiration Date January, 2013** | 5,000 | 140,000 | ||||||

iShares MSCI Brazil Index Fund, Exercise Price: $50.00, Expiration Date March, 2013 ** | 500 | 35,500 | ||||||

SPDR Gold Trust, Exercise Price: $157.00, Expiration Date March, 2013** | 250 | 46,000 | ||||||

|

| |||||||

Total PURCHASED PUT OPTIONS | 221,500 | |||||||

|

| |||||||

| ||||||||

TOTAL INVESTMENTS | 92.7 | % | $ | 75,116,045 | ||||

Other Assets In Excess Of Liabilities | 7.3 | % | 5,881,345 | |||||

|

|

|

| |||||

| Net Assets | 100.0 | % | $ | 80,997,390 | ||||

| ||||||||

The federal income tax basis and unrealized appreciation (depreciation) for all investments is as follows:

| Basis: | $ | 62,354,539 | ||||

|

|

| ||||

| Gross Appreciation | $ | 14,511,280 | ||||

| Gross Depreciation | (1,749,774 | ) | ||||

|

|

| ||||

Net Appreciation | $ | 12,761,506 | ||||

|

|

| ||||

| ** | Non-income producing security |

| † | Restricted security — Investments in securities not registered under the Securities Act of 1933, excluding 144A securities. At December 31, 2012, the value of these restricted securities amounted to $7,043,812 or 8.7% of net assets. |

Additional information on each restricted security is as follows (see Note A in Notes to Financial Statements):

Security | Counter- party | Acquisition Date(s) | Acquisition Cost | |||||||||

Colgate-Palmolive, Ltd. | MLCO | | 08/16/12 to 12/19/12 | | $ | 963,504 | ||||||

Fawaz Abdulaziz Alhokair & Co. | | MLCO & MSCO | | | 10/09/12 to 11/05/12 | | $ | 750,686 | ||||

Federal Bank, Ltd. | MLCO | | 12/04/12 to 12/11/12 | | $ | 1,054,209 | ||||||

Herfy Food Services Co. | MSCO | | 09/11/12 to 10/01/12 | | $ | 705,543 | ||||||

Jaiprakash Associates, Ltd. | MLCO | | 11/30/12 to 12/19/12 | | $ | 1,069,972 | ||||||

Kaveri Seed Co., Ltd. | MLCO | | 10/05/12 to 11/01/12 | | $ | 588,605 | ||||||

Page Industries, Ltd. | MLCO | | 04/27/12 to 05/11/12 | | $ | 480,548 | ||||||

Yes Bank, Ltd. | MLCO | | 08/22/11 to 09/28/12 | | $ | 665,449 | ||||||

GDR — Global Depository Receipt

MLCO — Merrill Lynch & Co., Inc.

MSCO — Morgan Stanley & Co., Inc.

NVDR — Non-Voting Depository Receipt

REIT — Real Estate Investment Trust

Regional weightings(a)(b)

Asia/Far East Ex-Japan | 59.2% | |||

South America | 9.9% | |||

Africa | 7.8% | |||

North America | 6.0% | |||

Middle East | 5.1% | |||

Eastern Europe | 2.9% | |||

Western Europe | 1.3% |

Top Ten Holdings(a)

NagaCorp, Ltd. | 3.9% | |||

Kolao Holdings | 3.5% | |||

Oldtown BHD | 3.0% | |||

Haier Electronics Group Co., Ltd. | 2.7% | |||

PT Tower Bersama Infrastructure Tbk | 2.1% | |||

Zenith Bank PLC | 2.0% | |||

Yoma Strategic Holdings, Ltd. | 2.0% | |||

Fibra Uno Administracion SA de CV — REIT | 1.9% | |||

Land & Houses PCL — NVDR | 1.9% | |||

Guaranty Trust Bank PLC | 1.8% |

(a) All percentages are stated as a percent of net assets at December 31, 2012.

| (b) | Excludes purchased options. |

Notes to Financial Statements are an integral part of this Schedule.

20

Driehaus Emerging Markets Small Cap Growth Fund

Schedule of Investments

December 31, 2012

Industry | Percent of Net Assets | |||

Automobiles | 5.6% | |||

Beverages | 1.9% | |||

Building Products | 0.9% | |||

Chemicals | 0.6% | |||

Commercial Banks | 9.5% | |||

Construction & Engineering | 2.8% | |||

Diversified Consumer Services | 1.3% | |||

Diversified Financial Services | 3.8% | |||

Electronic Equipment, Instruments & Components | 0.8% | |||

Energy Equipment & Services | 3.2% | |||

Food & Staples Retailing | 1.9% | |||

Food Products | 7.4% | |||

Health Care Equipment & Supplies | 0.8% | |||

Health Care Providers & Services | 2.4% | |||

Hotels, Restaurants & Leisure | 6.0% | |||

Household Durables | 2.7% | |||

Household Products | 0.5% | |||

Industry | Percent of Net Assets | |||

Industrial Conglomerates | 2.2% | |||

Machinery | 4.3% | |||

Metals & Mining | 0.5% | |||

Multiline Retail | 0.1% | |||

Oil, Gas & Consumable Fuels | 2.3% | |||

Other | 2.7% | |||

Personal Products | 2.3% | |||

Pharmaceuticals | 1.9% | |||

Real Estate Investment Trust | 3.8% | |||

Real Estate Management & Development | 9.1% | |||

Specialty Retail | 4.7% | |||

Textiles, Apparel & Luxury Goods | 2.6% | |||

Trading Companies & Distributors | 1.0% | |||

Transportation Infrastructure | 0.6% | |||

Wireless Telecommunication Services | 2.5% | |||

Other Assets in Excess of Liabilities | 7.3% | |||

|

| |||

TOTAL | 100.0% | |||

|

| |||