QuickLinks -- Click here to rapidly navigate through this document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

|

|

|---|

| (Mark One) |

| o | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | OR |

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2002 |

| | OR |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to |

Commission file number 333-6690

SUN MEDIA CORPORATION/CORPORATION SUN MEDIA

(Exact name of Registrant as specified in its charter)

BRITISH COLUMBIA, CANADA

(Jurisdiction of incorporation or organization)

333 King Street East, Toronto, Ontario, Canada M5A 3X5

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act: None.

Securities registered or to be registered pursuant to Section 12(g) of the Act: None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None.

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report: 1,261,000 Class A Shares issued and outstanding.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

o Yes ý No

Indicate by check mark which financial statement item the registrant has elected to follow.

o Item 17 ý Item 18

TABLE OF CONTENTS

| EXPLANATORY NOTES | | ii |

| FORWARD-LOOKING STATEMENTS | | ii |

| INDUSTRY AND MARKET DATA | | iii |

| PRESENTATION OF FINANCIAL INFORMATION | | iii |

| EXCHANGE RATE INFORMATION | | iv |

| PART I | | 1 |

| Item 1. | | Identity of Directors, Senior Management and Advisers | | 1 |

| Item 2. | | Offer Statistics and Expected Timetable | | 1 |

| Item 3. | | Key Information | | 1 |

| Item 4. | | Information on the Company | | 11 |

| Item 5. | | Operating and Financial Review and Prospects | | 27 |

| Item 6. | | Directors, Senior Management and Employees | | 41 |

| Item 7. | | Major Shareholders and Related Party Transactions | | 48 |

| Item 8. | | Financial Information | | 50 |

| Item 9. | | The Offer and Listing | | 51 |

| Item 10. | | Additional Information | | 52 |

| Item 11. | | Quantitative and Qualitative Disclosures about Market Risk | | 64 |

| Item 12. | | Description of Securities other than Equity Securities | | 65 |

| PART II | | 66 |

| Item 13. | | Defaults, Dividend Arrearages and Delinquencies | | 66 |

| Item 14. | | Material Modifications to the Rights of Security Holders and Use of Proceeds | | 66 |

| Item 15. | | Controls and Procedures | | 66 |

| Item 16. | | [Reserved] | | 66 |

| PART III | | 66 |

| Item 17. | | Financial Statements | | 66 |

| Item 18. | | Financial Statements | | 66 |

| Item 19. | | Exhibits | | 66 |

| Signature | | 70 |

| Certifications | | 70 |

i

EXPLANATORY NOTES

All references in this annual report to "Sun Media," "SMC" or the "Company," as well as use of the terms "we," "us," "our" or similar terms, are references to Sun Media Corporation, a company continued under the laws of British Columbia, and, unless the context otherwise requires, its subsidiaries and operating companies.

Unless otherwise indicated, information provided in this annual report, including all operating data presented, is as of December 31, 2002.

FORWARD-LOOKING STATEMENTS

This annual report contains both historical and forward-looking statements within the meaning of Section 27A of the U.S. Securities Act of 1933 (as amended, the "Securities Act") and Section 21E of the Securities Exchange Act of 1934 (as amended, the "Exchange Act"). These forward-looking statements are not historical facts, but only predictions, and generally can be identified by the use of statements that include phrases such as "believe," "expect," "anticipate," "intend," "plan," "foresee" or other words or phrases of similar import. Similarly, statements that describe our objectives, plans or goals also are forward-looking statements. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those currently anticipated. Factors that could materially affect these forward-looking statements can be found in this annual report. Potential investors and other readers are urged to consider these factors carefully in evaluating the forward-looking statements, including the factors described below under "Item 3. Key Information — Risk Factors" and are cautioned not to place undue reliance on these forward-looking statements. The forward-looking statements included in this document are made only as of the date of this annual report, and we undertake no obligation to publicly update these forward-looking statements to reflect new information, future events or otherwise. In light of these risks, uncertainties and assumptions, the forward-looking events might or might not occur. We cannot assure you that projected results or events will be achieved.

ii

INDUSTRY AND MARKET DATA

Market data and industry statistics used throughout this annual report were obtained from internal surveys, market research, publicly available information and industry publications. Industry publications generally state that the information contained in them has been obtained from sources believed to be reliable, but that the accuracy and completeness of this information is not guaranteed. Similarly, internal surveys and industry and market data, while believed to be reliable, have not been independently verified, and we make no representation as to the accuracy of this information.

PRESENTATION OF FINANCIAL INFORMATION

We state our financial statements in Canadian dollars. In this annual report, references to Canadian dollars, Cdn$ or $ are to the currency of Canada, and references to U.S. dollars or US$ are to the currency of the United States.

Our consolidated financial statements have been prepared in accordance with the accounting principles generally accepted in Canada, or Canadian GAAP. For a discussion of the principal differences between Canadian GAAP and the accounting principles generally accepted in the United States, or U.S. GAAP, see note 18 to our audited consolidated financial statements.

We are the successor company to 2944707 Canada Inc., a corporation to which Quebecor Inc., or Quebecor, transferred the majority of its newspaper operations, or Quebecor Newspapers, in December 1998. 2944707 Canada Inc. acquired Sun Media Corporation, or Old Sun Media, on January 7, 1999, and subsequently amalgamated with Old Sun Media on February 28, 1999. At the time of the acquisition of Le Groupe Vidéotron ltée, or Vidéotron, by Quebecor in October 2000, we were transferred to Quebecor Media Inc., or Quebecor Media, a subsidiary of Quebecor. For financial reporting purposes, Quebecor Newspapers is our predecessor, and therefore its consolidated results are included in this annual report for the year ended December 31, 1998. For subsequent years, the consolidated results include the results of Old Sun Media only from January 7, 1999, the date of its acquisition by Quebecor Newspapers.

We refer to EBITDA a number of times in this annual report. EBITDA for us means earnings before depreciation, amortization, restructuring charges, financial expenses, dividend income, income taxes, non-controlling interest and discontinued operations. EBITDA is not intended to be a measure that should be regarded as an alternative to other financial operating performance measures or to the statement of cash flows as a measure of liquidity. It is not intended to represent funds available for debt service, dividends, reinvestment or other discretionary uses; it should not be considered in isolation as a substitute for measures of performance prepared in accordance with U.S. or Canadian GAAP. EBITDA is used in this annual report because we believe that EBITDA is a meaningful measure of performance commonly used in the publishing industry and by the investment community to analyze and compare companies. Our definition of EBITDA may not be identical to similarly titled measures reported by other companies. We provide the calculation of EBITDA used in this annual report under Canadian GAAP and U.S. GAAP, and the reconciliation of EBITDA used in this annual report to cash flows under Canadian GAAP and U.S. GAAP, in footnote 7 to the tables under "Item 3. Key Information — Selected Financial Data."

iii

EXCHANGE RATE INFORMATION

The following table presents the average, high, low and end of period noon buying rates for the periods indicated, in the City of New York for cable transfers in foreign currencies, as certified for customs purposes by the Federal Reserve Bank of New York. Such rates are presented as U.S. dollars per $1.00 and are the inverse of rates quoted by the Federal Reserve Bank of New York for Canadian dollars per US$1.00. On March 25, 2003, the inverse of the noon buying rate was $1.00 equals US$0.6770.

Year Ended

| | Average(1)

| | High

| | Low

| | Period End

|

|---|

| December 31, 2002 | | 0.6370 | | 0.6619 | | 0.6200 | | 0.6329 |

| December 31, 2001 | | 0.6446 | | 0.6697 | | 0.6241 | | 0.6279 |

| December 31, 2000 | | 0.6727 | | 0.6969 | | 0.6410 | | 0.6669 |

| December 31, 1999 | | 0.6746 | | 0.6925 | | 0.6535 | | 0.6925 |

| December 31, 1998 | | 0.6722 | | 0.7105 | | 0.6341 | | 0.6504 |

Month Ended

| | Average(2)

| | High

| | Low

| | Period End

|

|---|

| February 28, 2003 | | 0.6613 | | 0.6720 | | 0.6530 | | 0.6720 |

| January 31, 2003 | | 0.6487 | | 0.6570 | | 0.6349 | | 0.6532 |

| December 31, 2002 | | 0.6414 | | 0.6461 | | 0.6329 | | 0.6329 |

| November 30, 2002 | | 0.6364 | | 0.6440 | | 0.6288 | | 0.6387 |

| October 31, 2002 | | 0.6337 | | 0.6407 | | 0.6272 | | 0.6406 |

| September 30, 2002 | | 0.6345 | | 0.6433 | | 0.6304 | | 0.6304 |

- (1)

- The average of the exchange rates on the last day of each month during the applicable year.

- (2)

- The average of the exchange rates for all days during the applicable month.

iv

PART I

Item 1. Identity of Directors, Senior Management and Advisors

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

Selected Financial Data

The following tables present some consolidated financial information derived from our consolidated balance sheets as at December 31, 2001 and 2002 and statements of income for each of the years ended December 31, 2000, 2001 and 2002 that are included in this annual report. The consolidated financial information as at December 31, 1998, 1999 and 2000 and the years ended December 31, 1998 and 1999 has been derived from our audited consolidated financial statements not included in this annual report. The information presented below the caption "Operating Data" is not derived from our consolidated financial statements. All information contained in the following tables should be read in conjunction with our consolidated financial statements, the notes related to those financial statements and "Item 5. Operating and Financial Review and Prospects."

Our consolidated financial statements have been prepared in accordance with Canadian GAAP. For a discussion of the principal differences between Canadian GAAP and U.S. GAAP, see note 18 to our audited consolidated financial statements.

| | Year Ended December 31,

| |

|---|

| | 1998(1)

| | 1999(1)

| | 2000

| | 2001

| | 2002

| |

|---|

| | (dollars in thousands)

| |

|---|

| AMOUNTS UNDER CANADIAN GAAP | | | | | | | | | | | | | | | | |

| Statement of Income Data: | | | | | | | | | | | | | | | | |

| Revenues | | $ | 295,123 | | $ | 827,068 | | $ | 850,087 | | $ | 838,136 | | $ | 853,610 | |

| Operating expenses | | | 238,296 | | | 639,678 | | | 644,760 | | | 637,292 | | | 631,277 | |

| Depreciation and amortization (2) | | | 6,929 | | | 46,951 | | | 46,671 | | | 47,259 | | | 27,035 | |

| | |

| |

| |

| |

| |

| |

| Operating income before restructuring charges | | | 49,898 | | | 140,439 | | | 158,656 | | | 153,585 | | | 195,298 | |

| Restructuring charges (3) | | | — | | | — | | | — | | | 17,800 | | | 2,195 | |

| | |

| |

| |

| |

| |

| |

| Operating income | | | 49,898 | | | 140,439 | | | 158,656 | | | 135,785 | | | 193,103 | |

| Financial expenses | | | 654 | | | 64,268 | | | 53,085 | | | 42,070 | | | 33,265 | |

| Income taxes (4) | | | 17,235 | | | 35,367 | | | 42,325 | | | 35,611 | | | 52,713 | |

| Income from continuing operations | | | 31,680 | | | 40,050 | | | 62,274 | | | 152,478 | | | 309,175 | |

| Net income (5) | | | 31,680 | | | 38,369 | | | 62,274 | | | 152,478 | | | 309,175 | |

Balance Sheet Data (at period end): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents | | $ | — | | $ | 2,617 | | $ | 3,447 | | $ | 39,168 | | $ | 51,046 | |

| Total assets | | | 122,492 | | | 1,218,093 | | | 1,206,409 | | | 2,898,046 | | | 3,335,892 | |

| Total debt | | | — | | | 710,207 | | | 595,195 | | | 554,512 | | | 515,147 | |

| Capital stock | | | 41,801 | | | 301,801 | | | 301,801 | | | 301,801 | | | 301,801 | |

| Shareholder's equity (6) | | | 36,566 | | | 334,931 | | | 397,426 | | | 2,139,193 | | | 2,599,080 | |

1

Other Financial Data and Ratios: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash from operating activities | | $ | 40,590 | | $ | 74,565 | | $ | 134,027 | | $ | 140,583 | | $ | 400,272 | |

| Cash used in investing activities | | | (16,774 | ) | | (606,864 | ) | | (19,705 | ) | | (1,618,497 | ) | | (431,959 | ) |

| Cash provided by (used in) financing activities | | | (600 | ) | | 535,937 | | | (113,492 | ) | | 1,513,635 | | | 43,565 | |

| EBITDA (unaudited) (7) | | | 56,827 | | | 187,390 | | | 205,327 | | | 200,844 | | | 222,333 | |

| EBITDA margin (unaudited) (7) | | | 19.3 | % | | 22.7 | % | | 24.2 | % | | 24.0 | % | | 26.0 | % |

| Capital expenditures | | $ | 4,915 | | $ | 13,565 | | $ | 19,806 | | $ | 19,207 | | $ | 10,309 | |

| Ratio of earnings to fixed charges (unaudited) (8) | | | N/A | | | 2.16x | | | 2.94x | | | 5.30x | | | 11.48x | |

Operating Data (unaudited) (9): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Monday to Friday Circulation | | | | | | 991,100 | | | 975,400 | | | 955,700 | | | 937,600 | |

| Saturday Circulation | | | | | | 1,033,200 | | | 1,013,100 | | | 973,900 | | | 1,004,300 | |

| Sunday Circulation | | | | | | 1,166,100 | | | 1,146,100 | | | 1,111,000 | | | 1,082,900 | |

| Paid Daily Publications (at period end) | | | | | | 16 | | | 15 | | | 15 | | | 15 | |

| Weekly Publications (at period end) | | | | | | 158 | | | 169 | | | 172 | | | 175 | |

| Other Publications (at period end) | | | | | | 16 | | | 20 | | | 19 | | | 18 | |

| Total Publications (at period end) | | | | | | 190 | | | 204 | | | 206 | | | 208 | |

AMOUNTS UNDER U.S. GAAP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Statement of Income Data: | | | | | | | | | | | | | | | | |

| Revenues | | $ | 295,123 | | $ | 827,068 | | $ | 850,087 | | $ | 838,136 | | $ | 853,610 | |

| Operating expenses | | | 239,920 | | | 641,247 | | | 645,623 | | | 638,275 | | | 632,232 | |

| Depreciation and amortization (2) | | | 6,929 | | | 46,951 | | | 46,548 | | | 47,135 | | | 27,035 | |

| | |

| |

| |

| |

| |

| |

| Operating income before restructuring charges | | | 48,274 | | | 138,870 | | | 157,916 | | | 152,726 | | | 194,343 | |

| Restructuring charges (3) | | | — | | | 2,394 | | | 5,792 | | | 17,800 | | | 2,195 | |

| | |

| |

| |

| |

| |

| |

| Operating income | | | 48,274 | | | 136,476 | | | 152,124 | | | 134,926 | | | 192,148 | |

| Financial expenses | | | 654 | | | 64,268 | | | 53,085 | | | 136,556 | | | 229,051 | |

| Income taxes (4) | | | 16,585 | | | 33,781 | | | 38,349 | | | 1,762 | | | (16,119 | ) |

| Net income | | | 30,706 | | | 35,992 | | | 59,718 | | | 90,982 | | | 181,266 | |

Balance Sheet Data (at period end): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents | | $ | — | | $ | 2,617 | | $ | 3,447 | | $ | 39,168 | | $ | 51,046 | |

| Total assets | | | 121,414 | | | 1,208,336 | | | 1,222,266 | | | 2,933,195 | | | 3,385,389 | |

| Total debt (10) | | | — | | | 710,207 | | | 616,354 | | | 2,287,816 | | | 2,599,871 | |

| Shareholder's equity (10) | | | 38,791 | | | 334,778 | | | 394,717 | | | 443,218 | | | 558,453 | |

Other Financial Data and Ratios (unaudited): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| EBITDA (7) | | $ | 55,203 | | $ | 185,821 | | $ | 204,464 | | $ | 199,861 | | $ | 221,378 | |

| EBITDA margin (7) | | | 18.7 | % | | 22.5 | % | | 24.1 | % | | 23.8 | % | | 25.9 | % |

| Ratio of earnings to fixed charges (8) | | | N/A | | | 2.12x | | | 2.82x | | | 1.67x | | | 1.72x | |

- (1)

- For financial reporting purposes, Quebecor Newspapers is our predecessor. Its consolidated results, therefore, are reflected for the year ended December 31, 1998. For subsequent years, the consolidated results include the results of Old Sun Media only from January 7, 1999, the date of its acquisition by Quebecor Newspapers.

- (2)

- Effective January 1, 2002, we implemented Canadian Institute of Chartered Accountants Handbook Section 3062, Goodwill and Other Intangible Assets.The new standard requires that goodwill and intangible assets with indefinite lives no longer be amortized, but instead be tested for impairment at least annually. At January 1, 2002, we had unamortized goodwill in the amount of $751.7 million, which is no longer being amortized. This change in accounting policy is not applied retroactively and the amounts presented for prior periods have not been restated for this change. If this change in accounting policy were applied to the reported consolidated statements of income, the impact of the change, in respect of goodwill and intangible assets with indefinite useful lives not being amortized, would be as follows:

2

| | Year Ended December 31,

|

|---|

| | 1999

| | 2000

| | 2001

|

|---|

| | (in thousands)

|

|---|

| AMOUNTS UNDER CANADIAN GAAP | | | | | | | | | |

| Net income | | $ | 38,369 | | $ | 62,274 | | $ | 152,478 |

| Add back goodwill amortization net of income taxes | | | 19,319 | | | 19,838 | | | 20,142 |

| | |

| |

| |

|

| Net income before goodwill amortization | | $ | 57,688 | | $ | 82,112 | | $ | 172,620 |

| | |

| |

| |

|

| AMOUNTS UNDER U.S. GAAP | | | | | | | | | |

| Net income | | $ | 35,992 | | $ | 59,718 | | $ | 90,982 |

| Add back goodwill amortization net of income taxes | | | 19,319 | | | 19,715 | | | 20,018 |

| | |

| |

| |

|

| Net income before goodwill amortization | | $ | 55,311 | | $ | 79,433 | | $ | 111,000 |

| | |

| |

| |

|

- (3)

- During 2002, we implemented restructuring initiatives, which resulted in the termination of approximately 60 employees. The 2002 results include a charge of $2.2 million representing severance and other personnel-related costs relating to these initiatives. We also implemented two restructuring initiatives during 2001, resulting in a reduction of over 350 employees. A charge of $17.8 million was recorded in 2001 and consisted primarily of severance, benefits and other personnel-related costs.

- (4)

- The net cash payments for income taxes were $28.0 million in the year ended December 31, 2000, $3.5 million in the year ended December 31, 2001 and net cash receipts of $0.6 million in the year ended December 31, 2002.

- (5)

- Net income for the year ended December 31, 2001 includes dividend income of $95.3 million related to our investment in $1.6 billion of the preferred shares of Quebecor Media, our parent company. Our investment in the preferred shares of Quebecor Media rose to $1.95 billion for the year ended December 31, 2002, and similarly, net income for the year ended December 31, 2002 includes dividend income of $203.2 million. See note 5 to our audited consolidated financial statements.

- (6)

- Shareholder's equity as of December 31, 2001 includes the outstanding balance on the $1.6 billion convertible obligation issued by us to our parent, Quebecor Media, in July 2001. On November 28, 2002, we issued a new convertible obligation to Quebecor Media in the amount of $350.0 million with terms and conditions substantially similar to the $1.6 billion convertible obligation issued in July 2001. Shareholder's equity as of December 31, 2002 includes the outstanding balance on $1.95 billion of these convertible obligations. These convertible obligations are classified as equity under Canadian GAAP because we may elect to convert their unpaid principal amounts and interest into our common shares at any time. The interest on the convertible obligations is charged to retained earnings. See note 9 to our audited consolidated financial statements.

3

- (7)

- EBITDA margin is EBITDA as a percentage of revenues. EBITDA is calculated from net income, and reconciled to cash provided by operating activities, as follows:

| | Year Ended December 31,

| |

|---|

| | 1998

| | 1999

| | 2000

| | 2001

| | 2002

| |

|---|

| | (in thousands)

| |

|---|

| AMOUNTS UNDER CANADIAN GAAP | | | | | | | | | | | | | | | | |

| Net income | | $ | 31,680 | | $ | 38,369 | | $ | 62,274 | | $ | 152,478 | | $ | 309,175 | |

| | Restructuring charges | | | — | | | — | | | — | | | 17,800 | | | 2,195 | |

| | Depreciation and amortization | | | 6,929 | | | 46,951 | | | 46,671 | | | 47,259 | | | 27,035 | |

| | Financial expenses | | | 654 | | | 64,268 | | | 53,085 | | | 42,070 | | | 33,265 | |

| | Income taxes | | | 17,235 | | | 35,367 | | | 42,325 | | | 35,611 | | | 52,713 | |

| | Non-controlling interest | | | 329 | | | 754 | | | 972 | | | 968 | | | 1,118 | |

| | Loss from discontinued operations | | | — | | | 1,681 | | | — | | | — | | | — | |

| | Dividend income | | | — | | | — | | | — | | | (95,342 | ) | | (203,168 | ) |

| | |

| |

| |

| |

| |

| |

| EBITDA as defined | | | 56,827 | | | 187,390 | | | 205,327 | | | 200,844 | | | 222,333 | |

| | Restructuring charges | | | — | | | — | | | — | | | (17,800 | ) | | (2,195 | ) |

| | Financial expenses | | | (654 | ) | | (64,268 | ) | | (53,085 | ) | | (42,070 | ) | | (33,265 | ) |

| | Current income taxes | | | (17,235 | ) | | (25,278 | ) | | (23,584 | ) | | (30,786 | ) | | (47,963 | ) |

| | Dividend income | | | — | | | — | | | — | | | — | | | 203,168 | |

| | Other items not involving cash | | | — | | | 245 | | | 1,324 | | | 1,219 | | | 537 | |

| | Change in non-cash operating working capital | | | 1,652 | | | (23,524 | ) | | 4,045 | | | 29,176 | | | 57,657 | |

| | |

| |

| |

| |

| |

| |

| Cash provided by operating activities | | $ | 40,590 | | $ | 74,565 | | $ | 134,027 | | $ | 140,583 | | $ | 400,272 | |

| | |

| |

| |

| |

| |

| |

| | Year Ended December 31,

| |

|---|

| | 1998

| | 1999

| | 2000

| | 2001

| | 2002

| |

|---|

| | (in thousands)

| |

|---|

| AMOUNTS UNDER U.S. GAAP | | | | | | | | | | | | | | | | |

| Net income | | $ | 30,706 | | $ | 35,992 | | $ | 59,718 | | $ | 90,982 | | $ | 181,266 | |

| | Restructuring charges | | | — | | | 2,394 | | | 5,792 | | | 17,800 | | | 2,195 | |

| | Depreciation and amortization | | | 6,929 | | | 46,951 | | | 46,548 | | | 47,135 | | | 27,035 | |

| | Financial expenses | | | 654 | | | 64,268 | | | 53,085 | | | 136,556 | | | 229,051 | |

| | Income taxes | | | 16,585 | | | 33,781 | | | 38,349 | | | 1,762 | | | (16,119 | ) |

| | Non-controlling interest | | | 329 | | | 754 | | | 972 | | | 968 | | | 1,118 | |

| | Loss from discontinued operations | | | — | | | 1,681 | | | — | | | — | | | — | |

| | Dividend income | | | — | | | — | | | — | | | (95,342 | ) | | (203,168 | ) |

| | |

| |

| |

| |

| |

| |

| EBITDA as defined | | | 55,203 | | | 185,821 | | | 204,464 | | | 199,861 | | | 221,378 | |

| | Restructuring charges | | | — | | | (2,394 | ) | | (5,792 | ) | | (17,800 | ) | | (2,195 | ) |

| | Financial expenses | | | (654 | ) | | (64,268 | ) | | (53,085 | ) | | (136,556 | ) | | (229,051 | ) |

| | Current income taxes | | | (17,235 | ) | | (25,278 | ) | | (23,584 | ) | | 3,503 | | | 21,082 | |

| | Dividend income | | | — | | | — | | | — | | | — | | | 203,168 | |

| | Other items not involving cash | | | — | | | 245 | | | 1,401 | | | 2,489 | | | (583 | ) |

| | Change in non-cash operating working capital | | | 3,276 | | | (19,561 | ) | | 10,623 | | | 89,086 | | | (10,590 | ) |

| | |

| |

| |

| |

| |

| |

| Cash provided by operating activities | | $ | 40,590 | | $ | 74,565 | | $ | 134,027 | | $ | 140,583 | | $ | 203,209 | |

| | |

| |

| |

| |

| |

| |

- (8)

- For the purpose of calculating the ratios of earnings to fixed charges, (i) earnings consist of income from continuing operations before income taxes and non-controlling interest, plus fixed charges, and (ii) fixed charges consist of interest expense, plus amortized premiums, discounts and capitalized expenses related to indebtedness.

- (9)

- Circulation figures represent the average daily paid circulation for the period indicated and include only the 15 paid daily newspapers that we publish. Operating data are not available for the year ended December 31, 1998.

4

- (10)

- Under U.S. GAAP, total debt as of December 31, 2001 includes the outstanding balance on the $1.6 billion convertible obligation issued by us to our parent Quebecor Media in July 2001. On November 28, 2002, we issued a new convertible obligation to Quebecor Media in the amount of $350.0 million with terms and conditions substantially similar to the $1.6 billion convertible obligation issued in July 2001. Under U.S. GAAP, total debt as of December 31, 2002 includes the outstanding balance on $1.95 billion of these convertible obligations. These convertible obligations are classified as equity under Canadian GAAP because we may elect to convert the unpaid principal amounts and interest into our common shares at any time. Shareholder's equity under U.S. GAAP, as of each of December 31, 2001 and December 31, 2002, does not include the applicable outstanding balance on these convertible obligations. See note 18 to our audited consolidated financial statements.

5

Capitalization and Indebtedness

Not applicable.

Reasons for the Offer and Use of Proceeds

Not applicable.

Risk Factors

Our substantial indebtedness and significant interest payment requirements could adversely affect our financial condition and prevent us from fulfilling our obligations.

We currently have a substantial amount of indebtedness. Our substantial indebtedness could have significant consequences, including the following:

- •

- increase our vulnerability to general adverse economic and industry conditions;

- •

- require us to dedicate a substantial portion of our cash flow from operations to making interest and principal payments on our indebtedness;

- •

- limit our ability to fund capital expenditures, working capital and other general corporate purposes;

- •

- limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate;

- •

- place us at a competitive disadvantage compared to our competitors that have less debt; and

- •

- limit our ability to borrow additional funds on commercially reasonable terms, if at all.

We will need a significant amount of cash to service our debt. Our ability to generate cash depends on many factors beyond our control.

Our ability to meet our debt service requirements will depend on our ability to generate cash. Our ability to generate cash depends on many factors beyond our control, such as competition, general economic conditions and newsprint prices. We cannot assure you that we will generate sufficient cash flow from operations or that future distributions will be available to us in amounts sufficient to pay our indebtedness or to fund our other liquidity needs.

Restrictive covenants in our debt instruments may reduce our operating and financial flexibility, which may prevent us from capitalizing on business opportunities and taking some actions.

The terms of outstanding debt instruments contain operating and financial covenants that restrict our ability to, among other things:

- •

- incur additional debt, including guarantees by our restricted subsidiaries;

- •

- pay dividends and make other restricted payments;

- •

- create liens;

- •

- use the proceeds from sales of assets and subsidiary stock;

- •

- create or permit restrictions on the ability of our restricted subsidiaries to pay dividends or make other distributions to us;

- •

- engage in transactions with affiliates;

6

- •

- enter into sale and leaseback transactions; and

- •

- consolidate, merge or sell all or substantially all of our assets.

In addition, events beyond our control, including prevailing economic, financial and industry conditions, may affect our ability to comply with covenants contained in our debt instruments. Our failure to comply with these covenants could result in an event of default which, if not cured or waived, could result in an acceleration of our debt and cross-defaults under our other debt. This acceleration and these cross-defaults could require us to repay or repurchase debt prior to the date it otherwise is due, which could adversely affect our financial condition. Even if we are able to comply with all the applicable covenants, the restrictions on our ability to manage our business in our sole discretion could adversely affect our business by, among other things, limiting our ability to take advantage of financings, mergers, acquisitions and other corporate opportunities that we believe would be beneficial to us.

We may still be able to incur substantially more debt, which could increase the risks described above.

The terms of our existing debt instruments do not fully prohibit us or our subsidiaries from incurring additional debt. We may be able to incur substantial additional debt in the future. If we do so, the risks described above could intensify.

We depend, to a certain extent, on our subsidiaries for cash needed to service our obligations.

For the year ended December 31, 2002, our subsidiaries generated approximately 36% of our revenues (before intercompany eliminations) and held approximately 47% of our consolidated total assets. We, therefore, need the cash generated by our subsidiaries from their operations and their borrowings to service our obligations. Our subsidiaries are not obligated to make funds available to us.

Our subsidiaries' ability to make payments to us will depend upon their operating results and will also be subject to applicable laws and contractual restrictions. Some of our subsidiaries may become subject to loan agreements and indentures that restrict sales of assets and prohibit or significantly restrict the payment of dividends or the making of distributions, loans or advances to shareholders and partners. Our existing debt instruments permit our subsidiaries to incur debt with similar prohibitions and restrictions in the future.

An active trading market for our 75/8% Senior Notes due 2013 may not develop.

There is currently no established trading market for our 75/8% Senior Notes due 2013. After we complete our offer to exchange our old notes issued February 7, 2003 for new notes that have been registered under the Securities Act, we expect that the liquidity of the market for any old notes remaining may be substantially limited. We do not intend to have the new notes listed on a national securities exchange. We have been informed by the initial purchasers that they currently intend to make a market in the new notes. However, they are not obligated to do so, and may cease their market-making activities at any time without notice. Accordingly, we cannot assure you of the liquidity of the market for the new notes or the prices at which you may be able to sell the new notes.

Our revenue is subject to cyclical and seasonal variations.

Our business is sensitive to general economic cycles. Our operating results are sensitive to prevailing local, regional and national economic conditions because of our dependence on advertising sales for a substantial portion of our revenue. Because a substantial portion of our advertising revenue is derived from local advertisers, our operating results in individual markets could be adversely affected by local or regional economic downturns. Similarly, a substantial portion of our advertising revenue is derived from retail advertisers, who have historically been sensitive to general economic cycles, and our

7

operating results have in the past been materially adversely affected by extended downturns in the Canadian retail sector. In addition, most of our advertising contracts are short-term contracts that can be terminated by the advertisers at any time with little notice. Also, newspaper publishing is labor intensive and, as a result, our business has a relatively high fixed cost structure. During periods of economic contraction, revenue may decrease while some of our costs remain fixed, resulting in decreased earnings.

In addition, our business has experienced and is expected to continue to experience significant fluctuations in operating results due to, among other things, seasonal advertising patterns and seasonal influences on people's reading habits. Given those seasonal patterns, our second and fourth quarters have historically been our strongest quarters, with the fourth quarter generally being the strongest and the first quarter being the weakest. In addition, because the majority of our circulation is based on single-copy rather than subscription sales, our circulation levels are more vulnerable to seasonal weather changes.

We may be adversely affected by variations in the cost of newsprint.

Newsprint represents our single largest raw material expense and one of our most significant operating costs. The newsprint industry is highly cyclical, and newsprint prices have historically experienced significant volatility caused by supply and demand imbalances. Since a period of relatively high prices in 1995, during which prices peaked at US$755 per metric tonne, the industry has experienced two further full pricing cycles. Over the twelve-month period from June 2001 to June 2002, newsprint prices declined approximately 28%, from US$625 to US$450 per metric tonne. In July 2002, newsprint producers announced a US$50 per metric tonne price increase, which was partially implemented in October 2002, and we expect that prices will continue to increase in the near term. Newsprint expense represented 18.2% ($117.2 million) of our total operating expenses (before depreciation, amortization and restructuring charges) for the year ended December 31, 2000, 19.7% ($125.7 million) for the year ended December 31, 2001 and 16.4% ($103.8 million) for the year ended December 31, 2002. As a result, volatile or increased newsprint costs have had, and may in the future have, a material adverse effect on our financial condition and operating results.

We have entered into a long-term agreement expiring December 31, 2005 with a newsprint manufacturer for the supply of most of our newsprint purchases. Our supply of newsprint may be threatened if this newsprint manufacturer is unable to supply us with sufficient newsprint to meet our needs. Our inability to obtain sufficient newsprint on acceptable terms when needed could materially increase our costs or disrupt our operations.

We operate in a highly competitive industry.

Revenue generation in the newspaper industry depends primarily on the sale of advertising and paid circulation. Competition for newspaper advertising is largely based on readership, circulation, demographic composition of the market, price and content of the newspaper. Competition for circulation is largely based on price, editorial content, quality of delivery service and availability of publications. Competition for advertising and circulation revenue comes from local, regional and national newspapers, radio, broadcast and cable television, direct mail and other communications and advertising media that operate in our markets. In recent years, competition with online services and other new media technologies has also increased significantly. In addition, consolidation in the Canadian broadcasting, publishing and other media industries has increased significantly, and our competitors include market participants with interests in multiple industries and media. We cannot assure you that our existing and future competitors will not pursue or be capable of achieving business strategies similar or competitive to ours. Some of our competitors have greater financial and other resources than we do. We may not be able to compete successfully in the future against existing or

8

potential competitors, and increased competition may have a material adverse effect on our business, financial condition or operating results.

Two of our publications represent a significant portion of our revenue.

Le Journal de Montréal andThe Toronto Sun have historically represented a significant portion of our revenue, and we expect that they will continue to do so for the foreseeable future.Le Journal de Montréal accounted for approximately 19% of our revenue in each of the years ended December 31, 2001 and 2002. Similarly,The Toronto Sun accounted for approximately 17% of our revenue for the year ended December 31, 2001 and 16% of our revenue for the year ended December 31, 2002. During the same periods, we derived approximately 20% of our advertising revenue fromLe Journal de Montréal, andThe Toronto Sun accounted for approximately 17% of our advertising revenue during the year ended December 31, 2001 and 16% of our advertising revenue during the year ended December 31, 2002. A significant decline in the performance ofLe Journal de Montréal orThe Toronto Sun or in general advertising spending in the markets they serve could cause our revenue to decrease dramatically, which could have a material adverse effect on our business, financial condition and operating results.

We may be adversely affected by strikes and other labor protests.

Approximately one-third of our employees are unionized. We are currently a party to 46 collective bargaining agreements. Seven of these collective bargaining agreements (representing approximately 229 employees) will expire on or before December 31, 2003. An additional 30 of these collective bargaining agreements (representing approximately 1,006 employees) will expire on or before December 31, 2006. Currently, there are nine collective bargaining agreements (representing approximately 361 employees) that have expired and are being negotiated for renewal. On January 27, 2003, approximately 160 employees in the editorial department ofThe Toronto Sun voted to certify a union. We expect to begin negotiating a collective bargaining agreement with these employees in 2003.

We cannot predict the outcome of any future negotiations relating to union representation or collective bargaining agreements. Pending the outcome of future negotiations, we may experience work stoppages, strikes or other forms of labor protests. Any strikes or other forms of labor protest could disrupt our operations and have a material adverse effect on our business, financial condition or operating results. Even if we do not experience strikes or other forms of labor protests, the outcome of labor negotiations could impair our operating results.

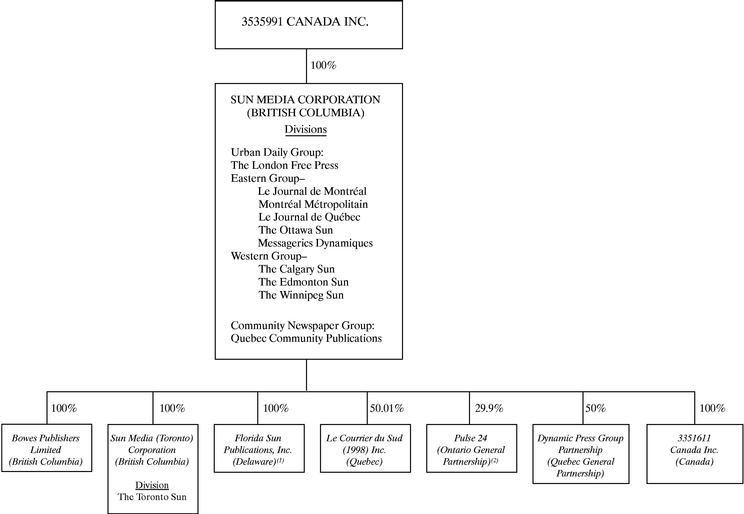

We are controlled by Quebecor Media.

All of our issued and outstanding common shares are held by 3535991 Canada Inc., a wholly owned subsidiary of Quebecor Media. As a result, Quebecor Media controls our policies and operations. The interests of Quebecor Media, as our sole equity holder, may conflict with the interests of the holders of the notes.

In addition, Quebecor Media has entered into certain transactions with us to consolidate tax losses within the Quebecor Media group. As a result of these transactions, we recognize significant income tax benefits. Quebecor Media may unwind these transactions at any time in its discretion, eliminating our ability to reduce our income tax obligations. See "Item 5. Operating and Financial Review and Prospects—Liquidity and Capital Resources—Purchase of Shares of Quebecor Media and Service of Convertible Obligations."

Also, Quebecor Media is a holding company with no significant assets other than its equity interests in its subsidiaries. Its principal source of cash needed to pay its own obligations is the cash that its subsidiaries generate from their operations and borrowings. We expect, to the extent permitted by the terms of our indebtedness and applicable law, to continue to pay significant dividends to

9

Quebecor Media in the future. See "Item 5. Operating and Financial Review and Prospects—Liquidity and Capital Resources—Payment of Dividends."

We may not successfully implement our business and operating strategies.

Our business and operating strategies include increasing our advertising and circulation revenues, expanding our complementary products and services, reducing our costs, achieving efficiencies through geographic clustering and further integrating our newspaper operations with the Quebecor Media group of companies. We may not be able to implement these strategies fully or realize their anticipated results. Implementation of these strategies could also be affected by a number of factors beyond our control, such as operating difficulties, increased operating costs, regulatory developments, general or local economic conditions or increased competition. Any material failure to implement our strategies could have a material adverse effect on our business, financial condition and operating results and on our ability to meet our obligations, including our ability to service our indebtedness.

We depend on key personnel.

Our success depends to a large extent upon the continued services of our senior management and our ability to retain skilled employees. There is intense competition for qualified management and skilled employees, and our failure to recruit, retain and train such employees could have a material adverse effect on our business, financial condition or operating results.

We are subject to extensive environmental regulations.

Substantially all of our facilities are subject to federal, provincial, state and municipal laws concerning, among other things, emissions to the air, water and sewer discharges, handling and disposal of hazardous materials, wastes, recycling, or otherwise relating to protection of the environment. Environmental laws and regulations and their interpretation have changed rapidly in recent years and may continue to do so in the future. Our properties, as well as areas surrounding such properties, particularly those in areas of long-term industrial use, may have had historic uses, including uses related to historic publishing operations, or may have current uses (in the case of surrounding properties) that may affect our properties and require further study or remedial measures. We are not currently planning any material study or remedial measure, and none has been required by regulatory authorities. However, we cannot assure you that all environmental liabilities have been determined, that any prior owner of our properties did not create a material environmental condition not known to us, or that a material environmental condition does not exist at any of our properties.

We may be adversely affected by fluctuations of the exchange rate.

Virtually all of our revenues and expenses, other than interest expense on U.S. dollar-denominated debt, are denominated in Canadian dollars. Except for our new revolving credit facility of $75.0 million, all our indebtedness is denominated, and interest, principal and any premium on our indebtedness will have to be paid, in U.S. dollars. As a result, we will be exposed to foreign currency exchange risk. We entered into transactions to hedge the exchange rate risk with respect to our U.S. dollar-denominated debt. However, these hedging transactions may not be successful due to any number of reasons, including the default of counterparties to these hedging transactions, and the resulting foreign exchange rate fluctuations may impair our ability to make payments in respect of our existing indebtedness. In addition, we may be required to provide cash or other collateral to secure our obligations with respect to any such hedging transactions. See "Item 5. Operating and Financial Review and Prospects—Quantitative and Qualitative Disclosures about Market Risk."

For the purposes of financial reporting, any change in the value of the Canadian dollar against the U.S. dollar during a given financial reporting period would result in a foreign exchange gain or loss on the translation of any U.S. dollar-denominated debt into Canadian dollars. Consequently, our reported earnings and debt could fluctuate materially as a result of foreign exchange gains or losses.

10

Item 4. Information on the Company

History and Development of the Company

Our legal and commercial name is Sun Media Corporation. Our principal executive office is located at 333 King Street East, Toronto, Ontario, Canada M5A 3X5, and our telephone number is (416) 947-2222. Our registered office is located at 800 Park Place, 666 Burrard Street, Vancouver, British Columbia, Canada V6C 3P3. Our agent for service of process in the United States is CT Corporation System, 111 Eighth Avenue, New York, NY 10011.

We are a corporation resulting from the amalgamation under theCanada Business Corporations Act on February 28, 1999 of 2944707 Canada Inc., which was incorporated on August 11, 1993, and Sun Media Corporation, or old Sun Media, which was continued from Ontario into the federal jurisdiction on February 12, 1999. We received certification and were continued from the federal jurisdiction into the jurisdiction of the province of British Columbia on July 3, 2001.

We are an indirect, wholly owned subsidiary of Quebecor Media. We conduct our business operations primarily through our divisions and through Bowes Publishers Limited and Sun Media (Toronto) Corporation, which are our two significant subsidiaries. We hold 100% of the outstanding shares of both Bowes Publishers Limited and Sun Media (Toronto) Corporation, and these subsidiaries are both British Columbia companies.

On February 7, 2003, we issued US$205.0 million in aggregate principal amount of 75/8% Senior Notes due 2013 and entered into a new credit facility that provides for a new term loan of US$230.0 million and a revolving facility of $75.0 million. The 75/8% Senior Notes due 2013 are unsecured and have a maturity date of February 15, 2013. Interest is payable semi-annually in arrears on February 15 and August 15 of each year, beginning on August 15, 2003. The net proceeds from the sale of the notes and the new credit facility were used to pay down in full all Sun Media loans and to pay a $260.0 million dividend to our parent company, Quebecor Media, of which $150.0 million will be used to reduce the long term debt of our affiliate Vidéotron. See "Item 5. Operating and Financial Review and Prospects — Subsequent Events."

Business Overview

We are the largest newspaper publisher in Québec and the second largest newspaper publisher in Canada, with a 21.0% market share in terms of weekly paid circulation, according to statistics published by the Canadian Newspaper Association. We publish 15 paid daily newspapers and serve eight of the top eleven urban markets in Canada. Each of our eight urban daily newspapers ranks either first or second in its market in terms of paid circulation. We also publish 175 weekly newspapers and shopping guides and 18 other specialty publications, including a free daily commuter newspaper. We publish the second and third largest non-national dailies in Canada based on weekly paid circulation:Le Journal de Montréal, with a paid circulation of 1.9 million copies, andThe Toronto Sun, with a paid circulation of 1.5 million copies. The combined weekly paid circulation of our daily newspapers is approximately 6.8 million copies.

In addition, we provide a range of commercial printing and other related services to third parties through our national network of production and printing facilities and distribute newspapers and magazines for other publishers across Canada.

For the year ended December 31, 2002, we generated revenues of $853.6 million and EBITDA of $222.3 million. For this same period, 68.4% of our revenues were derived from advertising, 19.7% from circulation and 11.9% from commercial printing and distribution operations.

11

Our Strategy

We aim to increase profitability and cash flow by pursuing the following business and operating strategies:

- •

- Increase advertising revenue. We plan to continue to diversify our advertising offerings to attract advertisers, and further target national and multi-market accounts with large spending budgets. We continue to integrate our urban and community newspapers to offer advertisers packages bundled by market instead of by publication. In connection with this integration, we are establishing centralized classified advertisement call centers to expand existing advertising business, as well as solicit new business. We also continue to expand our sales force and provide it with training programs to enhance its effectiveness. We are upgrading our software to enable our advertisement takers to upsell and increase yield per advertisement. In addition, we plan to expand our use of value-based pricing and marketing strategies, such as charging premiums for preferred positions in our publications, to maximize advertising revenue.

- •

- Increase circulation revenue. We plan to increase paid circulation of our newspapers by increasing the number of newspaper boxes and point-of-sale locations, as well as expanding home delivery service. We are further cultivating relationships with retail outlets to sell our newspapers. In addition, to increase readership, we continue to expand coverage of local news in our newspapers to differentiate their content from national publications and broaden their appeal and to target content for identified groups through the introduction of niche products, such asAt Homemagazine,Amateur Sports andVotre Argent. We also continue to invest in technology to enhance the effectiveness of our delivery and distribution operations.

- •

- Expand complementary products and services. We plan to launch new products and services and capitalize on our existing assets to further increase our revenues. We will continue to leverage our newspaper brands by developing new specialty and niche products, such as targeted supplements, special interest pullouts and coupon books. We plan to continue to develop and roll out our new media services, which include complementary advertising vehicles, such as online classified and display advertisements, banner advertisements, virtual shopping malls and on-line auctions. In addition, by deploying additional sales and marketing resources, we intend to market more aggressively excess capacity in our existing printing facilities. We also plan to expand our distribution network, which currently has a potential reach of over nine million Canadian households, and more aggressively promote our distribution services to existing and new customers. We believe these initiatives will expand our revenue base, diversify our revenue streams and reduce our dependence on the advertising market.

- •

- Reduce costs. We have expanded our implementation of "best practices" policies and benchmarking standards, including specific guidelines for staffing levels and employee productivity, throughout our operations. We also continue to seek lower cost alternatives for raw materials, equipment and services, and additional means to improve production efficiency, such as the reduction and standardization of paper sizes. In addition, we intend to control more rigorously the distribution of copies of our free newspapers by evaluating the needs of our advertising customers and improving the efficiency of our delivery operations. Finally, we seek to reduce costs and improve productivity by intensifying our employee training programs and investing in new technologies, such as computer-to-plate technology which streamlines the production process.

- •

- Achieve efficiencies through geographic clustering. The majority of our community newspapers are geographically clustered around our eight urban dailies. We continue to concentrate our ownership of publications into regional clusters in order to realize operating efficiencies, such as the consolidation and sharing of production, printing and distribution functions, as well as management and administration costs. In addition, we believe that our clustering strategy

12

Canadian Newspaper Publishing Industry Overview

Newspaper publishing is the oldest and largest segment of the advertising-based media industry in Canada. The industry is dominated by a small number of major newspaper publishers, of which we are the second largest with a combined weekly circulation (paid and unpaid) of more than ten million copies.

The newspaper market consists primarily of two segments, broadsheet and tabloid newspapers, which vary in format. With the exception of the broadsheetThe London Free Press, all of our urban paid daily newspapers are tabloids.

Newspaper companies derive revenue principally from advertising and circulation. According to industry sources, in 2001, the total Canadian daily newspaper industry revenue was $3.2 billion, with 79% derived from advertising and the remaining 21% coming from circulation. Total advertising revenue for the Canadian daily newspaper industry was $2.5 billion in 2001, which represented 23.7% of total Canadian advertising spending. Including revenues from non-daily newspapers, advertising revenues for the newspaper industry as a whole in 2001 were estimated to be approximately $3.3 billion, representing a 31% share of total Canadian advertising spending. From 1995 to 2000, advertising revenues for daily newspapers increased at an average annual rate of 6.3%. In 2001, as a result of a weakening economy and the events of September 11, daily newspaper advertising revenues declined by 3.1% compared to 2000. Zenith Media estimates that newspaper advertising revenues have remained flat in 2002. Total Canadian daily newspaper circulation revenue decreased by 1.5% to $682 million in 2001 despite a marginal increase in circulation volume.

Circulation revenues are derived from single copy newspaper sales made through retailers and vending boxes and home delivery newspaper sales to subscribers.

Advertising revenues and, to a lesser extent, circulation revenues are cyclical and are generally affected by changes in national and regional economic conditions. Recent statistics indicate that economic growth in Canada increased in 2002 relative to 2001. In addition, recent forecasts by the Bank of Canada project that Canadian Real Gross Domestic Product will grow at an average annual rate of 3.5% in 2002 and 2003. The improvement in the Canadian economy is expected to result in increased advertising expenditures. Zenith Media forecasts that newspaper advertising revenues in Canada will grow at a compound annual rate of 2.5% between 2002 and 2004.

Our Newspaper Operations

We operate our newspaper businesses in urban and community markets. A majority of our newspapers in the Community Newspaper Group are clustered around our eight urban dailies in the Urban Daily Group. We have strategically established our community newspapers near our regional printing facilities in suburban and rural markets across Canada and in Florida. This geographic

13

clustering enables us to realize operating efficiencies and economic synergies through sharing of management, accounting and human resources as well as production and printing functions.

The Urban Daily Group

On a combined weekly basis, the eight paid daily newspapers in our Urban Daily Group circulate approximately 6.4 million copies. These newspapers hold either the number one or number two position in each of their respective markets in terms of circulation. In addition, on a combined basis, over 50% of our readers do not read our principal competitor's newspaper in each of our urban daily markets, according to data from the NADbank® 2002 Study.

With the exception of the broadsheetThe London Free Press, the paid daily newspapers are morning tabloids published seven days a week. These are mass circulation newspapers that provide succinct and complete news coverage with an emphasis on local news, sports and entertainment. The tabloid format makes extensive use of color, photographs and graphics. Each newspaper contains inserts that feature subjects of interest such as fashion, lifestyle and special sections. During 2002, the Urban Daily Group launched a quarterly publication with a circulation of 500,000 copies to be distributed to its subscribers across Canada. In 2002, the Urban Daily Group also launched a free weekly newspaper in London, and it currently publishes a free Monday to Friday commuter newspaper in Montréal and two free weekly shopping guides. In addition, the Urban Daily Group includes the distribution businesses operated through Messageries Dynamiques and Dynamic Press Group.

Our Newspapers

Circulation is defined as average sales of a newspaper per issue. Readership (as opposed to paid circulation) is an estimate of the number of people who read or looked into an average issue of a newspaper and is measured by a continuous independent survey conducted by NADbank Inc. According to the NADbank® 2002 Study, the estimates of readership are based upon the number of people responding to the Newspaper Audience Databank survey circulated by NADbank Inc. who report having read or looked into one or more issues of a given newspaper during a given period equal to the publication interval of the newspaper.

The following chart lists our paid daily newspapers and their respective readership in 2002, as well as their market position by paid circulation during that period:

| | 2002 Average Readership

| |

|

|---|

Newspaper

| | Market Position by Paid Circulation(1)

|

|---|

| | Saturday

| | Sunday

| | Mon-Fri

|

|---|

| Le Journal de Montréal | | 706,600 | | 454,800 | | 660,300 | | 1 |

| Le Journal de Québec | | 225,600 | | 151,500 | | 194,500 | | 1 |

| The Ottawa Sun | | 109,200 | | 93,800 | | 128,400 | | 2 |

| The Toronto Sun | | 699,300 | | 1,018,900 | | 896,900 | | 2 |

| The London Free Press | | 173,600 | | 95,900 | | 162,600 | | 1 |

| The Winnipeg Sun | | 116,300 | | 121,200 | | 138,400 | | 2 |

| The Edmonton Sun | | 160,000 | | 193,900 | | 183,800 | | 2 |

| The Calgary Sun | | 166,400 | | 213,000 | | 221,700 | | 2 |

| | |

| |

| |

| | |

| | Total Average Readership | | 2,357,000 | | 2,343,000 | | 2,586,600 | | |

| | |

| |

| |

| | |

- (1)

- Based on paid circulation data published by the Audit Bureau of Circulations with respect to non-national newspapers in each market.

Le Journal de Montréal. Le Journal de Montréal is published seven days a week and is widely distributed by Messageries Dynamiques, which specializes in the distribution of publications. According

14

to the Audit Bureau of Circulations,Le Journal de Montréal ranks second in paid circulation, afterThe Toronto Star, among non-national Canadian dailies and first among French-language dailies in North America. The average daily circulation ofLe Journal de Montréal exceeds the circulation of each of its main competitors in Montréal,La Presse,The Gazette andLe Devoir, according to the Audit Bureau of Circulations.

The following chart reflects the average daily circulation ofLe Journal de Montréal for the periods indicated:

| | Year Ended December 31,

|

|---|

| | 2000

| | 2001

| | 2002

|

|---|

| Le Journal de Montréal | | | | | | |

| Saturday | | 321,400 | | 316,400 | | 314,700 |

| Sunday | | 275,000 | | 267,800 | | 264,800 |

| Monday to Friday | | 259,600 | | 260,900 | | 262,800 |

On March 12, 2001, we launchedMontréal Métropolitain, a free daily newspaper with an average weekday circulation of 60,000 copies, according to internal statistics. The editorial content ofMontréal Métropolitain concentrates on Montréal and Québec City news and competes withMetro, another free paper launched recently in Montréal.

Le Journal de Québec. Le Journal de Québec is published seven days a week and is widely distributed by Messageries Dynamiques.Le Journal de Québec is the number one newspaper in its market. The average daily circulation ofLe Journal de Québec exceeds the circulation of its main competitor,Le Soleil, according to the Audit Bureau of Circulations.

The following chart reflects the average daily paid circulation ofLe Journal de Québec for the periods indicated:

| | Year Ended December 31,

|

|---|

| | 2000

| | 2001

| | 2002

|

|---|

| Le Journal de Québec | | | | | | |

| Saturday | | 123,999 | | 121,700 | | 123,200 |

| Sunday | | 99,225 | | 98,600 | | 100,700 |

| Monday to Friday | | 96,127 | | 96,200 | | 98,500 |

The Ottawa Sun. The Ottawa Sun is published seven days a week and is distributed throughout the Ottawa region through its own distribution network.The Ottawa Sun is the number two newspaper in its market, according to the Audit Bureau of Circulations, and competes daily with the English language broadsheet,The Ottawa Citizen, and also with the French language paper,Le Droit.

The following chart reflects the average daily paid circulation of theOttawa Sun for the periods indicated:

| | Year Ended December 31,

|

|---|

| | 2000

| | 2001

| | 2002

|

|---|

| The Ottawa Sun | | | | | | |

| Saturday | | 45,800 | | 45,200 | | 41,000 |

| Sunday | | 54,200 | | 52,900 | | 49,200 |

| Monday to Friday | | 49,600 | | 49,600 | | 44,600 |

15

The Ottawa Sun also publishes theOttawa Pennysaver, a free weekly community shopping guide with circulation of approximately 186,000.

The Toronto Sun. The Toronto Sun is published seven days a week and has its own distribution network to serve the greater metropolitan Toronto area.The Toronto Sun is the third largest non-national daily newspaper in Canada in terms of circulation, according to the Audit Bureau of Circulations.

The Toronto Sun is unique in that Monday to Friday all circulation sales are from vending boxes and retail outlets. Home delivery is available on Sunday and in some designated areas on Saturday.

The Toronto newspaper market is very competitive.The Toronto Sun competes with Canada's largest newspaper,The Toronto Star and to a lesser extent withThe Globe & Mail andThe National Post. As a tabloid newspaper,The Toronto Sun has a unique format compared to these broadsheet competitors. The competitiveness of the Toronto newspaper market is further increased by several free publications, includingMetro Today, a free weekday commuter newspaper, and new niche publications relating to, for example, entertainment and television.

The following chart reflects the average daily circulation ofThe Toronto Sun for the periods indicated:

| | Year Ended December 31,

|

|---|

| | 2000

| | 2001

| | 2002

|

|---|

| The Toronto Sun | | | | | | |

| Saturday | | 173,000 | | 169,700 | | 169,300 |

| Sunday | | 384,900 | | 367,800 | | 350,700 |

| Monday to Friday | | 225,400 | | 215,300 | | 203,500 |

The London Free Press. The London Free Press, one of Canada's oldest daily newspapers, emphasizes national and local news, sports and entertainment and is distributed throughout the London area through its own network. It is the only local daily newspaper in its market.

In 1998, we revised the editorial content of the paper to provide greater coverage of local and regional issues. In April 1998,The London Free Press began publishing its first Sunday edition and now publishes seven days a week. During 2002,The London Free Press also completed the installation of two used Goss Headliner offset presses to replace its letterpress technology. The installation of these presses significantly improved print quality and increased page, color and insert capacity of the newspaper.

The following chart reflects the average daily circulation ofThe London Free Press for the periods indicated:

| | Year Ended December 31,

|

|---|

| | 2000

| | 2001

| | 2002

|

|---|

| The London Free Press | | | | | | |

| Saturday | | 121,400 | | 116,000 | | 112,200 |

| Sunday | | 64,800 | | 62,700 | | 61,700 |

| Monday to Friday | | 97,800 | | 93,900 | | 90,800 |

During 2002,The London Free Press launchedLondon This Week, a free weekly community newspaper with a circulation of approximately 104,000 copies. TheLondon Free Press also publishes theLondon Pennysaver, a free weekly community shopping guide with circulation of approximately 152,000.

16

The Winnipeg Sun. The Winnipeg Sun is published seven days a week. It serves the metropolitan Winnipeg area and has its own distribution network.The Winnipeg Sun operates as the number two newspaper in the Winnipeg market according to the Audit Bureau of Circulations and competes with theWinnipeg Free Press.

The following chart reflects the average daily circulation ofThe Winnipeg Sun for the periods indicated:

| | Year Ended December 31,

|

|---|

| | 2000

| | 2001

| | 2002

|

|---|

| The Winnipeg Sun | | | | | | |

| Saturday | | 44,600 | | 44,400 | | 45,100 |

| Sunday | | 58,800 | | 58,100 | | 56,400 |

| Monday to Friday | | 45,700 | | 45,900 | | 45,400 |

The Edmonton Sun. The Edmonton Sun is published seven days a week and is distributed throughout Edmonton through its own distribution network.The Edmonton Sun is the number two newspaper in its market, according to the Audit Bureau of Circulations, and competes with Edmonton's broadsheet daily,The Edmonton Journal.

The following chart reflects the average daily circulation ofThe Edmonton Sun for the periods indicated:

| | Year Ended December 31,

|

|---|

| | 2000

| | 2001

| | 2002

|

|---|

| The Edmonton Sun | | | | | | |

| Saturday | | 74,100 | | 72,700 | | 71,600 |

| Sunday | | 109,000 | | 104,700 | | 102,000 |

| Monday to Friday | | 72,300 | | 73,800 | | 72,200 |

The Calgary Sun. The Calgary Sun is published seven days a week and is distributed throughout Calgary through its own distribution network.The Calgary Sun is the number two newspaper in its market, according to the Audit Bureau of Circulations and competes with Calgary's broadsheet daily,The Calgary Herald.

The following chart reflects the average daily circulation ofTheCalgary Sun for the periods indicated:

| | Year Ended December 31,

|

|---|

| | 2000

| | 2001

| | 2002

|

|---|

| The Calgary Sun | | | | | | |

| Saturday | | 69,300 | | 67,200 | | 65,100 |

| Sunday | | 100,200 | | 98,400 | | 97,500 |

| Monday to Friday | | 68,800 | | 67,500 | | 65,300 |

Advertising and Circulation

Advertising revenue is the largest source of revenue for the Urban Daily Group. Advertising rates are based upon the size of the market in which each newspaper operates, circulation, readership, demographic composition of the market and the availability of alternative advertising media. Our strategy is to maximize advertising revenue by providing advertisers with a range of pricing and marketing alternatives to better enable them to reach their target audience. Our newspapers offer a

17

variety of advertising alternatives, including full-run advertisements in regular sections of the newspaper targeted to different readers (including food, real estate and travel); geographically-targeted inserts; special-interest pullout sections and advertising supplements.

Our principal categories of advertising revenues are classified, retail and national advertising. Classified advertising has traditionally accounted for the largest share of our advertising revenues in our urban daily newspapers (44.4% in the year ended December 31, 2002) followed by retail advertising (35.6% in the same period) and national advertising (17.5% in the same period). Classified advertising is made up of four principal sectors: automobiles, private party, recruitment and real estate. Automobile advertising is the largest classified advertising category, representing about 45.7% of all of our classified advertising in terms of revenue for the year ended December 31, 2002. Retail advertising is display advertising principally placed by local businesses and organizations. Our retail advertisers are principally department stores, electronics stores and furniture stores. National advertising is display advertising primarily from advertisers promoting products or services on a national basis. Our national advertisers are principally in the automotive sector. During 1999, we implemented an advertising initiative to maximize national and multi-market advertising sales by our publications. As a result of the initiative, our newspaper network has attracted major customers in several sectors of the Canadian economy, including the automobile, financial services, microcomputers and telecommunications industries.

We believe our advertising revenues are diversified not only by category (classified, retail and national), but also by customer and geography. For the year ended December 31, 2002, our top ten advertisers accounted for approximately 7% of the total advertising revenue and approximately 5% of overall revenue. In addition, because we sell advertising in numerous regional markets in Canada, the impact on us of a decline in any one market can be offset by strength in the others.

Circulation sales are the second-largest source of revenue for the Urban Daily Group. The Urban Daily Group's newspapers are available through newspaper boxes and retail outlets Monday through Sunday. We offer daily home delivery in every market except Toronto, whereThe Toronto Sun is home-delivered only on Sunday and in certain designated areas on Saturday. We derive our circulation revenues from single copy sales and subscription sales. Our strategy is to increase circulation revenue by adding newspaper boxes and point-of-sale locations, as well as expanding home delivery. In addition, to increase readership, we are expanding coverage of local news in our newspapers and targeting editorial content to identified groups through the introduction of niche products, such asAt Home magazine,Amateur Sports andVotre Argent.

Competition

The Canadian newspaper industry is mature and dominated by a small number of major publishers. According to the Canadian Newspaper Association, our 21.0% market share of paid weekly newspaper circulation is exceeded only by CanWest Media Inc., with a 30.1% market share, and followed by Torstar Corporation (13.8%), Power Corporation (9.2%), Bell Globemedia (6.4%) and Osprey Media (4.7%). In addition to competing directly with other dailies published in their respective markets, each of our newspapers in the Urban Daily Group competes for advertising revenue with weekly newspapers, magazines, direct marketing, radio, television and other advertising media. Competition for newspaper advertising is largely based upon readership, circulation, demographic composition of the market, price and content of the newspaper. Competition for circulation is largely based on price, editorial content, quality of delivery service and availability of publications. The high cost associated with starting a major daily newspaper operation represents a barrier to entry to potential new competitors of our Urban Daily Group.

ThroughLe Journal de Montréal andLe Journal de Québec, we have established market leading positions in Québec's two main urban markets, Montréal and Québec City.Le Journal de Montréal

18

ranks second in circulation among non-national Canadian dailies and is first among French-language dailies in North America.

The London Free Press is one of Canada's oldest daily newspapers and our only daily broadsheet newspaper.The London Free Press is the only local daily newspaper in its market.

The Toronto Sun is the third-largest non-national daily newspaper in Canada in terms of circulation. The Toronto newspaper market is very competitive.The Toronto Sun competes withThe Toronto Star and to a lesser extent withThe Globe & Mail andThe National Post. As a tabloid newspaper,The Toronto Sun offers readers and advertisers an alternative format to the broadsheet format of other newspapers in the Toronto market.

Each of our dailies in Edmonton, Calgary, Winnipeg and Ottawa competes against a broadsheet newspaper and has established a number two position in its market.

The Community Newspaper Group

In total, the Community Newspaper Group consists of seven daily community newspapers, 172 community weekly newspapers and shopping guides, and 16 farming and other specialty publications. We also own three additional community weekly newspapers and shopping guides and two specialty publications that are included in the Urban Daily Group. The Community Newspaper Group also distributes coupons, product samples and other direct mail promotional material through NetMedia, its distribution sales arm.

The total average weekly circulation of the publications in our Community Newspaper Group for the year ended December 31, 2002 was approximately 3.0 million free copies and approximately 548,200 paid copies. The table below sets forth the average daily paid circulation and geographic location of the daily newspapers published by the Community Newspaper Group in 2002:

Newspaper

| | Location

| | Average Daily Paid Circulation

|

|---|

| The Brockville Recorder and Times | | Brockville, Ontario | | 13,100 |

| Stratford Beacon Herald | | Stratford, Ontario | | 11,300 |

| The Daily Herald Tribune | | Grande Prairie, Alberta | | 9,200 |

| St. Thomas Time-Journal | | St. Thomas, Ontario | | 8,400 |

| Fort McMurray Today | | Fort McMurray, Alberta | | 7,100 |

| The Daily Miner & News | | Kenora, Ontario | | 4,600 |

| The Daily Graphic | | Portage La Prairie, Manitoba | | 3,600 |

| | | | |

|

| | Total Average Daily Paid Circulation | | 57,300 |

| | | | |

|

19

The weekly and specialty publications of the Community Newspaper Group are distributed throughout Canada and in Florida. The number of weekly publications on a regional basis is as follows:

Province or State

| | Number of Publications

|

|---|

| Alberta | | 44 |

| British Columbia | | 6 |

| Florida | | 8 |

| Manitoba | | 12 |

| Ontario | | 39 |

| New Brunswick | | 1 |

| Québec | | 56 |

| Saskatchewan | | 6 |

| | |

|

| | Total Publications | | 172 |

| | |

|

Our community newspaper publications generally offer news, sports and special features, with an emphasis on local information. These newspapers cultivate reader loyalty and create franchise value by emphasizing local news, thereby differentiating themselves from national newspapers. We also distribute coupons, flyers, product samples and other direct mail promotional material through NetMedia, the distribution sales arm of the Community Newspaper Group. Through its branch system and its associated distributors, NetMedia currently has the potential to provide advertising customers with distribution to over nine million Canadian households.