UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08549

Oak Associates Funds

(Exact name of registrant as specified in charter)

3875 Embassy Parkway, Suite 250

Akron, Ohio 44333

(Address of principal executive offices) (Zip code)

Charles A. Kiraly

3875 Embassy Parkway, Suite 250

Akron, Ohio 44333

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-888-462-5386

Date of fiscal year end: October 31

Date of reporting period: October 31, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| Oak Investment Philosophy |

Oak Associates, ltd., advisor to the Oak Associates Funds, has been managing concentrated, low-turnover portfolios for over 30 years. We appreciate the many long-term shareholders who invest alongside us in the Oak Associates Funds. Oak Associates employees, as well as their friends and families, maintain significant investments in the Funds. As fellow shareholders, we have a vested interest in ensuring that the highest standards are maintained and that the portfolios are positioned for future growth. Here is our approach to investing. | |

| Long-term focus To us, the appeal of an investment is driven by the long-term fundamentals of the company and its opportunity set, rather than short-term trading factors. We believe that this long-term mindset is increasingly valuable in today’s short-term oriented market. |

| Concentrated portfolios We construct our portfolios with our best ideas, which means that our favorite stock ideas aren’t diluted by investments in less-favored positions. Academic studies have shown that managers gave up performance because they failed to concentrate in their best ideas. Concentration takes discipline, conviction and experience. We continue to adhere to a strategy of concentrated portfolios. |

| Low turnover When we invest in a company, we do so with the intention of holding that stock for several years, not a few quarters. Low turnover can have the effect of minimizing trading costs as well as tempering the natural human instinct to act upon every data point. |

| Independent thinking Being a good investor often requires not doing what the rest of the market is doing. While it’s difficult to go against the crowd – because as humans we are physiologically wired to herd – we believe that long-term outperformance requires it. One benefit of being located in Akron, Ohio (aside from being a great place to live), is that we are removed from the financial centers in other areas of the country, minimizing our chances of being swept up by the herd mentality. We value independent thinking and believe it is beneficial to our investment perspective. |

| The value of a Fund’s investments will vary from day to day in response to the activities of individual companies and general market and economic conditions. Due to a limited number of underlying investments, funds that invest a signification portion of their assets in particular industry sectors or concentrated funds that focus on a particular industry or group of industries are more susceptible to the price movements of any one holding or industry and thus are generally more volatile than a portfolio invested in a wider variety of industries or industry sectors. |

Shareholder Letter

November 30, 2017

Dear Fellow Shareholder:

U.S. economic growth accelerated in 2017, as employment strengthened and the economies of our foreign trade partners improved. Long-awaited progress on wages also materialized, especially at the low end of the wage scale. For years we have heard about increasing income inequality and the need to do something to fix it. It remains a complex issue that has not been fully resolved, but it is interesting that, as it so often does, the free market has started to bring things back into balance on its own.

With no economic recession since 2009 and none in sight, stocks continued their ascent. This economic cycle has been slower moving than ones in the past. Some reasons for this include persistently low inflation, conservative behavior by company managements, and responsible lending practices by banks. While these factors have kept a lid on economic growth, they have also prevented a recession and the correction in stocks that usually accompanies it.

Robust corporate profitability continues to confound many, as margins stay high. This has allowed earnings to compound at a nice pace and for companies to return capital to shareholders in the form of dividends and share buybacks. While most focus on the dividend yields of stocks, we feel the growth in the dividends themselves has been an overlooked story of this bull market. Over the last seven years, S&P 500 dividends per share have grown at a compound annual rate of 11.7%. This translates to more than a doubling in nominal dividends over that period.

Stocks are likely also being helped by a more favorable regulatory environment and prospects for tax reform. As we write this, legislators are working towards an agreement that would lower the corporate tax rate, though it may not pass into law until 2018. Through a high tax rate on companies and a policy that, unlike in other countries, taxes profits earned abroad, the US corporate tax system has put American businesses at a competitive disadvantage for years. Changes to both of these issues are on the table.

The change in market leadership has been notable. For most of 2016 the stocks of lowly valued companies (“value”) outperformed, but almost perfectly in sync with the calendar turning to 2017 conditions changed abruptly, as shares of companies that are growing revenue and earnings at a fast pace (“growth”) started to lead the market. The Russell 3000 is a broad market index with companies of all sizes. Through mid-November, the growth portion of this index was up 23.5% in 2017, while the value portion was up only 5.6%; that is a massive gap. At times, it seems like the market is being dominated by a few huge companies, such as Facebook, Apple, Amazon, Netflix, and Alphabet (Google). We do own some of these stocks, but in general our portfolios don’t perform as well on a relative basis when the market is being led by growth. Over the long-term we expect our approach of investing in attractively-priced stocks to help our performance, as growth on average underperforms over the long-run – though in recent years this has not been the case.

Despite the recent outperformance of growth versus value, our long-term relative returns remain strong. Focusing primarily on our three largest Funds: over the last ten years, White Oak has returned 117% cumulatively, versus 106% for the S&P 500 and 112% for the Lipper Large-Cap Growth Funds Average. Pin Oak has returned 153%, versus 108% for the Russell 3000 and 84% for the Lipper Multi-Cap Core Funds Average. Red Oak has returned 217%, versus 149% for the Lipper Science & Technology Funds Average. Of course these include the painful correction of 2008/2009. The numbers for our Funds and the market since the correction are significantly better, and we implore our shareholders to understand that future returns are very unlikely to be as good. Market valuations are on the high end of the historic range and company profit margins are high. Both of these have created nice tailwinds for stocks in recent years, but their (we are speaking of valuations and margins) upside appears limited from here. That doesn’t mean stocks are a poor long-term

Shareholder Letter

investment – they still offer superior value to bonds and should offer positive returns over the long-term – but we believe it is important to keep expectations in check. We expect stock returns over the next ten years to be well below historical averages.

During the year we completed a successful transition to a new fund administrator, Ultimus Fund Solutions. These folks do all of the back-office work for our mutual funds so that we can focus primarily on the investing part. Our decision to change administrators was done for a variety of reasons and was part of a broader effort to provide high quality service at a reasonable cost to our shareholders. These efforts, along with strong growth in assets during the year, have helped reduce the expense ratios of our Funds, which translates into more money in your pocket.

August marked the 25-year anniversary of the Oak Associates Funds. The Funds were launched because we wanted all investors – not just institutions and high-net-worth individuals – to have the opportunity to invest with Oak. Today our seven mutual funds total more than $1 billion, and we sincerely thank you for helping us build this fund family into what it is today. We feel fortunate to be able to manage your money.

Best regards,

Mark Oelschlager, CFA

Co-Chief Investment Officer and Portfolio Manager

Co-Chief Investment Officer and Portfolio Manager

All investing involves risk. The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Visit www.oakfunds.com/Funds/Performance.aspx for standardized performance, including performance data current to the most recent month-end. The commentary above and later where it appears in this report, is for informational purposes only and does not represent an offer, recommendation or solicitation to buy, hold or sell any security. The specific securities identified and described do not represent all of the securities purchased or sold and you should not assume that investments in the securities identified and discussed will be profitable.

HIGHLIGHTS from the 2017 FISCAL YEAR

October 31, 2016 to October 31, 2017 (Unaudited)

| January 2017 | In “The Journal Report,” The Wall Street Journal recognized White Oak Select Growth, Red Oak Technology Select, Rock Oak Core Growth, and Live Oak Health Sciences among the top 10 best-performing in their Lipper categories based on total returns for 1-year ended 12/31/16. January 9, 2017. In the January 9 Barron’s “Lipper Mutual Fund Quarterly” section, Red Oak Technology Select was the top-performing Science & Technology fund in the fourth quarter of 2016, according to Lipper. Zacks Investment Research highlighted Live Oak Health Sciences among the best-performing healthcare funds of 2016 (“5 Best Performing Healthcare Mutual Funds of 2016”). January 23, 2017. |

| March 2017 | In the annual funds review in the March issue of Kiplinger’s Personal Finance, Pin Oak Equity appeared ranked among top 10 performing large company stock funds for the three-, five- and 10-year periods ended December 31, 2016, according to Morningstar. Pin Oak Equity Fund was highlighted by Mutual Fund Observer, an independent, online publication that analyzes mutual funds – with a special focus on innovative, independent, lesser-known funds. March 2017 edition. Mark Oelschlager commented in a USA Today story on the outlook for the healthcare sector (“Health Care Stocks Regain Footing Amid Fight Over Law: Group is second best in S&P 500 performance in 2017,” p. B1, by Adam Shell). March 21, 2017. Lipper Fund Awards 2017: Lipper recognized Red Oak Technology Select for its Consistently Strong Risk-Adjusted Performance for 10 years as of 11/30/2016 among 104 Science and Technology Funds at the Lipper Awards Ceremony on March 23, 2017. The March 27 issue of Citywire Professional Buyer, a bi-weekly magazine targeted to fund analysts and manager researchers, noted Red Oak Technology Select among top-performing technology funds for the three years through February 28, 2017. Pin Oak Equity and Red Oak Technology Select were included among Investor’s Business Daily’s 2017 “IBD Best Mutual Funds,” a supplement in the March 27 edition. IBD profiled Pin Oak Equity Fund as part of this supplement (“Contrarian Pin Oak Equity Rises to the Top” by Scott Lehtonen). March 27, 2017. Money Management Executive named Pin Oak manager Mark Oelschlager among top ten fund managers to watch. March 27, 2017. |

HIGHLIGHTS from the 2017 FISCAL YEAR

October 31, 2016 to October 31, 2017 (Unaudited)

| April 2017 | Investopedia highlighted Red Oak Technology Select among “top technology mutual fund picks for 2017” (“Top 4 Technology Mutual Funds for 2017,” by Sheila Olson). April 14, 2017. |

| June 2017 | Red Oak Technology Select was featured in MarketWatch’s article, “Google’s stock is still ‘compelling,’ says outperforming tech fund manager.” June 29, 2017 by Philip Van Doorn. |

| August 2017 | An August 22 Investopedia posting included Red Oak Technology Select among four top technology funds for 2017 (“Top 4 Technology Mutual Funds for 2017,” by Sheila Olson). |

| October 2017 | Red Oak Technology Select was named by The Wall Street Journal among best-performing stock funds for the ten-year period ended September 29. October 9, 2017. |

READ MORE AT WWW.OAKFUNDS.COM

TABLE of CONTENTS

| Performance Update | |

| White Oak Select Growth Fund | 2 |

| Pin Oak Equity Fund | 4 |

| Rock Oak Core Growth Fund | 6 |

| River Oak Discovery Fund | 8 |

| Red Oak Technology Select Fund | 10 |

| Black Oak Emerging Technology Fund | 12 |

| Live Oak Health Sciences Fund | 14 |

| Important Disclosures | 16 |

| Disclosure of Fund Expenses | 19 |

| Financial Statements | |

| Schedules of Investments | 20 |

| Statements of Assets and Liabilities | 40 |

| Statements of Operations | 42 |

| Statements of Changes in Net Asset | 44 |

| Financial Highlights | 48 |

| Notes to Financial Statements | 52 |

| Report of Independent Registered Public Accounting Firm | 63 |

| Additional Information | 64 |

White Oak Select Growth Fund

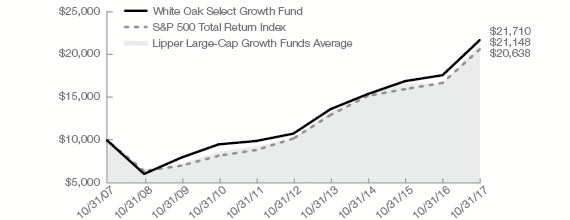

James D. Oelschlager Co-Chief Investment Officer & Portfolio Manager  Mark W. Oelschlager, CFA Co-Chief Investment Officer & Portfolio Manager  Robert D. Stimpson, CFA Portfolio Manager | White Oak Select Growth Fund (the “Fund”) gained 23.36% for the fiscal year ended October 31, 2017, while the S&P 500® Total Return Index returned 23.63% and the Lipper Large-Cap Growth Funds Average returned 27.29%. For the last ten years, the Fund’s cumulative return was 117.10%, versus 106.38% for the S&P 500® and 111.79% for the Lipper. Near the start of the fiscal year the Federal Reserve followed through with its multi-year admonitions that short-term interest rates would rise with signs of economic stability in the U.S. With the S&P 500® charging to new all-time highs, unemployment at a 10-year low, and high levels of both profits and margins, it was no surprise that the Fed raised rates. The hikes started in December of 2016 with a 25 basis points increase, followed by several additional quarter point rate hikes until the target rate reached 1.25%. Despite the start of the normalization in rates, U.S. stocks climbed strongly over the year. One segment that enjoyed the prospects of higher short-term interest rates and the prospects of a slower economic expansion was large-cap growth stocks. Companies that can demonstrate sales or earnings growth as economic conditions tighten are often assigned higher valuations. Higher rates also hampered higher yielding equity-based investment strategies, with utilities, dividend payers and REITS among the largest underperformers in the year. As a result, financials, a large weighting for the Fund, continued to perform well as higher rates boost net interest margins and earnings power. Technology stocks, another large weighting in the Fund, are also characterized for their growth qualities. Within the Fund, the best-performing holding was KLA-Tencor. The company, which makes process control equipment for semiconductor manufacturing, rose 48% as strength within the technology sector and emerging markets boosted sales. JP Morgan was the second best-performing holding, also gaining 48%, on broad strength across its businesses, improved credit quality and on the prospects of a more favorable regulatory environment. Teva Pharmaceuticals was the worst-performing stock in the Fund. Health care, in general, struggled, due to uncertainty over the current administration’s attempts to repeal and replace Obamacare, as well as vilification of drug companies over pricing. Poor results over the year prompted Teva to cut its dividend, an event that is rarely received well. Looking into 2018, we believe the potential for tax relief and a lower regulatory burden all bode well for corporate profits going forward. President Trump’s proclivity for more protectionist trade policies remains an issue to monitor. Overall, interest rates remain low and corporations continue to demonstrate fiscal restraint that tends to benefit shareholders. Thank you for your investment with Oak Associates Funds. |

Mutual fund investing involves risk, including the possible loss of principal. The value of the Fund’s investments will vary from day to day in response to the activities of individual companies and general market and economic conditions. Because the Fund may invest a significant portion of its assets in particular industry sectors which it believes hold the most potential for favorable returns, poor performance or adverse economic events affecting one or more of these overweighted sectors could have a greater impact on the Fund than it would on another mutual fund with a broader range of investments.

| 2 | 1-888-462-5386 | www.oakfunds.com |

Manager Discussion & Analysis

All data below as of October 31, 2017 (Unaudited)

| Fund Data | |

| Ticker | WOGSX |

| Share Price | $82.36 |

| Total Net Assets | $285.7 M |

| Portfolio Turnover | 12.92% |

| Sector Allocation^ | |

| Information Technology | 41.4% |

| Financials | 32.1% |

| Health Care | 11.8% |

| Consumer Discrectionary | 8.3% |

| Industrials | 3.7% |

| Consumer Staples | 2.0% |

| Energy | 0.2% |

| Cash & Other Assets | 0.5% |

| Top 10 Holdings^ | ||

| 1. | Alphabet, Inc. | 10.7% |

| 2. | Amazon.com, Inc. | 8.3% |

| 3. | Charles Schwab Corp. | 7.4% |

| 4. | KLA-Tencor Corp. | 6.9% |

| 5. | Cisco Systems, Inc. | 6.8% |

| 6. | Amgen, Inc. | 6.6% |

| 7. | Xilinx, Inc. | 5.1% |

| 8. | U.S. Bancorp | 5.0% |

| 9. | JPMorgan Chase & Co. | 4.6% |

| 10. | United Parcel Service, Inc., Class B | 3.7% |

^ Percentages are based on net assets. Holdings are subject to change.

Growth of $10,000 Chart

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). This chart and the table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| Average Annual Total Return | ||||

| 1 Year Return | 3 Year Return | 5 Year Return | 10 Year Return | |

| White Oak Select Growth Fund | 23.36% | 12.14% | 15.07% | 8.06% |

S&P 500® Total Return Index1 | 23.63% | 10.77% | 15.18% | 7.51% |

Lipper Large-Cap Growth Funds Average2 | 27.29% | 11.21% | 15.56% | 7.71% |

Gross/Net Expense Ratio (per the prospectus): 1.06%

Gross/Net Expense Ratio (as of fiscal year end October 31, 2017): 0.98%

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, please visit www.oakfunds.com or call 1-888-462-5386.

1 | Standard & Poor’s is the source and owner of the S&P Index data. 2 Lipper Inc. is the source and owner of the Lipper Classification data. See Pages 16 and 17 for additional disclosure. |

| Annual Report | October 31, 2017 | 3 |

Pin Oak Equity Fund

Mark W. Oelschlager, CFA

Co-Chief Investment Officer

Co-Chief Investment Officer

& Portfolio Manager

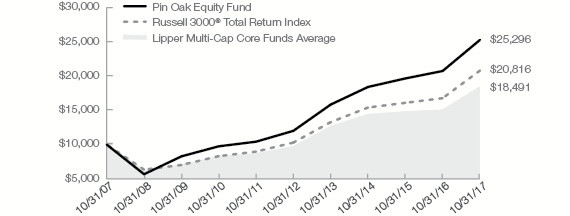

Pin Oak Equity Fund (the “Fund”) gained 21.86% for the fiscal year ended October 31, 2017, while the Russell 3000® Total Return Index returned 23.98% and the Lipper Multi-Cap Core Funds Average returned 21.97%. For the last ten years, a period that includes one of the worst financial crises in U.S. history, the Fund’s cumulative return was 152.96%, versus 108.16% for the Russell and 84.06% for the Lipper. This was the ninth consecutive fiscal year of positive returns for the Fund, a streak sure to end at some point. When Donald Trump was elected President of the United States in November 2016, it accelerated the upward move in interest rates as well as the rise in financial stocks, both of which were already underway before the election. This also continued the trend in the outperformance of the “value” stocks, or those considered inexpensive on various metrics. All of this helped the Fund outperform in late 2016. But 2017 has been a different story as more growth-oriented factors drew the attention of investors, propelling shares of “growth” companies higher. Pin Oak has some exposure to some of these companies, such as Alphabet (Google) and Amazon, but in general our investing style avoids the faster growers because of their higher embedded expectations and below-average return history. The unfavorable style bias offset the Fund’s strong sector positioning for the year. Our two largest sector weightings, by far, were financials and technology, which also happened to be the two best-performing sectors in the market for the past twelve months. |

As risks in the market have grown, our positioning has become incrementally more defensive, meaning recent purchases have been in areas with more stability. We have had a large exposure to the financial sector for years, and still do, but as the bank stocks have gone from extremely attractive to just attractive, we have trimmed the exposure there. We believe this is prudent risk management.

Leaders during the year included Internet conglomerate IAC/Interactive, whose shares doubled on strong results from online dating business Match and home services operation HomeAdvisor; financial services company Charles Schwab, which benefitted from rising interest rates; and multinational industrial giant Parker Hannifin, who reported accelerating sales growth and rising profit margins.

Laggards included land drilling contractor Nabors, who saw demand for its services slow; advertising company Interpublic Group, whose customers are increasingly turning to alternative channels; and pharmaceutical behemoth GlaxoSmithKline, which faced increasing competition in its respiratory franchise.

Thank you for your investment with Oak Associates Funds.

Mutual fund investing involves risk, including the possible loss of principal. The value of the Fund’s investments will vary from day to day in response to the activities of individual companies and general market and economic conditions. Because the Fund may invest a significant portion of its assets in particular industry sectors which it believes hold the most potential for favorable returns, poor performance or adverse economic events affecting one or more of these overweighted sectors could have a greater impact on the Fund than it would on another mutual fund with a broader range of investments.

| 4 | 1-888-462-5386 | www.oakfunds.com |

Manager Discussion & Analysis

All data below as of October 31, 2017 (Unaudited)

| Fund Data | |

| Ticker | POGSX |

| Share Price | $63.72 |

| Total Net Assets | $222.1 M |

| Portfolio Turnover | 7.55% |

| Sector Allocation^ | |

| Financials | 32.5% |

| Information Technology | 32.0% |

| Consumer Discrectionary | 10.8% |

| Health Care | 8.1% |

| Consumer Staples | 4.4% |

| Energy | 4.2% |

| Industrials | 1.4% |

| Materials | 0.7% |

| Cash & Other Assets | 5.9% |

| Top 10 Holdings^ | ||

| 1. | Alphabet, Inc. | 7.1% |

| 2. | Bank of New York Mellon | 5.6% |

| 3. | Charles Schwab Corp. | 5.0% |

| 4. | Paychex, Inc. | 4.5% |

| 5. | PepsiCo, Inc. | 4.4% |

| 6. | GlaxoSmithKline PLC ADR | 3.7% |

| 7. | Valero Energy Corp. | 3.6% |

| 8. | Travelers Cos., Inc. | 3.6% |

| 9. | IAC/InterActiveCorp | 3.6% |

| 10. | Amdocs Ltd. | 3.5% |

| ^ | Percentages are based on net assets. Holdings are subject to change. |

Growth of $10,000 Chart

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). This chart and the table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| Average Annual Total Return | ||||

| 1 Year Return | 3 Year Return | 5 Year Return | 10 Year Return | |

| Pin Oak Equity Fund | 21.86% | 11.15% | 16.06% | 9.72% |

Russell 3000® Total Return Index1 | 23.98% | 10.53% | 15.12% | 7.61% |

Lipper Multi-Cap Core Funds Average2 | 21.97% | 8.29% | 13.51% | 6.18% |

Gross/Net Expense Ratio (per the prospectus): 1.08%

Gross/Net Expense Ratio (as of fiscal year end October 31, 2017): 0.98%

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, please visit www.oakfunds.com or call 1-888-462-5386.

1 | Russell Investments is the source and owner of the Russell Index data. 2 Lipper Inc. is the source and owner of the Lipper Classification data. See Pages 16 and 17 for additional disclosure. |

| Annual Report | October 31, 2017 | 5 |

Rock Oak Core Growth Fund

Robert D. Stimpson, CFA

Portfolio Manager

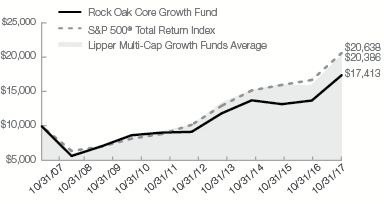

Rock Oak Core Growth Fund (the “Fund”) gained 27.02% for the fiscal year ended October 31, 2017, while the S&P 500® Total Return Index returned 23.63% and the Lipper Multi-Cap Growth Funds Average returned 27.44%. Over the last five years, the Fund has gained 13.70% per year on average. The fiscal year 2017 saw U.S. stocks climb higher on optimism over less regulation, tax reform and continued economic expansion. Despite President Trump’s inability to repeal and replace Obamacare as of this writing, optimism is high that Congress can implement tax reform. While the benefits to the economy or consumers are still uncertain, lower corporate tax rates and the repatriation of overseas capital could reward equity shareholders. The Federal Reserve had been prepping the investor community regarding its intentions to raise the Fed Funds rate for a very long time. Therefore, the December 2016 liftoff surprised no one and failed to thwart U.S. stocks’ advance. However, the likelihood of a higher interest rate environment and slower economic expansion did disproportionately benefit the large-cap growth segment of the market. Companies that demonstrate the ability to grow sales or earnings in a slowing economy often obtain a premium valuation as economic prospects narrow. This cycle was no exception. |

The Fund’s best-performing stock was Wyndham Worldwide, which rose 66%. The global hotel company has benefited from strength not only in the U.S. market, but also from the international market. Western Digital was the Fund’s second best performer. The hard disk drive maker climbed 56%.

The Fund’s largest laggard was media company Discovery Communications, which fell 27%. The outlook for the media industry remains clouded by new online competitors, changing demographics, and internet-based distribution models.

Going forward, Rock Oak remains focused on companies with strong earnings prospects that have also demonstrated a commitment to creating shareholder value. The outlook for U.S. stocks remains attractive in our view due to the low inflation, a stable growth environment and prudent financial management which supports company fundamentals.

Thank you for your investment with Oak Associates Funds.

Mutual fund investing involves risk, including the possible loss of principal. The value of the Fund’s investments will vary from day to day in response to the activities of individual companies and general market and economic conditions. Because the Fund may invest a significant portion of its assets in particular industry sectors which it believes hold the most potential for favorable returns, poor performance or adverse economic events affecting one or more of these overweighted sectors could have a greater impact on the Fund than it would on another mutual fund with a broader range of investments.

| 6 | 1-888-462-5386 | www.oakfunds.com |

Manager Discussion & Analysis

All data below as of October 31, 2017 (Unaudited)

| Fund Data | |

| Ticker | RCKSX |

| Share Price | $16.07 |

| Total Net Assets | $9.2 M |

| Portfolio Turnover | 29.49% |

| Sector Allocation^ | |

| Information Technology | 45.9% |

| Health Care | 17.2% |

| Consumer Discrectionary | 16.1% |

| Financials | 12.2% |

| Industrials | 5.8% |

| Consumer Staples | 2.0% |

| Cash & Other Assets | 0.8% |

| Top 10 Holdings^ | ||

| 1. | Amazon.com, Inc. | 5.7% |

| 2. | DXC Technology Co. | 5.6% |

| 3. | AbbVie, Inc. | 4.9% |

| 4. | SunTrust Banks, Inc. | 4.7% |

| 5. | Netflix, Inc. | 4.4% |

| 6. | L3 Technologies, Inc. | 4.4% |

| 7. | Western Digital Corp. | 4.3% |

| 8. | NetApp, Inc. | 4.2% |

| 9. | Hartford Financial Services Group, Inc. | 4.2% |

| 10. | Wyndham Worldwide Corp. | 4.0% |

| ^ | Percentages are based on net assets. Holdings are subject to change. |

Growth of $10,000 Chart

|

This chart represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). This chart and the table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Fee waivers are in effect; if they had not been in effect, performance would have been lower.

| Average Annual Total Return | ||||

| 1 Year Return | 3 Year Return | 5 Year Return | 10 Year Return | |

| Rock Oak Core Growth Fund | 27.02% | 8.22% | 13.70% | 5.70% |

S&P 500® Total Return Index1 | 23.63% | 10.77% | 15.18% | 7.51% |

Lipper Multi-Cap Growth Funds Average2 | 27.44% | 10.03% | 14.81% | 7.23% |

Gross/Net Expense Ratio (per the prospectus): 1.65%/1.25%

Gross/Net Expense Ratio (as of fiscal year end October 31, 2017): 1.51%/1.25%

The Adviser has contractually agreed through February 28, 2018, to waive all or a portion of its fee for the Fund (and to reimburse expenses to the extent necessary) in order to limit Fund total operating expenses (excluding interest, taxes, brokerage commissions, Acquired Fund Fees and Expenses) to an annual rate of not more than 1.25% of average daily net assets. This contractual fee waiver may only be terminated subject to approval by the Board of Trustees of the Trust.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, please visit www.oakfunds.com or call 1-888-462-5386.

1 | Standard & Poor’s is the source and owner of the S&P Index data. 2 Lipper Inc. is the source and owner of the Lipper Classification data. See Pages 16 and 17 for additional disclosure. |

| Annual Report | October 31, 2017 | 7 |

River Oak Discovery Fund

Robert D. Stimpson, CFA

Portfolio Manager

River Oak Discovery Fund (the “Fund”) gained 22.59% for the fiscal year ended October 31, 2017, while the Russell 2000® Growth Total Return Index returned 31.00% and the Lipper Small-Cap Growth Funds Average returned 29.16%. Over the last five years, the Fund has gained 12.31% per year on average. U.S. stocks rallied strongly in the first part of the fiscal year following the election of President Trump. Prospects for lower regulation and tax relief underscored the initial reaction by U.S. equities. Following the “Trump bump,” small-cap stocks traded sideways for much of 2017, then rallied in the beginning of the fourth quarter. The real beneficiaries within the U.S. market were large-cap stocks, particularly those characterized as growth companies. With the Federal Reserve finally following through on its rhetoric to raise interest rates, the likelihood of a slower economic expansion has caused companies that can demonstrate sales or earnings growth in a tighter monetary environment to receive a premium valuation from investors. |

A combination of low inflation and stable growth has also created an environment favorable to equity investments. Yet, for well over a year now, the Federal Reserve has been preparing investors for higher interest rates and finally began raising rates in December of 2016. Three additional interest rate hikes followed, but failed to thwart U.S. equities. Given the improvements in the stock market and low unemployment rate, which has fallen to a 10-year low of 4.1% as of October 2017, additional rate increases are likely as the Fed seeks to normalize rates and rearm its tool kit.

The Fund’s strongest performer this fiscal year was Kadant Inc., gaining 122%. The recycled paper and fluid management company beat earnings estimates several times during the year. Mercer International, a pulp and paper making company, was the Fund’s second best-performing holding, rising 93%. Both companies began the fiscal year at attractive valuations and may have benefited from the possibility of favorable protectionist policies under the new administration.

The Fund’s worst-performing stock was Endo International, a specialty pharmaceutical company, which lost 66%. Despite its inexpensive valuation, the company is challenged by falling sales, pricing uncertainty and high levels of debts. The position was sold due to its deteriorating financial solvency.

Looking into 2018, investors continue to show a preference for large-cap and growth stocks. We believe this is a distraction, however, which makes what we see as opportunities easier to identify among interesting small-cap stocks. A strong stock market helps boost investor sentiment and generally reduces risk aversion that typically hurts the appetite for the segment. The Fund is committed to seeking out niche companies with a strong commitment to creation of shareholder value.

Thank you for your investment with Oak Associates Funds.

Mutual fund investing involves risk, including the possible loss of principal. The value of the Fund’s investments will vary from day to day in response to the activities of individual companies and general market and economic conditions. Because the Fund may invest a significant portion of its assets in particular industry sectors which it believes hold the most potential for favorable returns, poor performance or adverse economic events affecting one or more of these overweighted sectors could have a greater impact on the Fund than it would on another mutual fund with a broader range of investments.

| 8 | 1-888-462-5386 | www.oakfunds.com |

Manager Discussion & Analysis

All data below as of October 31, 2017 (Unaudited)

| Fund Data | |

| Ticker | RIVSX |

| Share Price | $17.42 |

| Total Net Assets | $14.4 M |

| Portfolio Turnover | 43.50% |

| Sector Allocation^ | |

| Information Technology | 35.7% |

| Financials | 19.2% |

| Health Care | 12.9% |

| Consumer Discrectionary | 12.3% |

| Industrials | 11.3% |

| Materials | 4.4% |

| Consumer Staples | 3.2% |

| Cash & Other Assets | 1.0% |

| Top 10 Holdings^ | ||

| 1. | SolarEdge Technologies, Inc. | 5.9% |

| 2. | Kadant, Inc. | 5.5% |

| 3. | Advanced Energy Industries, Inc. | 5.4% |

| 4. | Assurant, Inc. | 4.4% |

| 5. | Mercer International, Inc. | 4.4% |

| 6. | Fortinet, Inc. | 4.1% |

| 7. | Cirrus Logic, Inc. | 4.1% |

| 8. | Kulicke & Soffa Industries, Inc. | 4.0% |

| 9. | Magellan Health, Inc. | 3.8% |

| 10. | Zions BanCorp | 3.5% |

^ Percentages are based on net assets. Holdings are subject to change.

Growth of $10,000 Chart

|

The chart represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). This chart and the table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Fee waivers are in effect; if they had not been in effect, performance would have been lower.

| Average Annual Total Return | ||||

| 1 Year Return | 3 Year Return | 5 Year Return | 10 Year Return | |

| River Oak Discovery Fund | 22.59% | 7.76% | 12.31% | 5.44% |

Russell 2000® Growth Total Return Index1 | 31.00% | 10.51% | 15.36% | 8.16% |

Lipper Small-Cap Growth Funds Average2 | 29.16% | 9.47% | 13.72% | 7.21% |

Gross/Net Expense Ratio (per the prospectus): 1.51%/1.35%

Gross/Net Expense Ratio (as of fiscal year end October 31, 2017): 1.41% /1.35%

The Adviser has contractually agreed through February 28, 2018, to waive all or a portion of its fee for the Fund (and to reimburse expenses to the extent necessary) in order to limit Fund total operating expenses (excluding interest, taxes, brokerage commissions, Acquired Fund Fees and Expenses) to an annual rate of not more than 1.35% of average daily net assets. This contractual fee waiver may only be terminated subject to approval by the Board of Trustees of the Trust.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, please visit www.oakfunds.com or call 1-888-462-5386.

1 | Russell Investments is the source and owner of the Russell Index data. 2 Lipper Inc. is the source and owner of the Lipper Classification data. See Pages 16 and 17 for additional disclosure. |

| Annual Report | October 31, 2017 | 9 |

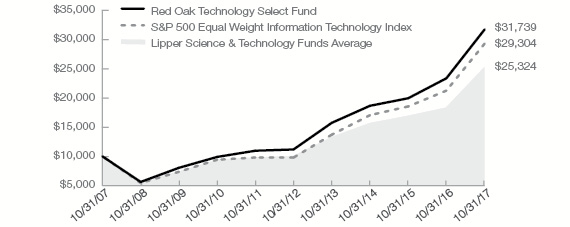

Red Oak Technology Select Fund

Mark W. Oelschlager, CFA

Co-Chief Investment Officer

Co-Chief Investment Officer

& Portfolio Manager

Red Oak Technology Select Fund (the “Fund”) gained 35.76% for the fiscal year ended October 31, 2017, while the S&P 500 Equal Weight Information Technology Index returned 37.82% and the Lipper Science & Technology Funds Average returned 37.47%. For the last ten years, the Fund’s cumulative return was 217.39%, versus 193.04% for the Index and 148.95% for the Lipper. The 10-year returns demonstrate a wide performance gap between the Fund and its peers. We attribute this to our focus on valuation and earnings sustainability, two factors that are sometimes overlooked in tech investing. The value of a company is the sum of its future profits. Therefore it is important to gauge how durable a company’s business is, especially in a sector like technology where things change so often. This is why we feel it is dangerous to base investment decisions on hot stories, one-year growth rates, and the like. |

Technology was the best-performing sector for the fiscal year, after being second in the previous year and second the year before that. There are 11 market sectors, so this performance by tech stocks the last three years is remarkable. Whether one is talking about the sector, the Fund, or tech fund averages, we believe these returns are unlikely to be duplicated in the coming years.

We have talked for years about how technology companies have been prime beneficiaries of the outsourcing trend, as many have moved to an “asset-light” business model by paying foreign entities to do what the companies can’t do as efficiently. This has driven profit margins and returns on capital higher. For years the market was reluctant to give them credit for this, meaning it was pricing the stocks as if the higher profitability would eventually reverse or be competed away. The reversal hasn’t come, and investors have gradually bought into the idea that the elevated profitability might be somewhat sustainable and pushed valuations higher. The stocks have also been aided recently by hopes for tax reform in the U.S.

The portfolio’s hit rate was high this past year, as more than 3/4 of all positions held for the full twelve months returned more than 25%, including mega-caps Amazon, Alphabet (Google), Facebook, Apple, and Intel. Two stocks whose returns exceeded 100% were semiconductor company NVIDIA, which rose almost 200% on accelerating revenue growth, and Internet conglomerate IAC/Interactive, which saw strength in its online dating segment and home service operation.

Laggards included Qualcomm, which is involved in legal disputes with various entities over the pricing of its CDMA licensing; Juniper Networks, due to struggles in the competitive market for networking equipment; and IT services company IBM, who is trying to manage a transition to cloud-based services.

Thank you for your investment with Oak Associates Funds.

Mutual fund investing involves risk, including the possible loss of principal. The value of the Fund’s investments will vary from day to day in response to the activities of individual companies and general market and economic conditions. Because the Fund may invest a significant portion of its assets in particular industry sectors which it believes hold the most potential for favorable returns, poor performance or adverse economic events affecting one or more of these overweighted sectors could have a greater impact on the Fund than it would on another mutual fund with a broader range of investments.

| 10 | 1-888-462-5386 | www.oakfunds.com |

Manager Discussion & Analysis

All data below as of October 31, 2017 (Unaudited)

| Fund Data | |

| Ticker | ROGSX |

| Share Price | $25.78 |

| Total Net Assets | $486.3 M |

| Portfolio Turnover | 14.63% |

| Sector Allocation^ | |

| Information Technology | 91.2% |

| Consumer Discrectionary | 3.5% |

| Industrials | 1.9% |

| Cash & Other Assets | 3.4% |

| Top 10 Holdings^ | ||

| 1. | Alphabet, Inc. | 9.0% |

| 2. | Intel Corp. | 4.9% |

| 3. | Microsoft Corp. | 4.8% |

| 4. | Facebook, Inc., Class A | 4.8% |

| 5. | Cisco Systems, Inc. | 4.1% |

| 6. | Oracle Corp. | 3.9% |

| 7. | Red Hat, Inc. | 3.8% |

| 8. | Apple, Inc. | 3.8% |

| 9. | Synopsys, Inc. | 3.6% |

| 10. | Amazon.com, Inc. | 3.5% |

| ^ | Percentages are based on net assets. Holdings are subject to change. |

Growth of $10,000 Chart

The chart represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). This chart and the table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| Average Annual Total Return | ||||

| 1 Year Return | 3 Year Return | 5 Year Return | 10 Year Return | |

| Red Oak Technology Select Fund | 35.76% | 19.35% | 23.19% | 12.24% |

S&P 500 Equal Weight Information Technology Index1 | 37.82% | 19.74% | 24.50% | 11.35% |

Lipper Science & Technology Funds Average2 | 37.47% | 16.98% | 19.86% | 9.34% |

Gross/Net Expense Ratio (per the prospectus): 1.09%

Gross/Net Expense Ratio (as of fiscal year end October 31, 2017): 0.97%

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, please visit www.oakfunds.com or call 1-888-462-5386.

1 | Standard & Poor’s is the source and owner of the S&P Index data. 2 Lipper Inc. is the source and owner of the Lipper Classification data. See Pages 16 and 17 for additional disclosure. |

| Annual Report | October 31, 2017 | 11 |

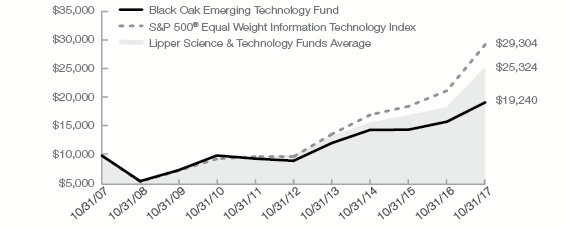

Black Oak Emerging Technology Fund

Robert D. Stimpson, CFA

Portfolio Manager

Black Oak Emerging Technology Fund (the “Fund”) gained 21.16% during the fiscal year ended October 31, 2017, while the S&P 500® Equal Weight Information Technology Index returned 37.82% and the Lipper Science & Technology Funds Average returned 37.47%. Over the last five years, the Fund has gained 16.20% per year on average. |

In general, stocks have enjoyed the low-inflation, slow growth environment and thrived despite the prospects of higher short-term interest rates. The path to normalized rates is still uncertain, but given the longstanding promotion from the Fed, the stock market has demonstrated a level of comfort with the plan and continues rallying higher despite the 1% increase in the Fed Funds rate to 1.25%.

The domestic U.S. economy also continues to charge forward. Nationwide the unemployment rate has recently fallen to 4.1% as of October 2017, a 10-year low. Congress is set to embark on tax reform and despite their failure to successfully repeal and replace Obamacare, prospects are high that some simplification to the tax code is likely. President Trump’s protectionist position on trade remains a concern and will be something to monitor going forward.

The Fund’s top-performing stock for the year was IXYS Corporation, which rose 133%. The company develops power semiconductor chips and was acquired by electronic component company Littelfuse in March 2017. Semiconductor processing equipment maker Lam Research was the Fund’s second best–performing holding, gaining 118% over the fiscal year.

The Fund’s worst-performing stock was Xperi, an audio technology company, which lost 35%. The company was sold during the year after net income turned negative due to higher operating expenses.

Going forward, the Fund will continue to seek opportunities within technology companies exposed to emerging niches, with solid earnings prospects, which are trading at favorable valuations.

Thank you for your investment with Oak Associates Funds.

Mutual fund investing involves risk, including the possible loss of principal. The value of the Fund’s investments will vary from day to day in response to the activities of individual companies and general market and economic conditions. Because the Fund may invest a significant portion of its assets in particular industry sectors which it believes hold the most potential for favorable returns, poor performance or adverse economic events affecting one or more of these overweighted sectors could have a greater impact on the Fund than it would on another mutual fund with a broader range of investments.

| 12 | 1-888-462-5386 | www.oakfunds.com |

Manager Discussion & Analysis

All data below as of October 31, 2017 (Unaudited)

| Fund Data | |

| Ticker | BOGSX |

| Share Price | $5.28 |

| Total Net Assets | $37.3 M |

| Portfolio Turnover | 39.38% |

| Sector Allocation^ | |

| Information Technology | 94.2% |

| Health Care | 5.2% |

| Cash & Other Assets | 0.6% |

| Top 10 Holdings^ | ||

| 1. | Apple, Inc. | 6.4% |

| 2. | Baidu, Inc. ADR | 5.3% |

| 3. | Lam Research Corp. | 5.2% |

| 4. | DXC Technology Co. | 4.9% |

| 5. | CA, Inc. | 4.6% |

| 6. | IXYS Corp. | 4.2% |

| 7. | Silicon Motion Technology Corp. ADR | 4.0% |

| 8. | Cirrus Logic, Inc. | 4.0% |

| 9. | Facebook, Inc., Class A | 3.9% |

| 10. | Tencent Holdings Ltd. ADR | 3.7% |

^ Percentages are based on net assets. Holdings are subject to change.

Growth of $10,000 Chart

The chart represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). This chart and the table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Fee waivers are in effect; if they had not been in effect, performance would have been lower.

| Average Annual Total Return | ||||

| 1 Year Return | 3 Year Return | 5 Year Return | 10 Year Return | |

| Black Oak Emerging Technology Fund | 21.16% | 10.00% | 16.20% | 6.76% |

S&P 500® Equal Weight Information Technology Index1 | 37.82% | 19.74% | 24.50% | 11.35% |

Lipper Science & Technology Funds Average2 | 37.47% | 16.98% | 19.86% | 9.34% |

Gross/Net Expense Ratio (per the prospectus): 1.28%

Gross/Net Expense Ratio (as of fiscal year end October 31, 2017): 1.17%

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, please visit www.oakfunds.com or call 1-888-462-5386.

1 | Standard & Poor’s is the source and owner of the S&P Index data. 2 Lipper Inc. is the source and owner of the Lipper Classification data. See Pages 16 and 17 for additional disclosure. |

| Annual Report | October 31, 2017 | 13 |

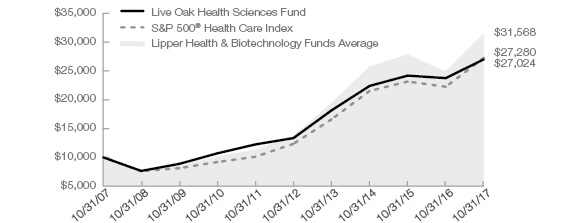

Live Oak Health Sciences Fund

Mark W. Oelschlager, CFA

Co-Chief Investment Officer

Co-Chief Investment Officer

& Portfolio Manager

Live Oak Health Sciences Fund (the “Fund”) gained 13.78% for the fiscal year ended October 31, 2017, while the S&P 500® Health Care Index returned 22.61% and the Lipper Health & Biotechnology Funds Average returned 26.42%. For the last ten years the Fund’s cumulative return was 170.24%, versus 172.80% for the Index and 212.76% for the Lipper. The Department of Justice blocked two large managed care mergers: Anthem-Cigna and Aetna-Humana. Despite this, the stocks have done very well, with Anthem, Cigna, and Aetna returning 74%, 66%, and 60% respectively during the fiscal year. All three were held in the Fund for the full year. The only large insurer that wasn’t involved in the consolidation drama was longtime holding UnitedHealth, which gained 51%. Incredibly, despite the rapid appreciation in the stock prices, these companies still offer investors above-average free cash flow yields. |

While managed care, medical device stocks and several of our other holdings had a strong year, this was a difficult period for the Fund on a relative basis, as in general the winners kept on winning and the losers kept on losing, creating a difficult environment for our style of trying to find overlooked opportunities. Pharmaceutical distributors (e.g. Cardinal Health -8%), pharmacy benefit managers (Express Scripts –9%), and generic pharmaceuticals (Teva Pharmaceutical -67%) held in the portfolio all weighed on returns. These stocks are being affected by concerns about pricing power and in some cases regulatory fears. In our opinion these worries are overblown and the market is pricing in an overly pessimistic scenario. The price-to-earnings (“P/E”) multiples on the distributors and pharmacy benefit manager stocks range from 8 to 12, while the generics are priced even lower. At a time when most companies are trading at a price-to-earnings ratio P/E in the high teens or low 20s, we believe these represent attractive entry points for long-term investors.

Thank you for your investment with Oak Associates Funds.

Mutual fund investing involves risk, including the possible loss of principal. The value of the Fund’s investments will vary from day to day in response to the activities of individual companies and general market and economic conditions. Because the Fund may invest a significant portion of its assets in particular industry sectors which it believes hold the most potential for favorable returns, poor performance or adverse economic events affecting one or more of these overweighted sectors could have a greater impact on the Fund than it would on another mutual fund with a broader range of investments.

| 14 | 1-888-462-5386 | www.oakfunds.com |

Manager Discussion & Analysis

All data below as of October 31, 2017 (Unaudited)

| Fund Data | |

| Ticker | LOGSX |

| Share Price | $19.98 |

| Total Net Assets | $64.7 M |

| Portfolio Turnover | 14.22% |

| Sector Allocation^ | |

| Health Care | 97.0% |

| Cash & Other Assets | 3.0% |

| Top 10 Holdings^ | ||

| 1. | Amgen, Inc. | 7.1% |

| 2. | Anthem, Inc. | 5.6% |

| 3. | Biogen, Inc. | 5.3% |

| 4. | Waters Corp. | 5.1% |

| 5. | C.R. Bard, Inc. | 5.0% |

| 6. | Express Scripts Holding Co. | 4.7% |

| 7. | McKesson Corp. | 4.1% |

| 8. | UnitedHealth Group, Inc. | 4.1% |

| 9. | Charles River Laboratories International, Inc. | 4.1% |

| 10. | Cardinal Health, Inc. | 3.8% |

^ Percentages are based on net assets. Holdings are subject to change.

Growth of $10,000 Chart

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). This chart and the table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| Average Annual Total Return | ||||

| 1 Year Return | 3 Year Return | 5 Year Return | 10 Year Return | |

| Live Oak Health Sciences Fund | 13.78% | 6.45% | 15.16% | 10.45% |

S&P 500® Health Care Index1 | 22.61% | 8.20% | 17.19% | 10.56% |

Lipper Health & Biotechnology Funds Average2 | 26.42% | 6.88% | 17.89% | 11.88% |

Gross/Net Expense Ratio (per the prospectus): 1.11%

Gross/Net Expense Ratio (as of fiscal year end October 31, 2017): 1.02%

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, please visit www.oakfunds.com or call 1-888-462-5386.

1 | Standard & Poor’s is the source and owner of the S&P Index data. 2 Lipper Inc. is the source and owner of the Lipper Classification data. See Pages 16 and 17 for additional disclosure. |

| Annual Report | October 31, 2017 | 15 |

Important Disclosures

As of October 31, 2017 (Unaudited)

Index Definitions and Disclosures

All indices are unmanaged and index performance figures include reinvestment of dividends but do not reflect any fees, expenses or taxes. Investors cannot invest directly in an index.

Lipper, a Thomson Reuters Company, is the source and owner of the Lipper Classification data contained in this material and all trademarks and copyrights related thereto. Any further dissemination or redistribution is strictly prohibited. Lipper Inc. is not responsible for the formatting or configuration of this material or for any inaccuracy in Oak Associates Funds’ presentation thereof.

Lipper Health & Biotechnology Funds – Funds that invest primarily in the equity securities of domestic companies engaged in health care, medicine, and biotechnology.

Lipper Large-Cap Growth Funds – Funds that, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) above Lipper’s USDE large-cap floor. Large-cap growth funds typically have an above-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value, compared to the S&P 500® Index.

Lipper Multi-Cap Core Funds – Funds that, by portfolio practice, invest in a variety of market-capitalization ranges without concentrating 75% of their equity assets in any one market-capitalization range over an extended period of time. Multi-cap core funds typically have average characteristics compared to the S&P SuperComposite 1500 Index.

Lipper Multi-Cap Growth Funds – Funds that, by portfolio practice, invest in a variety of market capitalization ranges without concentrating 75% of their equity assets in any one market capitalization range over an extended period of time. Multi-cap growth funds typically have an above-average price-to-earnings ratio, price-to-book ratio, and three-year sales per-share growth value, compared to the S&P SuperComposite 1500 Index.

Lipper Science & Technology Funds – Funds that invest primarily in the equity securities of domestic companies engaged in science and technology.

Lipper Small-Cap Growth Funds – Funds that, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) below Lipper’s USDE small-cap ceiling. Small-cap growth funds typically have an above-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value, compared to the S&P Small-Cap 600 Index.

NASDAQ is the source and owner of the NASDAQ Index data contained in this material and all trademarks and copyrights related thereto. Any further dissemination or redistribution is strictly prohibited. NASDAQ is not responsible for the formatting or configuration of this material or for any inaccuracy in Oak Associates Funds’ presentation thereof.

Russell Investments is the source and owner of the Russell Index data contained in this material and all trademarks and copyrights related thereto. Any further dissemination or redistribution is strictly prohibited. Russell Investments is not responsible for the formatting or configuration of this material or for any inaccuracy in Oak Associates Funds’ presentation thereof.

Russell 2000® Growth Total Return Index – The Russell 2000® Growth Total Return Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values.

| 16 | 1-888-462-5386 | www.oakfunds.com |

Important Disclosures

All data below as of October 31, 2017 (Unaudited)

Russell 3000® Total Return Index – The Russell 3000® Total Return Index measures the performance of 3,000 publicly held US companies based on total market capitalization, which represents approximately 98% of the investable US equity market.

Standard & Poor’s is the source and owner of the S&P Index data contained in this material and all trademarks and copyrights related thereto. Any further dissemination or redistribution is strictly prohibited. Standard & Poor’s is not responsible for the formatting or configuration of this material or for any inaccuracy in Oak Associates Funds’ presentation thereof.

S&P 500® Index – is a commonly-recognized, market capitalization weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance.

S&P 500® Equal Weight Information Technology Index – The S&P 500® Equal Weight Information Technology Index is an unmanaged equal weighted version of the S&P 500® Information Technology Index that consists of the common stocks of the following industries: internet equipment, computers and peripherals, electronic equipment, office electronics and instruments, semiconductor equipment and products, diversified telecommunication services, and wireless telecommunication services that comprise the Information Technology sector of the S&P 500® Index.

S&P 500® Health Care Index – The S&P 500® Health Care Index is a capitalization-weighted index that encompasses two main industry groups. The first includes companies who manufacture health care equipment and supplies or provide health care related services, including distributors of health care products, providers of basic health care services, and owners and operators of health care facilities and organizations. The second group consists of companies primarily involved in the research, development, production and marketing of pharmaceuticals and biotechnology products.

S&P 500® Total Return Index – The S&P 500® Total Return Index is a commonly recognized, market capitalization weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance.

Investment Definitions

Smart beta defines a set of investment strategies that emphasize the use of alternative index construction rules to traditional market capitalization based indices. Smart beta emphasizes capturing investment factors of market inefficiencies in a rules-based and transparent way.

Correlation is a statistic that measures the degree to which two securities move in relation to each other.

The P/E is the ratio for valuing a company that measures its current share price relative to its per-share earnings. The price-earnings ratio can be calculated as market value per share divided by earnings per share.

The KBW Bank Index is an economic index consisting of the stocks of 24 banking companies. This index serves as a benchmark of the banking sector. This index trades on the Philadelphia Stock Exchange, where it was created.

Book value of an asset is the value at which the asset is carried on a balance sheet and calculated by taking the cost of an asset minus the accumulated depreciation. Book value is also the net asset value of a company, calculated as total assets minus intangible assets and liabilities.

Free cash flow yield is an overall return evaluation ratio of a stock, which standardizes the free cash flow per share a company is expected to earn against its market price per share. The ratio is calculated by taking the free cash flow per share divided by the share price.

| Annual Report | October 31, 2017 | 17 |

Disclosure of Fund Expenses

As of October 31, 2017 (Unaudited)

All mutual funds have operating expenses. As a shareholder of a fund, your investment is affected by these ongoing costs, which include (among others) costs for portfolio management, administrative services, and shareholder reports like this one. It is important for you to understand the impact of these costs on your investment returns.

Operating expenses such as these, are deducted from the Fund’s gross income and directly reduce your final investment return. These expenses are expressed as a percentage of the Fund’s average net assets; this percentage is known as the Fund’s expense ratio.

The following examples use the expense ratio and are intended to help you understand the ongoing costs (in dollars) of investing in your Fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The table on the next page illustrates your Fund’s costs in two ways:

Actual Fund Return. This section helps you to estimate the actual expenses after fee waivers that your Fund incurred over the period. The “Expenses Paid During Period” column shows the actual dollar expense cost incurred by a $1,000 investment in the Fund, and the “Ending Account Value” number is derived from deducting that expense cost from the Fund’s gross investment return.

You can use this information, together with the actual amount you invested in the Fund, to estimate the expenses you paid over that period. Simply divide your actual account value by $1,000 to arrive at a ratio (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply that ratio by the number shown for your Fund under “Expenses Paid During Period”.

Hypothetical 5% Return. This section helps you compare your Fund’s costs with those of other mutual funds. It assumes that the Fund had an annual 5% return before expenses during the year, but that the expense ratio (Column 3) for the period is unchanged. This example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to make this 5% calculation. You can assess your Fund’s comparative cost by comparing the hypothetical result for your Fund in the “Expense Paid During Period” column with those that appear in the same charts in the shareholder reports for other funds.

Note: Because the return is set at 5% for comparison purposes — NOT your Fund’s actual return— the account values shown may not apply to your specific investment.

| 18 | 1-888-462-5386 | www.oakfunds.com |

Disclosure of Fund Expenses

As of October 31, 2017 (Unaudited)

Beginning Account Value May 1, 2017 | Ending Account Value October 31, 2017 | Annualized Expense Ratio | Expenses Paid During Period(a) | |

| White Oak Select Growth Fund | ||||

| Actual Return | $1,000.00 | $ 1,079.10 | 0.96% | $5.05 |

| Hypothetical 5% Return | $1,000.00 | $ 1,020.35 | 0.96% | $4.91 |

| Pin Oak Equity Fund | ||||

| Actual Return | $1,000.00 | $ 1,053.00 | 1.00% | $5.16 |

| Hypothetical 5% Return | $1,000.00 | $ 1,020.18 | 1.00% | $5.08 |

| Rock Oak Core Growth Fund | ||||

| Actual Return | $1,000.00 | $ 1,094.70 | 1.25% | $6.60 |

| Hypothetical 5% Return | $1,000.00 | $ 1,018.90 | 1.25% | $6.36 |

| River Oak Discovery Fund | ||||

| Actual Return | $1,000.00 | $ 1,075.30 | 1.35% | $7.06 |

| Hypothetical 5% Return | $1,000.00 | $ 1,018.40 | 1.35% | $6.87 |

| Red Oak Technology Select Fund | ||||

| Actual Return | $1,000.00 | $ 1,149.40 | 0.99% | $5.38 |

| Hypothetical 5% Return | $1,000.00 | $ 1,020.20 | 0.99% | $5.05 |

| Black Oak Emerging Technology Fund | ||||

| Actual Return | $1,000.00 | $ 1,073.20 | 1.15% | $6.03 |

| Hypothetical 5% Return | $1,000.00 | $ 1,019.39 | 1.15% | $5.88 |

| Live Oak Health Sciences Fund | ||||

| Actual Return | $1,000.00 | $ 1,008.10 | 1.01% | $5.10 |

| Hypothetical 5% Return | $1,000.00 | $ 1,020.13 | 1.01% | $5.13 |

(a) | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

| Annual Report | October 31, 2017 | 19 |

White Oak Select Growth Fund | Schedule of Investments |

As of October 31, 2017

| Shares | Fair Value | |||||||

| Common Stocks — 99.46% | ||||||||

| Consumer Discretionary — 8.34% | ||||||||

| Internet & Direct Marketing Retail — 8.34% | ||||||||

| Amazon.com, Inc. * | 21,545 | $ | 23,813,257 | |||||

| Consumer Staples — 2.04% | ||||||||

| Beverages — 2.04% | ||||||||

| PepsiCo, Inc. | 53,000 | 5,842,190 | ||||||

| Energy — 0.16% | ||||||||

| Energy Equipment & Services — 0.16% | ||||||||

Transocean Ltd. (a) * | 43,000 | 451,500 | ||||||

| Financials — 32.09% | ||||||||

| Capital Markets — 10.11% | ||||||||

| Charles Schwab Corp. | 472,900 | 21,204,836 | ||||||

| State Street Corp. | 83,500 | 7,682,000 | ||||||

| 28,886,836 | ||||||||

| Commercial Banks — 13.97% | ||||||||

CIT Group, Inc. (a) | 177,400 | 8,270,388 | ||||||

| TCF Financial Corp. | 511,000 | 9,310,420 | ||||||

| U.S. Bancorp | 263,000 | 14,301,940 | ||||||

| Wells Fargo & Co. | 143,000 | 8,028,020 | ||||||

| 39,910,768 | ||||||||

| Diversified Financial Services — 4.60% | ||||||||

| JPMorgan Chase & Co. | 130,600 | 13,139,666 | ||||||

| Insurance — 3.41% | ||||||||

Chubb Ltd. (a) | 64,600 | 9,742,972 | ||||||

| Health Care — 11.78% | ||||||||

| Biotechnology — 6.63% | ||||||||

| Amgen, Inc. | 108,000 | 18,923,760 | ||||||

| Health Care Providers & Services — 4.24% | ||||||||

| CVS Health Corp. | 85,600 | 5,866,168 | ||||||

Express Scripts Holding Co. (a) * | 102,000 | 6,251,580 | ||||||

| 12,117,748 | ||||||||

| 20 | 1-888-462-5386 | www.oakfunds.com |

Schedule of Investments | White Oak Select Growth Fund |

As of October 31, 2017

| Shares | Fair Value | |||||||

| Pharmaceuticals — 0.91% | ||||||||

Teva Pharmaceutical Industries Ltd. ADR (a) | 189,000 | $ | 2,608,200 | |||||

| Industrials — 3.70% | ||||||||

| Air Freight & Logistics — 3.70% | ||||||||

| United Parcel Service, Inc., Class B | 90,000 | 10,577,700 | ||||||

| Information Technology — 41.35% | ||||||||

| Communications Equipment — 8.61% | ||||||||

| Cisco Systems, Inc. | 571,000 | 19,499,650 | ||||||

| QUALCOMM, Inc. | 100,100 | 5,106,101 | ||||||

| 24,605,751 | ||||||||

| Internet Software & Services — 14.06% | ||||||||

| Alphabet, Inc., Class A * | 13,310 | 13,749,762 | ||||||

| Alphabet, Inc., Class C * | 16,495 | 16,769,477 | ||||||

| Facebook, Inc., Class A * | 35,900 | 6,464,154 | ||||||

| Salesforce.com, Inc. * | 31,100 | 3,182,774 | ||||||

| 40,166,167 | ||||||||

| IT Services — 6.74% | ||||||||

| Cognizant Technology Solutions Corp., Class A | 128,200 | 9,700,894 | ||||||

| International Business Machines Corp. | 61,900 | 9,536,314 | ||||||

| 19,237,208 | ||||||||

| Semiconductors & Semiconductor Equipment — 11.94% | ||||||||

| KLA-Tencor Corp. | 179,800 | 19,578,422 | ||||||

Xilinx, Inc. (a) | 197,200 | 14,531,668 | ||||||

| 34,110,090 | ||||||||

| Total Common Stocks | ||||||||

| (Cost $213,164,351) | 284,133,813 | |||||||

| Annual Report | October 31, 2017 | 21 |

White Oak Select Growth Fund | Schedule of Investments |

As of October 31, 2017

| Shares or Principal | Fair Value | |||||||

| Short-Term Investments — 8.74% | ||||||||

| Repurchase Agreement — 0.66% | ||||||||

| Tri-Party Repurchase Agreement with South Street Securities Wachovia Tri-Party, 0.88%, dated 10/31/17 and maturing 11/01/17, collateralized by U.S. Treasury Securities with rates ranging from 1.88% to 2.25% and maturity dates ranging from 9/30/22 to 1/31/24 with a par value of $1,906,817 and a collateral value of $1,915,104. | 1,877,552 | $ | 1,877,552 | |||||

| Collateral for Securities Loaned — 8.08% | ||||||||

Mount Vernon Liquid Assets Portfolio, LLC, 1.34% (b) | 23,081,485 | 23,081,485 | ||||||

| Total Short-Term Investments | ||||||||

| (Cost $24,959,037) | 24,959,037 | |||||||

| Total Investments — 108.20% | ||||||||

| (Cost $238,123,388) | 309,092,850 | |||||||

| Liabilities in Excess of Other Assets — (8.20)% | (23,435,097 | ) | ||||||

| NET ASSETS — 100.00% | $ | 285,657,753 | ||||||

(a) | Security, or a portion of the security position, is currently on loan. The total market value of securities on loan is $22,607,547. |

(b) | Rate disclosed is the seven day effective yield as of October 31, 2017. |

| * | Non-income producing security. |

| ADR — American Depositary Receipt |

The sectors shown on the schedule of investments are based on the Global Industry Classification Standard, or GICS® (“GICS”). The GICS was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by Ultimus Fund Solutions, LLC.

The accompanying notes are an integral part of the financial statements.

| 22 | 1-888-462-5386 | www.oakfunds.com |

| Schedule of Investments | Pin Oak Equity Fund |

As of October 31, 2017

| Shares | Fair Value | |||||||

| Common Stocks — 94.14% | ||||||||

| Consumer Discretionary — 10.80% | ||||||||

| Auto Components — 1.89% | ||||||||

Gentex Corp. (a) | 216,500 | $ | 4,202,265 | |||||

| Internet & Direct Marketing Retail — 2.55% | ||||||||

| Amazon.com, Inc. * | 5,120 | 5,659,034 | ||||||

| Media — 4.45% | ||||||||

Interpublic Group of Cos., Inc. (a) | 170,000 | 3,272,500 | ||||||

| Twenty-First Century Fox, Inc., Class B | 259,800 | 6,611,910 | ||||||

| 9,884,410 | ||||||||

| Textiles, Apparel & Luxury Goods — 1.91% | ||||||||

Hanesbrands, Inc. (a) | 188,000 | 4,230,000 | ||||||

| Consumer Staples — 4.41% | ||||||||

| Beverages — 4.41% | ||||||||

| PepsiCo, Inc. | 88,800 | 9,788,424 | ||||||

| Energy — 4.20% | ||||||||

| Energy Equipment & Services — 0.59% | ||||||||

| Nabors Industries Ltd. | 185,100 | 1,042,113 | ||||||

Transocean Ltd. (a) * | 25,000 | 262,500 | ||||||

| 1,304,613 | ||||||||

| Oil, Gas & Consumable Fuels — 3.61% | ||||||||

Valero Energy Corp. (a) | 101,800 | 8,031,002 | ||||||

| Financials — 32.52% | ||||||||

| Capital Markets — 10.61% | ||||||||

| Bank of New York Mellon Corp. | 242,300 | 12,466,335 | ||||||

| Charles Schwab Corp. | 247,251 | 11,086,735 | ||||||

| 23,553,070 | ||||||||

| Commercial Banks — 10.33% | ||||||||

CIT Group, Inc. (a) | 100,500 | 4,685,310 | ||||||

| Great Southern Bancorp, Inc. | 34,728 | 1,866,630 | ||||||

| International Bancshares Corp. | 70,535 | 2,863,721 | ||||||

| SunTrust Banks, Inc. | 105,000 | 6,322,050 | ||||||

| Wells Fargo & Co. | 128,400 | 7,208,376 | ||||||

| 22,946,087 | ||||||||

| Consumer Finance — 4.02% | ||||||||

| Capital One Financial Corp. | 83,300 | 7,678,594 | ||||||

| Annual Report | October 31, 2017 | 23 |

Pin Oak Equity Fund | Schedule of Investments |

As of October 31, 2017

| Shares | Fair Value | |||||||

| Consumer Finance (continued) | ||||||||

| Synchrony Financial | 38,000 | $ | 1,239,560 | |||||

| 8,918,154 | ||||||||

| Insurance — 7.56% | ||||||||

| Assurant, Inc. | 37,300 | 3,754,245 | ||||||

| Everest Re Group Ltd. | 21,400 | 5,081,430 | ||||||

| Travelers Cos., Inc. | 60,100 | 7,960,245 | ||||||

| 16,795,920 | ||||||||

| Health Care — 8.12% | ||||||||

| Health Care Providers & Services — 4.43% | ||||||||

| DaVita HealthCare Partners, Inc. * | 127,400 | 7,738,276 | ||||||

| McKesson Corp. | 15,300 | 2,109,564 | ||||||

| 9,847,840 | ||||||||

| Pharmaceuticals — 3.69% | ||||||||

GlaxoSmithKline PLC ADR (a) | 224,800 | 8,189,464 | ||||||

| Industrials — 1.38% | ||||||||

| Electrical Equipment — 0.15% | ||||||||

| EnerSys | 4,722 | 327,565 | ||||||

| Machinery — 1.23% | ||||||||

| Parker-Hannifin Corp. | 15,050 | 2,748,280 | ||||||

| Information Technology — 32.00% | ||||||||

| Electronic Equipment, Instruments & Components — 2.56% | ||||||||

| Flex Ltd. * | 320,000 | 5,696,000 | ||||||

| Internet Software & Services — 13.94% | ||||||||

| Alphabet, Inc., Class A * | 3,750 | 3,873,900 | ||||||

| Alphabet, Inc., Class C * | 11,759 | 11,954,670 | ||||||

| eBay, Inc. * | 191,000 | 7,189,240 | ||||||

| IAC/InterActiveCorp * | 61,456 | 7,930,897 | ||||||

| 30,948,707 | ||||||||

| IT Services — 9.55% | ||||||||

| Amdocs Ltd. | 120,572 | 7,849,237 | ||||||

Paychex, Inc. (a) | 156,349 | 9,973,503 | ||||||

Western Union Co. (a) | 171,000 | 3,396,060 | ||||||

| 21,218,800 | ||||||||

| Semiconductors & Semiconductor Equipment — 5.95% | ||||||||

| KLA-Tencor Corp. | 61,900 | 6,740,291 | ||||||

Xilinx, Inc. (a) | 87,700 | 6,462,613 | ||||||

| 13,202,904 | ||||||||

| 24 | 1-888-462-5386 | www.oakfunds.com |

Schedule of Investments | Pin Oak Equity Fund |

As of October 31, 2017

| Shares or Principal | Fair Value | |||||||

| Materials — 0.71% | ||||||||

| Metals & Mining — 0.71% | ||||||||

| Teck Resources Ltd., Class B | 76,814 | $ | 1,570,078 | |||||

| Total Common Stocks | ||||||||

| (Cost $163,785,621) | 209,062,617 | |||||||

| Short-Term Investments — 29.96% | ||||||||

| Repurchase Agreement — 6.19% | ||||||||