File No. 333-

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON FEBRUARY 20, 2015

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

| THE SECURITIES ACT OF 1933 | x | |||

| Pre-Effective Amendment No. | ¨ | |||

| Post-Effective Amendment No. | ¨ |

EQ ADVISORS TRUST

(Exact name of registrant as specified in charter)

1290 Avenue of the Americas

New York, New York 10104

(Address of principal executive offices)

(212) 554-1234

Registrant’s Telephone Number, including area code

STEVEN M. JOENK

AXA Equitable Funds Management Group, LLC

1290 Avenue of the Americas

New York, New York 10104

(Name and address of agent for service)

With copies to:

Patricia Louie, Esq. AXA Equitable Funds Management Group, LLC 1290 Avenue of the Americas New York, NY 10104 | Mark C. Amorosi, Esq. K&L Gates LLP 1601 K Street N.W. Washington, D.C. 20006 |

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes effective.

It is proposed that this Registration Statement will become effective on the 30th day after filing pursuant to Rule 488 under the Securities Act of 1933, as amended.

Title of securities being registered: Class IA and Class K shares of beneficial interest in the series of the registrant designated as the EQ/International Equity Index Portfolio.

No filing fee is required because the registrant is relying on Section 24(f) of the Investment Company Act of 1940, as amended, pursuant to which it has previously registered an indefinite number of shares (File Nos. 333-17217 and 811-07953).

EQ ADVISORS TRUST

CONTENTS OF REGISTRATION STATEMENT

This registration statement is comprised of the following:

Cover Sheet

Contents of Registration Statement

Letter to Shareholders

Notice of Special Meeting

Contractholder Voting Instructions

Part A – Proxy Statement and Prospectus

Part B – Statement of Additional Information

Part C – Other Information

Signature Page

Exhibits

AXA EQUITABLE LIFE INSURANCE COMPANY

1290 Avenue of the Americas

New York, New York 10104

, 2015

Dear Contractholder:

Enclosed is a notice and Combined Proxy Statement and Prospectus relating to a Special Meeting of Shareholders of EQ/International ETF Portfolio (the “ETF Portfolio”).

The ETF Portfolio is a series of EQ Advisors Trust (the “Trust”). The Special Meeting of Shareholders of the ETF Portfolio is scheduled to be held at the Trust’s offices, 1290 Avenue of the Americas, New York, New York 10104, on April 30, 2015 at , Eastern time (the “Meeting”). At the Meeting, the shareholders of the ETF Portfolio who are entitled to vote at the Meeting will be asked to approve the proposal described below.

The Trust’s Board of Trustees (the “Board”) has called the Meeting to request shareholder approval of the reorganization of the ETF Portfolio into the EQ/International Equity Index Portfolio, also a series of the Trust (the “Index Portfolio”) (the “Reorganization”).

The Board has approved the proposal and recommends that you vote “FOR” the proposal. Although the Board has determined that a vote “FOR” the proposal is in your best interest, the final decision is yours.

Each Portfolio is managed by AXA Equitable Funds Management Group, LLC. The Index Portfolio is sub-advised by an investment sub-adviser. If the Reorganization is approved and implemented, each Contractholder that invests indirectly in the ETF Portfolio will automatically become a Contractholder that invests indirectly in the Index Portfolio.

As an owner of a variable life insurance policy and/or a variable annuity contract or certificate that participates in the ETF Portfolio through the investment divisions of a separate account or accounts established by AXA Equitable Life Insurance Company (“AXA Equitable”), you are entitled to instruct AXA Equitable how to vote the ETF Portfolio shares related to your interest in those accounts as of the close of business on February 27, 2015. The attached Notice of Special Meeting of Shareholders and Combined Proxy Statement and Prospectus concerning the Meeting describe the matter to be considered at the Meeting.

You are cordially invited to attend the Meeting. Since it is important that your vote be represented whether or not you are able to attend, you are urged to consider these matters and to exercise your voting instructions by completing, dating, and signing the enclosed voting instruction card and returning it in the accompanying return envelope at your earliest convenience or by relaying your voting instructions via telephone or the Internet by following the enclosed instructions. For further information on how to instruct AXA Equitable, please see the Contractholder Voting Instructions included herein. Of course, we hope that you will be able to attend the Meeting, and if you wish, you may provide voting instructions in person, even though you may have already returned a voting instruction card or submitted your voting instructions via telephone or the Internet. Please respond promptly in order to save additional costs of proxy solicitation and in order to make sure you are represented.

Very truly yours,

Steven M. Joenk Managing Director AXA Equitable Life Insurance Company |

EQ ADVISORS TRUST

EQ/International ETF Portfolio

1290 Avenue of the Americas

New York, New York 10104

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS TO BE HELD ON APRIL 30, 2015

To the Shareholders:

NOTICE IS HEREBY GIVEN that a Special Meeting of Shareholders of the EQ/International ETF Portfolio (the “ETF Portfolio”), a series of EQ Advisors Trust (the “Trust”), will be held on April 30, 2015, at , Eastern time, at the offices of the Trust, located at 1290 Avenue of the Americas, New York, New York 10104 (the “Meeting”).

The Meeting will be held to act on the following proposal:

1. To approve the Plan of Reorganization and Termination adopted by the Board of Trustees of the Trust (the “Board”), with respect to the reorganization of the EQ/International ETF Portfolio, a series of the Trust, into the EQ/International Equity Index Portfolio, also a series of the Trust.

2. To transact other business that may properly come before the Meeting or any adjournments thereof.

The Board unanimously recommends that you vote in favor of the proposal.

Please note that owners of variable life insurance policies and/or variable annuity contracts or certificates (the “Contractholders”) issued by AXA Equitable Life Insurance Company (“AXA Equitable”), who have invested in shares of the ETF Portfolio through the investment divisions of a separate account or accounts of AXA Equitable will be given the opportunity, to the extent required by law, to provide voting instructions on the above proposal.

You should read the Combined Proxy Statement and Prospectus attached to this notice prior to completing your proxy or voting instruction card. The record date for determining the number of shares outstanding, the shareholders entitled to vote and the Contractholders entitled to provide voting instructions at the Meeting and any adjournments or postponements thereof has been fixed as the close of business on February 27, 2015. If you attend the Meeting, you may vote or provide your voting instructions in person.

i

YOUR VOTE IS IMPORTANT

Please return your proxy or voting instruction card promptly

Regardless of whether you plan to attend the Meeting, you should vote or provide voting instructions by promptly completing, dating, and signing the enclosed proxy or voting instruction card and returning it in the enclosed postage-paid envelope. You also can vote or provide voting instructions through the Internet or by telephone using the 16-digit control number that appears on the enclosed proxy or voting instruction card and following the simple instructions. If you are present at the Meeting, you may change your vote or voting instructions, if desired, at that time. The Board recommends that you vote or provide voting instructions to vote “FOR” the proposal.

By order of the Board,

Patricia Louie Vice President and Secretary |

Dated: , 2015

New York, New York

ii

AXA EQUITABLE LIFE INSURANCE COMPANY

CONTRACTHOLDER VOTING INSTRUCTIONS

REGARDING A SPECIAL MEETING OF SHAREHOLDERS OF

EQ/INTERNATIONAL ETF PORTFOLIO,

A SERIES OF EQ ADVISORS TRUST

TO BE HELD ON APRIL 30, 2015

Dated: , 2015

GENERAL

These Contractholder Voting Instructions are being furnished by AXA Equitable Life Insurance Company (“AXA Equitable”) to owners of its variable life insurance policies or variable annuity contracts or certificates (the “Contracts”) (the “Contractholders”) who, as of February 27, 2015 (the “Record Date”), had net premiums or contributions allocated to the investment divisions of its separate account or accounts (the “Separate Accounts”) that are invested in shares of the EQ/International ETF Portfolio (the “ETF Portfolio”).

The ETF Portfolio is a series of EQ Advisors Trust (the “Trust”), a Delaware statutory trust that is registered with the Securities and Exchange Commission as an open-end management investment company.

To the extent required by applicable law, AXA Equitable will offer Contractholders the opportunity to instruct it, as the record owner of all of the shares of beneficial interest in the ETF Portfolio (the “Shares”) held by its Separate Accounts, as to how it should vote on the reorganization proposal (the “Proposal”) that will be considered at the Special Meeting of Shareholders of the ETF Portfolio referred to in the preceding Notice and at any adjournments or postponements (the “Meeting”). The enclosed Combined Proxy Statement and Prospectus, which you should retain for future reference, concisely sets forth information about the proposed reorganization involving the ETF Portfolio and another series of the Trust that a Contractholder should know before completing the enclosed voting instruction card.

AXA Equitable Financial Services Company, LLC, a wholly owned subsidiary of AXA Financial, Inc., is the parent company of AXA Equitable. AXA Financial, Inc. is a wholly owned subsidiary of AXA, a French insurance holding company. The principal executive offices of AXA Equitable Financial Services Company, LLC and AXA Financial, Inc. are located at 1290 Avenue of the Americas, New York, New York 10104.

These Contractholder Voting Instructions and the accompanying voting instruction card, together with the enclosed proxy materials, are being mailed to Contractholders on or about , 2015.

i

HOW TO INSTRUCT AXA EQUITABLE

To instruct AXA Equitable as to how to vote the Shares held in the investment divisions of its Separate Accounts, Contractholders are asked to promptly complete their voting instructions on the enclosed voting instruction card(s), sign and date the voting instruction card(s), and mail the voting instruction card(s) in the accompanying postage-paid envelope. Contractholders also may provide voting instructions by telephone at 1-800-690-6903 or by Internet at our website at www.proxyvote.com.

If a voting instruction card is not marked to indicate voting instructions but is signed and timely returned, it will be treated as an instruction to vote the Shares “For” the Proposal.

The number of Shares held in the investment division of a Separate Account corresponding to the ETF Portfolio for which a Contractholder may provide voting instructions was determined as of the Record Date by dividing (i) a Contract’s account value (minus any Contract indebtedness) allocable to that investment division by (ii) the net asset value of one Share of the ETF Portfolio. Each whole share of the ETF Portfolio is entitled to one vote as to each matter with respect to which it is entitled to vote and each fractional share is entitled to a proportionate fractional vote. At any time prior to AXA Equitable voting at the Meeting, a Contractholder may revoke his or her voting instructions with respect to that investment division by providing AXA Equitable with a properly executed written revocation of such voting instructions, properly executing later-dated voting instructions by a voting instruction card, telephone or the Internet, or appearing and providing voting instructions in person at the Meeting.

HOW AXA EQUITABLE WILL VOTE

AXA Equitable will vote the Shares for which it receives timely voting instructions from Contractholders in accordance with those instructions. Shares in each investment division of a Separate Account for which AXA Equitable receives a voting instruction card that is signed and timely returned but is not marked to indicate voting instructions will be treated as an instruction to vote the Shares “FOR” the Proposal. Shares in each investment division of a Separate Account for which AXA Equitable receives no timely voting instructions from Contractholders, or that are attributable to amounts retained by AXA Equitable as surplus or seed money, will be voted by AXA Equitable either “FOR” or “AGAINST” the Proposal, or as an abstention, in the same proportion as the Shares for which Contractholders have provided voting instructions to AXA Equitable. As a result of such proportional voting by AXA Equitable, it is possible that a small number of Contractholders could determine whether the Proposal is approved.

ii

OTHER MATTERS

AXA Equitable is not aware of any matters, other than the specified Proposal, to be acted on at the Meeting. If any other matters come before the Meeting, AXA Equitable will vote the Shares upon such matters in its discretion. Voting instruction cards may be solicited by directors, officers and employees of AXA Equitable Funds Management Group, LLC, the investment manager of the Trust, or its affiliates as well as officers and agents of the Trust. The principal solicitation will be by mail but voting instructions may also be solicited by telephone, fax, personal interview, the Internet or other permissible means.

If the quorum necessary to transact business is not established or the vote required to approve the Proposal is not obtained at the Meeting, the persons named as proxies may propose one or more adjournments or postponements of the Meeting in accordance with applicable law to permit further solicitation of voting instructions. The persons named as proxies will vote in their discretion on any such adjournment or postponement.

It is important that your Contract be represented. Please promptly mark your voting instructions on the enclosed voting instruction card; then sign and date the voting instruction card and mail it in the accompanying postage-paid envelope. You may also provide your voting instructions by telephone at 1-800-690-6903 or by Internet at our website at www.proxyvote.com.

iii

PROXY STATEMENT

for

EQ/International ETF Portfolio,

a series of EQ Advisors Trust, and

PROSPECTUS

for

EQ/International

Equity Index Portfolio,

a series of EQ Advisors Trust

Dated , 2015

1290 Avenue of the Americas

New York, New York 10104

1-877-222-2144

This Combined Proxy Statement and Prospectus (the “Proxy Statement/Prospectus”) is being furnished to owners of variable life insurance policies and/or variable annuity contracts or certificates (the “Contracts”) (the “Contractholders”) issued by AXA Equitable Life Insurance Company (“AXA Equitable”) who, as of February 27, 2015, had net premiums or contributions allocated to the investment divisions of its separate account or accounts (the “Separate Accounts”) that are invested in shares of beneficial interest in the EQ/International ETF Portfolio.

The EQ/International ETF Portfolio is referred to herein as the “ETF Portfolio.” The ETF Portfolio is a series of EQ Advisors Trust (the “Trust”), an open-end management investment company registered with the Securities and Exchange Commission (“SEC”). This Proxy Statement/Prospectus also is being furnished to AXA Equitable as the record owner of shares and to other shareholders that were invested in the ETF Portfolio as of February 27, 2015. Contractholders are being provided the opportunity to instruct AXA Equitable to approve or disapprove the proposal contained in this Proxy Statement/Prospectus in connection with the solicitation by the Board of Trustees of the Trust (the “Board” or “Board of Trustees”) of proxies to be used at the Special Meeting of Shareholders of the ETF Portfolio to be held at 1290 Avenue of the Americas, New York, New York 10104, on April 30, 2015, at , Eastern time, or any adjournment or postponement thereof (the “Meeting”).

THE SECURITIES AND EXCHANGE COMMISSION HAS NOT APPROVED OR DISAPPROVED THESE SECURITIES OR PASSED UPON THE ADEQUACY OF THIS PROXY STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The proposal described in this Proxy Statement/Prospectus (“Proposal”) is:

To approve the Plan of Reorganization and Termination (the “Plan of Reorganization”) adopted by the Board, with respect to the reorganization of the EQ/International ETF Portfolio, a series of the Trust, into the EQ/International Equity Index Portfolio, also a series of the Trust.

The reorganization referred to in the Proposal above is referred to herein as the “Reorganization.” The EQ/International Equity Index Portfolio is referred to herein as the “Index Portfolio.”

This Proxy Statement/Prospectus, which you should retain for future reference, contains important information regarding the Proposal that you should know before voting or providing voting instructions. Additional information about the Trust has been filed with the SEC and is available upon oral or written request. This Proxy Statement/Prospectus is being provided to AXA Equitable and mailed to Contractholders and other shareholders on or about , 2015. This Proxy Statement/Prospectus and a proxy or voting instruction card also will be available at www.proxyvote.com on or about , 2015. It is expected that one or more representatives of AXA Equitable will attend the Meeting in person or by proxy and will vote shares held by AXA Equitable in accordance with voting instructions received from its Contractholders and in accordance with voting procedures established by the Trust.

The following documents have been filed with the SEC and are incorporated by reference into this Proxy Statement/Prospectus:

| 1. | The Prospectus with respect to the ETF Portfolio, dated May 1, 2014, as supplemented (File Nos. 333-17217 and 811-07953); |

| 2. | The Statement of Additional Information dated , 2015, relating to the Reorganization (File No. 333- ). |

For a free copy of any of these documents, please call 1-877-522-5035 or write the Trust at the address above.

The Trust is subject to the informational requirements of the Securities Exchange Act of 1934, as amended. Accordingly, it must file certain reports and other information with the SEC. You can copy and review information about the Trust at the SEC’s Public Reference Room in Washington, DC, and at certain of the following SEC Regional Offices: New York Regional Office, 3 World Financial Center, Suite 400, New York, New York 10281; Miami Regional Office, 801 Brickell Avenue, Suite 1800, Miami, Florida 33131; Chicago Regional Office, 175 W. Jackson Boulevard, Suite 900, Chicago, Illinois 60604; Denver Regional Office, 1801 California Street, Suite 1500, Denver, Colorado 80202; Los Angeles Regional Office, 5670 Wilshire Boulevard, 11th Floor, Los Angeles, California 90036; Boston Regional Office, 33 Arch Street, 23rd Floor, Boston, MA 02110; Philadelphia Regional Office, The Mellon Independence Center, 701 Market Street, Philadelphia, PA 19106; Atlanta Regional Office, 3475 Lenox Road, N.E., Suite 1000, Atlanta, GA 30326; Fort Worth Regional Office, Burnett Plaza, Suite 1900, 801 Cherry Street, Unit 18, Fort Worth, TX 76102;

ii

Salt Lake Regional Office, 15 W. South Temple Street, Suite 1800, Salt Lake City, UT 84101; and San Francisco Regional Office, 44 Montgomery Street, Suite 2600, San Francisco, CA 94104. You may obtain information on the operation of the Public Reference Room by calling the SEC at (202) 551-8090. Reports and other information about the Trust are available on the EDGAR Database on the SEC’s Internet site at http://www.sec.gov. You may obtain copies of this information from the SEC’s Public Reference Branch, Office of Consumer Affairs and Information Services, Washington, DC 20549, at prescribed rates.

iii

| 1 | ||||

| 1 | ||||

PROPOSAL: To approve the Plan of Reorganization adopted by the Board of Trustees with respect to the Reorganization of the EQ/International ETF Portfolio, a series of the Trust, into the EQ/International Equity Index Portfolio, also a series of the Trust. | 2 | |||

| 6 | ||||

| 7 | ||||

| 7 | ||||

Comparison of Investment Objectives, Policies and Strategies | 8 | |||

| 10 | ||||

| 10 | ||||

| 12 | ||||

| 13 | ||||

| 13 | ||||

| 14 | ||||

| 14 | ||||

Potential Benefits of the Reorganization to FMG LLC and its Affiliates | 17 | |||

| 17 | ||||

| 19 | ||||

ADDITIONAL INFORMATION ABOUT THE EQ/INTERNATIONAL EQUITY INDEX PORTFOLIO | 19 | |||

| 19 | ||||

| 20 | ||||

| 20 | ||||

| 22 | ||||

| 24 | ||||

| 25 | ||||

| 27 | ||||

| 27 | ||||

Payments to Broker-Dealers and Other Financial Intermediaries | 28 | |||

| 28 | ||||

| 31 | ||||

| 33 | ||||

| 33 | ||||

| 35 | ||||

| 38 | ||||

| 38 | ||||

| 39 | ||||

| 40 | ||||

| 40 | ||||

| 40 | ||||

| A-1 | ||||

APPENDIX B – More Information on Strategies and Risk Factors | B-1 | |||

APPENDIX C – Security Ownership of Certain Beneficial Owners | C-1 |

i

You should read this entire Proxy Statement/Prospectus carefully. For additional information, you should consult the Plan of Reorganization, a copy of the form of which is attached hereto as Appendix A.

This Proxy Statement/Prospectus is soliciting shareholders with amounts invested in the ETF Portfolio as of February 27, 2015, to approve the Plan of Reorganization, whereby the ETF Portfolio will be reorganized into the Index Portfolio. (Each of the ETF Portfolio and the Index Portfolio is sometimes referred to herein as a “Portfolio,” and together, the “Portfolios”)

The ETF Portfolio’s shares are divided into two classes, designated Class IA and Class K shares (the “ETF Portfolio Shares”). The Index Portfolio’s shares are divided into three classes, designated Class IA, Class IB and Class K shares; only the Index Portfolio’s Class IA and Class K shares (the “Index Portfolio Shares”) are involved in the Reorganization. The rights and preferences of the Class IA and Class K shares of the Index Portfolio Shares are identical to the rights and preferences of the corresponding class of ETF Portfolio Shares.

The Plan of Reorganization provides for:

| • | the transfer of all of the assets of the ETF Portfolio to the Index Portfolio in exchange solely for Index Portfolio Shares having an aggregate net asset value equal to the ETF Portfolio’s net assets and the Index Portfolio’s assumption of all the liabilities of the ETF Portfolio; |

| • | the distribution to the shareholders (for the benefit of the Separate Accounts, as applicable, and thus the Contractholders) of those Index Portfolio Shares; and |

| • | the complete termination of the ETF Portfolio. |

The Board of Trustees is proposing the Reorganization because it believes that the Reorganization will permit shareholders invested in the ETF Portfolio, a small Portfolio with limited prospects for future growth and corresponding limited ability to achieve economies of scale, to continue to invest in the Index Portfolio, a much larger Portfolio that pursues a substantially similar investment objective and has better growth prospects and lower expenses. For a detailed description of the Board’s reasons for proposing the Reorganization, see “Additional Information about the Reorganization — Board Considerations” below.

A comparison of the investment objectives, policies, strategies and principal risks of the ETF Portfolio and the Index Portfolio is included in “Comparison of Investment Objectives, Policies and Strategies” and “Comparison of Principal Risk Factors” below. The Portfolios have identical distribution procedures, purchase procedures, exchange rights and redemption procedures, which are discussed in “Additional Information about the EQ/International Equity Index Portfolio” below. Each Portfolio

1

offers its shares to Separate Accounts and certain other eligible investors. Shares of each Portfolio are offered and redeemed at their net asset value without any sales load. You will not incur any sales loads or similar transaction charges as a result of the Reorganization.

Subject to shareholder approval, the Reorganization is expected to be effective at the close of business on , 2015, or on a later date the Trust decides upon (the “Closing Date”). As a result of the Reorganization, each shareholder invested in shares of the ETF Portfolio would become an owner of shares of the Index Portfolio. Each such shareholder would hold, immediately after the Closing Date, Class IA or Class K shares of the Index Portfolio having an aggregate value equal to the aggregate value of the Class IA or Class K Shares, as applicable, of the ETF Portfolio that were held by the shareholder as of the Closing Date. Similarly, each Contractholder whose Contract values are invested in shares of the ETF Portfolio would become an indirect owner of shares of the Index Portfolio. Each such Contractholder would indirectly hold, immediately after the Closing Date, Class IA or Class K shares of the Index Portfolio having an aggregate value equal to the aggregate value of the Class IA or Class K shares, as applicable, of the ETF Portfolio that were indirectly held by the Contractholder as of the Closing Date. The Trust believes that there will be no adverse tax consequences to shareholders or Contractholders as a result of the Reorganization. Please see “Additional Information about the Reorganization — Federal Income Tax Consequences of the Reorganization” below for further information.

The Board has unanimously approved the Plan of Reorganization with respect to each Portfolio. Accordingly, the Board is submitting the Plan of Reorganization for approval by the ETF Portfolio’s shareholders. In considering whether to approve the Proposal, you should review the discussion of the Proposal set forth below. In addition, you should review the information in this Proxy Statement/Prospectus that relates to the Proposal and the Plan of Reorganization generally. The Board recommends that you vote “FOR” the Proposal to approve the Plan of Reorganization.

PROPOSAL: To approve the Plan of Reorganization adopted by the Board of Trustees with respect to the Reorganization of the EQ/International ETF Portfolio, a series of the Trust, into the EQ/International Equity Index Portfolio, also a series of the Trust.

In considering whether you should approve the Proposal, you should note that:

| • | The Portfolios have substantially similar investment objectives. The ETF Portfolio seeks long-term capital appreciation while the Index Portfolio seeks to achieve a total return (before expenses) that approximates the total return performance of a composite index comprised of 40% DJ EuroSTOXX 50 Index, 25% FTSE 100 Index, 25% TOPIX Index, and 10% S&P/ASX 200 Index, including reinvestment of dividends, at a risk level consistent with that of the composite index. |

2

| • | Both Portfolios provide diversified exposure to equity securities of foreign companies in various geographic regions around the world. There are, however, differences in the Portfolios’ principal investment policies and strategies of which you should be aware. These are set forth immediately below. For a detailed comparison of the Portfolios’ investment policies and strategies, see “Comparison of Investment Objectives, Policies and Strategies” below. |

| • | The ETF Portfolio invests primarily in exchange traded securities of other investment companies (“exchange traded funds” or “ETFs”) that, in turn, invest in equity securities of foreign companies. The Portfolio may invest in ETFs that invest in securities of companies of any size located in developed and emerging markets throughout the world. The Portfolio invests in ETFs in accordance with weightings determined by the Portfolio’s investment manager, and generally will be broadly diversified among various geographic regions. Unlike the Index Portfolio, the ETF Portfolio is actively managed and does not utilize an index investment strategy. |

| • | The Index Portfolio utilizes an index investment strategy and invests primarily in equity securities of companies represented in the DJ EuroSTOXX 50 Index (“EuroSTOXX 50”), FTSE 100 Index (“FTSE 100”), TOPIX Index (“TOPIX”), and S&P/ASX 200 Index (S&P/ASX 200”). The Portfolio intends to allocate its assets approximately 25% to securities in the FTSE 100, 25% to securities in the TOPIX, 40% to securities in the EuroSTOXX 50, and 10% to securities in the S&P/ASX 200. Actual allocations may vary by up to 3%. The EuroSTOXX 50, FTSE 100, TOPIX, and S&P/ASX 200 represent large-capitalization stocks of issuers in the Eurozone, the United Kingdom, Japan and Australia, respectively. The Portfolio invests in stocks selected by a stratified sampling construction process, commonly referred to as an indexing strategy, in which the Portfolio’s investment sub-adviser, selects a subset of the companies represented in each index based on its analysis of key risk factors and other characteristics. Such factors include industry weightings, market capitalizations, return variability and yields. Unlike the ETF Portfolio, the Index Portfolio generally does not invest in ETFs; however, it is permitted to invest in ETFs to a limited extent. |

| • | The Portfolios have comparable risk profiles, although there are differences of which you should be aware. Each Portfolio’s principal risks include equity risk, foreign securities risk, currency risk, and securities lending risk. The ETF Portfolio also is subject to ETF risk and emerging markets risk as principal risks while the Index Portfolio is not. The Index Portfolio is subject to index strategy risk and large-cap company risk as principal risks while the ETF Portfolio is not directly subject to such risks. For a detailed comparison of the Portfolios’ risks, see “Comparison of Principal Risk Factors” below. |

| • | AXA Equitable Funds Management Group, LLC (“FMG LLC” or the “Manager”) manages the assets of the ETF Portfolio. FMG LLC has selected AllianceBernstein L.P. (“AllianceBernstein”) as the sub-adviser (“Adviser”) |

3

to manage the assets of the Index Portfolio and it is anticipated that AllianceBernstein will continue to advise the Index Portfolio after the Reorganization. |

| • | FMG LLC serves as the investment manager and administrator for each Portfolio and would continue to manage and administer the Index Portfolio after the Reorganization. The Manager has been granted relief by the SEC to hire, terminate and replace Advisers and amend advisory agreements subject to the approval of the Board of Trustees and without obtaining shareholder approval. However, FMG LLC may not enter into an advisory agreement on behalf of a Portfolio with an “affiliated person” of the Manager, such as AllianceBernstein, unless the advisory agreement, including compensation, is approved by the Portfolio’s shareholders. For a detailed description of the Manager and the Adviser to the Index Portfolio, please see “Additional Information about the EQ/International Equity Index Portfolio — The Manager” and “ — The Adviser” below. |

| • | The ETF Portfolio and the Index Portfolio had net assets of approximately $62 million and $1.7 billion, respectively, as of January 31, 2015. Thus, if the Reorganization of the ETF Portfolio into the Index Portfolio had been in effect on that date, the combined Portfolio would have had net assets of approximately $1.8 billion. |

| • | Class IA shareholders of the ETF Portfolio will receive Class IA shares of the Index Portfolio and Class K shareholders of the ETF Portfolio will receive Class K shares of the Index Portfolio pursuant to the Reorganization. Shareholders will not pay any sales charges in connection with the Reorganization. Please see “Comparative Fee and Expense Tables,” “Additional Information about the Reorganization” and “Additional Information about the EQ/International Equity Index Portfolio” below for more information. |

| • | It is estimated that the annual operating expense ratios for the Index Portfolio’s Class IA and Class K shares, for the fiscal year following the Reorganization, will be lower than those of the ETF Portfolio’s Class IA and Class K shares, respectively, for the fiscal year ended December 31, 2014. For a more detailed comparison of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the EQ/International Equity Index Portfolio” below. |

| • | The maximum management fee for both the ETF Portfolio and the Index Portfolio is equal to an annual rate of 0.40% of its average daily net assets. The Portfolios are subject to same administration fee schedule. The ETF Portfolio and the Index Portfolio each pays FMG LLC its proportionate share of an asset-based administration fee for the Single-Advised Portfolios (defined below), which is equal to an annual rate of 0.12% of the first $3 billion of the aggregate average daily net assets of the Single-Advised Portfolios; 0.11% of the next $3 billion; 0.105% of the next $4 billion; 0.10% of the next $20 billion; 0.0975% of the next |

4

$10 billion; and 0.095% thereafter, subject to a minimum annual fee of $30,000. For a more detailed description of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the EQ/International Equity Index Portfolio” below. |

| • | The ETF Portfolio is subject to an expense limitation arrangement while the Index Portfolio is not. Pursuant to a contract, FMG LLC has agreed to make payments or waive its management, administrative or other fees to limit the expenses of the ETF Portfolio through [April 30, 2016] (unless the Board of Trustees consents to an earlier revision or termination of this arrangement) (“Expense Limitation Arrangement”) so that the annual operating expenses of the Portfolio (exclusive of taxes, interest, brokerage commissions, dividend and interest expenses on securities sold short, capitalized expenses, fees and expenses of other investment companies in which the Portfolio invests, and extraordinary expenses) do not exceed an annual rate of average daily net assets of 0.80% for Class IA shares and 0.55% for Class K shares of the Portfolio. |

| • | The Class IA and Class K shares of the Index Portfolio outperformed the corresponding share classes of the ETF Portfolio for the one-year period ended December 31, 2014. The Class IA shares of the ETF Portfolio outperformed the Class IA shares of the Index Portfolio for the five-year period ended the same date. Since inception through December 31, 2014, the Class K shares of the ETF Portfolio marginally outperformed the Class K shares of the Index Portfolio. Please see “Comparative Performance Information” below. |

| • | Following the Reorganization, the combined Portfolio will be managed in accordance with the investment objective, policies and strategies of the Index Portfolio. It is not expected that the Index Portfolio will revise any of its investment policies following the Reorganization to reflect those of the ETF Portfolio. If the Reorganization is approved, all of the ETF Portfolio’s assets (“Transferred Assets”) on the Closing Date will be transferred to the Index Portfolio. It is anticipated that immediately prior to the Closing Date, the ETF Portfolio will liquidate its securities holdings and hold cash. Therefore, it is anticipated that the Transferred Assets will consist of cash. The sale of portfolio holdings by the ETF Portfolio immediately prior to the Closing Date may result in the ETF Portfolio selling securities at a disadvantageous time and price and could result in it realizing gains (or losses) that would not otherwise have been realized and incurring transaction costs that would not otherwise have been incurred. It is also expected that, over time, the Index Portfolio will use the Transferred Assets to invest in equity securities of companies represented in the EuroSTOXX 50, FTSE 100, TOPIX, and/or the S&P/ASX 200. |

| • | FMG LLC will bear the expenses of the Reorganization described in this Proxy Statement/Prospectus. |

5

Comparative Fee and Expense Tables

The following tables show the fees and expenses of each class of shares of each Portfolio and the estimated pro forma fees and expenses of each class of shares of the Index Portfolio after giving effect to the proposed Reorganization. Fees and expenses for each Portfolio are based on those incurred by each class of its shares for the fiscal year ended December 31, 2014. The pro forma fees and expenses of the Index Portfolio Shares assume that the Reorganization was in effect for the year ended December 31, 2014. The tables below do not reflect any Contract-related fees and expenses, which would increase overall fees and expenses. See a Contract prospectus for a description of those fees and expenses.

Shareholder Fees

(fees paid directly from your investment)

ETF Portfolio | Index Portfolio | Pro Forma Index Portfolio (assuming the | ||

| Not applicable. | Not applicable. | Not applicable. |

Annual Operating Expenses

(expenses that you may pay each year as a percentage of the value of your investment)

| ETF Portfolio | Index Portfolio | Pro Forma Index Portfolio (assuming the Reorganization is approved) | ||||||||||||||||||||||

| Class IA | Class K | Class IA | Class K | Class IA | Class K | |||||||||||||||||||

Management Fee | 0.40 | % | 0.40 | % | 0.40 | % | 0.40 | % | 0.40 | % | 0.40 | % | ||||||||||||

Distribution and/or Service Fees (12b-1 fees) | 0.25 | % | 0.00 | % | 0.25 | % | 0.00 | % | 0.25 | % | 0.00 | % | ||||||||||||

Other Expenses | 0.19 | % | 0.19 | % | 0.14 | % | 0.14 | % | 0.14 | % | 0.14 | % | ||||||||||||

Acquired Fund Fees and Expenses | 0.42 | % | 0.42 | % | N/A | N/A | N/A | N/A | ||||||||||||||||

Total Annual Portfolio Operating Expenses | 1.26 | % | 1.01 | % | 0.79 | % | 0.54 | % | 0.79 | % | 0.54 | % | ||||||||||||

Fee Waiver and/or Expense Reimbursement† | (0.04 | )% | (0.04 | )% | N/A | N/A | N/A | N/A | ||||||||||||||||

Total Annual Portfolio Operating Expenses After Fee Waiver and/ or Expense Reimbursement | 1.22 | % | 0.97 | % | 0.79 | % | 0.54 | % | 0.79 | % | 0.54 | % | ||||||||||||

| † | Pursuant to the Expense Limitation Arrangement, FMG LLC has agreed to make payments or waive its management, administrative or other fees to limit the expenses of the ETF Portfolio through [April 30, 2016] (unless the Board of Trustees consents to an earlier revision or termination of this arrangement) so that the annual operating expenses of the Portfolio (exclusive of taxes, interest, brokerage commissions, dividend and interest expenses on securities sold short, capitalized expenses, fees and expenses of other investment companies in which the Portfolio invests, and extraordinary expenses) do not exceed an annual rate of average daily net assets of 0.80% for Class IA shares and 0.55% for Class K shares of the Portfolio. The Expense Limitation Arrangement may be terminated by FMG LLC at any time after [April 30, 2016]. |

6

This example is intended to help you compare the costs of investing in the Portfolios with the cost of investing in other investment options. The example assumes that:

| • | You invest $10,000 in a Portfolio for the time periods indicated; |

| • | Your investment has a 5% return each year; |

| • | The Portfolio’s operating expenses remain the same; and |

| • | The Expense Limitation Arrangement with respect to the ETF Portfolio is not renewed. |

This example does not reflect any Contract-related fees and expenses, including redemption fees (if any) at the Contract level. If such fees and expenses were reflected, the total expenses would be higher. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

ETF Portfolio | ||||||||||||||||

Class IA | $ | 124 | $ | 396 | $ | 688 | $ | 1,519 | ||||||||

Class K | $ | 99 | $ | 318 | $ | 554 | $ | 1,233 | ||||||||

Index Portfolio | ||||||||||||||||

Class IA | $ | 81 | $ | 252 | $ | 439 | $ | 978 | ||||||||

Class IB | $ | 81 | $ | 252 | $ | 439 | $ | 978 | ||||||||

Class K | $ | 55 | $ | 173 | $ | 302 | $ | 677 | ||||||||

Pro Forma Index Portfolio (assuming the Reorganization is approved) | ||||||||||||||||

Class IA | $ | 81 | $ | 252 | $ | 439 | $ | 978 | ||||||||

Class IB | $ | 81 | $ | 252 | $ | 439 | $ | 978 | ||||||||

Class K | $ | 55 | $ | 173 | $ | 302 | $ | 677 | ||||||||

Each Portfolio pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the example, affect a Portfolio’s performance. During the fiscal year ended December 31, 2014, the portfolio turnover rates for each of the ETF Portfolio and the Index Portfolio were 3% and 8%, respectively, of the average value of the Portfolio.

7

Comparison of Investment Objectives, Policies and Strategies

The following table compares the investment objectives and principal investment policies and strategies of the ETF Portfolio with those of the Index Portfolio. The Board may change the investment objective of a Portfolio without a vote of the Portfolio’s shareholders. For more detailed information about each Portfolio’s investment strategies and risks, see Appendix B.

| Acquired Portfolio | Acquiring Portfolio | |||

| ETF Portfolio | Index Portfolio | |||

Investment Objective | Seeks long-term capital appreciation. | Seeks to achieve a total return (before expenses) that approximates the total return performance of a composite index comprised of 40% EuroSTOXX 50, 25% FTSE 100, 25% TOPIX, and 10% S&P/ASX 200, including reinvestment of dividends, at a risk level consistent with that of the composite index. | ||

Principal Investment Strategies | Under normal market conditions, the Portfolio invests at least 80% of its net assets, plus borrowings for investment purposes, in ETFs. The Portfolio invests primarily in ETFs that, in turn, invest substantially all of their assets in equity securities of foreign companies. The Portfolio may invest in ETFs that invest in securities of companies of any size located in developed and emerging markets throughout the world. The Portfolio invests its assets in ETFs in accordance with weightings determined by the Manager, and generally will be broadly diversified among various geographic regions. | Under normal circumstances the Portfolio invests at least 80% of its net assets, plus borrowings for investment purposes, in equity securities of companies represented in the FTSE 100 Index, TOPIX Index, DJ EuroSTOXX 50 Index, and S&P/ASX 200 Index. The Portfolio intends to allocate its assets approximately 25% to securities in the FTSE 100, 25% to securities in the TOPIX, 40% to securities in the EuroSTOXX 50, and 10% to securities in the S&P/ASX 200. Actual allocations may vary by up to 3%. |

8

| Acquired Portfolio | Acquiring Portfolio | |||

| ETF Portfolio | Index Portfolio | |||

| ETFs are investment companies whose shares are listed and traded on U.S. stock exchanges or otherwise traded in the over-the-counter market and may be purchased and sold throughout the trading day based on their market price. Generally, each ETF seeks to track a securities index or a basket of securities that an “index provider” (such as Standard & Poor’s, Russell or Morgan Stanley Capital International) selects as representative of a market, market segment, industry sector, country or geographic region. An ETF portfolio generally holds the same stocks or bonds as the index it tracks (or it may hold a representative sample of such securities). Accordingly, each ETF is designed so that its performance will correspond closely with that of the index it tracks. By investing in the Portfolio, you will indirectly bear fees and expenses charged by the ETFs in which the Portfolio invests in addition to the Portfolio’s direct fees and expenses. The ETFs in which the Portfolio may invest are referred to herein as the “Underlying ETFs”. | The FTSE 100 is a market capitalization-weighted index representing the performance of the 100 largest UK-domiciled blue chip companies. The TOPIX is a capitalization-weighted index of all companies listed on the First Section of the Tokyo Stock Exchange. The EuroSTOXX 50 covers 60% of the free float market capitalization of the EURO STOXX Total Market Index, which in turn covers approximately 95% of the free-float market capitalization of the investable universe in the Eurozone. The S&P/ASX 200 represents the 200 largest and most liquid publicly listed companies in Australia. | |||

| The Manager uses a two-stage asset allocation process to create an investment portfolio of ETFs for the Portfolio. The first stage involves a strategic asset allocation that is intended to provide the Portfolio with broad exposure to international markets. At this stage, the Manager decides what portion of the Portfolio’s investable assets should be invested in various geographic regions. The Manager makes this determination using a proprietary investment process, based on fundamental research regarding the investment characteristics of the various regions, as well as its outlook for international economies and financial markets. The Manager determines, monitors and may periodically adjust asset allocations based on its analysis of data relating to the U.S. and international economies, securities markets and various segments within those markets. | The Portfolio’s investments will be selected by a stratified sampling construction process in which the Adviser selects a subset of the companies represented in each index based on the Adviser’s analysis of key risk factors and other characteristics. Such factors include industry weightings, market capitalizations, return variability, and yields. This strategy is commonly referred to as an indexing strategy. |

9

| Acquired Portfolio | Acquiring Portfolio | |||

| ETF Portfolio | Index Portfolio | |||

| The second stage of this process involves the selection of Underlying ETFs within each of the geographic regions identified as a result of the first stage of the investment process. The Manager seeks to select Underlying ETFs that represent investments in one or more countries that are expected to outperform the Portfolio’s benchmark over the intermediate term. In selecting the Underlying ETFs, the Manager analyzes many factors, including the Underlying ETF’s investment objectives, total return, portfolio holdings, volatility and expenses as well as quantitative and qualitative data regarding the market segments and economies of the country or countries represented in the Underlying ETF’s portfolio of investments. | ||||

| The Portfolio may lend its portfolio securities to earn additional income. | Same. |

Comparison of Principal Risk Factors

An investment in a Portfolio is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. You may lose money by investing in a Portfolio. The following table compares the principal risks of an investment in each Portfolio. For an explanation of each such risk, see “Additional Information about the Reorganization — Description of Risk Factors” below.

Risks | Index Portfolio | ETF Portfolio | ||||||

Equity Risk | X | X | ||||||

ETF Risk | X | |||||||

Foreign Securities Risk | X | X | ||||||

Currency Risk | X | X | ||||||

Emerging Markets Risk | X | |||||||

Index Strategy Risk | X | |||||||

Large-Cap Company Risk | X | |||||||

Securities Lending Risk | X | X | ||||||

Comparative Performance Information

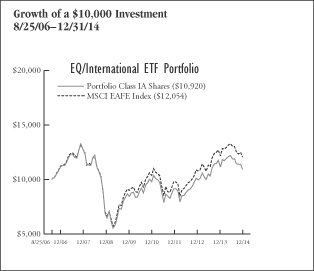

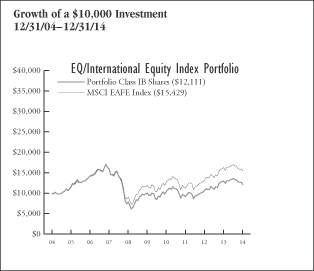

The bar charts and tables below provide some indication of the risks of investing in each Portfolio by showing changes in the Portfolio’s performance from year to year and by showing how the Portfolio’s average annual total returns for the past one-, five- and ten-years (or since inception) through December 31, 2014, compared to the returns of a broad-based market index. With respect to the Index Portfolio, the

10

additional broad-based market index shows how the Portfolio’s performance compared with the returns of another index that has characteristics relevant to the Portfolio’s investment strategy. The return of the broad-based market index (and any additional comparative index) shown in the right hand columns below for each Portfolio is the return of the index for the last 10 years or, if shorter, since inception of the share class with the longest history. Past performance is not an indication of future performance.

The performance results do not reflect any Contract-related fees and expenses, which would reduce the performance results.

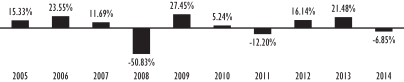

ETF Portfolio - Calendar Year Total Returns (Class IA)

Best quarter (% and time period) 24.81% (2009 2nd Quarter) | Worst quarter (% and time period) -20.89% (2011 3rd Quarter) |

Index Portfolio - Calendar Year Total Returns (Class IB)

Best quarter (% and time period) 25.05% (2009 2nd Quarter) | Worst quarter (% and time period) -26.12% (2008 4th Quarter) |

ETF Portfolio Average Annual Total Returns

(For the periods ended December 31, 2014)

| One Year | Five Years | Since Inception | ||||||||||

ETF Portfolio — Class IA Shares | -7.01 | % | 4.40 | % | 1.06 | % | ||||||

ETF Portfolio — Class K Shares | -6.90 | % | N/A | 8.26 | % | |||||||

MSCI EAFE Index (reflects no deduction for fees or expenses)* | -4.90 | % | 5.33 | % | 2.26 | % | ||||||

| * | Morgan Stanley Capital International (“MSCI”) EAFE® Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. |

11

Index Portfolio Average Annual Total Returns

(For the periods ended December 31, 2014)

| One Year | Five Years | Ten Years/ Since Inception | ||||||||||

Index Portfolio — Class IA Shares | -6.90 | % | 4.05 | % | 2.10 | % | ||||||

Index Portfolio — Class IB Shares | -6.85 | % | 3.96 | % | 1.93 | % | ||||||

Index Portfolio — Class K Shares | -6.65 | % | N/A | 8.25 | % | |||||||

MSCI EAFE Index | -4.90 | % | 5.33 | % | 4.43 | % | ||||||

40% DJ EuroSTOXX 50/25% FTSE 100/25% TOPIX/10% S&P/ASX 200 | -5.48 | % | 4.55 | % | N/A | |||||||

| * | MSCI EAFE® Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. |

| † | A combination of unmanaged indexes. EuroSTOXX 50 covers 50 stocks from 12 Eurozone countries: Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal and Spain. The FTSE 100 represents the performance of the 100 largest blue chip companies listed on the London Stock Exchange. The TOPIX is a free-float adjusted capitalization weighted index that is calculated based on all the domestic common stocks listed on the Tokyo Stock Exchange First Section. The S&P/ASX 200 represents the 200 largest and most liquid publicly listed companies in Australia. |

The following table shows the capitalization of each Portfolio as of December 31, 2014, and of the Index Portfolio on a pro forma combined basis as of December 31, 2014, after giving effect to the proposed Reorganization. Pro forma net assets may not total and net asset values per share may not recalculate due to rounding of net assets.

| Net Assets (in millions) | Net Asset Value Per Share | Shares Outstanding | ||||||||||

ETF Portfolio — Class IA Shares | $ | 4.1 | $ | 2.93 | 1,394,306 | |||||||

Index Portfolio — Class IA Shares | $ | 655.8 | $ | 8.82 | 74,332,022 | |||||||

Adjustments* | $ | — | $ | — | (931,702 | ) | ||||||

Pro forma Index Portfolio — Class IA Shares | $ | 659.9 | $ | 8.82 | 74,794,626 | |||||||

ETF Portfolio — Class IB Share | N/A | N/A | N/A | |||||||||

Index Portfolio — Class IB Shares | $ | 803.7 | $ | 8.69 | 92,498,388 | |||||||

ETF Portfolio — Class K Shares | $ | 91.4 | $ | 2.93 | 31,185,068 | |||||||

Index Portfolio — Class K Shares | $ | 157.2 | $ | 8.82 | 17,819,681 | |||||||

Adjustments* | $ | — | $ | — | (20,828,469 | ) | ||||||

Pro forma Index Portfolio — Class K Shares | $ | 248.6 | $ | 8.82 | 28,176,280 | |||||||

| * | Reflects adjustment for retired shares of the ETF Portfolio. |

12

After careful consideration, the Board unanimously approved the Plan of Reorganization. Accordingly, the Board has submitted the Plan of Reorganization for approval by the ETF Portfolio’s shareholders. The Board recommends that you vote “For” the Proposal.

ADDITIONAL INFORMATION ABOUT THE REORGANIZATION

Terms of the Plan of Reorganization

The terms and conditions under which the Reorganization would be completed are contained in the Plan of Reorganization. The following summary thereof is qualified in its entirety by reference to the Plan of Reorganization, a copy of the form of which is attached to this Proxy Statement/Prospectus as Appendix A.

The Reorganization will involve the Index Portfolio’s acquiring all the assets of the ETF Portfolio in exchange for Index Portfolio Shares and the Index Portfolio’s assuming the ETF Portfolio’s liabilities. The Plan of Reorganization further provides that, on or as promptly as reasonably practicable after the Closing Date, the ETF Portfolio will distribute the Index Portfolio Shares it receives in the Reorganization to its shareholders, for the benefit of the Separate Accounts, as applicable, and thus the Contractholders, by class. The number of full and fractional Index Portfolio Shares each shareholder will receive (for the benefit of each Separate Account, as applicable) will be equal in net asset value (as determined in accordance with the Trust’s normal valuation procedures), as of immediately after the close of business (generally 4:00 p.m., Eastern time) on the Closing Date, to the ETF Portfolio Shares the shareholder holds at that time (for the benefit of each Separate Account, as applicable). After such distribution, the Trust will take all necessary steps under its Amended and Restated Declaration of Trust, as amended (the “Declaration of Trust”), and Delaware and any other applicable law to effect a complete termination of the ETF Portfolio.

The Board may terminate or delay the Plan of Reorganization, and abandon or postpone, the Reorganization at any time prior to the Closing Date, before or after approval by the ETF Portfolio’s shareholders, if circumstances develop that, in the Board’s opinion, make proceeding with the Reorganization inadvisable for a Portfolio. The consummation of the Reorganization also is subject to various conditions, including approval of the Reorganization by the ETF Portfolio’s shareholders, completion of all filings with, and receipt of all necessary approvals, if any, from the SEC, and other customary corporate and securities matters. Subject to the satisfaction of those conditions, the Reorganization will take place immediately after the close of business on the Closing Date.

The Board, including the Trustees who are not “interested persons” (as defined in the Investment Company Act of 1940, as amended (the “1940 Act”)) of the Trust (the “Independent Trustees”), have determined, with respect to each Portfolio, that the interests of the Portfolio’s existing shareholders will not be diluted as a result of the Reorganization and that participation in the Reorganization is in the best interests of the Portfolio.

13

FMG LLC will bear the expenses of the Reorganization described in this Proxy Statement/Prospectus.

Approval of the Plan of Reorganization will require a majority vote of the ETF Portfolio’s shareholders. Such majority is defined in the 1940 Act as the lesser of (i) 67% or more of the voting securities of the Portfolio present at a meeting, if the holders of more than 50% of its outstanding voting securities are present or represented by proxy, or (ii) more than 50% of its outstanding voting securities. If the Plan of Reorganization is not approved by the ETF Portfolio’s shareholders or the Reorganization is not consummated for any other reason, the Board will consider other possible courses of action. Please see “Voting Information” below for more information.

Description of the Securities to Be Issued

The shareholders of the ETF Portfolio will receive Class IA or Class K shares of the Index Portfolio in accordance with the procedures provided for in the Plan of Reorganization. Each such share will be fully paid and non-assessable by the Trust when issued and will have no preemptive or conversion rights.

The Trust may issue an unlimited number of authorized shares of beneficial interest, par value $0.001 per share. The Declaration of Trust authorizes the Board to issue shares in different series and classes. In addition, the Declaration of Trust authorizes the Board to create new series and to name the rights and preferences of the shareholders of each series. The Board does not need additional shareholder action to divide the shares into separate series or classes or to name the shareholders’ rights and preferences. The Index Portfolio is also a series of the Trust.

The Trust currently offers three classes of shares of the Index Portfolio — Class IA, Class IB and Class K shares. The Trust has adopted, in the manner prescribed under Rule 12b-1 under the 1940 Act, a plan of distribution pertaining to the Class IA and Class IB shares of the Index Portfolio. The maximum distribution and/or service (12b-1) fee for the Index Portfolio’s Class IA and Class IB shares is equal to an annual rate of 0.25% of the average daily net assets attributable to such share class. Because these distribution/service fees are paid out of the Index Portfolio’s assets on an ongoing basis, over time these fees will increase your cost of investing and may cost more than paying other types of charges.

At a meeting of the Board held on February 12, 2015, FMG LLC recommended that the ETF Portfolio be reorganized into the Index Portfolio. FMG LLC noted that, in addition to regularly evaluating the performance of each portfolio of the Trust, it continually reviews the overall line-up of investment options and conducts in-depth analysis to provide recommendations to the Board to strengthen the Trust’s lineup. FMG LLC noted that it was recommending the Reorganization because AXA Equitable had determined to cease offering the ETF Portfolio as an investment option in

14

new Contracts because the Portfolio had failed to attract sufficient Contractholder interest. FMG LLC further noted that if AXA Equitable ceased offering the ETF Portfolio as an investment option in new Contracts, the ETF Portfolio’s future growth prospects and its corresponding ability to achieve economies of scale would be limited. FMG LLC also informed the Board that the AXA Allocation Portfolios and Target Allocation Portfolios, which are funds-of-funds of AXA Premier VIP Trust, an affiliated investment company, held approximately 95% of the outstanding shares of the ETF Portfolio as of December 31, 2014. FMG LLC, in its role as investment manager of the AXA Allocation Portfolios and Target Allocation Portfolios, had determined it appropriate to redeem these portfolios’ holdings in the ETF Portfolio and invest in the Index Portfolio. FMG LLC stated that it expected to complete this process in mid-February.

FMG LLC noted that the Index Portfolio has a substantially similar investment objective as the ETF Portfolio and, like the ETF Portfolio, provides diversified exposure to equity securities of foreign companies in various geographic regions around the world. The ETF Portfolio and the Index Portfolio both use the MSCI EAFE Index as their benchmark index (in addition, the Index Portfolio uses the 40% DJ EuroSTOXX 50 Index/25% FTSE 100 Index/25% TOPIX Index/10% S&P/ASX 200 Index, a combination of unmanaged indexes, as a benchmark index). FMG LLC noted that, given the ETF Portfolio’s lack of potential asset growth, FMG LLC believed it would be appropriate to reorganize the ETF Portfolio into the Index Portfolio. FMG LLC also noted that it believed the Reorganization would be beneficial to the shareholders invested in the ETF Portfolio because the Reorganization would provide a means by which Contractholders with amounts allocated to the ETF Portfolio could pursue a substantially similar investment objective in the context of a much larger fund with better growth prospects and lower expenses.

In determining whether to approve the Plan of Reorganization with respect to the ETF Portfolio and recommend its approval to shareholders, the Board, including the Independent Trustees, with the advice and assistance of independent legal counsel, inquired into a number of matters and considered the following factors, among others: (1) the potential benefits of the Reorganization to shareholders, including lower annual operating expenses by reorganizing into a Portfolio with lower annual operating expenses than the ETF Portfolio and greater potential to increase assets and thereby realize economies of scale in the Portfolio’s expenses and portfolio management fees as a result of asset growth; (2) comparisons of the ETF Portfolio’s and Index Portfolio’s investment objectives, policies, strategies, restrictions and risks; (3) the experience and qualifications of the Manager, Adviser and key personnel managing the Index Portfolio; (4) the effect of the Reorganization on the ETF Portfolio’s annual operating expenses and shareholder fees and services; (5) the relative historical performance records of the Portfolios; (6) any change in shareholder rights; (7) the direct or indirect federal income tax consequences of the Reorganization to shareholders and Contractholders; (8) any fees or expenses that will be borne directly or indirectly by the Portfolio in connection with the Reorganization; (9) the terms and conditions of the Plan of Reorganization and whether the Reorganization would result

15

in dilution of shareholder interests; (10) the potential benefits of the Reorganization to other persons, including FMG LLC and its affiliates, as discussed below in the section entitled “Potential Benefits of the Reorganization to FMG LLC and its Affiliates;” and (11) possible alternatives to the Reorganization, including the potential benefits and detriments of maintaining the current structure.

In connection with the Board’s consideration of the proposed Reorganization, the Independent Trustees requested, and FMG LLC provided to the Board, information regarding the factors set forth above as well as other information relating to the Reorganization.

In reaching the decision to recommend approval of the Reorganization, the Board, including the Independent Trustees, concluded that each Portfolio’s participation in the Reorganization is in its best interests and that the interests of existing shareholders of that Portfolio would not be diluted as a result of the Reorganization. The Board’s conclusion was based on a number of factors, including the following:

| • | The Reorganization will permit shareholders invested in the ETF Portfolio to continue to allocate amounts to a much larger Portfolio that pursues a substantially similar investment objective, provides comparable exposure to a diversified portfolio of investments in foreign securities, and has better growth prospects and lower annual operating expense ratios than the ETF Portfolio. |

| • | Following the Reorganization, FMG LLC will continue to serve as the investment manager and administrator of the Index Portfolio and the current Adviser will continue to serve as the Adviser to the Portfolio. |

| • | As a result of the Reorganization, each shareholder of Class IA or Class K shares of the ETF Portfolio would hold, immediately after the Closing Date, Class IA or Class K shares of the Index Portfolio, as applicable, having an aggregate value equal to the aggregate value of the ETF Portfolio shares such shareholder holds as of the Closing Date. |

| • | The Reorganization will be effected on the basis of each participating Portfolio’s net asset value, which will be determined in connection with the Reorganization in accordance with the Trust’s normal valuation procedures, which are identical for all of the Trust’s Portfolios. |

| • | Shareholders will not pay sales charges in connection with the Reorganization. |

| • | The Reorganization is not expected to have any adverse tax results to Contractholders. |

| • | FMG LLC will pay the expenses associated with the Reorganization. |

On the basis of the information provided to it and its evaluation of that information, the Board, including the Independent Trustees, voted unanimously to approve the Plan of Reorganization and to recommend that the shareholders of the ETF Portfolio also approve the Plan of Reorganization.

16

Potential Benefits of the Reorganization to FMG LLC and its Affiliates

FMG LLC may realize benefits in connection with the Reorganization. For example, the Reorganization would eliminate FMG LLC’s obligations under the Expense Limitation Arrangement by reorganizing the ETF Portfolio into the Index Portfolio which is not subject to any expense limitation arrangement.

In addition, the Portfolios are offered and sold through Contracts issued by AXA Equitable that may provide certain death benefit, income benefit or other guarantees to Contractholders. In providing these guarantees, AXA Equitable assumes the risk that Contractholder account values will not be sufficient to pay the guaranteed amounts when due, and therefore that AXA Equitable will have to use its own resources to cover any shortfall. AXA Equitable may enter into hedging transactions from time to time that are intended to help manage its risks under these guarantees. The Reorganization may enhance AXA Equitable’s ability to manage this risk, for example, by eliminating a Portfolio that has underperformed expectations. This could have a positive impact on AXA Equitable’s profitability and/or financial position.

A Portfolio’s performance may be affected by one or more of the following risks, which are described in detail in Appendix B “More Information on Strategies and Risk Factors.”

Equity Risk: In general, stocks and other equity security values fluctuate, and sometimes widely fluctuate, in response to changes in a company’s financial condition as well as general market, economic and political conditions and other factors.

ETF Risk: A Portfolio that invests in ETFs will indirectly bear fees and expenses charged by those ETFs, in addition to the Portfolio’s direct fees and expenses. The cost of investing in the Portfolio, therefore, may be higher than the cost of investing in a mutual fund that invests directly in individual stocks and bonds. In addition, the Portfolio’s net asset value will be subject to fluctuations in the market values of the ETFs in which it invests. The Portfolio is also subject to the risks associated with the securities in which the ETFs invest and the ability of the Portfolio to meet its investment objective will directly depend on the ability of the ETFs to meet their investment objectives. The Portfolio and ETFs are subject to certain general investment risks, including market risk, asset class risk, issuer-specific risk, investment style risk and portfolio management risk. In addition, to the extent a Portfolio invests in ETFs that invest in equity securities, fixed income securities and/or foreign securities, the Portfolio is subject to the risks associated with investing in such securities such as equity risk, market capitalization risk, investment grade securities risk, interest rate risk, credit/default risk, foreign and emerging markets securities risk and lower-rated securities risk. There is also the risk that an ETF’s performance may not match that of the relevant index. It is also possible that an active trading market for an ETF may not develop or be maintained, in which case the liquidity and value of a Portfolio’s investment in the ETF could be substantially and adversely affected. The extent to

17

which the investment performance and risks associated with the Portfolio correlates to those of a particular ETF will depend upon the extent to which the Portfolio’s assets are allocated from time to time for investment in the ETF, which will vary.

Foreign Securities Risk: Investments in foreign securities, including depositary receipts, involve risks not associated with investing in U.S. securities. Foreign markets, particularly emerging markets, may be less liquid, more volatile and subject to less government supervision than domestic markets. Security values also may be negatively affected by changes in the exchange rates between the U.S. dollar and foreign currencies. Differences between U.S. and foreign legal, political and economic systems, regulatory regimes and market practices also may impact security values and it may take more time to clear and settle trades involving foreign securities.

Currency Risk: Investments in foreign currencies and in securities that trade in, or receive revenues in, or in derivatives that provide exposure to foreign currencies are subject to the risk that those currencies will decline in value relative to the U.S. dollar, or, in the case of hedging positions, that the U.S. dollar will decline in value relative to the currency being hedged. Any such decline may erode or reverse any potential gains from an investment in securities denominated in foreign currency or may widen existing loss. Currency rates may fluctuate significantly over short periods of time for a number of reasons, including changes in interest rates, intervention (or the failure to intervene) by governments, central banks or supranational entities, or by the imposition of currency controls or other political developments in the U.S. or abroad.

Emerging Markets Risk: There are greater risks involved in investing in emerging market countries and/or their securities markets. Investments in these countries and/or markets may present market, credit, currency, liquidity, legal, political, technical and other risks different from, or greater than, the risks of investing in developed countries. In addition, the risks associated with investing in a narrowly defined geographic area are generally more pronounced with respect to investments in emerging market countries.

Index Strategy Risk: A Portfolio that employs an index strategy generally invests in the securities included in the relevant index or a representative sample of such securities regardless of market trends. Such a portfolio generally will not modify its index strategy to respond to changes in the economy, which means that it may be particularly susceptible to a general decline in the market segment relating to the relevant index. In addition, although the index strategy attempts to closely track its benchmark index, the Portfolio may not invest in all of the securities in the index. Also, the Portfolio’s fees and expenses will reduce the Portfolio’s returns, unlike those of the benchmark index. Cash flow into and out of the Portfolio, portfolio transaction costs, changes in the securities that comprise the index, and the Portfolio’s valuation procedures also may affect the Portfolio’s performance. Therefore, there can be no assurance that the performance of the index strategy will match that of the benchmark index.

18

Large-Cap Company Risk: Larger more established companies may be unable to respond quickly to new competitive challenges such as changes in technology and consumer tastes. Many larger companies also may not be able to attain the high growth rate of successful smaller companies, especially during extended periods of economic expansion.

Securities Lending Risk: A Portfolio may lend its portfolio securities to seek income. There is a risk that a borrower may default on its obligations to return loaned securities, however, the Portfolio’s securities lending agent may indemnify the Portfolio against that risk. The Portfolio will be responsible for the risks associated with the investment of cash collateral, including any collateral invested in an affiliated money market fund. The Portfolio may lose money on its investment of cash collateral or may fail to earn sufficient income on its investment to meet obligations to the borrower. In addition, delays may occur in the recovery of securities from borrowers, which could interfere with the Portfolio’s ability to vote proxies or to settle transactions.

Federal Income Tax Consequences of the Reorganization

It is anticipated that the Reorganization will not qualify, for federal income tax purposes, as a tax-free reorganization. As a result, gain or loss will be recognized by the ETF Portfolio and its shareholders, but no gain or loss will be recognized by the Contractholders. In addition, (1) each shareholder’s (a) adjusted basis for federal income tax purposes (“adjusted basis”) in the Index Portfolio shares it receives in the Reorganization will be the fair market value thereof at the time the Reorganization is consummated (“Effective Time”) and (b) holding period for those Index Portfolio shares will begin on the following day, and (2) the Index Portfolio’s (a) adjusted basis in the Transferred Assets will be the fair market value thereof at the Effective Time and (b) holding period for the Transferred Assets will begin on the following day.

Contractholders who had premiums or contributions allocated to the investment divisions of the Separate Accounts that are invested in ETF Portfolio Shares will not recognize any gain or loss as a result of the Reorganization. If the ETF Portfolio sells securities before the Reorganization, it may recognize gains or losses (which losses could be significant) on those sales. Any net gains recognized on those sales would increase the amount of any distribution the ETF Portfolio must make to its shareholders before consummating the Reorganization.

ADDITIONAL INFORMATION ABOUT THE EQ/INTERNATIONAL EQUITY INDEX PORTFOLIO

This section gives you information about the Trust, the Manager and the Adviser for the Index Portfolio.

19

The Trust is organized as a Delaware statutory trust and is registered with the SEC as an open-end management investment company. The Board of Trustees is responsible for the overall management of the Trust and each of its series (“portfolios”), including the Index Portfolio. As of February 3, 2015, the Trust issues shares of beneficial interest that are currently divided among eighty-six (86) portfolios, sixty-one (61) of which have authorized Class IA, Class IB and Class K shares, twenty-four (24) of which are only authorized to issue Class IB and Class K shares, and one (1) of which is only authorized to issued Class IA and Class K shares. This Proxy Statement/Prospectus describes the Class IA and Class K shares of the Index Portfolio.

FMG LLC, 1290 Avenue of the Americas, New York, New York 10104, is the Manager to each Portfolio. FMG LLC is registered with the SEC as an investment adviser under the Investment Advisers Act of 1940, as amended. FMG LLC also is registered with the Commodity Futures Trading Commission (“CFTC”) as a commodity pool operator (“CPO”) under the Commodity Exchange Act, as amended, and serves as a CPO with respect to certain portfolios of the Trust. FMG LLC currently claims an exclusion (under CFTC Rule 4.5) from registration as a CPO with respect to other portfolios, including the Index Portfolio. Being subject to dual regulation by the SEC and the CFTC may increase compliance costs and may affect portfolio returns. FMG LLC is a wholly owned subsidiary of AXA Equitable. AXA Equitable is a wholly-owned subsidiary of AXA Financial, Inc., a subsidiary of AXA, a French insurance holding company. FMG LLC serves as the investment adviser to mutual funds and other pooled investment vehicles, and had $103.9 billion in assets under management as of December 31, 2014.

The Manager has a variety of responsibilities for the general management and administration of the Trust and the portfolios. The Manager’s management responsibilities include the selection and monitoring of Advisers for the portfolios. In addition, the Manager may be responsible for the management of the portfolios’ investments in ETFs.

The Manager plays an active role in monitoring each portfolio (or portion thereof) and Adviser and uses portfolio analytics systems to strengthen its evaluation of performance, style, risk levels, diversification and other criteria. The Manager also monitors each Adviser’s portfolio management team to determine whether its investment activities remain consistent with the portfolios’ (or portion thereof’s) investment style and objectives.