File No. 333-

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON JUNE 10, 2009

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933 | x |

Pre-Effective Amendment No. | ¨ |

Post-Effective Amendment No. | ¨ |

EQ Advisors Trust

(Exact Name of Registrant as Specified in Charter)

1290 Avenue of the Americas

New York, New York 10104

(Address of Principal Executive Offices)

(212) 554-1234

(Registrant’s Area Code and Telephone Number)

STEVEN M. JOENK

AXA Equitable Life Insurance Company

1290 Avenue of the Americas

New York, New York 10104

(Name and Address of Agent for Service)

With copies to:

PATRICIA LOUIE, ESQ. AXA Equitable Life Insurance Company 1290 Avenue of the Americas New York, New York 10104 | CLIFFORD J. ALEXANDER, ESQ. MARK C. AMOROSI, ESQ. K&L Gates LLP 1601 K Street, NW Washington, DC 20006 |

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes effective.

It is proposed that this Registration Statement will become effective on the 30th day after filing pursuant to Rule 488 under the Securities Act of 1933, as amended.

Title of securities being registered: Class IA and Class IB shares of beneficial interest in the series of the registrant designated as the EQ/Common Stock Index Portfolio and the EQ/Small Company Index Portfolio.

No filing fee is required because the registrant is relying on Section 24(f) of the Investment Company Act of 1940, as amended, pursuant to which it has previously registered an indefinite number of shares (File Nos. 333-17217 and 811-07953).

EQ ADVISORS TRUST

CONTENTS OF REGISTRATION STATEMENT

This Registration Statement contains the following papers and documents:

Cover Sheet

Contents of Registration Statement

Letter to Shareholders

Notice of Special Meeting

Information Statement

Part A - Proxy Statement/Prospectus

Part B - Statement of Additional Information

Part C - Other Information

Signature Page

Exhibits

AXA EQUITABLE LIFE INSURANCE COMPANY

MONY LIFE INSURANCE COMPANY

MONY LIFE INSURANCE COMPANY OF AMERICA

1290 Avenue of the Americas

New York, New York 10104

July , 2009

Dear Contractholder:

Enclosed is a notice of a Special Meeting of Shareholders of each of the following Portfolios:

| • | EQ/Common Stock Index II Portfolio (formerly, the EQ/Oppenheimer Main Street Opportunity Portfolio) (the “Opportunity Portfolio”); and |

| • | EQ/Small Company Index II Portfolio (formerly, the EQ/Oppenheimer Main Street Small Cap Portfolio) (the “Small Cap Portfolio”) (together, the “Acquired Portfolios”). |

Each Acquired Portfolio is a portfolio of EQ Advisors Trust (the “Trust”). The Special Meeting of Shareholders of the Acquired Portfolios is scheduled to be held at the Trust’s offices, 1290 Avenue of the Americas, New York, New York 10104, on September 10, 2009 at 2:00 p.m., Eastern time (“Meeting”). At the Meeting, the shareholders of the Acquired Portfolios will be asked to approve the proposals described below.

The Trust’s Board of Trustees (“Board of Trustees”) has called the Meeting to request shareholder approval of the reorganization of each Acquired Portfolio into a corresponding series of the Trust (the “Acquiring Portfolios”) (the “Reorganizations”) as set forth below:

| • | the Opportunity Portfolio into the EQ/Common Stock Index Portfolio (“Common Stock Portfolio”); and |

| • | the Small Cap Portfolio into the EQ/Small Company Index Portfolio (“Small Company Index Portfolio”). |

The Board of Trustees has approved each of these proposals.

Each Acquired Portfolio and its corresponding Acquiring Portfolio have substantially similar investment objectives and substantially identical investment strategies. Each Portfolio is managed by AXA Equitable and sub-advised by one investment sub-adviser. In each case, if a Reorganization is approved and implemented, each Contractholder that invests indirectly in an Acquired Portfolio will automatically become a Contractholder that invests indirectly in the corresponding Acquiring Portfolio.

As an owner of an annuity contract or certificate and/or life insurance policy that participates in the Acquired Portfolios through the investment divisions of separate accounts established by AXA Equitable, MONY Life Insurance Company or MONY Life Insurance Company of America (each, an “Insurance Company”), you are entitled to instruct the applicable Insurance Company how to vote the Acquired Portfolio shares related to your interest in those accounts as of the close of business on June 30, 2009. The attached Notice of Special Meeting of Shareholders and Combined Proxy Statement and Prospectus concerning the Meeting describe the matters to be considered at the Meeting.

You are cordially invited to attend the Meeting. Since it is important that your vote be represented whether or not you are able to attend, you are urged to consider these matters and to exercise your voting instructions by completing, dating, signing, and returning the enclosed voting instruction card in the accompanying return envelope at your earliest convenience or by relaying your voting instructions via telephone or the Internet by following the enclosed instructions. Of course, we hope that you will be able to attend the Meeting, and if you wish, you may vote your shares in person, even though you may have already returned a voting instruction card or submitted your voting instructions via telephone or the Internet. Please respond promptly in order to save additional costs of proxy solicitation and in order to make sure you are represented.

| Very truly yours, |

Steven M. Joenk |

| President |

| AXA Funds Management Group |

| AXA Equitable Life Insurance Company |

EQ ADVISORS TRUST

EQ/Common Stock Index II Portfolio

EQ/Small Company Index II Portfolio

1290 Avenue of the Americas

New York, New York 10104

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON SEPTEMBER 10, 2009

To the Shareholders:

NOTICE IS HEREBY GIVEN that a Special Meeting of Shareholders of each of the following Portfolios, each of which is a portfolio of EQ Advisors Trust (the “Trust”), will be held on Thursday, September 10, 2009, at 2:00 p.m., Eastern time, at the offices of the Trust, located at 1290 Avenue of the Americas, New York, New York 10104 (the “Meeting”):

| • | EQ/Common Stock Index II Portfolio (formerly, the EQ/Oppenheimer Main Street Opportunity Portfolio) (the “Opportunity Portfolio”); and |

| • | EQ/Small Company Index II Portfolio (formerly, the EQ/Oppenheimer Main Street Small Cap Portfolio) (the “Small Cap Portfolio”) (together, the “Acquired Portfolios”). |

The Meeting will be held to act on the following proposals:

| 1. | To approve the Plan of Reorganization and Termination adopted by the Trust (the “Reorganization Plan”), which provides for the reorganization of the Opportunity Portfolio into the EQ/Common Stock Index Portfolio, also a series of the Trust. |

| 2. | To approve the Reorganization Plan, which provides for the reorganization of the Small Cap Portfolio into the EQ/Small Company Index Portfolio, also a series of the Trust. |

| 3. | To transact other business that may properly come before the meeting or any adjournment or postponement thereof. |

Please note that owners of variable life insurance policies or variable annuity contracts or certificates (“Contractholders”) issued by AXA Equitable, MONY Life Insurance Company or MONY Life Insurance Company of America (each, an “Insurance Company”) who have invested in shares of the Acquired Portfolios through the investment divisions of a separate account or accounts of an Insurance Company will be given the opportunity, to the extent required by law, to provide the applicable Insurance Company with voting instructions on the above proposals.

You should read the Combined Proxy Statement and Prospectus attached to this notice prior to completing your proxy or voting instruction card. The record date for determining the number of shares outstanding, the shareholders entitled to vote and the Contractholders entitled to provide voting instructions at the Meeting and any adjournment or postponement thereof has been fixed as the close of business on June 30, 2009. If you attend the Meeting, you may vote or give your voting instructions in person.

YOUR VOTE IS IMPORTANT

PLEASE RETURN YOUR PROXY CARD OR VOTING INSTRUCTION CARD PROMPTLY

Regardless of whether you plan to attend the Meeting, you should vote or give voting instructions by promptly completing, dating, signing, and returning the enclosed proxy or voting instruction card for the Portfolio in which you directly or indirectly own shares in the enclosed postage-paid envelope. You also can vote or provide voting instructions through the Internet or by telephone using the [12-digit control number] that appears on the enclosed proxy or voting instruction card and following the simple instructions. If you are present at the Meeting, you may change your vote or voting instructions, if desired, at that time. The Trust’s Board of Trustees recommends that you vote or provide voting instructions to vote FOR the proposals.

| By order of the Board of Trustees, |

| Patricia Louie |

| Vice President and Secretary |

July , 2009

New York, New York

AXA EQUITABLE LIFE INSURANCE COMPANY

MONY LIFE INSURANCE COMPANY

MONY LIFE INSURANCE COMPANY OF AMERICA

INFORMATION STATEMENT

REGARDING A SPECIAL MEETING OF SHAREHOLDERS OF

EQ/COMMON STOCK INDEX II PORTFOLIO

EQ/SMALL COMPANY INDEX II PORTFOLIO,

EACH A SERIES OF EQ ADVISORS TRUST,

TO BE HELD ON SEPTEMBER 10, 2009

DATED: JULY , 2009

GENERAL

This Information Statement is being furnished by AXA Equitable Life Insurance Company (“AXA Equitable”), MONY Life Insurance Company or MONY Life Insurance Company of America (each, an “Insurance Company” and together, the “Insurance Companies”), each of which is a stock life insurance company, to owners of their variable life insurance policies or variable annuity contracts or certificates (“Contracts”) (“Contractholders”) who, as of June 30, 2009 (“Record Date”), had net premiums or contributions allocated to the investment divisions of their separate accounts (“Separate Accounts”) that are invested in shares of one or more of the following Portfolios:

| • | EQ/Common Stock Index II Portfolio (formerly, the EQ/Oppenheimer Main Street Opportunity Portfolio) |

| • | EQ/Small Company Index II Portfolio (formerly, the EQ/Oppenheimer Main Street Small Cap Portfolio) (together, the “Acquired Portfolios”). |

Each Acquired Portfolio is a portfolio of EQ Advisors Trust (the “Trust”), a Delaware statutory trust that is registered with the Securities and Exchange Commission as an open-end management investment company.

To the extent required by law, each Insurance Company offers Contractholders the opportunity to instruct it, as the record owner of all of the shares of beneficial interest in the Acquired Portfolios (“Shares”) held by its Separate Accounts, as to how it should vote on the reorganization proposals (“Proposals”) to be considered at the Special Meeting of Shareholders of the Acquired Portfolios referred to in the preceding Notice and at any adjournment or postponement thereof (the “Meeting”). The enclosed Combined Proxy Statement and Prospectus, which you should retain for future reference, sets forth concisely information about the proposed reorganizations involving the Acquired Portfolios and corresponding series of the Trust that a Contractholder should know before completing the enclosed voting instruction card.

AXA Financial, Inc. is the parent company of each Insurance Company and is a wholly owned subsidiary of AXA, a French insurance holding company. The principal executive offices of AXA Financial, Inc. and each Insurance Company are located at 1290 Avenue of the Americas, New York, New York 10104.

This Information Statement and the accompanying voting instruction card are being mailed to Contractholders on or about July , 2009.

HOW TO INSTRUCT AN INSURANCE COMPANY

To instruct an Insurance Company as to how to vote the Shares held in the investment divisions of its Separate Accounts, Contractholders are asked to promptly complete their voting instructions on the enclosed voting instruction card(s); and sign, date and mail the voting instruction card(s) in the accompanying postage-paid envelope. Contractholders also may provide voting instructions by phone at 1-800- or by Internet at our website at .

If a voting instruction card is not marked to indicate voting instructions but is signed, dated and returned, it will be treated as an instruction to vote the Shares in favor of the Proposal(s).

i

The number of Shares held in the investment division of a Separate Account corresponding to an Acquired Portfolio for which a Contractholder may provide voting instructions was determined as of the Record Date by dividing (i) a Contract’s account value (minus any Contract indebtedness) allocable to that investment division by (ii) the net asset value of one Share of the Acquired Portfolio. At any time prior to an Insurance Company’s voting at the Meeting, a Contractholder may revoke his or her voting instructions with respect to that investment division by providing the Insurance Company with a properly executed written revocation of such voting instructions, properly executing later-dated voting instructions by a voting instruction card, telephone or the Internet, or appearing and voting in person at the Meeting.

HOW AN INSURANCE COMPANY WILL VOTE

An Insurance Company will vote the Shares for which it receives timely voting instructions from Contractholders in accordance with those instructions. An Insurance Company will vote Shares attributable to Contracts for which it is the Contractholder “FOR” each applicable Proposal. Shares in each investment division of a Separate Account for which an Insurance Company receives a voting instruction card that is signed, dated and timely returned but is not marked to indicate voting instructions will be treated as an instruction to vote the Shares in favor of the applicable Proposal. Shares in each investment division of a Separate Account for which an Insurance Company receives no timely voting instructions from Contractholders, or that are attributable to amounts retained by an Insurance Company as surplus or seed money, will be voted by the applicable Insurance Company either for or against approval of the Proposals, or as an abstention, in the same proportion as the Shares for which Contractholders (other than the Insurance Company) have provided voting instructions to the Insurance Company.

OTHER MATTERS

The Insurance Companies are not aware of any matters, other than the specified Proposals, to be acted on at the Meeting. If any other matters come before the Meeting, an Insurance Company will vote the Shares upon such matters in its discretion. Voting instruction cards may be solicited by employees of AXA Equitable or its affiliates as well as officers and agents of the Trust. The principal solicitation will be by mail but voting instructions may also be solicited by telephone, telegraph, fax, personal interview, the Internet or other permissible means.

If the necessary quorum to transact business is not established or the vote required to approve or reject a Proposal is not obtained at the Meeting, the persons named as proxies may propose one or more adjournments of the Meeting in accordance with applicable law to permit further solicitation of voting instructions. The persons named as proxies will vote in favor of such adjournment with respect to those Shares for which they received voting instructions in favor of a Proposal and will vote against any such adjournment those Shares for which they received voting instructions against a Proposal.

It is important that your Contract be represented. Please promptly mark your voting instructions on the enclosed voting instruction card; then sign, date and mail the voting instruction card in the accompanying postage-paid envelope. You may also provide your voting instructions by telephone at 1-800- or by Internet at our website at .

ii

COMBINED PROXY STATEMENT AND PROSPECTUS

July , 2009

EQ ADVISORS TRUST

EQ/Common Stock Index II Portfolio

EQ/Small Company Index II Portfolio

EQ/Common Stock Index Portfolio

EQ/Small Company Index Portfolio

1290 Avenue of the Americas

New York, New York 10104

1-877-222-2144

This Combined Proxy Statement and Prospectus (“Proxy Statement/Prospectus”) is being furnished to owners of variable life insurance policies or variable annuity contracts or certificates (“Contracts”) (“Contractholders”) issued by AXA Equitable Life Insurance Company (“AXA Equitable”), MONY Life Insurance Company or MONY Life Insurance Company of America (each, an “Insurance Company” and together, the “Insurance Companies”) who, as of June 30, 2009 (“Record Date”), had net premiums or contributions allocated to the investment divisions of an Insurance Company’s separate accounts (“Separate Accounts”) that are invested in shares of beneficial interest in one or more of the following Portfolios:

| • | EQ/Common Stock Index II Portfolio (formerly, the EQ/Oppenheimer Main Street Opportunity Portfolio) (the “Opportunity Portfolio”); and |

| • | EQ/Small Company Index II Portfolio (formerly, the EQ/Oppenheimer Main Street Small Cap Portfolio) (the “Small Cap Portfolio”) (each an “Acquired Portfolio” and together, the “Acquired Portfolios”) |

Each Acquired Portfolio is a portfolio of EQ Advisors Trust (the “Trust”), an open-end management investment company. This Proxy Statement/Prospectus also is being furnished to the Insurance Companies as the record owners of shares and to other shareholders that were invested in one or more of the Acquired Portfolios as of June 30, 2009. To the extent required by applicable law, Contractholders are being provided the opportunity to instruct the applicable Insurance Company to approve or disapprove the proposals contained in this Proxy Statement/Prospectus in connection with the solicitation by the Board of Trustees of the Trust (“Board”) of proxies to be used at the Special Meeting of Shareholders of the Acquired Portfolios to be held at 1290 Avenue of the Americas, New York, New York 10104, on Thursday, September 10, 2009, at 2:00 p.m., Eastern time, or any adjournment or postponement thereof (“Meeting”).

THE SEC HAS NOT APPROVED OR DISAPPROVED THE SECURITIES DESCRIBED IN THIS PROXY STATEMENT/PROSPECTUS OR DETERMINED IF THIS PROXY STATEMENT/PROSPECTUS IS ACCURATE OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

i

The proposals described in this Proxy Statement/Prospectus are as follows:

Proposal | Shareholders Entitled to Vote | |||

| 1. | To approve the Plan of Reorganization and Termination adopted by the Trust (the “Reorganization Plan”), which provides for the reorganization of the Opportunity Portfolio into the EQ/Common Stock Index Portfolio (the “Common Stock Portfolio”), each a series of the Trust. | Shareholders of the Opportunity Portfolio. | ||

| 2. | To approve the Reorganization Plan, which provides for the reorganization of the Small Cap Portfolio into the EQ/Small Company Index Portfolio (“Small Company Index Portfolio”), each a series of the Trust. | Shareholders of the Small Cap Portfolio. | ||

Each reorganization referred to in Proposals 1 and 2 above is referred to herein as a “Reorganization” and together as the “Reorganizations.” The Common Stock Portfolio and Small Company Index Portfolio are referred to herein together as the “Acquiring Portfolios” and individually as an “Acquiring Portfolio.” Each Acquired Portfolio and Acquiring Portfolio is sometimes referred to herein as a “Portfolio.” The consummation of one Reorganization is not contingent on the consummation of the other Reorganization.

This Proxy Statement/Prospectus, which you should retain for future reference, contains important information regarding the proposals that you should know before voting or providing voting instructions. Additional information about the Trust has been filed with the Securities and Exchange Commission (“SEC”) and is available upon oral or written request without charge. This Proxy Statement/Prospectus is being provided to the Insurance Companies and mailed to Contractholders and other shareholders as of the Record Date on or about July , 2009. It is expected that one or more representatives of each Insurance Company will attend the Meeting in person or by proxy and will vote shares held by the Insurance Company in accordance with voting instructions received from its Contractholders and in accordance with voting procedures established by the Trust.

The following documents have been filed with the SEC and are incorporated by reference into this Proxy Statement/Prospectus:

| 1. | The Prospectus and Statement of Additional Information of the Trust, each dated May 1, 2009, as supplemented, with respect to the Acquired Portfolios (File Nos. 333-17217 and 811-07953); |

| 2. | The Annual Report to Shareholders of the Trust with respect to the Acquired Portfolios for the fiscal year ended December 31, 2008 (File Nos. 333-17217 and 811-07953); and |

| 3. | The Statement of Additional Information dated July , 2009, relating to the Reorganizations (File No. 333- ). |

For a free copy of any of the above documents, please call or write the Trust at the phone number below or the above address.

Shareholders and Contractholders can find out more about the Acquired Portfolios in the Trust’s Annual Report listed above, which has been furnished to shareholders and Contractholders. You may obtain a copy of the Annual Report, free of charge, by writing to the Trust at the above address or by calling 1-877-222-2144.

The Trust is subject to the informational requirements of the Securities Exchange Act of 1934, as amended. Accordingly, it must file certain reports and other information with the SEC. You can copy and review information about the Trust at the SEC’s Public Reference Room in Washington, DC, and at certain of the following SEC Regional Offices: New York Regional Office, 3 World Financial Center, Suite 400, New York, New York 10281; Miami Regional Office, 801 Brickell Avenue, Suite 1800, Miami, Florida 33131; Chicago Regional Office, 175 W. Jackson Boulevard, Suite 900, Chicago, Illinois 60604; Denver Regional Office, 1801 California Street, Suite 1500, Denver, Colorado 80202; Los Angeles Regional Office, 5670 Wilshire Boulevard, 11th Floor, Los Angeles,

ii

California 90036; Boston Regional Office, 33 Arch Street, 23rd Floor, Boston, MA 02110; Philadelphia Regional Office, The Mellon Independence Center, 701 Market Street, Philadelphia, PA 19106; Atlanta Regional Office, 3475 Lenox Road, N.E., Suite 1000, Atlanta, GA 30326; Fort Worth Regional Office, Burnett Plaza, Suite 1900, 801 Cherry Street, Unit 18, Fort Worth, TX 76102; Salt Lake Regional Office, 15 W. South Temple Street, Suite 1800, Salt Lake City, UT 84101; San Francisco Regional Office, 44 Montgomery Street, Suite 2600, San Francisco, CA 94104. You may obtain information on the operation of the Public Reference Room by calling the SEC at (202) 551-8090. Reports and other information about the Trust are available on the IDEA Database on the SEC’s Internet site at http://www.sec.gov. You may obtain copies of this information from the SEC’s Public Reference Branch, Office of Consumer Affairs and Information Services, Washington, DC 20549, at prescribed rates.

iii

iv

This Proxy Statement/Prospectus is soliciting shareholders with amounts invested in one or more of the Acquired Portfolios as of the Record Date to approve the Reorganization Plan, whereby each Acquired Portfolio will be reorganized into the corresponding Acquiring Portfolio.

You should read this entire Proxy Statement/Prospectus carefully. For additional information, you should consult the Reorganization Plan, a copy of which is attached hereto as Appendix A.

On May 18, 2009, OppenheimerFunds, Inc. (“Oppenheimer”), the then-current investment sub-adviser (the “Adviser”) to the Acquired Portfolios, informed AXA Equitable that it had retained a new portfolio management team to manage the Acquired Portfolios and that the new portfolio management team proposed to utilize a new investment strategy to manage the Portfolios. AXA Equitable then commenced a review of the changes to the portfolio management team and the proposed investment strategy changes for the Acquired Portfolios. Based on its analysis of the changes to the portfolio management team, the proposed new investment style, process and other information, and a review of various alternatives for the Acquired Portfolios, AXA Equitable determined that it would be in the best interests of each Acquired Portfolio to (1) terminate the then-current Investment Advisory Agreement between AXA Equitable and Oppenheimer with respect to the Acquired Portfolios, (2) restructure the Portfolios as passive investment portfolios that seek to track the performance of their respective benchmarks (before deduction of portfolio fees and expenses), and (3) reorganize each Portfolio into another substantially identical passively managed portfolio offered by the Trust, rather than implement the changes proposed by Oppenheimer, appoint new Advisers to attempt to replicate the investment strategies of the Portfolios’ former portfolio management team or other alternatives. In connection with the restructuring of the Acquired Portfolios as index portfolios, AXA Equitable also determined that it would be appropriate to (1) reduce its management fee rate for managing the Acquired Portfolios to reflect the change from an active to a passive investment strategy and (2) appoint AllianceBernstein L.P. (“AllianceBernstein”) to manage the Acquired Portfolios on an interim basis using the new passive investment strategy for the Acquired Portfolios pending shareholder approval of the proposed Reorganizations.

In connection with its review of the Acquired Portfolios, AXA Equitable considered a variety of factors, including Oppenheimer’s proposed changes to the Acquired Portfolios as well as the continued viability of each Acquired Portfolio as a stand-alone investment option given that each Acquired Portfolio had failed to attract significant investor interest, had a relatively small asset base and was unlikely to attract significant new cash flow. AXA Equitable also considered that the Acquired Portfolios, as index-fund portfolios, would hold hundreds of equity securities as part of their investment strategies, which is consistent with the investment strategies of the Portfolios under the prior management of the former Oppenheimer management team. AXA Equitable also considered that, after converting to a passive investment strategy, the Acquired Portfolios would be substantially identical to other Portfolios of the Trust (namely, the corresponding Acquiring Portfolios) with respect to their investment policies, strategies and principal risks, and that the Reorganizations would be beneficial to the shareholders invested in the Acquired Portfolios because each Reorganization would provide a means by which Contractholders with amounts allocated to an Acquired Portfolio could pursue substantially similar investment objectives in the context of a larger fund with the potential for better growth prospects and lower expenses through greater economies of scale.

AXA Equitable informed the Trust’s Board of Trustees of the changes at Oppenheimer and of its ongoing review of the Acquired Portfolios at a Board meeting held on May 21, 2009. At a subsequent Board meeting on June 2, 2009, AXA Equitable recommended the proposals described above and certain related matters. At that meeting, the Board, including the Trustees who are not “interested persons” of the Portfolios (as that term is defined in Section 2(a)(19) of the 1940 Act) (the “Independent Trustees”), unanimously approved (1) the termination of the then-current Investment Advisory Agreement between Oppenheimer and AXA Equitable with respect to the Acquired Portfolios, (2) the restructuring of each Acquired Portfolio as an index portfolio that seeks to track its benchmark (before deduction of portfolio fees and expenses), (3) a reduction in the investment management fee payable to AXA Equitable by each Acquired Portfolio to reflect the change in each Acquired Portfolio’s investment policies and strategies from active to passive management, (4) an Interim Investment Advisory Agreement between AXA Equitable and AllianceBernstein (the “Interim Agreement”) with respect to the Acquired Portfolios under which AllianceBernstein would serve as the interim Adviser to each Acquired Portfolio, and (5) the Reorganization Plan (and the solicitation of shareholders of each Acquired Portfolio to approve the Reorganization Plan) under which each Acquired Portfolio would reorganize into the corresponding Acquiring Portfolio. Additional information regarding the Board’s consideration of the Reorganizations is included in the section entitled “Board Considerations” below.

1

The changes to the investment policies and strategies of each Acquired Portfolio, the reduction in the investment management fees payable by each Acquired Portfolio to AXA Equitable, and the Interim Agreement took effect on June 8, 2009. The Interim Agreement was approved and implemented with respect to each Acquired Portfolio without shareholder approval in accordance with Rule 15a-4 under the 1940 Act and will terminate 150 days after its effective date. Subject to shareholder approval, the Reorganizations are expected to be effective at the close of business on September , 2009, or on a later date the Trust decides upon (“Closing Date”).

The Reorganizations

Each Acquired Portfolio’s shares are divided into two classes, designated Class IA and Class IB shares (“Acquired Portfolio Shares”). Each Acquiring Portfolio’s shares also are divided into two classes, designated Class IA and Class IB shares (“Acquiring Portfolio Shares”). The rights and preferences of each class of Acquiring Portfolio Shares are identical to the corresponding class of Acquired Portfolio Shares.

The Reorganization Plan provides for, with respect to each Reorganization:

| • | the transfer of all of the assets of the Acquired Portfolio to the corresponding Acquiring Portfolio in exchange for Acquiring Portfolio Shares having an aggregate net asset value equal to the Acquired Portfolio’s net assets; |

| • | the Acquiring Portfolio’s assumption of all the liabilities of the Acquired Portfolio; |

| • | the distribution to the shareholders (for the benefit of the Separate Accounts, as applicable, and thus the Contractholders) of those Acquiring Portfolio Shares; and |

| • | the complete termination of the Acquired Portfolio. |

Each Acquired Portfolio has substantially similar investment objectives and substantially identical investment policies and principal risks as its corresponding Acquiring Portfolio. A comparison of the investment objective(s), investment policies, strategies and principal risks of each Acquired Portfolio and its corresponding Acquiring Portfolio is included in “Comparison of Investment Objectives, Policies and Strategies” and “Comparison of Principal Risk Factors” below. The Portfolios have identical distribution procedures, purchase procedures, exchange rights and redemption procedures, as discussed in “Additional Information about the Portfolios” below. Each Portfolio offers its shares to Separate Accounts and certain other eligible investors. Shares of each Portfolio are offered and redeemed at their net asset value without any sales load. You will not incur any sales loads or similar transaction charges as a result of a Reorganization.

Subject to shareholder approval, each Reorganization is expected to be effective at the close of business on the Closing Date. As a result of each Reorganization, each shareholder invested in shares of one or more of the Acquired Portfolios would become an owner of shares of the corresponding Acquiring Portfolio. Each such shareholder would hold, immediately after the Closing Date, Class IA or Class IB shares of the applicable Acquiring Portfolio having an aggregate value equal to the aggregate value of the Class IA or Class IB Acquired Portfolio Shares, as applicable, that were held by the shareholder as of the Closing Date. Similarly, each Contractholder whose Contract values are invested in shares of one or more of the Acquired Portfolios would become an indirect owner of shares of the corresponding Acquiring Portfolio. Each such Contractholder would indirectly hold, immediately after the Closing Date, Class IA or Class IB shares of the applicable Acquiring Portfolio having an aggregate value equal to the aggregate value of the Class IA or Class IB Acquired Portfolio Shares, as applicable, that were indirectly held by the Contractholder as of the Closing Date. The consummation of one Reorganization is not contingent on the consummation of the other Reorganization. The Trust believes that there will be no adverse tax consequences to shareholders or Contractholders as a result of the Reorganizations. Please see “Additional Information about the Reorganizations – Federal Income Tax Consequences of the Reorganizations” below for further information.

2

The Board has unanimously approved the Reorganization Plan with respect each Reorganization. Accordingly, the Board is submitting the Reorganization Plan for approval by each Acquired Portfolio’s shareholders. In considering whether to approve a proposal (a “Proposal”), you should review the Proposal for the Acquired Portfolio(s) in which you were a direct or indirect holder on the Record Date. In addition, you should review the information in this Proxy Statement/Prospectus that relates to all of the Proposals and the Reorganization Plan generally. The Board recommends that you vote “FOR” the Proposals to approve the Reorganization Plan.

| PROPOSAL 1: | APPROVAL OF THE REORGANIZATION PLAN WITH RESPECT TO THE REORGANIZATION OF THE OPPORTUNITY PORTFOLIO INTO THE COMMON STOCK INDEX PORTFOLIO. |

This Proposal 1 requests your approval of the Reorganization Plan, pursuant to which the Opportunity Portfolio will be reorganized into the Common Stock Portfolio.

In considering whether you should approve this Proposal, you should note that:

| • | The Opportunity Portfolio and Common Stock Portfolio have substantially similar investment objectives and substantially identical investment policies and principal risks. Below is a summary comparison of the two Portfolios. For a detailed comparison of the each Portfolio’s investment objectives, policies, strategies and risks, see “Comparison of Investment Objectives, Policies and Strategies” and “Comparison of Principal Risk Factors” below. |

• | The Opportunity Portfolio’s investment objective is to seek to achieve long-term capital appreciation. The Common Stock Portfolio’s investment objective is to seek to achieve a total return before expenses that approximates the total return performance of the Russell 3000® Index (the “Russell 3000”), including reinvestment of dividends, at a risk level consistent with that of the Russell 3000. The Russell 3000 is an unmanaged index that measures the performance of the 3,000 largest U.S. companies based on total market capitalizations, which represents approximately 98% of the investable U.S. equity market. Under normal circumstances, each Portfolio invests at least 80% of its net assets, plus borrowings for investment purposes, in common stocks of companies represented in the Russell 3000. The investment objectives of the Portfolios are substantially similar in that each Portfolio seeks to achieve capital appreciation through an investment in the equity securities of large-cap companies. Each Portfolio’s investments are selected by using a stratified sampling construction process in which the Adviser selects a subset of the 3,000 companies in the Russell 3000. Each Portfolio also may invest, to a limited extent, in derivatives and investment company securities, such as exchange-traded funds (“ETFs”) and up to 20% of the value of its total assets in futures contracts and options on futures contracts whose return depends on stock market prices. |

| • | Each Portfolio is subject to adviser selection risk, asset class risk, derivatives risk, equity risk, ETFs risk, futures and options risk, index-fund risk, market risk, small- and mid-cap company risk, large-cap company risk, portfolio management risk, securities lending risk, security risk and security selection risk as principal risks. For a detailed description of the investment objectives, policies, and strategies and principal risks of each Portfolio, please see “Comparison of Investment Objectives, Policies and Strategies” and “Comparison of Principal Risk Factors” below. |

| • | AXA Equitable (“Manager”) serves as the investment manager and administrator for each Portfolio and would continue to manage and administer the Common Stock Portfolio after the Reorganization. AXA Equitable has received an exemptive order from the SEC that generally permits AXA Equitable and the Board to appoint, dismiss and replace each Portfolio’s investment sub-adviser(s) (each, an “Adviser”) and to amend the advisory agreements between AXA Equitable and the Advisers without obtaining shareholder approval. AXA Equitable has appointed AllianceBernstein to manage the assets of each Portfolio. For a detailed description of the Manager and the Portfolios’ Adviser, please see “Additional Information about the Portfolios—The Manager” and “- The Advisers” below. |

3

| • | The Opportunity Portfolio and Common Stock Portfolio had net assets of approximately $35.48 million and $4.20 billion, respectively, as of December 31, 2008. Thus, if the Reorganization had been in effect on that date, the combined Portfolio would have had net assets of approximately $4.24 billion. |

| • | Class IA shareholders of the Opportunity Portfolio will receive Class IA shares of the Common Stock Portfolio, and Class IB shareholders of the Opportunity Portfolio will receive Class IB shares of the Common Stock Portfolio, pursuant to the Reorganization. Shareholders will not pay any sales charges in connection with the Reorganization. Please see “Comparative Fee and Expense Tables,” “Additional Information about the Reorganizations” and “Additional Information about the Portfolios” below for more information. |

| • | It is estimated that the annual operating expense ratios for the Common Stock Portfolio’s Class IA and Class IB shares, immediately following the Reorganization, will be lower than those of the Opportunity Portfolio’s Class IA and Class IB shares, respectively, for the last fiscal year, before and after taking into account an expense limitation arrangement that is in effect for the Opportunity Portfolio and after taking into account the restatement of fees of each Portfolio to reflect current fees. For a more detailed comparison of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the Portfolios” below. |

| • | The management fee for each Portfolio is the same and is equal to an annual rate of 0.35% of the Portfolio’s average daily net assets. |

| • | The administration fee schedule is the same for each Portfolio. Each Portfolio pays $30,000 per year, plus its proportionate share of the Trust’s administration fee for portfolios with a single Adviser, which is equal to an annual rate of 0.12% of the first $3 billion of the Trust’s total average daily net assets (exclusive of certain portfolios), 0.11% of the next $3 billion, 0.105% of the next $4 billion, 0.10% of the next $20 billion and 0.0975% thereafter. For a more detailed description of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the Portfolios” below. |

| • | Following the Reorganization, the combined Portfolio will be managed in accordance with the investment objective, policies and strategies of the Common Stock Portfolio. In connection with the changes made to the Acquired Portfolio’s investment policies and strategies, as described in the “Summary” section above, AXA Equitable and AllianceBernstein restructured the Acquired Portfolio’s holdings to pursue its new investment policies and strategies, which are substantially identical to those of the Common Stock Portfolio. AXA Equitable has reviewed the Opportunity Portfolio’s current portfolio holdings and has determined that the holdings generally are compatible with the Common Stock Portfolio’s investment objective and policies. Thus, AXA Equitable believes that, if the Reorganization is approved, all or virtually all of the holdings of the Opportunity Portfolio could be transferred to and held by the Common Stock Portfolio. However, it is expected that some of those holdings may not remain at the time of the Reorganization due to normal portfolio turnover. It is also expected that, if a Reorganization is approved, any holdings of the Opportunity Portfolio involved therein that are not compatible with the Common Stock Portfolio’s investment objective and policies will be liquidated in an orderly manner in connection with the Reorganization, and the proceeds of these sales held in temporary investments or reinvested in assets that are consistent with that investment objective and policies. The portion of the Opportunity Portfolio’s assets that will be liquidated in connection with the Reorganization will depend on market conditions and on the assessment by AXA Equitable and the Common Stock Portfolio’s Adviser of the compatibility of those holdings with the Common Stock Portfolio’s portfolio composition and investment objective and policies at the time of the Reorganization. The need for the Opportunity Portfolio to sell investments in connection with the Reorganization may result in its selling securities at a disadvantageous time and price and could result in its realizing gains (or losses) that would not otherwise have been realized and incurring transaction costs that would not otherwise have been incurred. |

| • | AXA Equitable will bear the Reorganization Expenses (as defined in the Reorganization Plan), which include the costs associated with the preparation and distribution of this Proxy Statement/Prospectus and with obtaining |

4

shareholder approval of the Reorganization, but exclude brokerage and similar expenses in connection with the Reorganization, which will be borne by the Portfolios. Please see “Additional Information about the Reorganizations” below for more information. |

Comparison of Investment Objectives, Policies and Strategies

The following table compares the investment objectives and principal investment policies and strategies of the Opportunity Portfolio with those of the Common Stock Portfolio. The Board may change the investment objective of a Portfolio without a vote of the Portfolio’s shareholders.

Acquiring Portfolio | Acquired Portfolio | |

Common Stock Portfolio | Opportunity Portfolio | |

| Investment Objective | ||

| Seeks to achieve a total return before expenses that approximates the total return performance of the Russell 3000, including reinvestment of dividends, at a risk level consistent with that of the Russell 3000. | Seeks to achieve long-term capital appreciation. | |

| Principal Investment Strategies | ||

| Under normal circumstances, the Portfolio invests at least 80% of its net assets, plus borrowings for investment purposes, in common stocks of companies represented in the Russell 3000. | Same. | |

| The Portfolio also may invest in securities and other instruments, such as futures contracts and options on futures contracts whose return depends on stock market prices. The Adviser selects these instruments to attempt to match the total return of the Russell 3000 but may not always do so. The contract value of the futures contracts purchase by the Portfolio plus the contract value of futures contracts underlying call options purchased by the Portfolio will not exceed 20% of the Portfolio’s total assets. | Same. | |

| The Portfolio may invest in investment company securities, such as ETFs, where appropriate futures contracts do not exist or if the Adviser deems advisable for other reasons, such as to gain exposure to certain sectors or securities that are represented by ownership in ETFs. | Same. | |

| The Portfolio’s investments are selected by a stratified sampling construction process in which the Adviser selects a subset of the 3,000 companies in the Russell 3000 based on the Adviser’s analysis of key risk factors and other characteristics such as industry weightings, market capitalizations, return variability and yield. | Same. | |

5

Comparison of Principal Risk Factors

Risk is the chance that you will lose money on your investment or that it will not earn as much as you expect. In general, the greater the risk, the more money your investment can earn for you and the more you can lose. Like other investment companies, the value of each Portfolio’s shares may be affected by its investment objective, principal investment strategies and particular risk factors. Consequently, each Portfolio may be subject to different principal risks. Some of the principal risks of investing in the Portfolios are noted below. However, other factors may also affect each Portfolio’s net asset value. There is no guarantee that a Portfolio will achieve its investment objective or that it will not lose principal value. The following table compares the principal risks of an investment in each Portfolio. For an explanation of each such risk, see “Additional Information about the Reorganizations – Description of Risk Factors” below.

Risks | Common Stock Portfolio | Opportunity Portfolio | ||

Adviser Selection Risk | X | X | ||

Asset Class Risk | X | X | ||

Derivatives Risk | X | X | ||

Equity Risk | X | X | ||

ETFs Risk | X | X | ||

Futures and Options Risk | X | X | ||

Index-Fund Risk | X | X | ||

Large-Cap Company Risk | X | X | ||

Market Risk | X | X | ||

Portfolio Management Risk | X | X | ||

Securities Lending Risk | X | X | ||

Security Risk | X | X | ||

Security Selection Risk | X | X | ||

Small- and Mid-Cap Company Risk | X | X | ||

Comparative Fee and Expense Tables

The following tables show the fees and expenses of each class of shares of each Portfolio and the estimated pro forma fees and expenses of each class of shares of the Acquiring Portfolio after giving effect to the proposed Reorganization. Fees and expenses for each Portfolio are based on those incurred by each class of its shares for the last fiscal year ended December 31, 2008, as adjusted to reflect the current fees for each Portfolio. The pro forma fees and expenses of the Acquiring Portfolio Shares assume that the Reorganization has been in effect for the last year ended on that date. There are no fees or charges to buy or sell shares of either Portfolio, reinvest dividends or exchange into other portfolios. The tables do not reflect any Contract-related fees and expenses, which would increase overall fees and expenses.

6

Annual Operating Expenses

(expenses that are deducted from Portfolio assets)

| Opportunity Portfolio | Common Stock Portfolio | Pro Forma Common Stock Portfolio (assuming the Reorganization is approved) | ||||||||||||||||

| Class IA | Class IB | Class IA | Class IB | Class IA | Class IB | |||||||||||||

Management Fee† | 0.35 | % | 0.35 | % | 0.35 | % | 0.35 | % | 0.35 | % | 0.35 | % | ||||||

Distribution and/or Service Fees (12b-1 fees)†† | None | 0.25 | % | None | 0.25 | % | None | 0.25 | % | |||||||||

Other Expenses | 0.68 | % | 0.68 | % | 0.11 | % | 0.11 | % | 0.11 | % | 0.11 | % | ||||||

Total Annual Portfolio Operating Expenses | 1.03 | % | 1.28 | % | 0.46 | % | 0.71 | % | 0.46 | % | 0.71 | % | ||||||

Less Fee Waiver/Expense Reimbursement* | -0.43 | % | -0.43 | % | N/A | N/A | N/A | N/A | ||||||||||

Net Annual Portfolio Operating Expenses | 0.60 | % | 0.85 | % | 0.46 | % | 0.71 | % | 0.46 | % | 0.71 | % | ||||||

| † | The management fee for each Portfolio has been restated to reflect the current fee. |

| †† | The maximum annual distribution and/or service (12b-1) fee for a Portfolio’s Class IB shares is 0.50% of the average daily net assets attributable to the Portfolio’s Class IB shares. Under an arrangement approved by the Trust’s Board of Trustees, the distribution and/or service (12b-1) fee currently is limited to 0.25% of the average daily net assets attributable to a Portfolio’s Class IB shares. This arrangement will be in effect at least until April 30, 2010. |

| * | Pursuant to a contract, the Manager has agreed to make payments or waive its management, administrative and other fees to limit the expenses of the Opportunity Portfolio through April 30, 2010 (unless the Board of Trustees consents to an earlier revision or termination of the arrangement) so that the Annual Portfolio Operating Expenses of the Opportunity Portfolio (exclusive of taxes, interest, brokerage commissions, capitalized expenses, fees and expenses of other investment companies in which the Portfolio invests and extraordinary expenses) do not exceed the amount shown above under Net Annual Portfolio Operating Expenses. The Manager may be reimbursed the amount of any such payments and waivers in the future, provided that the payments or waivers are reimbursed within three years of the payment or waiver being made and the combination of the Opportunity Portfolio’s expense ratio and such reimbursements do not exceed the Opportunity Portfolio’s expense cap. If the actual expense ratio is less than the expense cap and the Manager has recouped all eligible previous payments made, the Opportunity Portfolio will be charged such lower expenses. The Manager may discontinue these arrangements at any time after April 30, 2010. |

This example is intended to help you compare the costs of investing in the Portfolios with the cost of investing in other investment options. The example assumes that:

| • | You invest $10,000 in a Portfolio for the time periods indicated; |

| • | Your investment has a 5% return each year; |

| • | The Portfolio’s operating expenses remain the same; and |

| • | If applicable, the expense limitation currently in effect is not renewed. |

7

This example should not be considered a representation of past or future expenses of the Portfolios. Actual expenses may be higher or lower than those shown. The costs in the example would be the same whether or not you redeemed all of your shares at the end of these periods. This example does not reflect any Contract-related fees and expenses, including redemption fees (if any) at the Contract level. If such fees and expenses were reflected, the total expenses would be substantially higher. Similarly, the annual rate of return assumed in the example is not an estimate or guarantee of future investment performance. Based on these assumptions, your costs would be:

| Opportunity Portfolio | Common Stock Portfolio | Pro Forma Common Stock Portfolio (assuming the Reorganization is approved) | ||||||||||||||||

| Class IA | Class IB | Class IA | Class IB | Class IA | Class IB | |||||||||||||

1 Year | $ | 61 | $ | 87 | $ | 47 | $ | 73 | $ | 47 | $ | 73 | ||||||

3 Years | $ | 285 | $ | 363 | $ | 148 | $ | 227 | $ | 148 | �� | $ | 227 | |||||

5 Years | $ | 527 | $ | 661 | $ | 258 | $ | 395 | $ | 258 | $ | 395 | ||||||

10 Years | $ | 1,220 | $ | 1,507 | $ | 579 | $ | 883 | $ | 579 | $ | 883 | ||||||

Comparative Performance Information

The bar charts below illustrate each Portfolio’s annual total returns for the calendar years indicated and give some indication of the risks of investing in each Portfolio by showing yearly changes in the Portfolio’s performance. The tables below show each Portfolio’s average annual total returns for the periods shown through December 31, 2008 and compare the Portfolio’s performance to the returns of a broad-based index.

Past performance is not an indication of future performance. This may be particularly true for both the Opportunity Portfolio and the Common Stock Portfolio because prior to June 15, 2009 and December 1, 2008, respectively, each Portfolio had a different investment strategy and consisted entirely of an actively managed portfolio of equity securities. If each Portfolio had historically been managed using its current strategy, the respective performance of each Portfolio may have been different. In addition, prior to June 8, 2009, the Opportunity Portfolio was advised by a different Adviser. SEC regulations require the Portfolios to disclose this performance information to you, but you should note that it provides a limited basis for comparison between the Portfolios because of the relatively recent changes to the Portfolios.

Both the bar charts and the tables assume reinvestment of dividends and other distributions. The performance results do not reflect any insurance and Contract-related fees and expenses, which would reduce the performance results.

| Opportunity Portfolio – Calendar Year Total Returns (Class IB) | ||

| ||

Best Quarter (% and time period) 6.34% (2007 2nd Quarter) | Worst Quarter (% and time period) -22.63% (2008 4th Quarter) |

8

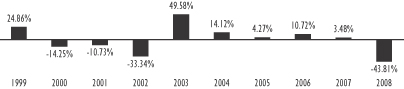

| Common Stock Portfolio – Calendar Year Total Returns (Class IB) | ||||||||||||||||||

| ||||||||||||||||||

Best Quarter (% and time period) 22.08% (2003 2nd Quarter) | Worst Quarter (% and time period) -25.39% (2008 4th Quarter) | |||||||||||||||||

| Opportunity Portfolio - Average Annual Total Returns (For the periods ended December 31, 2008) | ||||||

| One Year | Since Inception | |||||

Opportunity Portfolio – Class IA | -38.72 | % | -14.58 | % | ||

Opportunity Portfolio – Class IB | -38.87 | % | -14.80 | % | ||

Russell 3000® Index † | -37.31 | % | -13.03 | % | ||

| Common Stock Portfolio - Average Annual Total Returns (For the periods ended December 31, 2008) | |||||||||

| One Year | Five Years | Ten Years | |||||||

Common Stock Portfolio – Class IA | -43.67 | % | -4.95 | % | -2.85 | % | |||

Common Stock Portfolio – Class IB | -43.81 | % | -5.19 | % | -3.10 | % | |||

Russell 3000® Index*,† | -37.31 | % | -1.95 | % | -0.80 | % | |||

Standard & Poor’s 500 Composite Stock Index † | -37.00 | % | -2.19 | % | -1.38 | % | |||

† | Russell 3000® Index is an unmanaged index which measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market. Standard & Poor’s 500 Composite Stock Index (“S&P 500 Index”) is an unmanaged weighted index of common stocks of 500 of the largest U.S. industrial, transportation, utility and financial companies, deemed by Standard & Poor’s to be representative of the larger capitalization portion of the United States stock market. The index is capitalization weighted, thereby giving greater weight to companies with the largest market capitalizations. |

* | Effective December 1, 2008, the Common Stock Portfolio changed its benchmark from the S&P 500 Index to the Russell 3000® Index. The Common Stock Portfolio changed its benchmark because the Manager believes that the Russell 3000® Index reflects more closely the securities and sectors in which the Portfolio invests. |

The following table shows the capitalization of each Portfolio as of December 31, 2008 and of the Common Stock Portfolio on a pro forma combined basis as of that date after giving effect to the proposed Reorganization.

| Net Assets (in thousands) | Net Asset Value Per Share | Shares Outstanding | ||||||

Opportunity Portfolio – Class IA | $ | 2,938 | $ | 6.44 | 455,882 | |||

Common Stock Portfolio – Class IA | $ | 3,168,157 | $ | 11.11 | 285,144,671 | |||

Adjustments* | None | None | -191,487 | |||||

Pro forma Common Stock Portfolio – Class IA (assuming the Reorganization is approved) | $ | 3,171,095 | $ | 11.11 | 285,427,093 | |||

Opportunity Portfolio – Class IB | $ | 32,544 | $ | 6.44 | 5,049,773 | |||

Common Stock Portfolio – Class IB | $ | 1,034,651 | $ | 11.05 | 93,628,598 | |||

Adjustments* | None | None | -2,104,789 | |||||

Pro forma Common Stock Portfolio – Class IB (assuming the Reorganization is approved) | $ | 1,067,195 | $ | 11.05 | 96,578,733 | |||

| * | AXA Equitable is expected to bear the Reorganization Expenses as described in “Additional Information about the Reorganizations—Terms of the Reorganization Plan” below. |

9

After careful consideration, the Board unanimously approved the Reorganization Plan with respect to the Opportunity Portfolio. Accordingly, the Board has submitted the Reorganization Plan for approval by the Opportunity Portfolio’s shareholders. The Board recommends that you vote “FOR” Proposal 1.

* * * * *

| PROPOSAL 2: | APPROVAL OF THE REORGANIZATION PLAN WITH RESPECT TO THE REORGANIZATION OF THE SMALL CAP PORTFOLIO INTO THE SMALL COMPANY INDEX PORTFOLIO. |

This Proposal 2 requests your approval of the Reorganization Plan, pursuant to which the Small Cap Portfolio will be reorganized into the Small Company Index Portfolio.

In considering whether you should approve this Proposal, you should note that:

| • | The Small Cap Portfolio and Small Company Index Portfolio have substantially similar investment objectives and substantially identical investment policies, strategies and principal risks. Below is a summary comparison of the two Portfolios. For a detailed comparison of the each Portfolio’s investment objectives, policies, strategies and risks, see “Comparison of Investment Objectives, Policies and Strategies” and “Comparison of Principal Risk Factors” below. |

• | The Small Cap Portfolio has an investment objective to seek to achieve capital appreciation. The Small Company Index Portfolio has an investment objective to seek to replicate as closely as possible, before the deduction of Portfolio expenses, the total return of the Russell 2000® Index (the “Russell 2000”). These objectives are substantially similar in that each Portfolio seeks to achieve capital appreciation through an investment in the equity securities of small-cap companies. Under normal circumstances, each Portfolio has a policy to invest at least 80% of its net assets, plus borrowings for investment purposes, in equity securities of small-cap companies included in the Russell 2000. To achieve their respective investment objective, each Portfolio invests in a statistically small sample of the securities found in the Russell 2000, using a process known as “optimization” whereby the industry weightings, market capitalizations and fundamental characteristics of the Portfolio’s stocks are intended to closely match those of the securities included in the Russell 2000. The securities held by each Portfolio are weighted to make its total investment characteristics similar to those of the Russell 2000 as a whole, and over time, the correlation between the Portfolio’s performance (before the deduction of expenses) and that of the Russell 2000 is expected to be 95% or higher. Each Portfolio also may invest, to a limited extent, securities index futures contracts and related options, warrants and convertible securities. Each Portfolio also may invest in short-term debt securities and money market instruments to meet redemption requests or to facilitate investment in the securities included in the Russell 2000. |

| • | Each Portfolio is subject to adviser selection risk, asset class risk, convertible securities risk, derivatives risk, equity risk, futures and options risk, index-fund risk, liquidity risk, market risk, portfolio management risk, securities lending risk, security risk, security selection risk and small-cap company risk as principal risks. |

10

| • | AXA Equitable (“Manager”) serves as the investment manager and administrator for each Portfolio and would continue to manage and administer the Small Company Index Portfolio after the Reorganization. AXA Equitable has received an exemptive order from the SEC that generally permits AXA Equitable and the Board to appoint, dismiss and replace each Portfolio’s investment sub-adviser(s) (“Adviser”) and to amend the advisory agreements between AXA Equitable and the Advisers without obtaining shareholder approval. AllianceBernstein L.P. currently serves as the Adviser for the Small Cap Portfolio and the Small Company Index Portfolio and it is anticipated that it will continue to advise the Small Company Index Portfolio after the Reorganization. For a detailed description of the Manager and the Small Company Index Portfolio’s Adviser, please see “Additional Information about the Portfolios—The Manager” and “- The Advisers” below. |

| • | The Small Cap Portfolio and Small Company Index Portfolio had net assets of approximately $63.01 million and $647.28 million, respectively, as of December 31, 2008. Thus, if the Reorganization had been in effect on that date, the combined Portfolio would have had net assets of approximately $710.29 million. |

| • | Class IA shareholders of the Small Cap Portfolio will receive Class IA shares of the Small Company Index Portfolio, and Class IB shareholders of the Small Cap Portfolio will receive Class IB shares of the Small Company Index Portfolio, pursuant to the Reorganization. Shareholders will not pay any sales charges in connection with the Reorganization. Please see “Comparative Fee and Expense Tables,” “Additional Information about the Reorganization” and “Additional Information about the Portfolios” below for more information. |

| • | It is estimated that the annual operating expense ratios for the Small Company Index Portfolio’s Class IA and Class IB shares, immediately following the Reorganization, will be lower than those of the Small Cap Portfolio’s Class IA and Class IB shares, respectively, for the last fiscal year, before and after taking into account an expense limitation arrangement that is in effect for the Small Cap Portfolio and after taking into account the restatement of fees of the Small Cap Portfolio to reflect current fees. For a more detailed comparison of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the Portfolios” below. |

| • | The management fee for each Portfolio is the same and is equal to an annual rate of 0.25% of the Portfolio’s average daily net assets. |

| • | The administration fee schedule is the same for each Portfolio. Each Portfolio pays $30,000 per year, plus its proportionate share of the Trust’s administration fee for portfolios with a single Adviser, which is equal to an annual rate of 0.12% of the first $3 billion of the Trust’s total average daily net assets (exclusive of certain portfolios), 0.11% of the next $3 billion, 0.105% of the next $4 billion, 0.10% of the next $20 billion and 0.0975% thereafter. For a more detailed description of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the Portfolios” below. |

| • | Following the Reorganization, the combined Portfolio will be managed in accordance with the investment objective, policies and strategies of the Small Company Index Portfolio. In connection with the changes made to the Acquired Portfolio’s investment policies and strategies, as described in the “Summary” section above, AXA Equitable and AllianceBernstein restructured the Acquired Portfolio’s holdings to pursue its new investment policies and strategies, which are substantially identical to those of the Small Company Index Portfolio. AXA Equitable has reviewed the Small Cap Portfolio’s current portfolio holdings and determined that they generally are compatible with the Small Company Index Portfolio’s investment objective and policies. Thus, AXA Equitable believes that, if the Reorganization is approved, all or virtually all of those holdings could be transferred to and held by the Small Company Index Portfolio. However, it is expected that some of those holdings may not remain at the time of the Reorganization due to normal portfolio turnover. It is also expected that, if the Reorganization is approved, the Small Cap Portfolio’s holdings that are not compatible with the Small Company Index Portfolio’s investment objective and policies will be liquidated in an orderly manner in connection with the Reorganization, and the proceeds of these sales held in temporary investments or reinvested in assets that are consistent with |

11

that investment objective and policies. The portion of the Small Cap Portfolio’s assets that will be liquidated in connection with the Reorganization will depend on market conditions and on the assessment by AXA Equitable and the Small Company Index Portfolio’s Adviser of the compatibility of those holdings with the Small Company Index Portfolio’s portfolio composition and investment objective and policies at the time of the Reorganization. The need for a Portfolio to sell investments in connection with the Reorganization may result in its selling securities at a disadvantageous time and price and could result in its realizing gains (or losses) that would not otherwise have been realized and incurring transaction costs that would not otherwise have been incurred. |

| • | AXA Equitable will bear the Reorganization Expenses (as defined in the Reorganization Plan), which include the costs associated with the preparation and distribution of this Proxy Statement/Prospectus and with obtaining shareholder approval of the Reorganization, but exclude brokerage and similar expenses in connection with the Reorganization, which will be borne by the Portfolios. Please see “Additional Information about the Reorganizations” below for more information. |

Comparison of Investment Objectives, Policies and Strategies

The following table compares the investment objectives and principal investment policies and strategies of the Small Cap Portfolio with those of the Small Company Index Portfolio. The Board may change the investment objective of a Portfolio without a vote of the Portfolio’s shareholders.

Acquiring Portfolio | Acquired Portfolio | |

Small Company Index Portfolio | Small Cap Portfolio | |

| Investment Objective | ||

| Seeks to replicate as closely as possible (before the deduction of Portfolio expenses) the total return of the Russell 2000. | Seeks to achieve capital appreciation. | |

| Principal Investment Strategies | Same. | |

| Under normal circumstances, the Portfolio invests at least 80% of its net assets, plus borrowings for investment purposes, in equity securities of small-cap companies included in the Russell 2000. The Adviser seeks to match the returns of the Russell 2000. | ||

| The Portfolio may invest, to a limited extent, in securities index futures contracts and related options, warrants and convertible securities to simulate full investment in the Russell 2000 while retaining a cash balance for fund management purposes, to facilitate trading, to reduce transaction costs, or to seek higher investment returns when a futures contract, option, warrant or convertible security is priced more attractively than the underlying equity security or Russell 2000. | Same. | |

| The Portfolio may invest to a lesser extent in short-term debt securities and money market securities to meet redemption request or to facilitate investment in the securities included in the Russell 2000. | Same. | |

| The Portfolio invests in a statistically selected sample of the securities found in the Russell 2000, using a process known as “optimization.” This process selects stocks for the Portfolio so that industry weightings, market capitalizations and fundamental characteristics (price to book ratios, price to earnings ratios, debt to asset ratios and dividend yields) closely match those of the securities included in the Russell 2000. This approach helps to increase the Portfolio’s liquidity and reduce costs. The securities held by the Portfolio are weighted to make the Portfolio’s total investment characteristics similar to those of the Russell 2000 as a whole. | Same. | |

12

Comparison of Principal Risk Factors

Risk is the chance that you will lose money on your investment or that it will not earn as much as you expect. In general, the greater the risk, the more money your investment can earn for you and the more you can lose. Like other investment companies, the value of each Portfolio’s shares may be affected by its investment objective, principal investment strategies and particular risk factors. Consequently, each Portfolio may be subject to different principal risks. Some of the principal risks of investing in the Portfolios are noted below. However, other factors may also affect each Portfolio’s net asset value. There is no guarantee that a Portfolio will achieve its investment objective or that it will not lose principal value. The following table compares the principal risks of an investment in each Portfolio. For an explanation of each such risk, see “Additional Information about the Reorganizations – Description of Risk Factors” below.

Risks | Small Company Index Portfolio | Small Cap Portfolio | ||

Adviser Selection Risk | X | X | ||

Asset Class Risk | X | X | ||

Convertible Securities Risk | X | X | ||

Derivatives Risk | X | X | ||

Equity Risk | X | X | ||

Futures and Options Risk | X | X | ||

Index-Fund Risk | X | X | ||

Liquidity Risk | X | X | ||

Market Risk | X | X | ||

Portfolio Management Risk | X | X | ||

Securities Lending Risk | X | X | ||

Security Risk | X | X | ||

Security Selection Risk | X | X | ||

Small-Cap Company Risk | X | X | ||

13

Comparative Fee and Expense Tables

The following tables show the fees and expenses of each class of shares of each Portfolio and the estimated pro forma fees and expenses of each class of shares of the Acquiring Portfolio after giving effect to the proposed Reorganization. Fees and expenses for each Portfolio are based on those incurred by each class of its shares for the last fiscal year ended December 31, 2008. The fees and expenses for the Small Cap Portfolio have been adjusted to reflect the contractual fee changes that took effect for that Portfolio on June 8, 2009. The pro forma fees and expenses of the Acquiring Portfolio Shares assume that the Reorganization has been in effect for the last year ended on that date. There are no fees or charges to buy or sell shares of either Portfolio, reinvest dividends or exchange into other portfolios. The tables do not reflect any Contract-related fees and expenses, which would increase overall fees and expenses.

Annual Operating Expenses

(expenses that are deducted from Portfolio assets)

| Small Cap Portfolio | Small Company Index Portfolio | Pro Forma Small Company Index Portfolio (assuming the Reorganization is approved) | ||||||||||||||||

| Class IA | Class IB | Class IA | Class IB | Class IA | Class IB | |||||||||||||

Management Fee† | 0.25 | % | 0.25 | 0.25 | % | 0.25 | % | 0.25 | % | 0.25 | % | |||||||

Distribution and/or Service Fees (12b-1 fees)†† | None | 0.25 | % | None | 0.25 | % | None | 0.25 | % | |||||||||

Other Expenses | 0.65 | % | 0.65 | % | 0.20 | % | 0.20 | % | 0.15 | % | 0.15 | % | ||||||

Total Annual Portfolio Operating Expenses | 0.90 | % | 1.15 | % | 0.45 | % | 0.70 | % | 0.40 | % | 0.65 | % | ||||||

Less Fee Waiver/Expense Reimbursement* | -0.40 | % | -0.40 | % | N/A | N/A | N/A | N/A | ||||||||||

Net Annual Portfolio Operating Expenses | 0.50 | % | 0.75 | % | 0.45 | % | 0.70 | % | 0.40 | % | 0.65 | % | ||||||

| † | Restated to reflect current fees for the Small Cap Portfolio. |

| †† | The maximum annual distribution and/or service (12b-1) fee for a Portfolio’s Class IB shares is 0.50% of the average daily net assets attributable to the Portfolio’s Class IB shares. Under an arrangement approved by the Trust’s Board of Trustees, the distribution and/or service (12b-1) fee currently is limited to 0.25% of the average daily net assets attributable to a Portfolio’s Class IB shares. This arrangement will be in effect at least until April 30, 2010. |

| * | Pursuant to a contract, the Manager has agreed to make payments or waive its management, administrative and other fees to limit the expenses of the Small Cap Portfolio through April 30, 2010 (unless the Board of Trustees consents to an earlier revision or termination of the arrangement) so that the Annual Portfolio Operating Expenses of the Small Cap Portfolio (exclusive of taxes, interest, brokerage commissions, capitalized expenses, fees and expenses of other investment companies in which the Portfolio invests and extraordinary expenses) do not exceed the amount shown above under Net Annual Portfolio Operating Expenses. The Manager may be reimbursed the amount of any such payments and waivers in the future, provided that the payments or waivers are reimbursed within three years of the payment or waiver being made and the combination of the Small Cap Portfolio’s expense ratio and such reimbursements do not exceed the Small Cap Portfolio’s expense cap. If the actual expense ratio is less than the expense cap and the Manager has recouped all eligible previous payments made, the Small Cap Portfolio will be charged such lower expenses. The Manager may discontinue these arrangements at any time after April 30, 2010. |

This example is intended to help you compare the costs of investing in the Portfolios with the cost of investing in other investment options. The example assumes that:

| • | You invest $10,000 in a Portfolio for the time periods indicated; |

14

| • | Your investment has a 5% return each year; |

| • | The Portfolio’s operating expenses remain the same; and |

| • | If applicable, the expense limitation currently in effect is not renewed. |

This example should not be considered a representation of past or future expenses of the Portfolios. Actual expenses may be higher or lower than those shown. The costs in the example would be the same whether or not you redeemed all of your shares at the end of these periods. This example does not reflect any Contract-related fees and expenses, including redemption fees (if any) at the Contract level. If such fees and expenses were reflected, the total expenses would be substantially higher. Similarly, the annual rate of return assumed in the example is not an estimate or guarantee of future investment performance. Based on these assumptions, your costs would be:

| Small Cap Portfolio | Small Company Index Portfolio | Pro Forma Small Company Index Portfolio (assuming the Reorganization is approved) | ||||||||||||||||

| Class IA | Class IB | Class IA | Class IB | Class IA | Class IB | |||||||||||||

1 Year | $ | 51 | $ | 77 | $ | 46 | $ | 72 | $ | 41 | $ | 66 | ||||||

3 Years | $ | 247 | $ | 326 | $ | 144 | $ | 224 | $ | 128 | $ | 208 | ||||||

5 Years | $ | 459 | $ | 594 | $ | 252 | $ | 390 | $ | 224 | $ | 362 | ||||||

10 Years | $ | 1,071 | $ | 1,362 | $ | 567 | $ | 871 | $ | 505 | $ | 810 | ||||||

Comparative Performance Information

The bar charts below illustrate each Portfolio’s annual total returns for the calendar years indicated and give some indication of the risks of investing in each Portfolio by showing yearly changes in the Portfolio’s performance. The tables below show each Portfolio’s average annual total returns for the periods shown through December 31, 2008 and compare the Portfolio’s performance to the returns of a broad-based index.

Past performance is not an indication of future performance. This may be particularly true for both the Small Cap Portfolio and the Small Company Index Portfolio because a different Adviser advised each Portfolio prior to June 15, 2009 and January 2, 2003, respectively. In addition, prior to June 8, 2009, the Small Cap Portfolio had a different investment strategy and consisted entirely of an actively managed portfolio of equity securities. If the Small Cap Portfolio had historically been managed using its current strategy, the respective performance of each Portfolio may have been different. SEC regulations require the Portfolios to disclose this performance information to you, but you should note that it provides a limited basis for comparison between the Portfolios because of the relatively recent changes to the Small Cap Portfolio.

Both the bar charts and the tables assume reinvestment of dividends and other distributions. The performance results do not reflect any insurance and Contract-related fees and expenses, which would reduce the performance results.

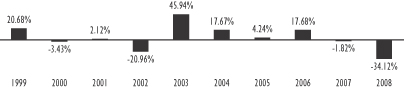

| Small Cap Portfolio – Calendar Year Total Returns (Class IB) | ||

| ||

Best Quarter (% and time period) 5.30% (2007 2nd Quarter) | Worst Quarter (% and time period) -27.36% (2008 4th Quarter) |

15

| Small Company Index Portfolio – Calendar Year Total Returns (Class IB) | ||||||||||||||||||

| ||||||||||||||||||

Best Quarter (% and time period) 22.95% (2003 2nd Quarter) | Worst Quarter (% and time period) -26.45% (2008 4th Quarter) | |||||||||||||||||

| Small Cap Portfolio - Average Annual Total Returns (For the periods ended December 31, 2008) | ||||||

| One Year | Since Inception | |||||

Small Cap Portfolio – Class IA | -38.06 | % | -15.92 | % | ||

Small Cap Portfolio – Class IB | -38.23 | % | -16.15 | % | ||

Russell 2000® Index† | -33.79 | % | -13.35 | % | ||

| Small Company Index Portfolio - Average Annual Total Returns (For the periods ended December 31, 2008) | |||||||||

| One Year | Five Years | Ten Years | |||||||

Small Company Index Portfolio – Class IA* | -33.94 | % | -1.11 | % | 2.70 | % | |||

Small Company Index Portfolio – Class IB | -34.12 | % | -1.36 | % | 2.51 | % | |||