Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16

under the Securities Exchange Act of 1934

For the month of June 2022

Commission File Number: 001-14550

China Eastern Airlines Corporation Limited

(Translation of Registrant’s name into English)

Board Secretariat’s Office

5/F, Block A2, Northern District, CEA Building

36 Hongxiang 3rd Road, Minhang District

Shanghai, China 200335

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F: ☒ Form 20-F ☐ Form 40-F

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ☐

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934: ☐ Yes ☒ No

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): n/a

Table of Contents

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| China Eastern Airlines Corporation Limited | ||||||

| (Registrant) | ||||||

| Date June 10, 2022 | By | /s/ Wang Jian | ||||

| Name: Wang Jian | ||||||

| Title: Company Secretary | ||||||

2

Table of Contents

Certain statements contained in this announcement may be regarded as “forward-looking statements” within the meaning of the U.S. Securities Exchange Act of 1934, as amended. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual performance, financial condition or results of operations of the Company to be materially different from any future performance, financial condition or results of operations implied by such forward-looking statements. Further information regarding these risks, uncertainties and other factors is included in the Company’s filings with the U.S. Securities and Exchange Commission. The forward-looking statements included in this announcement represent the Company’s views as of the date of this announcement. While the Company anticipates that subsequent events and developments may cause the Company’s views to change, the Company specifically disclaims any obligation to update these forward-looking statements, unless required by applicable laws. These forward-looking statements should not be relied upon as representing the Company’s views as of any date subsequent to the date of this announcement.

3

Table of Contents

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION

If you are in any doubt as to any aspect of this circular or the appropriate course of action, you should consult a stockbroker or other registered dealer in securities, bank manager, solicitor, professional accountant or other appropriate independent advisers.

If you have sold or transferred all your shares in China Eastern Airlines Corporation Limited, you should at once hand this circular to the purchaser or the transferee or to the bank, licensed securities dealer or other agent through whom the sale or transfer was effected for transmission to the purchaser or the transferee.

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular.

This circular appears for information purposes only and does not constitute an invitation or offer to acquire, purchase or subscribe for securities of the Company.

(1) PROPOSED NON-PUBLIC ISSUANCE

OF A SHARES UNDER SPECIFIC MANDATE;

(2) CONNECTED TRANSACTION IN RELATION TO THE PROPOSED

SUBSCRIPTION OF A SHARES BY CEA HOLDING; AND

(3) PROPOSED AMENDMENTS TO ARTICLES

Independent Financial Adviser to the Independent Board Committee and the Independent Shareholders

Capitalised terms used in this cover page shall have the same meanings as those defined in the section headed “Definitions” of this circular.

The AGM will be held at 2 p.m. on Wednesday, 29 June 2022, and the A Shareholders Class Meeting and the H Shareholders Class Meeting will be held at 2:30 p.m. on Wednesday, 29 June 2022 (or immediately after the conclusion or adjournment of the AGM which will be held at the same place and on the same date) at the Conference Room on Second Floor, CEA Development Co., Ltd., Auxiliary Building, No. 99 Konggang Third Road, Changning District, Shanghai, the PRC (中國上海市長寧區空港三路99號東航實業集團有限公司輔樓二樓會議室 ). A notice of the AGM and a notice of the H Shareholders Class Meeting, containing the resolutions to be considered at the AGM and the H Shareholders Class Meeting, applicable proxy forms and attendance slips of the AGM and the H Shareholders Class Meeting have been despatched by the Company on 13 May 2022.

If you are not able to attend the AGM, the H Shareholders Class Meeting and/or to vote at the meetings, you are requested to complete and return the proxy forms in accordance with the instructions printed thereon as soon as possible and in any event not less than 24 hours before the time appointed for the holding of the AGM and the H Shareholders Class Meeting (or any adjournment thereof) to Hong Kong Registrars Limited at Rooms 1712–1716, 17th Floor, Hopewell Centre, 183 Queen’s Road East, Wanchai, Hong Kong. Completion and return of the proxy forms will not affect your rights to attend in person and vote at the AGM and the H Shareholders Class Meeting (or any adjournment thereof), should you so wish.

9 June 2022

Table of Contents

PRECAUTIONARY MEASURES FOR THE AGM AND THE CLASS MEETINGS

In view of the uncertainties of the COVID-19, the Company will implement the following precautionary measures for the AGM and the Class Meetings to protect the attendees of the AGM and the Class Meetings from risk of infection including, but not limited to:

| (a) | compulsory body temperature checks will be conducted for every attendee of the AGM and the Class Meetings at the entrance of the venue; |

| (b) | every attendee of the AGM and the Class Meetings will be required to complete and submit a health status declaration form at the entrance of the venue; |

| (c) | every attendee will be required to wear a surgical face mask throughout the AGM and the Class Meetings; and |

| (d) | neither refreshments nor corporate gifts will be served at the AGM and the Class Meetings. |

Shareholders who attend the AGM and/or the Class Meetings on-site must pay attention in advance and abide by the regulations and requirements of Shanghai on health status declaration, quarantine and observation during the epidemic containment period. The Company will strictly comply with the epidemic containment requirements of relevant government departments and implement epidemic containment measures to protect the Shareholders who attend the AGM and/or the Class Meetings on-site under the guidance and supervision of relevant government departments. Shareholders who have fever and other symptoms or are not wearing masks as required or do not comply with the relevant epidemic containment regulations and requirements may not be admitted to the venue of the meeting. If the number of Shareholders who attend the AGM and/or the Class Meetings on-site reached the upper limit stipulated under the epidemic containment requirements of the relevant government departments on the date of the AGM and/or the Class Meetings, Shareholders present at the venue will have to enter into the venue on a “first sign in, first enter” basis, and Shareholders who sign in later may not be able to enter into the venue of the meeting.

For the health and safety of the Shareholders, the Company would like to encourage Shareholders to exercise their right to vote at the AGM and/or the Class Meetings by appointing the chairman of the AGM and/or the Class Meetings as their proxy and to return their proxy forms by the time specified above, instead of attending the AGM and/or the Class Meetings in person.

— i —

Table of Contents

| Page | ||||||

| DEFINITIONS | 1 | |||||

| LETTER FROM THE BOARD | 5 | |||||

| LETTER FROM THE INDEPENDENT BOARD COMMITTEE | 30 | |||||

| LETTER FROM THE INDEPENDENT FINANCIAL ADVISER | 31 | |||||

| APPENDIX I | FEASIBILITY ANALYSIS ON THE USE OF PROCEEDS FROM THE NON-PUBLIC ISSUANCE OF A SHARES BY CHINA EASTERN AIRLINES CORPORATION LIMITED | I-1 | ||||

| APPENDIX II | REPORT ON THE USE OF PROCEEDS OF THE PREVIOUS FUND RAISING ACTIVITIES BY CHINA EASTERN AIRLINES CORPORATION LIMITED | II-1 | ||||

| APPENDIX III | DILUTION OF CURRENT RETURNS BY THE NON-PUBLIC ISSUANCE AND REMEDIAL MEASURES BY CHINA EASTERN AIRLINES CORPORATION LIMITED | III-1 | ||||

| APPENDIX IV | FUTURE PLAN FOR RETURN TO THE SHAREHOLDERS FOR THE COMING THREE YEARS (2022–2024) OF CHINA EASTERN AIRLINES CORPORATION LIMITED | IV-1 | ||||

| APPENDIX V | GENERAL INFORMATION | V-1 | ||||

— ii —

Table of Contents

In this circular, unless the context otherwise requires, the following expressions have the following meanings:

“A Shareholders Class Meeting” | means the class meeting to be convened for the holders of A Shares on 29 June 2022 to consider, and if thought fit, approve (among others) the Non-public Issuance of A Shares under the Specific Mandate |

“A Share Subscription Agreement” | means the conditional share subscription agreement in respect of the Non-public Issuance of A Shares entered into between the Company and CEA Holding on 10 May 2022, pursuant to which, the Company has agreed to allot and issue to CEA Holding and CEA Holding has agreed to subscribe for A Shares in the amount of not less than RMB5 billion under the Non-public Issuance of A Shares |

“A Share(s)” | means the ordinary share(s) issued by the Company, with a RMB denominated par value of RMB1.00 each, which are subscribed for and paid up in RMB and are listed on the Shanghai Stock Exchange |

“AGM” | means the 2021 annual general meeting of the Company to be convened on 29 June 2022 to consider, and if thought fit, approve (among others) (i) the Non-public Issuance of A Shares under the Specific Mandate; (ii) the connected transaction in relation to the proposed subscription of A Shares by CEA Holding; and (iii) the proposed amendments to the Articles |

“Airbus S.A.S.” | means Airbus S.A.S., a company incorporated in Toulouse, France |

“Announcement” | means the announcement dated 10 May 2022 issued by the Company in relation to, among other things, (i) the Non-public Issuance of A Shares under the Specific Mandate; (ii) the connected transaction in relation to the proposed subscription of A Shares by CEA Holding; and (iii) the proposed amendments to the Articles |

“Articles” | means the articles of association of the Company, as amended from time to time |

“associate(s)” | has the meaning ascribed to it under the Hong Kong Listing Rules |

“Board” | means the board of directors of the Company |

“Boeing Company” | means Boeing Company, a company incorporated in Delaware, the United States of America |

“business day” | means a day (other than a Saturday, Sunday or statutory holiday) on which commercial banks in the PRC are open generally for normal business |

— 1 —

Table of Contents

DEFINITIONS

“CAAC” | means the Civil Aviation Administration of China |

“CAGR” | means the compound annual growth rate |

“CEA Holding” | means 中國東方航空集團有限公司 (China Eastern Air Holding Company Limited*), the controlling Shareholder |

“CES Finance” | means 東航金控有限責任公司 (CES Finance Holding Co., Limited), a wholly-owned subsidiary of CEA Holding and a Shareholder and connected person of the Company |

“CES Global” | means 東航國際控股(香港)有限公司 (CES Global Holdings (Hong Kong) Limited), a wholly-owned subsidiary of CES Finance and a Shareholder and connected person of the Company |

“Class Meetings” | means the A Shareholders Class Meeting and the H Shareholders Class Meeting |

“COMAC” | means 中國商用飛機有限責任公司 (Commercial Aircraft Corporation of China, Ltd.) |

“Company” | means 中國東方航空股份有限公司 (China Eastern Airlines Corporation Limited), a joint stock limited company incorporated in the PRC with limited liability, whose H Shares, A Shares and American depositary shares are listed on the Hong Kong Stock Exchange, the Shanghai Stock Exchange and the New York Stock Exchange, Inc., respectively |

“connected person(s)” | has the meaning ascribed to it under the Hong Kong Listing Rules |

“controlling Shareholder” | has the meaning ascribed to it under the Hong Kong Listing Rules |

“COVID-19” | means the novel coronavirus pneumonia disease, a pneumonia caused by a novel coronavirus, which was named as “COVID-19” by the World Health Organization |

“CSRC” | means China Securities and Regulatory Commission |

“Director(s)” | means the director(s) of the Company |

“Group” | means the Company and its subsidiaries |

“H Shareholders Class Meeting” | means the class meeting to be convened for the holders of H Shares on 29 June 2022 to consider, and if thought fit, approve (among others) the Non-public Issuance of A Shares under the Specific Mandate |

— 2 —

Table of Contents

DEFINITIONS

“H Share(s)” | means the ordinary share(s) issued by the Company, with a RMB denominated par value of RMB1.00 each, which are subscribed for and paid up in a currency other than RMB and are listed on the Hong Kong Stock Exchange |

“Hong Kong” | means Hong Kong Special Administrative Region of the PRC |

“Hong Kong Listing Rules” | means the Rules Governing the Listing of Securities on the Hong Kong Stock Exchange |

“Hong Kong Stock Exchange” | means The Stock Exchange of Hong Kong Limited |

“Independent Board Committee” | means the independent board committee of the Company comprising Cai Hongping, Dong Xuebo, Sun Zheng and Lu Xiongwen being all of the independent non-executive Directors, which is formed in accordance with the Hong Kong Listing Rules to advise the Independent Shareholders on the connected transaction in relation to the proposed subscription of A Shares by CEA Holding |

“Independent Financial Adviser” | means Octal Capital Limited, acting as an independent financial adviser to the Independent Board Committee and Independent Shareholders on the connected transaction in relation to the proposed subscription of A Shares by CEA Holding, which is a corporation licensed to carry on Type 1 (dealing in securities) and Type 6 (advising on corporate finance) regulated activities under the SFO |

“Independent Shareholders” | means the Shareholders, other than CEA Holding and its associates |

“JuneYao Group” | means 上海均瑤(集團)有限公司 (Shanghai Juneyao (Group) Co., Ltd.), which is ultimately owned as to approximately 36.1357%, 35.6338%, 24.0905%, 4.0151% and 0.1250% by Wang Junjin (王均金), Wang Han (王瀚), Wang Junhao (王均豪), Wang Chao (王超) and Wang Yingying (王瀅瀅), respectively |

“Latest Practicable Date” | means 2 June 2022, being the latest practicable date of ascertaining certain information included in this circular before the printing of this circular |

“Non-public Issuance of A Shares” | means the proposed issuance of not more than 5,662,332,023 A Shares (inclusive) by the Company to not more than 35 specific investors (inclusive) (including CEA Holding) who meet the conditions required by the CSRC, details of which are set out in the section headed “PROPOSED NON-PUBLIC ISSUANCE OF A SHARES UNDER SPECIFIC MANDATE” set out in the “Letter from the Board” in this circular |

— 3 —

Table of Contents

DEFINITIONS

“PRC” | means the People’s Republic of China, which for the purpose of this circular only, excludes Hong Kong, the Macau Special Administrative Region of the PRC and Taiwan |

“Pricing Benchmark Date” | means the first day of the issuance period of the Non-public Issuance of A Shares |

“RMB” | means Renminbi yuan, the lawful currency of the PRC |

“RPK” | means the passenger traffic volume, the sum of the number of passengers carried multiplied by the distance flown for every route |

“SASAC” | means the State-owned Assets Supervision and Administration Commission of the State Council (國務院國有資產監督管理委員會) |

“SFO” | means the Securities and Futures Ordinance (Chapter 571 of the Law of Hong Kong) |

“Shanghai Trading Days” | means a day on which the Shanghai Stock Exchange is open for trading of shares |

“Shareholder(s)” | means the shareholder(s) of the Company |

“Specific Mandate” | means the specific mandate to be granted by the Independent Shareholders at the AGM and the Class Meetings to the Board in relation to the Non-public Issuance of A Shares |

“Subscribers” | means not more than 35 specific investors (inclusive) (including CEA Holding) who meet the conditions required by the CSRC |

“%” | means per cent. |

— 4 —

Table of Contents

Directors | Legal address: | |

Liu Shaoyong (Chairman) | 66 Airport Street | |

Li Yangmin (Vice Chairman, President) | Pudong International Airport | |

Tang Bing (Director) | Shanghai | |

Lin Wanli (Director) | PRC | |

Cai Hongping (Independent non-executive Director) | Head office: | |

Dong Xuebo (Independent non-executive Director) | 5/F, Block A2 | |

Sun Zheng (Independent non-executive Director) | Northern District, CEA Building | |

Lu Xiongwen (Independent non-executive Director) | 36 Hongxiang 3rd Road | |

| Minhang District | ||

Jiang Jiang (Employee Representative Director) | Shanghai | |

| PRC | ||

| Principal place of business in Hong Kong: | ||

| Unit D, 19/F. | ||

| United Centre | ||

| 95 Queensway | ||

| Hong Kong | ||

| Hong Kong share registrar and transfer office: | ||

| Hong Kong Registrars Limited | ||

| Rooms 1712–1716, 17th Floor | ||

| Hopewell Centre | ||

| 183 Queen’s Road East | ||

| Wanchai | ||

| Hong Kong | ||

9 June 2022

To the shareholders of the Company

Dear Sir or Madam,

(1) PROPOSED NON-PUBLIC ISSUANCE

OF A SHARES UNDER SPECIFIC MANDATE;

(2) CONNECTED TRANSACTION IN RELATION TO THE PROPOSED

SUBSCRIPTION OF A SHARES BY CEA HOLDING; AND

(3) PROPOSED AMENDMENTS TO ARTICLES

| I. | INTRODUCTION |

Reference is made to the Announcement of the Company dated 10 May 2022 in relation to, among other things, the Non-public Issuance of A Shares under the Specific Mandate, the connected transaction in relation to the proposed subscription of A Shares by CEA Holding and the proposed amendments to the Articles.

— 5 —

Table of Contents

LETTER FROM THE BOARD

On 10 May 2022, the Board considered and approved the proposal for the Non-public Issuance of A Shares, pursuant to which the Company will issue not more than 5,662,332,023 A Shares (inclusive) to not more than 35 specific investors (inclusive) (including CEA Holding, the controlling Shareholder) who meet the conditions required by the CSRC. The proceeds expected to be raised (before deducting relevant issuance expenses) will be not more than RMB15 billion (inclusive).

According to the proposal of the Non-public Issuance of A Shares, the Company and CEA Holding entered into the A Share Subscription Agreement on 10 May 2022, pursuant to which in accordance with and subject to the terms and conditions under the A Share Subscription Agreement, the Company has agreed to allot and issue to CEA Holding and CEA Holding has agreed to subscribe for A Shares in the amount of not less than RMB5 billion under the Non-public Issuance of A Shares in cash.

The purpose of this circular is to provide you with information regarding, among other things, (i) details of the Non-public Issuance of A Shares under the Specific Mandate, the connected transaction in relation to the proposed subscription of A Shares by CEA Holding and the proposed amendments to the Articles; (ii) a letter from the Independent Board Committee; and (iii) a letter of advice from the Independent Financial Adviser, to enable you to make an informed decision on whether to vote for or against the proposed resolutions at the AGM and the Class Meetings.

��

| II. | PROPOSED NON-PUBLIC ISSUANCE OF A SHARES UNDER SPECIFIC MANDATE |

| 1. | Structure of the Non-public Issuance of A Shares |

Detailed proposal of the Non-public Issuance of A Shares is as follows:

| (1) | Type and par value of shares to be issued: | The shares to be issued under the non-public issuance are domestically listed ordinary shares (A Shares) denominated in RMB, with par value of RMB1.00 each. The aggregate par value of the A Shares to be issued under the Non-public Issuance of A Shares will be not more than RMB5,662,332,023 (inclusive). | ||

| (2) | Method and time of issuance: | The Non-public Issuance of A Shares is undertaken by way of non-public issuance to specific Subscribers, i.e. not more than 35 specific investors (inclusive) (including CEA Holding) who meet the conditions required by the CSRC. The Company will issue A Shares to the Subscribers at an appropriate timing within the validity period upon obtaining the approval of the CSRC. | ||

| (3) | Subscribers and method of subscription: | The Subscribers of the Non-public Issuance of A Shares shall be not more than 35 specific investors (inclusive) (including CEA Holding) who meet the conditions required by the CSRC. Among which, CEA Holding intends to subscribe for A Shares in the amount of not less than RMB5 billion under the Non-public Issuance of A Shares in cash. | ||

— 6 —

Table of Contents

LETTER FROM THE BOARD

| Apart from CEA Holding, other subscribers shall be legal persons, natural persons or other legitimate investment organizations such as securities investment fund management companies, securities companies, trust investment companies, finance companies, insurance institutional investors and qualified foreign institutional investors that meet the requirements of the CSRC. Securities investment fund management companies, securities companies, qualified foreign institutional investors and RMB qualified foreign institutional investors who subscribe for the shares using more than two products under their management shall be regarded as one subscriber. Trust companies, as subscribers, may only use their own funds to subscribe for the shares. | ||||

| Apart from CEA Holding, other subscribers shall be determined by the Board and its authorized persons, upon authorization by the general meeting, with the sponsor (a joint lead underwriter) based on the subscription quotations of the subscribers within the scope of authorization of the general meeting in accordance with relevant laws, administrative regulations, departmental rules or normative documents after obtaining the approval of the CSRC for the Non-public Issuance of A Shares. | ||||

| All subscribers will subscribe for the A Shares under the Non-public Issuance of A Shares in cash and at the same price. | ||||

| It is expected that the Subscribers (other than CEA Holding) and their respective ultimate beneficial owners are and will continue to be third parties independent of the Company and the connected persons of the Company after the completion of the Non-public Issuance of A Shares. If any Subscriber is or will become a connected person of the Company, the Company will take all reasonable measures to comply with the relevant requirements under Chapter 14A of the Hong Kong Listing Rules. | ||||

— 7 —

Table of Contents

LETTER FROM THE BOARD

| (4) | Pricing Benchmark Date, pricing principles and issue price: | The Pricing Benchmark Date of the Non-public Issuance of A Shares shall be the first day of the issuance period of the Non-public Issuance of A Shares. | ||

| The issue price of the Non-public Issuance of A Shares shall not be lower than 80% of the average trading price of A Shares in the 20 Shanghai Trading Days prior to the Pricing Benchmark Date (excluding the Pricing Benchmark Date, the same below), and the Company’s audited net assets per share attributable to ordinary shareholders of the parent company as at the end of the most recent period prior to the Pricing Benchmark Date, whichever is higher (i.e. the “base issue price”, with two decimal places according to the “round up method”). The average trading price of A Shares in the 20 Shanghai Trading Days prior to the Pricing Benchmark Date = the total trading value of A Shares in the 20 Shanghai Trading Days prior to the Pricing Benchmark Date/the total trading volume of A Shares in the 20 Shanghai Trading Days prior to the Pricing Benchmark Date. | ||||

| The Non-public Issuance of A Shares and the pricing principles for the issue price were mainly based on the requirements of the Administrative Measures for the Issuance of Securities by Listed Companies (Revised in 2020) (《上 市 公 司 證 券 發 行 管 理 辦 法 》( 2020 年 修 正 )) (the “Administrative Measures”) and the Detailed Implementation Rules for the Non-Public Issuance of Stocks of Listed Companies (Revised in 2020) (《上市公司非公開發行股票實施細則 》(2020 年修正 )) (the “Implementation Rules”) as stipulated by the CSRC. | ||||

| According to the requirements of Article 38 of the Administrative Measures, the non-public issuance of shares by a listed company shall comply with the following requirements, among other things, the issue price shall not be lower than 80% of the average price of the company’s shares over the 20 trading days prior to the price benchmark date. According to the requirements of Article 7 of the Implementation Rules, the “price benchmark date” is the reference date for calculating the base issue price. The price benchmark date for the non-public issuance of shares shall be the first day of the issuance period. The listed company shall not issue shares at a price lower than the base issue price. | ||||

| Based on the above, the Board is of the view that the pricing principles of the Non-public Issuance of A Shares comply with the requirements of relevant laws and regulations and is on normal commercial terms. | ||||

— 8 —

Table of Contents

LETTER FROM THE BOARD

| The Company’s audited net assets per share attributable to ordinary shareholders of the parent company as at the end of the most recent period prior to the Pricing Benchmark Date (i.e. as at 31 December 2021) is RMB2.7219 prepared in accordance with China Accounting Standards for Business Enterprises as disclosed in the annual report for the year ended 31 December 2021 of the Company, which is calculated as follows: | ||||

| Net assets per share attributable to ordinary shareholders of the parent company as at 31 December 2021 = equity attributable to the shareholders of the parent company as at 31 December 2021/number of ordinary shares of the Company outstanding as at 31 December 2021. | ||||

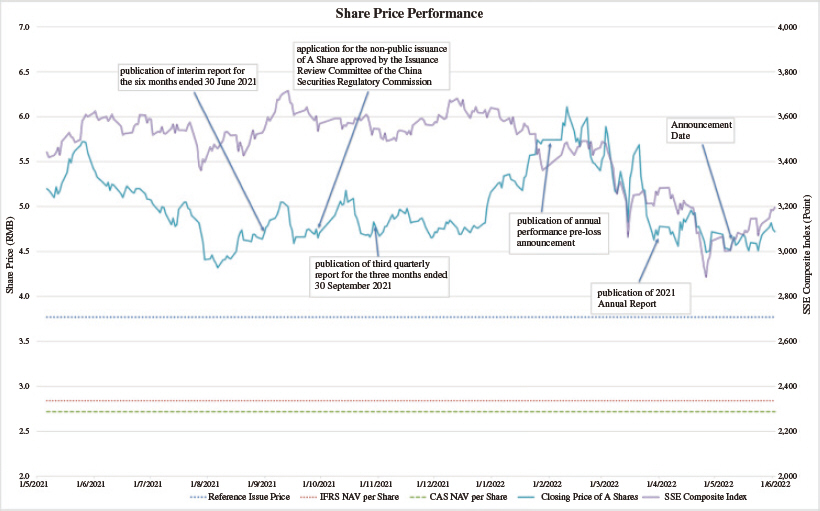

| For illustration purpose only, as at the Latest Practicable Date, the closing price per A Share quoted on the Shanghai Stock Exchange was RMB4.72 and the closing price per H Share quoted on the Hong Kong Stock Exchange was HK$2.77. | ||||

| In the event that the Company distributes dividends, grants bonus shares, allots shares, converts capital reserve into share capital or carries out any other ex-right or ex-dividend activities during the period from the balance sheet date of the audited financial report as at the end of the most recent period prior to the Pricing Benchmark Date to the issuance date, the above net assets per share attributable to ordinary shareholders of the parent company shall be adjusted accordingly. | ||||

| In the event that the Company distributes dividends, grants bonus shares, allots shares, converts capital reserve into share capital or carries out any other ex-right or ex-dividend activities during the period from the Pricing Benchmark Date of the Non-public Issuance of A Shares to the issuance date, the issue price shall be adjusted on ex-right or ex-dividend basis. | ||||

| On the basis of the aforementioned base issue price, the final issue price of the Non-public Issuance of A Shares shall be determined by the Board or its authorized persons, pursuant to the authorization of the AGM and the Class Meetings, with the sponsor (the lead underwriter) for the Non-public Issuance of A Shares through negotiations based on the subscription quotations of the subscribers and the principles such as price priority (i.e. the subscriber who offers higher price has the priority to subscribe the shares over the subscriber who offers lower price in the process of subscription) in accordance with relevant laws and regulations and requirements of regulatory authorities after obtaining the approval of the CSRC for the Non-public Issuance of A Shares. | ||||

— 9 —

Table of Contents

LETTER FROM THE BOARD

| As at the Latest Practicable Date, the Company has not engaged any sponsor or underwriter. The sponsor (the lead underwriter) will be engaged and the sponsor agreement will be entered into by the Board or its authorized persons in their sole discretion pursuant to the authorization granted by the Shareholders at the AGM on normal commercial terms. Further announcement(s) in relation to the Non-public Issuance of A Shares will be made by the Company as and when appropriate. | ||||

| CEA Holding will not participate in the market bidding process of the Non-public Issuance of A Shares, but has undertaken to accept the results of the market bidding and to subscribe for the A Shares under the issuance at the same price as other investors. If the issue price cannot be determined through bidding, CEA Holding will subscribe for the shares at the subscription price of 80% of the average trading price of A Shares in the 20 Shanghai Trading Days prior to the Pricing Benchmark Date (excluding the Pricing Benchmark Date, the same below), and the Company’s audited net assets per share attributable to ordinary shareholders of the parent company as at the end of the most recent period prior to the Pricing Benchmark Date, whichever is higher (i.e. the “base issue price”, with two decimal places according to the “round up method”). | ||||

| (5) | Number of shares to be issued: | The number of shares to be issued under the Non-public Issuance of A Shares is calculated by dividing the gross proceeds raised from the Non-public Issuance of A Shares by the issue price. The final number of A Shares to be issued is rounded down to the nearest integer, and shall not exceed 30% of the Company’s total share capital prior to the Non-public Issuance of A Shares, subject to the approval of the CSRC for the Non-public Issuance of A Shares. As at the Latest Practicable Date, the total share capital of the Company is 18,874,440,078 shares. Based on which, the number of shares to be issued under the Non-public Issuance of A Shares will not exceed 5,662,332,023 shares (inclusive), representing: (i) approximately 41.34% of the Company’s existing A Shares in issue and approximately 30.00% of its existing total share capital in issue as at the Latest Practicable Date; and (ii) approximately 29.25% of the Company’s enlarged A Shares in issue and approximately 23.08% of its enlarged total share capital in issue upon completion of the Non-public Issuance of A Shares. | ||

— 10 —

Table of Contents

LETTER FROM THE BOARD

| The final number of shares to be subscribed by CEA Holding shall be determined based on the subscription amount and the subscription price according to the following formula: Number of shares to be subscribed = subscription amount/subscription price, and the number of shares to be subscribed is rounded down to the nearest integer. | ||||

| In the event that the Company grants bonus shares, allots shares, converts capital reserve into share capital or carries out any other ex-right activities during the period from the date of the first announcement of Board resolution for the Non-public Issuance of A Shares to the issuance date, or there are changes in the total share capital of the Company prior to the issuance due to other reasons, the maximum number of shares to be issued under the issuance shall be adjusted accordingly. | ||||

| The final number of shares to be issued shall be determined by the Board or its authorized persons, pursuant to the authorization of the AGM and the Class Meetings, with the sponsor (the lead underwriter) for the Non-public Issuance of A Shares through negotiations based on the actual circumstances at the time of issuance within the aforementioned maximum number of shares to be issued in accordance with relevant laws, administrative regulations, departmental rules or normative documents after obtaining the approval of the CSRC for the Non-public Issuance of A Shares. If the CSRC or other regulatory authorities adjusted the aforementioned number of shares to be issued, the number approved by such authorities shall prevail. | ||||

| (6) | Amount and use of proceeds: | The gross proceeds to be raised from the Non-public Issuance of A Shares (before deducting relevant issuance expenses) will be not more than RMB15 billion, which are intended to be used in the following projects: | ||

| No. | Name of items | Proposed amount of proceeds to be applied | ||||

| (RMB billion) | ||||||

1 | Introducing 38 aircraft | 10.50 | ||||

2 | Supplementing the working capital | 4.50 | ||||

Total | 15.00 | |||||

— 11 —

Table of Contents

LETTER FROM THE BOARD

| After receiving the proceeds from the Non-public Issuance of A Shares, if the actual amount of net proceeds is less than the above proposed amount of proceeds to be applied, the Board or its authorized persons will, based on the actual amount of net proceeds and subject to relevant laws and regulations, within the scope of the above projects to be funded with the proceeds, adjust and finally determine the specific projects, priority and specific amount of proceeds to be applied to each project according to actual circumstances such as the progress of the projects to be funded with the proceeds and funding requirements. The insufficient portion of proceeds will be funded by the Company’s own funds or through other financing channels such as bank loans, financial lease and self-raised funds. As at 31 December 2021, the monetary capital of the Company was RMB12.962 billion and unutilised banking facilities of the Company was RMB21.338 billion. The interest rates and specific investment plan of the aforementioned financing channels shall be subject to the circumstances of market and commercial terms to be entered into between the Company and relevant banks or leasing companies. | ||||

| In order to ensure the smooth progress of projects to be funded with the proceeds and safeguard the interests of all Shareholders, before receiving the proceeds from the Non-public Issuance of A Shares, the Company may invest in the projects with self-raised funds according to the actual circumstances of the projects to be funded with the proceeds and replace such funds in accordance with relevant laws and regulations after receiving the proceeds. | ||||

| After receiving the proceeds from the Non-public Issuance of A Shares, the expected timeline of the proceeds to be used is as follows: | ||||

(i) the proceeds to be used for introducing 38 aircraft shall be invested according to the agreement of contracts and aircraft introduction plan. The 38 aircraft to be introduced are scheduled for delivery during the years from 2022 to 2024; | ||||

(ii) the proceeds to be used for supplementing the working capital shall be invested according to the fund need of the Company during its daily operation. | ||||

— 12 —

Table of Contents

LETTER FROM THE BOARD

| Pursuant to the Issue Regulation Q&A — Regulatory Requirements for Guiding and Regulating the Financing Activities of Listed Companies (《 發行監管問答 — 關於引導 規 範 上 市 公 司 融 資行 為 的 監 管 要 求 》) promulgated by the CSRC, for listed companies applying for non-public issuance of shares, the number of shares to be issued shall, in principal, not exceed 30% of the total share capital before the issuance (i.e. not more than 5,662,332,023 A Shares (inclusive)). To the extent permitted by the regulation above and taking into consideration the pricing principles, the fund need of investment project, the subscription intention of CEA Holding and the circumstances of securities market, etc., the proceeds to be raised from the Non-public Issuance of A Shares is determined to be not more than RMB15 billion. | ||||

| Based on the above, the Board is of the view that maximum amount of net proceeds to be raised from the Non-public Issuance of A Shares is fair and reasonable and in the interests of the Company and its Shareholders. | ||||

| (7) | Lock-up period: | Upon completion of the Non-public Issuance of A Shares, the shares subscribed by CEA Holding under the Non-public Issuance of A Shares shall not be transferred within eighteen (18) months from the date of completion of the issuance, and the shares subscribed by other subscribers under the Non-public Issuance of A Shares shall not be transferred within six (6) months from the date of completion of the issuance. Shares derived from the grant of bonus shares, allotment of shares or conversion of capital reserve into share capital by the Company for the shares under the Non-public Issuance of A Shares obtained by the subscribers shall also comply with the above lock-up arrangement. Upon expiration of the lock-up period, the transfer and trading of the shares subscribed by the subscribers under the issuance shall be handled in accordance with the then effective laws and regulations and the rules of the Shanghai Stock Exchange. | ||

| If the CSRC or the Shanghai Stock Exchange has promulgated new rules or requirements for the above lock-up period arrangement, the above lock-up period arrangement shall be revised in accordance with the new rules or requirements of the CSRC or the Shanghai Stock Exchange and implemented accordingly. | ||||

— 13 —

Table of Contents

LETTER FROM THE BOARD

| (8) | Place of listing: | The Company will apply to the Shanghai Stock Exchange for the listing of, and permission to deal in, the A Shares to be issued pursuant to the Non-public Issuance of A Shares. Upon expiration of the lock-up period, the A Shares to be issued under the Non-public Issuance of A Shares will be listed and traded on the Shanghai Stock Exchange. | ||

| (9) | Arrangement of accumulated undistributed profits before the Non-public Issuance of A Shares: | Both new Shareholders and existing Shareholders are entitled to the accumulated undistributed profits of the Company before the Non-public Issuance of A Shares upon completion of the Non-public Issuance of A Shares according to their respective shareholdings. | ||

| (10) | Validity period of the resolutions of Non-public Issuance of A Shares: | The resolutions in relation to the Non-public Issuance of A Shares shall remain valid for twelve (12) months from the date on which relevant resolutions are considered and approved at the AGM and the Class Meetings. | ||

Each of the following items in relation to the Non-public Issuance of A Shares will be considered and approved, and be implemented conditional upon approvals and/or authorisations having been obtained from the relevant authorities:

| (i) | type and par value of shares to be issued; |

| (ii) | method and time of issuance; |

| (iii) | Subscribers and method of subscription; |

| (iv) | Pricing Benchmark Date, pricing principles and issue price; |

| (v) | number of shares to be issued; |

| (vi) | amount and use of proceeds; |

| (vii) | lock-up period; |

| (viii) | place of listing; |

| (ix) | arrangement of accumulated undistributed profits before the Non-public Issuance of A Shares; and |

| (x) | validity period of the resolutions of Non-public Issuance of A Shares. |

— 14 —

Table of Contents

LETTER FROM THE BOARD

The proposal approving the Non-public Issuance of A Shares will be submitted, by way of special resolution, for the Independent Shareholders’ consideration and approval at the AGM, the A Shareholders Class Meeting and the H Shareholders Class Meeting.

| 2. | Proposal in relation to the Company being qualified for Non-public Issuance of A Shares |

Pursuant to laws, regulations and regulatory documents such as the Company Law of the PRC (《中華人民共和國公司法》 ), the Securities Law of the PRC (《中華人民共和國證券法》), the Measures for Administration of the Issuance of Securities by Listed Companies (《上市公司證券發行管理辦法》 ), the Implementation Rules for the Non-public Issuance of Shares by Listed Companies (《上市公司非公開發行股票實施細則》 ) and Issue Regulation Q&A — Regulatory Requirements for Guiding and Regulating the Financing Activities of Listed Companies (《發行監管問答 — 關於引導規範上市公司融資行為的監管要求》), the Board considers that the Non-public Issuance of A Shares by the Company satisfies the conditions of non-public offering of A shares after itemized verification of the actual situation and relevant matters of the Company.

The proposal in relation to the Company being qualified for Non-public Issuance of A Shares will be submitted, by way of ordinary resolution, for the Shareholders’ consideration and approval at the AGM.

| 3. | Proposal in relation to the “Proposal for the Non-public Issuance of A Shares by China Eastern Airlines Corporation Limited” |

The proposal in relation to the “Proposal for the Non-public Issuance of A Shares by China Eastern Airlines Corporation Limited” will be submitted, by way of special resolution, for the Independent Shareholders’ consideration and approval at the AGM, the A Shareholders Class Meeting and the H Shareholders Class Meeting.

| 4. | Proposal in relation to the “Feasibility Analysis on the Use of Proceeds from the Non-public Issuance of A Shares by China Eastern Airlines Corporation Limited” |

The “Feasibility Analysis on the Use of Proceeds from the Non-public Issuance of A Shares by China Eastern Airlines Corporation Limited” was prepared in Chinese language. The full text of the English translation of the “Feasibility Analysis on the Use of Proceeds from the Non-public Issuance of A Shares by China Eastern Airlines Corporation Limited” is set out in Appendix I to this circular. In the event of any discrepancy between the English translation and the Chinese version of the document, the Chinese version shall prevail.

The proposal in relation to the “Feasibility Analysis on the Use of Proceeds from the Non-public Issuance of A Shares by China Eastern Airlines Corporation Limited” will be submitted, by way of special resolution, for the Shareholders’ consideration and approval at the AGM, the A Shareholders Class Meeting and the H Shareholders Class Meeting.

— 15 —

Table of Contents

LETTER FROM THE BOARD

| 5. | Proposal in relation to the “Report on the Use of Proceeds of the Previous Fund Raising Activities by China Eastern Airlines Corporation Limited” |

The “Report on the Use of Proceeds of the Previous Fund Raising Activities by China Eastern Airlines Corporation Limited” was prepared in Chinese language. The full text of the English translation of the “Report on the Use of Proceeds of the Previous Fund Raising Activities by China Eastern Airlines Corporation Limited” is set out in Appendix II to this circular. In the event of any discrepancy between the English translation and the Chinese version of the document, the Chinese version shall prevail.

The proposal in relation to the “Report on the Use of Proceeds of the Previous Fund Raising Activities by China Eastern Airlines Corporation Limited” will be submitted, by way of ordinary resolution, for the Shareholders’ consideration and approval at the AGM.

| 6. | Proposal in relation to the A Share Subscription Agreement entered into between the Company and CEA Holding |

The proposal in relation to the A Share Subscription Agreement entered into between the Company and CEA Holding on 10 May 2022 (pursuant to which the Company has conditionally agreed to allot and issue to CEA Holding and CEA Holding has agreed to subscribe for A Shares in the amount of not less than RMB5 billion under the Non-public Issuance of A Shares) and the transaction contemplated therein will be submitted, by way of special resolution, for the Independent Shareholders’ consideration and approval at the AGM, the A Shareholders Class Meeting and the H Shareholders Class Meeting.

| 7. | Proposal in relation to the dilution of current returns by the Non-public Issuance of A Shares and remedial measures and the undertakings thereof by the controlling Shareholder, the Directors and the senior management |

In accordance with the Certain Opinions of the State Council on Further Promoting the Sound Development of Capital Markets (Guo Fa [2014] No. 17) (《國務院關於進一步促進資本市場健康發展的若干意見》 (國發[2014]17號)), the Opinions of the General Office of the State Council on Further Strengthening the Work of Protection of the Legitimate Rights and Interests of Minority Investors in the Capital Markets (Guo Ban Fa [2013] No. 110) (《國務院辦公廳關於進一步加強資本市場中小投資者合法權益保護工作的意見》 (國辦發[2013]110號)) and the Guidelines on Matters concerning the Dilution of Current Returns of the Initial Offering, Refinancing and Major Asset Restructuring (CSRC Notice [2015] No. 31) (《關於首發及再融資、重大資產重組攤薄即期 回報有關事項的指導意見》 (證監會公告[2015]31號)), in order to protect the rights to information and interests of minority investors, the Company carefully analysed and calculated the impact on the dilution of current returns caused by the Non-public Issuance of A Shares. Please refer to Appendix III to this circular for details of the main measures adopted by the Company for the dilution of current returns caused by the Non-public Issuance of A Shares and the undertakings thereof by the controlling Shareholder, the Directors and the senior management.

— 16 —

Table of Contents

LETTER FROM THE BOARD

The proposal in relation to the dilution of current returns by the Non-public Issuance of A Shares and remedial measures and the undertakings thereof by the controlling Shareholder, the Directors and the senior management will be submitted, by way of ordinary resolution, for the Shareholders’ consideration and approval at the AGM.

| 8. | Proposal in relation to the “Future Plan for Return to the Shareholders for the Coming Three Years (2022–2024) of China Eastern Airlines Corporation Limited” |

In order to improve and refine the scientific, sustainable, stable and transparent decision-making for dividend distribution and supervision mechanisms as well as further highlight the importance of return to the Shareholders, pursuant to the relevant requirements of the Notice regarding Further Implementation of Cash Dividend Distribution by Listed Companies (Zheng Jian Fa [2012] No.37) (《關於進一步落實上市公司現金分紅有關事項的通知》 (證監發[2012]37號)) and the No.3 Guidelines for the Supervision on Listed Companies — Cash Dividend Distribution of Listed Companies (CSRC Announcement [2013] No. 43) (《上市公司監管指引第 3號 — 上市公司現金分紅》 (證監會公告[2013]43號) ) issued by the CSRC and the Articles, the Company has formulated the plan for return to the Shareholders for the coming three years (2022–2024).

The “Future Plan for Return to the Shareholders for the Coming Three Years (2022–2024) of China Eastern Airlines Corporation Limited” was prepared in Chinese language. The full text of the English translation of the “Future Plan for Return to the Shareholders for the Coming Three Years (2022–2024) of China Eastern Airlines Corporation Limited” is set out in Appendix IV to this circular. In the event of any discrepancy between the English translation and the Chinese version of the document, the Chinese version shall prevail.

The proposal in relation to the “Future Plan for Return to the Shareholders for the Coming Three Years (2022–2024) of China Eastern Airlines Corporation Limited” will be submitted, by way of ordinary resolution, for the Shareholders’ consideration and approval at the AGM.

— 17 —

Table of Contents

LETTER FROM THE BOARD

| 9. | Proposal in relation to the authorization to the Board and its authorized persons to proceed with relevant matters in respect of the Non-public Issuance of A Shares in their sole discretion |

In order to ensure the efficient, orderly and smooth progress of the Non-public Issuance of A Shares, in accordance with laws and regulations such as the Company Law of the PRC, the Securities Law of the PRC, the Administrative Measures for the Issuance of Securities by Listed Companies and the Implementation Rules for the Non-public Issuance of Stocks by Listed Companies as well as relevant regulations of stock exchanges and the Articles, it is proposed to the Board to agree to propose to the AGM, the A Shareholders Class Meeting and the H Shareholders Class Meeting to authorize the Board and its authorized persons (i.e. the chairman and/or vice chairman of the Company) to, in their sole discretion, proceed with the specific matters related to the Non-public Issuance of A Shares, including but not limited to:

| (i) | authorizing the Board and its authorized persons, according to the proposal for the Non-public Issuance of A Shares considered and approved at the AGM, the A Shareholders Class Meeting and the H Shareholders Class Meeting as well as the specific proposal at the time of issuance, subject to all applicable laws and regulations and the regulations or requirements of relevant regulatory authorities or departments, to determine the method of issuance, number of shares to be issued, issue price, subscribers, time of issuance, date of commencement and expiration of issuance and etc., and to adjust the above proposal within the scope of the proposal for the Non-public Issuance of A Shares approved at the AGM, the A Shareholders Class Meeting and the H Shareholders Class Meeting when there is any change in the policies of regulatory authorities on non-public issuance of shares or when there is any change in market conditions; |

| (ii) | authorizing the Board and its authorized persons, subject to the regulatory requirements of the CSRC and other relevant regulatory authorities, to determine the issue price and the number of shares to be issued to the subscribers within the scope of the proposal for the Non-public Issuance of A Shares approved at the AGM, the A Shareholders Class Meeting and the H Shareholders Class Meeting; |

| (iii) | authorizing the Board and its authorized persons to revise, supplement, sign, submit, report and execute all agreements or documents related to the Non-public Issuance of A Shares and share subscription, including but not limited to subscription agreement, supplemental agreement to the subscription agreement and other documents to be signed for the purpose of the closing of the Non-public Issuance of A Shares, sponsor agreement, underwriting agreement, supervision agreement on proceeds, agreement on the engagement of intermediaries, all applications or filing documents submitted to regulatory authorities such as state-owned assets supervision departments, civil aviation supervision departments and the CSRC, written communications with state-owned assets supervision departments, civil aviation supervision departments and the CSRC on new share issuance and share subscription (if any) and etc., and to proceed with information disclosure matters related to the issuance in accordance with regulatory requirements; |

| (iv) | authorizing the Board and its authorized persons, upon completion of the Non-public Issuance of A Shares, to proceed with the registration, listing and lock-up of shares, to amend the relevant terms in the Articles related to the issuance according to the actual circumstances of issuance and submit to the relevant government departments and regulatory authorities for approval or filing, and to proceed with the registration of change in business, the registration and custody of new shares and other relevant matters with the administration for industry and commerce and other relevant government departments; |

— 18 —

Table of Contents

LETTER FROM THE BOARD

| (v) | authorizing the Board and its authorized persons, within the scope of the resolutions approved at the AGM, the A Shareholders Class Meeting and the H Shareholders Class Meeting, to make corresponding adjustments on the Non-public Issuance of A Shares and the plan for the use of proceeds at the request of the approval authorities, and approve and sign the corresponding amendments to issuance filings such as financial reports, profit forecasts (if any) and etc.; to make appropriate adjustments to the plan for the use of proceeds and its specific arrangements according to the actual progress and actual requirements of the projects to be funded with the proceeds; to self-raise funds to implement the projects to be funded with the proceeds before receiving the proceeds, and replace such funds after receiving the proceeds; and to make necessary adjustments to the projects to be funded with the proceeds in accordance with relevant laws and regulations, requirements of regulatory authorities and market conditions; |

| (vi) | authorizing the Board and its authorized persons to sign the documents related to the Non-public Issuance of A Shares, and to proceed with other matters related to the Non-public Issuance of A Shares; |

| (vii) | authorizing the Board and its authorized persons to set up a special account for the proceeds, and to proceed with the capital verification procedures related to the issuance; |

| (viii) | authorizing the Board and its authorized persons to decide and engage professional intermediaries (including sponsors, underwriters, accountants, lawyers and etc.) to undertake work related to the issuance, including but not limited to making and submitting documents in accordance with regulatory requirements and etc., and to decide the payment of remuneration to such intermediaries and other relevant matters; |

| (ix) | authorizing the Board and its authorized persons to decide and proceed with all other matters related to the Non-public Issuance of A Shares subject to all applicable laws and regulations and the regulations or requirements of relevant regulatory authorities or departments; and |

| (x) | the authorization shall remain valid for twelve (12) months from the date on which the resolution of this authorization is approved at the AGM, the A Shareholders Class Meeting and the H Shareholders Class Meeting. |

The proposal in relation to the authorization to the Board and its authorized persons the full discretion to deal with the relevant matters of the Non-public Issuance of A Shares will be submitted, by way of special resolution, for the Independent Shareholders’ consideration and approval at the AGM, the A Shareholders Class Meeting and the H Shareholders Class Meeting.

| III. | CONNECTED TRANSACTION IN RELATION TO THE PROPOSED SUBSCRIPTION OF A SHARES BY CEA HOLDING |

According to the proposal for the Non-public Issuance of A Shares, the Company and CEA Holding entered into the A Share Subscription Agreement on 10 May 2022, pursuant to which, in accordance with and subject to the terms and conditions under the A Share Subscription Agreement, the Company has agreed to allot and issue to CEA Holding and CEA Holding has agreed to subscribe for A Shares in the amount of not less than RMB5 billion under the Non-public Issuance of A Shares in cash.

— 19 —

Table of Contents

LETTER FROM THE BOARD

Principal Terms of the A Share Subscription Agreement

The principal terms of the A Share Subscription Agreement are the same as the proposed Non-public Issuance of A Shares disclosed above. Other principal terms of the A Share Subscription Agreement are as follows:

| Payment: | Upon the satisfaction of all of the conditions precedent stipulated in the A Share Subscription Agreement, CEA Holding shall subscribe for the A Shares issued by the Company in accordance with the A Share Subscription Agreement and make payment for such subscription into the designated bank account within five business days upon receipt of the payment notice of the subscription. | |

| Conditions precedent: | The A Share Subscription Agreement will become effective when it is duly signed by the Company and CEA Holding and all of the following conditions are fulfilled:

(i) according to the articles of association of CEA Holding, the competent body of CEA Holding has passed relevant resolution(s) to approve the subscription of A Shares by CEA Holding under the Non-public Issuance of A Shares and other relevant matters;

(ii) the proposal for the Non-public Issuance of A Shares and relevant matters have been considered and approved by the Board and the AGM and the Class Meetings;

(iii) the Non-public Issuance of A Shares has been approved by the bodies performing the supervision and management duty of state-owned assets; and

(iv) the Non-public Issuance of A Shares has been approved by the CSRC.

Neither the Company nor CEA Holding has the right to waive any of the conditions above.

As at the Latest Practicable Date, the Non-public Issuance of A Shares has been considered and approved by the Board and the board of directors of CEA Holding. None of the other conditions under the A Share Subscription Agreement has been fulfilled. | |

— 20 —

Table of Contents

LETTER FROM THE BOARD

| Liability for breach of contract: | Save for otherwise caused by any force majeure event, it shall constitute a breach of the A Share Subscription Agreement if any party fails to perform its obligations or undertakings under the A Share Subscription Agreement or the statements or guarantees made are false or materially incorrect.

If any party fails to perform the obligations, statements, guarantees or undertakings under the A Share Subscription Agreement, it shall constitute a breach of the A Share Subscription Agreement, and the non-defaulting party shall be entitled to require the breaching party to bear the liability for such breach. When the breach is caused by any force majeure event, the breaching party shall not be liable. After the A Share Subscription Agreement comes into effect, if CEA Holding gives up the subscription of the Non-public Issuance of A Shares without justified reasons, CEA Holding shall pay the Company damages equivalent to 5% of the subscription amount.

The non-fulfilment of any of the conditions precedent above shall not constitute any breach of the A Share Subscription Agreement by any party.

If any material adverse change in the operation of the Company occurs during the process of approval of the Non-public Issuance of A Shares, CEA Holding shall be entitled to give up the subscription and will not constitute a breach of contract. |

The resolution in relation to the proposed subscription of A Shares by CEA Holding which constitutes a connected transaction of the Company will be submitted, by way of special resolution, for the Independent Shareholders’ consideration and approval at the AGM, the A Shareholders Class Meeting and the H Shareholders Class Meeting.

| IV. | REASONS FOR AND BENEFITS OF THE NON-PUBLIC ISSUANCE OF A SHARES |

The proceeds to be raised from the Non-public Issuance of A Shares, after deducting relevant issuance expenses, will be used for introducing 38 aircraft and supplementing the working capital.

The projects to be funded with the proceeds will facilitate the expansion of fleet size and optimization of fleet structure, improve the Company’s air transportation capacity, ensure the sound development of the Company’s business, and promote the smooth implementation of the Company’s strategy. At the same time, the Company’s capital strength and scale of assets will be improved, and thus the Company will be able to effectively respond to the adverse impact of the COVID-19 pandemic, ease the pressure on capital requirements for its daily operating activities, maintain its sustainable development, and reinforce and enhance its industry position, thereby providing better investment returns for investors.

— 21 —

Table of Contents

LETTER FROM THE BOARD

After receiving the proceeds from the Non-public Issuance of A Shares, the scale of total assets and net assets of the Company will be increased, the financial condition of the Company will be further optimized, the working capital will be further enriched, and the capital strength, risk-resistance capability and subsequent financing capability of the Company will be improved.

The connected transaction in relation to the proposed subscription of A Shares by CEA Holding will enable the Company to obtain more support from the controlling Shareholder and further enhance its investment value. As one of the Subscribers of the Non-public Issuance of A Shares, CEA Holding shows its confidence in the future development of the Company and its determination in continuously supporting the development of the Company, which will facilitate the enhancement of investment value of the Company, thereby maximizing the interests of the Shareholders and effectively safeguarding the interests of the minority Shareholders.

Based on the foregoing, the Directors (including the independent non-executive Directors) are of the opinion that the terms of the A Share Subscription Agreement are fair and reasonable and in the interest of the Company and the Shareholders as a whole.

— 22 —

Table of Contents

LETTER FROM THE BOARD

| V. | EFFECT OF NON-PUBLIC ISSUANCE OF A SHARES ON THE SHAREHOLDING STRUCTURE OF THE COMPANY |

For reference and explanation purposes only, on the assumption that (i) there is no other change in the number of shares in issue of the Company from the Latest Practicable Date to the completion of the Non-public Issuance of A Shares; (ii) the Board exercises in full the Specific Mandate to issue new A Shares (i.e. 5,662,332,023 A Shares); (iii) CEA Holding has subscribed for 1,887,444,007 A Shares (i.e. one-third of the maximum number of shares to be issued under the Non-public Issuance of A Shares, which is proportional to the minimum amount in which CEA Holding has agreed to subscribe for (i.e. RMB5 billion) divided by the maximum proceeds expected to be raised (i.e. RMB15 billion) under the Non-public Issuance of A Shares); and (iv) other Subscribers have subscribed for 3,774,888,016 A Shares (i.e. the maximum number of shares to be issued under the Non-public Issuance of A Shares minus the number of shares assumed to be subscribed by CEA Holding), the potential changes in the shareholding structure of the Company are as follows:

As at the Latest Practicable Date | Immediately after completion of the Non-public Issuance of A Shares | |||||||||||||||

Number of shares held | Approximate percentage of the total number of shares in issue | Number of shares held | Approximate percentage of the total number of shares in issue | |||||||||||||

CEA Holding and its associates Note 1 | | 8,025,170,875 (A Shares | ) | | 42.52 | % | | 9,912,614,882 (A Shares | ) | | 40.40 | % | ||||

| | 2,626,240,000 (H Shares | ) | | 13.91 | % | | 2,626,240,000 (H Shares | ) | | 10.70 | % | |||||

|

|

|

|

|

|

|

| |||||||||

Subtotal | 10,651,410,875 | 56.43 | % | 12,538,854,882 | 51.10 | % | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Other non-public Shareholders Note 2 | | 3,960 (A Shares | ) | | 0.00 | % | | 3,960 (A Shares | ) | | 0.00 | % | ||||

|

|

|

|

|

|

|

| |||||||||

Subtotal | 3,960 | 0.00 | % | 3,960 | 0.00 | % | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Public Shareholders Note 3 | | 5,672,487,466 (A Shares | ) | | 30.05 | % | | 9,447,375,482 (A Shares | ) | | 38.50 | % | ||||

| | 2,550,537,777 (H Shares | ) | | 13.51 | % | | 2,550,537,777 (H Shares | ) | | 10.39 | % | |||||

|

|

|

|

|

|

|

| |||||||||

Subtotal | 8,223,025,243 | 43.57 | % | 11,997,913,259 | 48.90 | % | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Total | 18,874,440,078 | 100 | % | 24,536,772,101 | 100 | % | ||||||||||

|

|

|

|

|

|

|

| |||||||||

| Note 1: | As at the Latest Practicable Date, the total number of shares in issue of the Company is 18,874,440,078. CEA Holding directly and indirectly holds 10,651,410,875 shares of the Company in aggregate, representing approximately 56.43% of the total number of shares in issue of the Company, among which: |

| (i) | CEA Holding directly held 7,567,853,802 A Shares; |

| (ii) | CEA Holding, through CES Finance Holding Co., Ltd. (a wholly-owned subsidiary of CEA Holding), holds 457,317,073 A Shares; and |

| (iii) | CEA Holding, through CES Global Holdings (Hong Kong) Limited (a wholly-owned subsidiary of CEA Holding), holds 2,626,240,000 H Shares. |

| Note 2: | As at the Latest Practicable Date, Mr. Li Yangmin, a Director, directly holds 3,960 A Shares in the capacity of beneficial owner, and the shares held by him shall not be regarded as being in public hands. |

— 23 —

Table of Contents

LETTER FROM THE BOARD

| Note 3: | As at the Latest Practicable Date, Juneyao Group directly holds 311,831,909 A Shares and indirectly holds (i) 219,400,137 A Shares through Juneyao Airlines Co., Ltd.; (ii) 589,041,096 A Shares through Shanghai Jidaohang Enterprise Management Company Limited; (iii) 546,769,777 H Shares through Shanghai Juneyao Airline Hong Kong Limited; and (iv) 12,000,000 H Shares through Juneyao Airlines Co., Ltd. Therefore, Juneyao Group directly and indirectly holds approximately 8.90% of the shares of the Company in aggregate, and the shares held by it shall be regarded as being in public hands. |

It is expected that the Subscribers (other than CEA Holding) are not and will not become core connected persons after the completion of the Non-public Issuance of A Shares, and thus the shares held by them will be regarded as being in public hands.

| Note 4: | For reference and explanation purposes only, based on the aforementioned assumptions, the public float is expected to be approximately 48.90% upon completion of the Non-public Issuance of A Shares. |

| Note 5: | Any discrepancies in this table between totals and sums of amounts listed in the table above are due to rounding. |

For reference and explanation purposes only, based on the aforementioned assumptions, upon completion of the Non-public Issuance of A Shares, the shareholding percentage of CEA Holding in the Company will decrease from approximately 56.43% to approximately 51.10%. CEA Holding will remain as the controlling Shareholder of the Company, and the control of the Company will remain unchanged.

Upon completion of the Non-public Issuance of A Shares, according to the public information available to the Company and to the knowledge of the Directors, the Directors believe that the Company will continue to comply with the requirement of minimum public float under Rule 8.08(1)(a) of the Hong Kong Listing Rules.

| VI. | PROCEEDS RAISED OVER THE PAST 12 MONTHS |

On 9 November 2021, the Company completed the non-public issuance of 2,494,930,875 A Shares to CEA Holding, raising approximately RMB10.828 billion of gross proceeds. As at the date of the Latest Practicable Date, the proceeds from the previous issuance have been fully utilized. For details, please refer to the announcement of the Company dated 30 March 2022 published on the website of the Hong Kong Stock Exchange.

The use of the proceeds from the previous non-public issuance of A Shares of the Company is as follows:

| No. | Name of project | Amount of proceeds applied | ||||

| (RMB billion) | ||||||

1 | Supplementing the working capital | 4.828 | ||||

2 | Repaying debts | 6.000 | ||||

Total | 10.828 | |||||

The use of proceeds from the previous issuance is in line with the plan for the use of proceeds disclosed by the Company, and there is no material change in such respect.

Save as disclosed above, during the 12 months prior to the Latest Practicable Date, the Company did not conduct any other financing activities involving the issuance of equity securities.

— 24 —

Table of Contents

LETTER FROM THE BOARD

| VII. | PROPOSED AMENDMENTS TO THE ARTICLES |

Upon completion of the Non-public Issuance of A Shares, there will be changes in the Company’s registered capital, total amount of shares and etc. In light of the aforementioned circumstances, the Board proposed to seek the approval of the Shareholders at the AGM in respect of authorizing the Board and its authorized persons (it is advised that the persons authorized by the Board should be the chairman and/or the authorized persons of the chairman), upon completion of the Non-public Issuance of A Shares, pursuant to the results of the Non-public Issuance of A Shares, to make necessary amendments to the relevant terms in the Articles, and perform in time the obligations of disclosure of relevant information.

Details of the proposed amendments are as follows:

| (1) | Article 21 of the current Articles: |

As approved by the CSRC, the total amount of shares of the Company is 18,874,440,078 shares.

Amended to be:

As approved by the CSRC, the total amount of shares of the Company is [●] shares.

| (2) | Article 22 of the current Articles: |

The Company has issued a total of 18,874,440,078 ordinary shares, comprising a total of 13,697,662,301 A Shares, representing 72.57% of the total share capital of the Company, a total of 5,176,777,777 H Shares, representing 27.43% of the total share capital of the Company.

Amended to be:

The Company has issued a total of [●] ordinary shares, comprising a total of [●] A Shares, representing [●]% of the total share capital of the Company, a total of 5,176,777,777 H Shares, representing [●]% of the total share capital of the Company.

| (3) | Article 25 of the current Articles: |

The registered capital of the Company is RMB18,874,440,078.

Amended to be:

The registered capital of the Company is RMB[●].

The proposal to authorize the Board and its authorized persons to proceed with relevant matters in respect of the Non-public Issuance of A Shares in their sole discretion will be submitted, by way of special resolution, for the Shareholders’ consideration and approval at the AGM.

— 25 —

Table of Contents

LETTER FROM THE BOARD

| VIII. | IMPLICATIONS UNDER THE HONG KONG LISTING RULES |

As at the Latest Practicable Date, CEA Holding is the controlling Shareholder which held approximately 56.43% of the total number of shares in issue of the Company, and therefore is a connected person of the Company under the Hong Kong Listing Rules. Thus, the proposed subscription of A Shares by CEA Holding under the A Share Subscription Agreement constitutes a connected transaction of the Company and is subject to the reporting, announcement and Independent Shareholders’ approval requirements under Chapter 14A of the Hong Kong Listing Rules.

Mr. Liu Shaoyong, Mr. Li Yangmin, Mr. Tang Bing, Mr. Lin Wanli and Mr. Jiang Jiang, being the Directors of the Company, are also the directors of CEA Holding, and therefore are regarded as having a material interest in the Non-public Issuance of A Shares under the Specific Mandate and the proposed subscription of A Shares by CEA Holding under the A Share Subscription Agreement, and thus have abstained from voting on the relevant Board resolutions. Save as disclosed above, none of the Directors has any material interest in the Non-public Issuance of A Shares under the Specific Mandate and the proposed subscription of A Shares by CEA Holding under the A Share Subscription Agreement, and hence no other Director has abstained from voting on such Board resolutions.

The A Shares to be issued under the Non-public Issuance of A Shares will be issued pursuant to the Specific Mandate to be sought from the Independent Shareholders at the AGM and the Class Meetings.

| IX. | ESTABLISHMENT OF INDEPENDENT BOARD COMMITTEE AND APPOINTMENT OF INDEPENDENT FINANCIAL ADVISER |

The Independent Board Committee (comprising Cai Hongping, Dong Xuebo, Sun Zheng and Lu Xiongwen, being all of the independent non-executive Directors) has been formed in accordance with Chapter 14A of the Hong Kong Listing Rules to advise the Independent Shareholders on the connected transaction in relation to the proposed subscription of A Shares by CEA Holding.

Octal Capital Limited has been appointed as the Independent Financial Adviser to advise the Independent Board Committee and the Independent Shareholders on the connected transaction in relation to the proposed subscription of A Shares by CEA Holding.

| X. | GENERAL INFORMATION |

Information in relation to the Group

The Group is principally engaged in the operation of civil aviation passenger transport and related businesses.

Information in relation to CEA Holding

CEA Holding is principally engaged in the management of all the state-owned assets and equity interests invested and formed by the state in CEA Holding and its invested entities.

— 26 —

Table of Contents

LETTER FROM THE BOARD

As at the Latest Practicable Date, the controlling shareholder and the actual controller of CEA Holding is the SASAC, and CEA Holding is owned:

| (i) | as to 68.42% by the SASAC; |

| (ii) | as to 11.21% by China Life Investment Insurance Assets Management Company Limited* (國壽投資保險資產管理有限公司), which is directly wholly-owned by China Life Insurance (Group) Company* (中國人壽保險(集團)公司) and ultimately wholly-owned by the State Council of the PRC; |

| (iii) | as to 10.19% by Shanghai Jiushi (Group) Co., Ltd. * (上海久事(集團)有限公司), which is directly wholly-owned by SASAC of Shanghai Municipal Government; |

| (iv) | as to 5.09% by China Reform Asset Management Co., Ltd.* (中國國新資產管理有限公司), which is directly wholly-owned by China Reform Holdings Corporation Ltd.* (中國國新控股有限責任公司) and ultimately wholly-owned by the State Council of the PRC; and |

| (v) | as to 5.09% by China Tourism Group Co., Ltd.* (中國旅遊集團有限公司), which is directly wholly-owned by SASAC. |

| XI. | AGM AND CLASS MEETINGS |

The AGM will be convened at the Conference Room on Second Floor, CEA Development Co., Ltd., Auxiliary Building, No. 99 Konggang Third Road, Changning District, Shanghai, the PRC (中國上海市長寧區空港三路99號東航實業集團有限公司輔樓二樓會議室 ) at 2 p.m. on Wednesday, 29 June 2022 to consider, and if thought fit, approve resolutions relating to, among others, (i) the Non-public Issuance of A Shares under the Specific Mandate; (ii) the connected transaction in relation to the proposed subscription of A Shares by CEA Holding; and (iii) the proposed amendments to the Articles. Details of the AGM and the resolutions to be proposed at the AGM are set out in the “Notice of 2021 Annual General Meeting” despatched on 13 May 2022 by the Company.

The H Shareholders Class Meeting and the A Shareholders Class Meeting will be convened at the Conference Room on Second Floor, CEA Development Co., Ltd., Auxiliary Building, No. 99 Konggang Third Road, Changning District, Shanghai, the PRC (中國上海市長寧區空港三路99號東航實業集團有限公司輔樓二樓會議室) at 2:30 p.m. on Wednesday, 29 June 2022 (or immediately after the conclusion or adjournment of the AGM which will be held at the same place and on the same date), to consider, and if thought fit, approve resolution relating to, among others, the Non-public Issuance of A Shares under the Specific Mandate. Details of the H Shareholders Class Meeting and the resolutions to be proposed at the H Shareholders Class Meeting are set out in the “Notice of H Shareholders Class Meeting” despatched on 13 May 2022 by the Company.

— 27 —

Table of Contents

LETTER FROM THE BOARD

As at the Latest Practicable Date, CEA Holding is the controlling Shareholder which, together with its associates (including CES Finance and CES Global (both being wholly-owned subsidiaries of CEA Holding)) and Mr. Li Yangmin (a director of CEA Holding) held 10,651,418,795 shares of the Company in aggregate, representing approximately 56.43% of the issued share capital of the Company. Accordingly, CEA Holding, CES Finance, CES Global and Mr. Li Yangmin, who own shares of the Company, are required to abstain from voting in respect of resolutions 9, 10, 13, 14 and 17 set out in the “Notice of 2021 Annual General Meeting”, and CES Global, who owns H Shares, is required to be abstain from voting in respect of the resolutions 1, 2, 4, 5 and 6 set out in the “Notice of H Shareholders Class Meeting”. To the extent that the Company is aware having made all reasonable enquiries, as at the Latest Practicable Date:

| (i) | there was no voting trust or other agreement, arrangement or understanding (other than an outright sale) entered into by or binding upon CEA Holding, CES Finance, CES Global or Mr. Li Yangmin; |

| (ii) | none of CEA Holding, CES Finance, CES Global or Mr. Li Yangmin was subject to any obligation or entitlement whereby they had or might have temporarily or permanently passed control over the exercise of the voting rights in respect of their respective shares in the Company to a third party, whether generally or on a case-by-case basis; and |