File No. 333-

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON DECEMBER 21, 2010

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

| THE SECURITIES ACT OF 1933 | x | |

| Pre-Effective Amendment No. | ¨ | |

| Post-Effective Amendment No. | ¨ |

EQ Advisors Trust

(Exact Name of Registrant as Specified in Charter)

1290 Avenue of the Americas

New York, New York 10104

(Address of Principal Executive Offices)

(212) 554-1234

(Registrant’s Area Code and Telephone Number)

STEVEN M. JOENK

AXA Funds Management Group

AXA Equitable Life Insurance Company

1290 Avenue of the Americas

New York, New York 10104

(Name and Address of Agent for Service)

With copies to:

PATRICIA LOUIE, ESQ. AXA Equitable Life Insurance Company | CLIFFORD J. ALEXANDER, ESQ. MARK C. AMOROSI, ESQ. | |

1290 Avenue of the Americas New York, New York 10104 | K&L Gates LLP 1601 K Street, N.W. Washington, DC 20006 |

Approximate Date of Proposed Public Offering:

As soon as practicable after this Registration Statement becomes effective.

It is proposed that this Registration Statement will become effective on the 30th day after filing pursuant to Rule 488 under the Securities Act of 1933, as amended.

Title of securities being registered: Class IA and Class IB shares of beneficial interest in the series of the registrant designated as the EQ/Large Cap Growth PLUS Portfolio and EQ/Large Cap Value Index Portfolio.

No filing fee is required because the registrant is relying on Section 24(f) of the Investment Company Act of 1940, as amended, pursuant to which it has previously registered an indefinite number of shares (File Nos. 333-17217 and 811-07953).

EQ ADVISORS TRUST

CONTENTS OF REGISTRATION STATEMENT

This Registration Statement contains the following papers and documents:

Cover Sheet

Contents of Registration Statement

Letter to Shareholders

Notice of Special Meeting

Information Statement

Part A - Proxy Statement/Prospectus

Part B - Statement of Additional Information

Part C - Other Information

Signature Page

Exhibits

AXA EQUITABLE LIFE INSURANCE COMPANY

MONY LIFE INSURANCE COMPANY

MONY LIFE INSURANCE COMPANY OF AMERICA

1290 Avenue of the Americas

New York, New York 10104

, 2011

Dear Contractholder:

Enclosed is a notice of a Special Meeting of Shareholders of each of the following Portfolios:

| • | EQ/Capital Guardian Growth Portfolio (the “Capital Guardian Growth Portfolio”), and |

| • | EQ/Lord Abbett Growth and Income Portfolio (the “Lord Abbett Growth and Income Portfolio” and together, the “Acquired Portfolios”). |

Each Acquired Portfolio is a portfolio of EQ Advisors Trust (the “Trust”). The Special Meeting of Shareholders of the Acquired Portfolios is scheduled to be held at the Trust’s offices, 1290 Avenue of the Americas, New York, New York 10104, on April 20, 2011 at , Eastern time (the “Meeting”). At the Meeting, the shareholders of the Acquired Portfolios will be asked to approve the proposals described below.

The Trust’s Board of Trustees (the “Board of Trustees”) has called the Meeting to request shareholder approval of the reorganization of each Acquired Portfolio into a corresponding series of the Trust (the “Acquiring Portfolios”) (the “Reorganizations”) as set forth below:

| • | the Capital Guardian Growth Portfolio into the EQ/Large Cap Growth PLUS Portfolio, and |

| • | the Lord Abbett Growth and Income Portfolio into the EQ/Large Cap Value Index Portfolio. |

The Board of Trustees has approved these proposals.

Each Portfolio is managed by AXA Equitable Life Insurance Company (“AXA Equitable”) and sub-advised by one or more investment sub-advisers. In each case, if a Reorganization is approved and implemented, each Contractholder that invests indirectly in an Acquired Portfolio will automatically become a Contractholder that invests indirectly in the corresponding Acquiring Portfolio.

As an owner of an annuity contract or certificate and/or life insurance policy that participates in the Acquired Portfolios through the investment divisions of separate accounts established by AXA Equitable, MONY Life Insurance Company or MONY Life Insurance Company of America (each, an “Insurance Company”), you are entitled to instruct the applicable Insurance Company how to vote the Acquired Portfolio shares related to your interest in those accounts as of the close of business on January 31, 2011. The attached Notice of Special Meeting of Shareholders and Combined Proxy Statement and Prospectus concerning the Meeting describe the matters to be considered at the Meeting.

You are cordially invited to attend the Meeting. Since it is important that your vote be represented whether or not you are able to attend, you are urged to consider these matters and to exercise your voting instructions by completing, dating, signing, and returning the enclosed voting instruction card in the accompanying return envelope at your earliest convenience or by relaying your voting instructions via telephone or the Internet by following the enclosed instructions. Of course, we hope that you will be able to attend the Meeting, and if you wish, you may vote your shares in person, even though you may have already returned a voting instruction card or submitted your voting instructions via telephone or the Internet. Please respond promptly in order to save additional costs of proxy solicitation and in order to make sure you are represented.

| Very truly yours, |

| Steven M. Joenk |

| President |

| AXA Funds Management Group |

| AXA Equitable Life Insurance Company |

EQ ADVISORS TRUST

EQ/Capital Guardian Growth Portfolio

EQ/Lord Abbett Growth and Income Portfolio

1290 Avenue of the Americas

New York, New York 10104

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON April 20, 2011

To the Shareholders:

NOTICE IS HEREBY GIVEN that a Special Meeting of Shareholders of each of the following Portfolios, each of which is a portfolio of EQ Advisors Trust (the “Trust”), will be held on Wednesday, April 20, 2011, at , Eastern time, at the offices of the Trust, located at 1290 Avenue of the Americas, New York, New York 10104 (the “Meeting”):

| • | EQ/Capital Guardian Growth Portfolio (the “Capital Guardian Growth Portfolio”), and |

| • | EQ/Lord Abbett Growth and Income Portfolio (the “Lord Abbett Growth and Income Portfolio” and together, the “Acquired Portfolios”). |

The Meeting will be held to act on the following proposals:

| 1. | To approve the Plan of Reorganization and Termination adopted by the Trust (the “Reorganization Plan”), which provides for the reorganization of the Capital Guardian Growth Portfolio into the EQ/Large Cap Growth PLUS Portfolio, also a series of the Trust. |

| 2. | To approve the Reorganization Plan, which provides for the reorganization of the Lord Abbett Growth and Income Portfolio into the EQ/Large Cap Value Index Portfolio, also a series of the Trust. |

| 3. | To transact other business that may properly come before the Meeting or any adjournments thereof. |

Please note that owners of variable life insurance policies or variable annuity contracts or certificates (the “Contractholders”) issued by AXA Equitable Life Insurance Company, MONY Life Insurance Company or MONY Life Insurance Company of America (each, an “Insurance Company”) who have invested in shares of the Acquired Portfolios through the investment divisions of a separate account or accounts of an Insurance Company will be given the opportunity, to the extent required by law, to provide the applicable Insurance Company with voting instructions on the above proposals.

You should read the Combined Proxy Statement and Prospectus attached to this notice prior to completing your proxy or voting instruction card. The record date for determining the number of shares outstanding, the shareholders entitled to vote and the Contractholders entitled to provide voting instructions at the Meeting and any adjournments thereof has been fixed as the close of business on January 31, 2011. If you attend the Meeting, you may vote or give your voting instructions in person.

YOUR VOTE IS IMPORTANT

PLEASE RETURN YOUR PROXY CARD OR VOTING INSTRUCTION CARD PROMPTLY

Regardless of whether you plan to attend the Meeting, you should vote or give voting instructions by promptly completing, dating, signing, and returning the enclosed proxy or voting instruction card for the Portfolio in which you directly or indirectly own shares in the enclosed postage-paid envelope. You also can vote or provide voting instructions through the Internet or by telephone using the 12-digit control number that appears on the enclosed

proxy or voting instruction card and following the simple instructions. If you are present at the Meeting, you may change your vote or voting instructions, if desired, at that time. The Trust’s Board of Trustees recommends that you vote or provide voting instructions to vote FOR the proposals.

| By order of the Board of Trustees, |

| Patricia Louie |

| Vice President and Secretary |

, 2011

New York, New York

ii

AXA EQUITABLE LIFE INSURANCE COMPANY

MONY LIFE INSURANCE COMPANY

MONY LIFE INSURANCE COMPANY OF AMERICA

INFORMATION STATEMENT

REGARDING A SPECIAL MEETING OF SHAREHOLDERS OF

EQ/CAPITAL GUARDIAN GROWTH PORTFOLIO

EQ/LORD ABBETT GROWTH AND INCOME PORTFOLIO

EACH A SERIES OF EQ ADVISORS TRUST

TO BE HELD ON APRIL 20, 2011

DATED: , 2011

GENERAL

This Information Statement is being furnished by AXA Equitable Life Insurance Company (“AXA Equitable”), MONY Life Insurance Company or MONY Life Insurance Company of America (each, an “Insurance Company” and together, the “Insurance Companies”), each of which is a stock life insurance company, to owners of their variable life insurance policies or variable annuity contracts or certificates (the “Contracts”) (the “Contractholders”) who, as of January 31, 2011 (the “Record Date”), had net premiums or contributions allocated to the investment divisions of their separate accounts (the “Separate Accounts”) that are invested in shares of one or more of the following Portfolios:

| • | EQ/Capital Guardian Growth Portfolio, and |

| • | EQ/Lord Abbett Growth and Income Portfolio (together, the “Acquired Portfolios”). |

Each Acquired Portfolio is a portfolio of EQ Advisors Trust (the “Trust”), a Delaware statutory trust that is registered with the Securities and Exchange Commission as an open-end management investment company.

Each Insurance Company is required to offer Contractholders the opportunity to instruct it, as the record owner of all of the shares of beneficial interest in the Acquired Portfolios (the “Shares”) held by its Separate Accounts, as to how it should vote on the reorganization proposals (the “Proposals”) to be considered at the Special Meeting of Shareholders of the Acquired Portfolios referred to in the preceding Notice and at any adjournments (the “Meeting”). The enclosed Combined Proxy Statement and Prospectus, which you should retain for future reference, sets forth concisely information about the proposed reorganizations involving the Acquired Portfolios and corresponding series of the Trust that a Contractholder should know before completing the enclosed voting instruction card.

AXA Financial, Inc. is the parent company of each Insurance Company and is a wholly owned subsidiary of AXA, a French insurance holding company. The principal executive offices of AXA Financial, Inc. and each Insurance Company are located at 1290 Avenue of the Americas, New York, New York 10104.

This Information Statement and the accompanying voting instruction card are being mailed to Contractholders on or about February , 2011.

HOW TO INSTRUCT AN INSURANCE COMPANY

To instruct an Insurance Company as to how to vote the Shares held in the investment divisions of its Separate Accounts, Contractholders are asked to promptly complete their voting instructions on the enclosed voting instruction card(s); and sign, date and mail the voting instruction card(s) in the accompanying postage-paid envelope. Contractholders also may provide voting instructions by phone at 1-800- or by Internet at our website at .

If a voting instruction card is not marked to indicate voting instructions but is signed, dated and returned, it will be treated as an instruction to vote the Shares in favor of the Proposal(s).

The number of Shares held in the investment division of a Separate Account corresponding to an Acquired Portfolio for which a Contractholder may provide voting instructions was determined as of the Record Date by dividing (i) a Contract’s account value (minus any Contract indebtedness) allocable to that investment division by (ii) the net asset value of one Share of the corresponding Acquired Portfolio. At any time prior to an Insurance Company’s voting at the Meeting, a Contractholder may revoke his or her voting instructions with respect to that investment division by providing the Insurance Company with a properly executed written revocation of such voting instructions, properly executing later-dated voting instructions by a voting instruction card, telephone or the Internet, or appearing and voting in person at the Meeting.

HOW AN INSURANCE COMPANY WILL VOTE

An Insurance Company will vote the Shares for which it receives timely voting instructions from Contractholders in accordance with those instructions. An Insurance Company will vote Shares attributable to Contracts for which it is the Contractholder “FOR” each applicable Proposal. Shares in each investment division of a Separate Account for which an Insurance Company receives a voting instruction card that is signed, dated and timely returned but is not marked to indicate voting instructions will be treated as an instruction to vote the Shares in favor of the applicable Proposal. Shares in each investment division of a Separate Account for which an Insurance Company receives no timely voting instructions from Contractholders, or that are attributable to amounts retained by AXA Equitable as surplus or seed money, will be voted by the applicable Insurance Company either for or against approval of the Proposals, or as an abstention, in the same proportion as the Shares for which Contractholders (other than the Insurance Company) have provided voting instructions to the Insurance Company.

OTHER MATTERS

The Insurance Companies are not aware of any matters, other than the specified Proposals, to be acted on at the Meeting. If any other matters come before the Meeting, an Insurance Company will vote the Shares upon such matters in its discretion. Voting instruction cards may be solicited by employees of AXA Equitable or its affiliates as well as officers and agents of the Trust. The principal solicitation will be by mail but voting instructions may also be solicited by telephone, telegraph, fax, personal interview, the Internet or other permissible means.

If the necessary quorum to transact business is not established or the vote required to approve or reject a Proposal is not obtained at the Meeting, the persons named as proxies may propose one or more adjournments of the Meeting in accordance with applicable law to permit further solicitation of voting instructions. The persons named as proxies will vote in favor of such adjournment with respect to those Shares for which they received voting instructions in favor of a Proposal and will vote against any such adjournment those Shares for which they received voting instructions against a Proposal.

It is important that your Contract be represented. Please promptly mark your voting instructions on the enclosed voting instruction card; then sign, date and mail the voting instruction card in the accompanying postage-paid envelope. You may also provide your voting instructions by telephone at 1-800- or by Internet at our website at .

ii

COMBINED PROXY STATEMENT AND PROSPECTUS

, 2011

EQ ADVISORS TRUST

EQ/Capital Guardian Growth Portfolio

EQ/Lord Abbett Growth and Income Portfolio

EQ/Large Cap Growth PLUS Portfolio

EQ/Large Cap Value Index Portfolio

1290 Avenue of the Americas

New York, New York 10104

1-877-222-2144

This Combined Proxy Statement and Prospectus (the “Proxy Statement/Prospectus”) is being furnished to owners of variable life insurance policies or variable annuity contracts or certificates (the “Contracts”) (the “Contractholders”) issued by AXA Equitable Life Insurance Company (“AXA Equitable”), MONY Life Insurance Company or MONY Life Insurance Company of America (each, an “Insurance Company” and together, the “Insurance Companies”) who, as of January 31, 2011, had net premiums or contributions allocated to the investment divisions of an Insurance Company’s separate accounts (the “Separate Accounts”) that are invested in shares of beneficial interest in one or more of the following Portfolios:

| • | EQ/Capital Guardian Growth Portfolio (the “Capital Guardian Growth Portfolio”), and |

| • | EQ/Lord Abbett Growth and Income Portfolio (the “Lord Abbett Growth and Income Portfolio” and each an “Acquired Portfolio” and together the “Acquired Portfolios”). |

Each Acquired Portfolio is a portfolio of EQ Advisors Trust (the “Trust”), an open-end management investment company. This Proxy Statement/Prospectus also is being furnished to the Insurance Companies as the record owners of shares and to other shareholders that were invested in one or more of the Acquired Portfolios as of January 31, 2011. Contractholders are being provided the opportunity to instruct the applicable Insurance Company to approve or disapprove the proposals contained in this Proxy Statement/Prospectus in connection with the solicitation by the Board of Trustees of the Trust (the “Board”) of proxies to be used at the Special Meeting of Shareholders of the Acquired Portfolios to be held at 1290 Avenue of the Americas, New York, New York 10104, on Wednesday, April 20, 2011, at , Eastern time, or any adjournment or adjournments thereof (the “Meeting”).

THE SEC HAS NOT APPROVED OR DISAPPROVED THE SECURITIES DESCRIBED IN THIS PROXY STATEMENT/PROSPECTUS OR DETERMINED IF THIS PROXY STATEMENT/PROSPECTUS IS ACCURATE OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The proposals described in this Proxy Statement/Prospectus are as follows:

Proposal | Shareholders Entitled to Vote on the Proposal | |

1. To approve the Plan of Reorganization and Termination adopted by the Trust (the “Reorganization Plan”), which provides for the reorganization of the Capital Guardian Growth Portfolio into the EQ/Large Cap Growth PLUS Portfolio (the “Growth PLUS Portfolio”), also a series of the Trust. | Shareholders of the Capital Guardian Growth Portfolio | |

2. To approve the Reorganization Plan, which provides for the reorganization of the Lord Abbett Growth and Income Portfolio into the EQ/Large Cap Value Index Portfolio (the “Large Cap Value Index Portfolio”), also a series of the Trust. | Shareholders of the Lord Abbett Growth and Income Portfolio. | |

Each reorganization referred to in Proposals 1 and 2 above is referred to herein as a “Reorganization” and together as the “Reorganizations.” Each of the Growth PLUS and Large Cap Value Index Portfolios is referred to herein as an “Acquiring Portfolio” and together as the “Acquiring Portfolios.” In addition, the Growth PLUS Portfolio may be referred to herein as a “PLUS Portfolio.”

This Proxy Statement/Prospectus, which you should retain for future reference, contains important information regarding the proposals that you should know before voting or providing voting instructions. Additional information about the Trust has been filed with the Securities and Exchange Commission (the “SEC”) and is available upon oral or written request without charge. This Proxy Statement/Prospectus is being provided to the Insurance Companies and mailed to Contractholders and other shareholders on or about February , 2011. It is expected that one or more representatives of each Insurance Company will attend the Meeting in person or by proxy and will vote shares held by the Insurance Company in accordance with voting instructions received from its Contractholders and in accordance with voting procedures established by the Trust.

The following documents have been filed with the SEC and are incorporated by reference into this Proxy Statement/Prospectus:

| 1. | The Prospectus and Statement of Additional Information of the Trust, each dated May 1, 2010, as supplemented, with respect to all of the Acquired Portfolios (File Nos. 333-17217 and 811-07953); |

| 2. | The Annual Report to Shareholders of the Trust with respect to all of the Acquired Portfolios for the fiscal year ended December 31, 2009 (File Nos. 333-17217 and 811-07953); |

| 3. | The Semi-Annual Report to Shareholders of the Trust with respect to all of the Acquired Portfolios for the semi-annual period ended June 30, 2010 (File Nos. 333-17217 and 811-07953); and |

| 4. | The Statement of Additional Information dated , 2011, relating to the Reorganizations (File No. 333- ). |

For a free copy of any of the above documents, please call or write the Trust at the phone number below or the above address.

Shareholders and Contractholders can find out more about the Acquired Portfolios in the Trust’s Annual Report listed above, which has been furnished to shareholders and Contractholders. Shareholders and Contractholders may request another copy thereof, without charge, by writing to the Trust at the above address or by calling 1-877-222-2144.

The Trust is subject to the informational requirements of the Securities Exchange Act of 1934, as amended. Accordingly, it must file certain reports and other information with the SEC. You can copy and review information about the Trust at the SEC’s Public Reference Room in Washington, DC, and at certain of the following SEC Regional Offices: New York Regional Office, 3 World Financial Center, Suite 400, New York, New York 10281;

ii

Miami Regional Office, 801 Brickell Avenue, Suite 1800, Miami, Florida 33131; Chicago Regional Office, 175 W. Jackson Boulevard, Suite 900, Chicago, Illinois 60604; Denver Regional Office, 1801 California Street, Suite 1500, Denver, Colorado 80202; Los Angeles Regional Office, 5670 Wilshire Boulevard, 11th Floor, Los Angeles, California 90036; Boston Regional Office, 33 Arch Street, 23rd Floor, Boston, MA 02110; Philadelphia Regional Office, The Mellon Independence Center, 701 Market Street, Philadelphia, PA 19106; Atlanta Regional Office, 3475 Lenox Road, N.E., Suite 1000, Atlanta, GA 30326; Fort Worth Regional Office, Burnett Plaza, Suite 1900, 801 Cherry Street, Unit 18, Fort Worth, TX 76102; Salt Lake Regional Office, 15 W. South Temple Street, Suite 1800, Salt Lake City, UT 84101; San Francisco Regional Office, 44 Montgomery Street, Suite 2600, San Francisco, CA 94104. You may obtain information on the operation of the Public Reference Room by calling the SEC at (202)

551-8090. Reports and other information about the Trust are available on the IDEA Database on the SEC’s Internet site at http://www.sec.gov. You may obtain copies of this information from the SEC’s Public Reference Branch, Office of Consumer Affairs and Information Services, Washington, DC 20549, at prescribed rates.

iii

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 4 | ||||

| 5 | ||||

| 5 | ||||

Comparison of Investment Objectives, Policies and Strategies | 5 | |||

| 7 | ||||

| 8 | ||||

| 10 | ||||

| 10 | ||||

| 12 | ||||

| 13 | ||||

| 13 | ||||

Comparison of Investment Objectives, Policies and Strategies | 14 | |||

| 15 | ||||

| 15 | ||||

| 17 | ||||

| 17 | ||||

| 17 | ||||

| 18 | ||||

| 18 | ||||

| 20 | ||||

| 22 | ||||

| 23 | ||||

| 23 | ||||

| 23 | ||||

| 23 | ||||

| 24 | ||||

| 25 | ||||

| 26 | ||||

| 28 | ||||

| 28 | ||||

| 28 | ||||

| 30 | ||||

| 31 | ||||

| 31 | ||||

| 32 | ||||

| 33 | ||||

| 33 | ||||

| 33 | ||||

| 34 | ||||

| 34 | ||||

| 34 | ||||

| 35 | ||||

| A-1 | ||||

| B-1 | ||||

| C-1 |

iv

You should read this entire Proxy Statement/Prospectus carefully. For additional information, you should consult the Reorganization Plan, a copy of which is attached hereto as Appendix A (the “Reorganization Plan”).

This Proxy Statement/Prospectus is soliciting shareholders with amounts invested in one or more of the Acquired Portfolios as of January 31, 2011 to approve the Reorganization Plan, whereby each Acquired Portfolio will be reorganized into the corresponding Acquiring Portfolio. (Each Acquired Portfolio and Acquiring Portfolio is sometimes referred to herein as a “Portfolio.”)

Each Acquired Portfolio’s shares are divided into two classes, designated Class IA and Class IB shares (“Acquired Portfolio Shares”). Each Acquiring Portfolio’s shares also are divided into two classes, designated Class IA and Class IB shares (“Acquiring Portfolio Shares”). The rights and preferences of each class of Acquiring Portfolio Shares are identical to the corresponding class of Acquired Portfolio Shares.

The Reorganization Plan provides, with respect to each Reorganization, for:

| • | the transfer of all of the assets of the Acquired Portfolio to the corresponding Acquiring Portfolio in exchange for Acquiring Portfolio Shares having an aggregate net asset value equal to the Acquired Portfolio’s net assets; |

| • | the Acquiring Portfolio’s assumption of all the liabilities of the Acquired Portfolio; |

| • | the distribution to the shareholders (for the benefit of the Separate Accounts, as applicable, and thus the Contractholders) of those Acquiring Portfolio Shares; and |

| • | the complete termination of the Acquired Portfolio. |

A comparison of the investment objective(s), investment policies, strategies and principal risks of each Acquired Portfolio and its corresponding Acquiring Portfolio is included in “Comparison of Investment Objectives, Policies and Strategies” and “Comparison of Principal Risk Factors” below. The Portfolios have identical distribution procedures, purchase procedures, exchange rights and redemption procedures, which are discussed in “Additional Information about the Acquiring Portfolios” below. Each Portfolio offers its shares to Separate Accounts and certain other eligible investors. Shares of each Portfolio are offered and redeemed at their net asset value without any sales load. You will not incur any sales loads or similar transaction charges as a result of a Reorganization.

Subject to shareholder approval, each Reorganization is expected to be effective at the close of business on May 6, 2011, or on a later date the Trust decides upon (the “Closing Date”). As a result of each Reorganization, each shareholder invested in shares of one or more of the Acquired Portfolios would become an owner of shares of the corresponding Acquiring Portfolio. Each such shareholder would hold, immediately after the Closing Date, Class IA or Class IB shares of the applicable Acquiring Portfolio having an aggregate value equal to the aggregate value of the Class IA or Class IB Acquired Portfolio Shares, as applicable, that were held by the shareholder as of the Closing Date. Similarly, each Contractholder whose Contract values are invested in shares of one or more of the Acquired Portfolios would become an indirect owner of shares of the corresponding Acquiring Portfolio. Each such Contractholder would indirectly hold, immediately after the Closing Date, Class IA or Class IB shares of the applicable Acquiring Portfolio having an aggregate value equal to the aggregate value of the Class IA or Class IB Acquired Portfolio Shares, as applicable, that were indirectly held by the Contractholder as of the Closing Date. The consummation of any one Reorganization is not contingent on the consummation of any other Reorganization. The Trust believes that there will be no adverse tax consequences to shareholders or Contractholders as a result of the Reorganizations. Please see “Additional Information about the Reorganizations – Federal Income Tax Consequences of the Reorganizations” below for further information.

1

The Board has unanimously approved the Reorganization Plan with respect the Portfolios involved therein. Accordingly, the Board is submitting the Reorganization Plan for approval by each Acquired Portfolio’s shareholders. In considering whether to approve a proposal (a “Proposal”), you should review the Proposal for the Acquired Portfolio(s) in which you were a direct or indirect holder on the Record Date (as defined under “Voting Information”). In addition, you should review the information in this Proxy Statement/Prospectus that relates to all of the Proposals and the Reorganization Plan generally. The Board recommends that you vote “FOR” the Proposals to approve the Reorganization Plan.

| PROPOSAL 1: | APPROVAL OF THE REORGANIZATION PLAN WITH RESPECT TO THE REORGANIZATION OF THE CAPITAL GUARDIAN GROWTH PORTFOLIO INTO THE GROWTH PLUS PORTFOLIO. |

This Proposal 1 requests your approval of the Reorganization Plan, pursuant to which the Capital Guardian Growth Portfolio will be reorganized into the Growth PLUS Portfolio.

In considering whether you should approve this Proposal, you should note that:

��

| • | The Portfolios have identical investment objectives. Each Portfolio seeks long-term growth of capital. |

| • | The Portfolios have substantially similar investment policies. Each Portfolio invests primarily in large-cap equity securities. In addition, each Portfolio seeks to invest primarily in securities of companies that have “growth” characteristics (e.g., higher forecasted growth values and/or higher price-to-book ratios). Each Portfolio also may invest in foreign securities, derivatives (e.g., futures contracts) and exchange-traded funds (“ETFs”). There are, however, differences in the Portfolios’ primary investment policies and strategies of which you should be aware. |

One primary difference between the two Portfolios is that the Growth PLUS Portfolio normally allocates its assets among three investment advisers, each of which manages its portion of the Portfolio using a different but complementary investment strategy. One portion of the Growth PLUS Portfolio is actively managed by an investment sub-adviser (“Adviser”) (the “Active Allocated Portion”); one portion of the Portfolio seeks to track the performance of a particular index (the “Index Allocated Portion”); and one portion of the Portfolio invests in ETFs (the “ETF Allocated Portion”). The Capital Guardian Growth Portfolio is actively managed by one Adviser and does not have an Index Allocated Portion or ETF Allocated Portion; however, each Portfolio uses the Russell 1000 Growth Index as its benchmark index. The Capital Guardian Portfolio also may invest, to a limited extent, in ETFs.

In addition, while each Portfolio may invest in derivatives, the Growth PLUS Portfolio may invest in derivatives to a greater extent than the Capital Guardian Growth Portfolio and normally uses derivatives to a greater extent than the Capital Guardian Growth Portfolio to manage the Portfolio’s equity exposure (the “tactical strategy”).

Also, while each Portfolio may invest in foreign securities, the Active Allocated Portion of the Growth PLUS Portfolio may invest up to 25% of its total assets in securities of foreign issuers, while the Capital Guardian Growth Portfolio does not have a stated limit with respect to investments in foreign securities. For a detailed comparison of the each Portfolio’s investment policies and strategies, see “Comparison of Investment Objectives, Policies and Strategies” below.

| • | The Portfolios also have comparable risk profiles, although there are differences of which you should be aware. Each Portfolio’s principal risks include equity risk, foreign securities risk (including currency risk), investment style risk and large-cap company risk. The Capital Guardian Growth Portfolio, however, also is subject to depositary receipts risk and mid-cap and small-cap company risk, while the Growth PLUS Portfolio generally is not. In addition, the principal risks of investing in the Growth PLUS Portfolio also include derivatives risk, emerging markets risk, ETF risk, focused portfolio risk, index strategy risk and portfolio turnover risk, which are not principal risks of investing in the Capital Guardian Growth Portfolio. For a detailed comparison of the each Portfolio’s risks, see “Comparison of Principal Risk Factors” below. |

2

| • | AXA Equitable (the “Manager”) serves as the investment manager and administrator for each Portfolio and would continue to manage and administer the Growth PLUS Portfolio after the Reorganization. AXA Equitable has received an exemptive order from the SEC that generally permits AXA Equitable and the Board to appoint, dismiss and replace each Portfolio’s Adviser(s) and to amend the advisory agreements between AXA Equitable and the Advisers without obtaining shareholder approval (except with respect to Affiliated Advisers (as defined herein)). AXA Equitable has appointed one Adviser to manage the assets of the Capital Guardian Growth Portfolio. In particular, Capital Guardian Trust Company currently serves as the Adviser for the Capital Guardian Growth Portfolio. AXA Equitable has appointed two Advisers to manage distinct portions of the Growth PLUS Portfolio’s assets. In particular, Marsico Capital Management, LLC, which is responsible for the management of the Active Allocated Portion of the Growth PLUS Portfolio, and BlackRock Investment Management, LLC, which is responsible for the Index Allocated Portion of the Growth PLUS Portfolio, currently serve as Advisers to the Growth PLUS Portfolio and it is anticipated that they will continue to advise their respective portion of the Growth PLUS Portfolio after the Reorganization. In addition, AXA Equitable is responsible for the management of the ETF Allocated Portion of the Growth PLUS Portfolio and the implementation of the tactical strategy, and it is anticipated that it would continue to manage the ETF Allocated Portion and implement the tactical strategy for the Growth PLUS Portfolio after the Reorganization. For a detailed description of the Manager and the Growth PLUS Portfolio’s Advisers, please see “Additional Information about the Acquiring Portfolios - The Manager” and “- The Advisers” below. |

| • | The Capital Guardian Growth Portfolio and Growth PLUS Portfolio had net assets of approximately $351.1 million and $1.74 billion, respectively, as of October 31, 2010. Thus, if the Reorganization had been in effect on that date, the combined Portfolio would have had net assets of approximately $2.09 billion. |

| • | Class IA shareholders of the Capital Guardian Portfolio will receive Class IA shares of the Growth PLUS Portfolio, and Class IB shareholders of the Capital Guardian Portfolio will receive Class IB shares of the Growth PLUS Portfolio, pursuant to the Reorganization. Shareholders will not pay any sales charges in connection with the Reorganization. Please see “Comparative Fee and Expense Tables,” “Additional Information about the Reorganizations” and “Additional Information about the Acquiring Portfolios” below for more information. |

| • | It is estimated that the annual operating expense ratios for the Growth PLUS Portfolio’s Class IA and Class IB shares, for the fiscal year following the Reorganization, will be the same as those of the Capital Guardian Growth Portfolio’s Class IA and Class IB shares, respectively, for the fiscal year ended December 31, 2009. For a more detailed comparison of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the Acquiring Portfolios” below. |

| • | The maximum management fee for the Capital Guardian Growth Portfolio is equal to an annual rate of 0.65% of its average daily net assets, while the maximum management fee for the Growth PLUS Portfolio is equal to an annual rate of 0.50% of its average daily net assets. The administration fee schedule for the Capital Guardian Portfolio is $30,000 per year, plus its proportionate share of an asset-based administration fee for the Trust, which is equal to an annual rate of 0.12% of the first $3 billion of total Trust average daily net assets (exclusive of certain Portfolios, including the Growth PLUS Portfolio), 0.11% of the next $3 billion, 0.105% of the next $4 billion, 0.10% of the next $20 billion and 0.0975% thereafter. The Growth PLUS Portfolio pays AXA Equitable an annual fee of $32,500 plus its proportionate share of an asset-based administration fee, which is equal to an annual rate of 0.15% of the first $20 billion of the Growth PLUS Portfolio’s and certain other of the Trust’s multi-adviser portfolios’ aggregate average daily net assets, 0.125% of the next $5 billion of these portfolios’ aggregate average daily net assets, and 0.10% on these portfolios’ aggregate average daily net assets thereafter, and an additional $32,500 for each portion of the Growth PLUS Portfolio for which separate administrative services are provided (e.g., portions of the Growth PLUS Portfolio allocated to separate Advisers and/or managed in a discrete style). For a more detailed description of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the Acquiring Portfolios” below. |

3

| • | Following the Reorganization, the combined Portfolio will be managed in accordance with the investment objective, policies and strategies of the Growth PLUS Portfolio. It is not expected that the Growth PLUS Portfolio will revise any of its investment policies following the Reorganization to reflect those of the Capital Guardian Growth Portfolio. AXA Equitable has reviewed Capital Guardian Growth Portfolio’s current portfolio holdings and determined that all or a substantial portion of the Capital Guardian Growth Portfolio’s holdings is consistent with the Growth PLUS Portfolio’s investment objectives and policies and thus, if the Reorganization is approved, could be transferred to and held by the Growth PLUS Portfolio. However, it is expected that some of those holdings may not remain at the time of the Reorganization due to normal portfolio turnover. If the Reorganization is approved, the Manager will liquidate the Capital Guardian Growth Portfolio’s holdings that, based on market conditions and an assessment by the Manager and the Growth PLUS Portfolio’s Advisers, are not compatible with the Growth PLUS Portfolio’s current portfolio composition, investment objective and policies, or investment strategies. The proceeds of such liquidation will be held in temporary investments or reinvested in assets that are consistent with the Growth PLUS Portfolio’s investment objective, policies and strategies. Although any sale of portfolio investments in connection with the Reorganization would be conducted in an orderly manner, the need for a Portfolio to sell such investments may result in its selling securities at a disadvantageous time and price and could result in the Portfolio realizing gains (or losses) that otherwise would not have been realized and incurring transaction costs that otherwise would not have been incurred. |

| • | The Capital Guardian Growth Portfolio will bear its proportionate share of the expenses of the Reorganizations described in this Proxy Statement/Prospectus, subject to an aggregate maximum of $100,000 for the Acquired Portfolios. AXA Equitable generally will bear expenses of the Reorganizations in excess of this amount, subject to certain limitations. Please see “Additional Information about the Reorganizations” below for more information. |

Comparative Fee and Expense Tables

The following tables show the fees and expenses of each class of shares of each Portfolio and the estimated pro forma fees and expenses of each class of shares of the Acquiring Portfolio after giving effect to the proposed Reorganization. Fees and expenses for each Portfolio are based on those incurred by each class of its shares for the fiscal year ended December 31, 2009. The pro forma fees and expenses of the Acquiring Portfolio Shares assume that the Reorganization has been in effect for the last year ended June 30, 2010. The tables below do not reflect any Contract-related fees and expenses, which would increase overall fees and expenses. See a Contract prospectus for a description of those fees and expenses.

Shareholder Fees

(fees paid directly from your investment)

| Capital Guardian Growth Portfolio | Growth PLUS Portfolio | Pro Forma Growth PLUS Portfolio (assuming the Reorganization is approved) | ||||

| Not applicable. | ||||||

Annual Operating Expenses

(expenses that you may pay each year as a percentage of the value of your investment)

| Capital Guardian Growth Portfolio | Growth PLUS Portfolio | Pro Forma Growth PLUS Portfolio (assuming the Reorganization is approved) | ||||||||||||||||||||||

| Class IA | Class IB | Class IA | Class IB | Class IA | Class IB | |||||||||||||||||||

Management Fee | 0.65 | % | 0.65 | % | 0.50 | % | 0.50 | % | 0.50 | % | 0.50 | % | ||||||||||||

Distribution and/or Service Fees (12b-1 fees) | None | 0.25 | % | None | 0.25 | % | None | 0.25 | % | |||||||||||||||

Other Expenses | 0.16 | % | 0.16 | % | 0.20 | % | 0.20 | % | 0.18 | % | 0.18 | % | ||||||||||||

Acquired Fund Fees and Expenses | N/A | N/A | 0.02 | % | 0.02 | % | 0.02 | % | 0.02 | % | ||||||||||||||

4

Total Annual Portfolio Operating Expenses | 0.81 | % | 1.06 | % | 0.72 | % | 0.97 | % | 0.70 | % | 0.95 | % | ||||||||||||

Fee Waiver and Expense Reimbursement† | -0.11 | % | -0.11 | % | N/A | N/A | N/A | N/A | ||||||||||||||||

Net Annual Portfolio Operating Expenses After Fee Waiver and/or Expense Reimbursement | 0.70 | % | 0.95 | % | 0.72 | % | 0.97 | % | 0.70 | % | 0.95 | % |

| † | The expense reimbursement or fee waiver is expected to continue until April 30, 2012, unless the Board of Trustees consents to an earlier revision or termination. The expense reimbursement or fee waiver may be terminated by AXA Equitable at any time after that date. |

This example is intended to help you compare the costs of investing in the Portfolios with the cost of investing in other investment options. The example assumes that:

| • | You invest $10,000 in a Portfolio for the time periods indicated; |

| • | Your investment has a 5% return each year; |

| • | The Portfolio’s operating expenses remain the same; and |

| • | The expense limitation currently in effect is not renewed. |

This example does not reflect any Contract-related fees and expenses, including redemption fees (if any) at the Contract level. If such fees and expenses were reflected, the total expenses would be higher. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

Capital Guardian Growth Portfolio | ||||||||||||||||

Class IA | $ | 72 | $ | 248 | $ | 439 | $ | 991 | ||||||||

Class IB | $ | 97 | $ | 326 | $ | 574 | $ | 1,284 | ||||||||

Growth PLUS Portfolio | ||||||||||||||||

Class IA | $ | 74 | $ | 230 | $ | 401 | $ | 894 | ||||||||

Class IB | $ | 99 | $ | 309 | $ | 536 | $ | 1,190 | ||||||||

Pro Forma Growth PLUS Portfolio (assuming the Reorganization is approved) | ||||||||||||||||

Class IA | $ | 72 | $ | 224 | $ | 390 | $ | 871 | ||||||||

Class IB | $ | 97 | $ | 303 | $ | 525 | $ | 1,166 | ||||||||

Each Portfolio pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the example, affect a Portfolio’s performance. During the fiscal year ended December 31, 2009, the portfolio turnover rate for the Capital Guardian Growth Portfolio and Growth PLUS Portfolio was 50% and 43%, respectively, of the average value of the Portfolio.

Comparison of Investment Objectives, Policies and Strategies

The following table compares the investment objectives and principal investment policies and strategies of the Capital Guardian Growth Portfolio with those of the Growth PLUS Portfolio. The Board may change the investment objective of a Portfolio without a vote of the Portfolio’s shareholders. For more detailed information about each Portfolio’s investment strategies and risk, see Appendix B.

5

Acquiring Portfolio | Acquired Portfolio | |

| Growth PLUS Portfolio | Capital Guardian Growth Portfolio | |

| Investment Objective | ||

Seeks to provide long-term growth of capital. | Same. | |

| Principal Investment Strategies | ||

Under normal circumstances, the Portfolio intends to invest at least 80% of its net assets, plus borrowings for investment purposes, in securities of large-cap companies (or other financial instruments that derive their value from the securities of such companies).

For this Portfolio, large-cap companies mean those companies with market capitalizations within the range of the following indices at the time of purchase: S&P 500 Index (market capitalization range of approximately $1.1 billion - $322.7 billion as of December 31, 2009), Russell 1000 Index (market capitalization range of approximately $262.5 million - $322.7 billion as of December 31, 2009), S&P 100 Index (market capitalization range of approximately $6.3 billion - $322.7 billion as of December 31, 2009) Morningstar Large Core Index (market capitalization range of approximately $9.7 billion - $203.7 billion), NYSE 100 Index (market capitalization $14.4 billion - $322.7 billion as of December 31, 2009). | The Adviser seeks to achieve the Portfolio’s investment objective by investing primarily in equity securities of U.S. issuers and securities whose principal markets are in the U.S., including American Depository Receipts (“ADRs”) and other U.S.-registered foreign securities.

The Portfolio normally is invested primarily in common stocks or other equity securities of companies with market capitalization greater than $1.5 billion at the time of purchase. | |

| The Portfolio’s assets normally are allocated among three investment managers, each of which manages its portion of the Portfolio using a different but complementary investment strategy. One portion of the Portfolio is an Active Allocated Portion; one portion of the Portfolio is an Index Allocated Portion; and one portion of the Portfolio is an ETF Allocated Portion. Under normal circumstances, the Active Allocated Portion consists of approximately 30% of the Portfolio’s net assets, the Index Allocated Portion consists of approximately 60% of the Portfolio’s net assets and the ETF Allocated Portion consists of approximately 10% of the Portfolio’s net assets. Actual allocations among the distinct portions of the Portfolio may deviate from the amounts shown above by up to 15% of the Portfolio’s net assets. | No corresponding strategy. | |

| The Active Allocated Portion primarily invests in common stocks, but it also may invest in other equity securities that the Adviser believes provide opportunities for capital appreciation. | The Portfolio normally is invested primarily in common stocks or other equity securities. | |

| The Active Allocated Portion may also invest up to 25% of its total assets in securities of foreign issuers (which may include up to 15% of its total assets in emerging market countries at the time of purchase), which may be publicly traded in the United States or on a foreign exchange, and may be denominated in a foreign currency. | The Portfolio also may invest in foreign securities. | |

| The Active Allocated Portion also may engage in active and frequent trading to achieve the Portfolio’s investment objective. | No corresponding strategy. | |

6

| In choosing investments, the Adviser utilizes a “focus” style, which concentrates the Active Allocated Portion’s investments in a core position of 20-30 companies selected for their growth potential. | The Adviser seeks to invest primarily in securities that at the time of purchase exhibit one or more “growth” characteristics. | |

| The Index Allocated Portion of the Portfolio seeks to track the performance (before fees and expenses) of the Russell 1000 Growth with minimal tracking error. Generally, the Index Allocated Portion uses a full replication technique, although in certain instances a sampling approach may be utilized for a portion of the Index Allocated Portion. The Index Allocated Portion also may invest in other instruments, such as futures and options contracts, that provide comparable exposure as the index without buying the underlying securities comprising the index. | No corresponding strategy. | |

| AXA Equitable also may utilize futures and options to manage equity exposure. When market volatility is increasing above specific thresholds set for the Portfolio, the Manager may limit equity exposure either by reducing investments in securities, selling long futures and options positions on an index, increasing cash levels, and/or shorting an index. The Portfolio may invest up to 25% of its assets in derivatives, such as exchange-traded futures, and options contracts on indices or other similar investments. | No corresponding strategy; however, the Portfolio may invest, to a limited extent, in derivatives. | |

| The ETF Allocated Portion invests in ETFs that meet the investment criteria of the Portfolio as a whole. | The Portfolio may invest, to a limited extent, in ETFs. | |

Comparison of Principal Risk Factors

An investment in a Portfolio is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. You may lose money by investing in a Portfolio. The following table compares the principal risks of an investment in each Portfolio. For an explanation of each such risk, see “Additional Information about the Reorganizations – Description of Risk Factors” below.

7

Risks | Growth PLUS Portfolio | Capital Guardian Growth Portfolio | ||

Currency Risk | X | X | ||

Depositary Receipts | X | |||

Derivatives Risk | X | |||

Emerging Markets Risk | X | |||

Equity Risk | X | X | ||

ETF Risk | X | |||

Focused Portfolio Risk | X | |||

Foreign Securities Risk | X | X | ||

Index Strategy Risk | X | |||

Investment Style Risk | X | X | ||

Large-Cap Company Risk | X | X | ||

Mid-Cap and Small-Cap Company Risk | X | |||

Portfolio Turnover Risk | X | |||

Comparative Performance Information

The bar charts and table below provide some indication of the risks of investing in each Portfolio by showing changes in the Portfolio’s performance from year to year and by showing how the Portfolios’ average annual total returns for the past one, five and ten years through December 31, 2009 compare to the returns of a broad-based market index. Past performance is not an indication of future performance.

The performance results do not reflect any Contract-related fees and expenses, which would reduce the performance results.

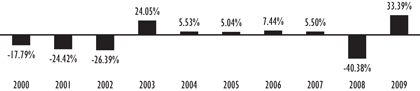

| Capital Guardian Growth Portfolio – Calendar Year Total Returns (Class IB) | ||||||||||||||||||

| ||||||||||||||||||

| Best Quarter (% and time period) | Worst Quarter (% and time period) | |||||||||||||||||

| 17.15% (2009 2nd Quarter) | -26.21% (2008 4th Quarter) | |||||||||||||||||

8

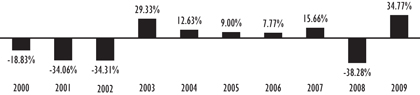

| Growth PLUS Portfolio – Calendar Year Total Returns (Class IB) | ||||||||||||||||||

| ||||||||||||||||||

Best Quarter (% and time period) | Best Quarter (% and time period) -28.50% (2001 3rdQuarter) | |||||||||||||||||

Capital Guardian Growth Portfolio - Average Annual Total Returns (For the periods ended December 31, 2009)

| ||||||

| One Year | Five Years | Ten Years | ||||

Capital Guardian Growth Portfolio – Class IA* | 33.73% | -0.84% | -5.35% | |||

Capital Guardian Growth Portfolio – Class IB | 33.39% | -1.09% | -5.52% | |||

Russell 1000 Growth Index† | 37.21% | 1.63% | -3.99% | |||

Growth PLUS Portfolio - Average Annual Total Returns (For the periods ended December 31, 2009)

| ||||||

| One Year | Five Years | Ten Years | ||||

Growth PLUS Portfolio – Class IA | 33.93% | 2.83% | -5.04% | |||

Growth PLUS Portfolio – Class IB | 34.77% | 2.50% | -5.31% | |||

Russell 1000 Growth Index† | 37.21% | 1.63% | 3.99% | |||

| * | For periods prior to the date Class IA shares commenced operations (October 2, 2002), Class IA share performance information shown is the performance of Class IB shares which reflects the effect of 12b-1 fees paid by Class IB shares. Class IA shares do not pay 12b-1 fees. |

| † | The Russell 1000 Growth Index is an unmanaged index of common stocks that measures the performance of those Russell 1000 Index companies with lower price to book ratios and lower forecasted growth values. The Russell 1000 Index is an unmanaged index of common stocks that measures the performance of approximately 100 of the largest companies in the Russell 3000 Index, and represents approximately 90% of the total market capitalization of the Russell 3000 Index. |

9

The following table shows the capitalization of each Portfolio as of June 30, 2010 and of the Growth PLUS Portfolio on a pro forma combined basis as of June 30, 2010 after giving effect to the proposed Reorganization.

| Net Assets (in millions) | Net Asset Value Per Share | Shares Outstanding | ||||||||||

Capital Guardian Growth Portfolio – Class IA | $ | 1.0 | $ | 10.52 | 97,067 | |||||||

Growth PLUS Portfolio – Class IA | $ | 851.7 | $ | 13.60 | 62,619,171 | |||||||

Adjustments* | — | — | (21,959 | ) | ||||||||

Pro forma Growth PLUS Portfolio – Class IA (assuming the Reorganization is approved) | $ | 852.7 | $ | 13.60 | 62,694,279 | |||||||

Capital Guardian Growth Portfolio – Class IB | $ | 309.2 | $ | 10.51 | 29,435,313 | |||||||

Growth PLUS Portfolio – Class IB | $ | 591.5 | $ | 13.22 | 44,734,875 | |||||||

Adjustments* | — | — | (6,047,359 | ) | ||||||||

Pro forma Growth PLUS Portfolio – Class IB (assuming the Reorganization is approved) | $ | 900.7 | $ | 13.22 | 68,122,829 | |||||||

| * | The Capital Guardian Growth Portfolio will bear its proportionate share of the expenses of the Reorganizations described in this Proxy Statement/Prospectus, subject to an aggregate maximum of $100,000 for the Acquired Portfolios. AXA Equitable generally will bear expenses of the Reorganizations in excess of this amount, subject to certain limitations. For additional information, please refer to “Additional Information About the Reorganizations - Terms of the Reorganization Plan” below. |

After careful consideration, the Board unanimously approved the Reorganization Plan with respect to the Capital Guardian Growth Portfolio. Accordingly, the Board has submitted the Reorganization Plan for approval by this Portfolio’s shareholders. The Board recommends that you vote “FOR” Proposal 1.

* * * * *

| PROPOSAL 2: | APPROVAL OF THE REORGANIZATION PLAN WITH RESPECT TO THE REORGANIZATION OF THE LORD ABBETT GROWTH AND INCOME PORTFOLIO INTO THE LARGE CAP VALUE INDEX PORTFOLIO. |

This Proposal 2 requests your approval of the Reorganization Plan, pursuant to which the Lord Abbett Growth and Income Portfolio will be reorganized into the Large Cap Value Index Portfolio.

In considering whether you should approve this Proposal, you should note that:

| • | The Portfolios have similar investment objectives. Each Portfolio seeks a combination of capital appreciation and income. The Large Cap Value Index Portfolio, however, seeks to achieve a total return before expenses that approximates the total return performance of the Russell 1000 Value Index, including reinvestment of dividends, at a risk level consistent with that of the Russell 1000 Value Index. The Lord Abbett Growth and Income Portfolio seeks capital appreciation and growth of income without excessive fluctuation in market value. |

| • | The Portfolios also have similar investment policies. Each Portfolio invests primarily in equity securities of large capitalization companies that are considered to be undervalued. However, there are differences in their primary investment policies and strategies of which you should be aware. |

The Large Cap Value Index Portfolio is an index portfolio, while the Lord Abbett Growth and Income Portfolio is an actively managed portfolio. The Lord Abbett Growth and Income Portfolio is managed in a value style under which the Portfolio invests primarily in equity securities of large companies that the Adviser believes are underpriced. In contrast, the Large Cap Value Index Portfolio is constructed and maintained

10

generally by utilizing a replication construction technique, which means that the Portfolio seeks to hold all of the securities in the Russell 1000 Value Index in the approximate weight each represents in the index. Accordingly, the Large Cap Value Index Portfolio will remain substantially fully invested in common stocks even when the common stock prices are falling and the adverse performance of a stock ordinarily will not result in its elimination from the Portfolio. The Lord Abbett Growth and Income Portfolio is not similarly constrained.

In addition, the Lord Abbett Growth and Income Portfolio may invest, without limit, in American Depositary Receipts and similar depositary receipts and may invest up to 10% of its net assets in other foreign securities that are primarily traded outside of the United States; the Large Cap Value Index Portfolio generally does not invest in depositary receipts or foreign securities. For a detailed comparison of each Portfolio’s investment policies and strategies, see “Comparison of Investment Objectives, Policies and Strategies” below.

| • | The Portfolios also have comparable risk profiles, although there are differences in the principal risks. Each Portfolio’s principal risks include equity risk, large-cap company risk and investment style risk. The Large Cap Value Index Portfolio, however, also is subject to index strategy risk as a principal risk, which is not a principal risk of the Lord Abbett Growth and Income Portfolio. In addition, the Lord Abbett Growth and Income Portfolio is also subject to currency risk, depositary receipts risk, emerging markets risk and foreign securities risk as principal risks, which are not principal risks of the Large Cap Value Index Portfolio. For a detailed comparison of the each Portfolio’s risks, see “Comparison of Principal Risk Factors” below. |

| • | AXA Equitable (the “Manager”) serves as the investment manager and administrator for each Portfolio and would continue to manage and administer the Large Cap Value Index Portfolio after the Reorganization. AXA Equitable has received an exemptive order from the SEC that generally permits AXA Equitable and the Board to appoint, dismiss and replace each Portfolio’s Adviser(s) and to amend the advisory agreements between AXA Equitable and the Advisers without obtaining shareholder approval (except with respect to Affiliated Advisers (as defined herein)). AXA Equitable has appointed one Adviser, Lord, Abbett & Co. LLC, to manage the assets of the Lord Abbett Growth and Income Portfolio. AXA Equitable has appointed one Adviser, SSgA Funds Management, Inc., to manage the Large Cap Value Index Portfolio, and it is anticipated that this Adviser will continue to advise the Large Cap Value Index Portfolio after the Reorganization. For a detailed description of the Manager and the Large Cap Value Index Portfolio’s Adviser, please see “Additional Information about the Acquiring Portfolios - The Manager” and “- The Advisers” below. |

| • | The Lord Abbett Growth and Income Portfolio and Large Cap Value Index Portfolio had net assets of approximately $194.3 million and $135.3 million, respectively, as of October 31, 2010. Thus, if the Reorganization had been in effect on that date, the combined Portfolio would have had net assets of approximately $329.6 million. |

| • | Class IA shareholders of the Lord Abbett Growth and Income Portfolio will receive Class IA shares of the Large Cap Value Index Portfolio, and Class IB shareholders of the Lord Abbett Growth and Income Portfolio will receive Class IB shares of the Large Cap Value Index Portfolio, pursuant to the Reorganization. Shareholders will not pay any sales charges in connection with the Reorganization. Please see “Comparative Fee and Expense Tables,” “Additional Information about the Reorganizations” and “Additional Information about the Acquiring Portfolios” below for more information. |

| • | It is estimated that the annual operating expense ratios for the Large Cap Value Index Portfolio’s Class IA and Class IB shares, immediately following the Reorganization, will be lower than those of the Lord Abbett Growth and Income Portfolio’s Class IA and Class IB shares, respectively, for the fiscal year ended December 31, 2009. For a more detailed comparison of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the Acquiring Portfolios” below. |

11

| • | The maximum management fee for the Lord Abbett Growth and Income Portfolio is equal to an annual rate of 0.65% of its average daily net assets, while the maximum management fee for the Large Cap Value Index Portfolio is equal to an annual rate of 0.35% of its average daily net assets. The Portfolios are subject to the same administration fee, which is equal to $30,000 per year plus the Portfolio’s proportionate share of the Trust’s administration fee for portfolios with a single Adviser, which is equal to an annual rate of 0.12% of the first $3 billion of the Trust’s average daily net assets (exclusive of certain portfolios), 0.11% of the next $3 billion, 0.105% of the next $4 billion, 0.10% of the next $20 billion and 0.0975% thereafter. For a more detailed description of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the Acquiring Portfolios” below. |

| • | Following the Reorganization, the combined Portfolio will be managed in accordance with the investment objective, policies and strategies of the Large Cap Value Index Portfolio. It is not expected that the Large Cap Value Index Portfolio will revise any of its investment policies following the Reorganization to reflect those of the Lord Abbett Growth and Income Portfolio. AXA Equitable has reviewed Lord Abbett Growth and Income Portfolio’s current portfolio holdings and determined that, because both Portfolios invest in equity securities of large capitalization companies that are considered undervalued, a portion of the Lord Abbett Growth and Income Portfolio’s holdings are consistent with the Large Cap Value Index Portfolio’s current portfolio composition, investment objectives and policies and, thus, could be transferred to and held by the Large Cap Value Index Portfolio if the Reorganization is approved. However, it is expected that some of those holdings may not remain at the time of the Reorganization due to normal portfolio turnover. If the Reorganization is approved, the Manager will liquidate that portion of the Lord Abbett Growth and Income Portfolio’s holdings that, based on market conditions and an assessment by the Manager and the Large Cap Value Index Portfolio’s Adviser, is not compatible with the Large Cap Value Index Portfolio’s current portfolio composition, investment objective and policies, or investment strategies. The proceeds of such liquidation will be held in temporary investments or reinvested in assets that are consistent with the Large Cap Value Index Portfolio’s investment objective, policies and strategies. Although any sale of portfolio investments in connection with the Reorganization would be conducted in an orderly manner, the need for a Portfolio to sell such investments may result in its selling securities at a disadvantageous time and price and could result in the Portfolio realizing gains (or losses) that otherwise would not have been realized and incurring transaction costs that otherwise would not have been incurred. |

| • | The Lord Abbett Growth and Income Portfolio will bear its proportionate share of the expenses of the Reorganizations described in this Proxy Statement/Prospectus, subject to an aggregate maximum of $100,000 for the Acquired Portfolios. AXA Equitable generally will bear expenses of the Reorganizations in excess of this amount, subject to certain limitations. Please see “Additional Information about the Reorganizations” below for more information. |

Comparative Fee and Expense Tables

The following tables show the fees and expenses of each class of shares of each Portfolio and the estimated pro forma fees and expenses of each class of shares of the Acquiring Portfolio after giving effect to the proposed Reorganization. Fees and expenses for each Portfolio are based on those incurred by each class of its shares for the fiscal year ended December 31, 2009. The pro forma fees and expenses of the Acquiring Portfolio Shares assume that the Reorganization has been in effect for the last year ended on June 30, 2010. The tables below do not reflect any Contract-related fees and expenses, which would increase overall fees and expenses. See a Contract prospectus for a description of those fees and expenses.

12

Shareholder Fees

(fees paid directly from your investment)

| Lord Abbett Growth and Income Portfolio | Large Cap Value Index Portfolio | Pro Forma Large Cap Value Index Portfolio (assuming the Reorganization is approved) | ||||

Not applicable. | ||||||

Annual Operating Expenses

(expenses that you may pay each year as a percentage of the value of your investment)

| Lord Abbett Growth and Income Portfolio | Large Cap Value Index Portfolio | Pro Forma Large Cap Value Index Portfolio (assuming the Reorganization is approved) | ||||||||||||||||||||||

| Class IA | Class IB | Class IA | Class IB | Class IA | Class IB | |||||||||||||||||||

Management Fee | 0.65 | % | 0.65 | % | 0.35 | % | 0.35 | %% | 0.35 | % | 0.35 | % | ||||||||||||

Distribution and/or Service Fees (12b-1 fees) | None | 0.25 | % | None | 0.25 | % | None | 0.25 | % | |||||||||||||||

Other Expenses | 0.18 | % | 0.18 | % | 0.15 | % | 0.15 | % | 0.16 | % | 0.16 | % | ||||||||||||

Total Annual Portfolio Operating Expenses | 0.83 | % | 1.08 | % | 0.50 | % | 0.75 | % | 0.51 | % | 0.76 | % | ||||||||||||

Fee Waiver and Expense Reimbursement† | -0.08 | % | -0.08 | % | N/A | N/A | N/A | N/A | ||||||||||||||||

Net Annual Portfolio Operating Expenses After Fee Waiver and/or Expense Reimbursement | 0.75 | % | 1.00 | % | 0.50 | % | 0.75 | % | 0.51 | % | 0.76 | % | ||||||||||||

| † | The expense reimbursement or fee waiver is expected to continue until April 30, 2012, unless the Board of Trustees consents to an earlier revision or termination. The expense reimbursement or fee waiver may be terminated by AXA Equitable at any time after that date. |

This example is intended to help you compare the costs of investing in the Portfolios with the cost of investing in other investment options. The example assumes that:

| • | You invest $10,000 in a Portfolio for the time periods indicated; |

| • | Your investment has a 5% return each year; |

| • | The Portfolio’s operating expenses remain the same; and |

| • | The expense limitation currently in effect is not renewed. |

This example does not reflect any Contract-related fees and expenses, including redemption fees (if any) at the Contract level. If such fees and expenses were reflected, the total expenses would be higher. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

Lord Abbett Growth and Income Portfolio | ||||||||||||||||

Class IA | $ | 77 | $ | 257 | $ | 453 | $ | 1,018 | ||||||||

Class IB | $ | 102 | $ | 336 | $ | 588 | $ | 1,310 | ||||||||

Large Cap Value Index Portfolio | ||||||||||||||||

Class IA | $ | 51 | $ | 160 | $ | 280 | $ | 628 | ||||||||

Class IB | $ | 77 | $ | 240 | $ | 417 | $ | 930 | ||||||||

Pro Forma Large Cap Value Index Portfolio (assuming the Reorganization is approved) | ||||||||||||||||

Class IA | $ | 52 | $ | 164 | $ | 285 | $ | 640 | ||||||||

Class IB | $ | 78 | $ | 243 | $ | 422 | $ | 942 | ||||||||

13

The Portfolio pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Portfolio’s performance. During the fiscal year ended December 31, 2009, the portfolio turnover rate for the Lord Abbett Growth and Income Portfolio and Large Cap Value Index Portfolio was 75% and 100%, respectively, of the average value of the Portfolio.

Comparison of Investment Objectives, Policies and Strategies

The following table compares the investment objectives and principal investment policies and strategies of the Lord Abbett Growth and Income Portfolio with those of the Large Cap Value Index Portfolio. The Board may change the investment objective of a Portfolio without a vote of the Portfolio’s shareholders. For more detailed information about each Portfolio’s investment strategies and risk, see Appendix B.

Acquiring Portfolio | Acquired Portfolio | |

| Large Cap Value Index Portfolio | Lord Abbett Growth and Income Portfolio | |

| Investment Objective | ||

| Seeks to achieve a total return before expenses that approximates the total return performance of the Russell 1000 Value Index, including reinvestment of dividends, at a risk level consistent with that of the Russell 1000 Value Index. | Seeks to achieve capital appreciation and growth of income without excessive fluctuation in market value. | |

| Principal Investment Strategies | ||

| The Portfolio normally invests at least 80% of its net assets, plus borrowings for investment purposes, in equity securities in the Russell 1000 Value Index. The Portfolio’s investments in equity securities in the Russell 1000 Value Index may include financial instruments that derive their value from such securities. The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. As of December 31, 2009, the market capitalization of companies in the Russell 1000 Value Index ranged from $262.5 million to $322.7 billion. | The Portfolio primarily invests in the equity securities of large, seasoned, U.S. and multinational companies that the Adviser believes are undervalued. Under normal circumstances, the Portfolio invests at least 80% of its net assets in equity securities of large companies. For this Portfolio, a large company is defined as a company having a market capitalization at the time of purchase that falls within the market capitalization range of companies in the Russell 1000 Index. As of December 31, 2009, the market capitalization range of the Russell 1000 Index was $262.5 million to $322.7 billion. This range varies daily. Equity securities in which the Portfolio may invest include common stocks, preferred stocks, convertible securities, warrants, and similar instruments. | |

| The Adviser does not anticipate utilizing customary economic, financial or market analyses or other traditional investment techniques to manage the Portfolio. The Portfolio is constructed and maintained by utilizing a replication construction technique. That is, the Portfolio seeks to hold all securities in the Russell 1000 Value Index in the approximate weight each represents in the Index, although in certain instances a sampling approach may be utilized. | In selecting investments, the Adviser attempts to invest in securities selling at reasonable prices in relation to its assessment of their potential value. The Adviser seeks to limit the Portfolio’s downside risk by investing in value stocks, which are stocks of companies that the Adviser believes are underpriced, and in large, seasoned companies, which tend to be less volatile than the stocks of smaller companies. | |

| The Portfolio will remain substantially fully invested in common stocks even when common stock prices are generally falling. Similarly, adverse performance of a stock will ordinarily not result in its elimination from the Portfolio. | The Adviser generally will sell a stock when it thinks it seems less likely to benefit from the current market and economic environment, shows deteriorating fundamentals or has reached the Adviser’s valuation target. | |

| No corresponding strategy. | The Portfolio may invest, without limit, in American Depositary Receipts and similar depositary receipts. The Portfolio limits its other investments in foreign securities that are primarily traded outside of the U.S. to 10% of its net assets. | |

14

Comparison of Principal Risk Factors

An investment in a Portfolio is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. You may lose money by investing in a Portfolio. The following table compares the principal risks of an investment in each Portfolio. For an explanation of each such risk, see “Additional Information about the Reorganizations – Description of Risk Factors” below.

Risks | Large Cap Value Index Portfolio | Lord Abbett Growth and Income Portfolio | ||

Currency Risk | X | |||

Depositary Receipts | X | |||

Emerging Markets Risk | X | |||

Equity Risk | X | X | ||

Foreign Securities Risk | X | |||

Index Strategy Risk | X | |||

Investment Style Risk | X | X | ||

Large-Cap Company Risk | X | X | ||

Comparative Performance Information

The bar charts and table below provide some indication of the risks of investing in each Portfolio by showing changes in the Portfolio’s performance from year to year and by showing how the Portfolios’ average annual total returns for the past one-year and since-inception periods through December 31, 2009 compare to the returns of a broad-based market index. Past performance is not an indication of future performance.

The performance results do not reflect any Contract-related fees and expenses, which would reduce the performance results.

15

| Lord Abbett Growth and Income Portfolio – Calendar Year Total Returns (Class IB) | ||||||||||

|

| |||||||||

| Best Quarter (% and time period) 18.23% (2009 2nd Quarter) | Worst Quarter (% and time period) -19.93% (2008 4th Quarter) | |||||||||

Large Cap Value Index Portfolio – Calendar Year Total Returns (Class IB) |

| |||||||||

|

| |||||||||

| Best Quarter (% and time period) 18.00% (2009 3rd Quarter) | Best Quarter (% and time period) -32.33% (2008 4th Quarter) | |||||||||

Lord Abbett Growth and Income Portfolio - Average Annual Total Returns (For the periods ended December 31, 2009)

|

| |||||||

| One Year | Since Inception (April 29, 2005) | |||||||

Lord Abbett Growth and Income Portfolio – Class IA | 18.33 | % | -0.29 | % | ||||

Lord Abbett Growth and Income Portfolio – Class IB | 18.14 | % | 0.51 | % | ||||

Russell 1000 Value Index† | 19.69 | % | 0.10 | % | ||||

Large Cap Value Index Portfolio - Average Annual Total Returns (For the periods ended December 31, 2009)

|

| |||||||

| One Year | Since Inception (October 3, 2005) | |||||||

Large Cap Value Index Portfolio – Class IA | 19.37 | % | -13.18 | % | ||||

Large Cap Value Index Portfolio – Class IB | 19.34 | % | -13.38 | % | ||||

Russell 1000 Value Index† | 19.69 | % | -1.57 | % | ||||

| † | Russell 1000® Value Index is an unmanaged index of common stocks that measures the performance of those Russell 1000 companies with lower price to book ratios and lower forecasted growth values. The Russell 1000 Index is an unmanaged index of common stocks that measures the performance of approximately 100 of the largest companies in the Russell 3000 Index, and represents approximately 90% of the total market capitalization of the Russell 3000 Index. |

16

The following table shows the capitalization of each Portfolio as of June 30, 2010 and of the Large Cap Value Index Portfolio on a pro forma combined basis as of June 30, 2010 after giving effect to the proposed Reorganization.

| Net Assets (in millions) | Net Asset Value Per Share | Shares Outstanding | ||||||||||

Lord Abbett Growth and Income Portfolio – Class IA | $ | 27.4 | $ | 8.41 | 3,262,539 | |||||||

Large Cap Value Index Portfolio – Class IA | $ | 2.8 | $ | 4.41 | 643,649 | |||||||

Adjustments* | — | — | 2,959,891 | |||||||||

Pro forma Large Cap Value Index Portfolio – Class IA (assuming the Reorganization is approved) | $ | 30.2 | $ | 4.41 | 6,866,079 | |||||||

Lord Abbett Growth and Income Portfolio – Class IB | $ | 144.1 | $ | 8.41 | 17,133,227 | |||||||

Large Cap Value Index Portfolio – Class IB | $ | 117.7 | $ | 4.39 | 26,827,888 | |||||||

Adjustments* | — | — | 15,681,261 | |||||||||

Pro forma Large Cap Value Index Portfolio – Class IB (assuming the Reorganization is approved) | $ | 261.8 | $ | 4.39 | 59,642,376 | |||||||