As filed with the Securities and Exchange Commission on October 24, 2019

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

________________________

FORM 20-F

|

| |

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

|

| |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended June 30, 2019

OR

|

| |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

|

| |

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the transition period from___ to___

Commission file number: 001 — 31545

HARMONY GOLD MINING COMPANY LIMITED

(Exact name of registrant as specified in its charter)

REPUBLIC OF SOUTH AFRICA

(Jurisdiction of incorporation or organization)

RANDFONTEIN OFFICE PARK, CNR WARD AVENUE AND MAIN REEF ROAD,

RANDFONTEIN, SOUTH AFRICA, 1759

(Address of principal executive offices)

Riana Bisschoff, Group Company Secretary

Tel: +27 11 411 6020, riana.bisschoff@harmony.co.za, fax: +27 (0) 11 696 9734,

Randfontein Office Park, CNR Ward Avenue and Main Reef Road, Randfontein, South Africa, 1759

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | Trading Symbol(s) | Name of Each Exchange on Which Registered |

| Ordinary shares, with no par value per share* | n/a* | New York Stock Exchange* |

| American Depositary Shares (as evidenced by American Depositary Receipts), each representing one ordinary share | HMY | New York Stock Exchange |

* Not for trading, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission.

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

The number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the last full fiscal year covered by this Annual Report was 539,841,195 ordinary shares, with no par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES x NO ¨

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. YES x NO ¨

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES x NO ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “accelerated filer and large accelerated filer” and "emerging growth company" in Rule 12b-2 of the Exchange Act. |

| | | |

Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Emerging growth company ¨ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing: |

| | |

US GAAP ¨ | International Financial Reporting Standards as issued by the International Accounting Standards Board x | Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

YES ¨ NO x

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

YES ¨ NO ¨

TABLE OF CONTENTS

This document comprises the annual report on Form 20-F for the year ended June 30, 2019 (“Harmony 2019 Form 20-F”) of Harmony Gold Mining Company Limited (“Harmony” or the “Company”). Certain of the information in the Harmony Integrated Annual Report 2019 included in Exhibit 15.1 (“Integrated Annual Report for the 20-F 2019”) is incorporated by reference into the Harmony 2019 Form 20-F, as specified elsewhere in this report, in accordance with Rule 12b-23(a) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). With the exception of the items so specified, the Integrated Annual Report for the 20-F 2019 is not deemed to be filed as part of the Harmony 2019 Form 20-F.

Only (i) the information included in the Harmony 2019 Form 20-F, (ii) the information in the Integrated Annual Report for the 20-F 2019 that is expressly incorporated by reference in the Harmony 2019 Form 20-F and (iii) the exhibits to the Harmony 2019 Form 20-F that are required to be filed pursuant to the Form 20-F (the “Exhibits”), shall be deemed to be filed with the Securities and Exchange Commission (“SEC”) for any purpose. Any information in the Integrated Annual Report for the 20-F 2019 which is not referenced in the Harmony 2019 Form 20-F or filed as an Exhibit, shall not be deemed to be so incorporated by reference.

Financial and other material information regarding Harmony is routinely posted on and accessible at the Harmony website, www.harmony.co.za. No material referred to in this annual report as being available on our website is incorporated by reference into, or forms any part of, this annual report. References herein to our website shall not be deemed to cause such incorporation.

USE OF TERMS AND CONVENTIONS IN THIS ANNUAL REPORT

Harmony Gold Mining Company Limited is a corporation organized under the laws of the Republic of South Africa. As used in this Harmony 2019 Form 20-F, unless the context otherwise requires, the terms “Harmony” and “Company” refer to Harmony Gold Mining Company Limited; the term “South Africa” refers to the Republic of South Africa; the terms “we”, “us” and “our” refer to Harmony and, as applicable, its direct and indirect subsidiaries as a “Group”.

In this annual report, references to “R”, “Rand” and “c”, “cents” are to the South African Rand, the lawful currency of South Africa, “A$” and “Australian dollars” refers to Australian dollars, “K” or “Kina” refers to Papua New Guinean Kina and references to “$”, “US$” and “US dollars” are to United States dollars.

This annual report contains information concerning our gold reserves. While this annual report has been prepared in accordance with the regulations contained in the SEC’s Industry Guide 7, it is based on assumptions which may prove to be incorrect. See Item 3: “Key Information - Risk Factors - Estimations of Harmony’s reserves are based on a number of assumptions, including mining and recovery factors, future cash costs of production, exchange rates, and relevant commodity prices. As a result, metals produced in future may differ from current estimates.”

This annual report contains descriptions of gold mining and the gold mining industry, including descriptions of geological formations and mining processes. We have explained some of these terms in the Glossary of Mining Terms included in this annual report. This glossary may assist you in understanding these terms.

All references to websites in this annual report are intended to be inactive textual reference for information only and information contained in or accessible through any such website does not form a part of this annual report.

PRESENTATION OF FINANCIAL INFORMATION

We are a South African company and the majority of our operations are located in our home country. Accordingly, our books of account are maintained in South African Rand and our annual financial statements are prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). This annual report includes our consolidated financial statements prepared in accordance with IFRS presented in the functional currency of the Company, being South African Rand. All financial information, except as otherwise noted, is stated in accordance with IFRS.

Effective July 1, 2018, our presentation currency changed from the US Dollar to the South African Rand, which is the functional currency for the majority of the group’s operations. The functional currency represents the currency of the primary economic environment in which underlying businesses operate. We believe that utilizing a presentation currency that is consistent with the functional currency for the majority of the group’s operations, in which approximately 85% - 90% of our revenue and costs are generated, provides more relevant financial information. The presentation of the results of our operations in US dollar may be difficult to understand as a result of the volatile exchange rate differential between the two currencies, which can distort the results and financial position when comparing the current year to prior years. It should be noted that the functional currencies of the group’s underlying businesses remain unchanged and that foreign exchange exposures will therefore be unaffected by the change.

In this annual report, we also present “cash costs”, “cash costs per ounce”, “cash costs per kilogram” “all-in sustaining costs”, “all-in sustaining costs per ounce” and “all-in sustaining costs per kilogram”, which are non-GAAP measures. An investor should not consider these items in isolation or as alternatives to production costs, cost of sales or any other measure of financial performance presented in accordance with IFRS. The calculation of cash costs, cash costs per ounce/kilogram, all-in sustaining costs and all-in sustaining costs per ounce/kilogram may vary significantly among gold mining companies and, by themselves, do not necessarily provide a basis for comparison with other gold mining companies. For further information, see Item 5: “Operating and Financial Review and Prospects - Costs - Reconciliation of Non-GAAP Measures”. We have included the US dollar equivalent amounts of certain information and transactions in Rand, Kina and A$. Unless otherwise stated, we have translated assets and liabilities at the spot rate for the day, while the US$ equivalents of cash costs and all-in sustaining costs have been translated at the average rate for the year (R14.18 per US$1.00 for fiscal 2019, R12.85 per US$1.00 for fiscal 2018 and R13.60 per US$1.00 for fiscal 2017). By including these US dollar equivalents in this annual report, we are not representing that the Rand, Kina and A$ amounts actually represent the US dollar amounts, as the case may be, or that these amounts could be converted at the rates indicated.

CAUTIONARY STATEMENT ABOUT FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements within the meaning of the safe harbor provided by Section 21E of the Exchange Act and Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), with respect to our financial condition, results of operations, business strategies, operating efficiencies, competitive positions, growth opportunities for existing services, plans and objectives of management, markets for stock and other matters.

These forward-looking statements, including, among others, those relating to our future business prospects, revenues, and the potential benefit of acquisitions (including statements regarding growth and cost savings) wherever they may occur in this annual report and the exhibits to this annual report, are necessarily estimates reflecting the best judgment of our senior management and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. As a consequence, these forward-looking statements should be considered in light of various important factors, including those set forth in this annual report. Important factors that could cause actual results to differ materially from estimates or projections contained in the forward-looking statements include, without limitation:

| |

| • | overall economic and business conditions in South Africa, Papua New Guinea, Australia and elsewhere; |

| |

| • | estimates of future earnings, and the sensitivity of earnings to gold and other metals prices; |

| |

| • | estimates of future gold and other metals production and sales; |

| |

| • | estimates of future cash costs; |

| |

| • | estimates of future cash flows, and the sensitivity of cash flows to gold and other metals prices; |

| |

| • | estimates of provision for silicosis settlement; |

| |

| • | estimates of future tax liabilities under the Carbon Tax Act (as defined below); |

| |

| • | statements regarding future debt repayments; |

| |

| • | estimates of future capital expenditures; |

| |

| • | the success of our business strategy, exploration and development activities and other initiatives; |

| |

| • | future financial position, plans, strategies, objectives, capital expenditures, projected costs and anticipated cost savings and financing plans; |

| |

| • | estimates of reserves statements regarding future exploration results and the replacement of reserves; |

| |

| • | the ability to achieve anticipated efficiencies and other cost savings in connection with past and future acquisitions, as well as at existing operations; |

| |

| • | fluctuations in the market price of gold; |

| |

| • | the occurrence of hazards associated with underground and surface gold mining; |

| |

| • | the occurrence of labor disruptions related to industrial action or health and safety incidents; |

| |

| • | power cost increases as well as power stoppages, fluctuations and usage constraints; |

| |

| • | supply chain shortages and increases in the prices of production imports and the availability, terms and deployment of capital; |

| |

| • | our ability to hire and retain senior management, sufficiently technically-skilled employees, as well as our ability to achieve sufficient representation of historically disadvantaged persons in management positions; |

| |

| • | our ability to comply with requirements that we operate in a sustainable manner and provide benefits to affected communities; |

| |

| • | potential liabilities related to occupational health diseases; |

| |

| • | changes in government regulation and the political environment, particularly tax and royalties, mining rights, health, safety, environmental regulation and business ownership including any interpretation thereof; court decisions affecting the mining industry, including, without limitation, regarding the interpretation of mining rights; |

| |

| • | our ability to protect our information technology and communication systems and the personal data we retain; |

| |

| • | risks related to the failure of internal controls; |

| |

| • | the outcome of pending or future litigation or regulatory proceedings; |

| |

| • | fluctuations in exchange rates and currency devaluations and other macroeconomic monetary policies; |

| |

| • | the adequacy of the Group’s insurance coverage; |

| |

| • | any further downgrade of South Africa's credit rating; and |

| |

| • | socio-economic or political instability in South Africa, Papua New Guinea and other countries in which we operate. |

The foregoing factors and others described under “Risk Factors” should not be construed as exhaustive.

We undertake no obligation to update publicly or release any revisions to these forward-looking statements to reflect events or circumstances after the date of this annual report or to reflect the occurrence of unanticipated events, except as required by law. All subsequent written or oral forward-looking statements attributable to Harmony or any person acting on its behalf are qualified by the cautionary statements herein.

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. SELECTED FINANCIAL DATA

The selected consolidated financial data below should be read in conjunction with, and are qualified in their entirety by reference to, our consolidated financial statements, and the notes thereto, set forth beginning on page F-1, and with Item 3: “Key Information - Risk Factors” and Item 5: “Operating and Financial Review and Prospects”. Historical results are not necessarily indicative of results to be expected for any future period.

Selected Historical Consolidated Financial Data

We are a South African company and the majority of our operations are located in our home country. Accordingly, our books of account are maintained in South African Rand and our annual financial statements are prepared in accordance with IFRS. This annual report includes our consolidated financial statements prepared in accordance with IFRS, presented in the functional currency of the Company, being South African Rand. The selected historical consolidated income statement and balance sheet data for the last five fiscal years are, unless otherwise noted, stated in accordance with IFRS, and have been extracted from the more detailed information and financial statements prepared in accordance with IFRS. The financial data as at June 30, 2019 and 2018 and for each of the years in the three-year period ended June 30, 2019 should be read in conjunction with, and is qualified in its entirety by reference to our audited consolidated financial statements set forth beginning on page F-1. Financial data as at June 30, 2017, 2016 and 2015 and for the years ended June 30, 2016 and 2015 have been derived from our consolidated financial statements, which are not included in this document.

The acquisition of Moab Khotsong was effective March 1, 2018 (see Item 5: "Operating and Financial Review and Prospects - B Liquidity and Capital Resources - Investing"). The results of the operations have been consolidated in the financial statements for fiscal 2018 from the effective date. Subsequent to the provisional preparation of the purchase price allocation, the effective date tax values were finalized, which affected the mineral right value, goodwill and deferred tax. The 2018 comparative amounts were re-presented for this change. See note 2 "Accounting Policies" and note 12 "Acquisitions and Business Combinations" in the consolidated financial statements in Item 18. The measurement period for the purchase price allocation closed during fiscal 2019.

On July 1, 2018, IFRS 9 Financial Instruments and IFRS 15 Revenue from Contracts with Customers become effective. The adoption did not have a material impact on the consolidated financial statements. See note 2 "Accounting Policies" of the consolidated financial statements in Item 18 for further details.

In fiscal 2019, we voluntarily changed the accounting policy regarding by-products credits, which resulted in a change of the allocation from cost of sales to revenue. As a result we have re-presented our financial statements for the comparative periods. See note 2 "Accounting Policies" in our consolidated financial statements in Item 18.

|

| | | | | | | | | | |

| | Fiscal year ended June 30, |

| | 2019 |

| 2018 |

| 2017 |

| 2016 |

| 2015 |

|

| | (Rand in millions, except per share amounts, cash costs per kilogram and ounce and all-in sustaining costs per kilogram and ounce) |

| Income Statement Data | | | | | |

| Revenue | 26,912 |

| 20,452 |

| 19,494 |

| 18,667 |

| 15,643 |

|

| (Impairment)/reversal of impairment of assets | (3,898 | ) | (5,336 | ) | (1,718 | ) | 43 |

| (3,471 | ) |

| Operating profit/(loss) | (2,538 | ) | (4,660 | ) | (944 | ) | 1,592 |

| (5,193 | ) |

| Gain on bargain purchase | — |

| — |

| 848 |

| — |

| — |

|

| Profit/(loss) from associates | 59 |

| 38 |

| (22 | ) | 7 |

| (25 | ) |

| Profit/(loss) before taxation | (2,746 | ) | (4,707 | ) | (148 | ) | 1,581 |

| (5,240 | ) |

| Taxation | 139 |

| 234 |

| 510 |

| (632 | ) | 704 |

|

| Net profit/(loss) | (2,607 | ) | (4,473 | ) | 362 |

| 949 |

| (4,536 | ) |

| Basic earnings/(loss) per share (SA cents) | (498 | ) | (1,003 | ) | 82 |

| 218 |

| (1,044 | ) |

| Diluted earnings/(loss) per share (SA cents) | (500 | ) | (1,004 | ) | 79 |

| 213 |

| (1,044 | ) |

| Weighted average number of shares used in the computation of basic earnings/(loss) per share | 523,808,934 |

| 445,896,346 |

| 438,443,540 |

| 435,738,577 |

| 434,423,747 |

|

| Weighted average number of shares used in the computation of diluted earnings/(loss) per share | 533,345,964 |

| 465,319,405 |

| 459,220,318 |

| 446,398,380 |

| 438,091,109 |

|

Dividends per share (SA cents)1 | — |

| 35 |

| 100 |

| — |

| — |

|

| Other Financial Data | | | | | |

Total cash costs per kilogram of gold (R/kg)2 | 439,722 |

| 421,260 |

| 436,917 |

| 392,026 |

| 369,203 |

|

Total cash costs per ounce of gold ($/oz)2 | 965 |

| 1,018 |

| 1,000 |

| 841 |

| 1,003 |

|

All-in sustaining costs per kilogram of gold (R/kg)2 | 550,005 |

| 508,970 |

| 516,687 |

| 467,611 |

| 453,244 |

|

All-in sustaining costs per ounce of gold ($/oz)2 | 1,207 |

| 1,231 |

| 1,182 |

| 1,003 |

| 1,232 |

|

| Balance Sheet Data | | | | | |

| Assets | | | | | |

| Property, plant and equipment | 27,749 |

| 30,969 |

| 30,044 |

| 29,919 |

| 29,548 |

|

| Total assets | 36,736 |

| 39,521 |

| 38,883 |

| 37,030 |

| 36,137 |

|

| Net assets | 22,614 |

| 25,382 |

| 29,291 |

| 28,179 |

| 26,753 |

|

| Equity and liabilities | | | | | |

| Share capital | 29,551 |

| 29,340 |

| 28,336 |

| 28,336 |

| 28,324 |

|

| Total equity | 22,614 |

| 25,382 |

| 29,291 |

| 28,179 |

| 26,753 |

|

| Borrowings (current and non-current) | 5,915 |

| 5,614 |

| 2,133 |

| 2,339 |

| 3,399 |

|

| Other liabilities | 8,207 |

| 8,525 |

| 7,459 |

| 6,512 |

| 5,985 |

|

| Total equity and liabilities | 36,736 |

| 39,521 |

| 38,883 |

| 37,030 |

| 36,137 |

|

| |

1 | Dividends per share relates to the dividends recorded and paid during the fiscal year. |

| |

2 | Cash costs per ounce and per kilogram and all-in sustaining costs per ounce and per kilogram are non-GAAP measures. Cash costs per ounce/kilogram and all-in sustaining cost per ounce/kilogram have been calculated on a consistent basis for all periods presented. Changes in cash costs per ounce/kilogram and all-in sustaining costs per ounce/kilogram are affected by operational performance, as well as changes in the currency exchange rate between the Rand and the US dollar for the US$/ounce measures. Because cash cost per ounce/kilogram and all-in sustaining costs per ounce/kilogram are non-GAAP measures, these measures should therefore not be considered by investors in isolation or as an alternative to production costs, cost of sales, or any other measure of financial performance calculated in accordance with IFRS. The calculation of cash costs, cash costs per ounce and per kilogram, all-in sustaining costs and all-in sustaining costs per ounce and per kilogram may vary from company to company and may not be comparable to other similarly titled measures of other companies. For further information, see Item 5:“Operating and Financial Review and Prospects-Costs-Reconciliation of Non-GAAP measures”. |

B. CAPITALIZATION AND INDEBTEDNESS

Not applicable.

C. REASONS FOR THE OFFER AND USE OF PROCEEDS

Not applicable.

D. RISK FACTORS

In addition to the other information included in this annual report and the exhibits, you should also carefully consider the following factors related to our ordinary shares and ADSs. There may be additional risks that we do not currently know of or that we currently deem immaterial based on information currently available to us. Although Harmony has a formal risk policy framework in place, the maintenance and development of which is undertaken on an ongoing basis so as to help management address systematic categories of risk associated with its business operations, any of these risks could have a material adverse effect on our business, financial condition or results of operations, leading to a decline in the trading price of our ordinary shares or our ADSs. The risks described below may, in retrospect, turn out to be incomplete and therefore may not be the only risks to which we are exposed. Additional risks and uncertainties not presently known to us or that we now believe are immaterial (and have therefore not been included), could also adversely affect our business, results of operations or financial condition. The order of presentation of the risk factors below does not indicate the likelihood of their occurrence or the magnitude or the significance of the individual risks.

Risks Relating to Our Business and the Gold Mining Industry

The profitability of our operations, and cash flows generated by those operations, are affected by changes in the price of gold. A fall in the gold price below our cash cost of production and capital expenditure required to sustain production for any sustained period may lead to losses and require Harmony to curtail or suspend certain operations

Substantially all of Harmony’s revenues come from the sale of gold. Historically, the market price for gold has fluctuated widely and been affected by numerous factors, over which Harmony has no control, including:

| |

| • | demand for gold for industrial uses, jewelry and investment; |

| |

| • | international or regional political and economic events and trends; |

| |

| • | strength or weakness of the US dollar (the currency in which gold prices generally are quoted) and of other currencies; |

| |

| • | monetary policies announced or implemented by central banks, including the US Federal Reserve; |

| |

| • | financial market expectations on the rate of inflation; |

| |

| • | changes in the supply of gold from production, divestment, scrap and hedging; |

| |

| • | gold hedging or de-hedging by gold producers; |

| |

| • | actual or expected purchases and sales of gold bullion held by central banks or other large gold bullion holders or dealers; and |

| |

| • | production and cost levels for gold in major gold-producing nations, such as South Africa, China, the United States and Australia. |

In addition, current demand and supply affects the price of gold, but not necessarily in the same manner as current demand and supply affect the prices of other commodities. Historically, gold has retained its value in relative terms against basic goods in times of inflation and monetary crisis. As a result, central banks, financial institutions and individuals hold large amounts of gold as a store of value and production in any given year constitutes a very small portion of the total potential supply of gold. However, as gold has historically been used as a hedge against unstable or lower economic performance, improved economic performance may have a negative impact on the price for gold. Since the potential supply of gold is large relative to mine production in any given year, normal variations in current production will not necessarily have a significant effect on the supply of gold or its price. Uncertainty on global economic conditions has impacted the price of gold significantly since fiscal 2013 and continued to do so in fiscal 2019, and is still relevant as is evidenced by the strategic risk profile of Harmony.

The volatility of gold prices is illustrated in the table, which shows the annual high, low and average of the afternoon London bullion market fixing price of gold in US dollars for each of the past ten years:

Annual gold price: 2009 - 2019 |

| | | | | | |

| | Price per ounce (US$) |

| Calendar year | High |

| Low |

| Average |

|

| 2009 | 1,213 |

| 810 |

| 972 |

|

| 2010 | 1,421 |

| 1,058 |

| 1,225 |

|

| 2011 | 1,895 |

| 1,319 |

| 1,572 |

|

| 2012 | 1,792 |

| 1,540 |

| 1,669 |

|

| 2013 | 1,694 |

| 1,192 |

| 1,411 |

|

| 2014 | 1,385 |

| 1,142 |

| 1,266 |

|

| 2015 | 1,296 |

| 1,049 |

| 1,160 |

|

| 2016 | 1,366 |

| 1,077 |

| 1,251 |

|

| 2017 | 1,346 |

| 1,151 |

| 1,253 |

|

| 2018 | 1,355 |

| 1,178 |

| 1,268 |

|

| 2019 | 1,546 |

| 1,270 |

| 1,372 |

|

On October 17, 2019, the afternoon fixing price of gold on the London bullion market was US$1,492/oz.

While the price volatility is difficult to predict, if gold prices should fall below Harmony’s cash cost of production and capital expenditure required to sustain production and remain at these levels for any sustained period, Harmony may record losses and be forced to curtail or suspend some or all of its operations, which could materially adversely affect Harmony’s business, operating results and financial condition.

In addition, Harmony would also have to assess the economic impact of low gold prices on its ability to recover any losses that may be incurred during that period and on its ability to maintain adequate reserves. The use of lower gold prices in reserve calculations and life of mine plans could also result in material impairments of Harmony’s investment in gold mining properties or a reduction in its reserve estimates and corresponding restatements of its reserves and increased amortization, reclamation and closure charges.

Foreign exchange fluctuations could have a material adverse effect on Harmony’s operational results and financial condition

Gold is priced throughout the world in US dollars and, as a result, Harmony’s revenue is realized in US dollars, but most of our operating costs are incurred in Rand and other non-US currencies, including the Australian dollar and Kina. From time to time, Harmony may implement currency hedges intended to reduce exposure to changes in the foreign currency exchange, which it started doing in fiscal 2016 and will continue as long as it is strategically viable. Such hedging strategies may not however be successful, and any of Harmony’s unhedged exchange payments will continue to be subject to market fluctuations. Any significant and sustained appreciation of the Rand and other non-US currencies against the dollar will materially reduce Harmony’s Rand revenues and overall net income, which could materially adversely affect Harmony’s operating results and financial condition.

Harmony's inability to maintain an effective system of internal control over financial reporting may have an adverse effect on investors' confidence in the reliability of its financial statements

Internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of the company’s financial statements for external purposes in accordance with IFRS as issued by the IASB. Disclosure controls and procedures are designed to ensure that information required to be disclosed by a company in reports that it files or submits under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in the rules and forms of the SEC. Harmony has invested in resources to facilitate the documentation and assessment of its system of disclosure controls and its internal control over financial reporting. However, a control system, no matter how well designed and operated, can provide only reasonable, not absolute, assurance with respect to the reliability of financial reporting and financial statement preparation. If Harmony were unable to maintain an effective system of internal control over financial reporting, investors may lose confidence in the reliability of its financial statements and this may have an adverse impact on investors’ abilities to make decisions about their investment in Harmony. See Item 15: "Controls and Procedures".

Harmony is exposed to the impact of any significant decreases in the commodity prices on its production. This is mitigated by commodity derivatives and hedging arrangements, but as Harmony has limitations for the volume of forward sales, commodity derivatives or hedging arrangements it may enter into for its future production, it is exposed to the impact of decreases in the commodity prices on the remainder of its unhedged production

As a rule, Harmony sells its gold and silver at the prevailing market price. In fiscal 2017, however, Harmony started a commodity hedging program. These contracts manage variability of cash flows for approximately 20% of the Group’s total production over a two-year period for gold and 50% for silver. These limits can be amended from time to time. Hedging instruments that protect against the market price volatility of gold and silver may prevent us from realizing the full benefit from subsequent decreases in market prices with respect to gold and silver, however, which could cause us to record a mark-to-market loss, thus decreasing our profits. See Item 11: "Quantitative and Qualitative disclosure about market risk".

Harmony’s remaining unhedged future production may realize the benefit of any short-term increase in the commodity prices, but is not protected against decreases; if the gold or silver price should decrease significantly, Harmony’s revenues may be materially adversely affected, which could materially adversely affect Harmony’s operating results and financial condition.

Global economic conditions could adversely affect the profitability of Harmony’s operations

Harmony’s operations and performance depend on global economic conditions. Global economic conditions remain fragile with significant uncertainty regarding recovery prospects, level of recovery and long-term economic growth effects. A global economic downturn may have follow-on effects on our business. These could include:

| |

| • | key suppliers or contractors becoming insolvent, resulting in a break-down in the supply chain; |

| |

| • | a reduction in the availability of credit which may make it more difficult for Harmony to obtain financing for its operations and capital expenditures or make that financing more costly; |

| |

| • | exposure to the liquidity and insolvency risks of Harmony’s lenders and customers; or |

| |

| • | the availability of credit being reduced-this may make it more difficult for Harmony to obtain financing for its operations and capital expenditure or make financing more expensive. |

Coupled with the volatility of commodity prices as well as the rising trend of input costs, such factors could result in initiatives relating to strategic alignment, portfolio review, restructuring and cost-cutting, temporary or permanent shutdowns and divestments. Further, sudden changes in a life-of-mine plan or the accelerated closure of a mine may result in the recognition of impairments and give rise to the recognition of liabilities that are not anticipated.

In addition to the potentially adverse impact on the profitability of Harmony’s operations, any uncertainty on global economic conditions may also increase volatility or negatively impact the market value of Harmony’s securities. Any of these events could materially adversely affect Harmony’s business, operating results and financial condition.

A further downgrade of South Africa’s credit rating may have an adverse effect on Harmony’s ability to secure financing

The slowing economy, rising sovereign debt, escalating labor disputes and the structural challenges facing the mining industry and other sectors have resulted in the downgrading of South Africa’s sovereign credit ratings. At the beginning of fiscal 2018, two of the three international ratings agencies, Standard & Poor’s and Fitch Ratings, rated South Africa’s long-term sovereign credit rating as non-investment grade at BB+. In November 2017, Standard & Poor's further downgraded South Africa's sovereign rating to BB with a stable outlook, due to among other things, declining consumption on a per capita basis, economic growth performance that is among the weakest of emerging market sovereigns and income inequality. In November 2017, Fitch Ratings affirmed South Africa’s sovereign credit rating of BB+ with a negative outlook. In March 2018, Moody's affirmed its Baa3 sovereign credit rating for South Africa and upgraded its outlook to stable. In May 2018, Standard & Poor’s affirmed its BB sovereign credit rating of South Africa with a stable outlook, however post year end in July 2019, the outlook was downgraded again to negative. Further downgrading of South Africa’s credit ratings by any of these agencies may adversely affect the South African mining industry and Harmony’s business, operating results and financial condition by making it more difficult to obtain external financing or could result in any such financing being available only at greater cost or on more restrictive terms than might otherwise be available.

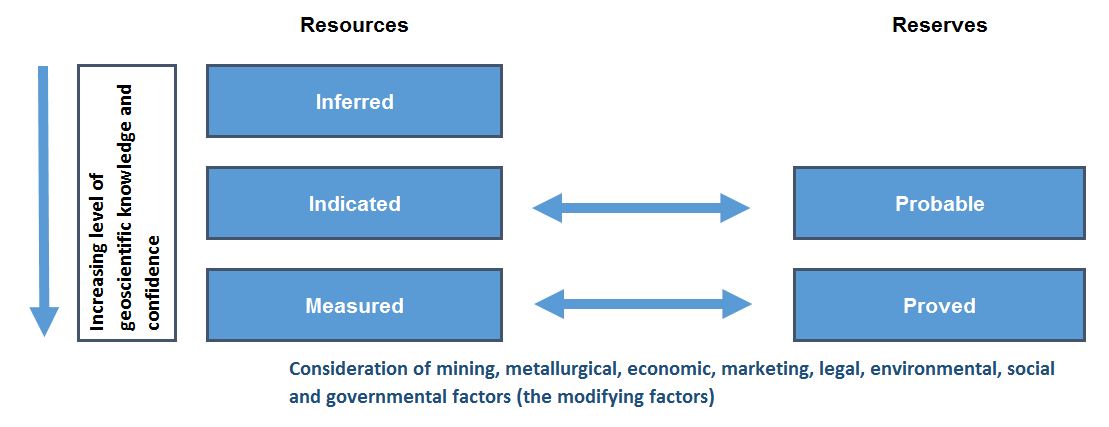

Estimations of Harmony’s reserves are based on a number of assumptions, including mining and recovery factors, future cash costs of production, exchange rates, and the relevant commodity prices. As a result, metals produced in future may differ from current estimates

The mineral reserve estimates in this annual report are estimates of the mill-delivered quantity and grade of metals in Harmony’s deposits and stockpiles. They represent the amount of metals that Harmony believes can be mined, processed and sold at prices sufficient to recover its estimated future cash costs of production, remaining investment and anticipated additional capital expenditures. Harmony’s mineral reserves are estimated based on a number of factors, which have been stated in accordance with the South African Code for the Reporting of Exploration Results, Mineral Resources and Mineral Reserves (“SAMREC Code”) and the SEC's Industry Guide 7. Calculations of Harmony’s mineral reserves are based on estimates of:

| |

| • | future commodity prices; |

| |

| • | future currency exchange rates; and |

| |

| • | metallurgical and mining recovery rates. |

These factors, which significantly impact mineral reserve estimates, are beyond Harmony’s control. As a result, reserve estimates in this annual report should not be interpreted as assurances of the economic life of Harmony’s gold and other precious metal deposits or the future profitability of operations.

Since these mineral reserves are estimates based on assumptions related to factors detailed above, should there be changes to any of these assumptions, we may in future need to revise these estimates. In particular, if Harmony’s cash operating and production costs increase or the gold price decreases, recovering a portion of Harmony’s mineral reserves may become uneconomical. This will lead, in turn, to a reduction in estimated reserves. Any reduction in our mineral reserves estimate could materially adversely affect Harmony’s business, operating results and financial condition.

Harmony’s operations have limited proved and probable reserves. Exploration for additional resources and reserves is speculative in nature, may be unsuccessful and involves many risks

Harmony’s operations have limited proved and probable reserves, and exploration and discovery of new resources and reserves are necessary to maintain current gold production levels at these operations. Exploration for gold and other precious metals is speculative in nature, may be unsuccessful and involves risks including those related to:

| |

| • | geological nature of the orebodies; |

| |

| • | identifying the metallurgical properties of orebodies; |

| |

| • | estimating the economic feasibility of mining orebodies; |

| |

| • | developing appropriate metallurgical processes; |

| |

| • | obtaining necessary governmental permits; and |

| |

| • | constructing mining and processing facilities at any site chosen for mining. |

Harmony’s exploration efforts might not result in the discovery of mineralization, and any mineralization discovered might not result in an increase in resources or proved and probable reserves. To access additional resources and reserves, Harmony will need to complete development projects successfully, including extensions to existing mines and, possibly, establishing new mines. Development projects would also be required to access any new mineralization discovered by exploration activities around the world. Harmony typically uses feasibility studies to determine whether to undertake significant development projects. These studies often require substantial expenditure. Feasibility studies include estimates of expected or anticipated economic returns, which are based on assumptions about:

| |

| • | future gold and other metal prices; |

| |

| • | anticipated tonnage, grades and metallurgical characteristics of ore to be mined and processed; |

| |

| • | anticipated recovery rates of gold and other metals from the ore; and |

| |

| • | anticipated total costs of the project, including capital expenditure and cash costs. |

All projects are subject to project study risk. There is no certainty or guarantee that a feasibility study, if undertaken, will be successfully concluded or that the project the subject of the study will satisfy Harmony’s economic, technical, risk and other criteria in order to progress that project to development.

A failure in our ability to discover new resources and reserves, enhance existing resources and reserves or develop new operations in sufficient quantities to maintain or grow the current level of our resources and reserves could negatively affect our results, financial condition and prospects.

The risk of unforeseen difficulties, delays or costs in implementing Harmony’s business strategy and projects may lead to Harmony not delivering the anticipated benefits of our strategy and projects. In addition, actual cash costs, capital expenditure, production and economic returns may differ significantly from those anticipated by feasibility studies for new development projects

The successful implementation of Harmony’s business strategy and projects depends upon many factors, including those outside our control. For example, the successful management of costs will depend on prevailing market prices for input costs. The ability to grow our business will depend on the successful implementation of our existing and proposed projects and continued exploration success, as well as on the availability of attractive acquisition opportunities, all of which are subject to the relevant mining and company specific risks as outlined in these risk factors.

It can take a number of years from the initial feasibility study until development of a project is completed and, during that time, the economic feasibility of production may change. In addition, there are a number of inherent uncertainties in developing and constructing an extension to an existing mine or a new mine, including:

| |

| • | availability and timing of necessary environmental and governmental permits; |

| |

| • | timing and cost of constructing mining and processing facilities, which can be considerable; |

| |

| • | availability and cost of skilled labor, power, water, fuel, mining equipment and other materials; |

| |

| • | accessibility of transportation and other infrastructure, particularly in remote locations; |

| |

| • | availability and cost of smelting and refining arrangements; |

| |

| • | availability of funds to finance construction and development activities; and |

| |

| • | spot and expected future commodity prices of metals including gold, silver, copper, uranium and molybdenum. |

All of these factors, and others, could result in our actual cash costs, capital expenditures, production and economic returns differing materially from those anticipated by feasibility studies.

Competition with other mining companies and individuals for specialized equipment, components and supplies necessary for exploration and development, for mining claims and leases on exploration properties and for the acquisition of mining assets also impact existing operations and potential new developments. Competitors may have greater financial resources, operational experience and technical capabilities - all of which could negatively affect the anticipated costs, which in turn could have a material adverse effect on our operating results and financial condition.

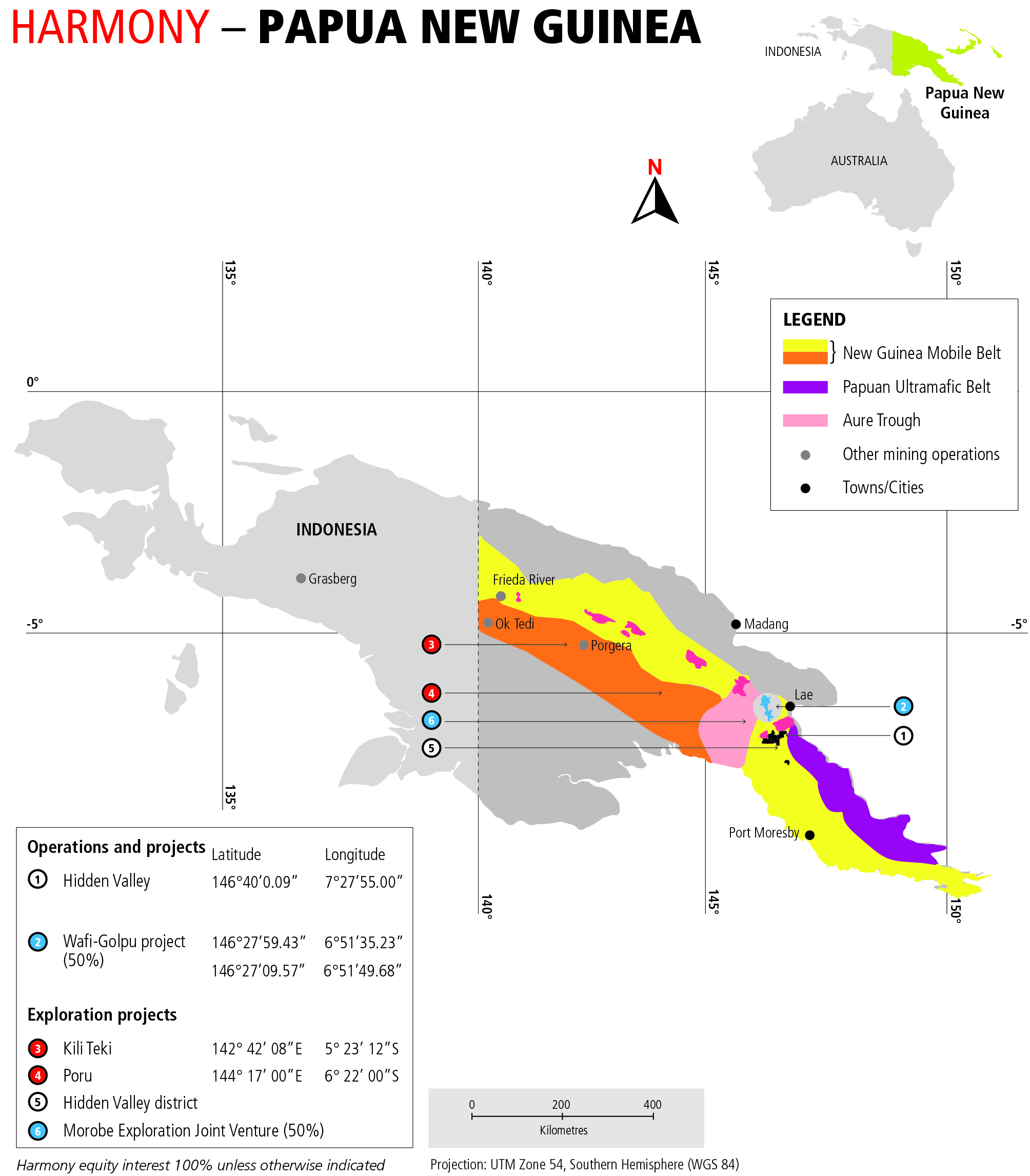

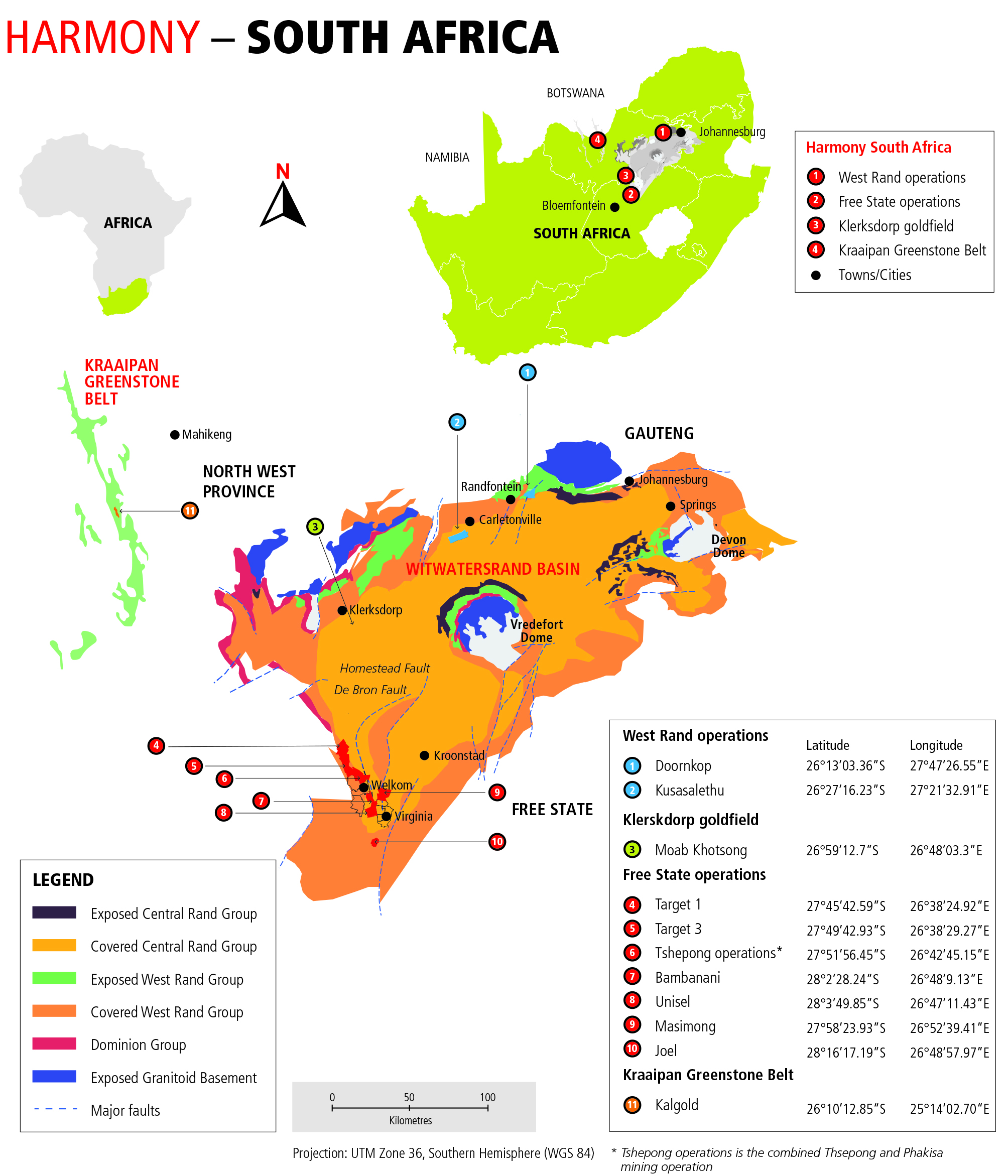

Harmony currently maintains a range of focused exploration programs, concentrating mainly on a number of prospective known gold and copper mineralized areas in the Independent State of Papua New Guinea (“PNG”) and the Kalgold open pit operation in South Africa. In order to maintain or expand our operations and reserve base, Harmony has sought, and may continue to seek to enter into joint ventures or to make acquisitions of selected precious metal producing companies or assets. For example, in 2018 Harmony acquired AngloGold Ashanti Limited’s Moab Khotsong and Great Noligwa mines together with other assets and related infrastructure (the "Moab Acquisition"). See below under "We may experience problems in identifying, financing and managing new acquisitions or other business combination transactions and integrating them with our existing operations. We may not have full management control over future joint venture partners". However, there is no assurance that any future development projects will extend the life of our existing mining operations or result in any new commercial mining operations. Unforeseen difficulties, delays or costs may adversely affect the successful implementation of our business strategy and projects, and such strategy and projects may not result in the anticipated benefits, which could have a material adverse effect on our results of operations, financial condition and prospects.

Risks associated with pumping water inflows from closed mines adjacent to our operations could adversely affect Harmony’s operational results

Certain of our mining operations are adjacent to the mining operations of other companies. A mine closure can affect continued operations at an adjacent mine if appropriate preventative steps are not taken. In particular, this could include the ingress of underground water when pumping operations at the closed mine are suspended. This can result in damage to property, operational disruptions and additional pumping costs, which could adversely affect any one of our adjacent mining operations and, in turn could adversely affect our business, operating results and financial condition.

With the Moab Acquisition, Harmony inherited a two-thirds interest in the Margaret Water Company for all pumping and water related infrastructure at its Margaret Water Shaft. The shaft operates for the purpose of de-watering the Klerksdorp, Orkney, Stilfontein, Hartbeesfontein ("KOSH") basin groundwater in order for Moab Khotsong operations and the mine operated by Kopanang Gold Mining Company Proprietary Limited (the mining company holding the remaining one–third interest in Margaret Water Company) (the only other mining company continuing operating) to remain dry and to prevent flooding of operational areas. Therefore it remains imperative for the shaft to continue pumping water. Flooding in the future resulting from a failure in pumping and water related infrastructure could pose an unpredicted "force majeure" type event, which could result in financial liability for us, and could have an adverse impact on our results of operations and financial condition.

Infrastructure constraints and aging infrastructure could adversely affect Harmony’s operations

Mining, processing, development and exploration activities depend on adequate infrastructure. Reliable rail, ports, roads, bridges, power sources, power transmission facilities and water supply are critical to the Company’s business operations and affect capital and operating costs. The infrastructure and services are often provided by third parties whose operational activities are outside the control of the Company.

Interference to the maintenance or provision of infrastructure, including by extreme weather conditions, sabotage or social unrest, could impede our ability to deliver products on time and adversely affect our business, results of operations and financial condition.

Once a shaft or a processing plant has reached the end of its intended lifespan, higher than normal maintenance and care is required. Maintaining this infrastructure requires skilled human resources, capital allocation, management and planned maintenance. Although Harmony has implemented a comprehensive maintenance strategy, incidents resulting in production delays, increased costs or industrial accidents may occur. Such incidents may have an adverse effect on Harmony’s operating results and financial condition.

Fluctuations in input production prices linked to commodities may adversely affect Harmony’s operational results and financial condition

Fuel, energy and consumables, including diesel, heavy fuel oil, chemical reagents, explosives, tires, steel and mining equipment consumed in mining operations, form a relatively large part of the operating costs and capital expenditure of a mining company. Harmony has no control over the costs of these consumables, many of which are linked to some degree to the price of oil and steel.

Fluctuations in oil and steel prices have a significant impact on operating cost and capital expenditure estimates and, in the absence of other economic fluctuations, could result in significant changes in the total expenditure estimates for new mining projects or render certain projects non-viable, either of which could have a material adverse effect on our business, operating results and financial condition.

Disruptions to the supply of electricity and increases in the cost of power may adversely affect our results of operations and financial condition

In South Africa, each of our mining operations depends on electrical power generated by the South African state utility, Eskom Limited ("Eskom"), which holds a monopoly in the South African market. Electricity supply in South Africa has been constrained over the past decade and there have been multiple power disruptions. Although the electricity supply in South Africa had improved prior to this year, Eskom began declaring load shedding in December 2018. The load shedding rose to Stage 4 (short of 4000 MW) in February 2019 and was reinstated in March 2019. Under Stage 4 load shedding, approximately 80% of the country’s demand is met through scheduled load shedding 12 times over a four-day period for two hours at a time, or twelve times over an eight-day period for four hours at a time. Eskom’s inability to fully meet the country’s demand has led and may continue to lead to rolling blackouts, unscheduled power cuts and surveillance programs to ensure non-essential lighting and electricity appliances are powered off. There is no assurance that Eskom’s efforts to protect the national electrical grid will prevent a complete national blackout.

Eskom's aging infrastructure, its need to replace or upgrade its power generation fleet and its deferral of routine maintenance due to financial constraints, may adversely affect electricity supply in South Africa. In addition, Eskom's ability to undertake necessary infrastructure and fleet upgrades, on commercially acceptable terms or otherwise, may be limited by the amount of debt it has outstanding, which has increased form R389 billion in fiscal 2018 to R441 billion on August 1, 2019. Any blackouts or other disruptions to power supply could have a material adverse effect on our business, operating results and financial condition.

Although management has been able to comply with the curtailment requirements in response to the load curtailment events experienced in our 2019 fiscal year and the first quarter of fiscal 2020 without incurring material production losses, there can be no guarantee that we will be able to comply with such curtailment requirements without incurring material production losses in the future. During the period of load shedding, Eskom used a significant amount of diesel to run its gas turbines and called on large power users to curtail their power demand. In addition, although Eskom applied to the National Energy Regulator of South Africa (“NERSA”), which regulates tariffs, for a 19.9% average increase in electricity tariffs for Eskom’s 2018 to 2019 financial year, NERSA granted Eskom a 5.2% electricity tariff increase for this period. Eskom has expressed concern that this increase may not be adequate to prevent future electricity interruptions and indicated that it intends to challenge NERSA’s decision not to grant the requested 19.9% tariff increase.

In addition to supply constraints, labor unrest in South Africa has before, and may in future, disrupt the supply of coal to power stations operated by Eskom, or the operation of the power stations directly, and result in curtailed supply. For example, in June 2018, during wage negotiations with the National Union of Mines ("NUM"), workers embarked on an illegal strike which resulted in power constraints and load curtailment. Despite the fact that Eskom has adopted a policy of asking households to reduce usage before asking industrial users to do so in order to reduce the economic impact of such disruptions, Eskom has warned that power constraints will continue.

In February 2019, the President of South Africa announced the vertical unbundling of Eskom. While full-state ownership will be maintained, the unbundling is expected to result in the separation of the Eskom’s generation, transmission and distribution functions into separate entities, which may require legislative and/or policy reform. It is expected that this process will take time to implement, causing continued poor reliability of the supply of electricity and an instability in prices and a possible tariff increase above inflation, which are expected to continue through the unbundling process. Should Harmony experience further power tariff increases, its business operating results and financial condition may be adversely impacted.

As mentioned above, although Eskom applied to NERSA for a 19.9% average increase in electricity tariffs for Eskom’s 2018/2019 financial year, NERSA granted Eskom a 5.2% electricity tariff increase for this period. In 2018, NERSA granted Eskom an additional 4.4% tariff increase adjustment from the Regulatory Clearing Account ("RCA") for the 2019/2020 financial year. As mentioned above, Eskom has indicated that it intends to challenge NERSA’s decision not to grant the requested 19.9% tariff increase and recently filed court papers to challenge the 4.4% tariff increase in the RCA ruling. In the same period, Eskom submitted their multi-year price determination application to NERSA for the 2018/2019 financial year to the 2021/2022 financial year, initially requesting 15% for these years. The application was later revised to 17%, 15% and 15% for the 2019/2020, 2020/2021 and 2021/2022 financial years, respectively. In March 2019, NERSA awarded Eskom tariff increases of 9.4% (effectively 13.8% when combined with the previously agreed 4.4% increase that comes into effect April 2019), 8.1% and 5.2%, for the 2019/2020, 2020/2021 and 2021/2022 financial years, respectively. NERSA also announced the approval of R3.869 billion from the RCA in costs incurred by Eskom over and above the previously regulated costs. The recovery period from the consumer is yet to be determined.

Eskom is also expected to submit to NERSA requests for three RCA applications for the 2014/2015, 2015/2016 and 2016/2017 fiscal years, amounting to nearly R66 billion. Should all three applications be granted and included in the tariff increase request in one year, this could result in approximately a 34% tariff increase. Should we experience further power tariff increases, our business operating results and financial condition may be adversely impacted.

PNG has limited power generation and distribution capacity, supplied by the state utility, PNG Power. This capacity is increasing but it is subject to disruptions in electrical power supply. Currently, Harmony mines and projects still partially or entirely rely on our own diesel-generated power. The cost of this power will fluctuate with changes in the oil price. Disruptions in electrical power supply or substantial increases in the cost of oil could have a material adverse effect on our business, operating results and financial condition.

Also, see Item 5:“Operating and Financial Review and Prospects - Electricity in South Africa.” and “Integrated Annual Report for the 20-F 2019 - Managing our Social and Environmental Impacts - Environmental management and stewardship” on pages 80 to 102.

We may experience problems in identifying, financing and managing new acquisitions or other business combination transactions and integrating them with our existing operations. We may not have full management control over future joint venture partners

In order to maintain or expand our operations and reserve base, Harmony has sought, and may continue to seek to enter into joint ventures or other business combination transactions or to make acquisitions of selected precious metal producing companies or assets. For example, in 2018 Harmony acquired AngloGold Ashanti Limited’s Moab Khotsong and Great Noligwa mines together with other assets and related infrastructure in the Moab Acquisition.

Acquiring new gold mining operations or entering into other business combination transactions involves a number of risks including:

| |

| • | our ability to identify appropriate assets for acquisition and/or to negotiate an acquisition or combination on favorable terms; |

| |

| • | obtaining the financing necessary to complete future acquisitions; |

| |

| • | difficulties in assimilating the operations of the acquired business; |

| |

| • | the changing regulatory environment as it relates to the Mining Charter (as defined below) and the general policy uncertainty in South Africa; |

| |

| • | difficulties in maintaining our financial and strategic focus while integrating the acquired business; |

| |

| • | problems in implementing uniform quality, standards, controls, procedures and policies; |

| |

| • | management capacity, and skills to supplement that capacity, to integrate new assets and operations; |

| |

| • | increasing pressures on existing management to oversee an expanding company; and |

| |

| • | to the extent we acquire mining operations or enter into another business combination transaction outside South Africa, Australia or PNG, encountering difficulties relating to operating in countries in which we have not previously operated. |

Any such acquisition or joint venture may change the scale of our business and operations and may expose us to new geographic, geological, political, social, operating, financial, legal, regulatory and contractual risks. Our ability to make successful acquisitions and any difficulties or time delays in achieving successful integration of any of such acquisitions could have a material adverse effect on our business, operating results and financial condition.

In addition, to the extent that Harmony participates in the development of a project through a joint venture or other multi-party commercial structure, there could be disagreements, legal or otherwise or divergent interests or goals among the parties, which could jeopardize the success of the project, particularly if Harmony does not have full management control over the joint venture. There can be no assurance that any joint venture will achieve the results intended and, as such, any joint venture could have a material adverse effect on our revenues, cash and other operating costs. See Item 5. "Operating and Financial Review and Prospects - Liquidity and Capital Resources - Investing."

Certain factors may affect our ability to support the carrying value of our property, plant and equipment, goodwill and other assets on our balance sheet, resulting in impairments

Harmony reviews and tests the carrying value of its assets when events or changes in circumstances suggest that this amount may not be recoverable and impairments may be recorded as a result of testing performed.

Our market capitalization on any reporting date is calculated on the basis of the price of our shares and ADSs on that date. Our shares and ADSs may trade in a wide range through the fiscal year depending on the changes in the market, including trader sentiment on various factors including gold price. Therefore, there may be times where our market capitalization is greater than the value of our net assets, or “book value”, and other times when our market capitalization is less than our book value. Where our market capitalization is less than our net asset or book value, this could indicate a potential impairment and we may be required to record an impairment charge in the relevant period.

At least on an annual basis for goodwill, and when there are indications that impairment of property, plant and equipment and other assets may have occurred, estimates of expected future cash flows for each group of assets are prepared in order to determine the recoverable amounts of each group of assets. These estimates are prepared at the lowest level at which identifiable cash flows are considered as being independent of the cash flows of other mining assets and liabilities. Expected future cash flows are inherently uncertain, and could materially change over time. Such cash flows are significantly affected by reserve and production estimates, together with economic factors such as spot and forward gold prices, discount rates, currency exchange rates, estimates of costs to produce reserves and future capital expenditures.

As at June 30, 2019, Harmony had substantial amounts of property, plant and equipment, goodwill and other assets on its consolidated balance sheets. Impairment charges of R3,898 million relating to property, plant and equipment and other assets were recorded in fiscal 2019. If management is required to recognize further impairment charges, this could affect Harmony’s results of operations and financial condition. See Item 5: “Operating and Financial Review and Prospects - Critical Accounting Policies and Estimates - Impairment of Property, Plant and Equipment” and “- Carrying Value of Goodwill.”

Given the nature of mining and the type of gold mines we operate, we face a material risk of liability, delays and increased cash costs of production from environmental and industrial accidents and pollution compliance breaches

The business of gold mining involves significant risks and hazards, including environmental hazards and industrial accidents. In particular, hazards associated with underground mining include:

| |

| • | cave-ins or fall-of-ground; |

| |

| • | discharges of gases and toxic chemicals; |

| |

| • | release of radioactive hazards; |

| |

| • | mining of pillars (integrity of shaft support structures may be compromised and cause increased seismicity); |

| |

| • | processing plant fire and explosion; |

| |

| • | critical equipment failures; |

| |

| • | accidents and fatalities; and |

| |

| • | other conditions resulting from drilling, blasting and the removal and processing of material from a deep-level mine. |

Hazards associated with opencast mining (also known as open-pit mining) include:

| |

| • | flooding of the open-pit; |

| |

| • | collapse of open-pit walls or slope failures; |

| |

| • | processing plant fire and explosion; |

| |

| • | accidents associated with operating large open-pit and rock transportation equipment; |

| |

| • | accidents associated with preparing and igniting of large-scale open-pit blasting operations; and |

| |

| • | major equipment failures. |

Hazards associated with construction and operation of waste rock dumps and tailings storage facilities include:

| |

| • | accidents associated with operating a waste dump and rock transportation; |

| |

| • | production disruptions caused by natural phenomena, such as floods and droughts and weather conditions, potentially exacerbated by climate change; |

| |

| • | dam, wall or slope failures; and |

| |

| • | contamination of ground or surface water. |

We are at risk from any or all of these environmental and industrial hazards. In addition, the nature of our mining operations presents safety risks. Harmony’s operations are subject to health and safety regulations, which could impose additional costs and compliance requirements. Harmony may face claims and liability for breaches, or alleged breaches, of such regulations and other applicable laws. The occurrence of any of these events could delay production, increase cash costs and result in financial liability to Harmony, which, in turn, may adversely affect our results of operations and our financial condition.

The nature of our mining operations presents safety risks

The environmental and industrial risks identified above also present safety risks for Harmony’s operations and our employees and could lead to the suspension and potential closure of operations for indeterminate periods. Safety risks, even in situations where no injuries occur, can have a material adverse effect on Harmony’s results of operations and financial condition. See Item 4: “Information on the Company - Business Overview - Regulation - Health and Safety - South Africa” and “Integrated Annual Report for the 20-F 2019 - Ensuring employee safety and well-being - maintaining stability in our workforce -Safety and health” on pages 33 to 49.

Illegal and artisanal mining, including theft of gold and copper bearing material, and other criminal activity at our operations could pose a threat to the safety of employees, result in damage to property and could expose the Company to liability

The activities of illegal and artisanal miners, which include theft and shrinkage, could cause damage to Harmony’s properties, including by way of pollution, underground fires, operational disruption, project delays or personal injury or death, for which Harmony could potentially be held responsible. Illegal and artisanal mining could result in the depletion of mineral deposits, potentially making the future mining of such deposits uneconomic.

Illegal and artisanal mining (which may be by employees or third parties) is associated with a number of negative impacts, including environmental degradation and human rights abuse. Effective local government administration is often lacking in the locations where illegal and artisanal miners operate because of rapid population growth and the lack of functioning structures, which can create a complex social and unstable environment.

Criminal activities such as trespass, illegal and artisanal mining, sabotage, theft and vandalism could lead to disruptions at certain of our operations.

Rising gold and copper prices may result in an increase in gold and copper thefts. The occurrence of any of these events could have a material adverse effect on Harmony’s financial condition on results of its operations.

Harmony’s insurance coverage may prove inadequate to satisfy future claims against it

Harmony has third-party liability coverage for most potential liabilities, including environmental liabilities. Harmony may be subject to liability for pollution (excluding sudden and accidental pollution) or other hazards against which we have not insured or cannot insure, including those for past mining activities. Harmony also maintains property and liability insurance consistent with industry practice, but this insurance contains exclusions and limitations on coverage. In addition, there can be no assurance that insurance will be available at economically acceptable premiums. As a result, Harmony’s insurance coverage may not cover the claims against it, including for environmental or industrial accidents or pollution, which could have a material adverse effect on Harmony’s financial condition.

Harmony’s operations may be negatively impacted by inflation

Harmony’s operations have been materially affected by inflation. Inflation in South Africa has fluctuated in a narrow band in recent years, remaining within or just outside the inflation range of 3% - 6% set by the South African Reserve Bank. At the end of fiscal 2017, 2018 and fiscal 2019, inflation was 5.1%, 4.4% and 4.5%, respectively. However, working costs, in particular electricity costs and wages have increased at a rate higher than inflation in recent years, resulting in significant cost pressures for the mining industry. See Item 5: "Operating and Financial Review and Prospects - Operating Results - Electricity in South Africa - Tariffs". Should Harmony experience further electricity or wage increases, its business, operating results and financial condition may be adversely impacted.

The inflation rate in PNG ended fiscal 2017 at 6.6% and 2018 at 4.7%, while the annualized inflation stood at 4.5% at the end of fiscal 2019.

Harmony’s results of operations, profits and financial condition could be adversely affected to the extent that cost inflation is not offset by devaluation in operating currencies or an increase in the price of gold.

The socio-economic framework in the regions in which Harmony operates may have an adverse effect on its operations and profits

Harmony has operations in South Africa and PNG. As a result, changes to or instability in the economic or political environment in either of these countries or in neighboring countries could affect an investment in Harmony. These risks could include terrorism, civil unrest, nationalization, political instability, change in legislative, regulatory or fiscal frameworks, renegotiation or nullification of existing contracts, leases, permits or other agreements, restrictions on repatriation of earnings or capital and changes in laws and policy, as well as other unforeseeable risks.

In PNG, a mining legislative review has been commissioned involving various PNG government agencies. The legislation being reviewed includes the PNG Mining Act 1992, PNG Mining (Safety) Act 1977 and applicable regulations. Mineral Policy and mining-specific sector policies including biodiversity offsets, offshore mining policy, sustainable development policy, involuntary relocation policy and mine closure policy, and the PNG government's right to acquire an interest in a mine discovery, the percentage extent of such right and the consideration payable for it, are also being reviewed. The Chamber of Mines and Petroleum of PNG, as the representative industry body, has been collating information from industry participants regarding the review of current legislation and policy and engaging with the PNG government as part of the response to the governments mining legislation review.

In 2014, the PNG Government instigated a review of the tax regime with a final report issued by the Tax Review Committee in October 2015. Pursuant to the tax regime review, certain adverse changes to the fiscal regime were introduced with effect from January 1, 2017, with the main changes being the introduction of an Additional Profit Tax, the cessation of the double deduction allowance for exploration expenditure, and an increase in the rates of interest withholding and dividend withholding taxes. Further changes, including a Capital Gains Tax, have been indicated to be introduced from 1 January 2020 and draft legislation has been issued for discussion. Harmony, via the Chamber of Mines, has submitted on aspects of the draft legislation.

It is difficult to predict the future political, social and economic environment in these countries, or any other country in which Harmony operates, and the impact government decisions may have on its business.

Actual and potential shortages of production inputs and supply chain disruptions may affect Harmony’s operations and profits

Harmony’s operational results may be affected by the availability and pricing of consumables such as fuel, chemical reagents, explosives, tires, steel and other essential production inputs. Issues with regards to availability of consumables may result from shortages, long lead times to deliver and supply chain disruptions, which could result in production delays and production shortfalls.

These shortages and delayed deliveries may also be experienced where industrial action affects Harmony’s suppliers. These issues could also affect the pricing of the consumables, especially if shortages are experienced. The price of consumables may be substantially affected by changes in global supply and demand, along with natural disasters such as earthquakes, climate change, extreme weather conditions, governmental controls, industrial action and other factors. A sustained interruption to the supply of any of these consumables would require Harmony to find acceptable substitute suppliers and could require it to pay higher prices for such materials. A sustained interruption might also adversely affect Harmony’s ability to pursue its development projects.

Any significant increase in the prices of these consumables would increase operating costs and adversely affect profitability, which could adversely affect our results of operations and our financial condition.

Harmony’s ability to service its debt will depend on its future financial performance and other factors

Harmony’s ability to service its debt depends on its financial performance, which in turn will be affected by its operating performance as well as by financial and other factors, and in particular the gold price, certain of which are beyond the control of the Company. Various financial and other factors may result in an increase in Harmony’s indebtedness, which could adversely affect the Company in several respects, including:

| |

| • | limiting its ability to access the capital markets; |

| |

| • | hindering its flexibility to plan for or react to changing market, industry or economic conditions; |

| |

| • | limiting the amount of cash flow available for future operations, acquisitions, dividends, or other uses, making it more vulnerable to economic or industry downturns, including interest rate increases; |

| |

| • | increasing the risk that it will need to sell assets, possibly on unfavorable terms, to meet payment obligations; or |

| |

| • | increasing the risk that it may not meet the financial covenants contained in its debt agreements or timely make all required debt payments. |

The occurrence of any of these events could adversely affect our results of operations and our financial condition.

Harmony’s ability to service its debt also depends on the amount of its indebtedness. In order to conclude the Moab Acquisition, Harmony increased its indebtedness. Harmony entered into a US$350 million three-year syndicated term and revolving facility in July 2017, of which US$295 million (R4,167 million) was drawn down and outstanding as of June 30, 2019. See Item 5: "Operating and Financial Review and Prospects - Liquidity and Capital Resources - Outstanding Credit Facilities and Other Borrowings".

In the near term, Harmony expects to manage its liquidity needs from cash generated by its operations, cash on hand, committed and underutilized facilities, as well as additional funding opportunities. However, if Harmony’s cost of debt were to increase or if it were to encounter difficulties in obtaining financing in the future, its sources of funding may not match its financing needs, which could have a material adverse effect on its business, operating results and financial condition.